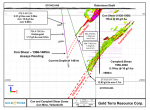

As reported, Skeena Resources (SKE.V) (SKREF) announced an up-sized, non-brokered C$8.1 million capital raise with no warrants attached. This is a tremendous outcome that de-risks Skeena’s Spectrum project by eliminating funding risk for the next 12-18 months. A number of institutions invested in this round and the prior one, and allows the company to actively pursue its dream list of drill targets with a comfortable cash cushion. On June 29th, Skeena received a 3-year drilling permit, began field work and camp construction, and is mobilizing two drills to the Spectrum high-grade gold project. Fieldwork, which commenced June 15, includes re-sampling of historic core, soil sampling and prospecting under the direction of Jacques Stacey, MSc, PGeol, Project Manager.

In addition, geological mapping is being led by Dr. Jim Oliver, PGeo, consultant. Camp and drill pad construction is underway, and drilling is expected to begin on or about July 2nd. A total of 10,000 to 12,000 m of drilling in 50 to 60 holes is planned for this season, with holes averaging 200 m, and ranging from 50 m to 350 m in depth. The drill program has been designed to expand the historic resource, while other holes will test the East Creek zone and other outlying targets. A NI 43-101 resource estimate is expected to be completed in the fall of 2015.

I see a good chance of Skeena delivering a solid maiden resource in the next 6 months and possibly a second one within 6 months of the maiden resource. In my opinion, if 1 million + ounces in a first or second resource report is achieved, the stock price of C$0.065 could double or triple by then, $0.065 would be a distant memory. Further, it’s my understanding that due in part to the historic data, a meaningful portion of the next two NI 43-101 reports could be in the Indicated category. Readers of my prior articles [Here], [Here] and [Here] know the following. Skeena is drilling on a site with a non NI 43-101 compliant historical resource of 244k ounces of gold and has confirmed high-grade gold with its own drill campaigns (see below). The company’s very valuable database of geological mapping, geochemical sampling, trenching and more than 100 diamond drill holes (>14,000 metres) and one adit on Hawk vein (278m of workings) makes the Spectrum Project more than merely an early-stage prospect. One of the foremost geologists on the planet, Ron K. Netolitzky, M. Sc, with extensive knowledge of the Gold Triangle of Northwestern British Columbia, is the Chairman and second largest shareholder. Add to the above facts, a large pile of cash on the balance sheet.

Although I’ve mentioned Mr. Netolitzky in prior articles, I’ve not explicitly stated his claim(s) to fame. Please consider the historic mines in NW B.C. where Netolitzky was the driving force behind.

Snip Gold Mine

1 million oz. Au (gold) produced at 25 g/t

Eskay Creek Mine

3.27 million oz. Au produced at 49 g/t AND 158 million oz. Ag (silver) produced at 2,406 g/t

Those mines sported bonanza grades, an indication to me that Skeena’s longer-term goal of 2-3 million ounces at a grade of 12+ g/t is not a pipe dream. Evidence of Skeena’s potential can be found in the drill results completed in 2014.

[NOTE: For convenience, highlights of Skeena’s drill results are as follows]

14-SP-003: 23.84 g/t Au over 6.5 m, including 40.43 g/t Au over 3.5 m

14-SP-004: 10.63 g/t Au over 27.0 m, including 66.00 g/t Au over 2.0 m and 20.4 g/t Au over 2.0 m, 9.2 g/t Au over 2.0 m, 8.0 g/t Au over 2.0 m and 22.7 g/t Au over 2.0 m

14-SP-005: 18.60 g/t Au over 2.0 m and 7.32 g/t Au over 2.0 m

14-SP-006: 43.80 g/t Au over 2.0

14-SP-007: 9.50 g/t Au over 2.0 m

14-SP-008: 4.58 g/t Au over 9.0 m

14-SP-009: 13.70 g/t Au over 4.0 m and 254.50 g/t Au over 2.0 m.

How Does Skeena Compare to Peer Junior Gold Companies?

For junior gold companies there are more differences than similarities. Jurisdiction, grade, depth of deposit, infrastructure, balance sheet, capital to reach production, strength of management and Board, etc. Instead of ticking off Skeena’s boxes on those metrics, I refer readers to page 18 of the company’s new (June) corporate presentation. In my analysis I replaced Pretium, Roxgold, Continental and Rubicon with much smaller companies Unigold, Nio Gold and Goldstrike Resources. I derived an average EV/oz of $47/oz. That figure does not include Goldstrike, an early-stage company in the Yukon, with no defined resource yet having an EV of $20 million. Skeena has an EV of $7.8 million. Assuming that company achieves a NI 43-101 compliant resource of 1 million + ounces on its first or second resource estimate, the company would be trading at an 83% discount on an EV/oz comparison.

Of course, Skeena has not booked 1 million ounces, it has ~244k ounces of historic non NI 43-101 compliant resource. That’s why it’s trading at an 83% discount! Still, if Skeena can step up with a solid maiden resource and if coming up short, a second resource report delineating 1 million + ounces in the next 6-12 months, I believe that the huge Ev/oz chasm would narrow. As a valuation exercise, if one gives the company credit for 1 million ounces and cuts the cash liquidity from $8 million to $4 million, (due to ongoing drilling) the pro forma EV of $11.8 would trade at an unwarranted 75% discount to peers. However, peers will presumably be spending cash, and raising capital, both of which would increase their EVs. Therefore, the pro forma discount could remain at 80% or more for a company possibly endowed with a NI 43-101 compliant resource of 1 million + ounces in the next 6-12 months.

For those skeptical of my pro forma 1 million ounce + resource premise, viewing it as too aggressive, I argue that one is getting that outcome virtually for free due to the massive valuation discount. This is where leverage comes into play, no not debt leverage, Skeena has no debt. If the company’s stock price were to double implying a $23.6 million EV, SKE.V would still be trading at a 50% discount to the peer $47 EV/oz metric. Clearly, there’s ample room for improvement in Skeena’s valuation relative to peers without suggesting that the entire valuation gap will be erased. Most of the peers are pre-PEA, unlike Skeena, most are not privy to very extensive historical data. Unlike peers, most don’t have a lead Geologist, Mr. Netolitzky, as capable, with proven success in the region. As mentioned, unlike Skeena, most don’t have a fully funded balance sheet with a 12-18 month liquidity runway.

Conclusion

With an admittedly unproven thesis on my part that Skeena Resources will achieve a NI 43-101 complaint resource of 1 million + ounces in the next 6-12 months, i.e. upon the first or second delivered resource report, I stand by my valuation exercise. Junior miners are inherently difficult to value, However, there’s only one key assumption, the million + ounce resource. I realize of course that this presumption is not just a key assumption, but the most important one. Given the luxury of being able to deliver not 1 but 2 NI-43-101 compliant resource reports in the next 6-12 months, supported by the unparalleled historical database, Mr. Netolitzky expertise and drilling results in 2014, I consider the overall risk/reward proposition as quite compelling.

Disclosure:

I, Peter Epstein, CFA, MBA, do not currently own any shares in Skeena Resources (SKE.v) or any other company listed herein. I have owned shares of Skeena Resources in the past and I may acquire share in the open market in the future. Investors should take care to conduct their own due diligence on small cap, speculative stocks. An investment in Skeena Resources may not be appropriate for all investors. Readers should review Skenna Resources’ website and corporate presentation as part of proper due diligence. The company’s Enterprise Value, “EV,” was derived by taking Skeena Resources’ outstanding shares, (including recently issued shares) and multiplying that number by the share price of $0.06 at the time this article was written. From that result, $8 million of cash was subtracted, equating to an EV of $7.8 million. Readers are reminded that Skeena Resources does not have a NI 43-101 compliant resource. It has a non 43-101 compliant historical resource of approximately 244k ounces of gold. The company hopes to provide readers and shareholders with a maiden NI 43-101 compliant resource before year end. The commentary in the article is based both on facts and opinions. All opinions are entirely my own and are not necessarily the same of Skeena Resources’ Management and Board. Skeena Resources is a sponsor of epsteinresearch.com., however readers please note that Mr. Epstein is not an investment advisor.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.