The question most gold bugs are probably asking themselves right now is this: How high must gold bullion go before the gold stock ETFs stage their own key breakouts and rally alongside gold?

- The answer, quite simply, is: Higher than the price is today. Disappointment and surprise are part of investing.

- So is diversification, and at the 2008 lows I was emphatic that the US stock market had to be bought. Now, I recommend investors lighten up, but don’t go 100% to the sidelines.

- Stocks, bonds, real estate, and gold are assets. They are not casino chips. Buy them modestly on price weakness and sell them modestly into price strength. It’s really that simple.

- Please click here now. Double-click to enlarge. Gold looks fabulous. It closed above the September highs yesterday and that’s significant.

- Please click here now. Double-click to enlarge this weekly chart. The big picture for gold, both technically and fundamentally, is superb.

- The Coronavirus is a serious matter, but it’s simply the newest of many positive drivers for gold. Government debt is the big one. Demographics in the West (and in China) is also a concern.

- Every month, more big-name money managers are buying gold as a respected asset, and rightly so!

- It’s important for young investors to stay away from people who have a negative view of gold. Keep a positive attitude and everything will be fine.

- Please click here now. India’s budget announcement is just days away and the gold industry is again pushing the government to cut its draconian import tax.

- I’m adamant that the tax is the main cause of the decline in GDP growth, from almost 10% to under 5%. That’s because the tax kills the spirit of Indian citizens. Once an entrepreneur’s spirit breaks, productivity inevitably declines.

- Prime Minister Modi is under substantial pressure to reverse the economic decline, so he’s likely to be more open to reducing the duty than in previous years. Western gold bugs should cheer for a duty cut, but don’t count that egg until it hatches.

- Please click here now. Double-click to enlarge this GDX weekly chart. There’s an ascending triangle in play with a nice $50 price target.

- It’s important the investors change with the times. What happened in the past is not what is happening now. For example, during the run to the 2011 highs, I was adamant that investors should focus on bullion more than the miners.

- Now the main focus should be on the miners.

- From the early 2016 lows in the $12 area, GDX has outperformed gold bullion. While bullion is up about 60% from those lows, GDX is up about 140%.

- For now, it’s a stock picker’s market. Unknown miners are soaring while a lot of the “good ‘ole boys” (the main holdings of ETFs) are struggling.

- Please click here now. Double-click to enlarge. This is another look at the GDX weekly chart. A massive bull flag on the GDX weekly chart is in play.

- Some patience is required, because weekly chart patterns take time to develop and activate.

- Conspiracy buffs may worry that the “Deep State” (Creep State?) doesn’t want to see gold stocks shooting higher if the US stock market falls. In this scenario, the Creep State wants the government and central banks to be the sole “economic saviours” for the people. Not gold, and certainly not mining stocks.

- That’s possible, but I think failed investors are also trying to get rid of gold stocks they bought years ago, and that’s helping create the GDX flag pattern. These investors are “weak hands”, but not as weak as the investors who sold out into the 2016 area lows.

- I believe this weak hand selling is almost done, and the flag pattern supports my prediction.

- Please click here now. Double-click to enlarge this GOAU chart. I like the “KISS” principle; keep it simple, superstar! For GOAU, buying in the $15 area or on a breakout over $18 is probably the best strategy an enthusiastic investor can employ right now.

- A pullback to $15 offers value, and a breakout over $18 offers excitement! Another tool that investors can use, quite frankly, is fine wine or mineral water. Savour the time as gold stocks trade sideways. Sip a drink and enjoy the GDX bull flag development and GOAU range trade action… then cheer boisterously as the upside breakouts occur!

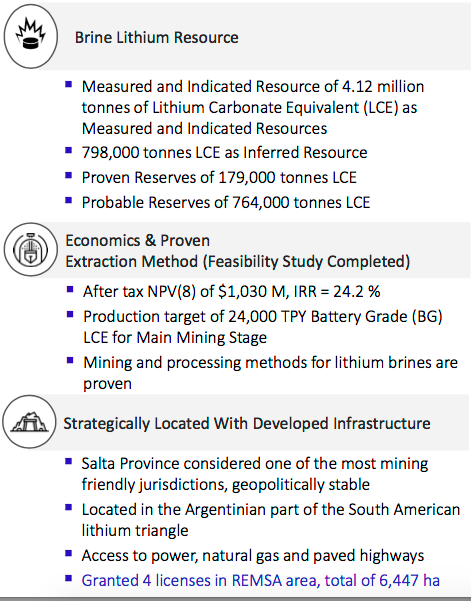

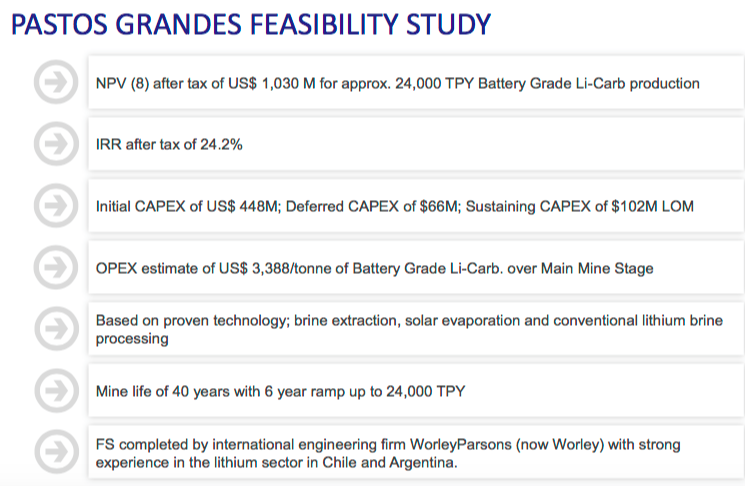

Earlier this month, the Mining Court of Salta granted Millennial Lithium’s (TSX-V: ML) / (OTCQX: MLNLF) Argentine subsidiary four mining licenses on its 100%-owned Pastos Grandes project in Salta province. Readers may recall that Millennial recently delivered a Bank Feasibility Study (“BFS“) and expects to reach initial production in 2022 (subject to funding & permits), ramping up to nameplate capacity of 24,000 tonnes LCE/yr. by mid-decade.

Farhad Abasov, president & CEO, commented:

“Millennial is pleased to have received four mining licenses which comprise ~97% of the property area at Pastos Grandes. Millennial expects the final license to be granted in the near future. The company continues to actively advance its three-tonne-per-month lithium carbonate plant & pilot evaporation ponds. Millennial is moving forward with financing, off-take and other key strategic initiatives with large industry players.”

This news comes on the heels of the October announcement that the National Mining Secretary of Argentina granted a Federal Fiscal Stability Certificate (“FFSC“) for Pastos Grandes. The Certificate outlines the tax regime, plus additional benefits bestowed on the Project, and officially confirms a reduction in the corporate income tax rate from 30% to 25%.

CEO Abasov commented,

“The granting of the FFSC assures the tax & additional benefit terms under which we can operate a lithium carbonate production operation. Receipt of the FFSC confirms our confidence that mining projects in Salta have the support of all levels of government.”

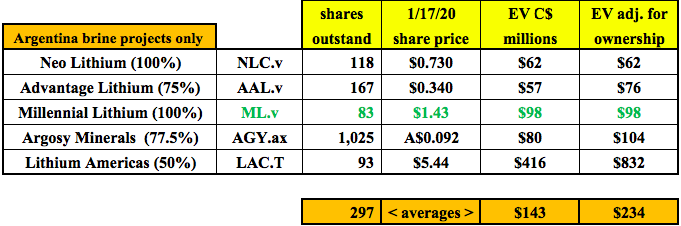

This means that, like Australian-listed, Galaxy Lithium’s Sal de Vida and Lithium Americas’ / Ganfeng’s 50/50 JV (Cauchari-Olaroz) brine projects in Argentina, Millennial’s Pastos Grandes has both a BFS & Fiscal Stability package.

At a time when many lithium brine projects in Chile & Argentina are moving very slowly — (or are stalled) — it’s clear that Millennial’s management team is working closely with all stakeholders to successfully advance Pastos Grandes.

Unlike most peers, Millennial has been blessed with ample cash liquidity. Even today it’s sitting on ~$23 million, enough to last well into 2021 if necessary.

Exciting times ahead….

Next is the lining up of strategic / financial partners, signing off-take agreements, raising construction capital, construction of ponds & plant and first production — expected in 2022. That’s about 12-18 months behind Lithium Americas’ JV project. Importantly, Millennial will greatly benefit from valuable lessons learned from Lithium Americas’ & Galaxy’s development progress, as well as expansions underway at Livent Corp. & Orocobre.

Chile’s Albemarle & SQM, and Argentina’s Livent, Orocobre, Galaxy & Lithium Americas are public companies. Problems with ponds or processing facilities at those companies will become known to Millennial’s technical team. Therefore, there’s a decent chance that mishaps at other projects can be avoided. Sometimes there are benefits to not being a first mover.

In addition to benefiting from the learning curve others are ascending, Millennial will enjoy regional infrastructure that is being built and/or expanded; roads, rail, power lines, natural gas pipelines, etc. Mining equipment & service providers are setting up offices to serve companies including Lithium Americas / Ganfeng, Livent, Orocobre, Galaxy, POSCO, Neo Lithium, Argosy Minerals, Advantage Lithium & Millennial.

Readers should not take for granted the fact that Millennial owns 100% of its project. By contrast, Advantage Lithium owns 75% of its flagship project, Argosy Minerals owns 77.5%, Lithium Americas, 50% and Orocobre Ltd., 66.5% of their respective projects.

Owning 100% of Pastos Grandes, with a BFS & Fiscal Stability pact in place, greatly enhances management’s ability to fund construction. Selling a meaningful portion of the project could raise a substantial amount of capital. That, combined with debt financing and (possible) advance payments from off-take agreements, would minimize the need for excessive equity capital.

Important de-risking events to continue in 1h 2020….

In speaking with CEO Farhad Abasov, he and his Board believe that news on one or more parts of a funding package could come within 3-6 months. Management is speaking with global industrial companies, some of which have already done substantial due diligence.

A few interested parties would like to see a staged ramp-up to minimize cap-ex. So, instead of moving to 24,000 tonnes LCE/yr. by 2025-26, getting to 10,000 tonnes and remaining at that level — only expanding if/when market conditions warrant. In that scenario, cap-ex could be reduced from US$448.2 million to under US$300 million. Then, operating cash flow could be deployed to partially fund an expansion from 10,000 to 24,000 tonnes at a later date.

Also, a few prospective partners have lithium extraction / processing technologies, or access to technologies, that (if they work at commercial-scale) could further optimize Millennial’s operating flow sheet, potentially enhancing project economics. In some cases, the need for evaporation ponds would be eliminated.

Giant auto & battery manufacturers can very comfortably afford to fund projects like Millennial’s with cap-ex requirements of around half a billion USD$. Although we haven’t seen much of that yet, it’s coming. Look no further than Benchmark Mineral Intelligence’s running tally of lithium-ion battery mega-factories.

Benchmark Mineral Intelligence has been tracking the number of global mega-factories for years. The number has soared, currently standing at 115.

Ranked by size, the top 10 global automakers; Volkswagen, Daimler, Toyota, Ford, BMW, GM, Hyundai, Tesla, Honda & Ferrari have an average EV of about US$135 billion. Any of these companies could fund even the largest lithium projects in the world. Yet, I estimate that fewer than ten new projects, brine, hard rock or clay-hosted, (>20,000 tonnes LCE/yr.) are likely coming online by 2025.

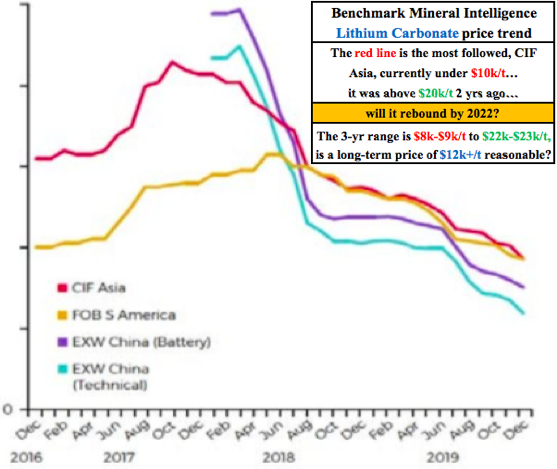

Lithium prices below US$10,000/tonne unlikely to last

One of the main reasons for such negative sentiment in the lithium junior space has been the decline in lithium prices from unsustainably high levels above US$20,000 / tonne. However, now below US$10,000 / tonne, prices may have overshot to the downside. Many analysts & pundits believe that 2020 or 2021 will mark a bottom in the three-year slide in prices.

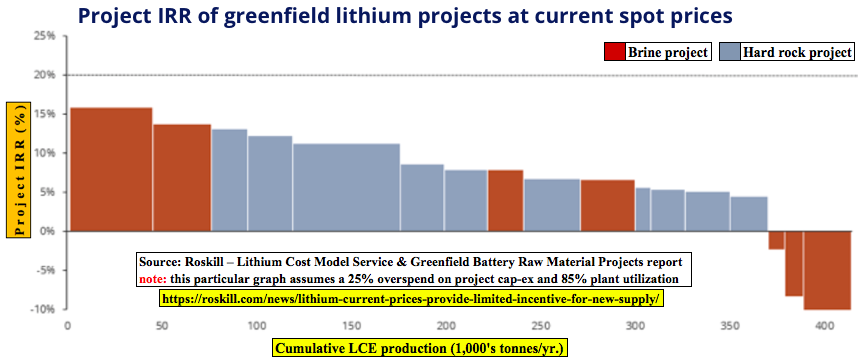

In the chart below, Roskill demonstrates why prices are likely to improve. At current spot levels, all advanced-stage hard rock & brine projects in the pipeline come in at under a 16% IRR. Some projects have negative IRRs; the average is closer to 5% than 10%.

Millennial is poised for a great decade, and the 2030s could be even better. Management expects Pastos Grandes to be next in line in Argentina after Lithium Americas / Ganfeng. Any project, anywhere in the world, that comes to market and ramps up over the next five years should enjoy strong demand for its lithium offerings.

A major global supply source (about 1/3 of the market) is experiencing unexpected bottlenecks, uncertainty & delays. In Chile’s Atacama salar, both Albemarle & SQM had planned massive expansions to lithium carbonate production, upwards of a tripling from 2018 to 2021. Two years into these expansions, annual production has hardly budged.

More uncertainty and caution is expected as local communities have convinced a Chilean environmental court to uphold claims of excessive water use by SQM & Albemarle, seriously threatening their expansion plans. Therefore, this news should be supportive of lithium prices in the mid-to-longer term.

Conclusion

Millennial Lithium has an excellent asset, more advanced (BFS-stage) than all but 2 or 3 global brine projects, with relatively low upfront cap-ex compared to other mining & metals projects. Producing a metal with expected annual demand growth of 15% (or more) over the next 10 years. Millennial has over $20 million in cash on its balance sheet.

Not many significant projects could possibly commence production by 2022. Not many at all, besides Lithium Americas & Galaxy. No new operations are coming in Chile in the next 3-5 years, a small handful in North America, (Bacanora, Standard Lithium). If lithium demand really takes off, few companies on the planet are better positioned to capture that need than Millennial Lithium.

Adjusted for ownership interests in their respective flagship projects, all but Lithium Americas trade at similar valuations. Any of these companies that successfully advance towards production [secure cornerstone investor(s), off-take agreement(s), commencement of construction, etc.] offer the potential for significant share price gains. Notice that Lithium Americas’ valuation is about four times that of the others.

Millennial is trading at just one-fourth the valuation, but could be only 12-18 months behind Lithium Americas. Is this 75% discount warranted? Lithium Americas is fully-funded on its 50% JV project and construction is well underway. Millennial owns 100% of its project, has ample cash liquidity, no debt, a BFS, 4 of 5 mining licenses have been granted and has secured a signed Federal Fiscal Stability Certificate.

If one believes like I do that lithium prices will rebound, Millennial Lithium (TSX-V: ML) / (OTCQX: MLNLF) could be an excellent way to benefit from the rebound.

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Millennial Lithium., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Millennial Lithium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

AX1 Capital Corp. retained Epstein Research for a six-month advertising campaign. AX1 Capital is closely affiliated with Millennial Lithium. It is 100%-owned by a single individual who has a contract for services with Millennial Lithium. This individual owns 150,000 restricted share units and a similarly modest number of warrants in the company. Therefore, readers should consider Epstein Research [ER] to be biased in favor of Millennial Lithium. Peter Epstein of [ER] does not own any shares, warrants, options or restricted share units of Millennial Lithium.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

- Chinese New Year buying and more deaths in war-torn Yemen have ignited yet another solid rally in gold.

- Please click here now: https://gracelandupdates.com/

wordpress/wp-content/uploads/ 2020/01/2020jan21gold1.png Double-click to enlarge. Gold is staging a breakout from an irregular bull flag pattern and doing so from strong support in the $1550-$1530 zone. - I’m projecting a near-immediate pullback to that support zone, and then an erratic rally to the $1613 area highs.

- There are reports that the massively indebted US government has tried to kill yet another Iranian military man (Abdul Reza Shahlai).

- Iran-backed rebels may be seeking revenge for US meddling. They just staged an attack on Saudi-backed Yemeni soldiers.

- As long as the US stock market continues to rise, Western mainstream media won’t want to rock the boat with anything more than minimal coverage… of what is obviously the most horrifying humanitarian crisis on Earth.

- Clearly, gold investors have a different view of the situation.

- Please click here now: https://gracelandupdates.com/

wordpress/wp-content/uploads/ 2020/01/2020jan21gold2.png The WGC (World Gold Council) has just published some fabulous statistics about gold. - Regardless of age, citizens of the world trust gold more than fiat, and what’s particularly significant… is that this is also true in the Western nations of Germany and America.

- Please click here now: https://gracelandupdates.com/

wordpress/wp-content/uploads/ 2020/01/2020jan21gold3.png Double-click to enlarge this weekly chart for gold. - Gold investors should feel very comfortable with their holdings. In fact, I will emphatically make the case that gold bullion investors have less to worry about now than at any point in the past 100 years.

- Government size, spending, and debt levels are “off the charts” in almost every major nation. Gold investors can sit comfortable because rather than reigning in the irresponsible actions of governments, central banks are promoting even more madness, with QE and rate cuts!

- What about the stock market? Well, the money elite at Davos appear concerned. They are looking at private equity. There’s a slow transition in the US stock market from strong hands to weak.

- The weaker hands are sure they will get out before it turns bad. I’m less confident than they are in their ability to do that. For now, the stock market doesn’t appear to be at risk of a crash, but there is limited upside.

- I recommend that investors own some positions in the US stock market, but don’t get carried away with it.

- That’s because America is at a point where government size, debt, and demographics make it very difficult to produce GDP growth above 1%… without even more debt and more government spending.

- Please click here now: https://gracelandupdates.com/

wordpress/wp-content/uploads/ 2020/01/2020jan21private1.png The elite are diversifying into private equity, and a lot of it is going to be Asia-oriented. This could speed up de-dollarization. - When the elite question publicly traded sector stocks and bonds in a high debt environment, “private money” like gold and bitcoin can be superior investments.

- Please click here now: https://gracelandupdates.com/

wordpress/wp-content/uploads/ 2020/01/2020jan21block1.png Double-click to enlarge this exciting bitcoin chart. A lot of the “alt” coins carry enormous risk, and they can be shorted on some of the exchanges. Bitcoin itself looks good. - There’s a bull wedge breakout in play on the weekly chart and a number of institutional investors have become more interested in getting in on the bitcoin action.

- The miners? Well, there is more risk with the miners than with bullion, but overall risk there has diminished dramatically as well. The AISC (all-in sustaining costs) of a lot of miners is vastly under $1400/ounce.

- Companies are in pretty good shape, and those engaging in excessive dilution are quickly shunned by investors.

- Please click here now: https://gracelandupdates.com/

wordpress/wp-content/uploads/ 2020/01/2020jan21miners1.png Double-click to enlarge this GOAU chart. As I projected, a pullback began at the $18 area highs, and it’s now halted near the dotted middle Keltner line. Once the price moves over $18, I expect GDX, GDXJ, SIL, and most individual miners to join the upside fun. - Mining stock investors will soon feel as comfortable as gold investors feel today… holding bullion rather than fiat!

Strong drill results have confirmed & expanded the Bend Vein target on Scottie Resources’ 100% controlled Bow property. During September, the Company completed 878 meters of diamond drilling, two km NE of the 100%-owned past-producing Scottie Gold Mine located in the Golden Triangle (“GT“) of northwest British Columbia, Canada.

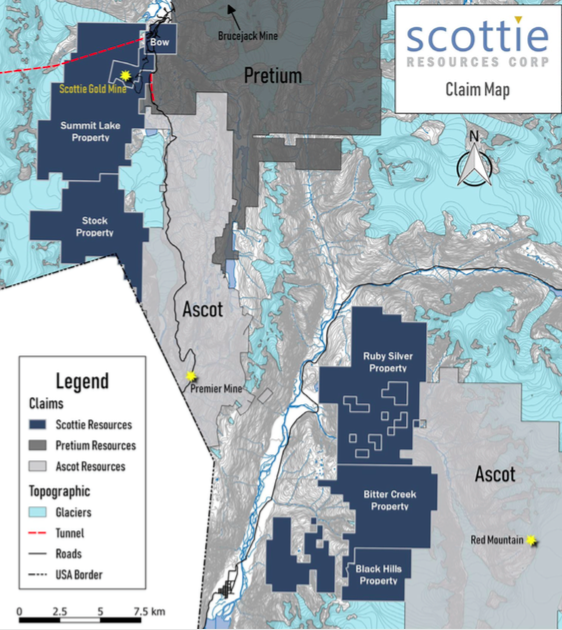

Readers are reminded that Scottie Resources Corp. (TSX-V: SCOT) owns or controls 18,500 hectares, all in the GT, across seven properties, contained in two groups of contiguous parcels. Some properties border Ascot Resources (between Ascot’s Premier Mine & Red Mountain projects), others border Pretium Resources’ property south of the world-class, high-grade, operating Brucejack mine. Pretium’s enterprise value (“EV“) is $3.3 billion.

Very high-grade gold at Bow, Scottie Gold & Summit Lake properties

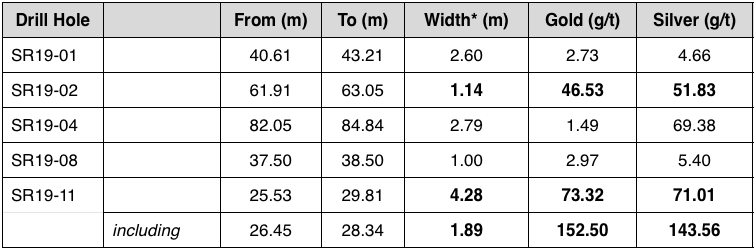

Drill hole SR19-11 hit an interval of 73.3 g/t gold (“Au“) and 71.0 g/t silver (“Ag“), or (74+ g/t Au Eq.) over 4.3 m, (true width 80%-90%). That blockbuster interval included 1.9 m of 152.5 g/t Au plus 143.6 g/t Ag, equal to (154+ g/t Au Eq.). Additional drill results are expected as soon as this week. Importantly, all of the reported intervals to date are near-surface, between 25 & 85 m in depth. The best intercept in this latest batch is between 25.5 & 30 m.

According to Scottie’s CEO & president Bradley Rourke,

“These new assays confirm the superb results of previous studies and demonstrate a truly under-explored high-grade gold & silver target. Past drilling on the Bend Vein only probed to a vertical depth of ~55 m. Our drilling this season proves that the mineralized structure extends deeper. We substantially increased the strike length of known mineralization. Drilling in the 2020 season will allow us to further prove the scale of this structurally-controlled, high-grade vein deposit.”

Scottie’s technical team integrated historical and recent (2018 / 2019) exploration work into new structural models to better understand the geometry of mineralization. Prior to the Company’s 2019 drill program, Bow’s Bend Vein had only 1,525 m of drilling on it. No exploration-style drilling had been done to test along the Bend fault structure to assess the potential of a bigger system.

Management is thrilled that drilling in 2019 substantiated the very high grades contained in the historically known ore block, and extended the structure both at depth and along strike. The drill campaign (so far) has already shown gold mineralization expanding east an additional 375 m. 2020 is off to a great start! Over the past year, management has achieved excellent bang for their exploration buck, with more results any day now.

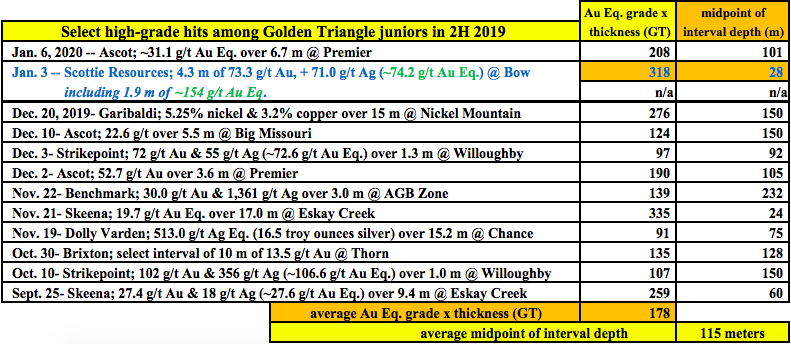

Previous drilling on the Bend Vein returned the following select high-grade assays.

Notice that drill hole SR19-11, mentioned above, had a [grade x thickness] of 318. Compare that to these other [high-grade] intervals in the GT in 2019. Also, the midpoint of each interval’s depth is provided. Scottie’s blockbuster interval was found at 28 meters. The average depth of peer intervals is 115 meters.

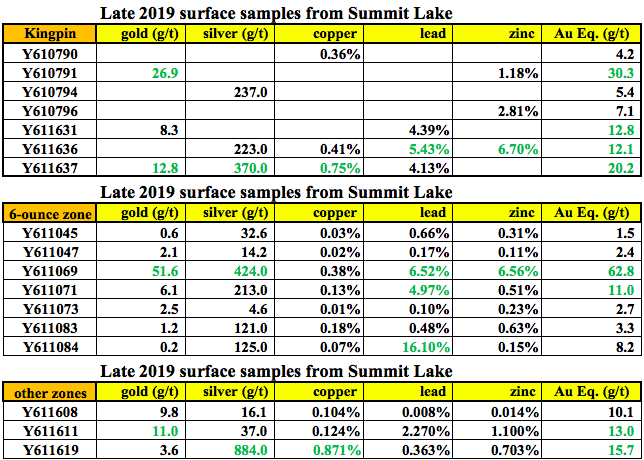

Surface grab samples at Summit Lake look very promising….

CEO Rourke & VP exploration Thomas Mumford, PhD are ecstatic over the latest drill results, and also recent surface samples from the much larger Summit Lake property.

The above surface (grab) samples were reported three weeks ago. The best eight (in green) range from 11.0 to 62.8 g/t Au Eq., and average 22.2 g/t Au Eq. There are high-grade showings of copper, lead, zinc & silver, (884 g/t = 28.4 troy oz./t Ag). Summit Lake, Bow and the past-producing Scottie Gold mine total 5,672 hectares. As can be seen in the map above, the top half of this three-property contiguous block borders Pretium.

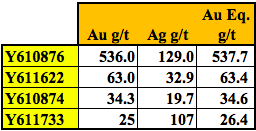

These impressive Summit Lake samples were reported about a month after even more exciting samples were announced on November 14th. The best four samples are listed below. They come from the newly discovered Domino zone on the 100%-owned Scottie Gold mine property.

Referring to the Domino zone, VP of Exploration Dr. Thomas Mumford commented,

“These initial sample results are exciting, their distribution and high-grade nature fit spectacularly well with our working geological model. This mineralized structure will be a high-priority drill target for the 2020 field season. The potential that it may connect to the Scottie Gold Mine mineralizing system make this an exceptional discovery. Sampling of many of these sites was only possible due to significant glacial retreat in recent years. We are eager to get back on the ground to find and delineate additional drill targets.”

Scottie Gold mine property hosts past-producing mine

We already know for certain that the Scottie Gold mine property hosts high-grade mineralization, from 1981-1985 it produced over 95,000 ounces of gold at a tremendous average grade of 16.2 g/t. That’s a much higher grade than Pretium’s world famous Brucejack mine is currently producing at (~9 g/t).

In addition to high-grade production records, there are some outstanding historical drill results at the Scottie Gold mine project as well. How about 108.3 g/t Au over 3.4 m, or 107.7 g/t Au over 4.2 m? Not bad at all! All known mineralization on Bow & Scottie Gold, from a total of 525 drill holes, is found at shallow depths. I find it encouraging that these blockbuster grades were found across 3.4 & 4.2 meters; not merely half-meter, one-hit wonders.

Mining M&A in N. America & the gold price making big moves!

Three big gold deals were announced in 4Q 2019 alone, including Kirkland Lake’s plans to acquire Detour Gold. If Detour is taken out, Pretium would be one of the last single-asset gold companies in Canada. Brucejack, situated less than 50 km from Scottie, is one of North America’s lowest-cost / highest-margin producers.

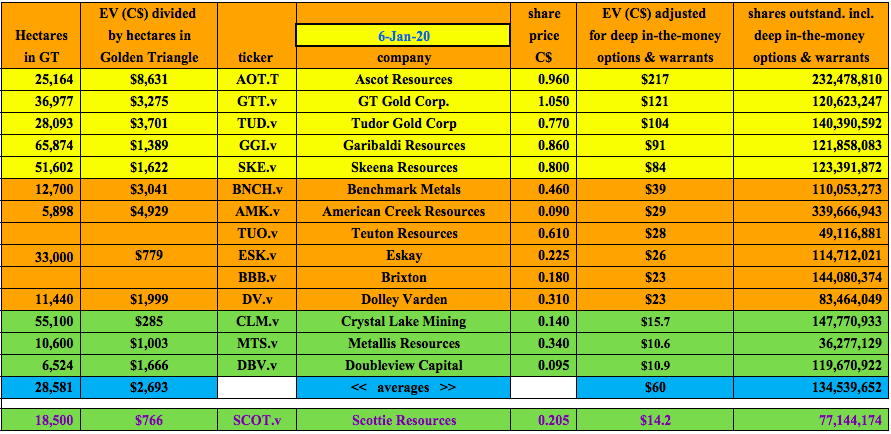

Pretium is 234x the size of Scottie Resources. If it’s not acquired, it might try to acquire one or more GT juniors like Ascot, GT Gold, Skeena Resources, Tudor Gold or Garibaldi Resources. As an aside, Seabridge Gold is also a potential acquirer. Those companies, with EVs ranging from $84 to $217 million, could in turn look to buy a company like Scottie Resources, with an EV of $14 million.

I don’t mean to overplay a takeout thesis, but, the gold price is now at US$ 1,576/oz., up ~US$ 112/oz. since U.S. impeachment proceedings & Iran / N. Korea troubles commenced, and up ~US$ 300/oz. from the low of 2019. Gold in $USD is the highest it’s been in 80 months. Furthermore, 2019 was reportedly the biggest year for gold mining M&A in N. America since 2010.

Neighboring Pretium & Ascot valuations bullish for Scottie

Looking at the map, it’s clear why Pretium might want to acquire Scottie Resources. Or, at least move to control the three properties where Pretium & Scottie share a border. Scottie’s valuation is so low relative to Pretium’s that it might be cheaper to pursue Scottie’s properties than to drill virgin areas on Pretium’s existing footprint.

Perhaps more likely — look at the map again — Ascot certainly has a compelling reason to care about Scottie, and the company’s digestible EV of $14 million is right in Ascot’s sweet spot. Ascot has multiple projects & properties, but only one with evidence of very high-grade mineralization like that of Scottie’s Bow (new drill results), Scottie Gold mine (past production + historical drill results + new surface samples) & Summit Lake (new grab samples).

Ascot’s EV of $210 million is 15x that of Scottie, and its share price is up 85% in the past two months alone, resulting in Ascot trading at $8,631/ha vs. $766/ha for Scottie. While Ascot’s Red Mountain & Premier projects have substantially more drill holes on them, both have lower gold grades, and high-grade mineralization starting roughly 100 meters deeper than that of Scottie’s near-surface deposits.

Tudor & GT Gold have giant intercepts of sub 1.0 to 1.5 g/t Au Eq. as thick as one kilometer or more. Grade x thickness readings for these assays are quite good, but drilling & mining through 1,000+ meters of rock can be costly & time consuming, especially if the projects are far from critical infrastructure.

Garibaldi’s assets in Canada are base metal (especially nickel + copper) heavy. Diversification into high-grade gold & silver could be an attractive option. With an EV of $96 million, it too could comfortably afford to make a run at Scottie. After 2020’s drill results (I believe Scottie is thinking about 5,000 m of drilling, subject to adequate funding), the company will be well more advanced.

Soon after 2020 drill results, one or more resource estimates likely

Within 12-18 months, management should be able to deliver a robust NI 43-101 compliant resource estimate from one or both of the Scottie Gold & Bow properties. In 2H 2021, shareholders might receive a third-party Preliminary Economic Assessments (“PEA“). In my opinion, Scottie could secure a JV or farm-in partner as soon as next year, upon which time funding requirements would drop dramatically.

Located at the southern end of the GT, Scottie’s properties are an easy drive of about an hour, on paved roads, from Stewart, BC. For the most part, infrastructure in the southern portion of the GT is significantly better than the middle & northern regions.

Conclusion

With gold prices and M&A activity up substantially, all eyes are on the Golden Triangle. However, not all of the GT juniors have had recent drilling success. Not all are focused on shallow, high-to-ultra-high-grade gold deposits. Not all have good infrastructure. Not all own or control 100% of sizable land packages. Not all have enterprise values of $14 million or less.

Scottie Resources (TSX-V: SCOT) is blessed with many positive attributes and has successfully advanced its flagship properties very nicely in 2018-19 with limited capital expenditures. There have been three major initiatives over the past several months, and three fantastic outcomes.

1] great new drill results on January 3rd at Bow, 2] excellent surface samples on the Scottie Gold mine property and 3] great grab samples at Summit Lake. This is a company to watch closely in 2020. In fact, watch closely the rest of January, as further drill results are imminent.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Scottie Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Scottie Resources are highly speculative, not suitable for all investors. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of Scottie Resources and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author

believes he’s diligent in screening out companies that, for any reasons, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts, financial calculations, etc., or for the completeness of this interview or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company. [ER] is not an expert in any company, industry sector or investment topic.

- As America loses a ridiculous trade war and manufacturing activity tumbles to 10year lows, the nation’s horrific GDP growth rate for 2019 was ranked an abysmal… number 107 in the world.

- The outlook for 2020 is even worse. The government’s debt to GDP ratio is more than 100%, and the rancid “end of empire” cake is now getting iced with maniacal debt-oriented warmongering.

- Is it any wonder that savvy investors are flocking to gold?

- Please click here now. Double-click to enlarge this spectacular daily gold chart.

- A bull flag may be forming at the $1575 resistance zone.

- This is important: I’ve predicted that gold needs to stage a few consecutive closings above that key $1575 price… to activate the next leg higher for gold and silver mining stocks.

- Please click here now. Double-click to enlarge this GOAU chart. As gold has arrived at the September highs around $1575 on the February futures chart, GOAU has arrived at its summer highs, in the $18 area.

- I’m aware of the substantial frustration amongst gold stock investors. That probably reached a crescendo yesterday, because the surge in bullion in the past few days of trading has been accompanied by very disappointing action in the gold stocks.

- Having said that, gold stocks dramatically outperformed bullion during the early part of the rally, and now both bullion and a lot of the miners are sitting near their summer highs.

- Please click here now. Double-click to enlarge. In the case of the silver miners, they are outperforming both gold and silver bullion.

- I sold most of my GOAU at $17.75 as it rallied into the $18 area, but I don’t have any “top call” for investors. I simply took some mining stock off the table into tremendous strength at modest resistance. It’s pruning the gold stocks tree, and nothing more.

- What should investors do now? Well, I plan to rebuy GOAU at either $17 (it’s already close to that price now), or on a breakout over $18, and suggest investors consider the same tactics.

- Please click here now. Double-click to enlarge this superb GOAU versus US stock market ratio chart.

- Has the Trump presidency been a failure or a success? Well, there’s been areas of success, such as tax cuts, deregulation, and basic law and order.

- Unfortunately, nothing has been done about the outrageous amount of government spending, and that’s why gold stocks look so good against the stock market on this ratio chart!

- Instead of the twitter tweets they get now, Americans need the kind of heart to heart talks that Ron Reagan used to give.

- The difference between the two presidents is obvious: Ronnie grew up relatively poor, whereas Donald grew up as a “frat boy”. It’s not Donald’s fault how he was raised, but it’s very difficult to give great heart to heart talks to blue collar workers when you have a silver spoon stuck in your mouth.

- Without televised presidential talks with America’s working class, focused on the need to dramatically chop government spending immediately and drastically, debt and spending will continue to soar. That means the nation’s pathetic GDP growth rate will sink even lower, and the purchasing power of the citizens will also continue to slide.

- Debt, tariffs, wages, and now insane warmongering are all putting upwards pressure on inflation. I’ve stated that America today most resembles the year 1966.

- Stagflation took off then, and it could be about to happen again.

- Hedge fund master Ray Dalio believes the best analogy is with 1937-1938, and everyone knows what happened in 1939… World War Two.

- US citizens couldn’t buy any gold in 1938, but they can today!

- Please click here now. Double-click to enlarge this weekly GDXJ chart. GDX $31, GDXJ $43, GOAU $18, and gold $1575 are all significant resistance zones. Gold bugs should now be aggressive accumulators. The pullback should end in just a few weeks, and much sooner if Iranian-US government tensions now devolve into actual war.

- Unlike the previous reactions from this resistance zone, I expect the current reaction to end very quickly, and explosive upside price action should carry gold towards my next $1800 target area quite quickly!

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |