Falcon Gold Corp.; 5 Canadian projects, mostly Au, + / Cu, Co, Ni, Ag, Pd & Pt

Peter Epstein epstein.peter4@gmail.com Epstein Research

Unless stated otherwise, all $$ = US$. Gold = “Au”, Silver = “Ag”, Copper = “Cu”, Cobalt = “Co”, Nickel = “Ni”, Palladium = “Pd” & Platinum = “Pt”

Gold producers are benefiting from a significant increase from ~$1,200/oz. nine months ago, to an eight-year high of $1,788/oz. in March, and ~$1,750/oz. in mid-May. Yet, gold bugs say we’re still in the early stages of a gold bull market. Pundits & analysts are moving price targets ever higher due to the shocking economic fallout and massive debt issuance / money printing resulting from COVID-19.

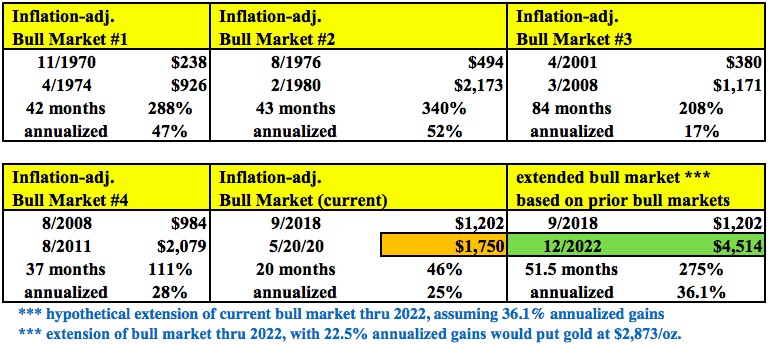

What might past bull markets say about today’s gold market?

In the four largest historical bull markets since 1970, the average inflation-adjusted gain has been +237% over an average 51.5-month period, for an annualized gain in each period of +36.1%. {See chart below}.

Notice that in today’s rally (the current bull market) the price is up +46% from September, 2018 to May 20, 2020 (~20 months). With this in mind, consider the following possible scenario between now and the end of next year.

If one were to extend the current bull market from 20 to 51.5 months (to December, 2022), and assume the average historical 36.1% CAGR, the gold price would hit $4,514/oz. Or, instead of using the four most robust bull markets of the past 50 years, consider the top two of the past 20 years.

In those more recent cases the average annualized gain was 22.5%. If gold were to increase by +22.5%/yr. from September, 2018 to December, 2022, it would reach $2,873/oz. Well respected Canadian economist David Rosenberg of Gluskin Sheff sees $3,000-$4,000/oz. possible within a few years. Last month, Bank of America forecasted $3,000/oz. within 18 months.

Importantly, the current gold price is already quite strong…

Do investors need $2,873 to $4,514/oz. for juniors with good quality mgmt. / tech. teams + high quality projects in safe jurisdictions to be multi-bag winners? Of course not. Readers are reminded that most PEA, PFS / BFS reports delivered over the past 7-8 years pegged long-term gold prices at between $1,100 & $1,300/oz.

A company I’m bullish on is Falcon Gold (TSX-V: FG), a junior miner that owns or controls exciting brownfield & greenfield opportunities in Canada. The Company has near-term catalysts that could turn its C$0.065 stock into something much greater within a matter of months. Falcon is fully-funded for a nine-hole diamond drill program at its flagship project.

Shares are tightly held, including by largest holder CEO Karim Rayani. Rayani has been an active buyer in the open market. With a market cap of C$4 million, this is a high-risk, high-return, high-grade gold story with near-term catalysts. In other words, exactly what investors with the ability to stomach high risk are looking for.

A funded (recently expanded to nine holes) drill program is well underway at the Company’s Central Canada Gold & Polymetallic project, ~20 km SE of Agrico Eagle’s Hammond Reef gold deposit, (Measured & Indicated resource of 4.5M ozs. Au). Central Canada hosts a past-producing mine with a 40-meter shaft and a 75-tonne/day mill.

Current drilling on flagship project offers near-term catalysts

While Hammond Reef lies on the Hammond fault, the Central Gold property lies on a similar major structure, running > 10 km along the Quetico Fault. Contiguous with the Central Gold project, the English Claims Option reported an interval of 0.64% Cu, 0.15% Co, 1.1% Zn & 0.35 g/t Au over a true width of 40 meters.

The first three shallow drill holes from the current program at the Central Canada project intersected mineralization over large intervals. One of the cores had visible gold in it. The first hole — designed to intersect the gold-bearing zone 20 meters west along strike of the historic producing shaft — intersected the zone from 33.5 to 79.8 m (46.4 m width) Note: {true widths unknown}

The second intersected the zone a further 70 m west, along strike of the shaft, from 26.9 to 62.2 m (35.3 m width). The third hit the zone 155 m west, along strike, of the shaft from, 26.8 to 59.8 m (33.0 m width). Assays on these three holes are expected this month. The results will inform the drilling of the next six holes.

Historical drilling by multiple operators dates back decades. In 1965, drilling returned several winners including; 44 g/t Au over 2.1 m, & 37 g/t over 0.6 m. In 1985, 13 holes included a 1.2 m interval of 27.5 g/t Au & 4.0 m of 7.1 g/t. In 2012, a wider interval, 23.3 m of 1.8 g/t, was delineated.

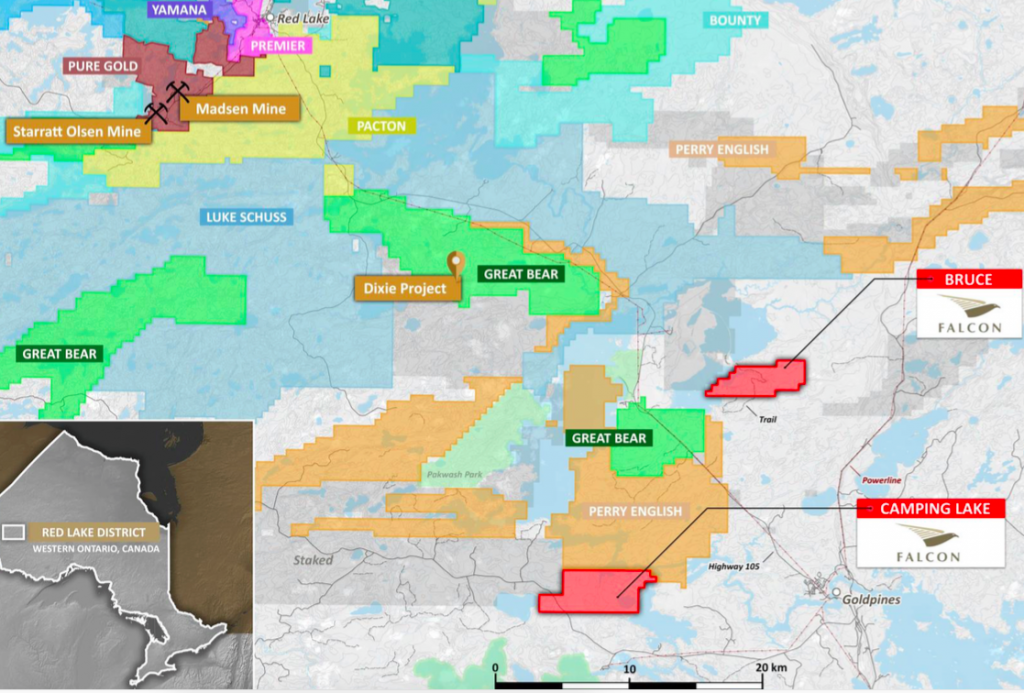

Red Lake mining district of northwestern Ontario

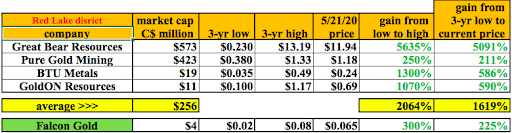

In addition to the Central Canada project, other Falcon properties could see drilling this year. There’s a tonne of attention on the Red Lake mining district as Great Bear Resources released yet another important drill hole at its blockbuster Dixie project. Their latest reported hole went much deeper than previous efforts and hit an intercept of 68.6 g/t over 2.7 m from 1,009 m downhole.

Falcon has two gold properties in the Red Lake district, Camping Lake & Bruce Lake. International Montoro has an option to earn a 51% interest in the Camping Lake property and can acquire a further 24% interest (for a total of 75%) for C$500K.

The property consists of five claims comprising 109 cell units (approx. 2,250 hectares / 5,560 acres), ~20 km south of Great Bear’s discoveries at Dixie Lake, and ~8 km south of BTU Metals Corp’s base metals targets.

Bruce Lake adds an additional ~3,460 acres to Falcon’s Red Lake district portfolio. The Project contains excellent targets for both Red Lake-style gold mineralization and gold-bearing base metal prospects. A combined ~3,650 hectares for both Bruce & Camping Lake, equates to roughly 20% the size of BTU Metals’ Dixie Halo project. BTU Metals has a market cap of C$20M.

Wabunk Bay Platinum, Palladium, Base Metals Project

At its ~1,192-hectare Wabunk Bay platinum & palladium / base metals project, also in the Red Lake district, Falcon hopes to follow up on a promising field program from last year.

Grab samples from 2019 assayed up to 760 parts per billion (“ppb“) Au, 0.272% Ni, 0.478% Cu, 171 ppb Pd & 221 ppb Pt. Select areas around Wabunk Bay are currently being explored by Eric Sprott-backed Argo Gold, which has reported ultra-high grades, such as 132 g/t Au over 1.8 m.

Spitfire & Sunny Boy Claims in BC, Canada

The Spitfire / Sunny Boy claims, totaling 502 hectares, are ~16 km east of the town of Merritt in south central British Columbia. Spectacular ultra high-grade gold values were reported on Falcon’s newly secured property, including 124 to 127 g/t Au, (midpoint of 4.0 ozs./ton) and 309 to 514 g/t Ag over 0.9 m. On the Master Vein, an extreme, ultra, high-grade gold value of 50.5 oz./t (about 1,570 g/t) was sampled in 1974.

Several copper discoveries in this prolific area became major mines, including Craigmont, Copper Mountain, Afton & Highland Valley. Southwest of Sunny Boy, soil geochemistry, magnetometer & VLF geophysics, trenching, sampling & diamond drilling returned a drill intercept of 3.8 g/t Au, 0.24% Cu & 32.9 g/t Ag over 13.4 m.

Due-diligence work last year confirmed the presence of gold mineralization along the Master Vein over a 300-meter strike length with samples ranging from 0.33 to 2.74 oz./t.

The Company is planning tightly spaced soil sampling, EM & IP geophysics & structural mapping to identify new mineralized structures. Although nothing has been announced, I’m hoping that a drill program can be done at Spitfire / Sunny Boy this year.

Conclusion

Five prospective projects, at least two of which are highly prospective in the near-term. The bonanza-grade, multi-ounce per ton showings at Spitfire / Sunny Boy alone could be a company-maker upon a successful drill program or two.

Likewise, the flagship, Central Canada Gold & Polymetallic project is also a potential company-maker. A total of nine assays will be announced in the next few months, the first of which, are due this month. Management is very pleased and cautiously optimistic about the visual inspection of the cores. As mentioned, one had visible gold.

In today’s metals / mining space, NOTHING is more sought after than new discoveries / high-grade gold intercepts at projects with blue-sky potential in safe jurisdictions (like Canada).

Make no mistake, Falcon Gold (TSX-V: FG) is a high risk exploration play, but now is arguably a wise time for investors with an appetite for risk to be looking at gold juniors. In past bull markets, top performing gold companies enjoyed gains in the thousands of percent. Falcon has a lot going for it. Drill results this spring & summer, possibly from multiple projects, could be a game-changer.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Falcon Gold, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Falcon Gold are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Falcon Gold was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

- Gold drifts sideways in typical weak season trading, silver looks better, and the miners look awesome!

- Please click here now. Double-click to enlarge this gold chart. It’s clear that both upside and downside breakouts are failing, and the gold price continues to ooze sideways.

- A rectangle pattern is in play. The good news is that basis the Edwards and Magee technical analysis handbook, there’s probably about a 67% chance that the breakout will be to the upside.

- Even if it’s to the downside, the target area is at $1575-$1600, which is mild corrective action.

- Please click here now. Double-click to enlarge this long-term gold chart. The $1800 area is a selling area because it is a resistance zone, but it’s also the build zone of a huge inverse H&S bull continuation pattern (where the right shoulder could become a flag!).

- Gold market investors need to be careful about selling too much and becoming too boisterous in making “top calls” in this key area.

- Please click here now. Double-click to enlarge this magnificent silver chart.

- A small H&S top formed, but I expect that the “King of Assets”, will push higher and destroy that pattern.

- Silver was hurt more than gold as the stock market swooned in the initial stage of the Corona crisis.

- Now, as the Fed money printers and government debt worshippers pull out all the stops to get their stock market “poster boy” higher…

- Silver is leapfrogging over gold.

- On the COMEX this morning, gold is down about $10/ounce, and silver is up, with the Dow up about 500 points. Silver has diverged from gold quite frequently during this stock market surge.

- Please click here now. Nouriel Roubini has recently done a spectacular interview with the New York Mag Intelligencer.

- He presents a sobering vision of what lies ahead for America. Just a few small rate hikes could turn the catastrophically weak economy and debt-obsessed government into an economic gulag.

- It’s the same scenario I’ve predicted, and the weekly gold chart price action suggests the odds of it happening are at least 90%.

- The government failed to save. It failed to prepare for any type of crisis, and it failed to get rid of the diabolical graduated income tax that fuels its never-ending size growth.

- Once the stock market poster boy implodes, the government emperor will be shown not only to have no clothes, but no skin, heart, or brain!

- Please click here now. Double-click to enlarge this US stock market chart.

- I’ve highlighted my key buy zones at 21,700 and 18,3000. The entire 27,000-30,000 area is a sell zone. I plan to sell there, with gusto!

- Please click here now. Double-click to enlarge what is obviously one of the world’s most spectacular ETFs, GOAU-AMEX.

- Note the action of my 14,5,5 series Stochastics oscillator, which I affectionately refer to as “Leo the Lion”. The bottom line is when a key weekly chart oscillator becomes overbought, it may quickly drop, or it can stay overbought for quite a long time.

- In the case of GOAU and most big-name gold stocks, I suggest that investors wait for that oscillator to drop under 80 before getting at all concerned about the health of this rally.

- The only reason to sell perhaps 10%-30% of gold stock positions now, is because the profits on miners bought at my gold $1577 and $1450 buy points are fabulous! The time to sell is when the investor feels fantastic.

- For some investors, that time is now. For others, that time lies ahead, but this metals market rally has legs, especially for the miners and silver bullion. A horn of plenty is in play, and everyone in the gold community can get their profit booking day!

- It’s the soft demand season for gold (April-Sept), and that means upside and downside breakouts can become “wet noodle” affairs.

- Bulls and bears who aren’t prepared for this type of sideways price action may get frustrated.

- Please click here now. Double-click to enlarge this short-term gold chart.

- My suggestion for investors is to focus on the important price zone of $1800 for modest selling, and $1675 and $1575 for buying.

- Most price action in between these zones is likely to be just “noise”… until later in the summer when stock market crash season (Aug-Oct) gets underway.

- Please click here now. Double-click to enlarge. My scenario of a gigantic inverse H&S bull continuation pattern on the long-term gold chart suggests gold has entered the right shoulder “build zone”.

- Gold could trade near $1800 numerous times and trade near $1675/$1575 numerous times, perhaps for as long as a year, before shooting above $2000.

- Investors need to prepare for all scenarios, not just those that feel good or seem most likely.

- The smart play is to just focus on the buy zones of $1675, $1575, be patient, and enjoy the right shoulder formation process.

- A glorious surge towards the $3000 area is the most likely event after the right shoulder is completed.

- Please click here now. If US Corona cases are truly beginning to subside, life can return to normal:

- The citizen horses can march back into the graduated income tax glue factory and send the government slave masters their money. The government will borrow even more money than it extorts from the citizens and quickly spend it on everything except crisis preparation. Then it will brag in hourly tweets about how great the debt-fuelled future will be. The bottom line:

- The old normal is back. Got gold?

- Please click here now. Double-click to enlarge. The big picture for gold is very bright, but in the short-term, silver looks more perky than gold!

- There’s solid staircase action in play, and stoploss enthusiasts could buy now with a stop at $14.90 or $14.50.

- If the July silver contract trades above $15.50, a surge to $16.50 and then to $18 is likely.

- The leading price action of some silver stocks suggests this is now the most likely scenario for the silver price.

- Please click here now. Double-click to enlarge. The only potential fly in the silver price ointment is of course a fall in the US stock market.

- The stock market has become the government’s “poster boy” for the economy. Minor issues like 25% unemployment, an out of control debt, no savings, and no preparation for crisis…

- These issues don’t worry the government, because the central bank’s electronic photocopiers keep printing money and pouring it into ETFs and government bonds.

- If there isn’t enough money printing and the stock market tumbles, silver could take a hit. No market is without risk, but the risk for silver investors is modest if it’s handled professionally. Investors can use stoplosses at my suggested price points. Or, just buy with modest size, so there’s not much pain on a price dip.

- Please click here now. Double-click to enlarge this “work of art” GDX chart. Is the magnificent uptrend “long in the tooth”, or is it just a prelude to a much bigger rally being ushered in by a significant weekly chart upside breakout?

- A price dip below the uptrend line would be disappointing, but it should be followed by simple consolidation, much like what is occurring on the gold bullion chart now.

- There’s resistance of size in the $37 area for GDX, and that’s where I suggest investors plan to do their first significant selling on this magnificent rally!

Timing is everything. Precious metals are up, while almost everything else is down. Gold has soared 38% from last year’s low. This is a big move, but few investors seem to appreciate its significance. Earlier this week, Bank of America announced a gold price target of US$3,000/oz. by the end of 2021. While that might sound aggressive, today’s price of US$1,740/oz. = ~C$2,463/oz. is already quite strong.

The current price is more than enough for well managed juniors, with attractive projects, in safe & prolific jurisdictions, to thrive. Right now, some of the best precious metal jurisdictions, as measured by low-costs plus ample exploration upside, include parts of Mexico, Canada & Australia.

In an April 13, 2020 Myrmikan Research investment letter, Manager Daniel Oliver made strong arguments that gold & silver prices are headed higher, perhaps much, much higher. Mr. Oliver has been published in Forbes, The Wall Street Journal, The Washington Times, Real Clear Markets, National Review, among others. He has a J.D. from Columbia Law School and an MBA from INSEAD.

Most important for the purposes of this article, Oliver is a Director of tiny silver / gold junior Vangold Mining (TSX-V: VGLD) / (OTCQB: VGLDF). {corporate presentation} In his commentary, he unveils three potential paths or scenarios for precious metals.

In the first scenario,

“…the magnitude of the dollar debt overhang is so large—tens of trillions—that policy makers cannot practically prevent the inverted credit pyramid from tipping over. The result is a panic more intense by magnitudes than 2008 or 1929. Gold does well on a relative basis, but falls in nominal terms.”

In the second scenario,

“….trillions of dollars does little to help local businesses & the working class. Wall Street, however, is not just saved, but levers up bailout largess to create spectacular increases in asset prices. Gold spikes in nominal terms as it did from 2009 to 2011 under similar conditions. Gold mining equities soar….”

Finally, in the third scenario,

“….the Fed’s helicopter drop of dollars precipitates a currency crisis. Gold bullion rockets toward $10,000 per ounce. Gold miners (especially marginal, higher risk players) have breath-taking increases, last experienced from 1978 to 1981.“

Oliver believes the first scenario is by far least likely to unfold, an end-of-the-world type of event that we need not focus on because the world would be over…. The remaining two paths are bullish, and extremely bullish, respectively for physical gold & silver and precious metals juniors.

Make no mistake, just because Dan Oliver and a growing cadre of investment experts are talking up precious metals doesn’t guarantee the price will shoot to the moon or even rise from current levels. However, giant hedge, mutual & generalist funds are looking closely at precious metals and the companies that explore for, develop and mine them.

Relative value funds have plenty of industry sectors to avoid, but only a few that offer potential upside combined with low correlation to, and diversification from, the overall market. Glowing reports of precious metals’ fabulous future are a lot more palatable given that a tsunami of global debt obligations will be issued, with no end in sight.

As bad, or perhaps even worse, is governments’ willingness, in a blink of an eye, to direct their central banks to print absurd amounts of money out of thin air. Combined, debt + unfunded & under-funded liabilities will explode much higher. Not by tens or hundreds of billions, but by trillions of dollars. It’s no longer just a theory (ongoing unbelievably large & unsustainable debt), the pandemic has made it a certainty.

Vangold Mining has many positive attributes. Its 100%-owned silver / gold project is in a safe and desirable location in central Mexico, the state of Guanajuato. At its peak in the 18th century, the mines of Guanajuato, especially the world famous Valenciana mine, were considered the largest and richest on the planet. In the 50 years from 1760 to 1810, Guanajuato (mostly from Valenciana) often accounted for 20% of global silver production, primarily from a single extraordinarily rich vein. {corporate presentation}

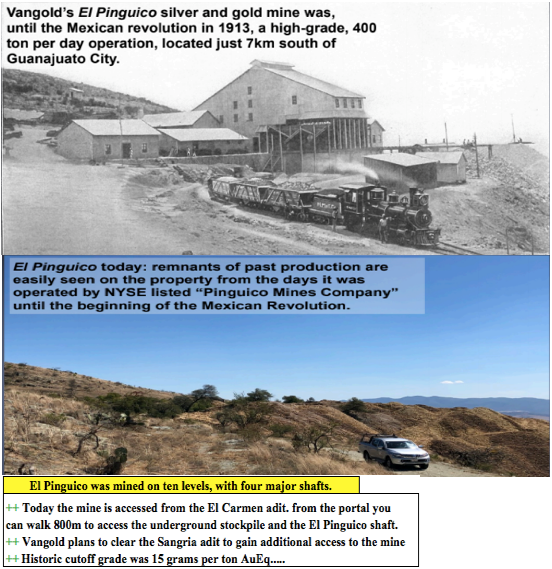

The company’s flagship property hosts the high-grade, past-producing El Pinguico mine that was only shut down due to the Mexican Revolution in 1913 {it wasn’t mined out}. The mine operated on ten levels with four major shafts. From the early 1890s until 1913, El Pinguico was one of the highest grade mines in Guanajuato.

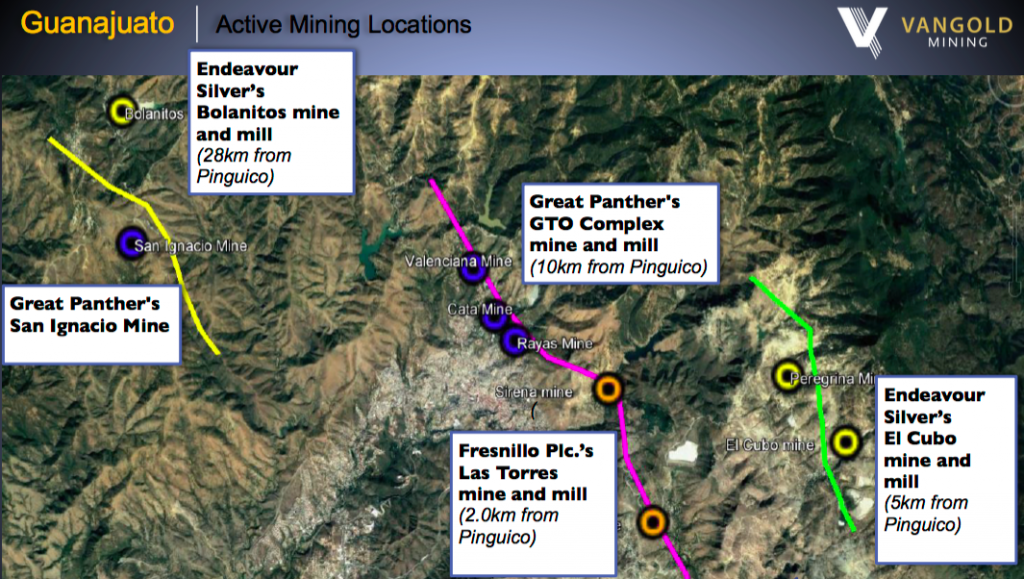

The cut-off grade was reportedly 15 g/t (0.48 oz./t) gold equiv. Mining was done exclusively at the El Pinguico & El Carmen vein systems, which are thought to be splays off of the Mother Vein. El Pinguico is surrounded by well-known players, including — Fresnillo PLC, Endeavor Silver, Great Panther and Argonaut Gold.

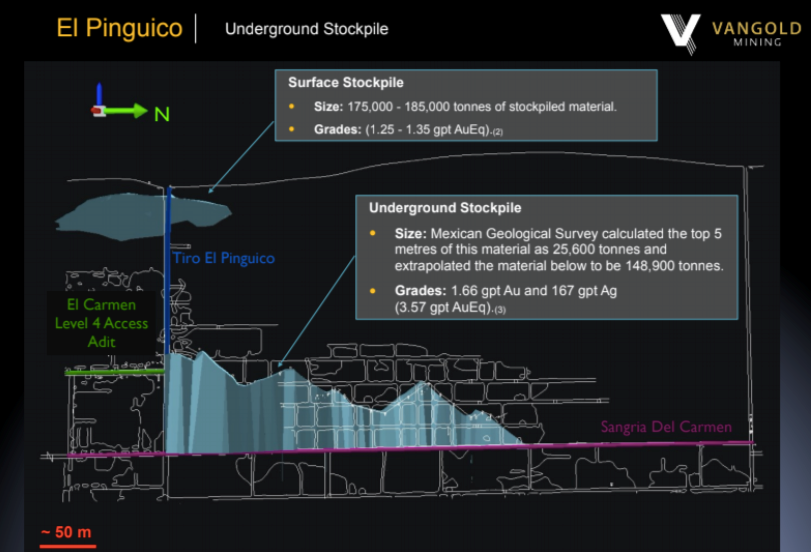

Modest near-term cash flow is possible from exploiting a surface stockpile this year, but more meaningful profit potential exists from extracting (and getting toll-milled) meaningful underground stockpiles grading ~3.6 g/t Au Eq. In 2012, the Mexican Geological Society estimated there were ~174,500 tonnes of material stockpiled underground. Assuming an 85% recovery, that equates to about a 20,000-ounce Au Eq. opportunity.

The plan is to reinvest net cash flow into new exploration & development activities at El Pinguico. It’s critical for readers to understand that Vangold has substantial exploration upside above & beyond monetization of stockpiles. Interestingly, the company stands to benefit from at least three things due to the global pandemic.

First, significantly lower energy costs, second, a favorable move in FX rates (weaker CAD$ & Mexican peso vs. the US$), and third, lower project costs (drilling, mining equipment & services, labor) as people will, presumably, be anxious to get back to work. Globally, unemployment rates are likely to remain elevated for an extended period.

Vangold has a substantial database of valuable exploration data including historical underground channel sampling & drilling. Samples from around the year 1909 include blockbuster grades. The best were; 0.7m @ 23.0 g/t Au + 3,858 g/t Ag, {~61.6 g/t Au Eq.}, another one of 0.8m @ 16.7 g/t Au + 3,054 g/t Ag, {~47.2 g/t Au Eq.}, and a third, 0.7m @ 15.7 g/t Au + 1,793 g/t Ag, {~33.6 g/t Au Eq.}.

As mentioned, prior mining at El Pinguico was from two vein systems (El Pinguico & El Carmen) thought to be offshoots of the Veta Madre (“Mother Vein”). The Veta Madre has been, and continues to be, incredibly important to the region. It stretches at least 25 km and has reportedly produced upwards of 1.2 billion ounces of silver.

From Endeavor’s website, “Silver was originally discovered by Spanish explorers in 1548 and subsequently at Guanajuato in 1552. Guanajuato is considered one of the top three historic silver mining districts in Mexico, having produced an estimated 1.0 to 1.2 billion ounces silver, plus 5 to 6 million ounces gold.”

The Veta Madre is also highly prospective for Vangold as it is known to extend to within 250 meters of the company’s border. Management believes it likely crosses through their property at between 400 and 600 meters depth. Importantly, Vangold is not the only company chasing the Mother vein.

With a much higher gold price, silver not so much (yet), especially in Mexican peso terms, the region has become one of the hotter mining jurisdictions in North America. C$10 billion Fresnillo PLC is reopening a prolific (1970’s to 2002) mine that will bring additional workers, equipment & mining services to the area. The mine reopening is happening next year, just 2 km from Vangold’s project.

In addition to Director Daniel Oliver, Vangold has a tremendous team for a company with a market cap of just C$2.7 million. Led by the highly experienced and well-connected James Anderson, who’s been working hard for the past year to revitalize this story, the company’s ship may have just come in. And, I should add, a rising (gold / silver) tide lifts all boats!

Readers should strongly consider taking a few minutes to review Vangold Mining’s (TSX-V: VGLD) / (OTCQB: VGLDF) brand new {corporate presentation}. Please visit the last two pages which extoll the considerable talents and experience of the management team.

Disclosures / disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Vangold Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Vangold Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned stock & warrants in Vangold Mining, and the Company was an advertiser on [ER].

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}