Gold and gold stocks finally showed a bit of weakness during the holiday shortened week. Gold had its biggest weekly loss in months, losing 3% to $1217/oz while the miners (GDX, GDXJ) declined about 5%. Silver lost 4%. If weakness in Gold and gold stocks continues then we should turn our attention to technical support and see if it will hold. Gold and gold stocks are trading above the 400-day moving average which has been key resistance since 2011. Holding that support in the days or weeks ahead would offer confirmation that a new bull has started.

The following chart plots the daily candles for GDXJ and GDX. GDXJ, which is showing more strength has initial support at $26 followed by strong support near $24 and $23. Note that the 50-day moving average, 400-day moving average and 38% retracement of the rebound figure to coincide in the low $24s. Meanwhile, GDX has initial support at $19 with strong support in mid $17s and at $17. The confluence of support in GDX is in the mid $17s.

Gold’s support is at $1190 to $1200/oz followed by the 400-day moving average at $1175/oz.

The 400-day moving average is important because it contained every rally in the precious metals complex from 2012 to 2015. During that period GDX tested and failed at the 400-day moving average three times. GDXJ tested and failed there once (in summer 2014). Gold spent a few days above its 400-day moving average in early 2015 but that proved to be an aberration. Silver, which has remained below its 400-day moving average since late 2012 failed to exceed it in recent days.

Turning to the fundamental picture, real interest rates (the major driver for Gold) have recently turned in favor of precious metals. As the picture shows, the real fed funds rate is negative again while the real 5-year yield has declined from nearly 2% to near 0%. The fundamental underpinning that precious metals lacked in recent years is now in place.

With respect to the miners, their fundamentals have been improving for over a year. The energy crash has reduced operating costs for many miners by a considerable margin. Furthermore, weakness in many local currencies has also reduced operating costs.

If Gold and gold stocks are in a new bull market then they will hold above their 400-day moving averages and rebound in the weeks ahead. Meanwhile, Silver would vault above its 400-day moving average. Given the forever bear of 2011-2015, there is now widespread fear and consternation about a correction or major rollover in precious metals. It is only natural to feel that after a sharp and persistent downtrend. We would be buyers on pullbacks to the 400-day moving average.

1.America was built by “citizen champions”. Should the current gold price action be described in a similar way, as a “rally of champions”? I think so.

2. Technically, gold is arguably overbought. It may be due for a correction according to cycle analysis, and yet the world’s mightiest metal just keeps moving relentlessly higher.

3. Please click here now. That’s a snapshot of the SPDR fund tonnage. Solid buying has boosted the holdings to more than 820 tons.

4. Also, a potential “rally accelerant” has suddenly manifested itself, in the form of an end to the Indian jeweller strike. Please click here now. Double-click to enlarge this key four hour bars gold chart.

5. It could be persuasively argued that gold has essentially traded sideways because of the strike.

6. Now that the strike is over, demand appears to be rising in the world’s most important gold market, and gold is rising up nicely, from a small inverse head and shoulders bottom pattern.

7. My $1320 area target remains within reach on this rally. In the big picture, I think that as bullish as Janet Yelllen’s first rate hike was for gold, her next one could turn the gold price rally into a serious “barnburner”!

8. Please click here now. Double-click to enlarge. This eight hour bars chart of the dollar versus the yen has ominous implications for the dollar.

9. A bear flag is in play. In the big picture, it’s almost impossible for gold to experience a major setback, when the dollar is tumbling against the yen. Pleaseclick here now. Double-click to enlarge. That’s a longer term chart of the dollar versus the yen, using daily bars.

10. An enormous top pattern is now in play, and dollar rallies are quite frankly best described as “pathetic”.

11. A breakdown from the current 111 – 115 range could unleash a new wave of dollar selling, yen buying, and gold/silver buying. That could easily push gold towards my $1320 target, and leave the dollar wallowing in the 105 -107 zone on the dollar-yen chart.

12. If a much bigger leg of the gold price lies ahead, silver will begin to dramatically outperform gold. Is there any evidence that such an event is on the horizon? Yes, there is!

13. Please click here now. Double-click to enlarge. That’s a daily bars chart for silver, and to say it looks inviting is arguably the understatement of the year.

14. There’s a beautiful inverse head and shoulders bottom pattern in play, with a technical target of $17.50 – $18.

15. Silver price enthusiasts should note that India is a massive silver buyer, so the end of the jeweller strike there could have an enormous impact on silver demand.

16. Silver is not just the poor man’s gold. In my professional opinion, it’s the world’s second mightiest asset, and it should be part of all investment portfolios.If an investor owns no silver at all, they can pay any price for a small amount of it. After that, they can use my unique “pyramid generator” for systematic capital allocation.

17. For another view of the silver price action, please click here now. Double-click to enlarge. This weekly bars silver chart is extremely interesting. Here’s why:

18. There’s a major trend line breakout in play, and the inverse H&S bottom pattern on the daily chart appears to be acting as a kind of “Launchpad” for the weekly chart breakout.

19. Note the beautiful position of both the RSI indicator at the top of the chart, and the 14,3,3 Stochastics series at the bottom of the chart.

20. Major breakouts tend to have this kind of “textbook” technical set-up, with RSI on the weekly chart well below the overbought zone, and the Stochastics oscillator staging a “flatline” event in an overbought condition. Once the $18 target has been acquired, I think silver will pause, and then move towards $25.

21. Silver price fans should also look at the SIL-NYSE silver stocks ETF, which is poised to lead bullion to more upside gains.

22. Please click here now. Double-click to enlarge. GDX continues to make superb upside progress towards my $23 target, on this weekly bars chart. Investors who may have become demoralized and sold their gold stocks at losses should not wait for any type of correction to get back into this powerful market. Here’s why:

23. Rather than selling off from the $23 area, GDX could instead form a high right shoulder, far above the $23 area. This is exactly what the silver bullion chart action is implying is going to happen! It’s clearly a glorious time for the Western gold community, and I’m becoming quite convinced that’s it’s about to become… even more glorious!

This week I had the distinct pleasure of interviewing Joe Lowry, aka “Mr. Lithium.” Our maiden interview in June of last year received a tremendous amount of interest, so we followed it with a very well received Part 2. Now, back by popular demand, we proudly present Part 3, in which the interviewer wonders…. Is this Lithium Love or Lithium Lust? Continue reading to find out.

As a reminder, I, Peter Epstein, have no prior or existing business relationship with Joe Lowry or any of his business interests. Nor do I have any prior or existing relationship with any company named.

Joe, I understand you’ve been traveling the world. Can you share comments on the lithium market to start us off?

Peter, nice speaking with you again. Yes, recently I spent a week in Australia, a week in Japan and a week in China. Please note though, I do this sort of trip several times a year. I have run a U.S. based, independent lithium advisory business for more than three years and have visited Asia more than two dozen times since then.

I began traveling to China on a monthly basis in 2000 – the year I moved to Japan. I made trips to such disparate places as Xinjiang, Tibet & Sichuan to meet lithium producers. I moved to China in 2005 and lived there for over five years, making trips to Japan every three weeks. My daughters considered Japan and China home, both graduated from high school in Shanghai.

Oh, and the short story on the market is;

The lithium shortage is real, the US$20,000+/Mt pricing for carbonate & hydroxide in China is real, and robust growth in lithium demand is real.

What was the biggest surprise for you on this trip?

I thought the recent 3x price run-up in China would be a major point of discussion, but that point was dwarfed by concerns over lack of supply. The overwhelming interest in lithium on the part of Australian investors was also a bit of a surprise.

Please explain how you are able to gain access to key lithium industry participants?

It’s All About Relationships…. I am perhaps the, “Forrest Gump” of the lithium business, blessed to be at the right place at the right time during twenty years of lithium demand growth. I took over responsibility for FMC Lithium’s carbonate and hydroxide businesses just as the lithium ion battery was being commercialized.

After five years of traveling to Japan every six to eight weeks to meet with customers from the emerging lithium ion battery market, I was asked to move there and take over responsibility for not only FMC’s Asia sales, but also a Japan-based lithium ion battery cathode production JV, and a profitable downstream JV producing both lithium metal & butyl lithium.

Business in Asia is much more relationship-based than it is in North America, I had the opportunity to forge great relationships in business meetings, at dinners, karaoke and on golf courses. Being a resident instead of a visitor was a great help as was acquiring language skills.

As mentioned, I traveled to Asia multiple times a year (and still do) and became a supplier in some cases, a customer in others, but more importantly a friend. Long story short: I’m a well-recognized face and a trusted one in the Asian lithium market.

Do you see evidence of a vibrant EV market in Asia / Australia?

I would say the vibrant growth in e-transportation is real. In 2015, e-buses in China were the major story, but all other forms of e-transportation are gaining traction. As is Energy Storage Solutions (ESS), albeit from a smaller base.

Which major countries are serious about facilitating widespread use of lithium ion batteries?

Due to the combination of population, air quality issues and the power of the government to, “influence” outcomes – China is the main story. I would lump major EU countries together as also being significant. Even India is making noise in both e-transport and ESS. The U.S. will also show growth, but as a follower, not a leader.

Aside from prices, what best reflects the state of the lithium industry?

Australia is now the center of the lithium universe. Talison plus Galaxy’s Mt Cattlin project, Neometals/Ganfeng’s Mt Marion and the potential of Pilbara Minerals are like to increase spodumene’s volume hegemony over brine at least until 2022.

To the extent that you can comment on pricing; past, present or future, please do!

One point I find extremely interesting is that the countries that always were low price buyers, trying to secure the cheapest Chinese product, have now been shut out due the price run-up in China and the VAT penalty creating a disincentive for exports.

I have been approached for help in securing product by companies in India and in similar markets, who in the past always sought the lowest price. These companies, faced with shutting down their plants, have offered US$28,000 – US$30,000/Mt, in advance, for lithium hydroxide.

Unfortunately, since they have no relationships, supply for these companies is hard to come by. What we considered the bottom of the market appears to prove that demand destruction is not a major concern. On the other hand, the Japanese have contracts at low prices for much of their 2016 volumes and seem to be in denial that they will have to pay much higher prices in 2017.

I see a return to a normalized global price range as a major theme for 2017.

Any thoughts on how Tesla’s (under construction) giga-factory fits into global battery markets?

Yes, good question. The western press seems fixated on the Tesla giga-factory; however Tesla is really just one of many large battery projects worldwide. China has multiple projects, some of which, although smaller than Tesla’s planned operation, are already in production and will grow in phases.

I think what Tesla is doing is great, but it’s only part of the global story.

Based on extensive meetings around the globe, are there critical events on the horizon that could shake things up?

As long as China continues a reasonable level of support for battery related initiatives and there is not a major global recession, I think lithium ion battery demand for non-consumer applications has reached a tipping-point, ensuring robust lithium demand for the next several years.

Some are forecasting price increases of 10%+ per year for a decade or more. What could disrupt the conventional wisdom of soaring demand?

The current US$20,000/Mt price in China already ensures great profits for even the highest cost producers. I believe in market forces. New spodumene capacity comes online more quickly than brine but if prices stay at the high teens for five years, I believe you will see at least a brief oversupply situation no later than 2024. As long as spodumene is a major lithium source, price is not likely to return to US$6,000/Mt in the next decade. Having said that, I do not believe 10% annual price increases for a decade is even a remote possibility.

Thank you once again for your keen insights and timely update on the lithium industry.

I think that was it…the correction in gold that I called mid last week. Yes, it’s still overbought. The drop was only about $50 per ounce, top to bottom. But I think the uptrend may now resume. Because this is not a gold bear market, dear reader. It’s a bull.

The longs who sold in expectation of the kind of correction we had in the bear market—where gold would grind lower every day for weeks while the gold stocks fell faster—are out and wanting to get back in. The shorts who pressed their bets the last few days may soon regret their actions.

Why? Because gold is the only game in town. The S&P rally is stalling at its 200 DMA, the economy continues to weaken, corporate earnings are in a serious downturn and stocks are still an eyelash short of all-time highs. The bad news is not priced in, dear reader. And now it looks like we have buyer exhaustion. Volume backed off again for a second straight day today (Tuesday, the 15th, 0.85 bln on the NYSE and 1.6 bln on the NASDAQ). Breadth was nearly 3 to 1 negative on both exchanges. This is a market that, if it isn’t going up, can go down in a hurry. And it isn’t going up.

The Japanese did not come up with more stimulus, the ECB shot its wad last week and tomorrow the Fed will do nothing. Next up is first quarter earnings preceded by a growing list of companies pre-announcing. They don’t pre-announce good news. So, look out below. The quiet period between corporate reporting periods is coming to a close. The holiday is over and so is this rally, in my opinion.

So, back to gold. The upside risks now looks greater than the downside risks, unlike last week. I may be early in making this call, but it’s better than being late. The move last month was big and fast. That’s how it is in bull markets.

1.As it often does, gold is pausing ahead of this week’s FOMC meeting. I don’t expect Janet Yellen to raise rates this week, although recent jobs reports and the oil price rally are likely tempting her to do so.

2. The limited recovery from the meltdown in global stock markets after her first rate hike is likely to convince Janet to hold off, but only until the next meeting.

3. That is when a fresh and potentially horrific US stock market meltdown is most likely.

4. Please click here now. That’s the daily gold chart. The sell-off that began last week is building the right shoulder of a solid inverse head and shoulders pattern, which is strengthening the overall technical picture.

5. For a look at key liquidity flows into and out of gold, please click here now. That’s a snapshot of the latest COT report, and I’ve highlighted the commercial bank actions in green.

6. The banks clearly are not afraid to “chase some price” in this general price area, as they added long positions as well as short ones quite recently.

7. The COT reports offer a look at what the banks have done in the past, but to understand what they are likely doing in the present, please click here now. That’s a short term gold chart, using five minute bars.

8. Note the sizable volume bars that are appearing. In my professional opinion, the banks have already covered tens of thousands of short positions, just in the past few trading sessions.

9. If my right shoulder projection plays out, I think they will have covered off many more, and will be adding long positions quite aggressively as they do that.

10. Please click here now. From a fundamental perspective, gold’s rally from December has been mainly based on three factors:

11. First, Janet’s rate hike created a huge panic in risk-on markets. Second, influential economists began suggesting that a new upcycle for commodities could begin later this year.

12. That caused money managers to commit to the entire commodity sector, on an ongoing basis as a value play.

13. Third, Chinese New Year buying was a strong seasonal factor.

14. Indian demand is often limited at this time of the year, but it has been more soft than usual because of hopes for a duty cut, and now a jeweller strike. If the strike continues, official Indian demand could be under 20 tons in March.

15. In the short term, it’s difficult for gold to make strong headway with Chinese New Year buying finished, and India being this quiet…unless some new fear trade catalyst is on the near-term horizon.

16. What could that be? For the likely answer, please click here now. Japanese central banker Kuroda left rates unchanged at the latest BOJ meeting, but many top bank economists feel he could be poised to do something drastic at the next meeting in April with his QEE program.

17. I’ve argued that rate hikes in America and NIRP (negative rates) in Europe and Japan are a potent combination for higher gold prices.

18. If Indian jewellers end their strike in April, as Janet hikes rates and Kuroda drastically ramps up QEE, gold could begin a much more aggressive rally than what has already occurred in the past few months.

19. Please click here now. While these comments about China tying gold reserves to GDP were arguably made by somebody “talking their book”, the PBOC has released official written statements about the key role of gold in the internationalization of the yuan.

20. The SGE gold price fix is scheduled, tentatively, for an April 19 launch date, and that time frame coincides with many other key events for price discovery in the West.

21. Tactics? As always, amateur investors who tend to panic during gold price pullbacks should buy put options. While I’m always massively net long gold, I also always make sure I add some short positions into rallies, following the “financial footsteps” of the commercial bank traders.

22. Please click here now. That’s the GDX weekly chart. It looks spectacular, but the most likely price action in the short term is a bit of a “sideways chop”.

23. That chop should see a couple of right shoulders form, as part of a big inverse head and shoulders bottom pattern. While anything is possible in any market at any time, including new lows for gold, I think the Western gold community is starting to look pretty good here, given the sizable institutional buying taking place “across the board” in gold stocks.

24. Because a lot of that buying is value-oriented, even if gold did “impossibly” go to a new low, the substantial institutional commitment to gold stocks that is in play now is likely to accelerate. Simply put, there’s a wave of confidence sweeping through the institutional investor community about gold stocks, and I think it’s time for the Western gold community to grab an extra gold stocks surfboard, and have some fun!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

With gold miners’ stock prices surging dramatically this year, investors’ attention is starting to return to the gold juniors. These smaller miners and explorers suffered terribly in recent years, all but abandoned as gold slumped to major secular lows. But even during gold’s darkest quarter, the fundamentals of the juniors actually mining gold remained quite strong. This portends explosive profits growth as gold recovers.

Most investors think of junior gold stocks as the Wild West of commodities stocks, with good reason. The legendary American humorist Mark Twain allegedly described a gold mine as a hole in the ground with a liar at the top! There are literally hundreds of gold juniors, a number that swells whenever gold grows more popular. And the great majority of these tiny companies truly are junk, they are indeed doomed to fail.

That grim reality is seldom due to nefarious intent, but to the almost-insurmountable challenges involved in finding an economic deposit of gold and bringing it to production. The whole process of exploring for gold, drilling to confirm it, designing a mine, securing the myriad of governmental permits necessary to mine, and then constructing a mine is exceedingly time-consuming and excessively capital-intensive.

As I did the research for this essay, I waded through the 2015 annual reports of dozens of junior golds. One that really stuck out came from elite explorer NovaGold, which owns a couple of the world’s biggest and best undeveloped gold deposits. Its chairman wrote an amazing article included in its annual report that outlines the extreme difficulty inherent in bringing any gold deposit to production, an essential read.

Last year, the average time it took to bring a gold deposit to production was 15 years. Think about what your own life was like 15 years ago, and it’s apparent that is a vast span of time. It is almost as long as the great 17-year secular-bull and -bear cycles in Long Valuation Waves that drive stock markets. Can you imagine how hard it would be to captivate investors’ attention for 15 long years? It seems impossible.

Yet that’s what junior golds have to accomplish. Banks won’t even think about loaning money to gold explorers yet to find a great deposit, so the equity markets are their only source of capital. They need to explore for years, while keeping investors interested enough to buy their periodic stock offerings. And then it takes another 15 years after a deposit is found to bring it into production. And that’s getting worse.

Industry projections of the time from discovery to production are expected to swell near 24 years in 2016, and 33 years by 2018! Tapping equity markets for a quarter to a third of a century before cash flows start coming in defies belief, especially considering the bull-bear cycles in gold are way shorter. Great junior gold explorers able to maintain investors’ interest during gold bulls usually lose it in subsequent bears.

So gold’s relentless weakness in recent years, driven by the Fed’s surreal stock-market levitation, has had a catastrophic impact on the junior gold explorers. Many didn’t survive as investors abandoned this sector and left it for dead, unable to raise enough capital to continue operations. And nearly all the rest had to vastly cut back their exploration, doing everything they could to survive a gold-stock apocalypse.

That culminated just months ago, with gold slumping to a dismal 6.1-year secular low in mid-December after the Fed hiked rates for the first time in 9.5 years. Gold stocks followed gold as usual, plunging to a fundamentally-absurd 13.5-year secular low in mid-January. Investor sentiment, and therefore juniors’ ability to raise capital, had never been worse according to countless battle-hardened industry veterans.

This has huge implications for future gold supply. The junior explorers are critical to the entire gold-mining industry since they discover new deposits essential for feeding the gold-mining pipeline. Since all existing gold mines are constantly depleting, the miners have to replenish their reserves with new deposits. With exploration plummeting in recent years, that pipeline will be severely impaired for many years to come.

That NovaGold annual report showed gold discoveries peaked way back in 1995 near a 3-year moving average of 140 million ounces. Despite soaring gold-exploration budgets as this metal was very strong between 2009 to 2012, 2014’s gold discoveries had plummeted 96% to around 5m ounces! The terrible plight of the junior gold explorers guarantees gold supplies are going to be constrained for at least a decade.

Global peak production near 102m ounces was hit last year, and industry projections show it falling for all foreseeable future years. The venerable World Gold Council recently confirmed this new trend in its Q4 Gold Demand Trends report. It showed that global mine supply dropped 9.3% YoY in Q4, which was its first quarterly decline since that once-in-a-century stock panic battered the gold miners in late 2008!

While the nightmare for the junior gold explorers couldn’t be worse, it’s super-bullish for gold. The near-total collapse of the gold exploration pipeline in recent years means it’s going to be almost impossible for world miners to ramp up gold supply no matter how high gold mean reverts as global investors deluge back in. Even after exploration spending rebounds, it will still take decades to start mining new deposits.

As a group, junior gold explorers are almost unanalyzable. They all burn capital relentlessly to search for new gold deposits or prove up reserves in ones they’ve found. They have no revenues with no gold to sell, so all their cash comes from stock offerings. The better ones always have a chance of being bought out by a miner, but explorers have no future cash flows to crunch until they get to the mine-build stage.

So while there are the rare super-successful explorers certainly worthy of investors’ hard-earned capital, I’ve always preferred the actual small miners over explorers in the junior-gold realm. By definition, the miners have overcome the odds to actually produce gold. So they have sales generating operating cash flows and profits, along with mining costs that make it easy to estimate their upside as the gold price recovers.

The definitive benchmark for junior gold stocks, including miners and explorers, is of course the GDXJ Market Vectors Junior Gold Miners ETF. As of the middle of this week, it included a whopping 52 of the world’s best junior gold stocks! In addition to miners and explorers, GDXJ also includes gold-streaming and royalty companies as well as silver miners. GDXJ’s managers do a great job finding excellent juniors.

Since recent years’ brutal gold weakness culminated in Q4’15, I’ve been very interested to see how the actual gold miners among the elite GDXJ components fared. Q4’s average gold price of just $1105 was the worst quarter seen since not long after the stock panic in Q4’09. With gold-mining-sector sentiment as hyper-bearish as it’s ever been in Q4’15, the junior gold miners’ stocks were pounded down near oblivion.

So I’ve been eagerly awaiting their Q4 financial reports. But as discussed in my essay several weeks ago on the Q4 performance of the larger gold miners in the GDX Market Vectors Gold Miners ETF, final full-year reports aren’t due until 90 days after year-end. They require fully-audited results right in the heart of CPAs’ busy season, which then have to be woven into complex annual reports that take time to produce.

But as these results gradually emerge, we can finally gain an understanding of how junior gold miners were actually doing in gold’s worst quarter in 6 years. These tables look at the top 34 holdings of GDXJ, over 91% of its total weighting. I dug into their latest reports to build a spreadsheet with a bunch of data to assess junior gold miners’ fundamental health when their stocks were being crushed in that dark Q4.

These tables show each GDXJ component stock’s symbol, exchange, current weighting in that ETF, market capitalization, cash costs per ounce, all-in sustaining costs per ounce, AISC projections for 2016, cash on hand, its percentage of market cap, Q4 cash flows generated from operations, along with Q4 production. This hard Q4 data proves that the junior gold miners’ deep stock-price lows were never justified.

Because of that quarter-long deadline on releasing Q4 audited results, unfortunately not all the GDXJ components have reported as of the middle of this week. Where data wasn’t published, nothing could be put into this table. Interestingly GDXJ’s largest holding, the amazing OceanaGold which I analyzed in depth a couple weeks ago, is also included in GDX. There’s some overlap between juniors and larger miners.

Despite the miserable gold conditions and horrendous sentiment utterly dominating Q4, the junior gold miners proved to be amazingly strong. The first metric for their health is cash costs per ounce, or how much they have to actually spend to produce each ounce of gold. They include all direct production costs, as well as mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses.

Cash costs have dominated gold-mining cost reporting since the 1990s, and are an acid-test measure of gold-miner survivability. As long as the gold price stays above cash costs, gold miners can continue to produce gold and pay their bills necessary to survive. After filtering out GDXJ’s explorers, the streamers and royalty companies, and silver miners, the elite junior gold miners reported average Q4 cash costs of just $628!

These smaller miners needed $628 to wrest an ounce of gold out of the ground, yet the lowest gold fell in Q4 was $1051 the day after that Fed rate hike! So unlike the extremely-bearish commentary that the falling junior-gold-stock prices fueled, this sector was never in jeopardy at all. The junior gold miners as a sector actually had cash costs in line with the larger gold miners’, as GDX’s Q4 average cash cost was $587.

But cash costs are misleading, as they don’t include many major expenses essential for mining gold. So in June 2013 the World Gold Council introduced the comprehensive all-in-sustaining-cost metric. This includes everything necessary to maintain and replenish gold-mining operations at current production levels. All-in sustaining costs are a monumental improvement over the deceptive cash-cost reporting.

All-in sustaining costs include all direct cash costs of mining gold, along with much more. Corporate-level administration is included, as the high-level people running companies are a sizable expense for mining gold. AISC also include exploring for new gold to mine, developing and constructing new mines, remediation, and reclamation. These costs are indispensable since gold mines are constantly depleting.

During dark Q4 when everyone abandoned the elite junior gold miners of GDXJ, they were operating at AISC levels of just $812 per ounce! Remember gold averaged $1105 in Q4, and fell to $1051 at worst. So even when Wall Street shrilly argued that gold was doomed to spiral lower during Fed rate hikes, an irrational notion contrary to market history, the junior gold miners were still earning large operating profits.

At gold’s secular nadir of $1051, the GDXJ junior gold miners were still earning a hefty $239 per ounce of gold mined! That equates to a very healthy 23% profit margin that many industries would die for. It is also interesting to see the junior gold miners’ all-in sustaining costs even better than the larger miners’ in GDX, which came in at an $836 average in Q4. The gold juniors never faced any existential threat at all!

The junior gold miners’ impressive profitability during gold’s worst quarter in 6 years is evident in their strong operating cash flows. The great majority of these elite miners were still earning plenty of money even as the gold price languished. As long as businesses can generate positive operating cash flows, and they haven’t been profligate in borrowing, they can continue operating as going concerns indefinitely.

Such strong operating cash flows naturally fed impressive quarter-end cash coffers in many of the elite junior gold miners. The majority of these GDXJ miners reported large cash positions in the double-digit percentages of their market capitalizations. More cash on hand obviously improves survivability in any scenario where profits are temporarily impaired, like an artificially-low bearish-sentiment-driven gold anomaly.

And if the junior gold miners could fare so well even in dark Q4, imagine how awesome their coming Q1 results will prove! As of the middle of this week, gold prices have averaged $1167 so far in Q1. That’s 5.6% above Q4’s average. Yet at junior gold miners’ Q4 average AISC of $812 per ounce, profitability in Q1 will already surge 21.3% to $355 per ounce. Gold miners’ profits leverage to gold is why they’re so alluring.

For the most part, gold-mining costs are essentially fixed during the mine-planning stage. So as gold prices mean revert higher, that translates directly into higher profits for the gold miners. This relationship is certainly not linear, with gold-mining profits rising far faster than gold prices. And throughout all the stock markets, any company’s underlying profitability ultimately determines how high its stock price can go.

With investors finally rushing back into gold for the first time since 2009, this battered metal is heading a heck of a lot higher. The last time investors returned at the magnitude seen so far in young 2016, gold was early in a mighty bull market that would see it soar 167% higher in less than several years. Another similar bull market off gold’s recent mid-December secular low would catapult it radically higher near $2800.

But there’s no need to be that optimistic to see the epic opportunities today in junior gold miners’ stocks. The last normal year before the Fed’s unprecedented open-ended QE3 campaign levitated stocks which decimated gold was 2012, where gold averaged $1669. Gold would merely have to rally 59% out of its mid-December lows to regain those levels, which is very conservative and tiny as far as gold bulls go.

The elite GDXJ junior gold miners also forecasted their 2016 AISC in their Q4 reporting, which averaged $850 per ounce. The miners always have strong incentives to overestimate costs and underestimate production in their forward guidance, giving them an opportunity to beat which investors tend to reward with a flurry of stock buying unleashing sizable rallies. But let’s assume that $850 AISC number proves true.

At 2012’s average gold price of $1669 and AISC of $850 per ounce, the junior gold miners would earn staggering profits of $819 per ounce! That is 180% higher than Q4’s levels on a mere 59% rally in gold. So the investment opportunities inherent in the junior gold miners remain vast today as gold inevitably mean reverts far higher out of its central-bank-conjured anomaly of recent years. These stocks will skyrocket!

And the future tense is very appropriate here. Since the junior gold miners are much smaller and riskier than the larger gold miners, which have multiple mines to greatly mitigate operational risks, junior gold stocks tend to vastly outperform their larger peers. Yet as of the middle of this week, GDXJ had only rallied 39.7% YTD compared to GDX’s 42.2%! That means the inevitable amplified junior-gold buying is still coming.

Gold and the gold stocks have blasted so dramatically higher in recent months that traders remain very skeptical about the staying power of these rallies. Unbelievably, sentiment remains quite poor in gold-stock land despite an extraordinary early year! And after any major gold low, investors first come back to the less-risky larger miners before finally growing comfortable enough to redeploy in the riskier junior miners.

Investors can certainly play this in GDXJ, which is the world’s premier junior-gold-stock ETF for good reason. But GDXJ certainly has issues too. With its 52 component stocks, it is seriously over-diversified which will really erode its potential gains. 20 holdings is about as far as diversification can be pushed before it becomes counterproductive. GDXJ is also diluted with those gold-royalty companies and silver miners.

I’ve been professionally analyzing and trading gold stocks for 16+ years now, and each time I delve into GDXJ’s holdings I’m amazed. It contains some companies that have fantastically-bullish fundamentals, the best of the junior-gold-mining world. But its managers also include other companies that leave me shaking my head in disbelief. I wouldn’t touch some of GDXJ’s stocks with a ten-foot pole, they’re really iffy.

So the best gains in the coming years from the super-high-potential junior-gold realm won’t come from an over-diversified and performance-diluting ETF like GDXJ, but from carefully-handpicked portfolios of the best of the junior golds. There are amazing junior gold miners and even explorers out there sporting superior fundamentals that all but guarantee their coming stock performance will trounce that of their peers.

Uncovering the best of the junior gold miners and explorers has long been one our specialties at Zeal. There aren’t many people in the world who’ve spent more time analyzing and trading gold stocks over the past 16 years. And we didn’t capitulate and walk away like most analysts in recent years, we kept on studying and learning. That makes our hard-won knowledge unparalleled and exceedingly valuable, as we won’t have to spend years getting back up to speed like most others.

The bottom line is the junior gold miners thrived even in dark Q4, gold’s worst quarter in 6 years. They were still mining gold at all-in sustaining costs hundreds of dollars below prevailing gold prices even at its secular lows. Their newly-reported strong Q4 fundamentals prove that the deep secular lows that their stock prices suffered were purely emotional, driven solely by traders’ extreme irrational bearishness.

Gold is only starting to mean revert higher as investors aggressively return, a process that tends to run for years once it gets underway. Gold’s new bull market will catapult junior gold miners’ profits radically higher, which investors will eagerly chase. So the battered junior gold stocks are right on the verge of soaring to lofty levels in the coming years that few could’ve imagined in Q4. It’s not too late to get deployed.

The mining industry just finished its annual conference in Toronto (known as the PDAC). As usual, there was more drinking and promoting than substance but a good time was had by all mostly because the metals are popping, especially gold.

Now, good miners are valuable people because mining is not an easy business. But what miners understand about metals markets—especially gold—can be put in a very small place. The Toronto Globe and Mail reported on the conference and the theories discussed there as to why gold is running higher. The village idiot would make more sense.

One theory, suggested by something called Capital Economics, is that gold’s new rush is based on economic optimism. Investors expect a surge in inflation as the U.S. economy picks up steam and so they are looking for a refuge. This is nonsense. Right now, investors are overwhelmingly expecting more of what we have—deflation. Surveys prove it. The Fed is wringing its hands because inflation is too low, contrary to all their projections. And as we have frequently noted, the US economy is on its way into a serious recession.

Another theory is that gold production is peaking, creating a shortfall of product. Goldcorp CEO David Garofalo said he used to be a skeptic about the peak gold theory, but has recently grown convinced. His company’s research shows gold production by major producers could decline 8 per cent between 2015 and 2018. This is beyond idiotic. There are about 5.7 billion ounces of above ground gold supply on planet earth. The industry produces about 80 million ounces per year, about 1.4% of available supply. Garofalo’s expected decline in production amounts to just 6 million ounces annually. If the entire gold mining industry disappeared tomorrow, it would make virtually no difference to the gold price.

However, one guy seemed to get it right. The gold price is rising, said this individual, because there is a rush to safety. “There’s a bit of strength right now in precious metals because all around the world people are losing faith in central bankers,” Randy Smallwood, chief executive officer of Silver Wheaton, told The Globe. That’s right, Randy. Financial markets are no longer a safe place for wealth. Gold is the best way to preserve wealth and has been for a few thousand years. Why? Because gold cannot default. And unlike paper money, gold is not printed by a central bank.

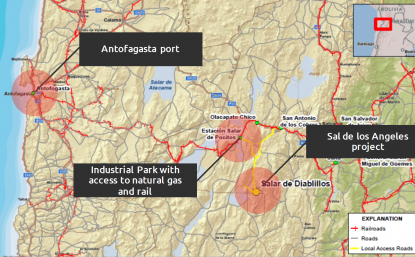

Last week, a promising partnership was announced in the lithium mining space with Aberdeen International Inc. (TSX:AAB), the private equity investor, and lithium pure play up-and-comer, Lithium X Energy Corp. (TSX-V: LIX), entering into a partnership agreement to acquire and develop a lithium-potash project located in Argentina. The partnership agreement outlines that Aberdeen International will acquire 80% of Potasio y Litio de Argentina SA, which owns 100% of the Sal de los Angeles lithium-potash project. This Sal de los Angeles project will be developed and operated by Lithium X over the next two years.

The Sal de los Angeles project has plenty going for it. Not only is it situated in the prolific “Lithium Triangle” in the Salta Province of Argentina, previous operators of Sal de los Angeles have invested roughly C$19 million in the property in exploration, drilling and testing. In addition, a positive Preliminary Economic Assessment (PEA) was prepared for the project in 2011.

We had the opportunity to sit down with David Stein, President, CEO and Director of Aberdeen International, to discuss in more detail the partnership between his company and Lithium X and what he looks forward to in working with Lithium X moving forward.

Partnering with a young, pure play lithium company like Lithium X has to be very exciting. What inspired Aberdeen International to establish a partnership with Lithium X? If possible, can you describe how Aberdeen first connected with Lithium X?

Lithium X basically didn’t exist when we were doing our diligence and negotiations to acquire this project in early-to-mid 2015. Right after closing the deal with Rodinia we started receiving interesting proposals, but we focused on Lithium X over the other opportunities because we felt their strong management team which had previous lithium brine experience in Argentina would be a great fit for the project and their access to capital would bring much-needed exposure to this exciting but under-the-radar asset.

What motivated Aberdeen and Lithium X to target specifically The Sal de los Angeles Project in Argentina in its partnership?

Sal de los Angeles (formerly known as Diablillos) is a large conventional lithium brine, located in a deep basin in a mining-friendly jurisdiction. It has been substantially de-risked technically by previous owners, and has many chemical and physical characteristics that suggest it should be among the lowest cost lithium producers in the world. The PEA completed in 2012 was extremely positive, and we expect to build on that as we move the project forward.

It’s been communicated in the press release published last week that Lithium X will serve as the operator at the Sal de los Angeles Project. In addition to serving in the financing of the project, will Aberdeen International have any operational or developmental responsibilities at Sal de los Angeles? How much of an advisory role will Aberdeen take on in the development of Sal de los Angeles?

Initially Aberdeen will have oversight over the project in two ways. We will have representation on a management committee that will run the project at the asset level. In addition we will initially have two directors on the board of Lithium X. Between corporate oversight and project oversight we will stay heavily engaged in the development of this asset going forward. Our main exposure to the success of the project will be through our large shareholding in Lithium X we receive on closing, so we are motivated to help then any way we can.

Last week’s press release described Sal de los Angeles as a “scalable” project? Can you elaborate on what that means when applied to this particular project? Can you also elaborate on the PEA that was prepared in 2011 and how much of an impact that had in deciding to acquire Sal de los Angeles?

The PEA was a very important part of our due diligence and decision to acquire the project, but of course we looked at how it would be updated now almost five years later. At the time the PEA was produced, lithium and the broader commodities market was still in a bull market and the PEA scoped two scenarios, both of which required substantial capex. What we like about the project, based on more recent internal studies we have done, is that we can build a much smaller, but still very profitable operation, to generate cash flow and de-risk the process before we expand and build a larger project. Unlike hard rock mining, brine production is very scalable based on the availability of capital.

Can you comment on the two year timeline for Sal de los Angeles’ feasibility study and how easy or difficult it will be for Lithium X to complete this study in the allotted time given to them?

While no work has been published since 2012, the previous owners did continue to collect data on the project up until now. Our view is two years will be more than enough time to produce a high quality feasibility study on the project.

Stepping back from this particular project, what do you think will be the most significant drivers of the lithium market over the next five years? How much confidence do you have that the burgeoning lithium battery market will be the most significant driver over the next five to ten years?

Demand will be the most significant driver. The market for large format rechargeable batteries (for example for cars) is growing rapidly, and with no technological alternatives on the near-term horizon, lithium demand should continue to benefit for many more years. That being said, supply will grow, slowly at first, to meet demand, and having a conventional project that can be fast-tracked into production is a huge advantage for Sal de Los Angeles.

Do you see any other lithium ventures besides this partnership with Lithium X in Aberdeen’s near future?

We have received a lot of positive market exposure over the past few months from this acquisition and subsequent deal with Lithium X. We are now seen as expert in the lithium space and we are being approached. We are always opportunistic – so it may make sense for Aberdeen to capitalize on these opportunities in the future.

Thank you very much, Mr. Stein.

According to a report on IncaKolaNews Clive Johnson, CEO of B2Gold has been involved in yet another incident where he let his apparent drinking problem and anger get the better of him. The scene of the incident was the BMO Global Metals and Mining Conference in Hollywood, Florida.

Apparently, during the day, in front of some other people, a female investor attending the BMO conference asked Clive a series of questions that made him uncomfortable. This is to be expected from the investment audience given the performance of the stock over the past 5 years: B2Gold.

Apparently Clive did not enjoy this line of questioning and being embarrassed in front of his peers, especially from a woman. However, despite looking very agitated and annoyed there were no further incidents at the event.

Fast forward a few hours to the open bar party held that evening. Clive, being near a bar where alcohol is served, had naturally drank way too many double vodka waters. And by other accounts was drunk and erratic.

Now we cut to IKN who told it beautifully:

“No one talks to me in that f__king way, I founded this f__king company, I’m a f__king CEO”

- Is there any minimum standard for how public company mining CEOs should behave in public?

- If Clive Johnson has a drinking and aggressiveness problem this bad, should he perhaps be focused on his own health, not running a public company?

2016 may be a noteworthy year for the Canadian-based Arizona Mining Inc. The resource company has made big gains on its Hermosa property, located 80 km southeast of Tucson, Arizona. With an 80 percent share of the property, Arizona Mining has been the catalyst behind the exploration of the site’s resource deposits over the last five years.

“The Taylor Deposit, a lead-zinc-silver carbonate replacement deposit, has a resource of 39.4 million tonnes in the Inferred Mineral Resource category grading 11% zinc equivalent (“ZnEq”) utilizing a 6 percent ZnEq cut off grade calculated in accordance with NI 43-101 guidelines,” notes the Arizona Mining website.

In order to gauge the viability of the site’s potential, “Arizona compiled a wealth of historic data — areas of Hermosa were previously explored by the American Smelting and Refining Co. (Asarco) — and combined it with an airborne versatile time domain electromagnetic survey in 2011,” as Northern Miner reporter, Matthew Keevil, writes.

Upon completing the comprehensive mapping and research phase, Arizona Mining ran a promising drill campaign that showed the potential of the site’s mineral and resource deposits.

“This is a perfect geological story in terms of zonation for these types of deposits. It was really just a matter of getting ourselves oriented and proceeding with the drilling as we move towards what is likely an intrusive source. It definitely looks like we’ve found the right location because we’ve had some wonderful drill intercepts,” said Arizona Mining’s Chief Operating Officer, Donald Taylor.

Arizona Mining is led and founded by Richard Warke, a mining veteran and serial entrepreneur who has founded multiple multimillion and billion dollar resource companies in the past, including Ventana Gold Corporation and Augusta Resource Corporation.

“The metallurgical tests we conducted on the site were very promising,” Richard Warke noted. “We are also invested in a silver-manganese manto oxide development project on another section of the same property.”

A 2013 open-pit pre-feasibility test found probable reserves of nearly 60 million tonnes grading 68 grams silver per tonne and 8.3 percent manganese on site.

Richard Warke also enlisted the assistance of James Gowans, a resource and mining executive with a history in the metallurgical and engineering sector. Gowans, the former CEO of De Beers Canada and co-president of Barrick Gold, sees great potential in the developments at the Taylor Deposit.

“I was retiring from Barrick and moving back to the Vancouver area when I got a call from Richard Warke about the project opportunity, and lead-zinc deposits are sort of like coming home for me,” Gowans said in an interview.

In mid-November 2015, Richard Warke announced Gowans’ appointment to the Presidency of Arizona Mining.

Since coming on board, the deposit numbers have been upgraded and now comprise 39.4 million tonnes in accordance with the NI 43-101 Inferred Mineral Resource category grading.

“This updated resource estimate confirms what the drill results and geology have been telling us for some time – that we have the potential makings of a significant zinc/lead/silver deposit,” says Gowans. “All drill holes completed since we initiated the drill campaign in the fall of 2014 encountered relatively high grade sulfide mineralization over significant thicknesses.”

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |