Founder of CEO.ca, Tommy Humphreys, had the opportunity today to discuss the current state of the junior mining industry, as well as his new journalistic endeavors, at the Subscriber Investment Summit. On the wash out in the junior mining space, Humphreys commented “… that this is not the time to buy a basket of juniors and hope there will be hot money coming in after. [This is] a time where we can focus and pick fewer stories with smaller share counts and better management teams.”

Tommy Humphreys also had the opportunity to discuss the mining newsletter – Resource Opportunities – that he will be part of, in collaboration with Lawrence Roulston. Among other objective points, the goal of the newsletter will be to avoid the industry distractions and focus on results-driven junior mining companies with strong management styles.

See the full presentation on YouTube below.

Last week we argued that the underperformance of the gold miners during Gold’s rebound was a bad sign. Since then the miners have plunged to new lows while Gold appears to be at the doorstep of a major breakdown below $1180. It shouldn’t be a surprise as it would simply be following the miners and Silver. The current bear market is getting very long in the tooth but it is not yet over. We see more losses ahead before a potential lifetime buying opportunity.

The HUI Gold Bugs Index is obviously very oversold but its not yet at strong support. It closed Thursday at 164 but should fall another 9% to support at 150. Currently the HUI is 26% below its 200-day exponential moving average and 19% below its 50-day moving average. The chart argues that those figures need to reach 40% and 27% before we deem the oversold condition extreme. If the HUI trades below 150 then it would mark an 11-year low. That is extreme!

Nick Laird of ShareLynx provided me data from the Barron’s Gold Mining Index (BGMI) which I uploaded to stockcharts.com. This index dates back to 1938 and allows for greater historical perspective. Data is updated weekly so I had to estimate the current price. The HUI, XAU and GDX are all down 10% or 11% on the week so I calculated a 10.5% loss on the week which is a price of 567. Lateral support, which dates back to the early 1990s as well as trendline support that dates back 50 years provide a strong confluence of support in the mid 400s. That is roughly 20% downside.

Another reason to expect more downside is Gold hasn’t even broken $1180 yet, though it may have by the time you read this. The price action has been textbook bearish. Gold failed to rally up to trendline resistance in the summer and then it declined in nine of twelve weeks. It rebounded for two weeks but quickly reversed at the 10-week moving average which is sloping down sharply. Also, the net speculative position in Gold as of a week ago was 25% of open interest. There are a fair amount of longs left to capitulate. Gold’s downside support targets are $1080, $1040 and $1000.

We’ve been warning for several weeks of the near-term downside potential in precious metals. It is being realized but that does not mean its over. The miners plunged to new lows in recent days yet they are likely to move lower before a major turn. Our work above suggests a minimum of 9% downside potential and as much as 20%. Meanwhile, Gold could fall another 15% to strong support at $1000. Opportunities are coming but they are not here yet. We want to see Gold and gold stocks decline further so that they become extremely oversold as they reach major support levels. That is the combination that could produce a lifetime buying opportunity in the weeks or months ahead.

The commodity equities are selling off as The Fed halts QE3. Commodities, metals and the junior miners are hitting multi year lows and falling below 2008 credit crisis levels. This is not a time to panic but continue to accumulate as the bear market may be reaching the final capitulation stage. This decline may be a sign that the quantitative easing may have lifted stock market indices, but it did little to improve demand and growth in the economy reflected by demand for energy and metals.

I just returned from the New Orleans Conference which was headlined by Alan Greenspan the former Federal Reserve Chairman from 1987 to 2006. It is interesting to note that Greenspan has become bullish on gold. He believes that quantitative easing did not accomplish what it was designed to do. It helped lift the stock market and stabilize the real estate market, however it fell short as the US economy is not really recovering like it should have. Gold is the best hedge against this uncertainty.

I happen to agree with him. Real estate values have jumped and stock market indices are hitting new highs. Only a small fraction of the US has gotten wealthier as the real economy continues to struggle. Greenspan is continuing to warn about the Fed’s exit from quantitative easing, which I am quite concerned about as well. Look at the recent volatility in the US dollar and treasuries. When the US dollar is moving parabolically higher like a dot com stock I exercise caution as this could have drastic effects on foreign exchange markets and international trade. The way to hedge against this volatility caused by government interventions and manipulations is precious metals and commodities. Accumulate during a bear market when it is on sale. A turnaround could be right around the corner.

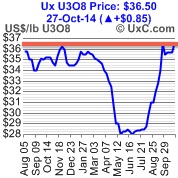

Contrarian value investors should be looking at emerging junior uranium producers and explorers that are still trading for pennies on the dollar. The uranium spot price has made a dramatic move higher as Japan begins turning back on nuclear reactors and large producers such as Cameco announce production declines. There is a lot of buying in the spot market and it should be soon reflected in the performance of the junior uranium miners (URA). Look for a breakout past $37 on the U3O8 spot price.

A town in southwest Japan approved the restart of a nuclear power station. This is a sign that if Japan who suffered greatly from the Fukushima disaster can turn back on reactors then the rest of the world should continue to build newer and safer next generation nuclear reactors. Japan turned off the nuclear reactors following Fukushima in March of 2011. However, nuclear reactors may start coming back online in 2015. Japan’s economy can no longer handle importing expensive oil and gas. Nuclear is vital to Japan’s economy and used to supply close to one-third of their overall energy needs.

Don’t forget that he US is the largest consumer of nuclear power yet produces less than 10% of what it demands every year. For decades, America relied on Russia to supply cheap uranium in the megatons to megawatts program. This deal concluded at the end of 2013 and Russia could continue tightening its control on uranium as a bargaining chip against economic sanctions from the West.

Smart money is buying small emerging junior uranium producers in the US where demand far outpaces supply. Anfield Resources Inc. (TSX.V: ARY)(OTCQB: ANLDF) released news that they are acquiring the Shootaring Canyon Uranium Mill from Russian nuclear giant Uranium One. They just announced approval from the Utah Division of Radiation Control to transfer the license.

Anfield acquired a portfolio of uranium assets around the mine with historical estimates of 6.8 million pounds of uranium. For only $5 million in cash and shares paid out over 4 years Anfield has jumped to become a major contender in the U.S. uranium industry.

Anfield now owns one of three licensed uranium mills in the United States with one of the largest uranium land packages of more the 65k acres. Owning the mill is crucial as it allows the company to have control all the way from mining to production of yellowcake. Anfield could be a major supplier of uranium to help with the current supply deficit in the United States.

As Anfield Resources CEO Corey Dias said, “We are extraordinarily excited about the acquisition at it is transformational for the Company. With the acquisition of one of only three licensed and permitted uranium mills in the United States, we have significantly accelerated our timeline with regard to becoming a uranium producer. The mill is currently in good condition as it has been on continuous care and maintenance since it ceased operations.” With a market cap of only $10 million Anfield may be a cheaper and a more undervalued situation than some of its peers.

Disclosure: I own Anfield Resources and the company is a website sponsor.

- As gold traded in the $1250 – $1255 area a week ago, I suggested the price would immediately decline from there, to the $1230 area or lower.

- That’s exactly what happened. Unfortunately, by late yesterday afternoon, the decline had become a bit frightening for some gold price enthusiasts. A nasty wave of selling quickly drove the price down to about $1222.

- To view the current daily chart, please click here now. A sell signal is currently in play on my “price stoker” (14,7,7 Stochastics). That’s clearly visible at the bottom of the chart.

- This is a quite reliable oscillator for minor trend price action, and the FOMC meeting that gets underway today is likely the fundamental price driver creating the price stoker sell signal.

- Hedge fund managers often like to move to the gold market sidelines, in advance of these FOMC meetings, and that appears to be the case this week.

- I expect that gold could stay under some pressure this week, until Friday’s US Employment Situation report is released, at about 8:30 AM on Friday.

- Please click here now. That’s the hourly bars chart. If gold were to trade in the $1219 area, that would be a rough 50% retracement of the $1183 – $1255 rally.

- Such pullbacks are perfectly normal after decent rallies. Please click here now. That’s the weekly chart, and the overall picture is a healthy one.

- Chinese demand is starting to rise again and Indian demand is superb. Gold is well-supported here, and investor fear is unwarranted.

- It appears that most gold analysts expend vastly too much energy trying to call gigantic rallies and declines, in history’s greatest asset. Most of the time, gold trades with modest volatility, and the price often moves sideways for substantial periods of time.

- On that note, please click here now. Double-click to enlarge. That’s the GDXJ weekly chart. Like gold itself, junior gold stocks continue to trade sideways.

- Note the enormous volume. A changing of the guard from weak to strong hands is good news, but it doesn’t necessarily mean that the price goes a lot higher, let alone in a short period of time. To attract institutional “hot money”, GDXJ must trade above $54.56 for many weeks.

- Watch the 14,3,3 Stochastics series, for an upside breakout above the 20 line, and watch for a crossover buy signal on the PPO indicator. That will be the first sign that GDXJ could be ready to rally to $54.56.

- The stock market is creaking. Several Fed presidents have expressed concerns about the level of interest rates. Please click here now. That’s the quarterly bars ratio chart of the Dow versus T-bonds.

- The Dow has not outperformed bonds since the year 2000.

- If it does outperform in 2015, I think it will simply be because bonds fall more than the Dow falls, as the Fed shocks most money managers, and raises interest rates.

- Please click here now. That’s the daily CRB commodity index chart. I’m looking for a big rally in “commods” in 2015. Here’s why:

- In the late 1970s, the Fed unveiled massive rate hikes, ostensibly to battle inflation that was almost out of control. Commodity markets crashed.

- In contrast, the Fed is not currently dealing with inflation that is out of control. A rise in rates in 2015 could cause the dollar to rally a bit more than it has against other fiat currencies.

- It’s important to understand how bonds prices move. When rates are very close to zero, as they are now, even a modest rise in interest rates can create a dramatic drop in the price of bonds.

- Junk bond prices are most susceptible to interest rate hikes. These bonds could look like they got hit with a financial nuclear bomb, if the Fed hikes rates even modestly.

- A number of key Fed officials have expressed substantial public concern about what they term the “disconnect” between the Fed’s planned interest rate policy in 2015 (rate hikes), and the perception of Wall Street money managers and economists, about what is coming (more QE, more free money). I’m in 100% agreement with these officials.

- Gold, commodities, and the general economy of America have little to fear from the Fed in 2015.That’s not the case for global stock markets, global bond markets, and global junk and mortgage markets.

- Faced with the twin horrors of the taper, and India essentially in handcuffs, gold has fared very well in 2014. Import statistics suggest that the citizens of India have now moved past the government restrictions as a concern, and are eagerly bidding for gold. As the Fed likely hikes rates in 2015, I expect gold to fare equally well, and perhaps much better!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

Risk taking is a natural part of life, especially in the capitalist system where the greater the risk, the increased potential reward. The TSX Venture Index which is made of the Canadian start ups in junior mining and high tech is hitting lows not seen since 2002 and the 2008 Credit Crisis.

Despite the record amount of global QE, investors are sitting in US dollars, treasuries and large caps rather than investing in new ideas especially in the resource arena. Higher risk capital entering start ups especially in junior mining has reached a new low as investors have been seeking liquidity and dividends.

Clearly, the strong global economy purported on CNBC has not yet been reflected on the TSX Venture Exchange yet. However, that may change over the next 3-5 years and now may be the time to buy up the best resource assets at historic lows. Over the past decade, The TSX Venture has at least doubled or tripled from these historical low levels where it is currently trading.

Major rallies over the past decade began when the Venture was trading below $1000. The Venture is trading at $790 as this is written. I wouldn’t be surprised to see a major bounce to the $2400 or $3400 level like it did back in 2009 and 2003.

The Junior Gold Miner (GDXJ) ETF appears like it could be approaching a major bottom in the $29 zone and could form a double bottom with the December Low over the next couple of weeks.

I just returned from the New Orleans Conference where I met with management of some exciting gold companies on the verge of major gains as they reach fundamental catalysts.

1)Pershing Gold (PGLC) just announced a financing with some of the most active and smartest US investors and now sits with over $20 million in cash, a fully permitted heap leach facility and an expanding gold resource base in Nevada. One of the insiders has been buying aggressively in the open markets which is a positive sign for a turn in the company. I expect Pershing to be uplisted to a major exchange such as the NYSE or Nasdaq in the near term. With the former Franco Nevada, Chief of US operations as its current CEO the weak junior mining environment could play into the advantage of cash rich and deep pocketed Pershing to pick up quality mining assets at a bargain to complement near term production at Relief Canyon.

I am excited to see this company break out of its recent downtrend, get uplisted and become recognized by the institutions possibly by the end of 2014.

2)Red Eagle Mining (RD.V or RDEMF) just published a Definitive Feasibility Study showing some of the best economics in the business on their San Ramon Deposit in Colombia. All that they are waiting for is the final environmental permit which could come soon and really boost the value of this asset. Red Eagle has some strong shareholder support from Liberty Metals and is one permit away from building one of the world’s most economic mines. Don’t think the project is toosmall, there is a lot of room for growth and was drilled in a way to get it into production the most cost effective way. The CEO Ian Slater did an excellent job to advance this project to get to a construction decision without blowing out its share structure and minimizing dilution.

3)Canamex Resources (CSQ.V) is hitting arguably the best drill results in Nevada right now on a regular basis and have attracted investment dollars from two NYSE gold producers such as Hecla and Gold Resource Corp. There are assays pending from both the Penelas East Discovery and historic resource area. I first told you about Canamex back in 2013 and it is now up 130% in 2014 as they are making a great discovery in Nevada at their Bruner Project. Canamex just announced step out drill results at the far northern end of Penelas East over 100 meters away from the nearest neighbor drill result. They intersected 22.9 meters of 3.29 g/tonne, which means that the project remains wide open to the north. A second core hole was drilled and intersected the high grade target. Results should come out in early November.

Canamex is pulling back to its 200 day moving average. It may be a good area of support to add as it is in a strong uptrend.

Disclosure: I own all 3 companies and they are all website sponsors. Do your own due diligence before and during your investment.

This fall, the Federal Reserve is expected to finally wind down its latest monthly bond-buying program known as Quantitative Easing. What will the end of this $4 trillion (and counting) debacle mean for precious metals markets?

The answer may be, not much.

That’s not to say that gold and silver prices won’t move following the Fed’s final taper. But it is to say that widespread anticipation of QE’s end has already been priced into the markets.

The U.S. Dollar Index rallied strongly from July through September – in part on euro weakness and rising investor expectations that the economic data will come in strong enough to allow the Fed to terminate its bond-buying campaign. Nominal strength in the dollar exerted downward pressure on the PMs. Gold slumped, and silver fell even more sharply.

Metals Markets Often Move Counter to Popular Expectations

It’s worth recalling what happened when the current cycle of Quantitative Easing (officially, “QE3”) was announced in back September 2012. At the time, many analysts assumed that QE3 would provide an immediate boost to gold and silver prices. Instead, the metals markets responded counterintuitively. They declined for several months following the Fed’s announcement.

Fast forward to October 2014, and almost nobody expects the end of QE to be bullish for precious metals. In fact, speculative interest in gold and silver sits at multi-year lows. Hedge funds are collectively showing one of their lowest net long positions in the silver market on record.

The Fed’s final termination of QE won’t make the hot money crowd suddenly turn even more bearish on metals. That crowd has already positioned itself in anticipation of such an announcement. When the announcement comes, it could be a non-event for precious metals markets.

At the same time, it could spark a revolt against the U.S. stock and bond markets, which have heretofore been floating on a rising sea of Fed liquidity. Previous cessations of Federal Reserve stimulus programs have led to significant corrections in equity markets.

When the Fed Finally Hikes Rates, It Will Probably Be Chasing Inflation Higher

Of course, the Fed has no immediate plans to unload the more than $4 trillion in bonds it has accumulated on its balance sheet. Nor has it yet committed itself to actually raising its benchmark Federal funds rate, despite widespread expectations that it will do so by mid 2015.

Fed chair Janet Yellen stated recently, “The appropriate path of policy, the timing and pace of interest rate increases ought to — and I believe will — respond to unfolding economic developments. If those were to prove faster than the committee expects, it would be logical to expect a more rapid increase in the Fed funds rate. But the opposite also holds true.”

In other words, if the economic numbers (especially those related to employment) start coming in ugly, the Fed might refrain from raising rates – or even introduce a new stimulus program. Yellen has repeatedly indicated that stimulating job growth, as she sees it, takes precedence over fighting inflation.

That means the Federal Reserve may not raise rates until inflation begins spiraling out of control. In a Wall Street Journal survey of 30 economists, all but three expect the Fed to wait too long before raising short-term rates rather than move too soon.

In the months ahead, the financial media can be expected to speculate incessantly on the Fed’s next move and when it might come. Disciplined precious metals investors should ignore the Fed-gaming chatter and focus instead on what real interest rates are doing.

The Fed doesn’t directly control whether long-term or even short-term rates are positive or negative in real terms. Negative real interest rates, which refer to rates that sit below the inflation rate, are generally bullish for precious metals. Negative real interest rates can persist or even become more deeply negative while the Fed is raising the short-term rate.

That’s what happened during the great precious metals bull run of the late 1970s. The Fed was perpetually behind the curve on rate hikes as inflation galloped higher.

Mike Gleason, a Director at Money Metals Exchange, noted in one of our weekly audio podcasts this summer, “During the great gold and silver bull run of the late 1970s, the Fed wasn’t slashing rates. It was doing the opposite. The Fed kept raising rates, but it didn’t get out ahead of inflation until [then-Fed Chairman] Paul Volcker stepped in and jacked rates up to punishing double-digit levels.”

Market Conditions Remain Favorable for Accumulation

There is a widespread misconception that only rate cuts or more QE would be bullish for gold and silver. To the contrary, if rising inflation pressures force the Fed to raise rates, that would potentially be quite bullish for gold and silver as well.

Instead of fearing rate hikes, metals investors should actually look forward to the next rate-raising cycle. That’s when the biggest gains in gold and silver could come.

At some point, yes, real interest rates may turn positive and precious metals prices may get overextended to the upside. But neither situation exists under current market conditions.

Now remains a favorable period for savvy investors to accumulate physical precious metals while the herd isn’t paying attention, premiums on common bullion products are low, and spot prices remain significantly discounted from their highs of three years ago.

Investors waiting for money to flow into the mining sector may want to consider some alternative trading ideas in the interim.

Colombian focused oil producer Petroamerica Oil Corp. (PTA.TSXV) offers a good risk-reward profile at its current valuation.

With $65 million cash and $35 million debt, Petroamerica trades at $210 million enterprise value (market capitalization – cash + debt). Over 2014, the company expects to produce an average of 6,600 barrels oil per day (bopd) with plans to grow to 30,000 bopd over the next 2-3 years. Comparable South American firms of that size are worth over $1.25 billion.

The company has seven high-impact exploration wells planned for the next six months that could triple the current proven and probable (2P) reserves base of over 10 million barrels. This is part of a 24 to 36 month runway of drilling inventory already in the portfolio that is significant for a company of Petroamerica’s size.

Petroamerica’s valuation is cheap relative to its peers both in Colombia and internationally. The recent oil price decline has put further pressure on energy companies across the board, but this decline is even more dramatic in the Colombian sector. Petroamerica’s stock has been cut in half from $0.44 to $0.24 over the past six weeks (last at $0.27).

Even at lower oil prices, Petroamerica’s operating netbacks remain over $50 per barrel. They have always received a premium for their high-quality light oil which can be used as a diluent in Colombia’s heavy oil pipelines. They expect to exit 2014 with $50 to $60 million in cash and growth is expected to be fully-funded internally.

Investors pay attention to executive chairman Jeff Boyce, a Calgary oil patch leader, who bought approximately 1.8 million Petroamerica shares at prices between $0.28 and $0.30 over the past month. Investors also look to Frank Giustra, the well known resource investor and philanthropist, who co-founded the company and is still a major shareholder (read Giustra’s thoughts on Petroamerica here).

But Petroamerica’s Chief Operating Officer Ralph Gillcrist, a PhD Scotsman with a career focused in the Colombian oil sector, has been instrumental to the company’s turnaround and successes thus far.

Dr. Gillcrist is an operations executive who also works with Chief Financial Officer Colin Wagner and Mr. Boyce to communicate with shareholders (Chief Executive Officer Nelson Navarette is Bogota-based and focused on in-country relations and operations).

One question Dr. Gillcrist has been getting lately refers to the company’s capital structure with 871 million shares outstanding after the recent acquisition of Suroco Energy. While he couldn’t comment for legal reasons, it just makes sense the shares will be consolidated in the near future, possibly at the upcoming annual general meeting in November. I’m optimistic the optics of that move could enhance the share price over time. Dr. Gillcrist reminds me that drilling success is a lot more important. Lower oil prices would also inevitably continue to hurt the stock.

The company has been criticized in the past for their lack of operatorship (an important aspect to any takeover story) and the company’s relatively low reserve life index (number of years they could produce at current levels without another discovery). With the acquisition of Suroco, Petroamerica has made steps to address both of these concerns. Unfortunately (or fortunately if you are a buyer) oil price volatility has scared many investors out of the space temporarily, depressing share prices further.

Colombia is an underappreciated and not fully understood sub-sector of the international E&P space. Concerns about security, infrastructure challenges and political instability have weighed on the Colombian oils since they peaked in 2010/2011. With most concerns being unfounded, the Colombian space offers investors with patience and a healthy risk appetite the opportunity to make many times their initial investment.

The Petroamerica that Ralph Gillcrist presented at the Subscriber Summit is undervalued, delivering on promises and drilling seven exploration wells in the next six months. Market volatility has made it all the more interesting.

Read a transcript of Ralph’s presentation below, review the PDF, and watch his video.

Ralph Gillcrist, Executive Vice President, Business Development and Chief Operating Officer, Petroamerica Oil Corp (PTA.v)

Recorded October 9, 2014 in Vancouver, Canada, at 11:40am PST

Ralph Gillcrist: It’s a pleasure to be in Vancouver. I also have to thank Tommy and Keith for allowing me to showcase Petroamerica to such a well attended investor conference.

The company has been in existence now for five years. We have all of our assets in Colombia, and we are listed on the TSX-Venture Exchange. In those five years, we have worked hard to get the portfolio to where it is today. And that is 12 blocks, distributed over 2 basins, covering more than a million gross acres with multiple exploration drilling targets that we hope to test in the next six months.

During the last three years or so, we have had exploration success in the Llanos Basin. Our success rate has been more than 60% using 3D Seismic and that has enabled us to get production up to more than 6000 barrels a day this year.

Additionally, earlier this year, in July, we made a transformative acquisition of a company called Suroco [Energy], and I think we have demonstrated to the markets that we are able to carry out transactions that are very accretive to our current shareholders.

In a snapshot, we are estimating that we will produce this year, on average, 6600 barrels of oil per day, mostly light oil, and we are anticipating that we will exit [the year] at 7400 barrels of oil per day this year.

If you look at the 2P reserves of the company, you can see that the Suroco acquisition more than doubled our 2P reserves base. At the end of 2013, the company was sitting on 4.9 million barrels of 2P reserves, and with Suroco, we have added 5.9 million barrels, to give the company more than 10 million barrels of 2P reserves on its books today.

If we look at the market cap, with the recent market turmoil, we have seen 1/3rd of our value wiped off in the last two weeks. What has that done, it means that we are now trading at a level of value that is equal to our proven reserves base. So I would say, a tremendous buying opportunity.

Our cash position today is $67 million dollars in the bank. We have a very under-leveraged balance sheet, with $35 million in Canadian debt, that expires in April of next year and we are currently looking to change out, and insider ownership is around 3%.

The Suroco acquisition was particularly transformative. I think it addressed a number of the market concerns that we had before, with concentration risk, sustainability, in terms of a short reserve life index, running room in the exploration portfolio, and the ability to operate our business.

The transaction has increased our Reserve Life Index from 2.8 to 4 years. As I mentioned earlier, we have more than doubled our 2P reserves base. With both Suroco and business activities that we have been undertaking ourselves, we now have a full portfolio of drilling opportunities for the next two to three years. We have added with the Suroco acquisition a really exciting new play in the Putomayo Basin, and in my career of 25 years, I would say it is exceptional for a small company to be able to build such a significant land position in a seismically driven amplitude play, where we have a definite lead on our competitors in terms of understanding how the play works, and the technology.

My view has always been to focus. I like to understand the geology, I like to understand the basin. That’s how we started out with our focus on the light oil trend in the deeper part of the Llanos Basin. We are adding new plays in the Llanos basin. Again, in the Putomayo [Basin], we now have more producing assets, and huge potential in this amplitude driven play that will play out in the next year or two.

In terms of our guidance and balance sheet, as I mentioned, we are looking to produce 6600 barrels of oil per day this year, we are looking to spend $53 million dollars, including the Suroco spend, post transaction. That’s equally split between exploration and development and additional $7 million for appraisal work.

You can see from our cash position today of $67 million plus the projected cash flows coming in for the 3rd and 4th quarters, and the remaining spend that we anticipate being fully funded and exiting the year with between $50-60 million dollars depending on where the oil prices settles.

I should add that our net-backs are some of the best in the world. Our netback for this year will be around $52-$54, depending on where the oil price settles.

If we look at projecting the growth of the company, in the dark green and the light green, you can see our 2P reserves production profile, and what the Suroco acquisition has done, it has given us a stable production base for the next two-three years of around 5000-7000 barrels a day. We plan to use the cash flow generated from that production to invest in and unlock enormous upside potential in exploration. We feel that on a risked basis, we can be up at 15000-18000 barrels a day, with some exploration success, in the next 18 months ago.

I mentioned earlier that we have a number of exploration catalysts. We will be drilling 4 wells in the Llanos basin, and 3 exploration wells in the Putomayo basin. These are high impact wells, targeting 29 million barrels of mean, un-risked, working interest reserves for Petroamerica, so potentially tripling the current reserves base.

What’s our vision moving forward? We would like to build the company. We think scale is important today in Colombia. We would like to build the company to levels of between 20-30000 barrels a day, with a 2P reserves base of more than 30 million barrels, a sustainable reserves life of more than 5 years. We think we can do that through a combination of organic growth, as we have demonstrated from within the portfolio, and selective acquisition when the market conditions are right.

So finally, what’s the value proposition? To cut to the chase, the vital signs of this company are strong. We have a healthy balance sheet. We have cash on the balance sheet, we have projected cash flows and production, we have a lot of catalysts coming up in the next six months, 7 high impact exploration wells, targeting new plays both in the Llanos and Putomayo basins. We have a very experienced management team that has always delivered on its promises, and I think it’s a tremendous bargain-basement opportunity today.

Petroamerica Oil Corp Cautionary Note

Editorial Policy, Disclaimer and Disclosure: Resource Opportunities is written, edited and published by Tommy Humphreys, 602-1228 Homer St., Vancouver, BC, V6B 2Y5. Tel: (604) 697-0026 www.ResourceOpportunities.com

Editorial Policy: Companies are selected for presentation in this publication strictly on the merits of the company. No fee is charged to the company for inclusion. Currencies: Dollar and $ refer to US dollars, unless stated otherwise or obvious from the context (for example, a share price on a Canadian exchange). Disclaimer: Author owns shares in Petroamerica Oil. Readers are advised that the material contained herein is solely for information purposes. Readers are encouraged to conduct their own research and due diligence, and/or obtain professional advice. Nothing contained herein constitutes a representation by the publisher, nor a solicitation for the purchase or sale of securities. The information contained herein is based on sources which the publisher believes to be reliable, but is not guaranteed to be accurate, and does not purport to be a complete statement or summary of the available data. Any opinions expressed are subject to change without notice. The owner, editor, writer and publisher and their associates are not responsible for errors or omissions. They may from time to time have a position in the securities of the companies mentioned herein, and may change their positions without notice. (Any significant positions will be disclosed explicitly.) Author is not a registered investment advisor and this is not a formal investment recommendation. We are not telling you to go buy or sell this stock. We are telling you that we bought this stock and that we highly recommend that you research the stock to see if it is a good fit in a well-diversified portfolio. We recommend that you do as much research as possible on every stock you purchase or sell prior to any action. We recommend that you consult your investment advisor or broker prior to any action. We are not liable for any transactions you make after reading this article. Do your own due diligence prior to making any investment decision. Additionally, we invest with a 12 month or longer time horizon. If your time horizon is shorter, you may consider other investments.

Copyright: This publication may not be reproduced in whole or in part, in any form, without the express permission of the publisher. Permission is given to extract parts of the report for inclusion or review in other publications only if credit is given, including the name and address of the publisher.

Briefly: In our opinion speculative long positions (half) in gold, silver and mining stocks are justified from the risk/reward perspective.

Yesterday, gold closed higher than it did in the previous several weeks, which seems like a very bullish development for the entire precious metals market until one realizes that miners are still close to their most recent lows.

In short, in our opinion, the answer to the title question is that miners could rally some more in the short term, but we don’t expect the rally to be significant. We expect to see significant rallies after the final bottom is reached (in a few weeks – months), but not before that – at least not based on the information that we have available today. Furthermore, it seems that the next local top will be reached shortly, but that it’s not in just yet.

Why? The USD Index is likely not done declining and the long-term resistance lines in gold have not been reached. What we wrote about these markets yesterday and on Friday remains up-to-date. Still, we would like to show you the latest short-term USD chart as we have added a target area to it (charts courtesy of http://stockcharts.com.)

The target area is relatively close in terms of both time and price. Most of the decline is probably behind us. We have previously written that we expect the USD Index to correct to the 38.2% Fibonacci retracement level and the biggest unknown is what the retracement should be based on – the May-Oct. or Jul.-Oct. rally. The former seems a bit more likely because the 38.2% based on the May-Oct. rally coincides with the 50-day moving average (blue line on the above chart).

As we have mentioned earlier, gold closed higher once again, which allowed for closing part of the long positions with greater profit yesterday.

As a reminder, we took previous profits off the table by closing short positions on Sep. 25 and we went long with half of the regular position on the same day (gold closed at $1,222.50, but the intra-day low was $1,206.60 and we changed the positions well before the markets closed). On Sep. 30 (when silver was below $17 and gold closed at $1,209.10) we wrote about doubling the long positions.

Yesterday’s move, however, materialized on relatively low volume. It was lowest in a few weeks, so the rally itself was not bullish. The price-volume combination suggests that the rally is running out of steam and the local top is close. This is in tune with what we can infer from the USD Index charts and from the long-term gold chart.

The USD Index is not the only thing that moves in cycles. The silver market has a cyclical nature as well. The white metal is likely to turn around in the next several days, and the most recent short-term move has been up. Consequently, we are quite likely to see a local top relatively soon.

The declining resistance line is now relatively close – about $0.27 away and more or less at the previous intra-day Oct high. Consequently, we could see the local top more or less at this price level. It seems that it would quite likely coincide with gold moving to its target price.

Now, in the case of mining stocks, what we see on the above chart per se is less important than what we learn when we compare it with the chart of gold. The above chart tells us that miners rallied yesterday, but the miners-gold link tells us that miners are still weak. This is particularly discouraging because the general stock market moved higher once again yesterday. In other words, we saw Friday’s bearish signal once again – miners did not soar or catch up with gold, even though they “should have”.

Overall, we can summarize the situation in gold, silver and mining stocks in a way that is similar to what we wrote yesterday. However, before we write the final paragraph, we would like to reply to a few questions that we received yesterday.

The first one is “how will you know we reach the final bottom for precious metals and the mining stocks? Will $1,000 and $14 be the final one or could we see a rebound and another plunge lower?” Our reply is similar to what we have written previously. We will be looking for confirmations at these levels. Significant support levels in gold and silver being reached – this is one thing that is likely to be seen at the final bottom, but there are also other things that we would like to see:

– We would like to see USD Index at a major resistance level.

– We would like to see the gold stocks to gold ratio plunge (but we would like gold stocks to show strength after a while, thus refusing to follow gold’s declines).

– We would like to see the silver to gold ratio plunge very visibly (to the point that it’s scary and most investors/traders panic).

– We would like to see websites dedicated to gold freeze for a while when people are so interested in the volatile downswing and keep refreshing these websites for latest prices (did you know that something like that occurred in 2011 right before the final top?).

– We would like to see a very bearish (preferably hateful or otherwise emotional) article on gold in the mainstream media.

– We would like our non-investing friends to call us asking what’s going on with gold as they’ve heard that it has declined so badly.

– We will see other sings that investors and traders sentiment toward gold is very bad.

In other words, we will be looking for confirmations that the bottom is in. The price itself is not enough. At this time it seems that the $1,000 – $1,100 area for gold, $14 – $16 for silver and 150 or so for the HUI Index will stop the decline, but there are no sure bets in any market. We will keep monitoring the situation and report to you accordingly.

The second question that we received is if we will let you know when we think the final bottom is in and if we will plan to take advantage of it using ETFs or quality mining stocks. The answer to the first questions is “yes”. In more detail, we will let you know when we think that the situation looks favorable enough to get back into the precious metals market with the long-term investment capital and when to open speculative long positions. As far as ETFs / mining stocks are concerned, we will quite likely use both.

We will most likely use ETFs / ETNs for speculation in the case of gold and silver (trading capital) and we will use quality mining stocks for investment purposes (individual mining stocks are also useful in the case of speculative trades).

In general – as you have read in the bottom part of each recent alert – we are now out of the precious metals market with the long-term investment capital. The gold & silver portfolio report shows you how the portfolio looked (in case of 3 sample investors: Eric, Jill, and John) before we exited the long-term positions. When we come back to the precious metals market, you can expect a similar structure. We will probably move more into platinum than we will into gold, though.

The third question was what stocks we prefer to buy when we think the bottom is in. The short answer is – the ones with the best outlook. How do we determine that? Using the Golden StockPicker and Silver StockPicker tools. We created these tools a few years ago based on our experience and insights and we have tested their performance several months ago – they have proven to be very helpful in case of both: selecting stocks for speculative trades, and in case of long-term investments.

Each day these tools create rankings of stocks based on their recent performance relative to gold. If they don’t give you the big bang for your gold-and-silver-exposure-seeking buck, stocks rank lower. If they do, and they provide leverage, they rank higher.

There are multiple ways to use these tools, but in short, for long-term investment purposes, the aim – in most cases – is to buy the best 5 stocks and then rebalance them (every 20 trading days in the case of silver stocks and every 50 trading days in the case of gold stocks). This approach created a lot of value as compared to the simple buy-and-hold approach. We conducted very thorough research on rebalancing mining stocks (the most comprehensive there is, to our knowledge) and you can read the corresponding report in our reports section. The report also features a few approaches regarding speculative purposes. In most cases, selecting top 2 mining stocks seems justified. For instance, take the current/last trade. We wanted to provide you with an example of how the Golden StockPicker works so we saved its results that were based on the Oct. 3 session.

Here’s the input screen:

Here’s the output screen (top 5 stocks):

The top 2 gold stocks were: GOLD and RGLD. The above readings were available on Oct. 6 so we will take Oct. 6 and yesterday’s (Oct. 20) closing prices into account. The HUI Index moved from 193.49 to 191.16 (thus moving lower by about 1.2%). At the same time, GOLD moved from $67.23 to $68.55 (thus moving about 2% higher) and RGLD moved from $65.36 to $68.04 (thus moving about 4.1% higher).

Of course, these tools are no crystal balls and they will not select top performers each and every time, but – as we have shown in the rebalancing report – they are very likely to improve the results that one gets on the mining stock trades.

To summarize, when the risk/reward ratio is favorable enough to get back in the precious metals market with the long-term investment capital, Golden StockPicker and Silver StockPicker will provide the mining stock rankings.

Summing up, while the situation in USD Index and in gold and silver suggests higher prices in the short term (not much higher, though), the bearish signal from the mining stocks makes the overall short-term outlook for the precious metals sector less bullish than was the case previously.

(…)

What’s next? We’ll be paying close attention to the events as they unfold and will let you – our subscribers – know when we think further adjustments (either taking the rest of the profits off the table, or adding to / changing positions) are justified from the risk/reward point of view.

To summarize:

Trading capital (our opinion):

It seems that having speculative (half) long positions in gold, silver and mining stocks is a good idea:

- Gold: stop-loss: $1,172, exit order: $1,257, stop loss for the UGLD ETF $11.29, exit order for the UGLD ETF $13.75

- Silver: stop-loss: $16.47, exit order: $18.07, stop loss for USLV ETF $23.94, initial target price for the USLV ETF $31.73

- Mining stocks (price levels for the GDX ETF): stop-loss: $19.94, exit order: $23.37, stop loss for the NUGT ETF $18.25, initial target price for the NUGT ETF $28.99,

In case one wants to bet on higher junior mining stock ETFs, here are the stop-loss details and initial target prices:

- GDXJ stop-loss: $28.40, exit order: $37.14

- JNUG stop-loss: $6.19, exit order: $16.34

Long-term capital (our opinion): No positions

Insurance capital (our opinion): Full position

Disclaimer

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski’s, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

Of the 15+ compelling stories told at our first ever Subscriber Investment Summit in Vancouver last week, one that stood out was NexGen Energy (NXE:TSXV), which made a rapidly growing Canadian uranium discovery in 2014 at the Arrow Zone.

NexGen’s CEO, Leigh Curyer, previously managed a $500 million private equity fund with the mandate of finding undervalued uranium assets to turn around for a profit. After leaving private equity he formed NexGen with the current Chairman and ex-Rio Tinto executive Chris McFadden.

Curyer, the accountant, says he focuses on a technical approach to mineral discovery and respect for the exploration dollar.

“This will be the lowest cost discovery in the Basin’s history,” Curyer told the audience of natural resource investors. “I’m a Chartered Accountant by trade so it’s inherent in my nature to be fierce with the (exploration) dollars.”

He says NexGen is spending approximately $8.50 on exploration for every $1.00 that is spent on corporate G&A (salaries, office rent, etc).

This was Curyer’s first public presentation since the release of hole AR-14-30 which stands as one of the best holes ever drilled in Saskatchewan, Canada’s Athabasca Basin, home to the world’s largest and richest uranium deposits.

Hole AR-14-30, which was drilled into the Arrow zone, hit multiple high-grade uranium intercepts including:

- 7.54% U3O8 over 63.50 metres

- Including 10.32% U3O8 over 46.00 metres

- Including 35.19% U3O8 over 7.00 metres

- Including 66.80% U308 over 0.50 metres

Curyer said, “Arrow, in a very short space of time, is developing into a significant world-class uranium discovery.”

NexGen has drilled 32 holes at the Arrow zone with 30 of them hitting high-grade uranium mineralization.

We visited the project this summer and were very impressed with what we saw (read: “All Signs Point to Arrow“).

Curyer and his exploration team led by Garrett Ainsworth (who received the Colin Spence Award for his part in discovering the Patterson Lake South deposit) have already identified an area of mineralization spanning 215 metres by 515 metres and starting from 100 metres deep to a depth of 730 metres.

They identified the high-grade uranium mineralization at Arrow by drilling large step-out holes; 200 metres along strike and 50 metres in width.

“You can miss Cigar Lake drilling step-outs at those distances, but we hit (mineralization) in 30 of 32 holes which tells you this thing was too big to miss,” explained Curyer.

Shortly after the release of AR-14-30, Cormark Securities announced a $10 million bought deal financing at a significant premium with NexGen. As a result, the company is cashed up with roughly $16 million in the treasury.

NexGen is already working to define and refine drill targets for a large winter drill campaign starting in January 2015. They also have another 16 assays pending from the summer 2014 program.

Watch Mr. Curyer’s video presentation below.

Visit www.nexgenenergy.ca for more information.

Disclosure: NexGen Energy Ltd. is a client and the author owns shares. This is not a recommendation to buy or sell securities. Always do your own due diligence.

Watch on YouTube:

“Three out of a thousand good looking prospects become mines,” according to Dave Lowell. The octogenarian geologist has discovered 18 ore bodies in his career, likely a world record, including La Escondida, the world’s largest copper mine.

In 2013, Lowell founded a new company, Lowell Copper (JDL.v), with the backing of billionaire resource investor Lukas Lundin, to once again go and hunt for large copper deposits.

The company picked up the Ricardo project in Chile, located 28-55km from CODELCO’s Chuquicamata mine, one of the world’s largest copper mines. Ricardo saw some drilling in the 1990’s with limited success, and is believed by some geologists to contain the missing segments of the Chuquicamata deposit, which is faulted and may have moved southward along the West Fissure onto the Ricardo property.

This morning, Lowell Copper announced they had received drill permits and will proceed with 4-6 deep drill holes at Ricardo this month. A team led by Lowell will be managing the program. With success additional holes will be drilled.

In New Mexico, Lowell Copper has also received drill permits to test its TC copper porphyry prospect, optioned from Rose Petroleum, and will commence a small one to two drill hole program this month.

Here’s the company’s news release: Lowell Copper Provides Project Exploration Update

In conversations with Lowell, we have learned a bit about how he hunts for copper deposits. He likes to turn over as many prospects as possible, starting at his desk. The best ideas are drill tested in “quick to fail” fashion so he doesn’t waste too much time on them if they don’t look like winners. His favourite tools of the trade are soil samples and drill holes, nothing too fancy.

Watch on YouTube:

Ricardo and TC are two of the more promising projects in the Lowell Copper portfolio, but I know the legend is also excited about the Santa Marta VMS target in Mexico optioned from Minaurum Gold. We would not be surprised to see Lowell option or acquire other projects.

Marcel de Groot, President of Lowell Copper, commented, “We are pleased to have received drill permits to test two attractive targets in our portfolio. Our business model is focused on low cost opportunities to discover world-class copper deposits using the unique and proven mine finding talents of Chairman and Founder David Lowell and his team. We are excited to apply this model on the Ricardo and TC projects through the upcoming drill programs and look forward to updating shareholders once these programs are completed.”

Disclosure: I own shares in Lowell Copper as a speculation. Always do your own due diligence.

At the Subscriber Investment Summit in Vancouver last Thursday, 35 year old Sandstorm Gold CEO Nolan Watson made the case for a new gold standard.

“I believe that if you take actual physical gold in a vault and transact it electronically, that will be the first time in my generation that we will have something that actually can be true money.”

Watson pointed out the US monetary base has tripled over the last nine years. “What they are effectively doing is government sanctioned theft of people’s life savings and it is very frustrating.”

“One day we will be able to use our phones to spend money in gold.”

Watch the video of Nolan’s presentation below, and here’s the full transcript:

Nolan Watson, Sandstorm Gold CEO, Subscriber Investment Summit Presentation

October 9, 2014 – Vancouver, Canada

NW: I am going to be talking a little bit about Sandstorm but even more than that in an environment today where gold prices are low and Sandstorm Gold being a gold company, I want to talk a little bit about reminding people why gold and why we’re in the gold business and more particularly with respect to Sandstorm, why we have built an entire business around gold and why we are going to continue to do things in the gold space and that will give you an indication on why it is important to us, how we think about it going forward in the future. As was mentioned I am the president and CEO of Sandstorm Gold. We are a NYSE and a TSX listed company. Our market cap is about half a billion dollars. We are five years old, Vancouver-based, and having a lot of fun building the company.

So, from a high level perspective I will talk a little bit Sandstorm here then talk a little about gold. So Sandstorm, we have a diversified portfolio of streams and royalties. I think everyone here is familiar with what a royalty is which is just revenue from the various companies. A stream is very similar to a royalty, the difference is minute. But effectively a stream is where we get a % of a mines production for the life of the mine and we pay a fixed ongoing number for that. For example, the average payment we make is between is about $400 per ounce and the the difference between $400 and spot, that’s our profit.

Today Sandstorm Gold we have $70 million in cash and no debt. Now is a good time to have cash on your balance sheet if you’re a company that is trying to continue to grow and diversify. Speaking of diversification as at today we have 46 streams and royalties so in 5 years since we started the company with one asset, we have been able to diversify and grow fairly quickly.

Today, 14 of our assets are currently cash flowing so we have significant cash flow from operations and we have gold price leverage, which is what I really want to talk about today. Unfortunately the gold price leverage has been working against us. Our plan is eventually the gold price leverage will be working for us.

I am a very passionate person about gold. In fact, many people do not know this about me but I am going to pull it out right here this is my wallet and everywhere with me in my wallet for years I have had this gold coin. I always keep it with my wallet because I want to remind myself that gold is money and when my kids ask my questions and I am not sure if I should say yes or no I flip it and that is how I parent.

Now getting into gold I think everyone fundamentally understands that the governments of the world are over levered. There was a bit of a mis conception in 2009 we really got over-levered around the world and therefore we’ve been in this deleveraging phase every since.

I think it would be surprising for most people to see, that if you look at a chart of the world total debt, divided by the world total GDP. Debt is now 210% of GDP, it is 30% higher than it was in 2009. The difference is the government’s have been levering themselves up.

I would be curious to see by the way of a show of hands that if anyone believes that the US government is expected to pay off its debt the same way you and I would be expected to pay off a mortgage.

Nobody, OK thats good.

The obvious thing that you have to do is expand the monetary base. A lot of people don’t fully understand what a monetary base actually is, it’s a bit confusing with M0, MB, M1, M2, and M3, and what are the definitions of these things. From a very high level perspective, if you take money and you put it into the system, and then in a fractional reserve banking system, it gets lent out and re-deposited into a bank and re lent again, that money grows with what is called a money multiplier. M1 is after the money multiplier effect.

The monetary base is just the actual amount of dollars that you put into the system before it actually started getting multiplied by that fractional reserve banking system.

And so, you would expect with world debt like this you that the one thing you would probably be doing is that you would be expanding the monetary base that we know is happening right now but we probably don’t realize at the extent at which this happening.

This is a chart of the monetary base for the last 40 plus years. It has tripled in the last 9 years. The velocity of money has been slowing down so we do not feel the effect yet on the price of gold and inflation, but make no mistake, this is how the government plans on getting their debt to GDP ratios back on side. What they are effectively doing is government sanctioned theft of people’s life savings and it is very frustrating, and it is something that I see. It’s not the sophisticated people who lose out. The sophisticated business people we know we have to put our money into hard assets.

I put my money in real estate, I put my money in gold, I put my money in other forms that can not get inflated away. It’s the person that slaves day in day out, putting money in their savings account, that when this money printing happens, and that money is devalued, those are the people that the government is stealing money from.

So, I just want to talk a little bit about why I think gold is important and refresh peoples memory

It sort of is an antiquated idea. For some of you that have grey hair in the room you will remember but for people like me graduating from university, I thought gold was an outdated concept. We have developed sophisticated monetary systems that are way better, we don’t need gold anymore.

To refresh people’s memory, money has three main characteristics, It is a unit of account, It is a store of value,. and it is a medium of exchange, and you have to have all 3 characteristics.

Paper clips are a good unit of account if we have 100 or 200 paper clips… obviously paper clips are not money.

Diamonds are a good store of value but every diamond is different from every other diamond so it is not good medium of account or medium of exchange unless you are a warlord in Africa.

Dollars are a great medium of exchange, because I bought my coffee with them this morning and they are a good unit of account. We all know they are a terrible store of value. A lot of people have said gold is money, well, technically. with the definition of money, the way we use it today, gold is not money… it’s a fantastic unit of account it is the best store of value gold is not a good medium of exchange anymore. I can’t spend that gold coin, in fact I have gotten stuck in countries before where credit cards were cut off because VISA just does that every now and again, but I had my gold coin with me and nobody let me spend it. For quite a while, gold has not been a good source of true definition of money.

I believe that with all the changes that are happening with technology and the banking system the emergence of things like bitcoin the fact that it is not going to be very long before you can take your handheld device and wave it at something at stores in fact it is already happening and that’s how you pay. Your payments are going to be done through your smartphone. There are companies like Square and now Apple Pay just launched a little while ago. Any exchange that you want in any currency on one device is going to be able to transact currencies very easily and so therefore, I believe that if you take physical gold actual physical gold in a vault and transact it electronically, that will be the first time in my generation that we will have something that actually can be true money. Clearly the central banks aren’t going to want it, the governments will not want it.

It will have to be something created outside the banking system, and eventually be a forced option on the banking system.

I do not believe that gold will not be the only money, I believe that governments will always want the right to print unlimited amounts of money. As a good example of that when I first started sandstorm one of my first investors, I have some awesome and very colorful investors

They sent me a letter and all it was, was a handwritten note that said, Never forget why you are in the gold business. What is was was it was a Zimbabwean currency. This is perhaps an extreme example of currency printing. This is a $100 trillion dollar note.. it is a real note and that is why we are in the gold business and that is why Sandstorm has built a business around gold. And you can get a very artificial sense of the lack of need for gold especially in days like today where people are seeing the gold price drop and gold companies drop. We believe in gold, and we are building a business around it. We are going to spend the United States dollars in our bank account on gold and buying gold ounces in the ground and that is what we do.

One of the criticisms that gold could ever be an legitimate currency is that if there is a 4 trillion dollar US monetary base today that is before the leveraging of the fractional reserve system. There is actually $2.7 trillion worth of gold sitting in vaults that is not including jewellery, jewellery would take that number closer to $6 trillion, now half of that is owned by central banks and half of that is owned by others. To compare that to the US monetary base only 10 years ago, the amount of gold today, at today’s price, is somewhere between the US monetary base of ten years ago and where it is today. So it is actually a viable currency, it is absolutely something that is technologically capable of doing. I do believe that there will be a new gold standard. Now, make no mistake even if that does not happen gold is a good safety of value and it has value for that today and we are going to continue building our business at Sandstorm irrespective of this issue. I truly am a believer that one day we will be able to use our phones to spend money in gold.

So, with 30 seconds left I have one slide left, Why Sandstorm?

- We have exploration upside with no exploration cost because of the fundamentals of our business;

- We have gold price upside because we are a gold royalty and streaming company and we have fixed cash costs forever;

- We have diversification so you do not get that one asset risk when you invest in a junior mining company.

That is what Sandstorm is and that is why we are doing it. We are excited to be running this business. Thank you.

This is not a recommendation to buy or sell securities. May contain errors. Contains forward looking statements. Always do your own due diligence.

Watch on YouTube:

Summary

• Three years ago in early 2011, I cautioned my readers to be careful to chase gold and silver higher as it was moving parabolic. Now it is oversold and ignored.

• Be careful now of parabolic rises in the S&P500 (SPY), Long term US Treasuries (TLT) and US dollar (UUP). Investors are scared and looking for liquidity.

• Silver (SLV) is trading below $17, Gold (GLD) is testing major support at $1200. The GDXJ has been outperforming and has not violated 2013 lows.

• If $1180 does not hold, gold (GLD) may test lower prices near $1050 as that is the approximate 50% retracement of the 2001-2011 bull market.

• Some smart traders are expecting a triple bottom at $1180 on gold with a bounce off current oversold levels with a small pullback in December for tax loss selling.

• Junior Gold Mining ETF (GDXJ) Makes Bullish Reversal at May Lows around $33.

Over three years ago on April 28, 2011 at a time when investors were piling with two fists into gold and silver ETFs, I wrote in this popular article published on Seeking Alpha, “The virtues of gold (NYSEARCA:GLD) and silver (NYSEARCA:SLV) are being addressed far and wide. My readers know the steady drumbeat of praise that is reaching a crescendo for the white metal scares the hell out of me. A parabolic rise has formed in silver and gold… Please note that at these times of extreme optimism volatile pullbacks become more prevalent. Parabolic rises must be approached with caution.” At that time all over the mainstream media huge gold predictions of $5000 were forecasted as Central Banks became net buyers of gold for the first time in many years.

The Chinese and Russians were some of the largest acquirers of physical gold. Also large hedge funds, some managed by industry giants such as Paulson, Soros, Rogers and Einhorn, began buying ETFs and junior miners. This led to a parabolic and overbought move in precious metals, which I cautioned my readers about in the referenced article above. It should be noted that a few days after this article was published, silver topped at $50 and gold rolled over a few months later at $1900.

Now silver is trading below $17 at prices not seen in years below its 2010 breakout price. Silver does look like it is approaching a major support uptrend at the $15 level. If $1180 does not hold, gold may test lower prices near $1050 as that is the approximate 50% retracement of the move from $300 in 2001 to $1900 in 2011.

It is evident that both precious metals are in a long term secular uptrend, yet the mainstream is completely ignoring gold and silver, the exact opposite of what was happening in 2011. Now we hear the steady drumbeat of the shorts who say deflation is here to stay with low interest rates. They say stick to financial assets like the dollar and large caps which brings music to my contrarian ears. Low interest rates and low inflation do not last forever. They fuel asset bubbles which burst.

Notice the recent bullish engulfing outside reversal in the junior gold miners on high volume. Major support may be entering the junior gold miners at May Lows at $33. This powerful reversal day could be a harbinger of a bullish change in trend.

The best investments are found with real assets in neglected sectors such as the junior miners which are trading at historic discount valuations. The junior mining sector has grown completely out of favor which gives me excitement in continuing my search for the best real assets in the world when there is not much competition.

The junior gold mining sector (NYSEARCA:GDXJ) is completely overlooked by the retail public, which makes contrarian investors who accumulate real assets content as they can find the best deals at big discounts. Now the same momentum funds that were piling into gold and silver in 2011, have been buying real estate (NYSEARCA:XHB), the dollar (NYSEARCA:UUP) and S&P500 ignoring mining and commodities.

For the past three years, the US economy has had low interest rates with supposedly low inflation. How long can that last when governments all over the world are using the printing press like never seen before? The financial markets are 100s of trillions of monopoly money not backed by anything. Remember, all the gold ever mined is under $7 trillion. The US government alone has a $17 trillion debt.

I will continue to search all over the Earth for the best real assets to hedge against inflation and decline of paper currencies. The worst way to hedge against inflation is by buying inflated assets. Right now, the S&P500 and dollar are historically overpriced, while real mineral properties can be bought for virtually pennies of a penny on the dollar. Despite record demand for gold and silver coin sales, the price continues to drop because of the strong dollar providing deeper value for acquirers of the most reliable form of money known to man.

On another note, the dollar is very strong right now moving parabolically, but that could be a trap. There are many potential black swans to change this trend of rate hikes. Ebola, Jihad Terrorism, Ukraine, Iraq and now China crackdown on Hong Kong protestors could spiral foreign exchange and commodity markets out of control. Gold and silver is the best financial hedge against war, uncertainty and instability. It may be time now if you are sitting on cash to diversify into physical gold and silver and the highest quality junior gold and silver miners (NYSEARCA:SIL) which have top properties, strong treasuries and experienced management teams.

Gold closed last week below $1200 for the first time but has since rebounded from support at $1180. Silver has also rebounded but only after declining in 11 of the past 12 weeks. Precious Metals endured a very rough September and became very oversold. With Gold near its daily low and the gold miners (HUI, GDX) near their December lows, a rebound was probable. Precious metals bulls need to stay patient and disciplined as we believe this is an oversold bounce in a sharp downtrend until proven otherwise.

We plot Gold and Silver in the weekly candle chart below. First, we should note that triple bottoms (in the bullish sense) are extremely rare. Gold does not have the look of a triple bottom or reverse head and shoulders pattern. Over the past 15 months Gold has continued to make lower highs. The most recent high (this summer) indicated greater weakness as it reversed course before reaching trendline resistance. Meanwhile, note that Silver recently brokedown from what appeared to be a triple bottom. Silver has declined in 11 of the past 12 weeks. It could rebound back to previous support in the mid $18s before resuming its downtrend.

Another reason to be skeptical is Gold and Silver have major, multiyear levels of support below current levels. As we noted last week, Gold has its 50% retracement at $1080 while the monthly charts for both metals illustrate the strength of support below $1100 in Gold and at $15 in Silver.

The same can be said for the mining stocks. As we pen this, GDXJ has about 11% downside to its December 2013 low. The HUI Gold bugs index has about 12% downside to multiyear support at 168. We also plot the HUI’s rolling rate of change over three months and one year.

There is huge upside potential in precious metals but in my view that will come after further downside. I believe we have to be patient and let this bounce take its course before the market embarks on its final decline. I am waiting for the market to test or break downside targets in an oversold state much stronger than at present. I see a potential lifetime buying opportunity emerging in the months ahead. In the meantime, stay solvent and consider learning more about our premium service including a report on our top 5 buys at the coming bottom.

Article originally published on October 7, 2014.

Briefly: In our opinion speculative long positions (full) in gold, silver and mining stocks are justified from the risk/reward perspective.

The precious metals market finally rallied yesterday. Gold moved lower in the first hours of the session, getting very close to the Dec. 2013 low, but it rallied before the session was over, finally closing over $16 higher. Is the final bottom in?

The final bottom – not likely. The local bottom – very likely. Let’s examine the charts and see what actually changed (charts courtesy of http://stockcharts.com.)

Click here for reference chart.

Yesterday, we wrote the following:

The Friday’s rally was huge and it’s no wonder that metals and miners declined. The move took place right after the cyclical turning point, so the odds are that we will not have to wait long for a reversal.

All in all, the outlook for the USD Index is still bearish based on the extremely overbought status, the turning point, and the fact that previous similar breakouts (as seen on the weekly chart) were invalidated.

We already saw a significant daily decline yesterday, so it could be the case that the corrective downswing in the USD Index is already underway. The odds will further increase once we see a move below the rising short-term support line (which is likely to be seen shortly).

What about the precious metals market? It rallied and it’s likely to rally even more.

Gold moved almost to its Dec. 2013 intra-day low, which is a very important support, so this fact by itself makes a move higher very likely. The fact that gold rallied shortly after declining to this level and ended the session over $16 higher (and forming a reversal hammer candlestick) makes the situation even more bullish. This kind of action is likely to be followed by further rallying.

We recently commented about the gold to USD Index ratio as something that could provide us with technical confirmations. Based on Friday’s and today’s price moves we saw a small decline below the 2008 high (and 2013 low) that was followed by another move higher. Before viewing the decline as a breakdown, please note that back in 2008 the ratio also moved very temporarily below the horizontal support only to invalidate this move and rally shortly thereafter. It seems that we are seeing this type of action once again.

Silver moved higher and is once again visibly above the rising, long-term support line. The white metal is likely to rally based on this support combined with its heavily oversold status.

Today, we would like to cover a very interesting event that happened in the platinum market yesterday. More precisely, it concerns the platinum to gold ratio. Namely, platinum became, very temporarily, cheaper than gold, and this situation was quickly reversed. The entire event happened on huge volume in the ratio (the ratio of volumes). This kind of action (significant events, reversals and huge-volume sessions) quite often happens at the end of a given move. In this case, the preceding move was definitely down.

As far as the mining stocks are concerned, our previous comments remain up-to-date:

Gold stocks are now very close (almost at) their 2013 low, which is a major support level. Combined with a strong support for gold and silver and their oversold status, the above provides us with bullish implications also for the mining stocks sector.

Just a little more strength in the HUI Index will mean an invalidation of the breakdown below 2 support levels, which will be another strong bullish sign.

Summing up, the situation in the precious metals market is still bullish for the short term, even if Friday’s intra-day action might suggest otherwise. Monday’s price action seems to be the true direction in which the market is likely to head next – up. The corrective downswing in the USD Index has probably already begun. The same goes for the precious metals sector, only in this case, the correction would be to the upside. A lot of money has been saved by staying out of the precious metals market in the past months with one’s long-term investments (details below), and it seems that the corrective upswing will provide additional profits from the trading capital.

To summarize:

Trading capital (our opinion):

It seems that having speculative (full) long positions in gold, silver and mining stocks is a good idea:

- Gold: stop-loss: $1,172, initial target price: $1,249, stop loss for the UGLD ETF $11.29, initial target price for the UGLD ETF $13.56

- Silver: stop-loss: $16.47, initial target price: $18.07, stop loss for USLV ETF $23.94, initial target price for the USLV ETF $31.73

- Mining stocks (price levels for the GDX ETF): stop-loss: $19.94, initial target price: $23.37, stop loss for the NUGT ETF $18.25, initial target price for the NUGT ETF $28.99,

In case one wants to bet on higher junior mining stock ETFs, here are the stop-loss details and initial target prices:

- GDXJ stop-loss: $28.40, initial target price: $37.14