The following interview of Galane Gold’s CEO Nick Brodie took place by phone and email on February 24-25. The opinions expressed are entirely those of Mr. Brodie. I own shares of Galane Gold. Please see applicable discloses at the bottom of this article.

Can you provide readers with an overview of Galane Gold’s operations and prospects?

Galane Gold owns the Mupane Gold Mine which is situated in Botswana. Mupane has produced over 650,000 ozs of gold since mining commenced there in 2005 and it is our view that it has a long future in front of it. Ore is currently sourced from open pits, underground mines and historical low grade stockpiles and is processed through a mill and conventional CIL plant. It has matured into a mine with a forecast all in operating cost of $1,050 per ounce and a rolling 5 year plan.

Every mining company boasts that they have a superb management and/or Board. Can you describe your team?

Galane inherited a mine which had lacked continuity in senior management. We saw it as a critical part of the turn-around of the mine that we built a strong team with specific experience in mining and processing in the Greenstone belt. The first step was to find a new General Manager and we quickly identified Wayne Hatton-Jones as the most suitable fit. He is a mining professional with over 26 years’ experience in Africa, Asia and Europe. Having worked previously at Goldridge, Galaxy Gold, Avocet, Randgold and Harmony with the majority of his experience being in the greenstone belt in South Africa. His background and qualifications are Metallurgical which was critical for us to manage the fact we were transitioning from a predominately oxide ore to a sulphide ore. In addition he had experience in managing the move from an open pit to underground operation. An example of what Wayne has brought is that before Wayne had arrived we were advised that the cost of moving to an underground operation at Tau would cost over $10m with his experienced we actually installed a force portal and the total cost was $500k.

As always in mining Wayne then gave us access to numerous strong individuals that he has worked with historically. In particular we recruited Geoff McLoughlin a metallurgist with 29 years’ experience in operation and plant design. He is currently in charge of implementing the gravity plant circuit which we has designed and will build in house. He also managed the screening plant construction which we acquired second hand for $30k and rebuilt at site and has given us access to over 2mt of previously considered low grade stockpile at a direct operating cost of $600 to $700 per ounce. Another new member of the team is Kevin Crossling who we recruited as the Business Development Manager and he is a geologist with over 16 years of experience especially in the Greenstone environment. His responsibility is identifying new opportunities at our brownfield mine sites as well as oversight of our mining operations. Finally and not to be forgotten we have managed to retain Charles Byron as our exploration geologist. He has been associated with the Greenstone belt in Botswana since 1995 and his experience is invaluable both as a repository of historic information but also as the individual who will assist us in our approach to replace resources and we deplete them.

On the board side I would say our strongest asset is Ravi Sood who has extensive experience and profile in the Canadian market. He is an active Chairman who takes a strong interest in the marketing of the Company and the long term strategy. He has raised over $1bn in capital for various projects and is always looking to see how he can assist with the operation.

February is almost over, are you able to reiterate 2015 production guidance of about 45k ounces of gold at all-in costs of roughly $1,050/oz?

Our latest presentation on our new website, which I recommend you visit, shows guidance of around 45k ozs and a rough all in cost of $1,050 per ounce. It should be noted that in 2015 the first 6 months of the year sees us spending over $6m on capital projects and in particular the completion of development underground and the instillation of the gravity circuit. Therefore production will be low and costs higher than this but it will be corrected in the second half when we start stoping underground and process the Tekwane ore.

The $1,050 all in sustaining cost is based on our current 5 year plan. When running the plan we base it on the current gold price of $1,200 per ounce and we have the advantage that we have various sources of ore. We therefore can base production, pit sizes, cut off grades etc… on what we believe provides the optimum return to shareholders at a particular gold price. We have the ability to reduce the cost, but at lower production levels, if the gold price decreases. For example, we could just process the low grade stockpiles for 2 years at a direct operating cost of between $600-$700 per ounce (current plan $850-$950). We can also increase production as we have excess capacity in the plan at the plant but have decided not to mine certain resources as they are marginal. With a higher gold price this decision would be reviewed. Most small producers are dependent on one source of ore and do not have this flexibility. Therefore, at current production levels if gold price increased by $100 we would not only add $4.5m to the bottom line and cash balance we could also take advantage of increasing production.

Please describe Galane Gold’s capital structure, namely shares outstanding and fully-diluted shares. What is your latest reported cash and debt balance?

We currently have 53m shares outstanding and 7m options and performance shares outstanding. Of the outstanding shares around 41% are held by IAMGold, 9% Sprott and 12% by management/board.

As at the end of Quarter 3 2014 the company had net current assets of around US$ 8.4m within that there was a cash position of US$12m offset by a current loan balance of US $3m. In addition the Company had long term debt of US$ 6m payable to Samsung and the Government of Botswana.

Galane Gold recently entered into a two year gold prepayment agreement with Samsung. Can you describe that arrangement?

Samsung has provided a US$5m loan facility to Galane Gold in return for:

· the sale and delivery of a minimum of 1,607 ounces of gold per month for a period of two years

· gold payable by Samsung at a fixed discount rate to the then prevailing spot price upon delivery of 1.5% for the first 12 months and 0.5% for the following 12 months.

· the loan facility is repayable by the Company in 18 equal principal payments

· approximate cost of capital of 8.9% per annum. Capped at 14.7%

It should be stated that there was over 12 months of legal and financial due diligence and the facility by Samsung before the facility was drawn down in September 2014. The funds were used to repay IAMGold facility which removed restrictive covenants on dividends, share repurchases and corporate activity; and also to add to working capital. We believe Samsung represents an attractive, strategic, non-dilutive funding solution for future opportunities.

What do you say to investors who might be uncomfortable investing in a Botswana based gold producer?

To be honest I am not sure why investors would be uncomfortable investing in a Botswana gold producer. It is ranked the best mining jurisdiction in Africa and in the top 10 in the world by the Fraser Institute. The country itself has a strong GDP with a AA rating plus no exchange control. The Government is a large stakeholder in Debswana and the Tati Nickel mine so understands the challenges faced by mining companies and as a result has created a transparent and well run mining code. I have worked in some more of the challenging mining environments like the DRC and Zimbabwe and so I can honestly say that I have not worked in such a supportive environment for mining companies. That includes a well-educated and knowledgeable workforce.

2014 was a disappointing year. Can you tell readers why operating performance was below forecast?

We had one major setback in the year which was the failure of the SAG mill motor. This adversely effected our milling rate for over 6 months while we sourced a new motor and repaired the damaged one. Fortunately part of our plan when we took over the mine was to make ourselves more flexible to gold price and adverse issues. The main way we did this is reduce the proportion of fixed costs of our overall operations from 70% to 30%. This enabled us to manage our production costs and mine from more economic sources. We therefore managed to sustain our cash balance during the period. In addition we had insurance cover for business interruption and we have agreed a settlement of $2m to cover the period while the SAG mill motor was down.

According to your corporate presentation, IAMGold Corp owns 41.5% of Galane Gold’s shares. Is this an overhang on the stock or a supportive long-term holder?

IAMGold have been a supportive shareholder who have given us the time and the opportunity to turn this mine around so that we now consider ourselves as a low cost producer with a long term life. It is true that by holding such a large block they do depress the share price but we believe that this has been a necessary evil to date to assist us in the turn around. I think we are now in a position where we need to manage their holding and reduce the effect it has on our share price. We are in discussion with IAMGold on how to achieve this but maintain a strong relationship with them.

Is Galane Gold looking to make acquisitions? If so, please describe your company’s strategy in this regard. Might IAMGold be interested in participating?

Galane Gold is now in a position where it can consider acquisitions. We have a robust mine plan which we are continually adding to, a low all in cost and a strong/experienced management team. The most obvious targets for us our Companies that are in the same position Mupane was before we took it over. We have proved we can turn around a mine and add life so they would be a perfect fit. Our management team have experience across the globe so we are not restricting our review of potential acquisitions to just Africa but it will have to make sense logistically for us.

On the flip side, is there any evidence or reason to believe that Galane is a takeout target itself?

If you look at our current market valuation compared to cash in bank then the question is why aren’t we a takeout target. Companies have shown interest and as I alluded to having a large shareholder like IAMGold has been beneficial to us in this respect. Any transaction that may happen we will ensure that we achieve what we believe to be a fair valuation for our shareholders.

Is it possible that Galane would make open market purchases of stock or pay a dividend with free cash flow? Is that even on the table?

One of the reasons behind the Samsung facility was to repay the IAMGold loan which had restrictive covenants on purchasing of stock and dividends. We now have the flexibility to do both and it something we review at every board meeting with regards to the timing.

Your corporate presentation states that Galane’s mine life is about 5 years. Can mine life be extended over time? At what capital cost?

Galane considers Mupane to be a mature mine now and has moved to a process of a rolling 5 year plan. For the last two years we have rolled the 5 year plan and replaced depleted resources with new resources. It is our intention to keep on doing this into the future. We have over 1,600 km2 of exploration area which has had a full soil geochemistry and areo-magnetics. Our short term targets are all brownfield sites e.g. Signal Hill, Golden Eagle and Tholo where we are extending existing drilling to confirm our view that we can commence underground mining. On top of that we have long term targets where we believe that we will find the next big resource for example Orapa Road. We have currently forecast an expenditure of $2m a year to replace depleted resources and continue work on the longer term targets.

Presumably you feel that Galane is undervalued. Why do you think that might be?

Yes, Galane is undervalued. This is because of a number of reasons

· Incorrect perception in the market over the cost of production and life of mine

· Lack of marketing – we have spent over 3 years turning the mine around and concentrating on the fundamentals. We believed that only once we achieved this which we had promised the market we would be in a position to return to the market to discuss what we had achieved.

· IAMGold shareholding this is perceived as an issue by potential shareholders who would like to understand what will happen to this block before investing.

As we have discussed we now believe that we have now in Mupane a low cost long term producer. We are addressing the issue of the IAMGold shareholding. So the only outstanding item is to re-educate the market through an extensive marketing program. We have plans in place to start this programme after the publication of the 2014 results. So in my view everything is in place to see a significant re-pricing of our stock.

Are there any misconceptions that prospective investors might have about Galane Gold that you would like to address?

What I would really like to get across to potential stakeholders is that Mupane is a mature mine that we believe has a long life in front of it and the resources to ensure that it can continue at current gold prices and lower. It is perfectly positioned to take advantage of any positive change in gold price.

1. The gold market is very firm, given that most Indian players are in “wait and see” mode. Demand in India has slowed tremendously in recent weeks, in anticipation of the February 28 budget release.

2. Please click here now. That’s the daily gold chart. When I issued a “book profits now” signal in the $1305 area, I did so because Indian demand was drying up quickly, and because the 14,7,7 Stochastics oscillator was above the 90 level.

3. During the ensuing decline from the $1308 area to the $1190 area, the Indian central bank announced more major changes to its gold market policies.

4.Banks can make loans to jewellers again, and gold coins can once again be imported.

5. This is very good news. Once the budget is announced on Saturday, I expect demand to begin to rise almost immediately, and certainly within a week or two. Also, the March – June wedding season is almost here, and there is a strong possibility that the import duties will be reduced in the budget.

6. Please click here now. Koos Jansen follows the Shanghai Gold Exchange (SGE) very closely. It’s welcome (and expected) news, to see that India will be the largest partner of the Shanghai Gold Exchange. Clearly, the world gold community has a very bright future, regardless of what happens in America.

7. In 2015, gold stocks are acting much better than gold itself, as I predicted they would. I expect this outperformance to continue for many years.

8. On that note, please click here now. That’s the daily chart for Barrick. There’s a superb inverse head and shoulders bottom in play. Also, note the beautiful buy signal occurring now, on the 14,7,7 Stochastics oscillator.

9. Newmont looks even better! Please click here now. That’s the daily chart. There’s a powerful momentum-style buy signal in play on the Stochastics oscillator, and it comes as Newmont stages a spectacular breakout from a pennant formation.

10. Newmont is acting like gold is about to leap $100 higher, and after the Indian budget is released… maybe it will!

11. Please click here now. That’s the GDXJ daily chart. While gold has declined about $118 from $1308 to $1190, junior gold stocks have consolidated in what is essentially sideways price action.

12. Wage hike pressures in the United States are growing, and I’ve predicted that rate hikes will be required to counter the inflation produced by higher wages.

13. Mining companies are in a sweet spot now. Game changing events are occurring on the demand side in both India and China, inflationary pressures are rising in America, and lower oil prices are reducing the costs of mining.

14. Please click here now. That’s the daily chart for oil. Most investors never thought oil could fall the way it did, and now many of them are trying to call the bottom.

15. I think they are wasting their time and money. The chart looks horrific, and I expect it to look that way for many years, keeping fuel costs low for mining companies.

16. Institutional money managers want to invest in markets that have stability, and the changes in India and China are bringing tremendous stability to the world gold market, as is the price of oil.

17. There’s more good news for the Western gold community. To view it, please click here now. I’ve never subscribed to the view that banks are carrying giant COMEX short positions that are so big they will blow up the banks, if the price of gold rises. Having said that, banks do operate substantial gold price hedging programs for their clients, and they have a vested interest in seeing their clients make money on those hedges.

18. Probes in London have resulted in fines for gold price manipulation, and the LBMA price fixing has been revamped. The new fixing mechanism is much more transparent than the old one.Transparency makes institutional money managers comfortable about placing sizable client money in the gold market.

19. Added transparency in the gold market is a good thing. The US Justice Department probe that is underway now should add even more transparency, and that will attract even more money managers to gold stocks.

20. Please click here now. This is a nice snapshot of the latest COT report for gold. I’ve highlighted the action of the commercial traders (banks) in green. They have been sizable buyers of gold, into the current price decline.

21. It appears they are betting on a duties cut in the Indian budget, but whatever the reason is for their current buy program, the commercial traders have a winning track record. Amateur investors who are shorting gold now, are essentially taking the other side of that trade.

22. That’s a dangerous and reckless approach to take in the gold market. As the Indian budget is released, the bearish amateur traders are at great risk of receiving a serious financial beating!

23. Please click here now. Janet Yellen is probably best described as the “Queen of fiat”. Statements she makes can affect T-bond prices quite dramatically, and in turn that can have some effect on the price of gold. Janet is scheduled to make some important statements today, and the T-bond chart suggests she will sound dovish.

24. To view the chart, please click here now. Note the blue downtrend line on this daily T-bond chart. I predicted that bonds would stage an upside breakout from that line, and they have. I think Janet’s speech today will be the trigger that creates a buy signal on the 14,7,7 Stochastics oscillator. I’ve highlighted that at the bottom of the chart. A surge in T-bond prices is almost always accompanied by a nice rally in gold!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

Chad Ulansky cut his teeth on Ekati, Canada’s first diamond discovery, but it’s uranium that he’s hunting for now in Canada’s frozen North.

The Kelowna geologist is president and CEO of Northern Uranium (TSXV:UNO), which is exploring in northwestern Manitoba just beyond the eastern edge of the prolific Athabasca Basin.

Ulansky got his start as a geologist with Chuck Fipke’s Dia Met Minerals, which discovered Ekati, Canada’s first diamond mine, at Lac de Gras in 1991. The discovery by Fipke and Dia Met partner Stu Blusson, which came after years of systematic exploration, rocked the global diamond industry and sparked the biggest staking rush since the discovery of gold in the Klondike.

The Ekati discovery also kick-started the Canadian diamond industry and upset the De Beers cartel. Canada is now the world’s third largest producer of diamonds by value, with four mines and another two under construction.

Last year, Fipke sold his 10% interest in Ekati for $67 million US to Dominion Diamond Corp., which owns 89% of the mine (Blusson retains a 10% interest).

The Fipke-Ulansky partnership began when Ulansky was just a teenager. An avid outdoorsman from a young age, Ulansky met Fipke when the geologist attended a presentation Ulansky gave to a Kelowna scout troop, and the two hit it off. Fipke told him he would call him at the end of the school year.

Sure enough, Fipke phoned in June and offered Ulansky a summer job, a gig that turned into a continuing, decades-long partnership.

Ulansky continued working for Dia Met until its purchase by BHP in 2001.

Along the way, he obtained a bachelor’s degree in geology at the University of Cape Town in South Africa, where he studied under renowned diamond geologist Dr. John Gurney.

Ulansky retained his love of the outdoors while living in Cape Town. In 2001, he set a record for the Three Peaks Challenge, a 50-km mountain running trail that involves ascents of the three major peaks above Cape Town — Devil’s Peak, Table Mountain and Lion’s Head.

URANIUM HUNT

He’s climbing a peak of a different sort as president and CEO of Northern Uranium, which is searching for an economic uranium deposit just outside the Athabasca Basin — home to dozens of competitors.

Northern Uranium has earned a 50% option on the Maguire Lake property from CanAlaska Uranium. The property borders on Saskatchewan and is located along the extension of the Mudjatik Wollaston tectonic zone, which runs southwest-northeast near the Manitoba border. The zone hosts many of the Basin’s major uranium deposits, including Cameco’s Cigar Lake, McArthur River and Key Lake.

Cigar Lake and McArthur River both have uranium grades above 20%, and Ulansky is out to prove that high-grade uranium exists on Northern Uranium’s property as well.

His thesis is that extensive glaciation stripped off the sandstone and sediments and left basement rock exposed, hosting shallow uranium mineralization.

There is some early evidence supporting his thesis. Prospecting work done by CanAlaska uncovered a boulder that contained 66% uranium oxide, and in situ grab samples have contained grades up to 9% U308.

Finding dozens of mineralized boulders in a small area is highly uncommon, Ulansky says, and Northern Uranium is now searching for the bedrock source of that mineralization.

“What we need geologically is all that uranium in trace quantities across huge volumes of rocks to be picked up and brought to one spot and concentrated there,” Ulansky says, talking about geological changes that occur over millions of years. “The mechanism for that is percolating fluids, waters that circulate through bedrock. When these fluids are slightly oxidizing, they scavenge uranium, they move thru cracks, fissures and preferentially strip out the uranium and carry it with them. The fluids migrate through rocks, when they get to a fault zone that’s permeable, they’ll rise to the surface and cool. Solubility drops and over millions of years, fluids will circulate and uranium will start to precipitate out.”

Northern Uranium has expanded on CanAlaska’s program using various methods — including electromagnetic, magnetic, ground gravity and radon surveys — to narrow down drill targets for a “focused” $1.5-million exploration program.

Airborne magnetics has identified faults that could provide an important pathway for mineralizing fluids, while electromagnetics has identified a 35-kilometre conductor path where precipitation of uranium mineralization is more likely.

RADON RESULTS STELLAR

Radon surveys — which are not being used by all early-stage uranium explorers in the Basin — are among the most useful tools in the hunt for uranium mineralization, Ulansky says.

Just as Fipke used diamond indicator minerals to find Ekati, Northern Uranium is using radon surveys to detect the presence of uranium mineralization.

“The silver bullet for uranium is radon. It’s a gas, highly mobile, very short half-life, that percolates up from uranium mineralization at depth,” Ulansky says.

“Imagine if you were exploring for gold and it uniquely gave off something called gold gas. You’d just go look for the gold gas.”

Radonex, the same company that completed radon surveys for Fission’s high-grade Patterson Lake South project did lake-based radon work for Northern Uranium, and the results were comparable to PLS’s, Ulansky says. Results from the land-based radon surveys were also strong.

However, the challenging part is that the radon signature is much larger than the uranium mineralization associated with it.

“We are very, very strong believers in the fact that there is high-grade uranium mineralization there, it’s just a matter of figuring out where it is,” Ulansky says. “I firmly believe there’s a major discovery to be found, and it’s just a matter of drill testing to find it.”

Watch: Mr. Fipke’s Canadian Mining Hall of Fame 2013 Induction Video

TARGET ZONE IDENTIFIED

Ulansky’s team has zeroed in on an area 3 kilometres wide by 10 kilometres long, centred over Maguire Lake. The target zone is northeast and up ice of the high-grade boulder discovered by CanAlaska.

“The ice direction is from northeast down to the southwest, so it certainly hasn’t come from the Athabasca, which is down-ice,” Ulansky says. “That’s telling us that up-ice there is some exceptionally rich mineralization to be found.”

During the 3 coldest months of winter, crews have been testing priority targets underneath the lake.

Early drilling has hit some uranium mineralization but not in economic quantities, Ulansky says.

Drill results are expected in the coming months, and with $500,000 in the treasury, Northern Uranium will need to raise money to fund more drilling.

Fipke is a special advisor and major shareholder.

“All the geology to date looks exceptionally promising, it’s just a matter of raising the funds to continue drilling,” Ulansky says.

Northern Uranium can earn up to an 80% interest in the project by spending an additional $8.4 million in two tranches and issuing 7.5 million shares and 3.75 million warrants over four years.

Ulansky remains a key player in Fipke’s group of companies; he’s president of Cantex Mine Development and president and CEO of Metalex Ventures. The two companies share Kelowna office space with Northern Uranium, helping keep the burn rate down to $10,000 a month.

The group of companies also own the drill rigs.

The radon and boulder indicators that Northern Uranium has are promising, but now comes the hard part: finding high-grade uranium mineralization. Ulansky compared the exploration effort to trying to break a plate at the bottom of a swimming pool blindfolded, with a pool cue. You know the plate’s there, but to smash it, you have to find it.

If you’re going for that type of swim, the partners you want are Chad Ulansky and Chuck Fipke.

To receive drilling news directly from the company, email info@northernuranium.com with the subject line, “Please add me to your email list.” That or call the company’s Kelowna office at 1.250.448.4110 for more information.

Author has a financial interest in Northern Uranium. The article is not intended to be investment or professional advice of any kind. Readers are strongly encouraged to independently verify all information contained in the article, as it may contain errors. Please see Terms of Use and Privacy Policy for important disclosures. Some of the statements contained herein may be forward-looking statements which involve known and unknown risks and uncertainties. Without limitation, statements regarding potential mineralization and resources, exploration results, and future plans and objectives of Northern Uranium are forward looking statements that involve various risks. The following are important factors that could cause Northern Uranium’s actual results to differ materially from those expressed or implied by such forward looking statements: changes in the world wide price of mineral commodities, general market conditions, risks inherent in mineral exploration, risks associated with development, construction and mining operations, the uncertainty of future profitability and the uncertainty of access to additional capital. There can be no assurance that forward-looking statements will prove to be accurate as actual results and future events may differ materially from those anticipated in such statements. Northern Uranium undertakes no obligation to update such forward-looking statements if circumstances or management’s estimates or opinions should change. The reader is cautioned not to place undue reliance on such forward-looking statements.

On February 10th, American Sands Energy Corp. [AMSE] provided an excellent corporate update regarding the engagement of Stifel, Nicolaus & Company as its exclusive investment banker and financial advisor. CEO, William Gibbs commented,

“We are excited to be working with Stifel. AMSE is approaching a pivotal point in our development as we work through the permitting process and move towards building our facility and beginning production. Stifel, with its expertise in the energy industry, is a significant addition to our team and we believe will be a great help in achieving our goals.”

I believe the retention of a full service investment bank with a strong reputation in the U.S. is a meaningful de-risking event. For those who don’t know Stifel Nicolaus, please consider the following,

“Stifel’s Investment Banking practice is principally focused on the middle-market. We have twelve industry-focused investment banking groups together with specialty groups providing coordinated financial sponsors coverage and private placement expertise. Stifel has extensive financial advisory and capital-raising experience, having completed over 3,100 public offerings, 900 M&A transactions and 400 private placements since 2000.”

Furthermore, progress towards the completion of permitting appears to be on track. According to CFO, Dan Carlson,

“We received the most recent comment letter from DOGM in early January. We are in the process of responding to the comments and expect to be resubmitting our application by the end of this week [mid February]. Based on the comments, and ongoing conversations with DOGM, the Company believes that we have met all their criteria and hope to finish the permitting process soon.”

I’ve written about American Sands Energy in the past and have routinely outlined what I believe to be the more significant risk factors. First on the list, in terms of timing, is the receipt of all the permits needed. As mentioned above, that risk factor appears to be fading. The second significant risk is obtaining financing for the processing facility. The amount of capital required was recently estimated at $123 million. That is a large figure, but represents the true amount needed to reach commercial production. On one hand, hiring Stifel, Nicolaus is an important step. However, one can not help but notice that the price of WTI Crude has fallen into the $50’s per barrel. Essentially, the oil price is a new risk factor, but one that could possibly be resolved as American Sands moves into production in about 2 years. In other words, I believe WTI Crude will rebound to $80/bbl or higher within 2-3 years i.e when the company should be really humming.

Having said that, the financing is expected to take place in 1h 2015. I still believe that an equity injection could probably get done at a significantly higher stock price after permitting is finalized and with the expert assistance of Stifel Nicolaus. Make no mistake, that capital round will result in meaningful equity dilution. Still, there remains tremendous upside once permitting and funding is in place, both likely in 2015. In my mind it’s a question of when, not if this ambitious project gets off the ground. As a reminder, a portion of the capital needed could come from non-dilutive sources such as project-level investments and equipment financing.

Therefore, this year could amount to a huge amount of de-risking from the completion of both permitting and a capital raise. Then, all eyes will turn to the building of the commercial scale facility to separate sand from the oil bitumen and the mining of ore. I would argue that getting permitting and funding done is a larger hurdle to clear then the mining and the construction of the 9,000/bbl per day facility. While the share price and crude oil price are disheartening, absolutely nothing changes the compelling story of the technology and the flowsheet. Recall that the oil sands in Utah are entirely different from the oil sands in Alberta, Canada. Upon reaching commercial production, operating expenses will be lower than that of the Alberta oil sand operations. Further– upfront capital per barrel of daily production will be a lot less.

That’s why Alberta oil sands companies are cutting cap-ex and people at an alarming and accelerating rate. Much of the oil sands in Canada have costs of $60-$80/bbl. American Sands announced in its February 10th update that its operating cost is estimated at $40/bbl of bitumen. Without going into too much detail, there are ample reasons to believe that global oil prices will rebound smartly in the next few years. Some analysts are calling for $80-$100/bbl crude, others still point to $50-$60/bbl crude in 2 years. Note, few if any analysts forecasted crude oil in the $50’s…

My view, shared by many pundits and analysts, is that much of the oil sands in Alberta will come offline if oil prices remain depressed, and that a significant portion of the U.S shale plays will start to slow as new capital will not be deployed. The shale plays won’t necessarily slow in the next few months, but it’s undeniable that at the current oil price, many planned wells in the U.S. will not see the light of day. Remember the shale oil plays start out strong but decline curves are very steep. In the first year alone, it’s not uncommon for a shale oil well’s production to decline by 50% or more. Therefore, a lot of newly drilled wells could keep supply at a high level for a period of time, but it’s a question of when, not if, crude oil prices rebound.

Finally, many observers of the oil market point out that a number of junior and mid-tier oil companies are carrying a lot of debt and are in serious trouble. When annual reserve calculations are made in March, investors will see a lot of write downs of high cost assets. Debt covenants will be breached. Finally, I should add that rig counts have already fallen dramatically in the U.S and elsewhere. To sum up, the oil price may remain depressed for the next 6-12 months, but the cure for low prices is….low prices. American Sands does not require a higher oil price for a least 2 years. Global demand for oil grows about 2% each year, which amounts to a few million barrels per day. The alleged over-suppy of crude in the markets today is pegged at 2-3 million barrels. As less capital is deployed for new and sustaining existing wells, the glut will be taken care of from natural oil well depletion matched with natural annual global demand of a few million barrels per day.

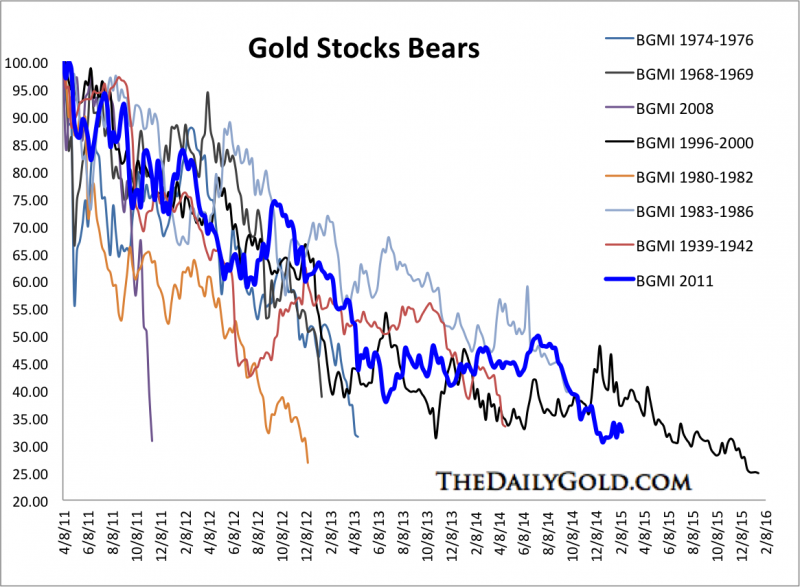

Precious Metals have had an interesting week. Both Silver and the gold stocks rebounded off their 50-day moving averages only to do a 180 the following day. Meanwhile Gold has given back most of its January gains. In this missive we consider the near term outlook for Gold and the gold stocks.

In the chart below we plot Gold and Gold priced in foreign currencies (Gold/FC) which is essentially the inverse of the US$ index. Gold put in a strong rebound, rallying over $150/oz from November through January. That was also its strongest rally in real terms in several years. As we can see, Gold/FC drove that rally as its driving the current decline (to some degree). Gold/FC has a bit more downside to go to reach support. The fact that Gold could not hold above $1240 tells us that Gold will need more time before it can retest trendline resistance. However, Gold’s strength against foreign currencies is a major character change that wasn’t in place during 2013-2014.

Turning to the stocks, let’s start with the bears analog chart. We use weekly data from the Barron’s Gold Mining Index which dates back to 1938. Back in December we noted that gold stocks were likely at their second most oversold point in history. The most oversold point was the months and weeks prior to the bottom in 2000. Markets can do anything in the short term but this chart makes a strong case that miners are extremely ripe for a new bull market.

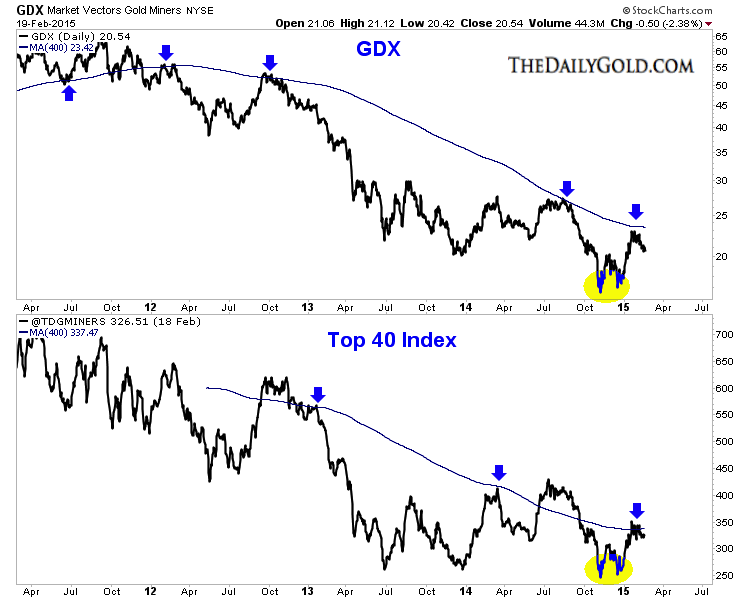

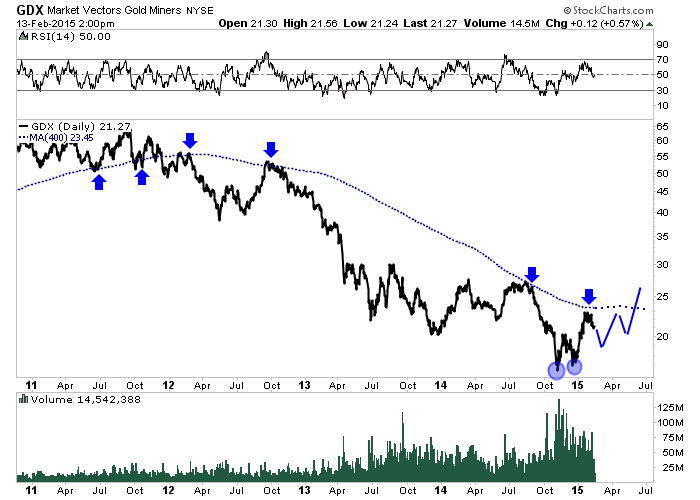

Next is a chart of GDX and our Top 40 Index. Both formed a strong double bottom at the end of 2014 and both will need to surpass their 400-day moving averages to be in a new bull market. The miners formed the recent low amid an extreme oversold condition. After a strong rebound, resistance has come into play. The range between strong support and strong resistance is getting smaller.

The trend for precious metals can be considered neutral or range-bound with a current bearish bias. After strong rebounds, Gold and gold shares are backing off from resistance. They aren’t yet ready to make major breakouts to lift them into bull markets. This is bearish but there have been key bullish developments in recent months which should caution bears. Both Gold and gold shares performed well amid a very strong US$ which signals a major change. Gold companies are benefitting from the collapse in energy prices and weak currencies within the jurisdictions they operate.

Because gold companies can benefit from lower energy costs and weaker foreign currencies, it’s quite possible that they could be the first, ahead of Gold to break into new bull market territory. Market heavyweights such as Jeff Gundlach and Jim Rogers may sense that as they recently became investors in the miners. A new bull market lies ahead sooner rather than later but investors and traders need to maintain their discipline and patience.

The following article was adapted from the August 27, 2014 issue of Resource Opportunities, our premium newsletter (the video below was taped in December 2014 and just released this morning).

North Arrow is a presenting sponsor at our upcoming Subscriber Investment Summit in Toronto on February 28th, at a truly critical time for the company.

Only a dozen or seats remain at the free conference, so please register now if you intend to be there.

North Arrow Minerals (NAR.TSXV) at a glance:

– Diamond exploration in Nunavut, Saskatchewan, Northwest Territories and Ontario

– Share price: $0.56

– Shares outstanding: 49.8 million

Catalysts:

– Processing of the Qilalugaq Q1-4 bulk sample, which hosts a population of fancy yellow diamonds, is underway and expected to be finished in April 2015. Preliminary indications are that the profile of the bulk sample is consistent with earlier, smaller samples, according to a Jan. 21 news release. A valuation of stones larger than .85 mm will follow processing.

– 3,000-metre drill program at the Pikoo diamond project in Saskatchewan.

Gem Hunting with a Diamond Pioneer

Our goal as junior resource investors is to identify mispriced assets and capitalize on the discrepancy.

Our mission at Resource Opportunities is to identify stocks with an attractive risk-reward profile, where the upside potential more than mitigates any downside risk. We are on the hunt for stocks that could double or triple in the short term, on the way to becoming ten-baggers and more.

Our featured stock in this edition of Resource Opportunities is run by a mining industry legend who delivered 1,000% plus returns to shareholders of his previous diamond play.

He was a first mover during one of the largest staking rushes the world has ever seen, giving his company valuable land positions that led to a world-class discovery.

And he’s back in the hunt, exploring for the same commodity that made him wealthy, in remote terrain that few mineral explorationists know better. His new company has assembled a portfolio of high-quality projects that other companies have spent millions developing. And he’s backed by a deep-pocketed mining tycoon whose multi-billion-dollar empire straddles the globe.

The explorer is Gren Thomas and the stock is diamond exploration play North Arrow Minerals.

The North is Thomas’s favoured exploration terrain, and Arrow describes the trajectory of his Aber Resources stock after the company’s discovery of Diavik. A one-time penny stock, Aber scaled heights of $50 a share en route to deals with Tiffany’s and the purchase of luxury jeweller Harry Winston. Aber’s successor company is Dominion Diamond, which owns 89% of the Ekati diamond mine (after buying Chuck Fipke’s 10% stake) and 40% of Diavik.

Like Mr. Fipke, Gren Thomas is a true pioneer in the Canadian diamond exploration scene.

After Fipke’s landmark discovery, Thomas teamed up with partners – including Christopher Jennings and Bob Gannicott – and quickly staked land to the southeast. They set to work evaluating kimberlite indicator minerals and identifying drill targets.

But diamonds are among the most difficult minerals to find – the geological equivalent of a needle in a haystack – and Aber proved it over the next few years with its fruitless hunt for an economic deposit. Then, in the spring of 1994, a breakthrough. An Aber field exploration crew led by Gren’s geologist daughter Eira Thomas was drilling the final hole before spring breakup, and pulled out core with an almost 2-carat diamond embedded in it – an almost unheard-of occurrence.

Twenty years later, diamonds are still being pulled out of that kimberlite at Diavik – one of the world’s richest diamond mines – and Canada is the world’s third-largest producer of the gems.

In addition to making investors rich and establishing Canada as a diamond powerhouse, Aber’s discovery helped cripple the De Beers cartel that had dominated all facets of the industry – from mining to trading to sales – for more than a century.

But there’s a small problem. The industry built on “Diamonds are forever” is slowly running out of the glittery commodity, just as global demand ramps up. According to Bain and Company, supply is expected to grow by 2% annually over the next 10 years, while demand grows by 5.1% annually – driven by consumer demand in the United States as well as China and India. Few new mines are coming onstream in the next few years.

New Canadian diamond supply is part of the solution. Gahcho Kue in the Northwest Territories is the largest new mine coming on-stream. It’s a 51-49% joint venture between De Beers and Mountain Province Diamonds (MPV.TO) that is slated to open in 2016, while Stornoway’s smaller Renard mine in Quebec is scheduled to begin commercial production in 2017.

Robust Canadian diamond exploration is also part of the longer-term solution. Interest in the sector is reviving as diamond veterans and new players alike head north to identify diamondiferous kimberlites and seek their fortunes. Analyst coverage is also on the rise – both Dundee Capital Markets and Barclays released extensive diamond research reports in 2014.

On the exploration side, Kennady Diamonds (KDI) was the rock star, for a while. Kennady was spun out of Mountain Province and owns the Kennady Lake North project adjacent to Gahcho Kue. The company is developing four diamondiferous kimberlites that are showing great promise, but the stock has hit some headwinds, dropping to $3.79 from highs of $8 in the fall. Kennady has a deep-pocketed major shareholder – Irish billionaire Dermot Desmond, who owns 37% of S.O.

Another notable junior explorer is Peregrine Diamonds (PGD), which boasts Canada’s highest-grade advanced-stage project in Chidliak, its flagship Baffin Island play, as well as impressive stone values. Peregrine also has the Friedland brothers in its corner, with a combined stake of about 34%. If a mine is built at Chidliak, the upside would be substantial, but this stock could severely test your patience in the meantime.

Most of Canada’s other diamond exploration plays are either early-stage or bolted on to producers. Canterra Minerals (CTM) is run by Randy Turner, who discovered De Beers’ Snap Lake mine and is exploring again in the same neighbourhood, while Margaret Lake Diamonds (DIA) has a land package adjacent to Kennady’s, and flew a gravity survey last year. Dominion Diamond (DDD) and Stornoway Diamonds (SWY) also have exploration projects.

Enter North Arrow Minerals and its chairman, Gren Thomas. Before interest in Canadian diamond exploration perked up again, Thomas optioned several “orphaned” properties, including three in the Stornoway Diamonds’ exploration portfolio. Thomas’s daughter Eira, currently CEO of Kaminak Gold (KAM), is a Stornoway cofounder.

North Arrow shares jumped from 40 cents to the 70-cent level in the days following the company’s Nov. 5, 2013 announcement of drill results from Pikoo, an east-central Saskatchewan project optioned from Stornoway. A 210-kg sample of drill core from PK150, the first kimberlite North Arrow discovered there earlier in 2013, returned 745 diamonds larger than the .106 mm sieve size, including 23 diamonds larger than .85 mm.

It was an exceptional result from such an early-stage project, fuelling optimism that North Arrow has an economic deposit on its hands. As Gren Thomas puts it, “we know enough about it now that we can say this thing, if there’s enough tonnes, it can be commercial.” North Arrow hit kimberlite in 9 of 10 drill holes completed on the property. Geologists spent the rest of last year collecting and evaluating 560 till samples to help define new drill targets, including several new kimberlite indicator mineral trains. A 3,000-metre drill program is now underway.

North Arrow earned an 80% share of the project from Stornoway, which retains 20% and passed on a one-time back-in right to acquire another 20%.

North Arrow’s most interesting property is the unpronounceable – and under-the-radar – Qilalugaq (kill-a-loo-gah-ck) project near Repulse Bay, Nunavut. North Arrow has optioned 80% of Qilalugaq, another of Stornoway’s “orphans,” but Stornoway retains a one-time back-in right to acquire another 20% of Qilalugaq by paying North Arrow three times its exploration costs. Over $25 million has been spent developing the property, which was originally staked by BHP Billiton Diamonds, so North Arrow is leveraging large amounts of cash spent by others.

Qilalugaq has size – its 12.5-hectare Q1-4 kimberlite is the largest diamondiferous kimberlite pipe found in the eastern Arctic. Qilalugaq is advanced – Q1-4 has an inferred mineral resource estimate of 26 million carats from 48.8 million tonnes of kimberlite, for an average diamond grade of 53.6 carats per hundred tonnes (low by Canadian standards but comparable to some of Renard’s pipes). And Qilalugaq has location – it’s 7 kilometres from tidewater.

Most importantly, Qilalugaq has rare yellow diamonds. Fewer than 0.1% of all diamonds are yellow, and fewer still are the yellow diamonds so vivid and intense they can be classified as “fancy yellows.” Colour is one of the 4 Cs of diamond grading, along with carat, clarity and cut. High-quality coloured diamonds command top prices.

How significant is the presence of yellow diamonds to diamond values? Consider the Ellendale mine in Australia, which is owned by Kimberley Diamonds. Ellendale is the world’s leading source of fancy yellows, contributing about half of the world’s supply from a depleting reserve. Ellendale’s fancy yellows make up only about 15% of total carats sold, but a whopping 80% of the company’s revenue.

No wonder North Arrow chairman Gren Thomas calls Qilalugaq “a potential company maker.”

Until recently, Kimberley sold all its fancy yellows to Tiffany’s – the luxury jeweller that had a relationship with Aber, continues to source diamonds from Aber successor Dominion Diamonds and has viewed some of North Arrow’s yellow diamonds. However, Kimberley announced Aug. 22 it would display 750 carats of its fancy yellows from Aug. 28 to Sept. 9 and sell them at auction on Sept. 10. Wonder if anybody from North Arrow stopped by to compare notes?

North Arrow has collected a bulk sample of more than 1,500 tonnes of kimberlite to determine size distribution, what proportion of Q1-4’s diamonds are yellow, and the quality of those yellows. The bags of kimberlite were shipped out on the annual sealift that arrived in Repulse Bay late last Summer. Processing began in October in Thunder Bay and North Vancouver, after which about 500 carats of the Q1-4 diamonds will be flown to Antwerp for independent evaluation. The results of that valuation are expected in the second quarter of 2015. That’s when Stornoway will have the one-time back-in right to an extra 20% of the project.

During our recent interview with North Arrow president and CEO Ken Armstrong, he helped set expectations for the diamond value. Operating Canadian diamond mines are typically in the order of $100 to $500 per carat, and a result of greater than $150 per carat would be significant for the small company.

“If we get a high valuation, then it immediately becomes a development track project with a pretty clear path for further evaluation,” Armstrong said. “We would enter into completing a preliminary economic assessment. The next field work would be more drilling, upgrade the resource to measured and indicated status, drill some deeper holes, some glory holes to 600 meters … to see if the kimberlite is still down there … and then following that up pretty quickly with a larger bulk sample … The project could be on its way, and it could happen very fast.”

North Arrow shares – which some days, don’t trade at all – are at about the same level they were when Resource Opportunities initiated coverage on Aug. 27.

But North Arrow chairman Gren Thomas has increased his ownership level since then – exactly what we like to see when a company’s stock does not reflect a company’s operational progress. Since Aug. 27, Thomas has purchased more than 380,000 North Arrow shares in the public market at prices ranging from 47 to 60 cents, according to INK Research. He owns about 6 million shares, a 14.3% stake.

North Arrow’s largest shareholder is a Lundin family trust, which owns about 23% of the stock. Billionaire Lukas Lundin has deep pockets and an outstanding track record of creating shareholder value, including at his dividend-paying African diamond producer Lucara Diamond (LUC.TO), which has a market cap approaching $800 million. Eira Thomas is one of Lucara’s largest individual shareholders. Lundin has participated in recent North Arrow equity offerings on a pro rata basis, most recently in February 2014 (at 65 cents). With Lundin as a supportive shareholder, raising more cash for exploration programs shouldn’t be a problem.

The links between North Arrow and the Lundin Group’s Lucara run deep. Eira Thomas is a Lucara director, was key to the formation of Lucara and owns about 2% of outstanding shares, while Lucara CEO William Lamb sits on North Arrow’s board of directors. “Lucara’s an outstanding diamond company, and I’m hoping of course we can do something similar with North Arrow here,” Gren Thomas told me.

With about 50 million shares outstanding, about $5 million in cash (as of October 31) and the stock at 56 cents, the market is assigning North Arrow Minerals an enterprise value of just $23 million. If even one of North Arrow’s projects proves economic, the company’s market capitalization should correct to multiples of that number.

We contend that North Arrow Minerals is a mispriced asset offering a better-than-average shot at dramatic share price appreciation. If that happens, we don’t know when it will happen. North Arrow is also a volatile and thinly traded stock.

However, the lack of liquidity on this closely held stock is a double-edged sword that works in your favour when good news comes out, as illustrated by the share price action following the Pikoo discovery in early November 2013. Gren Thomas and Lukas Lundin are unlikely to sell in the event of bad news, which offers some protection on the downside.

Because investing in diamond exploration plays is such a high-risk venture, a basket approach mitigates risk. But if we had to own a single diamond exploration stock, that stock would be North Arrow Minerals.

Watch our interview with North Arrow chairman Gren Thomas here.

Watch CEO Ken Armstrong discuss the Pikoo project here.

Sign up for North Arrow’s email list here.

Author is a shareholder in North Arrow Minerals. This is not intended to be investment advice of any kind and readers are strongly encouraged to do their own due diligence and consult a professional investment advisor before making any investment decision. This article and video contains “forward-looking statements” including but not limited to statements with respect to North Arrow’s plans, the estimation of a mineral resource and the success of exploration activities. Forward-looking statements, while based on management’s best estimates and assumptions, are subject to risks and uncertainties that may cause actual results to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: risks related to the successful integration of acquisitions; risks related to general economic and market conditions; closing of financing; the timing and content of upcoming work programs; actual results of proposed exploration activities; possible variations in mineral resources or grade; failure of plant, equipment or processes to operate as anticipated; accidents, labour disputes, title disputes, claims and limitations on insurance coverage and other risks of the mining industry; changes in national and local government regulation of mining operations, tax rules and regulations. Although North Arrow has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Always do your own due diligence.

Via EnergyandGold.com, The mining industry is continually depleting its inventory, which is why it has always been an M&A led business. Junior companies find and develop new deposits and then mid-tiers and majors take them out. This has been the way of the miners for generations.

There are few undeveloped high quality gold projects in the world currently, especially those that offer potential scale and long life. Even fewer of these deposits are high grade. Continental Gold’s Buriticá gold and silver project in Colombia is one of the richest gold deposits in the world, consistently ranked among the top gold development stories in the world by analysts. We had the opportunity to interview CEO Ari Sussman by Skype on Thursday, for an update on the exciting Buriticá project.

Scott Armstrong: Please put Continental Gold’s Buriticá project in the context of other undeveloped gold deposits out there? How does it stack up?

Ari Sussman: We are at the forefront of Colombia gold exploration and development and although I say we are at the forefront, Colombia as a country has a rich tradition in gold mining. In fact, Colombia is the oldest and richest producer of precious metals in Latin American history. The gold museum in Bogota is one of the great things to see if you are a precious metals buff, it has pieces dating back hundreds of years. It’s definitely worth visiting and seeing if you ever make it to Colombia.

The story of Colombia is really interesting and is full of geological potential. People get confused when they think of mining in Colombia and ask why weren’t there other major discoveries made over the past 30 years, prior to the very recent exploration successes. The answer is that Colombia went through a very difficult period of troubled security problem which inhibited foreign direct investment into natural resources. However, until former President Uribe and current President Santos There has been a drastic improvement and so what do we have in Colombia now? We have a country with as good of a political regime as exists in Latin America for foreign business practices to operate. In fact the Government political alignment has been pro-business oriented for more than 40 years. Couple this with an ever improving security situation since the turn of the century and you have an excellent opportunity to make resource discoveries.

Why do we like Colombia geologically? Well the obvious reason is the Andes mountain chain continues through Colombia and it turns out there has been little modern exploration done for metals, not just gold but for base metals and oil as well.

Additionally, Colombia sits above a triple plate junction where 3 tectonic plates coalesce. Some of the worlds largest mines are located in other countries with this setting style. It’s clear we’re at the beginning of a gold exploration renaissance, which of course has been through a difficult period during the past three years. However, similarities in this regard can be made to Peru from 1997-2001 or Chile a decade earlier. In fact, this gold renaissance only began in 2006 and I get asked this question a lot “Colombia, there’s really not a lot to show so far. There’s no new mines that have been built and nothing’s happened in Colombia.” I say wait a minute people, the average mine today from discovery to production is 18 years! That’s the timeline globally. From 2006 until today what has happened in Colombia in gold? You have our Buriticá Project which is 7,000,000 ounces of gold at high grade in all categories which is going to grow to well north of 10,000,000 ounces. You had a company called Ventana Gold which at the time of its purchase was around 3.5-4.0 million ounces. Eike Batista bought it and now it is purported to be north of 15,000,000 ounces. Lastly, you have AngloGold Ashanti, which made a discovery called La Colosa that is expected to grow to over 30,000,000 low grade ounces. All of these ounces were discovered from grassroots, with a much higher than average discovery rate based on meters of diamond drilling completed compared to most other countries within this very short time frame.

Our Buriticá project is the one that is going into production first. We are aiming to commence production in late 2017 or early 2018. We took over this project and started putting money into it in early 2010 which is when we listed on the TSX. So 8 years or so to reach production is a lot faster than the average project globally at 18 years. So there’s actually been excellent success in Colombia in a short time frame. Now obviously Colombia has suffered since 2011 when commodity prices peaked, but so has everywhere else in the world. As a consequence money has dried up and exploration efforts have slowed drastically. Most companies that didn’t find potentially economic projects have left the country to do something else. Today we are entering the smarter money phase in Colombia. This is the phase where we are starting to see deep pocketed majors with significant exploration budgets now looking aggressively to make or acquire discoveries of large-scale. Then there’s us at Continental Gold with our Buriticá Project and also our portfolio of earlier stage projects behind it which we think offer excellent potential.

Scott Armstrong: Is your plan at the Buriticá Project to develop the project to production yourself?

Ari Sussman: We would like to develop the project ourselves and have the team in place to do so but shareholder value comes first and we will ultimately pursue the path that is in the best interest of shareholders. I get asked a lot if we will sign confidentiality agreements (CAs) with other companies and I’ve always maintained that we will not entertain signing CAs until after we permit the project. The precedent has always been very clear in Latin America if you do sell a project the best value obtained is generally after permitting has already been completed.

Scott Armstrong: So where are you on the permitting front?

Ari Sussman: In Colombia you need a mining license and an environmental license to produce gold. We received our mining license in 2013, that’s a 30 year license, so we’re finished in that regard. Still outstanding is the environmental license and our guidance for completion of that has been for mid-2015 and we are on target to meet that guidance. So in a few short months we do expect to be permitted, sometime in the summer time.

Scott Armstrong: What are the biggest challenges for Continental?

Ari Sussman: There’s two sets of challenges: The actual challenges on the ground with the project and then there’s the perception challenge. Let’s take the perception challenges first. The perception of the market on Colombia is that you cannot permit projects and that is just dead wrong. It’s due to an unfortunate event involving a specific instance where a company was denied an environmental permit because they were operating on land, which at the time was deemed to be in a national park. That is a one off case and that’s an important point to make. If you look at Colombia there are dozens of small gold mines that are permitted and operating in the country. Also, the world’s largest open pit coal mine produces profitably in Colombia, along with many other large coal mines. BHP operates a very large nickel mine which, at one point, was the world’s largest nickel mine. The point is, Colombia has a tradition of permitting environmentally and socially responsible projects yet perception remains negative. However, once we get our permit I can assure that Colombia will be viewed as the country where you CAN permit, not the country in which you cannot.

The challenges which we have with the project itself, well it’s an underground mine so obviously there’s a lot of engineering that has to happen to bring this project to fruition. Our plan is to complete a feasibility study in mid-2016 and that will be our financing and construction decision point for Buriticá. However, if you follow our company you saw we announced a PEA (preliminary economic assessment) late last year and it was in the lowest quartile (costs) rendering it one of the higher quality unbuilt projects in the world. Our post-tax IRR was 31.5%, our net present value at a 5% discount rate was $1.1 billion and we outlined an 18 year mine life which produced well north of 300,000 ounces of gold per year in the first five years. It is a very robust high-grade project with modest capex and being underground, it will utilize a small footprint of land.

The real key to Buriticá, which I think is very important for investors to understand, is the scale of the project. Buriticá, hosts two vein systems side-by-side, which boast a remarkable vertical dimension. In fact, both vein systems have been drill tested down to 1.8 kilometers and remain open at depth. Also, both vein systems boast lateral strike lengths of at least 1 kilometer. Yet, the individual veins that were included in our resource estimates have much smaller dimensions than this. The reason for this, for the most part, is due to lack of drilling and we are confident that we are going to grow to well north of 10 million ounces of gold plus silver in time.

Scott Armstrong: Aside from the challenging overall market environment for junior explorers, how do you explain the poor stock price performance? What are investors not understanding?

Ari Sussman: I think it mainly has to do with this fear of not being able to permit. We are trading at a discount to our peers for the first time in a very long time, we had historically always traded at a premium given the quality of the asset and the high grade. I think this makes an excellent entry point for someone because of this discount and if you’re willing to bet on the company’s ability to deliver a permit as well as deliver overall growth of the resource I think the future looks quite bright. I should mention as well that we will be coming out with an updated resource estimate in the May/June time frame. We are looking to improve the internal quality of it, which means conversion of inferred ounces to the indicated & measured category. Also, we expect to deliver overall growth in terms of the total number of ounces of gold while maintaining the high grade status of the project.

Scott Armstrong: How much cash do you have, and what were the financing prices?

Ari Sussman: We have $67 million dollars US in the bank as of November 5th, 2014 and have a $30 million budget for calendar year 2015. We have enough cash to make it through the feasibility study in mid-2016 at which point we will go for project financing. The last financing was done in November of 2012 at $9.55/share.

Scott Armstrong: What is Continental missing in terms of infrastructure in Colombia right now?

Ari Sussman: We’re in a very infrastructure rich area, you drive to our project on the Pan-American highway and there is abundant electricity available in the area. But what are we missing in terms of infrastructure? The milling part of the site is going to be built at the base of a mountain and we need to bring a 6 kilometer paved road down to it, a short distance indeed.

Scott Armstrong: What should investors expect from Continental during 2015 in terms of milestones and accomplishments?

Ari Sussman: #1 Environmental permit #2 Updated resource estimate #3 Updated PEA during the 2nd half of the year #4 Drilling of new targets which I think is a big catalyst assuming we make a discovery of course and #5 We plan to list our shares in Colombia on the exchange.

Scott Armstrong: What kind of operating leverage will Continental have to a rising gold price and what is your all-in cost range on the Buriticá Project?

Ari Sussman: In our PEA we published costs, we didn’t do all-in sustaining costs because we don’t know all the variables yet. But total cash costs amounted to $389/oz for the first 5 years and about $415/oz over the life of the mine, these are lowest quartile numbers.

Scott Armstrong: Could you update us a bit on the security situation in Colombia?

Ari Sussman: Current estimates are that about 80% of the rural countryside in Colombia is safe to operate. There are some security hot spots left but these locations are generally well known and are away from more heavily populated areas. The main point with respect to security is that the statistics have been improving for years, in contrast to other countries in Latin America which are heading in the opposite direction.

Scott Armstrong: Are there any other juniors in Colombia which have caught your eye recently?

Ari Sussman: There are two. One is Red Eagle (RD.V) which is going through the permitting process as well and expects to complete permitting their proposed small gold mine at approximately the same time as Continental on roughly the same time schedule as for a proposed small gold mine at roughly the same timeline as Continental. Also, I want to mention Cordoba Minerals (CDB.V) of which Continental is a shareholder of and I represent it’s interest as Chairman of the Board. Córdoba has locked up a large land package covering a new porphyry belt in an area of excellent infrastructure. The Company made a grassroots discovery last year with some fantastic drill results including a hole at over 100 meters averaging well over 1% copper equivalent. This is a great early stage opportunity with a beaten up share price, there lots and lots of targets here if you are comfortable investing at an early stage.

Thank you for your time Ari and we look forward to following Continental Gold closely over the coming years as you move the Buriticá Project forward to production. Best of luck in 2015 to you and Continental!

Scott Armstrong of EnergyandGold.com, Guest Contributor to MiningFeeds.com

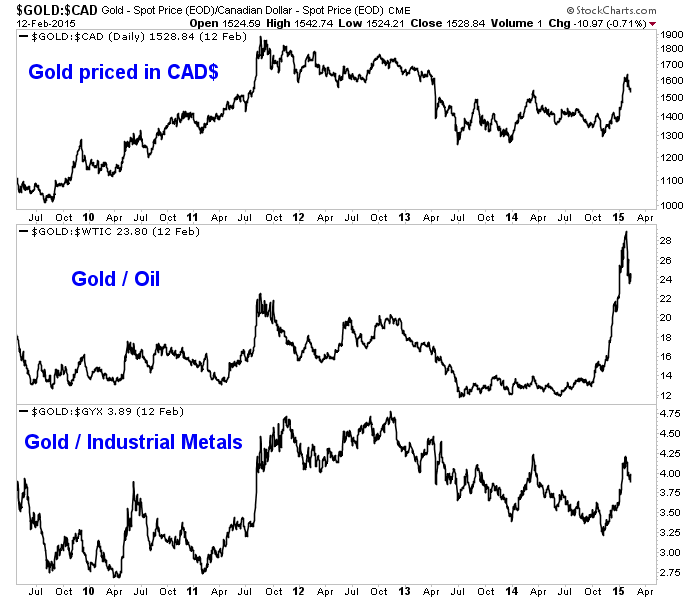

For the most part positive fundamentals (for gold mining companies) refers to rising Gold prices. However, this neglects the things under the surface which can affect margins as much as headline prices and in some cases more.

In the chart below we plot Gold priced in Canadian Dollars, Gold against Oil and Gold against Industrial Metals. Before we get to the chart let me explain why these ratios are important. First, the vast majority of gold mining firms are headquartered in Canada. The loonie is their local currency. The Canadian Gold price for firms that operate mines in Canada or explore in Canada can be more important than the US$ Gold price because their costs are in Canadian Dollars and not US$’s. Thus, a weak loonie rather than a weak US$ is a benefit.

Second, the Gold/Oil ratio is important because energy costs can account for 25% of a miner’s costs. Mining is an extremely energy intensive activity.

The chart below shows that the Gold price in Canada has surged while the Gold/Oil ratio has exploded. We also plot Gold against Industrial Metals as a proxy for other industrial related mining costs. That ratio has increased materially in favor of Gold but not to the degree of the other ratios.

As evidenced by GDX, the miners formed a strong double bottom and rebounded to the 400-day moving average which is key bear market resistance. The miners did not have that type of support at other lows (such as in June 2013 and December 2013). Moreover, the miners did not have improving margins thanks to plunging energy prices and a much weaker local currency.

The miners have made progress in recent months but the bear market won’t be over until GDX can clear its 400-day moving average. The good news is the miners formed a bullish double bottom after reaching arguably their second most oversold point (from a long-term sense) in the last 70 years. That was followed by the positive developments discussed above and word that the likes of Jeff Gundlach and Jim Rogers became investors in the sector. A new bull market lies ahead sooner rather than later but investors and traders need to maintain their discipline and patience.

North Arrow Minerals (NAR.V) is a promising diamond exploration company with a portfolio of projects in Northern Canada.

The company has extremely successful backers in the diamond industry, with Gren Thomas serving as Chairman, and his daughter Eira Thomas acting as an advisor to North Arrow. The Thomas’s led the Diavik diamond discovery in the early 1990s. Additionally, world renowned natural resources developers, the Lundin Group, led by patriarch Lukas Lundin, are major shareholders in the junior company. Mr. Lundin is coming off a big success building the Karowe diamond mine in Botswana with his Lucara Diamond Corp, and has been looking for assets to expand the company.

North Arrow’s highest priority project, Qilalugaq in Nunavut, is currently undergoing a bulk sample and diamond value, with results expected in the next quarter that could be transformational for the small company.

North Arrow’s second highest priority project, Pikoo in Saskatchewan, is a bonafide diamond discovery of its own.In 2013, the company drilled 2000 meters at Pikoo, hitting kimberlite in 9 of 10 holes, and finding significant quantities of commercial sized diamonds (news release here). These were some of the most promising initial diamond results in the history Canada’s diamond business.

“It’s a really good start,” CEO Ken Armstrong said during a December 2014 interview. “Textbook really.”

The company spent 2014 conducting two till sampling campaigns at Pikoo, generating 2-6 distinct new targets at the head of kimberlite indicator mineral trains.

Earlier this week, North Arrow commenced a 3000 meter drill program at Pikoo. The program will test some of the new targets, and continue to test the area around the 2013 discovery, known as PK-150.

If drilling hits kimberlite, samples will be then tested for diamonds. Results are expected throughout the Spring.

North Arrow shares hardly traded this week, which goes to show just how dead Canada’s mining markets are.

I am a shareholder in the company and have been covering it in our Resource Opportunities newsletter ($299/yr), and they are a sponsor of our upcoming Subscriber Investment Summit in Toronto on February 28, 2015. There are just a few spots left and we urge loyal CEO.ca readers to attend (Registration link).

Here’s a link to this week’s news release: North Arrow Drilling Program Underway at Pikoo, Saskatchewan

Sign up at North Arrow’s site to be first to hear of the results and keep your eyes on the company this Spring.

This is not intended to be investment advice of any kind and readers are strongly encouraged to do their own due diligence and consult a professional investment advisor before making any investment decision. This article and video contains “forward-looking statements” including but not limited to statements with respect to North Arrow’s plans, the estimation of a mineral resource and the success of exploration activities. Forward-looking statements, while based on management’s best estimates and assumptions, are subject to risks and uncertainties that may cause actual results to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: risks related to the successful integration of acquisitions; risks related to general economic and market conditions; closing of financing; the timing and content of upcoming work programs; actual results of proposed exploration activities; possible variations in mineral resources or grade; failure of plant, equipment or processes to operate as anticipated; accidents, labour disputes, title disputes, claims and limitations on insurance coverage and other risks of the mining industry; changes in national and local government regulation of mining operations, tax rules and regulations. Although North Arrow has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Always do your own due diligence.

Note, the opinions contained in this article are entirely my own. I am not an insider of Falco Resources, nor am I in possession of any non-public information. The information contained herein was obtained by reading company press releases, the February, 2015 corporate presentation and an informative video clip of CEO Trent Mell.

Impressive De-risking and Growth Announced by Falco Resources

On February 10th, Falco Resources (FPC.V) & (FPRGF) provided a road map for 2015. Not only is the company advancing its work on its flagship Horne Au-Ag-Cu-Zn project in Quebec, it has officially announced an aggressive drilling campaign with a budget of $3.7 million. The Horne Project area encompasses the former producing Horne and Quemont mines as well as the Horne 5 deposit. The Horne mine was operated by Noranda from 1927 to 1976 and produced 11.6 million ounces of gold and 2.5 billion pounds of copper. The Quemont mine is located 600 metres north of Horne and produced approximately 2 million ounces of gold and 400 million pounds of copper between 1949 and 1971. The Horne 5 deposit lies immediately below the historical Horne mine.

Together, Horne and Horne 5 share many similarities to Agnico-Eagle’s La Ronde mine located 40 kilometres to the east. Those orebodies are dynamic multi-metallic systems that remain open, plunging steeply to depth for several kilometers. How many juniors can one name spending $3.7 million on drilling alone? By the time initial metallurgy results come back at mid-year, a lot of juniors could be out of business, unable to afford the annual audit fees. Last I checked, auditors don’t accept shares in the companies they audit. Recall from prior articles I’ve written [Here] & [Here] that Falco essentially inherited a 2.8 million gold equivalent Inferred resource due to an extensive database containing roughly 80 years of Noranda’s exploration, development and production records on 14 past-producing mines.

Up to 5 Million Gold Equivalent Ounces by Year-End Could be a Game-Changer

This Inferred resource was delineated without a single drill hole by Falco and supports management’s ambitious plans to book up to 5 million gold equivalent ounces in the NI 43-101 categories of Indicated & Inferred in the 4th quarter. A takeaway from the February 10th press release is a reminder that the company is fully funded through 2015. Even if one does not actively support a takeout thesis, the value creation and de-risking from achieving 2015’s stated corporate initiatives could be a meaningful catalyst for the stock price. Comparing Falco’s exploration project to that of neighboring mines, 2 out of 3 analog mines (Agnico-Eagle’s Goldex and AuRico’s Young Davidson) have considerably lower ore grades and less than Flaco’s projected 5 million ounces of gold equivalent resources.

Although there was no groundbreaking news in Falco’s corporate update, I believe that it’s not only helpful for investors, but also for prospective acquirers of Falco. The initial results of metallurgy testing to establish recoveries for Au, Ag, Cu, and Zn due by mid-year, could be as important a catalyst as the next NI 43-101 resource update. Why? Because potential suitors need to check off a number of boxes before they get really interested. Some of those boxes may already have been checked, most notably that the company’s property being in an excellent jurisdiction with substantial access to infrastructure / labor and Falco having tremendous exploration upside outside the Horne land holdings.

Prospective Suitors Most Likely Watching Falco Very Closely