While serious concerns linger in the markets about the strength of the swing up, gold mining stocks have continued their leg higher. The first quarter of 2021 was a positive period for gold miners, creating a new extended rally to bring most back to pre-pandemic levels. While most of the biggest miners have been doing well, a drop in the gold stock benchmark and trading vehicle GDX VanEck Vectors Gold Miners ETF of 9.8% in Q1 demonstrates a lack of equality in the gains.

Sentiment Uncertainty Turns to Directional Confidence

Gold itself lost 10% through the period, but has rebounded quickly in Q2. This has been a big boost to miners, particularly in the US. It has been the majors that propped up the GDX in Q1; these stocks often amplify gold’s material moves by two or three times. As spot gold continues to recover, so does sentiment for gold miners, and the majors are seeing this more than others. The GDX reverted 21.8% higher in May, and continued to climb this month. During the same time, gold prices climbed 6.6%, with all indicators pointing to a better sentiment around gold and gold mining stocks.

Q1 2021 reported results show that the majors in particular are outperforming all other gold miners, with strong results and a growing share of the dominant gold-stock ETF. The top 25 GDX gold miners now account for 88.1% of the market cap of the ETF. This dominance is also borne out in the results, with almost all of the top gold mines by production and expansion in the U.S. being owned and operated by those same companies.

The top 25 stocks in the GDX reported recovering and powerful production numbers for Q1. Although total production dropped 2.8% in the period, total revenues jumped 10.5% YoY to $13.7B. This is one of the best quarters ever for this group.

Higher Commodity Prices Boosting Everything

The lower output was offset by 13.4% higher gold prices in the same period, boosting their bottom lines and pushing their financials along healthily. This has been a recurring trend in the mining industry as commodity prices continue to push higher every month with reopenings driving demand along and a positive outlook for the industry expands with every new project and restart announced. Production is nearing pre-pandemic levels again and investment in the first quarter picked up rapidly as miners raced to get back on track for 2021.

The bottom lines of the major gold miners in the ETF was impressive, with 47.1% high YoY earnings. Those soaring earnings and profits seem to be in line with a recovering industry and one that is moving faster than many other parts of the global economy. While some have tried to attribute this to low comparison from 2020, looking at most of these companies shows that this performance comes on the back of normal performance and not any over-compensation from the slowdown of last year.

The List of Winners

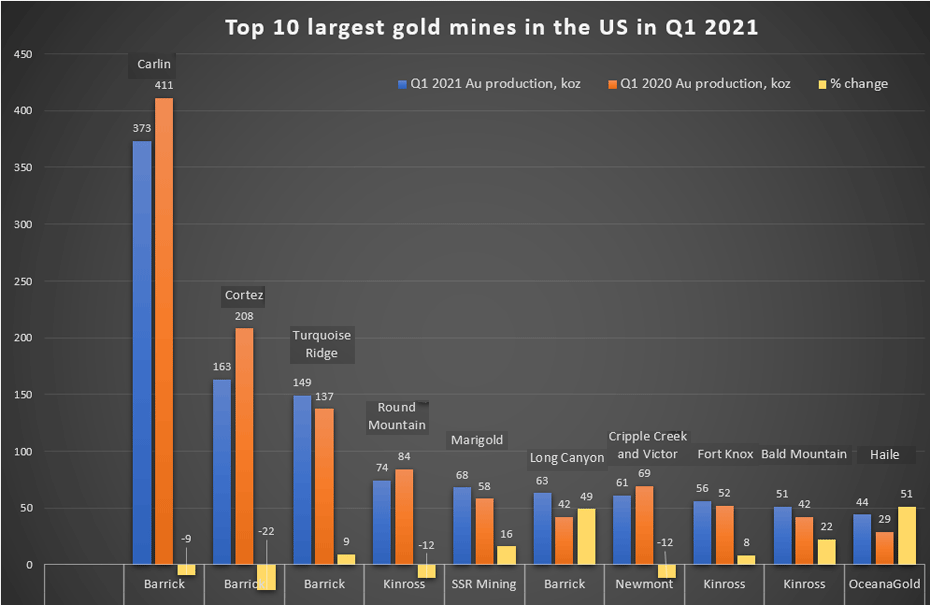

Kitco has put together a list of the top largest gold mines in the US based on gold production in Q1 2021, and it is clear that the biggest players continue to dominate not just the biggest gold stock ETF, but also production quantities.

Barrick takes four of the top ten spots, including the three top spots that seem to generally be reserved for the company across its Carlin, Cortez, and Turquoise Ridge mines. The biggest miners in the industry continue to dominate production and profits right now, but they are also lifting other stocks with them as gold prices rise and industry sentiment begins to reverse in Q2 2021.

| Operation | Major Owner/Operator | Q1 2021 Au production, koz | Q1 2020 Au production, koz | % Change | |

| 1 | Carlin | Barrick | 373 | 411 | -9 |

| 2 | Cortez | Barrick | 163 | 208 | -22 |

| 3 | Turquoise Ridge | Barick | 149 | 137 | 9 |

| 4 | Round Mountain | Kinross | 74 | 84 | -12 |

| 5 | Marigold | SSR Mining | 68 | 58 | 16 |

| 6 | Long Canyon | Barrick | 63 | 42 | 49 |

| 7 | Cripple Creek and Victor | Newmont | 61 | 69 | -12 |

| 8 | Fort Knox | Kinross | 56 | 52 | 8 |

| 9 | Bald Mountain | Kinross | 51 | 42 | 22 |

| 10 | Haile | OceanaGold | 44 | 29 | 51 |

Source: Kitco

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Roaring electric vehicle (EV) sales, battery production, and economic reopening continued to drive lithium prices higher in June. Most lithium producers are now working on ramping up further production during the expansion of a very favourable environment for them.

A Decade of Expansion

The coming decade could see a 1000% demand increase, at the current rate of expansion. To meet the global megafactory demand of 3,791 GWh by around 2030 may require lithium producers to step up to the plate faster than ever. This count is always shifting and could change by the time we get to the end of the decade, but there is no question that demand will continue to grow over the coming years, giving lithium miners more customers and profits.

More Price Runs

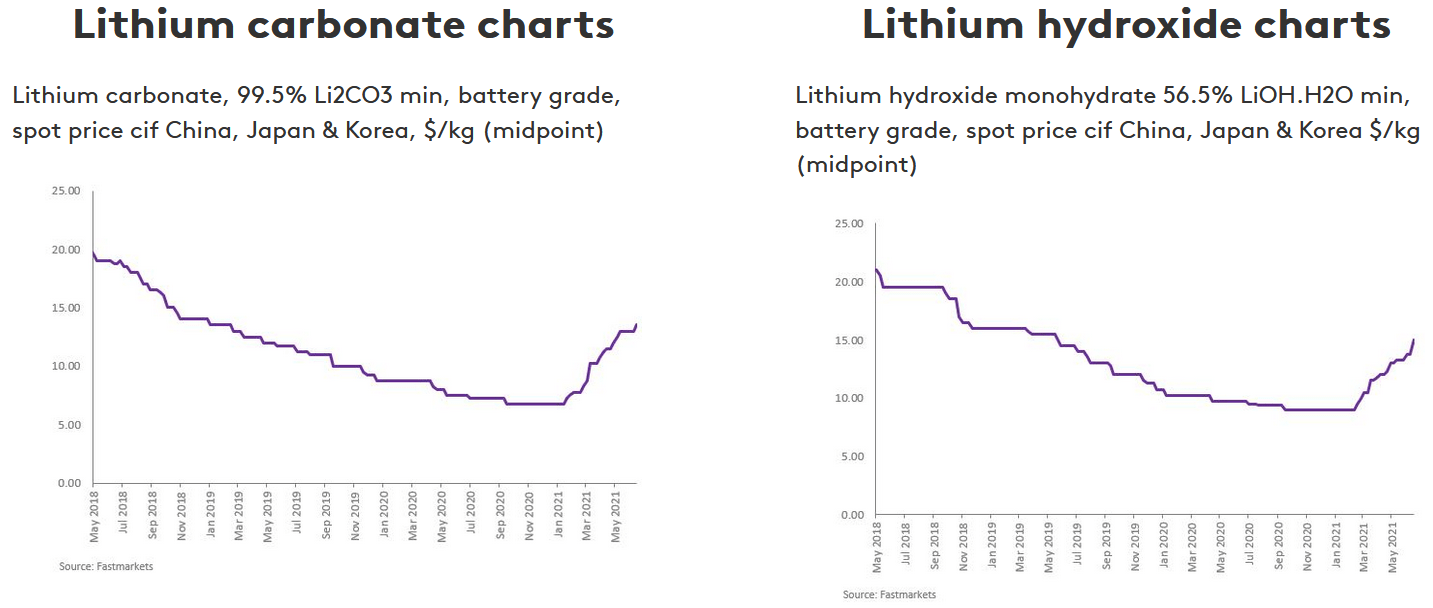

The past 30 days has see 99.5% lithium carbonate battery grade spot midpoint prices cif China, Japan and Korea at US$13.50/kg (US$13,500/t) and min 56.5% lithium hydroxide battery grade spot midpoint prices cif China, Japan and Korea at US$15.00/kg (US$150,000/t). The price charts for these look like they are bouncing off a trampoline with a heavy positive trend for May and June.

The main drivers for lithium (metal) demand are EVs and some of the high-tech sectors that require lithium for their products. EVs and energy storage make up the vast majority of demand for lithium, and this is where the bulk of the demand increases are expected to come in the future. Two of the fastest movers for this market are Europe, with 15% EV share, and China, with 10% EV share. A permissive and positive regulatory framework on top of stable and supported homegrown car manufacturers has given these two countries a leg up on accelerating their new EV sales timelines.

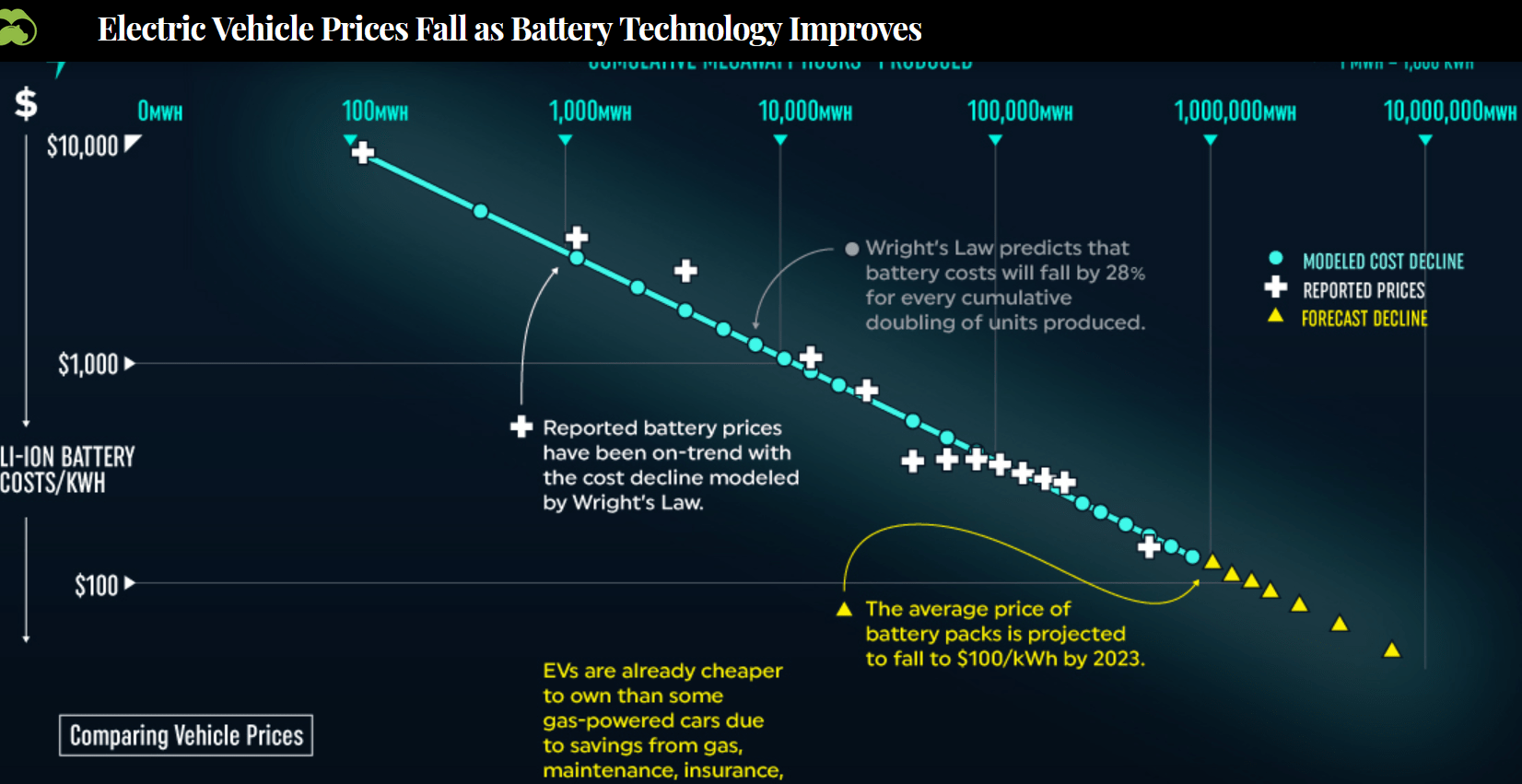

China in particular has pushed its domestic EV producers further with massive subsidies and government investment. As battery prices continue to fall, so do EV prices. In an article from Visual Capitalist, the linear correlation shows that the forecasted decline in Li-ion batteries could fall to around $100/kWh by 2023.

Miners Heading to the Moon

Some lithium mining companies are soaring on the backs of this news and their business models are in a great position.

Albemarle (NYSE:ALB)

Albemarle (NYSE:ALB) recently completed the sale of its fine chemistry services business to W.R. Grace and Co for about $570 million. The company is moving forward with its ESG goals for lithium mining as well, announcing on June 2 that “Albemarle releases sustainability report and environment target commitments.”

Orocobre (ASX:ORE) (TSX:ORL)

Orocobre (ASX:ORE) (TSX:ORL) announced that the “Olaroz Lithium Facility (Olaroz) operations increased the Gross Cash Margin more than $1,800/tonne with the sales price up more than 50%. Costs remained near all-time lows despite a much greater proportion of sales being battery grade material which has higher production costs…..Naraha Lithium Hydroxide Plant construction has continued throughout the period and is now approximately 94% complete.”

As the company continues to expand operations in time to fill the growing demand, investors could be more than happy to continue piling into the stock.

Galaxy Resources (ASX:GXY)

The company’s Mt Cattlin project is back to producing at full rate, with an acceleration of 2NW mining with the first phase of pre-strip to commence in H2 2021. The company joins many other miners in the race back to normal after the pandemic shut down some operations and forced mining companies to slow production. This was partly due to the pandemic itself, and the double-shock of the dropoff in demand from shutdowns.

Just the Beginning

We are likely just at the beginning of a long run of lithium prices continuing their steady growth. The U.S. has also unveiled its recent infrastructure plan which is set to require more lithium due to the massive needs coming from the electrification aspects of the plan. The plan will call for the superpower to start bringing in domestic and international supply for batteries, critical minerals (like lithium and copper) and semiconductors.

It also seems that there could be a cross-pollination within the tech, auto, mining, and energy industries. CATL and BYD (one of the key EV brands in China) is in talks with Apple for EV battery supply, as Apple is possibly aiming for a 2024 production start date for its own passenger vehicle. Volkswagen is also looking to “get actively involved in the raw materials business” according to a statement from the company.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

President Joe Biden is making a lot of people very happy lately, with his recent announcement of a new infrastructure deal set to create millions of jobs and boost demand for materials, minerals, and metals. The mining industry will have no small role to play in this plan, the result of a deal struck between five Democrats and five Republicans.

“The Bipartisan Infrastructure Framework”

The bipartisan deal will lay out a plan for spending hundreds of billions of dollars on key infrastructure projects in the United States, including building roads, bridges, and highways in a massive coordinated effort to stimulate the American economy and create jobs in every sector of the economy. Of course, much of the job creation will be happening in the construction, planning, and other sectors directly related to the projects. Still, most ancillary sectors as well as many of the services needed to sustain these projects will benefit as well, particularly for those areas in which the projects will be running.

“We’ve struck a deal. A group of senators – five Democrats and five Republicans – has come together and forged an infrastructure agreement that will create millions of American jobs.”

The announcement boosted London copper prices last Friday, with a positive outlook for any and all metals that will be needed to supply this multi-year multi-billion dollar challenge. Better demand for metals in the coming years could translate into bigger profits for miners, and a supply push that could keep copper mining companies working hard to expand their mine portfolios and increase production rapidly.

More Price Gains for Copper

Three-month copper on the London Metal Exchange advanced to $9,459 per tonne, and the most-traded August copper contracts on the Shanghai Future Exchange closed down 0.5% to $10,644.73 per tonne. This continues to plot copper’s rise to the possible $15,000 target set by Goldman Sachs earlier this year, and builds on the price momentum seen over the past two months.

While copper has been one of the biggest gainers this year, suppliers and steelmaker’s stocks surged after the announcement as well. Caterpillar jumped an additional 2.6% on Friday after a 3.8% gain on Thursday, the biggest in three months for the company.

Huge Plans Driving Huge Demand

The U.S. will require massive amounts of steel for this ambitious plan, and steel stocks are already reflecting that positive outlook. Friday saw U.S. Steel Corp. climb over 3% and the largest steel producer in the U.S. Nucor Corp. jumped 2% with the news. The bill and the infrastructure plan is a tide that is set to lift all boats, from the top of the supply chain to the bottom. Mining companies in particular will have their hands full filling the rising demand from this plan, and the supply dearth the market is experiencing now could accelerate with the possible new dynamic.

“The Bipartisan Infrastructure Framework represents the largest federal investment in public transit history – including the largest passenger rail investment since the creation of Amtrak. I might be a little biased, but that’s a big deal.

While the coming copper supercycle is something miners are sure to be looking forward to, they will also be kept on their toes for some time working to fulfill all of the potential this rocket ride will provide.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The economic recovery from the COVID-19 pandemic continues apace in Canada, with Statistics Canada (StatCan) reporting Wednesday that the real gross domestic product (GDP) of the natural resources sector rose 2.9% in the first quarter of 2021. This represents the third consecutive quarterly increase starting with the third quarter of 2020.

While the rest of the country has been locked down and hit harder by restrictions, the energy industry has been able to maintain operations and production while keeping pandemic safety measures in place. The report clocked the mining sector’s rise as stronger than the economy-wide real GDP (+1.4%), proving that the growing demand for natural resource products has not slowed down even as the overall economy recovers from the pandemic.

The real GDP of the mineral and mining subsector rose by 5.1% as production increased following rising prices. Commodity prices around the world have been pushed higher on growing demand and a lack of supply, along with supply-chain disruptions and bottlenecks. Mining products like copper and gold have risen steadily since the middle of 2020, putting more profits on the balance sheets of Canadian mining companies and strengthening the sector overall.

Non-metallic minerals rebounded 8.8%, a strong recovery considering the 9.4% drop in real GDP in the previous quarter. Potash mine reopenings have sped up following the lifting of many COVID-19 restrictions, and potash prices and demand both rose in the first quarter of 2021. Real GDP for metallic minerals increased 5.8% in Q1 2021, driven by the strength of copper production. Copper has been the strongest story of all, with prices skyrocketing amid a demand supercycle attributed to the global electrification goals, particularly in the United States, Canada, and Europe.

The mining sector has also been driving solid job growth, with employment in the natural resources sector rising 2.1% in the first quarter, logging its own third consecutive quarterly increase. The rate passed the total employment rate rise for the country at just 1% from the fourth quarter of 2020 to the first quarter of 2021. The energy and mining sector has been a strong driver of economic growth as the country pulls out of the pandemic restrictions and launches a full-scale expansion. The industry is outpacing the rest of the economy; however, it is also pulling the rest of the country’s averages out of the pits hit early last year.

Job recovery in the energy sub-sector was the strongest, adding 5,900 jobs, and the minerals and mining subsector adding 4,600 jobs. 2021 is expected to be a good year for the industry, as demand for commodities and rising prices continue to be steady tailwinds for mining companies in Canada and around the world.

Shares of Lundin Mining Corporation (TSX:LUN) (Nasdaq Stockholm:LUMI) closed down 9.4% on Monday at $10.27 after announcing that it would need to cut guidance at its copper-gold Candelaria complex in Chile. The guidance for 2021 production was cut to 150,000-155,000 of copper and 85,000-90,000 oz of gold on a 100% basis. The near-term adjustment comes after the company operated in line with forecasts to date during the second quarter of 2021 due to the short-term mining sequence in Phase 10 for the second half of the year.

The reduction hit the company and its shares hard as Candelaria originally accounted for over half of Lundin’s previous forecast 2021 guidance of 275,000-299,000 tonnes of copper and 170-180,000 oz of gold. The company took a hit knocking its market cap down to $7.6 billion

Adding New Precautionary Measures Slowing Output

The Candelaria open pit contains known fault zones, and Lundin Mining (TSX:LUN) (Nasdaq Stockholm:LUMI) is continuously monitoring these areas. Part of the change comes from the need to manage the production risks in a localized area of Phase 10 that, while nominal in volume, could eventually impact activities on lower levels of the site and on the main ramp. Reducing these risks means taking additional precautionary measures, including a wider step out in the area, mining smaller benches and with smaller blasts, and delaying mining immediately below the fault zone to later phases.

The reduction in output is the result of the additional caution during the mining process while in the Phase 10 fault zone areas. The additional measures will affect productivity and result in less ore production from the area over the remainder of 2021. The second half of 2021 is expected to return average copper mill feed grades for the Candelaria Copper Mining Complex of 0.64% from low-grade stockpiled ores. The expected feed grade for the year is 0.59% copper.

Future Guidance Uncertain

Lundin Mining (TSX:LUN) (Nasdaq Stockholm:LUMI) may need to update the outlook for the life-of-mine plan pending the outcome of a review. With these changes in mine sequence creating new impacts for the project, some further guidance may need modification. However, production outlook for the company’s other operations as well as cash-cost guidance will be provided in July along with the second quarter operating results, and these are expected to be generally the same.

The Candelaria mine has been a productive project for the company. In 2019, the company reinvested in the mine fleet to help with efficiency and bring the project into alignment with the company’s overall clean mining goals. The project goes back to 2014 when Lundin Mining (TSX:LUN) (Nasdaq Stockholm:LUMI) acquired an 80% interest and operatorship of the Candelaria Copper Mining Complex in Chile, with the other 20% owned by Sumitomo.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Batteries are being used in everything these days, as devices are increasingly mobile and cars begin to require energy storage. Power grids are slowly being converted for solar and wind generation, and infrastructure is being developed with electrification built into the plans. We could eventually see electrified roads that charge cars as they drive.

To make all of this possible, President Biden has announced an infrastructure, and EV plan, that would put electric vehicles and electrification of the economy at the forefront of economic priorities and a jobs creation strategy. To support these efforts, battery metals will be needed by the millions of tonnes, and the U.S. will need to look to allies and economic partners to fill the demand. Two of the most important partners in this venture could be Canada and Australia.

Biden’s Big Vision

The American plan outlines that processing should be done domestically, but due to supply chain constrictions and cost-analyses, the U.S. should look abroad for most supplies of EV metals and materials. There are significant barriers to this strategy that American mining companies have pointed out. Ultimately, U.S. miners believe that the government should promote mining domestically and boost jobs through the industry. Additionally, they note that countries like Chile and Australia – the two largest lithium producers – ship most of their product for processing into battery cathodes and other parts to Asia. To divert and change their supply chains to supply the U.S. would be unrealistic and extremely unlikely.

However, the U.S. still has a shortage to fill to meet future demand, as mining analysts are quick to note. They predict that the country may not be able to supply more than 30% of the overall lithium demand required to build EVs domestically by 2030. This view was seconded by Adamas Intelligence analysts in a recent review. With the country striving to meet climate goals that include half of all new automobile sales to be electric by 2030 and every car on the road to be electric by 2040, the mining industry will have its hands full for some time.

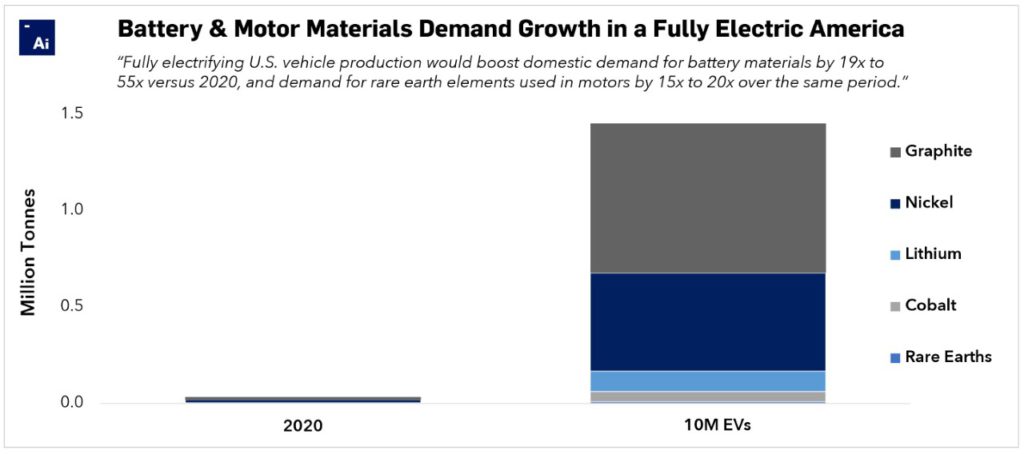

EV Batteries Set to Drive Huge Demand

Every year, approximately 10 million plug-in electric passenger vehicles and light trucks would need to be produced by 2030. This would grow battery capacity and motor power demand by 775-gigawatt hours, and 1,500 GW, respectively – every single year. Demand for raw materials would rise as well, far beyond what the U.S. could reasonably produce.

Metals and minerals like nickel, cobalt, copper, and lithium are all required for the battery production and many of the other components required for EVs. The U.S. hosts approximately 3% of known global nickel reserves, produces approximately 15% to 20% of the world’s Class 1 battery-grade nickel annually, and is the sixth-largest cobalt producer in the world. For the popular lithium-ion batteries used in EVs, all of these are essential and under-supplied right now. The energy-dense batteries that are likely to become more dense over time through investments in research and development continue to drive demand for nickel, cobalt, lithium, and more.

The U.S. Requires Stable, and Clean Mining Partners

Extraction is a complicated process, and with a growing focus on environmental, social, and governmental issues (ESG) at the forefront of the equation, mining companies are paying special attention to not just what they are mining, but how they are mining it. Canada in particular extracts all three of the mentioned minerals and metals above with a high degree of transparency and provenance, giving the country an advantage over other countries that may have looser regulations and enforcement.

For the U.S., to buy mined products from producers that did not mine in a safe or clean environment would be in opposition with the project’s overall goal of making the environment cleaner. To mine the materials necessary for the electrification of the economy in a clean way is a necessary element of this plan if it is to be done effectively. Canada and Australia also have stronger workers’ rights in effect and other jurisdictions with cobalt and nickel mining sometimes have issues with human rights as well.

Adamas Intelligence’s recent analysis reads, “In a fully electric America, it would need more than three times the nickel supply that Canada currently produces and 15 times its current cobalt supply annually.” The analysis goes on to say that although Australia – the world’s top lithium producer with 50% of global annual output – could benefit greatly from U.S. electrification, it is unlikely that the island nation would redirect exports from Asia. However, getting around this barrier is essential as the U.S. could buy all of Canada’s supply and still require much more.

Economic, Social, and Electric Goals Require Cooperation

The geo-political and economic alliance made between the G7 countries means that the partnerships for the common goals of electrification and clean-energy initiatives are fully aligned. It will be up to these friendly nations to come together to figure out how to meet those goals together while balancing their own electrification plans. While Canada might be able to supply a large chunk of the demand from the U.S., the northern neighbour’s own needs will have to be factored in as well. Canada has also set aggressive electrification targets along with Europe and Australia, and while U.S. demand is set to outstrip all of the other regions in the next ten years, these partners will need to work together to avoid supply vacuums and other issues as they all race toward the same targets.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Diavik property, Canada. Source: Rio TintoCopper stocks are on a tear this year, in no small part due to the rising price of copper as supply shortages and a surging demand boom converge to create some of the best conditions in recent history for stocks. While the current climate has been more than favourable for copper stocks, they have often had an advantage historically over gold and other precious metal stocks due to the red metal’s multiple industrial uses.

Rio Tinto (NYSE:RIO)

Producing iron ore, copper, diamonds, gold, and uranium, Rio Tinto is one of the largest mining companies in the world. The stock has doubled in the past year, reflecting the company’s return to near-full production capacity as well as a lifting of lockdown restrictions in the 35 countries it operates in globally.

Southern Copper Corporation (NYSE:SCCO)

With mining operations located in Peru and Mexico along with exploration operations in both those countries plus Chile, Southern Copper is one the largest integrated copper producers. The last year has seen SCCO stock soar 110%. Investors who have held the stock must be happy to see their positions double over the past 12 months.

Solaris Resources (TSX:SLS)

As a junior mining company, Solaris Resources holds a large amount of potential. The company is focused on its flagship Warintza project in Ecuador, for which it has reported positive assay results as it continues to expand the project to adjacent sites. Investors seem to like the progress, because the stock is up over 1000% since the IPO less than a year ago.

Freeport-McMoran Inc. (NYSE:FCX)

This company operates large and long-term geographically diverse assets that hold reserves of copper, gold, and molybdenum. The company’s scale is used to maintain a dominant position in the market, using properties like the Grasberg mineral district Indonesia, which is one of the largest copper and gold deposits in the world, to fortify its balance sheet. FCX stock is up 370% in the past year, as investors continue to pile into this veteran mining company delivering year after year.

Conditions Are Ripe for Copper Miners

Mining companies exploring and producing base metals like copper usually have higher dividend yields than hedges against inflation like gold stocks. They are also generally better value as they sit cheaper in relation to earnings and cash flow. With a low P/E, copper stocks usually have less distance to fall if markets take a hit, and the upside is higher when the stock runs. With lower risk and higher potential reward, copper stocks are always in favour with the investing community for short, and long-term plays.

Short-term, copper should be able to benefit from the rising demand coming from increased battery production and clean energy storage solutions. The increase of electric car sales and the electrification of infrastructure and power grids around the world requires huge amounts of copper to transport and store the energy. Labour shortages and technical delays in some regions of the world have also contributed to a general slowdown in copper production, but as 2021 rolls on, the environment is looking strong for copper mining companies and their stocks.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

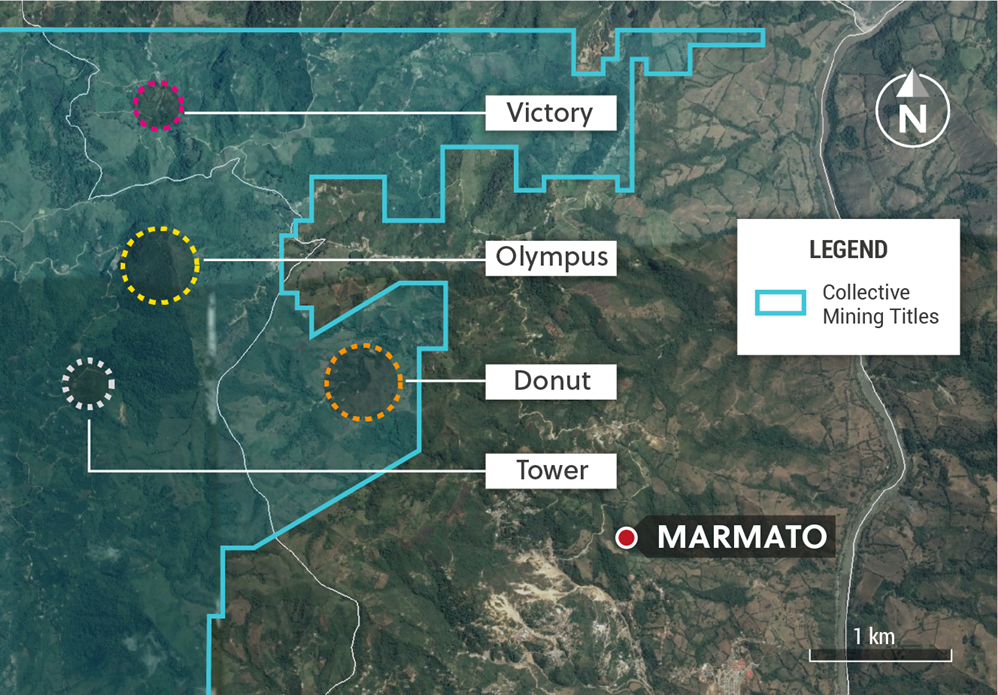

Collective Mining’s Guayabales project is making headway with the company identifying a new cluster of mineralized porphyries and associated gold-silver vein systems at the site in Cladas, Colombia. Situation contiguous and immediately along strike to the northwest from Aris Gold’s Marmato Gold Mine which contains proven and probable reserves of 2 million ounces gold, 4.35 million ounces silver, the Guayables project is rapidly advancing with intense geological mapping, soil and rock sampling programs, and has completed a high resolution, airborne geophysical survey.

Breaking New Ground

Collective is fortunate to be the first company to ever consolidate the prospective land package along strike to the northwest and adjacent to Marmato. The company is capitalizing on a significant section and the Guayabales project is a major leap forward for the company and the area.

The company’s interpretations of the survey and project is that the precious metal mineralization is related to a series of copper-gold-molybdenum porphyry intrusion, like at least partially responsible for the mineral endowment of the area. Current surface exploration has covered only 20% of the project area, but has identified four initial targets referred to as Donut, Tower, Olympus, and Victory.

Details provided by Collective Mining:

- The Donut target is part of a northwest trending and outcropping cluster of mineralized copper-gold-molybdenum porphyry intrusions. Shallow underground workings have exposed large zones of porphyry veining hosting various copper sulfides including chalcopyrite, chalcocite and lesser bornite with molybdenite and abundant pyrite. The Donut target displays intense zones of both potassic alteration and overprinting vein and stockwork systems. The porphyry zone is enveloped by a large scale (+1.5 km) and continuous anomalous zone of in-situ and coincidental gold, copper and molybdenum soil anomalism. Assay results are anticipated within the next 30 days from preliminary channel sampling program performed in existing underground workings and a maiden drill program is planned for September 2021.

- The Tower target, located in the western portion of the project area at the deformed contact between graphitic schists and diorite intrusives, incorporates a similar geological setting to the prominent Marmato gold-silver orebodies that are immediately to the south-east of this zone along strike. The north-south trending contact zone, recently exposed by a landslide, has exposed a 50 m x 50 m area of intense sericite-silica alteration with disseminated sulfides. This structure is exposed in old artisanal working located more than 1 kilometre to the NNW of the Tower outcrop. Detailed mapping and soil auger sampling of the entire target area is in progress to determine the dimensions of the target. Assays results from an extensive channel sampling campaign are expected within the next 30 days and will be followed shortly thereafter by a maiden drill program.

- The Olympus target hosts a large-scale sheeted vein and breccia, quartz-(carbonate) sulfide system, currently measuring over 400 metre true-width with an interpreted strike length of greater than 1 kilometre that trends to the Donut target. These late-stage porphyry-associated NW structures overprint a larger-scale porphyry style stockwork veinlet system within potassic altered quartz diorite porphyries and country rocks. Numerous artisanal workings have followed individual vein and breccia structures for +400 metres in strike length and reconnaissance grab samples have returned values of up to 72.4 g/t gold and 1,098 g/t silver. The exploration team is currently undertaking geological mapping and systematic soil and channel sampling in order to define the overall size of the target. A maiden drill program to test the Olympus target is anticipated to ensue in Q4, 2021.

- The Victory target is located in the north of the project area and consists of a stockwork of porphyry magnetite veinlets with disseminated sulfides hosted within altered diorite intrusive host-rocks. The large target area is outlined well by the airborne magnetics which illustrates a horseshoe shaped zone of high magnetic bodies enveloping a magnetic low. Multiple phases of altered and unaltered diorite intrusive were observed during reconnaissance fieldwork. Soil sampling mapping and rock channel sampling is in progress in this area with drilling planned for Q1, 2022.

Ari Sussman, Executive Chairman of Collective Mining stated, “This is the first time that any mining company has consolidated a commanding land package encompassing the northwest projection of the historically significant Marmato mine, which has been in continuous production for more than 500 years. Results to date from our Guayabales project are astounding, with multiple styles of precious and base-metal mineralization having been discovered covering more than 5 kilometres. The potential for discovering overprinting high-grade and bulk tonnage mineralized systems is excellent.”

Source: Collective Mining

The Guayabales Project

An initial 5,000 metre drill program has begun at the project with initial assay results projected for Q3 2021. The project is located in the Caldas region of Colombia, where Collective Mining works closely with the local Municipality and agriculture groups to invest in infrastructure, water access, and support for the coffee industry.

Collective Mining’s ESG approach to mining along with a focus on benefiting stakeholders at every step of the projects they work on has piqued investors’ interest in the company. The first day of trading saw Collective shares pop 205%, and the stock has moved higher since then.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Exploration company Tier One Silver (TSXV:TSLV) began trading on the TSX Venture Exchange on June 9, 2021, under the ticker TSLV. Spun out from Auryn Resources in October 2020, the company is exploring assets in Peru for silver, gold, and base metal deposits. While maintaining its mission of generating shareholder value, the company is also committed to the shared value that comes from implementing sustainable and responsible development and mining practices.

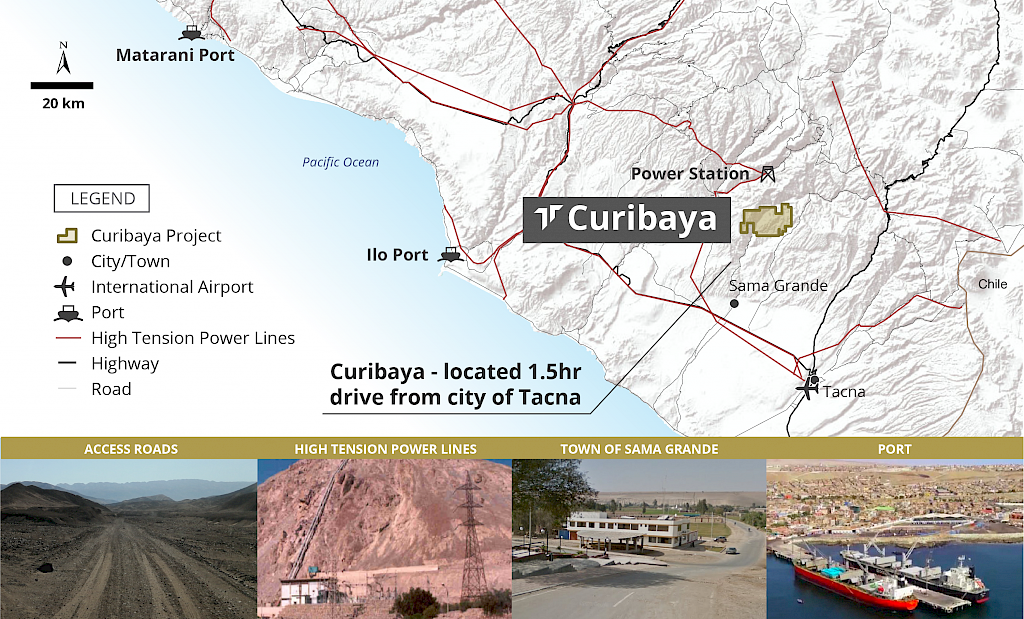

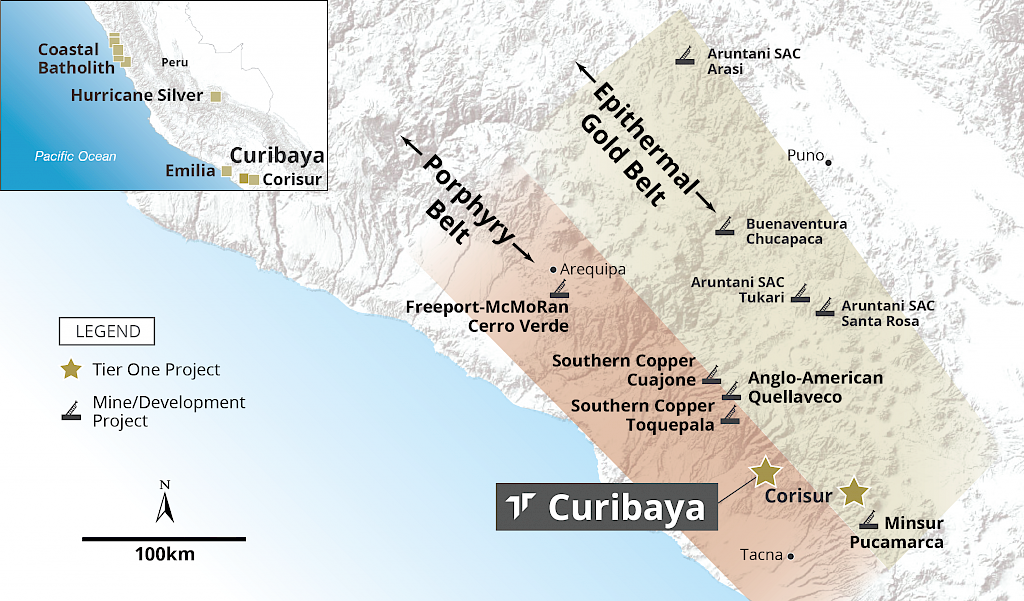

The pillars of the company’s environmental, social, and governmental (ESG) principles include health and safety, the protection of ecological and cultural heritage resources, social responsibility, as well as indigenous and local community engagement. Tier One Silver (TSXV:TSLV) is taking those principles into account at every one of its exploration assets in Peru, including Hurricane Silver, Emilia, Coastal Batholith, Corisur, and its flagship silver-gold project, Curibaya.

A True Flagship Property

The Curibaya property spans almost 11,000 hectares in a copper porphyry belt with some of the country’s largest porphyry deposits. Major mining companies are in the pophyry-rich area, including Freeport McMoRan, Southern Copper, and Anglo-American. The belt has returned high mineralization, and the deposits being within the same region, there is robust transportation and operational infrastructure in place, with easy access at multiple points. Located just 48 km north-northeast of the provincial capital Tacna, the property is accessible by road in just 1.5 hours.

Initial surface sampling programs have already returned multiple high-grade samples of silver, gold, and copper over a 4×5 kilometre alteration system. Although in its early stages, Tier One Silver (TSXV:TSLV) believes the Curibaya property holds precious metal intermediate sulfidation, epithermal, and copper porphyry targets.

Last week Tier One received a Peruvian Inicio de Actividades permit, which authorized the company to begin the inaugural drill program at the property. The authorization signals the end of the permitting process with MINEM, the Peruvian mining regulator, and the go-ahead for the company’s drill program at this significant flagship project.

Liftoff

Yesterday, the company announced that it had begun the first-ever drill program at the Curibaya property. Tier One Silver’s balance sheet is strong and is well-capitalized for a drilling capacity of 10,000 metres, with the initial phase of diamond drilling consisting of approximately 6,000 metres. Tier One Silver (TSXV:TSLV) holds an FTA (Ficha Tecnica Ambiental) drill permit), allowing the company to drill up to 40 holes from 20 drill pads. The drill plan includes about two kilometres by 1.5 kilometres in an area with strong alteration and high-grade surface mineralization. As the flagship project for the company, Curibaya is an excellent opening salvo to show the world and investors what it can do.

Peter Dembicki, President and Director of Tier One Silver, commented: “This is an exciting time for Tier One Silver shareholders as we begin diamond drill exploration at Curibaya – a project we feel has world-class potential due to its scale, exceptional high-grade silver and gold identified on surface over a significant area and the project’s location on a globally recognized prolific mining trend in Southern Peru. The detailed drill preparation completed by our technical teams will allow us to test multiple targets with each hole. This is the culmination of years of work at Curibaya by our team in Peru, and we couldn’t be more excited to test and gain an understanding of what we believe could prove to be a significant discovery.”

Expanding Tier One’s Reach, and Investor Options

Due to the success of the company’s listing on the TSX Venture Exchange, Tier One Silver (TSXV:TSLV) is also applying to list on the OTCQB Venture Market. This is a significant step for Tier One toward increasing its visibility within the U.S. capital markets. If listed on the exchange, the company will continue to trade on the TSXV. A listing on the American exchange would provide the company with greater exposure to the market and a platform to launch more drill programs and exploration as it raises more money.

After just over a week on the TSXV, the company has hit an average trading volume of 660,830 and a market cap of $193.7 million, foreshadowing a run of investor interest in the company that could propel its projects far into the future. As exploration continues, investors will be watching Tier One Silver (TSXV:TSLV) closely for continued progress, particularly at the Curibaya site.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Companies engaged in exploration, mining, and trading often have good returns and revenues. The past year has seen the VanEck Vectors Gold Miners ETF (GDX) underperform the broad market in the last 12 months, but the 11.8% return was more than solid. It is only against the backdrop of a 46.2% gain for the iShares Russell 1000 ETF or the S&P 500 that comparisons lose steam.

Mining for Gold Value

Gold mining companies within gold indexes, however, have been generating asymmetric returns. Many of the winners have continued to scoop up the gains of a rising gold price and a favorable market. Today we’ll take a look at those stocks which may be undervalued according to it’s P/E for June 2021.

Stock picking is often thought of as the reserve of people who have a special talent or gift, however, value investing is as simple as figuring out whether a business’s stock is cheap compared to its intrinsic value as measured by its price-to-earnings ratio. Taking a look at the 12-month trailing P/E ratio, the best value gold stocks are Centerra Gold Inc. (TSX:CG) (NYSE:CGAU), Jaguar Mining Inc. (JAG.TO), Torex Gold Resources Inc. (TSX:TXG), Karora Resources Inc. (TSX:KRR)), and Kinross Gold Corp. (TSX:K)).

Centerra Gold (TSX:CG) (NYSE:CGAU)

The Canadian gold mining and exploration company operates three mines at the moment producing 824,059 ounces of gold and 82.8 million pounds of copper in 2020 alone. The company ran into a speed bump at its Kumtor Mine in the Kyrgyz Republic when the Kyrgyz Government took control of the mine in mid-May. The company lost control of the mine and suspended previously issued guidance for 2021 due to the uncertainty of the situation. However, with a 12-month trailing P/E ratio of 4.1, the company could be a value play for some portfolios.

Jaguar Mining Inc. (TSX:JAG) (OTC:JAGGF)

Our second Canuck on the list explores and develops gold properties in the Iron Quadrangle in Brazil, a profitable greenstone belt in Minas Gerais, Brazil. With a 12-month trailing P/E of 5.4, Jaguar (TSX:JAG) (OTC:JAGGF) is a technical value play for a company operating in an area of mineral exploration dating back to the 16th century.

Torex Gold Resources (TSX:TXG) (OTC:TORXF)

Torex’s 100% owned Morelos Gold Property comprising 29,000 hectares in the Guerrero Gold Belt in Mexico is the flagship project for the company, in a portfolio that includes two other major mines in Mexico. The company’s P/E of 6.7 may be an indicator of an undervalued company waiting for the right attention from investors.

Karora Resources Inc. (TSX:KRR) (OTC:KRRGF)

Both of the company’s primary gold-producing operations are located in Australia along the Norseman-Wiluna Greenstone Belt. Net earnings for Q1 2021 came in at more than ten times YoY as revenue grew 9.2%. The company’s P/E of 6.7 could be an indication of a value play waiting to be unlocked with the kind of financial results from the first quarter of this year.

Kinross Gold Corp. (TSX:K) (NYSE:KGC)

With a diverse portfolio spanning Brazil, Chile, Ghana, Mauritania, and Russia, and forward guidance of 2.4 million gold equivalent ounces for 2021, Kinross (TSX:K) (NYSE:KGC). Net earnings rose 21% as revenues grew 12.1%, possibly making the company’s P/E of 6.8 a value indicator for 2021.

Hunting for Deals

Undervalued companies can be opportunities to pick up shares at bargain prices before the rest of the market figures it out. Stocks like Centerra Gold (TSX:CG) (NYSE:CGAU), Jaguar Mining Inc. (TSX:JAG) (OTC:JAGGF), Torex Gold Resource (TSX:TXG) (OTC:TORXF), Karora Resources Inc. (TSX:KRR) (OTC:KRRGF), and Kinross Gold Corp. (TSX:K) (NYSE:KGC) could be the value buys for 2021 for investors looking to add some gold stocks to their portfolios.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

China’s Ganfeng Lithium continues to expand its reach with Monday’s announcement that it will acquire a 50% stake of a special purpose vehicle set up by Australian-listed Firefinch Ltd., which owns the Goulamina hard-rock mine in Mali. Ganfeng will take at least half of its first-phase output as part of the $130 million deal.

Last year, a feasibility study was completed but a production start date has not been set yet. The Goulamina mine, laying about 150 km by road south of Mali’s capital Bamako has 108.5 tonnes of resources and high-grade spodumene concentrate, according to Firefinch’s presentation last month. The project is “one of the world’s highest-quality lithium assets”, and adds significant value to Ganfeng Lithium’s overall project portfolio.

For now, Genfeng will acquire offtake rights for 50% of the mine’s first-phase annual production capacity of 455,000 tonnes of spodumene concentrate, but has the option to acquire 100% if it helps Lithium du Mali raise debt or gives financial assistance to the company. On top of these terms, Mali’s government has the right to take 1-% of the equity free of charge and pay in cash for up to 10% more.

Ganfeng Lithium is one of the world’s largest lithium producers and could help the Mali-based company raise funds quickly. The Chinese company could help raise at least $64 million from banks or other financial institutions earmarked for development and construction of the mine, and has the option to provide the company with up to $40 million in direct financial assistance, according to a filing from Ganfeng.

Ganfeng lithium has projects in China, Mexico, Australia, Argentina, and Ireland. The company is one of the biggest lithium miners in the world and has significant sway in the African continent with so many projects and investments in the region. The company also signed a five-year deal last December with the Manono mine in the Democratic Republic of Congo (DRC) for spodumene concentrate, but does have an equity stake in the project.

With lithium being one of the most important elements for much of the technology in batteries powering everything from smartphones to electric vehicles, Ganfeng is mining a strategically important and economically valuable resource. Its partnerships and investments in Africa give it strong control of the mining and processing networks in the region, and it continues to expand around the world.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

As mining companies continue to shift away from dirtier, less efficient practices, electrification is one of the first things on their to-do list. For many, reducing carbon emissions on-site and throughout operations outside of mining is critical to attracting capital and remaining competitive. The rising costs of fuel and complex maintenance for combustion engines have given companies an incentive for change, and miners are stocking up on battery-powered trucks for hauling, transportation, and other tools that previously used diesel or gasoline to get the job done.

A Scandinavian Approach

Swedish equipment manufacturer Sandvik now expects that the market for battery-electric underground mining equipment will grow at a faster clip in two to three years. The dual goals of lowering emissions and cutting costs give these companies plenty of incentives to make the switch, with investors also looking on eagerly to see what companies are doing with respect to the all-important environmental, social, and governmental principles.

Sandvik’s mining business head said that the company could sell more electric than diesel-driven underground mining equipment in the coming ten years. Epiroc and Caterpillar, two of Sandvik’s main competitors and some of the largest suppliers in the world for the mining industry, will also be going head to head with the company to supply the tools necessary for the electrification coming down the line, beginning now.

Sandvik claims that its approximately 30 battery-electric loaders and trucks operating in underground mine production is the largest amount in current operation, more than any of its competitors. Still, this amount is less than 0.5% of its total fleet and shows how much runway there still is for this market segment to expand for equipment suppliers. As it continues to gain pace, it will drive much of the new equipment sales over the coming decade. Henrik Ager, head of Sandvik Mining and Rock Solutions, said, “In the past two years, we have gone from thinking that electrification might turn into a great technology shift to becoming certain that’s where we’re heading.”

He said that in two to three years, electric machinery should be fully proven to work in mines and be part of the discussions for all procurement. Approximately 60% of an underground mine’s energy consumption comes from infrastructure, mainly electrified. Still, the rest is consumed by loaders and trucks, transporting and hauling heavy materials from the site to refinement centers and processing plants or to stockpiles. Those loaders and trucks still primarily run on diesel, carrying up to 65 tonnes of rock at a time.

Good for the Environment, Good for Investment

For investment bank UBS, the electrification of the industry is not only an environmental benefit for all stakeholders but will bring savings for mining companies as well. Analyst Guillermo Peigneux Lojo said, “In the years to come we shall see an accelerated replacement cycle for especially underground mining equipment, although surface equipment will also benefit from solid growth rates.”

Barriers still remain until full adoption of electric vehicles and fully electric mines are the new normal. Battery-driven loaders and trucks are more expensive to buy, making the upfront costs unpalatable for some mining companies at the moment. However, down the road, the benefits are numerous. Savings on ventilation and cooling, high costs in underground mines can make it beneficial and profitable for mines to go completely electric right now.

Major mining companies have already begun the process of electrification at many of their mines. Newmont’s (NYSE:NEM) Borden gold mine and New Gold’s (TSX:NGD) Afton mine currently use Sandvik’s battery-electric equipment in their operations. The loaders and trucks, as well as some of the lighter equipment, use lithium-ion batteries, a technology that allows for faster charging and higher battery density, leading to more prolonged use between charges, an essential factor for rapid adoptions.

Mirroring The Ethos of Tesla and Elon Musk

Elon Musk’s Tesla has created a similar business model, focusing on bringing battery technology to the forefront of the mission, and bringing down the cost and effectiveness of the batteries in its vehicles. Sandvik’s vision is to do the same; the company is building around the battery instead of starting with the vehicle itself. The research and development costs are much lower, and the equipment being used is already efficient and effective.

“It’s the Tesla parallel. That is what they have done, and it’s much better,” Ager added.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

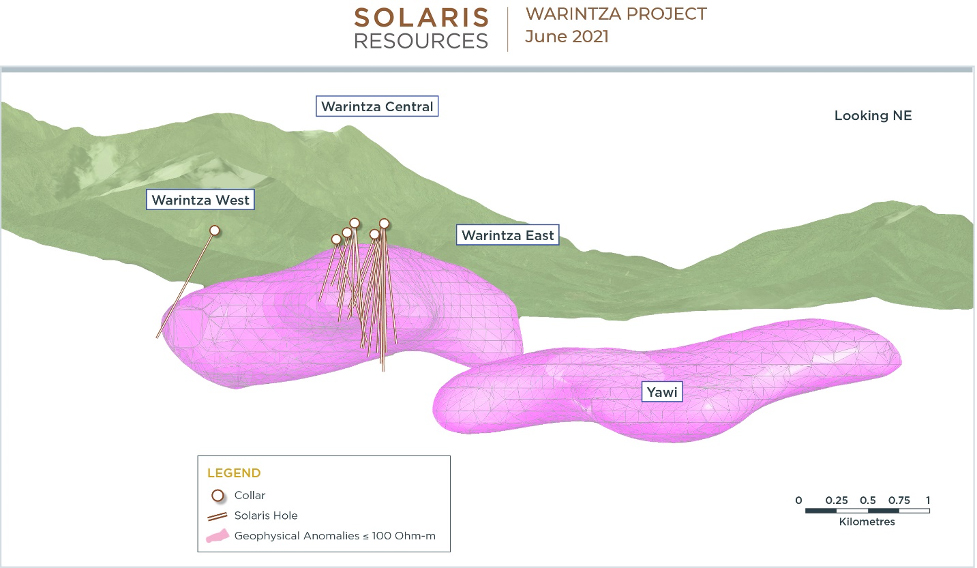

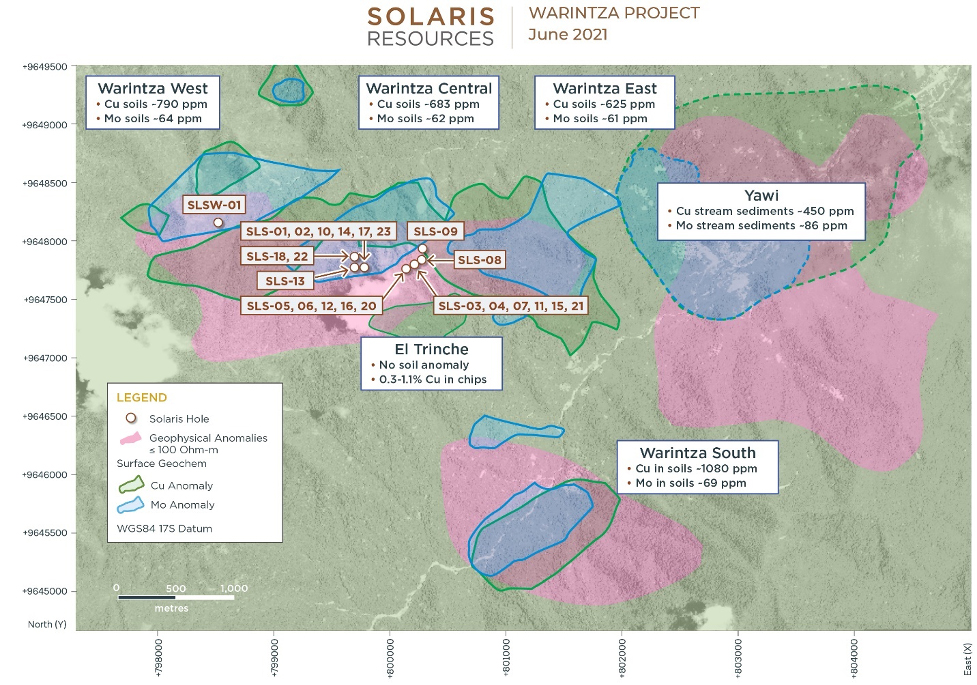

Solaris Resources (TSX:SLS) (OTC:SLSSF) continues to forge ahead at its flagship Warintza project in Ecuador; maiden drilling has begun at its Warintza East site. Located approximately 1km east of Warintza Central, it is one of five main targets with a 7km x 5km cluster of porphyry targets at the property. With a similar expression at Warintza Central, Warintza East is set to become another fruitful exploration site for the company.

Major News

Solaris (TSX:SLS) (OTC:SLSSF) has also defined a major copper porphyry target at Yawi after continued processing of geophysical and geochemical data. This extends the strike length of the Warintza cluster of porphyry targets to 7km, a massive bump in the potential for the project. Listed below are some of the highlights from the recent results and accompanying press release:

- Commenced maiden drilling at Warintza East, located approximately 1km east of Warintza Central, where recent drilling has intersected 1,029m of 0.73% CuEq¹, including 420m of 0.83% CuEq¹ from surface (see press release dated May 26, 2021)

- Warintza East is one of the five main targets within the 7km x 5km cluster of porphyry targets defined on the property and has a similar expression as Warintza Central, with overlapping copper and molybdenum soil anomalies associated with an underlying high-conductivity anomaly

- Further processing of the geophysical dataset (see press release dated February 16, 2021 for initial results) has revealed a much more extensive, high-conductivity anomaly at the recently-identified Yawi target, located approximately 1.5km to the east of Warintza East

- The large-scale geophysical anomaly at Yawi coincides with overlapping copper and molybdenum stream sediment anomalies; field crews are now completing additional sampling and reconnaissance work to define locations for initial drill testing

- Weather conditions are improving at site and drilling activities are once again ramping up, with eight drill rigs turning, the ninth rig set to commence in the coming days and the tenth rig being delivered

Source: Solaris Resources

The Warintza East site is the new frontier in the expanding Wartinza Project that continues to return positive assay results from its drill program. Located one kilometre east of the main Warintza Central site, East sits at a slightly lower elevation, with the target being defined by overlapping copper and molybdenum soil anomalies associated with an underlying high-conductivity anomaly. Warintza East’s first hold was collared in weathered porphyry uncovered by earthworks. The discovery was made during drilling platform construction.

Experts Agree; This is “A New Era for Solaris” (TSX:SLS) (OTC:SLSSF)

Mining engineer Lennin Munoz, commenting on the beginning of drilling at Warintza East, said, “For me, this is driving a new era for Solaris. This reflects what you get when you are in a porphyry cluster area; your targets will come and come. The upside is clear in all directions. The byproducts trend in Yawi’s direction is confirmed with these anomalies.”

Additionally, Solaris (TSX:SLS) (OTC:SLSSF) has identified a high-potential target at Yawi through the processing of geophysical data covering the 5km strike of the Waintza porphyry cluster known at the time. The geophysical anomaly appears to be an elongated lobe on the easter boundary of the area. Once coverage was extended more to the east, stream sediment sampling has more than doubled the size of the anomaly, defined the target area, and created an exciting development for the future of the drill program. Yawi field crew are not completing additional sampling and reconnaissance work for confirmation and to select specific locations for initial drill testing.

Vice President of Exploration for Solaris Resources Jorge Fierro commented: “We are very excited to commence the first-ever drilling at Warintza East, targeting the third major copper porphyry discovery within this richly-endowed but underexplored property. In addition, further data processing has revealed a much more extensive porphyry target at Yawi than previously understood with additional sampling now underway.”

Positive Results Continue to Flood In

The commencement of maiden drilling on top of recent positive assay results from the Warintza Central site has continued to push the stock higher. Thirty-one holes have been drilled at the Warintza Central site, with promising results having been reported for 22 of those drill holes. The new first hole at Wartinza East (SLSE-01) now aims to explore the new anomaly that extends continuously from Warintza Central to the target in the east.

Figure 1 – Long Section of 3D Geophysics Looking Northeast

Note to Figure 1: Figure looks northeast and depicts high-conductivity geophysical anomaly (defined at 100 ohm-m) generated from 3D inversion of electromagnetic data, encompassing from left to right Warintza West, Central, East, and the Yawi target (Warintza South lies off image to south).

Source: Solaris Resources

Figure 2 – Plan View

Source: Solaris Resources

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The mining sector has always used the latest technologies to stay at the forefront of its work and keep up with the times. From extraction to processing and even shipment, the industry requires technology at every level of the business.

Current Tech Needs

Spatial data visualization is used to create more detailed and precise 3D models for depth perception and detail. The human brain is better able to understand and relate to complex, interrelated issues using 3D modeling. Often, that modeling can be supported with virtual reality (VR) to create an artificial software environment of the model using real-life data. Using VR, miners can experience the mine for themselves, plan a new mine before moving forward, and clear plans in greater detail without being in the field.

From above, mining companies use automated drones to produce the same results as a helicopter flyover, with lower costs and operations time. These drones or unmanned aerial systems (UAS) can do safety and surveillance surveys, asset management, stockpile measurement, infrastructure inspection, time-lapse photography to check progress, site mapping, and more.

Using the latest technology allows mining companies to innovate and address challenges at a more efficient and cost-effective level. This technology is also driving a more sustainable approach to mining as the industry continues to accelerate its environmental, social, and governmental goals over the coming years.

Future Tech Ramps Up

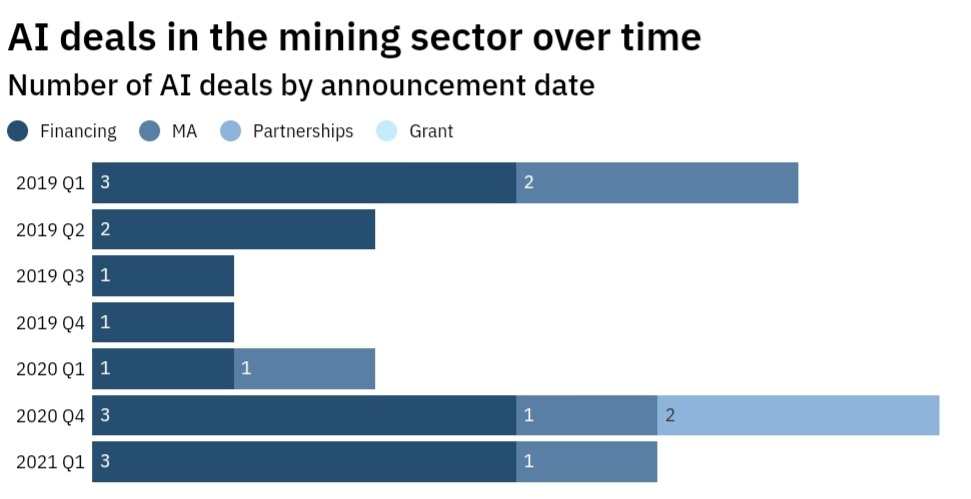

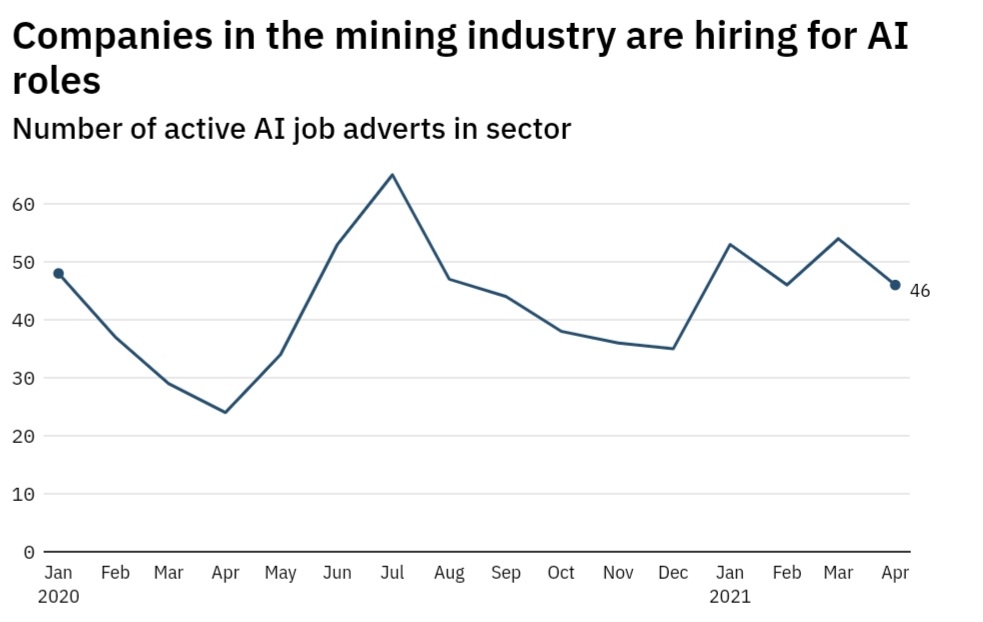

Now, a boom in the use of AI in the mining industry is set to shift the ground under miner’s feet. In the last few years, jobs, patents, and AI deals have been picking up, allowing the mining sector to take the next step into the future of operations and project management. According to an analysis of GlobalData data, AI is continuing to build a presence as companies complete more AI deals, hire for AI roles, and continue to mention it frequently in company reports, beginning in 2021.

The increase of financing, M&A, partnerships, and grants in the AI space has sped up, although there has been a slow down in the first quarter of 2021 from the fourth quarter of 2019.

Hiring continues to pick up as mining companies look to staff their teams with experts in AI development and implementation.

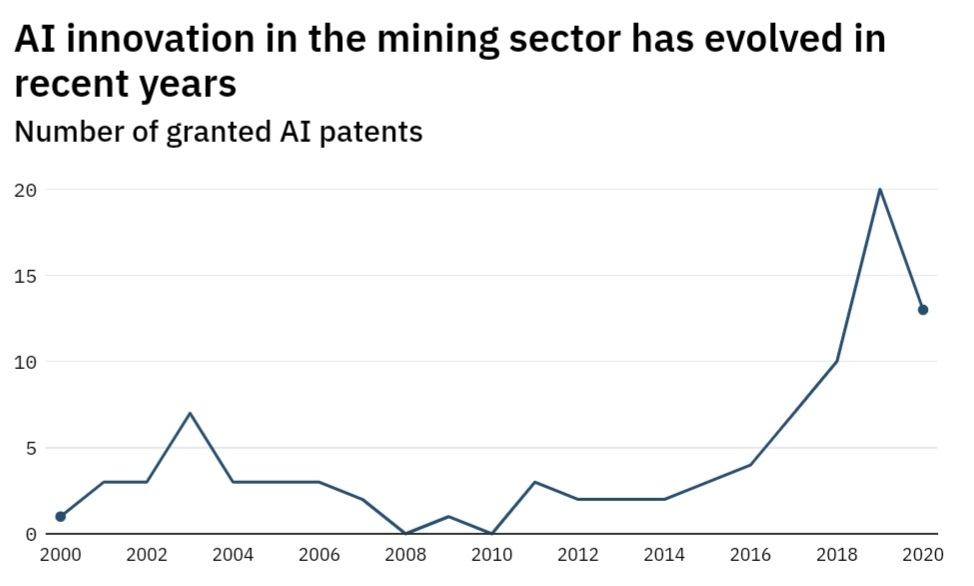

Another clear sign of the growing importance of AI in the mining industry is the rise of granted patents. From 2000 to 2014, there was an average of 2.4 mining patents related to AI granted. By 2020, that number rose to 13 patents, increasing the average number granted by 8.4.

These rapid shifts in technology are nothing new for the mining industry. The sector has always adapted quickly to the changing times and knows how to keep up with competitors both within the industry and among the many branches of the supply chain critical to its success. AI is helping companies use smart data and machine learning to improve operational efficiency, mine safety, and production workflow. Companies can now generate day-to-day data in half the time than what has been used in the field.

Some of the ways mining companies are using AI include mineral processing and exploration to find minerals more easily, as well as autonomous vehicles and drillers. Autonomous vehicles have been used in the industry for more than eight years, shuttling materials in their pit to pit operations and more. Drilling systems have also been equipped with AI to allow for a single operator that controls several drill rigs at once with AI-assisted software.

The efficiency and ESG gains made using AI and other technologies by the mining industry have given mining companies brand new ways to do their jobs, and produce at faster rates while maintaining social and environmental standards. The future is sure to see this trend accelerate, as the industry seems to be on the cusp of an AI boom.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Collective Mining (TSXV:CNL) is a strong partner for the communities in Colombia in which it operates. With ESG principles woven into the fabric of the company’s founding principles, Collective’s commitment to creating opportunities for all stakeholders solidifies the company’s position as a responsible miner.

Mining and Agriculture Integral to Stakeholder Success

Collective Mining’s (TSXV:CNL) strategic alliance with the Coffee Growers Committee of Caldas and the Municipality of Supia is based on the foundation that mining and agriculture work effectively together to create positive growth and development in Colombia. The Committee is part of the National Federation of Coffee Growers of Colombia (FNC), an influential and important institution in the agricultural industry. The coffee industry being one of Colombia’s most important industries alongside mining, the institution oversees the development of the coffee sector and ensures it remains healthy and profitable for everyone.

The company was awarded a notable recognition from the Municipality of Supia as a direct result of its work and contributions toward the improvement and development of the municipality’s infrastructure. Omar Ossma, CEO and President of Collective commented that, “Coffee is one of the main drivers of this region and this alliance is a very important step to promote sustainable coexistence of different economic activities with mining. We are honored to have received this recognition.”

Agricultural and mining ventures are integral to the South-American country, which has a long track record of positive gains in these areas. For Collective, supporting the Coffee Growers Committee of Caldas is a key component of the company’s 2021 ESG initiatives in Caldas. Caldas is well known for its rich coffee culture and is the second largest coffee producing department in the country. With 32,000 families in the department, the coffee industry is an integral part of the local economy and community.

An Alliance For Everyone

Members of the strategic alliance have invested in the development of local road infrastructure, improving access to water for local communities and supporting the municipality’s coffee producers. The total commitment from members of the alliance is $530,000 for 2021. 1,286 coffee growers covering 1,489 hectares of farmland in the Municipality of Supia will directly benefit as a result of the initiatives put forth by the alliance.

Collective’s (TSXV:CNL) alliance with the Committee and Supia has strengthened its bond with all stakeholders in the region, with Marco Antonio Londono Zuluaga, Mayor of Supia stating, “These are investments that will go directly to our small farmers and rural communities. We are pleased to have the support of Collective Mining in this initiative. It is key to work together and it is key to work as a team. This project demonstrates that responsible mining is possible.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

While the Democratic Republic of Congo made things slightly more complicated for miners by reestablishing an export ban, some mining companies are moving forward with new permits and the ability to export their full output.

Ivanhoe Mines (TSX:IVN) (OTCQX:IVPAF) has signed a copper concentrate and blister copper off-take agreement on competitive arm’s length commercial terms for 100% of the company’s Kamoa-Kakula project’s Phase 1 copper output. This is a decisive step in the right direction, as the projected output for Kamoa-Kakula is expected to hit 200,000 tonnes of copper per year. In the midst of a supply shortage, Ivanhoe Mines (TSX:IVN) (OTCQX:IVPAF) is set to fill some of the gaps.

This year, Kamoa Copper made its first jump into production on May 25. It began producing copper concentrate and made the first delivery to the Lualaba Copper Smelter on June 1. The project includes a high-tech, high-grade milling, flotation, and recovery process to produce the ultra-high grade, clean copper concentrate.

Strong Agreements In Place

Off-take agreements have been signed between Kamoa Copper and CITIC Metal (HK) Limited, and Gold Mountains (H.K.) International Mining Company Limited, a subsidiary of Zijin, for half of the copper products from the Kamoa-Kaula Phase 1 production. This deal encompasses all of the copper concentrate and blister copper resulting from the processing of copper concentrates at the Lualaba Copper Smelter.

Ivanhoe Mines (TSX:IVN) (OTCQX:IVPAF) has a strong partnership with the Lualaba Copper Smelter, located near its Kamoa-Kakula project, just outside the town of Kolwezi. The smelter signed a 10-year agreement with Ivanhoe Mines (TSX:IVN) (OTCQX:IVPAF) on May 31 for the processing of a portion of Kamoa’s copper concentrate production. The terms of the agreement will secure copper concentrate processing for Ivanhoe Mines (TSX:IVN) (OTCQX:IVPAF) and allow the company to maintain steady exports with permission from the DRC. With the first copper concentrates already delivered to the smelter (June 1), the first blister copper ingots are now due to be delivered within 30 days of delivery to the Lualaba Smelter.

Lualaba Smelter

The Lualaba Smelter is one of the biggest in the region and is wholly owned by Chinese companies. 60% of the smelter is owned by China Nonferrous Metal Mining Group (CNMC) from Beijing, and 40% is owned by Yunnan Copper from Kunming.

The smelter is the first modern, large pyro-metallurgical copper smelter built in the DRC and is located only 40 kilometers from the Kamoa-Kaula site. The smelter can be accessed via a recently-constructed road that gives Ivanhoe Mines (TSX:IVN) (OTCQX:IVPAF) easy access to the smelting site. It began operations in 2020, with plans to treat up to 150,000 wet metric tonnes of copper concentrates from Kamoa-Kakula.

Its mandate is to produce blister copper containing approximately 99% copper to be returned to Kamoa Copper. Then it will be collected by CITIC Metal and Zijin from a storage area at the smelter. From there, the copper will be exported by CITIC through the port of Durban, South Africa, a process for which CITIC will be completely responsible for arranging freight and shipment to the final destination.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

China’s iron ore imports have been on a tear in 2021 so far. March logged 102.1 million tonnes imported, and April dropped to 98.6 million tonnes. One of the most robust partnerships for this trade has been between China and Australia. Australia’s iron-rich reserves have been supplying China for years, and iron ore transactions account for a large part of the island’s GDP.

Most recently, though, iron ore prices are dropping, as China’s trade data for May showed shrinking profit margins for steelmakers, hitting enthusiasm with a wet blanket. China is responsible for more than half the world’s output, and any shift in their trade data always signals a shift in the market.

Steel Exports Hit Iron Ore Imports

May saw iron ore imports hit 89.8 million tonnes in May, significantly lower than March and April. Steel exports followed lower, down 34% from April to May to 5.3 million tonnes.

“The proportion of iron ore shipped to China from Australia fell a lot recently, and we can see the decline to continue in coming months,” said Wang Yingwu, an analyst with Huatai Futures in Beijing.

Iron ore and steel price dynamics are closely linked, with Chinese producers driving much of the demand. When exports slow or grow, overall demand can shrink by up to 15% from month to month. “The sharp drop in steel prices…has led to a sharp drop in the profits of steel mills,” according to a recent note from Sinosteel Future analysts.

That demand slowdown is also creating a lot of short-term volatility for iron ore as global supply remains tight, generally keeping prices high.

Global Iron Ore Production In a Delicate Balance

One producer feeling the squeeze is Vale (VALE). Last Friday, the company had to stop production at the Timbopeba mine in Brazil and a section of its Alegria mine. Prosecutors had ordered the evacuation of an area around the nearby Xingu dam in the state of Minas Gerais.

In an already tight market, these closures could account for up to 40,000 iron ore tonnes per day, according to Vale (VALE).

“It is unlikely the global balance will feel the full weight of this supply vacuum as Vale (VALE) fights to overturn this ruling as quickly as it was imposed,” managing director at Navigate Commodities in Singapore Atilla Widnell said.

Still, as iron ore prices continue to swing and ultimately climb, the squeeze is likely to continue for steel producers importing the valuable ore, even as steel exports continue to shrink in some parts of the world.

The most-traded September iron ore on China’s Dalian Commodity Exchange ended daytime trading 4.4% lower at 1,118 yuan ($174.70) a tonne.

Benchmark 62% Fe fines imported into Northern China (CFR Qingdao) were down 2.4%, changing hands for $202.42 a tonne, according to Fastmarkets MB, on Monday afternoon.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Junior mining companies are the prime drivers of new IPOs for the mining industry. The rewards for investing in these companies often far outweighs the risks, as getting in on the ground floor of a junior mining company can mean triple digit percentage point gains or more. Still, there are many questions on investors’ minds before they invest in a mining company, including the company’s plan for exploration, and how to evaluate whether the junior miner has a good chance of success.

Due diligence and risk management are just as essential when investing in junior mining companies, but factors as wide ranging as the strength of the management team and technical advisors, as well as the company’s ability to finance its exploration with a strong balance sheet, to the viability and potential of its chosen drill sites. Paying attention to the financials, operations, and the drill plan and results are all required to make better decisions when investing in junior mining companies. To get a better understanding of this potentially highly lucrative investment strategy, we spoke with Lennin Munoz, a geo engineer and mining industry veteran.

Mr. Munoz was able to provide us with some of his insights into why it is important to take a broad overall look of the company, as well as a detailed assessment of its drilling results and management philosophy.

Taking a deep dive into a junior mining company means going beyond the headlines and getting in the financials, and using critical analyses like NAV, IRR, CAPEX, and more to make an informed decision.

What are the critical analysis points you use to determine the strength and viability of a project?

Desirability, Viability, Feasibility and Sustainability. Inside the desirability angle for example if I look for a tier 1 or 2 deposit, I’ll definitely start with geology, for me the ORE BODY IS ALL! So good tonnage and grade is a key factor (e.g 1 Bt 1%Cu or 200 Mt 2g/t Au), then I analyze the viability of the project, for example, potential to be developed, metal production profile, CAPEX intensity, All in Sustaining Cost position in the cash cost curve. Then, I incorporate the feasibility perspective for example, mining methods, high grading programs in first years (payback), Geotech & hydrogeology, metallurgy, processing, tailings and water management, etc. This review helps me to complete my SWOT analysis, so at the end I include the sustainability framework to have a clear map of risks and opportunities, so I can at least measure which is my main risk and what the company is doing about it.

All of this process is summarized in a model where I define the metrics to rank investment opportunities, for example, NAV, IRR, payback, CAPEX, others. I like to calculate NAV/share since this is a comparable metric with the market value and I could make decisions according to my risk/reward ratio.

How important is the environment, social, and governmental (ESG) aspect for a junior mining company? How important is it for you as an investor, and are the companies doing this right changing views on the mining industry?

ESG is here and these important three letters are a must in any project valuation, for example, I use to review assets using a mining economics framework split in desirability, viability, feasibility, and sustainability (I used the Hutton model), is in this last point that ESG plays a key role, a decisive point that can determine any GO or No GO; my experience in the industry tells me that you can have the best skarn deposit, with a tremendous mine plan, already approved by your company’s board and be in a BFS stage, but without an environmental view, a social acceptance, will not fly. Or it can, but is this sustainable in the long term?

It’s difficult, will not be easy, net zero emissions as an example will be a very expensive initiative, but is here, I’ll try to be in Minexpo this September, I’ve reading very interesting material about new technologies in different vendors, thinking in carbon emissions, green energy, or any other idea aligned with the ESG framework.

Last but not least, and by the way I think the most important part, the social aspect, is that the industry is turning mindsets and thinking about how you can work in the same environment for mutual benefit. Learning from other’s mistakes through history is a very powerful tool in this sector. I think most of the developers are changing the strategy to implement a real social, and sustainable model.

Which companies are proving out those ESG commitments and critical analysis points the best right now?

Particularly, I really like what Solaris Resources (SLS.TO) is doing in Warintza, Ecuador. This is not an easy task, a lot of effort on the ground is required, and of course you need a tier 1 team to do that, a very skillful one that can understand what is happening and what are the needs of all the stakeholders. This level of envelopment is so incredible that Lasso and Arauz mentioned the project in public interviews, so the relevance of the project is across the country.

Let’s continue with what Anglo American (AAL.L) is doing, for example they are clear about the feasibility of 100% renewable energy for the Quellaveco Project; this is a very important greenfield development for Peru, first autonomous project, 100% renewable!

Another example is Vale (VALE), after Brumadinho in 2018 and all the facts down the road, they are turning to dry stacking tailings facilities, we are at an inflection point about waste management. Going to dry stacking is not cheap but thinking in long term and safety for stakeholders as a crucial factor to put the project in the feasibility side, could be invaluable.

Which mining jurisdictions do you feel are providing the strongest advantage for junior mining companies right now?

I like stable jurisdictions like the USA or Canada, my gold positions for example are there but I think more work on the permitting front should be improved.

I like what Ecuador is doing now, when you listen to a president (Lasso) talking about mineral resources development plans for the long term? They want to be a main exporter of commodities, like Chile or Peru.

I like Chile too, but this situation about the mining tax program proposal should be solved ASAP. In the same line, Peru, I think we’ll be good, we need to work more on the ESG front and establish long term plans to develop greenfield projects, but without a social view, it will be difficult. I like these countries but for sure stability is needed.

With copper’s coming supercycle, should the industry be concerned about supply/demand dynamics?

No, we are in a middle of a stock/global consumption rate amber alerts, but this is driven as a consequence of lower production rates from previous periods, I think big players will join the party during 2021 and 2022 and the price will correct – I expect a pullback in base metals in the next quarters, I expect a support range of $3.5 – $4.0/lb in the long term as new consensus. However, if we consider the current stress scenario in LATAM I’d say that if in the short term the situation in Peru and Chile is not solved, copper prices can expect a lot of volatility without precedents.

How might this tailwind play out in the short/long-term?

In my experience this situation is split in 2 channels, short term, where operations are printing cash at these prices, and operations in the early stage can be more flexible to run high grading programs, at the end the ones sitted in the first quartile of the cost curve like Southern are having a good year.

In the long term, the increase in copper price assumption has a direct impact in the cutoff calculation, this item is used to define the mineral reserves or in practical terms, the profitable ore, the lower cutoff, the higher reserves inventory you have (if the modifying factors allows this upgrade), so, if you present an annual information format (AIF) with additional reserves, it’s very probable you submit in parallel an update technical report (e.g NI 43 101) and therefore your valuation will be different, you expect to see an extension of the life of mine, more metal production, potential upsides, etc.

So it sounds like a positive environment for junior copper mining companies exploring over the next decade?

Absolutely, let’s take the long term explanation bove, marginal projects at $3/lb can be considered now in the development pipeline at these prices, which will depend on metrics but yes, upside is at hand.

Which companies/metals are on your watchlist or your prime investment candidates?

I like asymmetrical investments, and I think junior companies can provide that. Right now, a junior copper company is my favorite one. I like the “cost opportunistic” view, so if one thing is good, why gamble on things you don’t know? I think speculation is part of the markets but in my portfolio or watchlist, at least I consider companies where I can understand what they are doing, but if I can calculate the NAV under my method, that is a place where I will wait patiently.

The Mining Stocks Lennin Muñoz is Watching