- Is gold finally due to swoon or can it continue to rally?

- The naysayers point to overbought conditions on the weekly charts, COT reports showing a mammoth short position held by the commercial traders, and the upcoming stock market “crash season”.

- The bulls point to a peaking US business cycle, inflationary and growth-destructive tariffs, a tight job market, an increasingly dovish Fed, strong central bank buying, de-dollarization, out of control government spending and debt, and Chinese investors buying more gold instead of investing in their weak stock market.

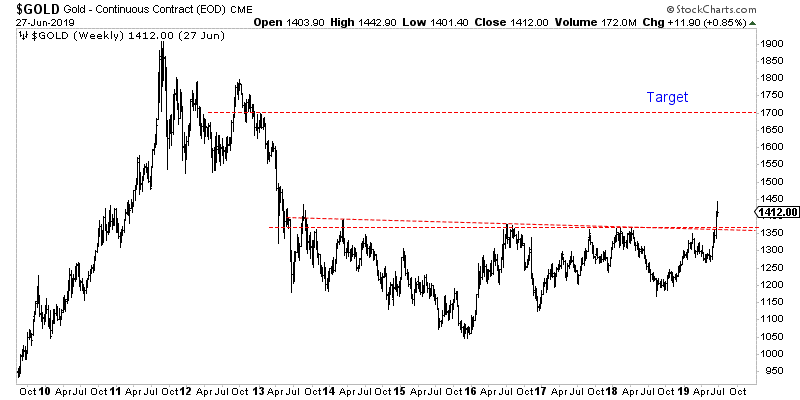

- Please click here now. Double-click to enlarge this awesome weekly gold chart.

- In the big picture, both fundamentally and technically, the bulls clearly have not just the edge, but a mighty wind at their backs.

- What about the short-term picture? Well, please click here now. Double-click to enlarge this daily gold chart. Even in the short-term, I give the edge to the bulls!

- There’s a rectangular drift in play, and per Edwards & Magee (writers of the technical analysis “bible”), rectangles have roughly a 67% chance of consolidating the existing trend, which is up.

- Even if the price were to reverse on a disappointing Fed announcement, there’s great intermediate time frame support at $1360-$1275.

- Institutional money managers are only going to become more enthusiastic about gold, silver, and the miners as the business cycle matures and the Fed becomes more dovish. Any pullback in the gold price now will be bought by their very strong hands.

- What about the stock market? If there’s a crash in September or October, would gold stocks suffer?

- Well, the CDNX index (where the “ultra-junior” miners trade) fell with the Dow during last year’s crash season swoon, but gold and most senior miners blasted higher!

- Please click here now. Double-click to enlarge this spectacular GDX versus US stock market ratio chart.

- From a performance perspective, gold stocks look poised to “destroy” the US stock market.

- A massive inverse H&S bottom breakout is in play.

- Please click here now. Double-click to enlarge this gold versus Nasdaq ETF chart (QQQ).

- In 2011 the dollar began breaking out from a huge base pattern against the yen. Gold began to break down from a huge double top pattern against the Nasdaq. This told me a general risk-on theme was emerging and I suggested investors sell some gold and put the proceeds into the stock market.

- Now, the opposite situation is beginning to take shape and investors should consider allocating some capital from the equity markets to gold, silver, and the miners now…

- And with bigger size when there’s a breakout over 9 on the weekly gold versus Nasdaq chart.

- Please click here now. Double-click to enlarge this GDX swing trade chart. I don’t see any reason for gold stock investors to be nervous, but for those who are, my swing trade service at https://guswinger.com/ is designed to wash those worries away.

- Investors get solid performance and low drawdowns trading NUGT/DUST and SQQQ/TQQQ. I’ve introduced text alerts to investor cell phones as an optional means of sending the trade alerts to busy business people who like the swing trade action.

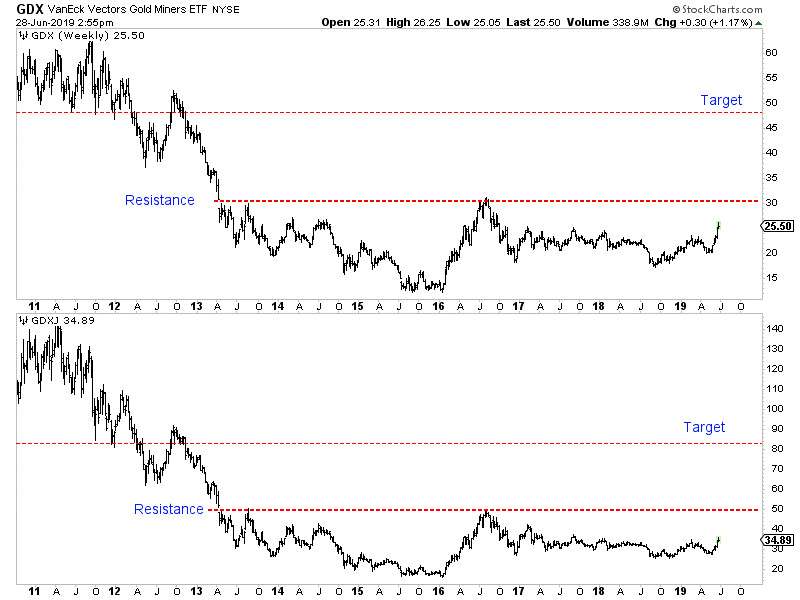

- Please click here now. Double-click to enlarge this GDXJ chart. The GDXJ ETF is called a “junior miners” ETF, but in my professional opinion, it’s really more of an intermediate producer ETF now.

- The current price action is truly exhilarating! An inverse H&S bottom and a marvellous bull pennant pattern both target the $45 price area. The $35-$36 zone is outstanding support.

- Aggressive gamblers can “step up to the JNUG plate” and buy the JNUG ETF. It’s a a triple-leveraged version of GDXJ.

- Whether JNUG, GDXJ, or individual component stocks of the ETFs are used, buyers of size can place a stoploss order under the pennant low to mitigate “Fed Day” announcement risk. Modest-size buyers don’t need stoploss orders. Just buy and prepare to watch GDXJ and its component stocks fly!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free report. “Wave My Golden Flags!” report. I highlight ten of the sweetest gold stocks staging massive bull flag and pennant action on the daily charts. I outline key tactics for investors who are ready to get richer!

Thanks

Stewart Thomson

Graceland Updates

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

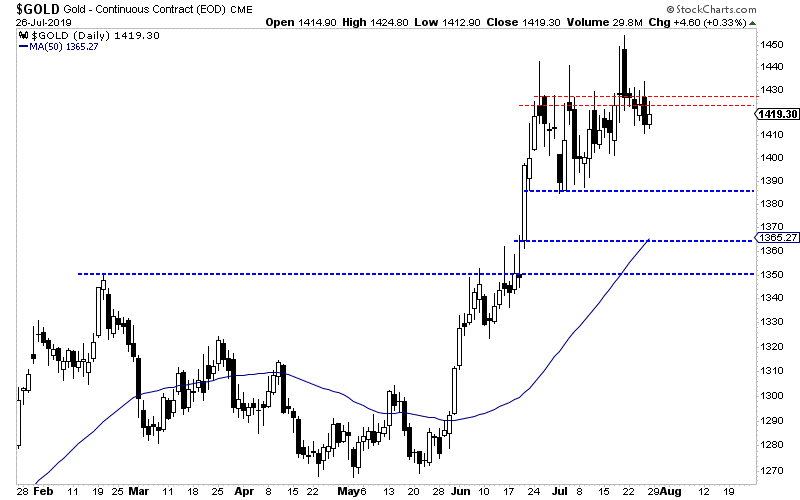

The precious metals sector appears to have started a correction.

It was roaring higher until natural resistance kicked in and the U.S. Dollar grinded its way higher, towards its 2019 high. Factor in the Fed decision this week and it has created a natural “buy the rumor, sell the news” event.

We cannot know for certain what the Federal Reserve will do or even more importantly, how the market will react. But we can take note of key levels in these markets.

Gold has held above $1400/oz but has been unable to break past resistance at $1420-$1425/oz. A retest of $1385/oz is quite possible and so is a test of $1365/oz.

Silver has outperformed Gold since it broke above its 400-day moving average, which provided strong resistance dating back to the end of 2017.

Silver encountered resistance at $16.60-$16.70/oz and could test initial support at $16.20/oz. Below that is strong support at $15.95/oz.

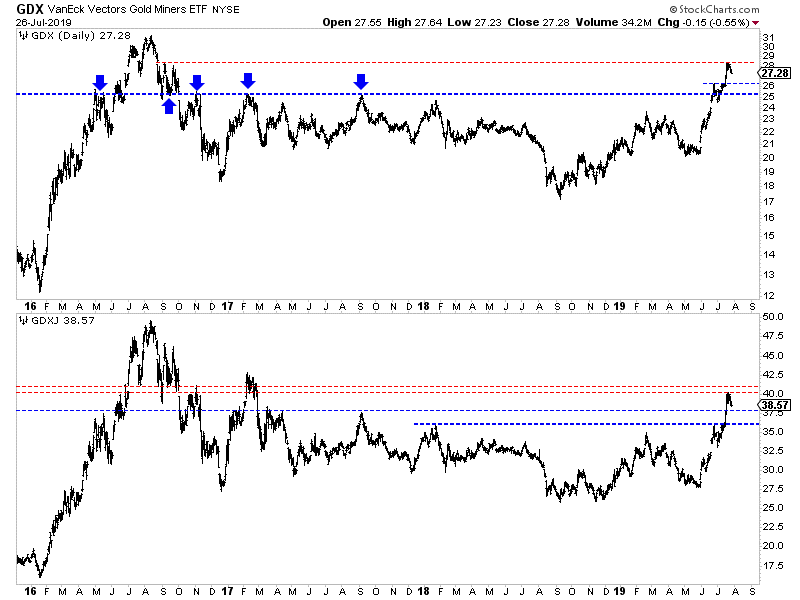

Turning to the gold stocks, we find a clear setup between support and resistance.

GDX, the ETF for large gold producers has resistance at $28 but good support above $25.00, which was previous resistance for nearly three years. Look for initial support around $26.00.

GDXJ, the ETF for the “senior” junior companies, faces resistance at $40-$41. It has initial support around $37.50 with strong support at $36.00.

Regardless of what the Fed does or says, my expectation is precious metals will test these levels and ultimately hold them. The Fed and global central banks want to ease policy and this figures to be more than a one-off.

Precious metals became overbought and a correction is in order.

Investors who smartly positioned in recent months should continue to hold their winners. If the sector continues to correct then look to be a buyer at the aforementioned support levels.

Look to focus your capital on fresh opportunities and value plays that are not very overbought or extended. To learn the stocks we own and intend to buy on this weakness that have 3x to 5x potential, consider learning more about our premium service.

Jordan Roy-Byrne CMT, MFTA

July 30, 2019

Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive.

Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly driven by gold, with the white metal amplifying moves in the yellow metal. Silver has generally leveraged gold by at least 2x in the past. And rarely silver skyrockets as higher prices and bullish sentiment feed on themselves in powerful virtuous circles fueling huge gains.

Silver’s legendary upside is largely the result of it being such a tiny market. Silver’s leading fundamental authority is the Silver Institute. In its latest World Silver Survey covering 2018, it reported that total world demand ran 1033.5m ounces last year. That was worth a mere $16.2b at 2018’s average silver prices, a rounding error in markets terms. That was just 1/11th the size of last year’s world gold demand worth $179.4b!

So when investors grow interested in silver again and start deploying capital, relatively-small inflows in absolute terms catapult silver far higher. This classic dynamic last worked in 2016. In roughly the first half of that year, silver rocketed 50.2% on the parallel 29.9% maiden upleg of this current gold bull. That made for 1.7x upside leverage to gold, remaining on the weaker side historically but still well worth riding.

Through gold suffered a severe correction in the second half of 2016, it still ended that year 8.5% higher. Silver’s 15.1% gain amplified that by 1.8x. The secret to gaming silver is it tends to act like a sentiment gauge for gold. When gold is relatively high and has been rallying, traders start assuming that will persist. And that’s when they want to buy silver. The white metal thrives mostly only when gold psychology is bullish.

In 2017 and 2018 gold fell deeper out of favor. The yellow metal wasn’t performing poorly, but it couldn’t break out to new bull-market highs. And contrarian investing was dying, with stock markets levitating to endless new record highs on hopes for big tax cuts soon and extreme Fed dovishness. With gold apathy stellar, silver didn’t stand a chance. Silver sentiment and thus price performance is totally controlled by gold.

Even though gold rallied a strong 13.2% in 2017, silver lagged at mere 6.4% gains. That 0.5x leverage to gold was terrible. The longer silver underperformed, the more traders capitulated on it and walked away. 2018 was even worse. Though gold only drifted 1.6% lower, silver plunged 8.6% making for horrendous 5.5x downside leverage. Silver wasn’t worth the big additional risk of its serious volatility compared to gold.

Thankfully silver’s dire fortunes started to change in early 2019, when I wrote my original essay on Silver Outperforming Gold. But unfortunately that was short-lived, as silver is slaved to gold. In mid-February the young gold upleg stalled out and reversed lower, after failing to break out to new bull-market highs. That kneecapped silver’s budding outperformance streak, casting it back to the underperformance wasteland.

By June 19th, silver was back to its recent miserable form. It was down 2.1% year-to-date despite gold enjoying a respectable 6.1% YTD rally. While we were taking advantage of the hellish sentiment to buy and recommend fundamentally-superior silver-mining stocks at crazy-low prices in our newsletters, it was hard to write about silver. Virtually no one was the least bit interested, with suffocating apathy universal.

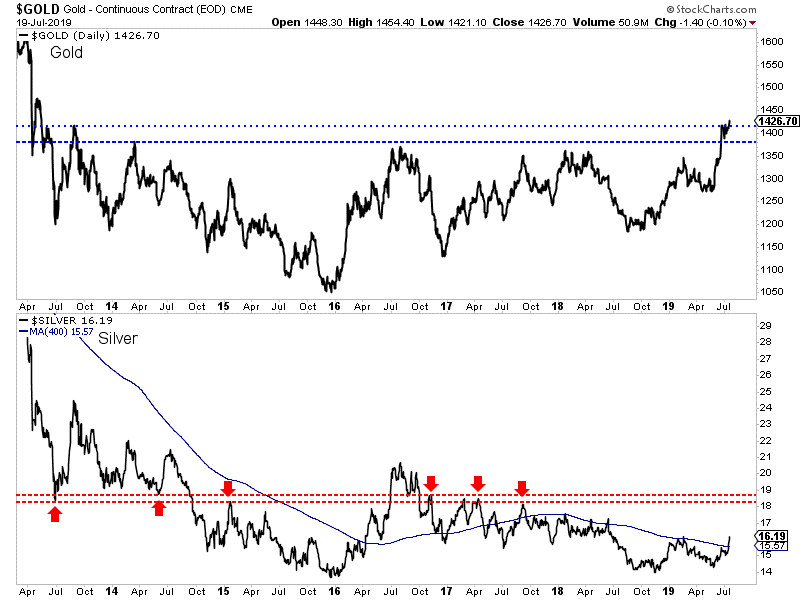

But silver started awakening from its bearish haze on June 20th, kicked in the butt by an extraordinary watershed event. That day gold finally surged to its first new bull-market high since way back in early July 2016, when this bull’s maiden upleg peaked! Gold’s $1389 close was also its highest in 5.8 years, starting to unleash powerful new-high psychology. In the 5 weeks since, that has increasingly infected silver.

Silver didn’t respond immediately to gold’s decisive bull-market breakout. On breakout day it stuck to its languid ways, only rallying 1.8% on a major 2.1% gold up day. The silver price action actually stayed relatively weak for the next several weeks. By July 11th gold was 3.4% higher from the day before that major breakout, while silver slumped 0.3% lower. But something interesting was brewing behind the scenes.

Silver investment demand is notoriously difficult to monitor. The best fundamental data available for this white metal is again from the Silver Institute’s World Silver Survey. But as awesome as that is, it is only published once per year. There is a high-resolution proxy for silver investment demand available daily though, the physical-silver-bullion holdings of the world’s largest and dominant silver exchange-traded fund.

That is the American SLV iShares Silver Trust, which has a huge first-mover advantage after launching way back in April 2006. As of the end of 2018, the Silver Institute’s data showed SLV commanded fully 49% of all the silver held by all the world’s silver ETFs! SLV’s holdings are published daily, and when they climb it reveals American stock-market capital flowing into silver. This dynamic is important to understand.

SLV’s mission is to track the silver price, giving stock traders full silver exposure. But the SLV-share supply and demand is independent of silver’s own. If stock traders are buying SLV shares faster than silver itself is being bought, SLV’s price will decouple from silver’s to the upside. SLV’s managers prevent this by shunting that excess share demand back into physical silver itself. The mechanics are simple in concept.

When SLV prices are being bid up faster than silver, new SLV shares are issued to absorb that differential demand. The capital raised from selling those shares is then used to buy more physical silver bullion. This enables SLV to act as a conduit for stock-market capital to flow into and out of silver itself. When SLV shares are sold faster than silver, this process reverses. SLV holdings reveal silver investment trends!

While silver was drifting sideways to lower in the first half of July and looking unimpressive, American stock investors were starting to buy SLV. Between July 2nd and 9th, SLV enjoyed daily holdings builds averaging 0.7% in 4 out of 5 trading days! At the same time the leading gold ETF’s holdings, which is of course the GLD SPDR Gold Shares, were mostly draws. Silver was attracting investors while gold wasn’t.

With gold consolidating high and largely holding over $1400, precious-metals sentiment was improving. After long ignoring gold and silver, investors were starting to take another look. Silver had not only really lagged gold’s breakout rally since mid-June, but it was radically undervalued compared to its dominant primary driver gold. We’ll explore that shortly. So smart contrarians were starting to shift back into silver.

This didn’t first become evident in silver’s price action until July 15th, just a couple weeks ago. That day silver rallied 1.2% despite gold only edging 0.1% higher. That was peculiar and out of character for silver in recent years, so it could’ve been an anomaly. But it proved otherwise. As of this Wednesday’s data cutoff for this essay, silver has outperformed gold in a major way for 8 trading days in a row! That’s incredible.

On the 16th silver climbed 0.9% while gold fell 0.9%. On the 17th and 18th silver surged 2.6% and 2.3% on 1.5% and 1.4% gold up days. The 19th saw silver only retreat 0.7% as gold dropped 1.4%. Then on the 22nd and 23rd silver rallied 1.0% and 0.2% despite gold’s 0.1% and 0.5% declines. This Wednesday the 24th saw silver climb 1.1% outpacing gold’s 0.6%. Such a strong outperformance streak is important.

Thus in the past couple weeks or so, silver has blasted 9.7% higher despite a mere 1.3% gold rally! That makes for epic 7.4x upside leverage, the kind silver enthusiasts dream about. This outperformance stretch is even more impressive because it was driven by big capital inflows into SLV by American stock investors returning to silver. As of this Wednesday SLV saw strong holdings builds for 6 trading days in a row.

That started with a monster 2.6% SLV build on the 17th, which proved the biggest seen by far since way back in January 2013! Gold largely holding over $1400 rekindled American stock investors’ interest in silver in a way not seen in 6.5 years. Over the next 5 trading days ending Wednesday, SLV’s holdings grew another 0.8%, 1.0%, 2.6%, 0.5%, and 0.5%. This silver-investment-buying streak is pretty amazing.

While silver’s outperformance of gold has exploded only in the last couple weeks, it has totally changed how silver looks since gold’s decisive bull-market breakout on June 20th. As of Wednesday, silver has now rallied 9.3% over that 24-trading-day span compared to gold’s 4.8% gain. That’s right back up to that historical 2.0x-upside-leverage norm. SLV’s holdings enjoyed 13 build days, 11 flat days, and 0 draw days.

They have catapulted SLV’s holdings 12.6% higher since the day before gold’s breakout. Via this leading ETF, American stock investors are now holding 1/8th more silver in absolute-ounces terms in just 5 weeks. Over this same span GLD’s holdings only climbed 7.6%. And it only saw 8 holdings-build days, 5 flat days, and a whopping 11 draw days. Something special, major, and likely pivotal is underway in silver!

Nevertheless, silver remains in an ugly place compared to gold. YTD as of this Wednesday, silver was just up 7.1% compared to gold’s 11.1%. Gold’s $1445 upleg-to-date high achieved on July 18th was its best level seen in 6.2 years. Silver’s own upleg-to-date high of $16.55 this Wednesday was merely a 1.1-year one. So though silver has started to outperform gold again, it has a long way to go to look impressive.

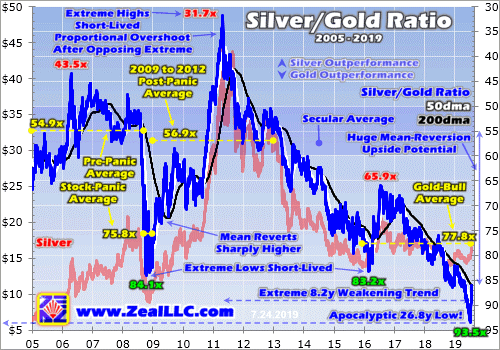

There’s no sugarcoating it, the carnage in silver in recent years has been catastrophic. Thanos himself couldn’t have done worse with a fully-stoned Infinity Gauntlet! While there were a half-dozen silver charts I considered sharing this week, this one is the most telling. It shows the Silver/Gold Ratio over the past decade-and-a-half or so. This SGR is the best measure of whether silver prices are relatively high or low.

The SGR simply divides the daily silver close by the daily gold close, but yields hard-to-parse decimals like 0.0116 this Wednesday. So I prefer to use an inverted-axis Gold/Silver Ratio instead, which is the same thing but offers easier-to-understand numbers like 86.1 mid-week. Silver prices had almost never been lower relative to gold in modern history before recent weeks! Silver is climbing out of a stygian abyss.

Back in mid-June just before gold’s decisive bull-market breakout changed everything, the SGR had fallen to an absurd 90.4x. In other words it took 90.4 ounces of silver to equal the value of a single ounce of gold. That was wildly out of whack with historical precedent. From 2005 to just before 2008’s first stock panic in a century, the SGR averaged 54.9x. From 2009 to 2012 after that panic, it averaged a similar 56.9x.

The SGR had generally meandered in the mid-50s for decades, so miners had long used 55.0x as the leading proxy for calculating silver-equivalent or gold-equivalent ounces. The SGR also experienced great cycles, long secular periods of silver outperformance where the SGR generally fell followed by multi-year spans of silver underperformance where the SGR rose on balance. SGR extremes were short-lived.

As gold surged over this past month, the SGR spiraled higher still to a mind-boggling 93.5x on July 5th. That was an apocalyptic 26.8-year low, the worst silver levels relative to gold since October 1992. That is longer than the average investing lifespan of today’s traders, over a quarter century! And 93.5x isn’t much better than the worst SGR since 1970, 100.3x seen briefly in February 1991. Silver has just been slaughtered.

For an incredible 8.2 years the SGR had been rising on balance, showing chronic underperformance relative to gold. This secular cycle is far-overdue to turn, and after extreme lows historically silver has spent years mean reverting higher relative to gold. 2008’s extraordinary stock panic offers a fantastic recent example of how greatly silver can soar after being battered down to extreme lows relative to gold.

Back in November 2008 in that most-extreme market-fear event seen in our lifetimes, the SGR was crushed to 84.1x. Silver was radically undervalued relative to gold, investors wanted nothing to do with it. Such a great disconnect between silver and gold wasn’t sustainable given their relative market sizes and the ratio at which they are mined. So over the next 2.4 years into April 2011, silver skyrocketed 442.9% higher!

After SGR extremes silver doesn’t just revert to the mean, but overshoots proportionally towards the opposite extreme. The SGR fell as low as 31.7x when that silver bull peaked over $48 per ounce. Odds are the SGR will again overshoot and at least return to the 40s before silver’s next bull fully runs it course. With silver not far off its lowest levels compared to gold in modern times in early July, it has vast room to soar.

Gold’s current bull market was born in mid-December 2015, and is what has driven silver higher during gold-bull uplegs. Since then, the SGR has averaged just 77.8x. That is actually higher than during that wild stock-panic span in late 2008, incredibly extreme! Over the past several weeks or so, the SGR has already started mean reverting falling as low as 86.1x this week. Silver’s upside potential from here is epic.

At $1400 gold and this miserable gold-bull-average 77.8x SGR, silver would need to trade at $18.00. That’s another 9% higher from this week’s levels. But again mean reversions off extremes don’t just stop at the averages, but keep going like a pendulum. That yields an SGR target of 62.1x, implying $22.56 silver at $1400 gold. Silver would have to power another 36% higher to regain those still-pathetic SGR levels.

If gold’s young secular bull persists for years to come as it ought to based on historic precedent, silver is going to climb far higher greatly lowering the SGR. If it just mean reverts back to that longstanding 55.0x average with no overshoot, that means $25.45 silver at $1400 gold. These SGR-mean-reversion-and-overshoot silver-price targets grow far bigger at higher prevailing gold prices and proportional-overshoot SGR lows.

The point of all this is silver is so radically undervalued compared to its primary driver gold that it needs to soar vastly higher to reestablish normal relationships. While silver’s outperformance over the past couple weeks is impressive, it hardly even registers coming off such extreme lows. Digging out of such a deep hole relative to gold, silver needs to rally higher on balance for many months or even years to come!

While investment buying including via silver ETFs like SLV will be the primary driver, silver futures will also play a big role. A couple weeks ago I wrote about gold’s high short-term selloff risk due to how the gold-futures speculators are now positioned, with excessively-bullish bets that are actually very bearish over the near term. A healthy gold pullback or correction would certainly drag silver down with it for a spell.

The most-bullish situation possible for gold- and silver-futures is for speculators to be all-out long upside bets and all-in short downside bets. That leaves them nothing to do but buy. That is 0% longs and 100% shorts. In the latest weekly Commitments of Traders report, specs’ gold-futures bets were running 75% on the long side and 10% on the short side up into their entire bull-market trading ranges. That’s really bearish.

By bull-to-date precedent, gold-futures speculators had room to sell 347.4k contracts but only room to buy 80.5k. That made for an ominous 4.3x ratio of potential selling outweighing potential buying. I bring this up because speculators’ silver-futures positioning was nowhere near as menacing. They are running 66% on the long side and 44% on the short side up into their gold-bull-market trading ranges, much less bearish.

Speculators had room to sell 97.4k silver-futures contracts and buy 65.8k in the latest CoT report, for a way-more-moderate 1.5x ratio of potential selling to potential buying. The takeaway here is silver has a lot more near-term futures-buying-driven upside potential than gold does. Together silver investment buying and silver-futures buying are powerful forces to catapult silver higher. But it all depends on gold.

If gold continues to consolidate high above or near $1400, that will foster the bullish sentiment necessary for silver buying to persist. New-high psychology driving gold investment buying could make this happen. But if something spooks the gold-futures speculators, they have massive room to sell which would quickly cascade and hammer gold lower. That would suck in silver, driving both into healthy short-term corrections.

But once speculators’ excessively-bullish gold-futures bets normalize, gold and silver should be off to the races again with silver really outperforming. So any material weakness should be used to aggressively accumulate physical silver bullion, SLV shares, and stocks of fundamentally-superior silver miners. Their upside potential trounces silver’s because their profits growth really amplifies higher prevailing silver prices.

Again silver soared 50.2% higher in largely the first half of 2016. The leading SIL Global X Silver Miners ETF rocketed a colossal 247.8% higher in essentially that same span! That made for huge 4.9x leverage to silver’s gains. Every quarter I analyze the fundamentals of the major silver miners of SIL, with the latest essay covering Q1’19 results. Now is the time to do your homework before silver really starts running again.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In recent months well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. Mid-week our unrealized silver-stock gains already ran as high as 113.8%!

To profitably trade high-potential gold and silver stocks, you need to stay informed about broader market cycles that drive them. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off summer-doldrums sale! The biggest gains are won by traders diligently staying abreast, always learning.

The bottom line is silver really started outperforming gold again in the last couple weeks. Silver surged dramatically on heavy investment buying, as evidenced by big differential SLV-share demand. This looks like a sea-change sentiment shift getting underway in silver, especially after it was crushed to its lowest levels relative to gold in well over a quarter century. Silver is long overdue to mean revert vastly higher.

Silver effectively acts like a gold sentiment gauge, with investment demand dependent on gold’s fortunes. The longer gold consolidates high or grinds higher, the more silver will be bought. Coming out of such radically-undervalued levels, silver’s future bull-market upside should greatly exceed gold’s. But silver will also get sucked into periodic gold corrections, which can be used as lower entry points to add silver positions.

Adam Hamilton, CPA

July 29, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

- At McDonald’s restaurant, customers can “supersize” their food orders. Can gold supersize its awesome 2019 price action?

- Well, please click here now: https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/07/2019jul23gold1.png Double-click to enlarge.

- The technical action on this gold chart is spectacular!

- Gold has formed a massive pennant formation. There’s no guarantee that it plays out, but if it does the technical target is in the $1560 area.

- A $1560 gold price would turn most gold producers into gargantuan cash cows, and the near-vertical rally already in play in silver would likely become a textbook barn burner.

- Please click here now: https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/07/2019jul23si1.png Double-click to enlarge. A pattern like a double bottom is now in play on the weekly silver chart.

- This pattern suggests the silver rally is just getting started and a breakout over the neckline would target the $18.50 area.

- The Western fear trade for gold is now the “price driver in play” for all the precious metals upside action, but the love trade is also providing solid and consistent support for the market.

- Interestingly, the Indian government tariff taxes of 12.5% have effectively revalued the price of the vast hoards of gold held by Indian citizens by 12.5%.

- In America, real interest rates continue to decline as the business cycle peaks. Any uptick in inflation could create an institutional “feeding frenzy” in gold stocks and silver stocks.

- Please click here now: https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/07/2019jul23realrates1.png Many bond market analysts believe that rate cuts from the Fed could accelerate the issuance of negative-rate bonds… dramatically!

- Please click here now: https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/07/2019jul23gold2.png Double-click to enlarge. Some gold analysts worry about the “large” commercial short position in gold on the COMEX, but I predicted years ago that when gold broke out of the bull continuation pattern… the commercial short position could rise to millions of contracts, with the price still going higher!

- That’s because there are so many institutional money managers getting involved with gold now. The bottom line: Cash pays nothing and has no upside, and a surge in inflation would destroy the bond market and potentially topple the US government.

- In this environment, institutional stock market investors are embracing gold and gold stocks. They are beginning to embrace silver too. Because silver is such a small market, even modest institutional buying is producing vertical price action!

- Another positive aspect to the arrival of institutional investors in gold, silver, and the miners may be of interest to conspiracy buffs who believe in price manipulation.

- I say that because institutional investors have in-house investigators who monitor the market action. They are quick to alert regulators when market trades don’t make sense.

- Whether serious gold price manipulation existed in the past is probably unknowable, but there’s no question that the current market feels “cleaner” and more stable than it did when hedge funds dominated the market.

- The SPDR fund (GLD-NYSE) is now at 825 tons, and the SLV-NYSE silver fund is now at 11,070 tons. Institutions are buying steadily.

- What happens if the Fed disappoints at next week’s key meeting? What happens if there’s no rate cut? Well, since 2014 I’ve talked about all Fed actions being positive for gold.

- Gold rallied on QT and rate hikes and the stock market tanked because of the safe haven bid. Gold also rallied on the recent Fed pause… much more than the stock market did!

- The bottom line: If the Fed doesn’t cut rates at next week’s key meeting the stock market will crash and gold will cash a huge safe haven bid. Everything the Fed does is now win-win for gold.

- Please click here now: https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/07/2019jul23gdx1.png Double-click to enlarge this fabulous GDX chart. I coined the term “flagification” to describe a market so powerful that numerous bull flags appear in succession. That’s happening with GDX and many gold miners now.

- For a look at the important weekly chart for GDX, please click here now: https://gracelandjuniors.com/wordpress/wp-content/uploads/2019/07/2019jul23gdx2.png Double-click to enlarge. If the bull flag on the daily chart plays out, GDX is going to my $30-$32 target zone, and to $37-$40 if the “supersize” bull pennant on the gold bullion chart activates.

- The breakout above $26 on the weekly chart has turned the entire $23-$26 area into a massive support zone, so any failure or churning in the flag/pennant formations is little more than an annoying bearish fly that should soon be swatted away by a growing army of excited institutional buyers.

ttps://gracelandjuniors.com

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Protecting The Profits!” report. I highlight the tactics used by top investors in the 1970s gold market to protect their profits after massive rallies in gold stocks and I apply those tactics to eight key stocks now!Graceland Updates

Stewart Thomson

Graceland Updates

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

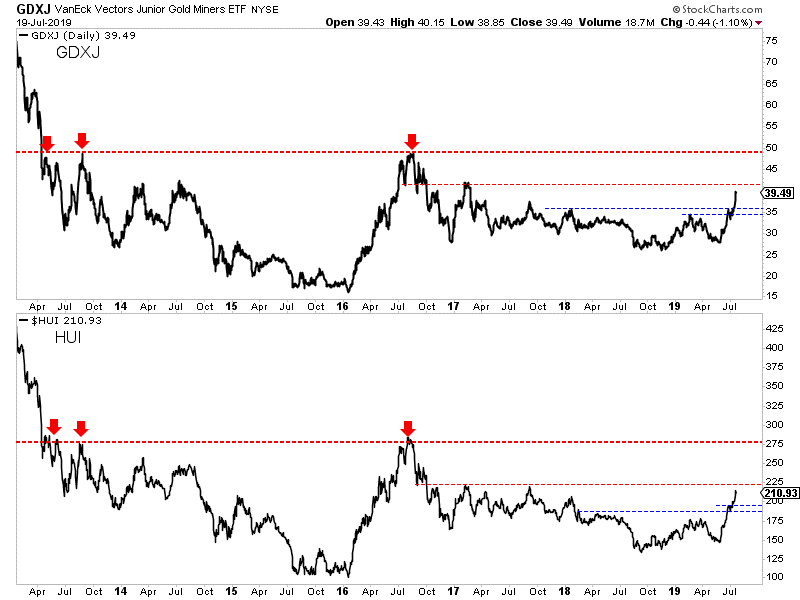

It was a huge week for the gold stocks. GDX gained nearly 7% while GDXJ surged over 10%.

Gold hit $1450/oz after Thursday before selling off Friday. Silver met the same fate on Friday but managed to close the week up over 6% and at a new 52-week high.

Let’s take a look at the current technicals.

Gold closed the week just below $1427/oz. If it remains above $1420-$1425, then it is likely to trend towards $1475/oz, which is the only resistance between $1425 and $1525.

If Gold trades back below $1420 then there is a risk it could test $1380 again.

Silver has taken out resistance at its 400-day moving average in convincing fashion but needs to surpass its February 2019 high. Its next major resistance target is the mid $18s.

Turning to the stocks, we start with GDX which is closing in on its 2016 high. Should Gold trend towards $1475/oz then GDX would likely retest that 2016 high at $31.

Breadth remains strong and so too is GDX’ relative strength. GDX relative to the S&P made a 21-month high and relative to Gold made a 2-year high.

Both GDXJ (juniors) and the HUI (miners only) still have room to go before reaching their 2016 highs.

In fact, both are facing some immediate overhead resistance. For GDXJ which closed at $39.50, that resistance is at $40-$41. For HUI which closed at 211, that resistance is at 220.

The support levels are $36 for GDXJ and 195 for the HUI.

If Gold and Silver maintain current levels, then the immediate bias remains higher and GDX could soon test its 2016 high.

GDXJ and HUI have roughly 30% upside to their 2016 highs. Such a move probably requires a move in Gold to at least $1525/oz.

However, if Friday was the start of a correction then GDX could test $26 and GDXJ could test $36.

For investors in the juniors and seniors, continue to hold winners. If the sector corrects, then look to take advantage of that weakness. If metals and shares maintain these levels then focus your capital on fresh opportunities and value plays that are not overbought or extended. To learn the stocks we own and intend to buy that have 3x to 5x potential, consider learning more about our premium service.

By Jordan Roy-Byrne CMT, MFTA

July 23, 2019

The gold miners’ stocks continue to rally on balance, after a major upside breakout extended their strong upleg. That’s driving mounting interest in this recently-forsaken sector. With the latest quarterly earnings season underway, traders will soon enjoy big fundamental updates from the gold miners. They are likely to report good Q2 results, with improving operational performances supporting further stock-price gains.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the US Securities and Exchange Commission by 40 calendar days after quarter-ends. The gold miners generally release their quarterly reports in the latter half of that window. So Q2’19’s will arrive between late July to mid-August.

After spending decades intensely studying and actively trading this contrarian sector, there’s no gold-stock data I look forward to more than the miners’ quarterly financial and operational reports. They offer a true and clear snapshot of what’s really going on, shattering the misconceptions bred by ever-shifting winds of sentiment. Nearly all fundamental analysis is based off the data gold miners provide in quarterlies.

So for many years I’ve delved deeply into gold miners’ quarterly results. They are the dominant source of information I use to winnow down the universe of gold stocks to the fundamentally-superior ones with the greatest upside potential. Every quarter after their latest earnings season ends, I research and write essays discussing the newest results from the major gold miners, mid-tier gold miners, and silver miners.

Q2’19’s full analyses are coming starting in mid-August once that 40-day post-quarter reporting deadline has passed. But before that I eagerly dive into individual companies’ results as they’re reported, since there’s so much to digest. Even earlier soon after a quarter ends, I start thinking about what gold miners’ latest quarterly results are likely to show collectively. Their aggregate trends can be somewhat predicted.

In high-level fundamental terms, gold mining is a simple business. These companies painstakingly wrest gold from the bowels of the Earth, then generally sell all they can produce at prevailing market prices. So their profits are effectively the difference between current gold levels and operating costs. The former is easy to calculate once a quarter ends, and the latter can be reasonably estimated for this sector as a whole.

Gold’s dramatic bull-market breakout a month ago and high consolidation since have greatly improved sector psychology. But gold’s big surge came late in Q2, minimizing its full-quarter impact. The early quarter was rough, with gold slumping to a new year-to-date low near $1271 in early May. The average gold prices in April, May, and June were $1286, $1284, and $1361. Gold was mostly sucking wind last quarter.

Thus Q2’19’s overall average gold price of $1309 was just a meager 0.4% better than Q1’s $1303. So the gold miners’ latest quarterly results aren’t going to get much help from gold’s young surge. That will really change in the current Q3 if gold can hold these high levels. With Q3 about 1/5th over, gold has averaged an awesome $1407 so far! So the higher-gold boost to gold-stock earnings is coming, but not in Q2.

Gold stocks really leverage higher gold prices because their mining costs are largely fixed. Quarter after quarter mining operations generally require the same levels of infrastructure, equipment, and employees. The vast majority of any gold mine’s future cost structure is actually determined during its planning phase, when engineers decide which ore to mine, how to excavate it, and how to process it to recover the gold.

Every quarter after results I analyze the all-in-sustaining costs reported by the world’s gold miners. These are the best measure of what it really costs to produce an ounce of gold. Over the past four quarters, the major gold miners of the leading GDX VanEck Vectors Gold Miners ETF reported average AISCs of $856, $877, $889, and $893. That in turn yields a trailing-four-quarter mean of $879 per ounce, a key cost metric.

With $1309 average gold in Q2’19 and AISCs likely near $879, that implies the large gold miners as an industry likely earned $430 per ounce last quarter. That’s actually a decent improvement considering the flat quarterly gold prices. Though gold averaged a similar $1303 in Q1, the GDX miners’ average AISCs that quarter came in a bit higher at $893. That implied $410 profits, which Q2 results should easily exceed.

$430 is up 4.9% quarter-on-quarter despite the relatively-flat average gold price! This is really impressive sequential profits growth relative to the broader stock markets, where earnings are stalling out. But if that is all we could hope for, I would’ve written on a different topic this week. The gold miners’ Q2’19 earnings are likely to well exceed expectations for an entirely-different reason, portending even-higher gold-stock prices.

Most traders assume gold miners produce their yellow metal at fairly-steady rates year-round. That sure makes sense given how capital-intensive gold mining is, how individual mines’ capacities and throughputs to process ore are fixed, and how expanding mines’ outputs takes years of construction. But surprisingly global gold mine production actually varies considerably quarter-to-quarter! This should really boost Q2 earnings.

The best global gold fundamental data is published by the World Gold Council, also on a quarterly basis. These Gold Demand Trends reports are essential reading for all gold-stock speculators and investors, as these miners are ultimately just leveraged plays on gold. The latest GDT covering Q1’19 was released in early May, with Q2’s due out in early August. One key number GDTs report is world gold mine production.

That happened to run 852.4 metric tons in Q1, nearly a third of which came from the major gold miners of GDX. Analyzing global gold mine production each quarter since 2010 reveals some fascinating quarter-to-quarter output trends. Over the last 37 quarters, calendar Q1s have seen gold mined average a sharp 7.2% QoQ plunge from the immediately-preceding calendar Q4s! Not a single Q1 saw sequential output growth.

From 2010 to 2019 Q1 gold mined fell 7.2%, 6.9%, 7.6%, 11.2%, 8.8%, 3.3%, 8.7%, 5.7%, and 5.6% from the respective Q4s. These drops and their uniformity across radically-different gold-price environments is stunning. For some reason the world’s gold mines suffer universal declines in their outputs early in calendar years. Why? This curious industrywide Q1 production slump results from an interplay of several factors.

Most gold miners run their accounting on calendar years. So early in new years they have new capital budgets to spend on maintaining and enhancing their existing operations. If they temporarily shut down their mills for repairs or minor upgrades, Q1s are usually when they do it. Weather plays a role too, as the majority of the world’s gold mines are in the northern hemisphere with the majority of the world’s land masses.

Winter creates operational challenges for gold mines, ranging from extreme cold to heavy snow or rains depending on their latitudes and elevations. So in addition to short planned shutdowns to work on infrastructure, adverse weather can impair operational efficiencies. But the main reason global gold-mine outputs plunge in Q1s is due to ore-grade-management decisions made by mine managers to maximize bonuses.

Gold deposits are not homogeneous, ore grades vary widely within them. So managers must choose which ore to mine, when to run it through their mills, and how to mix it with ores from other locations. The mills that crush the gold-bearing rock into small-enough chunks to recover the metal have fixed capacities in tonnage-per-day terms. So the less gold contained in the ore processed, the less gold the mines recover.

Mine managers often choose to dig through lower-grade ores, or run lower-grade ores through their mills, in Q1s. They save the higher-grade ores for later in calendar years. They often claim these decisions are related to early-year capital budgets being spent to improve outputs later in years. But there’s probably more to it, since this happens so universally across the world’s gold mines. Incentives have to play a role.

Gold-mine managers are often partially compensated based on how their stock prices are faring. This is usually a big factor in annual bonuses calculated near year-ends. These bonuses are the most-variable part of compensation, and can greatly boost income. After long years of study and talking with some of these guys, I’m convinced they choose to take any gold-output hits early in years to engineer strong finishes.

Q1 results are reported by mid-Mays, a long way out from year-ends. That’s the least-beneficial time in bonus terms for strong output to boost stock prices. Q2 results released by mid-Augusts and Q3 results published by mid-Novembers are far-more important. So mine managers feed their fixed-capacity mills better-grade ore mixes in Q2s and Q3s, after early-year maintenance is finished and summer weather is favorable.

Thus in calendar Q2s since 2010, global gold mine output according to the World Gold Council surged an average of 5.4% sequentially from Q1s! Over the past 9 years Q2s have seen huge QoQ global-output gains of 6.7%, 7.7%, 6.3%, 7.1%, 6.1%, 5.7%, 0.7%, 4.9%, and 3.4%. There has not been a single down Q2 in this span despite wildly-different gold-price environments. Such uniformity reveals deliberate planning.

Over roughly the past decade, world gold mine production has averaged -7.2% QoQ in Q1s, +5.4% in Q2s, another hefty +5.3% in Q3s, then just +0.5% in Q4s. That Q4 stalling is pretty telling too, as those Q4 results are typically released by mid-Marches which doesn’t affect annual bonuses when those quarters were underway. The gold miners contrive their best output reporting from late Julies to mid-Novembers!

So in these upcoming Q2’19 results, the gold miners are likely to report production about 5% higher than Q1’s! That big sequential output boost really increases overall corporate earnings. And it has another key benefit of reducing all-in sustaining costs. AISCs are calculated by spreading the costs of gold mining across all ounces produced. So the more gold mined, the lower the unit costs of producing it that quarter.

A year ago in Q2’18, the GDX gold miners’ average AISCs dropped a big 3.2% sequentially from the prior quarter’s to $856 per ounce. So it is certainly reasonable to expect Q2’19’s AISCs to retreat 3% or so from Q1’s $893, which yields $866 per ounce. Subtract that from Q2’19’s average gold price of $1309, and it yields likely earnings of $443 per ounce. That is 8.0% higher quarter-on-quarter from Q1’s results!

That’s conservative too. As detailed in my essay on the GDX gold miners’ Q1’19 results, that quarter’s average AISCs were skewed higher by a single anomalous outlier. That company expects costs to greatly retreat in Q2. Excluding it, the GDX gold miners averaged considerably-lower $874 AISCs in Q1. A 3% reduction to that on higher Q2 output leaves an excellent $848 AISC target, implying big $461 profits!

That represents a major 12.4% quarter-on-quarter surge, which should excite traders anytime. And with gold-stock sentiment already growing far more bullish thanks to gold’s bull-market breakout, there’s a good chance Q2 earnings’ positive psychological impact will be amplified. As long as gold hangs in there and doesn’t sell off, the gold miners’ stocks have real potential to rally considerably on good Q2 results.

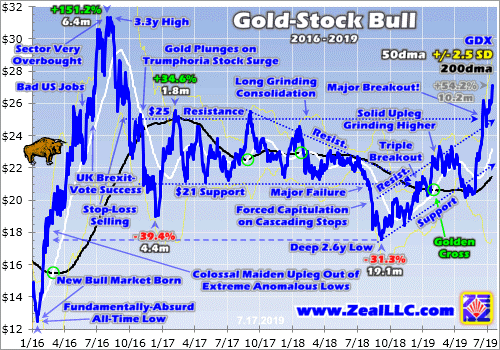

A couple charts offer some quick perspective. Gold’s breakout drove a major decisive upside breakout in gold stocks too as measured by their leading GDX benchmark. That dominant ETF is rendered in blue here, superimposed over its key technical lines. As of the Wednesday data cutoff for this essay, GDX had powered 54.2% higher in 10.2 months in its upleg to date. But gold-stock prices still remain relatively low.

Mid-week GDX hit $27.09 on close, its best levels in 2.8 years. But that remains well below gold stocks’ bull-to-date peak of $31.32 in early August 2016. The gold stocks ought to at least exceed those levels, which is another 15.6% higher from here. Good Q2 results interpreted through the lens of increasing sector bullishness should be enough to fuel a bull-market breakout. Gold argues for higher gold-stock levels.

Back in mid-2016 when GDX peaked at $31.32, gold merely hit $1365 at best. That was just after a quarter when the GDX gold miners’ AISCs averaged $886 per ounce. Gold was considerably higher this week, hitting $1425. And it has averaged $1408 for nearly a month since its bull-market breakout. So the higher prevailing gold prices this summer, and lower AISCs, should support much-higher gold-stock prices.

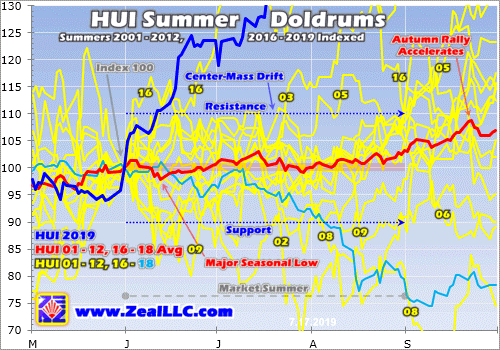

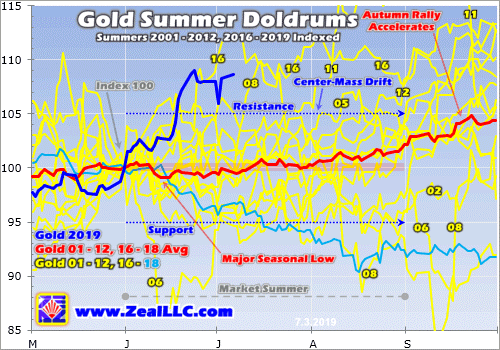

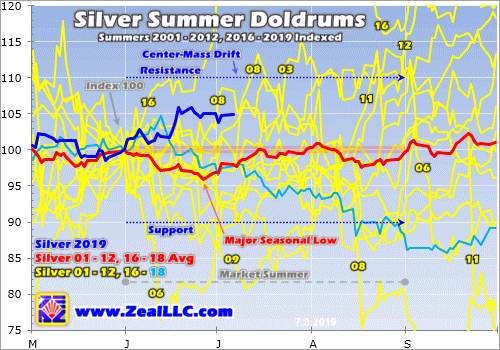

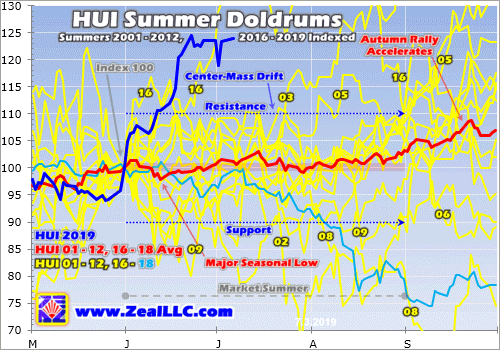

Showing just how strong gold stocks are and how unique today’s situation is, this last chart looks at gold stocks’ average performances in modern bull-market summers. I explained this indexed chart in depth in an essay on gold summer doldrums a couple weeks ago. The yellow lines show where the older HUI gold-stock index traded in past modern gold-bull-market summers, and the red line averages them together.

This year’s action is rendered in dark blue, revealing gold stocks’ best summer by far since 2016 after this gold bull’s massive maiden upleg! In the middle of this week the HUI rocketed 32.3% higher summer-to-date, literally off this seasonal chart I’ve gradually built up over the years. If there was ever a summer where gold stocks could punch out to new bull highs, this one is it. Their upside momentum is incredibly strong.

All this gold-stock bullishness aside, it is always wise to be wary when everyone else is getting excited. The potential for gold stocks to surge to new bull highs on good Q2 results is totally dependent on what gold does over the coming 6 weeks or so. While gold has shown awesome resilience in consolidating high and mostly holding $1400 over the past month, the gold selloff risk is high due to gold-futures positioning.

I wrote a whole essay last week explaining this in depth. In a nutshell, gold-futures speculators dominate short-term gold price action. Their current bets on gold are excessively-bullish, warning that their capital firepower to buy gold is nearing exhaustion. They are effectively all-in on long upside bets, and all-out on short downside bets. That leaves them vast room to sell hard on the right catalyst, pushing gold sharply lower.

There’s a chance new-high psychology can ignite enough investor gold buying to overpower and absorb any spec gold-futures selling. But realize gold-stock fortunes are still slaved to gold as always. Gold has to stay high to support new gold-stock highs. If gold materially falters and slumps into a healthy pullback or correction within an ongoing bull, the gold stocks will follow it lower regardless of how good Q2 results prove.

Buying high on strong upside momentum is always tempting, as that’s when traders feel the best about any sector. Bullishness and capital inflows soar as stocks power higher. But over time far-larger gains are won by instead buying low, adding positions when sectors are out of favor. The later you buy gold stocks in any upleg, the smaller their potential gains and the higher the odds a major selloff is looming.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In recent months well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. Mid-week their unrealized gains ran as high as 123.9%, 123.5%, and 116.5%!

To profitably trade high-potential gold stocks, you need to stay informed about the broader market cycles that drive them. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off summer-doldrums sale! The biggest gains are won by traders diligently staying abreast so they can ride entire uplegs.

The bottom line is the gold miners’ just-starting Q2’19 earnings season should prove impressive. That’s no thanks to gold, as its awesome bull-market breakout came too late last quarter to push its average price significantly higher. But the gold miners are still likely to collectively report sharply-higher Q2 output, which is normal after Q1’s deep production slump. That will also naturally lead to proportionally-lower costs.

Growing production combined with lower costs at slightly-higher gold prices should yield big profits growth for the gold miners. Their Q2 results will be more closely watched and better received since psychology is shifting much more bullish in this sector. That should fuel big gold-stock buying as long as gold holds up. The yellow metal has proven resilient so far, but faces an ominous overhang of gold-futures selling pressure.

Adam Hamilton, CPA

July 22, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

- It’s the ultimate “no-brainer” that serious American GDP growth (in the 6% range or higher) can only happen by eliminating the PIT (personal income tax) for the middle class.

- QE and low interest rates incentivize pathetic levels of debt-oriented GDP growth while incentivizing the government to get more reckless with the money that is borrowed and extorted from citizens as taxes.

- Elimination of the PIT would instantly turn the debt-bombed middle class of America into a “savings and purchasing power machine”.

- With higher rates and elimination of the PIT, government would be forced to shrink, banks would eagerly loan out the savings to mainstream business, and the middle class would consume with savings rather than credit card debt.

- The bad news: The PIT won’t be eliminated, and government worship of debt, QE, low rates, and extortion is not going away.

- The good news: That means the gold price is going higher!

- To view the key buy and sell levels for gold, please click here now. Double click to enlarge.

- Gold investors should be eager buyers of gold, silver, and the miners in the $1390 gold price area or on a breakout above $1440.

- Please click here now. Double-click to enlarge this key weekly gold chart.

- The most likely scenario for gold now is a rally towards $1500-$1523, followed by a significant pullback that will probably look a lot like the late 2009 pullback.

- What actually happens is almost certainly going to depend on the actions and statements from the Fed at the July 31 meeting.

- If the Fed isn’t as dovish as expected, gold could pullback towards $1320 quite quickly. A half point cut and a dovish outlook could produce a dramatic “target overshoot” for gold. A surge to $1750 would be quite realistic in that situation.

- Whatever happens, $1390, $1360, and $1320 are all key buy zones and $1440, $1500, and $1750 are all decent profit booking targets.

- Please click here now. Double-click to enlarge this daily silver chart. Like Rodney Dangerfield, silver doesn’t get much respect, but that’s because inflation has yet to really surge.

- Having said that, the silver chart is beginning to look quite bullish. A breakout from an inverse H&S bottom pattern has occurred, and the pullback was flag-like.

- The target of both the flag and the H&S pattern is the $16.50 area highs of February.

- From a risk-reward perspective, silver is beginning to look superior to the US stock market.

- Please click here now. Double-click to enlarge this swing trade chart.

- Swing trade enthusiasts can get in on the leveraged ETF action for gold stocks and the Nasdaq with my guswinger.com service. We are also carrying a massive Barrick position. Signals are available by email (and cell phone text for traders with US cell phone numbers).

- For an analytical look at the GDX daily chart, please click here now. Double-click to enlarge. I use a 24hour chart for GDX. On this chart, a surge above $26.45 would be a fresh buy signal not just for GDX, but for most intermediate and senior gold producers.

- Please click here now. Double-click to enlarge this silver stocks ETF chart.

- Note the recent superior performance of the silver miners compared to silver bullion.

- There is an H&S bull continuation pattern forming on the chart and I believe that pattern makes an “upside blast” to my $34 target price zone highly likely.

- The bottom line for gold and silver stocks: The action is solid, and the action is now!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Ultimate Gold Market Portfolio” report. I highlight tactics to assemble a pure performance portfolio of global metal miners, with key action points for each holding!

Stewart Thomson

Graceland Updates

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

Gold and gold stocks especially continue to shrug off bits and pieces of bad news.

No escalation in the trade war? The selloff lasted one day and the sector rebounded strongly the following day.

Strong headline jobs number? Again, the weakness was a buying opportunity.

This past week there was more.

The June CPI report came in hotter than expected, which could mitigate the degree the Fed eases in the future. Also, bond yields in the US have risen the entire week.

No dice.

Gold closed the week at $1412/oz while the gold stocks closed just inches from new highs on the daily charts.

Turning to the technicals of the gold stocks, we see both underlying and relative strength.

Nearly 95% of the large miners closed above the 200-day moving average. Meanwhile GDX relative to both the S&P 500 and Gold is above a rising 200-day moving average. The GDX to Gold ratio is at a 2-year high while the GDX to S&P 500 ratio is very close to a new 52-week high.

GDXJ is lagging GDX a bit but it is coming around.

90% of the ETF closed above the 200-day moving average. That is the highest reading in nearly three years.

GDXJ relative to the S&P and Gold has turned bullish and is holding above upward sloping 200-day moving averages.

The immediate upside targets for GDX and GDXJ are GDX $27.50 and GDXJ $37.50. The next level of targets would be GDX $30 and GDXJ $41.

Gold has endured some selling in the $1420-$1425/oz range but has remained bid around $1400/oz. A daily close above $1420/oz would remove much of the resistance from here to the low $1500s.

For investors in the juniors and seniors, continue to hold your winners and focus your capital on fresh opportunities and value plays that could move with the next leg higher. To learn which stocks we own and intend to buy that have 3x to 5x potential, consider learning more about our premium service.

Gold surged dramatically in recent weeks, powering higher to a decisive bull-market breakout. Gold’s first major secular highs in years have really improved sentiment, with bullishness mounting. But gold-futures buying fuel is largely exhausted, after the colossal amount expended to catapult gold back over $1400. That leaves this metal at high risk of suffering a major selloff, a healthy correction in an ongoing bull market.

Even the most-powerful bull markets flow and ebb, taking two steps forward before one step back. Gold is certainly no exception. At best in late June, its current bull extended to modest 35.4% gains over 3.5 years. Those weren’t linear, the path to gold’s recent breakout high was quite volatile. It included a 29.9% upleg, a 17.3% correction, a 20.4% upleg, a 13.6% correction, and today’s upleg running 21.2% at best.

This alternating repeating bull-market pattern is simple, uplegs are inevitably followed by material selloffs often extending into correction territory. Periodic corrections are essential to keep bulls healthy, working off the excessive greed that builds as uplegs peak. That risks sucking in too much capital too soon, prematurely burning out bulls. Corrections rebalance sentiment, bleeding away greed to extend bulls’ longevity.

Even though they are inevitable, normal corrections stress out the majority of traders. The selling taints their psychology and clouds their perspectives of longer-terms trends in play. They fret bulls are dying, and sell out too early and too low. Instead corrections should be embraced, as they offer the greatest opportunities to buy relatively low within ongoing bulls! Entering near correction lows amplifies gains.

While gold’s current bull clocked in at 35.4% total in late June, its three major uplegs added up to much-larger 71.5% gains. Traders had the potential to more than double gold’s headline gains by attempting to buy relatively low later in corrections and sell relatively high later in uplegs! Although impossible to game bull-market swings’ major lows and highs precisely in real-time, trading near them really boosts capital growth.

The reason gold faces high risk for its next major selloff today is speculators’ current positioning in gold futures. Unfortunately spec gold-futures trading has a wildly-disproportional influence over short-term gold price levels. The dominant reason is the extreme leverage inherent in gold futures, which greatly multiplies that capital’s impact on gold prices. This unfair reality has sorely vexed the gold market for decades.

When a normal investor buys gold outright, $1 of capital exerts $1 of buying pressure on the gold price. That’s the way markets are supposed to work. That can be extended with margin in the stock markets, which has had a hard legal limit of 2.0x since 1974. $1 of capital using maximum margin to buy shares in the leading GLD SPDR Gold Shares gold ETF can exert $2 of buying pressure on gold. That’s still reasonable.

But gold-futures trading is way out in its own extreme realm. Each gold-futures contract controls 100 troy ounces of gold. At this Wednesday’s data cutoff for this essay, gold closed at $1417. So each contract wields gold worth $141,700. An investor would have to put up $141,700 to control that much gold, or $70,850 using stock-market-legal-limit leverage on GLD shares. Futures speculators only need $4,000!

That’s no typo, this week the CME Group only requires traders to have $4,000 cash in their accounts for each gold-futures contract they want to trade. That is absurd, enabling extreme maximum leverage of 35.4x! That means a fully-margined gold-futures speculator can exert $35 of buying or selling pressure on gold with each $1 deployed. That temporarily outguns investors, even though they have vastly more capital.

The Federal Reserve has capped stock-market leverage at 2.0x for 45 years because extreme leverage has extreme risks. At 35.4x, a mere 2.8% gold move against speculators’ gold-futures bets would wipe out 100% of their capital risked! This constant threat of ruin forces these traders’ focus to an ultra-myopic short-term span, days or weeks at most. All they can do is ride gold’s immediate momentum, piling on.

As if arbitrarily declaring $1 of gold-futures capital should have up to 35x the influence on gold prices as $1 invested outright isn’t ridiculous enough, it gets worse. Unscrupulous traders can wield gold futures’ extreme leverage like a weapon to manipulate gold prices at key technical and sentimental junctures. One way is spoofing, slamming the market with huge gold-futures orders that are canceled before being executed.

This is not theoretical. In late June the U.S. Department of Justice levied $25m of criminal fines on Merrill Lynch Commodities for this very behavior! And that’s just the tip of the iceberg for gold futures’ extreme leverage being abused to defraud normal investors. This seriously needs to be legally capped at vastly-lower levels. The DoJ’s actual press release did a great job explaining how gold-futures spoofing works.

“…beginning by at least 2008 and continuing through 2014, precious metals traders employed by MLCI schemed to deceive other market participants by injecting materially false and misleading information into the precious metals futures market. They did so by placing fraudulent orders for precious metals futures contracts that, at the time the traders placed the orders, they intended to cancel before execution.”

“In doing so, the traders intended to “spoof” or manipulate the market by creating the false impression of increased supply or demand and, in turn, to fraudulently induce other market participants to buy and to sell futures contracts at quantities, prices and times that they otherwise likely would not have done so. Over the relevant period, the traders placed thousands of fraudulent orders.” These crooks should be in prison!

Compounding gold futures’ gold-price impact, the American gold-futures price is gold’s global reference one. So gold-futures trading moving the gold price heavily influences and sometimes totally controls the entire gold market’s psychology! Investors are motivated to buy and sell gold outright based on what is happening in gold futures. It’s impossible to understand and game gold without closely watching futures.

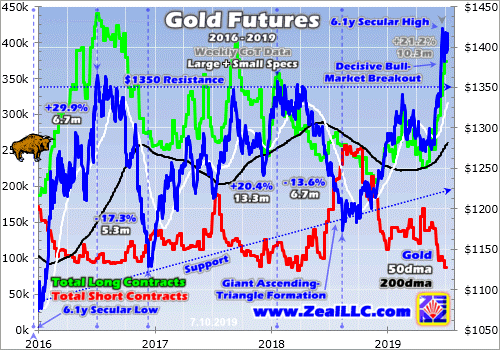

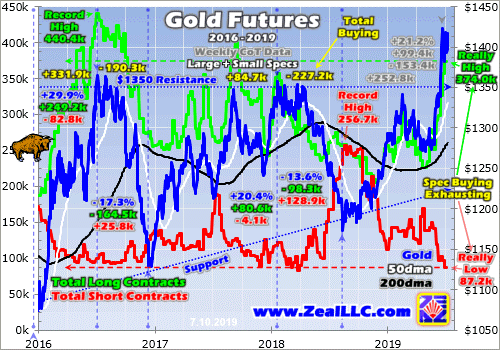

I had to break my chart into two parts today, lest it get too busy to parse. These superimpose gold’s price through its current bull market over speculators’ gold-futures positioning. Reported weekly by the CFTC in its famous Commitments of Traders reports, specs’ long contracts or upside bets on gold are shown in green while their short contracts or downside bets are rendered in red. They usually dominate gold action.

The wildly-disproportional influence on gold prices by speculators’ gold-futures trading is critical for all investors to understand. Let’s start with this gold bull itself, the cadence of its uplegs and corrections. Its maiden upleg erupted in mid-December 2015 out of deep 6.1-year secular lows in gold, and ultimately blasted up 29.9% in 6.7 months by early July 2016. Major selloffs inevitably follow major uplegs in any bull.

So gold plunged 17.3% over 5.3 months into mid-December 2016 in a severe correction. That was way bigger than normal, greatly exacerbated by Trump’s surprise election victory in early November that year. With Republicans controlling the presidency and both chambers of Congress, stock markets soared on hopes for big tax cuts soon. That crushed gold demand, as fully 5/8ths of that correction came after the election!

While ugly, gold remained in a bull market since that massive selloff didn’t cross the -20% threshold for a new bear market. Gold quickly rebounded from those deep lows and gradually powered to another nice bull-market upleg, up 20.4% over 13.3 months leading into late January 2018. This gold bull’s second major upleg was followed by its second major correction, a 13.6% drop over 6.7 months by mid-August 2018.

That birthed today’s third major upleg, which had extended to 21.2% at best over 10.3 months by late June. This past month saw gold get exciting again after decisively breaking out of its years-long giant ascending-triangle technical formation to surge to major new bull-market and secular highs. This bull’s pattern has been upleg, correction, upleg, correction, upleg. What comes next in this series is obvious.

Gold is at high risk for another major selloff, potentially a full-blown correction over 10% again, because of speculators’ gold-futures positioning. This next chart illuminates what the specs were doing during each of this gold bull’s uplegs and corrections including today’s newest one. These hyper-leveraged traders with their outsized impact on gold prices have effectively exhausted their near-term buying, threatening big selling!

This gold bull’s initial upleg in largely the first half of 2016 was massive, the biggest in this bull so far at 29.9%. That was partially fueled by gold-futures speculators buying a staggering 249.2k long contracts and buying to cover another 82.8k short ones! There are two kinds of buying and two kinds of selling in gold futures, and each set has the same price impact on gold. Thus they can be lumped together for analysis.

Specs can buy new gold-futures contracts to establish long positions, the normal way to buy. But they also buy to cover and close previously-established short positions. The upward pressure on gold from buying longs and covering shorts is identical. On the selling side they can sell their own existing longs, or effectively borrow gold-futures contracts they don’t own to short sell them. Both types hit gold the same way.

Speculators’ total gold-futures buying in this gold bull’s first upleg ran a mind-boggling 331.9k contracts! That’s the equivalent of 1032.4 metric tons of gold. For comparison, total global gold investment demand in the first half of 2016 ran 1091.6t per the World Gold Council’s latest fundamental data. That epic spec long buying catapulted their total upside bets to an all-time-record high of 440.4k contracts as that upleg peaked!

Keep these numbers in mind. This gold bull’s greatest upleg soared 29.9% higher on 331.9k contracts of total buying by gold-futures speculators. That forced their total longs to their highest levels ever seen of 440.4k contracts. As I’ll discuss shortly, today’s latest gold upleg is skating ever closer to those extreme levels. The ice gets pretty thin in that rarefied air of likely gold-futures buying being essentially exhausted.

This gold bull’s first major correction was largely driven by specs reversing that huge long build in largely the second half of 2016. Note the green spec-longs line above collapsed symmetrically to its massive surge in the preceding upleg. Specs dumped 164.5k long contracts and short sold 25.8k more over that severe correction’s exact span. That adds up to 190.3k contracts of total selling, the equivalent of 592.0t.

During gold-bull uplegs the green spec-longs line rises while the red spec-shorts line falls. Then in following corrections that reverses, the green line falling while the red one rises. Gold-futures buying and selling is heavily driving these major bull-market cycles in gold, and that’s not going to change until regulators wake up and radically curtail gold futures’ extreme inherent leverage. Gold’s second upleg straddled 2017.

That was somewhat peculiar, as the spec gold-futures long buying of 80.6k contracts and short covering of 4.1k only totaled 84.7k. That wasn’t much considering gold’s strong 20.4% upleg gains. But realize that gold upleg effectively topped much earlier in early September 2017. Its later upleg peak was marginal. As gold challenged its $1350 bull-market resistance, total spec longs soared as high as 400.1k contracts!

This gold bull’s second correction mostly unfolded during the first half of 2018, and was a textbook-perfect example of heavy spec gold-futures selling. Their green longs line plunged by 98.3k contracts, while their red shorts line rocketed an enormous 128.9k contracts higher. That correction bottomed last August as total spec shorts soared to their own all-time-record high of 256.7k contracts! That portended the next upleg.

Back in early September, I wrote an essay on the “Record Gold/Silver Shorts!”. Published when gold still languished way down at $1196, I concluded then “gold and silver soon soared on short-covering buying following all past episodes of excessive and record short selling. There’s nothing more bullish for gold and silver than extreme shorts! … Record futures shorts are the best gold and silver buy signals available.”

Speculators’ collective gold-futures positions provide both excellent buy signals near major gold lows and excellent sell signals near major gold highs. Smart contrarians get really bullish on gold when specs are really bearish as evidenced by relatively-low longs and relatively-high shorts. And it is just as prudent to get short-term bearish on gold when specs are excessively bullish with relatively-high longs and -low shorts.

This is exactly the situation we’re in today, and it’s growing ominously extreme. This gold bull’s third upleg powered 21.2% higher at best so far as of late June, propelling this metal to a new 6.1-year secular high of $1423. This awesome decisive-bull-breakout upleg was again fueled by enormous gold-futures buying by speculators. They added 99.4k long contracts, while buying to cover a staggering 153.4k short ones!

That adds up to total buying of 252.8k contracts as of gold’s latest peak in late June, or the equivalent of 786.3 metric tons of gold! That’s relevant because it is already 76% of the total gold-futures buying that unfolded during this gold bull’s huge maiden upleg in early 2016. Back then popular gold psychology was waxing really bullish, fostering that extreme gold-futures buying. Getting that high again today is a tall order.

The current gold-futures picture is even worse. While gold hit its latest interim high in late June, the gold-futures speculators kept on buying since. The weekly CoT reports are published late Friday afternoons current to the preceding Tuesdays. So the latest data available this week is current to last Tuesday July 2nd. That saw still more big spec buying, they added another 16.5k longs and covered another 10.2k shorts.

That extends this upleg’s total spec long buying to 115.9k contracts and short covering to 163.6k, making for a larger 279.5k total. Thus today’s upleg has already seen speculators buy 84% of the gold-futures contracts that they did during early 2016’s massive maiden upleg! That doesn’t leave much room to keep on adding more longs and covering more shorts to propel gold to major news highs in the coming weeks.

As of last Tuesday, total spec longs were already way up in nosebleed territory at 374.0k contracts! Out of the last 1070 CoT weeks since early 1999, only 2.2% saw spec longs higher. And that is getting closer to their all-time-record high of 440.4k in early July 2016. While they could conceivably go higher, that’s a hard ceiling until proven otherwise. Gold-futures speculators and their capital are finite, relatively small.

Out of all the world’s traders, only a tiny fraction are willing to run extreme 35x leverage and risk ruin on being slightly wrong on gold’s near-term direction. New gold highs really don’t mint sizable numbers of new gold-futures speculators either, as the risks are so crazy. And this small pool of gold-futures traders really don’t control much capital compared to broader markets. They’d be irrelevant without their extreme leverage.

So at some point gold-futures buying pressure literally exhausts itself. All the specs who want to be long gold have already bought in, expending all their available capital firepower. We can’t know in advance if it will happen at 375k longs, 400k, 425k, or 450k, but odds are it will be somewhere around there. Once the specs are all-in, all they can do is sell to start unwinding their excessively-bullish bets. That will hammer gold.

This relatively-young gold bull has seen three prior episodes where specs liquidated high longs, as seen in the falling green line above. Those were during this bull’s two corrections and a milder pullback in late 2018. Gold fell sharply each time, and this next episode of major spec long selling won’t prove different. At their latest 374.0k levels, spec longs are really high today with little room to buy and tons of room to sell!

The near-term gold risk is compounded by the fact spec shorts are also really low, just 87.2k contracts as of the last CoT report. That’s just a hair over the lowest levels of this entire bull market, 82.5k seen in late March 2018. So spec short-covering buying isn’t likely to go much lower, and in any case has a hard limit as these downside bets get closer to zero. Like spec long buying, spec short covering is largely exhausted.

Total spec gold-futures longs approaching bull-market and all-time-record highs, coupled with total spec gold-futures shorts just over bull-market lows, is very bearish for gold over the near-term! Remember by necessity these guys are short-term momentum followers, their extreme leverage will slaughter them if they are on the wrong side of gold for long. When gold noses over, their selling will intensify and cascade.

It certainly has the potential to snowball forcing another correction-grade gold selloff over 10%, which equates to a demoralizing sub-$1281 gold price. We might get lucky, the bullish new-high psychology could retard gold-futures selling. If the normalization of specs’ gold-futures bets is very slow, gold could see a milder pullback largely consolidating high. But we can’t bet on that based on all the bull-market precedent.