If you mention Ecuador in mining circles, you will get some raised eyebrows and mumbled cuss words from Canadian mining executives. This is because of Ecuador’s reaction in 2013 that looked like resource nationalism which resulted in a moratorium on mining activity and a hefty tax on profits. Ecuador’s infamous windfall profits tax and a series of other unfavorable provisions made almost any mining project unprofitable

The windfall profits tax was a 70-per-cent levy on excess profits, the terms of which, such as what are excess profits, had previously been subject to negotiation between company and government, leading to an uncertain business environment.

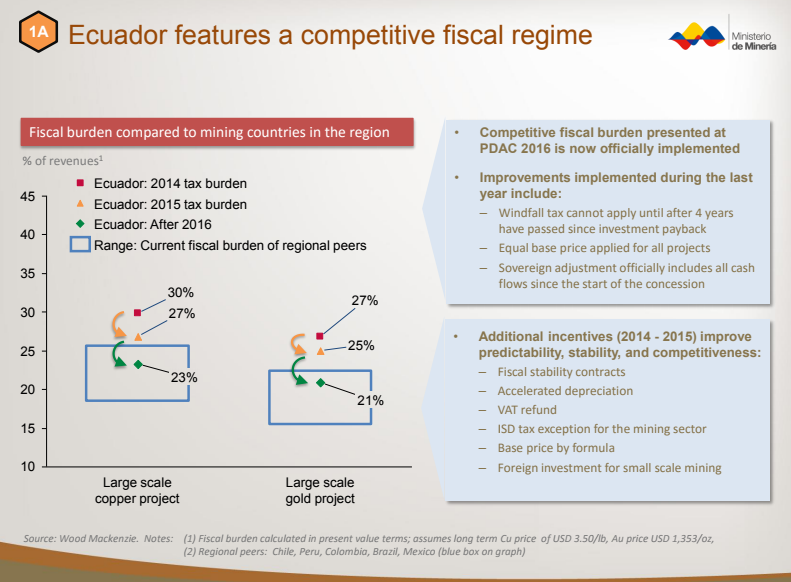

However, lessons were learned and Ecuador hopes to position itself as the up-and-coming mining investment destination in Latin America. The Ecuadorian government hired consultants Wood Mackenzie to provide recommendations and the country is adopting them quickly.

Ecuador, which depends on crude oil for half its national budget, is seeking to drum up more foreign investment after the recent crude price slump slashed government revenue. The government in 2015 separated the mining ministry from its oil ministry and announced plans to promote 36 projects to produce gold, copper and molybdenum estimated to be worth US$200bn.

It started in 2013 when Kinross Gold (TSX: K) walked away from the negotiating table after two years of fruitless talks with the Ecuadorian government over the investment conditions for the Fruta del Norte (FDN) project, one of Latin America’s biggest undeveloped gold deposits.

It also didn’t help that shortly before, IAMGOLD (TSX: IMG) had sold its Loma Larga project and left the country, and shortly afterwards, International Minerals sold its Río Blanco gold project and also said goodbye.

Kinross’ decision telegraphed to investors that negotiations with Ecuador were difficult and indicated to the country that its mining framework was not working. In exasperation and desperation, Kinross sold the construction-ready Fruta del Norte in 2014 for US$240 million, close to a quarter of what it paid to acquire the project in 2008.

Kinross bet on FDN and lost. The same year that Lundin Gold (TSX: LUG) bought the project, Ecuador embarked on a mission to make its mining framework more competitive and attractive.

Lundin obtained approval for the FDN environmental impact study in October 2016 and in December signed an exploitation agreement and an investment protection contract with the government. Construction of the 340,000 ounces per year mine has begun.

Lenin Moreno, who took office as President in May 2017, wants to attract US$4.6 billion in investment over his term in office for large-scale mining projects from companies including Lundin Gold, EcuaGold Mining, INV Metals, EcuaCorriente, Cornerstone Capital Resources (TSX-V: CGP), BHP Billiton and China Explorcobres. The investments hope to quadruple employment in the mining industry through 2022, according to Wood Mackenzie.

Two Chinese-owned mines are due for startup in the near term; the large-scale Mirador copper mine, controlled by the CRRC-Tongguan consortium, and the smaller Río Blanco, now operated by Junefield Mineral Resources.

There is a resurgence in exploration with several junior mining companies increasing activity in the country. Ecuador is looking to create a mining venture exchange. The plan is to link trading in junior mining stocks on the Toronto and Quito exchanges as part of a bid to finance US$488 million in exploration, the mining ministry said.

“We’re democratizing the industry. Local investors will be able to invest in mining, which is becoming a prosperous sector,” says deputy industrial mining secretary Henry Troya. “We’re building a sustainable industry.”

Other countries have gone down this road; Peru’s pioneering Lima venture exchange managed to list a dozen exploration companies at its height, including Karmin Exploration (TSX-V: KAR), Duran Ventures (TSX-V: DRV) and Red Eagle Mining (TSX-V: R). Santiago followed its example with its own venture exchange in 2014. However, with scant data on these exchanges, the scale of participation from Peruvian and Chilean retail investors is yet to be proved.

Ecuador has started to awarding exploration concessions after a hiatus of some six years, mines minister Javier Cordova told Mining Journal. Ecuador has overhauled its mining concessions registry and 237 concessions have been awarded to date to local and international mining companies, according to the ministry.

The ministry aims to boost mining exploration investment to US$600 million by the end of the year according to the newspaper El Telégrafo, citing Troya’s presentation at a mining conference in Quito. At least 27 companies have set up offices in Ecuador this year, including BHP Billiton, Newmont Mining, Fortescue Metals Group, Hancock Prospecting and Newcrest Mining.

The ministry is tracking mining exploration projects including Codelco-Enami JV Llurimagua and Cornerstone’s Cascabel. Ecuador’s mining chamber is further pushing the government to change both a tax on windfall profits and a capital gains tax to make the industry more competitive.

Improvements to the tax code that were implement in 2016 include: windfall tax cannot apply until after four years have passed since investment payback and an equal base price applied for all projects. These are some reforms and there is plenty of way to go.

With big pushes, often come big push backs, the question remains whether Ecuador can commit to mining reform and development without a backlash from its residents, it has happened in the past.

Mining is cyclical and investors need to make hay while the sun shines. Timing is everything and it appears senior Canadian mining companies are missing out on a period of economic optimism in the Ecuadorian mining industry after bearing the brunt of an unreceptive local climate in the past. Ecuador has made significant reforms and be sure there will be a lot of exploration news coming out of this region.

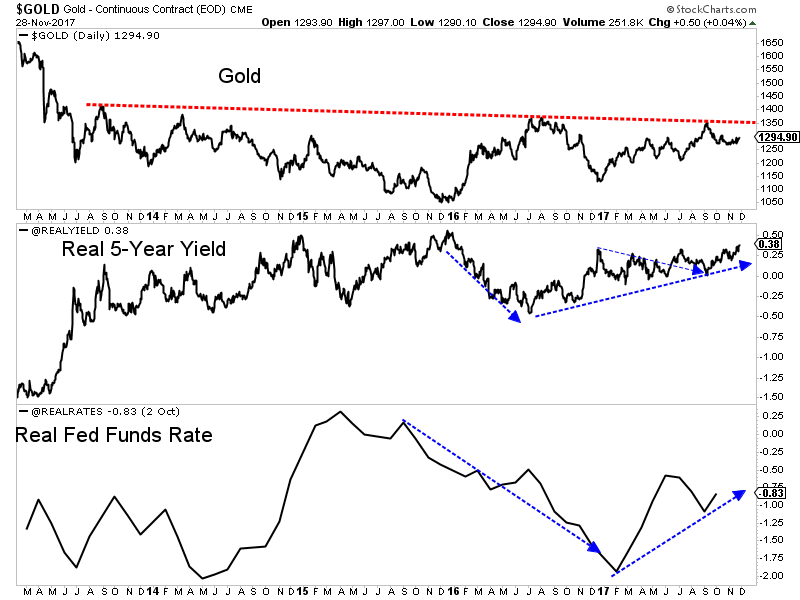

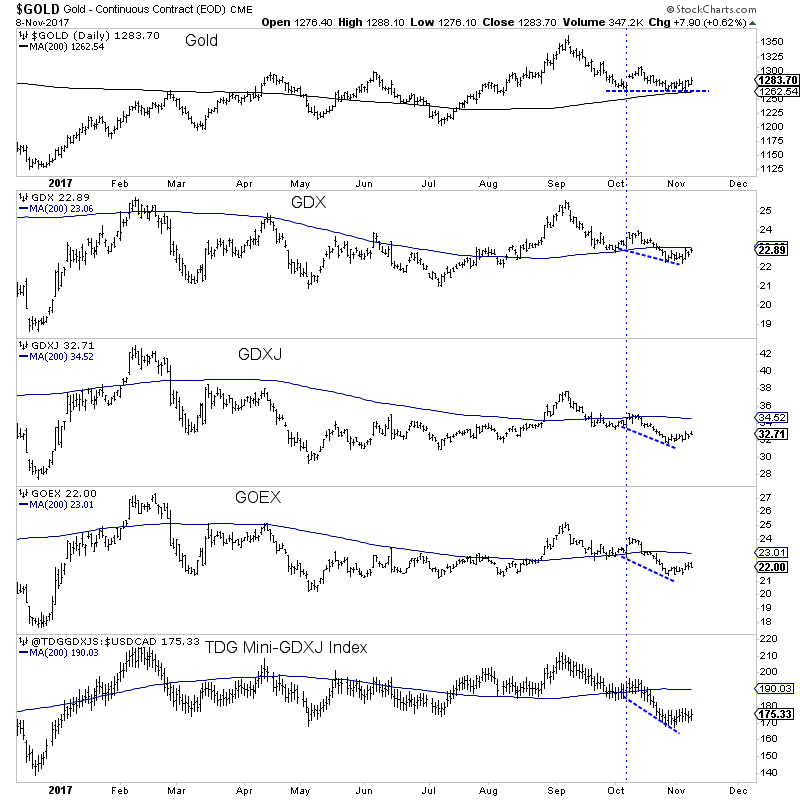

Too many technical analysts dismiss fundamentals. True, technicals usually lead fundamentals but understanding the fundamental drivers (when it comes to Gold) can give you an edge. Gold and gold stocks have remained below their 2016 peaks even in the face of a very weak US Dollar because the fundamentals are not there. Real rates have been stable in 2017 while the yield curve has been flattening. Until things change, Gold and gold stocks have little chance to breakout.

If you follow my work you know that there is a strong inverse correlation between the Gold price and real interest rates. Gold performs best when real rates are declining and especially when real rates decline while in negative territory. Real rates declined sharply into and during 2016 but have been rising or stable this year. The current problem for Gold is nominal yields have trended higher and faster than the rate of inflation.

In the chart below we plot Gold, the real 5-year yield (as calculated from the TIPS market) and the real Fed Funds Rate (rFFR). The US Treasury provides daily data of the real 5-year yield and we can see that it has trended higher since summer 2016 and is currently at its highest levels since Q1 2016. It has advanced nearly half a percent since its low a few months ago. Meanwhile, the rFFR has increased by more than 1% this year. That was after falling by nearly 2%.

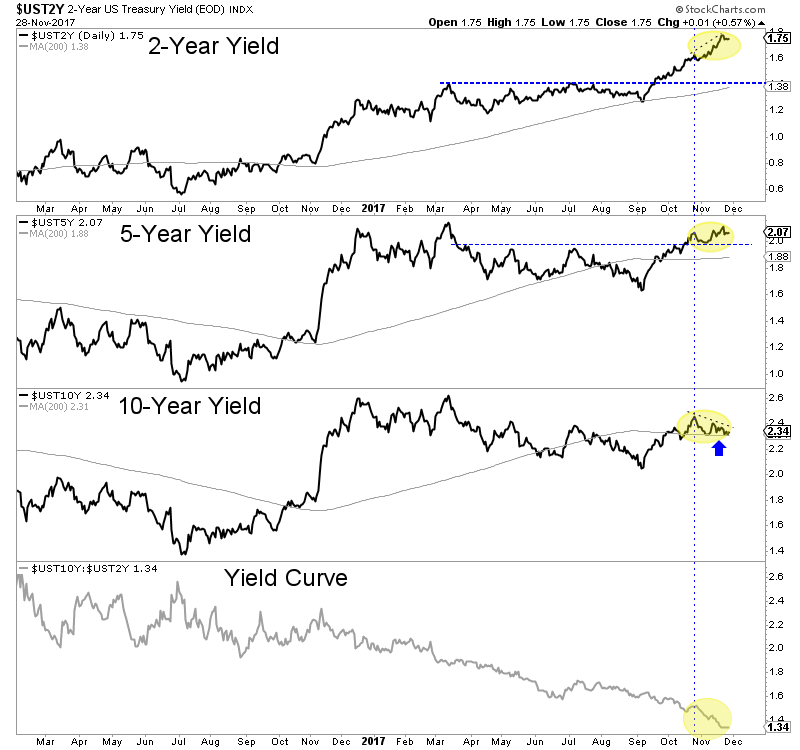

As we discussed weeks ago, a steepening yield curve (caused by falling short-term rates or rising long-term rates) is bullish for Gold. Some gold bugs are excited about a flattening yield curve as it could lead to inversion. While this may be true, a flattening curve is not bullish for Gold. Below we see that the yield curve continues to plunge (flatten) as the 2-year yield has surged and the 10-year is at the same level as two months ago. A bullish development for Gold would be the 5-year and 10-year yields exploding above their March 2017 highs while the 2-year yield arrests its torrid rise.

Gold and gold stocks are going to continue to struggle until the fundamentals align bullishly. Market action will of course lead fundamental changes but knowing the drivers to look for can help us anticipate the fundamental changes in advance. We think rising inflation is more likely than falling short-term rates to be the driver for Gold in 2018. In that case, we would anticipate hard assets to perform better, long-term rates to rise faster than short-term rates and inflation to outpace short-term rates. These things would sustain Gold beyond just a few months. In the meantime, the key for traders and investors is to find the companies with strong fundamentals and seek oversold situations with value and catalysts that will drive buying. To follow our guidance and learn our favorite juniors for 2018, consider learning more about our premium service.

Jordan Roy-Byrne CMT, MFTA

- The big picture for gold continues to strengthen. Please click here now. Double-click to enlarge.

- In 2016, gold began the year at about $1100, soared $300 an ounce to about $1400, but then it gave back about $250, and ended the year at about $1150 with only a $50 gain.

- That price action fit perfectly with my 2014 – 2017 theme of “rough sideways action, initially with a downside bias that develops into an upside bias”.

- The year 2018 should see solid Chindian demand, a reversal in US money velocity, and a peak in mine supply. That should push gold up from the enormous sideways trading pattern and into a substantial uptrend.

- Please click here now. Double-click to enlarge this key weekly gold chart.

- Note the fabulous increase in volume since 2016. This is very positive.

- One of my most important market mantras is that fundamentals make charts. I postulated the “gold will trade sideways with a slight downside bias” thesis in 2014 because I saw gold price discovery transitioning (slowly) away from the fear trade of the West and towards the love trade of the East.

- The imposition of the vile 10% import duty in India put millions of jewellery workers on the unemployment line and it caused a huge restructuring of the jewellery industry.

- The way it was playing out fundamentally suggested that an enormous inverse head & shoulders pattern would be created as that restructuring progressed.

- The transition in America from deflation to inflation and the peak in mine supply are supporting fundamental factors for the way the inverse head and shoulders pattern has been built.

- The bottom line is that in the right shouldering area of a massive inverse head and shoulders bottom pattern, investors should expect the price to trade sideways with an upside bias, and as the pattern nears completion, that upside bias will intensify.

- That’s exactly what is happening now. Gold is poised to end 2017 giving back very little of what it gained.

- Please click here now. Double-click to enlarge. The dollar’s action against the yen is a key indicator of the amount of risk that institutional investors are likely to take.

- On that note, the dollar has been very weak recently against the yen, breaking down from a bear wedge formation and forming a potential head & shoulders top. A potential weak right shoulder has yet to even materialize.

- Why is the dollar so weak? For the possible answer, please click here now. The US stock market has no more QE and falling interest rates to power it higher in the face of rather anemic real economy growth.

- Institutional investors are betting on tax cuts to keep the stock market party going, but it’s possible that major bank FOREX traders are selling the dollar in anticipation of a delay in getting the cuts done.

- I’m very disappointed with Corker’s plan to raise revenues (taxes) if tax cuts don’t generate growth. A chainsaw needs to be taken to US government spending, but it’s not happening. The US stock market could take a major hit if the tax cuts legislation fails.

- That could cause institutions to buy a lot more gold and assets like it. On that note, please click here now. Double-click to enlarge this spectacular bitcoin chart.

- Effective immediately, I’m raising my long term bitcoin target from $500,000 to $2million. I’ll go over the fundamentals and mathematics of that target upgrade in my nextwww.gublockchain.com update, but I’ll note that the reasoning is quite mundane.

- Still, I advised my subscribers to book some solid partial profits in the current $10,000 round number area early this morning. My accountant tells me that nobody gets poorer by booking a profit, and I agree!

- Do I think bitcoin has inherently more risk or less risk than the US dollar? That’s hard to quantify, but great profits can be booked now, and that’s really all that matters.

- Please click here now. Double-click to enlarge this nice GDX chart.

- There’s no question that some of the risky junior miners have had a very disappointing year, but most of the seniors are starting to look quite “perky”.

- GDX sports a beautiful bull wedge pattern, and the next US jobs report is scheduled for Friday, December 8. That report should be the catalyst for a great gold stocks rally. It should also start gold on its final advance towards the key $1400 neckline area of the massive inverse H&S bottom pattern, with an upside breakout occurring in 2018!

Thanks and Cheers!

Stewart Thomson, Graceland Updates

https://www.gracelandupdates.com

Email:

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

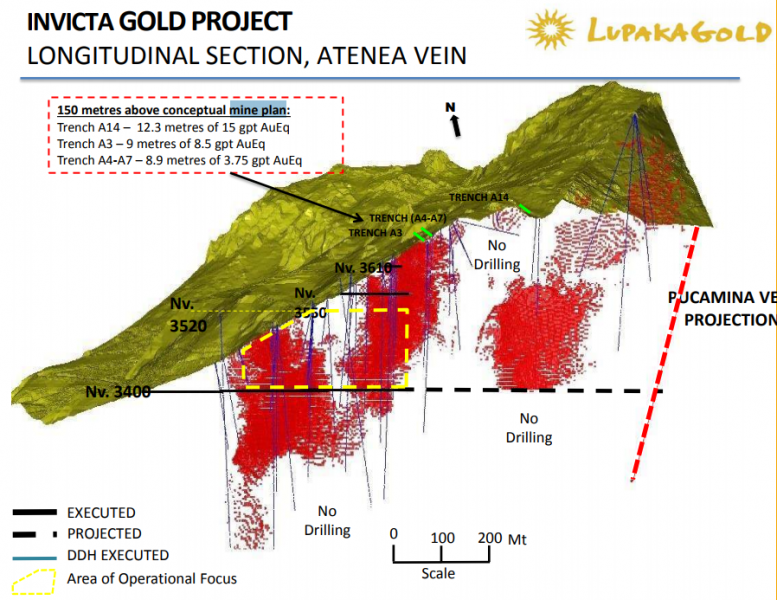

With the recent close of the sale of the company’s Crucero property to GoldMining (TSX-V: GOLD), Lupaka Gold Corp. (TSX-V: LPK) has secured the funds to take the next step with its Invicta Gold project. Today, the company announced the commissioning of a Preliminary Economic Assessment “PEA” for the Invicta Gold Project.

With the backing of Pandion Finance and its gold purchase agreement providing the necessary funding, Lupaka is motivated to meet its obligations which makes now an exciting time for the company and its shareholders.

The company has hired SRK to prepare the PEA. This provides a continuity of project knowledge as the project’s 2012 resources estimate was prepared by SRK and the company’s own internal mining studies of Invicta were prepared with assistance from SVS Ingenieros of Lima “SVS”, Peru, a subsidiary of the SRK Consulting Group. The company plans the completion of the PEA technical report in the first quarter of 2018.

The initial six-year mine plan that was developed and prepared by SVS, which outlined ~735,000 tonnes at a grade of ~6.1 g/t AuEq. for 23,000 oz. of gold equivalent a year, according to a rough calculation. The plan was developed from the 3,400-metre level and extends up 120 metres.

Drill results indicated that the mineralization extends at least as far below the 3,400 level as it does above. In addition, there is a well-defined section of measured and indicated directly along strike to the northeast that is within a few hundred metres, and of the same characteristics as the segment in the mine plan.

The first bulk sample in October 2015 produced a copper, lead and zinc concentrate that was sold to an off-taker. The concentrate was exceptionally clean and was absent of any penalty elements, so buyers could pay well for it because they can mix it with less clean concentrate and blend it.

The company completed its second run-of-mine bulk test in February 2016 and achieved good recoveries in concentrate streams — returning 87.5% gold, 91.2% silver, 91.5% copper, 90.03% lead and 90.1% zinc. The sample was a blend of approximately 80 % run-of-mine material and 20 % from a low grade stockpile derived from development.

The bulk sample was processed with the prime objective of producing a saleable concentrate and no effort was made to optimize content of specific metals, according to the company. The resulting concentrate was clean, with few penalty elements which is ideal for sale and blending with other concentrates.

Once in production, the hope is that cash flow from Invicta will be used to grow the operation. There are numerous zones outside of the Atenea vein that contain mineralization, and the targeted Atenea resource could increase, as development offers access to high-grade intercepts and underground drill sites. In addition, based on gold and copper within the under-explored quartz-sulphide vein zones, the company believes the Invicta resource could expand.

At 350 tonnes per day, Invicta could operate for between 10 and 15 years based on the current measured and indicated resource in the Atenea zone. However, the project is permitted to operate at 1,000 tonnes per day and the company would like to increase their resources through drilling, expand operations to the 1,000 tpd rate and build their own mill on site but for the time being will use third party transport and processing contractors. All of this could take production to over 70,000 AuEq. oz/yr, according to a cocktail napkin calculation.

Proceeds from Invicta will also be used for more exploration at its other projects in Peru — Josnitaro which is a whole other story, worthy of an update of its own.

***MiningFeeds was compensated to provide marketing services. As always, do your own diligence. The writer of this article, Nicholas LePan does own shares.

The following interview of Stephen Dunn, President & CEO of Crown Mining Corp. (TSX-v: CWM) was conducted by phone & email over about a 10-day period ended November 21st. Crown Mining has a NI 43-101 compliant mineral resource estimate of 2.1 billion Indicated & Inferred pounds Copper (“Cu“). In about 4 months, management plans to deliver a Preliminary Economic Assessment (“PEA“) on a portion of its 2.1-billion-pound resource.

Steve, please give readers an overview of Crown Mining.

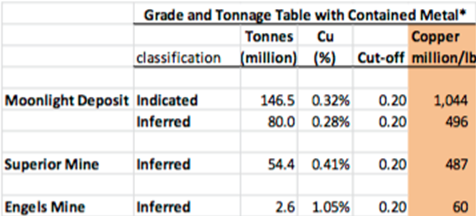

Crown Mining Corp. (TSX-v: CWM) is focused on advancing its 100% controlled Moonlight-Superior Copper project in Plumas County, which is in northeastern California. Moonlight-Superior has a NI-43-101 resource of 2.1 billion pounds Cu, 750,000 ounces Gold and 25,000,000 ounces Silver. At today’s spot prices, the gold & silver ounces equate to more than 400,000,000 pounds Cu Eq. Our property hosts 4 known Cu deposits.

The Moonlight deposit alone hosts a NI 43-101 Indicated mineral resource of ~161 M short tons at an average grade of 0.324%, equal to ~1 billion pounds Cu, and an Inferred mineral resource of ~88 M tons at an average grade of 0.282%, equal to ~ 500 M pounds Cu. So, combined, the Moonlight deposit hosts 1.54 billion pounds Cu [Indicated (68%) & Inferred (32%)].

Two other deposits, Superior & Engels, have a combined NI 43-101 Inferred mineral resource of ~63 short tons at an average grade of ~0.44%, equal to ~ 550 M pounds Cu.

Crown recently had third-party metallurgical testing done and is awaiting final results. Findings will be used in a PEA report that will be started soon and is expected to be finished by the end of March, 2018.

And, how about a brief summary of the history of your controlled property.

Copper was discovered in the 1880’s and the most prolific mining period took place from 1915 to 1930. During that time, 4.7 million short tons of ore were extracted, yielding 161,500,000 pounds Cu, (Cu grade 2.2%), 1,900,000 ounces Silver, and 23,000 ounces Gold. Recoveries were reportedly around 80%.

From 1962 to 1994, Placer AMEX drilled over 400 holes and calculated a (non NI 43-101 compliant) 4-billion-pound Cu resource. We have a lot of the Placer data. Even though our team is not relying on that 4-billion-pound figure, we think it speaks to significant exploration potential.

From 2004 to 2011, various juniors drilled 54 holes and conducted airborne geophysics, which supported a 2007 technical report containing a mineral resource estimate. That report remains NI 43-101 compliant today.

From 2013-2017 we acquired 132 unpatented claims and a lease for the 36 patents covering the Superior and Engels mines. In 2013 we published a third-party NI 43-101 compliant mineral resource report at Superior of about 500 M pounds Cu. In March 2016, we option 300 claims covering the Moonlight deposit and started a scoping study and metallurgical tests this year.

Is Crown Mining’s 2.1 billion pounds of Indicated & Inferred Copper (“Cu“) resource NI 43-101 compliant?

Yes, it is. That 2 billion + pound figure comes from two reports, one from 2013 and one from 2007, but both are NI 43-101 compliant. The reports cover 3 deposits, (Moonlight, Superior & Engels) but they are part of the same system, about 1.5 miles across as the crow flies. There are 4 known deposits in an area of about 7 sq. miles (18 sq. kms) in northeast California.

We hope to find one or more new deposits before it’s all said and done.

We already know we’re sitting on a large, bulk-scale, open-pittible Cu resource that will likely have meaningful Silver credits. We plan to publish a PEA in the first quarter of 2018 that will provide indicative answers to many important questions.

How much capital will you need to raise to deliver a PEA next year?

We run a tight ship, our cash burn is quite manageable. The avoidance of undue equity dilution is very important to us, that’s why we capped our recent capital raise at C$ 200k. [NOTE: Crown Mining has just 34 M shares outstanding]. That, along with cash on hand, will cover us through March or April. So, we don’t need to raise capital anytime soon. If all goes well, our share price will be meaningfully higher next spring after we release the PEA.

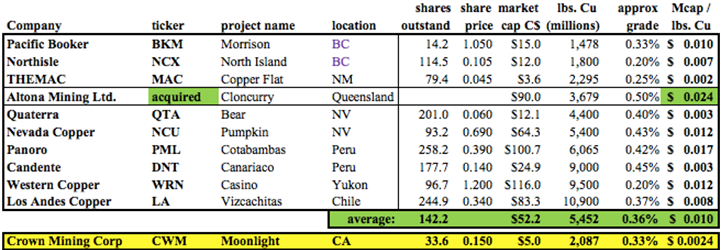

I believe we are in the early stages of a multi-year bull market in Copper that will be a tailwind for us next year. Analysts and pundits seem to indicate that a sustained Cu price above US3.50/lb., is an important milestone; a price at which producers are willing to put money to work through investments in new projects and pursue outright acquisitions of juniors like Crown Mining.

In fact, just a few days ago, Copper Mountain Mining (TSX: CMMC) announced a takeover of Australian-listed Altona Mining Ltd. at a headline valuation of ~ C$0.024 per pound of Cu resource. That valuation is 10x that of ours. {See chart below}. To be fair, Altona is well more advanced than we are, which accounts for some of the premium.

Large-scale, near-surface mineralization, in a safe jurisdiction, with good access to infrastructure is great, but poor metallurgy could end the story. What do you know about the project’s metallurgy?

That’s a good question. We are very much aware of the critical importance of what are recoveries might look like, and how much processing the ore will cost. Historical mining activity from 1915 to 1930 had recoveries around 80%. Placer Amex did various studies in the 1960’s that pointed to recoveries closer to 85%.

Earlier this year we commissioned a round of metallurgical testing by a well-respected third-party. We are awaiting the final detailed results, but I’m happy to report that, generally speaking, recoveries were approximately 85%, similar to the findings of Placer Amex.

Although the U.S. is obviously a safe jurisdiction with many mining friendly attributes, some readers will be concerned about “California permitting risk.” Are investor concerns warranted?

You’re right, we do get asked a lot about permitting risks in California. We believe that that once the permitting process starts, probably not before the 2nd half of 2018 at the earliest, we could be facing a timeline of roughly 3 years.

Most investors don’t understand the permitting process in California. The way in which it proceeds can actually work in favor of a company. The County is the lead agency to collaborate with in presenting proposed projects at the State level. Moonlight-Superior is in a remote, low population density, mining-friendly County near the Nevada State line.

We’ve spoken with a number of people in the area and have received positive feedback, but our main focus is really on delivering a PEA and then attracting a strategic partner.

We covered these topics, but to reiterate, what are the near-term catalysts for Crown Mining over the next 3-6 months?

Near-term catalysts include the release of a PEA around the end of March next year. Before then, we will be putting out a press release that details the results of third-party metallurgical testing done earlier this year. Finally, we expect to be in the position next month to announce a prominent new addition to our team.

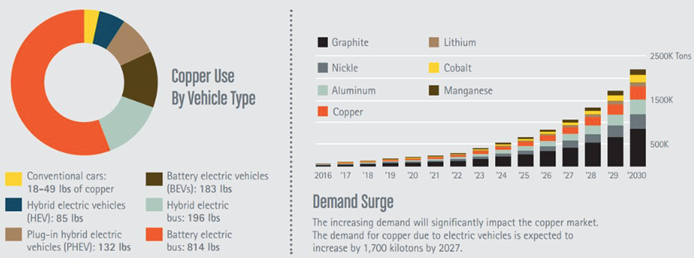

Underlying all of this is a strong Cu price, up about 50% from the summer of 2016’s prices near US$2/lb., and down about 4% from a high of US$3.24/lb. a month ago.

As the chart above clearly shows, Cu demand is very likely to be much stronger than anyone expected even just a year ago. The electrification of the global transportation fleet, grid-scale energy storage and the ongoing transition to renewable energy sources, especially wind power, are Cu intensive.

Yet, global supply constraints — (decades of declining ore grades at existing mines, fewer large Cu discoveries and ever growing geopolitical risks) — suggest that prices need to move higher, possibly a lot higher, to entice companies to invest large sums of capital on big projects.

We think 2018 will be an exciting year for juniors like Crown Mining Corp. (TSX-V: CWM) as more and more investors realize how incredibly important Cu is, and will be, to the world economy over the next few decades.

Thank you Stephen, I think we covered a lot of ground here. Good luck with the PEA!

Disclosures: The content of this interview is for illustrative and informational purposes only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research, [ER] including but not limited to, commentary, opinions, views, assumptions, reported facts, estimates, calculations, etc. is to be considered implicit or explicit, investment advice. Further, nothing contained herein is a recommendation or solicitation to buy or sell any security. Mr. Epstein and [ER] are not responsible for investment actions taken by the reader. Mr. Epstein and [ER] have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Mr. Epstein and [ER] are not directly employed by any company, group, organization, party or person. Shares of Crown Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Peter Epstein owned shares in Crown Mining and the Company was an advertiser on [ER]. By virtue of ownership of the Company’s shares and it being an advertiser on [ER], Peter Epstein is biased in his views on the Company. Readers understand and agree that they must conduct their own research, above and beyond reading this article. While the author believes he’s diligent in screening out companies that are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & [ER] are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article. Mr. Epstein & [ER] are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and [ER] are not experts in any company, industry sector or investment topic.

![]()

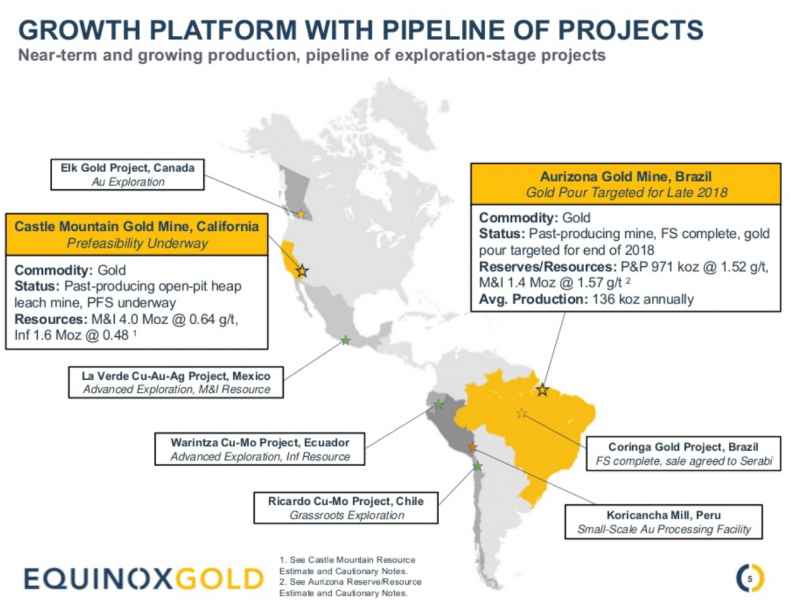

On Oct. 25, NewCastle (TSX-V: NCA), Trek Mining (TSX-V: TREK), and Anfield Gold (TSX-V: ANF) announced a three-way business combination to form Equinox Gold (TSX-V: EQX). The new company will be led by mining entrepreneur Ross Beaty as Chairman (who is investing US$20 million), Christian Milau as CEO, and Greg Smith as President (both from Trek). This will immediately create a well funded mid-tier gold company on the path to production with plenty of potential for investors.

A note from TD Securities’ Analyst Daniel Earle, outlined the value this deal will create. TD Securities views this transaction positively as the merger will create a company that is more than the sum of its parts.

“In essence, we have what we view to be two unfunded and poorly understood development stories merging with a cash shell to create a higher profile company, both in terms of its leadership and market size, with a fully funded path to eventual mid-tier production.“

The combined company is expected to have $98 million in cash less costs at closing, excluding any asset sales, plus a US$85-million credit facility with Sprott and a US$200-million development facility. TD has a $2.00 12-month target price which is based on 0.9x its pro forma Equinox corporate NAV5% of $2.25/share.

If investors were looking to benefit early from the merger of the three companies, TD notes that NewCastle is currently trading at 0.32x their corporate NAV of 5% as of Nov. 1 which represents a significant discount to its peer group of gold development-stage companies in TD’s precious metals coverage, which are trading at an average of 0.49x NAV5%.

The new company’s main two assets will be the 100-per-cent owned Aurizona Mine in the Brazilian State of Maranhao and the Castle Mountain Project in California. However, there are plenty of projects that could generate other sources of value.

The Aurizona Mine is a past producer from 2010 to 2015 under Luna Gold, which failed under the heavy burden of a 17-per-cent gold stream and debt facility owed to Sandstorm Gold. The stream was restructured in March 2015 to a sliding-scale royalty of three to five per cent (3% at <US$1,500/oz Au). The mine has 971 koz @ 1.52 gpt in reserves and 1.4 Moz @ 1.57 gpt (Measured & Indicated Resources, inclusive). Annual production of 136 koz at US$691/oz (AISC: US$754/oz) over a 6.5-year mine life. First gold coming out of the mine is expected in the first quarter of 2018.

The Castle Mountain project is a past producer from open pit/heap leach and a small mill from 1991–2002. An updated resource estimate is due in September following a 44 km infill drill program, with a Pre-Feasibility study expected in Q1/18. The property has a resource of 4.0 Moz @ 0.64 gpt (Measured & Indicated Resources). There is plenty of potential for further exploration and resource expansion at Castle Mountain, if permitting proceeds smoothly.

The company also has prospective claims and spin out possibilities in Ecuador, British Columbia, Mexico, Chile and Peru. The company has generated more cash from the sale of assets from Anfield raising $22 million from the sale of the Coringa Gold project and the spin-out of copper assets in Mexico (La Verde — 746 Mt @ 0.4% CuEq M&I+I), Ecuador (Warintza — 195 Mt @ 0.6% Inf.) and Chile (Ricardo — concept/exploration) in 2018.

The transaction, if approved by the shareholders of Newcastle and Anfield, is expected to close on or about Dec. 22, 2017, just in time for Christmas, a possible gift for weary gold investors.

Eight Colombian municipalities banned mining in their jurisdictions after local referendums won a majority vote in support of banning mining.

A series of municipalities across Colombia this year have demonstrated an overwhelming support for curtailing mining activities within their regions; a serious concern for investors and resource companies after the government of Colombia has been encouraging development to further build the peace with FARC.

An important sector that will benefit from the peace will be the extraction industries, especially the gold mining industry. During the years of conflict, the gold industry was plagued by internal criminal activity with unlicensed illegal mines bringing in approximately $7bn per year for armed groups and other criminal factions. The illegal mining also damaged the environment through polluting the water with substantial amounts of mercury used to separate gold from other minerals.

In an effort to clamp on down the violence and environmental damage of illegal mining, the government of Colombia has been encouraging foreign investment into the mineral industry while encouraging local governance in an effort to build the peace. FARC agreed to disarm but they have moved from the battlefield to politics, and with them come a very strong anti-development stance against foreign resource companies. Not all opposition to development is politically motivated but it also a part and parcel of changes to the mining code and as communities are experiencing control over projects for the first time.

The first vote of this year, held in February, took place in Cabrera with seven other municipalities followed to ban mining in their territory, according to Colombia Reports. Residents of Colombian municipalities have expressed a growing concern over the environmental impacts of mining on their towns––while some that farm for their livelihood are worried of how this may also impact crops nearby mining locations.

Colombia’s mining code had prohibited local authorities from suspending projects in their region, according to Bloomberg. A ruling enforced by Colombia’s Constitutional Court last year made these votes possible, as the ruling overturned the Colombian government’s exclusive authority to authorize mining projects. Now local politicians or residents that have obtained a certain number of signatures can call a referendum, reported Bloomberg. A mine or oil field that was already licensed to produced would not be impacted by the vote.

Residents of Cajamarca, located in the municipality of Tolima made headlines in March. The vote to man mining froze the current La Colosa project, controlled by AngloGold Ashanti, a gold mining company from South Africa. AngloGold Ashanti has invested $900 million towards mining projects in Colombia within the past decade, according to Reuters.

If the La Colosa project were to be completed, it would be one of the world’s largest open-pit gold mines. However, locals worry the mining in Tolima will negatively impact their water sources and pollute their environment, according to the BBC. The vote in Tolima, held on March 26, displayed overwhelming opposition against mining with 98.8 per cent against the project.

Just a few months later, in June 2017, a majority of locals in the Cumaral municipality voted in the first oil ban referendum passed in the country, which bans crude exploration, drilling and production, according to TeleSur.

Tauramena was the first municipality to enforce the ban, when a majority favoured to exile oil exploration in the country in December 2013, motivated by the population’s concern over the threat to water sources this practice may generate. The municipality located in Casanare, the central east region of Colombia, won the vote by 4,426 in favour of the ban out of 4,610 citizens that participated in the vote, according to El Espectador, a Columbian newspaper.

The municipality Cabrera, was the first to ban mining this year, as they voted in February, winning with 97 per cent in favour, according to El Espectador. The official question voters answered was, “Do you agree, yes or no, that mining projects and/or hydroelectric projects that transform or affect the use of land, water or agricultural vocation should be implemented in the municipality of Cabrera, Cundinamarca, as a Peasant Reserve Zone Township?” Only 23 voters approved this, according to the same source.

EMGESA, the Colombian electric power company that wants to impose mining and hydroelectric projects recently before the vote, the company restructured plans not to affect the municipality. However, a majority of voters in Cabrera wanted to protect the territory, as Cabrera has been recognized as a peasant reserve zone since 2000.

In response, the community of Cabrera has been working on a Sustainable Development Plan that does not consist of mining or hydroelectric plants. Paola Bolaños, a member of the Committee to Promote the Peasant Reserve Zone, said this project will ensure that the agricultural vocation is respected, reported by El Espectador.

Thus, a new era of peace is crucial for the government to take control of illegal mines in order to allow the economy to prosper while protecting the environment through greater provisions of the sector. Fundamentally, despite the peace plan costing $44bn over a 10-year period, it can be viewed as an investment into the stability of Colombia’s long-term peace prospects by ensuring effective governance.

Some resistance to mining is inevitable in a democracy especially in the nascent form of local governance permitted under the peace process. A further estimated 50 other municipalities will hold a referendum considering banning mining or not, within the next coming months, according to Colombia Reports.

This may be a setback for certain mining companies and the attractiveness of the country as mining jurisdiction in the short term. In the long run, if companies and communities can learn to work together it could improve the appeal of inviting extraction industries into the country. One should prefer the ballot box over a return to armed conflict. Colombians will be better off and so will the extraction industries with peace.

***MiningFeeds would like to make a special note that Savanna Craig contributed heavily to the writing and research of this article

The silver miners’ stocks have really languished this year, grinding sideways to lower for months on end. This vexing consolidation has fueled near-universal bearishness, leaving silver stocks deeply out of favor. But once a quarter when earnings season arrives, hard fundamentals pierce the obscuring veil of popular sentiment. The silver miners’ recently-reported Q3’17 results reveal today’s silver prices remain profitable.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. These are generally due by 45 days after quarter-ends in the US and Canada. They offer true and clear snapshots of what’s really going on operationally, shattering the misconceptions bred by the ever-shifting winds of sentiment. There’s no silver-miner data that is more highly anticipated than quarterlies.

Silver mining is a tough business both geologically and economically. Primary silver deposits, those with enough silver to generate over half their revenues when mined, are quite rare. Most of the world’s silver ore formed alongside base metals or gold, and their value usually well outweighs silver’s. So typically in any given year, less than a third of the global mined silver supply actually comes from primary silver mines!

The world authority on silver supply-and-demand fundamentals is the Silver Institute. Back in mid-May it released its latest annual World Silver Survey, which covered 2016. Last year only 30% of silver mined came from primary silver mines, a slight increase. The remaining 70% of silver produced was simply a byproduct. 35% of the total mined supply came from lead/zinc mines, 23% from copper, and 12% from gold.

As scarce as silver-heavy deposits supporting primary silver mines are, primary silver miners are even rarer. Since silver is so much less valuable than gold, most silver miners need multiple mines in order to generate sufficient cash flows. These often include non-primary-silver ones, usually gold. More and more traditional elite silver miners are aggressively bolstering their gold production, often at silver’s expense.

So the universe of major silver miners is pretty small, and their purity is shrinking. The definitive list of these companies to analyze comes from the most-popular silver-stock investment vehicle, the SIL Global X Silver Miners ETF. This week its net assets are running 6.6x greater than its next-largest competitor’s, so SIL really dominates this space. With ETF investing now the norm, SIL is a boon for its component miners.

While there aren’t many silver miners to pick from, major-ETF inclusion shows silver stocks have been vetted by elite analysts. Due to fund flows into top sector ETFs, being included in SIL is one of the important considerations for picking great silver stocks. When the vast pools of fund capital seek silver-stock exposure, their SIL inflows force it to buy shares in its underlying companies bidding their prices higher.

Back in mid-November as the major silver miners finished reporting their Q3’17 results, SIL included 29 “silver miners”. This term is used loosely, as SIL holds plenty of companies which can’t be described as primary silver miners. Most generate well under half their revenues from silver, which greatly limits their stock prices’ leverage to silver rallies. Nevertheless, SIL is today’s leading silver-stock ETF and benchmark.

The higher the percentage of sales any miner derives from silver, naturally the greater its exposure to silver-price moves. If a company only earns 20%, 30%, or even 40% of its revenues from silver, it’s not a primary silver miner and its stock price won’t be very responsive to silver itself. But as silver miners are increasingly actively diversifying into gold, there aren’t enough big primary silver miners left to build an ETF alone.

Every quarter I dig into the latest results from the major silver miners of SIL to get a better understanding of how they and this industry are faring fundamentally. I feed a bunch of data into a big spreadsheet, some of which made it into the table below. It includes key data for the top 17 SIL component companies, an arbitrary number that fits in this table. That’s a commanding sample at 92.7% of SIL’s total weighting.

While most of these top 17 SIL components had reported on Q3’17 by mid-November, not all had. Some of these major silver miners trade in the UK or Mexico, where financial results are only required in half-year increments. If a field is left blank in this table, it means that data wasn’t available by the end of Q3’s earnings season. Some of SIL’s components also report in gold-centric terms, excluding silver-specific data.

In this table the first couple columns show each SIL component’s symbol and weighting within this ETF as of mid-November. While most of these silver stocks trade in the States, not all of them do. So if you can’t find one of these symbols, it’s a listing from a company’s primary foreign stock exchange. That’s followed by each company’s Q3’17 silver production in ounces, along with its absolute year-over-year change.

After that comes this same quarter’s gold production. Pretty much every major silver miner in SIL also produces significant-if-not-large amounts of gold! While gold stabilizes and augments the silver miners’ cash flows, it also retards their stocks’ sensitivity to silver itself. Naturally investors and speculators buy silver stocks and their ETFs because they want leveraged upside exposure to silver’s price, not gold’s.

So the next column reveals how pure the elite SIL silver miners are. This is mostly calculated by taking a company’s Q3 silver production, multiplying it by Q3’s average silver price, and then dividing that by the company’s total quarterly sales. If miners didn’t report Q3 revenues, I approximated them by adding the silver sales to gold sales based on their quarterly production and these metals’ average third-quarter prices.

Then comes the most-important fundamental data for silver miners, cash costs and all-in sustaining costs per ounce mined. The latter determines their profitability and hence ultimately stock prices. Those are also followed by YoY changes. Finally comes the YoY changes in cash flows generated from operations and GAAP profits. But an exception is necessary for companies with numbers that crossed zero since Q3’16.

Percentage changes aren’t relevant or meaningful if data shifted from negative to positive or vice versa. Plenty of major silver miners suffered net losses in Q3’17 after earning profits in Q3’16. So in cases where data crossed that zero line, I included the raw numbers instead. This whole dataset offers a fantastic high-level fundamental read on how the major silver miners are faring today, and it’s reasonably well.

That’s reassuring given silver’s serious underperformance relative to gold this year. As a far-smaller market, silver usually amplifies gold’s advances by at least 2x. But as of the end of Q3, silver was only up 4.6% YTD compared to 11.3% for gold. That’s horrendous 0.4x leverage! And by mid-November as Q3’s earnings season wrapped up, silver’s YTD gain of 6.6% was still way behind gold’s 11.1% for 0.6x leverage.

Production is the lifeblood of miners, and thus the best place to start fundamental analysis. In Q3’17, these top 17 SIL components collectively produced an impressive 79.0m ounces of silver. If 2016’s world-silver-mining run rate is applied to this year’s third quarter, that implies 221.5m ounces of silver mined. Thus these top SIL silver miners would account for nearly 36% of that total, they truly are major silver players.

Their collective silver production looks robust, surging 3.7% YoY and climbing 0.6% sequentially quarter-on-quarter. Unfortunately that is misleading, with huge growth in a couple mining conglomerates masking sharp-to-catastrophic YoY declines for most of the rest of these elite silver miners. Fresnillo and Industrias Peñoles enjoyed gigantic 24% and 34% YoY gains in silver production off already-massive bases!

Fresnillo and Industrias Peñoles have an incestuous relationship, as the former used to be wholly owned by the latter. Industrias Peñoles spun off Fresnillo back in May 2008 on the London Stock Exchange. While Fresnillo’s financial reporting is decent, Industrias Peñoles’ is murky. Neither my decades studying financial statements as a Certified Public Accountant nor my rudimentary Spanish can penetrate very deep.

So I haven’t been able to track down how much of Fresnillo that Industrias Peñoles still owns, nor whether the silver production reported by these silver-mining behemoths is actually mutually exclusive. I’m assuming it is for this analysis, but I’m skeptical. Both companies reported their huge YoY growth in silver production was the result of Fresnillo’s new San Julián silver mine coming online, which is a big one.

San Julián produced 3499k ounces of silver in Q3’17 alone, along with fairly-large gold, zinc, and lead byproducts. It’s anticipated to produce 11.6m and 63.7k ounces of silver and gold annually for 12 years. Without San Julián, which could be double-reported between Fresnillo and Industrias Peñoles, the top SIL silver miners’ production would look very different. These elite silver miners have had a challenging year.

Excluding Fresnillo and Industrias Peñoles, the rest of these top SIL components saw their collective silver production fall a sharp 9.3% YoY to 45.9m ounces! It’s been quite ugly out there in silver-land, for both industry-wide and company-specific reasons. Between Q3’16 and Q3’17, the average silver price dropped 13.9% YoY to just $16.84. That was far worse than gold’s 4.2% YoY decline, testing silver’s economics.

With silver prices so weak, sentiment so bearish, and silver-stock prices so darned low, silver miners are both starved of capital for expansions and reluctant to invest heavily in the silver side of their businesses. Mining gold is far more profitable at today’s precious metals’ prices, so they continue to allocate scarce resources to growing their gold production. That certainly isn’t helping the purity of the major silver miners.

A couple long-time favorites of American investors saw silver production plummet over this past year. Tahoe Resources was originally spun off by Goldcorp to develop the incredible high-grade Escobal silver mine in Guatemala. Over the past year that country’s corrupt government shut this mine down after a frivolous and baseless lawsuit by anti-mining activists. They sued the government regulator, not Tahoe itself!

That lawsuit claimed Guatemala’s Ministry of Energy and Mines did not properly consult with the Xinca indigenous people before granting Escobal’s permits! That shouldn’t even be Tahoe’s problem if the government bureaucrats didn’t hold enough meetings, yet Escobal’s mining license was still temporarily suspended. It has since been reinstated, but the government is not breaking up an illegal roadblock to the mine.

This whole situation is ludicrous, highlighting why third-world countries stay that way. The government of Guatemala isn’t respecting the rule of law, which will greatly hurt future investment. It’s allowing violent anti-mine militants to physically attack trucks and their drivers heading to Escobal. They should be arrested and the blockade cleared. Thus Tahoe’s silver production collapsed 100% YoY from 5000k ozs in Q3’16!

SSR Mining saw a similar sharp 62% YoY plummet in silver production to just 1156k ounces in Q3’17. It had nothing to do with geopolitics like Tahoe’s mess, but is simply due to the forecast depletion of its old Pirquitas silver mine. SSR Mining, which used to be called Silver Standard Resources, is exploring in the area trying to extend the life of this mine. But most of its financial resources are being poured into its gold mines.

That gold focus among these top silver miners is common across SIL’s component companies. As the silver-percentage column above shows, most of these elite silver miners are actually primary gold miners by revenue! Only 6 of these 17 earned more than half of their Q3’17 sales from mining silver, and they are highlighted in blue. 8 of SIL’s top 17 component stocks are also included in the leading GDX gold miners’ ETF.

While they only comprised 10.0% of GDX’s total weighting in mid-November, this highlights how difficult it is to find primary silver miners. SIL’s managers have an impossible job these days with the major silver miners increasingly shifting to gold. They are really scraping the bottom of the barrel to find more silver miners. In Q3’17 they added Korea Zinc, making it SIL’s 4th-largest holding at 9.0% of this ETF’s total weighting.

That was intriguing, as I’d never heard of this company after decades of intensely studying and actively trading silver stocks. So I looked into Korea Zinc and found it was merely a smelter, not even a miner. The latest financial data I could find in English was 2015’s. That year Korea Zinc “produced” an incredible 63.3m ounces of silver! But it also smelted large amounts of zinc, lead, copper, and gold that same year.

I ran the numbers for the heck of it, and silver was implied as 32% of Korea Zinc’s 2015 revenues. The fact SIL’s managers included a company like this that doesn’t even mine silver as a top SIL component shows how rare major silver miners have become. The economics of silver mining at today’s prices are inferior to gold mining. Thus the average silver-purity percentage of revenues of these SIL miners is only 40.1%.

That’s right in line with the trend over this past year, with Q3’16, Q4’16, Q1’17, and Q2’17 seeing SIL’s top-component silver purity averaging 42.8%, 40.6%, 38.5%, and 37.6%. Silver mining is as capital-intensive as gold mining, requiring similar large expenses for planning, permitting, and constructing mines and mills. It needs similar heavy excavators and haul trucks to dig and move the silver-bearing ore.

But silver generates much lower cash flows due to its lower price. Consider hypothetical mid-sized silver and gold miners, which might produce 10m and 300k ounces annually. At last quarter’s average metals prices, these silver and gold mines would yield $168m and $384m of yearly sales. It’s far easier to pay the bills mining gold than silver, which is unfortunate. But until silver surges again, that’s the way things are.

While I understand this, as a long-time silver-stock investor it saddens me primary silver miners have apparently become a dying breed. When silver starts powering higher in one of its gigantic uplegs and way outperforms gold again, this industry’s silver-purity percentage will rise. But unless silver not only shoots far ahead but stays there while gold lags, it’s hard to see major-silver-mining purity significantly reversing.

Unfortunately SIL’s mid-November composition was such that there wasn’t a lot of Q3 cost data reported by its top component miners. 4 of its top 5 companies trade in the UK, South Korea, and Mexico, where reporting only comes in half-year increments. Lower down the list there are more half-year reporters, an explorer with no production, and primary gold miners that don’t report silver costs. So silver cost data was scarce.

Nevertheless, it’s always useful to look at the data we have. Industrywide silver-mining costs are one of the most-critical fundamental data points for silver-stock investors. As long as the miners can produce silver for well under prevailing silver prices, they remain fundamentally sound. Cost knowledge helps traders weather this sector’s fear-driven plunges without succumbing to selling low like the rest of the herd.

There are two major ways to measure silver-mining costs, classic cash costs per ounce and the superior all-in sustaining costs. Both are useful metrics. Cash costs are the acid test of silver-miner survivability in lower-silver-price environments, revealing the worst-case silver levels necessary to keep the mines running. All-in sustaining costs show where silver needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of silver, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q3’17, these top 17 SIL-component silver miners that reported cash costs averaged $4.86 per ounce. That plunged a whopping 13.6% YoY, making it look like silver miners are far more efficient.

But that too is misleading. This past quarter SIL’s 17th-largest component was Silvercorp Metals, which enjoys big lead and zinc byproducts at its China silver mines. These base metals are sold and used to offset the costs of silver mining. That forced SVM’s cash costs down to negative $5.16 per ounce, which dragged down SIL’s overall average. A year ago in Q3’16, SVM ranked 18th in SIL and missed the top-17 cutoff.

Still even ex-SVM, these top SIL silver miners reporting cash costs last quarter averaged just $6.54 per ounce. As long as silver prices stay above those extreme levels, the silver miners can keep the lights on. And there’s no way silver is going to plummet down under $7 in any conceivable scenario. So even at 2017’s vexingly-low gold-lagging silver prices, the major silver miners face no existential threats today.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain a silver mine as an ongoing concern. AISC include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current silver-production levels.

These additional expenses include exploration for new silver to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee silver mines. All-in sustaining costs are the most-important silver-mining cost metric by far for investors, revealing silver miners’ true operating profitability.

In Q3’17, these top 17 SIL components reporting AISC averaged just $9.73 per ounce. That was down 3.9% YoY, and far below last quarter’s average silver price of $16.84. Again SVM’s incredible byproduct production dragged down the average though. Ex-Silvercorp, these top SIL silver miners’ AISC ran at an average of $10.98 in Q3. That’s still well below prevailing silver prices, generating nice operating profits.

All-in sustaining costs and production are inversely related. Lower silver production, which many of SIL’s top components suffered last quarter, leaves fewer ounces to spread the big fixed costs of mining across. Thus AISC surged at Pan American Silver, First Majestic Silver, and SSR Mining. PAAS discontinued mining at an older mine, while other mines processed lower-grade ore that was on the way to better rock later.

AG’s lower production was due to land-access issues and mine inspections necessary following Mexico’s big earthquakes in mid-September. And of course SSRM is winding down its lone primary silver mine. Yet even with lower production driving higher per-ounce costs, the major silver miners still enjoyed solid operating profits. That’s certainly not apparent based on silver miners’ super-low stock prices mired in bearishness.

At $9.73 AISC, the major silver miners still earned big profits in the third quarter. Once again silver averaged $16.84, implying fat profit margins of $7.11 per ounce or 42%! Most industries would kill for such margins, yet silver-stock investors are always worried silver prices are too low for miners to thrive. That’s why it’s so important to study fundamentals, because technical price action fuels misleading sentiment!

Today’s silver price remains really low relative to prevailing gold levels, which portends huge upside as it mean reverts higher. The long-term average Silver/Gold Ratio runs around 56, which means it takes 56 ounces of silver to equal the value of one ounce of gold. Silver is really underperforming gold so far in 2017, with the SGR averaging just 73.5 YTD as of mid-November. So silver is overdue to catch up with gold.

At a 56 SGR and $1300 gold, silver is easily heading near $23.25. That’s 38% above its Q3 average. Assuming the major silver miners’ all-in sustaining costs hold, that implies profits per ounce soaring 90% higher! Plug in a higher gold price or the usual mean-reversion overshoot after an SGR extreme, and the silver-mining profits upside is far greater. Silver miners’ inherent profits leverage to rising silver is incredible.

While all-in sustaining costs are the single-most-important fundamental measure that investors need to keep an eye on, other metrics offer peripheral reads on the major silver miners’ fundamental health. The more important ones include cash flows generated from operations, actual accounting profits, revenues, and cash on hand. They generally corroborated AISC in Q3’17, proving silver miners are weathering low prices.

The collective operating cash flows of these top 17 SIL silver miners slumped 14.4% YoY to $1350m. That’s really impressive considering the 13.9% YoY drop in average silver prices, so these miners are holding their own despite silver really lagging gold this year. GAAP accounting profits looked far worse though, plunging 77% to just $88m. Many of these top SIL silver miners suffered net losses in Q3’17.

That was generally just the result of lower silver prices. There were two outliers, Tahoe Resources and Coeur Mining. With its silver mine temporarily shuttered by Guatemala, TAHO’s profits swung massively from +$63m in Q3’16 to -$8m in Q3’17. That $71m drop alone was responsible for 24% of the YoY drop in these top SIL silver miners’ GAAP profits. CDE simply had higher costs as it worked on expanding mines.

So its profits plunged from +$68m in Q3’16 to -$17m in Q3’17, for an $85m total drop. That accounted for another 29% of the total slide in collective top SIL miners’ profits. Other than that, the YoY declines were reasonable based on the lower silver prices. Interestingly these top 17 SIL miners’ collective sales surged 15.2% YoY to $3003m, driven by their aggregate silver and gold production rising 3.7% and 2.4% YoY.

And despite the weak silver prices, serious operational challenges, and ongoing expansions especially on the gold side of their businesses, these elite SIL miners’ total cash balances only edged 0.1% lower YOY to $2682m. So overall the silver miners’ operating results were pretty good in Q3’17 considering all the big trials they faced. Based on the individual miners’ travails, I was steeling myself for much worse.

Silver miners’ earnings power and thus stock-price upside potential will only grow as silver mean reverts higher. In mining, costs are largely fixed during the mine-planning stages. That’s when engineers decide which ore bodies to mine, how to dig to them, and how to process that ore. Quarter after quarter, the same numbers of employees, haul trucks, excavators, and mills are generally used regardless of silver prices.

So as silver powers higher in coming quarters, silver-mining profits will really leverage its advance. And that will fundamentally support far-higher silver-stock prices. The investors who will make out like bandits on this are the early contrarians willing to buy in low, before everyone else realizes what is coming. By the time silver surges higher with gold so silver stocks regain favor again, the big gains will have already been won.

While investors and speculators alike can certainly play the silver miners’ ongoing mean-reversion bull with this leading SIL ETF, individual silver stocks with superior fundamentals will enjoy the best gains by far. Their upside will trounce the ETFs, which are burdened by companies that don’t generate enough of their sales from silver. A handpicked portfolio of purer elite silver miners will yield much-greater wealth creation.

At Zeal we’ve literally spent tens of thousands of hours researching individual silver stocks and markets, so we can better decide what to trade and when. As of the end of Q3, this has resulted in 967 stock trades recommended in real-time to our newsletter subscribers since 2001. Fighting the crowd to buy low and sell high is very profitable, as all these trades averaged stellar annualized realized gains of +19.9%!

The key to this success is staying informed and being contrarian. That means buying low when others are scared, like late in this year’s vexing consolidation. An easy way to keep abreast is through our acclaimed weekly and monthly newsletters. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Easy to read and affordable, they’ll help you learn to think, trade, and thrive like contrarians. Subscribe today and get 20% off in our Black Friday Sale!

The bottom line is the major silver miners fared fine in Q3 despite some real challenges. A combination of silver continuing to seriously lag gold, along with anomalous company-specific problems, weighed on miners’ collective results. Yet they continued to produce silver at all-in sustaining costs way below Q3’s low prevailing silver prices. And their accelerating gold-production growth leaves them financially stronger.

With silver-stock sentiment remaining excessively bearish, this sector is primed to soar as silver itself resumes mean reverting higher to catch up with gold’s current upleg. The silver miners’ profits leverage to rising silver prices remains outstanding. After fleeing silver stocks so aggressively this year, investors and speculators alike will have to do big buying to reestablish silver-mining positions. That will fuel major upside.

Adam Hamilton, CPA

November 24, 2017

Copyright 2000 – 2017 Zeal LLC (www.ZealLLC.com)

- Gold surged higher on Friday. Then it gave all the gains back yesterday. Looking beyond this short term noise, gold is not an exciting market right now. What could make that change?

- Please click here now. Double-click to enlarge. Gold is trading in a rough sideways trend with an upside bias. This bias continues to strengthen, albeit very slowly. The technical action reflects the fundamentals and liquidity flows and clearly, patience.

- On that note, please click here now. I jokingly refer to the SPDR fund as “Spider Man”. Chindian demand is decent, but Spider Man looks like he’s caught in his own web; while there’s no significant selling, buying has come to a standstill.

- If Chindian demand is solid, gold doesn’t really need a lot of Western fear trade buying to move higher, but it must have some. That’s just not happening right now.

- The winds of change may be in the air, with US wage inflation pressures intensifying, an approaching debt ceiling debate, and a new Fed chair who stands ready to significantly reduce bank regulation.

- Without a bull cycle in money velocity, gold stocks and silver stocks will have a very hard time outperforming bullion on a consistent basis.

- The good news: these winds of change (especially the small bank deregulation favoured by Fed chair Powell) mean there is a very high probability that US money velocity ends its two decade bear market in 2018.

- Like Reagan, Trump’s administration is decreasing regulation and taxes while increasing debt. The main difference is that Reagan operated at the start of a business up cycle and at the end of an inflationary era. So, the Reagan administration could deflect government debt growth concerns with positive economic growth accolades.

- In contrast, the Trump administration is operating in the tail end of the business up cycle and in the tail end of a deflationary era. The bottom line: US GDP can grow for another year or two and hit 4% to 6% on the upside, but liquidity is going to flow from Wall Street and government bonds into the fractional reserve banking system as that happens.

- That’s because of quantitative tightening and rate hikes. Elderly American savers have essentially been nuked by QE and interest rates that are at multi-generational lows. Goldman predicts nine rate hikes in 2018 – 2019. I predict six, and the Fed dot plot suggests there will be seven.

- Whatever the number turns out of be, with a tail wind of tax cuts and bank deregulation, significant liquidity flows are going to move into thousands of America’s small banks.

- From there, it won’t be wasted on government bonds, which is deflationary. It won’t be used for stock market buybacks to give scummy corporate fat cats giant bonuses instead of giving American workers a pay raise.

- That money is going to go to Main street small business loans, and money velocity stands to make a significant reversal as that happens.

- As the business cycle peaks, even more money is going to flow into these banks… and into gold. In an economic downturn, Trump may need to look at unconventional policy like a new US Treasury gold buy program and high tariffs to manage the huge US government debt.

- Please click here now. Double-click to enlarge this dollar-yen chart. Different price drivers drive the gold price at different times. Sometimes gold leads a market, and at other times it follows. Currently, gold is playing follow the dollar-yen leader.

- An important head and shoulders top is forming on the dollar against the yen. I told my intestinally fortified readers to prepare for some gold market pain early yesterday morning, and the “reign of pain” arrived just hours later, exactly on cue!

- Nothing is out of order here. The dollar is rallying to form a right shoulder high against the yen, and that’s putting annoying but modest pressure on gold. Without the institutional support for gold stocks that comes with rising money velocity (particularly M2), the stocks get hit a lot harder than bullion.

- Fund managers like Ray Dalio recommend keeping 5% to 10% of assets in gold. Ray owns a lot of gold stocks as well. In the gold community, gold is generally owned more aggressively, often representing 40% in an investor’s portfolio, and more!

- I have no issue with the higher percentages (and partake in them myself). To build retained wealth (and maintain emotional stability) in the sector though, gold bugs need to buy significant price weakness.

- Holding some assets besides bullion and the miners is also important. Just as gold is a stock/bond investor’s tool to maximize returns and reduce drawdowns, mainstream stocks and bonds serve a gold investor in the same way.

- On that note, please click here now. Double-click to enlarge. I coined the term “gold bull era” to describe the long term growth of gold demand related to growth in China, India, and other Asian and mid-East markets.

- Please click here now. Double-click to enlarge. I’ve highlighted a solid upside breakout from a massive triangle pattern on this South Korean stock market ETF chart. I urge all gold bugs to buy and hold some China, India, South Korea, and Japan stock market ETFs and individual stocks. The bottom line: The Asian stock market upside breakouts represent stage one of the gold bull era. Don’t miss out on the wealth building fun!

- Please click here now. Another great holding for gold bugs is bitcoin. A lot of investors ask me how bitcoin staged a “forty bagger” move while gold has gone nowhere. The answer is simply that the supply of bitcoin is only 21 million coins. My long term (not that long) target for bitcoin is $500,000. If the supply of gold was only 21 million ounces, gold would already easily be at $500,000, but the demand-supply balance for gold is much more even (for now) than it is for bitcoin. Bitcoin shouldn’t be viewed as a competitor to gold. I’ve labelled bitcoin a positive member of the precious metals asset class family, and predicted it will play a major role in the gold bull era.

- Please click here now. Double-click to enlarge this exciting Chow Tai Fook chart. Chow is the largest gold jewellery retailer in China. I cover the wealth building action for Chow in my www.gracelandjuniors.com newsletter. Chow’s price action is also a truly vital indicator of what lies ahead for the Western gold mining stocks. It looks set to usher in the new year with an upside blast higher from a broadening consolidating pattern which should send the miners higher too!

Cheers

St

Stewart Thomson

Graceland Updates

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

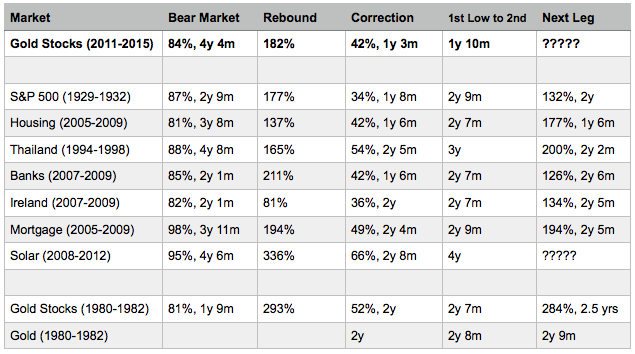

It has been a while since we’ve applied historical analysis to the precious metals sector. It is something we really enjoy as history can help define and contextualize current trends and help us spot opportunities. Back in March of this year we noted that the gold stocks could be following the path of recovery of housing stocks since their 2009 bottom. Recently, James Flanagan of Gann Global Financial has produced some excellent videos discussing some historical comparisons that are quite relevant to the gold stocks at present. We saw his videos, remembered our housing analog and wanted to take it a step further. What was the path of recovery of markets following mega bear markets?

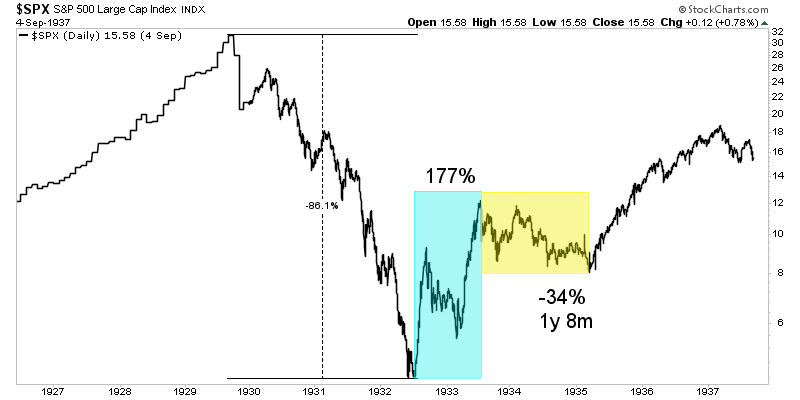

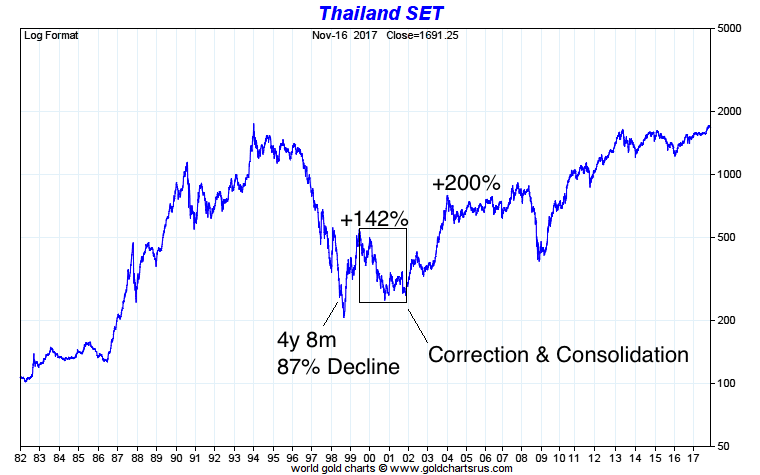

We define a mega bear market as at least an 80% decline that lasted roughly three to four years. The image below highlights the data we’ve compiled. Some of the bears are only two years long but they follow the general recovery path. That consists of a very strong initial rebound that lasts six to twelve months which is followed by a correction and consolidation which usually lasts 18 months to two years. Then, the market begins its next impulsive advance.

Next we will look at the three best fits to the gold stocks at present.

The housing stocks may be the best analog. They lost 81% during a bear market which lasted nearly four years. Then they recovered 137% before correcting 42% over 18 months. Over the next 18 months (from the 2011 low to 2013), the housing stocks gained 177%.

The S&P 500 during the Great Depression is also a good fit. The market lost 86% over nearly three years. That led to a 177% rebound which was followed by a 34% correction over one year and eight months. The market then rebounded 132% over the next two years.

Finally, Thailand is an interesting example. It lost 87% over a greater than four year bear market. Both time and price were similar to the bear market in gold stocks. After rebounding 142%, Thai stocks lost 54% over the next year and four months. While that low in late 2000 marked the corrective low in price, the market did not begin an impulsive advance for another year. However, it was worth the wait as the market gained 200% over the following two years.

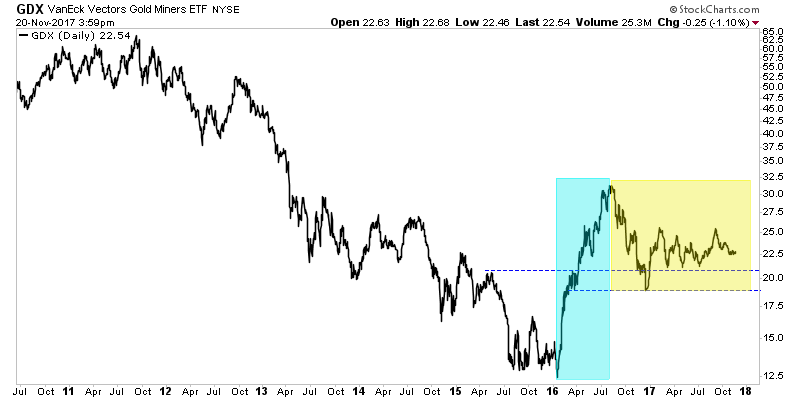

The gold stocks have followed the recovery path of these markets but there are some slight differences. The corrections and consolidations in Housing and the S&P 500 were less severe as those markets tested or at least came close to testing their initial rebound peaks. The correction in Thailand was more severe as that market shed 54% in 16 months. At present, gold stocks are in the 16th month of their correction and are down roughly 30%-35%. In any case, we expect the current correction and consolidation to continue into 2018.

There is no guarantee of a future breakout move in precious metals but the gold stocks are following a specific history of recoveries following mega bear markets and that history implies a major move higher should begin sometime in 2018. When we consider the time of the corrections and time between the two bottoms along with the slight weakness in gold stocks as compared to some of the examples, we expect the next significant low to be in Q2 or Q3 2018. The low does not necessarily have to be an absolute price low. It would mark the point from which the gold stocks would begin an impulsive advance. In the meantime, the key for traders and investors is to find the best companies and seek oversold situations with value and catalysts that will drive buying. To follow our guidance and learn our favorite juniors for 2018, consider learning more about our premium service.

Jordan Roy-Byrne CMT, MFTA

On November 1st, De Beers said that it will be closing its nearly depleted Victor diamond mine in northern Ontario in early 2019. Victor is the first in a line of legacy diamond mines world-wide that will be closing over the next 5-years.

Most notably, Rio Tinto’s illustrious Argyle mine in Australia is expected to shut operations in 2021. At peak production, in the mid-90’s, Argyle produced over 40M carats annually. To put that into perspective, total 2017 global diamond output is estimated at less than 150M carats.

De Beers Voorspoed mine in Botswana is on pace to reach end-of-life by the end of the decade, and a slew of the company’s alluvial mines in Namibia are planned to be phased out by 2022.

With global diamond demand forecast to grow at approximately 3.5% annually over the next five years, driven by middle class consumers in Mainland China and India, the industry’s fastest growing large markets, a supply gap down the line seems inevitable if forecasts hold.

Globally there only two new diamond projects in the works with annual production potential of in excess of 1M carats, one in Angola, the other in Russia. Further, new diamond project exploration has been limited by challenges in the upstream diamond industry’s primary jurisdictions.

Greenfields diamond exploration in South Africa is at multi-decade lows due to delays in granting of prospecting licenses and perceived risks of a new Mining Charter, and this year there was a production disruption at the Williamson diamond mine in Tanzania related to government changes in mining legislation.

In Botswana, home to De Beers’ primary asset base, the country has been heavily explored and most major diamond discoveries are assumed to already have been made. In Russia, most major diamond production in is controlled by government entities.

This makes Canada, already the third largest diamond producing nation in the world by value (see chart above), arguably the most prospective diamond exploration jurisdiction in the world. In May of this year, Canada’s leading diamond producer, Dominion Diamond (private), pledged to spend C$50M on exploration over next 5 years, the company’s first major greenfields exploration since 2007.

After being acquired for US$1.2B in July by private-held the Washington Companies (at a 44% premium to where the stock was trading the day before initial indication of interest was made), on November 1st Dominion reiterated plans of “reinvigorating” exploration programs in Canada.

Dominion is partnered with North Arrow Minerals (TSX-V: NAR) on the prospective “Lac de Gras” property, which is located within a diamondiferous kimberlite field in the Northwest Territories that is the source to some of the richest diamond deposits in the world, including Dominion’s two world-class mines, Ekati and Diavik.