After one of the worst bear markets in history, gold and the gold mining stocks began a new bull market cycle in 2016. With the first 8 months of the year filled with incredible gains, a correction in the market ensued. Of the two, the gold mining stocks were hit the hardest, sending a large portion of the company share prices down or sideways over the last 16 months.

Today, in the 1st quarter of 2018, physical gold continues to show strength, while the gold stocks continue to waiver. Personally, I think the prospects of a change in sentiment toward the gold stocks will happen in 2018, and mark the next leg up in this bull market cycle.

Why do I think this is the case? There are a few reasons:

- Lack of interest – In my opinion, the weed and blockchain sectors have captured the attention of the large majority of the speculative investors over the last year. Additionally, I have read numerous articles and headlines which allude to gold losing its luster, which I completely disagree with. I believe this is a sign of a great buying opportunity in the junior gold equities.

- 1,033 point correction on the DOW – The broader market has been on a tear for roughly 8 years, and up until this 1,033 point correction on the DOW a couple weeks ago, it didn’t appear to be slowing down. It’s my contention that we are seeing an inflection point downwards in the broader markets bull cycle. My guess is that past will be prologue, gold and gold equities will be the major beneficiaries.

- Inflation – Although, I do think a correction in the broader market becomes more likely with each passing week, I see tremendous inflation in the future. In my opinion, we are entering a major bull cycle in the base metals, which will inflate the cost of living. Real assets will be sought out to curb the destructive and silent force which is inflation. The caveat to this belief is the adoption of artificial intelligence, which will have a huge deflationary impact on the world. However, I think that is still 10 years away from having a profound impact.

- Scarcity and Cost to produce an ounce of gold – As Brent Cook has often pointed out, we are losing approximately the equivalent of the Carlin Trend each year, in terms of gold ounces, and the majority of what we do discover isn’t economic below $1250 USD/oz Au. When the cost of production is more than the price of the commodity, therefore, the price has to eventually go up. I must qualify this statement by saying that, according to regular accounting, gold isn’t scarce, given the fact that more than 95% of all gold that has ever been mined still exists today, albeit in vaults. I don’t, however, foresee gold becoming any less popular as a store of value and, therefore, believe that the scarcity reference is applicable.

Mining is a sector in which the most valuable commodity, for a junior company, is the people. The right people make the right choices no matter what portion of the market cycle they are in. Therefore, picking the right people, in my opinion, gives you a higher probability of being successful with your investments. Bottom line, if you like the metal and its prospects for price appreciation in the future, buy the metal. If you’re willing to do the due diligence, and can handle/manage the risk, there is huge potential in the junior mining stocks.

Which brings me to the company I would like to update you on today, Genesis Metals Corp.

Let’s take a look!

Genesis Metals Corporation (GIS:TSXV) & (GGISF: OTC)

NOTE: DTC eligible

MCAP – $9.4 million (at the time of writing)

Shares – 74,801,204

Fully Diluted – 104,845,092

Management Ownership – 12%

The Genesis Metals Team

A junior resource company is only as good as its people, and in the case of Genesis Metals, they’ve assembled a great team.

Genesis Metals’ CEO and Chairman, Brian Groves, is a 40-year veteran of the mining industry. Groves has explored in both Australia and Canada, working with AMAX Minerals, Noranda and Manager of Corporate Development at Placer Dome. Moving up the organizational ladder throughout his career, Groves has gained valuable experience in capital markets, project development, permitting and corporate strategy. Today, he leads a group of people who have not only worked together previously, but who have a history of success within the mining industry.

Working hand in hand with Groves is Jeff Sundar, President and Director of Genesis. Sundar has 18 years of experience in the mining industry, having held a VP and Director’s position while working with other Genesis Board members in Underworld Resources. Underworld, in particular, was a great success, as the 1.6 Moz White Gold deposit was sold to Kinross for $140 million. Sundar and the team look to replicate this success with Genesis in the years ahead.

Adrian Fleming, the former President and CEO of Underworld Resources and former VP Exploration of Placer Dome, joins the Genesis team as an Executive Director. Fleming is a Professional Geologist with over 30 years of experience in the mining industry. Some of Fleming’s most notable work experience includes the following:

- Former VP Exploration for Placer Dome based in Sydney Australia. Fleming spearheaded Placer Dome into Western Australia, where he directed the group and found the Big Bell Mine.

- Fleming co-led the team that found the high grade zone at the monster, 28 Moz gold equivalent, Porgera copper gold deposit, located in Papua New Guinea.

- Former VP Exploration for Golden Star in the early 90’s. Fleming directed the team that uncovered the Gross Rosebel Deposit, which has now grown to 17 Moz of gold.

- Fleming will be counted on to provide valuable input as Genesis moves forward with a plan to expand its Chevrier Gold Deposit resource, and explore the gold anomalies at their October gold project.

John Florek, the former Senior Geologist at Barrick Gold’s Famous Hemlo Mines, is on Genesis’ Board of Directors. Hemlo was a world-class gold deposit and is credited as being the catalyst for the 1980’s exploration boom. Florek co-led the exploration team that found an additional 2 Moz of gold, which extended the Hemlo mine life. He was also Senior District Exploration Geologist for Placer Dome in Red Lake, and in 2008, his team was awarded the Northwestern Ontario Prospectors award. Florek’s more than 20 years of experience in the mining business as a professional geologist should add great value for Genesis in the future.

Last, but certainly not least, Andre Liboiron is the Exploration Manager for Genesis’ projects, Chevrier and October. Liboiron is a Quebec native with more than 26 years of experience as a geologist in Quebec, as well as internationally.

Strategic Advisor

Robert McLeod, Genesis Co-Founder and former Chairman of Genesis’ Board, relinquished his position because of the heavy time commitment required by his primary focus as CEO of IDM Mining, a near term producer in BC’s Golden Triangle. Given the work history of the members of this management team, however, McLeod has agreed to remain with the company as a strategic advisor.

McLeod is on Casey Research’s Nexten list, which features the top young professionals in the mining industry. A quote taken from Casey Research’s profile of McLeod,

“Luck has nothing to do with it. Rob has the pedigree, the smarts, and the perseverance to have forged a stellar career in mining exploration and company development.” ~ Casey Research

Also, Genesis has added former Laurentian Bank Securities Mining Analyst and Peartree Securities Technical Advisor, Eric Lemieux. Lemieux is a geologist by trade and has 25 years in the mining industry with experience in a variety of areas, such as mineral exploration and project valuation. Lemieux’s addition to the Genesis team should prove advantageous as Genesis looks to develop their properties.

Strategic Shareholders

While the people who run junior resource companies are the core component for investment, looking at the people who choose to invest in the companies is a great gauge for potential value. In Genesis’ case, there are a few heavy hitters who have taken major positions in this junior gold exploration company.

The list of strategic shareholders is headlined by Osisko Mining, which acquired a 6.4% position in Genesis through a private placement announced in 2017. For those unfamiliar with Osisko Mining, they’re a major player in the gold sector, owning strategic positions in a lot of great companies, such as: Falco Resources, IDM Mining and Beaufield Resources. Outside of owning strategic positions in companies, Osisko is exploring their 70,000 Ha Windfall property, which is located in the Urban-Barry Greenstone Belt in Quebec. Osisko is known for their geological expertise and well timed investment in smaller junior gold companies. Their investment in Genesis speaks volumes about Genesis’ potential.

The strategic shareholders list is further headlined by Eric Sprott, who has acquired a 7.2% position in Genesis through a private placement announced in 2017. Sprott is a major player in the resource sector, with a history of successful investments throughout his career. Also, Sprott has multiple Sprott named companies offering various market related products across the sector. Over the last few years, he has taken strategic positions in a few junior gold companies such as Kirkland Lake Gold. Sprott’s investment, like Osisko’s, is a great gauge for potential value in Genesis.

For those who aren’t familiar, the Societé de development de la Baie-James (SDBJ) is a government run organization focused on the development of natural resource projects within Québec. Their mission statement is as follows;

“To promote the economic development, development and exploitation of natural resources, other than hydroelectric resources within the mandate of Hydro-Québec, of the James Bay territory, from a sustainable development perspective. In particular, it may encourage, support and participate in projects aimed at these ends.” ~SDBJ

Additionally, the SIDEX fund, which was created by the government of Québec to support mineral exploration activities within its borders, participated in the latest financing. Having both SDBJ and SIDEX as stakeholders in Genesis is a great sign of political support for Genesis’ Chevrier Gold Project. The strategic shareholders list is rounded out by Delbrook Capital, Gold 2000, US Global Investors and Medalist Capital. These organizations and people represent smart money in the sector and I’m happy to speculate along with them.

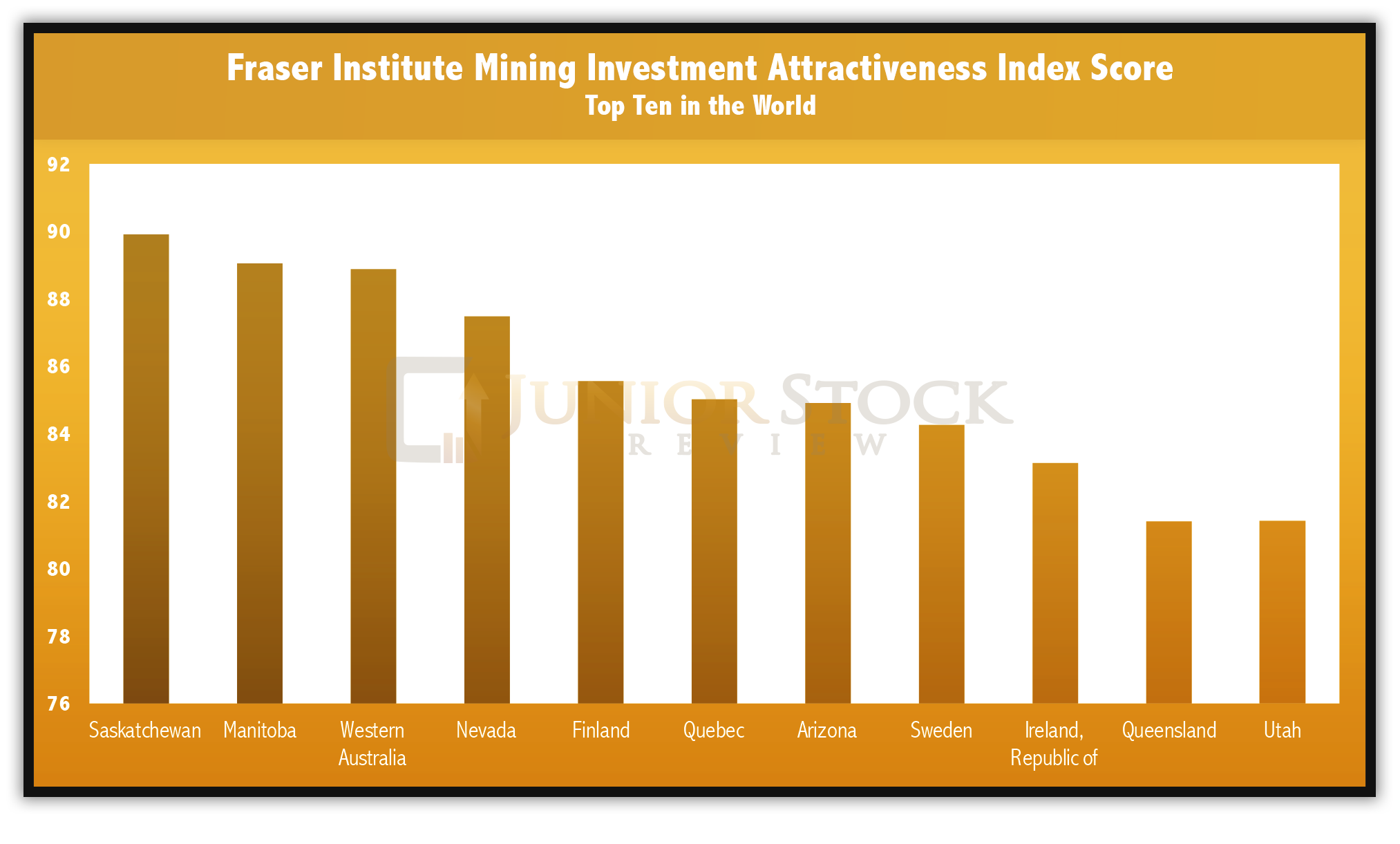

6th Best Jurisdiction for Mining Investment in the World

From a jurisdictional standpoint, it doesn’t get much better than Quebec when it comes to mining investment attractiveness. The Fraser Institute (FI) gives Quebec an index score of 85.02, ranking it 3rd in Canada and 6th in the world. FI’s mining investment attractiveness index score is reflective of both the mineral potential and the government policy perception of the region.

Source: Fraser Institute

Quebec’s Mineral Potential

Quebec is home to 25 producing mines and over 350 surface mineral mining operations, putting the value of Quebec’s mineral shipments at $8.7 billion in 2014 (Investissement Quebec). Quebec is Canada’s 2nd largest producer of gold, largest producer of iron and zinc, and the only North American producer of niobium. The mineral wealth is evident and is a big reason why FI ranks Quebec among the world’s top ten in mining investment attractiveness.

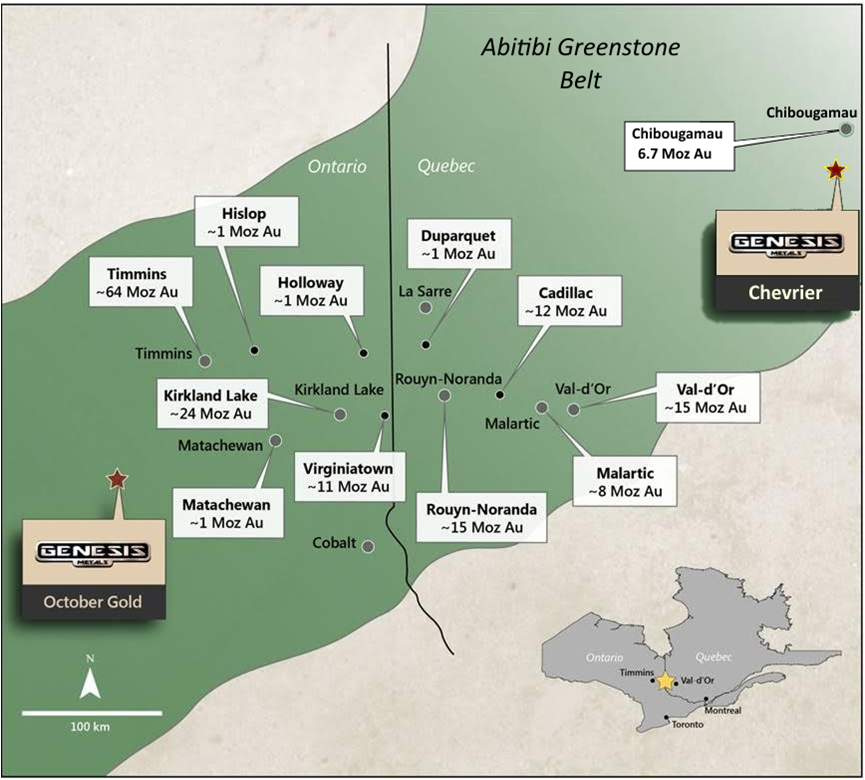

Highlighting Quebec’s world class mineralization is the Abitibi Greenstone Belt (AGB), which is 150 km wide and stretches 650 km from roughly Wawa, Ontario to Val d’Or, Quebec. The belt has produced millions of ounces of gold over its history, with the Cadillac Gold Camp, Virginiatown, Rouyn-Noranda Gold Camp, and Val d’Or Gold Camp being just a few of its largest contributors.

Source: Genesis Metals

Quebec Politics and Infrastructure

The government of Quebec supports mineral exploration within its borders with a tax credit system that refunds 25% of eligible exploration expenses for non-operating corporations, and 10% of eligible exploration expenses for operating corporations (Financial Incentives). So, roughly, for every $1 spent by a Quebec based mineral explorer, 25 cents will come back to the company, which can effectively be rolled right back into further exploration work. This is not only a huge plus for the company and its shareholders, but an ingenious way for the province to promote mineral exploration.

The long history of mining in the AGB means that most regions of the belt are accessible or near infrastructure such as highways, rail, power, and deep water ports along the St. Lawrence Seaway. Also, Quebec boasts some of the most competitive electricity rates in Canada, as its hydroelectric dams constitute a major portion of its electricity production.

Source: Genesis Metals

Source: Genesis Metals

Finally, Quebec takes great pride in a transparent mining system, which is built around three key pillars:

“Open access to resources is ensured on the largest possible portion of territory, Mineral rights are granted on a first-come, first-served basis and if a discovery is made, the title holder can be reasonably sure of obtaining the right to develop the resource.” ~ Investissement Quebec

Favourable politics and world class geology – for me, it doesn’t get much better than Quebec, as far as your investment buck goes!

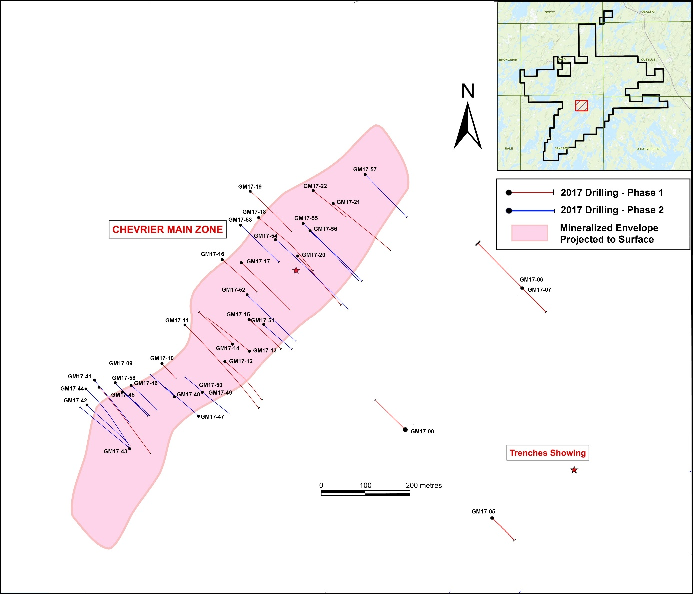

Gensis Metals Corp. – Chevrier Gold Project Phase 1 and 2 Drill Update

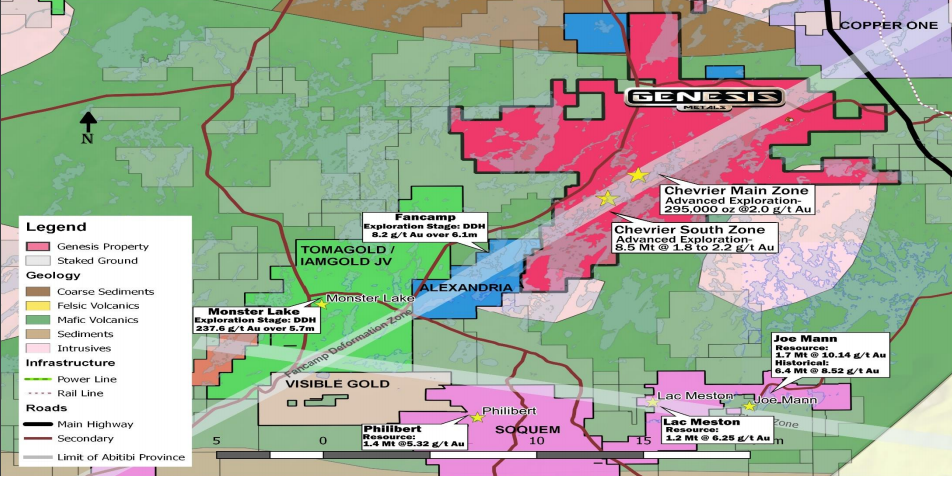

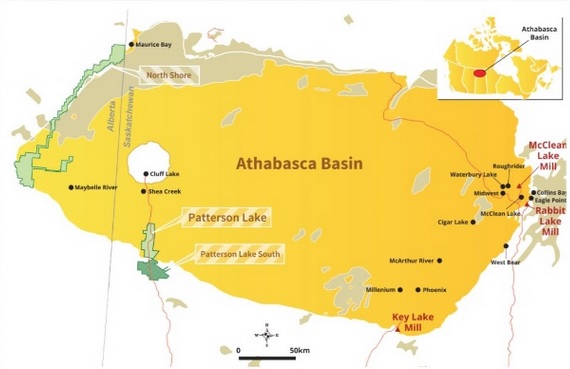

Genesis’ 100% owned Chevrier Gold Project encompasses 120 square km and is located 35 km south of Chibougamau, Quebec, in the heart of the Abitibi Greenstone Belt. Chevrier straddles 15 km of the Fancamp deformation zone, and is 15 km northeast of IAMGOLD’s high-grade Monster Lake gold discovery.

Chevrier has an existing NI 43-101 inferred resource for its Main Zone, which is 300,000 oz of gold at 1.99 g/t (1 g/t cut-off), and is open for further expansion at depth and to the north.

Phase 1 Drilling

Roughly 5,000 metres of drilling was completed in Phase 1 at Chevrier. The focus of the drilling was four fold; confirm historical Geonova drill holes by twinning, complete infill and step out drilling on the existing Main Zone Deposit, and finally, explore other IP and geological targets.

The results of the twinned and infill holes did not disappoint, as they confirm continuity of the shallow gold mineralization within Chevrier’s Main Zone. A full list of drill results can be found on SEDAR, a few of the highlights from the results are:

- Twinned hole GM17-09 returned 2.94 g/t gold (Au) over a width of 58.70 m (starting at 74.60 m down hole), which included an interval of 14.01 g/t over a width of 6.35 m.

- Hole GM17-20 returned 2.00 g/t Au over 35.20 m within a zone that graded 0.93 g/t Au over 94.90m starting at 91.5 m down hole.

- Hole GM17-21 returned 1.13 g/t Au over 38.05 m.

- Hole GM17-22 returned 1.06 g/t Au over 24.45 m.

- Hole GM17-16 returned 1.06 g/t Au over 14.22 m including: 3.50 g/t Au over 3.22 m.

Using the image below to reference the highlighted holes:

Chevrier Gold Project – 2017 Drilling

Trenching

The IP survey of the property identified a geophysical anomaly roughly 5 km northeast of the Chevrier Main Zone. During the Phase 1 drill program, Genesis completed exploration of this anomaly via trenching. In a news release on October 3rd, 2017, Genesis reported that they had identified a new area of gold mineralization in Trench 29, returning a channel sample of 2.55 g/t Au over 2.3 m. This area will be explored further in the future.

Phase 2 Drilling

On January 22, 2018 Genesis announced the results of its 5,000 metre Phase 2 drill program on the Chevrier Gold Project. The Main Zone was the focus of Phase 2, completing 18 holes of infill and step-out drilling. The results, in my opinion, look good. Check out highlights from the drill program:

- 8.73 g/t Au over 21.35 m including 37.97 g/t Au over 3.00 m in hole GM-17-42

- 3.59 g/t Au over 22.60 m in a separate zone in hole GM-17-42

- 4.26 g/t Au over 19.40 m including 8.99 g/t Au over 7.80 m in hole GM-17-48

- 4.47 g/t Au over 12.45 m within an interval of 1.08 g/t Au over 84.85 m in hole GM-17-46

- 5.06 g/t Au over 8.45 m and 1.23 g/t Au over 43.00 m in two intervals in hole GM-17-41

- 4.53 g/t Au over 13.80 m in hole GM-17-44

- 1.04 g/t Au over 50.05 m including 1.94 g/t Au over 17.10 m in hole GM-17-44

Putting the results into perspective, remember that the Main Zone’s existing inferred resource has an average grade of 1.99 g/t. The impact of these shallow, higher grade results should be realized in Genesis’ resource update for the project coming later this year.

Additionally, and of particular importance, was the step-out results which came from holes GM-17-45 and GM-17-46. These holes were drilled with the intent of testing for an extension of the mineralization from hole GM-17-09, which was drilled in Phase 1 (refer to the image above for the location).

The results from these two holes reveal a new north-east trending shallow extension of the mineralization discovered in GM-17-09. Specifically, from the drill results table in the news release , GM-17-45 returned a shallow interval (35.4 m down hole) of 63 metres at 0.5 g/t gold, while GM-17-46 returned a shallow interval (19.35 m down hole) of 84.85 metres of 1.08 g/t gold.

PUSH: Announcement of follow up drill program on the Main Zone, focusing on the high grade holes which were discovered in 2017.

PUSH: Chevrier Gold Project resource estimate update in 2018.

Chevrier South Zone

While Chevrier’s Main Zone, with its existing Inferred Resource, has garnered the bulk of drilling over the history of the Project, I believe there’s the possibility of some great results from Chevrier’s South Zone. Why? Although the South Zone doesn’t have an existing 43-101 resource, Met-Chem’s comments within the technical report state,

“the Chevrier South deposit contains a potential between 8.5 and 9.0 million tons of mineralized material grading 1.8 to 2.2 g/t Au.” ~ Met-Chem – 43-101 Technical Report on the Mineral Resource of the Chevrier Gold Project – pg.93

If you express the 8.5 million tons of mineralized material at 1.8 g/ton, you get 459,000 ounces of gold. Met-Chem’s reference to the possible resource size of the South Zone deposit is based off a small historical drill data set and its similarities in alteration and deformation like the Main Zone. The fact is, the South Zone needs further drilling before a 43-101 complaint resource can be officially estimated.

As Genesis intends to update the Chevrier Gold Project resource estimate in 2018, I believe there’s a good chance that we could see them refocus their attention on the Project’s South Zone. Given Met-Chem’s comments, I believe there’s good reason to believe drilling within the South Zone could have a tremendous impact on the updated resource estimate for the entire Project.

In my opinion, the updated resource on the Chevrier Gold Project, which will include both the Main and South Zones, will exceed 1 million ounces and should set Genesis up for a market re-rating, as its current sub $10 million MCAP doesn’t reflect the potential of what it possess.

PUSH: Watch for the announcement of a drill program on Chevrier‘s South Zone. The results from a South Zone drill program could have a major impact on Chevrier’s updated overall resource estimate.

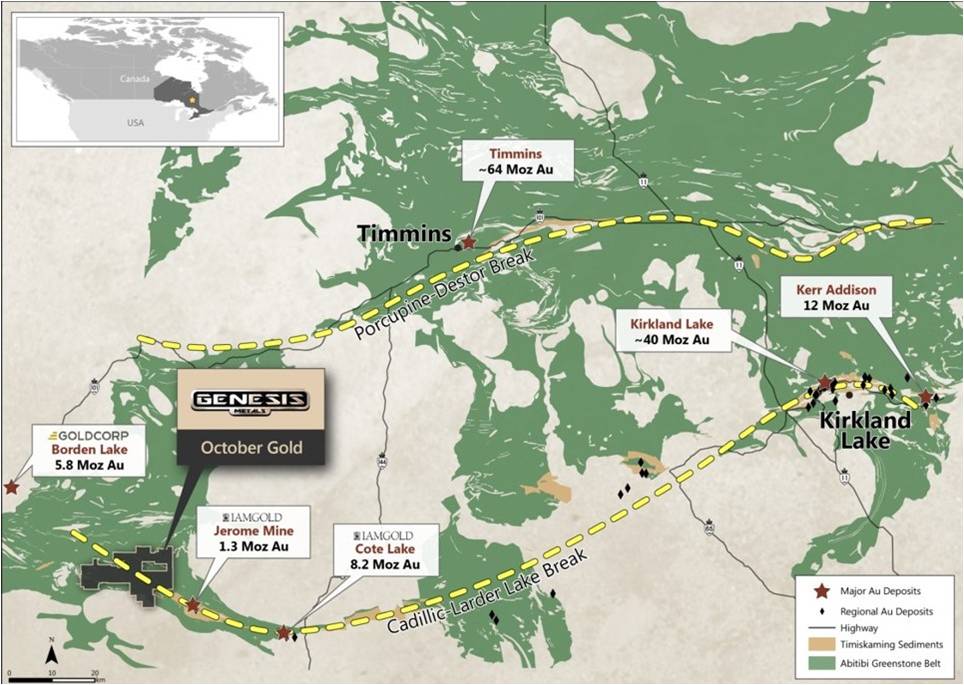

October Gold Project

Genesis also owns 100% of the 203 square km October Gold Project, located in the southern Swayze greenstone belt in Benton Township, Ontario. This project is located 35 km northwest of IAMGOLD’s Cote Lake deposit, and 50 km southeast of Goldcorp’s Borden Gold Deposit. The Cote Lake Deposit was purchased by IAMGOLD from Trelawney Mining for $585 million, while the Borden Gold Deposit was purchased by Goldcorp from Probe Mines for $526 million. This demonstrates how coveted this Ridout Deformation Zone is, and Genesis’ October Gold Project is right in the middle, and on trend.

IAMGOLD announced in a press release on June 5, 2017 that Sumitomo Metal Mining has acquired a 30% undivided participating joint venture interest in IAMGOLD’s ownership interest in the Cote Gold Project for an aggregate $195 million. Sumitomo’s interest in this area of Northern Ontario should bring more attention to the surrounding land claim owners, one of which is Genesis’ October Gold Project.

The October Gold Project straddles what is considered the western extension of the Larder Lake-Cadillac Deformation and a portion of the Ridout Deformation zone. Historic gold deposits on these deformations, Kirkland Lake and Kerr Addison-Chesterville, have historic gold production north of 49 Moz.

The October Gold property saw surface exploration work in 2011. The program comprised of Soil Gas Hydrocarbon (SGH) sampling and reconnaissance level gravity geophysical surveys.

“A SGH survey is a deep penetrating geochemical method that involves the analysis of various hydrocarbons associated with ore bodies at depth using a forensic and comparative approach for Identification. “ ~ Genesis

The program has identified two gold anomalies, which Actlabs, the interpreting laboratory, says have a high degree of confidence. This confidence is based on comparisons with other surveys that Actlabs has completed on other gold deposits. These anomalies will see future surface work which should better define where the diamond drilling should take place.

The October Gold project property is early stage, but holds very promising gold exploration potential.

Concluding Remarks

The Genesis Metals story is not without risk, as any gold exploration company runs the risk of not finding anything or not finding mineralization which is economic. In Genesis’ case, I believe further modelling of the gold grade distribution within the Main Zone, should feed nicely into Chevrier’s updated resource estimate later this year. While on the exploration side, drilling on Chevrier’s South Zone appears to be very promising.

Outside of the risk of exploration, Genesis has some compelling facts that make their story undervalued in comparison to the paltry sub $10 million MCAP that they currently possess, including:

- A proven management team: Groves, Sundar, Fleming, Florek, Liboiron and Mcleod

- Strategic Shareholders List Headlined by: Osisko Mining, Eric Sprott, Delbrook Capital, Gold 2000, US Global Investors, SIDEX/SDBJ and Medalist Capital

- Located in the 6th best jurisdiction in the world, Quebec

- PUSH: Announcement of a follow up drill program, focused on Chevrier’s Main Zone high grade drill holes, which were discovered in 2017.

- PUSH: Announcement of a drill program focused on Chevrier’s South Zone in 2018.

- PUSH: 2018 Chevrier Gold Project Resource Estimate Update – In my opinion this estimate could exceed 1 million ounces of gold.

- Great bang for their drilling buck, as their all-in drill costs thus far have roughly averaged $220 per metre

- Large land package with exploration potential, Chevrier Gold Project and October Gold Project

The next leg of the gold bull market is upon us, fortunes will be made in the coming years by buying right and sitting tight, investing in companies that look to add value for their shareholders. Genesis Metals (GIS:TSXV) is a great example of this and is a company in which I’m investing.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I do own Genesis Metals Corporation stock. All Genesis Metals Corporation analytics were taken from their website and press release. Genesis Metals Corporation is a Sponsor of Junior Stock Review.

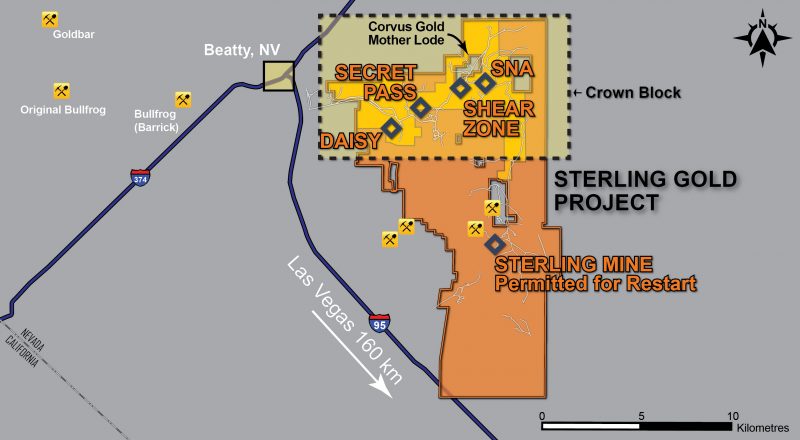

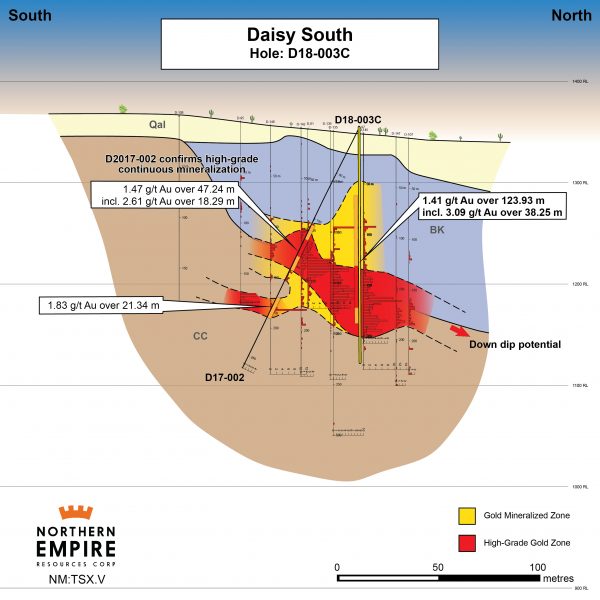

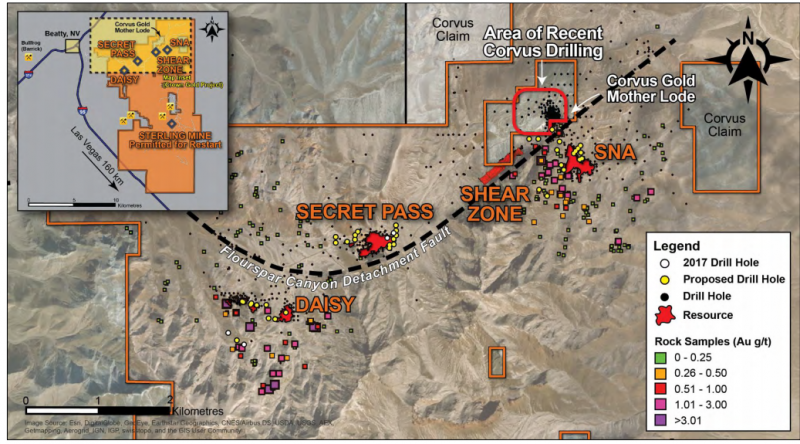

Northern Empire Resources Corp. (TSX-V: NM) released results from its Daisy Deposit as part of its 2018 15,000-metre drill program to expand resources at the Sterling Gold Project in Nevada. These results will go towards an updated resource due in the first half of 2019 and indicate the potential for an open pit, heap leach operation. The Daisy Deposit is located within the Crown Block of deposits in the north of the Company’s property.

Drill hole D18-003C was a vertical core hole that returned an intercept of 123.93 meters of 1.41 grams per tonne (g/t) gold (Au). The intercept included 38.25 meters of 3.09 g/t Au and oxides in the hole extended to a depth of 173 meters.

This is the third drill hole Northern Empire has reported from the Daisy Deposit. Results from last year included 47.24 meters of 1.47 g/t Au in hole D17-001 and 21.34 meters of 1.83 g/t Au in hole D17-002. All historical drilling at Daisy occurred before the introduction of NI 43-101 reporting standards, so confirmation drilling is required to expand the resource. Historical drilling was also all reverse circulation (RC), so core holes are vital for developing a comprehensive geological model.

In comparison to historical holes near D18-003C, yesterday’s result encountered mineralization closer to surface than expected. In concert with nearby mapping and sampling which returned surface grades of up to 15g/t, these results are demonstrative of the potential this system could be larger than previously thought.

Michael G. Allen, President and CEO, commented:

“D18-003C is the first of at least 10 exploratory, resource expansion, and infill holes that we plan to drill into the Daisy Deposit as part of our 15,000-meter program. The exceptional grade of these results is very encouraging. All of the mineralization from 67.88 to 173.22 meters down the hole was oxidized, as was the final 2.87 meters of mineralization. For the high-grade core of the deposit, where we cut 38.25 meters of 3.09 g/t gold, cyanide solubility assays averaged 90% of fire assay, indicating that the Daisy deposit may be amenable to open pit mining with heap leach recovery of gold.”

The broad intervals of relatively shallow, high-grade oxide mineralization present here are key if Daisy is to ever benefit from a low cost and efficient open pit, heap leach operation. The advantage of heap leach mining is that they generally have low all-in sustaining costs and provide rapid payback to the operator. The average grade of heap leach operations in Nevada is approximately 0.7g/t gold, which would make the inferred resource at Daisy of 174,000oz of gold at 2.12g/t triple that.

The Daisy Deposit is located in the Bare Mountain district known for its legacy of past production. The trend is along an east-west structure that hosts Barrick’s Bullfrog Mine on the westernmost extension and stretches to the east where Northern Empire’s SNA deposit and Corvus Gold’s (TSX: KOR) Mother Lode deposit. Mother Lode is located completely within Northern Empire’s claim package. Along this trend, more than four million ounces of gold have been extracted or identified in situ.

With several high-grade historical holes and showings, Northern Empire’s overall land package remains underexplored and numerous regional targets demand follow-up. For 2018, Northern Empire management put together a large exploration program with the intention to expand the resource through drilling. The company’s exploration is starting to demonstrate the potential at the Daisy Deposit.

The market has been responding positively to drill results. Since initial results released from the Daisy deposit on October, 04, 2017, shares in the company have moved from 77 cents per share to a year-high of $1.43, and at close of Feb. 23, 2018, $1.30. Upon release of the most recent results from Daisy, the stock rose 12 cents to $1.39 on 231,088 shares.

The company is also responding positively to these results with immediate plans to mobilize an additional drill rig to Daisy. Currently rigs are working on the SNA and Secret Pass deposits which are part of the Crown Block of deposits which includes the Daisy Deposit. In addition, field crews are mapping extensions of the known deposits and new drill targets.

This is just the beginning for Northern Empire in Nevada. Nevada is one of the largest gold producers in the world, renowned for open pit deposits which are amenable to heap leach mining. The early results from Daisy are indicating that the company is on the right track to adding high grade ounces to support the case for another open pit, heap leach mine in Nevada.

- For the past fifteen months or so, gold has repeatedly been turned back by immense technical resistance in the $1370 area.

- Please click here now. Double-click to enlarge this daily gold chart.

- There have been three clear attempts to push through the $1370 area since November of 2016. The first two failed miserably, but the current move looks much more positive.

- During the latest pullback from $1370, the bears have only managed to push the price modestly lower, to my key buy zone at $1310.

- The gold price promptly leaped higher as soon as it touched that area. This is very positive technical action. If the bulls fail a third time (unlikely), investors should be aggressive buyers at my $1270 and $1240 buy zones.

- Please click here now. Double-click to enlarge this gold chart for a closer look at the current price action.

- Gold is attacking the $1370 area from a symmetrical triangle pattern. Using the classic technical analysis promoted by Edwards & Magee, there is roughly a 67% chance of an upside breakout.

- That breakout would push the world’s mightiest metal through $1370… and open the door for a rush higher towards $1420, $1470, and $1520!

- Please click here now. Double-click to enlarge this exciting dollar versus yen chart.

- The dollar’s breakdown under the key 108 support area adds tremendous weight to the argument that gold is poised to surge above $1370.

- Most Trump supporters are focused on his campaign pledges regarding immigration, tariffs, defence, deregulation, and tax cuts. Their focus is on growth rather than inflation. That’s a mistake.

- Reduced immigration tightens the labour market, pushing inflation higher. Borrowing money to buy more bombs to expand an already-gargantuan military-industrial complex puts immense pressure on the bond market. Deregulation and tax cuts are also inflationary.

- While these pledges are indeed positive for gold, my main focus has always been on his more “thunderous” pledges regarding dollar devaluation and a haircut for T-bond investors.

- The dollar breaking 108 is a gamechanger, and the T-bond chart now looks like a train wreck. As bad as it looks now, this may be only the beginning of a bond market nightmare. The bottom line is that Jerome Powell could essentially drop financial nuclear bombs on that train wreck with relentless rate hikes, quantitative tightening, and small bank deregulation.

- To view the current T-bond train wreck chart, please click here now. Double-click to enlarge.

- The T-bond has arrived in the 142 target zone area of the H&S top pattern and a modest rally is expected. Having said that, fundamentals make charts.

- The negative fundamentals that Jerome Powell is set to put on the US government’s bond market table are going to put truly epic pressure on the government’s ability to finance itself.

- Trump is a brilliant businessman, but even a child operating a hot dog stand should clearly see that the US government’s debt problem has no solution other than some kind of bond market default, dollar devaluation, and gold revaluation.

- Trump is not concerned about the US debt problem, and nor should he be concerned if he’s a realist that knows there is no fix to the problem, only an end to it. An endgame that is incredibly positive for gold.

- Please click here now. Double-click to enlarge this GDX daily chart.

- Legendary mining expert David Harquail is launching a major drive to make gold an asset owned by most Western money managers. He’s bringing in heavyweight speakers like Alan Greenspan and other key central bank experts to bolster his presentations to institutional money managers.

- I’ve predicted that this would happen by the summer of 2018 as the Fed successfully transitions America from a deflationary vortex into a modest growth with significant inflation economy.

- King World News has covered the dramatic increase in free cash flow of most GDX component stocks. “Super Dave” Harquail is likely to get a US M2 money velocity bull market wind at his back (thanks to the efforts of Jerome Powell’s rate hikes and QT) as he makes his institutional presentations that highlight both bullion and the miners.

- If that happens, the Western gold community is very quickly going to be happily looking down at prices like GDX $32, $40, $55, $65, and even $100! Of course, that happiness can only happen if gold stock enthusiasts are prepared to take buy-side action right now in my key $23 to $18 GDX price range with a focus on their favourite individual miners!

Thanks and Cheers,

Stewart Thomson

Graceland Updates

https://www.gracelandupdates.com

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

![]()

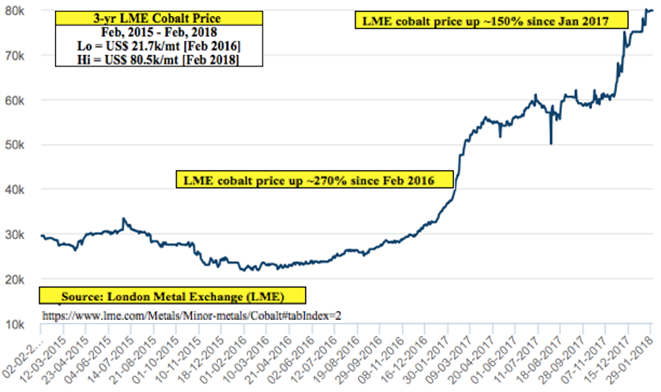

Power Americas Minerals (TSX-V: PAM) / (OTCQX: PWMRF) is well positioned among roughly 18 juniors exploring for Cobalt (“Co“) (and associated gold/silver) in the world-class, past-producing Silver-Cobalt Mining Camp in northeastern Ontario, Canada. Although reports vary, something on the order of 400-750 M ounces of Silver (“Ag”) and 40-50 M pounds of Co were produced in the district.

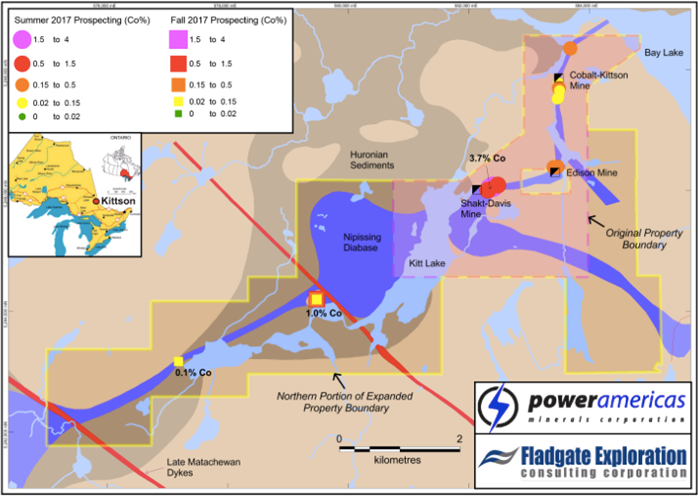

Power Americas has assembled a moderate-sized (vs. its peers) 3,330 hectare (~8,230 acre) land package, 100%-owned, on 15 un-patented mining claims.

Others have properties in and around the district, most notably First Cobalt Corp., (TSX-V: FCC) and Cobalt Power Corp. (TSX-V: CPO) who, like Power Americas, have substantially all of their assets in Ontario. First Cobalt is the bellwether Co name in the region, but it has a C$236 M market cap., ~24 times larger than Power Americas’ ~C$10 M market cap. Cobalt Power is a ~C$28 M company. NOTE: {First Cobalt has by far the largest Co footprint in Ontario, PLUS the only permitted cobalt extraction refinery in North America}.

Importantly, none of the new players have advanced beyond early exploration stage. All of these stocks are highly speculative, and most companies probably would not exist were it not for the booming Co price– which has nearly quadrupled — (from US$21.7k/tonne in Feb 2016 to US$80.5k/tonne in Feb 2018) in the past 2 years.

Importantly, Power Americas has additional drill results to report this month and next. The Company is looking for multiple hits of 1 or more meters of greater than 1.00% Co mineralization, which would be better than most peers in the district have reported so far.

Perfect Storm for Cobalt Prices?

In the Co price chart above, notice the steepness of the curve over just the past several months. Cobalt has almost quadrupled (up ~270%) since February 2016 and is up ~150% since the beginning of last year. The move in Co prices is very similar to that of lithium prices, although lithium prices began moving 6-9 months earlier, and have not been moving up lately the way Co prices have.

Readers are likely aware that over 50% of global Co supply comes from the DRC, and that end users are very anxious to source Co elsewhere due to ongoing concerns about child labor law abuses. Making matters worse, the DRC (suddenly) raised its royalty rate on Co from 2% to 10%, and imposed a 50% “super-profits” tax — defined as income earned on sales of Co at prices > 25% above the price in a Company’s Feasibility Study.

This news comes at the same time that a number of major automakers like BMW, Tesla & Volkswagen are reportedly searching for long-term off-take agreements for cobalt & lithium. Of note, BMW is said to be close to a 10-yr agreement with an unnamed party. The DRC will remain the largest producer for years to come, but the playing field is wide open for supply from Canada and other more business-friendly countries.

Given the proverbial perfect storm for cobalt prices, the early-stage projects / properties in and around Cobalt Ontario could be among the better alternatives for Co supply next decade. Getting back to Power Americas, the management team is excited about the drill results they will be reporting shortly.

Jeffrey Cocks, President & CEO, stated,

“We believe we have assembled a sizable, 100%-owned land package [3,330 ha] that encompasses and surrounds several historical cobalt mines in the most active Cobalt Mining Camp in Canada. We’re highly encouraged by our initial 2017 Exploration Program’s results, and very excited to build off these results with our 2018 winter program that is currently underway.”

Neil Pettigrew, VP Exploration, explained an important factor that differentiates Power Americas from many nearby peers,

“Cobalt mineralization on the Kittson property occurs both in veins and fractures, this gives us a wider target zone. The mineralized zone also displays a fairly consistent strike and dip, these advantages give us a faster pathway toward defining what could be the first new NI 43-101 compliant cobalt resource in the camp.”

The Company’s Co contained mineralization is similar to that of the famous Silver-Cobalt Camp in Ontario, Canada, located ~15 km to the east. It contains the historic Shakt-Davis and Cobalt-Kittson mines, 4 mine shafts and numerous historic workings; the deepest extending down to 628 feet, and combined, > 2,500 feet of lateral development.

In late 2017, management acquired an additional 100% interest in 10 unpatented mining claims totaling ~2,240 hectares. Eight of the new claims are contiguous to the Kittson property and are interpreted to host the western extension of the Shakt-Davis and Edison mine structures. The other 2 are ~5 km south of the Kittson properties’ southern boundary.

Drilling is the Main Catalyst This Quarter

Management announced on January 23rd that it has commenced drilling on the 100% owned Kittson-Cobalt project. A total of 18 holes and 2,000 meters is underway as a follow up on the Fall 2017 ultra-light drill program. Sixteen holes are planned at the historic Shakt-Davis mine, and 2 on the northern extension of the historic Edison mine. Drill holes lengths of 75 to 250 m will test mineralization both near surface and below historic workings. Drill results will be released later this month and into March.

The fracture zone hosting the Shakt-Davis mine has returned grab samples up to 3.66% Co and 1.62% Co over 0.3 m in shallow drilling. The northern extension of the Edison mine hosts numerous historic trenches which have returned up to 0.49% Co in grab samples.

On January 16th, the Company announced results of their diamond drill program on the Kittson-Cobalt project. Seven shallow holes, totaling 161 meters were drilled beneath overburden-filled historic workings in the Shakt-Davis mine area. The program successfully intersected a fracture zone that hosts the Shakt-Davis mineralization over a strike length of 55 m, up to ~30 m deep. The zone is 5-13 m wide (drilled core length).

Commenting on these results, CEO Cocks said,

“These results represent the first drilling since the 1940’s at the Shakt-Davis mine and confirm the cobalt-rich nature of this extensive fracture zone. The zone which hosts the Shakt-Davis mine is related to those which also host the Kittson & Edison mines to the north and east, respectively, cumulatively representing over 3 km of strike length.“

Veins hosting the mineralization at Kittson differ from the typical Cobalt Silver Camp veins in that they are lower in Ag but richer in Co, and are associated with zones hosting meaningful amounts of Au. From assessment files in the Cobalt MNDM office,

“Assays and analyses indicated 1.5% Co and minor Ag over a width of 1.37 m, with select grab samples indicating up to 4.0% Co, and others with up to 2.72 oz/t gold. A further test of hand-picked ore indicated values of 0.87 oz/t Au, 7.92% Co & 7.72% Ni. Another sample returned 97 oz/ton Ag & 0.336% Co.” (Born and Hitch, 1990).

Conclusion

Power Americas Minerals (TSX-V: PAM) / (OTCQX: PWMRF) has as good a chance as any to find promising cobalt mineralization in Cobalt Ontario. A key takeaway from this article should be that Power Americas owns properties that have evidence of mineralization that is lower in silver but richer in cobalt, and is associated with zones hosting meaningful amounts of gold. And, the Company has a substantially lower market cap at C$ 10 M than many of its peers in the district.

Finally, near-term drill results, if they show some hits containing relatively large intervals of greater than 1.00% cobalt– could attract investor attention and drive the share price higher.

Disclosures: The content of this article is for informational purposes only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research, [ER] including, but not limited to, commentary, opinions, views, assumptions, reported facts, estimates, calculations, etc. is to be considered implicit or explicit, investment advice. Further, nothing contained herein is a recommendation or solicitation to buy or sell any security. Mr. Epstein and [ER] are not responsible for investment actions taken by the reader. Mr. Epstein and [ER] have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Mr. Epstein and [ER] are not directly employed by any company, group, organization, party or person. Shares of Power Americas Minerals are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Peter Epstein owned shares and/or stock options in Power Americas Minerals and the Company was an advertiser on [ER]. By virtue of ownership of the Company’s shares and it being an advertiser on [ER], Peter Epstein is biased in his views on the Company. Readers understand and agree that they must conduct their own research, above and beyond reading this article. While the author believes he’s diligent in screening out companies that are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & [ER] are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article. Mr. Epstein & [ER] are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and [ER] are not experts in any company, industry sector or investment topic.

Gold is faring quite well today technically, though you sure wouldn’t know it from the rampant bearish sentiment. Gold’s price is in a strong uptrend over a year old, high in both its current upleg and young bull market. Gold isn’t far from breaking out to its best levels since September 2013, a really big deal. The stock markets even finally sold off after years of unnatural calm. Yet traders are still down on gold.

Across all markets price action drives psychology. When something’s price is rising, traders get excited and bullish on it. So they increasingly buy to ride that upside momentum, amplifying it. Of course the opposite is true when a price is falling, which breeds bearishness and capital flight. Given gold’s great technical picture today, investors and speculators alike should be growing enthusiastic about its upside potential.

But they really aren’t, which is certainly curious. Gold’s current upleg was born right before the Fed’s last rate hike in mid-December. Everyone thinks Fed rate hikes are very bearish for gold, but history proves the opposite as I argued near gold’s recent interim lows. In the 2.4 months since, gold has rallied 6.6% as of the middle of this week. That trounces the leading benchmark S&P 500 stock index’s mere 1.6%.

Gold’s rate of ascent since mid-December annualizes out to a 33% pace, which is pretty darned exciting! Yet gold’s two primary sentiment proxies, silver and the stocks of gold miners, show enthusiasm for gold is nonexistent. Over that same current-gold-upleg span, silver is only up 5.0% while the HUI gold-stock index clocked in with a dismal 1.8% gain. Normally silver and the gold stocks leverage gold upside by 2x to 3x!

As I discussed about a month ago, gold is on the verge of a major breakout that would greatly shift psychology back to bullish. Gold’s bull-to-date peak was carved in early-July 2016 at a $1365 close. For a variety of reasons gold stalled at best since. Just a month ago gold surged to $1358 though, and only a week ago it hit $1353. It wouldn’t take much of a rally to boost gold to new bull-market highs to catch the limelight.

Generally upside breakouts have to be decisive to really attract traders’ attention. I define that as 1% beyond the old level, so $1379 in gold’s bull-high case. That’s only a handful of good up days away, not far at all. And that’s close to $1383, which is gold’s best level in a whopping 4.5 years. Start pushing $1400 again, and even oblivious traders who’ve long forgotten about gold will realize something big is changing.

On top of these key technical upside-breakout levels so close, the sharp stock-market selloff is fantastic news for gold investment demand. The S&P 500 plunged 10.2% in just 9 trading days! That ended an all-time-record 405-trading-day span without a mere 5% pullback, and is the first stock-market correction in 2.0 years. Stock selloffs are very bullish for gold, as investors remember the wisdom of diversifying portfolios.

So gold’s popularity should really be mounting now given its strong price action. Yet that certainly hasn’t happened yet, gold’s sentiment is really curious. The prevailing psychology remains quite bearish, which feels much more like a major bottoming. The fear, anxiety, and apathy somehow still plaguing gold is the polar opposite of the greed and excitement near major highs. Gold is still overlooked, ignored, and shunned.

This weird sentiment anomaly totally disconnected from technical realities can and will turn fast, likely as gold decisively breaks out to new bull highs. That could happen anytime in the coming weeks or maybe months, it is nearing. But for now, it’s useful to understand why gold oddly remains so out of favor. The answer lies in the psychology of gold’s two primary driving forces, futures speculators and stock investors.

Gold-futures speculators exert inordinate influence on daily gold price action. This is primarily due to the extreme leverage inherent in futures trading. This week a single gold-futures contract that controls 100 ounces of gold has a maintenance-margin requirement of just $3500. That’s all the capital traders need to buy or sell a contract. But at this Wednesday’s $1323 gold, each contract controls gold worth $132,300.

That equates to extreme maximum leverage of 37.8x, death-defyingly high! For comparison, the legal limit in stock markets for decades has been 2.0x. At 35x leverage, each dollar speculators deploy in gold futures has 35x the gold-price impact of another dollar used to invest in gold outright. Such ridiculous leverage allows futures speculators to collectively punch far above their weights, dominating gold-price action.

As if that’s not unfair enough to normal investors, gold futures’ extreme leverage necessitates an ultra-short-term focus. Again at 35x leverage, a mere 2.9% adverse price move in gold would wipe out 100% of the capital speculators risked! So these guys are forced to think in terms of minutes, hours, days, or sometimes weeks for their trading time horizons. The months and years of investors may as well be eternities.

That incredibly-myopic view on gold creates all kinds of problems because data is far too sparse to justify ultra-short-term trading. The best fundamental data available on gold is only published once each quarter by the World Gold Council. Some other localized peripheral data is released monthly. So with insane leverage compressing down speculators’ gold outlooks into days or less, they have nothing to trade on.

Instead of backing way off on their leverage and taking rational longer-term trading spans, they fabricate their own gold-trading cues. The two they’ve collectively decided on are the price action in competing US Dollar Index futures and the closely-related Fed-rate-hike outlook. Developments there motivating gold-futures speculators to act are half of the explanation surrounding gold’s curious sentiment these days.

Nearly a month ago futures speculators bid gold up to $1358. They were watching USDX futures, as that leading US dollar benchmark was grinding inexorably lower. On February’s first trading day, the USDX slumped to a major 3.1-year secular low. That weak dollar is what drove gold tantalizingly close to a major bull-market breakout. But futures speculators were perplexed if not angry this was actually happening.

These elite traders hold tight to certain core beliefs with tenacity that puts religious zealots to shame. The main one is that Fed rate hikes are bullish for the US dollar and therefore bearish for gold. The idea is simple, higher rates boost dollar yields making it relatively more attractive than other currencies. So foreign investors rush to buy, bidding the dollar higher. Futures speculators know this is how the world works.

That logic appears sound, but what if their deeply-held thesis simply isn’t true? The Fed’s current rate-hike cycle began in December 2015 after 9.5 years with no rate increases, and 7.0 continuous years of a zero-interest-rate policy. The 5 hikes since coming off a near-zero base should’ve been wildly bullish for the USDX, right? Futures speculators bet heavily long the dollar and short gold heading into that initial hike.

Yet since the day before the Fed started its current rate-hike cycle, the USDX is down 8.3% and gold is up 24.7% as of the middle of this week! Clearly Fed rate hikes aren’t as bullish for the US dollar or as bearish for gold as futures speculators thought. You’d think they’d be smart enough to form their trading strategies based on hard data instead of mere conceptual arguments. But they steadfastly refuse to budge.

Gold started to sell off on Friday February 2nd in the wake of the latest monthly jobs report. It saw wage growth climb at its fastest annual pace since June 2009, stoking inflation fears. Higher inflation implies the Fed will have to hike rates faster. So the oversold USDX surged 0.7% higher that day, making for its biggest up day since late October. Gold-futures speculators saw that and fled, hammering gold 1.4% lower.

The S&P 500 happened to plunge 2.1% that day on those same inflation fears, its own worst down day since early September 2016 before Trump won the election kicking off the extreme taxphoria rally. That sharp stock-market drop shattering the unnatural calm was the dominant news that day. That led investors to assume gold fell because the stock markets sold off, but the real reason was that big dollar bounce.

That’s happened before. Back in late 2008 during that first stock panic in a century the USDX rocketed 22.6% higher in just 4.2 months, its biggest and fastest rally ever! That was in response to safe-haven buying as the S&P 500 plummeted 38.1% in that short span. But that epic dollar strength hammered gold a proportional 23.7% lower. Investors wrongly figured weak stock markets hurt gold, but it was the hot dollar.

When stock markets fall sharply, cash suddenly becomes much more attractive than stocks. So dollar demand surges as stocks plunge. Gold-futures speculators see that and dump gold, driving it lower. This dynamic fully explains gold’s weakness in recent weeks. Every single gold down day was the direct result of a parallel USDX rally! That was true in early-February’s S&P 500 selloff and then again this week.

Since the dollar’s action and the Fed-rate-hike outlook is the extent of gold-futures speculators’ entire trading worldview, they’ve been really bearish on gold as the dollar bounced twice this month. Thus they have greatly pared their long gold-futures positions. This chart superimposes gold over the total gold-futures long and short contracts held by speculators, published weekly in the Commitments of Traders reports.

CoT data is released late each Friday afternoon current to the preceding Tuesday close. So the latest-available data on speculators’ collective gold-futures trading when this essay was published is as of February 13th. In just the 3 CoT weeks since gold hit $1358, these guys dumped a massive 59.8k long contracts! That’s equivalent to 185.9 metric tons of gold, a huge amount. No wonder gold couldn’t rally during that.

But interestingly all that frenzied gold-futures long selling on modest US-dollar strength drove specs’ total longs back down to their gold-bull support line rendered above in green. Other than a brief break below leading into the Fed’s last rate hike, strong buying has soon followed earlier support approaches. That has fueled sharp gold rallies once spec longs hit support. That will likely prove true again in coming weeks.

Despite the extreme leverage they wield, gold-futures speculators’ capital is finite. They only have so much they can deploy on both the long and way-smaller short sides of the trade. So looking at where specs’ total longs and shorts are relative to their own past-year trading ranges offers an excellent approximation of how much buying or selling firepower these guys have left. That greatly affects gold’s outlook.

As of last Tuesday the 13th, their total longs were only running 35% up into their past-year trading range. That means these elite traders still had room to do nearly 2/3rds of their likely near-term buying! That’s very bullish. The short side was far-less bullish, with speculators’ total gold-futures shorting running just 14% up into their past-year trading range. That means 6/7ths of likely short-covering buying was already done.

The gold-price impact of buying new long contracts or buying to cover existing shorts is identical. If these total long and short trading ranges are combined, speculators’ effective total upside bets on gold were at 55%. That implies 45% of probable near-term buying remains! That’s exceptionally bullish with gold still up near major breakout highs. Normally near highs 80% to 90% of buying power has already been expended.

So once the USDX inevitably turns lower again, there’s lots of room for speculators to buy gold futures and push gold higher. The dollar weakness will likely reemerge on ballooning US deficits and debt. The Republican lawmakers are keeping the extreme out-of-control government spending of the Obama era intact, while simultaneously cutting taxes. Rising rates are also catapulting US interest expenses much higher.

And more Fed rate hikes aren’t likely to ride to the dollar’s rescue. The USDX entered the last Fed-rate-hike cycle between June 2004 to June 2006 relatively low, perfect conditions for a rally. Then the FOMC hiked 17 times in a row, more than quintupling its federal-funds rate to 5.25%. Yet the USDX still slipped 3.8% over that exact span, while gold powered 49.6% higher! Fed rate hikes haven’t proven great for the dollar.

The second driving force behind gold’s curious sentiment is little investor interest. Investors control vastly more capital than futures speculators. So when investment capital is moving into or out of gold in any significant way, it overpowers and drowns out all the daily gold-futures noise. Stock selloffs greatly boost gold investment demand, but not immediately. Investors first get distracted by the dollar-driven futures action.

The S&P 500 plunged 8.5% in just 5 trading day ending February 8th, a precipitous tumble. Yet instead of surging on that stock weakness, gold dropped 2.4%. Investors assume that was in sympathy with the stock markets. But it was really the result of the USDX surging a similar 2.0% over that span on safe-haven buying. The dollar surging on heavy demand in the hearts of stock-market selloffs delays gold’s reaction.

So investors weren’t yet flocking back to gold earlier this month. The world’s dominant gold ETF publishes its physical-gold-bullion holdings held in trust for shareholders daily. The GLD SPDR Gold Shares showed no holdings builds as stock markets recently plunged, indicating stock-market capital wasn’t yet flowing into gold. There were actually sizable draws over that span as stock investors dumped GLD shares.

When stock markets fall sharply, investors freak out. Fear flares so fast that people have to act instead of think. So they sell everything they can to raise cash, including gold. Weaker gold prices driven by futures selling in response to the surging USDX exacerbate any gold selling. In the heat of the moment investors think gold gets sucked into stock-market selloffs, that it really doesn’t move counter to stocks.

But once the biggest-fear days in stock-market selloffs pass, investors come to realize they are taking on too much risk with their stock-dominated portfolios. So they start rebuilding depleted gold positions in the wake of major stock-market selloffs. We’re indeed already seeing modest GLD builds return over the past week or so. And this same dynamic was actually what birthed today’s gold bull back in early 2016.

Heading into that first Fed rate hike in 9.5 years in December 2015, gold slumped to a brutal 6.1-year secular low. Because futures speculators are totally convinced Fed rate hikes are kryptonite for gold, history be damned. The S&P 500 had gone a near-record 3.6 years without a single 10%+ correction, so complacency was extreme. Investors believed stocks did nothing but rally, so they could hold them forever.

Finally back-to-back S&P 500 corrections arrived in mid-2015 into early 2016. This benchmark stock index fell 12.4% in 3.2 months, bounced most of the way back, and then dropped another 13.3% over 3.3 months into mid-February 2016. That first SPX correction only spurred limited gold investment buying. Stock investors weren’t very worried the lofty stock markets would head much lower again, so they procrastinated.

Yet after that second correction arrived shortly after, differential GLD-share demand exploded! Investors flocked back to gold to prudently diversify their stock-heavy portfolios. That heavy investment buying catapulted gold 29.9% higher in just 6.7 months, birthing today’s bull market. Gold kept rallying rather relentlessly until the stock markets finally made new highs which totally dispelled weaker-stock worries.

The same thing happened during and after 2008’s epic stock panic. Gold was hammered by the skyrocketing USDX during that extreme stock-market selloff. But in the following months gold investment demand blasted higher as investors realized they needed counter-moving gold allocations in their portfolios. That heavy gold investment demand persisted for years after the stock panic, driving gold to record highs.

History has shown over and over that gold investment demand is weak when stock markets are high and euphoric. Why buy gold when stocks apparently do nothing but rally indefinitely? But once corrections or new bear markets emerge to rebalance sentiment and knock back overvalued, overbought stocks, gold soon returns to favor. That doesn’t happen instantly, as safe-haven dollar buying temporarily forces gold lower.

But after major selloffs when investors start to realize that stock markets can fall too, they start thinking about gold again. It’s the ultimate portfolio diversifier. That post-selloff gold-investment process is very gradual, it takes months or years to rebuild significant gold positions relative to stock portfolios. Odds are a similar outcome will play out again following this latest sharp S&P 500 selloff, which likely isn’t over yet.

Given the radical gold underinvestment following this extreme stock bull, investors will likely have to do big gold buying for years to reestablish normal portfolio allocations. That will continue to fuel this young gold bull born in late 2015 in the previous stock-market correction. At best gold was only up 29.9% so far as of mid-2016, nothing yet. The last gold bull powered 638.2% higher over 10.4 years ending August 2011!

While investors can ride gold’s ongoing bull in GLD shares, far better gains will be won in the stocks of its leading miners. They tend to amplify underlying gold gains by 2x to 3x due to their profits leverage to gold. With gold so out of favor, the gold stocks are deeply undervalued today. That gives them huge upside as gold mean reverts higher, dwarfing everything else in all the stock markets. Fortunes will be won.

At Zeal we’ve literally spent tens of thousands of hours researching individual gold stocks and markets, so we can better decide what to trade and when. As of the end of Q4, this has resulted in 983 stock trades recommended in real-time to our newsletter subscribers since 2001. Fighting the crowd to buy low and sell high is very profitable, as all these trades averaged stellar annualized realized gains of +20.2%!

The key to this success is staying informed and being contrarian. That means buying low before others figure it out, before undervalued gold stocks soar much higher. An easy way to keep abreast is through our acclaimed weekly and monthly newsletters. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. For only $12 per issue, you can learn to think, trade, and thrive like contrarians. Subscribe today, and get deployed in the great gold and silver stocks in our full trading books!

The bottom line is gold’s curious sentiment today results from an interplay of factors. Safe-haven dollar buying erupted as usual during the stock markets’ first real selloff in a couple years. That led the gold-futures speculators to sell aggressively, driving gold lower. Investors saw gold falling with stocks and wrongly assumed stock selloffs aren’t bullish for gold. And their confidence in stocks remains very high.

But as stocks head lower again after their post-correction bounce, psychology will really shift. Investors will increasingly worry that stock weakness could persist for some time. They will remember gold is the ultimate portfolio diversifier, and start shifting capital back into it. The resulting investment buying will persist for months or even years, drowning out whatever the hyper-leveraged gold-futures speculators are up to.

Adam Hamilton, CPA

February 23, 2018

Copyright 2000 – 2018 Zeal LLC (www.ZealLLC.com)

- I’ve noted that when China’s markets go quiet during the “Golden Week” holiday, the gold price tends to soften.

- Please click here now. Double-click to enlarge this key gold chart. Price softness is expected during this holiday, and the good news is that it is occurring on very light volume.

- The bears would argue there’s a small double top in play, while the bulls have an inverse head and shoulders bottom pattern on their team. A bull flag pattern may also have formed.

- I’ve told investors to expect a substantial battle between the bulls and bears in the $1370 area, and that’s exactly what is taking place.

- Please click here now. Double-click to enlarge this US dollar versus Japanese yen chart. After tumbling through key support at 108, a relief rally is now in play.

- The 108 area is now resistance. For gold, the price action of the dollar against the yen is very important. I expect the dollar’s relief rally to fail in the 108 – 110 area, and then a descent towards par (100) should get underway.

- That would be a key signal that gold is going to move above $1370 and attract significant institutional interest by doing so.

- In terms of trading volume, gold is a huge market. On a daily basis, dollar volume for gold trading in London is about as big as all the dollar volume for all the stocks traded on the New York Stock Exchange.

- Banks trade gold as a FOREX market currency. In terms of volume, it’s the fifth most active in the world. So, when the gold price weakens as Chinese buyers go on holiday, that can affect other major markets.

- For example, today the Dow is down, bonds are down, but the dollar is up against the yen. That’s because Golden Week is pushing gold down against the dollar and FOREX traders are reacting to that in the dollar-yen market.

- Please click here now. Double-click to enlarge this T-bond chart. Most bank analysts thought that gold would fall if the Fed launched quantitative tightening and rate hikes. Instead, gold has rallied since the tightening cycle began, as I predicted it would.

- Most investors underestimate the effects of love trade demand for gold (or lack of it) on the world’s major markets. Gold demand growth in China and India can put pressure on US interest rates. That’s because bank FOREX traders react to the rise in the gold price by selling the dollar.

- Credit Suisse notes that countries like China are increasing their “dedollarization”. That’s more good news for gold.

- Trump and most congressmen are aggressively increasing the US government’s debt. I’ve argued that Trump likely believes there is no solution to the government’s debt problem other than gold revaluation, dollar devaluation, and T-bond default.

- Since there is no real solution and Trump is a pragmatist, he just lets the debt rise to the T-bond default/gold revaluation point. It’s a wise move on his part, and fabulous news for gold stocks!

- Please click here now. Double-click to enlarge this GDX chart. GDX has again entered my ultra-important $23 – $18 accumulation zone. Investors need to keep their eye on the US M2 money velocity reversal prize, because that is what will produce sustained outperformance of gold stocks against gold.

- On that note, please click here now. Fred Hickey does a spectacular job of outlining the mindboggling undervaluation of gold stocks versus bullion. The same is true for the silver stocks; the miners have cut costs but are trading at generational lows against bullion.

- Fred notes that for the average GDX component stock the spread between the company’s revenues and costs is about the same as it was in 2012, there are less GDX shares outstanding now, but the GDX ETF price is now about $22 versus about $45 in 2012!

- Many gold market analysts have noted the facts that Fred notes. To repeat, what creates a sustained outperformance of gold stocks versus bullion is inflation. To get serious inflation, money velocity must rise.

- To get a rise in money velocity, fiat money must move out of the deflationary hands of the US government (T-bonds) and into the fractional reserve banking system. To get that job done, rate hikes and quantitative tightening are mandatory catalysts.

- The great news is that Jerome Powell is now sitting in the Fed’s big chair. On March 21 he is going to set the tone for the rest of the year with his statements and actions. Jerome has stated that he doesn’t really follow the stock market.

- That’s a slap in the face for mainstream analysts that literally worship the US stock market as some kind of “supreme being”. Jerome is set to do a lot of the things that Paul Volker did in the 1970s (without the cigars, fanfare, and ego).

- Ben Bernanke promoted deflation with QE and rate chops. That produced a dramatic acceleration in the gold stocks versus gold bear cycle. Janet Yellen talked a great inflationary talk, enacted the right policies to get the inflationary job done, but moved at a snail’s pace.

- Jerome has tax cut inflationary wind at his back, and I expect most market gurus (mainstream and gold) to find themselves shell shocked when Jerome shows them on March 21 just how focused he really is on reversing US money velocity. Let’s hope the entire world gold community is as focused as I am on accumulating key gold stocks in my $23 – $18 buy zone for GDX, in preparation for a major league bull market in US money velocity!

Cheers

Stewart Thomson, Graceland Updates

Note: We are privacy oriented. We accept cheques, credit card, and if needed, PayPal.

Written between 4am-7am. 5-6 issues per week. Emailed at aprox 9am daily.

https://www.gracelandupdates.com

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

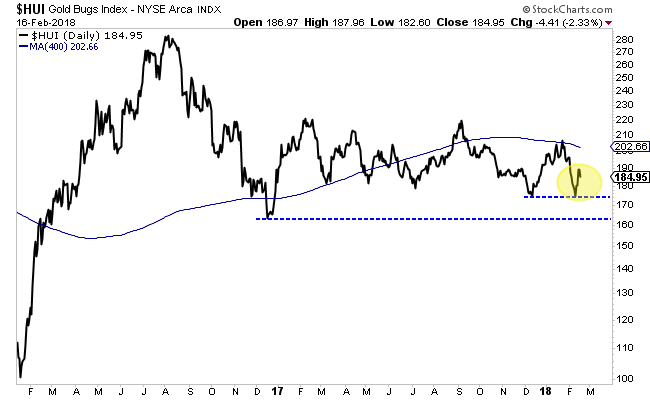

Gold has been on the cusp of a major breakout but someone forgot to tell the gold stocks. Gold is right back at resistance levels yet the various gold stock indices are off their September 2017 highs by 11% to 16%. The relative weakness in the gold stocks (and Silver) is a signal that Gold is unlikely to breakout now. In fact, if Gold were to correct here the gold stocks could threaten support and perhaps make new lows. While that sounds quite bearish, history shows that a break to new lows in gold stocks would be a massive buy signal.

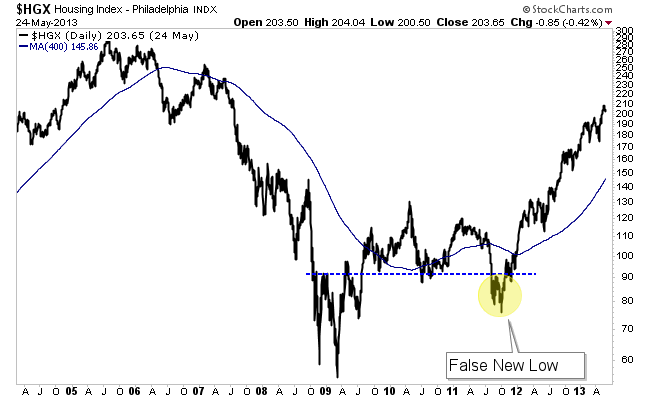

The history we refer to is the path of recovery for a market following a mega-bear, which we define as nearly 3 years and at least an 80% decline. There are three strong historical examples. Those are the S&P 500 during the Great Depression, Thailand after its bust in the mid to late 90s and the housing stocks after 2005 to the March 2009 low. The recovery in each (following the mega-bear) followed three distinct phases. There is a sharp initial rebound which is followed by a correction and lengthy consolidation which lasts at least 18 months. Eventually, the long consolidation ends and the market surges higher in an impulsive fashion.

The gold stocks are currently in the 19th month of their correction and consolidation. They bounced from support in December but retraced that entire bounce. After a second rebound from support, they could threaten a break of that support. Below we show the HUI Gold Bugs Index which does not include the royalty companies as GDX does. The HUI is not too far from its December 2016 low and could even break it if Gold were to correct.

Conventional technical analysis would imply that is a sell signal for the gold stocks.

But history argues the complete opposite.

In the 21st month of its correction and consolidation in 1935, the S&P 500 had broken down to a 2-year low. Was the market headed for a retest of the Great Depression low?

In the 19th month of its consolidation in the fall of 2011, housing stocks had broken to a 2-year low. Was the sector headed for a retest of the Global Financial Crisis low?

Thailand’s correction and consolidation phase was different than the others as it made its low only 15 months in but then consolidated and grinded slightly higher for the next 13 months before exploding to the upside. At its corrective price low 15 months in the index was at a 2-year low.

The HUI closed Friday just below 185. Its December 2016 low is 163.49. A 12% decline would put it below its December 2016 low and at a 2-year low.

The three historical examples all made 2-year lows before their correction and consolidation phase ended.

A potential failed breakout or correction in Gold could leave gold stocks vulnerable to a decline to new lows. While that sounds bearish, the historical context argues otherwise. Two of the three historical examples that show similarities to the gold stocks broke to new lows. Yet that break proved to be the best buying opportunity since bear market low. All three of the historical examples made 2-year lows before exploding higher. History shows that if the HUI Gold Bugs Index were to break to new lows it could be a false break and a massive buy signal. Quality juniors that are bought on forthcoming weakness (if Gold corrects) should deliver fantastic returns over the ensuing 12 to 18 months. To follow our guidance and learn our favorite juniors for the next 12-18 months, consider learning about our premium service.

![]()

‘In order to produce half a million cars a year…we would basically need to absorb the entire world’s lithium-ion production.’ – Elon Musk

“The skillsets that young people should learn about mining should apply to everything. We just need to do a better job of explaining to people in urban environments that the human activity of mining is absolutely fundamental to the way this planet is going to evolve. Completely and totally fundamental.” – Robert Friedland, Ivanhoe Capital

The future envisioned by industry leaders hinges heavily on the production of new materials to power and build the future. Leaders such as Elon Musk have been developing the blueprint for the future with electric cars, battery grids and renewable energy solutions. While, other leaders such as Robert Friedland are looking to supply the materials to build this future. Mr. Friedland makes the case and understands the story that is unrolling in real time. Mining is the critical component to meet the world’s demands for a sustainable future. The prerequisite for this future is mining and with every mineral discovery and development project, this future is coming closer.

Mr. Friedland is not the only miner that realizes the economy of tomorrow will require the development of new mining assets. Azincourt Energy Corp. (TSX-V: AAZ) is a Canadian junior exploration company that has been actively building their mining asset portfolio in anticipation of the future demand for minerals that will provide clean energy; from lithium to uranium to cobalt.

Azincourt Energy Chairman, Ian Stalker is an experienced mining executive that sees the writing on the wall when it comes to the materials and fuel that future technology will require. Mr. Stalker is a senior international mining executive with over 45 years of hands-on experience in resource development. Over his career Mr. Stalker has directed over twelve major mining projects, from exploration drilling to start-up, including gold, base metal, uranium and industrial minerals. He is currently CEO of LSC Lithium (TSX.V: LSC), and Chairman of Plateau Uranium (TSX.V: PLU), and is the former CEO of UraMin Inc., the London and Toronto listed public uranium company that was acquired by Areva for US$2.5 billion in August 2007. In a recent press release, Mr. Stalker outlined the current strategy for Azincourt.

“The lithium market is obviously very strong right now, and the near-term future for lithium demand remains extremely positive. Our decision to expand Azincourt’s focus to include lithium and other materials is something we feel strongly about. To get a foothold and exposure in this environment, at this time, is an important and strategic step for us.”

Azincourt recently acquired five lithiums projects in located in the Winnipeg River Pegmatite Field, Manitoba, Canada. Two of the projects, the Lithium One and Two projects, are adjacent to Quantum Minerals Corp.’s Cat Lake lithium project which includes a historical estimate from drilling in 1947 that defined 545,000 tonnes of 1.4 percent lithium oxide (Li2O). Drilling could prove up this ground.

Two other of the acquired lithium projects, the Lithman West and East projects are adjacent to the Tanco Mine lease property. These projects are part of the Winnipeg River pegmatite field which hosts numerous lithium-rich pegmatites or “hard-rock” lithium such as the Tanco pegmatite that has been mined at the Tanco mine since 1969 for spodumene, a major component for hosting lithium (Li), and other rare earth ores.