1. Gold is ending the year on a solid note. The bears promised that 2014 would be a horrible year for gold. Many bank economists predicted “double digit declines”.

2. None of their shrill predictions have come to pass. That’s because the gold bears overestimated supply from the West, and demand from China and India.

3. Please click here now. That’s the hourly bars chart for gold. I believe there is now an inverse head and shoulders bottom in play, and the short term price target of that pattern is the $1220 area.

4. Early yesterday morning, I told my subscribers that I expected gold would decline to the $1180 area to form the right shoulder of the pattern, and rally from there during the night.

5. That’s what happened. Regardless, gold price enthusiasts should understand that chart and cycle targets are not financial guarantees. They are indications of what is possible and likely.

6. As the year 2014 ends and 2015 begins, gold is postured quite bullishly, from both a fundamental and technical standpoint.

7. Please click here now. That’s the daily gold chart. The 14,7,7 Stochastics oscillator is now in an area where rallies of $50 – $150 in the price of gold often occur.

8. Please click here now. China officially imported almost 100 tons of gold in November, and Hong Kong imported about 50 tons.

9. As Reuters notes, direct imports into the Chinese mainland from countries other than Hong Kong are not revealed by China. The total tonnage imported into China and Hong Kong during November was likely somewhat higher than 150 tons, but even if they imported no gold directly at all, the demand is excellent.

10. India also officially imported about 150 tons in November. Clearly, Chindian demand is once again robust, and growing!

11. As the centres of gold price discovery move from London and New York to Shanghai and Dubai, the price action should mainly revolve around the love trade (gold jewellery).

12. Until 2014 began, the fear trade (Western debt and the outrageous behaviour of government and banks) was the main mechanism of gold price discovery. In my professional opinion, gold price volatility will diminish significantly as the love trade overshadows the fear trade.

13. The “shock and awe” growth of the Indian and Chinese economies is relentless. That means the growing dominance of the love trade on the global gold price discovery stage, is probably best described as a “clock that can’t be turned back”.

14. As terrible as the gold bears were at predicting the price of gold in 2014, if they keep failing to study the Chindian love trade for gold in meticulous detail, their price projections will go much more awry in 2015, than they did in 2014.

15. Gold stocks are prime beneficiaries of the Chindian gold bull era. Please http://www.graceland-updates.com/images/stories/14dec/2014dec30gdx1.png That’s the GDX daily chart, and it suggests that gold stocks could begin the new year with a solid rally.

16. A “textbook” double bottom pattern is in play. These patterns tend to be quite reliable.

17. Please click here now. This GDXJ chart is very similar to the GDX chart. The double bottom pattern suggests that GDXJ could rally to the $40 area in early 2015.

18. Also, GDXJ has been restructured. It now holds more producing gold companies, and that may reduce some of the volatility it experienced in the past.

19. Silver looks even more bullish than gold does, and I’ve recently swapped a modest amount of my gold bullion for silver.

20. Please click here now. There’s a nice inverse head and shoulders bottom in play on this daily silver chart.

21. Some individual silver stocks have the same pattern, and they have already staged strong volume-based breakouts to the upside. The stocks tend to lead silver, and they are supporting my thesis that silver itself is poised for a great rally early in 2015. My short term price target is $19.

22. Please click here now. That’s the hourly bars chart for oil. I have a $49 short term target for oil. The outlook for oil is grim, both in the short term and the long term.

23. In the short term, supply is overwhelming demand, and oil company earnings are suffering. In the long term, alternative energy is likely to reduce oil’s function to that of a useful lubricant, from the key fuel that it is now. In the coming decades, I expect the price of oil to ultimately return to pre-1973 levels.

24. Gold mining companies are entering 2015 with robust demand from China and India, and with a very stable outlook for fuel costs. This situation should entice substantial numbers of value-oriented fund managers into the sector, throughout the year!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

The 2000s gold bull has brought a lot of attention to West Africa. This attention has not always translated to success given the unstable geopolitical environment in this part of the world. But the diligent miners able to endure and overcome the challenges have been rewarded with some major discoveries that have been developed into profitable gold mines.

One country really thriving is Ghana. On the geopolitical front there’s probably no safer country in Africa with its government acting under a stable long-standing constitutional democracy and its tax and mining laws fairly well-legislated. And on the geological front there’s definitely no rival, with Ghana host to four massive underexplored gold-rich greenstone belts.

Ghana’s gold-mining success has resulted in a 35% increase in output over the last decade. It has grown to become Africa’s second-largest gold producer, and the 10th largest in the world. And when Asanko Gold’s flagship mine commissions in 2016, this country will see another huge boost in production.

The Asanko Gold we see today is a new-look company via its early-2014 acquisition of PMI Gold. Old Asanko (formerly Keegan Resources) and PMI were both early movers into West Africa. And their marriage is a match made in heaven given their outstanding logistical and corporate synergies.

This deal ended up bringing together the former Esaase and Obotan projects to form the newly-dubbed Asanko Gold Mine (AGM). AGM is located in the emerging Asankrangwa gold belt, just to the west of the better-known Ashanti gold belt where Newmont, AngloGold, and Goldfields operate several prolific gold mines. And its complex of deposits combine to make it one of the most robust gold projects in Ghana.

Obotan and Esaase are located about 30km apart. And both projects are known to have long histories of smaller-scale artisanal mining. This mining was primarily alluvial in nature, though it pointed towards an accessible hard-rock source. And the larger mining companies indeed found this source when they applied modern exploration techniques.

Obotan’s mineralization was the most intriguing early on. And large Australian miner Resolute Mining was able to delineate a multi-million-ounce deposit that it started mining via open-pit methods in the late 1990s. Unfortunately this operation was prematurely shut down as a result of bear-market-low gold prices around the turn of the century. And it ended up producing 730k ounces in this first go-around.

With gold prices heading higher in the subsequent years, Obotan and its large in-ground resource naturally attracted attention. And PMI Gold was the lucky winner of its prospecting license in 2006. That same year Asanko Gold took over the Esaase project located just northwest. And this kicked off an exploration cycle that would highlight the vast potential of the Asankrangwa gold belt.

Obotan and its flagship Nkran deposit was especially impressive. PMI’s aggressive exploration had uncovered a large richly-mineralized gold zone much more robust than Resolute had defined. Per the latest resource estimate it was found to hold 4.5m ounces of gold, including 2.5m ounces in the proven-and-probable reserve categories. And it was this core reserve base that would feed a wildly positive feasibility study in 2012.

PMI was able to procure Obotan’s mining lease shortly after completing the feasibility study. And in 2013 it continued to explore the project while performing pre-development work in preparation for a mine build. The critical component of this build was financing, which is no easy feat in these crummy gold markets. So PMI eventually decided its best bet would be to team up with neighbor and deeper-pocketed Asanko Gold.

Asanko’s Esaase project was advancing nicely, but it was keenly aware that Obotan was the real treasure of this emerging gold belt. Provocatively AKG had tried to acquire PMI about a year earlier, but to no avail. Its diligence paid off though, with the second go-around closing in February 2014.

Within a few months of the acquisition Asanko Gold approved construction at Obotan. And this would be the first of two phases in building out the greater and newly-dubbed Asanko Gold Mine. Obotan’s development would be followed by Esaase’s. And at full commercial production AGM will be one of Africa’s largest gold mines, producing in the neighborhood of 400k ounces per year.

Phase one’s $295m price tag is fully funded with the new company’s combined treasury and debt facility. And it is expected to pour its first gold in Q1 2016. And per a Definitive Project Plan just announced in November, this fantastic mine ought to be profitable even at lower gold prices.

Mining will occur via conventional open-pit methods. Since the ore is fresh/sulfide it’ll require milling, employing crush/grind/gravity/carbon-in-leach circuits. And the operation will run at a life-of-mine mill-feed rate of 8.2k metric tons per day. With life-of-mine recoveries and average grades that exceed 92% and 2.0 g/t respectively, phase-one production will average 190k ounces annually over a 12-year mine life.

AGM’s phase-one gold will be produced at all-in sustaining costs of only $781/ounce, easily in the lower quartile of industry average. And this will allow for a solid 20% after-tax internal rate of return at $1150 gold, and the IRR would obviously increase proportionally if AGM’s gold is sold at higher prices.

Phase-two production will come from the nearby Esaase deposit. Esaase is a grassroots discovery made by Asanko Gold. And its extensive exploration has defined a massive 5.9m-ounce deposit. AKG has performed multiple economic assessments at Esaase over the years. And the latest, a 2013 prefeasibility study, showed this project to also hold great economic potential.

Mining would focus on Esaase’s core 2.4m-ounce reserve base. The ore would need to be milled like Obotan’s, but processing would require the extra step of running through a flotation circuit. Feed grades and recoveries are a little lower than Obotan’s, but all-in sustaining costs would still be under $1000/ounce. And at a throughput rate of nearly 14k tpd, production from Esaase would average about 200k ounces per year over a 10-year mine life.

Interestingly since this PFS was performed prior to the PMI acquisition and was based on a standalone operation, it is essentially obsolete. Since Esaase will now be developed as the second phase of a larger mining operation, there are numerous synergies that ought to drastically improve the economics.

The biggest cost savings will come from not having to build standalone processing facilities. Esaase is close enough to Obotan that its ore can be trucked. The existing facility would need to be expanded and a flotation circuit would need to be added in order to accept Esaase’s ore, but presumably this would be much cheaper than building a full onsite facility from the ground up at Esaase.

There will also likely be many operational synergies. And for this reason AKG is in the process of performing a scoping study that would incorporate Esaase into a larger phased mining operation. This study is expected to be completed in Q1 2015. And if it comes back positive as expected, it ought to lead to more feasibility work that would hopefully culminate in development shortly after phase one achieves commercial production and starts spinning out cash.

Overall Asanko Gold’s AGM is one of the world’s elite development-stage gold projects. Its first phase of operation is fully permitted and fully funded. And thanks to rough market conditions that have annihilated the gold-mining sector, investors have the opportunity to get onboard this emerging mid-tier producer at bargain-basement prices.

As you can see in this four-year chart, Asanko Gold’s stock has fallen sharply since its 2011 all-time high. And the primary driver for this decline is the price action of AKG’s underlying metal. Since gold’s own 2011 all-time high, it has fallen into a deep dark cyclical bear market that has taken it to levels not seen since 2009. And this has been none too kind to highly-leveraged gold stocks like AKG.

AKG’s descent into bear-market mode got a kick start in September 2011 upon the release of Esaase’s first PFS. Unfortunately this PFS wasn’t well-received by the markets as a result of much higher costs than what was outlined in the previous assessment. Couple this with gold’s major September beat down, and AKG would see its stock price nearly cut in half in short order.

AKG finally caught its breath when gold bounced the following month, but it would be rough sailing over the next several years as gold gave up its ghost and entered into bear-market territory. With such an ugly downtrend there aren’t many positives to analyze from a technical perspective. So the true test of AKG’s resolve is how it performs on the rare occasions when gold gets legs.

Since its 2011 high gold has forged four meaningful uplegs. And it should be expected that gold stocks outperform their underlying metal amidst such uplegs. If they don’t, there’s really no reason to own them given their outsized risks compared to gold itself. And as you can see, AKG has been a consistent outperformer.

In the first two uplegs in 2012 AKG positively leveraged gold 3.0x, rising an average of 47% to gold’s 15%. AKG performed even better in 2013’s Q3 snapback upleg, soaring 67% to gold’s 18% (3.7x leverage). And then in early 2014 AKG again performed well, rising 51% to gold’s 16% (3.2x leverage).

This stock has already shown the ability to pop when gold shows signs of life. And since it is in better fundamental shape now than it was in these past uplegs, it really ought to fly when gold runs higher. The new-look Asanko Gold’s 10m+ ounce resource base really ought to attract investors when they return to this space. And with mine development now underway, institutional investors and the larger mining companies will take AKG a lot more seriously.

Overall AKG ranks as one of only a handful of quality junior gold stocks poised to thrive when gold turns the corner. The carnage of the last few years has really taken its toll on this sector, but this group is ready to roll when interest returns. And now is the time to load up on these stocks while they’re trading at such crazy-low levels.

The bottom line is new-look Asanko Gold controls the heart of one of Ghana’s most-exciting new gold belts. AKG’s flagship AGM project is host to over 10m ounces of gold resources. And a series of positive feasibility studies shows that its core reserves are amenable to profitable mining.

Asanko Gold will develop this exciting new mine in two phases, with fully-permitted and fully-funded phase one construction now underway. AGM is expected to pour its first gold in Q1 2016. And investors are able to take advantage of bargain-basement prices today to get in on one of the world’s premier gold-mine-development projects.

Another December and gold stocks have reached another extreme oversold condition. This was the case precisely 365 days ago and the precious metals complex, led by the miners rebounded strongly for nearly three months. A year later and the gold stocks are even more oversold. They’ve been in a bear market for more than three and a half years and in terms of price are very close to matching the worst bear market of all 1996-2000. Only time will tell if this is truly the end of the bear market but in any case miners have a shot to start 2015 off positively.

The following sentiment indicator was developed by sentimentrader.com. For various ETFs it considers options activity, fund flows, the discount to NAV and future volatility expectations. Like any indicator, it is only a single indicator and is best used in conjunction with other indicators. Interestingly, the Optix for GDX touched 27% two days ago. That is the lowest since GDX began trading in 2006.

Breadth indicators also indicate an extreme oversold condition in the miners. The bullish percentage index (% of stocks on a P&F buy signal) for the GDM index (forerunner to GDX) is currently at only 3% but was at 0% at last weeks low. It has only ticked 0% a handful of times in the past two years. Second, the percentage of stocks in the HUI trading above their 200-day moving average is currently 6% but was 0% at last weeks low. The last time both indicators were at 0% together (as they were last week) was in late 2008.

Here is a look at the updated bear analogs for the gold stocks. We use the Barron’s Gold Mining Index as it has the longest history. The current bear is in line with the 1996-2000 bear. After declining 69% over two and a half years that bear mounted a rebound that lasted over a year. That was followed by a decline to new lows. The current bear is down 68% and at this point on the scale is in the worst shape relative to all the other bears.

For further comparison to the 1996-2000 bear, consider the figures for the other indices. Then the XAU declined 73%. At its recent low it was down 73%. Then the HUI declined 83%. It’s been down as much as 77% in this bear. The GDM index has lost 75% in this bear market and 77% in the 1996-2000 bear market. Meanwhile, GDXJ has lost up to 86% in the current bear market.

As we noted last week, the miners appear to be holding their November low and have a tradeable setup. The HUI is trading between 155 and 175 while GDX is trading between 17 and 20. A short-term rally to resistance is definitely possible. Given the current extreme oversold condition, are the miners ready to rebound through resistance and rally the way they did last January? On the other hand, will the metals cooperate? After 2013 tax loss selling, GDXJ rebounded over 50% within two months. We are working hard to prepare subscribers for this opportunity. Consider learning more about our premium service which includes a report on our top 5 stocks to buy.

1. As the end of the year approaches, gold is swooning a bit. Please click here now.

2. That’s the daily chart for gold. A broad and gently sloping uptrend channel has been established, with very volatile price action between the channel lines.

3. I expect gold to trade in this manner throughout most of 2015. Short term volatility will be high, but the price will trend higher.

4. Gold is working off what is an overbought technical condition, and should be poised to stage a significant rally by early January.

5. Please click here now. That’s the daily oil chart. While the odds of a brief and violent rally are growing, the overall fundamentals are horrific. Demand for oil is collapsing around the world, and supply continues to increase.

6. While a modest rise in the price of gold in 2015 might not sound very exciting, when coupled with a further collapse in the price of oil, gold stocks could suddenly become the darling of institutional investors around the world.

7. Gold companies are much more efficient now than they were just two years ago. Lower fuel prices coupled with even modestly higher gold prices could produce a violent move to the upside, for the entire gold stock sector.

8. Demand for gold from China and India should see another year of superb growth in 2015. While gold may decline for another week or two, that’s mainly due to technical and seasonal factors. The ebb and flow of Indian demand is based on religion, and December is viewed as an inauspicious time to buy gold.

9. With key physical buyers taking a rest, the price is a little soft. Also, Western investors tend to buy when the price of any asset is high, and sell at a loss each December. They are adding to the gold price softness now.

10. I expect Chinese demand in 2015 to increase substantially. Trading volume on the Shanghai Gold Exchange (SGE) is experiencing truly dramatic growth, year after year. My subscribers know that I’ve predicted that volume on the SGE will surpass COMEX volume by early 2017.

11. Gold is clearly the ultimate asset, and it should offer the ultimate in stability to conservative investors for the next decade. Aggressive investors should focus on gold stocks.

12. Unfortunately, the outlook for the American stock market is much less rosy than it is for gold. Mainstream media claims that debt-soaked consumers working multiple part time jobs are somehow the “economic leader” of the world economy.

13. Now, the US stock market has lost a prime engine of earnings growth; oil. Healthcare and defensive stocks are keeping the huge stock market rally alive, but the impact of much lower oil prices won’t be felt for another quarter or two.

14. Technically, healthcare stocks look headed for trouble. Please click here now. This monthly chart of a key biotech ETF shows a rapidly deteriorating technical situation.

15. I think that the month of December in 2015 will see Western investors back at the “tax loss trough”, selling most of their US stock market investments.

16. American GDP numbers will be released this morning. With most of India’s gold buyers in “quiet mode” this month, that report could push gold to my $1150 – $1160 short term target area, and provide a short term boost to the US stock market.

17. US economic data generally has only a short term effect on the gold price. The long term price is determined mainly by the demand from China and India, compared to supply from mines and Western entities. Once the Western funds and retail entities have sold most of their gold, I expect Chinese and Indian jewellers to begin tapping Western central banks for the gold they hold, since mine supply appears to be peaking.

18. In the Western world, good economic data causes seemingly rational economists to make very irrational statements about gold. In contrast, in China and India, good economic news spurs gold demand. People celebrate the good news, by buying more gold!

19. As the West becomes more irrelevant to the global gold market, the questionable statements made by Western economists about gold will likely be ignored by most professional investors.

20. I doubt there will be much gold left anywhere in the West by the year 2050. Crypto currencies like bitcoin are more suitable as central bank reserve assets than gold. Rather than being held as useless bars by bankers and government bureaucrats who can’t be trusted, most gold should be held in the form of fabulous jewellery, by the citizens of the world. Also, he or she who has the most gold, makes the most rules. The citizens should make the rules, not bankers and “Gmen”,and in time they will.

21. The Swiss government just released that country’s latest import and export statistics, for the month of November. Please click here now. I’ve highlighted a few key numbers from that report.

22. While the United Kingdom did import about 64 tons of gold, it exported about 109. While gold price enthusiasts may be a little disappointed with the numbers from China, I should mention that Hong Kong also imported about 34 tons.

23. In 2013, Chinese demand surged far above 2012 levels, but Western exports overwhelmed Chinese and Indian imports, and the price declined. In 2014, demand roughly matched supply, and the price was neutral. By late 2015, I expect Chinese and Indian demand to place noticeable stress on available supply, and the price should begin moving aggressively higher.

24. Please click here now. That’s the daily GDX chart. Gold stocks are my “trade of the year” for 2015. Like gold, GDX is working off an overbought situation on the chart. There’s a bull wedge pattern in play. In the very short term, US economic data today could create panic selling, by Western gold stock shareholders that respond to that data with irrational action. With the Indian “titans of ton” quiet in December for religious reasons, the price movement in many gold stocks could be a bit frightening, but only for a few days. I’m a buyer of all irrational selling, and I think the entire Western gold community can look forwards to a very rational and profitable year, in 2015!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

The gold and silver stocks have put in a bullish weekly reversal but Gold and Silver have not confirmed it. The interplay between the metals and the shares has been complicated in recent weeks. Hopefully this missive will make some sense of it as the two groups are sending mixed signals.

Gold and Silver are charted below in weekly candle format. Before this week the metals looked bullish. Each tested support and rebounded strongly towards resistance. However, both metals gave back much of the recent gains. Bulls would say they are correcting and still in position to test resistance. Bears would say the metals failed to reach resistance and are headed to new lows.

Though the mining stocks are selling off today (Friday), they’ve completed a bullish reversal and double bottom on most weekly charts. Below we plot GDXJ, GDX and our Top 40 index. Other than GDXJ just about every miner index has completed a double bottom. Though GDXJ made a new low it did form a bullish reversal. GDX and the Top 40 index formed bullish hammers and potential double bottoms. We say “potential” double bottoms for a reason. The double bottom is a very bullish pattern in which the market should explode up from the second bottom. Only time will tell if the miners follow that path or if the reversal fizzles.

Interestingly, the metals and the miners have been disjointed in recent weeks. Gold lost 2% this week while Silver lost 6% yet the miners put in a positive reversal. During the two prior weeks metals rebounded strongly yet miners sold off. Part of that could be tax loss selling in the miners which has created additional weakness.

Investors and traders have a good setup in the miners. Downside support is defined by the double bottom. A weekly close below that could be the stop out point and would limit losses. Meanwhile, if the metals are destined to take out their October highs then the miners should explode higher sooner rather than later. After 2013 tax loss selling, GDXJ rebounded over 50% within two months. We are working hard to prepare subscribers for this opportunity.

Gold stocks have suffered a miserable few years, becoming a laughingstock even among contrarians. But this despised sector’s seemingly-endless downward spiral has left gold stocks vastly undervalued relative to gold, which drives their profits. The fundamentally-absurd disconnect between gold-stock price levels and gold can’t last. And it sure looks ready to end, making 2015 the year gold stocks shine again.

Any stock is a fractional ownership stake in a corporation, entitling shareholders to participate in that company’s profits. So over time, any stock price ultimately reflects a reasonable multiple of these very underlying earnings. If a stock price falls too low relative to corporate profits, investors step in to buy shares cheap bidding their prices higher. And the opposite is true if a stock grows too expensive relative to earnings.

In the gold-mining industry, the price of gold is the dominant driver of corporate profits by far. Mining costs are largely determined by the particular deposit being mined, and are largely fixed when any mine is designed and constructed. So gold miners’ profits are almost totally dependent on the price of gold. The higher it happens to be, the larger their margins grow since their costs generally don’t change much.

This dynamic is what has long made gold stocks attractive to investors. When the gold price rallies, the profits of gold miners rocket higher much faster. If a miner can produce gold for $900 an ounce, and sell it for $1200, its profits are $300. But if gold merely climbs 25% higher to $1500, that same miner’s profits double to $600. This inherent profits leverage to gold makes the gold stocks really amplify gold’s moves.

But as in all stock-market sectors, this key fundamental relationship between earnings and stock prices can be temporarily derailed by sentiment extremes. Sometimes investors get greedy, and bid gold-stock prices up far higher than their gold-driven profits could ever support. And other times they get scared, selling so aggressively that prices fall far below their earnings-supported levels. Great fear has plagued gold stocks.

This has hammered this sector to truly fundamentally-absurd levels relative to the metal that drives its profits. The leading gold-stock index is the NYSE Arca Gold BUGS Index, widely known by its symbol HUI. Back in early November, this gold-stock-sector measuring rod was crushed down to 146.8. The last time this index had been lower was a whopping 11.3 years earlier all the way back in July 2003.

The problem was these recent extreme lows were spawned by overwhelming fear, not underlying profits fundamentals. In early November 2014, the gold price fell just under $1150. But the last time the HUI had been so low over a decade earlier, gold was trading near $350. Does it make any sense at all for gold stocks to be trading at the same levels despite gold being 3.3x higher? No, it’s a crazy fear anomaly.

Gold stocks are priced as if gold was just 30% of its prevailing levels today. Imagine this same kind of vast fundamental disconnect in another industry. What if Apple’s stock was trading at levels reflecting it selling just 30% of the iPhones it’s actually selling? Investors would rush to buy it, knowing full well that extreme sentiment-driven fundamental anomalies never last for long. Why should gold stocks be any different?

And make no mistake, investors will return. Between the birth of gold stocks’ secular bull in November 2000 and its peak in September 2011, the HUI skyrocketed a mind-boggling 1664% higher! This nicely leveraged gold’s own 603% gain over that span, and trounced the benchmark S&P 500’s 14% loss. The investors who were willing to buy gold stocks cheap back in the early 2000s earned vast fortunes over a decade.

But sentiment started to turn in 2012, when the HUI slipped 11% despite gold gaining 7%. And 2013 was the year of QE3, the Fed’s wildly-unprecedented debt-monetizing money printing that spawned an incredible stock-market levitation. As the US stock markets inflated dramatically on nothing but Fed hot air, alternative investments like gold were wholesale abandoned. Why buy gold when stocks are soaring?

So in 2013 the HUI plummeted 55% to gold’s 28% loss. Truly gold stocks should have bottomed after such an extreme down year, as fear in this sector was off the charts. And indeed they spent most of 2014 regaining ground, but that great progress collapsed in recent months. Now year-to-date, the HUI has dropped 20% to a mere 2% gold loss, reflecting the ongoing extreme and irrational fear in this sector.

But gold stocks can’t fall relative to gold forever, they can’t be forced into a situation where their various earnings multiples are merely a fraction of the broader stock markets’ indefinitely. Like everything else in the markets, the relationship of gold-stock prices to gold levels is forever cyclical. Greedy uplegs push gold stocks well above reasonable levels relative to gold, then fearful corrections hammer them back below.

As this chart reveals, that relationship has swung the latter direction for far too long. Which means a major reversal is imminent, certainly in 2015. Plotted here is the popular GDX Gold Miners ETF as a gold-stock metric, in addition to the relationship between this and the GLD SPDR Gold Shares gold ETF. The GDX/GLD Ratio shows where gold stocks are trading relative to gold, which ultimately drives their profits.

Just this week, the GDX/GLD Ratio slumped to 0.149x. In other words, GDX’s share price was trading at just over 1/7th of GLD’s. Incredibly this is the lowest level ever witnessed, in these terms gold stocks have never been cheaper relative to gold! GDX was born in May 2006, the last time gold stocks were in favor. And even during 2008’s once-in-a-century stock panic, the GGR merely plunged to 0.227x at worst.

And that stock panic was almost certainly the greatest fear event we’ll witness in our lifetimes. The VIX fear gauge skyrocketed up to an astounding 81 in November 2008, epically high. So it’s mind-boggling that gold stocks are now much cheaper relative to gold than they were even in that incredible fear super-storm. That is supremely irrational and reflects the extreme fear-driven fundamental anomaly dogging this sector.

In absolute terms, GDX’s price fell to $16.59 in early November 2014. That was its worst levels in 6.0 years, since a single day near the stock panic’s climax in October 2008 where GDX briefly fell to $16.37 before bouncing sharply higher. So gold stocks have never been or almost never been more out of favor than they are today when measured in both relative-to-gold and absolute terms. It’s just a crazy anomaly.

And this devastating sentiment trend has been in place since late 2007, as evidenced by the GGR’s secular-resistance line shown above. When this key fundamental gold-stock ratio is falling, gold stocks are losing ground relative to gold. Gold, as represented by GLD, has been outperforming gold stocks on balance ever since. But gold stocks’ relationship to gold is forever cyclical, making this an extreme aberration.

In gold-stock uplegs, the equities outperform the metal so the GGR rises. In gold-stock corrections, the metal doesn’t fall as fast as the stocks so the GGR falls. So if you think of the gold price as a straight line, gold-stock price levels oscillate around that like a sine wave. Outperformance is always followed by underperformance which soon yields to outperformance again. And this cycle continues into perpetuity.

Typically this sentiment-driven oscillation sees gold-stock uplegs that run for up to several years on the outside, followed by gold-stock corrections that typically take 6 months or so. But incredibly today, the gold stocks have been underperforming gold on balance for an astounding 7.1 years! This makes zero sense fundamentally given prevailing gold prices of recent years, so it is solely the product of extreme sentiment.

The main thing that pushed this gold-stock underperformance into such extreme bear territory is the Fed’s hyper-manipulative QE3 campaign. Note above that gold stocks had bottomed and were climbing sharply in 2012 before the Fed hatched its QE3 scheme. But as QE3 convinced stock traders the Fed would arrest any material stock-market selloff, they abandoned alternative investments including gold stocks.

As the general stock markets soared with the Fed’s implied backstop in QE3, gold and its miners’ stocks were crushed. The worst of the selling came in 2013’s second quarter, when gold plummeted 22.8% in its worst quarterly loss in 93 years! GDX collapsed 35.3% in that span, the most extreme selling seen in gold stocks since late 2008’s panic. And they’d started recovering nicely this year, until recent months.

With the Fed’s QE3 manipulations enticing or forcing most investors into the dangerously-overvalued US stock markets, investors have largely been absent from the gold market. This has given American futures speculators carte blanche to run amuck. So in the last couple years the gold price has been dominated by their leveraged trades, particularly short-side bets. And recent months saw extreme gold-futures shorting.

As gold temporarily broke below its $1200 support zone in late October and early November, many remaining gold-stock investors capitulated. After years of misery, they finally gave up on this seemingly cursed sector. But that in itself is a major bottoming indicator, a major downside washout after years of falling prices. And that is one of the key components setting us up for a massive gold-stock upleg coming in 2015.

Why 2015? The sole reason gold suffered such an extreme down year in 2013 was the Fed’s stock-market-levitating QE3 campaign. Every time the stock markets started to sell off, the Fed either stepped in to jawbone them back higher or traders assumed it would. But after being born in September 2012 and ramping up to full steam in December 2012, the Fed finally killed off QE3’s new bond buying in October 2014.

With QE3 gone, and any QE4 a political impossibility for the Fed with the new Republican Congress, the stock markets just lost their driver that pushed them to such wildly overextended and overvalued levels. So sooner or later here, a major stock-market selloff is going to erupt and start cascading. And the Fed won’t be able to act to slow it down. It lost its window to monetize more debt, and interest rates are already at zero.

As this stock-market selloff persists, likely gradually growing into a new cyclical bear, the Fed-devastated alternative investments led by gold will return to favor. And as gold inevitably rebounds, the radically-undervalued gold stocks are going to soar. The Fed’s stock-market levitation killed gold in 2013, and the end of the Fed’s stock-market levitation in 2015 will restore gold. Gold stocks will simply amplify gold’s ride higher.

And their upside potential is truly epic. Once again, this week the GGR slumped to an all-time low of 0.149x. In the initial two-and-a-half years after the stock panic, this gold-stock valuation metric averaged a far-higher 0.419x. Merely to return to those normal-year levels, GDX (and the HUI) would have to nearly triple with a massive 182% gain! Can you imagine any other stock-market sector with such potential in 2015?

And the last time gold stocks were actually in favor with investors was before the stock panic. The pre-panic average GGR in the first eight calendar quarters of GDX’s existence was 0.591x. If gold stocks actually returned to favor again, which is certainly possible in a weak general-stock environment, they would at least quadruple from current levels. And I say at least for a couple reasons, gold and smaller gold stocks.

When the lofty US stock markets inevitably roll over and enter their overdue down cycle, gold is going to catch a major bid. Once again investors will start remembering the millennia-old wisdom of prudent portfolio diversification, so capital will flood back into the yellow metal. And given the extreme degree of underinvestment in the gold asset class today, this re-diversification is going to launch gold much higher.

As of the end of November, the 500 elite stocks of the S&P 500 had a collective market capitalization of $19,217b. Meanwhile GLD, the vehicle of choice for stock investors to gain gold exposure, was valued at just $28b. For centuries at least, the best investment advisors have recommended everyone have at least 5% of their portfolio in gold. But for our purposes today, let’s assume that can rise to merely 1%.

Today stock investors have just 0.15% of their capital in GLD as compared to their S&P 500 allocation. To get to 1%, which is still quite low historically, the amount of capital in gold at today’s prices would have to soar 6.9x! That much buying alone, not even counting traditional physical-gold investment, would certainly catapult the beaten-down gold price far higher. And that would flow through to the GGR.

As gold rallies, so will GLD which tracks the gold price. That means any given GGR will necessitate much-higher gold-stock levels. For example, back in 2012 before the Fed’s QE3 manipulations goosed the stock markets and decimated alternative investments, gold averaged just under $1675. That’s an amazing 41% above today’s levels! If gold just returned to pre-QE3 levels, gold-stock prices would soar accordingly.

Because of GLD’s annual 0.4% management fee over its decade since inception, it now trades at about 96.1% of the gold price. So let’s call $1675 gold $161 in GLD-share-price terms. At those levels and the initial post-panic-average GGR of 0.419x, GDX would have to rocket over $67. That’s a 275% upleg from current depressed gold-stock prices! Again, what other sector can quadruple from stock-market highs.

But gold-stock investors’ gains are likely to be even larger if they choose the right stocks. GDX and the HUI are dominated by the major gold miners, which have less upside potential than smaller gold miners. The large elites are so massive that it will take far more capital to overcome their inertia and drive their stock prices higher. The greatest performers in the next gold-stock upleg will be the best of the smaller miners.

GDX’s biggest holdings are mega-miners Goldcorp, Barrick Gold, and Newmont Mining. They have market capitalizations around $14.8b, $12.7b, and $9.5b today. It takes a lot of investor buying to push larger stocks higher. But the best of the smaller gold miners and explorers have market caps ranging from $0.1b to $2.5b, far smaller than the majors. So it will take far lower capital inflows to blast them higher.

A carefully-handpicked portfolio of the best of the smaller gold miners and explorers will trounce the coming gains in GDX and the HUI. The sheer profits leverage to gold many of these smaller miners have is breathtaking. And if they’ve survived this terrible and fearsome winnowing of the past couple years, they have cut costs to the bone. So their profits are going to explode higher as the gold price inevitably normalizes.

The bottom line is gold stocks are set to shine again in 2015. They’ve fallen relative to gold for far too long, driven by the impact of the Fed’s brazen stock-market manipulations on gold. But with QE3 done and any QE4 now politically impossible, the stock markets’ implied backstop has vanished. Without the Fed’s support, the next major selloff is going to be far larger. That will start bringing investors back to gold.

As gold rebounds and normalizes in this post-QE3 era, the wildly-undervalued gold stocks are going to just soar. Despite gold being way up near $1150 at the recent gold-stock lows, this sector was merely trading as if it was $350! This insane fundamentally-absurd disconnect can’t last for long, as all stocks are ultimately bid to levels reflecting their underlying earnings. So gold stocks are heading far higher soon.

- Is Santa Claus coming to town this year? To find out, please click here now. For US stock market investors, it looks like the Grinch just stole Christmas!

- Stock markets around the world are reeling, under pressure from the tumbling price of oil. On that daily chart of the Dow, it appears that all of this year’s gains may soon be lost.

- The FOMC meeting begins today, and Janet Yellen holds a press conference tomorrow afternoon. The Fed has consistently failed to raise inflation to their comfort zone, and the global oil price crash will make their job even harder now.

- If all the Fed says at the press conference is that “lower oil is good for consumers”, I’m concerned that institutional investors may lose confidence. The current global stock markets decline could morph into a horrific crash.

- In the big picture for gold, I’m vastly more focused on Chindian demand versus mine supply, than I am on anything that the Fed says or does. Regardless, if the Fed leaves the “considerable time” language in their statement tomorrow, that should provide a nice short term boost to gold prices.

- Please click here now. That’s the daily oil chart. Lower fuel prices may not be good for the Dow, but they should help gold mining companies lower their cost of production.

- Even mainstream news outlets like CNBC are recommending that investors buy gold stocks now, and I think that’s a wise move on their part.

- “Of course, it hasn’t been a great year for many commodities. Gold, too, is off of its highs, which makes Bill Baruch of iiTrader think it could succumb to tax-related selling in the sessions ahead. Still, Baruch says the better trade isn’t going short for the short-term, but looking for the buying opportunities that tax-pressured selling could create.” – CNBC News, December 14, 2014.

- Junior gold stocks are suffering some “tax loss selling”, but their overall decline is very minor compared with 2013. On that note, please click here now.

- That’s the daily GDXJ chart. In 2013, the price declined from about $85 to $29, and terrified many investors in the gold community. This year, it’s declined from $29 to $22. Note the difference in the slopes of decline on the chart.

- I think 2015 will be a good year for both the juniors and bigger producers. While deflation from lower oil prices will affect the prices of many consumer goods, the price of gold is largely determined by demand from China and India.

- That demand continues to grow, and in the case of India, it’s inelastic. “GST will replace the plethora of indirect taxes — excise, sales tax, service tax, entry tax and other local levies — with one single levy, helping create a national market for goods and delivery of services. State-specific levies and entry taxes lead to loss of revenue and cascading of taxes — taxes on taxes. Some estimates suggest GST could add as much as two percentage points to GDP. The government feels the improving fiscal situation because of softer crude prices and decontrol of diesel has given it room to meet compensation demands.” – The Economic Times, December 16, 2014.

- Note the prediction that the GST tax will add almost two percent to Indian GDP growth. I’ve predicted that India is on the cusp of entering an era of double digit GDP growth, an era that will ultimately create gold demand that is five times the size of the already-enormous demand in China.

- Please click here now. That’s the weekly GDX chart. A double bottom pattern is beginning to form, and the lower volume in the area of the second bottom suggests this should be a “textbook” formation.

- For a closer look at the chart, please click here now. That’s the daily GDX chart. It’s clear that volume is shrinking as the second bottom forms. My gold shares position has never been this large, and I’m ready for a fabulous year in 2015.

- I’ve suggested repeatedly that the world’s biggest geopolitical driver of the price of gold is the relationship between Pakistan and India, particularly in the Kashmir “Line of Control” region.

- Both nations have significant stockpiles of nuclear weapons. If Pakistan’s government were to become unstable, the situation could quickly escalate into a nightmare scenario.

- Please click here now. The Taliban and ISIS both want to rule Pakistan, and if they are even partially successful in achieving that goal, I would expect the price of gold to move significantly higher.

- Gold investors need to keep a very close eye on geopolitical events that occur in Pakistan, and particularly in the Kashmir region.

- I have received a number of emails from investors in the gold community, asking about the decision of the CME to implement price limits (collars) for gold and silver futures contracts. Collars can create violent price movements, because investors who get margin calls can’t liquidate when the price is halted. When trading begins again, the price can gap higher, causing another trading halt.

- Investors who are carrying large leveraged short positions could be wiped out if a series of trading halts were to occur while the gold price was moving violently higher.

- I want to finish today’s update with a look at the US dollar versus the yen. Over the past few months, a lot of forex traders thought gold would crash when the yen did, but that hasn’t happened. Gold has little risk from a rising dollar, because most Western investors don’t have any gold to sell, and Eastern buyers mainly buy jewellery for cultural and religious reasons rather than for investment.

- A falling dollar will make gold attractive to Western institutional buyers, which is a win-win situation for the gold community! Please click here now. That’s the weekly chart of the dollar versus the yen.

- For a closer look at it, please click here now. That’s the hourly bars chart. Note the head and shoulders top pattern that is clearly in play. The dollar looks set to crash against the yen, and I suspect Janet Yellen’s press conference could be the catalyst, and create a nice gold price spike to the upside. Rather than end 2014 on a down note, gold seems set to shock the gold community, and end the year with a big rally!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

For years I have highlighted a strategic metal called niobium. See my recent article on the topic by clicking on the following link below: http://seekingalpha.com/article/2288223-the-west-must-look-for-a-secure-supply-of-niobium

Recently Iamgold sold Niobec, one of the largest niobium mines in North America for $500 million cash and an additional $30 million once it comes into production.

See the news by clicking the link below: http://www.reuters.com/article/2014/10/03/iamgold-divestiture-idUSL3N0RY2CL20141003

This could be a huge boost for Niocorp (NB.V or NIOBF) which is up over 536% over the past two years while the TSX Venture has lost close to half its value.

See one of our first reports on Niocorp when it was still called Quantum Rare Earth Development from over two years ago by clicking here…

Niocorp just announced an off-take agreement with ThysenKrupp for 50% of its planned production. Niocorp CEO Mark Smith stated in the Press Release, “Having the Agreement in place and discussing debt and equity financing possibilities with ThyssenKrupp Metallurgical Products, clearly enhances NioCorp’s prospects of achieving those milestones.” See the full news release by clicking here…

This outperformance over the past two years could be due to Niocorp being run by veteran miner Mark Smith, the former CEO of Molycorp. The sale of Iamgold’s Niobec gives investors and analyst a valuation benchmark to be used when comparing Niocorp’s Elk Creek Deposit.

According to Niocorp CEO Mark Smith, the Niobec sale “demonstrates the strong demand and understanding of the strategic nature of niobium.”

Even though the precious metal and junior mining sector have been in decline for the past few years, there have been a few exceptions due to the high quality of both the management team and the asset. One of the areas of strength has been in a relatively unknown metal known as niobium. What is niobium and why is it so important?

Niobium is critical for high strength low weight steel that is required in the automobile, infrastructure and aviation industries. Niobium prices have increased steadily over the past 40 years, but may move higher at a faster rate as niobium demand is increasing due to its ability to reduce consumption of energy. A little niobium decreases the weight and increases fuel efficiency.

One of the junior niobium miners, Niocorp (NB.V or NIOBF) has been one of the best performers on the TSX Venture over the past year. The main catalyst was attracting top notch CEO Mark Smith who brought Molycorp’s (MCP) Mountain Pass Rare Earth Deposit into production.

Mark has decades of experience of bringing mines into production. Mark put his money where his mouth is and bought a large position over the past year in Niocorp which is developing North America’s largest and highest grade undeveloped niobium deposit near Elk Creek, Nebraska.

Mark has put together a quality team to advance the project towards a Bankable Feasibility Study. Niocorp is currently drilling a 3 stage program to move the resource from inferred to measured and indicated. The recent drilling program has been a huge success hitting some of the highest grade assays ever recorded at the project. Major players should begin noticing this high grade niobium material. Recently Niocorp engaged a firm “exploring the option of listing its securities on a more senior North America stock exchange.”

As Mark Smith, CEO of Niocorp said in the recent news release on the second stage drilling program,

“The final Phase II drilling results continue to be extremely encouraging and supportive of our project…I could not be more pleased with the overall high-grade assay results that have been delivered from both our Phase I and Phase II drilling program at our Elk Creek deposit…Third Phase drilling will be completed by mid-December 2014, and we are anxiously awaiting the upcoming analytical results.”

It appears the grades are higher at depth where the deposit remains open. In addition, there are additional targets to the southeast and northwest of the deposit.

Concurrently, a major metallurgical program is underway at two well known research labs at SGS Canada and Hazen. SRK Consulting has already initiated preliminary work on the feasibility study.

In conclusion, Niobium demand has been increasing for the past 40 years and should accelerate as demand is increasing for high strength low weight steel. Niocorp could be one of the largest suppliers of niobium in North America and take advantage of the increased consumption of niobium. Recent results both with the drill and on the metallurgy could attract significant strategic financial partners on this project in the coming months.

Mr. Smith is well recognized in the mining community, having recently served as CEO and Director of Molycorp, Inc., where he was instrumentally involved in taking that from a private company to a publicly traded producing mine. Prior to that, Mr. Smith was the President and Chief Executive Officer of Chevron Mining Inc. and managed the real estate, remediation, mining and carbon divisions of Unocal Corporation for over 22 years. During his tenure with Chevron Mining Inc., Mr. Smith also served as a Director of Companhia Brasileira de Metalurgia e Mineração (CBMM), part of the Moreira Salles Group, a private company that currently produces approximately 85% of the world supply of Niobium. Mr. Smith has a Bachelor of Science degree in engineering from Colorado State University and a Juris Doctor cum laude from Western State University, College of Law.

Niocorp is forming a potentially bullish flag pattern for over eight months. Look for a breakout into new highs at $.80.

See my recent interview with Niocorp (NB.V or NIOBF) CEO Mark Smith by clicking on the following link.

Disclosure: I own Niocorp and they are a website sponsor.

We’ve believed that Gold would need to break $1100 before we thought a bottom could start to develop. While that could still be the case, we are starting to see building evidence that precious metals could be forming a bottom.

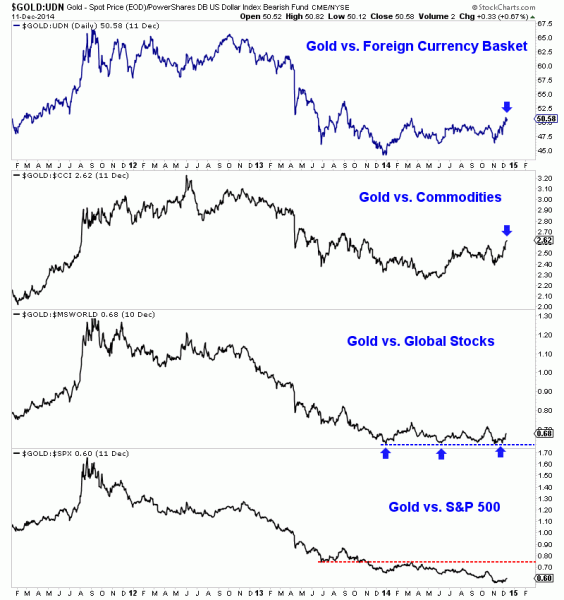

In the past we’ve written about the importance of Gold’s performance against other asset classes. Relative strength in Gold has preceded important bottoms in the Gold price during 2001, 2005 and 2008. That relative strength is starting to show. Below we plot Gold against various asset classes, which are noted in the chart. Several days ago Gold against foreign currencies (and the Euro) closed at a 15-month high. Gold has also moved to a 13-month high against Commodities. Also Gold may have bottomed against global equities as it has held support three times in 2014. Gold is weak only against the S&P 500.

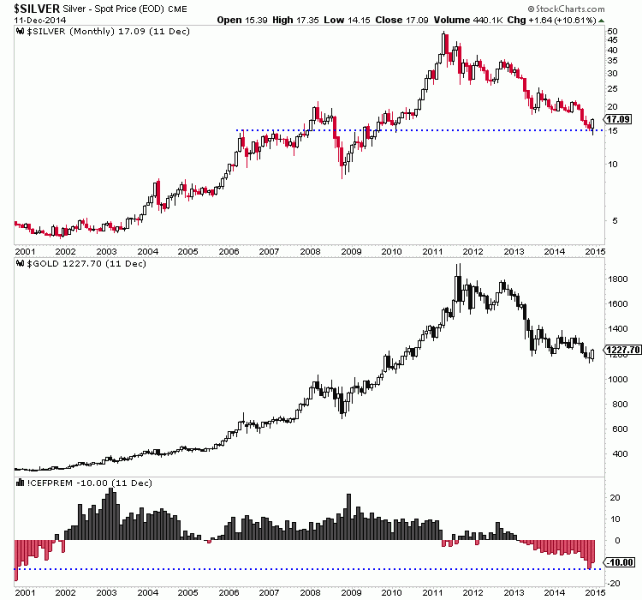

Below we plot Silver and Gold in a monthly chart along with the discount/premium to NAV for CEF, the Central Fund of Canada which holds physical precious metals. There are still two weeks left this month but thus far the monthly chart is making a strong statement. Silver has formed a strong bullish hammer after testing $14. The candle has just about engulfed the previous two months of trading. If the candle holds then this will be the strongest and most bullish candle since the bear began. In addition, CEF’s discount to NAV recently peaked at 13%. That is the highest discount in 14 years! Meanwhile, Gold is also in position to engulf the previous two candles. During the bear, Gold never came close to doing that at any of its lows.

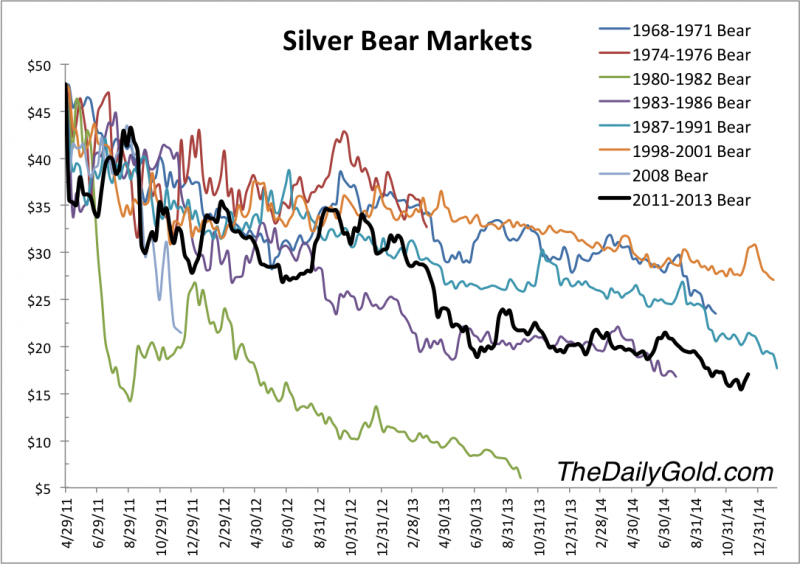

Sticking with Silver, lets take a look at the bear analog chart. Silver’s bear is already the second worst in price and the third worst in time. The two bears which lasted longer (albeit by only a few months) were considerably higher in price at this juncture. It’s really hard to imagine downside in Silver below $14-$15.

These are only a few charts from many we follow and consider but they are sending strong signals. We focus on Silver as it peaked before Gold and needs to show bullish signs for the bear market to terminate. Silver has put in what at this point appears to be a major bullish reversal and from major support at $15. Meanwhile, some (but not all) of its sentiment indicators reached true extremes and its bear analog tells us the current bear has gone deep enough and far enough. On the other side, we like what we are seeing from Gold. It is showing increasing relative strength against foreign currencies, commodities and to a lesser degree global equities. Strength in the US$ and US equities are the only things holding it back from a strong rebound. Those markets could be due for a correction.

Going forward, here are some things I will be watching to determine if a real bottom is in place. First, metals need to close the month strong and not lose current gains. Second, Gold needs to continue to show relative strength and especially against the S&P 500. Third, the miners (HUI, GDX, GDXJ) need to rebound strongly from this next low, whether it be a double bottom or false new low. In the past we’ve written that opportunities are coming. It appears that opportunities are now fast approaching with respect to the mining equities. We are working hard to prepare subscribers for these opportunities.

I recently read an article entitled, “Graphite One is Dead Money.” The author did a good job of pointing out the attributes of the Graphite One Resources (GPHOF) (GPH.v) story. And I commend the writer for writing a balanced piece considering both the pros and cons in a measured way. He mentions Graphite One’s massive flake graphite project called, Graphite Creek in Alaska, USA.

For example he said,

“it is not implausible that the resource could grow substantially from the most recent estimates to become the largest graphite resource in the world.”

The author also pointed out that trading volume in the stock is high. Further, the deposit was described as close to surface and, “it appears to have the potential to be a very low-cost mine in the future.” However the author is betting against Graphite One, saying that the company is,“unattractive except in the most optimistic scenarios for graphite prices.”

In my opinion this author in going through his list of negatives about Graphite One is really just speaking to the generic risks of most junior graphite companies. For example he says,

“maximizing leverage to the graphite space using graphite junior mining shares as option-proxies makes sense only to a very limited extent. Not only that, but it takes a fairly unique set of qualities to make a graphite junior attractive…”

Any investor in graphite juniors needs to know this is a high risk, high return sector. Still, it’s better to be a U.S. domiciled company like Graphite One then a third-world or Chinese producer. Right now, virtually all Venture-listed stocks have been hammered, perhaps in part due to tax loss selling. I feel the author could have taken any number of graphite and other sector stocks and picked them apart. It’s easy to play devil’s advocate.

I will now attempt to refute some of the statements made by this author. For example, he described Graphite One as an early-stage flake graphite company due to a small number of drill holes. I would not call this an early-stage project by any means given that it has a giant inferred resource and is soon coming out with a new resource report that will include a portion of indicated resources. Would the author instead want Graphite One to have spent additional capital to drill many more holes when they have already found so much? CEO Anthony Huston had this to say about the stage of development of the Graphite Creek deposit.

“Our deposit has unique characteristics that, taken together, put us above some of our peers. We believe that our high grades, low strip ratio, proportion of large flakes and lack of deleterious elements are some of the best in the industry. Further work on characterization of the mineralization in our advanced stage metallurgical processing test work will lead to a pilot scale test in fall of 2015 in preparation for the Feasibility Study.”

In fact, it’s interesting that the author of the other article mentions drilling in a negative light. Graphite One’s recent press release from December 1st describes in detail the company’s drilling success. In this press release the company announces assay results on 10 of 20 drilled holes, bringing the total holes drilled to almost 50. From the press release,

“Graphite One Resources is pleased to announce the results of the first ten holes of the recently completed twenty-hole diamond drill program on their Graphite Creek Project located near Nome, Alaska. All 10 holes intercepted significant widths of high grade, near surface graphite mineralization. Select intercepts include 7m of 20.98%, 50m of 6.13%, 38m of 10.57% and 23m of 8.70% graphite. Geology and assays confirm excellent vertical and lateral continuity of the mineralization.”

Despite what appears to be clear drilling success, the author suggests that a low cut-off grade of 3% is required to show a 10 million metric tonne resource. True. However, at a 7% cut-off there’s still 3.5 million in-situ tonnes. And, as the author states, Graphite One could just mine the ore using a 10% cut-off, which would provide for 1.1 million tonnes at an average grade of 12.8%. That alone would be a 22-year mine life at 50,000 tonnes per year. As mentioned, a new resource estimate is out in a few months that is expected to move some of the inferred resource to the indicated category. I would reserve judgment until I see that report.

Graphite One states that its Preliminary Economic Assessment, “PEA” will be released in the 2nd quarter of 2015. Yet, the author of the negative article says that we won’t see a PEA until, “2016 at the earliest.” I prefer to go with company guidance of a PEA delivered in the second quarter of 2015! [See page 21 of the company’s corporate presentation.] Further, with the size of the resource at Graphite Creek, the costs and scalability of the deposit may allow for multiple development scenarios to be delineated in the PEA.

Next, the author moves on to equity dilution. All graphite juniors are facing equity dilution at this time, why single out Graphite One? In fact, Graphite One in Alaska possibly has access to an Alaskan loan program that could deliver a very significant loan to the company post Bank Feasibility Study. According to this program’s website,

“With approximately $1.4 Billion under its management, the Authority has an ownership position in 8 Alaskan projects, has issued in excess of $1.3 Billion in Conduit Bonds and has a loan portfolio in excess of $400 million.”

Just ask Ucore, and Alaskan rare earths player what they think of this loan program known as AIDEA. That company is close to obtaining a $140 million loan from AIDEA.

The author says that the property is, “in the middle of nowhere.” I disagree. According to the company’s website, “The Property is 3 kilometers away from inter-tidal waters at the Grantley Harbour, approximately 20 kilometers away from road systems, and 3 kilometers from an airstrip to the southeast. Sure, a road might need to be built, along with some other infrastructure, but this is hardly in the middle of nowhere, especially with regard to its close proximity to barging and the town of Nome.

The company can barge graphite to an Alaskan seaport and then send it to west coast U.S. ports. Regarding another aspect of allegedly being in the middle of nowhere, management states that the project is a 45 minute drive from Nome, with a population of about 4,000. Don’t get me wrong, there will be challenges, but I believe some of the other graphite juniors around the world face similar or worse logistical challenges. As security of supply becomes increasingly important, sourcing graphite from the U.S., (which imports 100%) will become an important strategic advantage.

The author states that prospective investors need to be bullish on the demand for graphite. I agree. I’m bullish, as are a number of notable pundits including Simon Moores of Benchmark Mineral Intelligencewho states,

“Tesla’s giga-factory isn’t the only electric-vehicle battery factory on deck. Moores pointed out that 2014 also saw LG Chem break ground on its own factory in China, while Foxconn Technology has plans for its own plant in the same country.”

At least three giga-factories coming online, and there will be more. Some pundits believe that li-ion battery demand alone could require the output of 8-12 new graphite mines by the end of the decade. I think that Graphite One’s Graphite Creek will be one of those mines. Said another way, there’s going to be ample demand for a number of North America’s presumed front runners Mason Graphite (OTCQX:MGPHF), Focus Graphite (OTCQX:FCSMF), Northern Graphite (OTCQX:NGPHF) andAlabama Graphite (OTCQX:ABGPF), as well as Graphite One.

The author states that management lacks direct graphite experience. However, if the company is as far away from production as the author surmises, why hire more people, thereby increasing overhead? That lack of management experience argument can’t cut both ways. More importantly, Graphite One has retained the TRU Group to help it manage the company’s activities. If one wants to see solid evidence of graphite experience to the benefit of Graphite One, please click on the link to the TRU Group.

Graphite One’s exploration team since inception has been a group of Arctic exploration experts with years of experience working in the north of Alaska and Canada as well as around the world in harsh environments. The project manager is based out of Fairbanks. The consulting engineering and environmental experts are almost all Alaska based companies with years of experience evaluating and building projects in Alaska. The company will continue to use local contractors as the project moves through the Feasibility review.

The review of senior management and the Board is short-sighted as many of the senior management team have worked in multiple natural resource markets including uranium, coal, copper, lead, zinc, lithium, as well as gold and silver. Several Board members have diverse experience in multiple disciplines including exploration, production, capital raising and marketing of natural resources.

Conclusion

The graphite juniors are high risk investments. Graphite One, trading at about a third of the valuation of Focus and Mason offers compelling upside to a strong graphite market. The author of the negative piece referred to at length above suggests that strong graphite prices are needed to make Graphite One viable. I believe that strong graphite prices will be needed to make most graphite projects viable. There’s room for plenty of companies to serve the growing global demand for graphite. I believe Graphite One is likely to be one of those companies.

To a packed crowd in Vancouver yesterday, veteran junior resource analyst John Kaiser gave a presentation hosted by AME BC entitled, Confronting the Potential Extinction of a Canadian Institution.

Here is a link to the 59 slide PDF presentation, courtesy John Kaiser.

Mr. Kaiser has been closely involved with Canada’s venture capital markets for over thirty years. In the 80’s and early 90’s, he was a research analyst at various securities firms focused on the junior resource sector. In 1994 he started his own newsletter, known as Kaiser Research or Kaiser Bottom Fish Report, that has earned a reputation for being the most comprehensive data source on Canada’s public venture capital markets.

Mr. Kaiser has a bulletproof reputation and is a sought after guest on business television and at conferences.

In his presentation to the AME, BC’s mining lobby group, Kaiser begins by reviewing the junior resource markets from 1978 until today. In that time span, Canadian venture capital stock exchanges provided the early stage capital for countless wealth creating mineral discoveries, but has undergone a number of structural changes aimed at preventing frauds. In hindsight, Kaiser says these regulations are now overkill.

Kaiser believes there are four key narratives that drive investment in early stage mining equities, and notes that none of them appear to apply today. These Key Narratives are:

- Commodity Cycle

- Security of Supply

- Gold/Silver Bug

- Exploration/Discovery

Brokerage firms, which used to be the lifeblood of the business, are now making it difficult for their Investment Advisers to put their clients in the sector.

These Canadian financial institutions used to serve as “Network Hubs” for knowledge transfer and rumour mongering, but that’s gone now, according to Kaiser. Big banks have consolidated the brokerage industry in Canada and the business model has evolved away from transactional business. This has killed the after-market for high risk stocks.

Another issue with Canada’s venture capital model, according to Kaiser, is that only Accredited Investors (loosely: individuals earning over $200k a year for two years in a row or with more than $1 million liquid assets) can invest money directly into early stage companies, while regular investors are restricted from doing so, yet can buy all the stock they want in the open market.

This is “illogical” according to Kaiser and preventing cash from reaching companies. “Wealth and income do not imply sophistication,” he said.

Kaiser made a number of suggestions for how Canada can continue to be a world leader in financing mineral discoveries, which you can read in the presentation.

“Do not make the mistake of thinking that the world will suffer a future metals deficit if the Canadian public resource junior institution is allowed to die,” Kaiser warns.

Read the entire presentation here. It’s very good.

I just bought my first ever Australian listed stock. It’s a small speculative position that I initiated because I think the technology/mining/water play is just getting going, and has some great people involved.

The company is Clean TeQ Holdings (ASX:CLQ), and it has a roughly $20 million market capitalization.

Clean Teq is a technology business focused on continuous ion exchange for air and water purification, as well as minerals processing.

They say they can decrease water purification costs at mega projects by as much as 30%.

The minerals processing business is interesting in that continuous ion exchange can increase recoveries from previously uneconomic ores as well as tailings (waste) dumps.

The company is roughly 20% owned by mining legend Robert Friedland.

Clean TeQ is in the process of buying the Systerson scandium project in Western Australia from Ivanhoe Mines for roughly $1 million in stock.

The market for scandium currently is virtually non-existent, but resource analyst John Kaiser believes that with a reliable supply, demand could increase exponentially. Scandium, as an alloy, allows aluminum to be welded. Imagine airplanes without rivets, weighing 15-20% less.

Clean TeQ’s Chairman Sam Riggall is a Melbourne-based lawyer and close advisor to Friedland. Riggall helped negotiate the investment agreement between Rio Tinto and Mongolia to build the massive Oyu Tolgoi copper-gold project. In an earlier life, he worked as second in command in the project generation group at Rio Tinto under Sam Walsh and then Andrew Mackenzie. These men now run two of the world’s largest miners, Rio and BHP Billiton.

In a quick call from a taxicab in Australia, Riggall tells us Syerston could have the highest grade scandium deposit in the world, and is very shallow, making it amenable to mining. With nearly $30 million in historical work done on the project by Ivanhoe, Riggall thinks he can advance Syerston quickly.

The scandium business will really get going when one of the potential scandium developers (Clean TeQ, Scandium International, Jervois Mining, Platina Resources, etc.) completes a meaningful off-take agreement with an end user such as an aerospace or fuel cell manufacturer. Riggall thinks Clean TeQ has the best shot because of their minerals processing technology: they are currently testing scandium recovery in one of their test plants in Japan, with promising early-stage showings, Riggall said. The Ivanhoe involvement should also help open a few doors for the company.

In its water business, Clean TeQ is working on a large pilot project with a Chinese group and Riggall believes it could lead to multi-hundred million dollar projects, with significant margins for the small company.

Those water treatment revenues are lumpy, Riggall says, and he notes that the air purification business has become competitive, and less of a focus for the company.

Kaiser Research chief John Kaiser thinks that the scandium story is one of the few segments of the mining sector that offers promise for investors in today’s market environment. On a phone call late last week, Mr. Kaiser, a follower of more than a thousand venture-stage equities, commented that Scandium International was his current top pick. Its shares are up over 500% this year alone thanks to a meaningful push from Mr. Kaiser.

Still, there is little to no market for scandium yet, and until a meaningful order arrives from an end user Mr. Kaiser’s dream will remain just that – a fantasy. With that said, Friedland’s latest move suggests the scandium space is about to start heating up.

For more information, Mr. Kaiser suggests this white paper on scandium (Link here).

Further interviews with Mr. Kaiser and Mr. Riggall will make it to these pages in the coming weeks.

This is not investment advice and may contain errors. Always do your own due diligence.

In a recent article I wrote, “Gold and silver could gap higher by the end of 2014 and the top notch juniors could skyrocket.” I expected a breakout at $1205. It appears gold may be breaking that downtrend today.

Click here for reference chart.

For a couple of years metals were knocked out of favor and now oil is on its knees with a major three month deflationary selloff that came out of nowhere. This black swan may be due to increasing tensions between the West and East.

Japan and Europe are turning on the printing presses to prevent deflation causing investors to flock to US dollars and the S&P500. Don’t be so quick to chase them into the overbought markets.

The Fed needs to see more inflation and a cheaper dollar before raising rates. Once investors wake up and realize The Fed can’t tighten in this environment, the dollar parabolic rise will pop. Once the dollar rally fizzles out investors should once again return to the beaten down junior gold and silver sector which is testing 2008 Credit Crisis All Time Lows.

Remember we are in tax loss selling season and the time to buy discounted junior resource stocks is over the next 3 weeks. Since we are at such a low base the January effect could be quite powerful.

Cash is now king as other nations are following Europe and Japan beginning a major fiat currency war. The Russian Ruble is crashing and now the Russian economy is entering a major recession possible depression. What we are seeing with increasing tensions between the West and Russia and China and Japan are trade wars.

History shows that these policies lead to economic crashes which the metals and oil may be forecasting. These deflations could be followed by hyperinflations as governments resort to currency devaluations through quantitative easing.

Consumers in the US may be excited to see gas prices under $2 and their inflated retirement accounts, however these low prices could cause a ripple effect throughout the entire global economy.

We could be on the verge of the next major worldwide banking crisis especially in resource rich countries such as Russia, Canada and Australia. Major banks have been loaning out billions to oil and gas producers for production, construction and exploration. If we do not see a quick v shaped recovery expect the global unemployment rate to once again spike as well.

The US may be forced once again to resort to Quantitative Easing in 2015 to prevent this runaway US dollar price spike. Its the Fed policy to promote inflation and a stable dollar. A strong dollar moving parabolically higher could be a major challenge to US banks sitting on bad real estate and energy loans.

This could cause banks to stop lending and begin a massive deleveraging similar to 2008. Remember don’t fight the Fed who want asset prices to remain moving higher. They will try all attempts to prevent a runaway US dollar through competitive devaluation.

Notice the Canadian Venture is now testing 2008 lows while the S&P500 has broken way above pre Credit Crisis 2007 Highs. Since 2011, we have seen a decoupling between the S&P500 and the TSX Venture. For the past decade the two indices moved together. This changed in 2011 when the US began to slow down QE while the rest of the world accelerated it. This may have caused a historic decoupling not seen since the Dot Com Bubble in the late 90′s. If the Venture returned to previous 2007 levels and comparable ratios to the S&P500 then the TSX Venture could be trading at multiples of its current valuation.