Gold and silver prices have been declining as the US dollar begins to test multi-year highs. The US dollar is very overbought as investors fear that the US will raise interest rates while other countries continue to print money like the ECB and China.

This rally in the US dollar should not last long as it may be a dead cat bounce before the next downturn. This may actually be a great time to transfer cash into real assets such as gold and silver bullion, base metals and energy trading at multi year lows. The US deficit is continuing to increase especially as new wars are announced in Europe and the Middle East. The Fed will continue to support inflationary policies and prevent deflations at all costs. I doubt the US dollar will strengthen for much longer.

Rising deficits and war are usually quite bullish for gold and bearish for the dollar. Silver is already in new four year lows trading below $18. Gold has not yet violated the $1200 mark but may soon bounce off that level. The GDXJ is continuing to hold its 2013 lows.

Meanwhile, the US dollar is strong at new six year highs despite billions of dollars of bailout and quantitative easing. The Fed is running the risk of deflation and may actually be forced into more easing to prevent deflation. The U.S. must pay back its record debts with cheaper dollars.

Right now, the bottles of champagne are popping in the US as real estate and equity markets continue to hit new highs. However, the piper must be paid. Don’t be surprised to see the Fed eventually make a reverse move to devalue the dollar to pay down debts. Expect more bubbles to pop up not just in 3d printing, but in social media stocks and get rich quick real estate scams.

There is a huge cash position waiting on the sidelines to buy real money such gold and silver especially from China which just announced a new Shanghai Gold Exchange. China is sitting on large amounts of US dollars/bonds and must transfer that into the form of real money.

Look for huge volume and accumulation in gold and silver over the next few weeks and in some high quality junior mining stocks. Negative capitulation followed by strong accumulation could be the indicator that the smart money expects gold and silver to bottom. The question for many is when this will occur. Stay tuned to my premium report for signs of a potential bottom.

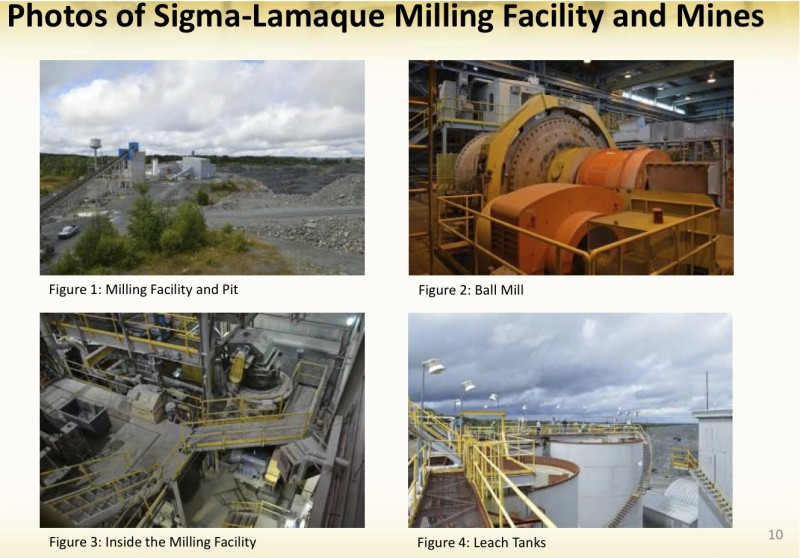

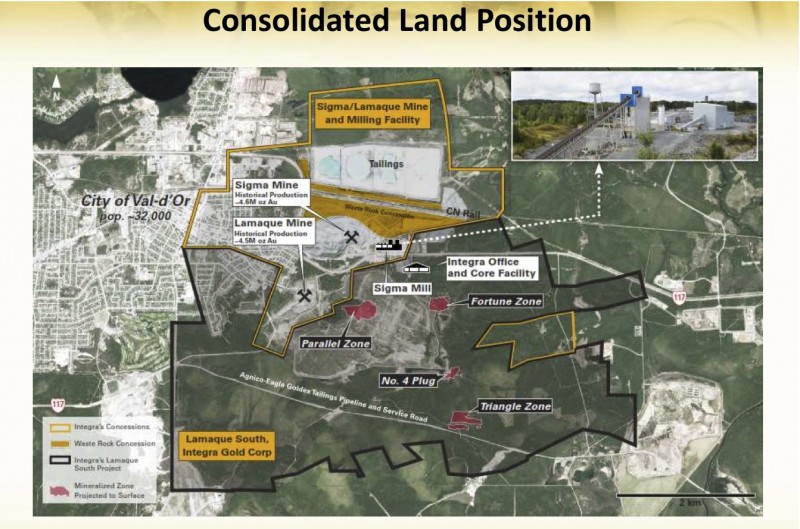

Do not forget we are seeing increased interest into the junior miners such as Integra Gold (ICG.V or ICGQF) which announced an oversubscribed financing over the summer. What is driving this investor demand for junior gold miners such as Integra Gold (ICG.V)?

Integra recently announced the acquisition of a 2200 tpd mill. With the acquisition Integra has access to the underground infrastructure which is located next to their project. Integra was able to pay pennies on the dollar for this asset as it was in bankruptcy. Integra paid $7.55 million in cash and shares for an asset valued at close to $100 million by some engineering firms.

The recent mill acquisition should improve project economics as Integra’s costlier plan to toll mill the ore is no longer necessary. With this mill, Integra becomes one of the only junior gold mining companies developing a new high grade gold operation with a permitted mill in one of the richest, stable and lowest cost mining jurisdictions in the world in Val d’Or, Quebec.

I expect the shares to lead the junior gold market when the sector turns as there are very few advanced high grade economic projects with a mill in a well known stable jurisdictions. Don’t forget Osisko received top dollar from the majors Agnico and Yamana. I wouldn’t be surprised if Integra Gold (ICG.V or ICGQF) is next.

If not already at the top of the list of the majors, I expect that the updated economic study which includes the mill scheduled to be released in the 2nd quarter of 2015 could catapult them to the top of the list as a potential takeout target.

Integra has just come onto the OTCQX under the symbol ICGQF and plans to be active this fourth quarter meeting with retail investors and institutions in the US as they now have a permitted mill. I recently met with management in Denver where they were one of the most talked about companies at the Precious Metals Summit. For many months, I have written that Integra’s Lamaque Project could be Quebec’s next major gold mine to come into production. With the recent acquisition of the mill, my prediction could be coming closer to reality.

Listen to my recent interview with Integra’s (ICG.V or ICGQF) Stephen De Jong by clicking here. Mr. De Jong continues to prove his ability to finance Integra through periods of weak metal prices and low investor sentiment having raised over $25 million in the past two years.

Disclosure: I am a shareholder and Integra is a website sponsor. Conflicts of interest apply.

1. I prefer the “KIS” motto to the more common “KISS”. I define it as, “Keep It Simple”. Simply put, gold bullion is the ultimate asset, but when the price declines, Western investors often become nervous.

2. Some investors try to mitigate their worry, by reviewing factors that make gold the “queen of assets”. That helps, but I think a simple focus on gold demand versus supply is all that is required to own gold without worry.

3. In 2009 – 2010, the fear trade (the Western super-crisis) created massive and consistent demand for gold. Institutional investors literally flocked into gold ETFs.

4. That demand became so huge that it started to equal Indian and Chinese gold jewellery demand. In turn, that caused global demand to overwhelm mine and scrap supply, driving the gold price relentlessly higher until 2011.

5. Another part of the fear trade is geopolitics, and today’s bombing of ISIS targets in Syria is probably why gold is rallying this morning. Unfortunately for gold price enthusiasts, geopolitics has yet to create the kind of demand that the super-crisis did.

6. While the super-crisis has faded as a price driver, and geopolitics is not yet in play, global demand is still roughly equal to global supply now, because Chinese demand has grown and Indian demand is returning to its normal state.

7. ‘With the festive season round the corner, analysts feel gold and jewellery sector may see higher sales. “Gold demand will get a boost as festivals such as Navratra and Diwali approach,” Bloomberg quoted Ashish Shah, Head of AC Choksi Share Brokers Equity.’ – The Financial Express News, September 23, 2014.

8. The bottom line is that there is nothing for investors to fear in regards to lower gold prices at this point in time, because demand and supply are well-balanced.

9. Still, there is a regular ebb and flow of Chindian demand. When it’s strong during a particular month, as it was in June when India officially imported over 100 tons (and probably another 20 – 30 tons in the black market), gold tends to rally $50 -$150 higher.

10. When demand is a bit soft, as it was in July and August, the price tends to decline, by about the same amount. Many analysts tend to get quite excited about these intermediate trend movements, but I would suggest they are movements like the tides of the oceans.

11. The simple fact is that the ebb and flow of Chindian jewellery demand does not suggest great bearish or bullish price action is imminent, but it does move the price modestly higher or lower on a regular basis.

12. Gold is probably the most stable market in the world right now, and whether the next $100 price movement is to the upside or downside is most likely going to be determined fundamentally by whether October Chindian jewellery demand has upside strength, or downside weakness. There are some hints as to what is likely coming:

13. Please click here now. As “Golden Week” begins in China, children are celebrating by walking across a sidewalk of gold!

14. Indian jewellery stocks are also rallying strongly, probably in anticipation of good sales during the Diwali season.

15. Technically, gold also looks ready to rally. Please click here now. I bought the recent “ebb” in Chindian demand, in modest size. Leveraged traders and options traders should wait for my price stoker oscillator to rise above the 20 line before buying, to capture a potential “momentum” style move.

16. I’ll be a very light seller at $1240 and $1270, and I’m hoping to see gold trade at those prices on this “stoker up cycle”. Gold has arrived at light sell-side HSR (horizontal support and resistance) near $1228 this morning, and ALGO traders are likely selling there.

17. Please click here now. This daily GDX chart looks bullish, and I’ve been a substantially bigger buyer of gold stock than bullion, into this decline.

18. Clearly, patience is required. Note the position of my price stoker on that GDX chart. The last time it flashed a full crossover buy signal (where the lines are under 20 when the signal occurs) for gold stocks was in early June. That’s over three months ago!

19. There has been a lot of drama displayed by investors and analysts since that last buy signal, but there is nothing out of the ordinary occurring with gold stocks. Chindian demand was modestly soft for a few months, and so the price of gold stocks, which are leveraged to gold, declined more aggressively than bullion did.

20. I sold some gold stock for gold bullion in late June, and now I’m buying it back, without any drama. I’d like to see the entire gold community join me as I do that, albeit in a very modest way.

21. Some investors in the gold community have asked me if I would buy the US stock market now. Please click here now. I only buy significant price weakness, so the answer is no. I will be a buyer of the Dow at 14,200. That’s the thick green HSR line I’ve highlighted on this monthly candlesticks Dow chart. Aggressive investors, who feel they are missing out on the action, could buy at 16,600 or 15,600. My personal focus for my stock market monies is the stock market of India, which is vastly outperforming the US stock market, and will probably continue to do so for many decades. I view the US stock market like a rotary phone relic, and India as a “must own” Iphone!

22. Sugar is a great asset, and it can be a key leading indicator for silver prices. Please click here now. This daily sugar chart looks excellent. There’s a commodity-style (short term) double bottom pattern in play, and my price stoker is pushing at the 20 line, on a crossover buy signal. This technical action suggests something similar is coming in the silver market.

23. Please click here now. That’s the daily chart for silver. Strong jewellery demand in October should produce sharply higher gold prices. If it’s strong enough, silver should be able to move well above sell-side HSR in the $18.75 area.

24. In closing today, I want to highlight an intriguing pattern that has developed on the COT report chart for gold. Sentimentrader charts commercial hedger activity very well. Please click here now. It appears that the commercial hedgers are steadily moving towards a net long position in the gold market, and there’s an inverse head and shoulders bottom pattern in play. Whether they are focused on the super-crisis, geopolitics, or gold jewellery, is unknown, but this bodes well, for all the world’s gold investors!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

Gold stocks have plunged in September, crushed by the withering selling pressure from heavy futures shorting hammering gold. As usual, these falling prices have kindled extreme bearishness on this left-for-dead sector. But despite this rotten sentiment, gold stocks’ young upleg remains very much intact technically. This impressive resiliency is fueled by these miners’ incredibly-cheap fundamental valuations.

Gold stocks are without a doubt the most despised sector in all the stock markets. Thanks to the Fed’s brazen debt monetizations and manipulations of interest rates, the global markets are distorted beyond belief. Stock markets have soared to extreme valuations on the Fed’s implied backstopping, leading to epic complacency, greed, and hubris. That artificial levitation sucked vast capital out of alternative investments.

When stock markets do nothing but rally thanks to the Fed, the perceived need for prudent portfolio diversification with alternative investments like gold has vanished. And with investor interest in gold virtually dead, the gold stocks have suffered mightily. Nearly everyone believes they are doomed to spiral lower forever. To be bullish on this loathed sector guarantees ridicule and mocking these days.

Nevertheless, a hardcore remnant of contrarian investors remains very bullish on this sector. They have studied market history, and remember core truths that the Fed has blasted from most minds. Markets are forever cyclical, they rise and fall. Any extreme in sentiment and prices is soon followed by a major reversal. Exceptionally-high greed-fueled prices soon fall, and exceptionally-low fear-drenched prices soon rise.

Contrarians know that successful investing demands buying low then selling high. And the cheapest stocks are always the most hated, the sectors with the most universal and overwhelming bearishness. They have the most potential to explode higher and multiply wealth when sentiment inevitably shifts the other way. That’s why smart investors including elite billionaire hedge-fund managers are long gold stocks today.

Gold-stock fundamentals are exceedingly easy to understand. Gold miners obviously mine gold. And their production costs are largely fixed when mines are built. So their profitability is determined by the gold price. When gold climbs, their profit margins and absolute earnings soar as their costs stay pretty stable. So these companies are ultimately a leveraged play on the gold prices which drive their profits.

Across all the markets, any stock’s underlying profitability determines what its fundamentally-sound price levels should be. Gold stocks are no exception, as they will eventually climb dramatically to trade at reasonable valuations relative to their profits. And not only will their earnings surge as the gold price itself recovers from today’s sentiment extremes, gold stocks are dirt-cheap relative to current low gold levels!

Gold stocks are now languishing at a fraction of their fair value relative to gold because of the epically bearish sentiment plaguing them. But such emotional extremes never last, they are inherently self-limiting and soon burn themselves out. When psychology in this gold-stock sector finally normalizes, the miners’ beaten-down stock prices are going to surge higher to reflect their earnings fundamentals.

This first chart highlights today’s extreme anomaly in gold-stock price levels that was indirectly driven by the Fed’s super-manipulative quantitative-easing campaigns and zero-interest-rate policy. It looks at the ratio of gold-stock price levels relative to the gold price that drives their profits. Since ETFs have grown so popular with traders, I’m using the dominant American ones as proxies for gold-stock and gold price levels.

Gold-stock prices are represented by GDX, the benchmark Gold Miners ETF. And gold prices are represented by the mighty GLD SPDR Gold Shares gold ETF. Dividing the price of the former by the latter and charting it over time shows whether gold stocks are gaining or losing ground relative to the metal that drives their profits and hence ultimately stock-price levels. This chart is still a stunning wake-up call.

This blue GDX/GLD Ratio line is the key to understanding why contrarians remain so bullish on such a seemingly-hopeless sector. Before 2008’s crazy once-in-a-century stock panic sucked in gold stocks, they traded at a pre-panic average GGR of 0.591x. In other words, a share of GDX was worth about 6/10ths of a share of GLD. The epic fear generated by 2008’s stock panic shattered that long-standing relationship.

GDX plummeted 71% in a matter of months, as many if not most gold-stock investors capitulated and sold low in the dark heart of that panic. Much like today, bearishness was off the charts. But as Warren Buffett has wisely said, the time to be brave is when everyone else is afraid. The greatest times to buy low are when a sector’s stock prices seem the most hopeless. With most investors out, they are just too cheap.

In late October 2008, the GGR had cratered to just 0.227x. The extreme and unsustainable selling that was driven by extreme and unsustainable bearish sentiment had crushed gold-stock prices to a fraction of their fundamentally-righteous levels relative to the metal that drives their profits. Then, like now, contrarians like me bullish on gold stocks were mocked. But we made fortunes as they inevitably mean reverted.

Over the next several years, GDX would more than quadruple with a 307% gain! Buying low pays off big. And coming out of such a crazy low-priced anomaly, gold stocks’ gains easily exceeded those of gold itself. So the GDX/GLD Ratio blasted higher, ultimately stabilizing around 0.419x over the next two-and-a-half years. That level is critical to remember, because it persisted during normal post-panic years.

By August 2011 gold itself grew very overbought and overdue for a major correction, which I warned about right as it topped. And as usual since gold stocks are leveraged plays on gold prices, they fell faster than gold which dragged the GGR back down. It bottomed and reversed normally in mid-2012, but then the Federal Reserve launched its unprecedented open-ended QE3 campaign to manipulate financial markets.

QE3 changed everything in the markets, and temporarily destroyed the demand for gold. Not only was the Fed monetizing bonds with new dollars created out of thin air, it was constantly jawboning that it was ready to ramp up QE if the economy (read “stock markets”) weakened. So stock traders took this as an implied backstop, a Fed put on stock prices. So market history be damned, they ignored all risks to keep on buying.

Capital fled from gold to chase the levitating general stock markets, driving a once-in-a-century gold plunge in the second quarter of 2013. Gold stocks were crushed on this, ultimately falling 69% from their peak on a GDX basis to hit their worst levels since the stock panic’s. But the amazing thing was the GGR actually fell to an all-time low well below late 2008’s. Gold stocks had never been cheaper relative to gold!

This mother of all gold-stock lows happened late last year, days after the Fed announced it was starting to slow down its massive QE3 bond monetizations. Ever since then, gold stocks have been fighting the extreme bearish sentiment headwinds to rally on balance. They are starting to regain ground compared to gold, with the GGR enjoying its best rallying streak so far this year since 2010. Gold stocks have already reversed!

For 6 long years, gold stocks lost ground relative to gold. As the relentlessly-downward-sloping GGR shows, they became cheaper and cheaper compared to their earnings power. The GGR kept being repelled at the strong secular resistance line shown above. But early this year the GGR made another attempt to break out to the upside, and that finally succeeded only a few months ago this past June.

This decisive GGR breakout on top of its strong new uptrend since late last year shows that gold stocks have reversed. The 6-year downtrend in their prices relative to gold is over. And that makes perfect sense. The markets are forever cyclical, no trend lasts forever. Contrary to the bears’ foolish assertions, there was just no way gold-stock prices could continue falling compared to the driver of their profits indefinitely.

After 6 years of the GGR retreating, how long is its mean reversion from bearish to normal to eventually bullish sentiment going to take? Several years at least, and likely longer since great market cycles tend towards symmetry. And that’s why gold stocks are so darned bullish and exciting today. They are dirt-cheap after years of falling out of favor, so their upside potential from here is enormous beyond belief.

Remember that in the normal post-panic years before overbought gold corrected and before the Fed’s extreme market manipulations of QE3, the GDX/GLD Ratio averaged 0.419x. This week it slumped to 0.199x, actually well below the worst levels of 2008’s epic stock panic. So merely for gold stocks to regain fundamentally-normal prices relative to gold at today’s levels GDX would have to surge 110% higher!

You read that right. Even at today’s dismal $1250ish gold prices, gold stocks would need to more than double from here to reflect the metal’s impact on their profitability now. And that’s a very conservative target for two reasons. First, after such extreme bearishness gold stocks shouldn’t stop rallying at merely normal sentiment. The great emotional pendulum should swing far back into the opposite greed side.

So at some point in the next several years, gold stocks are highly likely to power much higher than that post-panic GGR average. They’ll likely attain the pre-panic average of 0.591x, and maybe even higher for a short spell when euphoria flares. Second, gold itself isn’t going to keep languishing near $1250. As the Fed’s artificially-levitated stock markets inevitably roll over with QE3 ending, gold is going to surge.

Alternative investments thrive when conventional ones are struggling. So once the lofty stock markets decisively roll over, investors will remember gold’s unparalleled value as an essential asset to diversify portfolios. Capital will flood back in. Provocatively despite popular wisdom, rising rates will help this. Gold has thrived in rising and high-rate environments historically since they hit stocks and bonds hard.

That’s why I still strongly believe gold stocks are going to at least quadruple over the coming several years again just like they did after 2008’s anomalous stock-panic low. Pick any GGR higher than the post-panic average, and a gold price way higher than today’s, and the gold-stock price targets surge accordingly. At a 0.6x GGR and $2000 gold for instance, GDX would quintuple from today’s low levels.

Being a quasi-prominent contrarian on the stock markets and gold, my e-mail inbox explodes whenever the former surges near highs or the latter wilts. Myopic traders with no understanding of market and sentiment cyclicality gloat about how stocks will rise forever while gold falls forever. What a dumb bet. And weaker investors succumb to bearish groupthink and fret that some major new gold plunge is imminent.

But despite all the fear and bearishness on gold and gold stocks this past month’s futures-shorting-driven selloff has generated, its impact on the GGR is trivial. Note above that the recent weakness in gold stocks relative to gold barely registers in this long-term chart, and the GGR remains near both its 200-day moving average which recently turned higher and its new uptrend’s support. There is no damage.

That is true technically too. While gold stocks’ dirt-cheap fundamentals are the key reason contrarians are so bullish on them, their price action looks fine despite the past month’s selloff. This next chart looks at gold-stock technicals through the lens of the flagship GDX gold-stock ETF. Though its price action is a secondary concern, so many traders are worked up about this latest selloff that it bears examination.

Despite all the sound and fury and the bears’ supreme hubris this week, GDX remains within its major new uptrend that was born almost 9 months ago in late December 2013! Gold-stock prices are near support and look to be bottoming at another higher low. We’ve seen gradual and sustained buying of gold stocks by smart investors all year long despite the fierce headwinds from the Fed’s stock-market levitation.

GDX’s 200-day moving average, which usually signals the long-term trend direction, continues to move higher after reversing several months ago. And GDX’s 50dma crossed back above its 200dma twice this year, confirming gold stocks’ Golden Cross buy signal. There is literally nothing bearish about this chart, it is actually powerfully bullish for a young upleg. Gold stocks continue to advance on balance technically.

Long-term investors look to major downside fundamental-pricing anomalies to buy low, like the GGR today reveals. But short-term speculators look at trends and support approaches. And GDX’s chart clearly shows gold stocks are at their third best buying point since their decisive reversal late last year. Buying when prices near support in strong uptrends is one of the best ways to make money in trading.

Zooming out to the bigger picture technically, gold stocks have been consolidating sideways in a massive basing formation since last summer. The second quarter of 2013 was gold’s worst quarter in a whopping 93 years, so it spawned off-the-charts bearishness. Ever since, the vast majority of traders have been utterly convinced that gold, silver, and their miners’ stocks are doomed to spiral lower forever.

These weathervane bearish calls couldn’t have been more wrong though. Enough buyers emerged to snatch up all the sellers’ gold-stock shares, leading to the past 15 months’ bottoming consolidation zone. If gold stocks couldn’t be hammered lower with gold sentiment so epically bearish for so long, just imagine how they will soar when psychology mean reverts out of these extremes. It’s going to be amazing.

So with gold stocks exceedingly cheap fundamentally and at an outstanding buy point technically, what are you going to do? Have you forged yourself into a contrarian tough enough to fight the crowd and buy low? Or are you slave to herd groupthink? Will you buy low when a sector is deeply out of favor and reversing higher? Or will you wait until after gold stocks already double and miss the easy gains?

The right answers are so glaringly obvious. The high and loved stock markets can’t rise forever and are long overdue for a serious selloff. And low and hated gold and the stocks of its miners can’t fall forever and are long overdue for a gigantic mean-reversion upleg. With bearishness in gold extreme with it near consolidation lows, and its miners epically undervalued, how can this not be an ideal time to buy low?

At Zeal we’ve always been hardcore contrarians, buying low when few others will to multiply fortunes. So while gold stocks remain the pariah of the stock markets, we’ve continued to diligently research them to prepare for their coming massive moves higher. Just this week, we finished our latest 3-month project to ferret out the best advanced-stage junior gold explorers. These elites have vast upside potential dwarfing GDX’s.

The bottom line is gold stocks remain radically undervalued relative to the metal which drives their profits, even at today’s dismal gold levels. After falling faster than gold for 6 long years, this secular trend has reversed over the past year. This was despite the extreme bearishness plaguing this sector. Gold stocks’ mean reversion back up to normal valuations should run for at least several more years.

And after suffering such epic valuation anomalies, gold stocks are again due to at least quadruple like they did after 2008’s stock panic. The futures-shorting-driven gold selloff over the past month pushed gold stocks back down to their new uptrend’s support, creating a fantastic buying opportunity. While not everyone is smart or tough enough to fight the crowd and buy low, those contrarians that do will be richly rewarded.

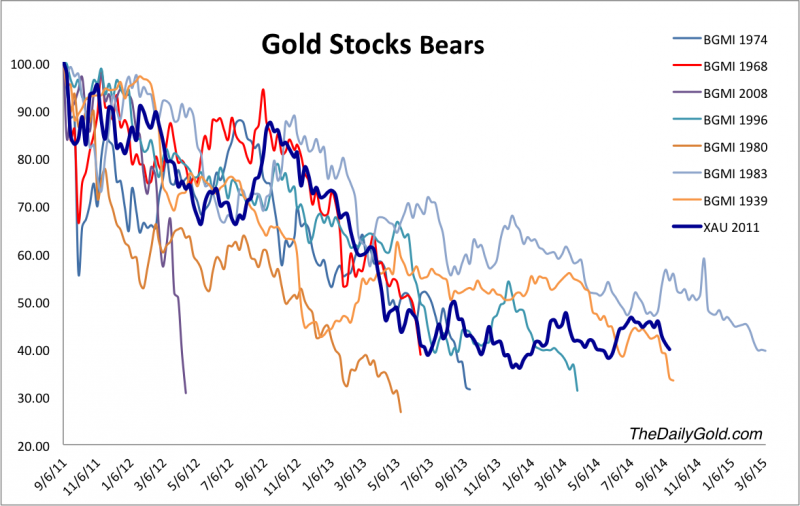

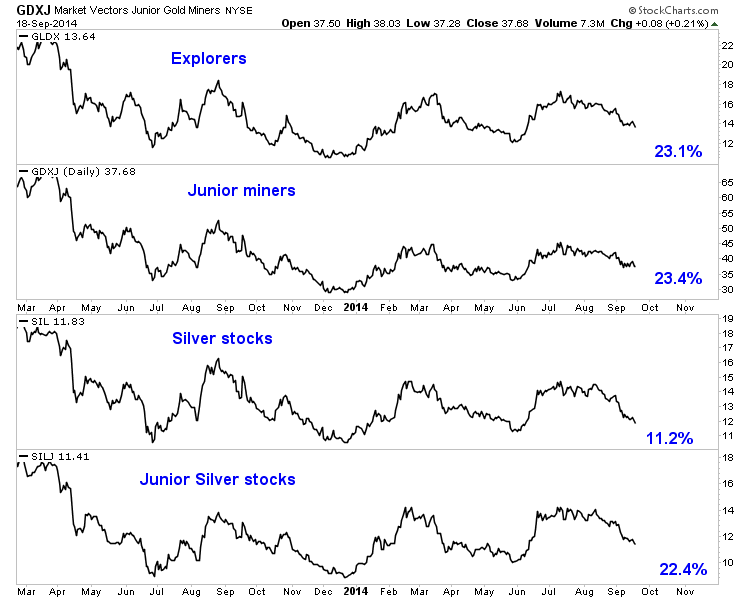

Since last summer, investing in the mining sector has been akin to riding a mini roller coaster. There have been two huge rallies, two sudden and sharp declines while more than a handful of individual stocks have rebounded over 200% from their lows. Nevertheless, as we noted a few weeks ago the weakness of the metals won out and are dictating the terms. Since we covered the metals in our last missive we wanted to focus soley on the miners. A look at the bear market analog chart as well as a very long-term chart of GDM illustrates the coming risks and opportunities.

Here is the updated bear analog chart for the gold stocks. The XAU is used for the current bear market. This chart helped identify the opportunity at the June 2013 and December 2013 lows. There has been only one bear market worse than 70%. If you believe the gold stocks have not bottomed then this is the second worst bear in terms of time. The chart argues that if the December low is taken out, it would be so only marginally. A 65% loss at the December 2013 low could become 67% or 68% but probably not anything worse.

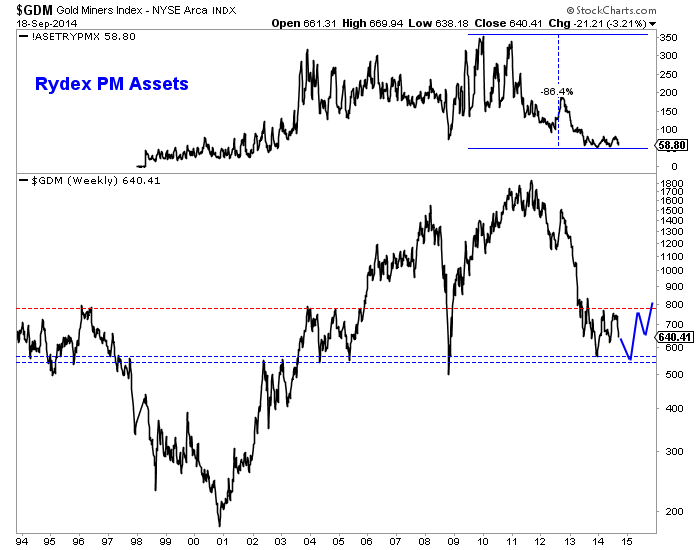

Below is a weekly line chart of GDM, the NYSE Gold Miners index and the basis for GDX. This is one of the broadest indices for miners. GDM has two levels of strong support which date back 20 years. GDM would have to decline 13% and 17% to test those supports. At the top, we plot the assets in the Rydex Precious Metals Fund which have dwindled 86%. We plot in blue a rough projection only for consideration purposes.

In looking at long-term charts of miners, I find that a double bottom (seen above) is definitely possible. In the chart below we plot GLDX, GDXJ, SIL and SILJ. Considering a 3% margin of error, three of the four ETFs would have to decline more than 25% to rule out a long-term double bottom.

The risk is quite clear. Failed moves produce fast moves. The miners failed to breakout and have tumbled. The late May lows mark the next support but these points do not amount to much beyond the daily charts. Furthermore, after $1200 Gold’s next strong support isn’t until $1080, the 50% retracement of the entire bull market. Hence, there is a growing risk of the miners falling to their December lows. Therein lies the opportunity. Only time will tell but that point could immediately mark a shift from risk to amazing opportunity.

A few months ago, I believed uranium would bounce off lows and make a powerful move higher. The spot uranium price is beginning a rebound rallying more than $3 per lb over the past few weeks.

I alerted my readers to the reality that end users of uranium are concerned about geopolitical stability and are actively looking for safe and long term secure supplies of U3O8. Any hiccup in production could significantly impact global supply.

Click here for reference chart.

Although there is abundant amounts of uranium in North America and Australia most of the production comes from unstable areas such as Kazakhstan, Niger and Russia. The recent sanctions with Russia could have a major impact on pricing.

Russia through Rosatom operates Kazakhstan production which is the largest supplier of uranium to the world. Europe and the US are some of the largest consumers of nuclear and have relied on cheap Russian uranium for decades.

What happens when the cheap uranium runs out especially at a time when demand is growing? A price spike with triples and quadruples in the junior miners.

China is leading the nuclear renaissance where they may build hundreds of reactors over the coming generation. Despite Japan and Germany’s kneejerk reaction to abandon nuclear temporarily after Fukushima, demand for uranium is rising.

Now only a few years later, Japan may turn back on their nuclear reactors and Germany may have to look at turning back on its nuclear reactors this Winter especially if Russia turns off the natural gas taps. The anti-nuke crowd may grow increasingly out of favor when the German population is freezing and in the dark.

End users may have to move quickly to secure supply from the junior uranium miners rather than rely on Russia. The major uranium producers such as Areva, Cameco and Rio Tinto have already been shutting down high cost marginal mines due to the low uranium spot price. Don’t underestimate black swans with Cameco which is dealing with labor challenges and technical obstacles in the Athabasca Basin.

In conclusion, expect the uranium price rebound to continue as end users buy in the market and look to secure deals with emerging producers. The supply side is just too volatile while demand is growing. Look for the uranium miners (URA) to breakout especially these three following companies:

1) Uranerz Energy (URZ) just announced its first sale of 75,000 pounds of uranium from Nichols Ranch in Wyoming into long term contracts with nuclear utilities. 2014 has been a transformational year for Uranerz as it started uranium production and is now generating cash flow. I have followed this company for years and am happy to see U.S. produced uranium fuel these domestic plants rather than it being imported from Russia. Uranerz has three long term uranium deals with two major US nuclear utilities and has a huge land position in the Powder River Basin. Do not be surprised to see a major like Cameco acquire this new producer.

2)Looking for huge leverage to uranium? One should consider Pele Mountain (GEM.V or GOLDF) trading at a nickel. The company has over 82 million lbs of uranium in the inferred category. In addition to the uranium, they own valuable rare earths and recently announced that they are working with Canmet, a branch of Natural Resources Canada on processing. CanmetMining has a long history of supporting optimization research at Elliot Lake. Although the processing for rare earths at Elliot Lake is well known as it produced rare earths in the 1980′s, new metallurgical research could drastically improve recoveries. Elliot Lake was home to some of the great Canadian uranium mines in prior decades which mined over 300 million pounds of uranium. Mining could return if end users want a secure and affordable source of uranium and critical rare earths right in mining friendly Ontario.

3)Anfield Resources (ARY.V or ANLDF) just acquired from Russia’s Uranium One, a US uranium mill and prospective uranium properties. This makes Anfield one of the few potential uranium producers in the U.S. as there are only three licensed uranium mills in the entire country. The other mill operators are trading at much higher valuations compared to Anfield. Having the ability to mine and mill uranium is a huge advantage now for Anfield.

Disclosure: I own these three stocks and they are all website sponsors. Conflicts of interest apply. Please do your own due diligence.

This year has seen a revival in aluminium prices along with prices for a number of other base metals, such as zinc and nickel. Whereas the strength in zinc and nickel prices has been mainly supply – driven, the picture for aluminium is more nuanced.

Aluminium is the second most produced metal in the world and is used in a wide range of applications, from construction and cars to packaging. The industry has been suffering from oversupply since 2007, mainly due to large capacity increases in China and the Middle East. Prices have been falling since 2011, leading to shutdown of smelters. These cuts in production have started to filter through to the markets and, since reaching a five-year low of 1,700 USD/tonne in February, prices quoted on the London Metal Exchange (LME) have been trending upwards.

Click here for reference chart.

Production cuts

It has been estimated that in the past few years, up to 5m tonnes of aluminium capacity has been shut, only 1m of which can be easily restarted. For comparison, world aluminium production in 2013 reached 50.6m tonnes. In 2014, the world’s biggest aluminium producers have announced production cuts. Russia’s Rusal cut its production by 8% in 2013 and by a further 12% y-o-y in Q1 2014 to the annual capacity of 883,000 tonnes. Alcoa, another major producer, cut its production to 551,000 tonnes in 2014. Over the last five years, Alcoa has permanently closed about 30% of its global aluminium smelting capacity.

These cuts have finally started to filter through to the market. World aluminium production during the period from January to June 2014 reached 30.1m tonnes, down 3% year-on-year. This was mainly driven by production declines in Europe (-5%) and North America (-8%), which more than offset increases in China (+8%) and the Middle East (+21%).

Falling stocks on the LME

Another factor often cited as a reason behind the recent strength in aluminium prices is falling stocks on the LME. Stocks at LME warehouses have fallen 13% this year, to two-year lows. However, they are still high by historical standards, at 4.7m tonnes. In addition, it is not clear to what extent this reduction reflects the underlying physical supply and demand in the market. There is speculation that this reduction was partly triggered by high storage costs in LME warehouses, and some of the metal leaving LME warehouses has been moving into cheaper non-bonded storage.

Concerns over feedstock supply

As with many other base metals, Indonesia’s ore export ban has been one of the factors driving prices for aluminium up in 2014. The ban, introduced in January 2014, prohibits the exports of unprocessed ores or minerals in their raw forms to encourage miners to process ores domestically before exporting. Indonesia accounts for over 60% of global exports of bauxite, a raw mineral used in the production of aluminium.

Is the strength in prices supported by demand?

At the same time, demand is strong in some key markets, notably from the automotive industry in the US. The transport industry is the largest end-use application for aluminium, accounting for one-quarter of global aluminium demand. In August, total car sales in the US rose to an annualised 17.5m vehicles, volumes not seen since before the recession, driven by an improving economy and falling fuel prices.

The picture is more mixed in Europe. Western European car sales rose to 640,123 in August, an increase of 1%, as weakening demand in Germany and France was offset by strong gains in the UK and Spain. However, the latest figures from China point at slowing demand growth. Sales of passenger cars in China rose to 1.47m vehicles in August, up 8.5% y-o-y, the weakest pace of expansion since March.

Outlook

So, on balance, it is likely that the aluminium market will remain strong over the next few months. However, several factors are making this outlook uncertain. The mentioned lack of clarity around the stocks situation is one factor. However, the major challenge for the sustainability of the recent rally in aluminium prices will be posed by developments in China.

China is responsible for over 40% of global aluminium production. Despite the oversupply that has persisted in the global market in recent years, production in China has been rising, as output in other major producing regions has fallen. In the four years to 2013, Chinese production grew 44% to 24.9m tonnes, with net exports steadily rising in recent years. However, not all the increase in production has been swallowed by exports and domestic consumption, and it is estimated that China will end the year with the largest excess supply in 14 years.

Economic growth in China has been slowing signs of slowing so far this year, with the latest data showing that China’s factory output, retail sales investment and imports all slowed in August, with factory output rising at the weakest pace in nearly six years. Should aluminium prices continue their rise, there is a substantial room for China to increase its exports which is likely to limit further increases in price.

I’ve been reading titles like this for years. The same for titles about the imminent tipping point of the adoption of electric vehicles. Well, we seem pretty close on EVs, what about solar? I don’t know how to define a tipping point in solar, but adoption is exploding. Everyone knows that the costs to manufacture solar panels continues to decline. Less well known is that the conversion rate of the sun’s energy is improving modestly each year as well. It’s like measuring both the declining costs of computers AND the increased computing power. There’s so much written about the benefits of solar power. I’m not here to convince readers of its potential. I’m here to show that strong growth in solar is virtually assured, tipping point reached or not.

I remain a fan of nuclear power for very-large scale BASE LOAD projects in countries with large populations. Solar will never replace base load electricity generation. However, who said that solar has to compete with nuclear? Since solar penetration is at much, much lower levels, growth rates will remain sky high. The key to solar’s growth will be speed to market. Nuclear reactors require years or even a decade to build and billions of dollars. Rooftop solar installation takes days. The actual installation period is not a fair comparison, there are approvals, permits and planning that may take weeks or even a month or two. Still, speed to market is the defining moment for small-scale solar.

Moving up to mid-scale solar installations on commercial buildings, car ports, hospitals, apartment buildings, manufactures, military bases, nursing homes, municipal buildings, prisons, malls, etc, the all-in costs are in the millions to tens of millions and the time from the GO decision to installation probably a year or less, (unless there’s local opposition, utility interference or bureaucracy), each of which will decline over time. Simply consider the high number of cash-strapped schools and municipalities. A zero down payment to lock in long-term rates while cutting costs 15%-30% will gain increasing acceptance. Perhaps even hitting a tipping point? Speaking of schools– they are especially interesting because they’re closed in the summer and would presumably be net generators of electricity by feeding the grid, i.e. making money in the summer!

CBD Energy a Highly Compelling Growth Opportunity

Speed to market will diminish opposition and bureaucracy. Improving technology and lower costs will assure wider adoption. From an investment perspective, which companies are best poised to benefit from this trend? When one thinks of solar companies, SolarCity may come to mind. That company has been a huge success. It now has an Enterprise Value, “EV” (market cap + debt – cash) of $7 billion. Yet, it’s forecast to continue to report negative net income for at least the next 2 years and trades at an tailing 12 months EV/Sales ratio of 33 times. Instead, I’m invested in a small cap NASDAQ-listed company, CBD Energy [CBDE]. Its market cap is $25 million. Which stock do readers think could double or triple over the next year? The giant SolarCity or CBD Energy which is trading at an EV/Sales ratio of less than 0.5x next 12 months revenues?

Which company will grow faster? CBD Energy forecasts revenue growth of about 60% a year in 2015 and 2016. Can the giant multi-billion solar plays match that growth? Perhaps some can, but I don’t want to bet on it. In addition to spectacular growth, the company will be net income positive from 2015 on. CBD offers a very compelling risk reward/reward opportunity. It has the flexibility to be nimble and make quick decisions. It has a stellar management team for a small cap. This is a company that’s flying under the radar because it just recently uplisted to NASDAQ. More importantly, it just recently entered the U.S. markets from its home base in Australia. SolarCity loves to quote its $3 billion revenue backlog. CBD has a backlog of greater than $100 million, yet its EV is 1/300th of Solar City’s. That’s 1/300th, but its revenue backlog is 1/30th that of SolarCity’s. Again I ask you, which company is more likely to double or triple?

CBD Energy is More Than Just a Residential Rooftop Solar Company

I focus on residential rooftop because it’s what most people are familiar with. If CBD could capture just 1% of the installs that SolarCity boasts about, that would equate to about $5 million of PROFIT a year. The company has proven that it’s a player by licensing the, “Westinghouse Solar” brand name. No solar company can compete with that household name, well known in multiple countries. However, CBD is more than just residential solar. To be clear, the company has expertise in that area, having installed more than 17,000 systems. The company also has a growing commercial-scale solar business, a wind segment and an energy efficiency business.

This company is poised to make a move in the renewables industry. It will never be a SolarCity, nor does it want to be. Profitability and high revenue growth are just fine. In addition to the three-pronged strategy, CBD is more geographically diversified than most peers. The company has operations in Australia, the U.S., the U.K. and “rest of world.” CBD has a committed line of credit of $20 million, an amount greater than its current market cap. It has close ties with contractors, hedge funds, private equity firms and banks that want to co-invest and/or acquire finished projects.

What do I mean? Consider that the company owns 10% of a large wind farm that it managed the building of and arranged the financing for. On that single project, which will be finished in December, the company expects to sell its interest for a $15 million pre-tax profit. $15 million is a huge score for a small cap. It moves the needle, it retires ALL debt, it funds robust growth. Each and every commercial-scale solar or solar project will move the needle. CBD is in the driver’s seat to make tuck-in acquisitions of peers and joint ventures with any number of larger players. Once this company’s valuation, backlog, profitability and growth become known to the market, I think the stock price could soar.

Disclosure: Mr. Epstein owns shares of CBD Energy. This article and all articles written on MyriadEquity.com by Mr. Epstein does not represent investment advice and express his opinions only. Mr. Epstein is not a registered investment advisor. Readers should consult with their own investment advisors before considering buying or selling any securities mentioned in this article. Mr. Epstein has no prior or existing relationship with CBD Energy.

This past week I have had to cut back on my publishing due to my travels to the Precious Metals Summit where I had back to back meetings with some of the top fund managers, investors and over 30 of the highest quality junior miners. I was able to get updates in person of current and past holdings as well as potential new first class opportunities with huge catalysts ahead.

The Post Labor Day rally in precious metals I expected has turned into the Post Labor Day Selloff for precious metals and many mining stocks. Many investors came back from Labor Day and sold their precious metals in favor of the U.S. dollar. This could be the worst possible trade right now. This could be the shakeout before the breakout in the precious metals. Generally this is a seasonally strong time for gold and silver. We may bounce off new lows below $1200.

Despite gold testing new lows, the junior miners are still in an uptrend since December of 2013. Is the outperformance of the junior miners indicating that gold may bottom here around $1200?

Click here for reference chart.

There is no doubt about it we are in the midst of a major low in gold and silver after one of the longest bear markets since Bre X. Gold and silver are testing lows at $1200 gold and $18.50 silver. It has been extremely painful bear market with many of these junior miners which were trading at $10 are now worth $.10.

However, the major funds and miners were well represented in Denver meeting with the juniors and have not given up. Merger and acquisitions are increasing with the recent deals of Osisko, Cayden and Brigus. Remember the producers are under pressure as they have to cut back on high cost production and are looking for lower cash cost resources in the junior mining sector.

That may be why Agnico Eagle paid over $205 million for Cayden’s early stage high grade gold discovery. Recent valuations of M&A transactions gives us a benchmark in analyzing future investment opportunities. Remember Cayden was very early stage and did not have a resource. They just had exceptional drill results. That is why I do not ignore early stage explorers trading at less than 1/10th of Cayden’s valuation.

Keep a close eye on high grade explorers such as Barisan Gold (BG.V) and Canamex Resources (CSQ.V). They have minuscule market caps but huge high grade drill results. I would speak to management of both companies and read both Barisan’s and Canamex’s recent news releases which are extremely impressive.

I will be carefully digesting some of those ideas I gathered in Denver both on the markets and the miners and share the findings with my premium subscribers over the next few days and weeks. I will give you some leads from some dynamic companies I met with at the conference gaining significant traction in the marketplace despite weak gold and silver prices.

1)Red Eagle (RD.V or RDEMF), a junior gold miner in Colombia just announced a Definitive Feasibility Study which shows very low cash costs, capex and some of the highest margins in the junior industry. It is beginning to breakout past $.30 and gain recognition by the investing public. A final permit could be coming in the near term which could prove to the world that this could be the next major producer in Colombia generating free cash flow quickly to shareholders.

2)Integra (ICG.V or ICGQF) a junior gold miner in Quebec is getting serious about production as they just acquired a major mill in Val d’Or for $7.5 million in cash and shares. This is one of the few juniors with financing, a high grade asset and a mill in the major mining district of Val D’or. This acquistion considerably derisks the asset. Look for further drilling success to boost recognition for this exciting high grade story progressing towards production in a gold district which just saw the major Osisko buyout by Yamana and Agnico Eagle.

3)Wellgreen (WG.V or WGPLF), a junior platinum miner in the Yukon announced a resource and metallurgy update which is a major development. It makes me quite excited for the upcoming updated Preliminary Economic Assessment set to be released in the 4th Quarter. This is one of the only advanced Platinum and Palladium deposits in North America which could eventually rival Stillwater. Unlike gold and silver, palladium and platinum are outperforming. One could buy Stillwater, a North American PGM Producer with a market cap of $2 billion or they can look at this junior trading with a market cap under $60 million. I have time and am looking for outsized gains and leverage in what may be the next Stillwater.

The time to buy and research the highest quality assets are during these sell-offs when the gold and silver charts get aborted and as support is violated. A break into new lows may set off a margin call where the price could move down rapidly. At that time some of these companies should be bought and not sold into the panic. Capitulation and when the sentiment is extremely negative is when the best buys can be found. Look for major capital to come into these situations after the weak hands are shaken out.

Investors expectations about the US recovery may be overblown. The US dollar is strong now because Europe is very weak now as they are in a major conflict with Russia over Ukraine. The US Dollar is being bought as a purported safe haven temporarily as investors expect the ending of QE.

Capital should eventually transfer from overbought equity and bond markets into commodities and precious metals. This has not been seen yet and I may be a little early, but history is on my side that hyper-inflations follow deflations. Better early than seconds too late.

Most of the investors and companies at this conference were the high quality survivors during the bear market that are still able to raise capital despite gold correcting more than 30% over the past couple of years. These winners tend to be the biggest winners in the coming bull market. These discounted valuations in the juniors have not been seen in the history of the junior markets.

The smart funds, major miners and high net worth individuals attended as the strategy may be finding the best stories that will not only survive but come out stronger after the final low in precious metals is formed.

The precious metals are in the longest bear market since Bre X. The US dollar and S&P500 are irrationally overbought. Gold and silver may once again test the 3 year lows at $1200 gold and may break that support causing a panic sell-off which ends in capitulation.

A flush out could be coming to mark the extreme bottom and turning point in the precious metals bear market. This is the best time to have a roster of high quality juniors with strong treasuries, excellent assets, management with track records and clean share structures.

Don’t panic as this is when some of the smart contrarian money will buy these real assets for even more pennies on the dollar then what they are trading at now. Look at 2009 after the credit crisis when so many people walked away from their homes only to try to buy back in at much higher levels. Don’t get sucked into the US Equity and Dollar euphoria as investors forget about the risks of all the printing of this money. Don’t sell out your junior miners for pennies on the dollar at possibly the worst time.

Remember this is the longest bear market in the juniors since the Post Bre X 1997-2001 debacle. The sentiment may be at the point of extreme capitulation causing a panic sell-off.

That is why the smart money may be ready to pounce on capitulation into the highest quality juniors. The extreme negativity when there are only sellers usually marks the bear market bottom.

Disclosure: I am long juniors mentioned in this article and they are website sponsors so conflicts of interest apply.

The Federal Reserve’s third quantitative-easing campaign is on track to wind down in late October. At that point the Fed will likely stop printing new money to buy bonds, a sea-change shift with ominous implications for the stock markets. Their entire surreal levitation during QE3 mirrored the huge growth in the Fed’s balance sheet from QE3’s bond monetizations. When they cease, another major selloff is likely.

QE3’s impact on the global financial markets has been vast beyond belief. The Fed launched QE3 in September 2012, just before the important United States elections. This goosed the US stock markets in that critical final couple months ahead of the elections, right when they were on the verge of selling off dramatically. Odds are very high that the Fed’s brazen market manipulation gave the election to Obama.

In the 28 presidential elections since 1900 prior to that 2012 one, the stock markets rallied in September and October 16 times. The incumbent party won 15 of those elections! And during the 12 times when the stock markets fell in September and October, the incumbent party lost 10. The Fed choosing to launch a stock-market-boosting QE campaign in those pre-election months forced stock markets higher.

If the S&P 500 (SPX) had dropped as it was set to do in September and October 2012, Obama would’ve almost certainly been a one-term president. The Fed’s colossal market and political manipulation was no accident. Since QE2, Republican lawmakers had been highly critical of the Fed’s money printing to buy bonds. The low interest rates that spawned enabled Obama’s record debt-fueled spending binge.

Since the Fed faced serious challenges to its independence all the way up to its very existence from a Republican president and Congress, it massively intervened in the markets to sway an election. And QE3 just got worse from there. The Fed expanded it to include direct monetizations of US Treasuries a few months later in December 2012. That forced rates lower, farther fueling Obama’s epic deficit spending.

QE3 was far different from QE1 and QE2, which were finite from their births. QE3 was the Fed’s first open-ended debt-monetization campaign, with no prescribed limits. This potentially unlimited scope of QE3 helped create an exceedingly unfortunate side effect in the stock markets. Since QE3 had no defined end, stock traders figured it would be around to backstop stock markets more or less indefinitely.

Led by uber-inflationist Ben Bernanke, the Fed’s dovish communications fanned this popular belief among traders. Over and over during QE3 the Fed implied that it was ready to act, in effect to increase the scale of QE3’s monthly money printing to buy bonds, if the stock markets slid. This incessant Fed jawboning left stock traders utterly fearless, as they figured the Fed would arrest any major stock-market selloff.

So every dip was quickly bought, leading to the stock markets soaring. The SPX blasted 29.6% higher in 2013, the only full year of QE3! And this flagship index is up 39.5% since QE3’s birth. And it wasn’t like the stock markets were low before the Fed hatched its QE3 scheme. As of the day before, the SPX had powered 112.3% higher over 42 months in a very large cyclical bull. Stock markets were already lofty.

Healthy stock bulls take two steps forward followed by one step back, major uplegs are followed by sharp corrections. These corrections, SPX selloffs between 10% and 20%, are essential as they help keep sentiment balanced. They bleed off greed before it grows too excessive and pulls too much future buying forward, killing the bull. The Fed’s implied backstop with QE3 short circuited this natural and crucial process.

When QE3 was launched just before those November 2012 elections, it had already been 11 months since the end of the last SPX correction. Typically they happen about once a year or so on average. And since QE3’s debt monetizations have been in force, the necessary sentiment-rebalancing selloffs have become smaller and farther between. Today the SPX is up to an insane 35 months since its last correction!

Provocatively the two previous full-blown corrections of this mighty cyclical stock bull cascaded right after QE1 and QE2 ended. When QE isn’t in force, the Fed’s implied backstop vanishes. So traders are not as quick to buy stocks indiscriminately, and sellers aren’t scared away. The Fed’s Federal Open Market Committee is on track to end QE3 at its upcoming October 29th meeting, an ominous omen for stocks.

Without QE3, the Fed can no longer backstop stock markets or even claim it can do so. Thanks to Ben Bernanke’s disastrous zero-interest-rate policy that’s robbed savers blind since December 2008, the Fed can’t cut interest rates if stock markets fall. And ramping up a QE4 is very unlikely if the Republicans regain control of the Senate in this year’s elections, as they could potentially vote to revoke the Fed’s very charter!

The implications of a post-QE world are vast for the stock markets. To better understand why, you need to grasp the mammoth scope of the Fed’s third quantitative-easing campaign. This chart shows the Fed’s balance sheet since 2008 when QE was initially born. This data is stacked within the Fed’s total balance sheet (orange), with US Treasuries (red) sitting on top of mortgage-backed securities (yellow).

I’ve written comprehensive essays outlining the history of QE, what the Fed did when and why it decided to act. But for our purposes today, let’s focus on the big picture. Prior to QE1’s birth during 2008’s once-in-a-lifetime stock panic, the Fed’s balance sheet averaged $875b in the first 8 months of that year. Today that number has ballooned an astounding 5.0x to $4377b. QE has quintupled the Fed’s balance sheet!

When central banks buy bonds, they do so by first creating the money necessary for the purchases out of thin air. It is pure inflation. And when bonds are bought with this new money, it is transferred to the bond sellers to spend immediately as they see fit and the bonds are transferred to the Fed’s balance sheet. So the $3502b in bonds the Fed has purchased so far equals the money it has printed for QE.

The Fed’s modus operandi for its three QE campaigns, and an intervening “twist” operation in the middle, has been very consistent. The Fed, ever cognizant of political pressure and withering attacks from Republicans who hate money printing, first launches each campaign at a relatively modest scope. And then soon after once the initial political storms blow over, it greatly expands the scale of its bond buying.

QE1 initially started at $600b, but then was soon expanded to a staggering $1750b total. Soon after it ended, QE2 started at $300b but was shortly tripled to $900b. Twist, the Fed selling the shorter-term Treasuries it held to buy longer-term ones to manipulate long interest rates lower, was also expanded. And QE3 followed this template, $40b in monthly buying shooting up to $85b total just a few months later.

QE3 was unique in its open-endedness, the Fed set no limits to its size up front as it did with QE1 and QE2. QE3 ended up running full-steam for all of 2013, boosting the SPX to its massive late-bull gain last year. But last December, the Bernanke Fed finally decided it better start slowing its epic monetary inflation before the inevitable resulting price inflation got out of control. So it started “tapering” QE3.

At every meeting since then, the FOMC has continued to slice away another $10b of new monthly QE3 buying starting the following month. And with QE3 down to just $25b per month today, the Fed only has room to do two more tapers since it has talked about taking the final $15b away at one time to avoid an undue trader fixation on that last $5b. And that full QE3 tapering should happen at the FOMC’s late-October meeting.

At that point, QE3 will have grown to $800b in mortgage-backed securities and $790b in Treasuries purchases for a total of $1590b. This won’t quite reach QE1’s supreme $1750b girth, but it sure dwarfs QE2’s $900b. It’s the Treasuries portion of QE3 that is the key component. That ran $300b in QE1 and $600b of new buying in QE2, so QE3’s massive $790b of buying easily takes the QE Treasuries crown.

All market interest rates key off of the “risk-free” yields of US Treasuries. So when the Fed prints money to buy Treasuries, it effectively pushes down interest rates for the entire markets as its artificial demand forces Treasury yields lower. In addition, the money printed and paid to the Obama Administration to buy Treasuries is immediately spent. So it is directly injected into the real economy, driving price inflation.

The Fed has been the dominant buyer of US Treasuries during the QE era since the 2008 stock panic, purchasing $1956b worth. This works out to just over 25% of all the Treasuries issued since the end of the US government’s fiscal-year 2008! Without the Federal Reserve buying up a quarter of all the debt the Obama Administration’s extreme overspending has burdened America with, rates would be far higher.

The extraordinary stock-market levitation spawned by the Fed’s implied backstopping during QE3 blasted US stocks up to dangerously-high valuations. And the primary reason euphoric stock traders have rationalized them away is bond yields remain super-low thanks to the Fed’s brazen interest-rate manipulations. But once QE3 ends, so does that downward pressure on Treasury yields and interest rates.

As rates rise, which is inevitable with a quarter of the world’s demand for Treasuries vanishing, stocks are going to look more and more overvalued relative to bonds. That alone is going to eventually lead to some serious selling pressure reemerging in the stock markets. And once a material selloff gets underway and the Fed’s implied backstop through QE3 is gone, that overdue selling is going start cascading.

Prudent investors and speculators today don’t have to guess about what the end of QE3 means for the lofty Fed-inflated US stock markets. We have the precedent of the ends of QE1 and QE2. This next chart looks at the flagship S&P 500 stock index superimposed over the Fed’s balance sheet. And out of all the many thousands of charts I’ve created over the years, this probably tops the heap as the scariest.

The stock markets are forever cyclical, so after the last cyclical bear that climaxed after 2008’s stock panic a new cyclical bull was justified and inevitable. I was one of the few contrarians who called for that bull right at the March 2009 bottom when bearishness and despair were suffocating. Nevertheless, this bull had a very high correlation with the Fed’s balance sheet. When QE was underway, stocks powered higher.

But whenever the Fed tried to wean complacent traders off the QE drug, the stock markets corrected hard. Right as QE1’s massive bond monetizations were ending, the SPX tumbled 16.0% in 2.3 months in this bull’s first correction. Provocatively the stock markets weren’t able to regain their footing until the Fed quickly stepped in to announce QE2. The timing of that mushroomed the Fed-backstopping-stocks notion.

Then during the QE2 money printing and bond buying the stock markets again climbed relentlessly without any correction-grade hiccups. But again the moment those QE2 debt monetizations ceased and the Fed’s balance sheet stopped rising, the SPX plunged again. This second and latest correction of this cyclical bull hammered 19.4% off the SPX in 5.2 months. This almost hit the 20% cyclical-bear threshold!

And once again it looked like the SPX didn’t bottom naturally, but through Fed intervention. The low of that last correction happened just as the Fed was announcing its Twist campaign to twist the yield curve by selling shorter-term Treasuries it owned to buy longer-term ones. This helped boost the SPX again into another major upleg, which was running out of steam and looking toppy in late 2012 as the US elections neared.

The SPX had actually stalled out in April 2012, without a single new high seen until September 2012 after first the European Central Bank and then the Federal Reserve announced new campaigns to buy bonds. After 5 months of zero upside progress before the ECB and the Fed’s QE3 announcement, would US stock markets have rallied into the 2012 elections without the Fed’s help? Odds are no way.

As Treasury monetizations are far more potent than mortgage-backed-bonds ones, the stock markets were weaker after QE3’s initial MBS buying and the resulting Obama win. But once the Fed expanded QE3 to include Treasuries in December 2012, the SPX started levitating. It soared in a very tight trading range mirroring the Fed’s ballooning balance sheet, with no material selloffs to rebalance sentiment.

This chart implies the entire reason the SPX rallied from 1500, the secular-bear resistance it would have almost certainly naturally topped at without the Fed’s manipulations, was QE3 and its accompanying dovish jawboning. In my decades of trading, I’ve probably never seen a more ominous chart than this SPX levitation perfectly tracking the Fed’s soaring balance sheet. The SPX/QE3 correlation is just stellar.

If the ends of QE1 and QE2 both sparked major corrections, why shouldn’t the end of the far-larger (in Treasury terms) QE3? Back in mid-2010 and mid-2011 when those earlier quantitative-easing campaigns ended, the stock markets where nowhere near as high and euphoric as they are today. Yet stocks still corrected hard when the Fed’s inflationary tailwinds, and implied backstopping, were removed.

Provocatively today’s lofty stock-market valuations are similar to those seen at the major SPX toppings as QE1 and QE2 ended. When all 500 SPX component companies’ individual trailing-twelve-month price-to-earnings ratios are averaged, they reveal the SPX trading at 26.6x near the end of QE1 and 24.1x near the end of QE2. The latest simple-average read for this metric as August 2014 ended was 26.1x.

This is dangerously high, as 28x is actually the historical threshold for a bubble! Add these extreme overvaluations on top of the prevailing extreme euphoria and complacency, cyclical-bull-topping technicals, and a greatly overextended cyclical bull, and it is hard to imagine the end of QE3 not spawning a major selloff! It is actually far more likely to cascade into a new cyclical bear than stay a mere correction.

Again the stock markets are forever cyclical, cyclical bulls are always followed by cyclical bears. The average size and duration of a cyclical bull within a sideways-grinding secular bear like we’ve seen in the stock markets since 2000 is a doubling in 35 months. Today’s bull has nearly tripled, up 196.1%, in 66 months! It is far too big and far too old, meaning a selloff’s highest-probability outcome is the next cyclical bear.

Cyclical bears tend to cut stock prices in half over a couple years or so, they are dangerous beasts not to be trifled with. And once QE3 is done, there is no more Fed backstop in place to motivate traders to instantly buy every minor dip. With short rates zero-bound thanks to ZIRP, the Fed has no room to cut interest rates to arrest a stock-market swoon. And again QE4 is very unlikely in this political environment.

The election-year stock-market studies I’ve seen are for the major presidential election cycles, not intervening midterm elections. But the results are likely similar. Rising stock markets make Americans feel better about everything, so we are more likely to vote for incumbents for more of the same. But we feel worse when stock markets are weaker, making us more prone to kick out the bums in hopes for change.

So if the stock markets are weaker in September and October 2014, the odds grow that the Republicans are going to retake the Senate. They already have an edge, as Obama and the Democrats are very unpopular for a variety of reasons including the disastrous and punishingly-expensive Obamacare burdens on Americans. Republican voters skew older and whiter too, more likely to vote in midterm elections.

The major corrections when QE1 and QE2 ended actually began a little earlier in anticipation, and it is reasonable to expect stock traders to start selling ahead of QE3’s rapidly-approaching end too. And since the Fed won’t risk the political wrath of the Republicans who will likely soon control the full Congress again, it isn’t going to launch a QE4 soon. So any stock selloff won’t have any hope of a Fed rescue!

Thus the end of QE3 is exceedingly ominous for these lofty stock markets. A major SPX selloff, whether it is merely a 20%ish correction or a new cyclical bear, will drive devastating losses in everything from the high-flying momentum stocks to the conservative SPX-tracking ETFs like SPY. And it has been so long since we’ve seen any material selloffs that the resulting hit to complacent and euphoric sentiment will be massive.

How can you protect yourself in this coming swoon? Buy gold. The entire precious-metals sector was abandoned and left for dead during the Fed’s QE3-driven SPX levitation. But alternative investments will return to vogue in a big way once normal stock-market behavior including selloffs resumes. The gains coming in the beaten-down precious-metals sector will be vast as flight capital floods in looking for safe havens.

The big risk of serious inflation igniting thanks to QE’s huge monetizations remains too, which will act like rocket fuel for gold. Even when QE3’s new buying ends soon, the Fed will still have $3.5t of bonds stuck on its balance sheet! That means $3.5t of new money injected into the economy that could start bidding on goods and services and driving up prices any time until the Fed can unwind its QE bonds bought.

To thrive when this SPX levitation reverses, you need good contrarian advice. The shills on Wall Street will claim everything is great, don’t worry, until late in the next cyclical bear. At Zeal we are hardcore contrarians who have long walked the walk. We tell it like it is, warning our subscribers when markets are topping and due to fall so they can sell high. And we help them buy low in other markets that are unloved.

The bottom line is the Fed’s third quantitative-easing campaign is due to end in late October. QE3 has massively boosted the stock markets, driving their extraordinary levitation of the past year-and-a-half or so along with the Fed’s jawboning. Once QE3 ends, so does the Fed’s implied backstop of stocks. Any selloff can’t be met with rate cuts thanks to ZIRP, and a new QE4 is extremely risky politically for the Fed.

So the overdue stock-market selling pressure is likely to cascade with the Fed no longer available to arrest it. Major stock-market corrections emerged as both QE1 and QE2 ended, and the stock markets are far more extreme today as QE3 winds down. And once again this end-of-QE selling is likely to start in anticipation of the actual event, an ominous omen for stocks that mirrored QE3’s Fed balance-sheet growth.

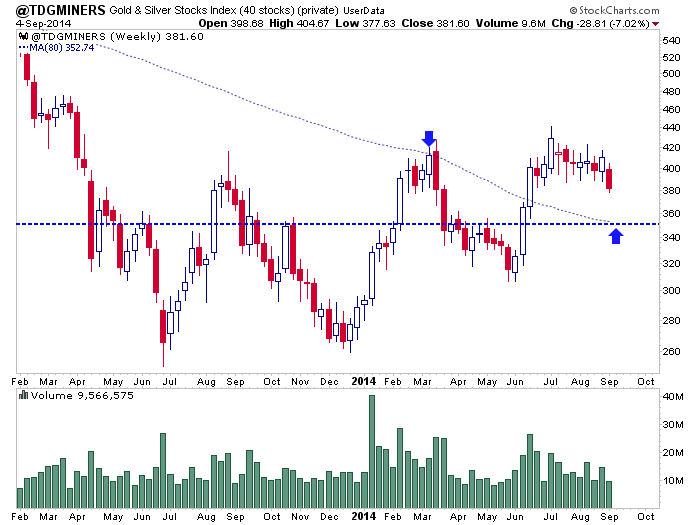

In recent weeks we wrote about the ongoing consolidation in precious metals miners. We touched on the history of September, not as a bullish month but as an important inflection point. With the miners holding up well and Gold still holding its lows we thought a breakout could be coming. Yet we’ve been whipsawed before. Several times over the past year (and as recently as late July) we’ve written about the possibility of a final low in Gold to precede the next impulsive advance in the miners. These scenarios came to a major head this week and the nasty decline across the entire sector suggests the bears are back for one last time.

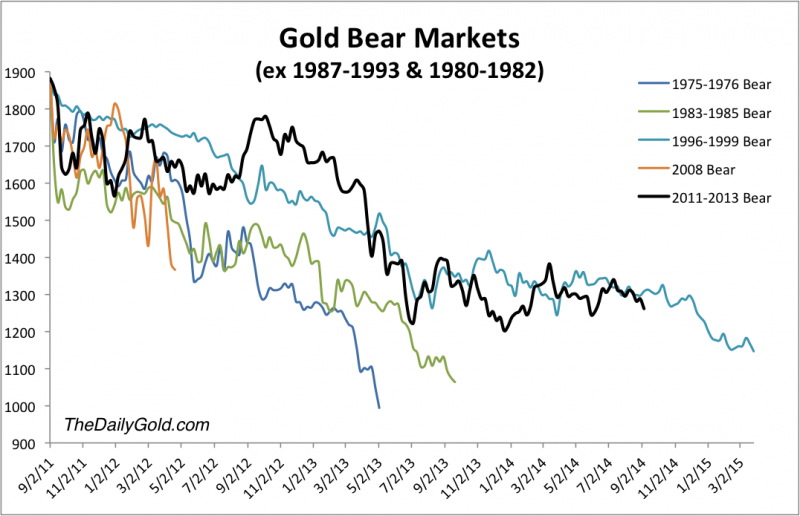

Below is our chart for Gold’s bear markets which are scaled to the 2011 peak. We exclude the two extreme bears (one lasted six years while the other was the post bubble crash). Longer bears tend to be less severe in price whereas the most severe bears in price tend to be short in time. Examples of that include the 1975-1976 and 1983-1985 bears. The 1987-1993 bear (the longest) only shed 35% while the 1996-1999 bear, which lasted three and a half years bottomed well above $1100 on the current scale. History makes a strong argument that while a new low is likely, anything much below $1100 appears unlikely.

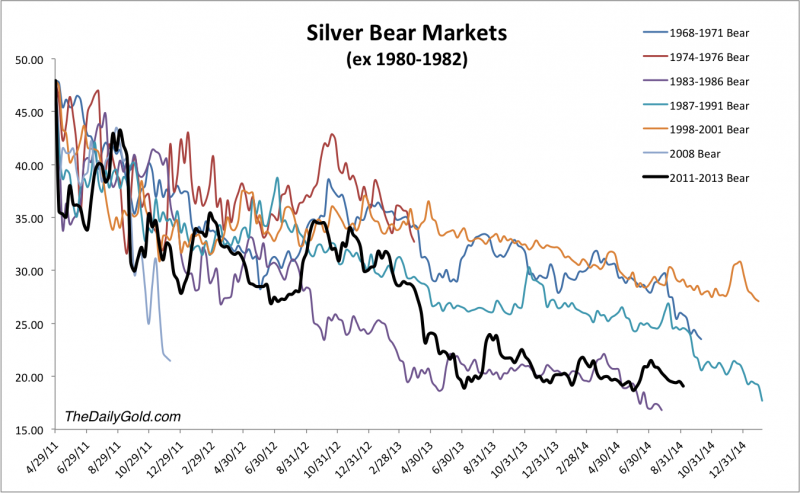

The next chart shows all of the bear markets in Silver sans the 1980-1982 bubble crash. A close below $18.82 would mark a new weekly low. This analog makes a very strong case that Silver’s bear is likely to end in the coming weeks or months.

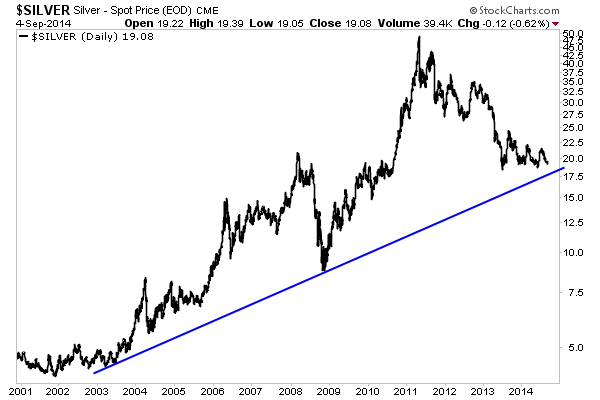

Staying with Silver, we note that while Silver could make a new low it would soon find 11-year trendline support. This is another reason we will be very bullish on Silver if it breaks to a new low.

So how does affect the miners?

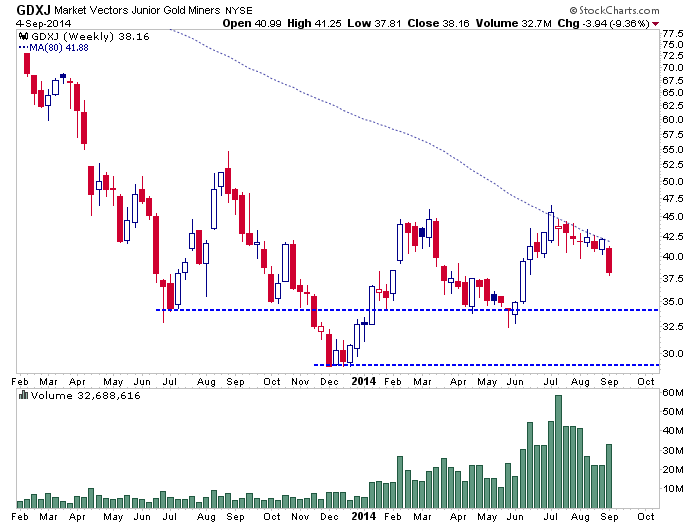

Until days ago the miners looked very strong and on the cusp of a breakout. That possibility has gone out the window. The chart below shows a nasty reversal in our top 40 index which is down 7% on the week and officially broke its consolidation low on Thursday. The index closed Thursday at 382 and the next strong confluence of support is near 350.

GDXJ is down 9% this week and sliced through support on big volume. The next strong support is the previous low around $33. There is nearly 15% downside to that strong support.

Going forward, $1240 Gold and $1200 Gold on a weekly basis are key levels to watch. The miners are very oversold in the short-term and should bounce along with Gold (from $1240). However, the bears have regained control. The bear analogs are quite clear and the miners have suffered major damage which implies more downside. I don’t envision a buying opportunity for the miners until Gold and Silver make new lows. This week could mark the start of that final plunge that has eluded us several times over the past year.

1. Gold has a rough general tendency to decline during the week leading up to the release of the US Employment Situation Report (jobs report).

2. Following the release of that report (Friday at 8:30AM), gold tends to begin a decent minor or intermediate trend rally.

3. Gold has exhibited this trading pattern for quite some time. It is likely to continue to do so, for the foreseeable future.

4. Please click here now. On this two hour bars chart for gold, I’ve highlighted the gold price action during the week leading up to the release of the August 1st jobs report. The minor trend decline is clear.

5. Please click here now. Here, I’ve highlighted the nice rally that began following the release of that report. The minor trend strength of the rally is clear.

6. To view the current gold price action, please click here now. The next jobs report is only a few days away, and gold is exhibiting a typical minor decline leading up to the release of the report. The minor trend decline is clear.

7. It’s important that the Western gold community doesn’t confuse the jobs report trading pattern for gold, with the big picture for gold.

8. The jobs report moves the price of gold in isolation from the big picture, and does so in a very minor way.

9. Amateur investors that use leverage to invest in gold, will easily be frightened by the price action created by night time liquidity flows from funds and banks on the COMEX, particularly as the jobs report approaches.

10. Many of the gold market sell-offs that precede the jobs report tend to begin around 2AM – 4AM New York time. Some gold community analysts have suggested that this is market manipulation that regulators should investigate on a trade by trade basis.

11. Regardless of whether there should be an investigation or not, leveraged gold investors should “dial down” their use of leverage, so they don’t read more into the gold price action than is actually there. Gold can easily trade in the $1250 – $1260 range before the release of Friday’s jobs report, and investors need to be able to handle that price action, without breaking down emotionally.

12. Please click here now. That’s the daily bars chart for gold. Technically, gold appears to set to rally from around the time the September 5th jobs report is released.

13. Is the rally likely to be a little one, or a big one? For the probable answer, please click here now. That’s the weekly bars chart for gold. It’s clear that larger rallies tend to occur after the price stoker (14,7,7 Stochastics series) lead line has declined to the 10 area.

14. It’s at about 38 now, which is a decent position, but one usually associated with minor trend rallies, rather than large intermediate trend movements.

15. Fundamentally, there’s a lot of good news for gold. Gold is the world’s strongest asset, and it’s getting stronger with each passing day. Please click here now. It appears that Chinese commercial bank holdings of gold have exceeded the gold held by the Chinese central bank, and their holdings appear to be accelerating.

16. During the first half of 2014, Chinese gold demand was not spectacular, but it was decent, and it appears to be rising again.