South America has been a major beneficiary of the 2000s gold bull, party to some big discoveries by the mining companies flocking there. Some of these discoveries have already been developed, with top-three producers Peru, Brazil, and Chile for example seeing their collective gold output increase by 25% since 2001. And some are in the pipeline, with production on the horizon.

These pipeline projects come in all sizes and are scattered across the continent. Naturally there are many located within the borders of the top three. But many reside elsewhere, including such exploration hot spots as Argentina and Colombia. One of South America’s finest development-stage projects belongs not to the aforementioned major countries though. It resides in Guyana, a small sparsely-inhabited nation that many folks are unfamiliar with.

The few people who have heard of Guyana are the ones who recollect a key event in modern US history. But I’m sure the Guyanese aren’t thrilled that the event defining their country was the infamous Jonestown massacre, an ordeal that involved the only-ever assassination of an active-duty US congressman.

Also in the US, reality-TV junkies recently got familiarized with Guyana as the backdrop for a season of Discovery’s wildly popular show Gold Rush. In 2013 Guyana produced in the neighborhood of 450k ounces of gold, mostly from small-scale mines. If the artisanals could do it, so could Gold Rush star Todd Hoffman and team right?

Hoffman’s team failed miserably, producing only enough gold to pay the cab fare back to the airport. Though this failure was mostly self-induced, and entertaining, viewers did get to witness the challenges of mining in a dense tropical rainforest. Guyana’s artisanal miners, known locally as pork-knockers, must work very hard to scrape the gold out of the ground.

Guyana’s artisanal success has attracted more than greenhorns like Todd Hoffman though. It has garnered commercial attention from larger mining companies seeking to find the source deposits. These geologically savvy companies see the big picture of what Guyana has to offer. They understand the prolific Guiana Shield, and its propensity to host greenstone belts full of near-surface mineral deposits highly concentrated with gold. And most importantly, they recognize how vastly underexplored this country truly is.

Aptly named Guyana Goldfields is one company willing to take on Guyana’s challenges in order to score a source deposit. Founder and current Executive Chairman Patrick Sheridan was an early mover into this country, with his team commencing exploration back in the mid-1990s. And their watershed event was the 1998 procurement of the Aurora project.

Gold mineralization was actually discovered at Aurora over 100 years ago. It even saw a bit of mining in the middle of the 20th century, to the tune of approximately 100k ounces. But it didn’t really see any modern exploration until right before Guyana Goldfields took over.

It took several years to build up some exploration momentum considering the state of the gold market around the turn of the century. But when Guyana Goldfields hit its stride, it uncovered a 2.0km-long mineralized corridor that it dubbed the Golden Square Mile. Significant to this was the discovery of Aurora’s flagship deposit just to the east of where historical mining occurred. And in 2007 it announced a maiden resource estimate that showed Aurora to host one of South America’s largest undeveloped gold deposits.

By 2011 Guyana Goldfields had performed numerous comprehensive exploration programs that served to feed a series of positive economic studies. That same year it was able to procure a mining permit, the first large-scale gold-mining license issued by Guyana in 20 years. And within a few months it completed Aurora’s long-awaited feasibility study.

As you can see in the chart below, the markets didn’t take too kindly to the results of this study. And GUY’s stock got simply obliterated, losing a whopping 80% in less than three months to its Q2 2012 low. Though the FS indicated excellent economic potential, even management expressed their overall disappointment with the results.

Aurora was too good of a project for its operators to accept mediocrity though, so Guyana Goldfields grabbed its bootstraps and set out to improve all aspects of the proposed mining plan. As part of its efforts it revised the resource estimate, which now sits at 8.4m ounces in all categories. And it used a core portion of this tally, 3.5m ounces in the proven and probable reserve categories, to feed the updated FS that was announced in January 2013.

The results of this updated definitive study were wildly positive, showing a marked improvement over the previous iteration. And despite this announcement coming at a time of rough sailing for gold and its associated equities, Guyana Goldfields set its sights on developing its gold mine.

Affording this confidence was a buildout that more than halved Aurora’s pre-production capex requirements over the previous study. It made sense operationally too, with projected all-in sustaining costs that’ll have it producing in the lower quartile of industry average. With AISC of only $698/ounce, this mine’s after-tax internal rate of return is calculated at 25% using $1150 gold.

Making the decision to build this mine really was a no-brainer for Guyana Goldfields. Patrick Sheridan thus set the gears in motion to move forward with Aurora’s development. And this included staffing up, with the mid-2013 hires of a new CEO and a new COO who both have developmental/operational experience.

New CEO Scott Caldwell was instrumental in helping to secure Aurora’s development capex. And the first phase of the buildout (~$249m) is now fully funded using a combination of hedge-free debt and equity. Mine construction is now in full gear, and Guyana Goldfields is targeting mid-2015 for commercial production.

Per the mine plan drawn up in the feasibility study, Aurora will produce an average of 194k ounces annually over a 17-year mine life. Mining will initially occur via open-pit methods, and then an underground component will be added in 2018. It’s estimated to cost approximately $151m to develop the underground infrastructure and expand the mill. And Guyana Goldfields hopes a big chunk of this will be funded via cash flow.

As a follow-up to the feasibility study, Guyana Goldfields smartly ran an alternative mining plan in case things really got bad in the gold market. It can obviously remain profitable even at lower gold prices, but it can choose to not go forward with the underground expansion if when the time comes it would be imprudent to expend such capital.

An open-pit-only scenario would obviously reduce the mine life, but it would also reduce life-of-mine AISC since there would be less sustaining capital, which would thus raise the IRR. In this scenario Aurora would produce an average of 177k ounces annually over a 13-year mine life. Guyana Goldfields doesn’t need to make up its mind on this for now, but it’s certainly a nice option to have.

It’ll also likely have more options as it continues to advance exploration at its Aurora project. Not only are there about 5m ounces of resources not included in the mining plan, the deposits are still open in several directions and there are numerous targets that have still yet to see drilling. I suspect Aurora will easily be a 10m+ ounce project down the road.

What an opportunity investors have to take part in one of the world’s premier development-stage gold-mining projects! There aren’t many out there that are fully funded, fully permitted, and that are in line to operate profitably even at lower gold prices. And as you can see in the chart below, investors can gobble up this stock at bargain-basement prices.

This chart plots the daily prices of gold (in red) and GUY (in blue) since 2011. And as would be expected, it’s pretty ugly. Following its 2011 all-time high, gold pulled back and consolidated in healthy fashion. But for a variety of reasons, primarily the Fed-backstopped levitating stock markets, gold crumbled in 2013. This obviously crushed the gold stocks, leaving most of their 4-year charts looking very similar to this one.

Ultimately with gold oversold and the stock markets overbought, a long overdue mean reversion is on the horizon. And when gold does finally come back to life, the radically oversold gold stocks are poised to skyrocket. And the ones that will really thrive are those with quality long-life high-margin assets that’ll greatly leverage a rising gold price.

Research analysts like myself attempt to find these stocks based on their fundamental setups. And one thing that tends to support the fundamentals is recent stock performance. Guyana Goldfields has spectacular fundamentals, but how has its stock done relative to gold?

For a non-producing junior, we need to focus on the future prospectivity of its assets. If the future is bright, then investors ought to bid the stock higher on gold strength. Gold of course hasn’t been very strong lately, but it’s had four meaningful uplegs subsequent to its 2011 apex. And as you can see, GUY’s overall performance amidst these uplegs is very encouraging.

The only chink in GUY’s armor was its performance during the first upleg in early 2012. Its 20% gain to gold’s 15% only gave it 1.3x positive leverage, which is quite pitiful all things considered. To compensate/reward for their many additional risks, gold stocks need to perform way better than gold on the upside, otherwise they’re not worth owning.

Fortunately this upleg was somewhat of an anomaly, one in which most gold stocks lacked meaningful leverage. Any momentum GUY had was also short-circuited by the release of its disappointing feasibility study in February. With gold soon heading back down, investors sold this stock with reckless abandon.

With the weak hands washed out and the prospects for a better-optimized mining plan, GUY performed much better during gold’s second upleg. And its 68% gain to gold’s 15% provided the kind of excellent positive leverage (4.5x) you hope for when you buy gold stocks.

Gold’s third and fourth uplegs came after GUY’s feasibility update. And with the future a whole lot brighter, investors rushed into this stock when the metal was bid higher. Gold’s respective 18% and 16% gains were met with GUY gains of a whopping 96% and 105%, offering outstanding leverage of 5.3x and 6.5x. And though gold has failed again following its early-2014 upleg, GUY has exhibited exceptional strength as seen in an uptrend that’s held for nearly 1.5 years.

Overall Guyana Goldfields’ spring is wound real tight. And its stock is poised to launch when gold finally gets some legs. GUY will likely be an outperformer considering its stellar fundamentals. And investors have a rare opportunity to grab it at bargain-basement prices.

GUY’s ascent will be accompanied by other elite gold stocks. And considering how hated this sector still is, most of its compatriots are also trading at silly-undervalued levels. At Zeal we’ve identified some of these other elites as part of our exhaustive sector-level research. And like Guyana Goldfields, their prospects are great and their stock prices are extremely cheap.

The bottom line is one of the finest gold-mine development projects in all of South America is located in the small country of Guyana. Guyana Goldfields was one of the first movers into this underexplored gold mecca. And its expert team rewarded it with the delineation of a fantastic complex of deposits that now have 10m+ ounce potential.

Guyana Goldfields overcame some adversity in getting to its final mining plan, an operation that is now projected to have stellar economics even at low gold prices. And its Aurora mine is now fully permitted, fully funded, and under construction with a go-live target of mid-2015. Investors can snatch up this stock for cheap right now. And based on its recent behavior, it is poised to pop once gold catches a bid.

On November 17th, Continental Gold Ltd. (TSX: CNL) published a Preliminary Economic Assessment (PEA) of its development-stage Buriticá gold project in Colombia. It was a fantastic report: the mine expected to produce 4.8 Moz of gold, with annual production of 314,000 at industry-low cash costs of US$389/oz over the first five full years.

That meant that at a gold price assumption of US $1,200/oz, the Buritica project was estimated to have a post-tax net asset value discounted at 5% of US$1.08 billion and an after-tax internal rate of return of 31.5%. That’s big news in an industry that has a dearth of significant-size development projects with robust margins and low capital costs.

However, two days later, on November 19th, Mike Hocking of Scotiabank controversially called into question a number of the company’s calculations, suggesting that:

“Either the cut-off grade or the stated dilution number appears to be incorrect. The PEA news release has outlined a resource of 20.1Mt at a diluted head grade of 7.8 g/t Au and 19.4 g/t Ag at a stated COG of 3 g/t and total dilution of 58% at a nil grade. This implies that the mine plan incorporates a small subset (33%) of the total resource at a much higher cut-off grade than 3g/t used for the resource or that the mill feed has a lower quantity of dilution than the stated 58%…

If it is indeed a smaller subset of the resource we estimate that the undiluted ore tonnes total 8.4Mt at 18.6 g/t Au and 46.1 g/t Ag for 5 Moz Au and 12.5 Moz Ag, before recoveries. This implies that the remaining 16.7Mt, containing 2Moz in the resource have an uneconomic undiluted grade of 3.6 g/t Au and 16.5 g/t Ag and will not be included in our valuation, even as near term option value (i.e. on a $/oz basis).”

-Scotiabank research report dated November 19, 2014

But, unfortunately, his argument is based on a misguided understanding of what dilution is.

Leading mining analyst, Daniel Earle, from TD Securities, cleared up the confusion created in a note to clients when he detailed how companies calculate mine plans from existing resource estimates. He pointed out that with a mine plan totaling 20.1 Mt at 7.8 g/t, including 58% dilution at zero grade, the mineable resource pre-dilution would have been 20.1/(1+0.58) Mt at 7.8*(1+0.58) g/t = 12.7 Mt at 12.3 g/t and not the much smaller 8.4 Mt that Mike Hocking came up with.

Daniel Earle concluded that the PEA results did not raise questions relative to the stated resources – that is, if you get the math right.

- While it hasn’t affected gold significantly, the price of oil has fallen quite dramatically over the past couple of months, and that’s bad news for oil companies. Profit margins are shrinking and layoffs could be coming, if the situation doesn’t improve.

- If oil continues to decline, the shale oil producers could get into serious trouble, and that could send America back into recession.

- Mainstream media promotes the idea that lower oil prices are good for consumers, but most consumers are deeply in debt, and it’s questionable whether lower oil prices are going to lead to any increase in consumer spending.

- All investor eyes should be focused on the upcoming OPEC meeting in Austria. It takes place on Thursday, which is Thanksgiving Day for Americans.

- Please click here now. That’s an oil options chart from Goldman Sachs. It suggests that the price of oil will move up or down by about $3.60 a barrel, as the OPEC production decision is announced.

- Please click here now. This chart shows US oil production reaching nine million barrels a day. High prices are needed to keep that production growth in a rising trend.

- Even if OPEC were to announce a major cut in production, that would only create a further rise in US oil production, putting renewed pressure on OPEC to cut production again.

- It’s a self-defeating exercise for OPEC to keep cutting production, while America increases production. Thus, I expect only token action to be taken by OPEC this week.

- How would a failure by OPEC to cut production affect the price of gold?

- For the possible answer, please click here now. That’s the daily gold chart. Note the position of the 14,7,7 Stochastics oscillator. The lead line is near 80, suggesting the gold rally from the $1130 area lows is “long in the tooth”.

- If OPEC disappoints commodity bulls, I think gold could decline, but only modestly, to the $1170 – $1180 area, and it might do so in anticipation of the OPEC decision.

- For any market to continue to rally in a technically overbought situation like gold is entering into now, it needs a catalyst to do so. Is there such a catalyst on the horizon?

- Well, please click here now. That’s the daily chart of the US dollar versus the Japanese yen. There’s a 14,7,7 Stochastics sell signal in play, and the dollar has definitely lost upside momentum over the past week.

- In the big picture, gold has performed admirably, while both the yen and oil have collapsed.

- If the yen can begin to rally, gold could gallop higher, to the $1250 – $1255 area, even while being technically overbought.

- It’s important for Western investors not to get overly-obsessed with the fear trade for gold, and ignore the love trade. Please click here now.

- The city of Dubai has long been recognized as the “city of gold”, and rightfully so. Five hundred jewellers are now in forces to build the world’s longest piece of gold jewellery, to promote the industry.

- The love trade (gold jewellery) has always been the biggest and most consistent driver of the gold price. I don’t expect that to change, regardless of what happens in America.

- The good news is that jewellers in China, India, and Dubai are in expansion mode, and it’s clear that Western mining stock shareholders stand to reap substantial reward from the relentless growth in gold jewellery demand.

- Please click here now. That’s the daily chart for GDX. It’s performing “according to plan”. There’s clear sell-side HSR (horizontal support and resistance) in play in the $20 area, and the rally has stopped there.

- Simply put, the traffic light has turned red, and the gold stocks sports car has stopped. After a brief rest, I expect higher prices. There’s nothing I see here that is fundamentally negative for gold stocks. Nothing.

- Gold stocks are well supported by the enormous expansion in the global gold jewellery business,and so is silver. To view the daily chart, please click here now.

- Silver tends to substantially outperform gold in the later stages of a rally, regardless of whether that rally is short term or long term. A move above the black downtrend line should attract lots of hedge fund buying, and extend the rally. A two day close above $16.75, should get that job done!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

Briefly: In our opinion no speculative positions are currently justified from the risk/reward perspective.

Yesterday was a day when the precious metals market took a breather, but it’s not true that nothing changed at all. Friday’s breakout in platinum was invalidated. Is this a “short again” signal?

In short, not really, because this signal – even though it’s bearish – is not enough to make the situation very bearish on its own.

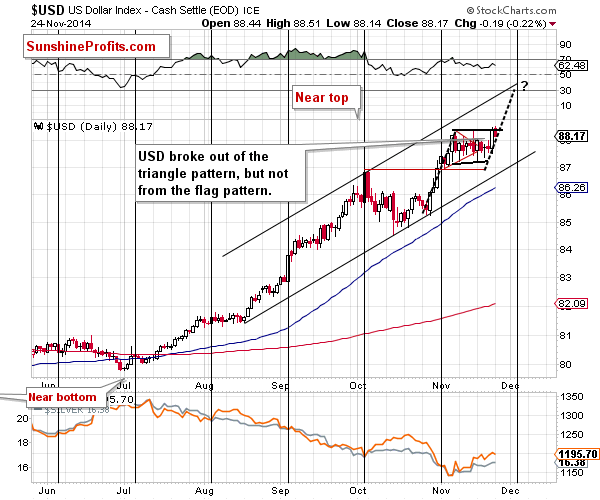

As usually, let’s start today’s analysis with the USD Index (charts courtesy of http://stockcharts.com.).

Not much changed from the short-term perspective, as the USD Index simply corrected some of its Friday’s rally and we didn’t see a breakout or breakdown from the flag pattern. Consequently, our yesterday’s comments remain up-to-date:

The USD Index moved visibly higher on Friday, breaking out of the triangle pattern. The implications are bullish but not strongly bullish, as the pattern started to resemble more of a flag than a triangle. Since the flag pattern was not broken, many traders probably thought that the situation hadn’t changed. This could explain the lack of response in the precious metals market. If we saw a strong breakout and metals didn’t react, then it would definitely be a sign of strength, but at this time, it could be the case that the market participants are still not viewing the dollar’s move as a something real.

(…)

The downside is limited in case of a breakdown, and the upside is visibly higher in case of a breakout. If we see a move similar to the one that preceded the recent consolidation, then we could see a move close to the 89 level that would materialize in the first part of December. This scenario seems quite likely also given the resistance line that would be reached (it would simply “fit”) and the cyclical turning point – we are likely to see at least a local top close to it.

We could see a small move lower before the rally starts, though. This means that the above doesn’t invalidate our previous outlook and price targets for the precious metals sector.

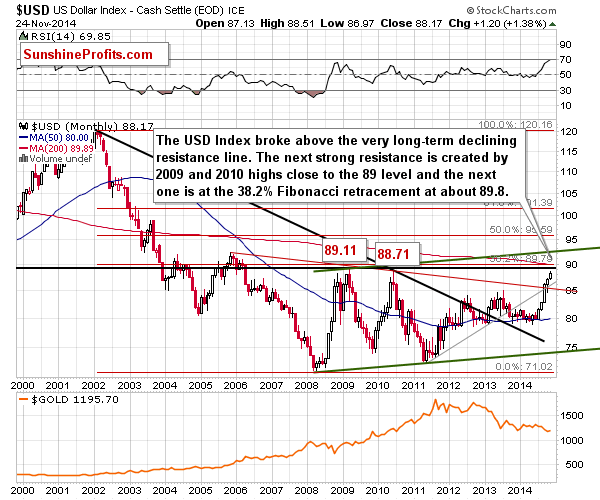

The above long-term chart should help in keeping things in perspective. As you can see, the next resistance level is very close – slightly above the 89 level. However, what’s also important is that if the USD Index moves even higher (for instance based on the expectation that the Fed will be hiking interest rates soon), it won’t be likely to move much higher, as the next significant resistance is just below the 90 level and it’s the 38.2% Fibonacci retracement level based on the entire 2002 – 2008 decline. Until the USD Index reaches at least the 89 level, the precious metals market will be likely to move lower based on the dollar’s future strength. However, if USD manages to rally to 89.8 or so and at that time gold is at one of the strong support levels, then we might consider speculative long positions in the precious metals sector. Would this be the final bottom for the precious metals market? It’s too early to say at this time – we will be looking for confirmations in other markets and ratios and report accordingly.

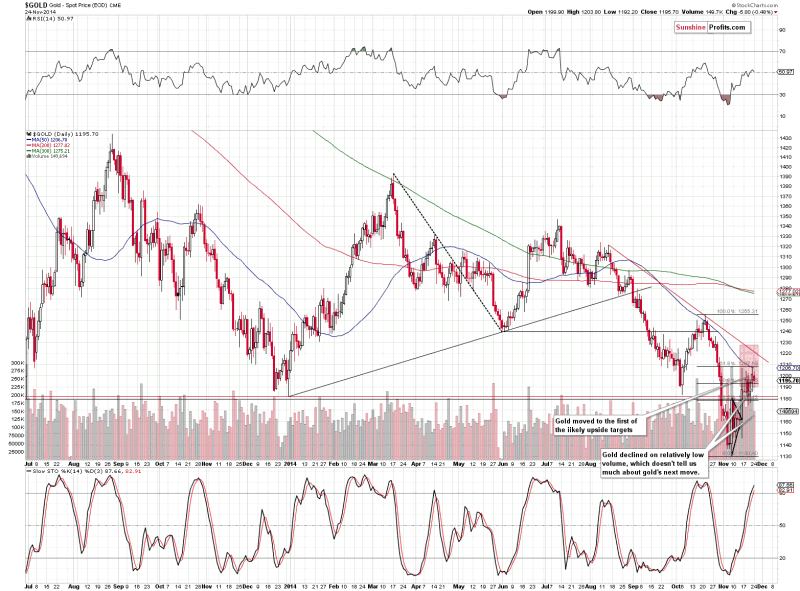

As basically nothing changed in the silver market (and what we wrote yesterday remains up-to-date) and changes are very similar in gold and mining stocks, we will comment on the last 2 markets simultaneously.

Both gold and mining stocks moved a bit lower yesterday and the move materialized on low volume. This doesn’t have meaningful implications as low volume during declines is something natural. High volume could confirm that the next decline is starting, but we saw no such thing.

Consequently, our yesterday’s comments on gold remain up-to-date:

(…) we can see that gold moved to the lower of our upside target levels. This level is created by the 61.8% Fibonacci retracement level and the 50-day moving average. The last time gold touched its 50-day MA, it was one day ahead of the top.

The implications of the above are bearish, but at this time we can’t rule out another $20 or so move higher, which would take gold to the declining resistance line.

Since gold moved higher along with the USD, we could very well see a further upswing (if the USD declines at least a bit), but if the USD breaks above the flag pattern, then gold will likely decline right away.

What about platinum?

We saw a breakout on Friday, but we warned that acting on this bullish signal might be premature, as the breakout was not confirmed:

We saw a breakout, but the continuation of the rally is still not the most likely outcome in our view. We will get a more meaningful bullish signal if this breakout is confirmed, for instance by 2 more consecutive closes above the resistance line. For now, the breakout remains unconfirmed and thus of limited significance.

Platinum turned south yesterday and the breakout was invalidated. This is a bearish sign, but as we mentioned earlier today, this signal on its own is not significant enough to make the outlook for the entire precious metals sector bearish enough for us to consider opening short positions – at least not yet.

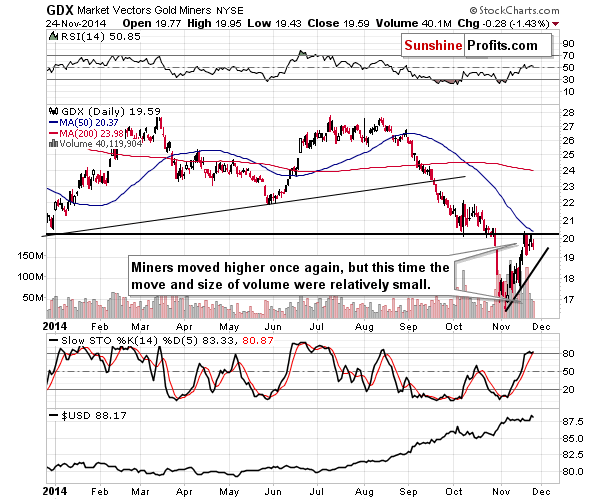

Summing up, we have some signs that the precious metals market is topping at this time (gold at a combination of resistance levels, the GDX ETF at the 2013 low, the USD Index’s rally and platinum’s breakout’s invalidation), but without a clearer and more definitive bearish confirmation it seems that opening a speculative short position is not justified from the risk/reward perspective. For instance, gold’s, silver’s, and miners’ ability not to decline on Friday when the USD rallied strongly is a bullish sign. We are very close to the point when short positions will be justified, but – in our opinion – we are not at it just yet.

As always, we will continue to monitor the situation and report to you – our subscribers – accordingly. We will aim to multiply the recent profits and will quite likely open another trading position shortly – stay tuned.

On an administrative note, the markets in the U.S. will be closed on Thursday and we expect the trading activities to be limited on Friday as well. Consequently, we there will be no Gold & Silver Trading Alerts on Thursday and Friday. The alerts will be posted until Wednesday and will then be posted normally beginning on Monday, Dec 1.

To summarize:

Trading capital (our opinion): No positions

Long-term capital (our opinion): No positions

Insurance capital (our opinion): Full position

You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

We were bullish on gold as far medium-term is concerned for the vast majority of the time until April 2013. After that we have generally been expecting lower prices. Are we gold bears? No – we view this decline as lengthy, but temporary. We expect gold to rally in the coming years, but instead of following the buy-and-hold approach, we exit the long-term precious investments at the most unfavorable times and re-enter when things look good again, thus saving a lot of money. Additionally, our Gold & Silver Trading Alerts help you profit from the short-term price swings.

Disclaimer

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski’s, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

Gold has suffered a rough couple of months, getting pounded below major support. One driver was stock-market capital flowing out of gold again, as evidenced by renewed differential selling pressure seen in gold-ETF shares. But this was minor compared to last year’s, despite extreme bearish sentiment plaguing gold. Gold-ETF selling exhaustion has effectively been hit, paving the way for big rebound buying.

The dominant gold ETF remains the American SPDR Gold Shares, which trades as GLD. This vehicle revolutionized gold trading for stock investors, creating a quick and efficient conduit for the vast pools of stock capital to migrate into and out of gold. And since GLD just celebrated its 10th birthday this week, it’s a great time to take another look at it. Starting from humble beginnings, GLD has matured into a gold juggernaut.

If you weren’t following the precious-metals realm back in the early 2000s, it’s hard to even imagine how different the pre-gold-ETF era was. Before GLD’s introduction in mid-November 2004 kicked it off, stock traders had no easy way to prudently diversify part of their portfolios into gold. Their only options were selling stocks to buy physical gold coins, trading gold futures, or buying gold-miner stocks as a gold proxy.

But for pure stock traders, all these posed real problems. While physical gold is awesome, buying coins is an inefficient and expensive process riddled with high premiums. Gold futures are a highly-leveraged and exceptionally-dangerous game most stock traders avoid like the Black Death. Though gold stocks can be wildly profitable, they are far riskier than gold itself due to an array of serious operational risks.

The gold ETFs led by GLD gave stock traders a cheap and easy way to bypass all these alternatives to gain direct gold-price exposure. GLD held physical gold bullion in trust for its shareholders. And all it took to buy GLD shares was a mouse click and trivial trading commissions. And even with GLD’s 0.4% annual management fee, it is still far cheaper than gold coins given the high premiums they command.

GLD was created specifically for American stock investors by the World Gold Council, the industry group funded by the world’s biggest and best gold miners. It was never intended to replace physical gold for investors, but to open up gold investing to stock traders who would never or could never (due to legal restrictions like in mutual funds) buy gold coins. Despite the silly conspiracy theories, GLD has been a great success.

And its resulting big footprint has forever altered the gold landscape. GLD is a tracking ETF, designed to mirror the gold price. But GLD’s shares trade independently of gold, leading to constant supply-and-demand mismatches. If they aren’t immediately addressed, GLD shares will decouple from gold and this ETF will fail its tracking mission. Literally the only way to maintain tracking is for GLD to act as a capital conduit.

Excess supply and demand of GLD shares from stock traders has to be quickly equalized into physical gold bullion. The mechanics of this are simple. When demand for GLD shares exceeds gold’s own, GLD will be bid up faster than gold and decouple to the upside. GLD’s custodians must step in to supply this excess share demand. They do this by issuing new GLD shares and immediately selling them.

The proceeds from expanding GLD’s share base are then plowed directly into physical gold bullion in a matter of hours. So excess GLD-share demand by stock traders effectively shunts their capital directly into gold itself, bidding it up faster and keeping GLD tracking it. Whenever GLD’s gold-bullion holdings are rising, it always means that GLD-share demand from stock traders exceeds the demand for gold itself.

But conduit ETFs are a double-edged sword. Sometimes stock traders want out of gold, and sell GLD shares at a faster rate than gold is being sold. This excess GLD-share supply will hammer GLD’s price below gold’s and cause it to decouple to the downside. That excess supply has to be quickly absorbed or GLD will fail. So its custodians immediately start buying back GLD shares to sop up the surplus offered.

They raise the capital to do this by selling some of this ETF’s underlying physical gold bullion. And that effectively pulls stock-market capital back out of gold, weighing on its price. Stated another way, excess GLD-share selling pressure is also shunted directly into gold itself. GLD opened up a major highway for stock-market capital to quickly flow into and out of gold, depending on the prevailing whims of stock traders.

When the gold miners launched GLD via their World Gold Council, they sought to address withering criticism from hardcore physical-gold-or-die conspiracy theorists by being hyper-transparent. Thus every single trading day, GLD publishes an exhaustive inventory of every single gold bar it holds in trust for its shareholders. This data includes serial numbers, refiners, weights, and purities. This week it was 863 pages long!

Having GLD’s holdings available daily is a fantastically-useful dataset, because it effectively shows whether stock-market capital is flowing into or out of gold. When GLD’s physical-gold-bullion holdings are rising, stock traders are buying gold on balance. And when GLD’s holdings are falling, stock traders as an aggregate are selling gold. Stock-market capital flows via GLD can greatly affect gold’s prevailing prices.

Differential GLD-share selling by stock traders indeed helped drive gold’s recent sharp selloff and major support breakdown over the past couple months. They dumped GLD shares faster than gold was being sold, forcing this world-leading gold ETF’s custodians to sell gold bullion to buy back the excess share supply offered. But provocatively, excess GLD-share supply was merely a minor factor in gold’s latest selloff.

Before we dig into that, strategic context is essential. Back in September 2012, gold was trading around $1750. That’s when the Federal Reserve launched its wildly-unprecedented third quantitative-easing campaign. QE3 involved the Fed conjuring paper money out of thin air and using it to buy up bonds, monetizing them. Naturally this was highly inflationary, and should have been great for gold like QE1 and QE2 were.

But curiously, QE3’s open-ended nature along with Fed jawboning about backstopping stock markets instead fomented a monster general-stock levitation. Stock traders believed the Fed would step up its money printing to arrest any significant stock-market selloff. And with this effective Fed Put, they aggressively and euphorically bought stocks while ignoring large and mounting fundamental, technical, and sentimental risks.

As the stock markets melted up last year thanks to the Fed, demand for alternative investments led by gold evaporated. Alternatives only shine brightly when conventional markets are struggling. This vexing dynamic led to a massive 22.8% gold plunge in 2013’s second quarter. This happened to be the worst quarter for gold in an astounding 93 years, an extreme once-in-a-century anomaly of epic gold selling!

This unprecedented gold mass exodus primarily came from two fronts. First was extreme futures selling by American speculators, which I’ve written a lot about. Second was extreme selling in GLD shares. Stock traders fled GLD at crazy rates, forcing it to vomit vast torrents of gold supply into the global market. And naturally heavy selling spawns a vicious circle, where lower prices drive more selling forcing prices even lower.

As the Fed-levitated stock markets melted up, GLD’s selling would increase as the desire for alternative investments and prudent portfolio diversification waned. Then when they pulled back periodically, the differential selling pressure in GLD would slow dramatically. The inverse relationship between the benchmark stock-market levels and GLD’s holdings is striking. And so was GLD’s impact on gold prices.

My chart today looks at the last couple years of GLD’s holdings with the gold price superimposed on top. Since GLD’s all-time-record holdings high in December 2012, all monthly draws and builds in GLD’s holdings are noted. And though GLD contributed greatly to gold’s once-in-a-century selling anomaly in 2013, in recent months its impact has been modest. This is actually a very bullish omen for gold going forward!

Not surprisingly, GLD’s holdings have a strong correlation with gold. When stock-market capital flows into physical gold bullion via this conduit, GLD’s holdings rise and that buying pushes gold higher. But when stock traders exit gold, their selling flowing through GLD forces this metal lower. And that’s the whole story of 2013. Extreme GLD-share differential selling spawned by the Fed’s stock-market levitation crushed gold.

The World Gold Council does the best research into global gold supply and demand. According to its latest numbers, gold demand dropped 11.1% in 2013 to 4081 metric tons. That was 509t less than 2012’s. But the largest gold-demand categories of jewelry and physical bars and coins actually grew dramatically last year, up 18.0% and 32.0% respectively. Only one category shrunk, and that was gold ETFs.

Gold demand through ETFs swung from 279t in 2012 to an astounding and probably never-repeatable negative 880t! Differential gold-ETF-share selling in 2013 added 880 tonnes of gold supply to the world markets, far more than that 509t total drop in global demand! So truly without the mass exodus of stock traders from gold ETFs, gold’s price would have actually risen last year instead of plunging by 27.9%!

And of that epic global gold-ETF selling, America’s GLD alone accounted for 553t or 5/8ths of the total. GLD is the dominant gold ETF by far, and can really impact the gold price when there are heavy supply-and-demand mismatches with its shares necessitating gold-bullion buying and selling. GLD’s holdings liquidation alone in 2013 exceeded the total drop in world gold demand, so it’s effectively solely responsible!

That epic outlying record draw was radically unprecedented. Remember that gold ETFs were only first introduced in late 2004, and GLD’s periodic draws before 2013’s extreme anomaly were vastly smaller. So the gold world had never before witnessed American stock traders pulling capital out of this precious metal en masse. Such an event was never even possible before in history before gold ETFs arrived.

While GLD’s epic draws last year were spread across every month of 2013, the second quarter was the epicenter. That quarter alone GLD’s holdings plummeted by 252t, or over 45% of 2013’s total. April 2013 alone, that month gold suffered a panic-like plunge when major support failed, saw a crazy 142.7t draw! That represented over a quarter of last year’s total GLD liquidations, the pinnacle of popular fear.

The inevitable selling exhaustion was finally hit in January 2014, following a mind-boggling 41.7% draw in GLD’s holdings of 564t over 13.2 months. Selling is always finite, there are only so many stock traders who own GLD and are susceptible to being scared into selling low. Thus GLD’s holdings stabilized this year, despite the Fed’s vexing ongoing stock-market levitation. They started grinding sideways.

Until the last couple of months that is. After seeing modest GLD holdings’ builds in February, March, June, and July, differential selling pressure resumed in September and October. The remaining stock traders owning GLD, the strong hands that weathered 2013’s extreme anomaly, were getting scared by gold’s steep selloff. This metal slumped to support in September, and then broke that key support last month.

While it’s never wise to sell into extreme lows, we can’t blame the stock traders for capitulating on gold given the extreme bearishness in recent months. As a full-time speculator, investor, researcher, and newsletter writer, I’m as deeply immersed in the precious-metals realm as anyone. And to me it sure felt like the recent gold bearishness even exceeded that of the spring of 2013 and the end of last year.

In fact fear had grown so crazy-high that gold stocks were recently pummeled to apocalyptic levels. The leading gold-stock index, the HUI, just fell to fundamentally-absurd 11.3-year lows! The last time gold stocks had traded so low, gold was merely $350. But earlier this month it was around $1150, or 3.3x higher. Gold-stock levels are a reflection of gold sentiment, and hadn’t been worse for over a decade.

So the universal fear infecting gold in the last couple months was the most extreme seen at least since its secular bull was born in April 2001. If there was ever an event to drive everyone wavering out of GLD shares, gold’s recent $1190 support break was it. Yet despite this the differential selling pressure on GLD shares remained modest. September and October only saw relatively-minor GLD draws of 25.1t and 28.7t.

For comparison, in 2013 GLD’s monthly draws averaged 46.0t! So the recent GLD-share selling was almost trivial relative to that epic extreme. Between mid-July and early November, gold’s price dropped 14.7% over 3.9 months. In that entire span, GLD’s holdings merely fell by 67.2t. There were multiple single months in 2013 that saw comparable or larger draws. GLD hasn’t been a major factor in gold’s recent selloff!

So why was gold so weak then if American stock traders weren’t to blame? Extreme selling by American futures speculators. Every week, their total gold-futures positions are revealed in the Commitments of Traders reports from the CFTC. And in the CoT-week span that most closely matches that recent gold drop, these guys dumped 36.6k long-side contracts while adding a breathtaking 74.1k short-side ones!

Some perspective is essential on these extreme numbers. Specs slashed their gold-futures longs by 14.8% in that short span, while ramping their shorts by 90.6%. Both moves resulted in heavy gold selling, at a total of 110.7k gold-futures contracts. This is the equivalent of a jaw-dropping 344.3 metric tons of gold supply unleased by American futures speculators alone! Obviously that dwarfs the 67.2t contributed by GLD.

Extreme futures shorting is the best kind of selling, as every single one of those contracts will soon have to be unwound. Speculators effectively borrow gold to sell it short in dangerous highly-leveraged bets, and they legally have to rebuy that gold soon to pay it back. So the near-record gold-futures shorting is super-bullish for gold and portends an imminent sharp short-covering rally. But back to our GLD focus here.

While American stock traders did capitulate as gold swooned to and through $1190 support, they only contributed less than 1/6th of the identifiable American gold selling. And that was in the most extreme fear-laden and hyper-bearish gold environment seen in over a decade! The modest differential selling pressure on GLD shares in light of this reinforces that selling exhaustion has effectively been reached.

Selling low is dumb, there’s no polite way to sugarcoat it. Smart investors and speculators buy low and sell high, and refuse to succumb to popular fear to do the opposite. GLD’s remaining shareholders are far stronger and smarter than the crop that abandoned gold last year. Their holdings are far more sticky, more likely to be permanent portfolio diversification rather than hot money spookable into fleeing on a whim.

Last week GLD’s holdings slumped to 720.6 tonnes, a 6.1-year low! The last time they were down here was September 2008, heading into that once-in-a-century stock panic. And gold was trading around $900. So theoretically ignoring churn, the remaining GLD shareholders are likely still sitting on nice gains in gold. Since they’ve held on this long, they are highly unlikely to join today’s irrational fear-blinded selling.

And if this proves true, GLD’s holdings have finally decisively bottomed and can only go higher. That will necessitate new stock-market capital inflows into gold via GLD. And the catalyst for stock traders returning to alternative investments led by gold will be these vexing Fed-levitated stock markets finally decisively rolling over very soon here. With gold so incredibly loathed, there is vast room for GLD buying.

As of its recent holdings low, GLD was worth about $27b. That same day, the total market capitalization of the elite S&P 500 stocks was $19,030b. If only 1% of that stock-market capital would diversify into gold, GLD’s holdings would soar by 7.1x! That equates to enough stock capital flowing into GLD to force its custodians to buy about 4400t of gold at today’s cheap prices. And 1% is really conservative in the grand scheme.

For decades if not centuries, the most prudent portfolio-construction wisdom advocated all investors holding 5% to 10% of their investable capital in gold for diversification and insurance. So seeing an overall 1% US allocation to gold as the stock markets roll over into what’s almost certain to be a new cyclical bear is a conservative projection. Alternative investments shine the brightest when conventional ones are weak.

The bottom line is the recent gold selloff was not primarily driven by American stock traders dumping their GLD shares. Though they did capitulate a bit, the great majority of the selling came from American futures speculators making leveraged downside bets on gold. The fact that stock traders largely held strong in the most bearish gold environment in at least a decade is a very bullish portent for gold prices.

With GLD’s holdings so incredibly low, there’s vast room for major stock-trader buying as gold inevitably recovers. As the Fed-manipulated stock-market melt-up starts cracking soon, investment demand for gold among American investors and speculators is going to soar. And the torrents of capital that will flow back into GLD shares will be shunted directly into underlying physical bullion, catapulting gold higher.

Gold’s reversal from $1130 to $1200 combined with sharp rebounds in the gold miners has given precious metals bulls some hope that the bottom may be in. A few weeks ago we noted that the sector was extremely oversold and a snapback rally could begin. Gold has been the tell for the bear market and a real bull market throughout the precious metals complex may not begin until Gold’s bear has ended. In this editorial we dig deeper into some things to watch as they pertain to Gold.

First we will focus on Gold’s volatility. The chart below shows Gold and two volatility indicators: the CBOE volatility index and average true range. Peaks in daily volatility have coincided with important peaks and troughs in the Gold price. Volatility declined from summer 2013 through summer 2014 before perking up as Gold declined from $1255 to $1130. Yet both volatility indicators are not close to extremes. Volatility does not necessarily need to reach an extreme to signal a bottom. However, the two biggest volatility spikes were at the 2008 bottom and 2011 peak. A sharp decline in Gold below $1100 towards major support combined with a spike in volatility could signal a major turning point.

I’m also focusing on the COT as its an excellent sentiment indicator. By some metrics (objective and anecdotal) Gold’s bear market has reached extreme territory. However, the COT is presently not at an extreme. We plot (as a percentage of open interest) the net speculative position and the gross short position. If these readings can exceed the 2013 extremes then they would be at 13-year extremes. A spike in the gross short position, while negative in the short-term provides future fuel (short covering) for a very strong rebound off the bottom.

Meanwhile, let’s not forget Gold’s relative strength. We shared the importance in a recent missive. We noted Gold’s relative strength tends to perk up before Gold itself bottoms. The chart below plots Gold against a foreign currency basket (the inverse of the US$ index) and Gold against the S&P 500. Gold is holding up well against foreign currencies but is coming to an inflection point. I don’t think its going to breakout yet but I could be wrong. Meanwhile, Gold continues to be very weak against the stock market.

Gold has been the tell for the bear market and my work leads me to believe the bottom is ahead and not behind us. Last week we noted the likelihood of a test of major support near $1000/oz rather than a bottom at an arbitrary level. In addition, Gold has yet to have a volatility spike on par with the spikes at the 2008 bottom and 2011 top. Moreover, current positioning in the futures market remains below the extremes seen in 2013. Finally, Gold has more work to do on the relative strength front before it can sustain a recovery.

All this being said, it is important to keep an open mind to various possibilities. Silver and the mining stocks are totally bombed out and we should pay close attention if they retest their lows. The weeks and months ahead figure to be enticing and exciting for precious metals traders and investors. Expect quite a bit of day to day volatility as we see forced liquidation and occasional short covering. Be patient but be disciplined. As winter beckons we could be looking at a lifetime buying opportunity. I am working hard to prepare subscribers.

No doubt this has been a tough year for commodities. A bear market like the one gold is experiencing right now hasn’t been seen since 2008. Meanwhile silver has been facing similar doldrums. And let’s not go into oil. Over the past several months, however, a bright light has emerged in the otherwise depressed commodities market. That bright light is uranium.

Over the past three years, or essentially since Japan’s Fukushima earthquake, the uranium market has faced undoubted hurdles. Japan’s earthquake and the damage this caused to the country’s nuclear program put a dark cloud on uranium. Uranium had essentially a PR nightmare, and following Japan’s earthquake in 2011, the price of the commodity dropped from $70 a pound to as low as $34.50 a pound.

November, however, was a different month for uranium, as the commodity enjoyed a fairly dramatic uptick in spot pricing. In fact, the Global X Uranium ETF reported that uranium was up 19 per cent for November and is now trading at its highest level in 18 months. The spot price of uranium as of November 19th is $44 a pound, which has put less pressure on uranium sellers.

There are several reasons for the positive news in uranium prices. One, on November 7th, it was announced that the Kyushu Electric Power Company received the okay to restart its two Sendai nuclear reactors in Japan, which will be the first reactors to be restarted since the 2011 meltdown. Clearly this announcement has helped further ignite activity in the uranium market. Second, China’s continued work in developing its own nuclear energy program will undoubtedly help to increase demand for uranium in the long-term.

But what’s been perhaps most influential in the uptick in uranium prices is the fact that prior to Japan’s announcement, several utilities made large purchases of spot uranium. In November, one U.S. utility purchased 10m pounds of uranium. To put that in perspective that represents about one fifth of the total amount of uranium that U.S. utilities purchased all of last year.

The question now is how to best interpret these facts and what are some of the other things that need to be known in order to make a comprehensive, enlightened decision on how uranium will perform in the future.

Some considerations that perhaps haven’t been given as much attention as they should:

The $65 to $70 a pound mark

The price of $44 a pound for uranium is certainly much better than when uranium was bottomed out at $28 a pound. Keep in mind, however, that we’re in the early chapters of a potential price rebound. Key indicators like the restarting of the nuclear program in Japan and the fact that many utilities long-term uranium contracts are coming to an end bode well for the commodity. Still, this is very early in what may or may not turn out to be a long-term price rebound.

What should also be considered is that in order to achieve profitability, uranium producers need a price level between $65 and $70 a pound, not $44 a pound. Without a further uptick in prices, there’s little incentive for producers to mine more uranium.

Trading so far thin and primarily on the spot market

The uranium market has enjoyed resurgence in part because utilities have re-entered the market. Many utilities established long-term, 10-year uranium contracts in 2006 and 2007. In 2007, about 92 per cent of all uranium was sold under long-term contracts. Utilities need uranium once more, which gives a reason for the utilities re-entering the market in November. That also means that many utilities will be in search of new uranium supplies over the next several years.

However, it’s important to realize that, one, thus far trading on the uranium market has been fairly thin despite the increase in uranium prices. It’s also important to understand that recent purchases of uranium have been made on the short-term spot market, with little or no change on mid or long-term uranium prices. How utility companies will be able to negotiate prices in new long-term contracts will undoubtedly play a role in how much opportunity uranium brings to investors.

The Russian X-Factor

Due to continued diplomatic tensions between Russia and the United States and Western Europe, an agreement has come to end between the United States and Russia allowing Russia to provide commercial grade uranium to the U.S. from dismantled nuclear warheads. This obviously has had an affect on uranium supply. Looking ahead, assuming tensions between Russia and the United States remain, a possibility exists that Russia could put further restrictions on their uranium supply, which of course would have an influence on future uranium prices.

It’s unfortunate that a beginning resurgence in the uranium market represents essentially one of the few highlights in the commodities this year. Be that as it may, there are many factors that play into uranium’s reversal and given the fact that long-term uranium prices remain questionable, how sustained this market reversal will be remains to be seen.

For months I highlighted that the low valuations in the junior resource space will attract large miners especially in the platinum and palladium (PGM) space which has a huge supply demand imbalance. This past week Antofagasta offered $.45 per share for junior miner Duluth Metals Twin Metals Ni-PGM deposit in Minnesota.

The Twin Metals Deposit is similar to Wellgreen’s (WG.V or WGPLF) as they are large PGM deposits in North America. Dundee put out a research note after the transaction which showed if Wellgreen was bought out at the same valuation as Duluth it would be priced at $1.85 share. Today’s price in the mid fifty cent range is quite cheap especially as we see the growing interest in Platinum and Palladium sources outside South Africa.

For many reasons I chose the Wellgreen asset over the Duluth asset. I had some concerns about permitting for Duluth whereas the Yukon is much more mining friendly. Wellgreen has much more exposure to nickel and PGM’s compared to Duluth and a much lower potential Capex. Wellgreen should be considered at these cheap levels especially in light of the recent Antofogasta purchase of Duluth.

I wouldn’t be surprised if Polymet, Stillwater and First Quantum are taking a look at Wellgreen especially as it has a lower capex. The upcoming PEA could be a huge catalyst to bring the project recognition in the eyes of the majors. They will be able to compare it to the recent benchmark of the Duluth transaction.

Wellgreen’s total in situ metal is over 19 million ounces of PGM’s and Gold in the open pit constrained resource. The overhang on the stock from previous management could soon be over and the new PEA could be quite exciting.

Disclosure: I own Wellgreen Platinum and they are a website sponsor.

As a follower and participant in the gold bull market from 2002 until now I can say unequivocally that the two most bearish periods sentiment-wise in the bull market so far are the fall of 2008, and right now. Therefore, by definition, the two most profitable times to buy gold stocks were in the fall of 2008, and right now. This simple concept is incredibly difficult for most people to understand and put into action.

The media will always lead you astray when it comes to these phenomenal buying opportunities. In early-2009 it was an incredible time to pick up just about any asset you could think of: real estate, stocks, commodities, etc. But the overwhelming mood on TV and the Internet back then was bearishness at that epic buying opportunity. My second favorite glaringly wrong example from the media was the end of 2012 when the media was petrified of the fiscal cliff. For a month straight in December 2012 that’s all you heard on CNBC, how the fiscal cliff was going to be terrible for stocks in 2013. But it turns out 2013 was an awesome year for stocks, and the bears in the media were 100% wrong.

What do early 2009 and late 2012 have in common? Both were the ends of periods that were bad for the markets. In 2009 of course it was the end of the epic stock market meltdown, and in 2012 it was a two year period from 2011-2012 where stocks didn’t make a lot of head way. Instead of being bullish at the bottom though the media extrapolated these negative periods out into the future and predicted more bearishness to come. The media is always focused on the short term and in sensationalizing whatever is happening right now. This puts way too much emphasis on the current state of the market and forgets the cyclical nature of the market over the long term. So at the turning point in long term cycles they are always going to be 100% wrong and look foolish.

You can’t listen to the average money manager these days either because like the media they are controlled by the tyranny of the present. They are slaves to quarterly performance, beating benchmarks, and siphoning profits from their customers who will go away if they lose money in the markets. Therefore they can’t be involved in getting in too early in a bear market and sustaining losses over a long period of time. That will ruin their business prospects for the future and they will avoid that whenever possible.

I personally believe what we saw at the end of October was the capitulation of professional money managers who had assets in gold and gold stocks. They finally threw in the towel at a key tax loss selling time of the year and decided to get out of gold and gold stocks. The evidence for this is the surge in volume across gold and gold stocks and massive losses over a short period of time. That usually only happens when the big money gets out all at once. But they are human like everyone else. And combined with the fact that their actions are way more affected by short term performance, it’s not surprising that we see massive liquidations of positions at the bottom of a trend, even by the “pros”.

Let’s talk about the life changing opportunity that those that are tied to the present are completely oblivious. Gold stocks are now at the tail end of a 4-year bear market if you go by the XAU gold stock mining index. Four year bear markets are typically brutal in gold stocks and this is one of the most brutal yet. But we know from the chart below that due to the cyclical nature of markets in general and of the gold market in particular, that what we should expect next is a bull market. And if its a bull market in gold stocks it should offer big gains.

Even during the secular bear market in gold from 1980-2000, the gold market went through cyclical bull markets that offered big gains for gold stocks. The 1993-1996 bull market is shown above and offered more than a 100% gain even though the secular trend for gold at that time was down.

Now starting in 2001 gold had shifted into a secular bull market which caused the bull market in gold stocks that launched in 2001 to be spectacular. This bull leg offered more than a 5-bagger for the XAU and even bigger gains for individual gold stocks. Then we got the 2008 meltdown, which produced the next epic buy point for gold stocks and a 3-bagger bull market. It was incredibly painful to buy at the depths of that 2008 bear market. But not only was there a 3-fold gain in the XAU, some of the individual returns on specific mining stocks during that period dwarfed anything else in the entire stock market. Silver Wheaton and First Majestic Silver are two stocks that come to mine that had 20-baggers from their 2008 lows.

I personally didn’t believe we would get another opportunity like 2008 in this gold bull market but here it is, staring us right in the face. And I think the prospects for this next bull run are truly mind boggling if you think about all the money that is going to come flooding back into this sector when the secular bull resumes.

Justin Smyth of Next Big Trade, Guest Contributor to MiningFeeds.com. Connect with him on Twitter: @nextbigtrade

On October 29th, Lake Shore Gold Corp. (TSX: LSG) reported their third-quarter financial results, boasting continued strong production and financial performance, with a 58 per cent increase in gold production and and a 15 per cent improvement in cash operating costs from the same period last year, among other highlights.

Lake Shore Gold’s CEO and President, Tony Makuch, commented in the company’s news release:

“Q3/14 is our fourth consecutive quarter of generating net free cash flow, a period during which our cash and bullion has increased by over $50 million. We have achieved solid production growth year over year, and are one of the lowest cost producers within our industry. Total cash costs per ounce sold were US$594 in Q3/14 and US$588 in 9M/14, while all-in sustaining costs averaged US$858 per ounce in Q3/14 and US$861 per ounce year to date.”

Several days prior to announcing their third-quarter operating performance, Lake Shore Gold was in the news with another company milestone – the successful results of its mineralization extension of 48 holes at its Timmins West Mine, which confirmed “… the presence of elevated gold values and [which] identified opportunities for extensions and new areas of gold mineralization [at the S2 Fold Nose in its Timmins West Mine].” Growing its resource base and extending its mine life is a critical focus for the company.

Taking a look at Lake Shore Gold’s performance over the past year, one can see that since mid-Q3 2013, the company, which is currently generating free cash flow and has been since Q4 2013, is making a strong case for sustained positive turnaround in operations.

As brief background, Lake Shore Gold is a major gold producer with exploration and development operations centred in the Timmins Gold Camp in northern Ontario, Canada. The company owns and manages two operating mines – Timmins West and Bell Creek – and a central mill, the latter of which underwent a large expansion in October 2013. The mill expansion ended up coming in at over 3,000 tpd, outpacing its nameplate capacity.

Lake Shore’s 50% throughput expansion completed in Q3 2013 can be seen as a genuine turning point in a company that’s historically been an underperformer, a point that’s allowed Lake Shore to generate strong free cash flow from Q4 2013 onward and that’s brought the company out of balance sheet issues.

The subject of Lake Shore’s balance sheet issues. 2013 also signaled the successful restructuring of $35mm in revolving debt, which Lake Shore is to re-pay to Sprott Resource Corp. (TSX: SCP.TO) by January 2015. In December 2013, Lake Shore modified its lending agreement with Sprott Resource and was able to extend its $35mm in revolving credit to November 2016, a move that removed significant stress on Lake Shore stock.

At the end of December 2013, Lake Shore Gold successfully re-paid $5mm of its debt to Sprott Resource, reducing their owed principal to $30mm. Following this, in June of this year, given Lake Shore’s strong operating results and growing free cash flow, the company announced that it had re-paid $10mm of its debt to Sprott Resource, reducing its principal owed to $20mm.

As mentioned, Lake Shore Gold has historically been considered an underperformer, with most analysts covering the stock rating Lake Shore Gold as a SELL. More recently, in December 2013, given Lake Shore’s measurably improved operating performance and its signal of genuine turnaround in operations, one broker updated Lake Shore’s stock from SELL to HOLD. As a sign of sustained and further improved operational output, in June 2014, two of the three banks covering Lake Shore revised their stock to HOLD, with one remaining at a SELL position.

Daniel Earle, who serves as Vice President and Director at TD Securities in Toronto, has provided in-depth analysis on the mining sector and precious metals for TD Securities since 2007, and has been a notable exception among the other analysts covering Lake Shore Gold.

Mr. Earle began covering Lake Shore Gold in August of 2008 and in June 2013, when the LSG stock hit a low of $0.16, Mr. Earle upgraded his recommendation of Lake Shore to a BUY, with a $0.70 target.

Since that time, Daniel Earle’s coverage has continued to be on key with the operational turnaround seen at Lake Shore Gold since the completion of its mill expansion in Q3 2013.

In August 13th, 2013, for example, Mr. Earle provided the following coverage for Lake Shore Gold:

“We believe the company is well positioned to achieve production guidance this year and together with a forecasted decline in capex over the second-half of the year, we believe sustainable free cash flow can be realized starting in Q4/13, marking a major turning point in the company’s history, in our view.”

On October 9th, 2013, Mr. Earle offered continued company coverage, stating:

“We would suggest that the company [Lake Shore Gold] has achieved an operational turnaround and that is a major breakthrough for the company.”

This was a prescient call, especially given that as of this quarter, with 9M 2014 production of 142.5 kozs and cash costs of US$588/oz (AISC of US$861/oz), Lake Shore Gold is on-track to beat its full year guidance of 160-180 kozs at US$675-US$775/oz (AISC of US$950-US$1050/oz). Moreover, this year, Lake Shore increased its cash and bullion by approximately $14mm in Q3 2014 to $67mm ($62mm in cash and $5mm in bullion), while repaying approximately $4.1mm of debt to Sprott Resource in Q3 2014

Given Lake Shore Gold’s sustained improved performance output through to the third quarter of this year, Mr. Earle remains at a BUY for Lake Shore Gold, while some other brokers have stubbornly maintained their SELL ratings as the stock has more than quadrupled in value.

There is no doubt that the current depressed precious metals sector will play its role in how Lake Shore performs for the rest of the year and into Q1 2015. However, the key point to consider is that Lake Shore’s recent exploration efforts have proven justified; moreover, the company operates on a free cash flow basis and remains able to aggressively re-pay its line of credit to Sprott Resource. All this bodes well for the stock, and with continued strong performance from the company, Lake Shore Gold’s stock will increasingly prove an attractive buy opportunity.

In a recent landslide election, Republicans took back control of the Senate and House. President Obama’s approval rating is very low. Although there a few making money in the stock market, the majority of the American people are fed up with close to 100 million people not working. Welfare and entitlement spending is out of control. The debt is still soaring close to $20 trillion and the dollar is rising making it even harder for politicians and banks to avoid default.

Somehow irrationally despite billions of dollars being printed under the guise of QE, the US dollar is rising. The question is how long do you really believe this dead cat bounce in the US dollar will last?

It may be just a bounce in a long term downtrend and is only relative to the other fiat currencies in fast decline. Smart investors should be accumulating gold and silver coins and high quality junior mining stocks trading now at historic lows. It should be noted that coin sales are picking up especially mint grade numismatics.

Avoid the large cap equities like the S&P500 (SPY) making a classic megaphone top, US dollar (UUP) and long term treasuries (TLT) as these are markets overbought and where the fundamentals do not justify the current valuation. I am very concerned about the exuberance in banking and real estate as the numbers of unemployed in America are still at record levels. Avoid “fairy tale” sectors which try to say that Price Earning Ratios do not matter or that we are in a new era which justifies obscene valuations.

The Middle East Arab Spring has turned into an Islamic Winter. Black swans could still be on the horizon. Now the US is looking to team up with Iran to fight ISIS and possibly ignoring the threat of Iran’s nuclear ambitions. Russia just stated What we are seeing with the rise of the dollar and decline in commodities may be part of the war no longer fought with bullets and missiles but with foreign exchange rates. The ruble is collapsing along with the Russian Economy. China and Russia may begin to look to trade in Yuan to avoid the negative consequences of currency wars.

Those with US dollars are able to purchase gold and silver at low prices despite record demand. The US Mint is showing record sales. Many have asked how is gold and silver going down in price when demand is at record levels? The only answer is that some games are being played in the paper market. This week the regulators just fined the major banks for manipulating exchange rates. Investors may be just beginning to lose faith in the manipulated paper markets and are just buying physical coins. Some numismatics such as Mint Grade Morgan and Peace Silver dollars have had a nice rise this past year despite a decline in gold (GLD) and silver (SLV) prices.

The junior gold miners (GDXJ) are hitting record volumes which indicates massive capitulation. The bear may be getting exhausted. We know that bear markets end in panic and many bail at the low. This time of the year the San Francisco Resource Conference was a main gathering for junior mining investors for many years. Now it is cancelled. This indicates to me that the public investor has panicked out chasing the bull market in US large caps, the dollar and long term treasuries.

When the retail investor is gone, the smart money accumulates. Don’t rush, there may be retests of this bottom and long term resource investors should look to add to high quality position on weakness during this tax loss season. Remember that bear market bottoms and tax loss selling season are some of the best times to buy at a discounted price. In this resource bear market over the past four years picking the winners has been challenging, but still I continue to search for the juniors who are the winners.

Gold and gold miners have rebounded but remain in a technically weak position. Both markets have failed to move beyond the highs made last Friday. The same happened to the gold stocks in early October. They exploded higher one day but failed to muster anything after that. At that time Gold continued its rally for a few weeks. This time Gold has struggled to sustain Friday’s gains. While we are coming to the end of the bear market and one should not be too bearish, the downside target of $1000/oz Gold remains well in play.

The chart below shows the weekly Gold close since 1980 and the net non-commercial (speculative) position as a percentage of open interest. From this chart we can deduce the two most important levels: $720/oz and $1000/oz. Give or take $5/oz, $720/oz was the secondary peak in 1980, the peak in 2006, small resistance in 2007 and major support in 2008. Gold’s bottom in 2008 wasn’t random. It bottomed at an important pivot point around $700/oz. Today, Gold is in a downtrend without any major support until the $1000/oz level. That level marked important support and resistance from 2008 to 2010 and is the next major support.

As a percentage of open interest, the net speculative position is 13%. It’s low of 5% in 2013 marked an 11-year low. If Gold declines near $1000/oz, I’d bet the net speculative position would fall below 5% and reach a 13-year low. That qualifies as extreme bearish sentiment. The physically backed ETFs CEF and GTU are already showing sentiment at major multi-year extremes.

The $1000/oz target expressed above also fits very well with history as we’ve shown numerous times in this bear analog chart.

While the downside for Gold and Silver may be limited (in percentage terms), the downside for miners could be quite a bit more. With Gold trading at $1160/oz, it would have to fall about 13% to reach $1000/oz. That is not so bad if you hold Gold. However, a 13% fall in Gold could cause a 20% fall in the miners or more. If a gold producer has a $200 profit margin at $1200/oz then he does not have much profit at $1050 Gold. If a junior has a deposit that can earn good money at $1300/oz then that isn’t worth much if Gold drops to $1050. Thus, a fair amount of downside potential remains in play. On the other hand, it works in your favor if you buy very low and Gold recovers.

In any event the bear market is very close to its end. The weeks and months ahead figure to be enticing and exciting for precious metals traders and investors. Expect quite a bit of day to day volatility as we see forced liquidation and occasional short covering. Opportunities are fast approaching so pay attention. Be patient but be disciplined. As winter beckons we could be looking at a lifetime buying opportunity. I am working hard to prepare subscribers.

Legal marijuana is staking its future in Canada as a rush of investors and venture capitalists compete to win the easy, early profits from medicinal sales.

Yet every one of the hundreds of companies jumping into the fray have their sights set on one development they all believe is inevitable: recreational pot use.

Last year the Canadian government changed the rules around supplying medical marijuana, basically privatizing production. In doing so they created a $140 million a year industry, which Health Canada thinks will be worth $1.3 billion in a decade.

“Very rarely do you have a sector that is going from nothing to a multi-billion dollar industry in no time,” says Khurram Malik, Investment Banking and Equity Research at Jacob Securities, who covers the marijuana industry. He thinks Health Canada is too conservative in their estimate since they haven’t factored in the 40% growth rates of the past couple years.

“We expect it to be a $1.3 billion industry in the next couple years, not in 2024,” says Malik.

Several hundred companies have rushed in to try and get a piece of the weed action, clamouring for one of Health Canada’s much coveted production licenses. So far the government has issued just 13 licenses, with five held by public companies that now range in value from $25 million to $80 million. Those companies include Organigram(OGI:TSXV), Bedrocan Cannabis (BED:TSXV), Tweed Marijuana (TWD:TSXV),Mettrum Health (MT:TSXV), and T-Bird Pharma (TPI:TSXV).

These are impressive valuations for new companies without proven earnings. However, many investors think the prices are justified, in part because of the potential margins. Health Canada has recommended a price of about $7.60 per gram, which is what many suppliers are charging. But production costs are estimated to be around $1.50-$2 per gram.

“People like the sector because of huge potential margins,” says Aaron Keay, an investor, competitive poker player and deal-maker who has previously represented Canada on the soccer field.

Keay ditched the struggling resource industry, where’s he’s successfully raised millions and helped build a few companies, to position himself in the burgeoning medical marijuana business earlier this year.

And he’s not alone. Several resource companies have jumped on the hype, like Affinor Resources becoming Affinor Growers (AFI:CNSX), and Supreme Resources changing its name to Supreme Pharmaceuticals (SL:TSXV). But Keay says the company he’s helped put together, Organigram (OGI.TSXV), isn’t a latecomer or a pretender, as it actually has a production license and some strong differentiators.

Keay and a partner, Panama-based financier Dave Doherty, used their last shell company to help bring Organigram public in August, and put up $1 million in bridge financing to tide it over until the listing. Shares in the shell are up fivefold from the previous financing price, and those investors hold most of the freely-trading stock in Organigram. The rest is locked up for a minimum 4-month escrow period expiring in December.

Company CEO Denis Arsenault also believed enough in medical marijuana and Organigram to come out of retirement and put up $700,000 of his own money in the company. He has seen his investment grow by multiples already too, at least on paper.

The two aren’t the only ones trying to make big returns as first-movers in the medical marijuana industry. With the help of Jacob Securities’ Khurram Malik, and Jordan Securities’ Justus Parmar, Organigram more than doubled its initial $0.85 financing from $3 million to $7.5 million and the issue was still four times oversubscribed. Arsenault says the company won’t need to go back to the market for additional cash before reaching profitability, unless it’s to jump on a consolidation opportunity or to increase production capacity because of higher-than-expected demand.

Keay says interest was high because the company fundamentals are strong.

“Organigram could easily do $40-50M in revenue in a couple years, and they have the management team to navigate the marketing, production, and regulatory challenges,” says Keay.

Where share prices go in the near-term is really anyone’s guess. With no quarterly financials out yet everyone’s guessing at production numbers, profit margins, and just how smoothly companies can expand.

“It’s an industry in its infancy. So there’s going to be a lot of volatility and variability,” says Neal Gilmer, a research analyst at Clarus Securities. “All the companies are scrambling to scale production to meet demand. It’s hard right now to determine which companies will be successful at that.”

Malik says most companies are struggling to meet expectations, like Greenleaf Medicinals, which lost its license in April after it had to recall a shipment of mouldy weed.

“Everyone’s having challenges scaling up. To grow marijuana in general is pretty easy, it literally does grow like a weed,” says Malik. “But to grow it at scale, and to grow it using Health Canada’s protocol and exact standards is a complete nightmare…. One of these companies could blow up. It’s the frank reality that they could realize they just don’t know how to grow.”