Argentinian lithium producer Orocobre (TSX: ORL) recently reported lower than expected lithium production in its third fiscal quarter because weather interfered with its evaporation rates of its lithium brines. This reveals two problems with lithium brine production: reliability and geography. Another source of lithium is rising to met these problems, hard rock lithium mining.

One analyst pointed out that Orocobre’s production problems “clearly demonstrate” that production is not a straightforward process. “Weather events are beyond the control of Orocobre, but this reaffirms that there is still room to improve on the robustness of operations and reduce production variability from we ather impacts,” the analyst stated.

The company reported a 25-per-cent lower evaporation rate compared with the same quarter in 2017 which caused production problems and lithium output to fall 29 percent to 2,802 tonnes of Lithium Carbonate equivalent, from 3,937 tonnes in the December quarter. Its February rates were the lowest since 2011.

Weather has clear impacts on the production at lithium brine operations and with global demand for lithium on the rise, more reliable and consistent methods of production will be required. Lithium brine operations are limited to select climates and regions that can support sufficient weather to ensure economic processing.

Demand for the metal is set to grow by 600,000-800,000 tonnes of lithium carbonate equivalent over the next 10 years, Daniel Jimenez, senior commercial vice president at SQM, said.

The global lithium industry will need $10 billion to $12 billion of investment over the next decade to meet surging demand amid the electric vehicle boom, Daniel Jimenez of Chilean miner SQM said.

Not all lithium is equal and not all lithium is mined the same way. There are two significant sources of lithium, Lithium Brines and Lithium-Cesium Tantalum Pegmatites (hard rock).

According the United States Geological Survey’s 2018 Mineral Commodity Summaries, Australia was the largest producer of lithium. It produced 18,700 MT of lithium last year, up 3,300 MT from the previous year. The 34-percent increase has been attributed to two new spodumene operations that ramped up production to meet strong demand.

Australia hosts the Greenbushes lithium asset, which is operated by Talison Lithium, a subsidiary jointly owned by Tianqi Lithium (SZSE:002466) and Albemarle (NYSE:ALB). Greenbushes is the longest continuously operating mining area in Western Australia, having been in operation for over 25 years.

These production figures helped to push Australia as the top lithium producing country and it shows how hard rock lithium mines have the potential to disrupt traditional sources of lithium from older operators of lithium evaporation ponds.

Hard rock lithium deposits are not limited to select climates and regions and are going to help fill the demand as they are more evenly geographically distributed across the globe and are less dependant on a changing climate for production.

It was music to gold bug ears.

We’ve all heard the seemingly shocking or outrageous price targets for Gold. So it’s not new.

But this time from a non gold pusher. Someone with credibility in the larger financial world and a track record to boot.

Gundlach’s comment was included in every piece of Gold literature that recently crossed my desk. No doubt, if Gold starts breaking to the upside, Gundlach’s quote will be used by aggressive marketers and publishers. But I digress.

According to ZeroHedge, Gundlach said that based on classic chart reading, there is an “explosive, potential energy” of a huge “head and shoulders bottom” base, signaling a move of $1000/oz.

But there’s one problem.

I like Jeff Gundlach. He’s way smarter and way more successful than me.

But there’s no technical basis for $1000/oz upside in Gold.

The measured upside target from the recent years of consolidation projects to $1700/oz. Upon a break above $1375/oz, the target becomes $1700/oz, with a pit stop likely around $1550/oz.

The next strong technical targets, following $1700 are $1800 and $1900, the all-time high.

The biggest moves (in nominal terms) in most markets occur after breakouts to new all time highs.

As you can see, Gold is one of the best examples of this. Look at how Gold surged after 1971, 1978 and 2009.

Gold Weekly Line Chart

The potential breakout through $1375/oz would be the most significant one since 2005 when Gold took out +20 year resistance to make a new multi-decade high. Sure, the breakouts in 2008 and 2009 were quite significant but Gold’s bull market was already well established.

Circling back to Gundlach’s target, I don’t see anything technically that points to $2,375 being a strong target. The strongest targets are $1700, $1800 and $1900. The most significant upside move would likely be a retest of the all time high. That is roughly $525/oz of upside.

But upside of $1000/oz sounds better and makes for better headlines than $525/oz of upside. In other words, it will get picked up by media outlets. (Think of Jim Rickards $10,000 target which has been given quite a bit of coverage on mainstream outlets).

My guess is Gundlach thinks Gold is going to break to the upside and his $1000/oz upside call is a way for him to get credit for calling the breakout while remaining front and center in the media.

At present, Gold is trying to recover after failing to make a weekly close above $1350/oz for five consecutive weeks. The good news is the gold stocks have held up quite well and so too has Gold priced against foreign currencies. If these conditions persist during weakness in Gold then it suggests Gold would have another chance to breakout sooner rather than later. In anticipation of that breakout, we have been accumulating the juniors with 300% to 500% upside potential over the next 18-24 months. To follow our guidance and learn our favorite juniors, consider learning more about our premium service.

The gold miners’ stocks have mostly been consolidating low this year, exacerbating bearish sentiment. Even with gold grinding higher in a solid uptrend and nearing a major upside breakout, the gold stocks just can’t get any love. But that may be about to change, with gold and its miners’ stocks in the midst of their spring rally. Strong seasonal tailwinds make May one of the best months of the year in gold-stock bulls.

Gold-stock performance is highly seasonal, which certainly sounds odd. The gold miners produce and sell their metal at relatively-constant rates year-round, so the temporal journey through calendar months should be irrelevant. Based on these miners’ revenues, there’s little reason investors should favor them more at certain times of the year than others. Yet history proves that’s exactly what happens in this sector.

Seasonality is the tendency for prices to exhibit recurring patterns at certain times during the calendar year. While seasonality doesn’t drive price action, it quantifies annually-repeating behavior driven by sentiment, technicals, and fundamentals. We humans are creatures of habit and herd, which naturally colors our trading decisions. The calendar year’s passage affects the timing and intensity of buying and selling.

Gold stocks exhibit strong seasonality because their price action mirrors that of their dominant primary driver, gold. Gold’s seasonality generally isn’t driven by supply fluctuations like grown commodities experience, as its mined supply remains fairly steady all year long. Instead gold’s major seasonality is demand-driven, with global investment demand varying dramatically depending on the time within the calendar year.

This gold-demand seasonality is well-known and heavily studied. The seasonal gold year starts in late July as Asian farmers begin reaping their harvests. They plow some of their surplus income into gold. That’s followed by the famous Indian wedding season in autumn, with its heavy gold buying for brides’ dowries. That culture believes festival-season weddings have greater odds of yielding long, successful marriages.

After that comes the Western holiday season, where gold jewelry demand surges for Christmas gifts for wives, girlfriends, daughters, and mothers. Following year-end, Western investment demand balloons after bonuses and tax calculations as investors figure out how much surplus income the prior year generated for investment. Then Chinese New Year gold buying flares up after that heading into February.

These understandable cultural factors drive surges of outsized gold demand between summer and late winter. But interestingly there is one more gold-demand spike in spring. Over the years I’ve seen a variety of theses explaining this April-and-May seasonal gold rally, but nothing definitive like for the rest of the year’s gold seasonality. As silly as it sounds, I suspect spring itself is the reason for this demand surge.

Sentiment exceedingly influences investing, which requires optimism for the future. Investors won’t risk deploying their scarce capital unless they believe it will grow. And the glorious expanding sunshine and warming temperatures of spring naturally breed optimism. The vast majority of the world’s investors are far enough into the northern hemisphere that spring has a major impact. This seasonality extends to stocks too.

Since it’s gold’s own demand-driven seasonality that fuels the gold stocks’ seasonality, that’s logically the best place to start to understand what’s likely coming. Price action is very different between bull and bear years, and gold is absolutely in a young bull market. After being crushed to a 6.1-year secular low in mid-December 2015 on the Fed’s first rate hike of this cycle, gold powered 29.9% higher over the next 6.7 months.

Crossing the +20% threshold in early March 2016 confirmed a new bull market was underway. Gold corrected after that sharp initial upleg, but normal healthy selling was greatly exacerbated following Trump’s surprise election win. Investors fled gold to chase the taxphoria stock-market surge. Gold’s correction cascaded to monstrous proportions, hitting -17.3% in mid-December. But that was shy of a new bear’s -20%.

Gold’s last mighty bull market ran from April 2001 to August 2011, where it soared 638.2% higher! And while gold consolidated high in 2012, that was technically a bull year too since gold just slid 18.8% at worst from its bull-market peak. Gold didn’t enter formal bear-market territory at -20% until April 2013, thanks to the crazy stock-market levitation driven by extreme distortions from the Fed’s QE3 bond monetizations.

So the bull-market years for gold in modern history ran from 2001 to 2012, skipped the intervening bear-market years of 2013 to 2015, and resumed in 2016 to 2017. Thus these are the years most relevant to understanding gold’s typical seasonal performance throughout the calendar year. We’re interested in bull-market seasonality, because gold remains in its young bull today and bear-market action is quite dissimilar.

This chart averages the individually-indexed full-year gold performances in those bull-market years from 2001 to 2012 and 2016 to 2017. 2018 isn’t included yet since it remains a work in progress. This chart distills out gold’s bull-market seasonal tendencies in like percentage terms. Quantifying gold’s bull-market seasonal tendencies requires all relevant years’ price action to be recast to be perfectly comparable.

That’s accomplished by individually indexing each calendar year’s gold price action to its final close of the preceding year, which is recast at 100. Then all gold price action of the following year is calculated off that common indexed baseline, normalizing all years regardless of price levels. So gold trading at an indexed level of 105 simply means it has rallied 5% from the prior year’s close, while 95 shows it’s down 5%.

This methodology renders all bull-market-year gold performances in like percentage terms. That’s critical since gold’s price range has been so vast, from $257 in April 2001 to $1894 in August 2011. Finally each calendar year’s individually-indexed gold prices are averaged together to arrive at this illuminating gold-bull seasonality. Gold has always tended to enjoy strong rallies in the spring months of April and May.

During these modern bull-market years from 2001 to 2012 and 2016 to 2017, gold’s spring rally tended to start in mid-March on average. From that major seasonal low following the winter rally, gold often starts grinding higher before its gains accelerate through April and most of May. This spring rally has generally run its course by late May. Across the 14 bull years in this study, gold averaged nice spring rallies of 3.7%.

This spring rally unfolds rapidly, with an average duration of just 2.2 months. That makes it the smallest and shortest of gold’s three major seasonal rallies, falling way behind the champion 9.5% winter rally that precedes it and strong 6.6% autumn rally that follows the summer doldrums. Nevertheless, it is still well worth trading. 3.7% gains still really make a difference, and naturally about half of years exceed this average.

This year gold’s spring-rally bottoming came on March 20th, when gold closed at $1310 the day before the Fed was universally expected to hike for the 6th time in this cycle. That was March’s 14th trading day this year, right in line with gold’s average seasonal low on March’s 10th trading day. And so far gold has largely followed the spring-rally seasonal pattern since, gradually grinding higher from late March to mid-April.

Climbing the typical 3.7% from that spring low into May’s spring-rally topping would propel gold to $1358. That’s right on the verge of being a major decisive breakout from the horizontal $1350 resistance line that gold-futures speculators watch like hawks. And it isn’t far from new bull-market highs above July 2016’s $1365 bull-to-date peak. As I wrote last week, this spring rally really ups the odds gold is nearing a bull breakout!

And given its performance in April, gold ought to see a bigger May rally than usual this year. On average in these 14 modern bull-market years, gold climbed 1.8% in Aprils then another 1.3% into its late-May spring-rally toppings. But as of the middle of this week, gold was actually down 0.1% month-to-date in April. That’s poor performance by April standards, setting up this May for a strong mean-reversion rally.

Historically this spring-rally April-May span is often self-equalizing. If gold materially underperforms or outperforms its seasonal averages in April, its May performances tend to mean revert and overshoot in the opposite direction. Back in 2009 for example, gold fell 3.4% in April but then blasted 10.0% higher in May! In 2016 gold surged 5.1% in April before dropping 6.1% in May. Weak Aprils often lead to strong Mays.

If gold is bid too aggressively in April, the resulting excitement entices in and exhausts all available near-term buying before the summer doldrums. That certainly hasn’t happened this year. Gold rallied into mid-April, but reversed sharply on a strong short-covering rally in US Dollar Index futures. Thus gold has largely drifted sideways on balance this month. So the usual spring buying likely hasn’t even started yet!

That leaves traders with full capital firepower to flood back in in May, likely as the sharp USDX rally runs out of steam. The delayed spring-rally gold buying this year can all be compressed into May, which really increases the odds of outsized gains. While nothing is guaranteed in seasonals since they merely use multi-year averages to reveal trend tendencies, strong Mays are definitely more likely following weak Aprils.

And as goes gold, so go gold stocks. Gold stocks also exhibit strong seasonality, which is of course the direct result of gold’s own seasonality. Since gold-mining costs are largely fixed when mines are being planned, fluctuations in gold’s price flow directly into amplified moves in gold-mining profits. Higher gold prices drive much-higher earnings for the gold miners, which attract in more investors to bid up stock prices.

The ironclad historical relationship between the price of gold, gold-mining profitability, and therefore the gold-stock price levels is exceedingly important to understand. If you need to get up to speed, I wrote an essay looking at gold-stock price levels relative to gold early last month. Fundamentally gold stocks are leveraged plays on gold. Thus they really outperform in the spring due to gold’s strong seasonal rally.

This next chart applies this same bull-market-seasonality methodology used on gold directly to the gold stocks. It looks at the average annual indexed performance in the flagship HUI NYSE Arca Gold BUGS Index in these same bull-market years of 2001 to 2012 and 2016 to 2017. Because of gold’s dominant influence over gold-mining earnings, gold-stock seasonality naturally mirrors and amplifies gold’s own seasonality.

Gold stocks’ seasonal spring rally is much stronger than gold’s, buttressing that spring-optimism-drives-stock-buying thesis. Between mid-March and early June, the gold stocks have averaged hefty 12.8% rallies in these 14 modern bull-market years. That makes for exceptional 3.5x upside leverage to gold’s 3.7% seasonal spring rally! Interestingly this is gold stocks’ best seasonal leverage to gold’s gains by far.

While the HUI averaged 15.5% surges during gold’s winter rally, that only made for 1.6x upside leverage to gold’s big 9.5% gain. And the HUI’s 10.5% average gain during gold’s autumn rally also only amplified gold’s 6.6% gain by 1.6x. So while the gold-stock spring rally’s 12.8% average gains rank second out of these three seasonal rallies, it offers the most bang for the buck in gold-stock upside compared to gold!

This year the gold stocks’ spring-rally bottoming happened on March 20th, the same day as gold’s. The HUI slumped to 169.2 that day. Since then this leading gold-stock index has recovered 6.9% as of the middle of this week, trouncing gold’s 1.0% spring-rally gains so far. A merely-average spring rally would take the HUI to 190.9 by late May or early June, which is another 5.6% higher from here. That’s worth riding.

But if gold’s seasonal spring rally is compressed into May, and strong buying forces it over $1350 or even better its $1365 bull-to-date high, the gold miners’ stocks have far more near-term upside potential. For the most part gold stocks remain deeply out of favor, forgotten or ignored. But they will explode back on to speculators’ and investors’ radars if major new gold highs attract the financial media’s interest and attention.

Again as I discussed last week, gold’s nearing bull breakout will work wonders for not only psychology but hard gold-mining profits. The gold stocks are radically undervalued today compared to their actual underlying fundamentals. In Q4’17 gold averaged about $1276 per ounce, but the major gold miners of the leading GDX VanEck Vectors Gold Miners ETF reported average all-in sustaining costs of just $858 per ounce!

So they were already collectively earning fat operating profits of $418 per ounce. And these are going to soar in Q1’18, because the average gold price surged 4.1% quarter-on-quarter to $1329. Since mining costs are largely fixed, all-in sustaining costs will likely stay flat from Q4. That means major gold miners’ operating profits are likely to rocket 12.7% QoQ to $471 per ounce! That will delight contrarian investors.

The gold miners will be releasing these latest Q1 results between now and mid-May, right when gold is powering higher in its seasonal spring rally. So the gold stocks are certainly set up for an outsized spring rally this year! The potent combination of absurdly-cheap gold-stock prices, surging earnings forcing their valuations even lower, and higher gold prices attracting financial-media attention should really stoke traders’ interest.

This last chart breaks down gold-stock seasonality into even-more-granular monthly form. Each calendar month between 2001 to 2012 and 2016 to 2017 is individually indexed to 100 as of the previous month’s final close, then all like calendar months’ indexes are averaged together. Slicing up seasonal tendencies this way shows May has averaged the second-strongest monthly gold-stock gains in modern bull-market years.

During these 14 Aprils in modern gold bull-market years, the gold stocks as measured by the HUI saw average gains of 1.6%. But the lion’s share of the spring-rally gains came in May, where average gains more than tripled to 5.0%! For decades if not longer, May has been one of the best and most-important months to be heavily long gold miners’ stocks. Only February proved better seasonally at a +5.4% average.

The key to gold stocks’ spring rally is to get your capital deployed in mid-March, when gold stocks swoon to their spring-rally bottoming. In intra-month terms the initial gains are often fast in late March as gold stocks rebound out of oversold lows. But then the spring rally tends to slow down in April, discouraging impatient and short-sighted traders. The real gains come in May, and next month’s setup is exceptionally bullish.

Of course the standard seasonality caveat applies that these are mere tendencies, not primary drivers of gold or gold stocks. Seasonal tailwinds can be easily drowned out by bearish sentiment, technicals, and fundamentals. Seasonality doesn’t always work, especially when it doesn’t align with the primary drivers of sentiment, technicals, and fundamentals in that order. Thankfully that certainly isn’t the case this year.

The gold miners’ stocks aren’t entering their second-strongest month of the year overbought after a big rally. Quite the contrary, they have really underperformed year-to-date on excessive bearishness. This week the HUI was actually still down 6.0% so far in 2018, far behind gold’s modest 1.6% gain! Since gold-mining profits amplify gold price moves, gold-stock prices tend to leverage gold by 2x to 3x much of the time.

Thus spring rally aside the HUI should already be up 3.1% to 4.7% year-to-date, or trading between 198.3 to 201.4 compared to this week’s anomalously-low 180.8. That’s another 9.6% to 11.3% higher from here even if gold merely stays near $1325. The gold stocks are overdue to mean revert higher no matter what gold does! Gold’s spring rally will simply hasten and enlarge gold stocks’ long-delayed next upleg.

The farther gold rallies in May in one of its strongest spans of the year seasonally, the closer it will get to major breakouts and new highs. The higher gold climbs, the more attention it will get from the financial media, investors, and speculators. As their sentiment turns bullish again, capital will flood back into the beaten-down gold stocks. The gold miners’ coming surging earnings in their Q1 results are icing on the cake.

While investors and speculators alike can certainly play gold stocks’ coming spring rally with the major ETFs like GDX, the best gains by far will be won in individual gold stocks with superior fundamentals. Their upside will trounce the ETFs’, which are burdened by over-diversification and underperforming gold stocks. A carefully-handpicked portfolio of elite gold and silver miners will generate much-greater wealth creation.

At Zeal we’ve literally spent tens of thousands of hours researching individual gold stocks and markets, so we can better decide what to trade and when. As of the end of Q4, this has resulted in 983 stock trades recommended in real-time to our newsletter subscribers since 2001. Fighting the crowd to buy low and sell high is very profitable, as all these trades averaged stellar annualized realized gains of +20.2%!

The key to this success is staying informed and being contrarian. That means buying low before others figure it out, before undervalued gold stocks soar much higher. An easy way to keep abreast is through our acclaimed weekly and monthly newsletters. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. For only $12 per issue, you can learn to think, trade, and thrive like contrarians. Subscribe today, and get deployed in the great gold and silver stocks in our full trading books!

The bottom line is gold stocks experience a strong spring rally seasonally. This is driven by gold’s own seasonality, where outsized investment demand arises at certain times during the calendar year. Gold usually enjoys a strong spring rally likely driven by the universal optimism this season brings. And since gold drives gold miners’ profitability, their stock prices naturally follow it higher while amplifying its gains.

And gold stocks’ already-strong spring rally is likely to prove exceptional this year. Gold stocks have really lagged gold so far in 2018, despite fat earnings rapidly growing with higher gold prices. Once gold nears breakouts, traders are going to remember the gold miners and be amazed by their dirt-cheap stock prices wildly disconnected from fundamentals. They will flood back into this small sector catapulting it higher.

Adam Hamilton, CPA

April 27, 2018

Copyright 2000 – 2018 Zeal LLC (www.ZealLLC.com)

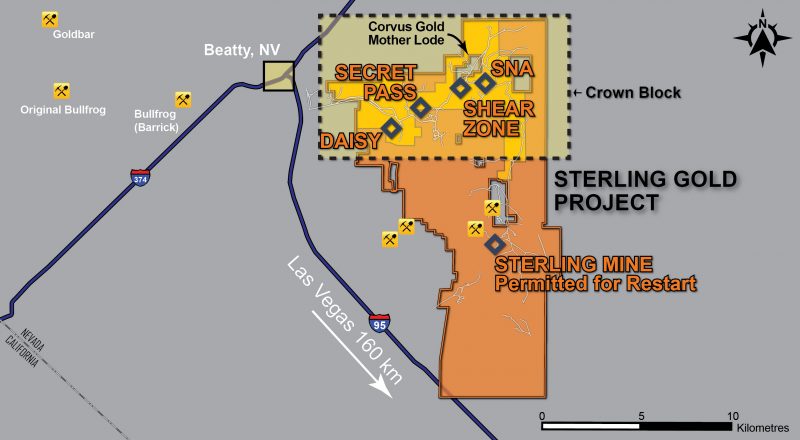

The Critical Investor profiles a miner that is ramping up its gold mine in Nevada on time and on budget.

Pan Mine, Nevada

1. Introduction

Fiore Gold Ltd. (F:TSX.V; FIOGF:OTCQB) has progressed its Pan Mine in Nevada, U.S. in a very steady fashion, on time and on budget. Exploration for additional resources (and hopefully years of mine life as well) has been successful so far, and a new COO has been hired. Recently, the latest financials regarding the first quarter of the new year were released, which are always an interesting reference of the state of a company, especially with producers. Therefore, it was time to have a closer look at Fiore Gold, Frank Giustra’s baby. Besides an update on proceedings, the other purpose of this article will be the outlining of future cash flow and valuation potential, as I view Fiore Gold as misunderstood by the markets at the moment.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. Pan Mine

The ramping up of the Pan Mine is progressing according to plan, and the company is actually ahead of schedule, as the production rate increased from the planned 10,000 tpd capacity to 14,000 tpd, which was supposed to happen much later. The highlights of the first quarter of fiscal year 2018 are according to the news release:

Revenues of $8.26 million from the sale of 6,467 gold ounces with a gross margin of $2.54 million or 31%.

Inventory of 11,335 estimated recoverable ounces placed on the leach pad at Pan as of December 31, 2017.

Working capital of $13.51 million as of December 31, 2017.

The first full quarter of steady-state production at the Pan Mine in Nevada.

Operating costs ($/ore ton) 6.2% below budget for the quarter.

Successful construction of the Phase II heap leach pad at the Pan Mine, adding an additional 2.2 million square feet of leach pad space. Approximately $5.3 million of capital expenditures for the Phase II expansion was treated as sustaining capital costs for the quarter, resulting in significantly higher All-In Sustaining Costs (AISC) for the current period.

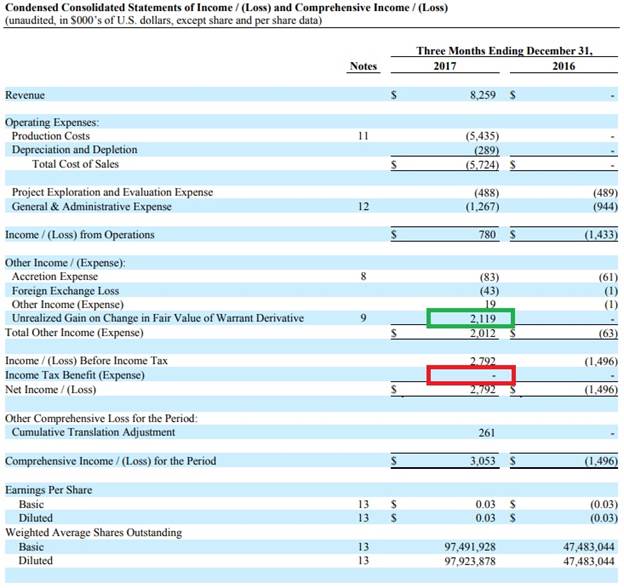

Let’s dig a little deeper into the financials here. In the first quarter of the current financial year, Fiore was surprisingly able to report a comprehensive income of $3.05M, or roughly 3 cents per share. However, this strong net profit was predominantly caused by an unrealized benefit from the fair value of the warrants (in green) and the lack of any tax payments (in red):

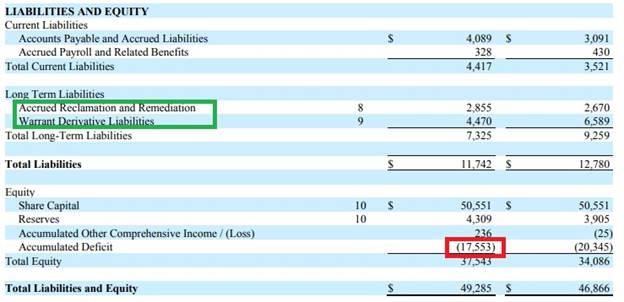

The tax holiday is into effect as the company has substantial carry forward losses (in red):

The operating income in the first quarter was $780,000. Fiore Gold is debt-free though, as the long-term liabilities (in green) aren’t long-term debt obligations.

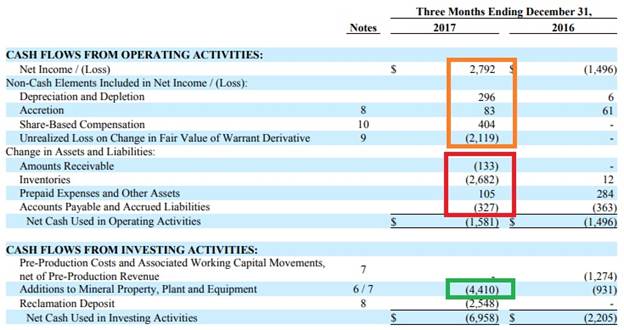

The cash flow statements indicate a ramping up producer as well. The operating cash flow (or OCF, before changes in Fiore’s working capital position, which is the most reliable figure for small producers, especially when ramping up, as OCF after changes can vary a lot in this case) was approximately $1.5M (OCF in orange, without changes in working capital in red, for an operating cash flow of approximately 225 dollar per ounce), and this wasn’t sufficient to cover the $4.4M in capital expenditures (in green):

However, there are two important remarks to make here.

First of all, Fiore Gold plans to produce 35,000-40,000 oz Au this year. Even if the lower end of this guidance is used, Fiore Gold will still have to produce about 35,000 – 6,467 = 28,500 oz Au in the next three quarters of its financial year. This equates to an average of 9,500 oz Au per quarter, or an increase of almost 50% compared to the Q1 production rate.

This means that if production increases, the economies of scale will start to have an effect and the operating margins will improve. Keep in mind that the quoted margin of $225/oz in the first quarter includes $1.267M in G&A expenses. The G&A cost per ounce was $195 in Q1, when this fixed cost could be spread out over 9,500 oz, it drops to $133/oz, which is a pretty substantial improvement. On top of that, the other relatively fixed expenses will also be divided over more ounces. So, the margins will increase as more gold is being produced.

Second, Fiore Gold has guided for a full year capex of $5.5M (red):

On a side note but an important one: comparing the 2018 forecast for gold ounces mined vs gold ounces produced shows a global recovery target of about 50%. However, the Feasibility Study provides a recovery of 72% for an operation with crushers and an agglomerator, and 60% for a run-of-mine operation. As Pan is a heap-leach operation ramping up production, it is never easy to start up heap leach mines, and recoveries often seem a matter of trial and error it seems before all issues are ironed out. The option to add a $14M crusher and agglomerator is a likely one but still uncertain, depending on the outcomes of ongoing test work. A decision on the C&A circuit will likely be made mid-2018, and a realistic timeline on eventual completion of this will be Q1 2019 according to management. At the last PDAC I met with CEO Tim Warman, and he had this to add:

“The idea was always there to use the crusher and the belt agglomerator, but it was such a close call that we decided this could be best tested in a production environment using available space on our newly constructed Phase II leach pad.”

As current working capital stands at $13.5M and the Pan mine is about to become free cash flow positive, the timing is perfect. Let’s continue with the budgeted $5.5M. A big part of this was spent in Q1 alone which means the earlier planned capital expenditures in the next few quarters will be substantially lower as well. Fiore Gold has started a drill program but the combination of higher operating cash flows (due to production increases and margin expansions) and a lower capex should ensure Fiore Gold reaches positive free cash flow.

The interesting thing is that Fiore’s operating costs are pretty much fixed which means the additional ounces will be high-margin ounces. Assuming a production increase of 3,000 ounces per quarter, the operating cash flow will very likely increase by $2.75-3.25M per quarter (assuming $1,300/oz Au, and no taxes will be due for the first few years as mentioned earlier) towards $4.25-4.75M per quarter. Besides this, keep in mind that gold stands at $1353/oz at the time of writing, which could add a further $0.5M per quarter. Furthermore, I’m also assuming the sustaining capex will reach an average of $1.5M per quarter; this should result in Fiore Gold generating approximately $2.75-3.25M per quarter in free cash flow until the taxes start to kick in. And on top of that, U.S. corporate taxes enjoyed a big haircut recently thanks to Trump, so this is beneficial for Fiore in the future. Production will probably improve according to guidance, resulting in an annualized $17-19M operating cash flow in H2, 2018. Using a $1350/oz gold price would result in an annualized $19-21M operating cash flow, which is huge for a small producer in Nevada with just a C$65M market cap. More on this later; let’s have a look at ongoing exploration.

3. Exploration

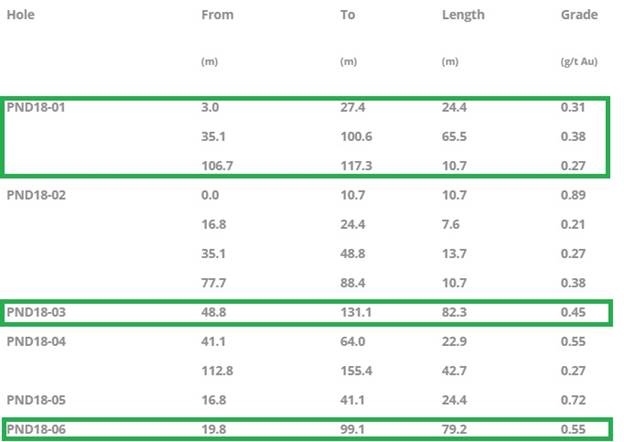

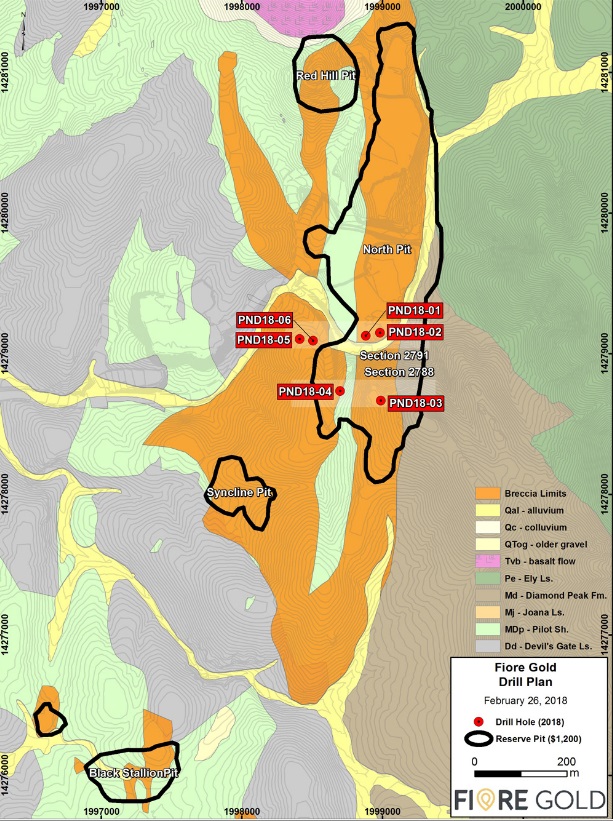

Besides production, Fiore Gold is also busy with exploration on every asset at this time. I will focus on the infill- and stepout drilling on Pan, as management is looking to extend the mine life substantially. The results of the first six holes were released a month ago, and delivered good intercepts, the best ones highlighted in green:

As a matter of fact, all holes returned economic mineralization as the mine cut-off grade is 0.14-0.21g/t Au, according to CEO Tim Warman:

“These first six holes show excellent potential to increase the resource and reserve base both at depth and laterally beyond the current mine plan boundaries. We’re extremely pleased with the success rate so far, with each of the first six holes encountering mineable widths of gold mineralization above the mine cut-off grade. This is a very good start to a program that we’re confident will allow us to extend operations at Pan well beyond the current mine life.”

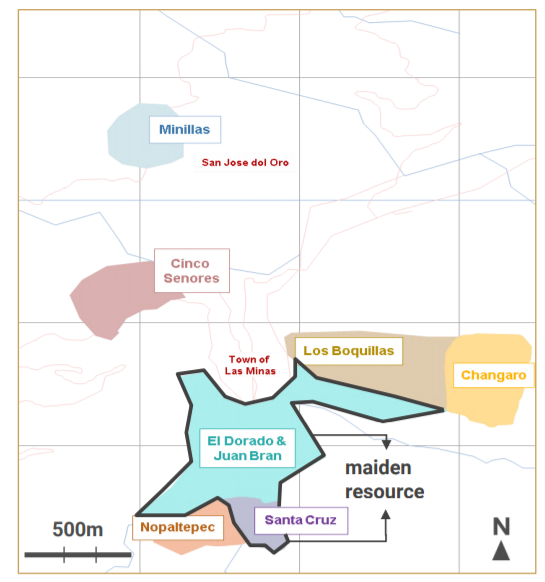

In order to get an idea of locations of drill collars here is a map representing them:

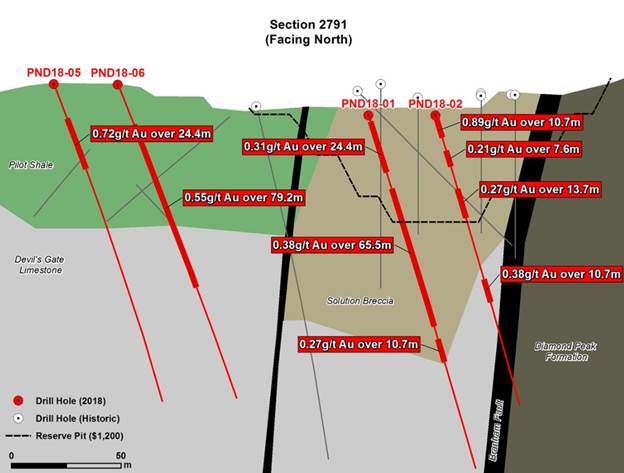

To get a good impression about the significance of these intercepts, let’s have a look at this section:

It will be clear that if Fiore manages to prove up sufficient mineralized tonnage below/west of the current pit outline between PND18-06 and PND18-01, a new and much deeper pit outline could be based on these intercepts and significantly expand mineable reserves/resources. In case ongoing drilling would generate the same kind of results for the entire southern part of the North pit, I wouldn’t rule out an increase of 100-150koz Au, which in turn would extend the life of mine (LOM) to eight to nine years from the current six years.

As the company returned some good intercepts on Pan recently, I felt it was time to ask CEO Tim Warman for some color on proceedings:

TCI: 13 holes were completed, and 6 assays reported so far. When can we expect the remaining 7 assays?

TW: We expect to have those in early April. Through the end of March, we have drilled about 10,000 feet (about 3,000 m), and we expect to do 15,000-20,000 ft RC and DD combined.

TCI: Hole 5 and 6 seem to have resulted in economic mineralization, but hole 3 as an extension at depth at relatively low grade seems unlikely to be economic considering the increased strip ratio?

TW: We think the mineralization of hole 3 isn’t too deep but this area needs more drilling for sure to define new resources.

TCI: Where exactly is further drilling targeted?

TW: Drilling in this first phase is targeting areas close to the North Pit, as well as some smaller future satellite pits in the central part of the deposit.

TCI: I see that RC drilling is used a lot in this round of drilling; don’t you have the risk of contamination with this method in this environment? I recall the same thing happening when Gustavson was working out the resource estimate for Pan in the not-too-distant past.

TW: There is always a bit of smearing with RC, but we understand the deposit a lot better now than in the Midway days. For this type of resource expansion, doing only DD is too expensive now, although we will be doing about 5,000 ft of diamond drilling in key areas.

TCI: Is the Gold Rock resource update planned for late 2018?

TW: We are still planning the program for Gold Rock; we like to fund this from incoming Pan cash flow and use the rig from Pan when drilling is finished there. This will probably be April or May after the snow is cleared.

TCI: Do you have new plans for the Chile asset and the Washington asset?

TW: We are still reviewing plans for the Chilean assets, although we just announced some good exploration results from Rio Loa. As for the Washington asset, we’re talking to a few people about it but it’s still in the early stages.

TCI: The Gold Rock FEIS (= EIA) has been submitted for review, and the Federal Record of Decision should be received before mid-year. What is the status nowadays?

TW: The Record of Decision wraps up the Federal permit, which is the one that takes the longest. The various state permits typically take six to eight months, but we won’t start applying for those until we’ve done a lot more engineering work, since they require fairly specific information.

TCI: Last question: what can you tell us about met work for Gold Rock so far?

TW: The recovery appears to be pretty good, actually a little better than at Pan, Gold Rock has a recovery of about 65-75%. And as you know we are looking at improving Pan recoveries by adding a crusher and an agglomerator.

This concludes the short interview with Tim Warman, which provided a solid update on exploration and related subjects. Now it’s time to take a look at ways how to value Fiore Gold.

4. Valuation

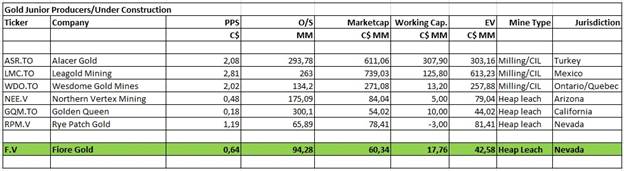

When Fiore Gold is compared to a few other junior gold producers (some data coming from Haywood’s weekly update the Weekly Dig) it can be seen that Fiore Gold is pro forma (as a ramping up producer) valued on EV/CF ratios comparable to the more adventurous jurisdictions like Turkey or Mexico:

And part II:

For the best jurisdictions in this list, Ontario/Quebec and Nevada, the EV/CF metric is substantially higher, and I don’t even consider the corresponding companies top notch although Rye Patch got acquired by Alio Gold very recently.

At a current market cap of about C$61M, it seems that Fiore Gold is valued only on the Pan NPV, when using my estimate from another article on the company:

the current exploration assets, of which I estimate El Peñon at C$1M and Cerro Tostado at C$4M

about C$7M in cash, zero debt

the Pan Mine with a C$65M NPV and ramping up production

the Gold Rock historical deposit and the exploration potential of both Pan and Gold Rock combined at C$20M

Golden Eagle at C$5M, bringing the total NAV at C$102M.

Obviously, Pan is discounted by investors, as it is still ramping up production and is looking at adding the crusher and agglomerator for better recoveries, and the market doesn’t appear to assign much value to the other assets. Especially Gold Rock could be capable to add a $80-100M NPV in a few years as it is a bigger and higher grade mineralized project in my view. Nevertheless, the valuation of a producer is usually much better represented by the market cap to operational cash flow ratio (which varies from about 8 to 12 (even 16 for very profitable mines) in good jurisdictions at current gold prices/sentiment), which can be narrowed down further to EV/CF.

When looking at this metric and using the operating cash flow estimates mentioned earlier in this article, the re-rating potential becomes clear. With a potential estimated OCF of $17-19M (= C$22-25M), the company would be valued at 2.0/2.8 times cash flow which is very cheap on EV/CF and P/CF metrics for a profitable Nevada gold play. When Fiore Gold starts generating quarterly cash flows as estimated, and coverage picks up, I am happy to stick with my forecast for a potential double. Increased resources should be able to add LOM years for Pan, and a solid resource on Gold Rock could likely further support a higher valuation.

5. Conclusion

Ramping up to 14,000 tpd steady state went almost flawless for Fiore Gold, as the company did save on operational costs, but didn’t reach its desired 60% run of mine recovery, as it expects to get to 50% for the full year 2018. Therefore, the option to add a crusher and an agglomerator is being evaluated at the moment, increasing recovery, hopefully in line with FS levels. When this staged development would be completed, Fiore Gold will likely boast an annualized cash flow of about C$22-25M, which in turn deserves a much higher share price based on producer average multiples. It is a stock that demands more patience than others, but in the current positive gold environment investors could very well be nicely rewarded in the not-too-distant future.

Pan Mine; scenery

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

Disclaimer:

The author is not a registered investment advisor. The author holds a long position in this stock. Fiore Gold is a sponsoring company. All facts are to be checked by the reader. For more information go to fioregold.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long term commodity pricing/market sentiments, and often looking for long term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

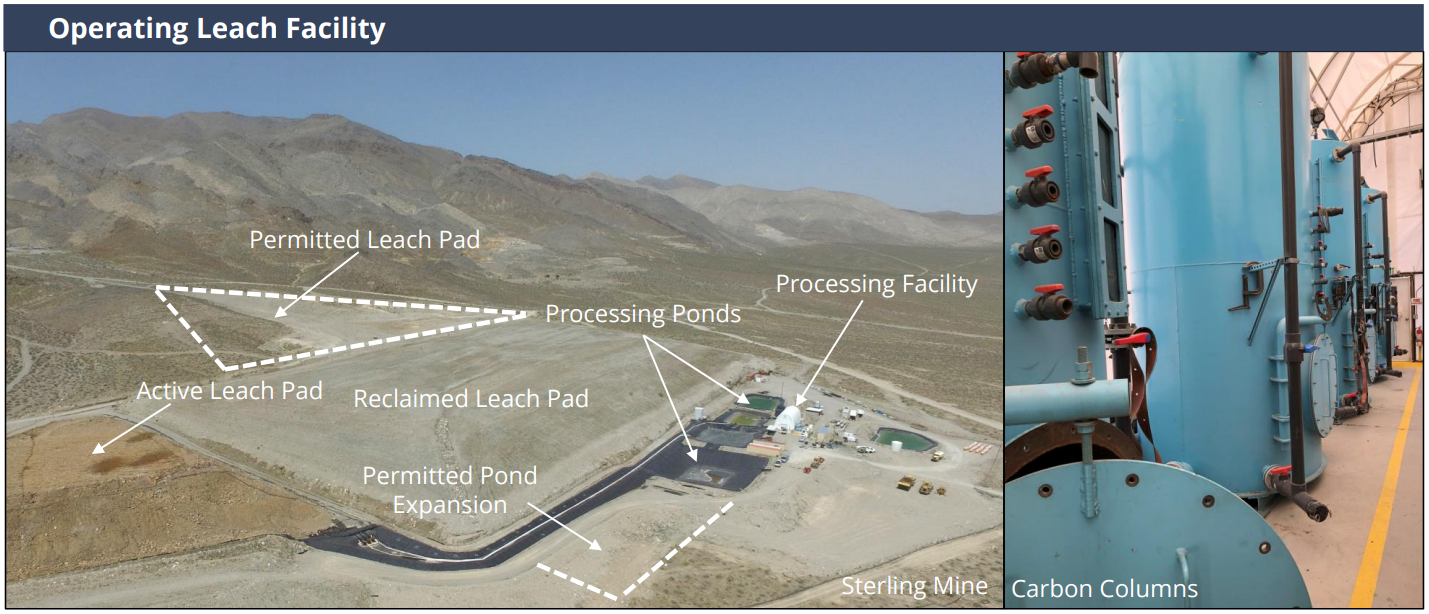

Heap leaching has become a popular method of extracting gold, writes mining consultant Nicolaas C. Steenkamp and Leon Louw, writer, editor and specialist in African affairs and mining.

Heap leaching is used to extract gold, copper, silver, uranium, and iodine. This method was first employed to extract copper at the Bluebird mine in the US in the early 1960s, and then by several gold mines in the western parts of the US a few years later. Since then, heap leaching has been adopted successfully by many mines across the world.

Heap leaching occurs after the mining and crushing of low-grade ores, usually in an opencast mine. High-grade ores and ores not amenable to cyanide leaching at coarse particle sizes require further processing to recover the gold values. These processing methods can include further grinding, concentration, pressure oxidation, and roasting, which is used to treat these ores to expose the gold particles prior to cyanidation.

The crushed ore undergoes an agglomeration stage, after which the agglomerated ore is deposited onto the heap leach pad. The heaped ore is irrigated with a lixiviant (a liquid medium) to dissolve the metals and generate the leachate. The lixiviant will depend on the target metal being extracted.

The pad is compacted and then lined with a high-density polyethylene membrane, which prevents toxic compounds and elements (such as cyanide and the leachate solution) from entering the groundwater system.

The leachate is collected in a pond or tank, and it is referred to as a pregnant or value-bearing solution. The solution is then processed to recover the metals. In gold operations, recovery is affected through carbon adsorption or the Merrill-Crowe process. The barren solution, together with additional lixiviant, is recycled back to the heap.

Heap leaching can take anything from a couple of months to several years. In the case of gold recovery, heap leaching generally requires 60 to 90 days to leach the ore, compared to the 24 hours required by a conventional agitated leach process. Gold recovery is also usually only 70% compared with 90% recovery in an agitated leach plant. Other metals, such as copper, use solvent extraction and electrowinning to extract the target metal from the solution.

According to Phil Bundo, process engineering director at Senet, mines need large reserves, a large resource, and significant real estate if they want to employ the heap leach method. “To build a big heap and accommodate all the associated equipment, a large space is required; and to fill that space, a mine needs to produce enough ore,” says Bundo. Bundo adds that climatic conditions like rain can negatively affect a heap leach operation, although this would not ordinarily be enough cause to discard heap leaching as a processing method. Resources and reserves play a much bigger role in determining whether heap leaching will be viable.

Heap leaching is not that popular in South Africa because it is more applicable to shallow opencast mining, and South African gold mines are mostly underground operations. The method is, however, being used on a large scale in the copper mines of South America and, according to Bundo, it will be used more and more on the African continent in future.

Weighing up the alternatives

According to Bundo, there are other recovery methods, besides heap leaching, to consider when mining gold. These include gravity concentration, carbon in pulp (CIP), and carbon in leach (CIL). “The methodology selected is a function of the mineralogy of the ore. If the gold is associated with oxides, for example, it can be amenable to heap leaching. The grade also plays a key role. Heap leaching is used for low-grade oxides, while high-grade ore (with or without oxides) is better suited to CIP or CIL methods,” says Bundo.

Bundo explains that while heap leaching is not as costly as CIL or CIP, the recovery achieved is also not as efficient. “CIP and CIL are costlier in terms of initial capital and operational costs, but they provide the benefit of high recovery,” says Bundo. In cases where the oxides are amenable to heap leaching and cannot economically justify the construction of a CIL or CIP plant, then the operations start off with heap leaching to generate sufficient capital to finance the CIP or CIL circuits when mining more refractory ore.

“It is also important to remember that if the gold is associated with sulphides or other minerals, heap leaching cannot be effectively employed as recoveries are generally low. In such cases, it is advisable to install a CIP or CIL system from the beginning,” says Bundo.

The higher capital and operational investment in methods such as CIP and CIL are due to the more aggressive techniques used to recover the gold. A CIP process will, for example, involve crushing, milling, and agitator tanks. Heap leaching requires less aggressive techniques: a chemical solution is simply sprayed on heap ore. As the solution percolates through the heaped ore, it dissolves the gold. The solution is then collected and treated further by adsorption.

The heap leach stack must be porous enough to allow the solution to drip or to drain through the stack. There are potential recovery failures due to the inability to obtain the optimal flow solution. High clay content is achieved by agglomeration prior to stacking the piles.

Further research is underway to both increase the recovery of metals and reduce the risks of the solutions used and generated during the process. Heap leaching has the potential of extending the life of mine or bringing mines under care-and-maintenance back into production by reprocessing the tailing or fine-residue dumps.

Agglomerating the ore

Part of the preparation stage is known as agglomeration, in which an agglomeration drum is used. Although heap leaching is efficient on its own, its efficiency is greatly improved by adding an agglomeration drum. Agglomeration drums are also called ore drums, agglomerators, and heap leaching drums. Agglomeration is based on a rotary drum design that tumbles ore fines, in the presence of the leachate, through its interior to promote uniformity and to mix the leachate and fines. The agglomeration step happens after the ore is crushed, but before it is heaped.

Using an agglomeration drum to agglomerate the ore fines will ensure that the crushed ore particles are more uniform, making it easier for the leaching solution to travel through the channels between the particles to help maximise recovery (increased percolation). In addition, adding the agglomeration drum allows the leaching solution to mix with the ore fines. As the ore fines are agglomerated, the solution is sprayed throughout the drum and mixed thoroughly with the ore fines, which ultimately makes the process more efficient.

“The agglomeration drum is the start of the heap leach stacking process, which ends at the leaching pad,” says Theo Winterbach, mechanical and materials handling manager at Senet. From the agglomeration drum, the material is transferred via an intricate conveyor system to the heap leach pad. “The heap leach pad covers a large area and the product has to reach the entire pad. The system thus requires multiple conveyors to transfer the material to the furthest point of the pad,” says Winterbach. The agglomerate should be transferred as smoothly as possible, as it is important to keep it intact. One benefit of having multiple and mobile equipment is that a company will not have to lay out all the capital in the beginning. Once the team has decided where the pad will be located, they can acquire only the necessary equipment until production starts ramping up. “The added advantage is that the mobile equipment allows for a certain amount of flexibility; therefore, the entire system can be moved to ensure that the conveyors feed the stacker at the end of the chain,” says Winterbach. A typical heap is between eight and 10 metres high. The normal flow of material is from the agglomeration drum to the grasshoppers and then to the linear index conveyor, which delivers it to the stacker machine.

Stacking the heap

The linear index and stacker machine need to move backwards as the stockpile is stacked in preparation for the leaching. At times (depending on the size of the heap leach pad), the entire set of machines has to be fully retracted and repositioned to a new position on the heap leach pad before the process is repeated. When the entire system needs to be adjusted, front-end loaders or other applicable equipment can be used to move the equipment, as most of the equipment, including the stacker, is wheel or track driven. A combination of wheels and tracks is used to minimise the bearing pressure on the pad.

The stacker can slew and move backwards and forwards in a linear fashion. Heap leach pads require special preparation in construction. According to Bundo, a pad should slope by one or two degrees so that the solution can gravitate to the pond, and there should be sufficient aggregates underlying the surface. Moreover, the high-density polyurethane (HDPE) liners that cover the surface are critical to prevent the chemical solution from seeping into the groundwater. Special collection pipes are installed underneath the pad to direct the solution to the relevant ponds.

Pros and cons

For Breton Scott, managing director of Bowline Professional Services, the most important advantage of heap leaching is that it lowers the capital and operating expenses relative to other traditional methods like flotation, agitation, and vat leaching, especially where low-grade ores and tailings are present. It also has a potentially rapid payback period.

“Heap leaching further eliminates some environmental concerns and restraints. The main benefit, in terms of the environmental impact, is that it requires less energy and water,” says Scott. Moreover, the method has uncomplicated design and equipment requirements, and the construction phase is a lot faster than other treatment methods.

Although Scott says that the heap leach method is not seriously affected by climate, he mentions that a lower efficiency has been noted at low temperatures. “High rainfall areas may also dilute the solution, requiring additional monitoring,” he says.

The risks associated with heap leaching are mainly related to environmental concerns, should the pad construction process not be done correctly from the design stage. Potential issues with the regional water balance are highlighted as a risk, along with the possible exposure of the solutions used to the surrounding areas. Heap leaching does, however, have a much lower potential of acid mine drainage. The costs associated with pollution control and closure efforts are one of the main continual expenses in such operations.

“The drilling of water-monitoring boreholes and regular testing of the groundwater by an accredited water-quality laboratory would be required if the heap leach method is used,” says water laboratory analyst, Ben Steyn. “Tests would generally include pH, dissolved solids, and heavy metals.”

“The biggest question a mine needs to ask itself is whether it has an ore body that is amenable to heap leaching. Senet prefers to get involved in a project from the test work phase, which enables us to prove that heap leaching, as a processing method, will work for the project. We not only consider heap leaching, but also all the other options available. It is always a trade-off between the capital investment and recovery,” Bundo concludes.

About Leon Louw:

Leon specializes in African affairs and doing business in Africa, and has been writing about mining in Africa for 8 years. He was born in Johannesburg, South Africa, and has traveled Africa extensively, especially southern Africa. He has a BA degree with a specialization in African studies and an honours degree in Africa Politics. He also have a national diploma in Nature Conservation and an honours degree in Environmental Management. It is is passion to promote business in Africa and I can assist companies that are interested in doing business in African countries.

The thrill of victory and the agony of defeat. Gold investors focused on the Western markets and government debt fear trade tend to feel the same kinds of thrills and agony that professional athletes regularly experience.

Here’s a good example: For a few days, silver soars higher on what appears to be the guaranteed start of a long-term uptrend. Within days or just hours, the gains are suddenly gone, and the price appears to be going much lower with absolute certainty.

Please click here now. Double-click to enlarge this positive-looking gold chart.

Bullion banks around the world arguably have the most effect on gold price discovery and they focus on physical supply versus demand.

Given that India’s gold-focused Akha Teej festival ended April 18, and Chinese jewellery demand is slightly soft (with dealer interest at $1320 – $1300), it’s clear that gold is not quite ready to surge above $1370 and begin a new era of sustained trading above $1400.

Also, some Fed speakers have hinted that the pace of Fed rate hikes could be slower than expected. At first glance, that would seem to be positive for gold, but fear trade price discovery is about how rates affect risk.

In the current environment, modest rate hikes support a “risk-on” theme. For a closer look at what I mean, please click here now. Double-click to enlarge this US dollar versus yen chart.

Bank FOREX traders view the dollar as risk-on and the yen and gold as risk-off, and rightly so. Given the beyond-insane financial state of the government, aggressive rate hikes from the Fed put the government at serious risk of being able to finance itself.In that situation, the dollar falls against the yen and gold.

In the immediate time frame, money managers believe that Powell will hike rates very gradually. That incentivizes money managers to take risk and invest in the dollar, because it will pay a higher rate of interest without putting too much pressure on the government’s ability to make its principal and interest payments on its debt.

Gold peaked in February as Chinese New Year buying peaked. Now it’s made another modest peak as Akha Teej buying peaks, with Western money managers believing that the Fed cares about the US government’s debt problems. These money managers also believe the Fed cares about the stock market.

Under Greenspan, Bernanke, and Yellen, the Fed cared. I don’t believe Powell cares what the ramifications of his actions are for the “spendaholic” government or for the Wall Street vampires that require low rate policy for their stock market buyback programs.

Please click here now. Double-click to enlarge this key bond market chart.

This chart tells me that the Fed is going to become vastly more aggressive with rate hikes and inflation is going much higher. The current price and time zone is the calm before that storm.

I expected Trump to launch tariffs, and he’s done that. Most investors are focused on whether the tariffs are good or bad for growth, rather than on the fact that they are inflationary.

Please click here now. I didn’t predict the sanctions that have been applied to Russia by the US government, although I’m not really surprised.

That’s because most of what all governments do involves the insane use of sticks much more than the sane use of carrots. Regardless, sanctions are here and they are inflationary. I view sanctions as nothing more than aggressive tariffs.

More are coming as governments (especially the US government) seek new sources of revenue to pay their debts as inflation and rates rise.

Please click here now. Double-click to enlarge this GDX chart.

While many fear traders involved with gold stocks are nervous today, I don’t see anything to be concerned about. I suggested GDX would make a short-term peak at about $23.25 as Akha Teej demand peaked with the Fed in between rate hikes.

It’s done that and investors who have insured their “bull era ride” with GDX put options in that $23 area are now looking very good indeed. Some of these options rose 15% just in yesterday’s trading. The bottom line: Insurance works, whether it is home, auto, or price insurance for gold stocks.

Please click here now. I have two short term scenarios for GDX. The first involves the current pullback ending in the $22 area, and the second one shown here has the pullback end at around $21. Put options enthusiasts and those carrying a short position in GDX against their portfolio of individual miners could cover off half the puts at around $22 and the rest near $21.

As with gold and silver bullion, I have no concerns at all about the current price action in gold stocks. Most have staged huge rallies recently and many are above their February highs. A pullback is normal and expected as major Chindian festival demand peaks at a time when the Fed is in between major policy action.

Chindian income growth versus limited mine supply is the main driver of higher gold prices for the long term. There are no “upside breakouts” in that process. It’s ongoing and relentless. The inflationary policies of the debt-plagued US government and the Fed’s increasingly aggressive QT and rate hikes in response to that will generate significant institutional interest in gold stocks as gold trades above $1400.

All the fundamentals are in place to create significant inflation and debt financing problems for the West. They are also in place to create significant income growth in the East for a long period of time. The only thing that astute investors need to build sustained and significant wealth in the coming gold bull era is a very modest amount of patience and rational thought. It’s the greatest time in history to be invested in the precious metals asset class, and getting greater by the day!

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

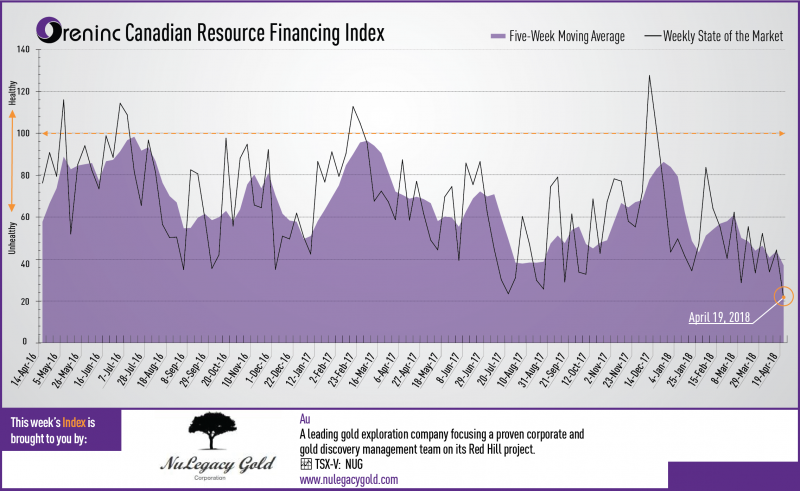

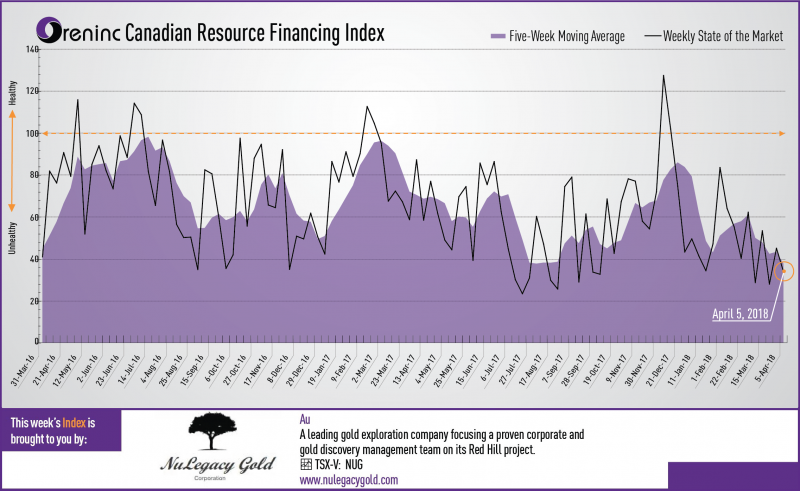

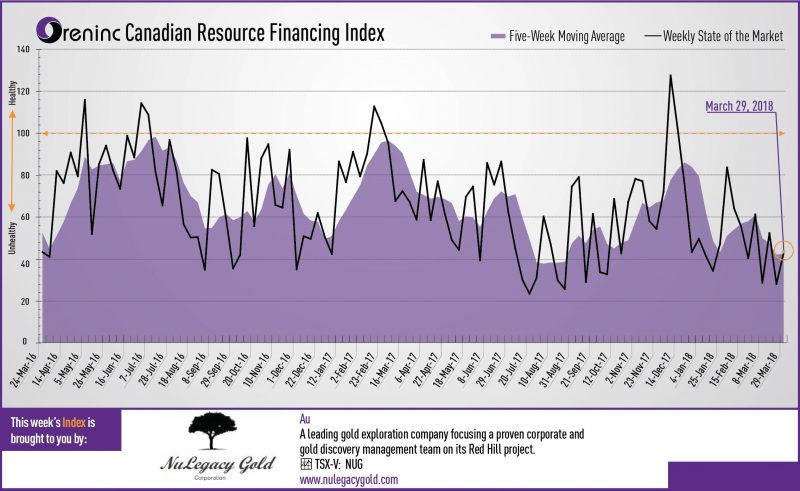

Last week index score: 44.24 (updated)

This week: 21.62

Prospero Silver (TSX-V: PSL) announced a non-brokered private placement to raise up to C$1.0 million through the issuance of up to 11.1 million units @ C$0.09.

The Oreninc Mining Deal Club sent out its sixth financing alert to its subscribers. Sign up today to get the details and an opportunity to participate: www.miningdealclub.com

The Oreninc Index halved in the week ending April 20th, 2018 to 21.62 from an updated 44.24 a week ago as broker action evaporated (again).

US tariffs and sanctions against steel and aluminium imports, particularly from Russia, are ripping through various metal markets with aluminium and nickel prices spiking. Aluminium prices have spiked 30% since the start of April to a seven-year high due to sanctions against Rusal. Fears that supplies of steel-additive nickel could come into Trump’s crosshairs if more sanctions against Russian businesses and businessmen are rolled out has seen its price spike on the London Metals Exchange, recording its highest one-day move since 2008 and hitting three-year highs.

On to the money: total fund raises announced tumbled to a paltry C$22.6 million, a six-week low, which included no brokered financings and no bought deal financings. The average offer size dropped to a barely visible C$1.1 million, a six-week low. The few financings announced and bringing with them a general return to the full warrant to attract interest.

Another week of failed expectations for gold as strong performance throughout the week fell at the end as the US dollar index strengthened following news that US initial weekly jobless claims dropped to 232,000, its lowest level in three weeks according to the Labor Department.

Gold closed down at US$1,336/oz from US$1,346/oz a week with a mid-week high of US$1,349/oz. Gold is now up 2.58% this year. Meanwhile, the US dollar index had a stronger week and closed up at 90.31 from 89.80 a week ago. The van Eck managed GDXJ saw early week gains dissipate at the close to finish the week exactly where it started at US$33.49 despite a mid-week high of US$34.06 last week. The index is down 1.88% so far in 2018. The US Global Go Gold ETF also saw strong growth but gave up less as the week ended to close up at US$13.04 from US$12.81 a week ago with a mid-week high of US$13.11. It is up 0.23% so far in 2018. The HUI Arca Gold BUGS Index closed down at 184.18 from 184.43 last week. The SPDR GLD ETF saw a week of consolidation as its inventory remains at 865.89 tonnes.

In other commodities, silver put in a growth spurt and despite losing some shine at the end of the week closed up at US$17.11/oz from US$16.65/oz a week ago wit ha mid-week high of US$17.24/oz. Coppers price growth continues and closed up at US$3.15/lb from US$3.07/lb from US$3.05/lb last week. Oil continues to post gains to close up at US$68.40 a barrel from US$67.39 a barrel a week ago. This puts its price back to levels levels last seen in December 2014. Despite US president Donald Trump saying the oil price is getting too high, it looks set to go higher as OPEC and Russia look to maintain supply restraint, even though surplus oil has largely been worked out of the system.

The Dow Jones Industrial Average closed up at 24,462 from 24,360 last week with a mid-week high of 24,786. Likewise, Canada’s S&P/TSX Composite Index grew to 15,484 from 15,273 the previous week. The S&P/TSX Venture Composite Index also closed up at 804.96 from 795.94 last week.

Summary:

Number of financings decreased to 20, a two-week low.

No brokered financings were announced this week, a two-week low.

No bought-deal financing was announced this week, a two-week low.

Total dollars tumbled to C$22.6m, a six-week low.

Average offer size also fell to C$1.1m, a six-week low.

Financing Highlights

EnGold Mines (TSX-V: EGM) opened a C$3.5 million offering on best efforts basis.

10.0 million flow-through units @ C$0.30 and 2.0 million non-flow-through units @ C$0.26 with Canaccord Genuity as agent.

Each flow-through unit consists of one share and one warrant exercisable @ C$0.40 for two years. Each common unit consists of one share and one warrant exercisable @ C$0.35 for two years.

Over-allotment option of up 1.5 million flow-through units and 300k common units on the same terms.

Gross proceeds will be used to continue exploration at the Lac La Hache copper, gold & silver property in the Cariboo region of BC, Canada.

Major Financing Openings:

Engold Mines (TSX-V: EGM) opened a C$7.04 million offering on a best efforts basis. Each unit includes a warrant that expires in 24 months. The deal is expected to close on or about May 14th.

Vela Minerals (TSX-V: VLA) opened a C$2.5 million offering on a best efforts basis.

Renaissance Gold (TSX-V: REN) opened a C$2.5 million offering on a best efforts basis. Each unit includes a warrant that expires in 60 months.

Coronet Metals (TSX-V: CRF) opened a C$2.02 million offering on a best efforts basis. Each unit includes a warrant that expires in 24 months.

Major Financing Closings:

North American Nickel (TSX-V: NAN) closed a C$15 million offering on a best efforts basis. Each unit included half a warrant that expires in 24 months.

Sama Resources (TSX-V: SME) closed a C$5.25 million offering on a strategic deal basis. Each unit included a warrant that expires in 24 months.

Rise Gold (CSE: RISE) closed a C$3.52 million offering on a best efforts basis. Each unit included a warrant that expires in 36 months.

Toachi Mining (TSX-V: TIM) closed a C$3 million offering on a best efforts basis.

Company News

Prospero Silver (TSX-V: PSL) announced a non-brokered private placement to raise up to C$1.0 million through the issuance of up to 11.1 million units @ C$0.09.

Each unit will consist of one share and half of a warrant exercisable @ C$0.16 for two years.

The net proceeds will be used for general working capital purposes, its generative exploration programs and exploration expenditures on its property portfolio in Mexico.

Looking to drill 6,000m in 2018.

Analysis

With the initial phase of its strategic arrangement with Fortuna Silver drawing to a close, and 2018 exploration planning underway, Prospero is raising cash to be able to contribute to funding ongoing and future exploration work under the arrangement. However, given the current low stock price, it is evident that the company is also looking to minimize shareholder dilution by undertaking a minimum raise. 2018 work will look to continue to validate Prospero’s exploration strategy to discover blind epithermal systems.

About Oreinc.com:

Oreninc.com is North America’s leading provider of relevant financing information in the junior commodities space. Since 2011, the company has been keeping track of financings in the junior mining as well as oil and gas space. Logging all relevant deal and company information into its proprietary database, called the Oreninc Deal Log, Oreninc quickly became the go-to website in the mining financing space for investors, analysts, fund managers and company executives alike.

The Oreninc Deal Log keeps track of over 1,400 companies, bringing transparency to an otherwise impenetrable jungle of information. The goal is to increase the visibility of transactions and to show financings activity in a digestible format. Through its daily logging activities, Oreninc is in a position to pinpoint momentum changes in the markets, identify which commodities are trending and which projects are currently receiving funding.

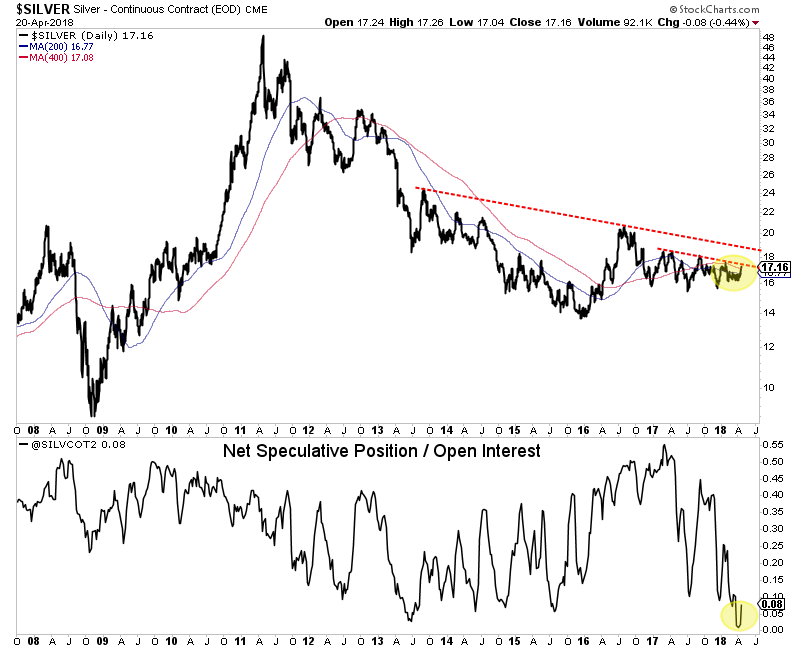

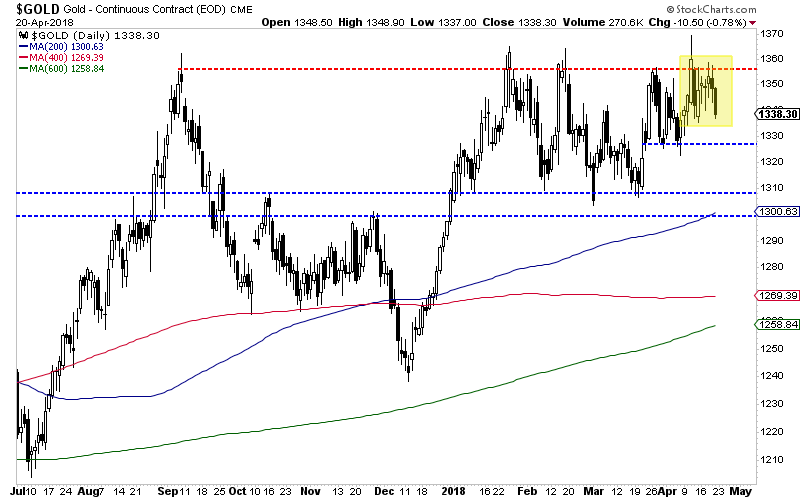

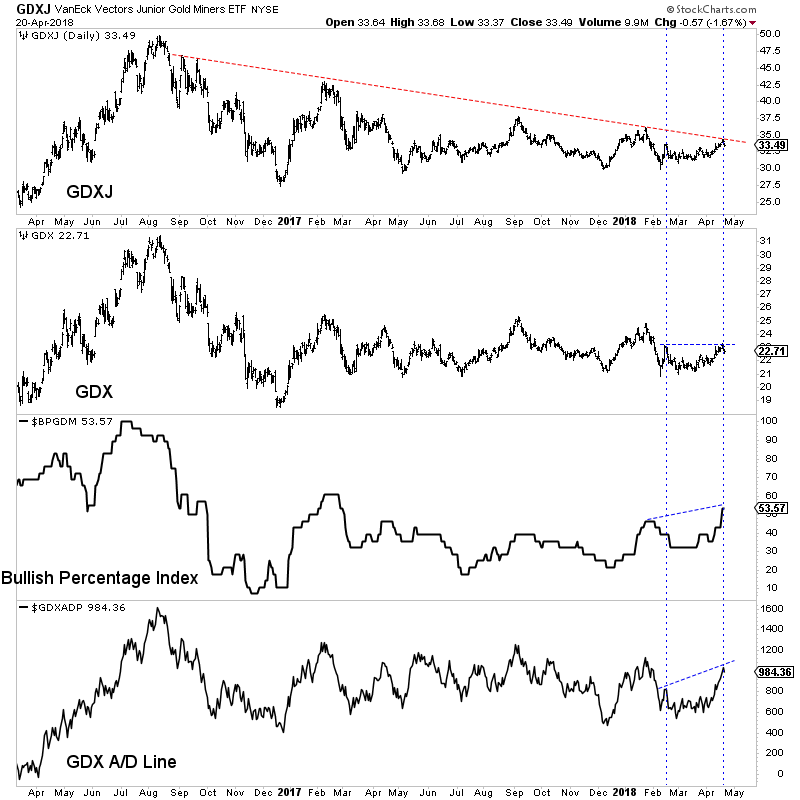

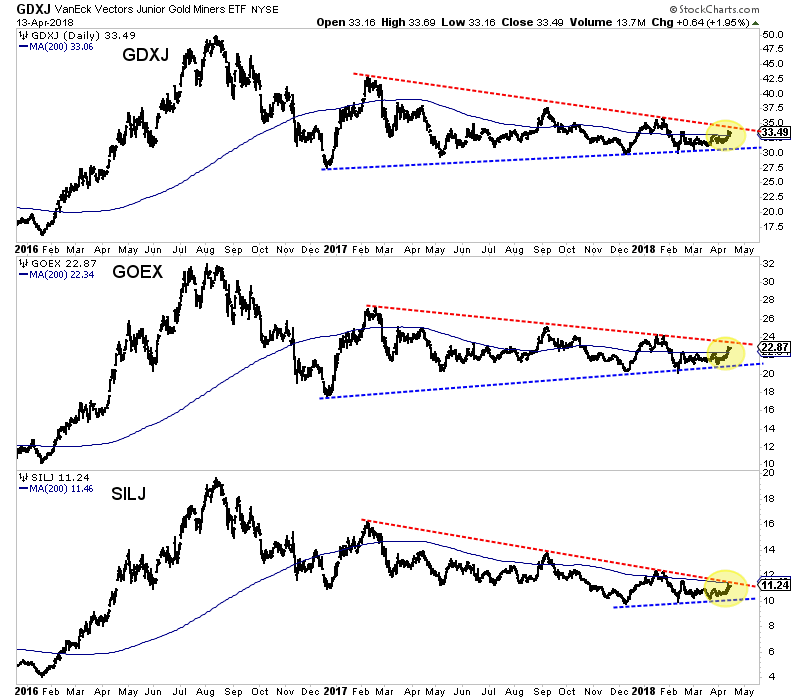

It was an interesting week in the precious metals complex. There appeared to be the start of a short squeeze in Silver (hedge funds were heavily short) but it ceased at an important resistance. Meanwhile, Gold closed the week on a weak note, losing $1340-$1350. The gold stocks, like silver closed the week below technical resistance. The price action in the complex continues to suggest that a breakout in Gold is the key to unleashing strong outperformance from Silver and the gold stocks.

While Silver has very supportive sentiment, it has not broken out from its downtrend yet. The net speculative position was at 1.1% a few weeks ago, an all time low. That won’t spring Silver by itself unless Silver can surpass critical resistance in the mid $18s. And that may not happen until Gold breaks $1360-$1370. Silver has strong support in the low to mid $16s.

Silver & Silver Net Speculative Position

Moving to Gold, the daily chart below shows Gold losing $1340-$1350 after rejection again at $1360. Immediate support for Gold lies at $1325 which if broken would lead to a test of $1300-$1310 and the 200-day moving average.

Gold Daily Candles

We have a few observations to share with respect to the gold stocks. First, GDXJ has pulled back from trendline resistance around $34. Second, breadth indicators for GDX such as the advance decline line (A/D) and the bullish percentage index (BPI) are showing a positive divergence. The BPI has reached a 52-week high while the A/D line is not far from its January peak when GDX nearly hit $25. So while GDX has been relatively weak, its internals are showing more strength.

Silver and the gold stocks have yet to break important resistance as Gold once again was turned back at major resistance. If the US Dollar, which closed at 90.07, rallies up to its 200-day moving average at 92, Gold would likely test $1300-$1310. Should Silver and the gold stocks hold up well in that scenario (which could be suggested by current breadth) then it would imply a good rebound from the sector back to resistance points. Lower prices in the juniors would be a welcome sign and another opportunity to accumulate ahead of a major breakout in the not too distant future. In anticipation of that breakout, we have been accumulating the juniors with 300% to 500% upside potential over the next 18-24 months. To follow our guidance and learn our favorite juniors, consider learning more about our premium service.

Gold remains largely forgotten, off the radars of most investors. But that’s likely to change soon as this leading alternative investment is nearing a major bull breakout. Once gold climbs to decisive new bull-market highs, sentiment will turn and investors’ interest will surge. Their resulting buying will rapidly drive gold higher, attracting in more capital inflows. Gold is only a couple modest up days away from that key breakout.

Universally in all markets, traders’ psychology is completely dependent on price action and levels. When prices are high and rising, speculators and investors alike eagerly buy in. They love chasing winners, so buying begets buying. This creates powerful self-reinforcing virtuous circles, with rising prices helping to entice in ever-more traders. In recent years this dynamic catapulted the market-darling FANG stocks higher.

With capital inflows following performance, investments that aren’t high and rallying naturally see waning popularity. That’s the story of gold over the past couple years or so. Gold’s last new bull-market high came way back in early July 2016, when it hit $1365. That was 21.3 months ago, which may as well be an eternity in terms of sentiment. In most traders’ minds, gold has effectively been dead and buried ever since.

While contrarian investors always follow gold, most mainstream investors don’t. They only get interested when gold is powering up to major new highs. This psychology holds true everywhere in the markets, it’s certainly not unique to gold. A handful of mega-cap tech stocks have soared since Trump’s election win in November 2016, but other mega-cap tech stocks have lagged far behind. Traders always pursue performance.

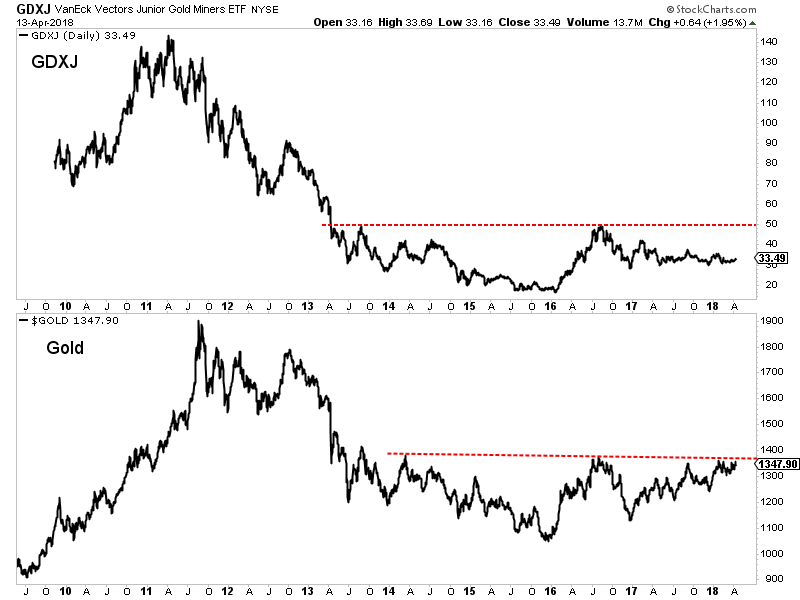

This first chart looks at gold’s technical price action over the past couple years or so. A mighty new bull market erupted out of deep despair, blasting higher with steep gains. But the gold-investment-driving force behind it soon reversed, so this young bull stalled out. Gold hasn’t been able to best those initial bull highs ever since. So with no new highs to spark excitement, gold has slipped off investors’ radars.

Gold prices are heavily influenced by gold-futures speculators. The extreme leverage inherent in futures trading enables these traders to punch way above their weight in bullying the gold price around. There is nothing these guys fear more than Fed rate hikes, even though history proves that’s absolutely irrational. So heading into the Fed’s first hike of this cycle in December 2015, gold slumped to ugly 6.1-year secular lows.

But such extreme bearishness made no sense, as gold has thrived in past Fed-rate-hike cycles. So once that initial rate hike came and gold didn’t plunge, speculators rushed to buy back in to gold futures after that $1051 low. They were soon joined by investors with their huge pools of capital. They were spooked by the first stock-market corrections in 3.6 years, which boost gold demand to diversify stock-heavy portfolios.

Thus gold soared 29.9% higher in just 6.7 months in essentially the first half of 2016, easily crossing that classic +20% new-bull-market threshold. Gold’s $1365 bull peak in early July 2016 was closely tied to stock-market fortunes, coming the very day before the flagship US S&P 500 stock index achieved its first new record close in 13.7 months. With stock markets off to the races again, gold investment demand waned.

Gold had been very overbought after such a blistering rally, and speculators had record long positions in gold futures which is a contrarian indicator. But gold still consolidated high in the summer of 2016 until it was hit by two anomalous events. First gold-futures stops were run as gold fell below $1300, driving a sharp drop to its 200-day moving average. Gold recovered quickly from that until Trump’s surprise win.

Very few traders expected Trump to stage a colossal underdog upset and win the presidential election in early November 2016. It was an extreme contrarian position, seen as madness. Interestingly as I wrote the very weekend before that voting, a powerful stock-market indicator predicted Trump would indeed win! That soon came to pass, shocking speculators and investors into greatly reevaluating their outlooks.

With Republicans soon to control the presidency and both chambers of Congress, traders’ euphoria flared to eye-searing brilliance. They were captivated by hopes for big tax cuts soon, and rushed to buy stocks with reckless abandon. As the stock markets surged first on Trumphoria and later taxphoria, gold fell deeply out of favor. Investors abandoned it since they felt no need to prudently diversify their soaring portfolios.

Thus a normal healthy gold correction after a strong upleg cascaded into a 17.3% plunge over 5.3 months ending in December 2016. Such sharp losses naturally devastated gold psychology among traders. The bull market was still alive and well technically, as gold didn’t cross that -20% new-bear trigger. But gold was still left for dead as the levitating stock markets sucked in most capital. Traders had largely moved on.

But gold still looked really bullish in mid-December 2016, as I explained within days of that correction low. Investors were radically underinvested in gold after fleeing in the election’s wake. And the truly incredible psychology unleashed by the Republican sweep wasn’t sustainable or repeatable. It’s pretty rare where nearly everyone gets presidential and congressional elections so wrong! So gold was overdue for some buying.

Ever since that post-election anomaly it has indeed powered higher on balance in the solid uptrend you can see in this chart above. Gold has been relentlessly carving a series of higher lows and higher highs, which made for a 20.4% upleg over the next 13.3 months. That’s actually big enough to qualify as a new bull market, but again gold never entered a bear. Such strong price action should’ve improved sentiment.

But it really didn’t. The extreme taxphoria last year made 2017 one of the most-extraordinary years on record for the US stock markets. The S&P 500 ceaselessly levitated to a massive 19.4% gain in the first year of the Trump Administration, accompanied by record-low volatility. With big US stocks powering higher so dramatically and painlessly, who needed gold? It tends to rally when stock markets are selling off.

While contrarians were rightfully impressed with gold’s strong bull-market uptrend since those anomalous post-election lows, mainstream investors didn’t know or care. Everything was rainbows and unicorns for them, despite dangerous bubble valuations in the stock markets. While gold’s 13.2% rally in 2017 would command attention normally, the 35% to 57% gains in the FANG stocks overshadowed it and stole the limelight.

There’s no doubt over a year of gold seeing higher lows and higher highs is very-bullish price action. All students of the markets would recognize this viewing gold charts. But climbing support and resistance lines are lost on the financial media and mainstream investors. Investments only start garnering talk and mindshare when major new highs are hit. Popular psychology is totally dependent on that one technical aspect.