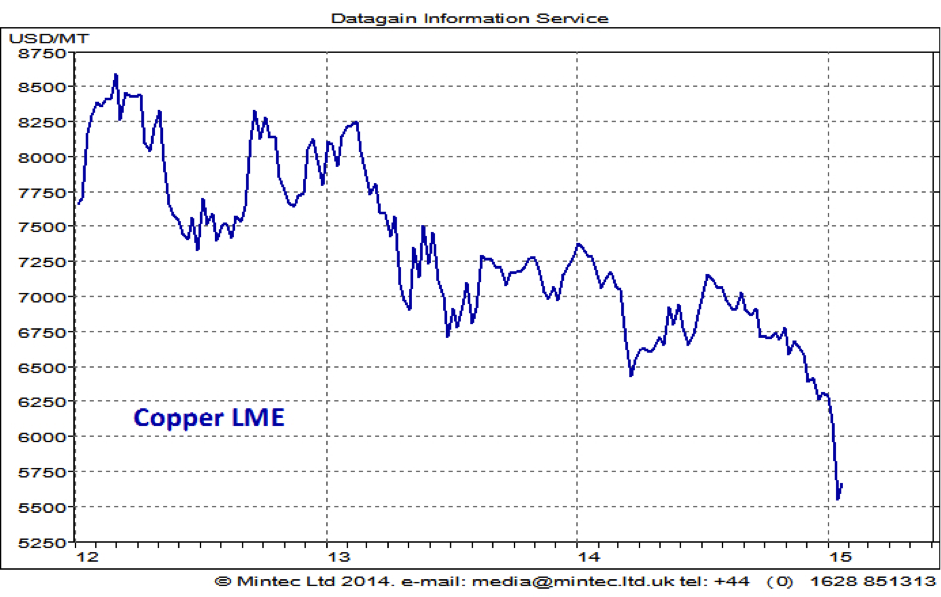

Copper prices fell sharply at the start of the year, 11% down since the beginning of January. Prices have been in decline since mid-2014, broadly in line with the trend seen in other base metals; however, it was an extent of the fall that was remarkable, with prices declining in January more than for the whole of 2014 – down 14%. There is always a great degree of uncertainty and speculation around copper pricing, so understanding what is behind the price movement is a tricky business. So, what are the key factors driving copper prices?

Click here for reference chart.

Economic sentiment

Copper is the third most widely used metal after steel and aluminium. Of all the non-precious metals, it is the best conductor of electricity, and as such is widely used for cables and wiring. It is therefore crucial for sectors such as electricity, consumer electronics and transport. Copper prices are particularly sensitive to changes in the global economic environment due to its use in a broad range of industrial and consumer applications.

Global economic sentiment has deteriorated in 2014, particularly in the second half. Although the US economy has been strong in recent months, the rest of the world, notably China and the eurozone, have generally been below expectations.

In January, the forecast for eurozone for 2015 was cut to 1.2%, down 0.2 percentage points compared to previous forecasts, with deflation considered a major threat to economic recovery both for the eurozone and globally. The GDP of the euro area is still below the pre-crisis level, unlike in the US, where the pre-crisis peak has been surpassed.

Economic growth in China continues to slow after the rapid growth seen over the last decade. China’s growth has slowed to 7.4% in 2014, falling under the government target of 7.5%. Growth for 2015 is expected to be even lower at 7.1% due to the continuing slowdown in real estate investment.

With most of the expected increases in future global consumption coming from outside the US, this disappointing international economic news have been pushing copper prices downward in recent months.

Supply and demand

In the first half of the year, it looked like situation was improving in the copper market, continuing the trend seen in 2013, with even small surplus expected for 2014. However, towards the end of the year, analysts have cut back their surplus forecast, and some are even expecting a small production deficit, estimated at around 160,000 for the first 10 months of 2014.

World mine production is estimated to have increased by around 2% in the first ten months of 2014. With the exception of Chile, where production remained largely unchanged, output rose from most producers.

Despite slowdown in some major economies, a strong demand growth was posted in the first ten months of 2014. World consumption is estimated to have reached 1.9m tonnes, up 11% y-o-y. Notably, higher than expected demand was recorded for China, where lower supply of high-grade scrap led to the use of more cathode. In addition, demand in China was driven by the ongoing expansion of the nation’s electricity grid infrastructure. Demand from China is estimated to have risen by 18%. Outside China, world demand rose by 5%, driven largely by growth in the EU and Japan, up 11% and 10% respectively.

China

The determination of the price of copper is increasingly dominated by China, which is responsible for over 40% of global consumption. Consumption growth has slowed in China in recent years, but still remained at relatively high levels. One area that adds uncertainty in global copper market is unknown size of stocks in China. Significant part of copper stocks in China is widely believed to have been used as collateral for financing deals, rather than for physical consumption. The extent and scale of these activities are largely unknown, although the trend is reported to be on the decline in recent months. However, offsetting this, estimates for strategic buying by the State Reserve Bureau (SBR), one of the most influential players in the global metals markets, doubled for 2014.

Outlook

Looking ahead, demand is likely to remain robust in 2015. Tightness in scrap metal prices is likely to continue in 2015. As is strategic buying by China’s State Reserve Bureau (SRB), albeit the scale of this expected buying is uncertain. Recent sharp falls in prices have been largely driven by cuts to global economic growth and falling prices of other major industrial commodities. So, in this context, the sharp falls of recent weeks look exaggerated. Although expectations of slowdown in global economic growth is likely to continue to drive prices down, relatively tight fundamentals and policies in China aimed to support its economy, including continued investment in infrastructure and monetary easing by central bank, will limit price declines.

Jordan Trimble, 27 is currently the youngest CEO of any publicly traded mining company. This young dynamo entered the business straight out of university and is now running Skyharbour Resources (SKY.V). Skyharbour is a uranium junior holding a very prospective land position(over 390,000 hectares) in the prolific Athabasca Basin.

Jordan made several property deals in the past couple years while at the same time studying for his CFA exam, which he just completed (and is now a CFA charter holder). He has also put together an experienced team led by head geologist Rick Kusmirksi who is the former VP exploration for Cameco.

Skyharbour has numerous exploration properties that offer shareholders a shot at making a uranium discovery. One of the properties acquired (Way Lake) already has a 43-101 inferred resource of 7 million pounds of uranium.

Recently Tommy Humphreys sat down with Jordan to talk about how and why he entered the mining business, what he has learned so far, and what investors can expect from Skyharbour in 2015.

Here is the full transcript:

Jordan Trimble, Skyharbour Resources CEO,

TH: So Jordy you came into the business in 08 or 09?

JT: It was actually the beginning of 2010. I was in the office for a summer when I was out of school which was actually 09. I kind of saw just the initial part of the recovery from the financial crisis but really didn’t get going full time till until early January 2010.

TH: It was great timing. I would like to review quickly the Bayfield experience with you. So your group has just sold one of its stable companies to New Gold.

JT: New Gold.

TH: Bayfield it is called and Jordan was there I think when they had that great Burns Block discovery in 2010 and everybody was making money. What has been the experience of going from boom times to bust and what have you learned through the process?

JT: You know I was fortunate to get in during a boom as we saw. It was an incredible boom. I mean it was one of the best bull markets when you talk with people who have been doing it again for many decades.This was one of the better ones; that recovery from the bottom up to 2010/2011. When I started really my initial deal I was working on was Bayfield with Jim. We would go out to Toronto and we’d market and raise capital. We were travelling a lot, we were on the road a lot for it.

The experience for me being young and impressionable, it really kind of lit a fire under my belly in a good way where I saw the core of it. I saw the good side of this industry. I saw what you can do when you raise capital and you go and explore and you put the right ingredients together.

You have the right team, you have the right management, a big thing obviously is the technical team. Bob Marvin was our geologist, great geologist. You have the right assets, right projects, right methodology, and you have the right structure so on and so forth. You hear about this all the time. In that case we did have a much better market. When you have the right ingredients it showed me how lucrative and how quickly you can create value and create wealth. There are very few other industries/sectors out there where you can have that kind of return in that short of time.

TH: Do you think investors have forgotten that?

JT: Yes, I think so. We have seen it over the last 3-4 years now investors are losing or have lost sight of that. As we are seeing the only people financing these early stage deals and projects are the ones that have seen the cycles and have the wisdom and the experience to know that it will turn around eventually.

TH: How do you be a great junior mining CEO?

JT: In this market in particular you really need to be prudent with each dollar. Whether that is going towards the exploration, whether that is going towards the G&A, marketing etc.

Right now there are a lot of companies out there that are just trying to survive.I think it is healthy what we are going through, there are too many issuers out there and you have heard this lots. This has been an underpinning theme over the last couple years. I agree, it is basic supply and demand you have too much supply out there right now and that’s fixing itself.

I think as a CEO as a manager of these companies, you are not going to be the jack of all trades.I don’t pretend to be a geologist. My focus, my expertise is more on the market and finance side of things. If you can find the best geologists, you can find the best technical guys, you can find the best team that you can surround yourself with. I think that is the probably one of the top top criteria points: be able to work with them and be able to have them work together in harmony and that is tough to do.

TH: But the biggest job of a CEO right now is to find the money now right?

JT: Right now absolutely it is. In our space (the junior side of things) that is the biggest part. We have been fortunate – again the group that I work with has been around for over 20 years and seen ‘the good the bad and the ugly’ in these markets and have always been able to raise capital. Always survived.

TH: Where is money going to come from for the sector?

JT: From my perspective right now it is coming from the high net worth individuals/ sophisticated investors that have historically been focused in the resource space. I see that continuing depending on what type of a company what type of a market cap you are looking at, for the smaller cap companies. I think that will be the source of financing for a little bit here.

TH: Pros. So you just passed the CFA level three so you’re a CFA charter holder now?

JT: I am.

TH: Congratulations.

JT: Thank you.

TH: So what was your hope in taking the CFA? Trying to better understand the buy side or?

JT: You know, I get asked that a lot. I think that for investors, a lot has changed in our industry in the last 20 or 30 years, like the way they do their due diligence. The way investors analyze and pick stocks is changing fundamentally.

I really see value in being able to understand how this sector and how these investments play into a broader portfolio. You know you’re not going to have 100% of your portfolio locked in on junior exploration companies.

However, as an alternative investment there is a place for this asset class. It is a high risk, high return asset class. If you want access to an asset class that fits in your portfolio that diversifies your portfolio, this asset class works. I want to be able to convey that to the retail investor and to the hedge fund manager.

The CFA was really a channel for me to understand how a portfolio manager thinks and I learned how to converse with them on a different level, not just do the elevator pitch if you will.

TH: So Jordy now that you passed… I guess they say the hardest financial exams are behind you now.. the CFA… Do you think you can get the stock up now?

JT: (laughter) I didn’t see much correlation there but you know I hope so.

TH: So what is going on with Skyharbour right now – you’re a small uranium explorer and where does it stand?

JT: Skyharbour needless to say is my main focus. I have dedicated my life to it and I am going to see it through to the end. I am a young guy and this is my first deal, and I am going to make sure it works out right. What really excited me initially about getting involved and putting the deal together was uranium. This was the sector that I wanted to get the company involved with.

Just some basic, basic things that stood out to me: you had a sub sector within the resource space that had been absolutely crippled by black swan events; you had the uranium bubble burst in 2007; you had the financial crisis which was of course global but nonetheless uranium companies were caught up in that; and then you had Fukushima. So this sub sector had been absolutely thrashed around and as a result, unlike other commodities, there are a lot less uranium companies out there now than there were seven years ago.

We have really had a bear market for a while. I mean you had a little move up from 2009-2011 until Fukushima. Ironically enough Fukushima marked the top of the resource space anyway in March 2011. The Uranium spot price chart has been in a decline for years, not three or four like you have seen in the other metals. We have seen oil pull off but uranium has really been getting beat up for a long period of time.

I looked at that and I looked at the average global cost of production out there. You are talking $50-$60 per pound all in cost. Yet you had a spot price that has been trading between call it $30-$40. You are trading at a significant discount to the average global cost of production.

At the time I was initially putting the deal together, uranium stood out as a true contrarian bet and really the entry point to me at the time made a lot of sense. I knew it wasn’t going to turn around overnight but there were opportunities to put a deal together. Bring in the team. First and foremost.. Rick Kurmirski, Tom Drolet… Jim Petit who is the chairman. Bring in the right experienced team and then go and acquire the projects that we could get at pennies on the dollar and continue to build the company.

TH: So Jordan, why should anyone follow Skyharbour now?

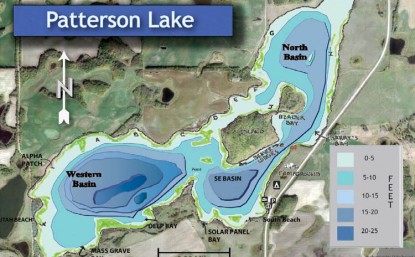

JT: We are trading at a $2.5-$3 million dollar market cap right now. We have assembled one of the largest and most prospective land packages in the basin to date. Historically, if you look at what projects like this are sold for when there are discoveries, (Hathor for example and you look at Patterson Lake South what Alpha ended up selling 50% of the project for. These aren’t 2X or 3X returns these are 20-30X returns. They are multi hundred million dollar deals. That’s a function of them being in the basin with high grade mineralization. You are hunting in elephant country. If you’re doing exploration make sure you are going after something big that is going to be worth something even in a down market like we are in right now.

TH: Any last words?

JT: All in with Skyharbour we are building a vehicle that investors can go to if:

1: They like the uranium space and they see upside there.

2: There are 3 main value drivers, 3 main projects in the company right now. Way Lake, Mann Lake, and the Syndicate project… so we cover different target types.. We have more traditional unconformity style as well as basement hosted targets outside of the basin so we have diversity in the portfolio.

3: They care about the team – we have Rick Kusmirski and Tom Droulet, who is a nuclear engineer and a keynote speaker at a lot of energy conferences – a very knowledgeable guy in the nuclear space and the utility space as well.

I think we have put together the right ingredients for success. There are really two main catalysts: obviously you have a rising tide market that turns around but we have no control over that.

The biggest thing for us is putting the right ingredients in the pot here, to give ourselves and our investors the best opportunity the best shot of getting exposure to a discovery, which creates a lot of value, which generates huge returns for investors.

To find out more about Skyharbour Resources Ltd. (TSX VENTURE:SYH) visit the Company’s website at www.skyharbourltd.com.

This blog post includes certain statements that may be deemed to be “forward-looking statements”. All statements in this release, other than statements of historical facts, that address events or developments that management of the Company expects, are forward-looking statements. Although management believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance, and actual results or developments may differ materially from those in the forward-looking statements. The Company undertakes no obligation to update these forward-looking statements if management’s beliefs, estimates or opinions, or other factors, should change. Factors that could cause actual results to differ materially from those in forward-looking statements, include market prices, exploration and development successes, continued availability of capital and financing, and general economic, market or business conditions. Please see the public filings of the Company at www.sedar.com for further information.

Article written by James Fraser, Mining Analyst (ccd).

Article originally published on January 23rd, 2015.

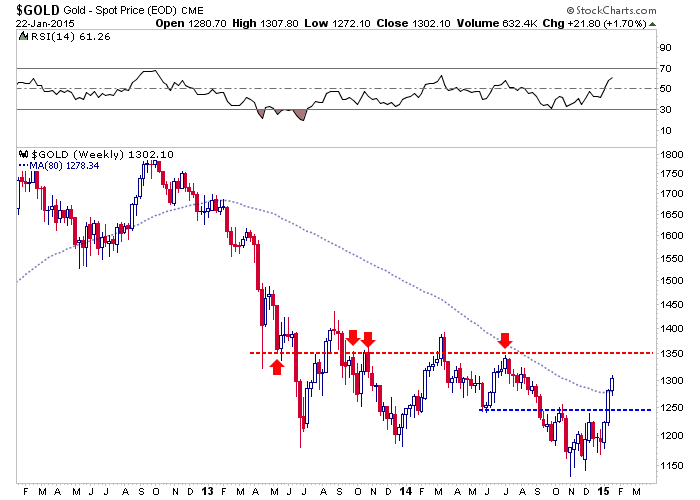

In recent days and weeks we noted key levels for Gold at $1250 as well as $1270-$1280. Over the past two weeks Gold easily cleared $1250 and continued to $1300. Today it is trading around $1290 and will close above its 80-week moving average for the second consecutive week. That last happened in late 2012. Gold continues to show strength and far more bullish than bearish signs.

The weekly candle chart below shows the key levels for Gold which are essentially $1250 and $1350. Gold should have strong support at $1250 while facing resistance at $1330-$1350. A weekly close above $1350 or monthly close above $1330 would signal to the remaining bears that the bear market is over.

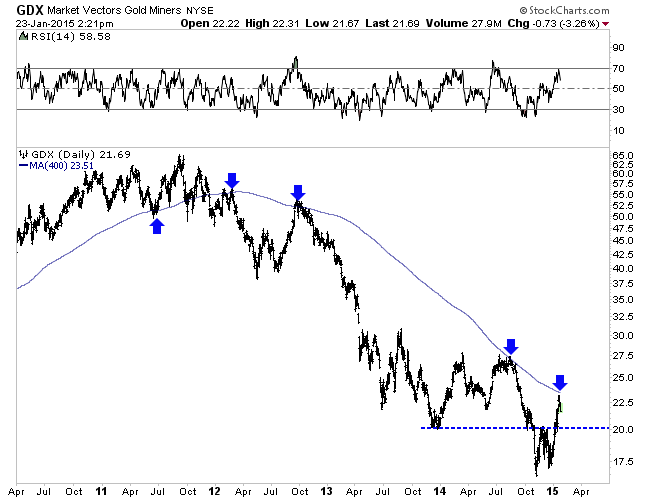

Moving to the stocks, the bellwether for the sector, GDX is backing off after nearly touching its 400-day moving average. We’ve often noted the importance of this particular moving average. The chart shows how the average has marked very important points over the last four years.

Going forward, the key support levels to watch would be $1250 Gold and $20 GDX while the key resistance levels are $1350 Gold and the 400-day moving average ($23.50) for GDX. A dip to or near those support levels would be a buying opportunity.

One catalyst for the next impulsive advance might be a correction in the US Dollar. Precious metals have performed exceedingly well as the greenback has rallied over 7% in the past six weeks and over 12% since October. Yet, public opinion recently touched a record high and the daily sentiment index recently hit 98% bulls. Gold is already trading near the equivalent of $1500/oz against foreign currencies. Any sustained US$ weakness could send metals and miners quite a bit higher. While I believe the bear market is over, I’ll be looking for more confirmation in the weeks and months ahead.

As a young man, Peter Tallman fell in love . . . with rocks. It happened with the help of an unwitting 80 year old mentor named Harold, who was given the job of teaching young Peter how to build a stone fireplace. After struggling unsuccessfully to break the first boulder for the job (an effort that included blood and no small amount of exasperation), Peter was shown by the older stone worker just how to go about making a cut. The seasoned geologist and CEO of Klondike Gold still recalls the story with a chuckle. “Harold didn’t think I was that bright”, he admits.

But with that first simple cut of a boulder, the dye was cast for Peter Tallman’s lifetime relationship with rocks. And beyond seeing the pursuit of geology as a great way to travel the world, Tallman has made a successful career, and a lot of money as a result of his passion for mining and his no – nonsense approach to running a company.

[Editor’s Note: We are not independent of Klondike Gold. We helped recruit Mr. Tallman for the position of Klondike CEO and we own shares in the company. Needless to say, we like the story.]

Tallman has extensive experience, both as a geologist and a businessman. He talks (with a little wonder in his voice) of the time he was hired by Murray Pezim and given the position, “Vice-President of Everything”. Tallman was a key player in the latter part of Pezim’s activities on Howe Street, overseeing some 80 odd companies for the crusty old promoter. When asked what his role was, he explains: “My job was to keep them all straight”. Prodded as to whether he was successful at that, Tallman replies with a twinkle in his eye: “As much as you could be.”

In fact, Tallman learned a great deal working with Pezim. He understood at the time that geology is a young man’s game, and he wanted to learn about the corporate world. “Murray provided me with probably the best education possible on the regulatory framework, and financing, and introduction to the brokerages.” For him, it was a completely different universe.

In the years since, Tallman has had a diverse career in the mineral exploration business both as a consultant and an entrepreneur. He personally invested in a couple of large properties in Newfoundland, which he put into Messina Minerals. “It was an old belt that needed a rethink”, he explains. A couple years into the story a new discovery was made and the company became the talk of Canadian exploration. The stock went from 10 cents to $4.10, before falling back to earth. He also ran exploration programs for a number of companies including Ethos Gold, a once promising Yukon exploration play.

Messina was bought by Canadian Zinc last year, which freed Peter Tallman up for new adventures. That was when we tapped him to take a look at Klondike Gold for his Yukon experience and matter-of-fact approach to business. Happily he saw potential in what he casually describes as ‘a mess’, and since becoming CEO a year ago, he has embarked on a major clean up.

Klondike has a convoluted and even sketchy ownership history. Twice in the past thirty years investors have valued Klondike’s property over $100 million, and today it’s worth less than $5m. I won’t go into the sordid history of deals made and broken, including my own personal loss as an investor, but suffice it to say that despite all of this, Peter Tallman saw an opportunity.

So after a year of cleaning house, which included selling money draining properties in Portugal and in BC, taking over (formally) Klondike Star, so that Klondike now owns 100% of everything that was originally in the company, rolling back the stock, and paying back all the old debts, Klondike is a new company with 100% title to all their assets and a million dollars in the treasury.

But now to the exciting part: exploration. This past summer Tallman had a crew in Dawson looking at the rocks. Despite all this gold having been found in the past, nothing significant was ever discovered. Tallman and his team developed an exploration model and concentrated on Eldorado Creek, where they looked at the bedrock for evidence to see if they might be right. “There are outcrops there that can be seen”, he says, excitedly. “Everywhere we predicted there would be gold, we found it.”

To put Klondike’s exploration potential into perspective, Tallman tells us that before he got involved with the company there were 4 documented occurrences of visible gold in bedrock on the Klondike properties, after 30 years of exploration. Tallman and his team found another 40 in a couple of weeks. He says the initial results are encouraging, so now the hard work remaining is to systematically put the pieces together; figure out where to find tonnage, grade, etc.

What differentiates Klondike from other juniors is grade. Tallman explains that he is not comfortable with the grade model that has majors exploring for big deposits with low grade characteristics. His target for Klondike is super high grade quartz veins. He believes Klondike’s veins have great potential grade. “Idiotically high grade potential” is how he terms it, making for easy economics.

Exploration for Klondike in 2015 will involve more of the same. They will continue to prospect, take a look at all the placer cuts, map them, and they will also begin geophysics to determine where the structures are. Tallman is also committed to continuing to build co-operation and trust with the local placer mining community. So far, he is encouraged.

The CEO is not guaranteeing any drilling this year, as he says there’s nothing that drains the treasury faster that a wasted drill hole. One gets the distinct impression that Peter Tallman wants to be sure he’s done all he can to ensure that investors’ money is well spent.

As for his TV gig, ‘Gold Rush’ has been a bit of a ‘gold mine’ for Tallman, or Klondike, more to the point. Although he frowns at being cast as the big bad claim owner, the involvement of Discovery Channel brings money into the company, and the exposure is already showing a return.

To this wary investor, Klondike Gold looks like a whole new company with Peter Tallman at the helm. He’s believes there’s a lot of potential, he’s determined they’re going to find gold, and they’re going to have a ton of fun in the process. We’re definitely along for the ride.

This article contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws. This information and statements address future activities, events, plans, developments and projections. All statements, other than statements of historical fact, constitute forward-looking statements or forward looking information. Such forward-looking information and statements are frequently identified by words such as “may,” “will,” “should,” “anticipate,” “plan,” “expect,” “believe,” “estimate,” “intend” and similar terminology, and reflect assumptions, estimates, opinions and analysis made by management of Klondike in light of its experience, current conditions, expectations of future developments and other factors which it believes to be reasonable and relevant. Forward-looking information and statements involve known and unknown risks and uncertainties that may cause Klondike’s actual results, performance and achievements to differ materially from those expressed or implied by the forward-looking information and statements and accordingly, undue reliance should not be placed thereon. Risks and uncertainties that may cause actual results to vary include but are not limited to the availability of financing; fluctuations in commodity prices; changes to and compliance with applicable laws and regulations, including environmental laws and obtaining requisite permits; political, economic and other risks; as well as other risks and uncertainties which are more fully described in our annual and quarterly Management’s Discussion and Analysis and in other filings made by us with Canadian securities regulatory authorities and available at www.sedar.com. Klondike disclaims any obligation to update or revise any forward-looking information or statements except as may be required.

The following interview was conducted on January 15-16 by phone and by email. Falco Resources’ SVP of Business Development, Dean Linden was very accommodating making time for me in his busy schedule.

Please describe Falco Resources to readers unfamiliar to the story.

– Falco Resources (FPC.V) / (FPRGF) is one of Quebec’s largest mining claim holders with over 750km of the former Noranda mining camp, including 14 former producing mines. The camp has historic gold production of 19M oz of gold and is the last Abitibi gold camp which is not controlled by a major gold producer. We have made a discovery of sorts at the Horne Complex with a maiden 43-101 inferred resource from historical data containing 2.8 million gold equivalent ounces.

Can you describe some of the key players on Falco’s team?

– The profile of our board and management teams is unlike most junior mining companies, as it is made up of people who have built and operated some of the most successful mines in the Abitibi, including Agnico-Eagle, (AEM), AuRico Gold (AUQ) and Osisko Gold Royalties (OR.TO). It’s a real tribute to the quality of Falco’s asset base that it has been able to attract this type of relevant and extensive experience.

Please tell us about Falco’s capital structure and key shareholders.

– We have a very strong balance sheet with about C$ 12 million in cash and no debt. Osisko is our largest shareholder at almost 12%. We have 93 million shares outstanding.

You essentially inherited a maiden 43-101 Inferred resource of 2.8 million gold equivalent ounces, will that resource grow in 2015?

– We had to do the compilation and analysis ourselves to come up with this resource estimate but we did indeed inherit an incredibly complete database of almost 4,400 historic drill holes. We were able to exploit a remarkable library of Noranda’s historical data spanning 50 years to essentially rediscover a gold-rich deposit. In 2015, we intend to increase the size of the resource by at least 30% and upgrade the resource to the measured & indicated categories.

Please describe the Horne 5 project in more detail.

– From the 1930s to the 1960s, Noranda embarked on a very ambitious drill program in the Horne 5 Zone. Horne 5 sits immediately below the Horne Mine but it was a lower grade ore body and mining techniques of the period did not yet allow for large scale bulk mining of this type of ore body. In addition, the gold price was fixed at only $35 per oz, so the Horne 5 zone was not economic at that time. When we went into the Noranda archives we digitized almost 4,400 drill holes that had been spaced every 15 meters throughout the orebody. This level of drill density is very uncommon and it gave us great deal of confidence in this resource. We still see lots of opportunity to take it from its current 2.8 million ounces to close to 4 million ounces in 2015.

You’ve said that LaRonde is a good analog to Horne 5, please explain.

– LaRonde is one of three modern bulk underground mines that Horne 5 could be modeled after. LaRonde is Agnico Eagle’s flagship mine and is located 80 kilometres to the east of us. Paul Henry Girard, who is a member of our board, was the VP of Canadian Operations for Agnico and was involved with the construction and operation of Laronde. When he joined Falco, Mr Girard saw an uncanny resemblance between Laronde and Horne 5. Since then, however, we have come to see similarities with another Agnico operation, the Goldex mine, as well as AuRico’s Young-Davidson mine – both in the Abitibi. LaRonde is a much deeper mine with a higher cost structure than we envision for Horne 5, so we need to inspire our stakeholders from the best features at each of these 3 world-class operations in conceiving Horne 5. Large stopes, paste backfill, automated ore handling and a large tonnage shaft system are some the features that come to mind.

Falco’s controlled property is quite large, are there opportunities to monetize some of your land portfolio?

While we are moving very aggressively in the exploration of Horne 5, it represents just a small piece of our land position. There are a number of other highly prospective areas of the camp and we cannot cover them all with our limited resources. There is a great deal of interest in this area of the world from a mining perspective. Falco is one of the largest landholder in the area and I do see opportunities to option and JV some properties in the camp. Our cost to maintain the camp is very manageable though, so we can be patient and do deals that make sense for Falco shareholders.

How important to the overall economics of your project(s) is the copper, zinc and silver?

– The grade of the resource currently stands at 3.4g/ton gold equivalent. Actual gold content represents more than 75% of the value of the current resource estimate, so the by-product metals are important but this is clearly a gold mine. Silver was not included in the initial resource estimate and we expect to address this in 2015 with a confirmation drill program. If all goes as planned, we anticipate up to 15 g/t silver content but this will not materially change the gold weighting once this is converted in a gold equivalent grade.

How important is the 80 years of historical Noranda drilling data?

– The importance of the Noranda database is difficult to articulate. The short answer is that Falco could not have come up with a resource estimate on a $500,000 budget without it. The database was solely responsible for the Horne 5 discovery and not one drill hole was required. The work was done and the data maintained by Noranda, a world-class mining company. The data was meticulously maintained with no detail overlooked. As a result, our ‘discovery’ cost is less that 0.25/oz of gold. This compares to a global average discovery cost of $40/oz worldwide and $24/oz in Canada. Falco is probably the most efficient exploration company in the world.

Given that Falco’s property includes 14 formerly producing mines, hasn’t the low hanging fruit already been picked?

– That is a very important question. Noranda was a copper producer, and they built a large copper smelting complex in Rouyn-Noranda in the 1920s. The mandate of the Company was to feed copper to the smelter. Gold was not important and was only produced as a byproduct of copper production. Despite never being a focus the camp produced 19 million ounces of gold (along with almost 3 billion pounds of copper) making it amongst the most prolific gold camps in the Abitibi. During the 50-year operating life of the Horne mine, from 1927-1976, gold averaged less than US$45/oz, or less than US$300/oz on an inflation-adjusted basis. Needless to say, with current economics the narrative of the camp has changed dramatically and opportunity abounds in this camp.

Is Falco funded for 2015? How much drilling will you do?

– We currently have C$ 12 million the treasury. We will spend about $3.4 million on our Horne 5 drilling program, an additional sum on engineering and other studies and about $2 million on regional exploration in 2015. This part of Quebec is home to some of the finest drillers anywhere in the World. We certainly benefit by these Companies wanting to work close to home and the competitive market for services as our many of our peers have reduced their activities.

Falco’s corporate presentation says that Falco controls the last of the large Abitibi Greenstone Belt mining camps, please explain.

– The vast majority of the Abitibi Greenstone Belt is controlled by major gold producers like Goldcorp (GG), Agnico, Yamana (AUY), Hecla (HL) and AuRico, with the exception of this camp

How is Falco Resources different from the number of mid-tier and majors surrounding you?

– Falco is unlike any exploration company in the world. Firstly, we control an entire mining camp. It is extremely rare that a junior is able to acquire consolidated mining claims in a place as prolific as the Abitibi Greenstone Belt. Secondly, the value of the Noranda data library is hard to quantify. Falco bought the data in an analog form meaning it was in paper form and kept in file cabnets. Our efforts to digitize this data on just the first of 14 former producers resulted in the discovery of a 2.8 million gold equivalent ounces. This database was controlled and maintained by the same company for 80 years. It is not something that we will likely see again. Thirdly, our enterprise value per gold equivalent ounce is about $13, which is a very compelling entry point relative to a number of our peers.

Are there any misconceptions about Falco Resources that you would like to address?

– Generally speaking I think that we are living in skeptical times in the junior mining space. The burden of proof weighs heavily on juniors and we readily accept this burden. The first issue we have to address is the tendency to paint everyone with the same brush such that a misstep by a peer reflects badly on the entire industry. Management teams build companies and I am very proud of the team that we have. The second issue is that the average grade of gold deposits has been on a steady decline and some investors will not look at deposits with grades below 5-6 g/t. This ignores mining methods, metallurgy, infrastructure needs and a plethora of other variables. Our 3.4 g/t gold equivalent deposit is of a higher grade than two of the three world-class mines that we are benchmarking ourselves to. I am confident that we will convert non-believers over time. We have a good following already and our job is to add to that – one investor at a time.

Silver looks to be on the verge of a major new upleg, finally emerging from the past couple years’ ugly sentiment wasteland. This beleaguered precious metal recently bottomed as futures speculators threw in the towel on their extreme shorting. And while investors’ ongoing silver stealth buying continues, it’s been modest. So there is vast room for capital inflows to accelerate dramatically as gold mean reverts higher.

Silver has always had a special allure for hardened contrarian investors. Its price action is exceptionally volatile, with massive rallies erupting from time to time that multiply capital deployed in it. With silver’s relatively-small market size, it doesn’t take a lot of new investment buying to catapult prices higher. And shifting sentiment, a powerful self-feeding motivator, fuels the big swings in capital flows that really move silver.

When investors wax bullish on this white metal, its price soars with a fury few other investments can match. Later when silver falls out of favor again, prices collapse. And that’s the miserable story of the past couple years. Silver dropped 19.7% in 2014 after plunging a brutal 35.6% in 2013. Such dismal performance naturally left silver universally despised, the pariah of the investment world. But that is changing.

Silver is ready to run again, a very exciting prospect given the huge uplegs it is renowned for. Silver’s fundamentals are quite unique. Though it is primarily an industrial metal with steady global supply and demand, investment capital can slosh in and out in a big way. The bullish sentiment that’s necessary to trigger big silver demand spikes comes from one thing, gold prices. Gold dominates silver psychology.

When gold is weak like during recent years, investors shun silver so its price crumbles and languishes. But when gold strengthens, investors flood back into the white metal. Silver leverages and amplifies gold’s gains, making it one of the best investments when gold is returning to favor. And gold’s long-overdue mean-reversion rebound upleg out of recent years’ crazy anomalous lows is now underway.

While ultimately gold drives silver through that sentiment link, the daily capital flows responsible for most of the white metal’s price action largely come through two major conduits. Stock investors add or shed silver exposure by buying or selling shares in the iShares Silver Trust, the flagship silver ETF that trades as SLV. And silver futures are the epicenter of speculation, where traders make big leveraged bets.

Both the levels of SLV’s physical-silver-bullion holdings and American speculators’ aggregate long and short contracts in silver futures reveal silver is almost certainly embarking on a major new upleg. Each of these critical capital pipelines into silver shows great room for more investor and speculator buying. And that will come as gold continues recovering on balance, unwinding its extreme anomaly of recent years.

Since the pools of stock-market capital are so vast, let’s start with SLV. This ETF’s mission is to track the price of silver so stock investors can gain diversifying exposure in their portfolios. Since the supply and demand for SLV shares almost never exactly matches that of underlying silver, differential buying and selling of ETF shares develops. If not addressed, it would soon force SLV to decouple from silver and fail.

In order to keep SLV share prices closely mirroring the silver price, this ETF’s custodians have to quickly equalize any excess share supply and demand into silver bullion itself. When stock investors buy SLV shares faster than silver is being bought, SLV threatens to decouple to the upside. So its custodians issue new shares, adding supply to satisfy this excess demand. The cash raised is used to buy silver bullion.

Conversely when SLV shares are being sold faster than silver, it will soon fail to the downside. The only way to prevent this is to equalize the excess SLV-share supply into silver itself. SLV’s custodians do this by buying back excess SLV shares, with these purchases funded by selling some of the silver bullion held in trust for SLV shareholders. Thus SLV holdings levels are a key barometer of silver demand.

And they now reveal low stock-investor exposure to silver prices, which is very bullish since that leaves lots of room for new buying as gold continues recovering. This first chart shows SLV’s physical-silver-bullion holdings in red, with SLV prices superimposed on top in blue. As stock investors see gold and therefore silver starting to move decisively higher, they are likely to buy tens of millions of ounces in short order.

Silver’s last mini-mania peaked in April 2011, above $48 per ounce. For most of the time since, silver has been grinding lower on balance. As of early November 2014 in SLV terms, silver had fallen a brutal 69.7% over 3.5 years. That powerful bear market left silver universally loathed, deeply out of favor with investors and speculators. Most assumed that vexing downward spiral would persist indefinitely.

But considering how rotten and epically bearish silver sentiment has been, the trend in SLV’s holdings has been rather amazing. Since way back in May 2012, years before silver would finally bottom, the bullion that SLV holds in trust for its shareholders has risen on balance. That means stock investors were buying SLV shares faster than silver was being bought, or selling them slower than it was being sold.

This contrary uptrend has witnessed dazzling episodes of strong differential buying, most notably in early 2013, mid-2013, and late 2014. Unfortunately silver prices didn’t respond super-favorably to any of these since American futures speculators were dumping vast amounts of silver contracts at the same times. But if these speculators had merely been neutral on silver, its price would have soared on SLV buying.

But after SLV’s holdings hit a relatively-high 350.2m ounces as December 2014 dawned, this ETF was slammed by heavy year-end differential selling pressure. That month alone its holdings fell 5.3%, and were down 6.8% total by last week. That represents massive silver selling pressure of 23.8m ounces. And the reason for this is easy to understand. Silver had really underperformed, and institutions dominate SLV.

Pension funds, mutual funds, and hedge funds are the largest SLV shareholders by far. They always want to show winners on their trading books as years end, when many investors make decisions about which funds to allocate capital to. So there is lots of so-called window dressing in December, funds buying high-performing stocks while selling laggards. With SLV down 19.5% last year, it was sure the latter.

In addition, in early November silver had just slumped to a deep new 4.7-year low on extreme futures shorting. Bearishness was off-the-charts epic, with virtually everyone convinced silver was doomed to spiral lower indefinitely. So I suspect plenty of fund managers capitulated after that, saying the heck with silver. Their exit certainly contributed to the major differential selling pressure SLV suffered last month.

But actually lower SLV holdings are bullish. They imply stock investors are way underexposed to silver, and leave lots of room for capital to migrate back in. With gold recovering, the odds are very high that stock investors will soon return to SLV in a serious way. The resulting differential buying pressure on SLV shares should easily blast this ETF’s holdings back up near their multi-year resistance near 352m ounces.

That would require 25.6m ounces of stock-investor silver buying in short order, a big number. To put this in perspective, the venerable Silver Institute reported total global silver investment demand in 2013 of 256.0m ounces. That equates to 21.3m per month. SLV’s holdings are poised to quickly surge by at least 25m, likely in a matter of weeks. This is big marginal investment demand in such a short period of time!

And that projection is far too conservative. Note above that SLV’s holdings surged up to or over their uptrend’s resistance when silver prices were quite weak. Imagine how much more intense the stock-investor silver buying through SLV will be if silver is actually surging. I fully expect that this year SLV’s holdings will easily surpass their all-time record high of 366.2m ounces achieved back in April 2011.

That would require enough differential buying of SLV shares to force its holdings 39.8m ounces higher, a massive boost in investment demand. And even at that old record, the amount of capital parked in SLV would still be small. Since silver prices were so high that last time silver was really in favor, SLV’s silver bullion held in trust for its shareholders was worth $17.2b. But silver is priced far lower these days.

So the same record SLV holdings levels would be worth merely $6.2b today, just over a third as much. And capital measured in single-digit billions is a trivial drop in the bucket for the stock markets. It will only take a tiny fraction of stock investors parking some diversifying capital in SLV to blast its holdings dramatically higher. And all the resulting ETF underlying physical bullion buying will accelerate silver’s upleg.

In the investing world, nothing begets demand like higher prices. Investors don’t want to own anything until it is already rallying, and the longer and higher it climbs the more they buy. So uplegs in silver, and anything really, tend to be self-feeding. Buying drives prices higher, which entices in still more buyers, which lifts prices even higher, and the cycle grows. So silver investing via SLV has vast upside potential.

But in recent years stock-investor capital alone has proved insufficient to ignite a major silver rally. And that is where silver’s dominant day-to-day price driver comes in, the silver futures trading by American speculators. With investors largely missing in action still after silver’s excessively-weak past couple years, futures speculators’ trading is silver’s primary driver. This critical relationship is crystal-clear in this next chart.

It shows American speculators’ total long and short contracts in silver futures on a weekly basis as reported by the CFTC in its famous Commitments of Traders reports. The green line is the total long contracts speculators hold, bullish bets on silver prices. And the red line is their total shorts, the bearish bets. The yellow line shows both series’ deviation from normal years’ averages, while SLV is rendered in blue again.

Silver’s extreme 4.7-year lows back in early November were solely the result of extreme selling by those American futures speculators. They effectively capitulated, convincing themselves the universal hyper-bearish outlook for silver was righteous. So they aggressively shed long contracts while spectacularly ramping shorts, subjecting silver to withering selling pressure. It’s impressive silver didn’t crater much lower.

Back in July after gold surged on the Fed’s Janet Yellen claiming there was no inflation, speculators’ leveraged long-side bets on silver hit a 3.7-year high of 90.3k contracts. But as bearishness set in again thanks to heavy gold-futures shorting, their longs collapsed by 20.5% or 18.5k contracts by early December. With each contract controlling 5000 ounces of silver, that was a lot of selling for the markets to absorb.

We are talking about a staggering 92.6m ounces slamming the markets in less than 5 months! It’s no wonder silver slumped to major new lows under such a massive onslaught. But it gets even worse, as the new shorting by speculators was far more extreme than their long liquidation. Between late July and early November, speculators’ total shorts skyrocketed an astounding 166.2% or 43.7k contracts!

Now in the futures markets, the price impact of an existing long contract being sold or a new short one being added is identical. So speculators shorting 43.7k new contracts deluged the markets with a truly mind-boggling 218.5m ounces of silver in just over 3 months! That is the equivalent to over 5/6ths of 2013’s total global investment demand. Silver’s resiliency despite that epic selling was actually amazing.

Silver’s secular bull was born back in November 2001 at just $4 an ounce, and our weekly CoT data on futures speculators’ positions extends back farther to January 1999. Speculators’ bearish bets on silver in early November of 70.0k contracts was the highest ever seen since at least then. I suspect it was an all-time record high! Speculators had likely never been more bearish, never more leveraged against silver.

But since silver’s swoon was relatively mild compared to that mammoth futures selling, there had to be great latent investor demand out there absorbing that torrent of supply. The fact that investors were quietly buying when everyone was convinced silver was doomed is super-bullish. Their ranks and capital inflows will swell dramatically as gold continues mean reverting back up to far-higher normal levels.

And speculator futures buying is going to fuel the early gains before investors fully take the baton in silver’s next mighty upleg. Since silver futures are so highly leveraged, selling them short is an exceedingly-risky bet. Today the CME Group only requires margin of $6500 on deposit for each silver-futures contract speculators hold. But at $17 silver, a 5000-ounce contract is worth $85,000. That’s leverage of 13.1x!

Stock speculators have been legally limited to 2-to-1 leverage since 1974, 13 to 1 is crazy. Speculators who run minimum margin will lose 100% of their capital risked if silver merely moves 7.6% against their bet. And silver’s super-volatile history shows it doesn’t take long, a day or two, for such big swings to erupt. This risk is particularly acute for the speculators short silver, since they legally have to buy to cover.

Shorting requires speculators to effectively borrow silver before they sell it, with the hope of buying it back later at lower prices to repay their debts. The only way to settle those debts is to close their short contracts by buying offsetting longs. This buying is compulsory as silver rallies and erodes their capital risked, so they quickly buy to cover. And as you can see, the short covering has already been fast and furious.

But it’s not over yet! In the latest CoT week, speculators were still short 35.9k contracts. This remained well above their average short levels of 21.5k in the normal years between 2009 to 2012. So merely to mean revert to those norms, not even overshoot in the other direction which is always the case after extremes, they still have to buy to cover another 14.4k contracts. That equates to another 72.1m ounces of buying!

Meanwhile the long-side speculators will get more bullish and bold as silver rebounds, partially on short covering. They will ramp up their bets again, inevitably pushing their total contracts back up near long-side uptrend resistance around 93k contracts. That would require 17.5k contracts of buying, or another 87.4m ounces. And don’t forget the 39.8m or so likely coming from stock traders through SLV very soon.

Add speculator short covering, long contracts rebounding, and stock-investor SLV buying, and silver is looking at potential near-term buying over the coming few months of a staggering 199.3m ounces! That is the equivalent of nearly 4/5ths of the entire silver investment demand for all of 2013. The potential silver upleg that much buying in a relatively short period of time would fuel is massive. Silver is truly ready to run.

And really that’s just the start. Traditional silver investing doesn’t come through silver futures or ETFs, but through physical bars and coins. And once the futures buying and ETF buying pushes silver high enough for long enough to convince investors this new upleg is the real deal, traditional physical demand will soar and take the baton. Futures and ETF buying really just jump starts the even-larger main show.

With silver’s prospects out of its recent extreme lows looking so incredibly bullish, all investors need to get silver exposure in their portfolios. Physical silver bars and coins, and even SLV, are fine ways to do it. But their upside is limited to silver’s gains, they can’t leverage it. Meanwhile the best of the silver miners’ and explorers’ stocks will amplify silver’s upleg by multiples, potentially earning fortunes for investors.

The bottom line is silver is ready to run higher in a major new upleg. Silver is ultimately driven by gold’s fortunes, so as gold continues mean reverting higher silver is going to catch a massive bid. This buying will initially come from American stock traders and futures speculators. They will aggressively buy SLV shares faster than silver is being bought, cover still-large silver-futures shorts, and add new silver-futures longs.

This major buying, likely to approach a couple-hundred million ounces in a matter of months, will serve to launch silver higher. And nothing attracts investors like rallying prices, so global investment demand will ramp dramatically. Investors are so underexposed to silver after leaving it for dead in recent years that they will need enormous buying to attain any reasonable silver exposure. Silver will soar on these inflows.

My friend Peter Tallman is president CEO of Klondike Gold Corp (TSXV:KG), a company that today holds the key claims in the heart of the 1898 Klondike Gold Rush region near Dawson City, Yukon, where some 20 million ounces of placer gold was recovered at surface, with the hard rock source of the gold never found.

The property has been called the greatest gold anomaly on the planet after the Witwatersrand.

Klondike was promoted aggressively during the 20th century. Twice in the last 30 years it had a greater than $100 million market capitalization, while today’s it’s just under $5 million.

The problem, frankly, is that some of its managers squandered many millions of investor dollars on non-core academic studies, stock promotion and related party transactions, lining their own pockets with the promise of a new gold rush, without ever coming up with substantial exploration results (these are my personal opinions, and do not reflect the views of the company). Klondike Gold Corp had become somewhat of a joke in Dawson City, Yukon for this reason.

Decades of bad history in the Klondike came to an end last year with the appointment of Peter Tallman to the President and CEO position of the company.

Tallman was formerly “Vice President of Everything” for Murray Pezim, one of Canada’s best-known and most colourful mining promoters. Tallman has multiple discoveries to his credit and significant experience in the Yukon.

In his first year on the Klondike Gold job, Tallman settled all of the company’s debts, disposed of its non-core assets, consolidated 100% ownership of the key claims for the first time in many years, rolled back the stock and finally Klondike Gold has some money in the bank (approx $1 million today).

The company has the most unique promotional plan I have ever seen for a junior explorer. Discovery Channel’s Gold Rush program has optioned one of Klondike Gold’s properties, giving it at least the cash equivalent of 100 ounces of gold in 2014, which is likely to be increased this year and the next. Klondike Gold and CEO Peter Tallman also get free exposure to approximately 4 million viewers of that television series per week, not to mention the online exposure.

While 2014 was a year of corporate cleanup, the company did manage to generate some positive field results. A news release out this morning says that during summer 2014, Klondike Gold found a fault system not previously imagined. Prospecting around it located veins with assay grades up to kilograms per tonne gold (1766 g/t Au is 51.5 oz/ton Au). These are uber high grades.

Read: Klondike Gold Reports Lone Star Property Rock Sample Assays

CEO Peter Tallman is not promising a drill program this summer at Klondike, however the field work will continue and he tells me that he’s very excited for the 2015 exploration season there.

Tallman oversaw a massive gold exploration program for Ethos Gold a couple of years ago not far from the Klondike area. The work was hailed as a methodical exploration program at scale. Ethos walked away when results weren’t encouraging enough.

Klondike Gold has another thing going for it. Successful mining financier Frank Giustra, who founded countless successful natural resources ventures, owns just under 20% of the company. Giustra also founded Lionsgate Films and his entertainment connections helped Klondike land its television joint venture. The Klondike property is something of a curiosity for Giustra. He thinks it’s a long shot, but he’s had success in a similar setting twenty years ago. In the early 1990s, Giustra backed Robert Friedland’s Fairbanks Gold which brought a new exploration approach to the Fairbanks Gold Rush region of Alaska. A deposit was quickly proven up, sold for US $152 million, and today is operated by Kinross.

We recently taped an interview with Klondike Gold CEO Peter Tallman which will be live on CEO.ca shortly.

Please note we are not independent in our coverage of Klondike Gold. We helped to find Mr. Tallman for the job (thank you Fred Leigh). Klondike Gold is a CEO.ca a sponsor and author holds a share position.

With that said I am very proud to have this conflict of interest with Klondike Gold Corp.

Now if they can just find the hard-rock source of the Klondike, Discovery Channel and CEO.ca will be watching.

Read Klondike’s latest news release: Klondike Gold Reports Lone Star Property Rock Sample Assays

In a lead up to the shareholder proxy vote later this month, the conflict between Meson Capital Partners, as lead by Ryan Morris, and Aberdeen International Inc. (AAB.TO) continued this week as the two parties issued releases reiterating their respective arguments.

As a recap, Ryan Morris’ Meson Capital Partners LLC, a San Francisco-based activist investment firm working in concert with Nightscape Capital (UK) LLP, recently forced Aberdeen International, a prominent Canadian resource investment firm, into a shareholder proxy vote on Aberdeen’s current board leadership. Meson Capital Partners and Nightscape Capital own a combined total of approximately 9% of Aberdeen shares.

Ryan Morris’ criticism of Aberdeen centres on the company’s “abysmal” performance and what Morris considers excessive leadership compensation. In November last year, Morris’ takeover attempt of Aberdeen’s board began when he publicly protested a private placement transaction executed by the company.

In the shareholder proxy vote ending on January 30th, 2015, Aberdeen’s shareholders will have the opportunity to vote whether they would like new board leadership, as represented by Ryan Morris himself and his list of nominees, or whether they would like Aberdeen’s leadership to remain as is.

As Ryan Morris explains in his January 12th press release, he not only opposes Aberdeen’s November private placement transaction, but plans on completing court proceedings in relation to the transaction.

Spelling out his leadership plan in further detail, Morris goes on to promise “… to maximize the value of Aberdeen for all shareholders which includes a commitment to an immediate capital return of at least $0.15 per Aberdeen share.”

How Ryan Morris intends to return this kind of capital to Aberdeen shareholders in a financially sound way is a big question.

This is an important to question to ask, especially considering that Morris is only thirty years old and has limited investment experience. Moreover, the performance of his Morris Capital Fund since 2010 has been consistently lacking, particularly when compared to the S&P 500. In fact, one year in the past, the Morris Capital Fund underperformed the S&P by as much as -41.4%.

As Morris explains, he and his nominees intend to immediately monetize Aberdeen’s stake in Rio Alto Mining, which, according to Morris, is a “non-core asset”. Following this, Morris and his nominees intend to return the net proceeds of this sale to company shareholders, which will form a major part of Morris’ promised $0.15 capital return. One issue with this is that selling 4.7 million shares of Rio Alto will not be possible without seriously driving down the share price and therefore the yield of this sale will be much lower than he anticipates.

Laying out a plan like this and highlighting the returned value to Aberdeen shareholders might gain favor with some retail investors. However, whether Morris and his nominees can in fact monetize Aberdeen’s Rio Alto Mining assets without negatively affecting value is an entirely different story. Unfortunately, Morris’ press release does little to offer details as to how he will accomplish this.

Following Ryan Morris’ press release, on January 14th Aberdeen leadership published a letter highlighting the potential destructive consequences of Ryan Morris’ bid for Aberdeen leadership.

Detailing a plan for long-term value creation, Aberdeen’s letter spells out a number of points damaging to Morris’ takeover attempts and calls Ryan Morris a short-term investor who simply wants to make short-term profit on Aberdeen by liquidating as much of the company as he can.

Aberdeen’s letter comments that shareholders will be responsible for the costs of the proxy battle, a fact that will greatly diminish Morris’ ability to return $0.15 per Aberdeen share to company shareholders.

Also hurting Morris’ ability to return $0.15 a share will be the fact that change of control fees will be imposed on Aberdeen if Morris and his nominees do win control of the company.

These fees are not something to be ignored. They will cost Aberdeen and its shareholders approximately $8 million and cancelling them will not be an option, despite whatever Morris may claim. Of course if Aberdeen’s current management remains on the board, change of control fees will not be applied and this charge will not diminish the share price.

All of this puts Ryan Morris’ campaign in an immediate and definite disadvantage.

Another significant detail standing in the way of Morris’ proposal is the fact that Aberdeen’s company’s by-laws require that the majority of Aberdeen directors be Canadian residents. Unfortunately for Ryan Morris, most of his nominees, including himself, are U.S. residents, making it very questionable whether Morris and his new leadership could even convene in a board meeting if voted in.

There is little doubt that company leadership plays a significant role in the performance of company stock and, in turn, how much profit is returned to company shareholders.

Unfortunately, a change in leadership through the kind of takeover attempt Ryan Morris is pursuing is no guarantee that Aberdeen’s performance will strengthen. Nor does it mean that Morris and his new leadership will be able to execute the strategies he’s been so vocal about it.

In fact, if you look at notable activist investors and notable company takeovers in the past, including Morris’, many have ended in failure, with company value eroding instead of being created or strengthened.

This is an uncertainty that investors in Aberdeen International need to soberly consider.

The fact that Aberdeen International’s current board has a plan of action that’s more realistically attainable should also be considered.

Shareholders should note that Aberdeen’s current leadership have begun implementing company changes, most recently by inviting the experienced mining minds of John Begeman and Bernie Wilson to Aberdeen’s board. Shareholders should also note that the changes Aberdeen’s current leadership is proposing are far more realistic than anything Ryan Morris has offered so far.

In the next several weeks, Morris may pull more promises out of his hat, but whether he and his nominees can actually strengthen Aberdeen’s stock performance if they are voted in remains very questionable.

The following article of the CEO of Terraco Gold’s Todd Hilditch was conducted by phone and email on January 8-9.

Please describe Terraco Gold to investors who don’t know your story.

Terraco Gold (TCEGF) is a gold focused company with assets in the western U.S. that gives investors and shareholders exposure to gold equity ownership through gold royalties and gold in the ground.

Please describe Terraco’s capital structure, including cash and debt.

Terraco has 134 million shares issued and outstanding and 146 million shares fully diluted. The company has no traditional debt but does have an option to consolidate a royalty position of up to 3% on Barrick Gold’s (ABX) Spring Valley project for approximately USD$16 million which equates to buying gold at $184/ounce. The options expire at the end of 2016. The company has current assets of approximately $500k including cash. The issued and outstanding shares have not changed, as a result of financing, in 5 years based on creative cash infusions with royalty transactions.

Who are Terraco’s largest shareholders? How much equity is owned by the management team and Board?

Terraco is largely held by retail shareholders, which has been one of its strengths in a very tough junior market. Insiders own 9% collectively with the CEO, Todd Hilditch owning near 5% of the 9%.

Has there been any insider buying lately?

From January 1, 2014, until January 6th, 2015, Terraco insiders bought 1,020,000 shares including the CEO buying 775,000 shares. Non-Insiders and strong shareholders continue to add to their positions.

What is Terraco’s quarterly cash burn rate?

The current quarterly burn rate is approximately $100,000.

Terraco’s most valuable asset is its (up to) 3% Net Smelter Royalty “NSR” option on the Barrick/Midway Gold (MDW) Spring Valley project in Nevada. Please describe that particular asset.

Terraco negotiated the purchase (from royalty owners) and financing (from large private equity firms) of over $30 million in gold royalty assets on Barrick Gold’s Spring Valley project, where Barrick has now spent over $70m to take the project to pre-feasibility. As part of the multiple transactions Terraco negotiated, it also financed itself without issuing a single share of dilution to shareholders of over $6m in order to advance its Idaho Project and general working capital.

The resulting asset to Terraco is direct royalty ownership and royalty options to acquire up to 50% of the acquired Spring Valley NSR royalty (up 6%) for a net benefit to Terraco of up to 3% NSR. Terraco’s option exercise price (free debt in other words) is roughly $16m which equates to less than $184/ounce gold as a price to Terraco. The best way to see how the NSR royalty covers Spring Valley is to go to Terraco’s website and view the Spring Valley presentation on the home page.

Is there a way to roughly and conservatively estimate the value of the (up to) 3% NSR options based on a given gold price and the current number of measured & indicated ounces at Spring Valley?

There is a rough way to estimate value but it does require one to rely on certain mining market and typical mining assumptions for this type of deposit. A simple, albeit not bullet proof way, is to take the number of ounces outlined/expected to be mined times expected/typical gold recoveries resulting in a rough number of ounces produced and multiply that figure by the NSR royalty (in Terraco’s case up to 3%) for the attributable ounces to the royalty owner and finally, multiply that by the price of gold you are comfortable using.

Based on certain assumptions and parameters available in the market, some of which is directly provided by Barrick JV partner Midway Gold in their most recent NI43-101 report filed on SEDAR and others from research reports by Canaccord and Cormark, Terraco management feels that based on an assumed 14 yr mine life, assumed 80% recoveries and a $1,250 gold price, that future cash flow from Spring Valley would be between $100-$150 million to Terraco. Of course these assumptions are open to change / substantiation based on Barrick’s mining parameters and also on more gold found, but if you applied a NPV(5%) discount to the above (as a research report did) the valuation for Terraco far exceeds the current market capitalization.

Barrick is clearly interested in expanding in Nevada. Is there evidence that Barrick is more likely to pursue Spring Valley over a number of its other Nevada interests?

Barrick has been highlighting Spring Valley for the last 5 months in its investor presentations (available on their website) to which Spring Valley is profiled as one of their few Nevada based focused PFS projects. In the last year alone Barrick has spent over $17m at Spring Valley and we don’t see them slowing down as Barrick spends more time back in Nevada.

How will you raise the $16.1 million exercise price required to pay to Barrick by 12/22/16?

Our royalty transaction is not with Barrick, it’s with two private equity firms who wrote the large checks, but we have several scenarios that we can employ prior to the option exercise deadline. Keep in mind that our royalty option is a hedge on gold at less than $184 per ounce based on the Barrick resource so funding the required option payments is not expected to be a problem.

We are also are not in a rush as we have time and it is better for us to, “option the car with no payments” versus, “buy it” in today’s market. Our options to fund closer to the end of 2016 could include: an equity raise, a debt instrument, a combination of equity/debt or selling a portion of the currently held royalty to fund the option exercise. In the meantime, we have an interest free debt/option at the equivalent of $184 per ounce of gold….which we think is pretty valuable.

Can Barrick meaningfully slow its development work at Spring Valley or does it have to hit annual development milestones?

Barrick has earned its interest from Midway of 75% ownership and the project is a flagship PFS Nevada asset with over $70m spent to date so we don’t believe Barrick will slow its development. That said, that is up to the Barrick/Midway Gold joint venture. Terraco is not privy to the joint venture agreement so we cannot comment on whether Midway can require continued spending after the earn-in.

According to your corporate presentation, “Terraco’s royalty portfolio in Spring Valley results in a cost base to Terraco of $283/oz.” Please explain.

At the conclusion of the 3 royalty acquisitions, the aggregate amount of money required by Terraco to exercise all three royalty options by 2016 (again a free debt carry or hedge) multiplied over the number of ounces covered / applicable in that royalty (Spring Valley NI43-101) came to $283…in fact with the new NI43-101 report, with in excess of 5.4 million ounces of gold, the estimated new cost base, once exercised, to Terraco is $184 per ounce.

Can you give readers a description of both Terraco’s VP of Exploration and its consulting geologist?

We are blessed to have two gentlemen with strong geological pedigrees to which both have been discovered or co-discovered several economic gold deposits. Our VP Exploration, Charles Sulfrian, was involved in the original sampling/discovery of the deep post deposit which ultimately formed part of the ore body (Betze -Post) that Barrick operates under its flagship Nevada Goldstrike Mine. Ken Snyder, a consulting geologist to Terraco, discovered for Pierre Lassonde’s Newmont Gold (NEM), the Midas Gold (MDRPF) (Ken Snyder) Mine which was Newmont’s lowest cost producing mine for a period at Newmont.

Terraco’s corporate presentation describes Idaho’s Nutmeg Mountain Gold Project as, “advanced stage.” Please describe this project.

Nutmeg hosts a NI43-101 compliant gold resource near a million ounces. The deposit is open in several directions for resource growth and under better market conditions, Terraco will advance the project into a PEA, to which much of the work has been completed.

Please describe the earlier-stage gold exploration opportunity at your 100% owned Moonlight Project adjoining the Spring Valley Project.

Our Moonlight Project adjoins Barrick’s Spring Valley project to the north and is now sandwiched to the south side of Sumitomo Corporation in a joint venture with Renaissance Gold (RNSGF). Moonlight is on strike geologically with the major fault system (Black Ridge Fault) that structurally controls the two deposits on our south end being Spring Valley and the silver producing Rochester Mine that operates under Coeur Mining (CDE).

The project has blue sky in its 35sq km land package and is amongst numerous major mining companies. Once again, in better market condition, Terraco will spend a significant amount more time and money to test Moonlight for gold and silver. In an earlier drill campaign (2008-2009) Terraco encountered up to 2 ounce silver within a 10 meter intersection (see Terraco’s website), so we know the Moonlight project has mineralization, it is a matter of defining the silver in the north and the gold in the south of the project.

Can you name any companies besides Barrick and Franco-Nevada (FNV) that have the experience and financial wherewithal to acquire Terraco outright?

I think there are many companies that have that ability and can come in many possible forms. Our Spring Valley royalty options are a tremendous asset for any royalty company (Osisko Gold Royalties(OKSKF), Royal Gold (RGLD), considering Barrick is a good operator and has the financial ability to go to production in a great Nevada jurisdiction. In addition, there are other gold mining companies that may find our suite of hybrid type assets intriguing. Other players in the area include Pershing Gold (PGLC) and Rye Patch (RPMGF)

Are there any misconceptions about Terraco that you would like to address?

Not really though a few investors have hinted that it would be better for our valuation and market capitalization to exercise all the remaining NSR options so that we have full ownership today. Although I understand the opinion, I would argue that those investors and shareholders that have long term belief in the royalty would agree with us that it makes more sense in this very difficult, low share price, environment to not leverage ourselves today in ownership when we have the ability and time (free debt/option) to wait until market conditions/share prices improve before taking on equity dilution or debt required by the end of 2016.

The other argument in favor of not exercising is that while we have another 23 months before we need to exercise the remaining royalty options, the Spring Valley project will continue to be de-risked by Barrick which also helps our value proposition by Barrick adding more ounces and moving into pre-feasibility. These items should help our share price. …..thus the ultimate reason to not exercise too early.

The contention between Aberdeen International Inc. (AAB.TO) and Meson Capital Partners LLC, headed by thirty-year-old Ryan Morris, continues, with Aberdeen International raising the firepower on January 1st when it published a strong-toned circular to its shareholders in defense of its current leadership.

Despite the sour conditions the mining and precious metals market have faced over the past year, Aberdeen International, one of the prominent resource investment firms in Canada, has seen stronger returns in 2014, especially compared to Junior Gold Miner ETF averages.

As Aberdeen’s Circular highlights, the company’s stock enjoyed healthy performance in 2014, with the AAB stock having a 27.29% total shareholder return, compared to a return of -22.31% for the Junior Gold Miners ETF (GDXJ). See below comparison table.

As the Circular further highlights, Aberdeen’s stock in 2014 outperformed many of the company’s comparable peers, particularly in the last quarter of the year.

As the Circular further highlights, Aberdeen’s stock in 2014 outperformed many of the company’s comparable peers, particularly in the last quarter of the year.

The contention between Aberdeen International and Meson Capital Partners, a San Francisco-based investment firm with a 4% stake in Aberdeen, began in November last year when Meson Capital’s Ryan Morris, an activist investor with a spotty track record, cried foul after Aberdeen executed a private stock sale.

The contention between Aberdeen International and Meson Capital Partners, a San Francisco-based investment firm with a 4% stake in Aberdeen, began in November last year when Meson Capital’s Ryan Morris, an activist investor with a spotty track record, cried foul after Aberdeen executed a private stock sale.

Following that, Morris, in concert with UK investment firm, Nightscape Capital LLP, waged a proxy battle to replace the seven directors at Aberdeen International with new leadership (new leadership which would include Morris himself).

Aberdeen shareholders now have a chance to participate in a proxy vote to decide whether Aberdeen International’s current leadership should be replaced with Ryan Morris and his nominees.

This proxy vote ends on January 30th, 2015.

Current Aberdeen leadership for its part has been proactive in response to the takeover threat. Not only has the company enhanced its board by appointing several new directors, all who have significant mining experience, Aberdeen has also implemented fresh cost-cutting policies.

New Lead Director of Aberdeen’s board, Bernie Wilson, comes with significant experience in corporate governance and also happens to be the founder of the Institute of Corporate Directors (“ICD”) Corporate Governance College in Canada.