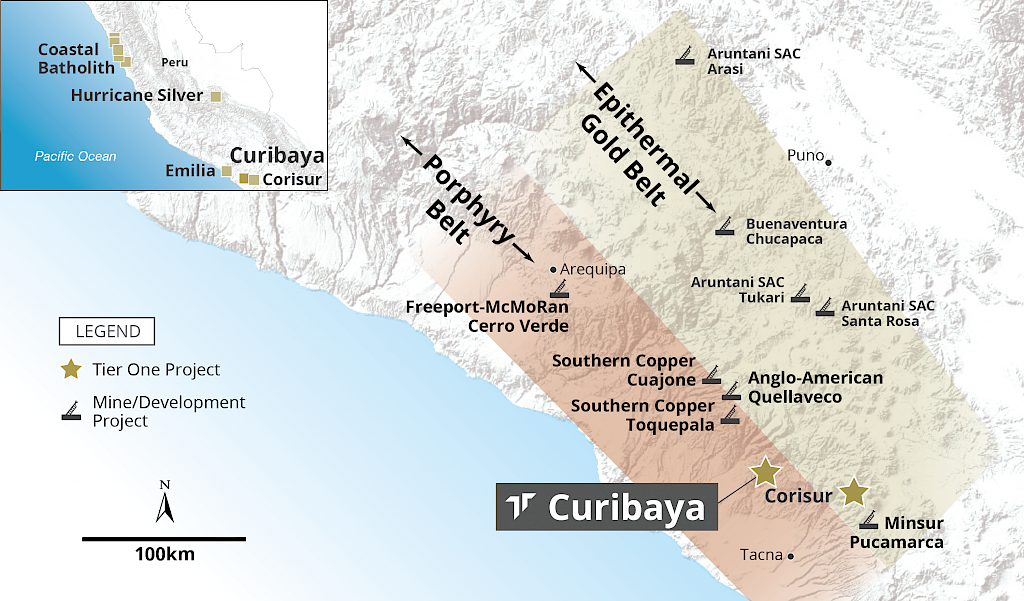

Tier One Silver (TSXV:TSLV) has made major strides in its Curibaya silver-gold mining project in Southwestern Peru by expanding its property from 11,000 hectares to 16,800 hectares. This land extension came after weeks of mapping and sampling since it covers the post mineralization volcanic cover.

The company hopes to further increase the scope of its ground-based induced polarization (IP) geophysical survey so that it can map the whole mineralized area in the Curibaya mining region. According to Founder Ivan Bebek, it may be one of the more profitable enterprises for the company,

CEO Peter Dembicki commented:

“We are excited by what we’re seeing so far with our ongoing drill program at Curibaya and are pleased to expand our land position prior to receiving our first results. Ongoing surface sampling has continued to extend the alteration and mineralization footprints, and therefore, we are expanding our IP survey as well. We look forward to a very busy second half of 2021 with results from drilling and surface sampling.”

Management Shakeup for a Strong Path Forward

This expansion at Curibaya comes at a time of change in the company’s development as it has recently appointed a new President/CEO, Director, and Vice-President of Communications. Collective was spun out from Auryn Metals, and these changes bring financial expertise and signal confidence in future profits and dividends for shareholders. According to Bebek, this can be achieved with this new team and the budding flagship project in the Curibaya region.

Christy Strasesh was recently appointed by the company board of directors and brings a wealth of experience to the company’s financial strategy and management. She has over 15 years of experience with capital markets and with a CFA designation, has ample history with investment management.

Natasha Frakes was recently appointed VP of Communications, having worked with Tier One Silver’s founders Ivan Bebek and Shawn Wallace since she joined Torq Resources in 2018 as their Manager of Investor Relations. With a background in journalism, she has worked for CBC Vancouver and CBC Calgary and thus has a fundamental and comprehensive understanding of media. She has previously done communication work for three different companies in the mining industry; Fury Gold Mines, Tier One Silver, and Sombrero Resources.

Tier One’s (TSXV:TSLV) new President and CEO, Peter Dembicki, has ample experience with capital markets and investment strategies. He has managed many corporate finance projects and has an extensive network of high net worth venture capitalists and corporations. Being a member of Canaccord, a multi billion-dollar investment company, he oversaw many lucrative deals and will be a valuable asset to the financial health of Tier One at large.

This is likely the biggest change for the company, and likely point to a more fiscally strong future for the company and more profitable dividends for shareholders. Since joining the team, Dembicki commented

“I am thrilled to be joining the Tier One team. The track record of success of management, the caliber of the technical team and the quality of assets led to my decision to join the Company. I am looking forward to the numerous catalysts ahead, including exploration at Curibaya, growing the project portfolio, and pursuing world-class discoveries, with a primary focus on silver, as we enter the precious metals bull market.”

The company began trading on the TSX Venture Exchange on June 9, 2021, under the ticker TSLV on the TSX Venture Exhange and TSLVF on the OTC Markets. The company’s exploration plans and its strong ties with local communities, and commitment to environmental, social, and governance (ESG) principles are what has made it so attractive for investors thus far. The company has also applied for listing on the OTCQB, to expand options for US investors and broaden the investor base.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

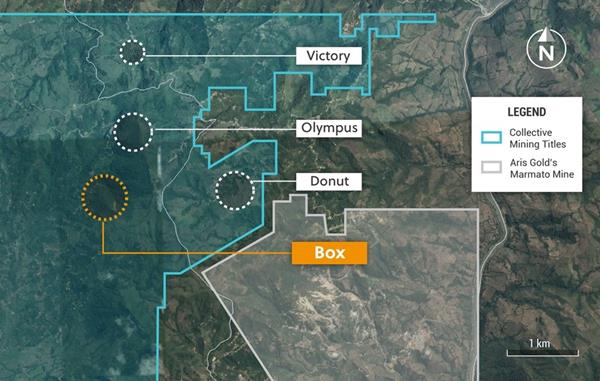

Earlier today Collective Mining Ltd. (TSXV:CNL) announced results for its exploration campaign. The Guayabales project is on the border with Aris Gold’s Marmato gold mine, another profitable mining area with 2.0 million ounces of gold and 4.35 ounces of silver. According to the newest reports, the metal mineralization in the Guayabales mining site includes gold-copper-molybdenum porphyries and high grade precious and base metal vein systems.

Ari Sussman, the company’s CEO, commented on the recent results:

“The Box discovery demonstrates the excellent potential of the Guayabales project which now hosts at least three mineralized porphyry bodies, gold bearing breccia and multiple zones of high grade, gold and silver veins. Our exploration continues to discover new mineralized zones and our reconnaissance work to date has only covered about fifty-percent of the concession. The future looks bright for Collective and we are planning a lot of target drill testing in the near future”

Highlights (Table 1 and Figures 1-4)

The Company’s initial channel and rock sampling at the recently discovered target area called the Box within the Guayabales Project returned promising gold and silver assay results from both vein and porphyry mineralized systems. Surface mapping has demonstrated the presence of two mineralized systems along a stream traverse over a 600 metre horizontal distance. The northern portion of the Box target (“Box North”) hosts porphyry mineralization with a vein overprint and the southern portion of the Box target (“Box South”) contains vein mineralization and occurs 300 metres higher in elevation than Box North. The following results are highlighted:

- Box South is a gossan of weathered sulphides and quartz veining located in a quartz diorite dyke at the faulted contact with carbonaceous schists. The fault zone can be traced for several kilometres and is an important structure for porphyry and vein emplacement. Exposure is related to a landslide surface and outcrop is limited to an area measuring approximately 35 metres X 50 metres. Gold and Silver mineralization is associated with anomalous lead and antimony in the sericite and chlorite altered porphyry and is related to extensive pyrite and quartz veining. Channel sampling returned the following intercepts:

Table 1: Channel Sampling Results*

| Channel | Interval (m) | Au g/t | Ag g/t |

| CH_1 | 19 | 0.9 | 75.8 |

| CH_2 | 28 | 1.5 | 61.0 |

| CH_3 | 20 | 2.4 | 100.9 |

| CH_4 | 10 | 2.6 | 79.2 |

| CH_5 | 8 | 3.0 | 142.7 |

*The Company’s channel sampling program consists of continuous two metre samples taken along the exposed rock at surface.

- The Box North target is hosted within diorite and quart diorite intrusive. Mineralization relates to sheeted quartz and sulphide veinlets hosting pyrite, chalcopyrite and occasional molybdenum in association with disseminated sulphides. There is also a higher grade vein polymetallic vein overprint. The intrusive bodies display secondary biotite, magnetite and sericite which are typical porphyry alteration assemblages. Exposure is limited to outcrops in streams, nevertheless rock samples returned seven values above 1 g/t gold (gold values of 14.8 g/t, 9.6 g/t, 5.1 g/t, 5.0 g/t, 2.3 g/t, 2.2 g/t and 1.6 g/t) and fifty per cent of the samples are anomalous in gold. All of these samples locate within an anomalous Au, Mo and Ag soil area covering a 400m diameter. Silver and base metal results for the rock samples are still pending.

- The Box target highlights both porphyry and vein style mineralization and a vertical zonation in alteration assemblages from Box South to Box North over an elevation difference of 300 metres. Further follow up work is in progress involving detailed soil and rock sampling. An induced polarization (“IP”) survey is planned to cover this area and other zones with porphyry potential in the near future.

Figure 1: Plan View of the Guayabales Project and the Box Target

https://www.globenewswire.com/NewsRoom/AttachmentNg/2e97e599-4e55-4a23-a3c5-55c9e65f5871

Figure 2: Plan View of the Box Target Highlighting North and South Targets

https://www.globenewswire.com/NewsRoom/AttachmentNg/2a84a9e2-237c-41a4-9bc3-6b1a9e93132f

Figure 3: Plan View of the Box South Channel Sampling Results Illustrating all 2 Metre Sample Interval Values

https://www.globenewswire.com/NewsRoom/AttachmentNg/458f1ffe-e5b9-4b0c-b146-71565e62ed58

Figure 4: Box North Porphyry Style Mineralization in Stream Outcrop Illustrating Porphyry Alteration, Silicification, Quartz Veining and Pyrite-Chalcopyrite Veins

https://www.globenewswire.com/NewsRoom/AttachmentNg/25af5748-902a-4836-9cb6-2a383cd84b96

Source: Collective Mining

The Guayabales project has been underway for some time now and is one of the hottest new mining projects in gold deposit-rich Colombia. The company is composed of many executives who previously played a role in the massive Continental Gold company, which led to a discovery and a billion-dollar sale.

The excitement about the Guayabales project is largely centered around its close proximity to the Aris Gold Marmato mine which is known for wide porphyry mineralization and narrow veins in its lower mine. The results that came out today seem to indicate that the Guayabales could hit similar returns for the project.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The African continent is known for its wealth of different minerals, mostly its abundance of oil, gold and diamonds. However, Africa is one of the world’s most important sources of copper and has some of the most impressive copper belts. In fact, Africa is among the top 10 copper producing regions in the world. Copper production is dominated mainly by Zambia, South Africa and the Katanga province in the southern Democratic Republic of Congo. Many other African nations contribute to total copper production.

The price of copper, and other commodities, has reached a record high in recent years and months. Not surprisingly, thieves have turned their criminal efforts to the theft of copper-laden trucks and copper in general. Thieves have even been involved in the malfunctioning of the state-owned railroads in Africa, stealing copper cables from the railway network to sell the valuable metal.

Copper trucks and the electrical installation of trains in Africa have not been the only companies affected by copper theft. There have also been a number of utility outages due to copper cable theft in previous years. Although copper is a common theft, vandalism of other metals such as aluminum conductors installed on transmission lines and steel from support towers has been reported over the past few years.

Glencore, one of the world’s largest copper producers, owns two large-scale copper and cobalt mines in the country: Katanga and Mutanda, which produce copper cathodes and cobalt hydroxide.

Between January and May of this year, at least 66 copper trucks belonging to merchant miners, including Glencore, Trafigura and Traxys, have been shrewdly robbed. The robberies were carried out while the trucks, loaded with copper, were on their way to different ports.

According to sources who declined to be identified because of the sensitivity of the problem, kidnappings have increased in recent months in Botswana, The Democratic Republic of Congo, South Africa, Tanzania and Zambia due to rising copper prices. At least 60% of the kidnappings have occurred in South Africa.

The Democratic Republic of Congo is Africa’s leading copper producer and the fourth largest copper producer globally. In 2019, the DRC’s copper mine production amounted to 1.3 million metric tons. Zambia, meanwhile, is Africa’s second largest copper producer and accounts for 70% of the continent’s total copper production.

Copper mined in Zambia and Congo accounts for about 10% of global supplies, estimated at 24 million tons, and is transported to ports in southern Africa. Occasionally, trucks loaded with copper en route to their destination are intercepted and robbed by organized crime gangs to re-sell the copper locally or transport it for sale in neighbouring countries.

In order to re-sell the stolen copper, the criminals melt the copper to remove the serial numbers and ownership marks. Eventually the stolen goods arrive in China or other countries where the high demand for copper has reached an all-time high of over $10,700 per ton in May. As manufacturing activity accelerated and economies opened up after COVID-19, global demand picked up, helping to drive copper prices higher by the ton.

As noted by Reuters, with an average truck carrying between 32 and 34 tons of copper cathodes, the thefts would amount to approximately $21 million worth of copper at current prices. It also added that in June and July, more trucks have been stolen. The source did not provide exact figures for the thefts in those months, however, one truck that was robbed on July 9 was reported to be worth $470,000.

Currently around $9,700, copper prices and metals used mostly in the energy and construction industries have risen more than 50% in the last 12 months.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Rio Tinto (NYSE:RIO) announced record earnings and dividends today as commodity prices continue to surge as the global economy starts to reopen. The company paid out over $9.1 billion in dividends to shareholders. The company’s stock also showed massive signs of growth, rising by 3% in the same day and moved up to a $138 billion market capitalization.

The rise in profits for the Anglo-Australian iron-ore mining company has been spurred on by rising demand for raw materials over the past year. According to recent reports, the average iron ore price rose to nearly $168.40 per dry metric ton, a near doubling from the raw price in 2020. This massive growth in price helped the miner’s yearly earnings increase from $4.75 billion in 2020 to nearly $12.17 billion in 2021, which was much higher than any analyst predicted.

Success Amid Disruption

Rio Tinto specializes in iron ore production, the key raw material necessary for the production of steel. The demand has been particularly from high China, who is one of the largest iron ore consumers on the planet. This is only projected to increase as China pushes for massive infrastructure development projects and as Brazil continues to struggle with supply problems, driving the price of steel through the roof.

The results on Wednesday also came during a transitional period for the company, after its former chief executive Jean Sebastian Jacques controversially stepped down last year. Since the new Chief Executive Officer Jakob Stausholm took over, the surge in prices have boded well for Rio Tinto’s future even as it struggled with some internal production issues.

Many of these production issues are similar to the ones many other manufacturers have dealt with during the COVID-19 pandemic. Due to restrictions on non-essential labour in numerous countries, the company has often found it difficult to get their workforce on site, which led to massive issues in its copper development project in Mongolia and its iron ore mining production in Western Australia.

Rio Tinto’s CEO recently stated: “In the first half we experienced too much operational instability. We have to sharpen the consistency of our performance. While today’s results clearly demonstrate the underlying quality of our asset base, our operational performance clearly is not where it has been in the past or where we want it to be.”

Green Vision

The company aims to further use their profits not only to fill the pockets of shareholders, but to invest in production capabilities in newer green energy projects. Just this Tuesday, it announced a massive $2.4 billion spending initiative for a lithium mine in Serbia. Lithium is one of the primary materials used for rechargeable batteries and aims to diversify their product lines.

Jefferies analyst Christopher La Femina commented on the company’s plans, saying: “Rio appears to be shifting from austerity and capital returns to more of a focus on growth. While Rio had some operational issues in the period, the big picture here is that these are stellar financial results.”

With the promising dividends and growth in raw materials prices and their increased infrastructure investment, Rio Tinto’s massive profits could continue to grow for 2021.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Egypt is looking to unlock its vast untapped mineral potential, as the country currently only has one commercial gold mine in operation, Centamin’s (LON:CEY) (TSX:CEE) Sukari. Egypt holds a rich mining history that ultimately led to Pharaonic gold jewellery, and one of the biggest gold markets in the world. However, mining has languished in the country as legislative blocks have been in place for years.

The country opened up new tender rounds in a bid to bring in $1 billion of investment every year. While gold is the focus, copper also holds high potential, and would be a good catalyst for an economy that has been hit hard by COVID-19. Five firms signed gold exploration contracts in Egypt, one of them being Barrick Gold (TSX:ABX) (NYSE:GOLD).

Big Canadian Ambitions

The company signed four gold exploration deals in Egypt’s Eastern Desert, according to the ministry of petroleum and mineral resources. Barrick will explore in 19 new blocks in the Eastern Desert after it won the international tender launched last year. While far short of the $1 billion target, initial exploration investment will total $8.8 million.

This is the first time Barrick will operate in Egypt, in a bid to tap under-explore and undeveloped reserves that have largely sat dormant.

Untapped and Under-Developed

A long period of dormant mining activity was primarily due to Egypt’s past system of royalties and profit-sharing agreements. By increasing rates on miners, companies found it difficult and unprofitable to explore for and mine minerals in the country. In 2020, the country finally streamlined regulations and made it easier for mining companies to form joint ventures with the Egyptian government. To increase investment and interest in the country as a mining jurisdiction, the state also limited royalties to a maximum of 20%.

While still high among many other industry standards, this improved outlook for the mining industry in the country has Barrick exploring in a region that is largely untapped.

A Line Forms to Get in the Door

Other companies that won concessions include B2Gold, Centamin, AKH Gold, Lotus Gold, and Red Sea Resources, and Aton Resources. Another Canadian company, Aton Resources (TSXV:AAN) secured a license in early 2020 and launched its exploration drilling and development program shortly after.

The company aims to build Egypt’s second operating gold mine on the 600 square-kilometre Abu Marawat concession, located 200 km north of Centamin’s Sukari gold mine. The site has inferred resources of 2.9 million tonnes grading 1.75 grams gold per tonne, 29.3 grams silver per tonnes, 0.77% copper, and 1.15% zinc.

While a small start, the first companies entering Egypt’s mining industry now are some of the biggest players from around the world. Canada is well-represented in the group, as Barrick and Aton begin their activities with ambitions to bring projects on line and into production as quickly as possible.

Egypt’s New, Better, Mining Framework

The new framework for the sector with the elimination of a requirement to form joint ventures and the capping of state royalties at 20% is a welcome change for miners who aim to explore and mine in the country. One major barrier that remains is the tendering process itself.

Sami El Raghy, Chairman of Australia-based Nordana Pty Ltd. said, “No other successful mining countries use this process. They all have a clear transparent mining laws stipulating the qualification, obligations and the right of investors. (They) work on the principle first come, first served.”

The $1 billion investment target is a big one, and the millions being poured into Egypt’s mining and energy industries now are a drop in the bucket. However, the government has set a target date of 2030 for this goal for this key geographical and trading partner that links Africa with the Middle East. To meet it, more open laws and structures may be necessary before the country begins to see the kind of investments that could feasibly get it to its target by 2030.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

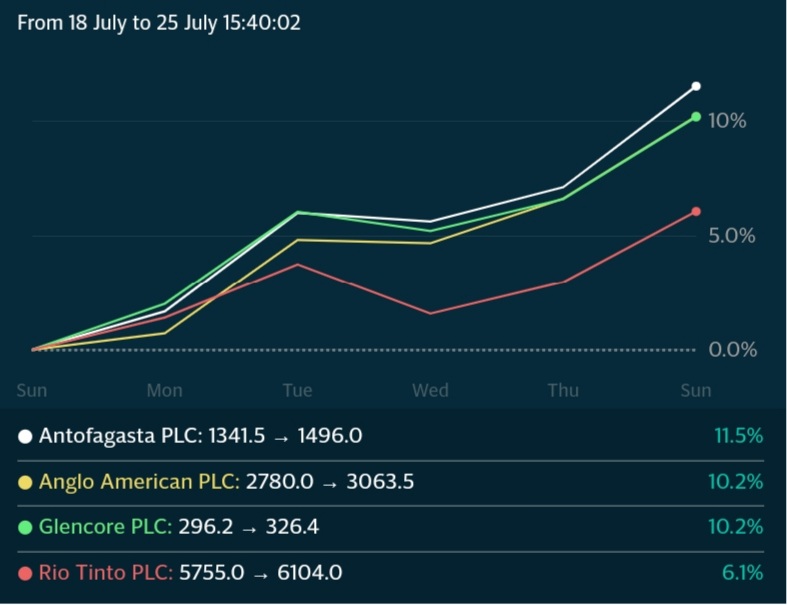

This is set to be a big week for mining earnings, as some of the world’s biggest mining companies will begin to show the market exactly how much this commodity boom is helping. This week will see the top five western diversified mining companies report earnings, and investors should be watching for record profits that could drive dividend payouts to match.

Analysts estimates show that the top five miners may have raked in a combined $85 billion in the first half of 2021, double the number from 2020. Of course, lockdowns and supply chain meltdowns had serious effects on earnings last year. As processes slowed to a halt and demand dropped off a cliff, mining companies mainly were sitting on their hands like the rest of the economy.

However, the latter part of 2020 saw engines start up and restrictions lifted in many mining-friendly jurisdictions, and 2021 has accelerated the commodity price gains from last year.

The first to report on Wednesday will be Rio Tinto Group and is expected to announce $22 billion in profits for the first half of the year, equalling the same amount as its total profits in 2020.

Other companies such as Glencore, Anglo American, and Vale SA were also expected to post massive profits for the first six months of 2021, and possibly their highest-ever numbers for the six months to June period, according to estimates from analysts compiled by Bloomberg.

The sector has seen a revival of its activities faster than most other sectors of the economy as the industry has been one of the primary beneficiaries of the recovery stimulus injected into the global economy. With trillions of dollars in recovery packages going out, demand for commodities has bounced off 2020 lows to skyrockets higher every single month. Demand for commodities like iron ore, aluminum, steel, and copper are driving prices higher every week while inflation pressures continue to spread through the economy.

This bull run for commodities has been a huge gift for mining companies who have the tailwind of demand and higher prices for their production to account for big profits.

Ben Davis, an analyst at Liberum Capital, said, “This should be a pretty much stellar set of results all round. We’re expecting record dividends from BHP and Rio, while Anglo and Glencore also have the potential to surprise.”

Stocks have been on a tear lately, up double digits in some cases in a single week, so there may be room to move higher on earnings news. Freeport-McMoRan already hinted at its blockbuster results when it announced it had wiped out $5 billion in debt over the last 12 months, blasting past a target month ahead of the planned schedule.

A record dividend was also paid out by Anglo American Platinum Ltd. (79% owned by Anglo American) on Monday of $3.1 billion, equal to 100% of first-half headline earnings. In a significant understatement, CEO Natascha Voljoes said the company was in a “strong financial position” and that the company was able to deliver “industry-leading returns.”

Everyone is set to benefit from higher profits from miners this year, beyond stakeholders and investors in the companies themselves. Government should also see higher tax receipts from miners, who contribute significantly to the global economy and often up to a third of any given domestic economy in many regions like South and Central America, and Africa.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Aluminum may be a serious competitor if copper prices continue to rise at the current rate, with supply/demand dynamics changing the landscape for many miners and suppliers. Julian Kettle, Wood Mackenzie Senior Vice President, Vice-Chair Metals and Mining says, “Too many forecasts ignore the fact that aluminum is a serious competitor to copper in a number of high volume applications, including high and mid voltage power cable, busbars, transformer windings, and motor windings.”

These things will all form the backbone of a growing global decarbonization trend that is set to accelerate in the next decade and the following years. Copper prices seem to be the main competitive sticking point, with prices expected to rise to between $15,000-$20,000 a tonne. However attractive the deal might be, when it comes to government spending, price is less of an issue. With much of the demand for battery technology coming from infrastructure projects and electric vehicle manufacturers, copper is not under threat from aluminum any time soon.

The Market Continues to Vote

Some countries have attempted to slow copper price growth by releasing more product to the market. China’s attempt to slow copper prices ultimately failed because the growing trend is now bigger than just the copper market. The global economy will be driven by a new for the red metal no matter how much copper is available at any price.

Yesterday, copper prices rose yet again, as China announced it would release fewer reserve metals than expected. Copper for delivery in September rose to touch $9,554 per tonne midday Thursday on the Comex in New York. That single-day bump of 1.6% could be further confirmation that the next leg up in the price cycle has begun.

The world’s second-largest economy will sell another 30,000 tonnes of copper, 90,000 tonnes of aluminum, and 50,000 tonnes of zinc from its state reserves on July 29. However, the amounts were less than anticipated, and the market is reacting accordingly. Anna Stbalum, a commodities broker at Marex Spectron said, “It is slightly less than the market expected, but it should be priced in already as it’s pretty well flagged.”

The risks of more copper flooding the market are low, with a dearth of new copper projects looming as demand continues to rise. China is primarily a consumer of copper, and domestic production is quite low. While the temporary slowdown in price growth for copper may be attributed to some market moves from the Eastern power, it is a band-aid on a bullet wound that won’t stop bleeding.

Copper supply is too low for China to fill the gap. The global market showed a deficit of 75,000 tonnes in April, compared to a 13,000-tonne deficit in March, according to the International Copper Study Group in the most recent monthly bulletin. Globally, consumption hit 2.14 million tonnes, with output reaching 2.07 million tonnes. That gap is expected to keep growing.

The Only Viable Option

When it comes to wiring, base plates, and electrical conductivity in general, copper is the first choice by far. Copper cables and their superior conductivity properties cannot be ignored. Aluminum’s conductivity sits approximately 40% lower than copper, making it an alternative but not a very efficient one.

However, in an era where copper prices continue to gain steam in a price cycle that is showing no signs of slowing down, the question of whether aluminum might be a viable, cheaper alternative to copper is a serious one.

The leading argument suppliers might use when choosing aluminum over copper is that the density difference between the two and the cost gap is enough to overlook the lower efficiency. Aluminum cables are about 52% lighter than a copper cable equivalent due to a 30% lower density. The result might be a better property offering handling and installation benefits as it is simpler to transport and manipulate.

While copper prices may be a barrier in the future if companies and governments need lower-cost solutions, the density issue is not one they can likely accommodate. Battery density continues to rise, and higher voltage, faster-charging batteries are needed to continue to make EVs viable for mass consumption.

For the level of battery density required and the output demanded by consumers, copper is the only viable option. The speed and efficiency at which copper conductivity functions are irreplaceable as of right now, even if aluminum prices continue to follow their trend of rising slower than copper.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

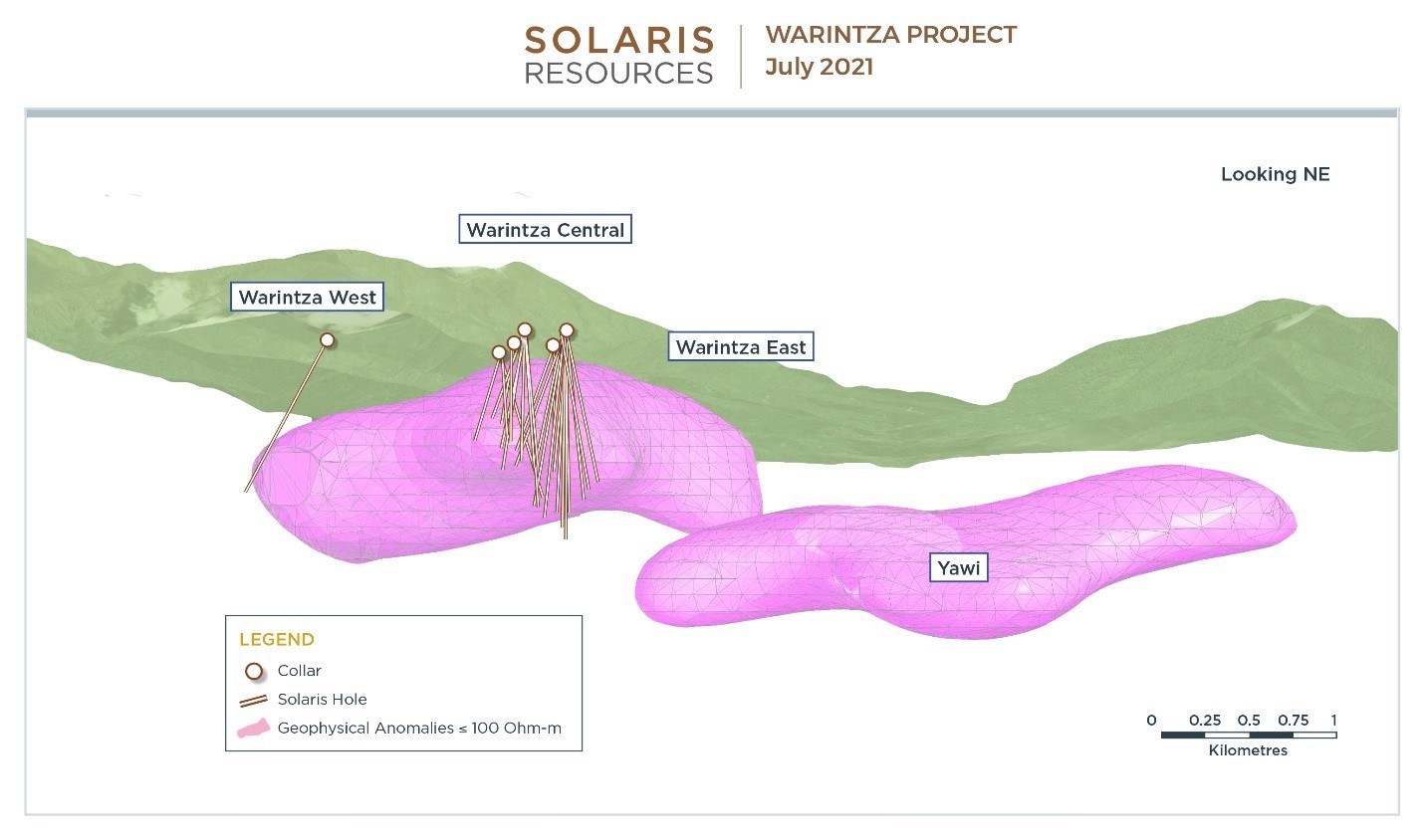

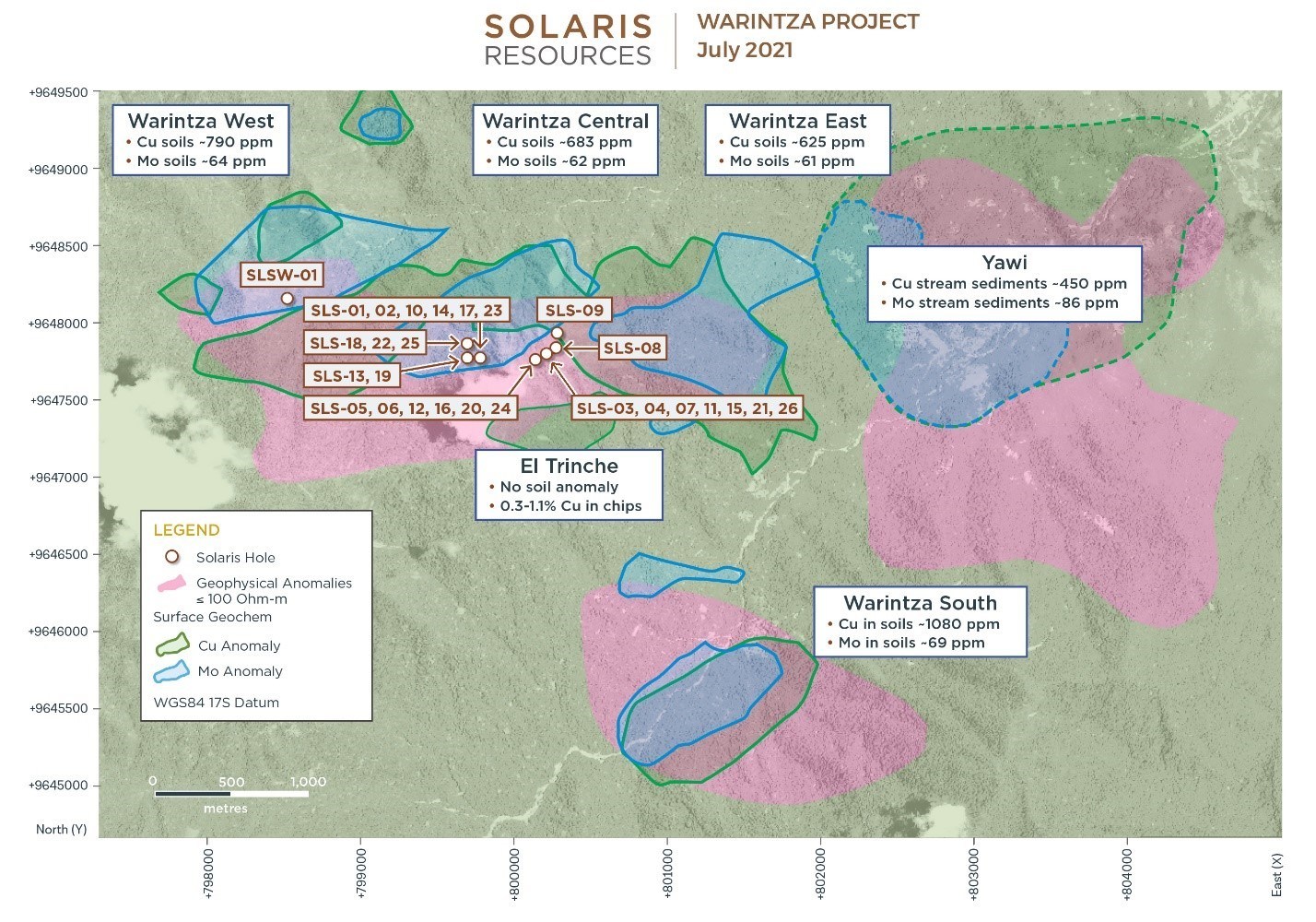

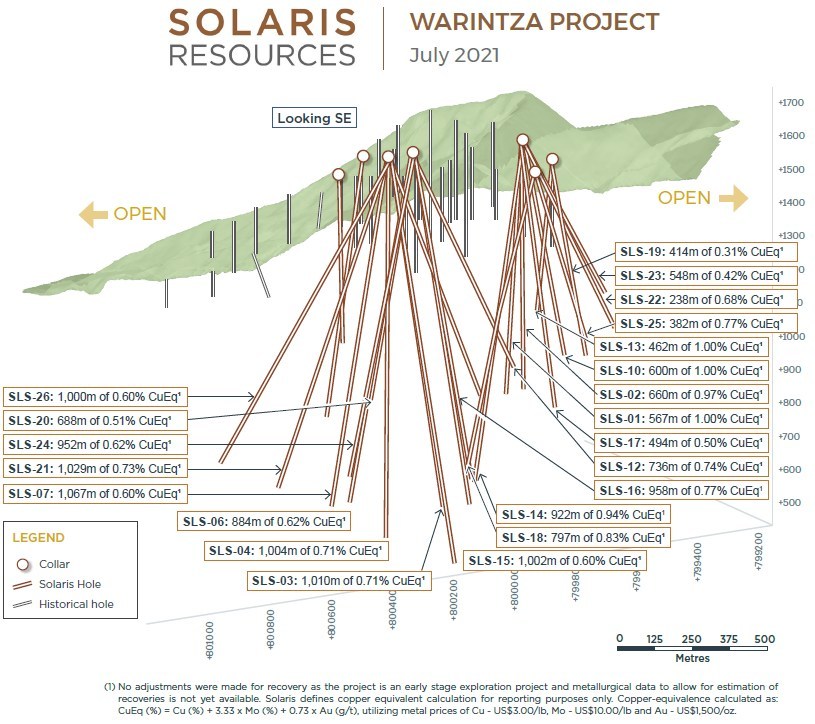

On Tuesday, Solaris Resources (TSX:SLS made significant gains in their Warintza drilling campaign in southeast Ecuador and announced a new discovery at Warintza East, located ~1km east from their Warintza Central deposit where resource expansion drilling is ongoing. Warintza East is part of a more extensive copper mining campaign in the Warintza area that spans over a 35 square kilometre region and comprises five main mining targets.

Solaris Resources has been a massive player in the South American copper drilling industry for some time now, with copper and gold projects in Ecuador, Chile, Peru, and Mexico. However, their recent work in the Cordillera del Condor Mountain region of Ecuador is one of their more exciting and promising projects to date. The area is known to be ripe with tens of millions of tonnes of contained copper and millions of ounces of gold and hosts nearby mines of Lundin Gold’s Fruta del Norte mine and a Chinese consortium’s Mirador mines.

We spoke with Daniel Earle, CEO of Solaris Resources, on the results at the Warintza project and took a look at some of the biggest reasons why this company is set for the next major leap.

So far, each stage of the drill program has continued to yield positive results with discoveries. Three discoveries have been made so far, with two more targets still left to drill. Mr. Earle said, “We drilled a hole at what we call Warintza West in February, which resulted in a discovery there, and then just yesterday we drilled a hole at Warintza East, which resulted in a new discovery there. So now three discoveries within this cluster of copper deposit targets, and that leaves two more major targets to drill in the future.”

“All of our drill holes, and all of the historical drill holes, have all hit economic copper mineralization, so there is nothing drilled on this property that hasn’t resulted in economic copper.”

With Warintza South and Yawi next up on the list of discovery drilling as well as expanding Warintza Central and East, more results seem likely to continue the trend of fruitful discoveries as every single target has been a success so far.

Cash balances will allow for a very long runway for the company, with about $60 million on the balance sheet right now and approximately $20 million needed for the remaining 2021 capex: “We will be testing Warintza South and Yawi targets before the end of the year. And all of that will be covered by the $20 million budget.”

That will leave a sizable remainder for the company as it looks toward its next possible major milestone, a sale.

“By the time the calendar rolls over to 2022, we are going to be looking at a process to sell this entire company. We will still be in a very strong cash position.”

With the stock breaking above $13 recently and showing no signs of abating, the company is still not at a valuation that might match the scale of the current drilling at the Warintza Central deposit and existing and potential discoveries at the other regions.

The Company is undergoing a resource expansion drill campaign at Warintza Central which hosts a historical inferred resource of 124 million tonnes grading 0.7% copper equivalent, based on very limited, shallow historical drilling. An updated resource estimate is expected in Q4 2021 and drilling has already demonstrated that the new resource will be an order of magnitude larger. The company’s target at Warintza Central alone is to define a copper resource of 1 billion tonnes, which could ultimately see Solaris Resources triple its current valuation, not inclusive of any additional discoveries made on the property.

Mr. Earle pointed out that the Augusta Group track record bears out a pattern that may serve as a useful model for its exit strategy: “Our last company within the Augusta Group, we sold for $2.1 billion in 2018, that was at a multiple of essentially 100 percent of the net asset value of the primary assets. In Solaris today, we are trading at approximately one-third of that level.”

“So we have a lot of work to do to extract a representative evaluation here at Solaris.”

Pushing that valuation is another tailwind the market is providing: “This copper price cycle is going to be much more powerful because of greater fiscal and monetary stimulus, and number two, we have these megatrends in place of decarbonization and electrification.”

“Electrification of the residential sector, of the industrial sector, smart grids, grid storage, all these other kinds of areas of growth that are all incredibly copper intensive.”

That need is bigger than ever, possibly pointing to something bigger than just the effects of a price cycle. While copper price behaviour has matched expectations, the effect is also being multiplied by current conditions and the grand expectations of an electric future beyond anything anyone has ever seen before.

In understanding the scale and importance of Warintza, Daniel Earle notes that it is important to consider the context within which it resides and possible comparables for the project and company, “I think the key is just to understand the context around what we have here and what we are going to achieve, and to look at the global comparables for an asset like this.”

“You have to look at some of the best copper development assets in the world if you want to understand the context of what we are trying to do.”

A key copper project in Peru – Anglo American’s (LN:AAL) Quellaveco, may be a potential future comparable once the resource estimate is released. While that mine has a long proven track record, Warintza may be the project to match or surpass it. Solaris holds some other key advantages with its project that may allow the company to get a higher return out of its exploration efforts.

“We’re going to do it at much lower elevation, adjacent to a highway, adjacent to a power grid that is supplied by low cost, emission-free, renewable power, with abundant freshwater, with a low-cost and skilled labor force in Ecuador.”

“You realize that this is something totally unique.”

First Results Are In

Highlights are listed below, with corresponding images in Figures 1 and 2 and detailed results in Tables 1-2. A dynamic 3D model is available on the Company’s website.

Highlights

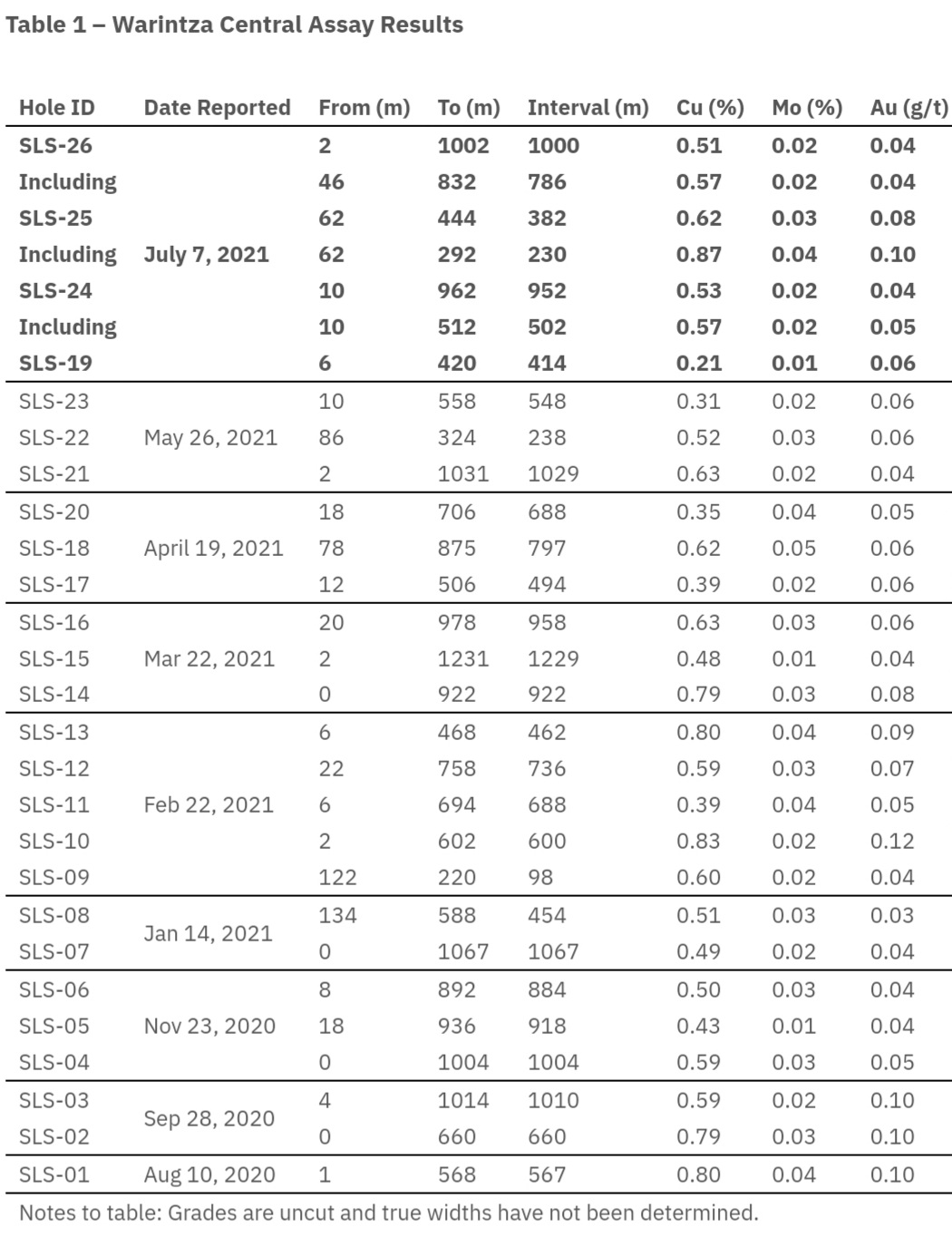

- SLSE-01 was the first hole ever drilled at Warintza East and collared approximately 1,300m east of Warintza Central, where recent eastern extension drilling intersected 1,000m of 0.60% CuEq¹ from surface (see press release dated July 7, 2021), with the Central zone still open in this direction

- SLSE-01 was drilled to a total depth of 1,213m with assays reported herein for the first 320m of core from surface, which were given priority in transport, cutting, preparation and assaying – results for the balance of the hole are expected in late August/early September

- SLSE-01 returned 320m of 0.46% CuEq¹ from surface, including 54m of 0.70% CuEq¹, in an open interval, marking a significant new discovery from surface at Warintza East, one of the five main targets within the 7km x 5km cluster of porphyry targets defined on the property

- Warintza East is defined by coincident overlapping copper and molybdenum soil anomalies, measuring approximately 1,200m in strike, and a high-conductivity geophysical anomaly that extends from the target through Warintza Central (refer to Figure 1)

- Further drilling will target the expansion of Warintza East, with a focus on the open area between Warintza Central and this new discovery (refer to Figure 2)

Table 1 – Warintza East Partial Results

| Hole ID | Date Reported | From (m) | To (m) | Interval (m) | Cu (%) | Mo (%) | Au (g/t) | CuEq¹ (%) |

| SLSE-01 | July 20, 2021 | 0 | 320 | 320 | 0.36 | 0.02 | 0.05 | 0.46 |

| Including | 0 | 54 | 54 | 0.49 | 0.01 | 0.05 | 0.56 | |

| Including | 162 | 216 | 54 | 0.60 | 0.02 | 0.04 | 0.70 | |

| Notes to table: True widths cannot be determined at this time. | ||||||||

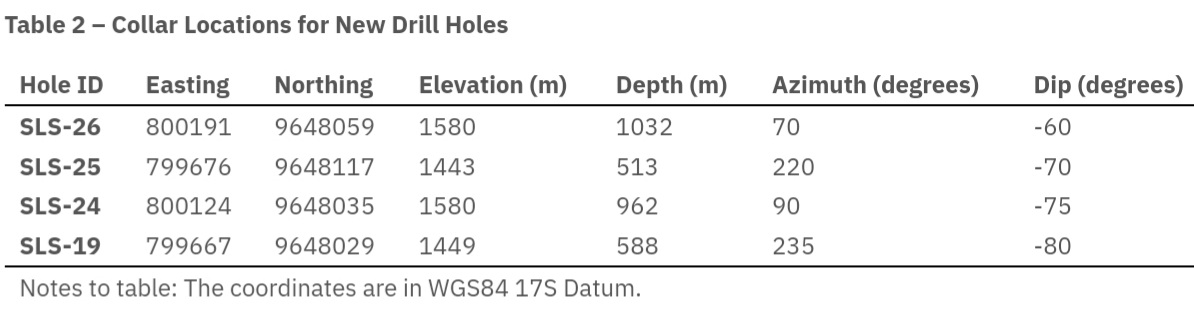

Table 2 – Collar Location

| Hole ID | Easting | Northing | Elevation (m) | Depth (m) | Azimuth (degrees) | Dip (degrees) |

| SLSE-01 | 801485 | 9648192 | 1170 | 1212 | 260 |

Source: Solaris Resources

Figure 1

Figure 2

Source: Solaris Resources

Future Plans

In the upcoming weeks, the company plans to continue resource expansion drilling at Warintza Central, with the updated resource estimate expected in Q4 2021, as well as continue discovery drilling at Warintza West and East and undrilled targets at Warintza South and Yawi. Solaris’ VP Exploration commented on the drilling campaign, “The discovery at Warintza East marks the third major copper discovery within the voluminous 7km x 5km Warintza porphyry cluster. Importantly,the footprint of Warintza East overlaps conceptual pit designs for Warintza Central, which itself continues to grow eastward with recent results. Future drilling will focus on the open, undrilled area between these two zones.”

Copper prices have been on a rapid rise and have even recently hit all-time highs. With global demand for copper predicted to only rise further, the Warintza project’s expected ROI seems to have one direction – higher.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Recent channel sampling results announced by Collective Mining (TSXV:CNL) from its Guayabales Project in Colombia gave the company a promising confirmation of the work they are doing at the site. Located in a deposit-rich area, the project is situated contiguous, immediately along strike, and to the northwest of Aris Gold’s Marmato gold mine, which contains proven and probable reserves of 2.0 million ounces gold and 4.35 million ounces silver.

Collective Mining holds the option to earn up to a 100% interest in the Guayabales project, making it a critical site for the company. If the results bear out what initial exploration efforts have hinted at, then this could be a fantastic investment opportunity for a buyout or developer looking for their next site.

Much of the excitement around Guayabales also comes from its proximity to the Marmato mine from Aris Gold. The mine is located in the Marmato gold district in the Caldas department, a mountainous region approximately 80 kilometres south of Medellin, Colombia. The mine has excellent infrastructure, is located near the Pan American Highway, and has access to the national electricity grid running near the property.

For Collective Mining, the Marmato mine is a strong hint at what may be possible at Guayabales. The mineralization in the Lower Mine at Marmato includes wide porphyry mineralization, and the mineralizations in the Upper Mine is characterized by narrow veins where an existing operation mines material using conventional cut-and-fill stope methods.

The potential for Guayabales to return results similar to or even better than the Marmato mine is not lost on the company or investors. As results continue to come in from drilling, Collective Mining (TSXV:CNL)will be looking to realize the many promises of the district, which has been mined since pre-Colonial times by the Quimbaya people.

On June 21, Collective Mining released results from its project from geological mapping, soil and rock sampling programs, and the completion of a high-resolution, airborne geophysical survey. The interpretation of that data points in the direction of a series of copper-gold-molybdenum porphyry intrusions, as indicated by the previous metal mineralization encountered throughout the property.

While current surface exploration activity has covered only less than 20% of the project area, four initial targets have been identified. These targets lie along a NW-trending and mineralized structural corridor that incorporate both porphyry-style copper-gold-molybdenum mineralization and associated high-grade gold-silver (base metal) vein systems.

Lying immediately along strike and at a higher elevation to Marmato, the Guayabales project has the potential to be the next significant discovery in the region. If the company finds what the latest results seem to hint at, then the drill program could bring Collective Mining (TSXV:CNL) much closer to a sale or deal with an established producer for a profitable deal.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Investors are only starting to fully grasp the implications of the copper boom we are in right now. As they continue to snap up copper mining stocks as fast as possible, there is always a temptation to pick up the most prominent names first. After all, those names often produce the most, invest the most, and generate solid returns for investors. However, most of the growth plays still seem to be in the companies that fly under the radar for the time being.

A Producer and Explorer

One of the companies investors might be turning their attention to soon is Three Valley Copper (TSXV:TVC). The Canadian copper mining company’s project is located in the prolific Cretaceous belt of Chile that hosts a large number of rich deposits. The company produces Electrolytic Copper Cathodes (Grade A) of 99.999% purity. That copper is often used in electric equipment like technology, battery parts, and the copper can easily be drawn and formed into wires.

With the current focus on global decarbonization efforts, this particular type of copper is seeing massive demand growth. Electrolytic copper undergoes refining or purification through the process of electrolysis. That purification is by far the simplest method of achieving purity levels 99.999% in copper and makes Three Valley Copper’s (TSXV:TVC) product particularly valuable in a world that is rapidly going electric.

Two-Pronged Approach

The company has two main deposits: Papomono Masivo and Don Gabriel. The company’s strategy is to produce ECC, while simultaneously exploring its property to increase the visibility of the mine and extend the life of the mine. Both deposits are located in a 10 kilometre wide corridor of middle to upper Cretaceous volcanic rocks. This property is bounded by north-south-trending faults and stands as examples of stratabound, manto-type copper deposits.

To focus efforts and ensure the maximization of the property, the company has divided each deposit into some main areas. The Papomono deposit has seven:

- Papomono Masivo

- Papomono Norte

- Manto Norte

- Papomono Sur

- Papomono Mantos Conexión

- Papomono Cumbre

- Epitermal

The Dan Gabriel deposit has two:

- Don Gabriel Manto

- Don Gabriel Vetas

Both deposits sit in one of the most copper-rich regions in the world, in Chile, the number one global copper producer and the number one country in copper reserves. While production has started and the company is operating at regular capacity as pandemic restrictions lift, less than 10% of the property has been explored. This gives Three Valley Copper plenty of room for expansion through exploration of a property that Vale once explored, expanded, and then sold. The mining giant invested $250 million in construction and infrastructure build-out before selling the deposits to a private family business.

A Rich Project History

Three Valley Copper (TSXV:TVC) purchased 70% of the property in October 2017 for $40 million and then increased its ownership to 90% in 2021. Currently, technical studies have been completed, with a technical report issued, and the company has set its sights on its more than 46,000+ hectares of land for the future.

Papomono

Three Valley Copper has begun the Papomono Masivo underground development with construction already underway. The company expects to complete the construction phase by the end of 2021, positioning itself for more expansion the following year.

Don Gabriel

Open-pit expansion is currently underway at the Don Gabriel deposit, with expectations of both deposits bringing the company to full utilization of the facilities by 2023. This strategy will allow Three Valley to increase revenues and drive down unit costs.

Three Valley Copper’s (TSXV:TVC) strategy of producing the purest copper on the market (Electrolytic Copper Cathodes) by mining its own deposits and purchasing third-party ore to fill in any supply gaps when needed is positioning the company as a premier destination for future tech and battery companies. With calls from the United States for a massive infrastructure plan and companies like Tesla begging for more nickel and copper for their production, mining companies like Three Valley are set for the next leg of copper price runs.

The added bonus of the company’s potential for further discoveries on its massive property means that Three Valley’s (TSXV:TVC) production and stock may be one of the best value propositions in the copper space. The sub-$1 price today seems to be highly attractive in a space where copper miners are seeing gains in the hundreds if not thousands of percentage points, and the price of copper is on a serious run.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Rio Tinto’s Richards Bay mineral sands mine has seen multiple violent incidents over the years. The South African Police Service has been involved in numerous incidents in which workers, families, and subcontractors have dealt with difficult circumstances.

After a senior manager at RBM was assassinated in late May, the company was forced to halt operations at the site. In late June, the company made the decision to keep the Richards Bay Minerals mining and smelting operations in South Africa’s KwaZulu-Natal province shuttered so that safety and security could be improved for workers.

A Cold-Blooded Assassination

The late May tipping point was the assassination of Nico Swart, RBM’s general manager of operational services. While driving to work on a Monday morning, more than 20 high-caliber bullets were fired into his vehicle. The incident is being investigated by the South African Police Service, who hope to find some answers for Swart’s family, friends, and coworkers. Multiple setbacks have hindered progress at the project, as in April, RBM officials said that they were talking with government authorities to “permanently address violent protests around its operations before resuming work on the Zulti South project.” However, things have not improved since, and the company is taking final steps.

On Monday, Rio Tinto announced that its operations at the Richards Bay Minerals (RBM) project in South Africa would remain shut despite further talks with the government. The murder of one of their top managers and the unsolved case has proven too difficult to overlook for all parties, it seems.

Regular Violence From Protestors

The project employs about 5,000 people and will be a hit to Rio Tinto’s bottom line as well as the good the project does for the local economy. The Minerals Council of South Africa condemned the violence and the “failures” of law enforcement up to this point. The government had tried to prevent the suspension of activity at the minerals sands project. It is an integral part of the local economy, and Rio Tinto represents a strong economic partner for the country.

However, the council said in a statement that, “Continued acts of lawlessness including blockages of roads, burning of equipment and intimidation of staff at mining operations are not only unacceptable and damaging to the country’s reputation as an investment destination, but also impact the lives and livelihoods of mining employees, their families, and surrounding communities.” The untenable situation is expected to calm down now that the project is halted.

Optimistic Tone, But a Long Uphill Battle

Rio Tinto also commented on Monday, stating that everyone is looking forward to the resumption of operations as soon as possible. The optimistic outlook from the company may suggest it intends to broker a deal with local communities or create a new project. “But the safety of our people and the security of our operations must be assured before we can return to work,” a spokesperson said.

The company owns a 75% interest in the mine, which has been plagued by violent incidents related to violent protests. In 2018, Rio Tinto had to freeze operations twice because of violent protests by contractors and then stopped work at the mine again in 2019 when one of its employees was shot. This latest event makes it unclear whether Richards Bay will ever be able to resume normal operations, which includes mining, refining, and smelting of heavy minerals or ore deposits. A joint venture Rio Tinto and Blue Horizon (owns 24%), the remaining shares are held in an employee trust.

RBM produces ilmenite, rutile, and zircon, some of which are highly valuable and used in things such as sunscreen, paint, and even smartphones.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

CEO of Solaris Resources (TSX:SLS) Daniel Earle recently sat down with Tom Bodrovics of Palisades Gold Radio to discuss everything from copper, work, and the mining industry. Daniel’s background is in mining engineering and has worked in banking, commodity forecasting, and financial analysis.

Daniel discusses his choice to invest his life savings in Solaris and become the CEO of a copper mining company, the reasons why copper is so critical, Ecuador as a mining jurisdiction, and the company’s ESG strategy in a changing world. The full interview can be found in the video above.

Copper is Key

With all the attention on rising copper prices and the push for decarbonization around the world with electric vehicles (EVs) and battery storage, Solaris is in the middle of a favourable copper cycle. Mr. Earle explains his decision to become the CEO of Solaris, and why the current copper price cycle is both impressive and completely normal: “We’re at a period in this copper price cycle where we’ve essentially completed the first leg of the cycle. Coming off the pandemic, or the cycle lows in March of last year, copper prices basically more than doubled and then corrected a little bit.”

“This is actually pretty normal for a copper price cycle. If you consider the perspective that’s provided by the prior two cycles, then you would have seen a similar thing with the copper price basically doubling in one year and then going on over the next couple years to double again.”

“So you get a quadrupling across on normal copper price cycles. You would have seen that in the mid-2000s cycle for example, copper went from about $1 at the start of the cycle, to a peak price of $4/pound in 2007 in less than three years.”

The Copper Supercycle

The current copper price cycle has been called a “supercycle”, with Goldman Sachs pegging its copper price target at $15,000. If the current price cycle continues in a similar fashion to those of the past two decades, the doubling and then quadrupling of the copper price could see the industry continue to heat up.

Earle noted: “I think it’s important to just keep in mind the kind of framework that this exists in. We spoke about copper and the industry dynamics of supply and demand, geopolitics, and so on, and how they would affect copper. But just bear in mind the bigger picture; people talk about a supercycle for commodities which, if you define that as just sort of above trend price growth for commodities as a whole then yes, I think you can make a case for that.”

When Do We Get to Peak Copper?

If there is a peak, we are likely not there just yet. “If you look at the existing supply profile, peak copper lands around the middle of this decade, maybe 2024 maybe 2025 if you look at existing production, planned production and then possible production.”

“Then from there, the production that’s committed starts to roll off and that’s when the gap really starts to open up to demand, growing through a steady pace through to the middle of the decade, and then accelerating from there when green demand really starts to take off exponentially,” Mr. Earle commented.

World War Copper?

Electric vehicles and battery storage are likely to be the two main drivers for copper demand over the coming years. Many countries have pledged that sales of new cars will only include electric vehicles by 2030, with others pledging a slower but committed transition away from combustion engine sales.

The evolving dynamics could eventually put copper in the middle of a geopolitical spotlight as it could be considered a critical or strategic metal. However, the market is not there yet but could translate to not just higher copper prices, but much higher multiples for equities measured against EBITDA.

“I think we wouldn’t say today that copper is considered a strategic metal. Certainly among investors, you haven’t seen a lot of rhetoric out of governments around copper supply. So that discussion is confined to some of these battery metals, and before the battery metals, the rare earth space is where you saw that kind of discussion. And then of course investors take that discussion and they apply it in the market.”

If the situation were to change and put copper at the forefront of national strategies for energy storage and infrastructure, that shift could play out in the market in a similar fashion to lithium companies: “You see it reflected in higher market multiples, so if you look at lithium companies, you have these companies that are trading at twenty to thirty times EBITDA. If you look at the copper companies without this kind of rhetoric, without this emphasis on the importance of these companies and the metal they’re supplying, you need copper companies to quadruple before they get to those kinds of multiples.”

“You’d be talking about Freeport trading at something like $160 a share, or $280 a share for Southern Copper, $120 First Quantum shares if you were to get the same kind of strategic consideration and appreciation by the market.”

“So we’re not there yet, but I think as this cycle evolves, as the supply deficit that we’re talking about actually materializes and then widens, and you get a really dramatic price response from the middle of this decade through the end of this decade, you get well into not just record price but multiples to prior record prices. Where we get to $6 and $8 copper prices. That’s when I think that you can expect that copper will begin to be considered a strategic metal, and that’ll have obviously really dramatic implications for the equities.”

“Dramatic Implications for the Equities”

What that means for Mr. Earle’s Solaris Resources is yet to be seen, but with the stock up over 1,100% since its IPO, it seems that the current copper price cycle could be supportive of a continued run higher. With the added possibility of copper being classified as a strategic metal for several governments, higher copper prices could translate to equities with multiples far higher than have been seen thus far.

“It’s obviously going to be uneven because you’ve got these different profiles of costs, different commodities. But certainly we’re going to have really rapid demand growth, where as we get to coordinated, synchronized global growth stimulated by all this incredible fiscal largess in an accommodative policy environment. And then we’ve got constrained supply so we have had tremendous under-investment in the mining sector over the last seven years or so,” Mr. Earle explained.

Under-Investment Could Accelerate Effects of Price Runs

That under investment has fueled a dearth of new copper projects that is amplifying the effects of the supply demand dynamics for copper. Pushing the timeline a few years ahead and this could play out on an exponential scale reflected in commodity prices and equities.

While the current climate has all the makings of a supercycle, not all commodities will react the same way, with some winners pulling ahead far faster than others. Most of the metals and minerals needed for the green transition like copper and lithium will be the fastest runners, with most other commodities being pulled up alongside them.

Earle went on: “So we would have gone from something like $200 billion a year of investment in the last cycle to a quarter of that coming towards the beginning of this cycle. So tremendous under-investment because of this investor push for the return of capital. Which is wonderful during the trough of the cycle to keep share prices strong, but it doesn’t make sense across the next cycle when you need to be bringing on supply.”

“Because this is a depleting business and you need to continually reinvest. I think when you look at that contrast between the demand that we’re going to have, and this inability of the supply side to respond, you see the makings of this supercycle here, uneven as it may be across different commodities.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Yesterday, Sudbury MP Paul Lefebvre and Nickel Belt MP Marc Serre announced that the Centre for Excellence in Mining Innovation (CEMI) will receive $40 million in funding from the Canadian Federal Government for the Mining Innovation Commercialization Accelerator (MICA) Network. The $112.4 million project is funded through public and private investments, to accelerate the development and commercialization of innovative technologies in the mining sector. Headquartered in Sudbury, MICA will operate with strong partnerships with the Bradshaw Research Initiative for Minerals and Mining, InnoTech Albert, Saskatchewan Polytechnic, MaRS, Le Groupe MISA, and the College of the North Atlantic.

The goal of the organization is to make the mining sector more productive and sustainable. On top of the environmental and innovative benefits of the project, MICA is also expected to support the creation of 900 jobs and at least 12 new businesses. The project is a big boost to the Sudbury economy, and the federal government’s commitment of $40 million to the project demonstrates Ottawa’s clear commitment to the project and the mining industry. MICA is planning for the commercialization of at least 30 new products, services, or processes for the mining industry and its operations.

A Wide Scope for the $109 Billion Sector

The project is a robust network of over 350 mining companies, industrial suppliers, academic and researchers, as well as industrial innovators. The idea is to create a network within which to share expertise and new technology from within the mining industry, and bring in new innovations from outside the industry. The project should also extend the lives of mines and cut the time it takes to bring new mineral deposits into production, according to the federal government. A backlog of mining projects waiting for approval in provinces like British Columbia on Canada’s west coast has created a bottle neck for new projects, but extending and expanding the life and scope of existing mines could help with production.

Canada’s mining industry is worth an estimated $109 billion, and the sector provides a massive tax base and job creation engine for the country. As one of the most stable and profitable mining jurisdictions in the world, the MICA project makes Canada an even more attractive partner and mining hub for the global industry.

“We all know Sudbury is the hub of mining activity, and its resource extraction companies are hungry for innovation,” said Charles Nyabeze, VP, Business Development and Commercialization, Centre for Excellence in Mining Innovation Inc. (CEMI). “MICA will be a conduit for them to find those innovations. We had to spend a lot of time strengthening the network, reaching out across Canada to identify the partners that we need. The most important thing is for us to find partners that allow us to tap into the innovations ecosystem of Canada and really harness that potential.”

Green and Global Ambitions on the Horizon As Well

While Canada is a clear focus for MICA, it will not be the only client served by MICA. Nyabese went on: “The bigger client is the global mining industry, and we’re really looking forward to making sure Canada takes its place as a leader in technology development and makes a difference on a global scale. We foresee the global mining industry looking at MICA as the primary source for new innovations.”

Essentially, the MICA project will act as an innovation ecosystem working toward modernizing mining and improving its productivity and environmental performance. Canada’s mineral supply chain will be strengthened as a result of the project, and domestic and export sales from Canadian innovators should increase. The core purpose of the project is also geared toward helping Canada reach its ambitious carbon emissions goals over the next decade and beyond, as the mining industry will be a large component of meeting those targets.

Doug Morrison, CEMI’s president-CEO and the leader of MICA commented, “The commercialization of innovations in the mining industry has never been more important than it is today. Supplying the demand for the minerals and metals needed to advance the green transition to a low-carbon economy is critical, but if mines are to produce more and do so faster, cheaper, and more sustainably, implementing innovation is essential. CEMI believes a national innovation network is necessary to identify innovative solutions and integrate them into the system-solutions that the mining industry needs. The MICA Network will help mobilize investments, grow Canadian SMEs and establish Canada’s leadership role in addressing climate change.”

“This is a shift in my focus, from proposals to rolling out and running the program.”

After years of planning MICA is ready to hit the ground running. The project has been in the planning stages for at least three year. The first intake projects will likely be shovel-ready projects to advance the mission of the project as quickly and efficiently as possible. Approximately 80 projects have been secured during the proposal-writing process, and those projects will begin imminently.

Nyabeze commented, “I’m really excited. This is a shift in my focus, from proposals to rolling out and running the program. The momentum is there and there are a lot of people who have been anxiously waiting to become a part of this network.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

A new publication by Toronto-based research group Capitalight Research called Critical Metals for a Sustainable World is calling for an average copper price of $4.20 per pound in 2021. This comes on the heels of May 10th’s new record of $4.88 per pound, and multiple reports about supply issues set to hit copper supplies around the world.

The inaugural edition of the report notes that “trend copper prices must remain well above long-term ‘incentive levels’ to justify new mine development”. This would require a copper price of at least $3.50 per pound. The report’s name also hints at how important the metals used for the coming sustainable energy transitions will be. The company has dedicated an entire publication to these ‘critical’ metals that include copper, lithium, nickel, and even steel.

Mega Imbalance

Demand for copper is set to outstrip supply in the coming years, with the second half of the current decade accounting for most of that growth. The report mentions that global copper demand will grow by 3.8% in 2022 to about 25 million tonnes. This will need to be offset by new discoveries, higher production, and most importantly, new mines. Some companies are already racing to fill the gap.

Invanhoe’s (TSX:IVN) Kamoa-Kakula mine in the Democratic Republic of Congo (DRC) is coming online just at the right moment. After some delays at the project, the mine is moving forward with the DRC granting approvals and initial works beginning. Teck Resources (NYSE:TCK) also has a new project in the works, called Quebrada Blanca Phase 2. The company commented that it expects, “the current mine expansion wave will peak in 2024 and a large projected gap in required mine supply will open up in the second half of the decade.”

It’s Electrifying!

Much of the demand is to come from energy storage and electric vehicles. Many countries are pushing for full-scale reworkings of their infrastructure and rewriting laws to ensure that new cars sold after on or after 2035 or similar time targets are 100% electric. President Biden’s Bipartisan Infrastructure plan is calling for a brand new recharging network to be built across the country, with a massive amount of the critical metals mentioned in the Capitalight report required to build all of it.

The Critical Metals for a Sustainable World report also mentions that demand for copper “from renewable power projects, energy storage and electric vehicles could double by 2025 to 8.5 million tonnes and unlike recent years, prices will be driven less by short-term macroeconomic development in China and more by rising demand linked to global decarbonization.”

Current Plans Are Not Enough

It also goes on to say that although the supply concerns will be muted slightly by new copper mines coming on stream from companies like Teck Resources (NYSE:TCK) and Ivanhoe Mines (TSX:IVN), the research company expects that, “the current mine expansion wave will peak in 2024 and a large projected gap in the required mine supply will open up in the second half of the decade.”

Opportunities are waiting just around the corner, as an exciting decade gets fired up for copper miners around the world.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

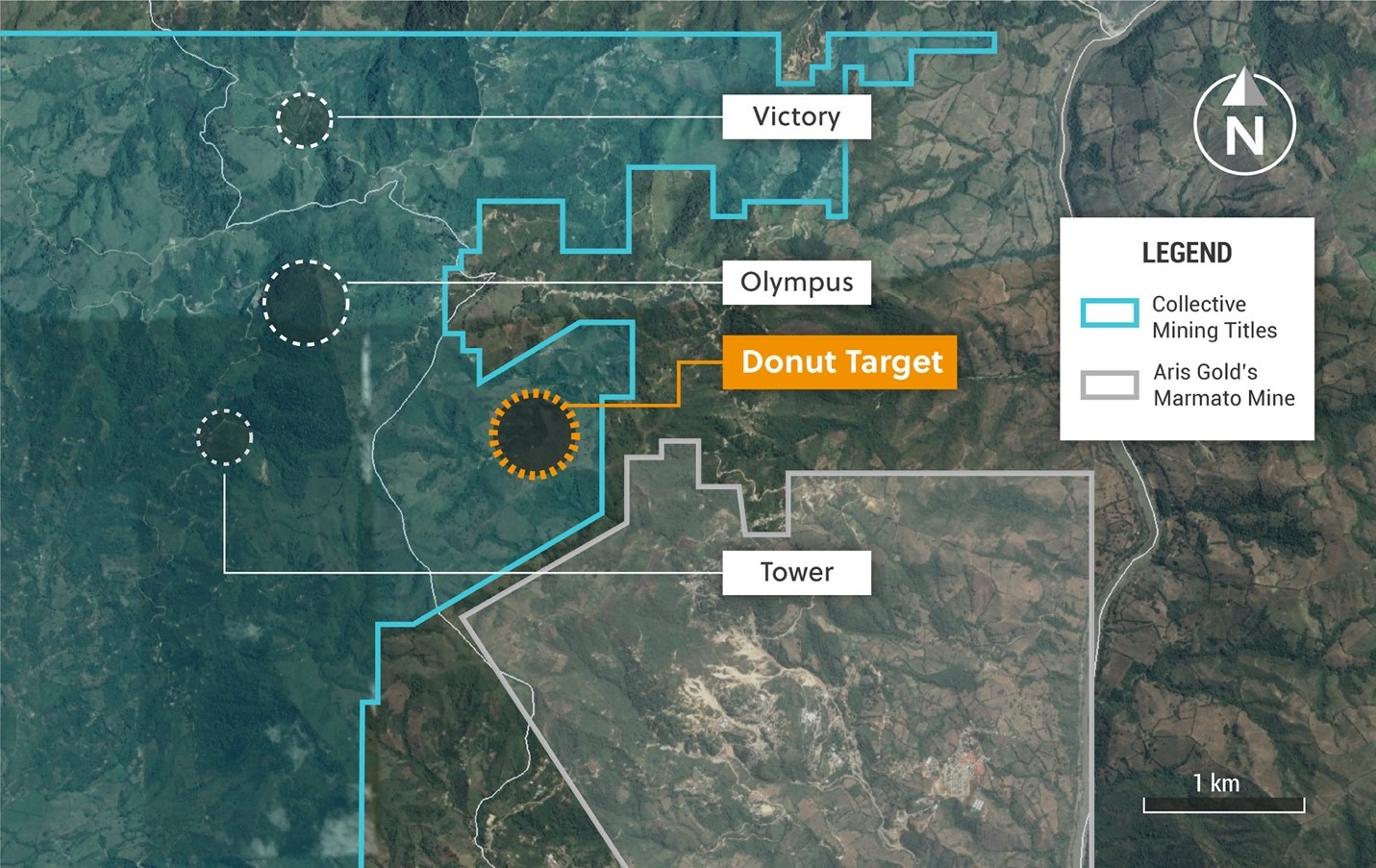

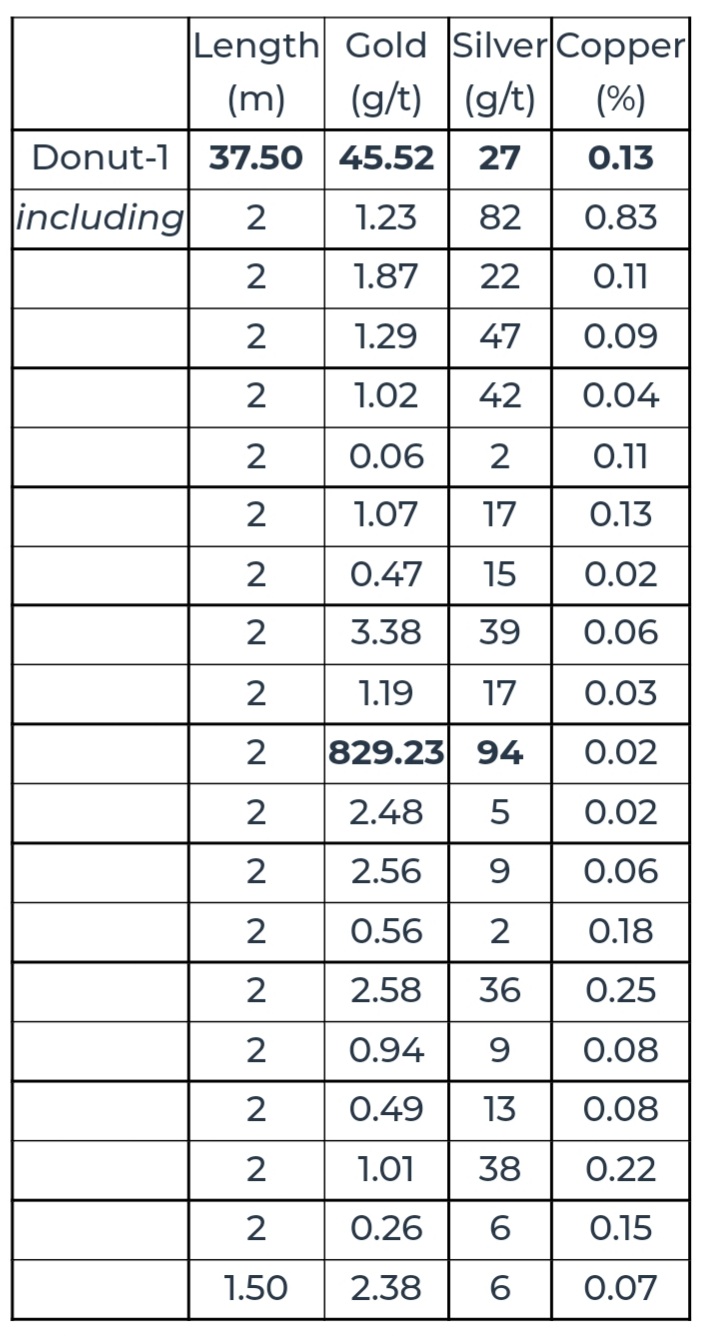

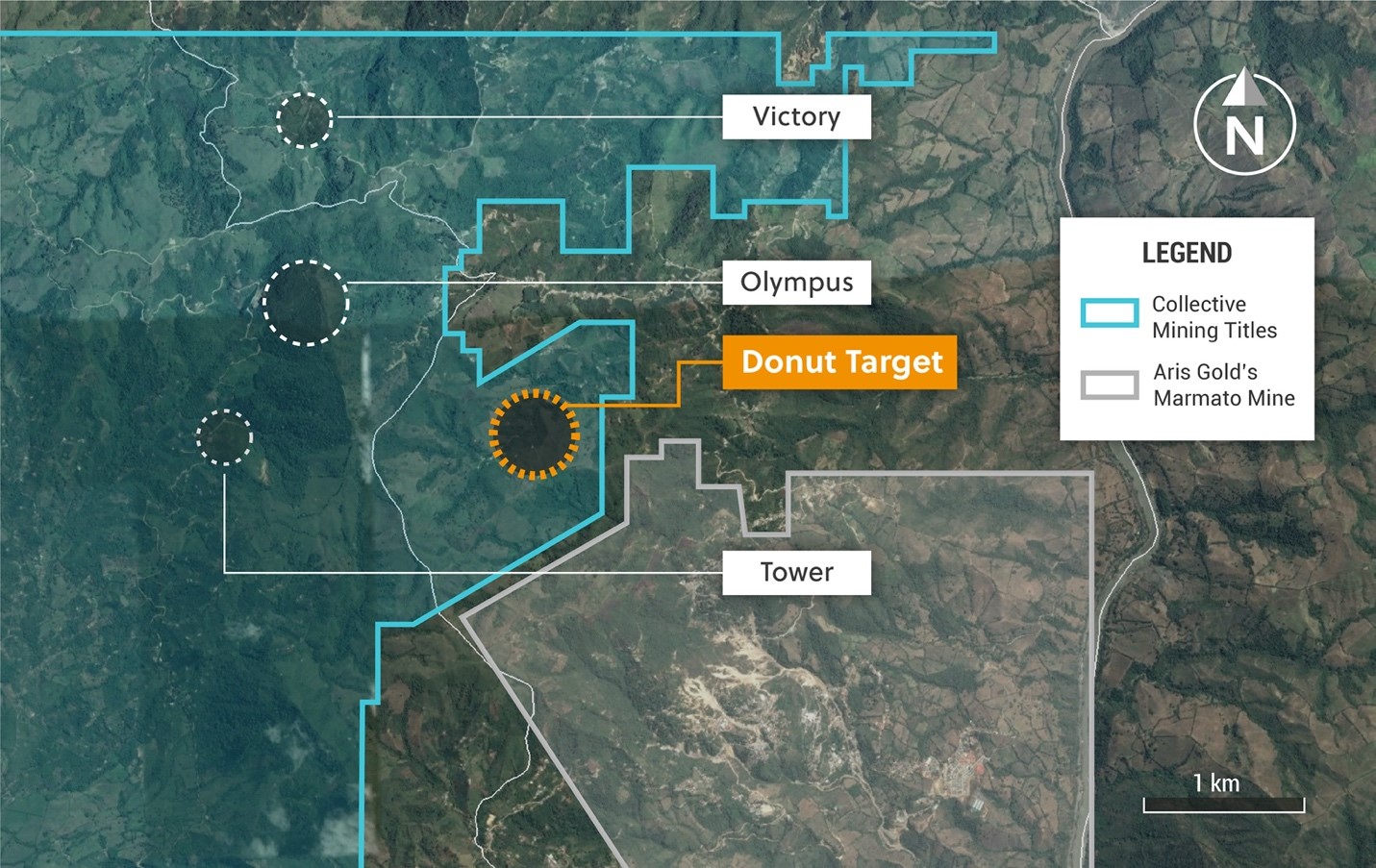

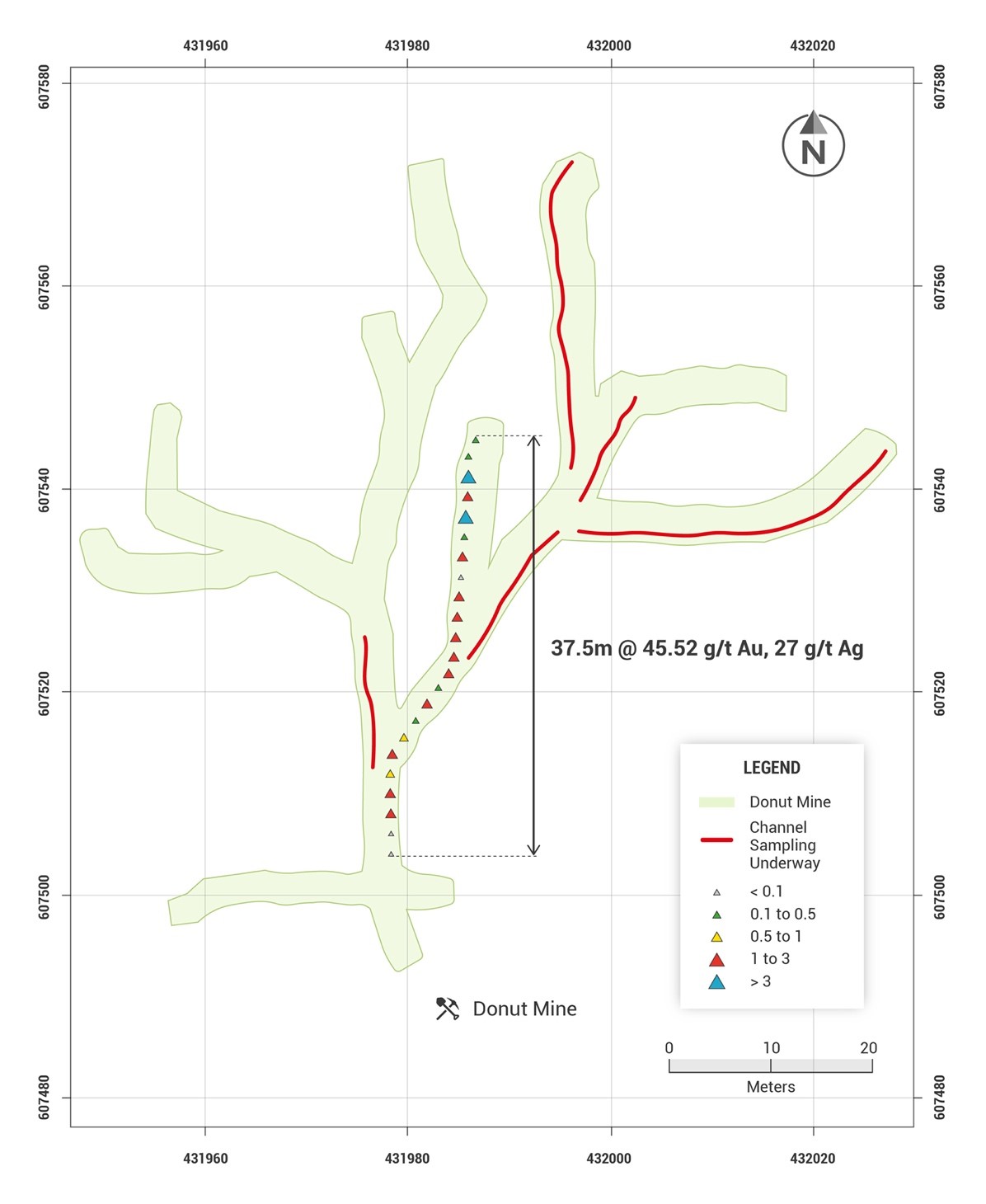

Collective Mining (TSXV:CNL) has provided an update on its flagship Guayabales Project this morning, announcing new channel samples 45.52g/t gold and 27 g/t silver along 37.5 metres in the underground development. The Guayabales project is a key focus for the company, with Collective (TSXV:CNL) interpreting the abundant precious metal mineralization encountered throughout to be related to a series of copper-gold porphyry intrusions hosted within the project tenements.

The Guayabales project is situated contiguous, immediately along strike and to the northwest of Aris Gold’s Marmato gold mine, for which Collective believes could be at least partially responsible for the rich mineral endowment of the Guayabales Project.

This is an important step for Collective Mining which is advancing on its Guayabales and San Antonio projects in Colombia. The company is looking to initiate its first-ever drill program in late August 2021, giving investors something to watch out for going forward. Collective will continue with channel sampling now to cover all underground workings and the target currently remains open to the north, north-west, east, and at depth.

“We are off to a very exciting start at the Guayabales project. The robust and continuous high-grade channel sampling results validate our geological model for the property. We look forward to initiating a first-ever drill program at the Donut target,” commented Ari Sussman, Executive Chairman.

Highlights From the Results (Table 1 and Figures 1-3)

The Company’s initial channel sampling campaign at the Donut taget (“Donut”) within the Guayabales Project has returned high-grade gold and silver assay results from a shallow underground tunnel. Mapping of this tunnet has exposed a gold-copper porphyry stockwork of veinlets with overprinting polymetallic vein systems. Additionally, the mineralized zone outlined by channel sampling results announced herein displays excellent grade continuity with results as follows:

Table 1: Channel Sampling Results*

Figure 1: Plan View of the Guayabales Project and the Donut Target

Figure 2: Plan View of the Donut Mine Showing the Grade Ranges for Channel Sampling Assay Results

Figure 3: Donut Target porphyry style mineralization in underground workings showing abundant copper mineralization.

Figure 4: Donut Target porphyry style mineralization in underground workings showing abundant copper mineralization.

Source: Collective Mining

Source: Collective Mining

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Wednesday brought good news for Australian mining company Sandfire Resources (ASX:SFR) as Botswana granted the company a mining license for its Motheo copper project in the Kalahari Copper Belt. The project is coming close to finalized permitting now, as this was one of the two major conditions before moving forward on the $208 million project.

Initial site works for the project began earlier in 2021 that included sterilization drilling, building a 15km access road to improve infrastructure, and the construction of a critical 200-person camp that will house workers and their families in some cases.

Next steps include bringing more staff on-site as the company begins construction of the process plant and other key infrastructure. Jobs created from the construction alone are expected to be a major boost to the local economy. Orders have also been placed for all key process equipment and long-lead items in preparation for the launch of the project. “We are absolutely delighted to now be in a position to move to full-scale construction at Motheo. I would like to thank the Government of Botswana for their support throughout the approvals process, which will see Motheo come on-stream in 2023 as one of very few new copper mines commencing production globally,” managing director and CEO Karl Simich said in a statement.

A Long-Term Play

The mine will be developed over a two-year period. Mining is planned to start in 2022 and the company plans to ramp-up operations for early 2023 as it approaches output that same year.

Simich said, “Motheo is expected to generate approximately 1000 jobs during construction and 600 full-time jobs during operations, and represents the foundation for Sandfire’s long-term growth plans in Botswana. Our vision is that Motheo will form the centre of a new, long-life copper production hub in the central portion of the world-class Kalahari Copper Belt, where we hold an extensive ground-holding spanning Botswana and Namibia. Sandfire is looking forward to becoming a major long-term player in the Kalahari Copper Belt, which represents one the last under-explored large-scale copper provinces anywhere in the world.”

Big Production to Help Botswana Diversify Exports

The company expects the mine to produce for 12.5 years, generating an approximate $664 million in pre-tax cash flows and $987 million EBITDA over the first ten years of operations at a calculated cost of $1.76 per copper pound. The project is set to launch during a time when copper demand is soaring and a lack of new copper projects gives companies opening new mines a big advantage in the market. Sandfire realizes this and is moving swiftly to capitalize on the seemingly perfect timing of their new project.

The open pit mine is expected to produce 3.2 millions tonnes a year. Botswana is a diamond-heavy mining jurisdiction, and the country relies on the gem for 70% of the nation’s export revenue. This project would be a step toward reducing its dependence on diamonds and diversifying its exports.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

For consumers and industrial businesses alike, silver is a critical component and prized precious metal. It is an efficient electric and thermal conductor, and it is highly valued for its electrical applications. The coming wave of electrification across broad swathes of the global economy is likely to continue pushing silver prices higher as demand picks up. This is not a trend that is going away any time soon.

Silver investors love it as well because of its behaviour as a commodity and its investment characteristics. It has a similar perception as a safe-haven metal like gold, making it a solid hedge against inflation and economic bumps that might shake other assets like stocks.

While investors might love silver, they almost always choose mining companies exploring, producing, or refining the metal. Whether it’s a big producer like First Majestic Silver or an exciting new exploration company like Tier One Silver, there are a few options for investors looking for exposure to silver in this trending market.

First Majestic Silver (TSX:FR) (NYSE:AG)

2020 was a tricky year for this popular Canadian miner, but silver generated 60% of the company’s revenue in 2020, making it a prime choice for silver investors. The company’s projects are focused in Mexico, with three mines operating in the country. It also has several other silver mines under development.

The company is not shy about its ambitions to become the largest silver producer in the world, and these mines are sure to take it one step closer to its goal. While spot silver may rise and fall with a more macroeconomic dynamic in play, stocks like this one are able to outperform silver prices. The company’s returns are based on their production and progress. Therefore it is up to investors to decide whether the Mexican mines and new mines under construction are setting the company up for long-term success.

The development of the new projects will likely be the catalyst for a run higher on the chart. Any sign that the company can increase its production while reducing mining costs either at existing sites or the new ones will likely give it a boost to outperform the precious metal.

It should also be noted that a rising tide can lift all boats, and that the likely steady climb for silver over the coming decade could provide a strong tailwind for the company regardless of changes to operations or how closely it hews to its new development plans.

The RSI reading on First Majestic recently hit 28.7, a new low and a possible indication that it is oversold. Traders will be looking for any momentum higher, especially if recently heavy selling is in the process of exhausting itself. Entry point opportunities abound for silver stocks as averaging out the cost of these shares is a long-term choice for the inevitable green revolution coming down the pipeline right now.

Tier One Silver (TSXV:TSLV)

We move from Mexico to Peru next, with an exploration company showing promising progress on its multiple projects in Peru. Tier One’s strengths lie in the abilities of the management and technical teams, with a strong record of cap raises, discovery, and monetization of exploration successes. The company’s flagship project Curibaya has received a lot of attention globally lately, with the first drill program commencing recently, but the company’s impressive portfolio of projects also includes:

- Hurricane Silver

- Emilia

- Coastal Batholith

- Corisur

Its recent expansion of the land position at Curibaya now includes an extension of the mineralized system. The expansion gives Tier One 50% more land at the site, taking it from 11,000 hectares to 16,800 hectares.