Lithium stocks were hot a year ago, now they’re not. Brine projects in Argentina commanded rapt attention, now no one cares. Clay-hosted Lithium projects were non-starters 2-3 years ago, now they’re in the “maybe” column. Clay-hosted Lithium projects are “unconventional,” meaning untested, and therefore difficult or impossible to fund. However, “unconventional” need not mean difficult to move forward or impossible to fund. What if I told you about a company with a project that had relatively low-grade Lithium, is pre-PEA, and is located in southern Arkansas? Sounds attractive, right? No, it sounds highly….. “unconventional.” Last I checked, Arkansas was not in the heart of the Lithium Triangle.

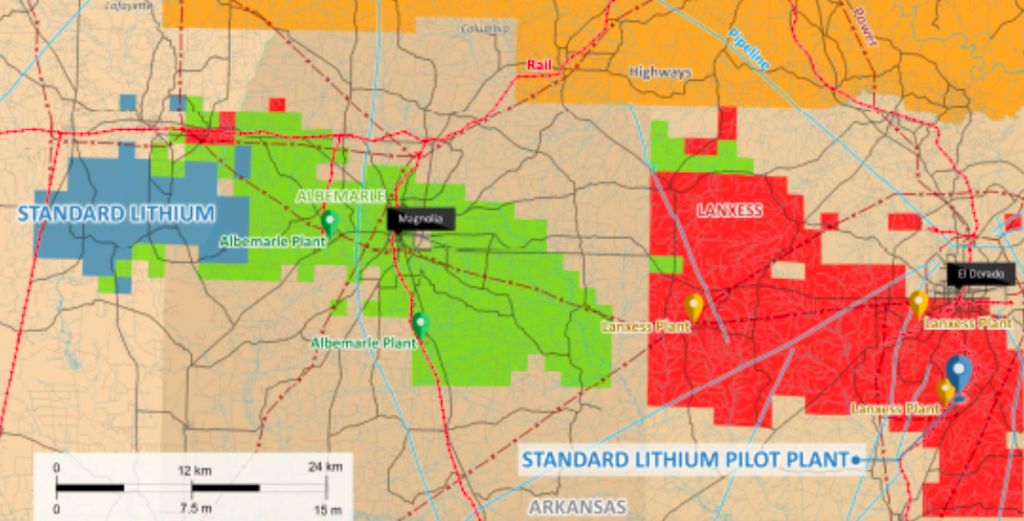

Sometimes unconventional is not all bad. Standard Lithium (TSX-V: SLL) / (OTCQX: STLHF) is a company like no other, and that’s a good thing. Although pre-PEA (PEA now underway), Standard’s 150,000 acre Arkansas Lithium project, called the LANXESS project, has been de-risked in a surprising number of important ways. For instance, while other mining juniors talk about being near, “past producing mines,” the LANXESS project is currently in operation, at massive commercial scale — but producing Bromine from brine, not Lithium (yet). It is a past-producer, but also a present & future producer!

The LANXESS project is hardly early-stage. All of the project’s infrastructure is in place and currently in use. Power, rail, gas, water, tanks, chemicals, pumps, tankers, trucks, drilling equipment, wells, roads, pipelines, etc. 24/7/365, dozens of wells are pumping billions of gallons of brine (salty water), annually, containing Bromine, Lithium and other elements, through 3 nearby processing facilities. The LANXESS project happens to be smack in the middle of North America’s largest brine production & processing facilities. These facilities have been in operation for decades.

Think about the risks avoided here. The Project is in the U.S., thousands of experienced workers are in place working, there’s no discovery or resource expansion risk (the resource is already large enough), the Project is by and large already permitted, it’s in environmental compliance. There’s local community support (no Aboriginal or First Nations issues).

Year-round operations, port access in the Gulf of Mexico, workers go home each night (no fly-in / fly-out). Best of all, the Project is in commercial-scale operation right now, albeit for Bromine. These are logistical items that Lithium companies in Argentina & Chile, not to mention Australia & Canada, would die for, milestones that can take years and hundreds of millions of dollars to obtain.

Not only are operations in place at a large commercial scale, but pumping history, hydrology & geology is all readily available to Standard Lithium for review. This and other data enabled the Company to estimate a 3.1 M metric tonne Lithium Carbonate Equiv. (“LCE“) Inferred resource at the LANXESS project. So, we can be reasonably certain that there’s considerable resource size. However, to be safe we await the Inferred resource being converted to Measured & Indicated, which is expected later this year.

One might think that pulling Lithium out along with the Bromine would be straightforward, it’s not, it proved to be quite a technical challenge. However, a challenge on the verge of being solved, as Standard Lithium is operating a mini pilot plant that has already produced battery-grade Lithium Carbonate. However, this process needs to be scaled up very significantly.

I’ve mentioned several ways in which the Company’s Project is de-risked, taking that theme to a whole new level is a prospective JV with LANXESS (hence the project name). Standard Lithium signed a MOU with LANXESS in May 2018 and a JV term sheet in November. LANXESS is a giant German chemical conglomerate that would provide substantial help on the technical, operational, sales / marketing and R&D fronts.

Assuming reasonable project economics, LANXESS has committed to finance 100% of the commercialization of the Project. LANXESS’, (through its wholly-owned subsidiary) Great Lake Chemicals, operations in Southern Arkansas encompass more than 150,000 acres, 10,000 brine leases & surface agreements and 250 miles of pipelines. LANXESS extracts brine from wells located throughout the area and transports it to 3 Arkansas processing plants through a network of pipelines.

Executing the JV would be huge, LANXESS would own a majority of the Project, but funding is without question the largest risk factor these days. LANXESS funding would be the biggest de-risking event of them all. Several world-class brine projects in Argentina are all but stalled due to a lack of project funding. That’s even though those projects are “conventional” proposing to use conventional solar evaporation ponds. And then there’s Quebec’s Nemaska Lithium, they were billed as fully-funded, until they found a ~C$400M hole in their funding basket. Nothing against Nemaska, Lithium projects are complex and unique. Delays and cost over-runs are the norm.

Standard Lithium’s processing technology, if operating at commercial scale, would process enormous volumes of brine in days vs. over a year for solar evaporation ponds. The technology is designed to be easily and conveniently scalable, it’s modular. If need be, the Company could plan production based on market conditions. Management is not going to run into a ~C$400M cap-ex problem, the amount of operating data available is immense and remember, most of the infrastructure is already in place.

So, what does all of this mean for Standard Lithium? Assuming LANXESS comes on board (LANXESS named Standard Lithium and the Arkansas lithium project during the opening minutes of their 4th Quarter earnings call), they have many risk factors covered, including the biggest risk, project funding. Instead of facing the daunting task of having to raise hundreds of millions in equity capital to fund a commercial development, the Company is probably looking at raising closer to C$25M over the next 18 months. They just closed an C$11M bought deal financing.

Risk Factors

The main risk factor is scaling their proprietary technology from pilot to commercial-scale. With regard to this risk, I think it’s a question of when, not if, the Company achieves this milestone. A moderate delay would be disappointing but would not deliver a fatal blow. Standard Lithium hopes to eventually reach a run-rate of ~20,000 tonnes/yr. LCE. That will likely take several years, after first achieving limited commercial production potentially as early as 2021. Ultimately, production of 30,000+ tonnes/yr. LCE for decades is a possibility, by optimizing the well fields and tapping into the Company’s nearby TETRA Project area.

What might the mid-year PEA show? We don’t know yet, but we can make some educated guesses. Cap-ex? In Argentina, the average Lithium brine project cap-ex requirement from among 6 well known projects is C$540 M. The LANXESS project will be built in stages, so the cap-ex will be substantially lower. Remember, most of the infrastructure is already in place and in operation.

Op-ex should be on the low side as well. For example, the Company has ready access to some of the cheapest chemical reagents in the world. And, the Lithium operations will be sharing some costs with the Bromine operations. Brine exits the Bromine operations at 70 degrees Celsius, so no extra energy needs to be added as it enters the Lithium facilities. Management’s goal is to be in the bottom quartile on the cost curve.

Look at “conventional” brine producer Orocobre Ltd., it’s in year 4 of commercial operation, but is still running at ~70%-80% of nameplate capacity. This is no knock on Orocobre, they were the first new brine project in Argentina in 20 years, it just demonstrates how very difficult each unique brine (chemistry) project is. And the weather, it has been surprisingly rainy this year and last, which is bad news for solar evaporation ponds. Global warming?

In the early-to-mid 2020s there will be fierce competition for scarce resources in Argentina (labor, executives with brine project building experience, consultants, water, power, mining services & equipment, environmental work & construction activities (at 4,000 meter elevations), access to governmental agencies for permits & approvals). Among the 6-10 brine projects in Argentina at PEA-stage or more advanced, several might never reach production. Several others could be delayed by 1,2,3,4 years in reaching nameplate capacities of 20k-35k tonnes/yr. LCE.

Conclusion

Standard Lithium (TSX-V: SLL) / (OTCQX: STLHF) will not be fighting for scarce resources, (another risk avoided) there should be no operating or infrastructure bottlenecks, the weather is not a factor. There won’t be cost blowouts. If a Bank Feasibility Study calls for first production in mid-2021, and LANXESS is committed to project finance, operations & off-take, it will likely happen pretty much on time and on budget.

For hard rock producers in western Australia my understanding is that the situation is a lot better, but we could still see bottlenecks as many hard rock producers try to ramp up supply at the same time. Instead of companies failing, perhaps we will see a wave of M&A in western Australia.

That higher degree of certainty is worth a lot in the wild west of Lithium project development. And, if the brine projects in the Lithium Triangle can’t deliver close to nameplate capacity in the early-to-mid-2020’s, there’s going to be tremendous demand for Standard Lithium’s output, and Lithium prices will likely be high. Who knows, maybe even the “unconventional” clay-hosted Lithium producers will have their day in the sun?

March 29, 2019

Peter Epstein

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Standard Lithium, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Standard Lithium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of Standard Lithium and the Company was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

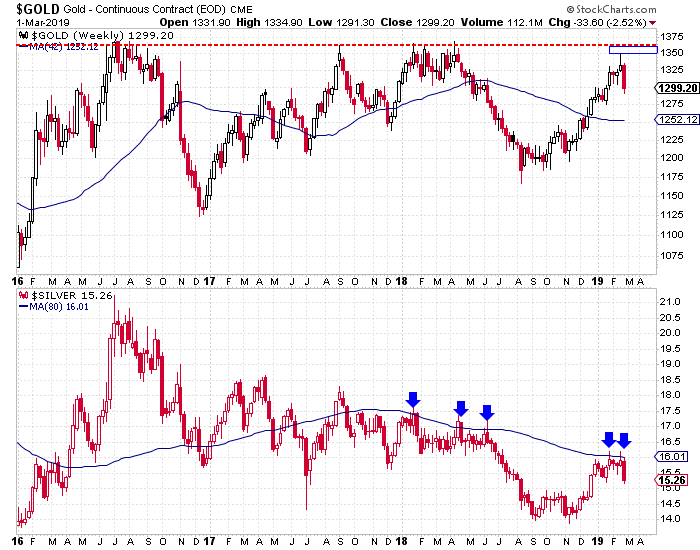

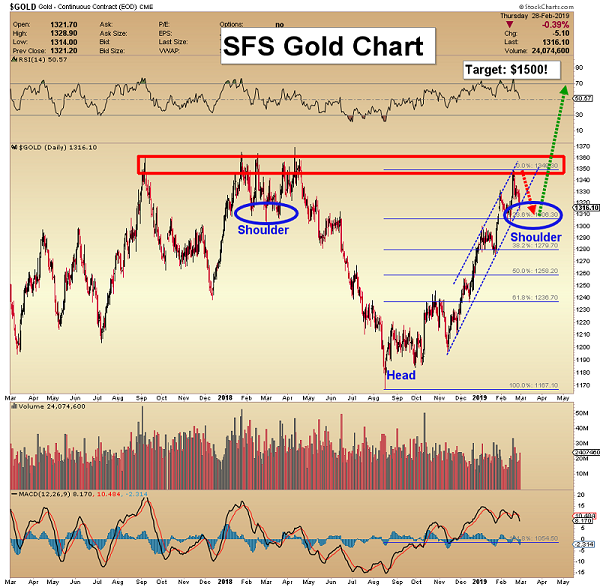

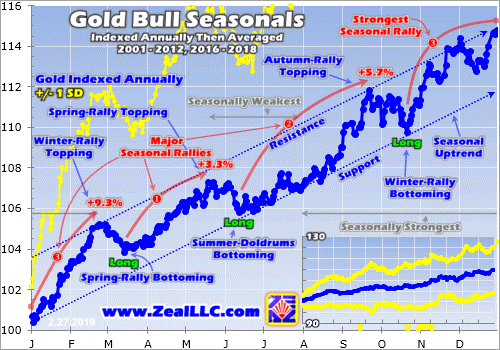

- Please click here now. Double-click to enlarge this long-term gold chart. Fundamental and technical analysis are both strongly supporting gold’s rally towards the key $1400 area.

- Having said that, COMEX price action mainly reflects action in the physical market and this is the weak season for gold.

- Investors need patience. News in the West that “should” push gold $100/ounce higher is in play, but modest physical market demand in China and India means that rallies are modest.

- Please click here now. If this news was happening during the Chinese New Year Jan-Feb peak physical demand time frame, gold would be staging a “barn burner” rally.

- Instead, it’s contained in a $1280-$1350 consolidation range.

- Please click here now. Double-click to enlarge this daily gold chart.

- The bottom line: Gold is on a journey to the $1400-$1420 price zone, but it’s not a rocket ride. It’s more of what I call a “bull era plod”.

- The other fact to keep in mind is that the inversion of the US yield curve with artificially low rates isn’t suggesting that American economic growth is “cratering”.

- Growth is slowing down, but it’s too early to predict that a recession is imminent. A US-China trade deal could provide some medium-term support for stock markets without being negative for gold.

- Central bank gold accumulation is another positive factor, but it’s currently only about 50-60 tons a month. In the weak season Chindian demand often drops from 200+ tons a month to about 60-80.

- Central bank and Western fear trade demand is decent, but isn’t making up for the shortfall caused by the drop in Chindian demand. That’s being reflected in commercial trader action on the COMEX.

- Gold is rallying strongly from the $1280 zone because Chindian dealers are buyers there. They are fading their buying in the $1310-$1320 area, leaving Western money managers to do the heavy lifting. That’s no easy task with Chindia quiet.

- To put it simply, Western financial news is gold-supportive in content, but until Chindian buying resumes in size gold will be more of a trader’s market than the start of a “huge bull run”.

- The good news is that $1280-$1350 gold is a great price for the miners, and many are surging to one fresh high after another!

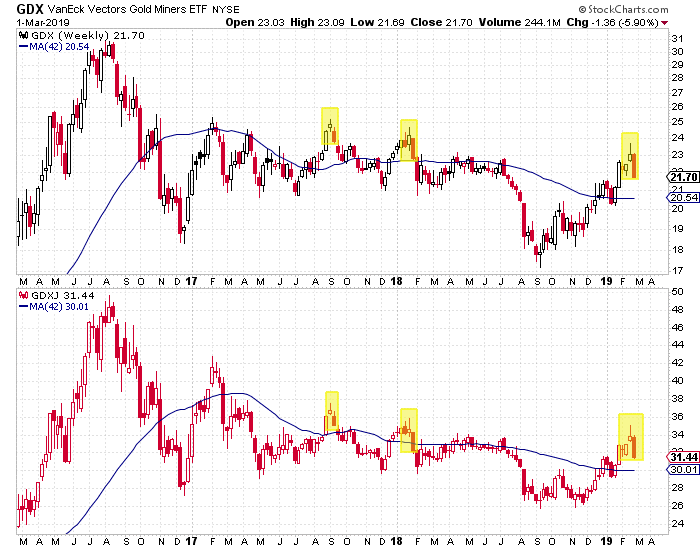

- Please click here now. Double-click to enlarge this fabulous GDX chart.

- I’ve suggested that a Friday close of $23 or higher for GDX and $14 for Barrick (GOLD-NYSE) would open the door to a much more significant rally for most gold and silver mining stocks.

- GDX closed above $23 yesterday and Barrick closed above $14. It’s not Friday yet, but this is a very positive sign!

- I don’t expect gold to move above $1350 until Chindian demand begins to strengthen in August… unless there’s a major economic shock in the West.

- Having said that, when it does rise to $1400-$1420, I expect a massive bull run to occur in the miners.

- The logic for this outlook is that most analysts have underestimated the profits that miners will make at $1400+, and global stock markets are likely to swoon again in the Aug-Oct crash season.

- In Sept 2018, gold was in the $1200 range. If it is in the $1400 area in Sept 2019 with stock markets swooning, institutional money managers could engage in a gold stock buying frenzy!

- A September rate cut from the Fed to calm the panic would likely enhance the frenzy.

- Please click here now. Double-click to enlarge this silver stock ETF chart.

- Note the recent rise of the key TRIX indicator above the zero line. That’s the sign of a technically healthy market. A sustained bull run for silver stocks would be signalled by a Friday SIL-NYSE close above $30!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Barrick & Agnico Lead The Juniors Higher!” report. I highlight money making tactics for Barrick, Agnico, and key juniors that are joining the upside fun!

Thanks!!

Cheers

Stewart Thomson

Email:

Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

Since last spring we’ve written over and over again about a Fed rate cut being the catalyst for a bull move in gold stocks.

The history is almost bulletproof. Many lows in gold stocks over the past 60 years coincided with the end of rate hikes.

At present the Federal Reserve is in pause mode and the market is on the cusp of pricing in a rate cut. Friday, Fed funds futures showed a 56% chance of a rate cut by January 2020.

However, precious metals have yet to make new 52-week highs. The gold stocks (GDX & GDXJ) are much closer to doing so than the metals.

Simply waiting for the Fed to cut rates risks missing out on some upside. As market timers, we have to anticipate it.

Is there a leading indicator for the Fed moving from a pause to a cut?

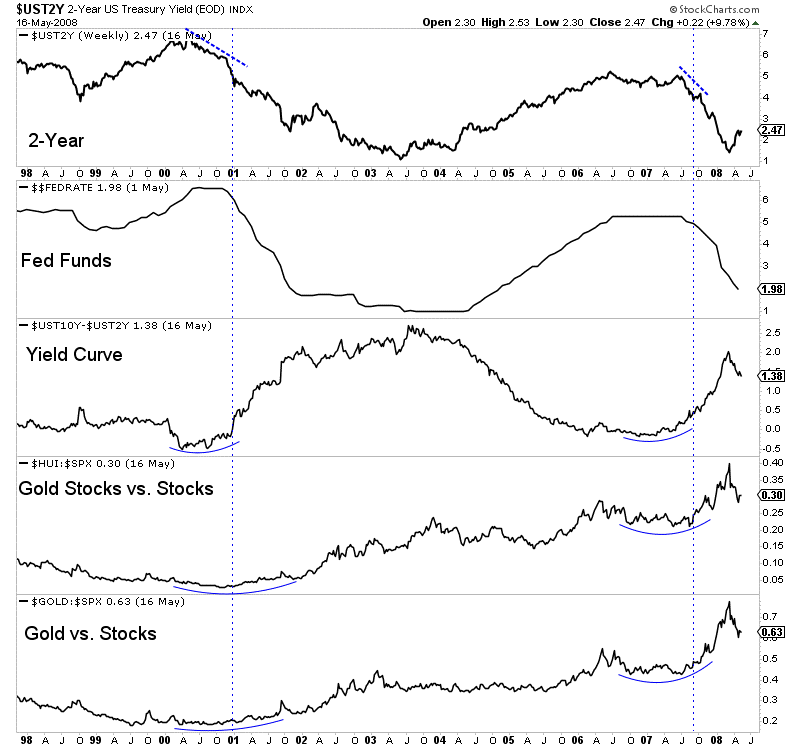

Take a look at the chart below in which we plot data from the last two instances of new rate cut cycles: 2001 and 2007. The vertical lines highlight the Fed’s first cut in those two cycles.

There are several observations to make.

First, Gold and gold stock relative performance accelerated after the rate hikes.

Second, the 10-year and 2-year yield spread began to steepen prior to that outperformance and prior to the rate cuts. And that’s because the 2-year yield, which is a proxy for the Fed funds rate, was trending lower in advance of the first cut.

In short, the sharp decline in the 2-year yield preceded the Fed moving from a pause to a cut. Prior to both the 2001 and 2007 cuts, the 2-year yield had declined by over 1%.

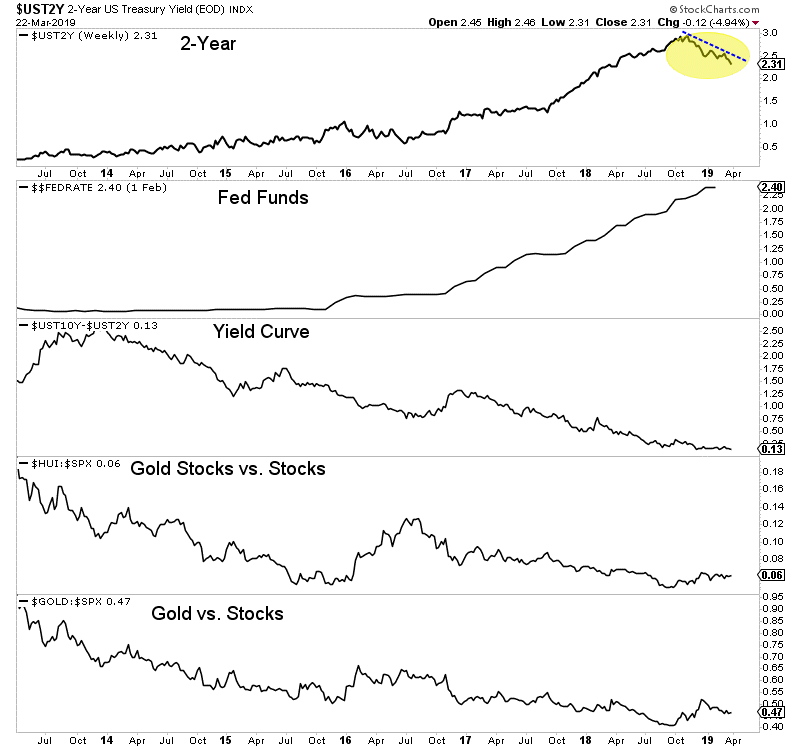

How does this compare to today?

The yield curve has yet to steepen and precious metals have not begun or confirmed outperformance against the stock market.

However, the positive sign for precious metals is the 2-year yield has already declined from nearly 3% down to 2.24% as we pen this.

Every cycle is different and each has its own nuances but we cannot ignore the current decline in the 2-year yield. The closer it gets to 2.00%, the more the market will price in a rate cut.

With its decline to 2.24% today (Monday) the market has now priced in a 73% chance of a rate cut by January 2020. Not surprisingly, precious metals are trading higher.

If the 2-year yield continues to decline then precious metals (and gold stocks especially) should build more and more evidence that they are in a new bull market. To learn what stocks we are buying and think have 3x to 5x potential, consider learning more about our premium service.

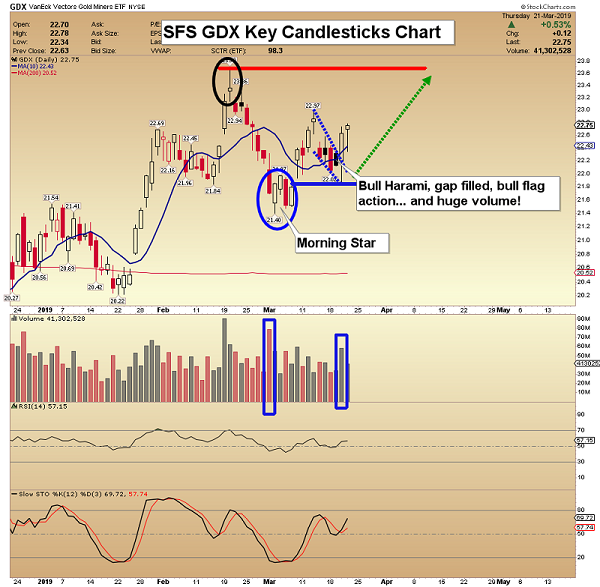

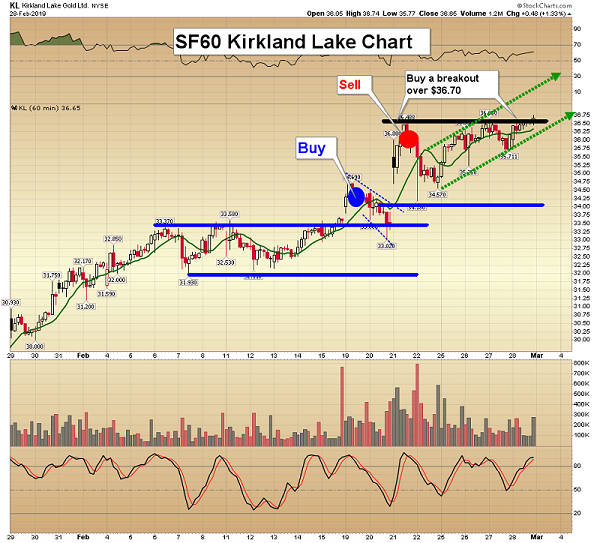

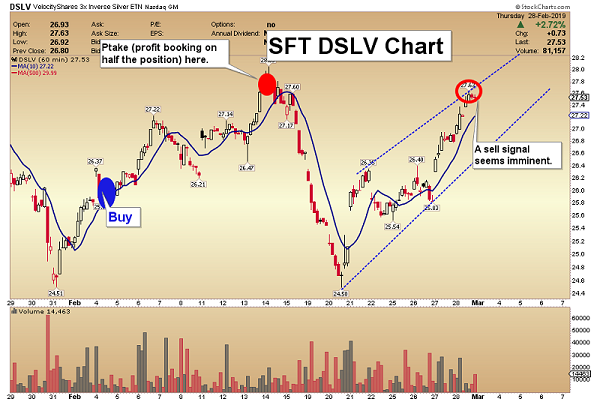

Here are today’s videos and charts (double-click to enlarge):

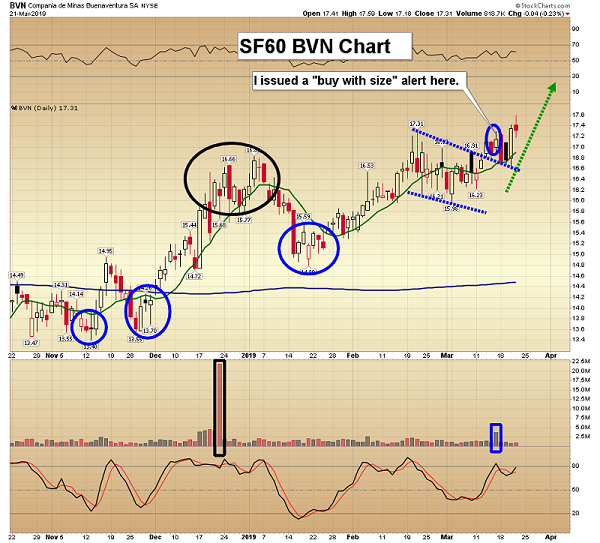

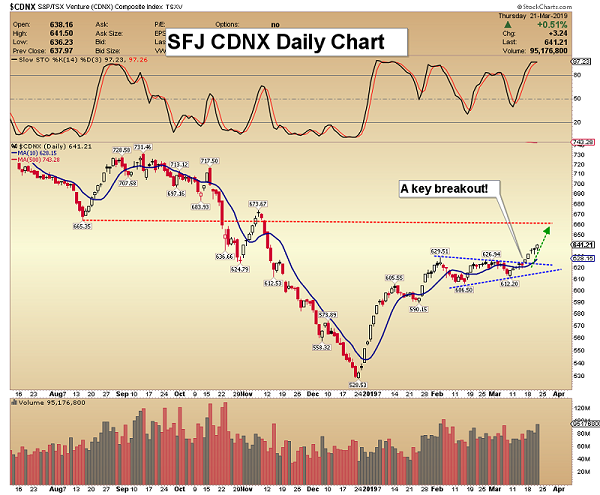

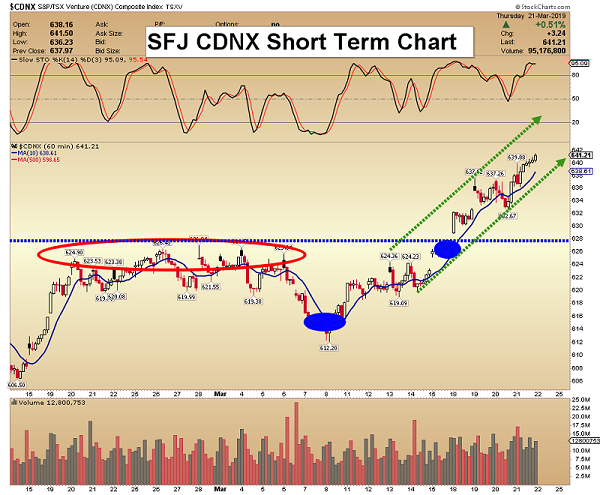

SFS Key Charts, Signals, & Video Analysis

SF60 Key Charts, Signals, & Video Analysis

SF Trader Key Charts, Signals, & Video Analysis

SFJ Key Charts, Signals, & Video Analysis

March 26, 2019

Morris Hubbartt

Unique Introduction For Website Readers: Send me an email to signals@superforcesignals.com and I’ll send you my free “Candlesticks Of Thunder!” junior gold stocks video report. I’ll also include 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you!

Stay alert for our Super Force alerts, sent by email to subscribers, for both the daily charts on Super Force Signals at www.superforcesignals.com and for the 60 minute charts at www.superforce60.com

About Super Force Signals:

Our Super Force signals are created thru our proprietary blend of the highest quality technical analysis and many years of successful business building. We are two business owners with excellent synergy. We understand risk and reward. Our subscribers are generally successful business owners, people like yourself with speculative funds, looking for serious management of your risk and reward in the market.

Frank Johnson: Executive Editor, Macro Risk Manager.

Morris Hubbartt: Chief Market Analyst, Trading Risk Specialist.

Email:

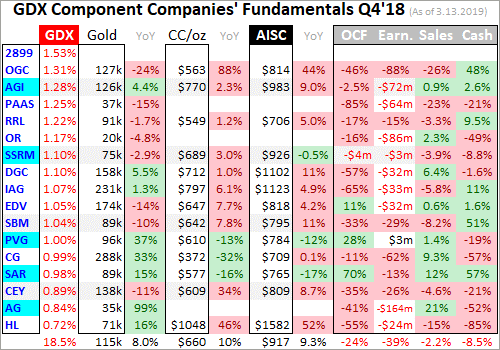

The mid-tier gold miners’ stocks have been rallying on balance in recent months, carving a solid young upleg. They’ve mostly finished reporting their latest fourth-quarter results, revealing how they are faring fundamentally. Their operating and financial performance is very important for investors, as the mid-tier realm is where most of the gold-stock sector’s gains accrue. They fared really well in a challenging quarter.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Required by the U.S. Securities and Exchange Commission, these 10-Qs and 10-Ks contain the best fundamental data available to traders. They dispel all the sentiment distortions inevitably surrounding prevailing stock-price levels, revealing corporations’ underlying hard fundamental realities.

While 10-Qs with filing deadlines of 40 days after quarter-ends are required for normal quarters, 10-K annual reports are instead mandated after quarters ending fiscal years. Most gold miners logically run their accounting on calendar years, so they issue 10-Ks after Q4s. Since these annual reports are larger and must be audited by independent CPAs, their filing deadlines are extended to 60 days after quarter-ends.

The global nature of the gold-mining industry complicates efforts to gather this all-important fundamental data. Many mid-tier gold miners trade in Australia, South Africa, Canada, the United Kingdom, and other countries with quite-different reporting requirements. These include half-year reporting rather than quarterly, long 90-day filing deadlines after year-ends, and dissimilar presentations of operating and financial results.

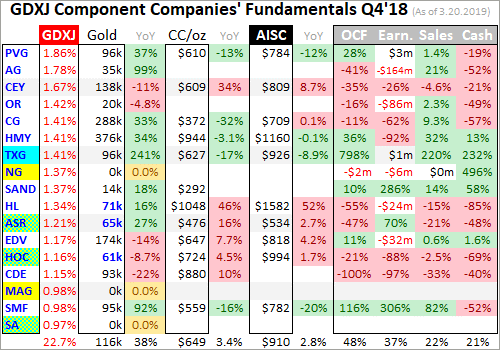

The definitive list of mid-tier gold miners to analyze comes from the GDXJ VanEck Vectors Junior Gold Miners ETF. Despite its misleading name, GDXJ is largely dominated by mid-tier gold miners and not juniors. GDXJ is the world’s second-largest gold-stock ETF, with $4.1b of net assets this week. That is only behind its big-brother GDX VanEck Vectors Gold Miners ETF that includes the major gold miners.

Major gold miners are those that produce over 1m ounces of gold annually. The mid-tier gold miners are smaller, producing between 300k to 1m ounces each year. Below 300k is the junior realm. Translated into quarterly terms, majors mine 250k+ ounces, mid-tiers 75k to 250k, and juniors less than 75k. GDXJ was originally launched as a real junior-gold-stock ETF as its name implies, but it was forced to change its mission.

Gold stocks soared in price and popularity in the first half of 2016, ignited by a new bull market in gold. The metal itself awoke from deep secular lows and surged 29.9% higher in just 6.7 months. GDXJ and GDX skyrocketed 202.5% and 151.2% higher in roughly that same span, greatly leveraging gold’s gains. As capital flooded into GDXJ to own junior gold stocks, this ETF risked running afoul of Canadian securities laws.

Canada is the center of the junior-gold universe, where most juniors trade. Once any investor including an ETF buys up a 20%+ stake in a Canadian stock, it is legally deemed a takeover offer. This may have been relevant to a single corporate buyer amassing 20%+, but GDXJ’s legions of investors certainly weren’t trying to take over small gold miners. GDXJ diversified away from juniors to comply with that archaic rule.

Smaller juniors by market capitalization were abandoned entirely, cutting them off from the sizable flows of ETF capital. Larger juniors were kept, but with their weightings within GDXJ greatly demoted. Most of its ranks were filled with mid-tier gold miners, as well as a handful of smaller majors. That was frustrating, but ultimately beneficial. Mid-tier gold miners are in the sweet spot for stock-price-appreciation potential!

Major gold miners are increasingly struggling with declining production, they can’t find or buy enough new gold to offset their depletion. And the stock-price inertia from their large market capitalizations is hard to overcome. The mid-tiers can and are boosting their gold output, fueling big growth in operating cash flows and profitability. With much-lower market caps, capital inflows drive their stock prices higher much faster.

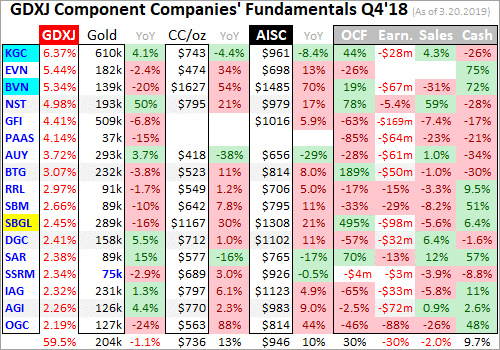

Every quarter I dive into the latest results from the top 34 GDXJ components. That’s simply an arbitrary number that fits neatly into the tables below, but a commanding sample. These companies represented 82.1% of GDXJ’s total weighting this week, even though it contained a whopping 71 stocks! 6 of the top 34 were majors mining 250k+ ounces, 17 mid-tiers at 75k to 250k, 8 “juniors” under 75k, and 3 explorers with zero.

These majors accounted for 19.8% of GDXJ’s total weighting, and really have no place in a “Junior Gold Miners ETF” when they could instead be exclusively in GDX. These mid-tiers weighed in at 44.3% of GDXJ. The “juniors” among the top 34 represented just 14.8% of GDXJ’s total. But only 4 of them at a mere 6.1% of GDXJ are true junior golds, meaning they derive over half their revenues from actually mining gold.

The rest are primary silver miners, gold-royalty companies, and gold streamers. GDXJ is overwhelmingly a mid-tier gold miners ETF, with sizable small-major exposure. Investors and speculators need to realize it is not a junior-gold investment vehicle as advertised. GDXJ also has major overlap with GDX. Fully 28 of these top 34 GDXJ gold miners are included in GDX too, with 23 of them also among GDX’s top 34 stocks.

The GDXJ top 34 accounting for 82.1% of its total weighting also represent 36.6% of GDX’s own total weighting! The GDXJ top 34 clustered between the 11th- to 40th-highest weightings in GDX. Thus over 4/5ths of GDXJ is made up by almost 3/8ths of GDX. But GDXJ is far superior, excluding the large gold majors struggling with production growth. GDXJ gives much-higher weightings to better mid-tier miners.

The average Q4’18 gold production among GDXJ’s top 34 was 164k ounces, just over half as big as the GDX top 34’s 302k average. Despite these two ETFs’ extensive common holdings, GDXJ is increasingly outperforming GDX. GDXJ holds many of the world’s best mid-tier gold miners with big upside potential as gold’s own bull gradually powers higher. Thus it is important to analyze GDXJ miners’ latest results.

So after every quarterly earnings season I wade through all available operational and financial results and dump key data into a big spreadsheet for analysis. Some highlights make it into these tables. Any blank fields mean a company hadn’t reported that data as of this Wednesday. The first couple columns show each GDXJ component’s symbol and weighting within this ETF as of this week. Not all are US symbols.

19 of the GDXJ top 34 primarily trade in the US, 5 in Australia, 8 in Canada, and 2 in the U.K. So some symbols are listings from companies’ main foreign stock exchanges. That’s followed by each gold miner’s Q4’18 production in ounces, which is mostly in pure-gold terms excluding byproducts often found in gold ore like silver and base metals. Then production’s absolute year-over-year change from Q4’17 is shown.

Next comes gold miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated, hard GAAP earnings, revenues, and cash on hand with a couple exceptions.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. In cases where foreign GDXJ components only released half-year data, I used that and split it in half where appropriate. That offers a decent approximation of Q4’18 results.

Symbols highlighted in light blue newly climbed into the ranks of GDXJ’s top 34 over this past year. And symbols highlighted in yellow show the rare GDXJ-top-34 components that aren’t also in GDX. If both conditions are true blue-yellow checkerboarding is used. Finally production bold-faced in blue shows the handful of junior gold miners in GDXJ’s higher ranks, under 75k ounces quarterly with over half of sales from gold.

This whole dataset together compared with past quarters offers a fantastic high-level read on how mid-tier gold miners as an industry are faring fundamentally. While Q4’18 proved challenging with lower average gold prices, the GDXJ miners generally weathered it well. These elite mid-tier miners did much better last quarter than the major-dominated GDX elites. Their profits and stock prices are ready to soar with higher gold.

GDXJ’s managers have continued to fine-tune its ranks over this past year, making some good changes. For some inexplicable reason, one of the world’s largest gold miners AngloGold Ashanti was one of this ETF’s top holdings as discussed last quarter. AU was finally kicked out and replaced with a smaller major gold miner Kinross Gold and a mid-tier Buenaventura. Together they now account for 11.7% of GDXJ’s weighting.

Reshuffling at the top makes year-over-year changes less comparable, particularly given KGC’s larger size relative to most of the rest of the GDXJ top 34. Neither it nor BVN were included in GDXJ a year ago, and are new additions since Q3’18 results. Both are sizable GDX components, probably added to GDXJ to keep the weightings down in its smaller Canadian components. 4 other stocks climbed into the top 34.

Torex, Alacer, Hochschild, and Seabridge were already in GDXJ a year ago but weighted below the top 34. GDXJ is largely-but-not-entirely market-cap weighted, so it’s normal for components to rise into or fall out of the top 34 as their stock prices move higher or lower. All the following comparisons between Q4’18 and Q4’17 are across the two slightly-different GDXJ-top-34 sets, not the exact companies shown above.

Production has always been the lifeblood of the gold-mining industry. Gold miners have no control over prevailing gold prices, their product sells for whatever the markets offer. Thus growing production is the only manageable way to boost revenues, leading to amplified gains in operating cash flows and profits. Higher production generates more capital to invest in expanding existing mines and building or buying new ones.

Gold-stock investors have long prized production growth above everything else, as it is inexorably linked to company growth and thus stock-price-appreciation potential. The top 34 GDXJ gold miners excelled in that department, growing their aggregate output by a big 12.8% YoY to 5.1m ounces! That’s really impressive, trouncing both the major gold miners dominating GDX as well as the entire world’s gold-mining industry.

Last week I analyzed the GDX majors’ Q4’18 results, which revealed they are still struggling with serious challenges. The GDX top 34’s total production fell 3.9% YoY when adjusted for a mega-merger. That was worse than total global output slumping 0.9% YoY according to the World Gold Council. So GDXJ’s mostly-mid-tier gold miners really stand out. They are bucking the industry trend with strong production growth.

Again GDXJ’s top 34 components start at the 11th-highest weighting within GDX. Most of the production problems occurred above that threshold, in GDX’s top 10 components which include the world’s largest major gold miners. Their immense average production of 630k ounces in Q4’18 was nearly 4x the 164k average among GDXJ’s top 34! Those GDX top 10 also accounted for a dominant 59.1% of its total weighting.

GDXJ excluding these depleting giants and reallocating their heavy weightings across smaller majors and mid-tier gold miners makes all the difference. The big majors’ waning production and large market caps act as an anchor retarding GDX’s upside. GDXJ doesn’t share that burden, which helped its top 34 show such strong production growth. There’s no reason to own the large majors with their serious challenges.

Also interesting on the GDXJ production front last quarter was silver. This “Junior Gold Miners ETF” also includes major silver miners, both primary and byproduct ones. The GDXJ top 34’s silver mined rocketed 53.8% higher YoY to 31.2m ounces! For comparison the GDX top 34’s total reported output of 28.8m ounces actually slumped 1.5% YoY. The smaller GDXJ mid-tiers are way better than majors at growing their outputs.

The mid-tier gold miners continue to prove all-important production growth is doable off smaller bases. With a handful of mines or less to operate, mid-tiers can focus on expanding them or building a new mine to boost their output beyond depletion. But the majors are increasingly failing to do this with the super-high production bases they operate at. As long as the majors are struggling, it’s prudent to avoid them.

GDXJ investors would be better served if this ETF contained no major gold miners producing over 250k ounces a quarter on average. They still command nearly 1/5th of its weighting, which could be far better reallocated in mid-tiers and juniors. If VanEck kept the major gold miners in GDX where they should be, it could give GDXJ much-better upside potential. That would make this ETF more popular and successful.

In gold mining, production and costs are generally inversely related. Gold-mining costs are largely fixed quarter after quarter, with actual mining requiring about the same levels of infrastructure, equipment, and employees. So the higher production, the more ounces to spread mining’s big fixed costs across. Thus with sharply-higher YoY production in Q4’18, the GDXJ top 34 should’ve seen proportionally-lower costs.

There are two major ways to measure gold-mining costs, classic cash costs per ounce and the superior all-in sustaining costs per ounce. Both are useful metrics. Cash costs are the acid test of gold-miner survivability in lower-gold-price environments, revealing the worst-case gold levels necessary to keep the mines running. All-in sustaining costs show where gold needs to trade to maintain current mining tempos indefinitely.

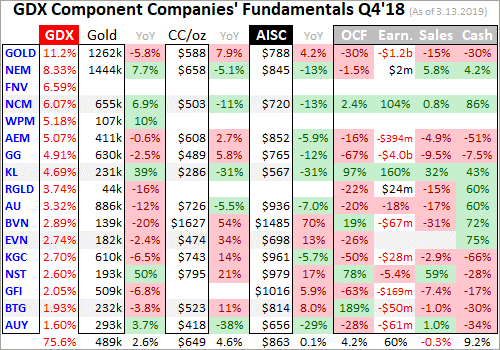

Cash costs naturally encompass all cash expenses necessary to produce each ounce of gold, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q4’18 these top-34-GDXJ-component gold miners that reported cash costs averaged $698 per ounce. That was up a sharp 10.8% YoY, and considerably worse than the GDX top 34’s $655 average.

Those were the highest GDXJ cash costs seen since at least Q2’16, when I started this research thread. But even $698 is far lower than prevailing gold prices, showing the mid-tier gold miners face no existential threat. And GDXJ’s high cash costs last quarter aren’t righteous anyway, as they were skewed higher by an extreme outlier. One of the new GDXJ companies Buenaventura reported crazy cash costs of $1627 per ounce!

Excluding that wild anomaly, the rest of the GDXJ top 34 averaged cash costs of $662 which was right in line with Q3’18’s $663. They’d be even lower without Sibanye-Stillwater, a troubled South-African major gold miner that saw cash costs soar 30.1% YoY to an ugly $1167. If that too is excluded the overall average falls to $642. So for the most part the mid-tier gold miners’ cash costs remain really low relative to gold.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain gold mines as ongoing concerns. AISCs include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current gold-production levels.

These additional expenses include exploration for new gold to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee gold mines. All-in sustaining costs are the most-important gold-mining cost metric by far for investors, revealing gold miners’ true operating profitability.

The GDXJ top 34 reporting AISCs averaged $932 per ounce in Q4’18, which was also up a sizable 7.1% YoY. That was also barely the highest seen since at least Q2’16, contradicting the big production growth these miners achieved. But once again this was heavily skewed by extreme outliers, including both BVN and SBGL. Hecla also reported a stunning 52.3% YoY surge in its gold AISCs to a nosebleed $1582 per ounce!

Both BVN and SBGL reported sharply-lower YoY production, helping explain their huge cost surges. HL’s is more temporary, as it expects 2019 gold AISCs to average a still-high-but-much-lower $1250. Without these abnormal situations, the rest of the GDXJ top 34 averaged excellent AISCs of just $863 per ounce. That would be down 0.8% YoY, and is close to the GDX majors’ $837 average also excluding BVN and HL.

Yet even at that skewed artificially-high $932 per ounce, the elite GDXJ gold miners have great potential to enjoy surging profits and hence stock prices. Gold was relatively weak last quarter, averaging $1228 which was 3.8% lower YoY. That implied the mid-tier gold miners as an industry were earning $296 per ounce. That’s still a 24% profit margin, proving Q4’18’s major GDXJ lows weren’t fundamentally righteous.

Gold is faring much better in this almost-over Q1’19, averaging $1303 which is up a big 6.1% quarter-on-quarter. Assuming GDXJ-top-34 AISCs are flat, these elite mid-tier gold miners are earning around $371 per ounce this quarter. That implies enormous 25.3% QoQ profits growth! We won’t know for sure until after Q1’s earnings season, near mid-May. But the mid-tiers’ fundamentals should’ve greatly improved.

Bigger profits driven by higher gold prices are sure to attract investors back to the still-beaten-down gold-stock sector in a big way. The gold miners will stand out even more with earnings growth expected to be scarce in the general stock markets this year. If gold continues marching higher on balance as it ought to, and GDXJ average AISCs retreat as BVN and HL get anomalous costs under control, GDXJ profits will soar.

The GDXJ top 34’s hard accounting results in Q4’18 were mixed, but way better than GDX on all fronts. These elite mid-tier gold miners reported total sales of $7.4b last quarter, up a strong 12.1% YoY. That is right in line with their 12.8% YoY total gold production growth. That huge 53.8% YoY surge in their silver output helped offset the 3.8% YoY decline in average gold prices. The mid-tier gold miners’ revenues are strong.

Compare that to the GDX top 34, which saw sales plunge 10.3% YoY in Q4 due to 3.9%-lower merger-adjusted gold output. Those strong GDXJ-top-34 revenues kept operating-cash-flow generation solid, totaling $2.2b which was down 9.2% YoY. That again crushed the majors in the GDX top 34, which saw OCFs plummet 30.4% YoY. The divergence between how mid-tiers and majors are faring these days is gaping.

The elite GDXJ mid-tier gold miners also invested in growing their production, so their collective total cash on hand slid 14.3% YoY to $5.9b. The GDX majors saw a similar 14.6% YoY decline in their cash, yet they certainly didn’t spend enough to offset their depleting mines. The only real blemish on the GDXJ top 34’s Q4 results came in hard GAAP profits. Their aggregate bottom line collapsed to a $732m loss last quarter!

That was far worse than Q4’17’s $26m loss. Much of this was due to big non-cash impairment charges, writedowns of the carrying value of gold mines and deposits due to lower gold prices and forecasts. If gold miners expect lower gold prices going forward, they have to flush the resulting expected economic losses through current-quarter results when those impairments are perceived. That hammered overall results.

Honestly the Q4’18 impairments seemed pretty unnecessary, with average gold prices merely down 3.8% YoY. 2018’s full-year average gold price actually rose 0.8% YoY. Major impairments usually happen in years gold plunges sharply, like 2013’s brutal 27.9% plummeting. Something like that really changes the economic assumptions underlying gold mines. But gold only slumped 1.6% last year, which is utterly trivial.

Some of the bigger impairment charges came from First Majestic Silver and Osisko Gold, which wrote off $168m and $166m. This primary silver miner and gold-royalty company aren’t even mid-tier gold miners. And the perpetually-troubled South African majors Gold Fields and Sibanye-Stillwater which have long tainted GDXJ reported big half-year losses implying $169m and $98m in Q4. These alone total $601m of losses.

That accounted for nearly 5/6ths of the GDXJ top 34’s total GAAP losses last quarter. While many of the elite mid-tier gold miners reported small losses, the great majority of the surge in losses came from a handful of stocks. Overall the GDXJ GAAP profits looked relatively decent compared to the majors. GDX’s top 34 reported a staggering $6.0b in accounting losses in Q4’18! The mid-tiers are thrashing the majors.

GDXJ’s mostly-mid-tier component list of great gold miners is really faring well, especially compared to the struggling large gold miners. Investors looking to ride this gold-stock bull should avoid the world’s biggest gold producers and instead deploy their capital in the mid-tier realm. The best gains will be won in individual smaller gold miners with superior fundamentals, plenty of which are included within GDXJ.

Despite being the world’s leading gold-stock ETF, GDX needs to be avoided. The major gold miners that dominate its weightings are struggling too much fundamentally, unable to grow their production. Capital will instead flow into the mid-tiers, juniors, and maybe a few smaller majors still able to boost their output and thus earnings going forward. None of this is new, but the major and mid-tier disconnect continues to worsen.

Again back in essentially the first half of 2016, GDXJ skyrocketed 202.5% higher on a 29.9% gold upleg in roughly the same span! While GDX somewhat kept pace then at +151.2%, it is lagging GDXJ more and more as its weightings are more concentrated in stagnant gold mega-miners. The recent big mergers are going to worsen that investor-hostile trend. Investors should buy better individual gold stocks, or GDXJ.

One of my core missions at Zeal is relentlessly studying the gold-stock world to uncover the stocks with superior fundamentals and upside potential. The trading books in both our popular weekly and monthly newsletters are currently full of these better gold and silver miners. Mostly added in recent months as gold stocks recovered from deep lows, our unrealized gains are already running as high as 74% this week!

If you want to multiply your capital in the markets, you have to stay informed. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. As of Q4 we’ve recommended and realized 1076 newsletter stock trades since 2001, averaging annualized realized gains of +16.1%! That’s nearly double the long-term stock-market average. Subscribe today for just $12 per issue!

The bottom line is the mid-tier gold miners are thriving fundamentally. They are still rapidly growing their production while majors suffer sharp output declines. The mid-tiers are holding the line on costs, which portends strong leveraged profits growth as gold continues grinding higher on balance. The performance gap between the smaller mid-tier and junior gold miners and larger major ones is big and still mounting.

Investors and speculators really need to pay attention to this intra-sector disconnect. Gold and its miners’ stocks should power far higher in coming years as the lofty general stock markets roll over. But the vast majority of the gains will be concentrated in growing gold miners, not shrinking ones. This means the mid-tier and junior gold miners will far outperform the majors. The smaller miners have superior fundamentals.

Adam Hamilton, CPA

March 25, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

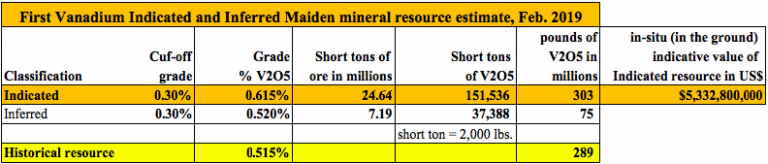

Defense Metals (TSV-V: DEFN) / (OTCQB: DFMTF) is a great name. The Company is defending against Chinese dominance of Rare Earth Elements (“REEs“), and Defense Departments require select REEs to defend their countries! Several REEs are very difficult or impossible to replace in critical applications, yet enable products essential to modern civilization. Any company outside of China that can reliably produce a few key REEs will have a license to print money. This week, SGS Canada provided select head assay results from a 30-tonne bulk sample. Four REE assays were reported in this press release {see chart below}. Using the price/kg of each metal, the in-situ value is ~US$ 535/t. That’s equivalent to ~ 0.41 troy ounces Gold or ~12.8 g/t Gold.

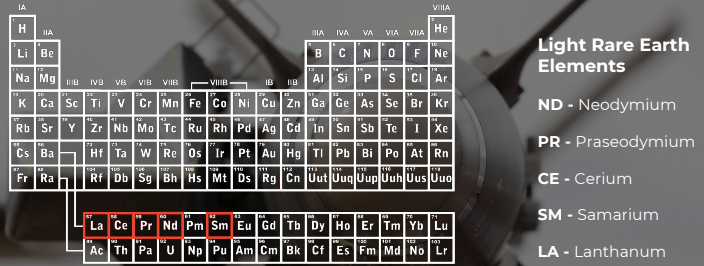

In the following interview of CEO Max Sali, readers will learn more about REEs and about Light Rare Earth Elements (“LREEs“), which REEs are in highest demand, and for which applications. Spoiler alert, Neodymium & Praseodymium are in the top 4 or 5. I asked Max why his team believes that its deposit of LREEs might be economically viable given the odds stacked against any deposit becoming a mine. To finish off, we discussed some early-stage uranium assets the Company picked up in the famous Athabasca basin. {Corporate Presentation}

Please give readers the latest snapshot of Defense Metals.

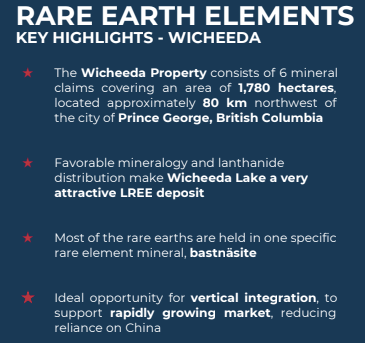

Sure. Defense Metals (TSV-V: DEFN) / (OTCQB: DFMTF) is focused on sourcing, exploring and developing rare earth & uranium properties in Canada. Our flagship project is the Wicheeda rare earth deposit. NOTE: {here’s a good, brand new article by Rick Mills on Defense Metals}

The Wicheeda deposit (6 mineral claims, 1,780 hectares) is 80 km northwest of Prince George, in British Columbia, (“BC“) Canada, and contains potentially exploitable concentrations of Rare Earth Elements. The deposit was explored in the 1970’s & 1980’s, but received little further attention until 2008 when it was drilled by Spectrum Mining Corp. They reported an Inferred resource of 11.3 million tonnes. More recently, SGS Canada provided us with an important update on the deposit. Four REE assays from a 30 tonne bulk sample we sent them earlier this year showed significant concentrations of both Neodymium & Praseodymium.

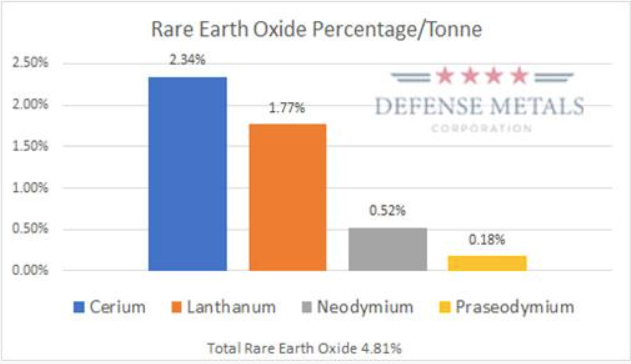

The Wicheeda deposit is a very exciting project because we can potentially get it into production fairly quickly, especially given nearby infrastructure (roads, rail, water, power, labor, mining equipment & services). A favorable mineralogy & Light Rare Earth Element (“LREE“) distribution make the Wicheeda deposit highly attractive. Some impurities can be removed through electromagnetic separation done on site. The press release we put out this week was important because it gave us a new understanding of the deposit, {see graph below}. Total Rare Earth Oxide (“TREO“) was 4.81%, which we feel is attractive.

Wicheeda is ideally suited for open pit mining and conventional flotation to produce a REE-enriched oxide concentrate. In addition to Lanthanum, Cerium & Neodymium, we also have Praseodymium. Importantly, the deposit is open in most directions and outcrops at surface, meaning a low strip ratio and the potential for expansion. Encouraging bench-scale tests have been done, giving our team the goal of a 60%+ concentrate.

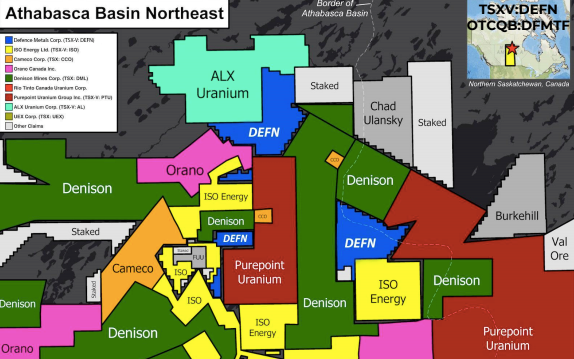

Although the main focus is our rare earth deposit, we also have 2 prospective uranium properties (5 claims blocks), in the heart of the eastern Athabasca basin near Denison Mines and IsoEnergy. Both of those companies are spending millions on drilling this year. IsoEnergy has made a new high-grade discovery 5-10 km from one of our properties.

Which rare earths are in the deposit? Which rare earths in your deposit are most valuable?

The following REEs can be found, Lanthanium, Cerium, Praseodymium, Neodymium, Samarium, Europium, Gadolinium, Yttrium & Dysprosium. There are also trace amounts of a few others. Neodymium & Praseodymium are the most valuable in the suite.

How have the prices of your most important rare earth metals trended over the past few years?

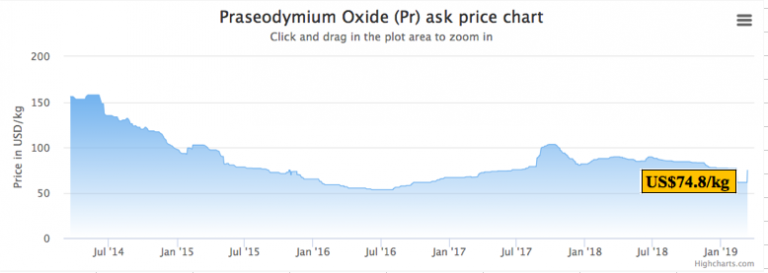

Neodymium and Praseodymium are the most important rare earth metals we have identified at the Wicheeda deposit. Neodymium (Nd) & Praseodymium (Pr) are the two rare earth elements which form the majority of rare earth permanent magnets. Below are 5-yr price charts from Kitco. The most recent prices of US$62.0 per kg for Neodymium Oxide and US$78.4 per kg for Praseodymium Oxide are down from recent highs, but up 35%-40% from mid-2016 lows.

Does management have any indicative information on metallurgy, the potential recoveries of individual metals?

Bench-scale flotation and hydrometallurgical test work was done on Wicheeda deposit drill cores at a SGS Lakefield lab during 2010/2011. SGS successfully developed a flotation flow sheet that recovered 83% of the rare earth oxide (REO) and produced a concentrate grading 42% REO. Subsequent hydrometallurgical testing in 2012 on a 2-kg sample of the concentrate grading 39.7% TREO (total REO) produced an upgraded and purified precipitate containing 71% TREO through a process of pre-leaching and roasting.

SGS Canada is well into the planned work program which includes chemical & mineralogical characterization, grindability & laboratory flotation testing on a 200-kg subsample (of the 30 tonne surface bulk sample). The objectives are to validate the process and confirm that conditions of the previously established 2010/2011 bench-scale drill core flotation test work can be upscaled to the current bulk sample; in addition to further optimization of the process flowsheet.

What will management learn from SGS Canada’s work?

As mentioned, Defense Metals delivered a 30 tonne surface bulk sample from the Wicheeda deposit to SGS Canada. SGS is conducting a multi-phase program of bench-scale metallurgical test work preparatory to commissioning larger scale flotation pilot plant testing. Larger scale pilot plant production is expected to validate bench-scale metallurgy and produce LREE product samples for potential off-take partners. The ultimate goal of the test work is to finalize the process flowsheet prior to the commissioning of larger-scale pilot plant testing. SGS has agreed to give us regular updates on its progress. In addition, Defense Metals plans to re-assay the ‘pulps’ used to produce a new 43-101 Inferred resource estimate. A Preliminary Economic Assessment (“PEA“) will follow.

Defense Metals also has uranium assets in the eastern Athabasca basin, please describe those properties.

Yes, these properties are early stage, and total nearly 10,000 hectares. We have people reviewing the historical work done on the properties, which actually comprise 5 claim blocks. We will likely do some airborne electromagnetic survey work, but to be honest, the eastern Athabasca basin is a hotbed of activity, so we may just allow our neighbors to drill around us and see what they find. Our holding costs on the properties are extremely low.

We are very pleased to have Dale Wallster join our technical advisory board. Dale is a geologist & prospector with 35 years’ experience in North American mineral deposit exploration, with a focus on the targeting & discovery of unconformity-related uranium deposits. He was President & Founder of Roughrider Uranium Corp., a company acquired by Hathor Exploration in 2006 for its strategically located uranium properties in the Athabasca Basin. Dale and his team are widely credited for the discovery of Hathor’s Roughrider deposit. In January 2012, Hathor became a wholly-owned subsidiary of Rio Tinto as part of a C$650 million acquisition.

Why should readers consider buying shares of Defense Metals?

Defense Metals (TSV-V: DEFN) / (OTCQB: DFMTF) offers an attractive, early-stage way to play the REE market. Our LREE deposit appears to be sizable and is open in multiple directions. It contains potentially economic amounts of select rare earth metals. At least 2 of the REEs, Neodymium (Nd) & Praseodymium (Pr) are quite valuable and in high demand for use in permanent magnets. There are indications that the metallurgy of the Wicheeda deposit is favorable and considerable testing is being done on metallurgy.

If the Company receives additional positive reports from SGS Canada, that could be a catalyst for our share price, as it would provide support for the thesis that we can put the project into initial production fairly quickly. While still early-stage, the Wicheeda deposit has had ample historical work done on it dating back decades, and is undergoing significant, wide-ranging testing right now. If we can advance this project in 2019 the way that we think we can, our current market cap of C$5.1 M = US$3.8 M (23.75 M shares outstanding) could prove to be an attractive entry point.

Thank you Max, that was very interesting, congratulations on the new assay results.

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Defense Metals, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Defense Metals are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned shares in Defense Metals and it was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic. [ER] may buy or sell shares in Defense Metals and other advertising companies at any time.

1. The latest U.S. central bank announcement was a win-win for gold.

2. If the Fed surprised analysts and hiked rates, the stock market probably crashes, and gold stocks rally strongly.

3. As expected, the Fed did nothing and gold stocks outperformed.

4. It’s a clear win-win situation for gold bugs around the world.

5. I’m adamant that the U.S. stock market would already look somewhat akin to the 1929 bear market if the Fed had not killed its “ QT on auto pilot ” and “ rates are years away from being normalized ” statements.

6. In contrast, there was/is no QE in China or India. In addition, interest rates are twice as high in China as America, and three times as high in India.

7. The bottom line: Stock markets are propelled significantly higher or lower by central bank policy. Chinese and Indian central banks have vastly more long-term ability to “ juice ” their stock markets higher than the Fed does.

8. This leaves aside the “minor detail” that there are three billion citizens in Chindia. The Chindian population absolutely dwarfs the U.S. population. The citizens are gold-oriented workaholics growing their economy at 6%-7% annually.

9. Most incredible of all: This growth is happening against the background of a quasi-communist government in China and a mafia-like government in India.

10. What happens as those governments transition to the more business-friendly type of government that exists in America? Answer: Vastly more wealth and vastly more demand for gold!

11. Please click here now: [ https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/03/2019mar19bankgold1.png ] The almost universal enthusiasm for gold amongst elite bank analysts around the world right now is highly impressive.

12. Their support for gold on this $70/ounce pullback has been unwavering and Commerzbank analysts appear to be predicting that a surge to the $1700 price zone is imminent!

13. These heavyweight bank analysts influence the decision-making process of institutional money managers. They also affect mainstream financial media. Gold is gaining news coverage as an asset class to be respected.

14. Please click here now: [ https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/03/2019mar19bankgold2.png ] Bank America’s elite gold market analysts note the steady progress being made with global de-dollarization.

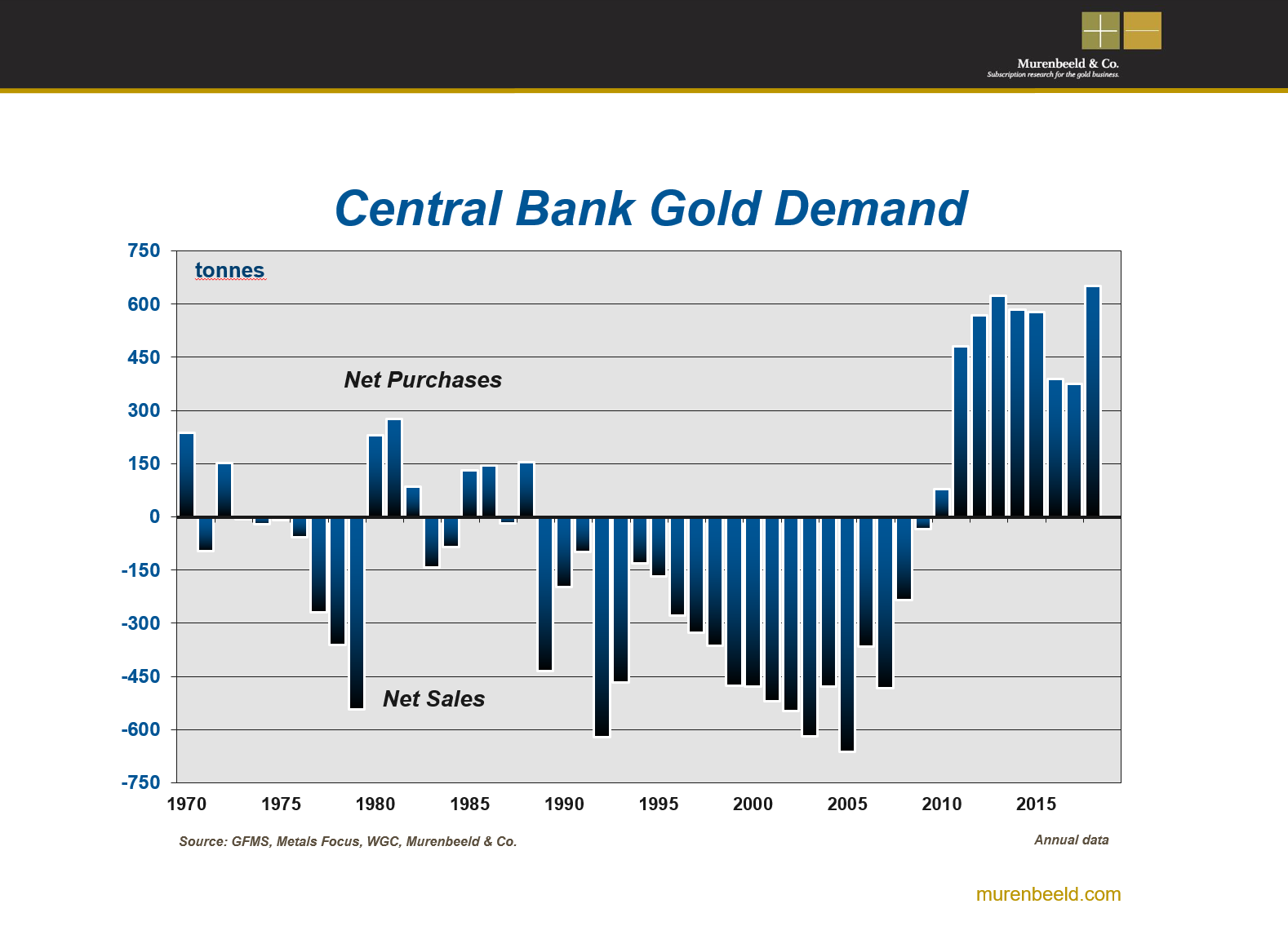

15. The bulk of the action taking place on that front involves fresh and steady allocation to gold by central banks. India’s savvy central bank was a massive buyer near the 2009 lows and now it appears to be committing to a monthly buy program.

16. For gold price forecasting, retail investor sentiment is becoming less important than it was in the past. What matters now is central bank sentiment and bank analyst sentiment. The phrase that describes that sentiment best is: Solid as a golden rock!

17. Please click here now: [ https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/03/2019mar19gold1.png ] Double-click to enlarge. As relentless Chindian demand growth, limited mine supply growth, and central bank de-dollarization all take the centre stage of price discovery in the eyes of the elite bank analysts, negative technical formations like this H&S top will continue be voided, and gold’s uptrend will continue.

18. As gold pulled back to the $1280 I suggested that could be the new floor for the price. The powerful rally in the rupee taking place against the dollar now is triggering a surge in Indian dealer demand. In turn, that’s causing powerful commercial bank traders to cover short positions.

19. Trump is working hard to reverse the damage to global stock markets that his tariffs caused and the Fed has become highly supportive with its statements and actions. I see no reason for that to change with this week’s FOMC policy announcement and Trump is going to intensify his efforts to get a trade deal that is friendly to stock markets.

20. I’m “ long and strong ” the U.S. stock market, the Indian stock market, the Chinese stock market, and the entire precious metals sector… with a wide array of investment vehicles.

21. Please click here now: [ https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/03/2019mar19gdx.png ] Double-click to enlarge this GDX daily chart. While I’m long DUST-NYSE at my [http://www.guswinger.com/ ] swing trade service, that’s a mechanical short-term system designed to produce solid profits during wild volatility events like the Fed meet.

22. In the big picture, volume is soft on down days for most gold stocks. Volume is rising as the price rises. That’s bullish. Most importantly, the GDX price action can be themed as… “ solid” . As gold rallied to $1350, I predicted that many individual miners would keep rallying as gold pulled back.

23. A big feature of the current $70/ounce gold price consolidation has been the continued rally of many miners . A rise in gold to the $1520 area would turn these miners into cash cows, and a further rally to Commerzbank’s $1700 predicted price should cause an institutional feeding frenzy!

24. Gold is steadily reclaiming its title as “ ultimate asset ”, which means it rises in good times and bad. If global stock markets rise, gold rises. If global stock markets crash, gold rises. Owning gold is now the “ ultimate no-brainer ” tactic for central banks and heavyweight bank analysts. Let’s hope that sentiment envelops 100% of the Western gold community… right here, right now!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Golden Seniors!” report. I highlight key senior gold stocks with incredible upside potential that are trading at under $10/share. It’s essentially an opportunity to buy senior producers at junior prices! I include key buy and sell zones for each great stock.

Thanks!!

Cheers

Stewart Thomson

Graceland Updates

mail:

stewart@gracelandupdates.com

stewart@gracelandjuniors.com

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

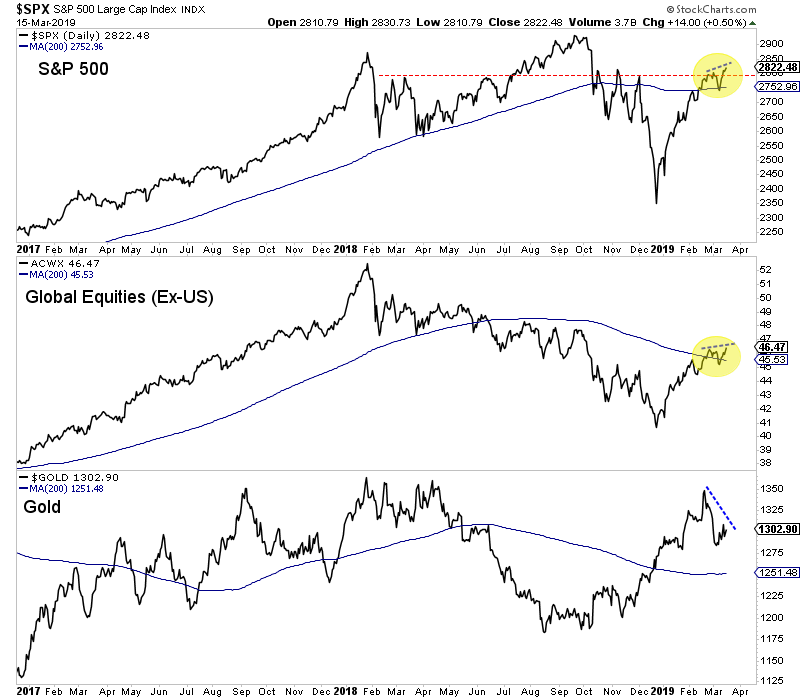

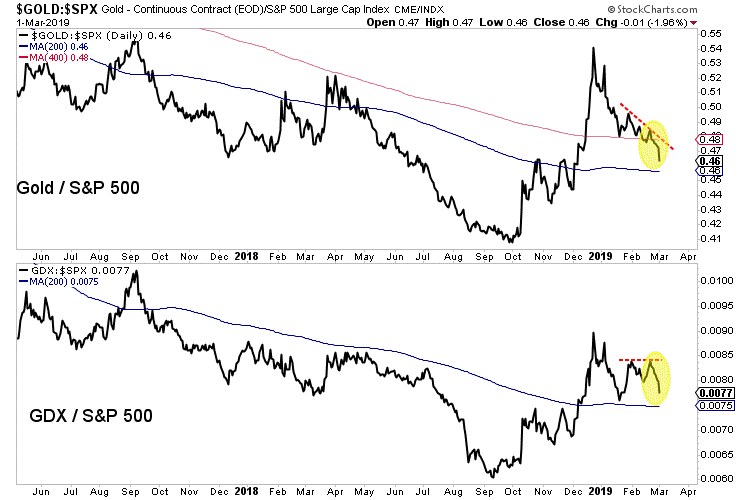

In recent weeks we noted the bullish outlook for the stock market.

Friday the S&P 500 as well as ACWX (global equity ETF ex US stocks) closed above resistance and made higher highs.

Not surprisingly, as US and global equities have avoided a bear market (for the time being), precious metals have weakened. It’s not a surprise that as Gold failed to breakout both the S&P 500 and global equities (ACWX) held their 200-day moving averages and then made a higher high.

The very recent underperformance in Gold and precious metals is better illustrated in the ratio charts below.

Gold against stocks made a very strong move in the fourth quarter but instead of digesting or consolidating that move, the ratios have steadily declined. The same could be said for the GDX ratios as they have formed rounding tops.

The implication is obviously not favorable for precious metals because outperformance of the stock market is a necessity for a bull market and especially so, given the current context.

That being said, one positive for the precious metals complex is the miners are outperforming the metals. Last week the GDX to Gold ratio hit a seven and a half month high.

Another positive is breadth has not deteriorated yet. The GDX advance decline line is only a tiny bit off the recent high and 73% of the HUI and 65% of GDXJ are above the 200-day moving averages.

Ultimately and to continue to beat the dead horse, a bull market in precious metals cannot begin without outperformance against the stock market. That will likely coincide with the Fed moving from pause mode to rate cuts.

The immediate outlook is bullish for stocks and therefore do not expect Gold to breakout or begin a bull market. It’s unclear if renewed stock market strength will lead to a larger topping pattern or if its an indication that growth will stabilize for the rest of 2019.

Regardless, until Gold outperforms stocks and the Fed is ready to cut, we are focused on the companies that can perform without a rising Gold price. To learn which juniors have 3x to 5x potential over the next 12 to 18 months, consider learning more about our premium service.

The major gold miners are grinding higher in a solid upleg, fueling growing interest in this small contrarian sector. They’ve mostly finished reporting their fourth-quarter results, revealing how they are really faring fundamentally. Collectively the world’s biggest gold miners continue to face serious challenges, which often stem from declining production. That makes stock picking more important than ever for investment success.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Required by the U.S. Securities and Exchange Commission, these 10-Qs and 10-Ks contain the best fundamental data available to traders. They dispel all the sentiment distortions inevitably surrounding prevailing stock-price levels, revealing corporations’ underlying hard fundamental realities.

While 10-Qs with filing deadlines of 40 days after quarter-ends are required for normal quarters, 10-K annual reports are instead mandated after quarters ending fiscal years. Most gold miners logically run their accounting on calendar years, so they issue 10-Ks after Q4s. Since these annual reports are larger and must be audited by independent CPAs, their filing deadlines are extended to 60 days after quarter-ends.

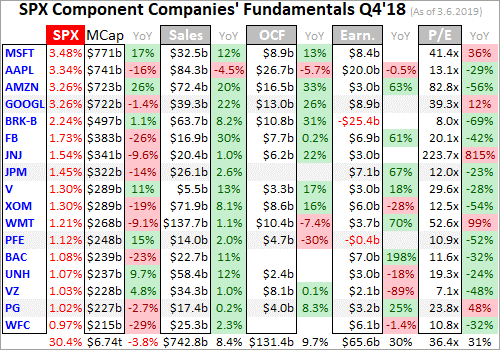

The definitive list of major gold-mining stocks to analyze comes from the world’s most-popular gold-stock investment vehicle, the GDX VanEck Vectors Gold Miners ETF. Launched way back in May 2006, it has an insurmountable first-mover lead. GDX’s net assets running $10.6b this week were a staggering 47.1x larger than the next-biggest 1x-long major-gold-miners ETF! GDX is effectively this sector’s blue-chip index.

It currently includes 45 component stocks, which are weighted in proportion to their market capitalizations. This list is dominated by the world’s largest gold miners, and their collective importance to this industry cannot be overstated. Every quarter I dive into the latest operating and financial results from GDX’s top 34 companies. That’s simply an arbitrary number that fits neatly into the tables below, but a commanding sample.

As of this week these elite gold miners accounted for fully 94.1% of GDX’s total weighting. Last quarter they combined to mine 300.8 metric tons of gold. That was 35.2% of the aggregate world total in Q4’18 according to the World Gold Council, which publishes comprehensive global gold supply-and-demand data quarterly. So for anyone deploying capital in gold or its miners’ stocks, watching GDX miners is imperative.

The largest primary gold miners dominating GDX’s ranks are scattered around the world. 21 of the top 34 mainly trade in US stock markets, 6 in Australia, 5 in Canada, and 1 each in China and the United Kingdom. GDX’s geopolitical diversity is good for investors, but makes it more difficult to analyze and compare the biggest gold miners’ results. Financial-reporting requirements really vary from country to country.

In Australia, South Africa, and the UK, companies report in half-year increments instead of quarterly. The big gold miners often publish quarterly updates, but their data is limited. In cases where half-year data is all that is made available, I split it in half for a Q4 approximation. While Canada has quarterly reporting, the deadlines are looser than in the States. Some Canadian gold miners drag their feet in getting results out.

While it is challenging bringing all the quarterly data together for the diverse GDX-top-34 gold miners, analyzing it in the aggregate to see how they are doing is essential. So each quarter I wade through all available operational and financial reports and dump the data into a big spreadsheet for analysis. The highlights make it into these tables. Blank fields mean a company hadn’t reported that data as of this Wednesday.

The first couple columns of these tables show each GDX component’s symbol and weighting within this ETF as of this week. While most of these stocks trade on U.S. exchanges, some symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each gold miner’s Q4’18 production in ounces, which is mostly in pure-gold terms. That excludes byproduct metals often present in gold ore.

Those are usually silver and base metals like copper, which are valuable. They are sold to offset some of the considerable expenses of gold mining, lowering per-ounce costs and thus raising overall profitability. In cases where companies didn’t separate out gold and lumped all production into gold-equivalent ounces, those GEOs are included instead. Then production’s absolute year-over-year change from Q4’17 is shown.

Next comes gold miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated, hard GAAP earnings, revenues, and cash on hand with a couple exceptions.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. Companies with symbols highlighted in light-blue have newly climbed into the elite ranks of GDX’s top 34 over this past year. This entire dataset together is quite valuable.

It offers a fantastic high-level read on how the major gold miners are faring fundamentally as an industry. Unfortunately they were generally struggling on multiple fronts in Q4’18. The more quarterly reports I read and data I gathered, the more apparent it became that many if not most of the world’s biggest gold miners continue to face serious challenges. That makes GDX itself way less attractive to gold-stock investors.

GDX’s holdings grew much more concentrated over this past year, with the top 34’s total weighting rising from 90.5% in Q4’17 to 94.1% in Q4’18. That is partially due to increased merger-and-acquisition activity driven by big gold miners trying to replace depleting production. For years many have proven unable to replenish mined gold organically, leaving buying other companies the only option to maintain mining tempos.

Production has always been the lifeblood of the gold-mining industry. Gold miners have no control over prevailing gold prices, their product sells for whatever the markets offer. Thus growing production is the only manageable way to boost revenues, leading to amplified gains in operating cash flows and profits. Higher production generates more capital to invest in expanding existing mines and building or buying new ones.

Gold-stock investors have long prized production growth above everything else, as it is inexorably linked to company growth and thus stock-price-appreciation potential. But for some years now the major gold miners have been struggling to grow production. Large economically-viable gold deposits are getting increasingly harder to find and more expensive to exploit, with the low-hanging fruit long since picked.

More and more gold-industry experts believe peak gold is nearing, after which global mine production will start declining. For many years now new deposit discoveries and mine builds have failed to keep pace with depletion at existing mines. So production growth is slowing. According to the World Gold Council’s latest fundamental data, global mine production only edged 0.8% higher in 2018 compared to 5.3% in 2013!

GDX’s major gold miners are the biggest in the world, with access to many billions of dollars of capital to expand their operations. Yet even with those vast resources by his sector’s standards, the top 34 have still failed to grow their production. In Q4’18 they collectively produced 9.7m ounces of gold, plunging a colossal 7.5% YoY from Q4’17’s 10.5m! That is shockingly bad, and the root of the major gold miners’ problems.

Total world gold production per the WGC merely slipped 0.9% YoY last quarter. Incidentally that was just the second YoY quarterly decline in the past 32 quarters, adding more fuel to peak-gold theories. Across all of them growth averaged 2.5% YoY. Seeing the top 34 GDX gold miners’ production plunge at 8.3x the world rate in Q4’18 is very concerning. Many major gold miners are stagnating, retarding GDX’s potential.

Just over half of GDX’s top 34 gold miners, fully 18 of them, suffered average production declines of 8.9% YoY! The worst in terms of impact came from GDX’s largest component Barrick Gold. GOLD’s gold mined fell 5.8% YoY in Q4’18, representing 1/10th of the total drop among the GDX top 34. Barrick is so desperate to buy production to offset its serious depletion that it recently purchased major gold miner Randgold.

That deal completed on January 1st, 2019, so GOLD’s Q4’18 results don’t yet reflect it. Randgold mined 374.6k ounces last quarter, which was actually up an impressive 9.9% YoY. That helps explain some of the big production drop among the GDX top 34. Randgold’s production was included in the GDX top 34 in Q4’17, but of course its stock no longer exists this week when I downloaded GDX’s current component list.

Adding Randgold’s Q4’18 production in cuts the GDX top 34’s production decline to 3.9% YoY. Going the other way and instead removing it from Q4’17’s total leaves the top 34’s mined gold down 4.4% YoY. But that’s still much worse than that overall 0.9% YoY decline in global gold mine production last quarter. As I explained in depth in a mid-February essay, gold-stock mega-mergers won’t solve this depletion problem.

Before Q4’18, Randgold suffered 4 quarters in a row of falling production averaging declines of 7.4% YoY. Barrick’s quarterly production has fallen for 6 quarters in a row, averaging hefty 13.4% YoY drops! Merging depleting major gold miners together doesn’t magically boost their collective production. It just masks production declines for a single year, the first 4 quarters comparing post-merger results with pre-merger ones.

Once those great cross-merger YoY comparisons pass, the relentless depletion in both companies’ gold mines will quickly become apparent again. The larger any gold miner, the harder it is to grow and even just maintain production levels. Because exploration budgets largely collapsed since 2013 when gold plunged and crushed gold stocks, the global pipeline of bigger economic gold deposits to mine has mostly dried up.

GDX’s top-two components have always been Barrick Gold and Newmont Gold. This week together they accounted for 19.5% of its total weighting and a whopping 28.0% of the top 34’s total Q4’18 gold mined! Had Barrick’s and Randgold’s merger been consummated in Q4, GOLD’s production would’ve soared over 1.8m ounces. Newmont didn’t want Barrick to surpass it, so in January it announced it was buying Goldcorp.

GG produced 630k ounces of gold in Q4, which will be added onto Newmont’s production going forward once this deal is done. Had Newmont and Goldcorp been together in Q4’18, this gold-mining behemoth would’ve produced nearly 2.1m ounces! Those levels are staggering, and will really increase these two mega-miners’ dominance over this sector and GDX. These mergers’ pro-forma impact on GDX is massive.

Using Q4’s numbers, Newmont and Barrick would’ve accounted for a colossal 38.8% of the GDX top 34’s entire gold mined including Randgold. Their collective weighting in this leading gold-stock ETF would shoot over a quarter. So the overall GDX future performance will be more dominated by Newmont and Barrick than ever before. If they can’t grow production from such stratospheric levels, they’ll retard GDX’s upside.

With gold deposits increasingly harder to discover, and taking even longer to get permitted and brought into production at ever-higher costs, the biggest gold miners are going to find it impossible to even maintain their outputs. Any production growth is going to come from smaller gold miners, and their stocks will soar to reflect it. Unfortunately the impact on GDX will be muted, since its weightings are tyrannized by the giants.

Kirkland Lake Gold has been one of the best-performing gold stocks over this past year. In 2018 its stock rocketed 69.9% higher as GDX fell 9.3%! The reason investors flocked to KL is it has rapidly grown its gold output, which soared 38.8% YoY in Q4’18. That greatly boosted its sales, operating cash flows, and profits. More gold produced spreads out the big fixed costs of mining across more ounces, amplifying earnings.

No matter how awesome KL’s management has proved, such production growth was only possible from a relatively-low base. KL produced 167k ounces of gold in Q4’17, compared with around 8x that from each Newmont and Barrick. The biggest gains in gold-stock prices won’t come from super-major-dominated GDX, but from smaller mid-tier gold miners. Investors will continue to prize and richly reward production growth.