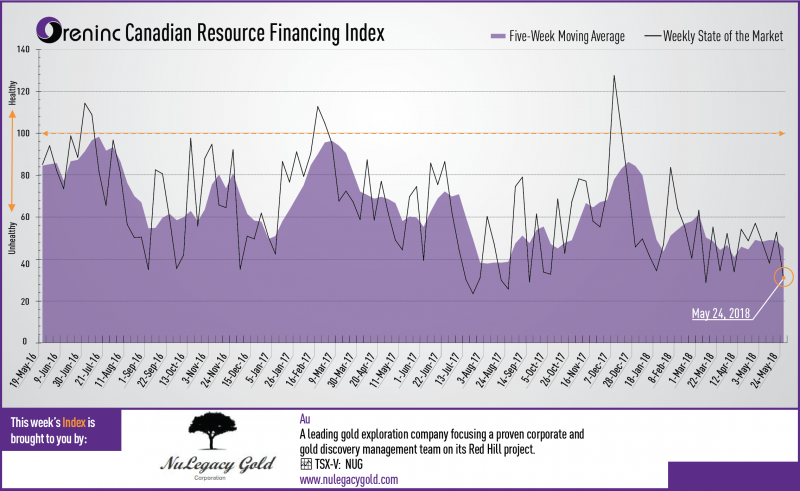

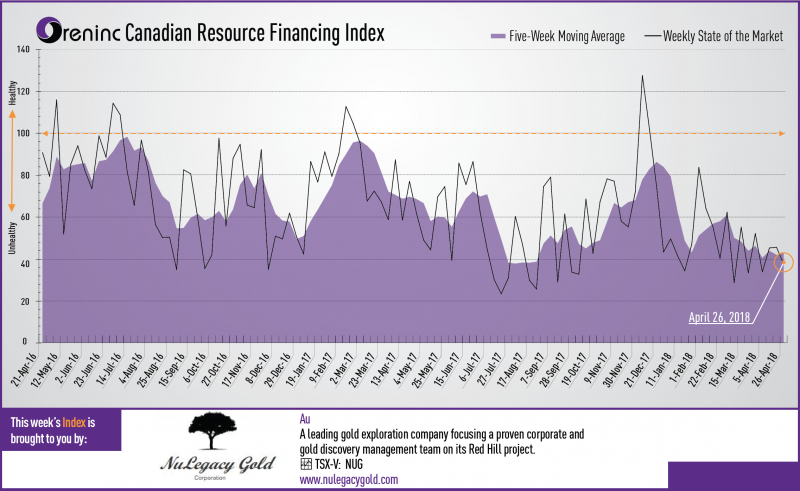

The Oreninc Index fell in the week ending May 25th, 2018 to 30.90 from 52.74 a week ago despite gold recovering from the prior weeks’ fall below US$1,300/oz.

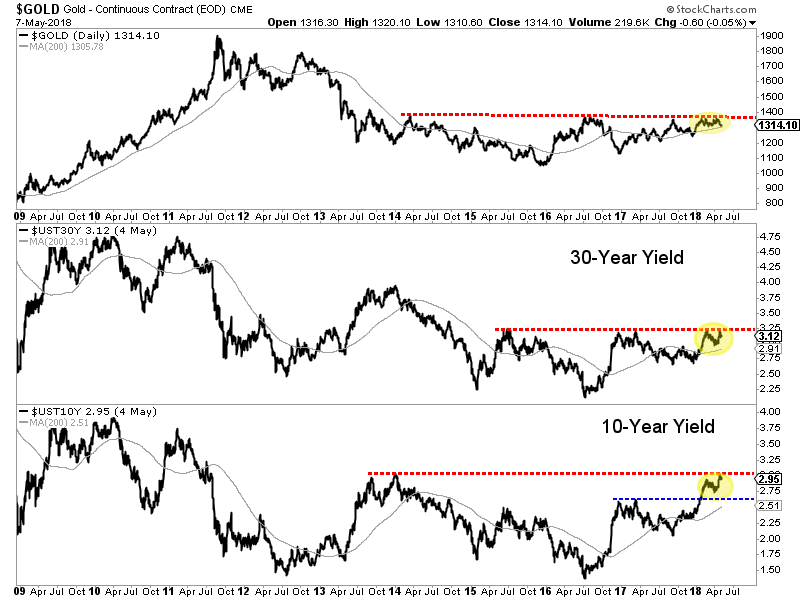

Gold recovered from a brief sojourn below the US$1,300/oz level as risk returned with US president Donald Trump calling off a landmark summit with North Korean leader Kim Jong Un. The yield on the US ten-year treasury fell below 3% as suggestions from the US Federal Reserve about a temporary rise in inflation raised questions over whether there will be multiple interest rate increases this year. All good news for gold. All eyes will be on the US Federal Reserve Open Market Committee meeting on June 12-13.

On to the money: total fund raises announced fell to C$38.8 million, an eleven-week low, which included two brokered financings for C$10.8 million, a two-week low and one bought deal financing for C$7.0 million, a two-week low. The average offer size fell to C$2.9 million, a three-week low and the number of financings fell to 13, an eleven-week low.

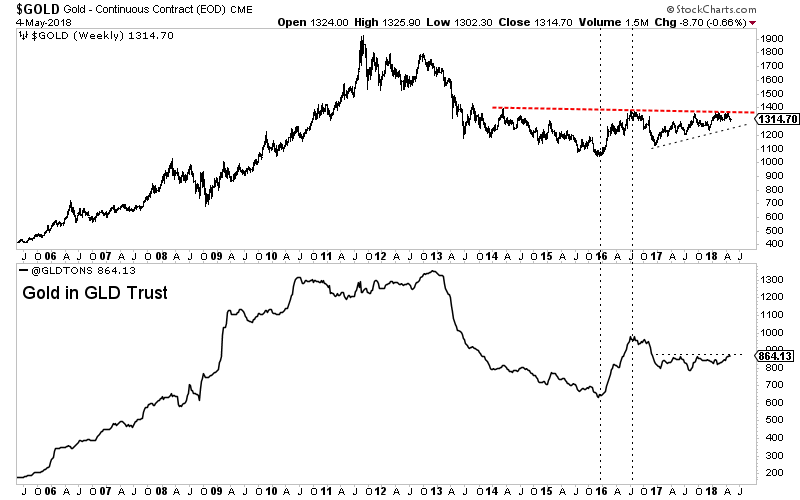

Gold closed at US$1,309/oz from US$1,293/oz a week ago. Gold is now down 0.04% this year. The US dollar index continued to increase and closed up at 94.25 from 93.63 a week ago. The Van Eck managed GDXJ made a slight gain after a volatile week closing up at US$32.89 from US$32.84 last week. The index is down 3.63% so far in 2018. The US Global Go Gold ETF fell slightly to close at US$12.93 from US$12.98 a week ago. It is now down 0.61% so far in 2018. The HUI Arca Gold BUGS Index closed up at 180.20 from 177.75 last week. The SPDR GLD ETF continued to sell off and closed its inventory at 848.50 tonnes from 855.28 tonnes a week ago.

In other commodities, silver made a small gain on a volatile week to close up at US$16.51/oz from US$16.44/oz a week ago. Copper showed a similar pattern to close up at US$3.07/lb from US$3.06/lb last week. Oil was the main loser of the week with its price taking a dump at the end of the week to close down at US$67.88 a barrel from US$71.28 a barrel a week ago.

The Dow Jones Industrial Average returned to growth to close up at 24,753 from 24,715 last week. Canada’s S&P/TSX Composite Index showed a slight loss to close down at 16,075 from 16,162 the previous week. The S&P/TSX Venture Composite Index also closed down at 775.41 from 786.39 last week.

Summary:

Number of financings crumbled to 13, an eleven-week low.

Two brokered financings were announced this week for C$10.8m, a two-week low.

One bought-deal financing was announced this week for C$7.0m, a two-week low.

Total dollars plunged to C$38.8m, an eleven-week low.

Average offer size dropped to C$2.9m, a three-week low.

Financing Highlights

Probe Metals (TSX-V: PRB) opened a C$14 million financing.

Bought deal with Sprott Capital Partners and a syndicate of underwriters

Flow through units @ C$1.90 and non flow-through units @ C$1.15

Each unit consists of one share and half a warrant exerciseable @ C$1.45 for two years.

Underwriters option to purchase C$2.1 million in units.

Gross proceeds will fund exploration on Probe’s projects in Québec.

Closing is expected on June 19th.

Major Financing Openings:

Great Bear Resources (TSX-V: GBR) opened a C$7.83 million offering on a best efforts basis. Each unit includes half a warrant that expires in 24 months.

Probe Metals (TSX-V: PRB) opened a C$7 million offering underwritten by a syndicate led by Sprott Capital Partners on a bought deal basis. Each unit includes half a warrant that expires in 24 months. The deal is expected to close on or about June 19th.

Probe Metals (TSX-V: PRB) opened a C$7 million offering on a best efforts basis. The deal is expected to close on or about June 19th.

Para Resources (TSX-V: PBR) opened a C$6.4 million offering on a best efforts basis. Each unit includes a warrant that expires in 36 months.

Major Financing Closings:

SRG Graphite (TSX-V: SRG) closed a C$8 million offering underwritten by a syndicate led by National Bank Financial on a best efforts basis. Each unit included a warrant that expires in 12 months.

Wealth Minerals (TSX-V: WML) closed a C$6.25 million offering on a best efforts basis. Each unit included half a warrant that expires in 24 months.

Zinc One Resources (TSX-V: Z) closed a C$3.89 million offering on a best efforts basis. Each unit included half a warrant that expires in 36 months.

Alexandra Capital (TSX-V: AXC) closed a C$2.6 million offering on a best efforts basis.

About Oreinc.com:

Oreninc.com is North America’s leading provider of relevant financing information in the junior commodities space. Since 2011, the company has been keeping track of financings in the junior mining as well as oil and gas space. Logging all relevant deal and company information into its proprietary database, called the Oreninc Deal Log, Oreninc quickly became the go-to website in the mining financing space for investors, analysts, fund managers and company executives alike.

The Oreninc Deal Log keeps track of over 1,400 companies, bringing transparency to an otherwise impenetrable jungle of information. The goal is to increase the visibility of transactions and to show financings activity in a digestible format. Through its daily logging activities, Oreninc is in a position to pinpoint momentum changes in the markets, identify which commodities are trending and which projects are currently receiving funding.

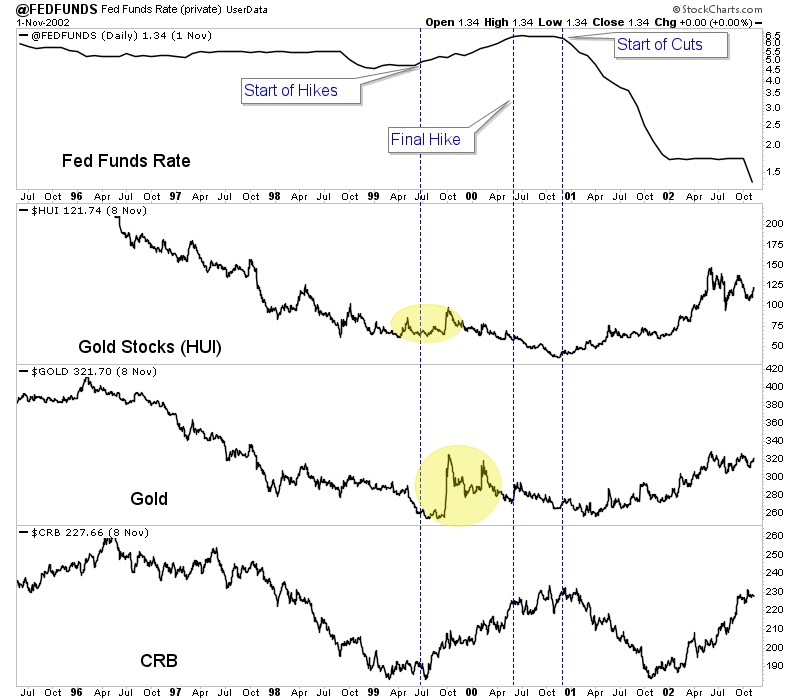

Despite the insistence of some, precious metals have not been in a bull market. After a big pop at the start of 2016, the sector has trended lower. Sure, Gold has traded up towards a major breakout but Silver and the gold stocks have trended lower. When the US Dollar corrected significantly, the stock market outperformed precious metals. Does that sound like a Gold bull market to you? The moribund performance has left us wondering what could turn the tide. A quick study of Fed history with the context of current conditions is very instructive as to when Gold could begin a true bull market.

Fundamentally speaking, we know that Gold performs best when real rates are declining or will soon begin declining. That usually entails either accelerating inflation (surpassing the increase in nominal rates) or falling rates amid stable inflation. At this juncture we are leaning towards the latter as the eventual catalyst for Gold.

We were curious how Fed policy and policy changes impacted precious metals so we decided to plot the Fed Funds rate (above) along with gold stocks (middle) and Gold (bottom). We used the gold stocks (Barron’s Gold Mining Index) because they have a longer history than Gold. The vertical lines in blue mark lows in the BGMI that coincided with peaks in the Fed Funds rate (FFR) while the vertical lines in red mark lows in the BGMI that coincided with a bottom in the FFR.

Fed Funds Rate, Gold Stocks & Gold

Outside of the highly inflationary 1970s, the best bull markets in gold stocks began around the time the Fed Funds rate peaked (or in other words when the Fed ended its rate hikes). Lows in 1993, 1999 and 2016 coincided with the start of a new hiking cycle. However, unlike the lows in 1972 and 1976, inflation did not accelerate enough to drive more than a rebound.

Does that signal that gold stocks (and precious metals at large) need an end to the rate hikes?

The period from 1999 to 2001 is very instructive as there are several similarities between 1999-2000 and 2016-2017.

Like 1999, 2016 followed a nasty bear market in Gold and hard assets.

Also, the 1999 bottom in precious metals and commodities occurred around the time the Fed began a new cycle of rate hikes. Sound familiar to 2016?

As the Fed continued to hike into 2000, Gold and gold stocks trailed off but commodities were able to make higher highs until the very end of 2000. Commodities have not been quite as strong this time but they have outperformed precious metals which have trailed off since the initial rebound.

Gold and gold stocks ultimately bottomed and began spectacular rebounds around the time the Fed moved from a pause in rate hikes to rate cuts at the very start of 2001.

Unless there is an acceleration in inflation, the turning point for precious metals figures to be around the time the Fed ends its rate hikes. That would likely coincide with Gold regaining outperformance against the stock market, which we have noted as Gold’s missing link (from an intermarket perspective). Weakness in the economy and stock market would lead to an end to the rate hikes and then rate cuts. That would be the time Gold and gold stocks begin a major move higher. In the meantime we continue to focus on and accumulate the juniors that have 300% to 500% return potential. To follow our guidance and learn our favorite juniors for the balance of 2018, consider learning more about our service.

The next Fed rate hike is only about two weeks away, and another ramp-up in monthly quantitative tightening is scheduled for the end of June.

Investors are generally quite positive about the economy, but they don’t have much cash to invest. Most citizens of the Western world have meagre savings, a lot of debt, and inflation threatens to make matters worse for them. A lot worse.

Please click here now. With each passing month, more institutional money managers and influential analysts voice major concerns about inflation being the catalyst that ends the US equities bull market.

Please click here now. Double-click to enlarge. The Dow has gone nowhere since Powell became Fed chair, and I expect it to go nowhere throughout his tenure. That’s the best-case scenario. I shouldn’t mention the worst-case, because almost nobody believes that the Dow can crash in inflationary inferno. That’s not only the worst-case scenario, it’s by far the most likely one.

Investors could buy very light positions in the buy zone I’ve highlighted on this Dow chart, and sell them in my sell zone, but sand in the bull market hourglass is running out fast. It’s really a trade for gamblers. Serious investors need to be lightening up here. In my US stock market portfolios, I’m at about 30% cash, and it’s rising.

Central bank tightening is a global theme and barely out of the starting gate. It’s happening against the background of rising US government debt, corporate debt, citizen debt, and inflationary tax cuts.

Citizens and governments are generally euphoric, as they were in 2007, 1999, and 1929. The difference between now and previous peaks in euphoria is that the average citizen doesn’t have much cash to spend this time. It’s gone.

Please click here now. Double-click to enlarge. Since oil made its low in 2016, energy and tech stocks have received significant mainstream media attention.

Oil is in a danger zone now. At a bare minimum, a supposedly healthy correction is overdue. Trump wants oil lower and federal election campaigning has started in India. Indian currency and bond markets are being ravaged by high oil prices and global central bank tightening. Modi just flew to Russia and met with Putin. His meeting marked the top in oil.

I think the sell-off in oil could become more significant than most investors are prepared for, but once it’s over the arrival of significant global inflation will drive oil towards $200 a barrel.

By this time next year, gold should be challenging the $1500 area, and perhaps trading as high as $1650 – $1750. On that note, please click here now. Luis Oganes is an institutional heavyweight. He’s on the inside. When he speaks, gold bugs need to drop what they are doing and pay attention. He’s not only predicting gold will be at $1700 next year, but has the potential to surpass that juicy target price!

Few investors realize that the major mining stocks that I hold in my www.gudividends.comportfolio are up an average of 150% from that 2016 oil market low. They have blown away technology and energy stocks, and left the global stock market indexes even further behind.

Most importantly, as inflation transitions from an institutional investor concern to an outright wrecking ball, I expect this fabulous performance of the giant base metal miners to continue, with gold and silver miners shooting past all market sectors to become the ultimate market darlings.

Please click here now. Double-click to enlarge. The dollar is again in freefall against the yen, and that suggests the dollar will soon be taken to the woodshed by gold.

Investing champions like Ray Dalio are working hard to make investors understand that gold is not simply a fear trade hedge. Instead, it is the ultimate portfolio returns enhancer in good times as well as bad.

Having said that, as inflation becomes a massive theme in 2019, investors can give gold any label they want. That won’t matter. What matters is that institutional money managers will be buying it with both hands…and with three if they had an extra hand!

Please click here now. Double-click to enlarge. There’s nothing more glorious than a great gold price rally, and a big one is getting underway now.

Note the technical perfection being showcased by the “queen of assets” on this short-term chart. A symmetrical inverse head and shoulders bottom breakout was followed by a picture-perfect pullback to the neckline, and now, as I predicted, the queen of assets is following the yen and beating on the dollar like King Kong beating on a tin can.

My next target is $1327, and I think gold can now reach up and touch that price with very little effort. It’s a great place for short term profit booking and it should happen ahead of the key June 13 Fed meet. After that pause and likely right shoulder low, gold should blast through $1375, and make a medium-term beeline towards $1450.

Please click here now. China just launched an important physical metals trading platform yesterday. Attention all silver bugs: Trading begins with base metals, but will quickly expand to include… silver bullion!

I’ve referred to a future dominated by China and India being the gold and silver “bull era”. A key part of that thesis involves COMEX price discovery for gold and silver becoming vastly more related to physical demand versus physical supply.

Price discovery has been dominated in the past by Western hedge funds gambling on gold-irrelevant nonsense from “Fed speakers” and “gold doesn’t pay interest” mainstream media propaganda. Bull era price discovery is already happening with gold, and silver is next on deck. Investors can write that down and take it to the bank. The silver bullion bank!

Please click here now. Double-click to enlarge this superb GDX chart. Many of the component stocks are in roaring uptrends. GDX itself has been coiling sideways since mid-April in a bullish drift. That should be resolved with a significant rally that stuns most analysts with its intensity.

The financial system and QE-oriented gold fear trade is alive but on the back burner. There’s a new generation of gold bugs in the Western gold community who understand that inflation is coming and will be here to stay. The love trade and the inflation trade will form the backbone of the bull era. Eager investors around the world who know this is true are now aggressively accumulating portfolios of gold stocks, in preparation for decades of upside fun!

Thanks!

Cheers

St

Stewart Thomson

Graceland Updates

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

Over the last month, I’ve received numerous questions pertaining to the direction of the gold price. The fact is, I don’t have a crystal ball and, while I believe we will see higher gold prices in the future, I have no idea when, and really, I don’t care.

Why? Simply, I don’t invest in junior mining companies because I believe the price of gold is going to go up. I believe you invest in junior mining companies because you see value creation via discovery, or you see a clear path in the development of a project into a future mine.

There are many ways to make money in the junior resource sector, but for me, it’s a process which is linked to finding quality – the best people, who pick the best projects and execute well thought-out plans to achieve a specific goal.

In particular, discovery pays in any part of the market cycle and, therefore, while the risks associated with exploration are HUGE, I think it’s prudent to invest in the highest quality gold exploration companies the market has to offer.

Today, I would like to bring your attention to Klondike Gold Corp., a gold exploration company that is cashed up and ready to execute a 5000m drill program in the heart of the Yukon.

Let’s take a look!

Klondike Gold Corp. (KG: TSXV)

MCap – $24 million (at the time of writing)

Shares – 95 million

Fully Diluted – 120 million

Cash – $7 million

Ownership:

Frank Giustra – 14%

Eric Sprott – 13%

Key Investors – 10%

Insiders – 11%

NOTE: As you can see from the ownership breakdown, Klondike is tightly held by a small number of hands. Specifically, Canadian billionaires, Frank Giustra and Eric Sprott, who collectively control almost a third of the company’s outstanding shares and, I think, speaks to the upside potential that is seen in Klondike Gold and its district sized land package in the heart of the Yukon.

Klondike Gold’s Leadership

Klondike Gold Corp. is led by CEO, Peter Tallman, who is a geologist by trade and has over 35 years of experience in the mining industry.

During a conversation with Tallman, he related his start in the mining sector back to when he was in his early teens and helped build a log cabin just south of Algonquin Park, located in central Ontario. The key to this experience didn’t have anything to do with building or geology, but was important because Tallman became an avid and skilled canoeist, which would later be a key component in him attaining his first geology job outside of university.

After completing his geology degree at the University of Western Ontario, Tallman’s first job was with Selco (later BP-Selco), where he was hired to prospect for diamonds in northern Ontario. A key prerequisite for this job was proficient canoeing skills, which Tallman had in spades, and so he got his start in the mining business. Additionally, with Selco, he moved to Newfoundland where, while working in a remote corner of the province, chipped the discovery outcrop of what later became the Hope Brook gold mine.

Tallman has worked for a number of different companies in senior roles, over the course of his career, including Noranda Exploration, Prime Equities International (Murray Pezim), and Messina Minerals, just to name a few. Each of these experiences over the course of the last 35+ years has prepared Tallman well for leading Klondike Gold in their mission to discover an economic gold deposit in the Klondike.

The Klondike team is rounded out by CFO, Jessica Van Den Akker, and Board of Director members, Gordon Keep (CEO of Fiore Management & Advisory Corp.), John Pallot, Steve Brunelle and Tara Christie. The team has recently expanded the team with the addition of Ian Perry, VP Exploration who has extensive experience managing advanced exploration projects towards development stage.

Yukon

As the company name suggests, Klondike Gold is focused on gold exploration in Canada’s Yukon Territory. For those who may not be familiar with Canada’s geography, the Yukon is located north of British Columbia and it shares its western border with Alaska.

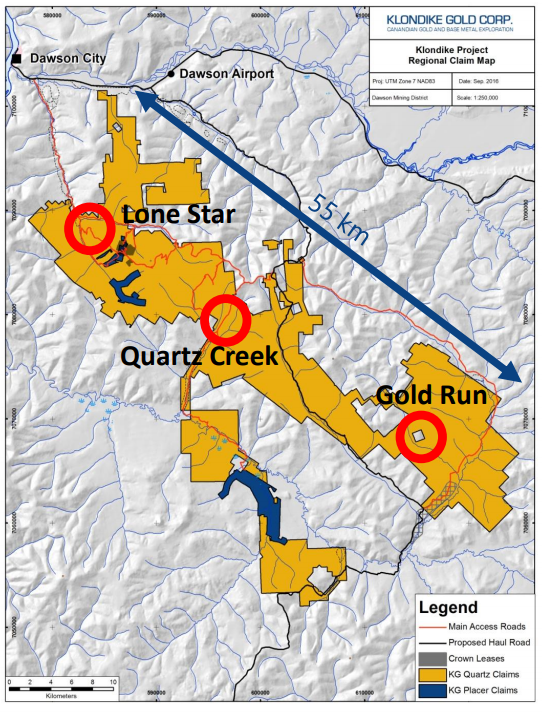

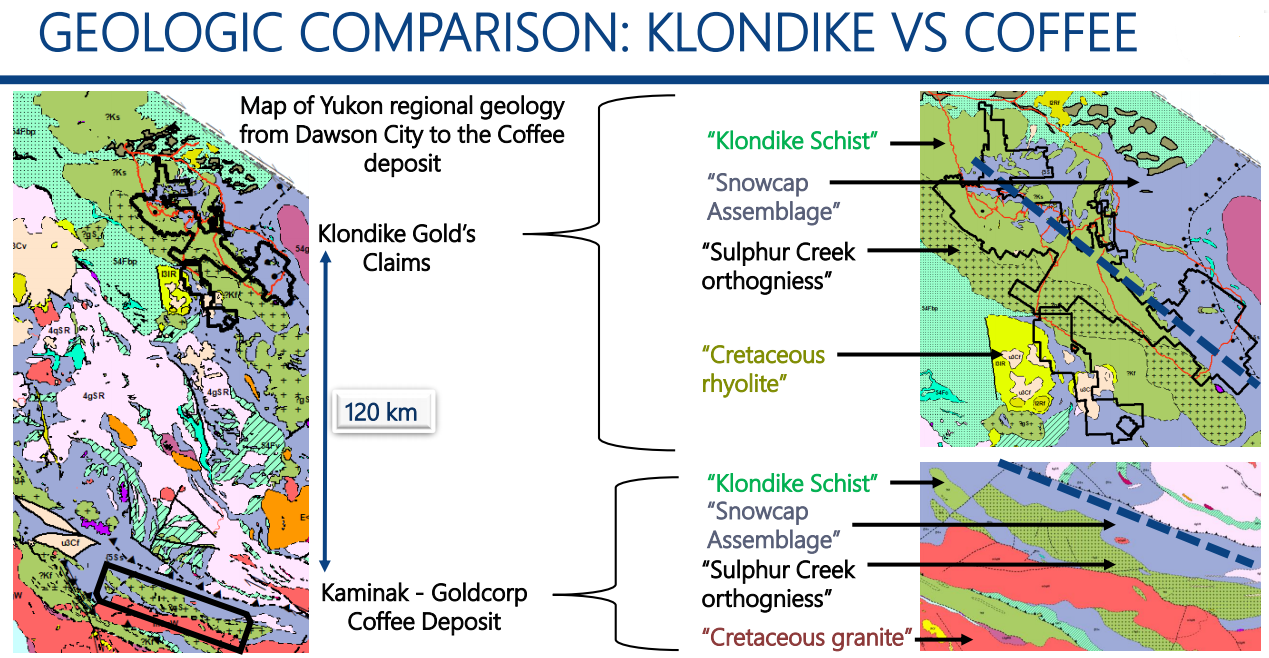

Klondike Gold Regional Claim Map

Klondike Gold owns 100% of its 2,942 contiguous claims, totaling 557 square kilometers, which sit in close proximity to Dawson City. Dawson City was built to support gold miners during the Klondike Gold Rush of the 1890s and hosts the major infrastructure needed for the exploration and development of mining projects, such as an airport, access to supplies and electrical infrastructure.

13th in the World for Mining Investment Attractiveness – Fraser Institute Ranking

The Yukon is a premier jurisdiction for mining and attained a score of 79.67, or 13th in the world, for mining investment attractiveness, according to the Fraser Institute’s 2018 rankings. The Fraser Institute uses a number of criteria in evaluating a jurisdiction, such as political stability, mining law, taxation and, arguably the most important, mineral potential.

The Yukon has well developed infrastructure, including more than 4,800km of all-weather roads, airports, power, Internet and cell phone service. Additionally, for companies that require international export of their concentrates, deep sea ocean ports are accessible across the Yukon’s western border in Alaska.

Yukon Mining Alliance

Uniquely, to my knowledge, many of the junior and major mining companies with projects in the Yukon have formed the Yukon Mining Alliance (YMA) with the Yukon Provincial Government and the Canadian Northern Economic Development Agency.

The YMA’s mandate is to,

“promote Yukon’s competitive advantages as a top mineral investment jurisdiction and its member companies and their Yukon-based project.” ~ YMA

In my opinion, this is a huge advantage of investing in companies with projects in the Yukon, as clearly, the marketing and promotion of mining within the Territory’s borders is a major priority. Bottom line, narrative plays a big role in the success of junior mining companies, and with the added help of the YMA, Yukon-based companies have a distinct advantage working together to promote the Yukon mining jurisdiction narrative.

Personally, I have seen the YMA presence at a couple of the top mining conferences in Canada, such as PDAC and Cambridge’s Vancouver Resource Investment Conference (VRIC). The YMA is putting the Yukon on the map for interested resource investors which, I believe, will pay off in spades as we move into the next leg of the bull market.

Klondike Gold Rush

The Klondike Gold Rush began in August of 1896, as three prospectors, George Carmack, Jim Mason and Dawson Charlie, discovered gold in what they referred to as “Rabbit” Creek, or what is now referred to as Bonanza Creek. With the discovery and the rush to stake their claim, word quickly spread of their discovery, and so spurred a historic gold rush in Canada’s Yukon Territory and the United States’ Alaska.

It’s estimated that the Klondike Gold Rush attracted 100,000 people from all walks of life, testing their luck against the odds to find their fortune. Many of the new American prospectors found their way north via ships boarded in Seattle. Former ports, such as Dyea, Alaska, were accessible at high tide and allowed prospectors to begin the lengthy trip north toward the center of the Gold Rush, Dawson City, which is roughly 700km north.

Unfortunately, for the vast majority of newly minted prospectors, their aspiration of discovering a fortune never happened; if it wasn’t the weather and the long trip to the prospective gold claims, it was the exorbitant costs that came with exploring and living in the north. In many of the articles I read while researching the Klondike Gold Rush, many estimated costs being 10 times higher than what many of the people would have experienced in their former lives, living in Toronto, New York or Chicago.

The Klondike Gold Rush is estimated to have produced $29 million in gold over its 3 year span. Additionally, the Yukon Geological Survey estimates that a total of 20 million ounces of gold has been extracted from the Klondike goldfields since 1896. Gold mining can be credited with spurring the development of much of Canada’s and America’s northern most territories and states. In my opinion, the Yukon holds tremendous mineral potential and will only increase its prestige within the mining community.

Tr’ondëk Hwëch’in First Nation

Klondike Gold’s claims lie within the Tr’ondëk Hwëch’in First Nation lands, which are in the Dawson City area. To note, Goldcorp’s Coffee Gold Project, which was acquired from Kaminak Gold Corp, and sits 130km south of Dawson City, is also within the Tr’ondëk Hwëch’in First Nation lands.

Tr’ondëk Hwëch’in First Nation is based in Dawson City and consists of roughly 1,100 Hän-speaking people. The First Nation is governed by an elected Chief and four councillors, who take direction from the Elder’s Council, a group of Tr’ondëk Hwëch’in people, aged 55 and over. The governing body oversees all agreements affecting the First Nation, including finance, health, social programs, housing and natural resources.

In recent news, the Tr’ondëk Hwëch’in First Nation signed a collaboration agreement with Goldcorp over the development of their Coffee Gold Project. In my opinion, the success of this negotiation was imperative to any of the mining companies exploring or developing within the Tr’ondëk Hwëch’in lands, giving each company a glimpse of what a future deal with them might look like, if they are able to discover an economic deposit or move forward with the development of what they already have.

Klondike Gold Project

As stated earlier, the Klondike has a rich history in gold mining, as 20 million ounces of placer gold have been mined there. The question that Tallman and his team at Klondike Gold are trying to answer is, where did the placer gold come from? When this question is finally answered, there’s a good possibility that the discovery of an economic gold deposit will follow soon thereafter.

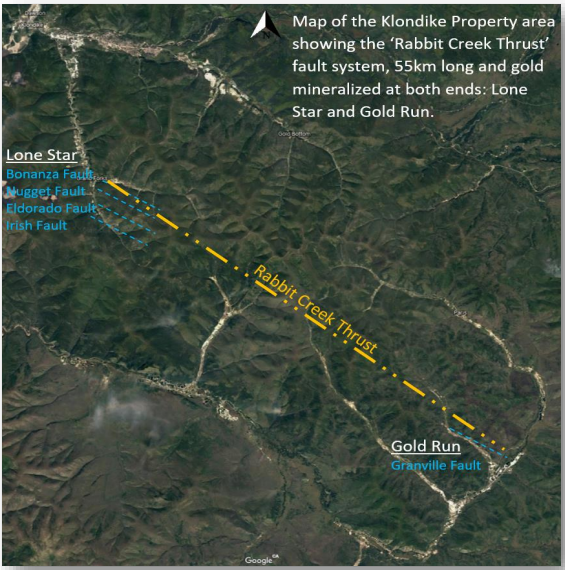

Thus, since taking the helm of Klondike Gold, Tallman has set out to determine if the fault system, which he identified in his original desktop review of the company, plays a role in controlling gold mineralization. Specifically, in our discussion of the property, Tallman refers to the Rabbit Creek Thrust Fault, which stretches roughly 55 km from the Lone Star target to the Gold Run target.

Tallman believes that this is a very important fault and, ultimately, is the key driver in the gold mineralizing event. As you can see in the image above, secondary fault systems, which Tallman refers to as horse tail faults, have been identified around the outer limits of the Rabbit Creek Thrust Fault, and are the areas of focus for Klondike’s upcoming drill program.

What I found most interesting about our conversation regarding the geology of the targets is how they resemble Goldcorp’s, formerly Kaminak Gold’s, Coffee Gold Project geology. Examining a few of Klondike’s slides from their latest Corporate Presentation, they outline the similarities in geological structures.

Klondike Gold Corporation Presentation – Slide 16

In my opinion, the identification of these similarities is a HUGE plus for Tallman and his team, as they are using the knowledge and processes laid out by Kaminak to influence their plans for exploration on their Lone Star and Gold Run targets. Not only does this make the exploration more efficient, but also speaks to the potential of what Klondike may have in terms of gold mineralization.

While it’s important to understand downside risk before investing in a junior mining company, it’s also very important to understand the upside potential. Therefore, I think it’s safe to say that the upside potential for Klondike can be found in a comparison to the Coffee Gold Project, which has 2.16 million ounces of gold reserves (Proven and Probable) and an additional 2 million ounces of gold resources (Indicated and Inferred). To note, Goldcorp paid Kaminak roughly $100/oz in ground for Coffee. Given Klondike’s current MCAP, the upside potential looks very good.

2018 Exploration

Klondike’s plan for its 2018 exploration program has three main components:

Airborne Mapping – Complete 2500 to 3000 line kilometers of airborne surveys across the entire 557 square kilometer property. In my discussion with Tallman, he stated a few times how inadequate the old government geological maps of the property are. Accurate maps of the property are integral for efficient drill target gathering.

Soil Sampling – Groundtruth Exploration has been hired to complete 5000 soil samples and complete the ortho-photographic modelling footage via drone. Airborne mapping overlain with soil sampling data will help the Klondike team narrow down their focus for the diamond drill program.

Drill Program – 50 to 70 holes will be drilled for an estimated total of 5000 meters. This is a preliminary drilling budget, which Tallman suggests could be expanded, depending on results. Drilling on Klondike’s Lone Star target should begin very soon, with drilling on the Nugget and Gold Run targets to follow.

PUSH: Watch for drill results in the weeks ahead, as Klondike should have steady news flow of drill results over the next couple of months.

Metallurgical Work

Additionally, Tallman mentioned that they will be drilling a few holes of HQ core, which has a diameter of 96mm, which is almost 20mm larger than that standard NQ or CHD 76 core which is typically used in exploration drilling. Why the larger core size? Klondike will be using the larger core sample for the beginnings of a metallurgical study, which should shed some light onto economic viability of the Klondike mineralization.

Concluding Remarks

In my opinion, Klondike Gold has the basis for success when it comes to gold exploration:

Experienced management team which is supported by smart money, via billionaire investors, Frank Giustra and Eric Sprott.

District scale land package of 557 square kilometers with the premier mining jurisdiction that is the Yukon. NOTE: The Yukon ranks 13th in the world in mining investment attractiveness as per the Fraser Institute’s 2018 Survey.

The Klondike Goldfields have produced 20 million ounces of placer gold over their history.

Extensive 2018 exploration program, which includes airborne mapping, soil samplings and a 5000m drill program. High news flow throughout the summer.

Exploration program is supported by a robust plan which is rooted in the geological similarities between Klondike’s target geology and Goldcorp’s 4 Moz Coffee Gold Project, which is just south of Dawson City.

CASH – $7 million

Gold exploration is a risky endeavour, one that is fraught with more failure than success. In Klondike Gold’s case, failure is a very real possibility, however, I believe with the strengths outlined above, Klondike has positioned themselves to have the best possible probability of success in discovering economic gold as we as investors could hope. Therefore, I’m a buyer of Klondike Gold and am looking forward to a summer of what I think will be good news flow and share price appreciation!

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I do own shares in Klondike Gold Corp. All Klondike Gold Corp. analytics were taken from their website and press release. Klondike Gold Corp. is a Sponsor of Junior Stock Review.

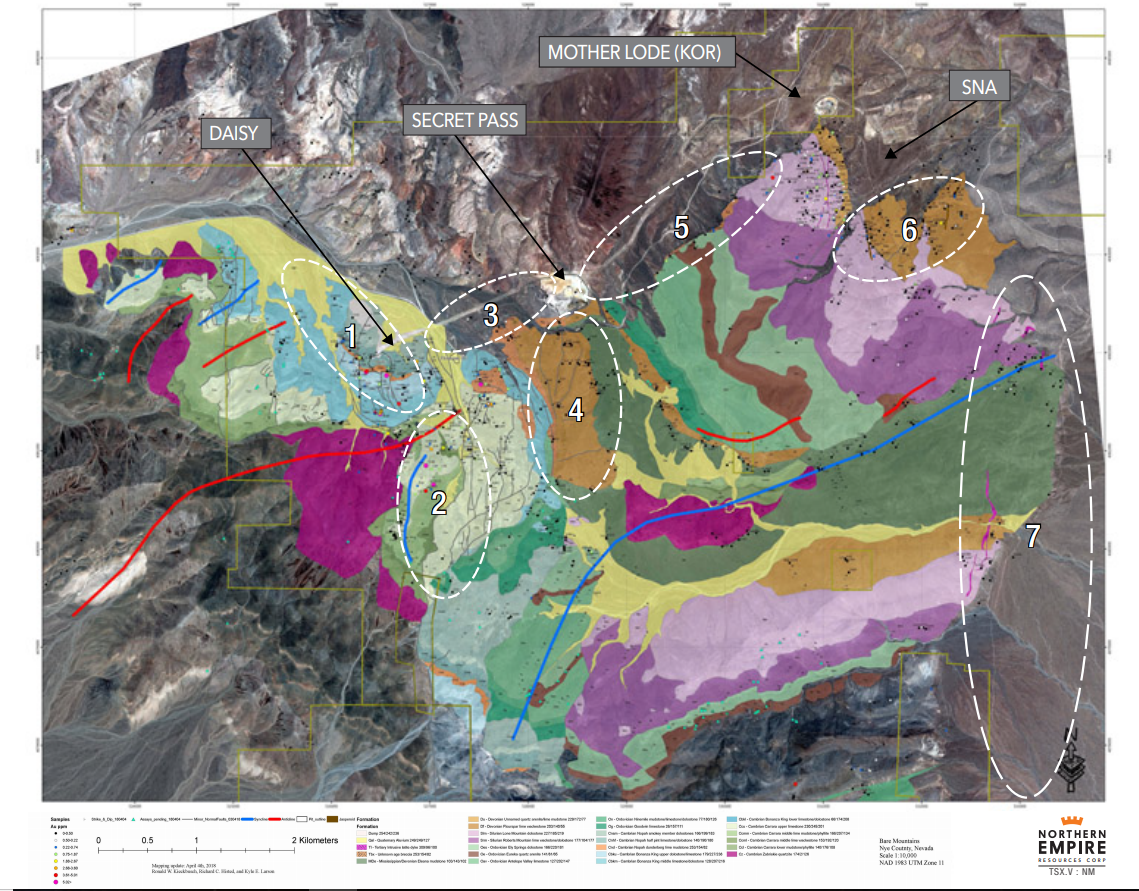

Northern Empire – The Sterling Gold Project Site Visit

On April 6th, I had the opportunity to visit Northern Empire’s Sterling Gold Project, located north-west of Las Vegas, Nevada. My visit was great and really gave me a good perspective of the Sterling Gold Project’s scale and its potential for further resource expansion.

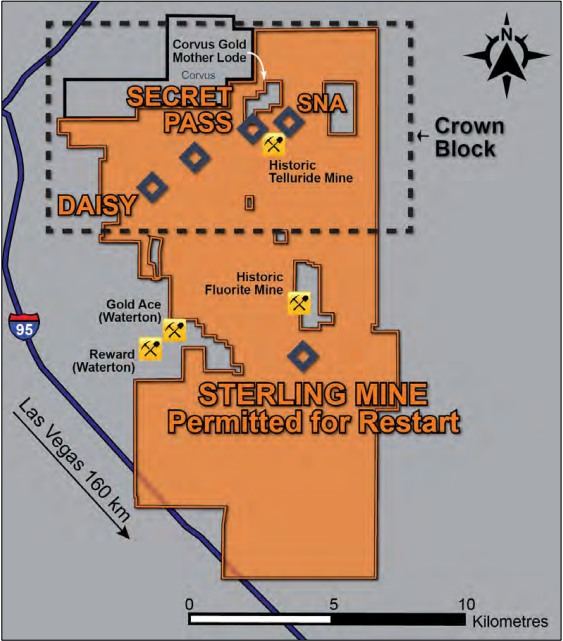

In particular, the Crown Block stood out as having great exploration potential, as not only is this area a focus for Northern Empire, but also has drawn a lot of attention from Corvus Gold, whose Mother Lode Open Pit is completely surrounded by Northern Empire.

In all, I left the site visit very optimistic that Northern Empire’s 2018 drill program should shed a lot of light onto the Sterling Gold Project’s potential and am eagerly awaiting news flow!

Las Vegas

After landing in Vegas, I hopped in an Uber to get to my hotel. As this was my first visit to the area, I was mesmerized by the bright lights, massive celebrity advertisements and sheer size of the Las Vegas Strip.

View from the bridge connecting the Bellagio and Ballys

Las Vegas truly is the center of the universe when it comes to marketing, because the corporations that reside here clearly understand human behaviour and how to manipulate it. Everything about the strip is designed to put a smile on your face while simultaneously extracting the maximum amount of money from your wallet.

Along the strip, a Starbuck’s tall Americano is $5.50 USD, a tall can (493ml) of domestic beer $10.00 USD, and a ‘big gulp’ slushy with rum or tequila will run you $30 USD. These prices remind me of those typically reserved for sporting events or concerts, which may be a good comparison for the confines of the Vegas Strip.

A view of New York New York from my hotel parking lot

While my comments here may seem negative to some, they aren’t meant to be. I have a high regard for the marketing expertise that has created this ‘wonderland.’

View of the Bellagio

Bottom-line, even if you aren’t a gambler, Las Vegas is a place that everyone should visit at some point in their lives. It truly is unique in terms of what it has to offer.

Sterling Gold Project

The day of the site visit started early, as we met in the lobby of the hotel at about 6:30 am. I, however, hadn’t adjusted to the 3 hour time change and was up some time before. One thing about starting your day at 4 am in Vegas is that you aren’t alone. That said, I’m sure most of the people I encountered at that time of the morning had yet to go to bed!

From our hotel, it was about a 2 hour drive up the I95 to the Sterling Gold Project. Given the size of our group, we split up into 3 vehicles. In the SUV with me was Executive Chairman, Doug Hurst, and The National Investor newsletter Editor/Publisher, Chris Temple. Both men are very experienced in the mining and investment worlds and shared several, great anecdotal stories about their experiences and lessons they’ve learned from the sector.

Drones and Area 51

Roughly half way to our destination, we drove past a U.S. Air Force base which, famously or infamously, is the site of at least a portion of the U.S. drone fleet.

A drone flying in the Sterling Gold Project Vicinity

One of the most intriguing, yet mysterious, sites along the way was Area 51. Of course, you can’t actually see Area 51, but many of the businesses along the highway have names inspired by this mysterious U.S. Air Force base. I’m by no means an expert on the lore surrounding Area 51, but after spending the day at the Sterling Gold Project, you very quickly become aware of a U.S. military presence.

2 (small) Helicopters in the distance

Walker Lane Trend

The Walker Lane Trend extends north-west from Las Vegas to Reno, running parallel to the Nevada and California state borders. While not as famous as the Carlin or Battle Mountain-Eureka Trends in the northern portion of the state, the Walker Lane Trend has a very rich gold mining history.

It’s estimated that 50 million ounces of gold have been discovered within the Walker Lane Trend, with the Comstock Lode Mine located near Reno being, arguably, the most famous. Additionally, the Round Mountain and Bullfrog Mines are other examples of gold producing mines within the trend.

Interestingly, Barrick’s past producing 2.3 million ounce Bullfrog Open Pit Gold Mine can be seen from Northern Empire’s Crown Block. I was able to snap a photo, while standing at the top of the Secret Pass Open Pit – see below.

View from the Secret Pass Open Pit – Barrick’s Bullfrog Mine

Satellite Image of the Crown Block

As you can see in the satellite image above, the Bullfrog Detachment Fault and the Fluorspar Canyon Detachment Fault run in a similar east-west fashion, and lay host to the past producing open pit mines. Also, the Faults divide the tertiary volcanic rocks in the north and the sedimentary rocks in the south.

Sterling Mine

The site visit began at Northern Empire’s permitted Sterling Mine, which is in the southern region of the property. After completing our site safety orientation and collecting our PPE, we hit the road, making our first stop at the heap leach pads.

Sterling’s Main Entrance Road, Looking away from the Sterling Mine

Sterling’s Main Entrance Road, Looking at the Sterling Mine

Currently, there’s one active leach pad; at the time of our visit, it was being turned over by the bulldozer featured in the photo below. The ore is mixed on the pad to help oxygenate the pile and break up any fluid channels that formed over the last cycle. Ultimately, this leads to higher recoveries in the processing plant. These are simple smart things that the Company does to improve efficiency show the respect that they treat shareholder capital. Also to note, the existing facilities and processing plant appear to be in great shape, which is a real plus when it comes time to begin production.

Active Leach Pad

We then moved into the Sterling Mine open pit area, more specifically up onto the Water Tank Hill, which gives a great vantage point for viewing all three open pits.

Northern Empire CEO, Mike Allen, on Top of Water Tank Hill

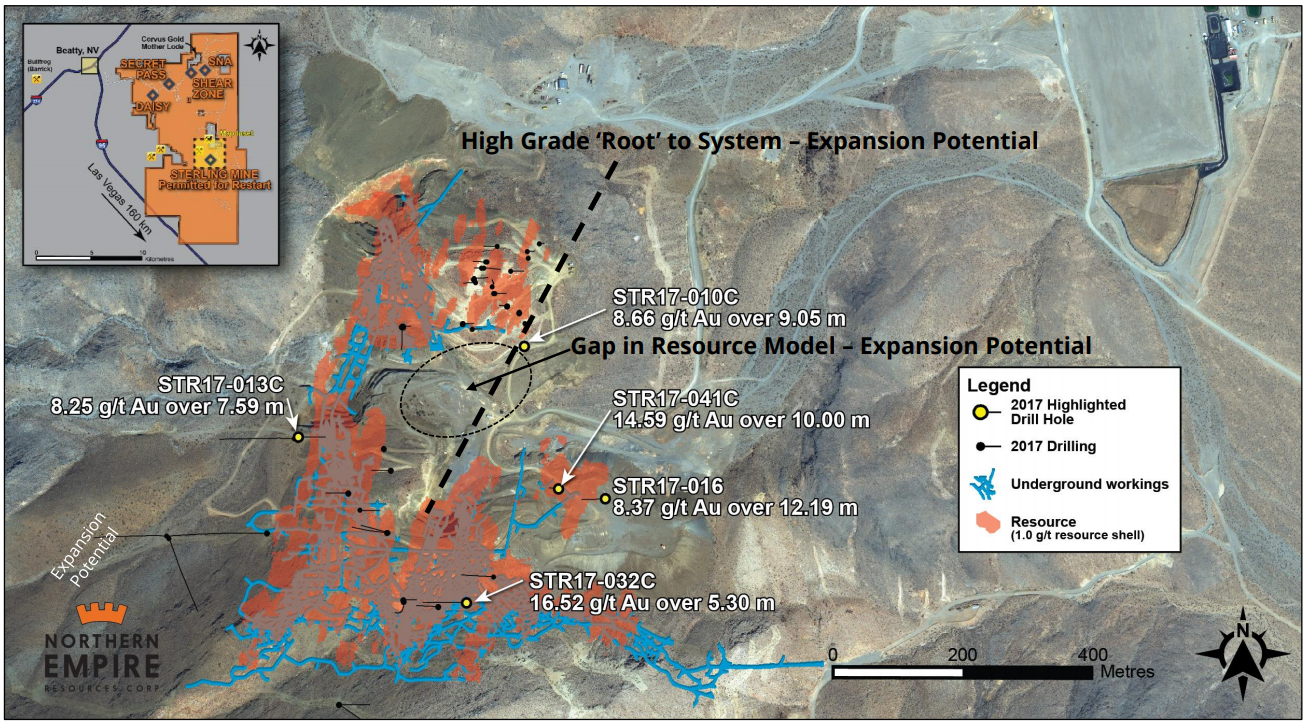

While standing on Water Tank Hill, CEO, Mike Allen, took the opportunity to explain how they will attempt to expand the Sterling Mine resource. As explained in my introductory article, the company will follow up on recent high-grade drill holes that sit on the pit shell edge, as seen in the satellite photo below.

Sterling Gold Project Mineralization – Core Shack

Next, we headed back to the main offices for lunch and a look at the core shack. As with all Carlin-Style gold, the core doesn’t possess any eye-catching visible flakes or nuggets, but instead it is the orange oxidized material (the more broken up the better) which should catch your eye, as it is gold bearing. The samples, however, were still very interesting as the fluorite and calcite mineralization found on the property can be seen in the core samples. In the photo below, for instance, the purple mineral is fluorite.

Core Sample with Purple Mineral Fluorite

In fact, the Sterling property boundaries not only surround Corvus Gold’s Mother Lode Project, but also historic fluorite and mercury mines, which can be seen in the property map below. Interestingly, it was mentioned during the visit that the fluorite mine was hampered by gold contamination, what a wonderful issue to have!

Sterling Gold Project

Sterling Mine Site Manager Chuck Stevens , who worked previously in the Sterling underground mine, showed me a few excellent calcite samples in his office and, additionally, pointed out the massive calcite sample sitting outside the geologist’s office trailer. Also, Executive Chairman, Doug Hurst, pointed out a couple of cinder cones which lie just east of the property; another example of the geological diversity of the property and its surrounding area. The immediate area around Northern Empire’s Sterling Project features fluorite, decorative rock, precious metals and marble mines demonstrating both the endowment of the area, the impact of mining on the local economy, and the ability to permit both large and small mines effectively.

NOTE: A Cinder Cone is formed by volcanic eruptions of mafic / intermediate lavas, which collect to build a cone around a volcanic vent. On the east side of I95, on your way up to the Sterling Gold Project from Las Vegas, a cinder cone is currently being mined for decorative stone used in landscaping.

The Crown Block

Yours truly with the Secret Pass Open Pit in the background

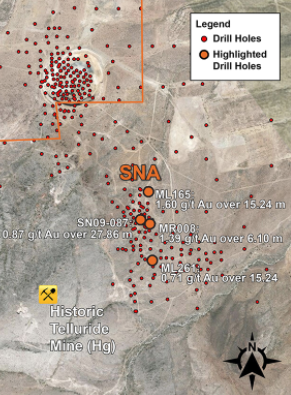

Heading back out onto the I95, we then headed north toward the town of Beatty, to the Crown Block. As you will remember from my introductory article, the Crown Block is made up of 4 main targets: Daisy, Secret Pass, Shear Zone and SNA, all of which are located along the Fluorspar Canyon Detachment Fault.

Our first two stops were at Daisy and Secret Pass deposits, where Senior Geologist, Ron Kieckbusch, and Exploration Manager, Rich Histed, discussed the geology of the area, the work they completed in 2017, and where they were headed in 2018.

Geology of Crown Block

South of the fluorspar detachment fault, mapping has defined an asymmetric fold-thrust belt in the sediment package, with a northwest vergence and northeast plunge likely of Mississippian age (327-290 Ma).

It’s my understanding that the folding of the sediment package generated perpendicular faults, which were later made larger during a caldera collapse. For those who aren’t familiar, a caldera is a large volcanic crater, which can be formed by either an explosive volcanic eruption or the collapse of surface rock into an empty magma chamber. The now larger faults become easier conduits for fluid flow, thus explaining the mineralizing event.

Geological Mapping and Geochemical Sampling

Currently, 30% of the 141 square-kilometer property package has been geologically mapped and geochemically sampled, with the Crown Block being the primary focus. Mapping and sampling is a very efficient and cheap way of acquiring drill targets. In total, 580 rock chip samples have been taken, returning grades within a range of undetectable to a high of 13.85 g/t gold, and 34 samples returned greater than a 1.0 g/t gold.

As stated, the mapping and sampling within the Crown Block has identified new exploration targets, which were noted in the April 25th news release and can be found in the image above.

Road Zone – located north of the Daisy Deposit and features several up-dip surface samples of greater than 1.0 g/t gold, which indicates potential for shallow mineralization.

Gold Ace Fault – located south and up-dip of the Daisy Deposit and features a large undrilled area of high-grade surface samples, including a high of 13.85 g/t gold.

Crowell Extension – located east of the Daisy Deposit and features reported gold grades of up to 7.0 g/t from the historic Crowell fluorite mine. The Crowell Extension target has a strike length of roughly 800 meters.

Radio Tower – Anomalous surface geochemistry to the south of the Secret Pass pit indicate a possible target at depth.

Secret Pass East – As the name suggests, this target lays on the under-explored eastern portion of the large Secret Pass Deposit. Surface sampling has returned up to 5.0 g/t gold and represents a potential strike length of roughly 1200 meters.

Ronko Jasperoids – Located south of the SNA, undrilled Jasperoids returned sample values of up to 2.0 g/t at surface. Jasperoids are excellent host rocks for mineralization and represent a strike length of roughly 500 meters.

Range Front Fault Zone – Range front fault systems have, historically, laid host to many of the largest Carlin-Style gold deposits in Nevada. The range front fault, which runs along the eastern portion of the land package, is sizeable and untested, which has the potential to host a large deposit. Historic sampling returned values upwards of 5.0 g/t gold at surface on secondary structures. It should be noted that range front structures host 3 deposits on the eastern side of the Bare Mountain Range; Motherlode, SNA and the 144 Zone.

In my opinion, there is a TON of potential here, as Northern Empire begins to expand and fill the gaps between these historic deposits. As seen in the image above, it looks like one big shallow gold system, with good grade. In the gold mining world, it doesn’t get much better!

With the identification of these high prospective targets, Northern Empire is expanding their current drill program to 18,000 meters and have already begun the permitting process for a larger 50,000 meter program, which will focus on expanding the Crown Block resource and testing these new regional targets.

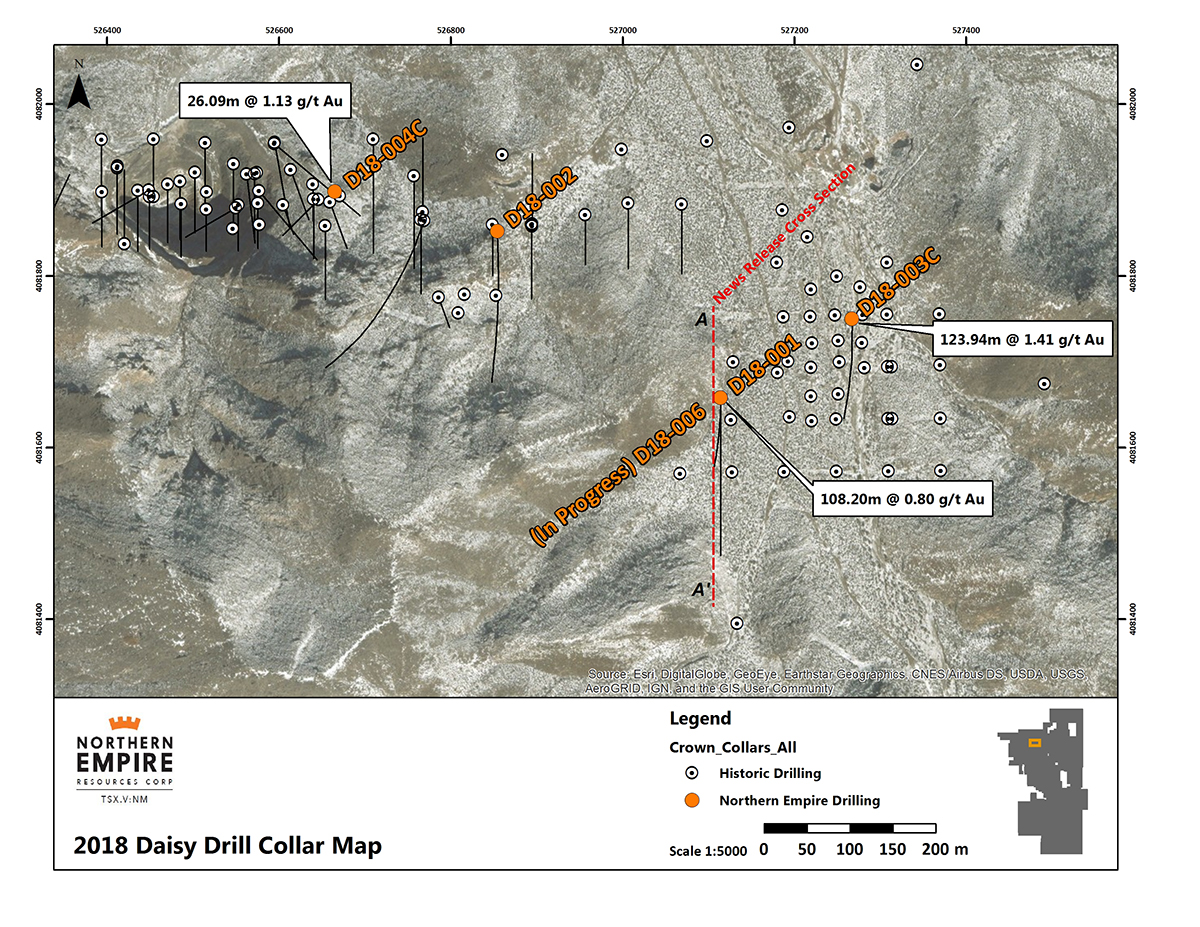

Exploration Drill Results – Daisy and Secret Pass

Step-out drill results from the Daisy and Secret Pass, released May 2nd, not only returned good grades and widths, but confirm that both deposits are open for expansion. The results are highlighted by,

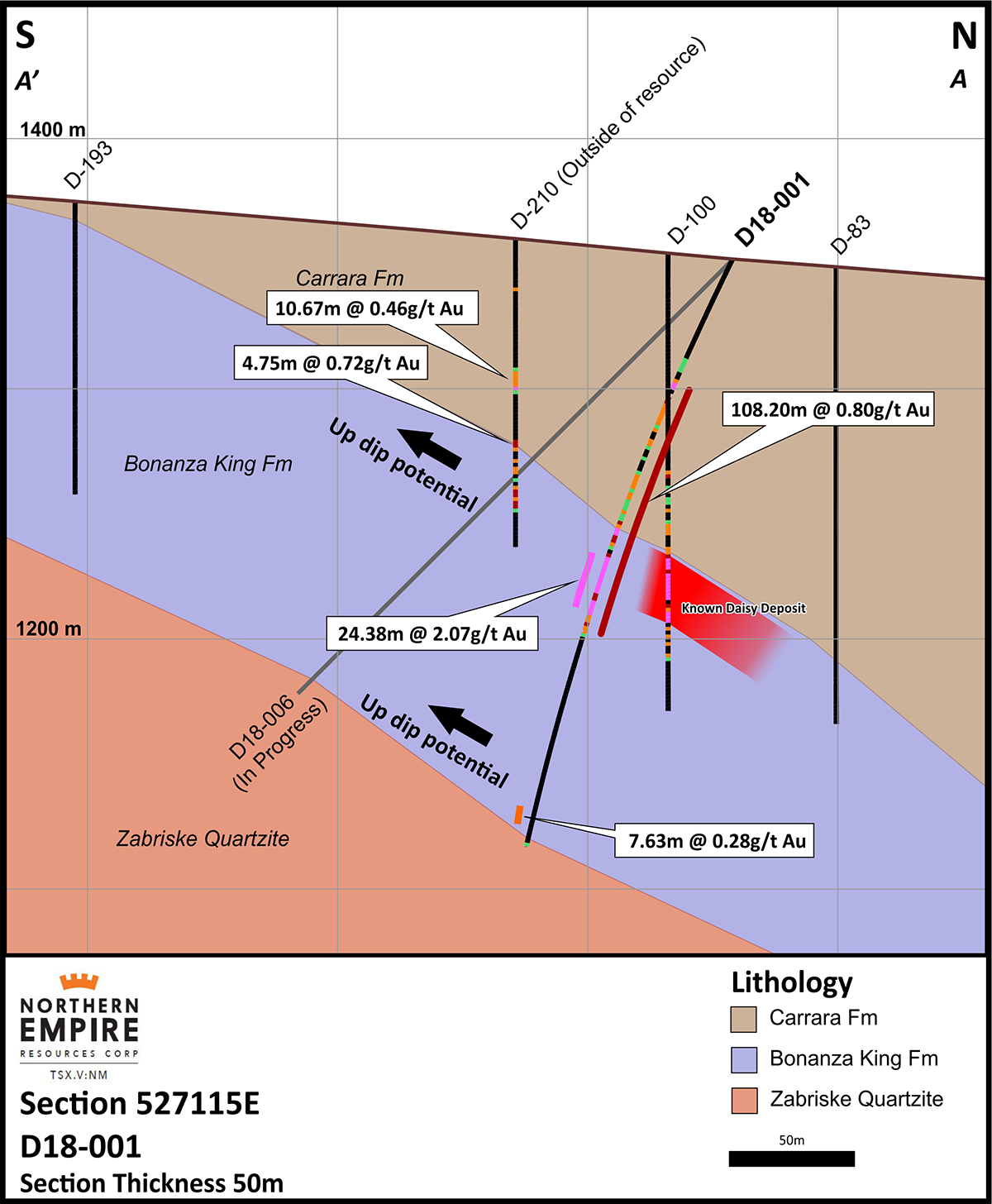

The highlighted D18-001 step-out hole encountered mineralization 53.35 meters down the hole, which was shallower than expected. Additionally, mineralization was encountered at the base of the Cararra formation, which suggests that there is a possibility for further mineralization to be discovered lower in the stratigraphic sequence. In all, the drill results confirm that the Daisy Deposit remains open up-dip for further expansion. Please see the news release for complete details.

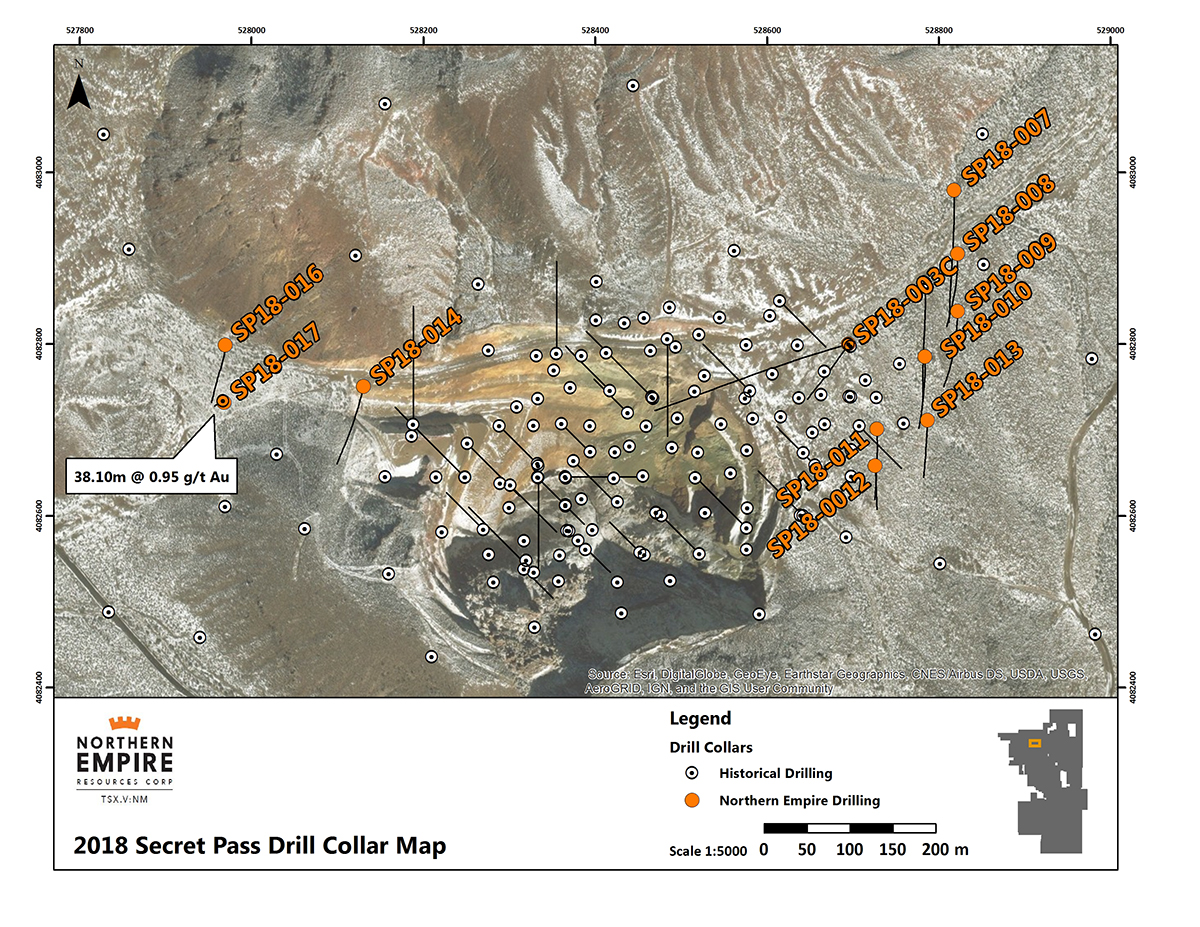

Secret Pass Drilling

The highlighted SP18-017 drill hole stepped out 200m west from the known Secret Pass Deposit and 196.9 meters deep encountered mineralization grading 0.95 g/t gold over 38.1 meters. To note, this hole was terminated before losing mineralization. Northern Empire states within the news release that they intend on re-drilling the hole to better understand the full extent of what has been discovered. This step-out is a great result as it confirms that the Secret Pass Deposit mineralization is open to the west.

Corvus Gold

The last stop of the day was at the SNA Deposit, in the north-east corner of the property. As we approached the SNA Deposit, we first drove past Corvus Gold’s Mother Lode Open Pit, which is completely encompassed by Northern Empire’s Crown Block.

Corvus Gold’s Mother Lode Open Pit

For those who are not familiar, the Mother Lode Deposit has been a major focus for Corvus over the last year, with 10,000m of drilling in 2017 and another 13,000m of drilling planned for the first half of 2018. For those that may not be familiar, Corvus has a MCAP around $300 million, which is largely based on the drilling success at Mother Lode. I find this interesting as a Northern Empire shareholder, because I’m intrigued by the amount of drilling that’s occurring around the existing open pit and, specifically, how that mineralization may extend out toward, or connecting to, the SNA Deposit.

Examining the satellite image below, you can see the concentration of Corvus drill holes not only in the vicinity of the open pit but, more importantly, along the claim boundary.

This is a fairly obvious observation, one that didn’t get past Northern Empire management; while viewing the SNA Deposit during our visit, drilling was taking place along the Corvus claim boundary. In news released April 17th, Northern Empire confirmed that the Mother Lode mineralization does extend south towards the SNA deposit and have drilled significant gold grades from structures which cut favourable host rock for Carlin-type gold mineralization beneath the historic Telluride Mercury Mine.

Northern Empire Drilling beside Mother Lode Open Pit

Concluding Remarks

As I’ve said in the past, site visits are an excellent way for you to bring your due diligence to the next level, and nothing beats seeing the property and interacting with the people in person. My visit to the Sterling Gold Project was no different, as it gave me a better view of the upside potential of the property and the type of people managing the company.

Just to recap, here’s a list of what I see as the strengths for Northern Empire:

Good management team with extensive experience exploring and developing gold projects in Nevada.

The Fraser Institute ranks Nevada 3rd in the world for Mining Investment Attractiveness.

Northern Empire is in possession of all the necessary production permits to restart the Sterling Mine.

The Sterling Mine potential production scenario should be low-cost, as the Carlin Style gold mineralization will be mined from an open pit and is amenable to heap-leaching.

Exploration Potential – The Crown Block, especially, holds a lot of resource expansion potential as it appears all of the existing deposits have the potential to be larger; potentially, one large, shallow and good grade gold system.

18,000 meter drill program underway and a larger 50,000 meter drill program on the horizon as it is currently being permitted!

Existing inferred global resource of 985,000 ounces of gold at 1.29 g/t.

CASH – $16 million!!

I believe there’s a lot of upside potential for Northern Empire if they’re able to execute their plan of expanding the resource at both the Sterling Mine and the Crown Block. I look forward to good news flow over the coming months as this story really begins to come together on the back of their 18,000m drill program.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I do own shares in Northern Empire Resources. All Northern Empire Resources’ analytics were taken from their website and press release. Northern Empire Resources is a Sponsor of Junior Stock Review.

Mr. Wonderful, Kevin O’Leary, and Frank Holmes recently took different side the gold (bullion) vs. gold stocks. Gold and gold stocks are two different asset classes and saying which one is better. One is a commodity (Gold) and the other is equity (Gold Stocks). It’s like comparing multiple championships winning athletes, Sydney Crosby (NHL), Lebron James (NBA), and Tom Brady (Football) and saying one of these players is the best athlete of all-time. Gold and gold stocks offer two different purposes for an investor’s portfolio.

WHY OWN GOLD BULLION?

You own gold in bullion form and keep it in storage as an insurance policyfor your other financial assets. It acts as a counterbalance against other assets in your portfolio. Investors flock to gold as a “safe-haven” asset, just like cash because they aren’t willing to take on risk. Gold is like a cash position in your portfolio, you don’t get paid to own it. Think of Gold as another currency (cash position) that you have exposure too, and you can use it as a counterbalance against your riskier assets. If gold isn’t important, then why do Central Banks own it on their balance sheet? For investors, it’s a way of being your own Central Bank.

“I have a 5% weighting in gold. The GLD and physical bullion. Which I store and pay for the storage. The value of the commodity is whatever it is every day. Kevin O’Leary (Kitco)

Kevin O’Leary isn’t the only one who has gold as a counterbalance in their portfolio. Here is what Ray Dalio of Bridgewater thinks about gold:

“We can also say that if… things go badly, it would seem that gold (more than other safe haven assets like the dollar, yen, and treasuries) would benefit, so if you don’t have 5% – 10% of your assets in gold as a hedge, we’d suggest that you relook at this.” – Ray Dalio

Egyptian billionaire Naguib Sawiris investing half his net worth in gold

“And people also tend to go to gold during crises and we are full of crises right now. Look at the Middle East and the rest of the world and Mr. Trump doesn’t help.” (Marketwatch)

JP Morgan

“Underweight equities, long duration, long gold, and long the yen as Fed policy slows the economy and real rates collapse.” JP Morgan via ZH

GOLD TRADING LIKE A COMMODITY

After the dollar-gold window was broken in the 1970’s gold trades more like a commodity because it isn’t pegged to the US dollar. That is why gold, has better matched the cycle of the commodity booms since that time. Will it be treated again likebefore? We think that “Yes, gold will more than likely be pegged in some form to a currency at some point in the future”. Will it be more like past gold standards? Maybe, history repeats, just not exactly the same as before. It could be in a digital format because that is the way the world is going. We aren’t sure. But we follow the worldview that there are cycles and history repeats. We think that the mantra, “This could never happen” means it can happen again and probably will happen, just in a different twist. Everything has a time when it gets center stage. Gold standards will come, and then they will go. For now gold trades more like a commodity.

GOLD STOCKS AND CYCLE

When O’Leary says gold miners are horrible investments is a bit of hype and bluster.

O’Leary:“The history of mining has been abysmal… I don’t need to have a manager in the middle screwing up his capital cost allowance, not controlling his costs. (Kitco)

This is like saying all technology stocks are profitable like Apple.

The gold sector has one major commonality with every other sector. They are all cyclical! The question is, what cycle do they follow? Gold mining stocks and gold are part of the larger commodity cycle. If you understand the cycle, you understand that there is a time to buy and a time to sell. Gold miners generate an incredible amount of free cash flow once the sector has bottomed. Why? Management teams are forced to really look at their costs and focus on generating profits because investors demand it. Just like after the Dotcom bust, investors started to demand revenue, not just user growth. Let me say that again…Revenue! Profits were demanded as well.

Kevin O’Leary is right when he says “More and more investors are thinking the way I do. They are thinking about return of capital.”

But you are seeing it some darling tech stocks right now, focusing exclusively on growth with disregard for profits.

Look at Wayfair, an e-commerce company sells home goods online. Revenues have increased by more than 4X, yet $0 in profits over the past three years.

During the last gold peak, investors demanded growth in terms of ounces at all cost from management, and in the bottom, investors reversed course and realized profits are essential for survival. You know its approaching a top when its ounces at all costs. The technology sector has recently been like this, companies like Tesla(TSLA), Wayfair (W), where it has been growth at all costs. As the tech cycle turns, investors will demand profits from these companies, not just customer growth on Wayfair and auto deliveries from Tesla. This is a 100% guarantee because investors will get spooked when the cycle turns and expect profits. Right now, investors have been rewarding gold miners for delivering on production and showing profitability. In 2017, gold miners delivered record dividends. Gold miners are set to show strong revenues in 2018 because of the continued elevated gold price above $1,300.

“Tesla will be profitable & cash flow+ in Q3 & Q4, so obv no need to raise money,” tweeted Musk

OTHER WAYS TO INVEST THAN ROYALTY STOCKS & GOLD MINERS?

But there is more than one way to play the gold sector. I am always amazed, when I speak with portfolio managers and receive emails, they always bring up explorers, producers, and royalty stocks to invest in stocks. Seek where the profits are, and you will find the gold. Look at Apple, it generates the most profits in the cell-phone industry over the past 8 years, its revenue grew incredibly over that same time-period. So why not repeat the same process in the gold sector?

We think there is a better way to think about investing in gold & silver stocks, and commodity stocks in general. Does the company generate a percentage of their sales related to gold and silver? It opens you up to many different companies with exposure to other commodities or other industries. Seek companies that are growing revenue, but still, give you exposure to gold and silver.

We can see the day when companies that derive a percentage of their revenue from precious metals will be added to ETFs.

Mining Services

Major Drilling

KGHM

Swick Services

Financial Services

Sprott

GoldMoney

Canaccord Genuity

CME Group

Commodities Trading

Glencore

Refining & Distribution

Johnson Matthey

Umicore SA

Some of these companies are directly involved in operating mines, by providing useful services to the mining industry. While still being able to get exposure to the gold and silver. The additional value is you may be getting exposure to multiple commodities and in some case entirely different industries outside of mining that are growing.

YOU NEED REVENUE GROWTH

Frank Holmes taking a more factor-based approach, with one-factor, focused on revenue growth. This factor is important because revenue growth attracts investor money.

. “The royalty companies have done well and those stocks that basically show better revenue per share, reserves per share, production per share, they far outperform.”Holmes.

And if the company can grow revenue per share and/or cash flow per share this help share prices higher. Would you invest in a company that isn’t growing its revenue? This is why royalty stocks attract investors because they are able to grow revenue consistently over longer periods than the miners. The ability to add cash flowing royalties every year is like adding a new mine but a lot faster than a miner can.

Gold miners’ revenues are tied primarily to two items: 1. Production and 2. Gold Price. Investors are willing to pay up for anticipated growth in production because a new mine is starting up or an existing mine is ramping up for further production. Investors are not willing to pay up for growth, they will sell. The higher the expected growth potential, the higher the anticipated returns. But, watch out if the company slips up. Investors will punish the share price like we recently saw with Pretium Resources and New Gold.When the commodity price is falling faster than the production growth, this will take down all stocks in the sectors. This is why it’s important to focus on higher quality companies, with low AISC or have high operating margins. It minimizes your risks on the downside because they can maintain dividends, and their revenue is less impacted.

You can see why royalty and streaming companies like Franco-Nevada and Royal Gold are so popular because they offer fairly consistent revenue per share and cashflow per share growth relative to gold miners.

PROTECTION & GROWTH

Gold and gold stocks provide investors with two very different sets of risks and opportunities to protect and grow their wealth. You own gold primarily as an insurance policy against your portfolio and the financial system. You own gold stocks as a way to potentially increase your wealth by focusing on growth, management ownership and catalysts. Two different asset classes that are part of the overall portfolio. By understanding the cycle that they both follow, you can enjoy the ups and take money off the table when the crowd is all in.

Written by Paul Farrugia, BCom. Paul is the President & CEO of First Macro Capital. He helps his readers identify mining stocks to hold for the long-term. He provides a checklist to find winning gold and silver miner stocks and any commodity producer.

Disclaimer:

The information contained herein is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your financial situation – we are not investment advisors, nor do we give personalized investment advice. The opinions expressed herein are those of the publisher and are subject to change without notice. It may become outdated, and there is no obligation to update any such information.

Investments recommended in our publications, blog posts, emails, online communications, or any online contents published by any party of First Macro Capital and its affiliated companies should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company in question. You should not make any decision based solely on what you read here.

First Macro Capital writers and publications do not take compensation in any form for covering those securities or commodities. First Macro Capital employees and agents of First Macro Capital and its affiliated companies own some of the stocks mentioned in this article, prior to the writing of this article.

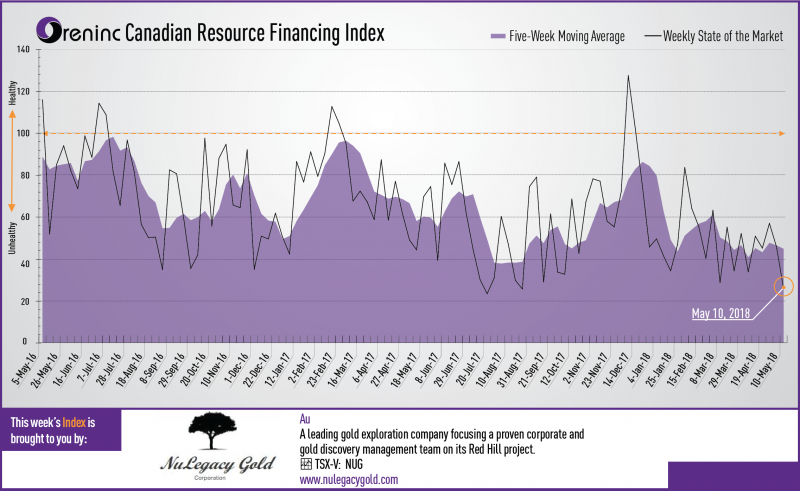

Last week index score: 36.21 (updated)

This week: 52.74

The Oreninc Index rose in the week ending May 18th, 2018 to 52.74 from an updated 36.21 a week ago despite good falling below US$1,300/oz.

Gold finally gave way and fell below the US$1,300/oz level to hit a year-to-date low as the US dollar continued to strengthen, the US ten-year treasury hit a 3% yield and economic data continued to show positive results.

US dollar strength is overpowering geopolitical risk concerns which continue to swirl around: the past week saw the US open its new embassy in Israel in Jerusalem. The ceremony was attended by president Trump’s daughter, Ivanka and provoked mass protests by Palestinians during which Israeli security forces killed dozens.

President Trump’s blunt, hard ball approach to issues also threatened to derail the possibility of talks with North Korean leader Kim Jong-Un after the US carried out extensive war air exercises with South Korea.

On to the money: total fund raises announced increased to C$81.7 million, a two-week low, which included five brokered financings for C$50.5 million, a nine-week high and two bought deal financings for C$20.0 million, a one-week high. The average offer size grew to C$3.5 million, a two-week low and the number of financings grew to 23, a two-week high.

Gold fell to US$1,293/oz from US$1,319/oz a week ago after hitting a low of US$1,285/oz. Gold is now down 0.75% this year. The US dollar index increased again and closed up at 93.63 from 92.54 a week ago. The van Eck managed GDXJ suffered as a result closing down at US$32.84 from US$33.85 last week. The index is down 3.78% so far in 2018. The US Global Go Gold ETF also fell to US$12.98 from US$13.35 a week ago. It is now down 0.23% so far in 2018. The HUI Arca Gold BUGS Index closed down at 177.75 from 182.24 last week. The SPDR GLD ETF again saw sales to close its inventory at 855.28 tonnes from 857.64 tonnes a week ago.

In other commodities, silver also gave up ground to close down at US$16.44/oz from US$16.66/oz a week ago. Likewise, copper closed down at US$3.06/lb from US$3.11/lb last week. Oil continued to post gains to close up at US$71.28 a barrel from US$70.51 a barrel a week ago.

The Dow Jones Industrial Average again saw losses to close down at 24,715 from 24,831 last week. Canada’s S&P/TSX Composite Index continued to see growth to close up at 16,162 from 15,983 the previous week. The S&P/TSX Venture Composite Index also closed up at 786.39 from 782.92 last week.

Summary:

Number of financings grew to 23, a two-week high.

Five brokered financings were announced this week for C$50.5m, a nine-week high.

Two bought-deal financings were announced this week for C$20.0m, a one-week high.

Total dollars decreased to C$81.7m, a two-week low.

Average offer size tumbled to C$3.5m, a two-week low.

Financing Highlights

Canadian Zinc (TSX: CZN) entered into an equity financing agreement with RCF VI to purchase 100 million shares @ C$0.20 for gross proceeds of $20 million.

RCF VI will be issued 50 million warrants exercisable @ C$0.25 until December 31st 2018.

The proceeds will be used to repay a US$10 million bridge loan advanced by RCF VI and the ongoing development of the Prairie Creek Zn-Pb-Ag project in Northwest Territories, Canada.

Major Financing Openings:

Canadian Zinc (TSX: CZN) opened a C$20 million offering underwritten by a syndicate led by Resource Capital Fund VI on a best efforts basis. Each unit includes half a warrant that expires in seven months.

Troilus Gold (TSX-V: TLG) opened a C$10.01 million offering underwritten by a syndicate led by GMP Securities on a bought deal basis. The deal is expected to close on or about June 5th.

Rio2 (TSX-V: RIO) opened a C$10 million offering underwritten by a syndicate led by Clarus Securities on a bought deal basis. The deal is expected to close on or about June 7th.

Troilus Gold (TSX-V: TLG) opened a C$7.01 million offering on a best efforts basis. The deal is expected to close on or about June 5th.

Major Financing Closings:

West African Resources (TSX-V: WAF) closed a C$34.3 million offering on a best efforts basis.

Silvercrest Metals (TSX-V: SIL) closed a C$17.25 million offering underwritten by a syndicate led by PI Financial on a bought deal basis.

South Star Mining (TSX-V: STS) closed a C$4.19 million offering underwritten by a syndicate led by Echelon Wealth Partners on a best efforts basis. Each unit included a warrant that expires in 24 months.

Renaissance Gold (TSX-V: REN) closed a C$3.12 million offering on a best efforts basis.

About Oreinc.com:

Oreninc.com is North America’s leading provider of relevant financing information in the junior commodities space. Since 2011, the company has been keeping track of financings in the junior mining as well as oil and gas space. Logging all relevant deal and company information into its proprietary database, called the Oreninc Deal Log, Oreninc quickly became the go-to website in the mining financing space for investors, analysts, fund managers and company executives alike.

The Oreninc Deal Log keeps track of over 1,400 companies, bringing transparency to an otherwise impenetrable jungle of information. The goal is to increase the visibility of transactions and to show financings activity in a digestible format. Through its daily logging activities, Oreninc is in a position to pinpoint momentum changes in the markets, identify which commodities are trending and which projects are currently receiving funding.

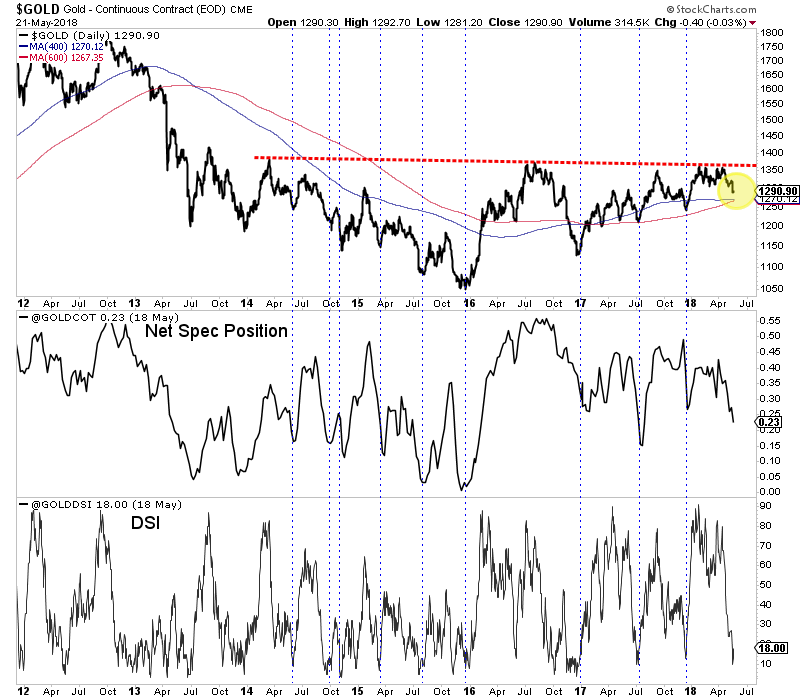

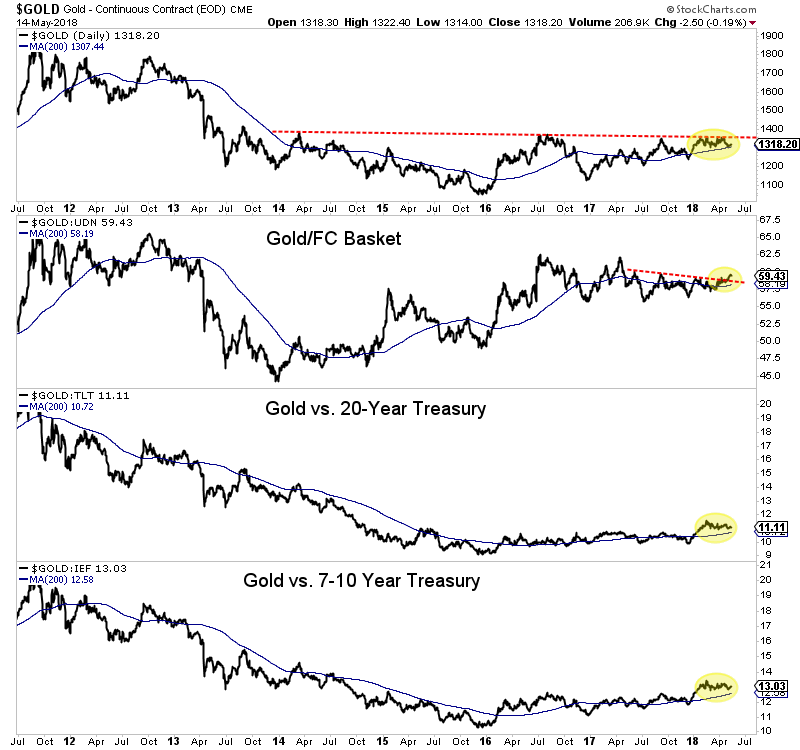

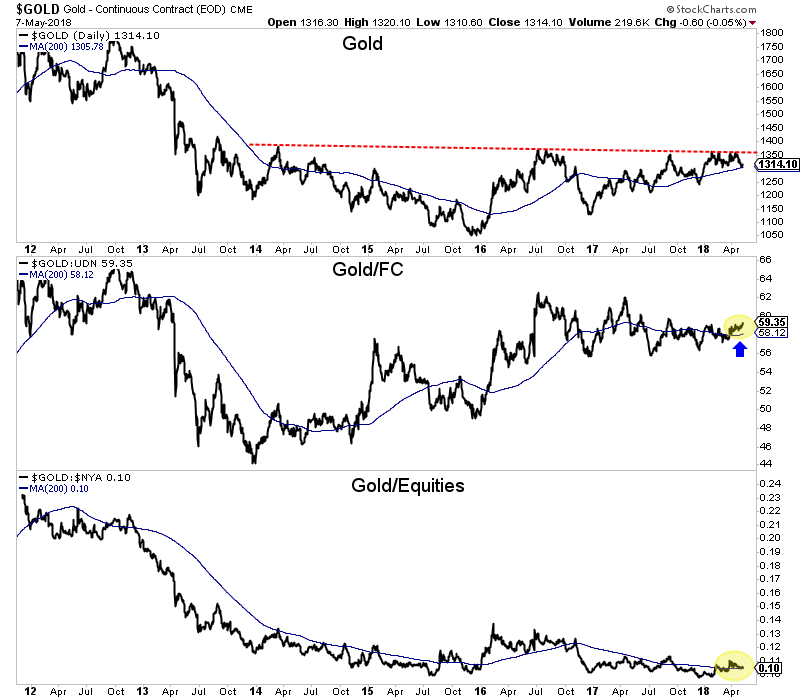

Gold failed to breakout in the spring and recently lost weekly support at $1310. Meanwhile, the gold stocks have held up well in recent weeks (considering Gold) but still have much to prove. Silver couldn’t rally much when its net speculative position was at an all time low. The question now is where do things go from here. The price action is not bullish but with a Fed hike looming and negative sentiment, Gold could be poised to snapback after testing lower levels.

The technicals for Gold show a strong confluence of support at $1265 to $1270. It has traded as low as $1281 in recent days. Trendlines and long-term moving averages coalesce at $1265 to $1270. On the weekly chart, $1265 stands out as a key level. A little bit more selling could bring Gold down to key support.

Gold with Sentiment Indicators

The sentiment indicators (shown at the bottom of the above chart) are encouraging and would be more so with a test of that aforementioned support. The net speculative position as of last Tuesday hit 22.7% of open interest, which is one of the lowest readings of the past two years. The daily sentiment index hit only 10% bulls last week. It’s 21-day average is 32% bulls and if that fell below 30% it would mark a 9-month low.

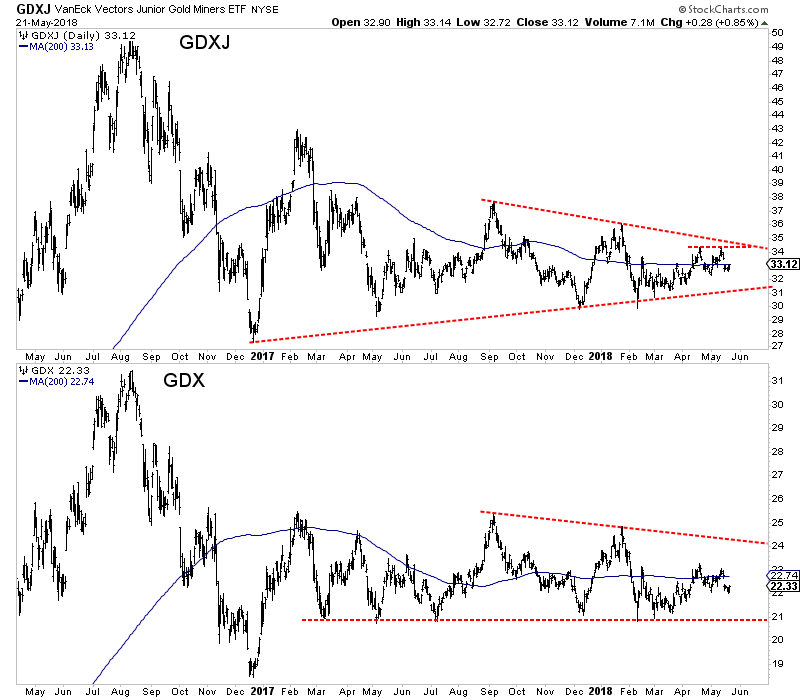

Turning to the miners, we find a sector that continues to be wedged in between support and resistance. GDXJ has trendline and lateral support in the $31s with key resistance in the low $34s. GDX has immediate support at $22 and strong support at $21 while initial resistance is at $23. If Gold is to have another chance to breakout in the months ahead then GDX and GDXJ need to surpass their April highs.

GDXJ, GDX Daily Bar Charts

While we are concerned about Gold for the remainder of 2018, it could be setting up for a summer rally and especially if it drops to strong support around $1265. Sentiment would reach even more encouraging levels and that coupled with strong technical support could produce a rebound. In the meantime we continue to focus on and accumulate the juniors that have 300% to 500% return potential over the next 12 to 18 months. To follow our guidance and learn our favorite juniors for the balance of 2018, consider learning more about our premium service.

Gold continues to act superbly for eager buyers in this time of seasonal softness. Against a background of static mine supply, Chinese demand is strengthening slightly and Indian demand is moderately soft.

The price action reflects these key fundamentals perfectly. Please click here now. Double-click to enlarge this important daily gold chart.

Amateur investors should focus on $100 per ounce price sales for gold. From the recent $1375 area highs, that makes my $1280 support zone even more important for accumulators of the world’s mightiest metal.

Some investors are concerned that rising oil prices will increase the AISC (all-in sustaining costs) of miners significantly. That was a legitimate concern during the past two decades when deflation and collapsing money velocity ruled the gold stocks roost.

America now looks eerily similar to the late 1960s, when inflation began to emerge. The oil shock of 1973 sent fuel prices skyrocketing, but gold stocks were bought aggressively by investors who were very worried about rampant inflation.

Gold stocks soared as fuel costs soared. That was then, and I believe it is poised to be now. Here’s why:

Bullion is a major asset class. In terms of dollar volume, more bullion trades daily in London than the entire NYSE daily volume. It’s the fifth most active FOREX contract in the world. Simply put, the market for bullion products is gargantuan.

In contrast, gold stocks are a very small sector of the market. So, it only takes modest institutional buying to boost prices, and boost them quite significantly.

Please click here now. Double-click to enlarge. This hourly-bars gold chart is technically positive. Some “build-out” of the right shoulder is possible, but that won’t take long.

The next COMEX option expiry day is May 24, and it should be the catalyst that launches the next great rally for the entire precious metals asset class.

Please click here now. In 2014 I predicted that China would lead a “gold bull era” where investors buy exponentially more physical gold with their smart phones.

Key gold jewellery manufacturers and retailers in China are seeing a significant increase in sales now, and I’ve predicted this is only the very beginning of what will be a glorious multi-decade ramp-up in online demand for gold.

Please click here now. Top technicians at Goldman see the $1275 price zone as the outskirts of a key buying area, but it’s possible that the low for this “price sale” is already in!

Please click here now. The fundamental drivers of American inflation are arguably as strong or even stronger now than they were in 1968.

US demographics bear similarity to that time; in the late 1960s, the baby boomers were young and rebellious. The London Gold Pool was ending. The free-trade for gold didn’t get completely launched until about 1974, but some gold products (like certificates) were free-trading by the late 1960s and gaining popularity. Most importantly, it was happening as rates and inflation rose.

A lot of analysts draw parallels between the economic policy of the Trump administration and the Reagan administration, and the policy is similar, but the Fed policy and the business cycle are not.

Both administrations used tax cuts to promote growth, but the Reagan administration had the start of the greatest rate cutting cycle in American history as wind at its back. It also took office at the end of a major economic downturn.

The Trump administration faces a rate hiking cycle, the late stage of the business cycle, and the end of a twenty year bear market in money velocity. The business upcycle has featured huge stock market buyback programs with only modest expenditure on business expansion. That’s very inflationary.

What’s essentially happening is the US private economy is expanding but overheating, and the US government is pushing rates higher with its huge budget deficit.

An inflationary genie is poised to leap out of the bottle in a very big way. The US private economy should continue to grow in the 3% range, but inflation will soon emerge. The big loser in this situation is the US government, and rightly so.

More inflationary tax cuts are almost certainly coming. These cuts are necessary. Even after Trump’s first tax cut, US small business taxes are still about twice as high as supposedly “socialist” Canada’s rate.

Please click here now. Double-click to enlarge. The US dollar bear market rally against the yen is probably almost over. A last push towards 112 – 115 is possible, but when Powell announces his next rate hike on June 13, it’s likely the end of the rally.

Please click here now. Double-click to enlarge this GDX chart. While GDX appears sleepy, many GDX component stocks are in powerful uptrends now. This often happens ahead of a major advance for indexes and ETFs like GDX.

Investors should watch the $23.25 price zone for GDX very closely. A two-day close above that line in the sand should ignite a multi-month advance towards my $30-$35 target zone, and probably by year-end. That’s a huge percentage gain for eager accumulators who buy with gusto now!

Thanks!

Cheers

St

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

The major gold miners’ stocks are still largely grinding sideways, mired in a bearish sentiment wasteland. Traders tend to assume low stock prices must be righteous, reflecting weak fundamentals rather than poor psychology. But once a quarter earnings seasons’ bright fundamental sunlight parts the obscuring fogs of popular sentiment. The gold miners’ just-reported Q1’18 results prove they remain deeply undervalued.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the US Securities and Exchange Commission by 45 calendar days after quarter-ends. Canadian companies have similar requirements. In other countries with half-year reporting, many companies still partially report quarterly.

The definitive list of major gold-mining stocks to analyze comes from the world’s most-popular gold-stock investment vehicle, the GDX VanEck Vectors Gold Miners ETF. Its composition and performance are similar to the benchmark HUI gold-stock index. GDX utterly dominates this sector, with no meaningful competition. This week GDX’s net assets are 25.7x larger than the next-biggest 1x-long major-gold-miners ETF!

GDX is effectively the gold-mining industry’s blue-chip index, including the biggest and best publicly-traded gold miners from around the globe. GDX inclusion is not only prestigious, but grants gold miners better access to the vast pools of stock-market capital. As ETF investing continues to rise, capital inflows into leading sector ETFs require their managers to buy more shares in underlying component companies.

GDX’s component list this week ran 49 “Gold Miners” long. While the great majority of GDX stocks do fit that bill, it also contains gold-royalty companies and major silver miners. All the world’s big primary gold miners publicly traded in major markets are included. Every quarter I look into the latest operating and financial results of the top 34 GDX companies, which is just an arbitrary number fitting neatly into these tables.

That’s a commanding sample, as GDX’s 34 largest components now account for a whopping 92.1% of its total weighting! These elite miners dominate world gold mine production, which ran 770.0 metric tons in Q1’18 according to the World Gold Council’s recently-released Q1 Gold Demand Trends report. The top 34 GDX gold miners reported collectively mining 286.5t of gold last quarter, nearly 3/8ths of the world’s total!