The following interview of Gold Resource Corp.’s (GORO) CEO Jason Reid, CEO President & Director was conducted by phone and email on March 26-27. The company is unique in that it pays a monthly dividend in cash or in physical gold or sliver. The shares currently yield about 4% annually. The company has no debt and tens of millions in cash on the balance sheet, covering the current annual dividend by a ratio of 4 to 1. Mr. Reid believes that GORO is a true success story in an otherwise difficult gold & silver market. Please read this informative interview to learn more.

Can you please give readers an overview of Gold Resource Corp. (GORO)?

Gold Resource Corporation “GRC” (Ticker: GORO) is a gold & silver producer targeting projects featuring low costs and high returns on capital. The Company’s primarily focus is on cash flow, with a history of meaningful monthly dividends. The Company’s “Oaxaca Mining Unit” consists of 100% interest in 6 potential high-grade gold & silver properties in the State of Oaxaca, Mexico. The Company established its, “Nevada Mining Unit” exploration campaign in September, 2014.

GRC declared commercial production July 1, 2010 from a shallow, high-grade open pit at its El Aguila project, enabling GRC to reach production & cash flow rapidly, thereby allowing for a tight capital structure for a producer. In March of 2011, GRC announced production from its polymetallic La Arista vein system. The Arista deposit contains high-grade gold, silver, copper, lead and zinc The Arista deposit is open along strike and at depth. The Company targets extensions of this deposit and is exploring its Oaxaca and Nevada Mining Units to increase production over time.

Please describe your current capital structure.

GRC has one of the tightest capital structures of any gold producer. In an industry where 200-500 million shares outstanding is not unusual, GRC has just 54 million. Having a tight capital structure enables GRC to distribute a monthly dividend, increasingly rare in our industry. Our dividend yield, near 4%, equals or exceeds that of the Majors. Our dividend reminds investors that management has fiscal discipline, a shareholder friendly philosophy. Rest assured, management does not issue debt or shares to pay its dividend or for operations. Our capital structure is not happenstance, but a concerted effort from day one.

Let’s get this question out of the way…what would it take for GRC to raise its monthly dividend in 2015?

GRC’s current monthly dividend is $0.01 per share. When gold and silver prices were in a bull market back in 2011 and early 2012 our monthly dividend grew to $0.06 per share. As metal prices are in a bear market, our dividend has pulled back as a function of less cash flow with which to distribute. When metals prices pick back up, cash flow permitting, we want to increase the dividend. Having said that, we make no guarantees regarding the dividend.

We have a track record that has enabled us to distribute over $103 million to our shareholders since commercial production began in July, 2010. Our “IPO” in 2006 was at $1.00 per share and we have returned ~$1.95 per share. We are very proud of this achievement, let alone for a junior company in the mining space. We have taken GRC’s dividend a step beyond other companies by offering shareholders the ability to convert their cash dividend into .999 fine gold and/or .999 fine silver GRC one-ounce rounds and take physical delivery of those rounds.

In reading through transcripts of a number of Gold Resource Corp’s conference calls, there appears to be reasons other than the gold price that have hurt your share price. Things like water issues, CO2 issues, a lawsuit, a management shake-up, missing production targets and higher costs than expected. Are these issues behind the company now?

The mining industry has challenges irrespective of the recent gold and silver price collapse. There are challenges we can expect and plan for and those that we cannot. When dealing with Mother Nature one creates the best business plan one can, assembles the best team and works hard to achieve Company goals in the safest possible work environment for our employees. As an underground miner operating below the water table, we have to deal with groundwater. We have had challenges at times with excess groundwater that slowed our mine development.

Dealing with unexpected water inflows takes more time and money than one might expect, resulting in less production and missed targets. However, we have also had our share of successes along the way. I can assure you that we pay close attention to this issue and have a handle on it. Water will always be a concern at our Arista Mine and additional pump stations are an integral part of our development plans.

We have also experienced CO2 gas issues in some of our deeper development levels. CO2 gas is not out of the ordinary for an underground miner, but does require additional planning. Development slows when installation of additional ventilation, hinders development time and costs are temporarily higher. We try to plan for it, but not every level or area has CO2 gas, so we deal with it as needed. Our costs vary, but we have been in the low cost peer group over the long term. The last two years, we have focused on cost cutting and we have had success. We continue to evaluate additional opportunities to lower costs.

The Company defended itself against a securities class action lawsuit. We are optimistic that we are close to a resolution. The district court ruling was appealed to the 10th Circuit Court of Appeals, where that court upheld the original decision to dismiss the case. We await any decision by the securities class action case to further appeal the ruling. Once those appeal deadlines pass without further action, the securities class action will be terminated.

Do you have a better understanding of the risks facing Gold Resource Corp today?

Yes. That’s a key takeaway. We think we are better positioned to attack and resolve challenges as they arise. Each mine is different and has unique challenges. The shape and grade of the ore body, metallurgy, rock competency, infrastructure, water, gas and personnel. At the beginning a game plan is set to address all these issues, but as with any business that game plan evolves over time when the business plan meets the reality of operations.

For the fourth quarter of 2014, you released preliminary results that indicated Gold Resource Corp. missed production guidance. Please explain what happened.

We had a great 2014 despite a difficult third quarter with lower than targeted production and an on-site managerial change. We bounced back in the fourth quarter and GRC produced record amounts of both gold and silver. The industry, and GRC, reference a precious metal gold equivalent production total which takes the silver we produce, converts that into a dollar value based on market prices, then converts that dollar value back into gold ounces for a combined number of precious metal gold equivalent ounces. It is a quick way to calculate production using a silver to gold ratio.

The equation hurts production totals when metal market prices fall like they did during the third and fourth quarter as the aforementioned ratio worked against the gold equivalent total. That took place during 2014 as we lost several thousand gold equivalent ounces to the metal price drop. Had the metals not fallen we would have reached the low end of our annual production range even with our tough operational third quarter.

How important were the drill results that went out in your January 27th press release? Roughly how much would it cost to bring Switchback into production, and how many years might it take?

The market gives little credit to good news, while severely punishing bad news. The Switchback news is an example of good news ignored. 500 meters from our largest deposit, our producing Arista mine, we discovered multiple high-grade veins at Switchback in what is either an extension of the Arista deposit or its own significant deposit. This could be very important. We are developing a preliminary mine plan for Switchback to get a handle on costs. It’s too early to give a time frame, but we have a history of advancing projects faster than most. If warranted, we plan to advance Switchback in a similar manner. Operating cash and capital permitting, we would like to advance development at Switchback by year end.

After all drilling, exploration, development, maintenance cap-ex….everything, are you free cash flow positive at $1,200/oz gold? (including your base metal credits)

Our all-in sustaining cash cost per ounce was $1,073 for 2014. We had approximately 6,500 ounces of gold concentrate waiting to be processed into dore at year end. Had we been able to sell those ounces, our all-in sustaining costs would have been under $1,000. We remain among the low cost peer group by anyone’s measure, reflected in our profitability for the last three years during the metal prices collapse. Reporting of costs has been difficult for the industry. It has struggled for years to establish uniform cost metrics.

Every mine has unique characteristics which don’t always fit into a uniform cost metric, like the World Gold Council’s all-in sustaining cash paradigm. Cost metrics and cost are very important, but of greater importance is the question does the company make money? I was on a non-deal road show several years back when a fund manager made the following comment regarding low cost producers saying “I have met many low-cost producers that don’t make any money.” That statement stuck with me and I am pleased to be able to say that not only do we make money, but we continue to pay a monthly dividend. That speaks to our potential when metal prices rebound.

With the gold & silver price depressed, is the contribution from lead, copper and zinc more important? Do those base metals alter your thinking of how to proceed?

Yes. We are focusing primarily on margin as opposed to ounces, and that is reflected in our recent proven & probable reserve report as well as in our 2015 mine plan. We applied a $110 per tonne Net Smelter Return “NSR” break even criteria of all metals, precious and base, in the block model for the reserve report this year. Our production goals and production totals will retain a precious metal gold equivalent, while using base metals as by-product credits. What changes is that the NSR approach focuses on exploiting the Arista’s polymetallic (gold, silver, copper, lead and zinc) deposit, as opposed to our past focus where we targeted gold and silver using a precious metal cutoff grade and then processed whatever base metals happened to be present.

The former approach focusing only on mining precious metals was adequate when metal prices were much higher, but during the current declining metals market the NSR approach aims to extract the greatest dollar value of all metals from each tonne mined. During this volatile metal market we are focused primarily on margin, high-quality ounces, as opposed to chasing ounces and leaving behind valuable metals that make money. We care more about making money and less about the number of ounces we produce.

Management is excited about the prospects for Switchback. However, with the dividend at $0.01, is that a signal that there’s not enough cash flow to support efforts at Switchback and cap-ex at the existing mine?

The dividend is payed after project cap-ex, taxes and exploration. We achieved our entire 2013 mill expansion with our cash flow while still distributing a dividend. While we make no guarantees, we target a similar situation with additional development and cap-ex spending at switchback.

Would Switchback represent a second mine, i.e. distinct from your existing mine, thereby de-risking the overall company?

Switchback would most likely be developed by leveraging the existing depth of the Arista mine development. By doing so, we could potentially advance Switchback much faster and at less cost. However, it would likely leverage Arista’s advancement so it would not be entirely distinct.

If Gold Resource Corp. reached a point where additional capital was needed, would you consider utilizing a moderate amount of debt to mitigate the size of a possible equity raise? What about JV’s or Farm-Outs?

We fought tooth and nail to achieve our tight capital structure. Our goal is to continue development using cash flow from operations as we have for many years. If additional capital is warranted, we would consider equity raises or a combination of cash and equity. We are not fans of debt, hence our zero long term debt status. JV’s and farm-outs don’t excite us much. We are open minded to all options and plan to make decisions based on the best interests of our shareholders. If a deal is accretive and makes good business sense we would take a hard look at it.

Are there any misconceptions about Gold Resource Corp. that you would like to address?

There were many misconceptions around GRC going into production and being in production for years without a formal reserve report. We had internal estimates to justify our decisions, but to advance a project based on that drew staunch criticism. Looking back, by doing so we reached production sooner and diluted our shareholders far less. Though criticism and second guessing surrounded this move early on, we now have one of the tightest capital structures to show for it and we can use that to our advantage.

I think many misconceptions are driven from the that fact we are very different in the mining industry and some assume that is a bad thing. We look at mining as a business and are out to make money. We do make money. This is in contrast to peers that rely on continued equity raises and rolling over debt to stay alive. GRC has zero long term debt. What used to be misconception and criticism is turning into a meaningful positive for the Company.

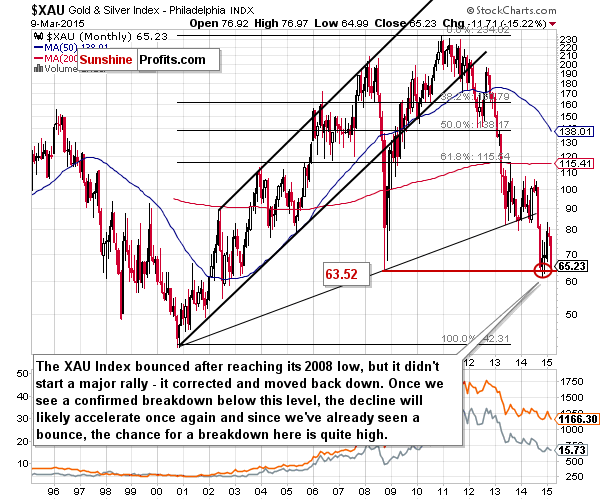

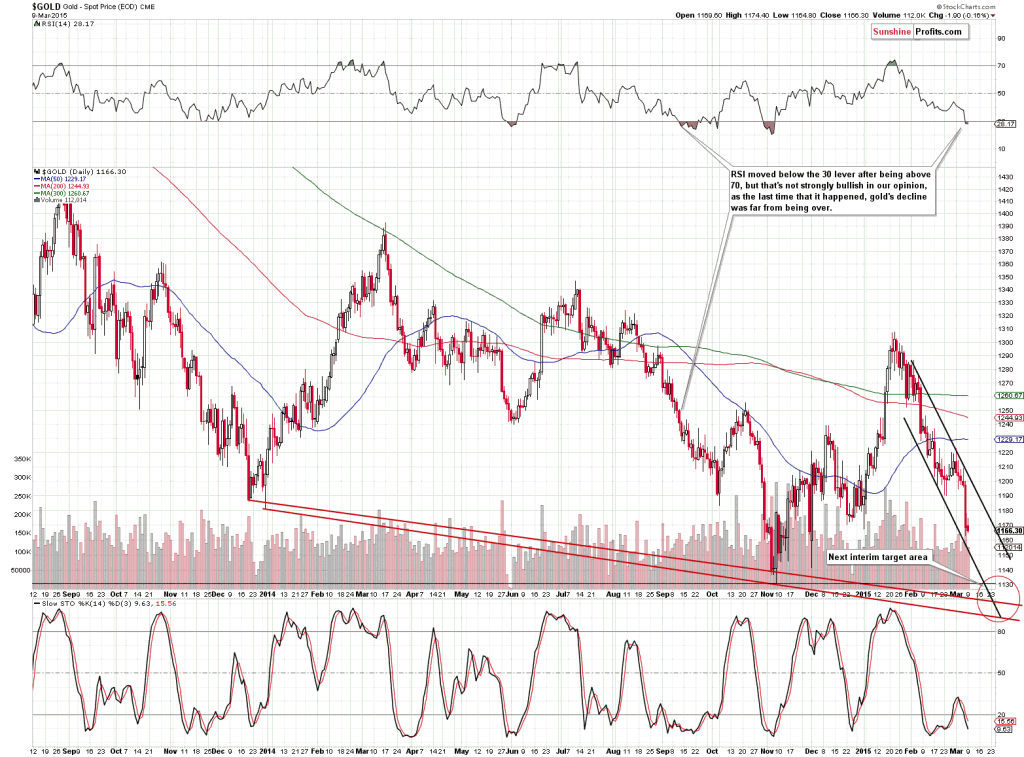

The precious metals complex has established a floor of support over the past five months. For Gold it is around $1150/oz and for Silver it is around $15.50/oz. Pick any miner index and you’ll see the support at the November and December lows. These lows could mark a base of support from which a new bull market takes hold. On the other hand, they could also mark support that if broken could lead to a final but nasty capitulation.

Below is a weekly candle chart of Gold and Silver. Support for Gold is now well defined around $1150. There is major resistance at $1220-$1240 as well as $1300. Meanwhile, Silver has support around $15.50 with resistance at $17.50 to $18.50. If the metals can takeout their January highs then they would definitely be in a new bull market. Conversely, if metals takeout their March lows to the downside, then it could mark the final breakdown of the bear market.

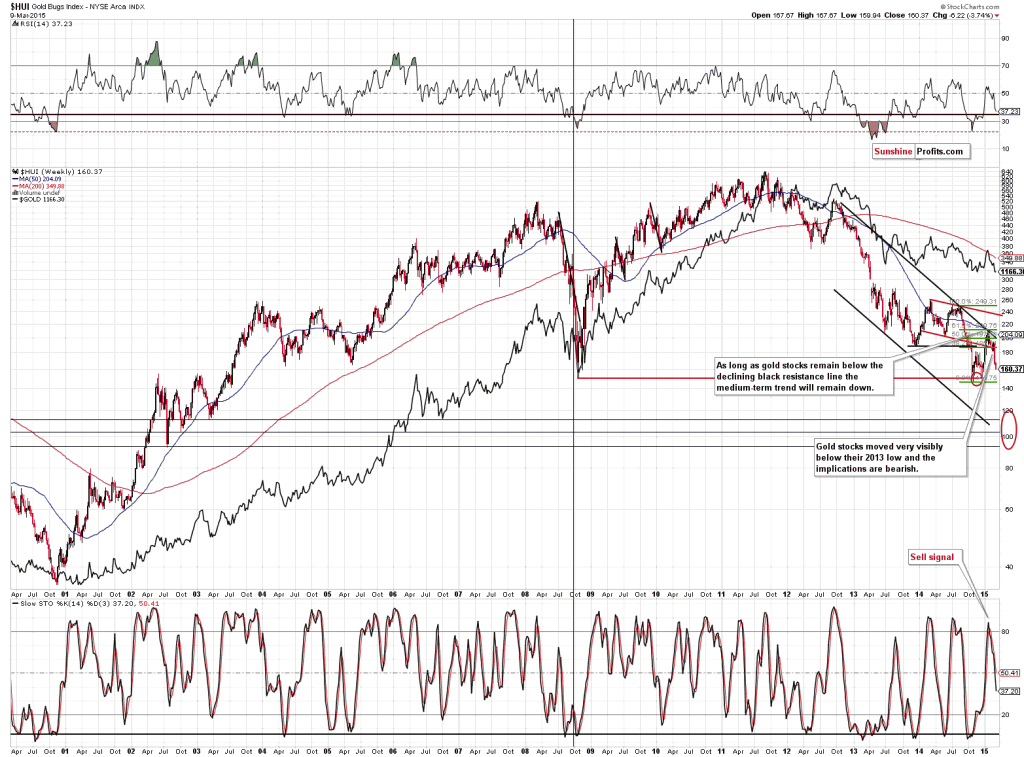

The miners are now showing relative weakness as they are down for the week while the metals are up. The HUI closed the week at 166. It failed to reach first resistance at 180, though it still could. The HUI has a confluence of strong resistance just above 200 with strong weekly support around 155. A weekly close below 155 could trigger a final breakdown while a surge above 200 would signal a new bull market.

I do see some fundamental positives for precious metals. Real rates and real yields may be headed lower in the future. Yields are declining and Fed hikes could be put off again. Inflation, ex energy seems to be slowly ticking up. Meanwhile, problems in Greece could boost Gold even in US$ terms. Any trouble in US equities could certainly be a catalyst for precious metals.

This being said, we need to respect the charts which can be considered bearish until precious metals take out higher levels or until they breakdown and become extremely oversold. I’m leaning to the latter scenario. Protect yourself and your portfolio so you can benefit from a final breakdown. In that scenario, technical indicators and sentiment indicators would reach major extremes as diehard bulls are forced to capitulate. Those are the conditions for great buying opportunities that can lead to a bear market bottom.

Silver reversed sharply higher over the past week or so, surging dramatically. This was just after it had successfully retested major secular lows, ramping the odds this strong buying is the vanguard of a long-overdue major new upleg. As usual, silver’s coming gains will be fueled by gold’s own advance. As the yellow metal mean reverts higher initially on heavy futures short covering, capital will flock back to silver.

Silver is a fascinating market. It’s undeniably primarily an industrial metal, as the latest annual data from the world’s leading authority on silver supply and demand shows. The venerable Silver Institute reports that fully 54% of global silver demand in 2013, and 62% in 2012, was for industrial fabrication. In those same years, worldwide investment demand (coins, bars, ETFs) accounted for just 23% and 20% respectively.

Nevertheless, for millennia silver has also attracted investors as a precious metal and governments as a hard currency. From time to time silver captivates investors again, and they flood into this relatively tiny market and bid silver prices sharply higher. These large investment-demand spikes quickly overwhelm the normally-dominant industrial demand, which is naturally slow to change. So silver is catapulted higher.

The magnitude of these investment-driven silver surges can be enormous, multiplying fortunes rapidly. The greatest ones are the stuff of legend, and have left silver with something of a cult following. This volatile metal is always being watched by contrarian investors, who are ready to return when it starts running again. And there is a single overwhelmingly-dominant catalyst that brings investors running back.

The price of gold. Almost without exception, all of silver’s biggest and strongest spikes, uplegs, and bull markets in modern history have been fueled by parallel gold rallies. From an investment perspective, silver is ultimately just a leveraged play on gold. If you want to mischievously provoke hardcore silver zealots, call silver “gold’s little lapdog”. Silver investment demand is almost totally dependent on gold’s fortunes.

The historical data proves this in spades, it is unassailable. Gold drives silver, full stop. Silver prices are super-highly-correlated with gold prices over any reasonable period of time. Silver’s rallies, uplegs, and bull markets correspond almost exactly with gold’s rallies, uplegs, and bull markets. Investors return to silver when gold is strong, and abandon silver when gold is weak. Gold is the key to silver investment demand.

This is true even over the past couple years, which have been extraordinarily anomalous. Way back in late 2012, the US Federal Reserve launched its wildly-unprecedented open-ended third quantitative-easing campaign. Nothing like QE3 had ever happened before, and it along with high Fed officials’ associating jawboning epically distorted the stock markets. QE3 is what drove the past couple years’ levitation.

The Fed’s direct QE3 Treasury monetizing held interest rates artificially low. This enabled corporations to borrow over a trillion dollars very cheaply, which they used to buy back their own stocks. These vast buybacks greatly boosted the broader stocks markets. Meanwhile, the Fed kept implying to stock traders that it was backstopping these anomalous markets, ready to ramp up QE3’s size to arrest any material selloff.

Thus the Fed’s QE3 campaign radically altered investor sentiment and capital flows. Everyone wanted to buy high in overvalued, overextended, and euphoric stock markets. The Fed hypnotized traders into believing stock markets only rise, that there was no significant downside risk. And as stocks surged, demand for alternative investments that move contrary to stock markets like gold and silver collapsed.

Since nothing like QE3 had ever happened before, the resulting bear-market slide in precious-metals prices is also largely unparalleled. This first chart looks at silver and gold prices over the past couple years or so, the era of the Fed’s QE3 stock-market levitation. And even in one of the most extreme and artificial environments imaginable for silver investment demand, silver prices still mirrored gold’s nearly perfectly.

Statisticians measure data correlations through a construct known as the coefficient of determination. It’s also called R squared, because it is calculated by multiplying the correlation coefficient, symbolized as R, by itself. I bastardize this to r-square, as it flows better in writing. R-square effectively reveals how much movement in one dataset is directly mathematically related to movement in another dataset.

Since the dawn of 2013 when the Fed’s epic QE3 anomaly got underway, silver and gold have had a correlation r-square of 94.7%! That means nearly 95% of silver’s daily price action is directly explainable by gold’s daily price action, or vice versa. And there’s zero doubt about the direction of causality, gold is driving silver and not the other way around. This truth isn’t evident in a chart, it comes from experience.

I’ve been investing for decades, but have spent the last 15 years or so intensely focused as a dedicated student of the markets. In addition to endless research, data-crunching, and writing, a critical part of this is watching the markets all day everyday. When you spend all those years observing how prices react in real-time, causality becomes readily apparent. While many things move gold prices, only one really moves silver.

Like silver, gold prices are affected by shifting sentiment that alters investment and speculation demand. Major catalysts for this range from stock-market fortunes, to how the US dollar is faring, to releases of major US economic data, to a wide range of publications and comments by the Federal Reserve and its officials. The large gold market moves first when sentiment shifts, then the small silver market follows.

This reaction is usually rapid, happening within minutes when gold moves significantly. And as long as that gold trend lasts, hours, days, weeks, months, even years, silver tends to mirror and amplify gold’s price action. Silver surges when gold is strong, and slumps when gold is weak. In a very real sense, silver is a gold sentiment gauge. Investors and speculators only flood into it when they are bullish on gold.

When gold plummeted in the second quarter of 2013 first on panic selling as major multi-year support failed then later on the Fed’s QE3-taper scare, silver plummeted with it. When gold surged sharply on heavy short covering in the third quarter of 2013, silver surged right along with it. This decades-old trading pattern continued last year, silver dutifully rallying with gold and selling off with gold like always.

Whether you look at the past couple years or four decades, gold fuels silver. And within the Fed’s extreme QE3 anomaly since early 2013, which is starting to unwind, almost 95% of silver’s daily price action was directly explainable by gold’s own. This is stunning, as it necessarily means everything else is in the remaining 5%! Just think of the endless commentaries written on silver, ex-gold they’re barely material.

Because of gold price action’s overwhelmingly-dominant impact on silver sentiment among investors and speculators, gold trumps everything else silver-related. This includes worldwide silver supply-and-demand fundamentals, silver technicals, even silver conspiracy theories. If you want to multiply your capital in silver by buying it low then later selling it high, all that really matters is what gold is going to do.

Back in early November 2014, silver collapsed to a brutal 4.7-year low of $15.37. The Fed’s crazy stock-market levitation had gutted demand for all alternative investments, they were starving for capital and rotting into oblivion. Then just a couple weeks ago, silver slumped again to $15.48. This was less than 1% above that secular low. But silver’s low retest proved successful thanks to gold’s subsequent sharp surge.

In these grossly-distorted markets of the past couple years, the lion’s share of big moves have been driven by the Fed. Its Federal Open Market Committee that manipulates interest rates and prints money meets 8 times a year, and its latest decision was just released on March 18th. And again the Yellen Fed pulled out all the stops to portray itself as dovish, signaling that rate hikes were likely to be delayed and gradual.

The US dollar, which had been rocketing parabolic on rate-hike hopes, collapsed on that. This helped ignite a sharp gold rally as futures speculators scrambled to cover extreme shorts. And naturally as gold surged, silver joined it. Over four trading days starting on that FOMC meeting, gold powered 3.7% higher which silver really amplified to a big 9.8% gain. And I suspect that gold-fueled silver buying is only beginning.

With the Fed’s stock-market levitation seducing investors away, the gold price action in the past couple years has been totally dominated by American futures speculators. When they sell aggressively, gold tanks. When they buy aggressively, gold surges. And since their selling has been so extreme in the past couple of months, they have big near-term buying left to do which will catapult gold and therefore silver higher.

This next chart looks at American speculators’ total positions in gold-futures contracts, both long-side bullish bets and short-side bearish ones. This data is published once a week by the CFTC in its famous Commitments of Traders reports. The latest read before this essay was published reflected these bets as of Tuesday March 17th. And boy were they bullish for gold, which portends a major parallel silver rally.

After its deep early-November secular low, gold was doing really well heading into early 2015. By late January it had powered 14.2% higher to $1303. But then for reasons including the surging US stock markets and US dollar, American futures speculators started to aggressively dump gold. This is readily apparent in this chart, in the recent sharp drop in long-side contracts and sharp rise in short-side ones.

Between late January and this latest CoT report, this single group of traders liquidated an astounding 79.4k long-side contracts. Since each contract controls 100 ounces of gold, this is equivalent to 247.0 metric tons! That is far too much gold supply too quickly for normal gold investment demand to absorb, so gold prices started crumbling. This heavy selling forced speculators’ total bullish bets back under support.

And futures speculators also simultaneously piled on to the short side, exacerbating gold’s sharp selloff. Between early February and this latest CoT report, they sold short 75.8k contracts! They were effectively borrowing gold they didn’t have, dumping it into the market, and hoping to buy it back later at some lower price to repay their debts. This extreme shorting added the equivalent of another 235.8t of gold supply.

Add that up, and in just 6 to 7 weeks American futures speculators alone spewed an astounding 482.9t of gold into the markets! It’s actually an incredible testimony to the strength of latent gold investment demand that this metal didn’t just collapse under such a brutal onslaught. According to the World Gold Council, in all of 2014 global gold investment demand ran 904.6t. Over half of that supplied in weeks is staggering.

Gold only fell 11.8% on that deluge of futures supply, and silver was very resilient with a mere 15.2% loss of its own. Usually silver really leverages gold’s downside too. Silver is looking so bullish today because this extreme gold-futures selling is reversing into buying. We’ve already seen that start since that latest FOMC meeting, which happened to come the very next day after this latest CoT positions data.

The ironic thing about futures speculators, who are considered very sophisticated traders, is they are terribly wrong as a herd at extremes. They are the most bearish right as prices are low and bottoming, as evidenced by high short positions and low long positions. This chart highlights short peaks in red, and all of them occurred when gold was in the process of bottoming right before a major new rally got underway.

While futures speculators have no obligation to reestablish long positions, they are legally required to cover their shorts. The past couple months’ big gold-futures shorting binge was one of the most extreme ever witnessed from a variety of metrics. That left speculators with a whopping 146.2k gold-futures contracts they had borrowed and sold, one of the highest levels in history. These must soon be reversed.

Futures speculation is a radically-riskier endeavor than stock trading. Not only is it a zero-sum game where every dollar won is a direct dollar lost by an opposing trader, but the leverage available is far beyond extreme. The maintenance margin for a single gold-futures contract controlling 100 ounces of gold worth $120,000 at $1200 is merely $4000. That means traders’ leverage can run as high as 30 to 1!

30x leverage is terrifying, as a mere 3.3% move against a futures bet supported by minimum margin will wipe out 100% of a trader’s capital risked. In the stock markets, leverage has been legally limited to just 2x since 1974. Whenever gold started rallying again, which happened in spades after that latest FOMC meeting, these futures speculators would be forced to cover or face catastrophic losses of their capital.

The only way to cover futures shorts is to buy offsetting long contracts to close them. The upside price impact of adding new longs and buying longs to cover shorts is identical. So all the extreme gold-futures short selling of recent months would soon reverse into major buying. And given how high speculators’ total short bets were, the subsequent buying was guaranteed to be big. This chart helps understand why.

The Fed’s anomalous stock-market levitation sparked such extreme short selling that gold suffered its worst quarter in 93 years in Q2’13! Those initial lows around $1200 have essentially held in all of the subsequent speculator gold-futures shorting spikes since. After each shorting binge, speculators were quick to cover and push their bearish bets back down to support. That’s where their exposure wasn’t excessive.

Today that speculator short-position support line is around 60k contracts, or 75k if you want to consider support in horizontal terms. Merely to return to these normal levels, American speculators will have to buy to cover either 86.2k or 71.2k contracts in a matter of weeks to months on the outside. This is the equivalent of 268.2t or 221.5t of gold, both enormous amounts! This will certainly catapult gold sharply higher.

Now remember the latest CoT data by the time this essay was published was as of the afternoon before that latest FOMC meeting ignited this inevitable gold-futures short covering. So some fraction of this has already happened. But we’re only a week into a process that has generally taken a couple months to unfold after the other major shorting peaks of the past couple years. So this gold-futures buying is far from over.

Gold rallied pretty dramatically in the past short-covering frenzies, despite still facing howling headwinds in the form of the levitating US stock markets and the US dollar shooting parabolic. As this latest short-covering episode gets underway, these are shifting to tailwinds as the euphoric US stock markets and US dollar weaken. So this next gold rally initially sparked by futures short covering is likely to grow much larger.

Not only will other futures speculators pile in to chase gold’s upside with new long-side bets, but legions of investors will return via gold ETFs and physical bullion. And as gold powers higher, silver is going to leverage its gains like usual. The first chart illustrated that silver is super-highly-correlated with gold, and mirrors and amplifies its moves. And the second one shows that gold is in for a major short-covering rally.

So with big gold buying fueling silver, the white metal is likely early on in its next major upleg. Investors and speculators alike can capitalize on silver’s next big move in several ways. They can go the traditional route and buy silver coins and bars. Stock traders can deploy capital in the silver ETFs to obtain the same portfolio exposure. These are led by the flagship iShares Silver Trust, which trades under the symbol SLV.

But silver itself and the silver ETFs will merely pace silver’s advance at best. Traders looking to leverage silver’s next upleg can do it with the beaten-down silver stocks. Since silver has fallen so deeply out of favor, the stock prices of the best silver miners and explorers are absurdly cheap. They are discounting a nonsensical future where silver never materially rallies again. So when it does, they’re going to soar.

The bottom line is silver looks to be embarking on a major new upleg, as it just reversed sharply higher after a successful retest of major secular lows. This initial strong silver buying was fueled by major short covering in gold futures, a multi-month process that’s likely just getting underway. Silver sentiment has always been highly dependent on gold’s fortunes, since traders overwhelmingly focus on it to time silver moves.

Over the anomalous past couple years where markets were grossly distorted by the Fed, almost 95% of silver’s daily price action was directly explained by gold’s own. This gold dominance of silver will likely continue as the Fed starts normalizing policy, reversing the market extremes it spawned. So as the gold price mean reverts higher, investors and speculators will flood back into silver and ultimately catapult it to huge gains.

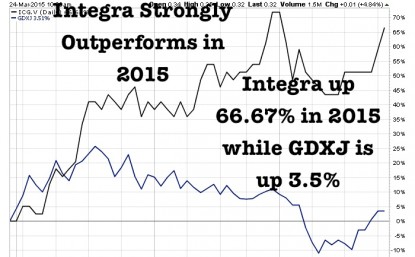

One junior gold miner that I have been very bullish on for many months is outperforming the GDXJ benchmark by a wide margin. Integra Gold (ICG.V or ICGQF) is up over 60% in 2015 alone outperforming the GDXJ by 50 percentage points. This is incredible relative strength and confirms my prediction that this is one of the premier junior gold mining companies on the entire exchange.

They are on the verge of a major 52 Week High breakout as they announce very impressive drill results. These results are significant as they confirm extensions of the Triangle Deposit and show that all zones remain open laterally and at depth. The results are exceptional and I expect more to come as there are eight drills turning on the property with five drills in the Triangle Zone. Look at these high grade results driving the share price to test 52 week highs.

– TM-15-01 (Zone T7) – 14.78 grams/tonne gold (“g/t Au”) over 2.0 metres (“m”)

– TM-15-02 (Zone T1) – 14.79 g/t Au over 10.0 m

– TM-15-05 (Zones T0 and T10) – 8.01 g/t Au over 4.5 m and 11.47 g/t Au over 8.0 m

– TM-15-06 (Zones T5, T10, and T11) – 7.00 g/t Au over 7.0 m, 5.19 g/t Au over 5.0 m and 11.78 g/t Au over 1.0 m; and

– TM-15-08 (Zone T10) – 15.55 g/t Au over 5.0 m

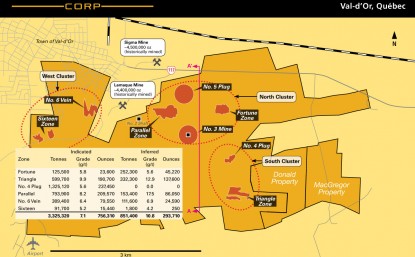

Integra recently announced an updated resource in early February which showed a major increase in the indicated category. Integra Gold (ICG.V or ICGQF) owns 100% of the Lamaque South Gold Project in Val-d’Or, Quebec and is currently drilling 50k meters with eight diamond drills.

If you know of a more active junior in a stable jurisdiction tell me. I can’t find another company as exciting as Integra. Integra recently made a bullish golden crossover of the 50 and 200 day moving average and is hitting new six month highs past $.325 as investors see the significant increase in resource at the highest grade target and the exploration upside on the project.

Integra is a unique junior as they own 100% of a project which has a low cap-ex and high grade returns in an area with a ton of M&A activity. Management has experience operating gold mines in Val D’or and advancing this project into production. It is a dream team of Quebec miners with decades of experience mining in Val D’or.

It appears that the technical team has shown wider zones at depth in the Triangle Zone increasing the overall grade and size of the resource. What is significant about this is that historically the most productive and profitable ore in the neighboring mines were in the lower zones.

This year Integra appears to be extending a number of holes at depths below 900m with up to eight core rigs drilling. I believe the majors are beginning to recognize the growth potential of this high grade gold project in mining friendly Quebec as long as the major institutional funds.

Integra recently appointed Charles Oliver to the board. Charles was the lead portfolio manager for Sprott and has decades of experience evaluating mining investments. He may be an excellent liaison for Integra to gain even further recognition among his network of financiers as they move toward production.

In addition, Integra just added Petra Decher from Franco Nevada to the board and Jacques Simoneau who was the exploration manager for Goldcorp at the Eleonore Mine in Quebec which grew to over 7 million ounces of gold.

Integra is making a bullish golden crossover of the 50 and 200 day and breaking new six month highs made in September of 2014. It could go into new 52 week highs at $.40 once drill results spread through the investment community.

I just interviewed Integra Chairman George Salamis who started his career in Val D’or with Placer Dome. He explains his history working in Quebec and the current technical team assembled to build value and take this asset to the next level. Listen to the interview by clicking here….

Disclosure: I am a shareholder of Integra and the company is a website sponsor. Please do your own due diligence!

1. On March 20, 2015, global gold price discovery changed. Transparency was introduced to the London gold market, as the new “LBMA Gold Price” was launched.

2. In my professional opinion, the changes in London are ushering in an entire new era of gold price stability, consistency, and transparency, and that will attract large money managers to this spectacular asset.

3. The tortoise always beats the hare. Allow me to elaborate: while net gains of $1 – $2 a day in the price of gold may seem boring, with roughly 250 trading days in a year, that can translate into price appreciation of $250 – $500.

4.When the Western fear trade dominated gold, the London gold price was set by shadowy figures making private telephone calls to each other. Volatility was huge, and many money managers used large bank loans to make leveraged bets on the price.

5. Now, the Eastern love trade is starting to overwhelm the fear trade. It’s a theme that will probably accelerate very dramatically in the second half of this year.

6. Also, the transparency in London will attract unleveraged money managers that take a very long term approach to their investments, with a focus on gold stocks.

7. Without the Eastern love trade, gold probably would trade in the $700 – $1000 area, if another financial crisis didn’t occur. That’s because Western fear traders simply don’t buy enough tonnage to overwhelm mine and scrap supply, except in the most extreme and temporary situations.

8. In contrast, the Eastern love trade should produce consistent 5% – 15% annual gold price appreciation, with very limited volatility, for decades to come. I expect to see gold stocks make a “stealth” change over the next 1 -2 years, from being the most hated asset class in the world, to one of the most respected.

9. Please click here now. That’s the daily chart for gold. There’s a strong possibility that an inverse head and shoulders bottom is forming now.

10. Gold may react a bit here in the $1190 area, because of minor trend sell-side HSR (horizontal support and resistance). After the pause/pullback, I expect the rally to continue. Gold should reach $1220, before another pause in the upside action occurs.

11. Please click here now. That’s the seasonal chart, courtesy of Dimitri Speck. Clearly, gold needs to be accumulated, on any short term weakness.

12. There’s more good news in the immediate term, for gold price enthusiasts. March 26 is option expiry day for the COMEX April gold contract. That’s just two days from now, and gold often tends to rally after the options expire.

13. I recently swapped some gold for silver. Silver is referred to as a “game” by many hedge fund managers, but I think they may need to reconsider the use of that moniker. That’s because the increased transparency in the London market applies to silver as well as gold.

14. Please click here now. That’s the daily chart for silver. There’s a great breakout in play, from a bull wedge pattern. Silver could reach the $18.50 area quite quickly, once the March 26 option expiry day is in the past. Traders should book decent profits in the $17.50 – $18.50 zone.

15. A lot of analysts believe that Chinese gold demand is much higher than is reported in the mainstream media. I think they may be looking at a tree, rather than the forest. Here’s why:

16. The London gold market needed to be overhauled, and it was, but Shanghai also lacks transparency. A new “Shanghai Gold Fix” should be operational before this year ends, and I expect it to feature the same transparency that now exists in London.

17. Once the Shanghai market becomes as transparent as London, there will tremendous pressure on the New York COMEX directors, and on US commodity regulators, to bring that market to the level of excellence showcased in London and Shanghai. In 2016, Dubai should also get recognition as another major centre of transparent gold price discovery.

18. Most investors in the gold community believe America will experience another major financial crisis that will result in tremendous money printing, and higher gold prices. Financial meltdowns will occur repeatedly in the future, but when the next one will actually arrive, is perhaps more difficult to discern than most analysts are willing to admit.

19. What is crystal clear, is that the general industrialization of China and India, regardless of economic cycles, is a long term process that is increasing gold demand from both Chindian citizens and central banks. With gold markets around the world entering a fabulous new era of “growth with transparency”, gold stocks are poised to receive enormous inflows of institutional capital.

20. On that note, please click here now. GDX is a key holding for me. This daily chart shows the 14,7,7 Stochastics oscillator in rising mode, with the lead line only at about 38. There’s plenty of room for higher prices before that key oscillator becomes overbought. I think GDX can reach $23.40 if gold reaches $1250. If gold can reach the recent highs of about $1308, GDX should trade near the summer highs in the $27 zone.

21. Please click here now. That’s the daily chart of the Australian dollar, against its US counterpart. There’s a key breakout in play. Please click here now. Australia is viewed as part of the Western world, but its geographic location force the country to benefit from the staggering growth occurring in China and India.

22. A rally in the Australian dollar at the same time as Australian gold stocks rally could createsubstantial profits for investors based outside of Australia. On that note, click here now. That’s the daily chart for Newcrest, one of the world’s top ten gold producers.

23. The company has roughly a twenty-five year mine life, which should produce enormous returns for shareholders, in the Chindian-based “gold bull era”. I recommended buying the stock at $13, $12.25, and $11.50, and two of those three buy points were hit, before the stock blasted higher in the past few days. Still, I will caution traders not to get greedy; some profits should be booked, as the stock approaches the $14.50 area.

24. As this year proceeds, I think Western gold stock investors will find themselves in a fresh new mindset. Fear of lower prices and demands for much higher ones will be replaced with strong confidence, as gold stocks stage a “choo choo train” advance on the price grid, to nicely higher prices!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

The following interview of Nevada Copper’s CEO & President Giulio Bonifacio was conducted by email and phone in the week end March 19, 2015. The views expressed herein are those of Mr. Bonifacio. The author, Peter Epstein, had no prior or existing relationship with Nevada Copper. Peter Epstein does own shares of the company.

Please provide a description of Nevada Copper for readers not familiar with the story.

We have our advanced stage Pumpkin Hollow project in Nevada consisting of a fully permitted, 6,500 tons/day underground copper mine development, with the main shaft having recently achieved a major milestone by reaching 1,900 feet main haulage level. We expect the nearby 70,000 tons/day open pit copper project to receive permits in June, 2015 as a result of the landmark passage of the Land Bill which was pass by the Senate and signed into law by the President Projected average copper production for the first five years is approximately 75 million lbs/year from our Stage 1 underground mine and an additional 220 million lbs/year from a Stage 2 open pit mine. The project is located near Yerington, Nevada, close to existing infrastructure including road, rail, labor, water and power. We have substantial reserves and resources including copper, gold, silver, as well as a large iron resource all of which have further open extent and upside. [Note: Please visit the Nevada Copper corporate website (www.nevadacopper.com) and review the Pumpkin Hollow virtual tour].

Could you touch upon the highlights of Nevada Copper’s last 2 press releases before I delve more deeply?

Let me start by saying both press releases are important, demonstrating the ongoing de-risking of the company. The February 10th press release offered a detailed update of our progress. Highlights are that the passage of the Yerington land bill was signed into law by President Obama on December 19th. Binding agreements were executed with the City of Yerington to allow for land conveyance from the City to Nevada Copper. This is extremely important because it will consolidate the entire Project on privately held land so that no Federal activities will be needed, just State permitting. Receipt of all State permits for our open pit operation are expected by June.

With the passage of the Land Bill and receipt of permits, the previously announced Stage 2 Open Pit optimization and updated Feasibility Study (see November 4, 2014 News release) is being modified to allow for the inclusion of high grade supplemental mill feed from our East and E2 underground deposits. The results of which will lead to an, “Integrated Feasibility Study.” The February 26th press release announced the achievement of another significant major milestone at our Pumpkin Hollow project, reaching the 1,900 foot main haulage level at its 24-foot diameter concrete-lined production sized shaft. This gives us essential information about the subsurface ground conditions and most importantly we will now move towards a 8,000 meter development drilling program by way of underground drill stations that will commence in early May. This drilling will further test the open extent of the underground deposits and further improve an already high grade profile. Drilling of the underground deposits was suspended in early 2011 in view of the then proven and probable reserve and desire to more effectively and efficiently drill the underground deposits from underground upon accessing the main haulage level..

Again, State permitting for the open pit mining operation will be achieved by mid-2015.

Can you explain the recently announced intention of delivering an Integrated Feasibility Study?

By integrated we mean using a single process facility which would reduce overall cap-ex by eliminating the need for a separate smaller mill. This would allow for synergies and economies of scale with respect to tailings management, permitting, ore stacking and electrical infrastructure, among other things. Integrated also means higher grade in the initial years from the inclusion of underground copper ore averaging about 1.5%-2.0%.

Since we expect to receive permits by mid 2015, we are exploring the idea of reorienting our engineering work on the open pit feasibility study towards a single, large 70,000 tons/day concentrator with dual sources of mill feed. This Integrated Feasibility Study contemplates replacing the staged project (6,500 tons/day Stage 1 underground project followed by a 70,000 tons/day Stage 2 open pit project). Instead, in an Integrated approach, mill feed would comprise an average of 63,500 tons/day of open pit ore blended with 6,500 tons/day of our high grade ore from the Eastern underground deposits.

This is an exciting development which is the result of achieving the landmark passage of the Land Bill, especially as a number of strategic and financial parties have indicated their interest and desire to participate in the Integrated operation. We think the interest we’re receiving in this regard is a vote of confidence in our Pumpkin Hollow project as well as further evidence of the de-risking of our company.

As you said, Nevada Copper has completed the sinking of the shaft at Pumpkin Hollow. It’s been reported that the company will move forward with 800 feet of lateral development? What’s the goal here?

Yes, Nevada Copper is moving forward with approximately 800 feet of lateral development at the 1,900 foot main haulage level and construction of drill stations for purposes of locating and expanding high grade ore to enhance our already high grade profile. A very important step as this will enhance our ability to mine higher grade ore in the early years of production. The lateral development will also establish key work areas for future development and provide for future access to the East ore zones. Of course it will also extend and expand our deposit.

In an integrated Feasibility scenario, how large would the Pumpkin Hollow project be compared to existing or emerging projects?

That’s a good question. In my opinion, an Integrated scenario could result in a substantial new copper producer by North American standards. Estimated production of up to 130,000 to 140,000 tonnes/yr (~280 to 300 million lbs/year) of copper annually in the earlier years. We believe that pulling forward production and mining higher grade copper in the early years could materially improve our project economics. Having said that, we need to see the results of the study before jumping to conclusions.

Roughly speaking, how big a change could these initiatives have on project economics?

Early access to the highest grade ore for the longest period possible would be huge. That’s why Integrating the underground drill program could have a big payoff. We are optimistic and internally we believe that the integrated plan looks promising. All I can say beyond that is we eagerly await the Integrated report results.

Some CEO’s are happy to voice their opinions on future commodity prices, others are content to say, no one can really know. Do you have an opinion?

We follow the major producers statements on future copper prices and, “consensus” prices decks that we see from the research community. We agree with many pundits and industry participants that the copper price will be higher than it is today. We concur with many others that copper is likely to be comfortably above $3/lb, in 2016 and beyond this level as we move to 2017. Below $3/lb there’s zero incentive to bring new copper production online. [Note: copper is up 11% from its January low and has outperformed gold by 15% in the past 60 days–Source Kitco.]

Could you sell or farm out any properties not connected with Pumpkin Hollow?

No, Pumpkin Hollow is our sole asset. However, we might be able to do something with our Iron Ore/Magnetite by-product as a future revenue source. While I can’t reveal details, we have been in serious discussions with a substantial steel player on our iron resource. Please also note that the staged approach allows for a significant growth profile should we move Pumpkin Hollow to production on this basis so effectively one project two mines. With that said and in view of the landmark passage of the land bill the integrated profile is clearly of significance in terms of what it represents both in size, future growth and jurisdiction which is one of best mining locations worldwide.

How advanced are discussions with prospective partners for the Pumpkin Hollow project? Is interest coming from strategic, financial, streaming/royalty hedge fund and private equity sources?

We have been in discussions with all of the above types of funding parties for quite some time. Discussions are progressing nicely, with parties at various stages of due diligence. As I mentioned earlier the impetus to engage in the Integrated Feasibility Study came partly from us, but also from some of these interested parties.

Nevada Copper’s stock is up 28% since the beginning of February and the copper price is up 10%. Are more investors are, “getting it?”

Absolutely, slowly but surely the investment communities are finally getting that Nevada Copper will be a fully permitted project of significant size in an ideal safe mining jurisdiction in one of the best mining States in the U.S. Further, we have infrastructure, no currency risk and all the community and political support possible.

Can you please give readers a snapshot of your capital structure, especially your cash balance?

Sure. We have 80.5 million shares outstanding and US$ 36 million of cash as of December 31st. We have 7.6 million options at an average strike price of C$ 2.25 per share, so we have 88 million shares fully-diluted. [Note: March 19th share price was C$ 1.73 for a market cap of C$ 139 million].

It’s been Management’s goal for the 2015 underground drill program is to find 2%-3% Copper equivalent grades. What would that do for the overall underground grade?

We want to identify additional high grade 3%+ ore blocks for early production and incorporate those prospective intersections into our production plans as the underground deposits are high grade and several drill intercepts have returned value greater than 5%..

How important is the company’s 20,000 meter surface drill campaign, is it largely infill drilling or step out drilling?

I’m glad you asked that. It’s both… and it will provide continued news flow in which we can update stakeholders along the way. The leverage in our project is in the open pits. We think that this drill program could add significant size and grade which we hope could lead to a re-rating of our valuation. This by no means takes away from the 8,000 meters of drilling we are doing underground, which will add size and and grade. In fact, this could be very high grade ore, which would really benefit our operations in the early years.

To the extent that you feel Nevada Copper is undervalued, why might that be?

Well, every CEO believes his or her stock is undervalued! For early stage companies, under or over valuation is really hard to call. For us, we can’t be entirely sure why our advanced stage, development company is undervalued. There may be misconceptions on our land bill and our permitting progress. Or, concern over how we will fund our company through to initial production. We have relatively low daily trading volume in our stock, which could hinder institutional investment. Having said that, our under-valuation comes at a time when many peers are also undervalued. Recent weakness in copper prices has not helped our cause. We have six sell-side analysts covering us with price targets ranging I believe from about $2.5 to $5 per share. I see no reason why our stock couldn’t get into that range this year. Although to be clear, that’s not a prediction on my part.

As we close the gap with producing companies and de-risk our project even more, we think that our current valuation of C$ 0.03 per proven reserve pound in the ground will increase. Consolidation in our sector has frequently been done at valuations of more like C$ 0.10 – C$ 0.15 per proven reserve pound in the ground. There’s plenty of room for that spread to narrow.

Are there any misconceptions about Nevada Copper that you would like to address?

We already touched upon that. I would add that I hope investors know that Nevada Copper should be fully permitted for our large open pit project in the short term. Perhaps some don’t comprehend that we have a project with significant size and grade, especially if our Integrated Feasibility comes in with strong economics. I would remind investors that Pumpkin Hollow is located in one of the safest and best jurisdictions on the planet. I would point out that among the top 10 copper producing countries, there’s China, Russia and the DRC, not to mention one of the worlds’ largest copper mines owned by Freeport-McMoRan in Indonesia that’s been in the news lately. In fact, I would much rather be in Nevada than Chile or Peru, two other top 10 producing countries.

The mining exploration business is very risky, with about 3 out of a 1000 good looking prospects becoming mines.

That’s why some smart small exploration companies follow the “prospect generator” business model of generating ideas and finding more established partners to pay for the drilling. This shares the upside, but more importantly, gives the prospect generator multiple shots at discovery without unnecessary equity dilution.

An example is Vancouver-based, Mexico-focused micro-cap

Evrim Resources (TSXV:EVM), which has 5 partner funded drill-programs planned for 2015.

The company is interesting for a few reasons. To start with, it boasts some impressive backers include John Tognetti (Haywood Chairman) Rick Rule (Sprott USA Chairman), Paul van Eeden (fund manager) and Adrian Day (fund manager).

The company has a roughly $6.2 million market capitalization and about $3.1 million in cash with its shares trading at $0.185. A month ago, Evrim’s CEO told me that cash runway could last until early 2017.

All previous financings done by Evrim have been at much higher prices, with rounds at $0.50, $0.32, and again at $0.32. The company has never issued warrants, which is unusual in junior mining finance and a positive for Evrim as it protects the share structure.

Additionally, the thing about Evrim that really caught my eye is the appointment of Alain Charest as Senior Geologist back in early February. Mr. Charest has made several discoveries in Mexico and is one of the most experienced and active explorationists in the country.

It was for these reasons we asked CEO.ca cameraman Carter Smith to visit the Evrim booth at the PDAC, the world’s largest mining convention, on March 1, 2015 in Toronto. Both CEO Paddy Nicol and Senior Geologist Alain Charest were present to quickly discuss the company’s 2015 plans.

Here is a transcript of the above video:

Paddy Nicol, President and CEO: For 2015, for Evrim, we have 4 drill programs planned on 2 of our projects with one of our exploration partners, Silvercrest. We’ve also got a 5th drill programmed planned with Arcellor Mital down in Sonora. The first four for gold exploration, and the 5th drill program is for iron-ore exploration.

The first set of results came out earlier last week, and it was a discovery on one of our projects. First time ever, we’re looking forward to seeing additional results come from that project over the next little while.

What we’re looking for, is a discovery on our Ermitaño project, and we’re basically looking to build resources now, and step out from what they’ve found already. The first stage program was a success and it’s basically building on what they’ve discovered to date.

Alain Charest, Senior Geologist: I’ve 21 years of experience in Mexico, and a few discoveries behind my belt. Joining the team of Evrim, I think there’s very good opportunity right now to pick up some very high quality projects in Mexico. It’s time to go shopping, be selective, there’s some good stuff out there. I think with the team of Evrim in Vancouver and our team in Mexico, there’s a good opportunity to bring some new projects to the company that’s basically going to give some more value to the shareholders and Evrim itself.

Forward Looking Information

This interview includes certain statements that may be deemed “forward looking statements”. All statements in this interview, other than statements of historical facts, that address events or developments that Evrim Resources Corp. (the “Company”) expects to occur, are forward looking statements. Forward looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects”, “plans”, “anticipates”, “believes”, “intends”, “estimates”, “projects”, “potential” and similar expressions, or that events or conditions “will”, “would”, “may”, “could” or “should” occur.

Although the Company believes the expectations expressed in such forward looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward looking statements. Factors that could cause the actual results to differ materially from those in forward looking statements include market prices, exploitation and exploration successes, and continued availability of capital and financing, and general economic, market or business conditions. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward looking statements. Forward looking statements are based on the beliefs, estimates and opinions of the Company’s management on the date the statements are made. Except as required by securities laws, the Company undertakes no obligation to update these forward looking statements in the event that management’s beliefs, estimates or opinions, or other factors, should change.

Billionaire mine developer Robert Friedland has said that real wealth in the mining sector is created by finding something.

Friedland would know this, having driven 5+ world-class mining discoveries in his career. He knows that to find a mine you have to spend a lot of money, and drill a lot of holes.

Another secret weapon of Friedland’s is people; he surrounds himself with impressive technical minds, and provides them with big budgets and plenty of autonomy to test their theories. Statistically speaking, explorationists who have already found mines are more likely to make future discoveries.

I first met Dave Broughton on an Ivanhoe Mines field trip to South Africa and D.R. Congo last year. Friedland stood beside Broughton at the site of Ivanhoe’s world-class Kamoa copper discovery. There, a Broughton led team had chased an exploration concept from stream and soil anomalies to drill targets and eventually, a world-class discovery. Kamoa was the first major copper discovery in the D.R.Congo in a hundred years.

At the 2015 PDAC conference in Toronto, Dr. Broughton and Mr. Friedland received the Thayer Lindsley International Discovery Award for their work finding Kamoa. This was the second time the Ivanhoe Group had won the prestigious award at mining’s largest convention.

Just a few hours before Dr. Broughton received the award, he met up with Exploration Insights editor Brent Cook, CEO.ca cameraman Carter Smith and myself to talk a bit about his exploration methodology, as well as his plans for a next discovery.

David Broughton, Kaizen Discovery, Brent Cook, Exploration Insights, and Tommy Humphreys, CEO.ca discuss Kaizen’s Discovery Trail at the PDAC in Toronto, Mar 1, 2015:

Tommy Humphreys: I’m here with Dave Broughton who is the exploration boss at Kaizen Discovery as well as Ivanhoe Capital Group, a very accomplished geologist, and my friend Brent Cook, editor of Exploration Insights. I wanted to introduce these guys because I think some of the work that Kaizen is doing is very fascinating and Brent hadn’t heard the story yet, and knows more than I do. To start off, what is the award that you’re receiving today and what brings you to PDAC?

Dave Broughton (DB): We are receiving, on behalf of a whole lot of people, the Thayer Lindsay Discovery Award, which is given every year by the PDAC for a significant international discovery. It’s the second time Ivanhoe Group has won this. They won it for OT at the inaugural event when they first awarded it a number of years ago.

Brent Cook (BC): So now you’re up in the Yukon for something different?

DB: Kaizen, late last year, picked up a package of land and took over a small company with an adjoining package of land up in the Western part of Nunavut, and its another stratiform copper play like the won we found at Kamoa [Ivanhoe Mines’ DR Congo copper discovery]. There’s copper everywhere you land, so there are good signs when you just get on the ground and wonder around. That’s been appreciated for a long time, it was discovered initially in the 60’s and some work was done then, but really, nothing’s happened for about 20 years. The last group of people to be in there in a significant way on the play we’re really excited about was Cominco and that was in the early 90s.

There really are two plays, there’s a volcanic hosted copper play, that has a lot of very high grade copper, well known, load copper, I guess you’d call it, in volcanic rocks, and there’s a more, less appreciated play, which is what we’re really excited about, and it’s in the sedimentary rocks overlying it. The rocks are similar in age to those in the copperbelt which is intriguing, and there’s mineralization that’s outcropping and in most places its covered, certainly 95% cover. 150 kilometer strike of these sedimentary rocks with copper showing here and there but it really hasn’t been tested.

BC: How many holes have been put into this?

DB: Well, Cominco put about a half a dozen holes at the far eastern end of the area and the rest is basically untouched.

BC: What did they find?

DB: They hit mineralization, they didn’t hit an ore grade intersection over ore grade widths, but there are lots of holes at Kamoa or Kupferschiefer, or anywhere you want to go in these systems, you don’t always hit ore on your first hole. The usual things right: persistent and all that.

BC: What sort of width and thickness are we talking in this horizon from the drilling you’ve got so far?

DB: You’ve got mineralization over meters in lenses and so on. There is some government geophysical data that gives up some idea as to what the big structures might be that might help control mineralization. We have some old prospecting that we know about. It’s really going to be getting on the ground and walking those contacts and making up our own mind of where we can find mineralization. And then we’re looking at doing a series of widely spaced stratigraphic holes, just like you would in other districts. You’ve really got to step back. These things go for kilometres, Kamoa is 50 square kilometres in area, so you really have to look at it at a base of scale and then narrow in on what you find. We’re going to take a big scaled approach to start with and test as much of the strike length as we can, I think.

BC: What’s the access like?

DB: The access is actually excellent. We’re just south of the old town of Coppermine.

BC: Ah, the old famous Coppermine?

DB: It’s a short helicopter ride from there to the project. There’s an airstrip, regular air service. There’s an old air strip actually on one of the properties we’re going to use for direct access with a fixed wing aircraft, so it doesn’t get much better in that sense.

BC: Conceptually, what do you need to see, what do you need to find there to take it to the Kamoa stage, or up to a stage where its a world class deposit or something that’s really profitable.

DB: Like anywhere, you want to drill a discovery hole that’s got an ore grade and width and then you want to step out from that and build tons. That’s what it’s all about.

BC: What grade do you need?

DB: Up there, good question. Kamoa’s average grade is close to 3%, there are other deposits around the world that have that. If you get 3% copper of sufficient width, you’re in business.

BC: So that’s how we can judge your program. Although admittedly the first round is basic geology which I think is really smart. Get a handle on what’s going on and then zero in. If we’re going to watch this play, it’s about, first off, we get the concept, it’s coming together or it’s not coming together, here’s our targets, next round or two rounds after that, we’re getting low cost minable widths over 3+% copper, okay.

DB: That’s the objective but like anything, you find what you find, and you go with it. They are mining the Kupferschiefer at under 2%. It really depends on all sorts of other factors, I’m not going to be able to predict that.

BC: You’re not that good yet?

DB: Not that good yet, sorry.

BC: What sort of shape is the company in? How much cash do you have and what’s your market cap?

DB: We’re in good shape. We’ve got a unique strategic relationship with the Japanese trading houses, they fund a number of our exploration projects, and we’ve got a long history of relationships with them, going back to the Ivanhoe Group as well. That’s kind of our key strategic difference that we’ve got. In addition, we’ve got a treasury and no debt so that helps too.

BC: They are funding by way of placements, or getting a piece of the project, or an offtake agreement, what’s their relationship?

DB: It varies project to project. We have projects in BC where they are funding the exploration directly. They are interested in the offtake in the long term for Japan that’s really what’s driving them. And we’re interested in the metals that work for that reason.

BC: That was Kaizen. They are looking for stratiform copper in Nunavut. Actually pretty interesting concept. If they can pull together a large enough volume of rock at 3%, which is what they’re after, it sounds like the infrastructure is not too bad, that could be quite significant. They’ve got a good deal structured with a number of Japanese groups, so its worth watching for sure.

Discuss @ chat.ceo.ca

FORWARD-LOOKING STATEMENTS

Statements in this video and article that are forward-looking statements are subject to various risks and uncertainties concerning the specific factors disclosed here and elsewhere in Kaizen’s periodic filings with Canadian securities regulators. When used in this video and article, words such as “will, could, plan, estimate, expect, intend, may, potential, should,” and similar expressions, are forward-looking statements. Information provided in this document is necessarily summarized and may not contain all available material information.

Although Kaizen has attempted to identify important factors that could cause actual results, performance or achievements to differ materially from those contained in the forward-looking statements, there can be other factors that cause results, performance or achievements not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate or that management’s expectations or estimates of future developments, circumstances or results will materialize. As a result of these risks and uncertainties, the results or events predicted in these forward-looking statements may differ materially from actual results or events.

Accordingly, readers should not place undue reliance on forward-looking statements. The forward-looking statements in this news release are made as of the date of this release. Kaizen disclaims any intention or obligation to update or revise such information, except as required by applicable law, and Kaizen does not assume any liability for disclosure relating to any other company mentioned herein.

Disclosure: Author is a small shareholder in both Ivanhoe Mines and Kaizen Discovery. This is not investment advice. Consult a professional investment advisor prior to making any investment decision.

The following interview of CEO Corrado De Gasperis of Comstock Mining (LODE) was conducted by phone and email over the week ending March 16th. The views and opinions expressed by Mr. De Gasperis are entirely his own. I, Peter Epstein have no prior or existing relationship with any company named herein.

Please describe Comstock Mining (LODE) to readers not familiar with your story.

We are a Nevada-based, permitted and producing gold and silver mining company, trading on the NYSE MKT exchange under the symbol LODE. The Company has already achieved unprecedented results, like consolidating substantially all of the historic, world-class Comstock Lode mining district south of Virginia City, with approximately 8,300 acres (over 10 square miles) along an approximately six-mile long, contiguous mineralized trend. The Comstock Lode district is best known for producing over 8 million ounces of gold and 192 million ounces of silver, primarily in the late 1800’s, including 33 bonanzas, but no one has ever been able to take this massive, fragmented, complex property position with all of its dynamics, and put it under one roof, until now (not to mention permitting it and going into production).

There’s been a lot of local press reports about a road adjacent to your property that needs to be re-routed. Is this a big a deal, will it impact production?

The road in question is a state route, SR-342, that was built on loose fill and eroded from weather events to the point that it needs to be re-routed. We will move the road as we were planning on doing anyway, but it will help the State, help the County and accelerate many of our business and reclamation plans. Classic win-win-win.

Some shareholders feel that production growth has been slower (or even much slower) than expected. Do you agree?

Yes, we had originally planned for ramping up Lucerne to a 40,000 gold equivalent ounce run rate per annum last year, but those mine plans, and a lower gold price, required us to modify. We increased our economic cutoff rate and we also invested significant resources on enhancing the geologic controls, resulting in a much more reliable and predictable mine plan. These cumulative changes initially resulted in much higher strip ratios before we worked through that section of the mine and reached the flatter, lower strip sections of the Lucerne Mine.

Concurrently, we also dramatically reduced costs, by over $11 million dollars, year on year. Today, we not only have a drastically improved strip ratio but we can also leverage a much lower and more flexible cost structure as we expand. During this same period, we received permitting approvals to expand the scope of the initial mine area, going from about 180 acres under permit to approximately 1,300 acres under permit. I am proud of how our team responded to the adversity and we feel we are much better positioned for profitable growth by working through that adversity.

Why isn’t your second mine, Dayton, not in production yet?

The Dayton is our second, high priority target area. Our original drilling, although limited, quantified over 0.5 million gold equivalent ounces of initial resource. Last year, we restructured the purchase to completely eliminate the royalty (it’s 100% owned and royalty free) and rezoned all the lands to a mining designation. We have since done geophysical, structural and core drilling, with significant continuity of the mineralized structure confirmed and further discoveries identified. We are planning to complete the exploration and development drilling this year, formalize our feasibility for the full mine plan and facilitate the permitting, all in 2015.

What is the biggest pushback you get from prospective investors in Comstock Mining?

Investors have been waiting for cash flow and are excited to see that cash flow reinvested in exploration and development with positive results. Our recent drill results on the Eastside of Lucerne are the first example of that. The last three quarters, we were cash flow positive from operations, yet the Company was still reducing costs, expanding permits, acquiring and very effectively re-zoning land, developing the mine, and expanding the heap leach pad. With dramatically lower costs, we guided to full profitability for the first half of 2015. The stronger that track record, the stronger the investment interest will be.

Can you give us a snapshot of your latest capital structure including cash, preferred shares and debt?

Our capital base has been strong since we recapitalized in 2010, with an exceptionally high quality base of institutional investors. We have 89.8 million shares outstanding, with $48.6 million of additional permanent equity in a preferred stock, which, if converted, represents another 53.6 million common shares, for a little over 143.4 million fully diluted shares. At the end of 2014, the Company had approximately $1 million drawn on a $5 million Revolver, $6.9 million in equipment financing and $3.6 million for notes payable on land purchases. The Company also had $5.3 million in cash.

What are the terms of the preferred shares? Do you believe the preferred shares are an overhang on Comstock’s stock?

No, not since our preferred stock represents permanent equity capital that has no debt-like features. The holders of the preferred stock have been investors for between 5-10 years, and have provided significant funding for the initial consolidation and production growth phases of the Company. The preferred stock is convertible to a fixed underlying number of common shares. The average conversion price is $1.10 (ranging from $0.65 – $1.65).

To the extent that you think Comstock is undervalued, why do you think that might be?