The recent fall in gold prices has dampened its prospects for 2017 by analysts like BMO Capital Markets, which is forecasting prices to hit $1,175 an ounce next year, down sharply from the $1,413 BMO previously called for. The yellow metal has come under pressure since the U.S. election thanks to a stronger dollar and expectations of higher interest rates in 2017. The Federal Reserve raised rates a quarter point, citing a strengthening economy and better jobs numbers. When rates are climbing, gold becomes a less attractive investment, in part because it’s not yield-producing.

Gold is still up for the year by 7.4%, but earlier in the year, it was up three times that much. Precious metals are highly sensitive to interest rate hikes, which tend to boost the value of the dollar against commodity prices. There could be as many as three interest rate hikes in the U.S. next year, which has increased bullish sentiment for the greenback. Consider that the U.S, dollar hit an all-time high in February 1985 during which time gold hit a bottom of $284.25 an ounce.

The U.S. dollar, as measured against a basket of currencies, has been on a tear since Donald Trump’s victory in the presidential elections, hitting 14-year highs. Conversely, gold on the Comex market in New York has dipped to $1,138.80 an ounce, levels not seen since the beginning of February this year.

BMO’s forecast wasn’t entirely bearish saying, “in our view, global political uncertainty combined with the fragility of economic recovery within Europe and continued quantitative easing continue to be supportive of precious metals when the markets refocus on these systemic risks.” Furthermore, BMO argues that markets have already priced in the impact of the rate hikes expected to take place in 2017.

Underscoring the number of unpredictable factors currently influencing gold, Goldcorp Chairman of the Board and Director, Ian Telfer, who was interviewed by MiningFeeds earlier this year, says 2016 will go down as a volatile year as far as commodity prices are concerned.

“There’s been a number important factors that have fueled that volatility, among them expectations of higher interest rates and some political developments that moved the market,” Ian Telfer commented.

After more than 35 years in the mining industry, Telfer says the business was more fun when prices were $1,800.00 U.S. an ounce, but no one can control that.

“If you’re in business long enough, you learn to ride these market ups and downs, knowing full well history tends to repeat itself,” he added.

Egon von Greyerz is the founder and Managing Partner Matterhorn Asset Management. He told reporter Greg Hunter he is focussed on wealth preservation and sees physical gold as a way to protect value.

“This year, we went up to over $1,300, and now we are back down to $1,100 and change today. If you are buying gold for wealth preservation, you know what you are looking at on a computer screen is not the real price of gold, just the paper price of gold and the manipulation of gold,” he said.

Von Greyerz says the market price has little to do with the true value of physical gold, as far as paper currencies is concerned. Paper is one thing — physical gold is something much more enduring, according to precious metals investors. He says long term investors don’t fret about fluctuating prices.

Precious metals speculators hopeful of a rally got a significant one in the first half of the year and may be feeling disappointed about the drop in price over the last two months of 2016.

For those who are into gold for the long haul, the same economic factors that have attracted investors to precious metals over the decades are still very much in place and will remain so in 2017.

In a little followed– highly volatile niche of the stock market – public venture capital investing, CEO.ca has become an invaluable web site to crowdsource due diligence and discuss speculative investment ideas.

The site was founded in 2012 by Vancouver-entrepreneur Tommy Humphreys as a blog about Canada’s top investors and morphed into a chat application in early 2015, allowing its users to chat and share articles about their ideas.

Some of the Canadian stock market’s biggest success stories of late have unfolded on CEO.ca — like NexGen Energy (NXE.TO), which discovered arguably the richest uranium deposit ever, while its shares soared from $0.30 to nearly $3.00 before gaining backing from Hong Kong’s richest man, Li Ka Shing. CEO.ca was bullish on the company early, and was the first platform to publish a site visit report.

Later, Humphreys interviewed the company’s largest hedge fund holder and the former Chief Mine Engineer of Canada’s largest uranium miner to explain the significance of NexGen’s new discovery.

NXE.TO (Daily – 2 Year)

As the rest of the world caught on, CEO.ca subscribers literally made millions – The NXE channel at ceo.ca/NXE continues to provide a vibrant daily conversation on the outlook for NexGen and Uranium.

Lithium X Energy (LIX.V) is another CEO.ca success story. Humphreys introduced it to CEO.ca readers at $0.15 in October 2015 and shares reached $2.85 by April 2016.

Humphreys — along with a cadre of CEO.ca regulars consisting of both retail and professional investors — pounded the table for dozens of early stage miners that went on to increase in value over 500% over the past year as the four year bear market in commodities ended.

Popular CEO.ca stocks, and those featured by Humphreys, are some of the investing world’s most volatile, and exciting.

Massive Alaskan copper-gold-moly deposit Northern Dynasty Minerals (AMEX: NAK, TSX-V: NDM) was north of $20/share in 2011 and CEO.ca readers were alerted to this idea under $0.33 in Summer 2015 – Shares are back up above $2.50 today on Trump bullishness.

CanAlaska Uranium (CVV.V) moved from $0.12 to $1.50 in the first 8 months of 2016, and is currently on its way back down after disappointing diamond exploration results.

Sabina Gold and Silver (SBB.TO) rallied from $0.35 past $1.75 last year on a new CEO and rising gold prices, but has stumbled below $1 recently on permitting issues.

Cordoba Minerals (CDB.V) was profiled at $0.10 and jumped to $0.90+ following investment from mining legend Robert Friedland and is still going strong.

To quote Humphreys, “2016 was the year we were waiting for.”

I caught up with Tommy over the Christmas holiday to get his take on the resource market and CEO.ca.

CEO Technician: What did you learn in 2016 both as an investor and as an entrepreneur?

Tommy Humphreys: In 2016 you didn’t have to be smart, just long, to have a great year. Simply put, I basically had a five year plan where I wanted to be long this space when it turned and it finally turned this year and it was worth waiting for. Part patience, part dumb luck, and extreme risk tolerance.

Some of the hard lessons learned in previous years helped in 2016, like appropriate position sizing. One of my mentors advised me to always “get your bait back” when the market affords you the chance – take some money off the table. During the summer some of my positions became worth real money, and I took advantage of the liquidity in the market to take some profits and diversify a bit into some lower risk investments. This worked out well as the resource market has cooled off to close out the year.

CEO Technician: What do you think of the market right here and do you think it’s time to begin accumulating again?

Tommy Humphreys: I am not smart enough to know where the gold market is headed — and gold drives most of this sector. But I do know that sentiment has turned from bullish in the summer to despair again. In many cases stock prices have come down 50% since Trump’s election. I’ve had quite a few bids get hit in the last couple of weeks, bids that I didn’t think would get hit. I plan to bet what I can afford to lose in names I know well that have come off. I’m buying in private placements, with sweeteners attached like warrants, as well as in the market when it’s an asset I like.

I still think we’re early in the resurgence in the resource sector; we are seeing signs of a turn in uranium and there’s an article on the Bloomberg home page about gold miners running out of metal – People are beginning to be receptive to pro-commodity themes and there’s a scarcity of good assets.

The amazing thing about the junior sector is that asymmetric returns are possible for those who can stomach the risks. You can become a millionaire on two trades, starting with ten grand. A ten bagger on ten grand is a hundred grand, and a ten bagger on a hundred is a million. Rob Hirschberg’s story illustrates this:

CEO Technician: Tell me some more about the resource sector and what you’ve learned about how cycles evolve.

Tommy Humphreys: The venture market is relatively straightforward. You have a few very high quality discoveries that have seen tremendous amounts of capital invested to de-risk them, as well as good luck. These take many years to unfold. NexGen’s Arrow deposit is an example of this and it will get taken out. That’s the rare success story.

For every NexGen there’s dozens of ‘me too’ companies whose management teams earn a good living merely looking for the next potential strike. These companies tend to have the biggest marketing budgets, and frankly distract investors from the best quality deposits. Most of these plays don’t ultimately work out, but without them, there are no NexGens.

The resource space is more subject to macro themes than other sectors. For example, this year companies that didn’t even have a good project still returned 400-500% from the lows to the peak. Nothing changed in their business or the quality of their projects. The only thing that changed was the market’s perception of the sector they are in. People are always paying up today for the potential of something big tomorrow, so I want to pay as little today to get exposed to potential in the future.

CEO Technician: What is the biggest mistake that an investor can make in the resource sector?

Tommy Humphreys: Emotional purchases, and inappropriate (too large) position sizing.

The first time I ever flew on a private jet (it was a tiny cigarette sized plane with a hilarious bathroom that would make you miss commercial airlines) a famous mining entrepreneur on the flight was raving about a copper junior’s drill results. When the plane landed I bet a huge chunk of my then investable assets on the deal. Classic mistake. The market was already frothy when I bought (2011) and It turned out to be a 75% loss in six months.

Junior stocks also tend to be incredibly volatile, and have massive price swings throughout the year. The smart speculator takes time to buy and sell positions, to get a better average cost, and always has some dry powder around to take advantage of panic selling in the market, which happens from time to time.

CEO Technician: Tell us about CEO.ca and how has your business model and the site’s traffic evolved throughout the year?

Tommy Humphreys: CEO.ca is a dream business for me. I am really excited to be working on a mobile investor product to help people get better faster information.

CEO.ca continues to be subsidized by advertising. We have about the same sized advertising business we had last year and the year before, but the traffic and time spent on the site is up over 600% thanks to a rising market and community content. I would like to be selling more sponsorships, but our small team can only do so many things well, and right now we are more focused on the web product.

We are constantly experimenting. For example, in mid-year we stopped providing an ongoing free publication. It was taking a big chunk of the budget but providing a small fraction of the traffic. Few users complained and traffic has doubled since, which surprised me. I would like to invest more in content and research, but would like a better economic case to do so.

Our focus in 2017 will again be on the product. We want to build the best possible mobile stock market watchlist, with even better data and news feeds and of course, chat. We want to better help people identify quality users and ideas. I’ve been saying for months that we are about to introduce a CEO.CA pro service, and we are. ASAP!

And I’ll continue to seek knowledge and compelling investment and speculation opportunities and will share what I learn with the CEO.ca community.

CEO Technician: What are you feeling bullish about going into 2017?

Tommy Humphreys: I am bullish on DIY (do it yourself) investing and the role of web interfaces to make the experience better. That’s why I keep doubling down on CEO.ca and Spiel, our platform. As far as stock ideas, Continental Gold $CNL, which I have an interest in, is very attractively priced under $3.75, in my personal opinion (not investment advice). The sector needs grade and growth, and companies like CNL are going to deliver, so I want to be there.

CNL.TO (2-Year)

CEO Technician: From a technical perspective the CNL chart is very interesting with a multi-month consolidation underway between ~$3.10 and ~$4.69 – a breakout above $4.70 would target $7+, whereas a breakdown below $3.10 would be bad news.

I certainly learned a lot from this conversation and I would like to thank Tommy for the interview. 2017 looks to be an exciting year for the resource sector and for CEO.ca! Go to CEO.ca for a free account.

DISCLAIMER: The work included in this article is based on SEDAR filings, current events, interviews, and corporate press releases. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. This publication is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.

Original article found here: https://ceo.ca/@Goldfinger/how-a-niche-canadian-stock-market-app-outperformed-the-world-in-2016

1. At this time last year, most gold investors and analysts were predicting lower prices for gold. Many of them were shorting it.

2. The shorts were obliterated, because gold bottomed the day after the December 2105 FOMC meeting. It soared about $330 an ounce, from about $1045 to above $1375.

3. It’s been said that history doesn’t exactly repeat, but it does rhyme. On that note, please click here now. Double-click to enlarge this daily bars gold chart.

4. Gold has a cyclical tendency to decline ahead of a rate hike, and rally after it is announced.

5. This time, the US election may delay the rally, but create one that is bigger and more sustained than the rally of 2016. Here’s why:

6. Republican parties have cyclically been associated with significant US dollar downtrends. The next presidential inauguration occurs on January 20, 2017.

7. Donald Trump has repeatedly stated that he wants a lower dollar. He’ll have control of both the senate and the congress, putting him in a position of tremendous power to impose his will on US markets.

8. Please click here now. Double-click to enlarge. Most technicians are now wildly bullish on the US dollar index.

9. They are excited about what appears to be an “upside breakout”, and there’s no question that the US dollar index could move higher until inauguration day.

10. Note the RSI non-confirmation with the price on that daily bars US dollar index chart. The dollar’s technical strength is weakening quite dramatically.

11. For a big picture view of the dollar’s price action during the past few presidencies, please click here now. Double-click to enlarge.

12. As rates rise, and Trump increases government debt while cutting taxes, the US government’s credit rating could get downgraded, adding more downwards pressure on the dollar.

13. Janet Yellen initially endorsed a “high pressure” economy, but after the latest FOMC meeting she said that she’s not necessarily looking for easy money policy to continue.

14. That’s superb news for inflation enthusiasts, because higher rates incentivize banks to move money out of government bonds and into the fractional reserve banking system.

15. Trump’s tax cuts will further incentivize the banks to make loans to the private sector, and move even more money out of the US government bond market.

16. The bottom line is that Janet Yellen can create a higher pressure economy with rate hikes than without them. With Donald “The Golden Trumpster” in power, inflation may rise much faster than anticipated, regardless of what Janet does.

17. I expect US money velocity to bottom by the summer of 2017 and begin a long term bull cycle, mainly because of the policies of both Trump and Yellen.

18. Gold stocks can dramatically outperform gold in that environment. On that note, please click here now. Double-click to enlarge this GDX daily bars chart.

19. There’s no question that GDX is in a downtrend. The pattern of lower minor trend lows and lower highs is what defines a downtrend in any market.

20. Please click here now. Double-click to enlarge. That’s another look at the GDX daily chart. In strong uptrend, the RSI oscillator tends to oscillate between the 70 area and 50. In a downtrend, RSI tends to oscillate between 20 and 50.

21. Amateur investors tend to be obsessed with trying to figure out whether a market is making a major bottom, top, or about to accelerate its trend. I would argue that such an obsession doesn’t build wealth that is sustained. It’s a subtle form of gambling, and gamblers tend to lose money on an ongoing basis.

22. Rather than trying to gamble on whether GDX will continue its current pattern of lower highs and lower lows or not, my suggestion to the world gold community is to simply wait for a pattern of higher highs and higher lows to appear. That’s what defines an uptrend.

23. Please click here now. Double-click to enlarge. That’s a third view of the GDX daily chart. There is support in the $17 – $18 area, and an important buying area. Importantly, this chart shows that there was no uptrend in place in the days following last year’s rate hike. GDX declined to a final low in January of 2016, but it wasn’t until the spring that an uptrend was apparent. The bottom line:

24. Professional investors have a lot of patience, and amateur investors need to focus on developing it. It’s highly likely that a new and sustained uptrend in precious metals will begin, once the weak dollar policy of the Trump administration becomes clear!

Stewart Thomson of Graceland Updates, Guest Contributor to MiningFeeds.com

Gold is one of the high profile assets and it occupies a strategic position in the markets because of its safe-haven properties. You’ll be hard-pressed to find a diversified portfolio that doesn’t have exposure to gold. More interesting is the fact that investors often flock to gold during times of increased volatility and uncertainty in the economic landscape. In fact, the price of gold tends to soar when the equity markets experience weakness in stocks.

However, the current trading price of gold often prices many retail traders and investors out of the gold trade. For instance, gold currently trades around $1,165 an ounce and a $10,000 investment would buy you a mere 8.6 ounces before commissions. Hence, many investors and traders who could have profited from gold are often forced to stay on the sidelines because they can’t afford the investment. This article however provides insights on how to trade gold without owning the bullion.

Meet gold binary options

Gold binary options are derivative assets that allow you to profit on the price movements of the yellow metal without you buying or owning the bullion. The binary options are derivative assets in the sense that you are trading the contracts, which helps you to track the price movements in gold at a fraction of the cost requirements for investing in gold bullion.

The first reason retail traders love trading gold with binary options is that it allows you to access the gold markets without an exorbitant trading capital. Secondly, gold binary options allow you to trade gold in a “controlled” environment where you don’t need to worry about massive reversals that could lead to the loss of previous gains. Thirdly, gold binary options have a definite payout so that you’ll know how much you stand to gain even before you place your trade.

Major types of gold binary options

Touch/No Touch Binary Trades

In this kind of binary option trades, you’ll need to place a trade on the possibility that the price of the precious metal will (or won’t) get to a predetermined price known as the strike price. When you place a trade on the possibility that the price of gold will reach that strike price – you are placing a Touch binary trade. If you place a trade on the submission that the price of gold won’t reach that strike price, you are placing a No-Touch binary trade.

The Touch/No Touch option has different variations such as the double touch option and double one touch option. The most important thing is that the yellow metal should trade in line with your forecast before the contract expires.

In/Out Binary Trades

This kind of gold binary option trade often becomes prominent when the yellow metal is trading within a range. The upper trend line on the trading chart could form a resistance point while the lower trend line will form a support level. Binary option traders with exposure to gold could place In/Out binary option trades on the possibility that the yellow metal will stay within the range or get out of the range before the expiry of the contract.

You’ll place an In trade if you expect the yellow metal to stay within the range over a certain period – you’ll earn a predetermined payout if the bullion stays within that range. You can place an Out binary options trade on the possibility that gold will breakout above the resistance trendline or breakdown below the support trend line – you’ll also be rewarded if the trade follows your forecast.

High/Low Binary Trades

This binary options trade is similar to the traditional options that stocks traders use to hedge their portfolios. In the High/Low gold binary option trade, you’ll place trades on the possibility that that the yellow metal will end the session higher or lower than its “current” price before the end of the session.

If you place a High binary trade, you are putting your money on the possibility that the price of the yellow metal will be higher than the strike price when the contract expires. If you place a Low binary trade, you’ll put your money on the possibility that the price of the yellow metal will be lower than the strike price at the end of the session.

A word or two on brokers

It is important that you choose a broker that will make your binary options trading simple, stress-free, and profitable. You might want to read reviews of different brokers in order to know the trusted binary options brokers in the market. For instance, most brokers offer web-based trading platforms while some brokers often go the extra mile to provide a mobile app. Beginners might also want to sign up with a trader that has a loaded resource center and real-time assistance support system.

You might also want to choose a broker based on their reputation for paying bonuses and payouts. It is also important that you choose a regulated broker so that you can have a third-party endorsement of their trustworthiness.

This article is written by guest author, Luis Aureliano.

On October 27, 2016 Dajin Resources Corp. (“Dajin”) (TSX-V: DJI) (OTC: DJIFF) (Germany: C2U1) announced the completion of a share purchase agreement with Lithium S Corp. (“LSC”), granting LSC the right to earn a 51% interest in the Company’s South American subsidiary, Dajin Resources S.A. (“Dajin SA”). LSC can earn 51% with a cash payment of C$1.0 M (paid) and by incurring expenditures of C$2.0 M on mineral concessions, (or concession applications), held by Dajin S.A. In addition, LSC injected a further C$500,000 by subscribing to common share units in Dajin. Importantly, Dajin now has virtually no capital requirements in Argentina until LSC earns its 51%. Therefore, the C$1.5 million in cash from LSC can be used to fund the Company’s activities in Nevada. More about Nevada later, this article is about activities in Argentina.

As a result of this transaction, Dajin (Market Cap $18 M) has graduated from one of about a dozen publicly-traded, non-producing lithium juniors in Argentina, [up against peers like Lithium Americas [TSX: LAC] (Market Cap $235 M), Lithium X Corp [TSX-V: LIX] (Market Cap $145 M) and Neo Lithium Corp [TSX-V: NLC] (Market cap $85 M)], to part of a larger, highly prospective lithium brine play. Dajin SA has hitched its wagon to LSC, who is working with by privately-held Enirgi Group, which in turn is wholly-owned by The Sentient Group of Global Resources Funds. The Sentient Group has over $2 billion in assets under management, mostly in metals, minerals & energy assets across the globe.

Who is LSC Corp? Who is Enirgi Group?

LSC was co-founded by mining entrepreneurs and financiers Stephen Dattels & Michael Beck for the express purpose of acquiring, exploring and advancing green field lithium brine projects in the heart of the, “Lithium Triangle,” in northern Argentina. Dattels & Beck have considerable financing and deal making expertise, vast experience in natural resources, and a track record of successful ventures around the world. LSC has entered into option agreements on a number of mining properties and exploration permits (including concessions held by Dajin SA). LSC is in an ideal position, the right place at the right time, in collaboration with a premier partner, Enirgi Group.

Enirgi Group is a global, diversified industrial and specialty chemicals company that owns and operates a portfolio of world-class assets around the world. Management has publicly announced intentions to make a major move into lithium through the Salar del Rincónproject, its advanced lithium project in Argentina. As part of Rincón, the management team plans to build and operate a 50,000 tonne per annum lithium carbonate processing plant at Rincón, located in the province of Salta, Argentina. This project, featuring Enirgi’s proprietary Direct Extraction Process (“DEP”) technology, is backed by a Definitive Feasibility Study boasting an after-tax NPV(9%) of $1.36 billion.

As a frame of reference, Rincón would be approximately 3 times the size of Orocobre Ltd’s current operational target of 17,500 tonnes/yr. LCE. Further, Enirgi believes that the quality of its processed lithium products is superior to that of most other’s.

Since 2008, approximately $200 million has been invested in the Rincón Project, including the construction of a commercial-scale demonstration plant. The Group’s Chemicals division employs over 85 individuals on site and in Salta, Argentina. The project is supported by a team of over 100 mechanical, electrical & chemical engineers from Enirgi’s Innovation Division in Sydney, Australia. Enirgi Group,

“…is pursuing its longer-term plan to increase its production capacity by scaling the Rincón Project into a larger Regional Processing Facility that will utilize Enirgi Group’s game-changing DEP Technology for the development of the Salar del Rincón…” — July 21st Press Release

More important for LSC & Dajin is the plan to,

“…leverage the application of the DEP technology to other lithium brine resources in the region. Strategies may include applying DEP Technology at other lithium salars… and/or securing and supplying brine feedstock for the Rincón Project from other lithium brine salars.” — July 21st Press Release

Besides FMC Corp [NYSE: FMC], SQM [NYSE: SQM]/LAC and Orocobre, there’s probably no other company capable of becoming a major player in lithium, in Argentina, in the next 3-4 years. This simple fact is very encouraging for LSC, and by extension – Dajin SA’s concessions in the Salinas Grandes, see map.

But enough about Enirgi, how does this all pertain to LSC? To Dajin?? Here’s the key. Last summer, Enirgi and LSC entered into a MOU with respect to a strategic collaboration on the exploration and development of their combined lithium properties, exploration permits, provincial concessions (excluding Salar del Rincón Properties).

Therefore, LSC’s raison d’être is largely to support and compliment, by prudent exploration, Enirgi’s grandiose lithium dream. Next in line on the gravy train is Dajin. LSC needs to have viable lithium deposits at the ready to feed Enirgi’ ascent to lithium stardom. And, Dajin SA is playing a significant role by contributing a sizable portfolio, one that enhances what LSC brings to the table, for the benefit of all parties. The portfolio contains 93,000 hectares (230,000 acres), within 25 concessions, in Salinas Grandes, Argentina.

The Dajin story unfolding in Argentina reminds me of Lithium Americas’ announcement in March 2016 of a JV with giant lithium producer SQM. When that news hit the tape, my initial reaction was lukewarm, at best. I thought that LAC selling half its flagship Cauchari-Olaroz project was a great deal for SQM, but not necessarily for LAC. However, I failed to appreciate the tremendous benefits SQM is contributing to the project by providing critical financial backing and very substantial technical / managerial experience.

The probability of LAC owning 50% (instead of 100%) of a prominent mine soared, as did the stock price.

I see a similarity in LSC’s vote of confidence in Dajin’s Argentinian lithium portfolio. The financial terms mentioned in the opening paragraph are important, but even more important is that the probability of Dajin ultimately owning 49% (instead of 100%) of an economically viable project, is considerably higher, and the Company probably has at least a year before it will need to contribute a meaningful amount of cash, if warranted. Yet, Dajin’s stock price is down 36% (in line with the sector) since the August 8th announcement of the now completed LSC/Dajin transaction.

LSC & Dajin — betting heavily on Enirgi Group, not a bad bet!

If the Rincón project is successful, the processing plant could potentially be expanded to accept additional lithium brine feedstock, or modular DEP plants could be built on the concessions found to have economically viable resources. Enirgi has effectively outsourced the lithium exploration and development business, (outside of its own Rincón project), to LSC. Any property that’s acquired, optioned or controlled by LSC, (including properties controlled by Dajin SA) will be prudently advanced.

Therefore, instead of butting heads with a growing list of lithium juniors with designs on Argentina, Dajin now has a clear path towards potentially monetizing its highly prospective concessions. As mentioned, LSC is responsible for the first C$2 million of project expenditures and has already banked C$1.5 million in cash from LSC.

At the risk of beating a dead horse, to recap, if Enirgi and LSC make a big splash in northern Argentina, Dajin will be in the enviable position of being able to raise capital on favorable terms to maintain its 49% stake, or monetize some or all of it. In the meantime, Dajin does not need to deploy additional capital in Argentina. Instead, management will spend a lot more time and resources in Nevada, where it has 3 attractive prospects, Teels Marsh, Gabbs Valley & Alkali Lake.

More on these projects in my next update of Dajin Resources Corp. (“Dajin”) (TSX-V: DJI) (OTC: DJIFF) (Germany: C2U1).

December 2016 Corporate Presentation

Interview of Dajin Director Catherine Hickson (Audio)

Disclosures: The contents of this article are for informational purposes only. Readers fully understand and agree that nothing contained in this article by Peter Epstein about Dajin Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered, in any way whatsoever, implicit or explicit investment advice. Further, nothing contained herein is a recommendation or solicitation to buy, hold or sell any security. The content contained herein is not directed at any individual or group. Peter Epstein and Epstein Research [ER] are not responsible, under any circumstances whatsoever, for investment actions taken by the reader. Peter Epstein and [ER] have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Peter Epstein and [ER] are not directly employed by any company, group, organization, party or person. The shares of Dajin Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers of this interview that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned shares of Dajin Resources and the Company was a sponsor of Epstein Research. Any comparison between or among stocks is for illustrative purposes only and should not be taken as fact or relied upon. Readers understand and agree that they must conduct their own due diligence above and beyond reading this interview. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & [ER] are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for its completeness. Mr. Epstein & [ER] are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and [ER] are not experts in any company, industry sector or investment topic.

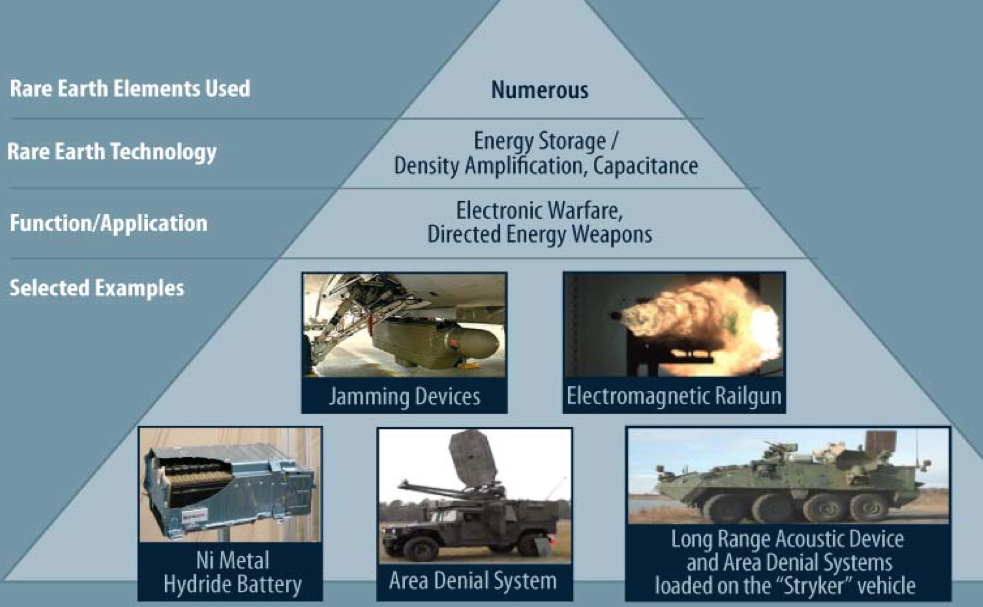

Ucore Rare Metals [TSX-V: UCU] / [OTC: UURAF] continues to make confident strides in the commercialization of its Molecular Recognition Technology (“MRT”) platform, contained in an enterprise to be co-owned between Ucore and IBC Advanced Technologies, Inc. Key to the enterprise is that it has exclusive rights to deploy the entire SuperLig®/MRT catalogue of metals separation products to monetize tailings applications anywhere in the world, in addition to mining and recycling applications in the REE and PGM sectors.

With over 60 SuperLig® products already developed for a wide range of metals, the opportunity is a large one, and Ucore is pursuing a technology licensing plan to get MRT in to the maximum number of applications. Diverse applications include inserting MRT directly into operating facilities (and/or bolting MRT onto the back-end waste handling function), recycling, remediation and, “urban mining,” which entails separating high-value metals (“HVMs”) such as Heavy REEs, PGMs, lithium, cobalt and tungsten.

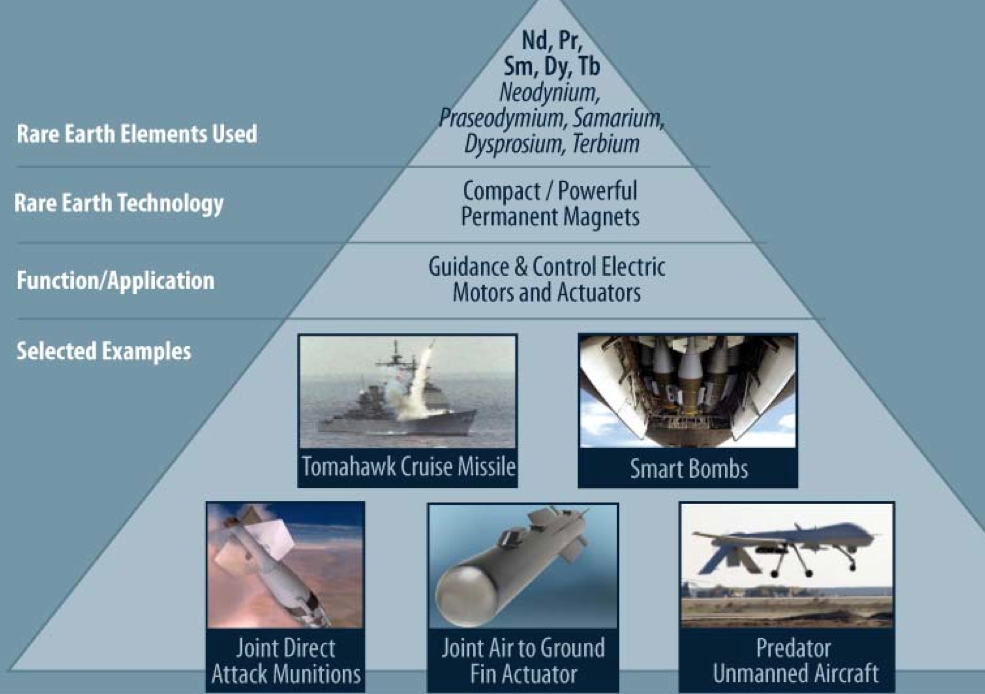

There are a handful of mission critical REE, green energy & high-tech metals that could become difficult to reliably secure under certain adverse circumstances. Some examples from my review of various (mostly government agency) reports, the REEs dysprosium, yttrium, erbium, europium, terbium pop up a lot. Oil was of crucial importance in last century’s wars, will electric battery components and REE be this century’s show stoppers? It’s no secret that in addition to an insatiable need for various REE, the U.S. Department of Defense (“DOD”) is front and center in the analysis and adoption of EVs for military, national defense, homeland security & communications activities.

In addition to its broader vision to license MRT technology in to multiple metals sectors, Ucore has a near term agenda focused on accessing some of the highest demand HVMs in the U.S. On November 15th, the Company announced it has engaged in planning & development of a Strategic Metals Complex (“SMC”), capitalizing on the MRT platform developed for the recently completed SuperLig One pilot plant in Salt Lake City. The SMC will be a commercial production plant designed to separate feedstock containing critical rare earth elements /metals (“REE”) (e.g., dysprosium, neodymium, terbium), and PGMs (rhodium, palladium & platinum).

This is proof that Ucore is ready to roll, detailed engineering work is well underway. Initial feedstock is expected to be sourced from, “recycling, swarf and tailings-generation partners in the automotive and REE permanent magnet industries.” Ucore technology partner IBC has extensive experience in this area, for instance in PGM applications used successfully by operators such as Impala Platinum in South Africa. The potential economics for MRT plant placements are impressive. Based on my experience with similar licensing platform agreements, annual royalty fees of between 2% and 5% are fairly common. That, and an upfront licensing fee, plant design & maintenance fees, and recurring revenue from the sale of proprietary materials and services. In my opinion, mandates with large companies like Teck Resources (NYSE: TCK) could easily have Net Present Values in the tens of millions of dollars.

President/CEO & Director Jim McKenzie commented,

“Our pilot facility provides a blueprint for construction of a new generation of SuperLig® separation facilities to add to already-existing MRT installations around the globe. This Strategic Metals Complex represents not just a transition by Ucore towards near-term production and revenue, it represents a reaction to a very real domestic need for high-purity energy metals. In turn, the SMC represents a significant progression for Ucore, capitalizing on the innovative design of SuperLig®-One, and leveraging this platform in to full scale production.”

My interest in Ucore is reinvigorated. Simply stated, MRT is faster, less energy intensive, generates fewer emissions and waste, does not use solvents or toxic chemicals, has a smaller surface and environmental footprint, requires less cap-ex and will enjoy lower op-ex. Now here’s where things get more interesting. While an important theme underpinning Ucore remains the same, I believe it takes on new urgency with the election of Donald Trump. That theme being– Security of Supply of indispensable REE and critical green energy / high-tech metals. Few may realize that China not only controls, but completely dominates, the global supply of rare earth oxides, includes mining, processing & refining.

It’s reported that over 95% of pure, separated REE produced last year were in China, REE in the hardware and software applications enabling National & Homeland Security and the capability of conducting both offensive and defensive military operations.

In addition to the paramount importance of knowing where one’s electricity, food & water come from, and the risk of supply disruptions therein, knowing which REE and other HVMs our modern society cannot live without, is necessary and prudent. In World Wars I & II, people knew exactly which materials were essential to the war effort, tin, rubber, aluminum & steel, among others…. Does the West need to enter into a “hot” war to learn which metals are in fact critical?

Which critical metals will be most vulnerable to steady, secure supply to the U.S. DOD and DOE?

Am I being alarmist with the talk of WW III? Perhaps, but no matter what the future holds, I think that Ucore Rare Metals is well positioned to thrive in a world becoming more dangerous and more dependent on technology, with no end in sight. Investment funding for companies like Ucore are increasingly becoming available, for example this “Innovation Summit” organized by “America’s largest angel investment fund, representing over $2.5 billion in early-stage, high-risk technology funding...”

Regardless of what readers think of Mr. Trump, he has explicitly stated things that favor larger military budgets. Without further commentary, here is what he has said, 1) Japan and Korea should strongly consider defending themselves 2) western Europe is not paying nearly enough for the military protection provided by the U.S. 3) given items 1, & 2, the belief that the military has been meaningfully underfunded and is in desperate need of a face lift. In addition to National Defense considerations, remember that Trump is gunning for China as well.

A larger U.S. military budget correlates well with larger military expenditures around the world. That’s why a group of 6 well known military and homeland security stocks including Raytheon (NYSE: RTN), Lockheed Martin (NYSE: LMT), Harris Corp (NYSE: HRS) L-3 Communications (NYSE: LLL), Rockwell Collins (NYSE: COL) and General Dynamics (NYSE: GD) is up 15% since November 8th, vs. the S&P500, up 4%. Why should it be any different for Ucore, on the leading edge of new, green, high-tech platforms that will shape global geopolitics and our technology paradigm for decades?

Finally, readers might recall that President-elect Trump said he will designate China a “currency manipulator,” and slap a 45% tariff on Chinese imports. Given that country’s giant pile of U.S. Treasuries, and its control and utter dominance of all things REE, a trade war with China could be a dangerous undertaking.

As has been reported in detail by Ucore, REE and hard to replace or substitute HVMs are essential ingredients in a large and growing number of DOD & Department of Energy (“DOE”) applications, not to mention in mining and industrial settings. Also contained in prior Ucore press releases is evidence that its MRT platform has been proven and independently verified, at pilot scale and ready for production scale in the near future.

What makes MRT superior to other proposed solutions? Relying heavily on last century’s separation technologies like solvent extraction is an ill-advised and increasingly non-viable strategy, especially in China. It’s impossible to ignore the horrendous air and water pollution, perhaps the worst on the planet, in Chinese cities. Not only is China de-emphasizing coal and going all-in on nuclear power, it already leads the world in wind and solar power and the electrification of its transportation sector. MRT is not only greener, it will deliver desperately needed security of supply to global end users, especially in the U.S.

Just-in-time processing and supply chains are the norm. Turning complex facilities and integrated systems off, and on, is time consuming, costly and introduces unnecessary operating risks. It’s alarming that U.S. agencies, both inside and out of the DOD, not to mention powerful industry trade associations, have failed to address this critically important issue. The ongoing failure to obtain some semblance of security of supply is a clear and present danger.

Conclusion

The implications for REE mining and production outside of China, are profound. Ucore Rare Metals [TSX-V: UCU] / [OTC: UURAF] is in a prime position to 1) benefit from higher REE & HVM prices 2) be part of the solution of the rallying cry for security of supply, and 3) address increasing demand for products and technologies that accelerate the game-changing shift away from fossil fuels.

All roads lead to greater use of select metals like the ones mentioned, but also greater use of metals that galvanize steel and can be used in next generation alloys. However, perhaps most important to recognize, is that some of the REE/HVMs most in demand and most difficult to secure in the future, might not be on anyone’s radar screen today. That’s why the flexibility afforded by over 60 SuperLig® products embedded into Ucore’s flagship enterprise with IBC on MRT is an increasingly important and valuable asset.

ETP inflows again commandeered the gold investment market in Q3. Demand for bars and coins was, almost without exception, weaker across all markets.

Investment demand in Q3 totaled 335.7t, 44% up year-on-year and 8% above the five-year quarterly average demand for the sector of 311.4t. Year-to-date investment reached a record of 1,389.2t, 10% above the previous Q1–Q3 high of 1,268.5t from 2010.

The motives behind, and geographical distribution of, inflows into ETPs are discussed in detail in Key themes. Momentum behind these inflows has tapered off slightly, but Q4 has still seen marginal inflows. In the context of a 10% fall in the price, this highlights that price momentum is secondary to the strategic motives underpinning investment. Overall, we maintain a positive outlook on the sector, particularly given the fragile macroeconomic backdrop, such as negative interest rates and geopolitical risks.

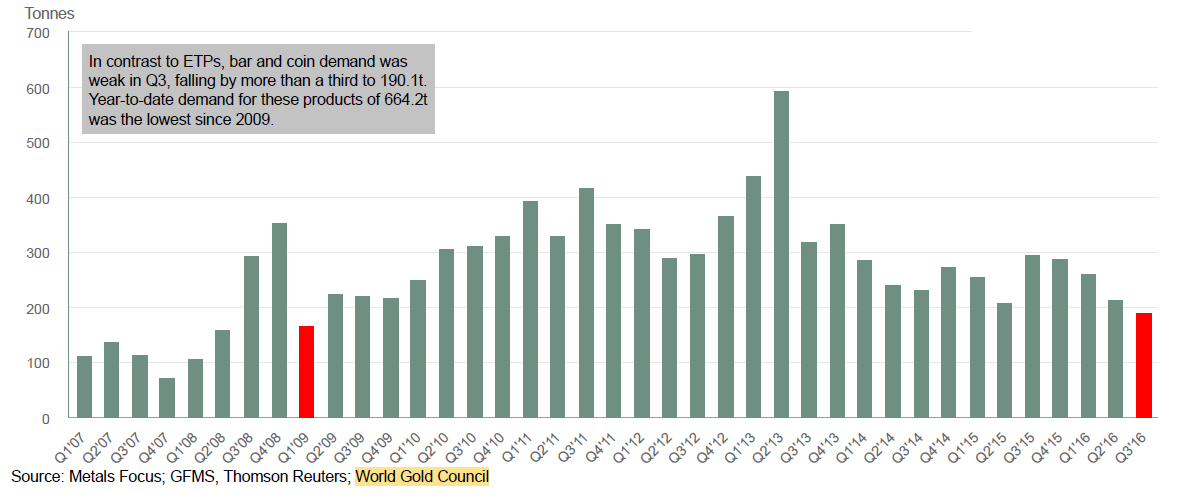

Bar and coin demand was contrastingly weak in Q3, falling by more than a third to 190.1t. Year-to-date demand for these products of 664.2t was the lowest since 2009. The high gold prices that were a major cause of weakness in the jewellery sector were similarly off-putting for investors, and the lack of momentum in the price during the quarter was a further deterrent. Market research shows that investors look for a low, or rising, gold price as a signal to buy – both of which were notably absent in the third quarter. But the price drop in the opening weeks of Q4 has provoked a response in some markets. Our Focus Box ‘Q4 Update: impact of prices on consumer demand’ provides further detail on investors’ perceptions of – and reactions to – recent price moves.

Chart 8: Retail investment demand has been weak

- Year-to-date retail investment demand for bars and coins is at its lowest level since 2009.

- High gold prices were a major cause of weakness across most markets. Weak demand in India was compounded by the government’s focus on curbing cash transactions.

- Demand may improve in Q4; the price drop in the first week of October resulted in an uptick in retail investor interest in the US, India and China.

Indian bar and coin demand very weak in 2016 to date; Q4 holds better prospects

Investment demand fell for the third consecutive quarter in India, down 30% to 40.1t. At just 100.7t, year-to-date

demand for bars and coins is the lowest for 12 years, below that even of 2009 when the first quarter saw negative investment for the only time in our time series. Investors already reluctant to buy at such persistently high gold prices, were also put off by the government’s focus on curbing cash transactions. Demand for gold bars was more greatly affected by the measures than that for gold coins, as cash remains one of the primary means of purchasing gold bars. Surging stock markets bumped gold further out of the spotlight.

Despite the depressed market, there is a growing market for branded gold coins in India, which – going forward – should support investment demand in India. The Indian Gold Coin, from MMTC has sold 185kg since its launch in November 2015 and is currently available through around 300 outlets. Similarly, the Tola Coin will appeal to customers who look for purity and brand. In another move, IBJA launched a personalised coin this festival season. IBJA has launched a store in Mumbai and wants to set up 100 stores in the next three years. Our report ‘India’s gold investment evolution’, produced in conjunction with MMTC, takes a detailed look at the market for branded gold coins in India.

European investment sank to an 8-year low, but net demand masks underlying activity

Europe’s bar and coin market failed to replicate the flows pouring into ETPs in the region. Investment in bars and coins fell to an 8year low of 37.6t in Q3, down 37% from the same period last year. The year-on-year decline is all the more marked for the fact that Q3 2015 was the strongest third quarter for four years, as investors responded to the falling gold price. Nevertheless, bar and coin demand during the most recent quarter was unarguably anaemic – 38% below the five-year quarterly average of 61.1t.

The weakness is largely reflective of a sharp bout of selling in July. This was triggered by the jump in the gold price – the short-lived response to the UK’s Brexit vote – which saw the euro-denominated gold price reach three year highs. The price based in sterling was even more marked, due to the selloff in the pound in the immediate wake of the referendum.

On the face of it, the 11% decline in UK bar and coin demand seems to indicate that investors in that market were inactive. This was far from the case. Gross levels of both buying and selling were elevated during the quarter, indicating a heightened level of activity in trading gold bars and coins. The two sides largely cancelled each other out, creating net demand of just 2.4t for the quarter. This pattern was repeated across the region: selling back of existing holdings swelled the stock of bars and coins available for purchase in the secondary market. This helps to explain depressed sales of newly minted coins.

The focus among French investors on selling into the price rally, resulted in a second consecutive quarter of net negative investment. Year-to-date investment is marginally negative at 0.2t. A negative fourth quarter would result in annual disinvestment in France for the first time since 2008, prior to the global financial crisis.

For Q1–Q3, demand is 14% down on 2015 and consequently Europe has slipped to second place in market size: on a year-to-date basis, China’s bar and coin market is the world’s largest.

Bar and coin investment still weak in China; funds diverted to ETPs

Retail investment in China stabilized after the washout of the preceding quarter, but the decline from 2015 levels was acute. Q3 demand of 41t – down 23% – equated to a year-to-date total of 162.5t, almost bang in line with last year.

Bar and coin purchases from commercial banks and large retailer chains dropped sharply in the third quarter: data from a couple of commercial banks show sales of gold falling by, on average, 50% year-on-year. GAPs saw net redemptions as the 2year high in the price in early July prompted a spike in liquidations.

The decline in demand was partially offset by direct individual withdrawals from the SGE, which remained elevated – many multiples of the withdrawals in Q3 2015. But more permanent attrition resulted from investors diverting funds to ETPs. Lower transaction costs and the introduction of online platforms and mobile applications offering access to ETPs with minimal entry requirements attracted many erstwhile bar and coin investors.

As well as a reticence to buy gold at high price levels, lower disposable incomes were a key factor underlying the weak demand picture.The sluggish economy, lower take home incomes and rising housing outlays have fostered a desire among Chinese households to build a cash buffer. The pressure of rising real estate prices on disposable incomes is a function of the degree to which property is used as an avenue for investment in China. Research by Knight Frank, in constructing their Prime International Residential Index, put Shanghai as the third fastest growing property market globally.

The fourth quarter has started on a more positive note in China, thanks to the price drop in early October. Consumers were swift to respond to lower prices and remain alert to any further buying opportunities.

Heightened price sensitivity still a feature of the US market

US demand for gold bars and coins almost halved from Q3 2016, down 43% to 17.4t. The year-on-year comparison in US investment was never going to be easy; Q3 2015 was an exceptional quarter which saw demand jump as the gold price dipped. Putting the recent quarter into context, it is 5% stronger than the five year quarterly average of 16.6t. And year-to-date demand is 14% ahead of last year at 62.8t.

Indicative of the fact that US retail investors remain keenly aware of price fluctuations in gold, September saw a surge in sales as bargain hunting emerged on the dip down in prices towards US$1,300/oz. And October has continued in similar fashion, with sales of Eagle coins surging thanks to the weaker gold price.

Middle Eastern investment sinks to record low

Paltry levels of Middle Eastern demand were largely a function of weakness in Iran. This is partly due to a downwards revision in our data series to reflect a shift from investment to jewellery purchases amid a dearth of newly minted gold coins: indeed, the market faced net disinvestment in the face of high gold prices. But demand in other regional markets was also far from healthy. Bar and coin investors faced similar challenges to jewellery consumers: high gold prices, lower oil revenues squeezing incomes and political instability all contributed to the lowest level of regional investment in our time series of just 1.9t – a fraction of the 19.7t five year quarterly average.

The 47% year-on-year drop in Turkey’s bar and coin demand was partly the result of last year’s strong Q3 base. Demand has bumped along in the range of 4–5t since the beginning of last year, with the exception of the third quarter when political turmoil coincided with lower prices to spark a rush for safe haven holdings of gold. Demand is expected to continue in a similar vein for the rest of the year, given very high local prices (due to lira weakness) and the persistent negative geopolitical climate.

Investment in the smaller Asian markets shelved in the face of high prices

Retail investment demand across the smaller markets in Asia stalled in the face of higher gold prices. Investors viewed the price hike as temporary and held off from making any purchases of bars and coins in anticipation of a correction back towards US$1,300/oz. A 4 relatively benign inflation environment across markets including Thailand and Indonesia also undermined the motive for buying gold as an inflation hedge. Fourth quarter demand is expected to pick up as October’s price drop offered a good buying opportunity for those waiting for lower prices.

Footnotes:

1. Read more: https://www.gold.org/mygoldguide/newsandtrends/indiangoldcoin

2. Read more: http://www.businessstandard.com/article/ptistories/ibjagoldtosetup100storesin3years116101200503_1.html

3. Read more: http://www.gold.org/research/indiagoldcoin

4. Knight Frank, The Wealth Report 2016.

This content provided by the World Gold Council

Last week we wrote that the 2016 bull market in Gold and gold stocks had gone off course. It had moved too far out of the historical boundaries to remain a bull market. There was also other evidence of such including but not limited to rising real yields. Gold’s last hope was to hold $1200-$1210 and rebound back to the highs. It has broken bull market support ($1200-$1210 and $1230) and could be on its way to $1050 in the next few months.

The monthly candle chart of Gold is shown below. Gold is down 7.4% on the month and has sliced through the important support at $1200-$1210 as well as the 20-month moving average at $1201 and the 40-month moving average at $1231. The 40-month moving average has been an excellent primary trend indicator throughout Gold’s history. There is a little support at $1150 but nothing standing in the way of Gold heading for a retest of its low at $1050.

Gold is not only weak in nominal terms or US Dollar terms but it is showing weakness in real terms. Below we plot Gold against foreign currencies (the US Dollar basket) and the NYSE, a broad equity index. Gold/FC has been strong for several years but it has lost support and looks headed lower. Meanwhile, Gold/NYSE lost support at its 400-day moving average and could retest its 2015 low.

Gold is clearly broken but its decline is due for a pause. Gold has been strongly correlated to the bond market which may have made an interim low last Wednesday. Also, the gold stocks are showing a positive divergence. Even as Gold lost $1200/oz and traded down to $1171/oz, the gold stocks (GDX, GDXJ) did not make a new low. Furthermore, the market has now fully priced in a quarter point rate hike in December.

The odds favor a rebound in the days and potentially weeks ahead. Traders and investors should use the rebound to de-risk their portfolios, raise cash and hedge if the opportunity presents itself. Don’t think about buying until we see sub $1080 Gold and an extreme oversold condition coupled with uber bearish sentiment. For professional guidance in riding the bull market in Gold, consider learning more about our premium service including our favorite junior miners for 2017.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |