By Jennifer Schell, B.COMM, MBA

Investment Advisor

Making it Rain!

This morning I was reading the paper on my way to the office and I learned that gold was formed by a neutron star collision, resulting in pressurized debris that rained down onto our Earth— fresh from the Universe. This is why people are so star struck with gold!

As an industry, mining is extremely capital intensive and relies heavily on investments from the public to make their projects come to fruition. These projects cost millions upon millions to fund. But as an investor, it’s difficult to know how to differentiate a good project from one that can leave investors broke and jaded.

Skim the corporate presentation and they will generally break this out for you. Here’s what you need to know:

| Sound Capital Structure | |

| Shares Outstanding:The shares indicate the ownership of the Company. | Usually ranges from 60 Million to 150 MillionBe on the lookout for the fully diluted shares, such as stock options and warrants which when added together, contains all of the shares. This is called: “fully diluted shares.” Once these are exercised, they can dilute your holdings because more shares are added to the float for the buyers and sellers of the stock. It’s in your best interest to include those in your calculation. It will take more momentum for the stock to move up. |

| Working Capital | Money in the bank is good and this money is what is needed to pay for the expenses. Use your judgement. If management doesn’t have enough money to complete the next phase of the project (see *Pipeline from part 2 of 3), they will likely do a capital raise. This will involve diluting equity, so your shares outstanding will go up and this may cause the stock price to drop. |

| Debt | Look to see how much is owed and pay attention to the terms, because the debt will have to be paid back at some point and the interest rates and payments may be steep. Debt holders also get paid before you do as a shareholder if the company defaults. If the terms don’t seem reasonable or achievable, this can be a red flag. If there’s no mention of debt in the corporate presentation, you can check the company’s financial statements. |

| Market Capitalization = Shares Outstanding

X Share price |

This will give you an idea of how much money is invested in the company already. It shows the value of the Company. This is useful because you can compare the market capitalizations of similar companies to see where your junior gold company compares with other juniors. |

During my many conversations with mining professionals, they described having a “gut instinct” as to whether or not the people they chose to work with would be synergistic. One individual described his team as “only as good as its weakest member.” This is very true. because good people like to invest with good people. This is why the management team is the most important part of the project. If they can’t properly execute, it won’t get off the ground.

Now that you know the basics, before drilling down to the core of the quality of the resource and capital structure, assess management first and proceed down the checklist. Remember, to keep the gold standard. Good luck with your digging and don’t forget to rock on!

CIBC Wood Gundy is a division of CIBC World Markets Inc., a subsidiary of CIBC and a Member of the Canadian Investor Protection Fund and Investment Industry Regulatory Organization of Canada.

This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2017.

Jennifer Schell is an Investment Advisor with CIBC Wood Gundy in Toronto The views of Jennifer Schell do not necessarily reflect those of CIBC World Markets Inc.

By Jennifer Schell, B.Comm, MBA

Investment Advisor

Some Dig it, We Drill it!

I’m frequently asked why I have such a youthful glow to my skin. “What’s your secret?”: they always inquire. To the horror of ‘helicopter’ parents everywhere, I explain that my Dad is a geotechnical engineer and he designed mining tailings sites. Back in the day, he used to bring my sister and I to his site visits, regularly. Before toxins and pollution were of major concern, we used to play in the giant tailings, sand dunes which were comprised of uneconomical waste rock. Therefore, I guess you could say that I was “resourceful” with my skincare regime.

The objective of a junior mining company is to convert Mineral Resources to Mineral Reserves. With every step, when new data and research is obtained, the resource is modified into the next stage of the process.

| Mineral Resources: Geological Evidence and Sampling has been done to confirm that solid material exists to be economically interesting to extract from the Earth. | Mineral Reserve: Mineral Resources that have been converted to reserves by doing more detailed and extensive studies, under the blessing of the Qualified Person. | |

| Inferred Mineral ResourceThere is some evidence to support grade and quality but more exploration is needed for confirmation. | Needs more work to morph into the next category.

*Only used in the Pre-Economic Assessment (PEA) |

|

| Indicated Mineral ResourceThe physical characteristics, such as density and shape are modelled. This is where the qualified person (QP) comes in. At this stage, the resource can be used for the Pre-Feasibility Report. | Probable ReservesIt’s economical, but there are some reservations or “unknowns.” These have to be explained by the QP. | |

| Measured Mineral ResourceAt this point, you have enough information to start designing a mine. | Proven ReservesIt’s predictably economical! |

Every time a mining company publishes news to the public regarding their Mineral Resources, Mineral Reserves and Mining Studies, they have to be up to the Standards of Disclosure for Mineral Projects, called the (National Instrument 43-101). 1 The National Instrument 43-101 is a Canadian set of rules and guidelines to ensure that mining companies report their results in a transparent way to the capital markets. It ensures that proper scientific methods and that “Qualified People” (QP) assess the results. These people are the overlords of the mining project and they are generally geologists and engineers with professional designations and are qualified with over 5 years’ experience. This technical reporting is a big deal. It verifies the validity of the resource to ensure that sneaky people don’t shave down their ex’s gold jewellery and melt it onto a core sample.

Good news makes the stock price rise and so you should be on the lookout for the following events to occur within the mining pipeline:

| A Series of Fortunate Events: Mining Pipeline | |

| Environmental Study | In Canada, mining and the resource industry in general, are very important economic drivers for the economy. It’s also very important that these companies operate in a socially responsible way. Although there is always room for improvement, as a country, we are lucky to have some of the highest environmental and safety standards and there are many benefits to the communities surrounding these projects. Before the project can begin, the team must consult with the First Nations communities and provide the ministry of environment with a satisfactory plan that any pollutants will be managed and contained. Licensing and permitting are also obtained during environmental due diligence. |

| The Pre-Economic Assessment | The PEA accompanies Mineral Resources. It’s a pre-economic study to see if the project is worthwhile pursuing before the real spending begins. The Pre-Economic Assessment discusses everything in terms of Resources and this is the only report where you are allowed to include the Inferred Resources into your calculations.

Proven Reserves are actually there, Probable Reserves are most likely there given the calculations and data, while Inferred Resources are there in an ideal world. If you find more resources than the inferred estimate, the stock price can rise but keep in mind that technical reports must be validated by the qualified person before they can become actual “Mineral Reserves.” The success of the mining project depends on the assets that are in the ground and how capable management is to assemble a process to make its extraction cost effective. After, there is a feasibility study to discuss the capital costs involved in the development of the project into a mine. Drilling Companies will usually have a colourful map of their property with a legend showing their drill holes, often represented by red dots. The good ones with the most probability for gold are called “targets.” They also draw horizontal and vertical lines through the holes. When they drill, they often drill on an angle. Drill holes, although they seem quite simple in theory, are actually very pricy and can cost about $100,000 to drill one hole of core. So, you have to be very precise where you choose to drill, or you could spend millions of dollars for nothing. Metallurgy Report This section often gets overlooked, but it is very important. You can have the best gold reserves in the world, but if you can’t separate the gold effectively from the rest of the surrounding rock, then the project may no longer be feasible. For clarification, rocks are made up of minerals, which are inorganic, naturally occurring solid substances. In mining, ore refers to minerals (such as metals) that are economically valuable and can be extracted profitably. The ‘gangue’ minerals are everything else. They are essentially economically worthless minerals that surround the ore. Once chemicals have been used to separate the gold from the other minerals, there is often heavy metal waste. Also, some naturally occurring toxic elements exist with the gold in the earth’s crust, such as arsenic. Fortunately, new technologies are being developed because mining is crucial for the inputs to create all that we love: including cell phones, cars, planes buildings etc. There is a very cool science called 2bioremediation, “that uses bacteria to remove the noxious ions from the environment.” If you’re environmentally conscious, I encourage you to look into it. For gold recoveries, consensus prefers a rate of recovery of 75% or better. Resource Estimation Calculating the Production Rate for your Discovery The economic feasibility of the project depends on the Production Rate of the project. Some Notable Benchmarks:

The Formula is: Tonnes (Mt) X Grade (grams/tonne) / Conversion factor to Troy Ounces 31.1035 = Ounces (Moz)

|

| Pre-Feasibility Study also called (Preliminary Feasibility Study) | 1This is the minimum prerequisite for the conversion of mineral Resources to Mineral Reserves. At this point, management has determined the preferred mining method – either open pit or underground mining and pit configuration. The mineral processing method is also established, meaning that the way they extract the gold from the ore will be identified. There is also a financial analysis to assess the costs of the operation. Everything has to be ready so that a “Qualified Person” can take a look at the work and rightfully determine if these Mineral Resources are worthy of conversion to Mineral Reserves. |

| Feasibility Study | 1The feasibility study is highly technical and has a lot of economic studies done to determine the appropriate development option for the mineral project. It determines if it is worth the investment in the ground, for additional drill holes and eventual development to make the project feasible to sell into the market. At this point, things get real and the resource is essentially audited by a professional to confirm that all of the resources are actually there as stated. This stage is imperative so that they can get institutions to provide them with financing, which requires sound capital structure. |

These figures were provided by the mining executives that I’ve met over the last couple of years and can be used as a reference point for evaluation. All projects are unique, so there is likely to be some deviation from the benchmarks. When necessary, further research into the project may be required.

References:

1 www.cim.org, The Canadian Institute of Mining, Metallurgy and Petroleum

CIM DEFINITION STANDARDS – For Mineral Resources and Mineral Reserves,

Prepared by the CIM Standing Committee on Reserve Definitions, Adopted by CIM Council on May 10, 2014, 10/18/2017

2 Muibat Omotola Fashola,1 Veronica Mpode Ngole-Jeme,2 and Olubukola Oluranti Babalola1,*

Yu-Pin Lin, Academic Editor, Heavy Metal Pollution from Gold Mines: Environmental Effects and Bacterial Strategies for Resistance, 13(11): 1047., Int J Environ Res Public Health. 2016 Nov; PMCID: PMC5129257; Published online 2016 Oct 26. doi: 10.3390/ijerph13111047; P.2,10/18/2017

- I’ve suggested that investors may need to look beyond the head and shoulders top formations that recently appeared on bullion and many precious metal stocks.

- Please click here now. Double-click to enlarge this daily gold chart. Intermediate uptrends often consist of three legs. In 2017, gold has had two legs up.

- The next US jobs report is scheduled for release on Friday. Will it be the catalyst that launches a third leg higher for gold? I’m not sure, but I am sure of what’s important for gold, which is that it is generally very well supported here, both technically and fundamentally.

- The bottom line: Gold held in ETFs is quite steady. China’s economy has softened, but only modestly. That light softness is almost certainly related to the government’s action taken to reduce pollution.

- Chinese mine production has fallen as excessively polluting operations have been shut down. That’s adding support to the gold price.

- In India, the economic growth has slowed more noticeably than in China, and that does have an effect on gold demand. This growth slowdown has been mitigated by a rise in the rupee against the dollar, which lowers the cost of gold for Indians.

- Along with commercial traders on the LBMA and the COMEX (aka “the banksters”), Indian buyers are the most eager buyers when the gold price drops.

- On that note, please click here now. The US Treasury wants India’s central bank to reduce its purchases of US dollars.

- As India recovers from the disastrous demonetization program that pounded the nation’s GDP growth, the dollar could enter the “meat and potatoes” zone in a major bear market against the rupee.

- That would put gold on sale in a major way for Indians, and demand could surge.

- Please click here now. The dollar looks like a train wreck against the rupee on this one year chart, and that happened with the Indian central bank buying the dollar aggressively!

- What happens if US government pressure works, and the Indian central bank pares back its dollar buying?

- For the likely answer, please click here now. This seven year chart shows how strong the dollar was against the rupee from 2011 – 2016.

- The dollar has now started what is likely to be a multi-decade bear market against the rupee. This should add significantly to the (already relentless) growth in Indian citizen demand for gold.

- In America, most analysts predict there will be only a few rate hikes in the 2018 – 2019 time frame. In contrast, the US central bank predicts seven. Goldman Sachs’ top economist predicts nine.

- I predict there will be six. Regardless of what the exact number turns out to be, if its six or more, American M2 money velocity should begin a major bull cycle. Of the three main money velocity measurements used by the Fed, M2V tends to correlate best with the action of gold stocks versus bullion. A major bull cycle in M2V would blast gold stocks higher in a bull cycle with intensity that has not been seen since the 1970s.

- The St. Louis Fed has stated that the US inflation rate would have reached 33% as a result of QE, if money velocity had not collapsed. A more relentless pattern of rate hikes and accelerated QT will almost certainly create a surge in M2 velocity.

- I think most of the world will be stunned by what happens with inflation over the next 24 months. That’s because the QE “money ball” that is only inflationary potential energy becomes kinetic energy as it is flushed out of government and central banks and into the fractional reserve banking system.

- Trump’s tax cuts against a background of rising government debt should ice that inflationary cake in a very big way.

- Please click here now. GOAU-AMEX/ARCA is a relatively new gold stocks ETF.

- I like the fact that about 60% of the holdings are in Canada, which is arguably the best mining jurisdiction in the world, and certainly one of them. I’m a buyer on every 50 cents price decline until the price rises to $20. I would urge all gold stock enthusiasts to check out the main holdings in this ETF carefully, and eagerly!

- Please click here now. Double-click to enlarge this key GDX chart. GDX is bouncing from an important triangle apex point. It’s unknown whether the bounce will fail in the neckline area of the head and shoulders top pattern.

- What is known is that investors need to be focused on a major worldwide transition from QE, low rates, and deflation… to QT, higher rates, and inflation.

- Bullion has outshined the miners for twenty years, and now it’s becoming time for the miners to lead, and lead for a very long period of inflationary time!

Thanks

Cheers

St

Stewart Thomson

Graceland Updates

Written between 4am-7am. 5-6 issues per week. Emailed at aprox 9am daily.

https://www.gracelandupdates.com

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

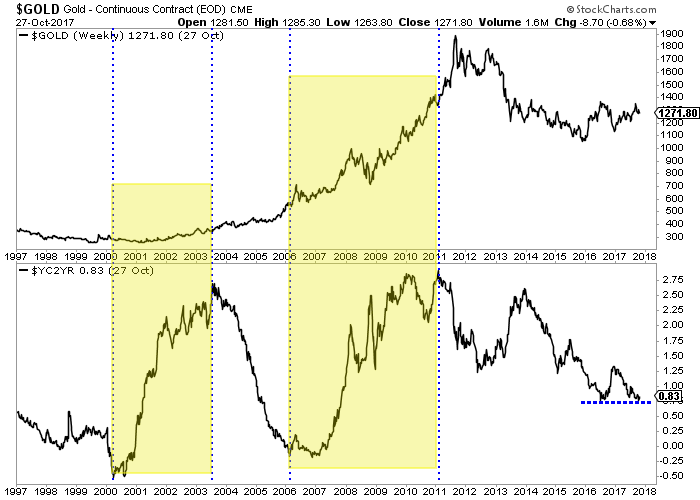

Over the past two years, Gold has been inversely correlated to bond yields. In a low inflation environment, falling bond yields drive real interest rates lower which benefits Gold. Conversely, rising yields are generally negative for Gold. When long-term yields exploded higher in the second half of 2016, Gold declined hard. Now with long-term yields threatening a potential major move higher, Gold and gold stocks have sold off and there is a risk of further losses. However, at somepoint rising yields can push Gold higher.

To answer the question of when we must understand what drives Gold.

Gold performs best amid falling or negative real interest rates. That occurs when inflation is rising faster than interest rates or when interest rates are falling faster than inflation.

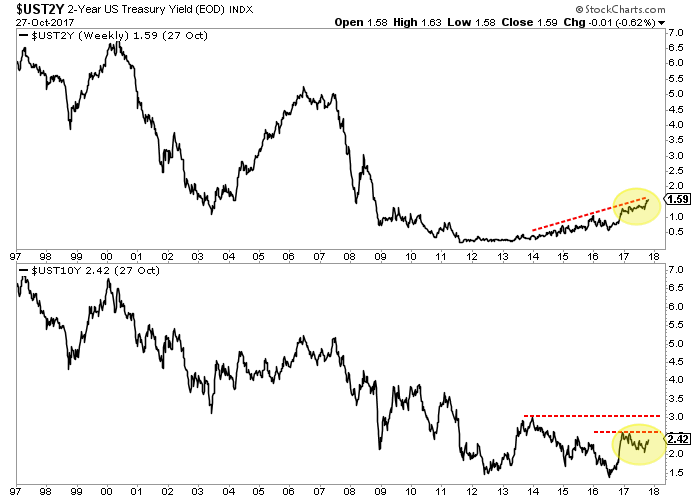

In terms of the yield curve, a steepening curve is bullish for Gold. Two analysts I enjoy reading (Gary Tanashian and Steve Saville) write about this frequently. Steve Saville recently wrote that a steepening yield curve reflects either increasing inflation expectations or risk aversion linked to declining confidence in the economy or financial system. The curve can steepen due to rising inflation or plummeting interest rates and in particular short-term rates. The chart below, which plots Gold and the yield curve (bottom) highlights recent periods of a steepening yield curve. Both periods were driven by a sharp decrease in short-term yields.

The yield curve (above) has stabilized at present as both short (2-year) and long-term bond yields (10-year) are rising again. To answer the original question, rising yields will be bullish for Gold only when long-term yields are rising faster or in other words, when inflation is rising faster than short-term yields. For example, if the 2-year yield (often a proxy for the Fed funds rate) peaks at 2.00%-2.25% but the 10-year yield surges well above 3.00%, that would be bullish for Gold.

Gold and gold stocks have failed to surpass their 2016 peaks and continue to go nowhere because the fundamentals are not yet bullish. Real interest rates are currently trending higher and the yield curve is flattening, not steepening. That could change if inflation expectations increase which would cause long-term yields (10-year) and inflation to rise faster than short-term rates or the Fed funds rate. The prognosis for Gold and gold stocks remains bearish into year end as we wait for lower prices and a low risk buying opportunity. The good news is those who buy weakness in the months ahead could position themselves for strong profits in 2018. Find the best companies and wait for the sector to get oversold and test strong support. To follow our guidance and learn our favorite juniors for 2018, consider learning more about our premium service.

Jordan Roy-Byrne CMT, MFTA

By Jennifer Schell, B.COMM, MBA

I grew up in Sudbury, Ontario in the 1980’s, where mining was ingrained into our childhoods…

Every morning before school—while eating breakfast— the local radio station would host a contest giveaway. All you had to do was call in and provide a safety tip on-air. If you were the lucky caller, the station would then send you an “Inco-branded-industrial-grade-backpack” (*Inco has since been taken over by Vale.) The best part was that the backpack contained pretty packaged samples of copper flakes, nickel and pyrite—fool’s gold. As I recall, the pyrite was shiny and very popular with the kids, myself included.

Since that moment, I’ve never lost my affinity for shiny things. Over the years, I’ve met with hundreds of talented women and men in the mining industry who have executed on these projects. After listening to many presentations, here are some basic factors to consider when you’re evaluating a mining project to invest in.

Identify your Mining Company

If you want to do a quick assessment, “google” the company’s name and go to their corporate website. Most of this information will be located in the corporate presentation in a PDF document, where they highlight all of the best features of the project. You can also go to www.sedar.com and you can look up further documents if you feel so inclined.

Can you Dig it?

There are 3 major categories of mining stocks: explorers, developers and producers. True gold-diggers want big rewards for all of their trouble, and so, the focus will be junior explorers. Junior explorers hope that they find a large deposit so that the developers and producers can take them over in a buyout. Geologists and investors get very giddy over undiscovered parcels of land with loads of unexplored potential because it’s like a treasure hunt for them and the payoff can be huge. Most financial analysts do not cover the explorers, so it’s difficult to find research on them. Junior exploration projects are hit or miss. You can either win big or you can lose everything.

Look at the Management Section: Super Important!

The first thing to do, is to check out the management tab. Under this tab, the Bios of the team are listed. The team usually boasts about their previous achievements in this section. The idea is that if they have a track record for success, they are likely to pull a good team together to replicate the process again.

Mining is an expensive business, so look for a combination of competent business people, geologists, engineers and lawyers. The CEO has to be a good marketer so that people are aware of the story. Look for issued press releases and for those regarding trade shows and media appearances, as well as recorded interviews to assess their interactions.

Since it’s hard to meet these people in person, watching them on television or on some online podcasts can give you an indication as to whether or not they demonstrate passion for their company and if they are decent people. Notice how the executive responds to the interviewer’s questions. If the executive is respectful, confident and knowledgeable, this is a good sign. If however, the executive is arrogant and condescending, you may want to shy away. The mining circle is small and friendly. If the leader of the Company displays toxic personality traits, they are likely to cause board and management disagreements.

Location, Location, Location!

When it comes to an ideal mining location, the country should be politically stable and situated in a place with a positive mining track record, in the right geological environment. I always like to hear how the team was drawn to the property. People like to hoard real estate—especially land. Since the places I look for are known gold destinations, I like the stories where the land has been in the family of non-miners for a number of years until their heirs lost interest and decided to sell it.

Just like when you buy a piece of real estate, it’s vital that your deposit is located on a good piece of property and you need to know the key development risks. To eventually tap into the full potential of the resource, you need proper infrastructure, such as roads, water and electricity, as well as workers. The more remote the property, the more expensive it is to get the resource out of the ground and into the proper outlets to sell the commodity. For example, if you had to build electric powerlines, it could cost at least $1.5 Million per KM. Fortunately, you can go onto Google Earth and you can locate your project to see what’s around it in terms of infrastructure.

Now that you’ve identified a company; have looked into management and found a good location, you can begin to mine your own business!

CIBC Wood Gundy is a division of CIBC World Markets Inc., a subsidiary of CIBC and a Member of the Canadian Investor Protection Fund and Investment Industry Regulatory Organization of Canada.

This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2017.

Jennifer Schell is an Investment Advisor with CIBC Wood Gundy in Toronto. The views of Jennifer Schell do not necessarily reflect those of CIBC World Markets Inc.

This epic central-bank-easing-driven global stock bull is starting to be strangled by the very central banks that fueled it. This week the European Central Bank made a landmark decision to drastically slash its quantitative easing next year. That follows the Fed’s new quantitative-tightening campaign just getting underway this month. With CBs aggressively curtailing easy-money liquidity, this stock bull is in serious trouble.

The US flagship S&P 500 broad-market stock index (SPX) has powered an incredible 280.6% higher over the past 8.6 years, making for the third-largest and second-longest bull market in US history! The resulting popular euphoria, a strong feeling of happiness and confidence, is extraordinary. So investors brazenly shrugged off the Fed’s September 20th QT and the ECB’s October 26th QE-tapering announcements.

That’s a grave mistake. Extreme central-bank easing unlike anything witnessed before in history is why this stock bull grew to such grotesque monstrous proportions. Without QE, it would have withered and died years ago. Central banks conjured literally trillions of new dollars and euros out of thin air, and used that new money to buy assets. This vast quantitative easing inarguably levitated the world stock markets.

QE greatly boosted stocks in two key ways. Most of it was bond buying, which forced interest rates to deep artificial lows nearing and even under zero at times. This bullied traditional bond investors looking for yield income into dividend-paying stocks. The record-low interest rates fueled by QE were also used to justify extremely-expensive stock prices. QE aggressively forced legions of investors to buy stocks high.

The super-low borrowing costs driven by QE’s crushing downward pressure on interest rates also unleashed a vast corporate-stock-buyback binge unlike anything ever witnessed. Corporations borrowed trillions of dollars and euros to use to buy back their own stocks, boosting their stock prices. QE both enabled and provided the incentives for this anomalous extreme financial engineering, indirectly levitating stock markets.

Stock traders’ apparent belief over this past month that the Fed starting to reverse its QE through QT and the ECB greatly slowing its QE will have no meaningful impact on QE-levitated stock prices is absurd. The simultaneous reversal and slowing of QE in the States and Europe is a hellstorm relentlessly bearing down on hyper-complacent traders. It’s the financial equivalent of a Category 5+ super-hurricane, a juggernaut.

This Thursday the ECB announced it is slashing in half its ongoing QE bond monetizations from their current €60b-per-month pace to €30b per month for the first 9 months of 2018. After that the ECB’s QE will likely cease entirely, since it is running out of available bonds to buy because the ECB’s total QE has been so vast. That means ECB QE will collapse from €720b this year to €270b next year, a radical 62.5% plunge!

The idea that stock markets won’t miss €450b of ECB bond buying next year is ludicrous. The ECB has been monetizing bonds continuously with at least a €60b-per-month pace since March 2015. That will make for colossal total QE from then to December 2017 exceeding €2040b, growing to over €2310b by September 2018. €60b per month falling to €30b for most of next year and then likely zero will have a huge impact.

At current exchange rates, that €450b drop of ECB QE from 2017 to 2018 translates into $530b. That is likely enough all alone to tank global stock markets reliant on aggressive central-bank QE like crack cocaine. But add that on top of the Fed’s first-ever quantitative tightening now getting underway, and 2018 will see the greatest central-bank tightening in history. How can that not drive an overdue stock bear?

I discussed the Fed’s new QT campaign and likely market impact in great detail a month ago right after it was announced. While the Fed’s own QE bond buying formally ended in October 2014, it held all those bonds on its balance sheet until this month. Starting this quarter, the Fed is allowing $10b per month to roll off as they mature. That effectively destroys the money created to buy those bonds, removing QE capital.

$10b per month isn’t much initially, but the Fed is slowly ramping that to a target of $50b per month by Q4’18. The math is simple. Total Fed QT in 2017 will only run $30b, a rounding error relative to the vast size of QE’s trillions of monetized bonds. But in 2018 that Fed QT will add up to $420b. Add that to the $530b of ECB QE here in 2017 but not coming in 2018 due to the taper, and markets face $950b of CB tightening!

Can the world’s two most-important central banks collectively withdraw almost a trillion dollars of liquidity in 2018 alone without blowing a gaping hole in these lofty stock markets? Not a freaking chance! And 2019 looks even worse. Total ECB QE will likely run at zero, down from €720b this year. That translates into $850b. And the Fed’s QT will run at its terminal full speed of $600b annually. That adds up to $1450b!

So on top of 2018’s $950b less of ECB QE and new Fed QT compared to this year, 2019 faces another $1450b of collective tightening from the Fed and ECB relative to 2017. That means $2.4t of central-bank liquidity that exists in this record stock market year will vanish over the next couple years. I can’t imagine a more-bearish omen for excessively-large QE-inflated stock bulls than such a vast reversal of CB flows.

This first chart ought to shatter the Wall Street myth that today’s monster stock bull was driven by profits instead of extreme central-bank QE. It superimposes the SPX over the Fed’s balance sheet, which is where those QE-financed bond purchases rest. This is the most-damning chart in the stock markets, no mean feat at such extremes. Fed QT and far-less ECB QE is the stuff of nightmares for QE-inflated stock markets!

While the Fed initially birthed QE back in late 2008’s first stock panic in a century, QE’s primary impact on the stock markets started in early 2013. That was soon after the Fed first launched and then quickly more than doubled its third QE campaign. QE3 was radically different from QE1 and QE2 in that it was open-ended, with no predetermined size or duration. That gave it a gargantuan impact on stock psychology.

Whenever the stock markets started to sell off, Fed officials would rush to their soapboxes to reassure traders that QE3 could be expanded anytime if necessary. Those implicit promises of central-bank intervention quickly truncated all nascent selloffs before they could reach correction territory. Traders realized that the Fed was effectively backstopping the stock markets! So greed flourished unchecked by corrections.

This stock bull went from normal between 2009 to 2012 to literally central-bank-conjured from 2013 on. The Fed’s QE3-expansion promises so enthralled traders that the SPX went an astounding 3.6 years without a correction between late 2011 to mid-2015, one of the longest-such spans ever! With the Fed jawboning negating healthy sentiment-rebalancing corrections, psychology grew ever more greedy and complacent.

QE3 was finally wound down in October 2014, leading to this Fed-evoked stock bull soon stalling out. Without central-bank money printing behind it, the stock-market levitation between 2013 to 2015 never would’ve happened! Without more QE to keep inflating stocks, the SPX ground sideways and started topping. Corrections resumed in mid-2015 and early 2016 without the promise of more Fed QE to avert them.

2013 was the peak-QE3 year, when the Fed monetized a staggering $1020b in bonds through QE. Such vast central-bank liquidity injections catapulted the SPX 29.6% higher that year! The Fed tapered QE3 in 2014, which added up to $450b of additional bond buying that year. And the SPX only rallied 11.4%. Fed QE dropped by 56% between 2013 and 2014, and stocks’ rallying shrunk 62%. That’s certainly no coincidence.

Then in 2015 when Fed QE was zero, the SPX slipped 0.7%. See the pattern here? The more QE from central banks, the more the stock markets rise. Those vast capital injections from the Fed levitated the US stock markets by forcing yield-starved bond investors into stocks and facilitating immense corporate stock buybacks. This QE-driven stock bull peaked in mid-2015 soon after the Fed ceased its own QE!

The bear market that follows every stock bull should’ve started in late 2012, but the Fed warded it off with its massive open-ended QE3 campaign. That ultimately totaled $1590b before it ended in late 2014, when the delayed stock bear should’ve begun. Indeed it looked like it had, as the SPX started rolling over without Fed QE boosting it. The SPX suffered its first corrections in 3.6 years in mid-2015 and early 2016.

There’s a stellar probability the dominant reason the overdue stock-market bear didn’t arrive in 2015 was the ECB started its own QE campaign in March that year. The ECB effectively took the QE baton from the Fed, keeping world stock markets levitated through massive liquidity injections. ECB QE levitated European stock markets through the same mechanisms as the Fed QE had earlier levitated the US ones.

The global stock markets are heavily interconnected. Both rallies and selloffs in either the United States, Europe, or Asia often create the psychology necessary to drive similar moves in the other markets. So the ECB’s QE directly buoying European stock markets bled into US stocks, fending off the overdue bear that the end of the Fed’s QE should’ve awoken. It was hopes for more ECB QE that rekindled this tired bull.

The Fed’s QE3 bond buying was tapered to zero in November 2014. From that announcement in late October that year, the SPX would rally another 7.3% into May 2015 on sheer momentum and euphoria. After that it drifted sideways to lower for the next 13.7 months, suffering two corrections. It wasn’t until July 2016 that a new bull high was finally seen. That was soon after the UK’s surprise Brexit vote to leave the EU.

That June 2016 referendum stunned European leaders, potentially threatening their entire project to unite Europe. Thus the ECB’s central bankers rushed to vociferously promise to do anything necessary to maintain market stability through the Brexit process. So the SPX only broke out of its mounting bear trend thanks to hopes for more ECB QE! That rally soon fizzled until Trump’s surprise victory unleashed Trumphoria.

This extreme Trumphoria stock rally since early last November was driven by euphoric hopes for big tax cuts soon, not central-bank easing. But without the ECB’s colossal €720b or the equivalent of $850b in QE over the past year since the election, odds are this Trumphoria rally would’ve either been far more muted or never even existed. The Fed’s QT and ECB QE tapering are grave threats to QE-inflated stock markets.

The chart above proves how heavily dependent the SPX is on the Fed’s balance sheet, which has never materially shrunk before 2018. The European stock markets have seen a similar phenomenon as the ECB’s balance sheet ballooned under QE. Germany’s flagship DAX stock index is Europe’s leading one. In 2016 the DAX rallied 6.9% on over €720b of ECB QE. So far this year the DAX is up 12.8% on €600b of QE YTD.

There is absolutely no doubt these global stock markets are greatly reliant on extreme central-bank QE to keep levitating to new record highs. So the stock markets are in world of hurt in 2018 and 2019, with total central-bank liquidity from the Fed and ECB falling by $950b and $1450b respectively relative to 2017! There’s probably never been a greater bear-market catalyst than record QE being thrown into reverse.

If the Fed’s QT and the ECB’s QE taper proves so devastating to stocks, won’t these central bankers simply stop doing it? They certainly don’t want to tank stock markets, as both the US and European economies really need high stocks’ wealth effect to thrive. If stock markets fall enough to spawn some real fear in Americans and Europeans, they will pull in their horns on spending which hurts the real economies.

Still I suspect the Fed and ECB won’t and can’t stop their new tightening campaigns for several reasons. Both central banks are doing everything they can to be as gradual and transparent as possible to avoid spooking markets, which is wise. Such slow rampings of the Fed’s QT and the ECB’s QE taper aren’t likely to spark a sharp stock-market plunge. They’ll just gradually turn the screws to stocks, slowly forcing them lower.

Major bear markets tend to cut stock prices in half, although worse losses are likely after such extreme fake central-bank-goosed bull-market toppings. But these bears that inevitably follow bulls generally play out over a couple years. There are about 250 trading days per year, so a 50% loss spread across two years works out to a trivial average of 0.1% per day! No one will panic if CB tightening slowly boils the bulls.

And the reason both the Fed and ECB are tightening is to reload easing ammunition for the inevitable next financial crisis. The more QE the Fed can reverse with QT, and the less the ECB’s balance sheet bloats, the more room they will have to relaunch QE when they get scared again in the future. Central bankers know it’s critical to slow, stop, and unwind QE so they rebuild room to aggressively ease again later.

Finally both the Fed and ECB spent long months if not years preparing traders psychologically leading into these CBs’ QT and QE tapering. If either central bank chickens out and pulls back in response to stock markets slowly rolling over, that itself risks igniting intense selling. The only reason the CBs would slow their crucial normalizations from extreme QE is if they feared another looming massive financial crisis.

Traders would read any course change to less tightening by either central bank as an admission of serious problems in global markets, and rush for the exits. Not carrying through on these carefully-laid tightening plans would also severely hobble these CBs’ credibility, and thus their future abilities to calm markets in a crisis. The die is cast on Fed QT and ECB QE tapering, it can’t be changed without creating big problems.

If this radically-unprecedented transition from extreme easing to extreme tightening was happening in normal fairly-valued stock markets, it would still ominously portend a major bear. But thanks to these goofy central banks artificially enlarging and prolonging this stock bull through their QE, stocks have soared way up to bubble valuations! The extreme overvaluation rampant in stock markets today greatly magnifies the risks.

This last chart looks at the average trailing-twelve-month price-to-earnings ratio of the 500 SPX stocks, both in simple-average and market-capitalization-weighted-average terms. The past year’s Trumphoria rally on big-tax-cuts-soon hopes catapulted valuations into nosebleed bubble territory. Such extremes would herald an imminent bear market even if the most extreme CB easing in all of history wasn’t reversing.

This is a complex chart with dire ramifications for investors, which I last discussed in depth in late June. For our purposes today on central banks starting to strangle this extreme bull they’ve nurtured, look at the blue SPX-valuation lines. The average SPX-component P/E ratio in both simple and MCWA terms is now over 28x. At Zeal we calculate this crucial valuation data each month-end, so September’s is the latest.

Weighted by market capitalization, the SPX stocks’ average P/E in late September was 28.7x earnings! In simple-average terms, it looked even worse at 29.3x. These numbers are conservative too, because we cap all trailing-twelve-month P/E ratios at 100x to avoid outliers skewing the overall average. Amazon alone with its insane 250x P/E would catapult these up to 31.7x and 29.6x respectively. Valuations are extreme.

The US stock markets’ average trailing P/E over the past century and a quarter is 14x, which is fair value. Double that at 28x is formally a bubble, where we are today. Euphoric traders get so excited about stock markets rallying forever that they are willing to pay any price to get in, eagerly buying stocks high instead of prudently waiting to buy low. The higher the prevailing valuations, the greater the downside risk stocks face.

While valuations aren’t a market-timing tool, bubbles always eventually pop. There are no exceptions to this rule in history. When bubbles fail stocks fall sharply, entering major new bear markets. In order to trade at 14x fair value based on today’s corporate earnings, the SPX would have to literally be more than cut in half to 1225ish! The white line above shows where the SPX would trade at that historical 14x fair value.

Even more ominous, valuation mean reversions following stock prices getting too high in bulls never just stop at the mean. Instead momentum carries them through 14x to a proportional overshoot below that to undervalued levels. So there’s a high probability the inevitable next stock bear won’t bottom until stocks are trading well under 10x earnings, which would make for a bigger-than-50% bear from today’s bubblicious levels.

The key point here is stock markets are exceedingly risky on bubble valuations alone after central banks’ unprecedented extreme easing forced them so high for so long. Even if the Fed wasn’t embarking on QT to reload for future easing, even if the ECB wasn’t tapering QE because it’s running out of bonds to buy, a new stock bear would be a near-certainty on extreme valuations alone. Bulls are always followed by bears.

But throw in Fed quantitative tightening and ECB quantitative-easing tapering on top of that, and we are set up for one of the worst stock bears on record after one of the biggest and longest bulls ever. Truly these central banks that fostered this monstrous bull are now starting to strangle it. The next couple of years are going to see literally trillions of dollars less CB liquidity than the markets have enjoyed in 2017!

Again between Fed QT ramping and ECB QE tapering, 2018 is on track to see a colossal total $950b less capital injected from the Fed and ECB compared to this year. And based on the Fed’s and ECB’s current plans which are hard to slow or stop without destroying market confidence, 2019’s CB liquidity will come in at another $1450b lower than 2017’s. We are talking about $2.4t of effective tightening over the next 2 years!

There is zero chance stock markets will be able to ignore such radically-unprecedented CB tightening. $1.2t a year is a devastating hit to liquidity. Remember in 2013 the SPX soared 29.6% on $1020b of Fed QE via QE3. What’s going to happen to stock markets in 2018 when that reverses to -$420b with Fed QT alone, or 2019 at another -$600b with Fed QT running full speed? Add ECB tapering on top of that.

The unpopular hard truth euphoric investors don’t want to hear is stock markets ain’t gonna be pretty under Fed QT and ECB QE tapering. For the love of all things good and holy, take this seriously! Just like in all past stock-market toppings, greed and complacency are extreme so traders have no fear of this imminent central-bank-tightening threat. But it’s a Category 5+ hellstorm, unprecedented in stock-market history.

Investors really need to lighten up on their stock-heavy portfolios, or put stop losses in place, to protect themselves from the coming valuation mean reversion in the form of a major new stock bear. Cash is king in bear markets, as its buying power increases as stock prices fall. Investors who hold cash during a 50% bear market can double their stock holdings at the bottom by buying back their stocks at half price!

Put options on the leading SPY S&P 500 ETF can be used to hedge downside risks. They are cheap now with euphoria rampant, but their prices will surge quickly when stocks start selling off materially. Even better than cash and SPY puts is gold, the anti-stock trade. Gold is a rare asset that tends to move counter to stock markets, leading to soaring investment demand for portfolio diversification when stocks fall.

Gold surged nearly 30% higher in the first half of 2016 in a new bull run that was initially sparked by the last major correction in stock markets early last year. If the stock markets indeed roll over into a new bear in 2018, gold’s coming gains should be much greater. And they will be dwarfed by those of the best gold miners’ stocks, whose profits leverage gold’s gains. Gold stocks rocketed 182% higher in 2016’s first half!

The key to thriving and multiplying your fortune in bull and bear markets alike is staying informed, about broader markets and individual stocks. That’s long been our specialty at Zeal. My decades of experience both intensely studying the markets and actively trading them as a contrarian is priceless and impossible to replicate. I share my vast experience, knowledge, wisdom, and ongoing research in our popular newsletters.

Published weekly and monthly, they explain what’s going on in the markets, why, and how to trade them with specific stocks. They are a great way to stay abreast, easy to read and affordable. Walking the contrarian walk is very profitable. As of the end of Q3, we’ve recommended and realized 967 newsletter stock trades since 2001. Their average annualized realized gain including all losers is +19.9%! That’s hard to beat over such a long span. Subscribe today and get ready before CB tightening crushes stocks!

The bottom line is the Fed and ECB have started strangling this extraordinary stock bull they nurtured. After being levitated for years by trillions of dollars and euros of quantitative easing, these central banks have started tightening. The Fed has birthed quantitative tightening, which will increasingly reverse its own extreme QE. On top of that the ECB will radically slow its own QE next year, for unprecedented tightening.

This is the death knell for QE-inflated stock markets driven to extreme bubble valuations by epic central-bank monetary injections. The Fed and ECB are finally taking away their easy-money punch bowls, with truly-dire implications for stock markets. Trillions of dollars and euros of tightening in the next couple years will finally unleash the long-overdue stock bear delayed by QE, which will likely prove proportionally oversized.

Adam Hamilton, CPA

October 27, 2017

Copyright 2000 – 2017 Zeal LLC (www.ZealLLC.com)

By now, most readers invested in the Lithium (“Li“) sector know about brine deposits, especially those located in South America’s “Lithium Triangle” (Chile, Argentina & Bolivia). And, many are familiar with conventional hard rock mining for Li, most of which takes place in western Australia.

However, readers likely know very little about a third source of potential Li supply; from claystone deposits. One small company betting on a technology solution to unlock its mineral wealth is Cypress Development Corp. (TSX-V: CYP) / (OTCBB: CYDVF). 49.5 M shares outstanding @ C$0.185 = C$ 9 M market cap. C$1.5 M in cash.

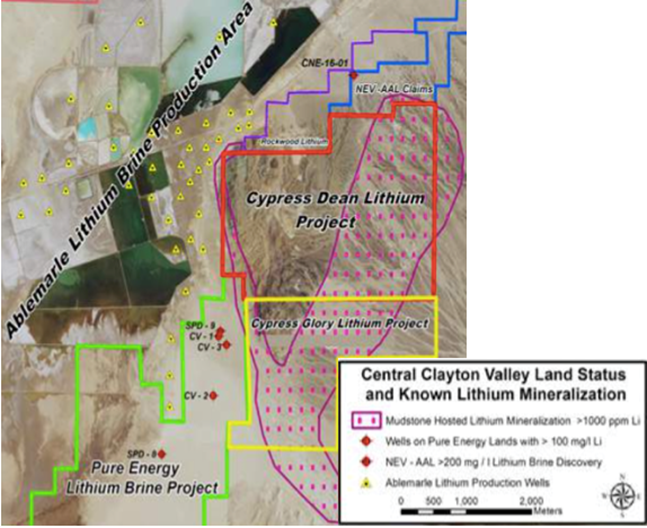

Cypress controls 100% of the contiguous Dean and Glory claim blocks covering an area totaling 4,220 acres in Clayton Valley, Nevada, immediately east of Albemarle’s Silver Peak Li operations and Pure Energy Minerals’ project (PEA-stage, C$330 M after-tax NPV(8%) on its southwest boundary. Management believes that the consistent nature of the currently known Li mineralization is highly encouraging for both the potential size and potential resource extraction methodologies. (see corporate presentation, but please return!)

To date, all of Cypress’ drilling has been on the Dean property where a 9-hole drill program was completed earlier this year. But, a recent press release explains that Cypress plans to drill 12 holes totaling 4,000 feet. The 2017 fall program will be divided between the Dean and Glory projects…. Upcoming drill results represent an important near-term catalyst for the company.

Li Prices up 200% — a Game Changer For Unconventional Li Deposits

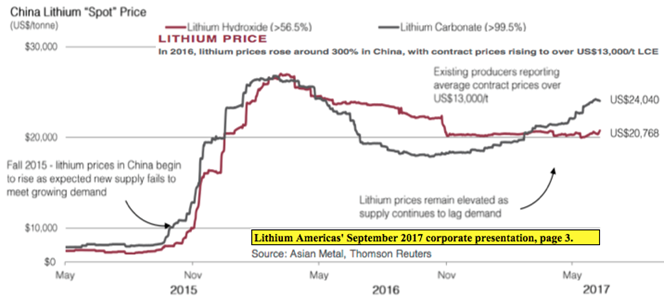

What readers have probably heard about what I call “unconventional Li deposits” (i.e. not brine or hard rock) is true, there’s currently no meaningful commercial-scale production from claystone deposits anywhere in the world. However, it’s very important to recognize one crucial observation…. Li prices have roughly tripled in just the past 2 years. In fact, spot prices in China have quadrupled, (see chart below) currently perched above US$ 20k/metric tonne, at or near all-time highs.

Today’s very strong Li prices are a game changer, greatly incentivizing the world to invent a better mousetrap. The exciting thing in my view is that more and more mousetraps are being built and tested. Not just methods to extract Li from claystone, but dozens of Li brine processing technologies, some of which could be amenable to unconventional Li deposits.

Simply put, if or when a commercial technology or technologies to exploit unconventional Li deposits is developed, the value of claystone properties such as those held by Cypress could soar.

We’ve seen this movie before…. Consider the oil shale industry 10-15 years ago when the benefits of horizontal drilling were first becoming known. Speculators started grabbing acres surrounding known fracking hotspots, (not knowing how much, if any, hydrocarbon abundance was in place) initially paying $100-$200/acre. Within a few years, the best located acres were trading at $10,000-$20,000/acre.

Unlike outright speculation on oil shale, in Cypress’ case we already know there’s Li in the ground, possibly high-grade compared to brine deposits, possibly large tonnage compared to hard rock deposits. What we don’t know yet is if it’s technically and environmentally feasible to separate the Li from the clay, mud and other materials and profitably sell it. So, again, that’s the primary risk of investing in Cypress Development Corp. A big risk, but a known risk that can be weighed against other risks that Li juniors face.

There is another notable risk factor. Access to water in Nevada is extremely important. In Clayton Valley, and many other arid parts of the State, it can be very difficult to obtain water rights. However, Cypress might not have the same risk exposure as peers looking to exploit traditional brine resources. The Company does not propose to tap Li-saturated brine that a neighboring party could claim to own or control.

Cypress will need access to process water, not the minerals (lithium/boron/potassium) in the water– a big difference. And, the amount of water required would presumably be far less (and probably recyclable) because Cypress would not be filling giant solar evaporation ponds like Albemarle’s nearby Silver Peak processing facilities.

Neighbor Lithium Americas’ Delivering New PFS in Mid-2018…

So, how close is the industry to solving these complex technical & environmental challenges of commercial extraction of Li from claystone deposits? In my opinion, closer than many might guess, but with the important caveat that each deposit is unique. For example, Lithium Americas (TSX: LAC) / (OTCQX: LACDF) has a clay deposit, the Lithium Nevada project, (formerly Kings Valley) that was actively explored, developed and promoted in 2009-2013, when the company was called Western Lithium USA Corp.

A Preliminary Feasibility Study (“PFS“) on Kings Valley was completed in 2012, and a pilot plant running Kings Valley ore operated successfully in Germany for years. A substantial amount of effort and capital was deployed, but with a Li price in the US$5,000/t area, LAC decided not to pursue the project. Fast forward to 2017, LAC is developing a new production flow sheet that will incorporate a number of operational improvements, but by far the biggest enhancement to the project’s actual economics will be a much higher long-term Li price assumption.

As I write this, LAC just committed to delivering a brand new PFS by June 30, 2018, and commented,

“While proprietary, much of our work relies on the application of commercially available solutions that could be deployed quickly and reliably.” Also, according to LAC management, “…the Lithium Nevada Project’s Li clay resource is the largest known lithium resource in the U.S.”

This suggests, in my opinion, that LAC will be putting out a PFS next year that contains a Net Present Value (“NPV”) in the hundreds of millions of U.S. dollars. The market will take notice, and since LAC’s market cap is currently ~C$ 1 billion (due almost entirely to the company’s JV with SQM on a world-class Li brine project in Argentina), LAC should meet with success in attracting global battery & car manufacturers, among others, to the table to talk about strategic investments and off-take agreements.

Will Global Geoscience & Bacanora Prove Clay Deposits Economic?

Bacanora Minerals (TSX-V: BCN) has done a tremendous amount of work on unconventional Li deposits. In its case, in Mexico, on the Sonora Lithium clay deposit. Management is close to delivering a Bank Feasibility Study (“BFS“). Bacanora has been operating a pilot plant for over 2 years and reportedly has the kinks worked out. Japanese trading giant Hanwa is a strong financial backer and has a robust off-take agreement in place with Bacanora.

Nevada neighbor Global Geoscience Ltd. (ASX- GSC) is an Australian-listed junior with a clay deposit in Nevada. It is finishing up a PFS on its Rhyolite Ridge Lithium-Boron Project that has an estimated 3.4 million tonnes of Li carbonate. Unlike Cypress’s project, Rhyolite Ridge’s economics rely on the co-production of boric acid. This is not necessarily a good or bad thing; it just highlights that each project is unique. GSC shares have nearly quadrupled in the past year.

Bacanora’s market cap is ~C$ 190 M. Global Geoscience’s market cap is ~C$ 310 M. Both are making steady progress towards unlocking the value of their unconventional Li deposits. I believe that positive developments for these and other unconventional Li companies will provide a flow of really good news for Cypress. The Company has about 49.5 M shares outstanding post the recently closed capital raise. Its market cap is just ~C$ 9 M.

I strongly believe that with big news from Lithium Americas, Bacanora Minerals and Global Geoscience next year, Cypress will be on the radar screens of a number of global Li players, both financial & strategic companies.

MGX Minerals (TSX-V: XMG) is another technology-backed unconventional Li deposit winner that grabbed the attention of investors in 2017. Its stock price is up ~500% in the past year. MGX is harnessing technology to extract Li from oilfield brine wastewater. Like LAC, BCN & GSC, MGX is not in operation. MGX’s market cap is about C$ 80 M.

Cypress; in the Right Place at the Right Time and a Cheap Valuation

First Cypress has to prove up an attractive maiden resource, then it simply needs to continue following in the footsteps of Lithium Americas, Bacanora & Global Geoscience as those companies publish a PFS and/or a BFS, lock-in large strategic/financial partners and off-take agreements. But fear not, none of the clay deposits will be in large-scale production anytime soon, so they won’t even put a dent in a possible supply crunch around the turn of the decade, and won’t put a cap on Li prices!

Make no mistake, Cypress’ projects are earlier-stage than the companies I’ve mentioned, but in some respects might not be higher risk. For example, the Dean and Glory projects would probably have lower strip ratios than many global Li projects (both conventional & unconventional).

Management Team is Amazing for a Small Company

Typically, small companies have trouble attracting big talent, but not so in this case. Why? Because smart people saw the opportunity, they saw what I’m describing in this article, basically, they saw the writing on the wall…. there’s not going to be enough Lithium! All potential commercial-scale Li sources will be pursued to the ends of the earth. And, with the Li price at US$20k/t+ vs. US$5k/t, the “when” can’t come fast enough.

That’s why Bill Willoughby, PE, PhD joined the Company this year. What better person to have as CEO than a rock star, PhD mining Engineer during a once in a lifetime opportunity like this? (the paradigm shift from ICE- powered to EV). Bill has nearly 30 years’ experience at natural resource development companies. Will this be his greatest success to date? Dr. Willoughby was kind enough to provide the following quote, an exclusive for this article,

“We feel our project is unique due to its location and physical traits. To our knowledge, Clayton Valley has the only deposits of lithium claystone that are situated next to an existing brine operation. Besides location, our deposit is shallow, flat-lying soft rock in which the lithium appears readily soluble. With the large apparent size, we’ve seen from our drilling and the lateral extent of the deposit, we believe all these factors combine to a unique opportunity to develop a significant new source of lithium.”

In addition, the Cypress team has used, and continues to work with, very well-known and respected ALS / Chemex in Reno, NV and SGS lab in Ontario.

Cypress is sitting on Li–bearing property that could be worth a hell of a lot more than its C$ 9 M market cap. This will not be an overnight success, a near-term commercial-scale producer, but actual production is not what’s required for a higher valuation. What’s needed is a credible path towards that end, management is on that path and working diligently.

All 9 previous holes at Dean encountered significant Li values within claystone, which ranged up to 1,790 ppm Li (1,790 mg/L Li) and averaged 900 ppm Li (900 mg/L Li) throughout the average drill-depth of 243 feet. Mineralization outcrops at surface, and average Li mineralization thickness is greater than 210 feet. The program covered an area measuring about 12,000 feet in length by 4,000 feet in width. The Li-bearing claystone is considered open in all directions.

South of the Dean claim block, extensive sampling by Cypress on the Glory claims identified Li mineralization in surface exposures of claystone which ranged up to 3,800 ppm Li (3,800 mg/L Li) over 9,500 feet along the same trend encountered on the adjoining Dean claims. Results suggest a strong possibility of continuous mineralized volume of a highly leachable Li-rich claystone at surface on the Glory project.

The goal of the work on both properties is to substantiate the potential to produce Li directly from the mineralized claystone with a low-cost and environmentally friendly approach, without the need for roasting or other costly mining and complex treatments. Cypress is proceeding with additional leach studies to determine the amount of Li extraction possible from the claystone and provide further data on the feasibility of a large-scale leach extraction method.

So, to recap so far; in my opinion it seems reasonable that Cypress will be able to come up with a maiden mineral resource estimate in the next 6 months. Further, based on historical samples, drilling and other exploration, there’s reason to believe that the maiden resource could be sizable and relatively high-grade. The claystone mineralization is soft and near-surface, so there’s no doubt that ore would be easy and low-cost to extract. The main risk is that there is no known technology that can process Cypress’ Li deposits cost effectively and in an environmentally friendly manner.

From the latest Cypress press release, quote,

“Cypress believes its claystone deposit in Clayton Valley has the potential to contain a significant resource of lithium, and may have physical and logistical features that could make it a productive, long-term source of lithium. In addition to the ongoing drilling program, Cypress is continuing studies to determine the exact nature and distribution of the lithium mineralization in the claystone, and identify an effective means of extraction.”

Conclusion

Boy this time next year, there could be two half-billion dollar Li clay projects in Nevada! Either or both project owners might have lined top Battery or EV manufacturers to drive them forward. Notice I haven’t even mentioned Nevada’s Tesla, there’s no need, it could be anyone, literally dozens and dozens of companies. If so, will tiny Cypress Development Corp. (TSX-V: CYP) / (OTCBB: CYDVF) still be valued at C$ 9 M?

Although years away from commercial-scale production, Cypress is year(s) ahead of unconventional Li deposits that have not been staked, permitted for initial exploration, sampled or had preliminary testing or metallurgy done…. Remember, each deposit is unique, and most high-grade Li deposits might not be nearly as amenable as Cypress’ Dean and Glory projects to potential exploitation due to distance from infrastructure, depth of deposit, grade, continuity, chemistry (concentration of coincident deleterious elements) jurisdiction, and other factors.

Cypress Development is a company worthy of further investigation by readers. Here are some places to go for further information.

JuniorStockReview by Brian Leni P.Eng

Ahead of the Herd article by Rick Mills

The Stateside Report by Vince Marciano

Energy & Gold Ltd. Website by Scott Armstrong

Disclosures: The content of this interview is for illustrative and informational purposes only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research, [ER] including but not limited to, commentary, opinions, views, assumptions, reported facts, estimates, calculations, etc. is to be considered implicit or explicit, investment advice. Further, nothing contained herein is a recommendation or solicitation to buy or sell any security. Mr. Epstein and [ER] are not responsible for investment actions taken by the reader. Mr. Epstein and [ER] have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Mr. Epstein and [ER] are not directly employed by any company, group, organization, party or person. Shares of Cypress Development Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Peter Epstein owned shares in Cypress Development Corp. and the Company was an advertiser on [ER]. By virtue of ownership of the Company’s shares and it being an advertiser on [ER], Peter Epstein is biased in his views on the Company. Readers understand and agree that they must conduct their own research, above and beyond reading this article. While the author believes he’s diligent in screening out companies that are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & [ER] are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article. Mr. Epstein & [ER] are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and [ER] are not experts in any company, industry sector or investment topic.

The silver miners’ stocks have mostly drifted sideways this year, looking vexingly comatose. Such dull price action repels speculators and investors, so they’ve largely abandoned this lackluster sector. That weak trader participation has led to silver stocks’ responsiveness to silver price moves decaying. What can shock silver stocks out of their zombified stupor? And how soon is such an awakening catalyst likely?

Silver stocks’ flatlined behavior so far in 2017 is surprising and odd. Silver-stock prices are ultimately driven by silver-mining profits, which are overwhelmingly driven by prevailing silver price levels. Silver in turn is slaved to gold’s fortunes, the yellow metal is the white metal’s dominant primary driver. With gold faring quite well this year despite the euphoric record stock markets, silver and its miners’ stocks should be shining.

Since silver is a tiny market compared to gold, silver’s moves tend to leverage gold’s. The best global silver and gold supply-and-demand fundamental data available comes from the Silver Institute and World Gold Council respectively. According to them, worldwide silver and gold demand last year ran 1027.8m ounces and 4337.4 metric tons. Along with average prices, these can be used to approximate market sizes.

Silver and gold averaged $17.12 and $1250 last year. Run these numbers, and 2016’s total global silver and gold markets were worth about $17.6b and $174.3b. This latest-available data shows silver’s market is literally an order of magnitude smaller than gold’s! With silver only enjoying 1/10th the capital flows of gold, silver tends to be far more responsive. Any dollar of buying or selling is 10x more impactful for silver.

The silver market’s small size is one of this metal’s greatest strengths. Compared to the vastly-larger broader markets, it doesn’t take much new buying to catapult silver dramatically higher. Speculators and investors alike usually get interested in shifting capital into silver when gold is already rallying. Silver then tends to rally much more than gold, leveraging its upside, because silver inflows are relatively larger.

Given gold’s good performance this year, silver and the stocks of its miners should’ve surged. Year-to-date gold is up 11.3%, well ahead of full-year 2016’s 8.5% gain. But instead of amplifying gold’s 2017 advance by 2x to 3x like usual, silver is only up 6.7% YTD as of this week. This makes for really poor leverage to gold of 0.6x. Last year silver rallied 15.1%, yielding still-weak-but-more-normal 1.8x upside leverage.

Silver’s serious underperformance relative to gold this year has greatly retarded traders’ interest in the silver miners’ stocks. The leading silver miners’ trading vehicle and sector-index proxy is the SIL Global X Silver Miners ETF. Because of the great profits leverage to silver inherent in the silver miners, their stocks usually amplify silver’s upside. But YTD SIL is only up 4.0%, for extremely-poor 0.6x leverage!

Gold stocks aren’t having a great year either, with their leading GDX ETF only up 11.5% YTD compared to gold’s 11.3% gains. Like silver stocks, their gains tend to multiply their underlying metal’s gains by 2x to 3x. But the gold stocks’ weak in-line performance so far in 2017 highlights just how bad silver stocks’ lagging performance is. They have been largely drifting comatose this year, hardly even responding to silver.

Silver stocks have serious problems, and they certainly aren’t fundamental. Every quarter I analyze the latest operating and financial results from the top silver miners of SIL. They will soon start reporting their new Q3’17 results, but the prior quarter’s are the latest now available. In Q2’17 SIL’s elite top silver miners reported average all-in sustaining costs of $11.66 per ounce, well below average silver prices of $17.18.

That implies hefty industrywide silver-mining profits of $5.52 per ounce. While the average silver price did slump 2.0% sequentially in Q3 to $16.84, that’s certainly no fundamental threat. Assuming flat mining costs, the silver miners still should’ve been able to earn $5.18 per ounce last quarter. That’s down 6.2% quarter-on-quarter, but is still very profitable. Fundamentals can’t explain silver stocks’ vexing malaise this year.

That narrows down the suspect list to technicals and sentiment. This first chart looks at the price action in SIL and silver over the past couple years or so. Silver miners’ responsiveness to silver moves was excellent last year, but is decaying dramatically this year. With speculators and investors abandoning this sector, it’s barely budging. That has spawned a vicious circle convincing other traders to avoid silver stocks.

Silver stocks’ troubling lethargy is new this year. Back in December 2015 two days before the Fed’s first rate hike of this cycle, silver slumped to a major 6.4-year secular low in concert with gold. Silver stocks bottomed just over a month later in January 2016 paralleling the gold stocks. SIL fell to an all-time low in split-adjusted terms that day. A couple months earlier, Global X had executed a 1-for-3 reverse split in SIL.

Silver stocks were so deeply out of favor in late 2015 that this leading ETF’s managers feared SIL’s price would collapse low enough to risk delisting! Out of that very despair, strong new bull markets in silver and its miners’ stocks were born. In just 6.9 months from mid-January to mid-August 2016, SIL rocketed 247.8% higher on a 40.6% silver rally! That made for outstanding 6.1x upside leverage to silver prices.

Naturally silver and its miners’ stocks were soon sucked into gold’s correction following its own new bull’s initial upleg. Those silver and SIL corrections ballooned to monstrous proportions, thanks to gold-futures stops being run then Trump’s surprise election victory unleashing stock-market euphoria. So over the next 4.2 months, silver and SIL plunged 20.1% and 42.5%. SIL’s downside leverage to silver of 2.1x was modest.

2016’s behavior is the way silver stocks normally react to silver-price moves. The blue SIL and red silver lines above were closely intertwined last year. Silver stocks generally rallied and fell sharply in lockstep with silver itself. This normal behavior carried over into the first couple months of 2017, when SIL surged 33.6% between late December 2016 and early February 2017 on a mere 12.5% parallel rally in silver itself.

Silver stocks were leveraging silver’s upside by 2.7x, near the high end of their usual 2x to 3x range. So back in late January the silver stocks’ 2017 prospects looked really bullish. Things started going awry in February and March. The silver stocks corrected hard, plunging 21.1% in a month on a relatively-small 4.5% silver pullback. That made for big 4.7x downside leverage that was quite excessive, scaring traders.

So they started to flee silver miners’ stocks, a trend that’s continued ever since. With each subsequent silver rally since March, silver stocks have become less and less responsive to silver upside. This year’s blue SIL line above is no longer mirroring and amplifying the underlying volatility in the red silver line. It’s as if silver stocks are flatlining relative to silver, which is very strange. I can’t recall seeing anything like this.

Thus silver stocks have been stuck in a descending-triangle consolidation pattern for much of this year. They finally enjoyed breakouts from this triangle’s upper resistance and SIL’s 200-day moving average in August, mirroring similar major breakouts in gold stocks. But silver stocks’ responsiveness to silver continued decaying. In a month leading into early September, SIL only climbed 11.3% on an 11.5% silver rally.

Technically it looks like silver stocks have largely disconnected from silver. They’ve lapsed into this super-weird zombified comatose state. Speculators and investors alike aren’t the least bit interested in silver miners today, because they’re performing so poorly. And the resulting lack of participation in this sector scares away other traders, exacerbating the problem. Silver stocks have effectively been left for dead.

After decades studying and actively trading silver stocks, I’ve pondered this strange anomaly quite a bit in recent months. It’s certainly not fundamentally-driven, as silver miners’ earnings are looking good. It’s likely not technical either. While silver stocks are really underperforming, they haven’t suffered a serious selloff. SIL’s triangle support around $33 has held rock solid all year long, so this is a consolidation not a correction.

That leaves sentiment as the culprit behind silver stocks’ vexing stupor this year. Traders’ psychology is important in all markets, but disproportionately so in silver. Silver is a tiny highly-speculative market, exceptionally sensitive to shifting winds of sentiment. While weak technicals breed bearish sentiment and that becomes self-reinforcing, there had to be some root causes poisoning silver psychology earlier this year.

I suspect multiple factors are to blame. Once again silver sentiment is heavily dependent on gold. In the wake of Trump’s election win almost a year ago, stock markets soared in Trumphoria on hopes for big tax cuts soon. That hammered gold, which is hostage to stock-market fortunes. Gold is an anti-stock trade that usually moves counter to stock markets, so gold investment demand collapsed after the election.

Gold’s own psychology was utterly miserable late last year, exceedingly bearish. When gold fell to $1128 right after the Fed’s second rate hike of this cycle last December, Wall Street forecasts calling for a plunge under $1000 exploded. Traders don’t get interested in silver until gold is already rallying, so the extreme gold gloom and doom late last year certainly tainted silver sentiment. It has yet to recover from that.

Though gold bounced sharply and has enjoyed a good 2017, silver oddly didn’t join in. Gold itself likely played a major role. Despite gold’s gains this year, gold sentiment has remained pretty bearish. With the stock markets magically levitating in Trumphoria on those fervent big-tax-cuts-soon hopes, gold was flying under traders’ radars. With virtually no enthusiasm for gold, silver psychology had nothing to feed on.

The speculative traders who flock to silver for its sharp rallies and big gains were finding greener pastures elsewhere. Throughout the year various mainstream stock-market sectors have surged, so traders could find strong gains outside the precious metals. I’m certain this year’s extraordinary bitcoin bubble diverted interest away from silver too. The stratospheric skyrocketing of bitcoin prices has captivated traders.

Bitcoin’s value is hyper-speculative, as bitcoins are a synthetic virtual construct given perceived worth by software creating artificial scarcity. Having been in the financial-newsletter business for almost a couple decades now, I hear and read endless market anecdotes. This year I’m seeing the same types of traders who are usually interested in speculative silver raving about bitcoin instead. Bitcoin is a speculative mania!