Three Valley Copper Corp. (TSXV:TVC) has announced a corporate and operating update for its 91.1% owned Minera Tres Valles property near Salamanca, Region de Coquimbo, Chile. The company also provided guidance for 2022 and 2023, and news of a new copper porphyry target.

December 2020 saw construction begin at Papomono Masivo which has proven and probable reserves of approximately 102 million pounds of contained copper with an average grade of 1.51%4. Papomono’s development is currently at 71% for horizontal works and 85% for vertical works. Expectations are that Papomono will be completed at the end of 2021 or in early 2022. Production is expected to then ramp up in 2022.

“We continue to improve the development rate of this project during the month of August (the advance rate being the best month on record), and we expect the fourth quarter’s projected advance rate to be similar,” said Joe Phillips, COO of the Company. “We have completed the critical ventilation shaft and the ore pass which will further accelerate the speed of our continued advance. We remain on track to commence the caving/mining process in December 2021 or early 2022.”

2022 and 2023 to Capitalize on Momentum

Guidance for 2022 and 2023 has also been provided by Three Valley Copper (TSXV:TVC) since the positive progress for the Papomono project is moving swiftly:

Copper production is expected to significantly increase in 2022 compared to 2021’s production range of 4,500 to 5,500 tonnes as the initial construction of the PPM project concludes and mining of PPM begins during the 2022 ramp-up year. Thereafter, it is expected that annual production between 13,000 and 16,000 tonnes of copper cathode will be attained in 2023 approaching the operation’s full production capacity. The Company’s production profile includes mineralized material from both Don Gabriel and PPM during 2022 and predominantly from PPM during 2023 together with material from ENAMI and third-party miners expected during both years. Looking forward to 2022 and 2023, Cash Costs are expected to fall significantly driven by higher grades from PPM and throughput coupled with decreased capital development and other sustaining capital programs. As the Company exits 2021 and completes its budgeting process, updates to this preliminary guidance may be required.

Source: Three Valley Copper

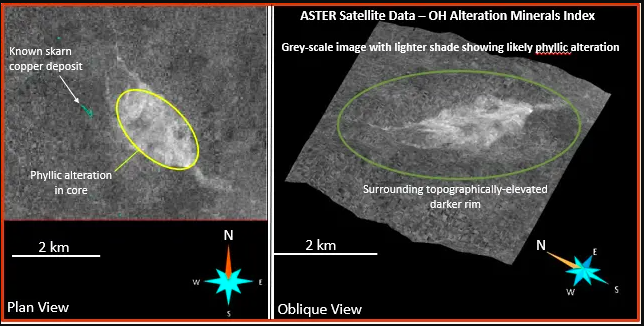

New Target Identified

Three Valley Copper commenced its near-mine exploration program at Minera Tres Valles on September 15 and has now announced it has identified a new copper porphyry target in its license area.

Previously mapped as a late Cretaceous granitoid intrusive, the identified targets displays likely hydrothermal alteration characteristics of the phyllic zone of porphyry copper deposits. This was determined after processing ASTER satellite data from the United States Geological Survey.

The newly identified central core is approximately 2 kilometres by 1 kilometre, and this outlines the surface footprint of the new target. A nearby copper deposit has been described as a skarn, and it should be noted that copper skarns are often nearby porphyry deposits. The fact that they are often located near one another is a very positive indicator for this new target and Three Valley Copper.

Michael Staresinic, President and CEO of Three Valley Copper commented, “John Mortimer, our exploration consultant, has identified an exciting target for the Company. Copper porphyry deposits are associated with some of the largest long-life copper mines in the world, with Chile hosting the greatest concentration of these deposits. This target is an example of the broader potential of this property as we continue to identify additional targets on our 46,000-hectare land package. This target forms part of our new exploration sections in our corporate presentation available on our website at https://www.threevalleycopper.com.

The recently announced exploration campaign will continue as planned, focusing on 6,000 to 8,000 metres of proposed drilling near Minera Tres Valles’ existing mines. Once this exploration campaign is completed, Three Valley Copper (TSXV:TVC) will direct its efforts toward this new exciting copper porphyry target.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Canada’s Premium Nickel Resources (PNR) has bought Botswana’s abandoned state copper mine known as BCL to resume operations within three years, said Minister of Minerals, Green Technology, and Energy Resources Lefoko Moagi on Tuesday. PNR was granted exclusive rights in February for a six-month due diligence review of BCL, which went into liquidation in 2016.

The company has signed contracts to buy two of the three shafts and related infrastructure, he said, without specifying the value. Moagi added that PNR was negotiating a separate deal to buy another BCL Group mine, the Tati nickel mine. In February, BCL liquidator Trevor Glaum said that PNR would begin construction of the mining infrastructure and prepare to operate, subject to a feasibility study, with a cost expected to exceed $400 million.

The mine produced at peak times an average of 40,000 tonnes of copper and nickel per year, but high operational costs and low international commodity prices led to its liquidation in 2016.

What the sale may reflect is an opportune moment for a Canadian miner to take advantage of high commodity prices and a particular focus on copper and nickel in the modern, green economy.

Five years ago, Botswana was not positioned to maximize the economic potential of the mine. However, the moment is here for these projects which can be brought into production quickly. With new projects rare and undersupply threatening pricing dynamics, these are the kinds of deals we may be seeing more frequently in the future.

That the project is located in Botswana poses some questions about the viability of the project and its operations. Mining in the country has suffered somewhat more recently, and complications always remain.

Geographical Questions

Without a doubt, Botswana is one of the world’s most successful developing countries. COVID-19 aside, the country has been on track for consistent growth.

Botswana is located in the centre of southern Africa, between South Africa, Namibia, Zambia and Zimbabwe. Once seen as a backwater with no natural resources, Botswana has long been ignored by the British Empire.

After being one of the poorest countries in the world when it gained independence in 1966, Botswana has become one of the world’s most successful developing countries. Important mineral and diamond wealth, good governance, prudent economic management and a small population of more than two million people have made Botswana a middle-income country with a transformation plan to become a high-income country by 2036.

Botswana is a high-middle-income country often touted as one of Africa’s few success stories. But despite rising profits from the country’s multinational diamond mining, the country’s bushman communities continue to suffer. The government is also grappling with a steady influx of Zimbabweans fleeing their country’s economic crisis.

Mineral extraction has made Botswana one of Africa’s richest countries. Despite this enormous wealth, Botswana remains a highly unequal country. It ranks as the most unequal country in the world on various measures of inequality, such as the Gini index.

From Diamonds, to Copper, Nickel, and more

Botswana is also known as one of the world’s largest sources of ethical diamonds, making diamonds from the country popular with consumers who care where their diamond is produced.

Mining contributes 34% of the country’s gross domestic product (GDP) and 50% of its taxes. Since diamonds were discovered in South Africa in 1967, mining revenues have been invested in infrastructure, schools, and medical centers. The industry is also considered a beneficiary of minerals, creating jobs and boosting the country’s economy.

Today, only about 20 percent of Botswana’s 2 million inhabitants are engaged in diamond mining. But the country is seeking to diversify its economy, betting that sustainable tourism will help maintain a high standard of living in the future. And projects in mining continue to hold enormous value in copper and nickel such as the one purchased by Premium Nickel Resources

Although Botswana has long been known for low inflation and controlled wage growth, a 2013 study by the Botswana Institute for Development Policy Analysis, a non-governmental think tank, on export diversification found that non-mining labor in the local private sector is more expensive than the regional average. For example, diamond processing companies claim that the cost per stone in Botswana is $60 to $65, compared with $20 to $30 in China and $12 to $25 in India.

While a recovery with favourable prospects for the global diamond industry is expected in 2021, the economic impact of COVID-19 is likely to be deeper and longer-lasting. Developments in the diamond industry will have a telling effect on the near-term recovery, given Botswana’s dependence on the commodity.

Mineral exploration in diamond-dependent Botswana will continue despite the difficult economic conditions facing the country’s mining industry, which will have a negative impact on its economic health, says Charles Siwawa, CEO of the Mining and Exploration Organisation of Botswana (Chamber of Mines). The minerals he outlines are coal, copper, silver, lead, zinc, manganese, and iron ore, which remain attractive due to the amount of ore uncovered, as well as minerals that are economically viable. He points out that financial analysts have assured the Chamber that the mines in Botswana have net mineral values and can make positive contributions to the economy.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

When hunting for the best mining stocks, it can often feel like playing the lottery. Most companies seem to be exploring in the dark, hoping for the right combination of mineralization and luck. However, some companies use historical data and advanced mapping to target their projects and drill programs, and Collective Mining is one of those companies.

Collective Mining (TSXV:CNL) is an exploration and development company working to identify and explore gold projects in South America. The Collective team was previously responsible for discovering, permitting, and constructing the largest gold mine in Colombia, and ultimately selling that company (Continental Gold) to Zijin Mining for C$2 billion. It would be an understatement to say that this team has experience with exploration success.

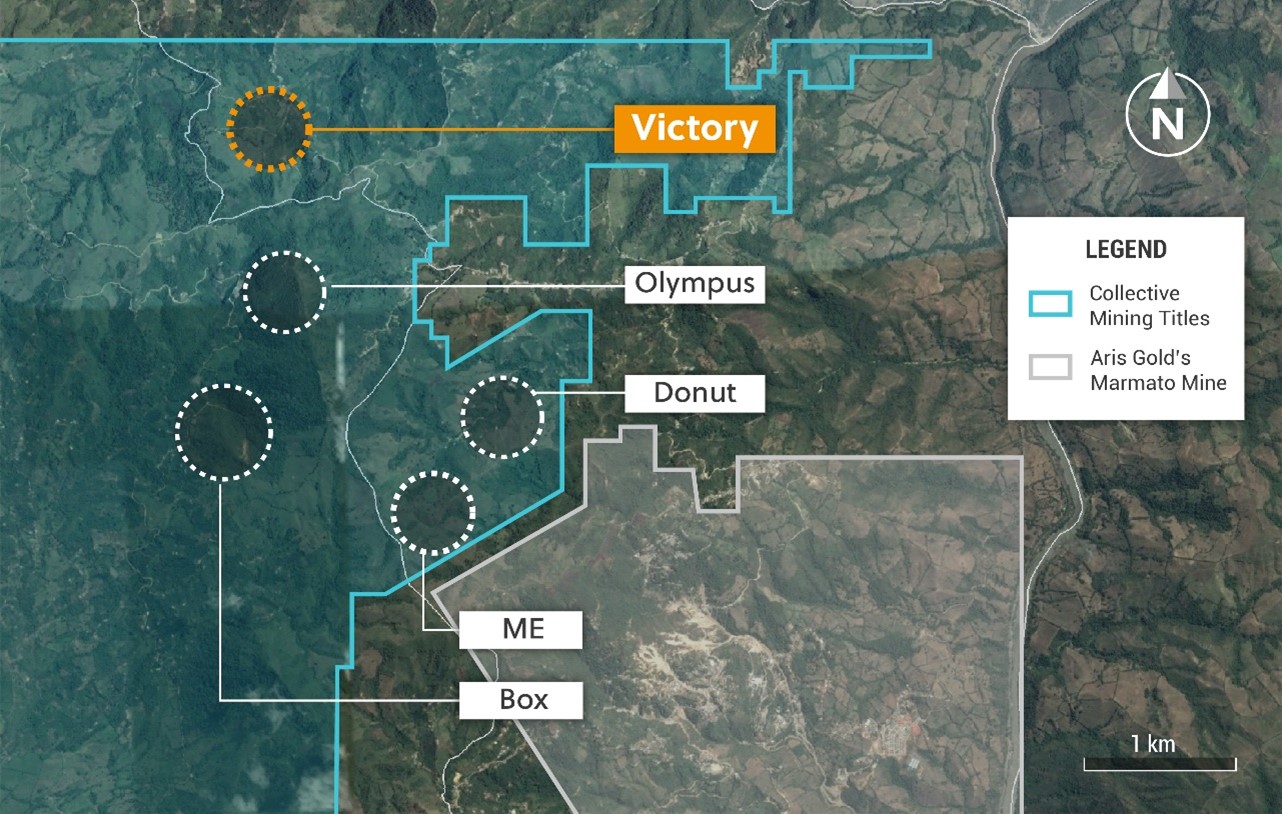

So when the company set up a new project at its Guayabales and San Antonio sites, it sent up a flare to the industry that something beyond the nearby Marmato Mine might be sitting just below the surface. Aris Gold is advancing and managing the Marmato Gold Mine, sitting right next door.

The Neighbour

Aris Gold operates the Marmato Mine in Colombia, where a modernisation and expansion program is underway. The Marmato mine is located in the Marrato Gold District of the Department of Caldas, a mountainous area about 80 km south of Medellin, Colombia.

Marmato is a 13-year mine that currently boasts gold reserves of 2.0Moz @3.2g/t, M&I gold resources of 4.1M0z @ 3.2g/t, inferred gold resources of 2.2 Moz @ 2.6 g/t, and strong production in place. Marmato has a processing capacity of 5,500 tpd, equalling 165koz per year in LOM average production, with an LOM average AISC of $US880 per oz. Marmato is producing, and the extension will help.

However, this is an established project that hasn’t fully lived up to the hype of the discovery. Capex for the lower mine expansion is in place and set at an estimated US$268 million. The lower mine is going to need to pay off huge if that investment is to pay for itself and then some.

While Marmato has seen some success, investors are beginning to wonder if there is a better value investment just down the road, with Collective Mining’s Guayables project.

The New Kid on the Block

The Guayabales Project is located approximately 75 km south of Medellin in a strike area adjacent to the Marmato Gold Mine. The Marmato mine has a long history dating back to pre-colonial times and was used as security for financing the war of independence against Spain. The project is located along the NW trend of the Marrato Mineralized Corridor and represents an immediate NW extension of this trend.

Collective Mining (TSXV:CNL) may present somewhat of a more attractive opportunity because of the size of the untapped potential. Yes, there can be a first-mover advantage that Aris Gold has enjoyed for some time. However, the second mover is the one that gets to learn from the first’s mistakes and improve everything.

For one, Collective isn’t wasting any time. The company announced in mid-September that its 7,500 metre diamond drilling program had commenced. That program will include drill testing at five targets including Donut, Box, Olympus, Victory, and ME. Additionally, investors won’t have to wait for assay results very long, as the first assay results are anticipated in October.

Last week, the company already filed a NI 43-101 Technical Report for the Guayabales Project as well, wasting no time in getting results to investors.

Collective might also have a more attractive capital structure with only 47.2 million shares outstanding, and no warrants exist. While it is early stages still, the company’s $26 million cash balance is a strong start for a project that is already showing strong early signs of high-grade mineralization. Certainly choosing a site along a proven deposit adjacent to a producing mine is helping. Marmato hosts 6.3 million oz – how much might Guayabales have?

Is Guayabales the Next Marmato?

So is Guayabales the next Marmato? Well, the sites share many similarities including the same host rocks, structural trends, styles of mineralization, and types of alteration. Additionally, it should be noted that precious metals mineralization at Marmato is exposed at a vertical extent of more than 1,000 metres. For some context, exploration at Guayabales has only been limited to the upper 100-200 metres of the system.

So, there could be a potential 80%+ of the system unexplored at this point, with tens of millions to spend expanding the drill program further. Any one of the five targets could end up yielding a large, mineralized porphyry system.

Guayabales includes a package of 3,333 ha, close to connections to the national electricity and natural gas grids that run just 3 kilometres east of the project. Sitting in the middle of the 250 kilometre long Middle Cauca Gold Belt hosting approximately 100 million oz Au and 11+ billion pounds Cu, this is seemingly the best possible property in the area.

Asking now whether Guayabales is the next Marmato seems premature, but at this rate, it might not be. Guayabales presents possible greater potential upside for investors who might already be decided that the proven reserves and life of mine at Marmato just aren’t cutting it. Instead, the market now is more likely deciding whether Guayabales will be bigger than Marmato, and whether the team that sold Continental Gold in a multi-billion dollar deal is about to hit its second home run.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Mining companies have become some of the biggest companies to make sweeping, rapid changes to their business models, operations, and social responsibility charters in the last five years. With net-zero emissions goals being set around the world for the developed world from anywhere from 2030 to 2050, companies will need to keep up.

The mining industry’s renewed commitment to ESG (environmental, social, governance) principles has meant that a new operational standard is in place. For many, that means reducing emissions to zero.

Canadian gold mining company IAMGOLD (TSX:IMG) is taking the pledge to achieve net negative greenhouse gas emissions (GHG) emissions by 2050 at the latest. This is a challenging task, but one that can be accomplished with the right amount of investment and commitment.

Gordon Stothart, President, and CEO of IAMGOLD (TSX:IMG) said on Monday, “In our view, reversing the effects of climate change does not mean stabilising emissions; it demands that we reduce the total volume of greenhouse gases going into the atmosphere and the world’s oceans year over year. We know that we are losing habitat at an unsustainable pace.”

The company’s strategy will be two-pronged, with the first target focused on GHG reduction from scope 1 and scope 2 emissions. This largely focused on heavy and light vehicle fleets and power generation and supply. This is the easiest to accomplish because the technology exists, and investment will only be needed for implementations.

The second prong of the strategy includes the second target of GHG removals. This is done by supporting the effects of climate change by supporting net positive biodiversity and protecting carbon sinks. To do this, IAMGOLD (TSX:IMG) will use nature-based solutions, creating habitat for flora and fauna at a faster rate than it disturbs. This net-zero approach will ultimately cancel out any of the effects of disturbance in local habitats from mining operations.

Stothart continued, “Absolute reductions form a critically important part of IAMGOLD’s strategy in actively combating climate change, with investments in nature-based carbon offset projects supporting greenhouse gas removals.”

Mining companies are held to a much higher standard these days, and reporting is necessary at every step of the process. In 2022, an external verification will be completed on its emissions reporting, the company will develop and announce medium-range time targets for reductions and removals for targets 1 and 2, and publish a solid roadmap and timelines for how the company will achieve its ultimate goal by 2050 of net negative emissions.

How the Industry is Adapting

The mining industry is adopting ambitious and ambitious sustainability targets to promote safer and more sustainable mining activities that will have a positive impact on society. It is cutting CO2 emissions as fast as possible for projects, with the aim of increasing their overall value to society.

Most companies have targets set for 2030, and 2050, that create a step-by-step process for achieving net-zero or net negative emissions by those dates. Many companies are reducing emissions and compensating for CO2 emissions that can’t be avoided to create a sustainable world for future generations. The best way to help the mining industry meet its emissions targets is to improve its operational efficiency in the short term and invest in renewable energy sources in long term.

The need for change is increasingly permeating the mining sector and technological advances offer miners opportunities to reduce their direct and indirect emissions. Looking to the future, feasibility studies of new and existing mine extensions will be assessed according to the impact on emissions and the way in which mines can achieve sustainability.

Electrification of the plant and other operations is a crucial way to reach zero in mining, processing, and transport. Many of the hardest-to-electrify heavy industries and mining processes have emissions that are difficult to eliminate and are part of the energy mix over which miners have no direct control. Consider the steel industry which over the next 20 years must eliminate 17 billion tonnes of direct and indirect CO2 emissions. This is a challenge, but one that the industry is taking on, head-on.

Removing 6.1 billion litres of diesel from copper mines per year – equivalent to 105,000 barrels per day – would reduce a quarter of all greenhouse gas emissions produced. The copper mining industry is pushing hard for net-zero emissions, as a metal that can be used for electric energy storage and transportation. This green technology metal is critical to the future of net-zero emissions, and so mining companies are committing to making the production process green as well.

Most diversified miners have set bold net-zero targets in oil and gas. The major benefit of all of these goals is that miners can provide the supply growth and demand for the energy transition they need to decarbonize their own sector. Mining is the key to the refinement of metals that can be used in wind, solar, electric vehicles, storage, and transmission, and will be essential if the world is to achieve the Paris target of net emissions by 2050.

For them, the route to eliminating their own operational greenhouse gas emissions by 2050 is feasible if not attractive. The world’s largest mining companies by market capitalisation, BHP Group (ASX:BHP), and Rio Tinto (ASX:RIO), have espoused ambitions for net-zero emissions, as has been noted in previous analyses of mining companies as serious and feasible targets.

As a result, many mining companies have set ambitious carbon emissions targets that are consistent with the Paris climate agreement from 2015 and strive to attain net emissions zero.

Net CO2 emissions occur when greenhouse gas emissions released by an organization are offset by an equivalent amount of carbon capture from the atmosphere. For many mining companies, this means determining a baseline level of GHG emissions and then looking for ways to reduce these emissions, commonly called decarbonization.

Although there are practical limits to how much GHG emissions can be reduced in mining, several innovative approaches that will be explored in the future are promising. New technologies, better use of data and smart automation are helping mining companies to become more energy efficient around the world.

Vale, one of the world’s largest mining companies, has been outlining its greenhouse gas reduction commitments for some time. Having the industry giants committing to this goal is a signal to the rest of the industry, no matter what size company, that it is a real and possible target.

The World Bank estimates that the transition to a net-zero emissions economy will require demand growth of up to 500%. On an individual raw material basis, demand for cobalt is estimated to increase by 20% by 2040. Copper, nickel, and other metals necessary for electric technologies for infrastructure and in particular EVs will share in that demand growth as well. If demand grows by many multiples as predicted, then this trend is one that will grow to be unstoppable in the near term, and perpetually inevitable in the long term.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Nickel is an indispensable compound in steel production and is known as the “silent saviour” because it plays a role in the global transition to clean energy and is one of the key metals for battery assembly in electric vehicles for companies like Tesla, Volkswagen, Mercedes, and more. In 2020, despite the global pandemic, global nickel production totalled 22 million tonnes. Global nickel mining production is expected to rise again this year, with GlobalData estimating an increase of 6.8% to 25 million tonnes.

According to the US Geological Survey, total nickel reserves are estimated at 94 million tonnes. That total counts Australia and Indonesia as holding some of the largest reserves in the world, with big production numbers as well.

Production slowdowns were not a particular problem for the nickel mining industry, and the industry was more than able to make up for lockdowns and restrictions by keeping operations running in multiple countries using caution and the right safety measures. The total 22 million tonnes produced in 2020 is a testament to the resiliency of the industry and the fact that while demand may have shrunk temporarily in the period, production must continue to keep up with ongoing demand that continues to rise.

The Top 10 Nickel Producers

Russia Norilsk Nickel (OTC:NILSY)

Russia Norilsk Nickel (Nornickel) was the top nickel producer with approximately 178 kilotons (kt) of production, up from 172 kn in 2019. The Nornickels Kola Division, which includes five mines, is being reviewed for its environmental footprint and has pledged $5 billion over the next decade to clean up the pipelines on the Kola Peninsula.

Vale (NYSE:VALE), Glencore (OTC:GLNCY)

From its Brazilian proejcts, Vale (NYSE:VALE) is in second place with 167.6kt, down from about 171kt the year before. PT Vale Indonesia says it plans to begin construction of its Pomalaa nickel project next year. The mining giants in third, fourth and fifth place are Glencore (OTC:GLNCY), which has assets in Australia, Canada and Europe and collectively produced 101.6kt and 108kt in 2019 ; followed by BHP (ASX:BHP) with 74.8kt from its nickel west business in Australia, and Anglo American (LSE:AAL) with 43.6kt from its Brazilian business.

The Chinese company MCC JJJ Mining, whose production is based on its ownership of 85% of Ramu Mine in Papua New Guinea, rounds out the top ten and is one point behind Finnish Terrafame with 28.6 kts of nickel production in 2020. Perth-based IGO produced 29.5kts and Terrafames followed close behind with 28.7kTS.

A Metal for an Electric Future

Nickel is known as the “silent saviour” because it plays a role in the global transition to clean energy and is one of the key metals for battery assembly in electric vehicles. The nickel group is of extreme importance to the global economy and the mining industry in countries in every corner of the globe.

Metallic mineralization occurs in the hard nickel group, which includes nickel, cobalt, copper and chromium. The economic concentration of nickel is found in sulphide and laterite-rich deposits in Australia, Indonesia, South Africa, Russia and Canada which together account for more than 50% of the nickel resources in the world. Nickel mining has increased significantly over the last three decades, and known nickel reserves and resources are growing rapidly.

Due to the enormous use and demand for Canada’s nickel specifically, nickel-related products are exported to more than 100 countries. Nickel and its compounds are indispensable for the manufacture of countless products on which we depend.

Nickel, long used as a corrosion-resistant material in the steel industry, has exploded due to the mass production of cheap electronic equipment, most of which uses nickel in manufacturing. Demand for nickel has also increased in recent years and is becoming increasingly important in the electric vehicle industry. As demand for renewable energy increases, electric cars are increasingly dependent on copper, nickel, cobalt and other metals.

As the world moves away from fossil fuels, the demand for copper, nickel, cobalt and other metals will continue to rise. A 2017 World Bank report says that the industry will demand copper and nickel by 2050 at an increase of 250% if the world builds enough wind technology to keep global warming below 2 degrees – an increase over the Paris climate agreement benchmark. With the additional need from energy storage technologies, the demand for nickel will increase by 1,200 percent.

The same applies to cobalt, which is needed for lithium-ion batteries and can be degraded. According to a report by the World Bank on a low carbon future, there will be strong demand for a wide range of base and precious metals. In addition to the usual suspects such as cobalt and lithium-ion, the list includes aluminium, silver, steel, nickel, lead and zinc.

Cobalt is a silver-grey metal that was developed as a by-product of copper and nickel mining and is an important component of the cathode of lithium-ion batteries. Nickel is another ingredient needed in batteries and is expected to account for a large proportion of future batteries.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

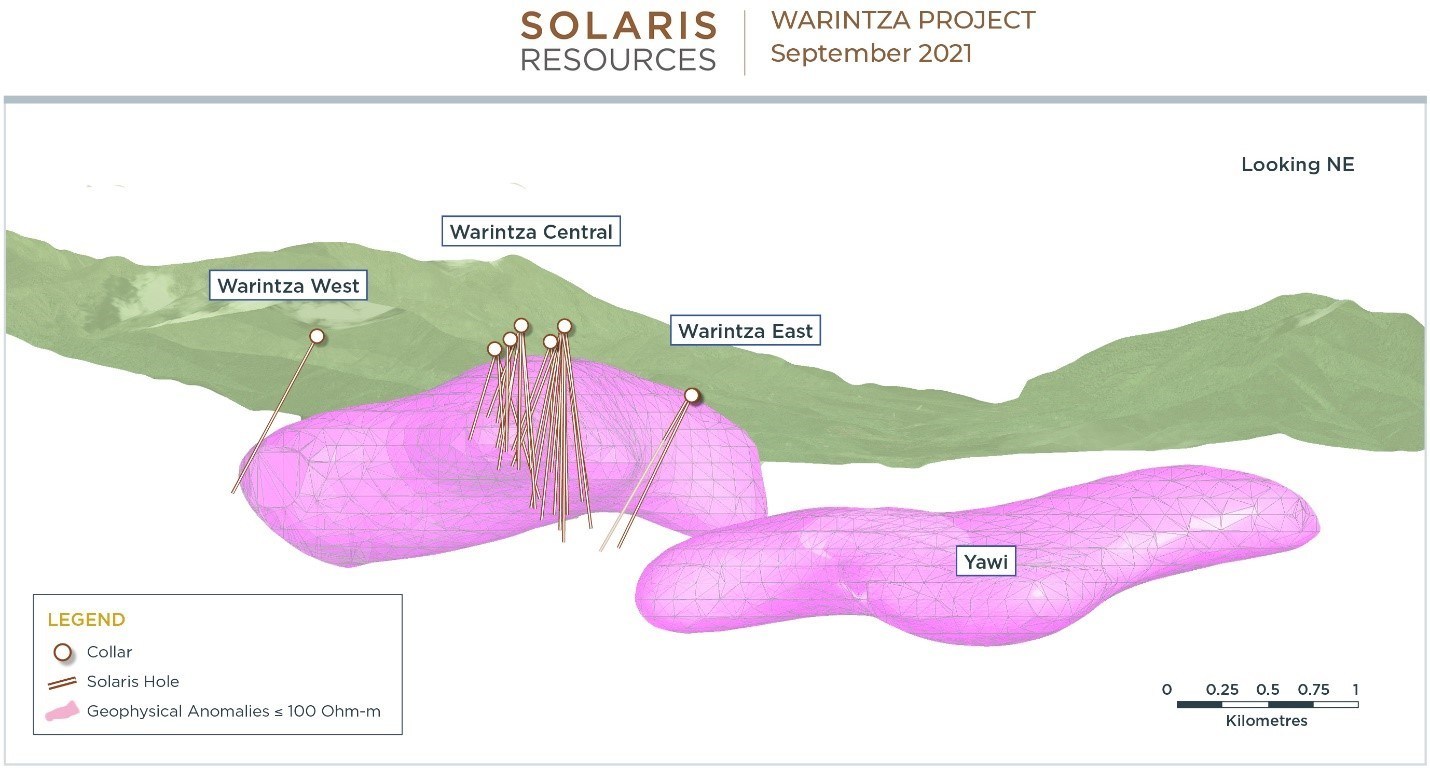

New assay results from Solaris Resources’ (TSX:SLS) Waritnza East discovery have return long intervals of copper prphyry mineralization from surface, from the first two holes. The high-grade links identified between Warintza East and Warintza Central is now being targeted, as this area to the north may yield a higher-grade mineralization.

Highlights

- The first two holes at Warintza East, as detailed below, both returned long intervals of copper porphyry mineralization from surface across a significant portion of the undrilled gap to Warintza Central, suggesting potential continuity between the two zones

- Visual observation of mineralization in the second hole and step-out drilling completed northeast of Warintza Central suggest an offset in the east-west corridor of higher-grade mineralization to the north that is being targeted in ongoing drilling

- SLSE-01, collared approximately 1,300m east of Warintza Central and drilled to the southwest, returned 396m of 0.42% CuEq¹ from surface, with the full length of the hole of 1,213m assaying 0.28% CuEq¹

- SLSE-02, collared from the same platform but drilled to the northwest, returned 320m of 0.48% CuEq¹, including 62m of 0.68% CuEq¹ from surface, from the first 320m of core for which assays have been received, with the last 10m of the interval grading 0.47% CuEq¹

- Visual observation of core from SLSE-02 suggests that a much broader interval of mineralization may exist than the portion for which assays have been received and reported herein; remaining assays are expected in October, along with the results of step-out drilling from Warintza Central

- Warintza East is the third major discovery within the 7km x 5km Warintza porphyry cluster and is defined by coincident copper and molybdenum soil anomalies, measuring approximately 1,200m in strike, and a high-conductivity geophysical anomaly that extends from the target through Warintza Central (refer to Figure 1)

Figure 1 – Long Section of 3D Geophysics Looking Northeast

Figure 2 – Plan View Showing Wartinza East Drill Hole Traces

Table 1 – Warintza East Results

| Hole ID | Date Reported | From (m) | To (m) | Interval (m) | Cu (%) | Mo (%) | Au (g/t) | CuEq¹ (%) |

| SLSE-02 | September 27, 2021 | 0 | 320 | 320 | 0.39 | 0.02 | 0.04 | 0.48 |

| Including | 0 | 62 | 62 | 0.59 | 0.01 | 0.06 | 0.68 | |

| SLSE-01 | 0 | 1213 | 1213 | 0.21 | 0.01 | 0.03 | 0.28 | |

| Including | 0 | 396 | 396 | 0.33 | 0.02 | 0.04 | 0.42 | |

| Notes to table: True widths cannot be determined at this time. | ||||||||

Table 2 – Collar Location

| Hole ID | Easting | Northing | Elevation (m) | Depth (m) | Azimuth (degrees) | Dip (degrees) |

| SLSE-02 | 801485 | 9648192 | 1170 | 1191 | 275 | -50 |

| SLSE-01 | 801485 | 9648192 | 1170 | 1213 | 260 | -45 |

| Notes to table: The coordinates are in WGS84 17S Datum. | ||||||

| (1) | No adjustments were made for recovery as the project is an early-stage exploration project and metallurgical data to allow for estimation of recoveries is not yet available. Solaris defines copper equivalent calculation for reporting purposes only. Copper-equivalence calculated as: CuEq (%) = Cu (%) + 3.33 × Mo (%) + 0.73 × Au (g/t), utilizing metal prices of Cu – US$3.00/lb, Mo – US$10.00/lb and Au – US$1,500/oz. |

Mr. Jorge Fierro, Vice President, Exploration, commented: “With this latest discovery at Warintza East and the growing footprint of Warintza Central to the north and east returning some of the strongest intervals reported to date, the conceptual pit shell is expected to be extended to the north and east showing the potential to ultimately become one multi-kilometre ‘superpit’ joining the two areas. Future drilling will focus on the open, undrilled area between these two zones.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Uranium had been sitting at historic lows for most of the last decade, but as demand and sentiment surrounding uranium turned around slowly, prices have begun to turn around. Prices have risen by 40% in the month of September alone, overtaking all other major commodities. A few weeks ago, millions of pounds of supplies were scooped up by the Sprott Physical Uranium Trust. That deal alone was enough to push prices significantly higher in a single day and put the uranium story on the map of every miner, trader, and refiner.

Uranium has gotten somewhat of a bad reputation after a series of disasters at multiple reactors. The visuals of those accidents were enough to turn people off from the idea of having a reactor near their town or home. However, the price changes happening now show that buyers are ready and the industry might be set for a resurgence.

Barriers for Uranium Not Insignificant

It’s a massive bet on the importance of nuclear power in a carbon-free future. The problem, at least for investors who have pumped hundreds of millions and in some cases billions of dollars into this bet, is that a debate is raging over whether nuclear power should return to the forefront. Nuclear energy has been taboo since the Fukushima disaster in Japan, and the 2011 meltdown and recent accidents show that reactors are too dangerous for some people to stomach. And because nuclear power is carbon-free, it has attracted opposition from progressives and environmentalists who have concerns about radioactive waste.

According to Chris Gadomski, a leading nuclear analyst at Bloomberg NEF, only 50 reactors are under construction, a 20-year low. Still, in his view, there is nothing overdone about the uranium rally.

Producer stocks were in a frenzy that now seems to have peaked. Cameco Corp. fell more than 13% after hitting a 10-year high last week. Exploding uranium prices now seem to have hit the brakes. Futures trading in New York fell as much as 9.8% on Tuesday before ending losses and closing the day at $49.75 a pound, 0.3% lower than that.

Kazatomprom, the world’s largest uranium producer, warned that recent price moves have fueled financial investors in utilities that use the radioactive metal as fuel for their reactors. There is also speculation about a new Sprott Physical Uranium Trust and what it might do next after its aggressive move several weeks ago.

Nuclear power has always been controversial, but the debate has never been more polarized. Uranium skeptics tend to agree that nuclear power will account for a larger share of electricity generation if global governments implement their ambitious plans to wean themselves off fossil fuels. Supporters anticipate a nuclear fission renaissance that could mobilize $5.9 trillion in global investment by 2050 — the year dozens of nations, including the US — aim for net-zero economies.

A Viable Option

Worldwide, awareness is growing that the closure of coal and natural gas-fired power plants is leading to blackouts. Dependence on wind, solar and hydropower is proving cumbersome, as evidenced by the constant threat of blackouts in California and rising energy prices in Europe. This is where the promise of nuclear power, with its round-the-clock carbon-free electricity, comes in.

To unlock this potential, Sprott Fund has been buying uranium daily. The pace of its purchases has changed and is now a regular occurrence on the open market, contributing to price swings. The surge in demand comes at a time of historically low prices as pandemic mine disruptions prompted uranium producers, including Cameco, to buy more in the market to fulfill their long-term contracts with consumers. That helped push uranium futures up to $50.80 last week, the highest level since 2012.

In fact, Sprott’s purchase has eliminated inventories that have been hanging on the market since Fukushima and led to the shutdown of most of Japan’s nuclear reactors. Disasters such as Fukushima and accidents such as Chernobyl and Three Mile Island have made nuclear power look suspicious for years.

From East to West

But some governments are rethinking that approach. Illinois Governor J.B. Pritzker signed a sweeping climate change bill this month that subsidises Exelon Corp with $700 million over five years, prompting the company to change course and keep two nuclear power plants in the state alive. According to the China Nuclear Energy Association, the short-term objective in China is to approve six to eight new reactors a year by 2025, with 70 gigawatts in operation and 40 more under construction.

And in Japan, nuclear power is slowly returning. So far, Japan has restarted one-third of its 33 operational reactors under Fukushima safety regulations, with the remainder to be restarted by 2030. Taro Kono, the minister of administrative reform who has emerged as a leading candidate to succeed Prime Minister Yoshihide Suga, has said that nuclear power will be necessary to some extent if the country is to meet its pollution-reduction targets.

That is not to say that this will not be an uphill battle. Some nations are turning to nuclear power again, while others are phasing out nuclear power. Germany, for example, will shut down its last reactor this year.

Better, Safer Tech, and a Quiet Uranium Revolution

At the same time, the future of nuclear power is fueled by a new generation of smaller reactors that are expected to be faster and cheaper. They will need less uranium than the huge conventional plants currently in operation and have the potential to dampen the commodity market. But it will take at least a decade to get them up and running. In the meantime, the big question is whether investors’ gains in demand will be enough to support the market.

All the right pieces are in place for the next part of the cycle. It is possible that the recovery in the spot market could be a catalyst to encourage more utilities to get involved and sign long-term contracts. That would not only change the future of the uranium market and industry, but the energy industry around the world.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

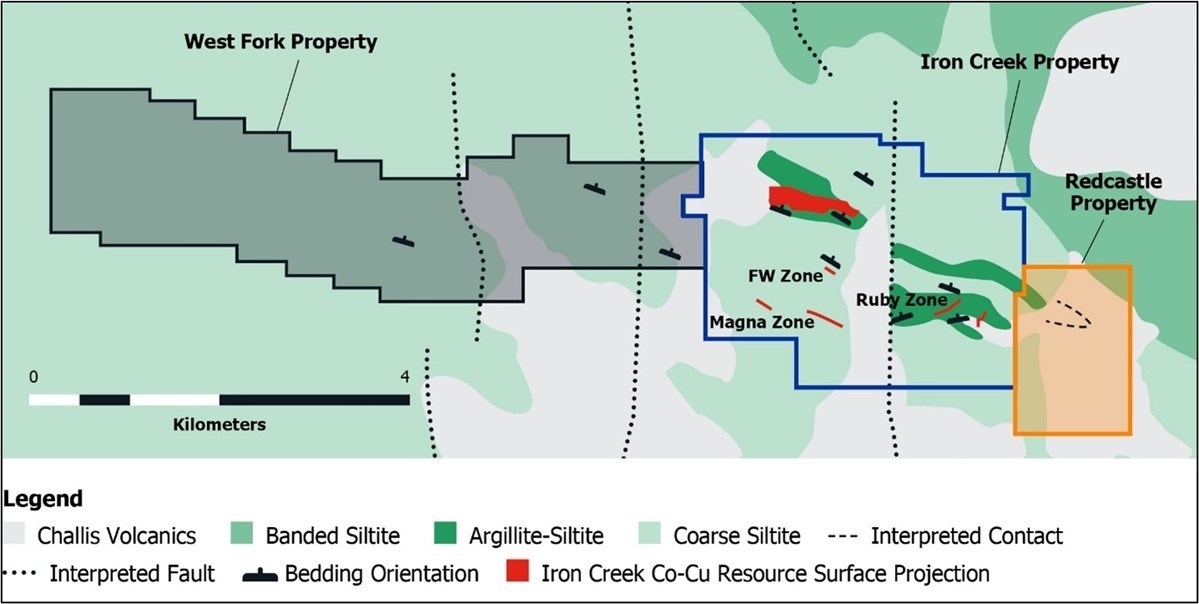

First Cobalt Corp. (TSXV:FCC) has now resumed drilling at its wholly-owned cobalt-copper project in Idaho, USA, Iron Creek. After a brief pause in the program, the company is ready to begin drilling again in the midst of favourable market conditions and with new goals to increase the size of the current resource.

First Cobalt’s goal is to double the size of the current resource over the next two years in light of strong commodity prices and the rapid adoption of electric vehicles in North America. Drilling will focus on expanding east-west strikes as resources dwindle. Our previous drilling campaign expanded the resource by striking at 900 meters and diving down to 600 meters.

Highlights

- North American EV sales reached 325,000 units in the first half of 2021, up 128% year-on-year from 142,000 units in the corresponding period 2020. Nearly 100% of vehicles sold in North America so far in 2021 were delivered with cobalt-bearing NCM and NCA lithium-ion batteries

- C$2.5 million budget will include 4,000 metres of drilling to test extensions to the deposit, which is currently open to the east, to the west and at depth, demonstrating excellent potential for resource growth

- The drill campaign follows successful meetings in Washington between executives from First Cobalt and senior elected officials, including the Idaho delegation to Congress, and civil servants from several departments and agencies

- Iron Creek is one of only two primary cobalt resource projects in the United States, where cobalt is considered a critical mineral due to America’s reliance on foreign supply of this strategic mineral

Source: First Cobalt Corp.

The company plans to drill an additional 4,000 meters and expect initial results by the end of the fourth quarter of 2021. The company also has a permit for a North American hydrometallurgical refinery, which is critical for the development and manufacture of batteries for electric vehicles.

The Iron Creek Cobalt Copper Project in Idaho, USA, is one of the only two advanced primary cobalt resource projects in the US located in the Idaho Cobalt Belt and is considered to be the largest unextracted cobalt resource in the United States. First Cobalt owns the Iron Creek Project and several major cobalt and silver properties at the Canadian cobalt deposit. Following successful results of a geophysical survey campaign, the company has identified several important targets within a 2 km radius of the project.

First Cobalt has also identified satellite targets near the project, including the Ruby Zone Cobalt-Copper Target Area, located approximately 1 km from the project. By May 2021, the company had doubled its position to approximately 1600 hectares, which, according to the project plan, covers approximately 10 km and harbour rock horizons with a high potential to find additional cobalt or copper resources.

In addition, metallurgical testing of the cobalt ore continues to improve the concentrations of the processing systems. The Company completed more than 30,000 meters of drilling in 2017 and 2019 before suspending exploration to focus on developing its refining business and supplying electric vehicle battery manufacturers. The mineral resource estimates outlined above for the company’s NI43-101 indicate a resource of 12.3 million pounds of cobalt and 2.9 million pounds of copper, and inferred resources of a further 12.7 million pounds of cobalt and 4.0 million pounds of copper.

In addition to drilling, exploration activities for First Cobalt Corp. (TSXV:FCC) include extensive rock sampling at the outcrops, a new road has been constructed to gain access to the drilling, and rock mapping has been completed on the West Fork property. Magnetic and geophysical soil surveys are planned for the Redcastle Property, in addition to a coverage of the ruby-cobalt-copper target east of the first cobalt deposit.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Rainbow Rare Earths (LON:RBW) together with K-Technologies have signed an agreement to use their separation method at the miner’s Phalaborwa rare earth project in South Africa.

K-Technologies is a Florida-based U.S. company that specializes in the development of chemical processing technologies. The technology that K-Tech has developed is an intellectually protected proprietary technology, which is used for the downstream separation of rare earth elements more efficiently and rapidly than traditional extraction techniques.

The agreement provides that Rainbow will be able to use the separation method in southern Africa for four years. Rainbow will pay a license fee of $5.5 million for each site where K-Tech’s technology is deployed.

Top of the Line

This new technology uses continuous ion exchange chromatography which helps the separation processing of useful elements with fewer steps in the process. This represents significant savings in time and money as it has lower operating costs compared to traditional technology.

George Bennett, CEO of Rainbow Rare Earths said that at Phalaborwa, the technology allows targeting rare earth oxides such as neodymium, praseodymium, dysprosium, and terbium. These elements together represent virtually the value of the entire basket of important rare earths.

Bennet said, “In addition to the anticipated capex and opex savings, when compared to a traditional separation circuit, the IP will enable Rainbow to participate efficiently in the downstream separation process, allowing us to capture the full rare earth oxide price for our material.”

Through this agreement, Rainbow will be able to efficiently participate in the procurement of today’s most valuable rare earth oxides.

Rainbow Rare Earths has also explored in Zimbabwe since last year primarily around the Gungwa deposit where it has been reported by the U.S. Geological Survey to host cerium and lanthanum.

According to the U.S. Geological Survey (USGS), the group of 17 minerals that are involved in high-tech electronics and military products are as common as copper. But they are known as rare earths because rare earth minerals oxidize quickly and their extraction is highly complex.

Two Key Projects

Rainbow Rare Earths is a mining company with two major projects in Africa. The Phalaborwa Project in South Africa and the Gakara project in Burundi, East Africa.

The Phalaborwa project represents an environmental opportunity and is distinct from other rare earth development projects because it has low levels of radioactive elements. The project is located on a brownfield site in a South African mining town and benefits from the availability of associated skilled labor. Phalaborwa is an excellent location for the project as it has strong rail connections, which facilitate the import, export, and transport of any specialized reagents.

In addition, the Phalaborwa project is fully Environmental Impact Assessment cleared. The planned processing of material at Phalaborwa brings major environmental benefits by depositing clean, benign gypsum suitable for use in the construction and fertilizer industries.

Rainbow’s strategy is to become a responsible producer of rare earth metals globally. Its primary rare earth focus is NdPr. This element is considered key component driving the global green technology revolution.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

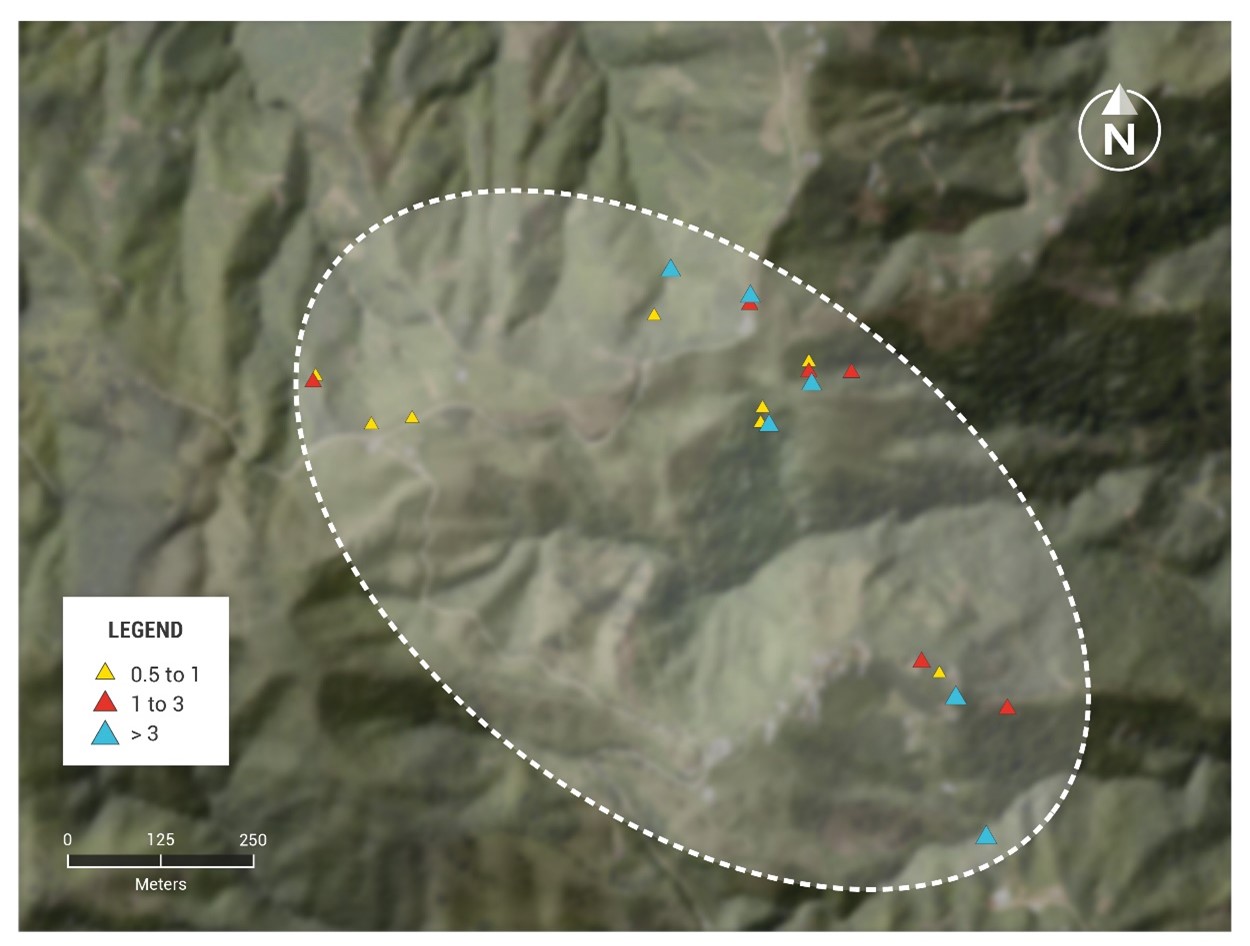

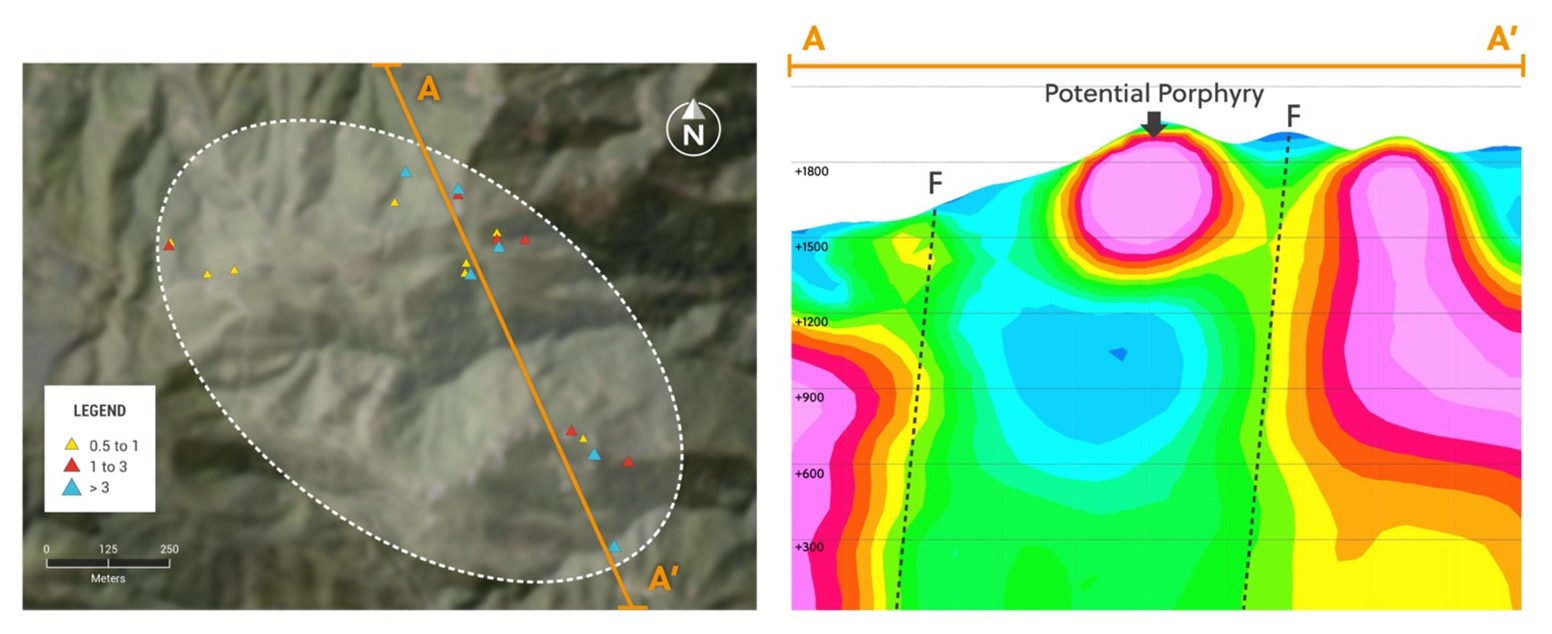

Collective Mining (TSXV:CNL) has provided an exploration update on its Victory target. Victory is the fifth major target identified by the company at its flagship project, Guayabales, in the Caldas area of Colombia. The project is located on a continuous strip northwest of the million-ounce deposit of Aris Gold’s Marmato mine. The Company has interpreted that the abundant precious metal mineralization encountered at the project is related to several mineralized styles, including gold, copper, and molybdenum porphyry associated with breccias, high-grade precious metals, and base metal loading systems, and superimposed enriched porphyry bodies. Victory is located to the north of the project and hosts fine-grained diorites showing porphyry alteration of potassium sericite.

Executive Chairman of Collective, Ari Sussman, commented on the update, “Victory is a target area with potential to yield a large, mineralized porphyry system and I congratulate the exploration team for their endeavours in a region with very limited outcrop exposure. Once the Induced Polarization (“IP”) survey is finished, we plan to model all the data and drill test this target in Q4, 2021. The Company has now outlined five targets with porphyry and high-grade vein potential within the Guayabales project in less than six months of exploration work. I am confident that our recently initiated maiden drilling program at the Guayabales project will yield significant discoveries in the near future.”

These veins are associated with widespread pyrite and occasional molybdenum and chalcopyrite. The late vein formation includes sphalerite and galenasulphides. Quartz and magnetite veins as well as stockwork sheets within the vein system have been identified and these veins set the trend for the NNW.

Rock fragments and soil anomalies at Victory were located near a magnetic anomaly outlined by magnetic inversion modeling and airborne magnetic data. The anomaly has a circular diameter and is about 500 meters long and extends to a depth of 900 meters below the surface. Clear structural corridors and deposits of the porphyry system were identified in the field and confirmed by magnetic anomaly modelling and aerial data.

Field work continues at Victory Target, with ARCE Geofisicos conducting an in-depth IP survey using its own AGDA technology. The study will generate 3D data of chargeability and resistance at a minimum vertical depth of 800 meters and is designed to search for common sulphide porphyry systems and resistive vein clusters within the floor. The highly anticipated NI 43-101 Technical Report on the Guayabales Project is approaching completion and is expected to be filed with SEDAR by September 2021.

Highlights (Table 1 and Figures 1-4)

- Victory is a coincidental robust gold, silver, copper and molybdenum soil anomaly with abundant high-grade gold rock chip samples overprinting a magnetic high anomaly.

- The Victory target is large, measuring 1,000 metres east-west by 600 metres north-south by at least 250 metres vertically (exposed outcrop over different elevations) and is open for expansion in all directions.

- 22 rock channel and chip samples returned values above 0.5 g/t gold over widths of 1 to 3 metres including 12 samples above 1 g/t gold and a maximum of 6 g/t gold. These samples were obtained from very small outcrop exposures in streams due to Victory being 95% covered by colluvium and landslides. Gold mineralization is related to porphyry veinlets (A, B and Magnetite veins), hydrothermal breccia and a late polymetallic vein overprint with results as follows:

Table 1 Rock and channel sampling at the Victory Target

| Sample ID | Length (m) | Au g/t | Ag g/t |

| CM002422 | 1.5 | 6.0 | 14 |

| CM000161 | 1.0 | 5.0 | 5 |

| CM000182 | * | 4.1 | 10 |

| CM002136 | 2.0 | 3.7 | 7 |

| CM000279 | 1.0 | 3.3 | 3 |

| CM001052 | * | 3.0 | 5 |

| CM000204 | * | 2.6 | 5 |

| CM002218 | 2.0 | 1.9 | 1 |

| CM000243 | 1.0 | 1.8 | 6 |

| CM000159 | 2.0 | 1.6 | 1 |

| CM000278 | 0.0 | 1.4 | 2 |

| CM002419 | 1.7 | 1.1 | 1 |

| CM001014 | * | 0.8 | 4 |

| CM000203 | * | 0.8 | 2 |

| CM000240 | 1.0 | 0.8 | 4 |

| CM002415 | 1.3 | 0.7 | 1 |

| CM002138 | 2.0 | 0.7 | 1 |

| CM000174 | 0.8 | 0.6 | 14 |

| CM002203 | 0.5 | 0.6 | 19 |

| CM000245 | 3.0 | 0.6 | 2 |

| CM002137 | 0.7 | 0.6 | 2 |

| CM002199 | 0.6 | 0.5 | 2 |

| *Grab sample |

An initial drilling program is currently being planned for Victory as part of the Company’s maiden 7,500 metres program currently under way at the Donut target. Drilling at Victory is expected to commence in Q4, 2021.

Source: Collective Mining

Figure 1: Plan View of the Guayabales Project and the Victory Target

Figure 2: Plan View of the Victory Target Area

Figure 3 (1&2): Magnetic Inversion Section and Plan View Across the Victory Target

Figure 4 (1-4): Victory: Porphyry Style Mineralization in Outcrop Samples

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Ecuador expects to start production of four major mining projects by the end of President Guillermo Lasso’s first term in office in 2025, as he seeks to diversify the economy beyond oil exports, the Ministry of Natural Resources said on Friday. Lasso has been trying to attract private investment to boost the economy, which was in a deep recession last year, exacerbating Ecuador’s cash-strapped economy.

To do so, the President has issued a new decree, paving the way for investment in the nation and mining projects. This has the potential to open the floodgates for miners looking to expand or begin mining in the mineral-rich country.

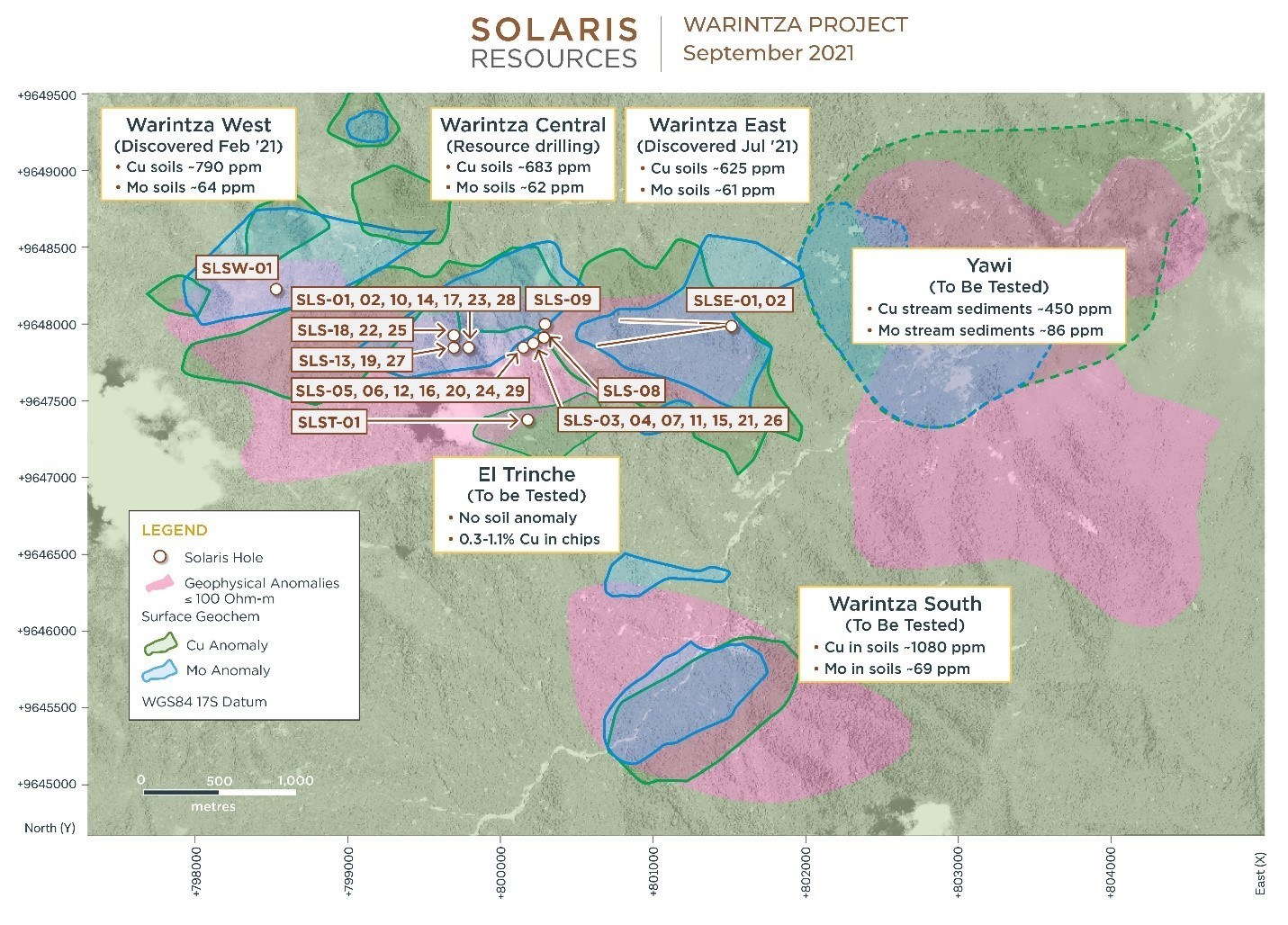

Ecuador has rich mineral resources but lags behind its Andean neighbors Peru and Chile in the development of large mines. Many large mining projects in Ecuador face resistance from local communities and are struggling to fill informal miners who have slowed their development. However, the right approach with consultation with local communities has proven to be extremely effective. Successful projects like Solaris Resources’ (TSX:SLS) Warintza Project have been proven to be some of the most promising copper projects in the entire Andean region, and have been models of how mining companies can work hand in hand with local communities to uphold critical ESG principles.

Three gold concessions of Canadian companies Dundee Precious Metals (TSX:DPM) in Loma Largo, Atico Mining Corp (TSXV:ATY) in Plata, and Adventus Mining Corp (TSXV:ADZN) in Curipamba are in advanced exploration phase and could begin production by 2023, the Department of Energy, Non-Renewable Energy and Natural Resources said in its statement. The Cascabel concession, operated by Australia’s SolGold Plc, is expected to start copper production by 2025, the ministry added.

The largest copper mine in South America, the Mirador Project, operated by a subsidiary of the Chinese consortium CRCC Tongguan, commenced production in mid-2019. Its first major gold mine, the Canadian Lundin Gold Inc.’s (TSX:LUN) Fruta del Norte mine project, started in November this year. Its authorities expect exports of mineral resources to reach $1.6 billion a year, an increase of 7.4% from 2020.

With Ecuador positioning itself as a nation of open arms for the mining industry, it is set to catch up to, and surpass its neighbours in the coming years and decades.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

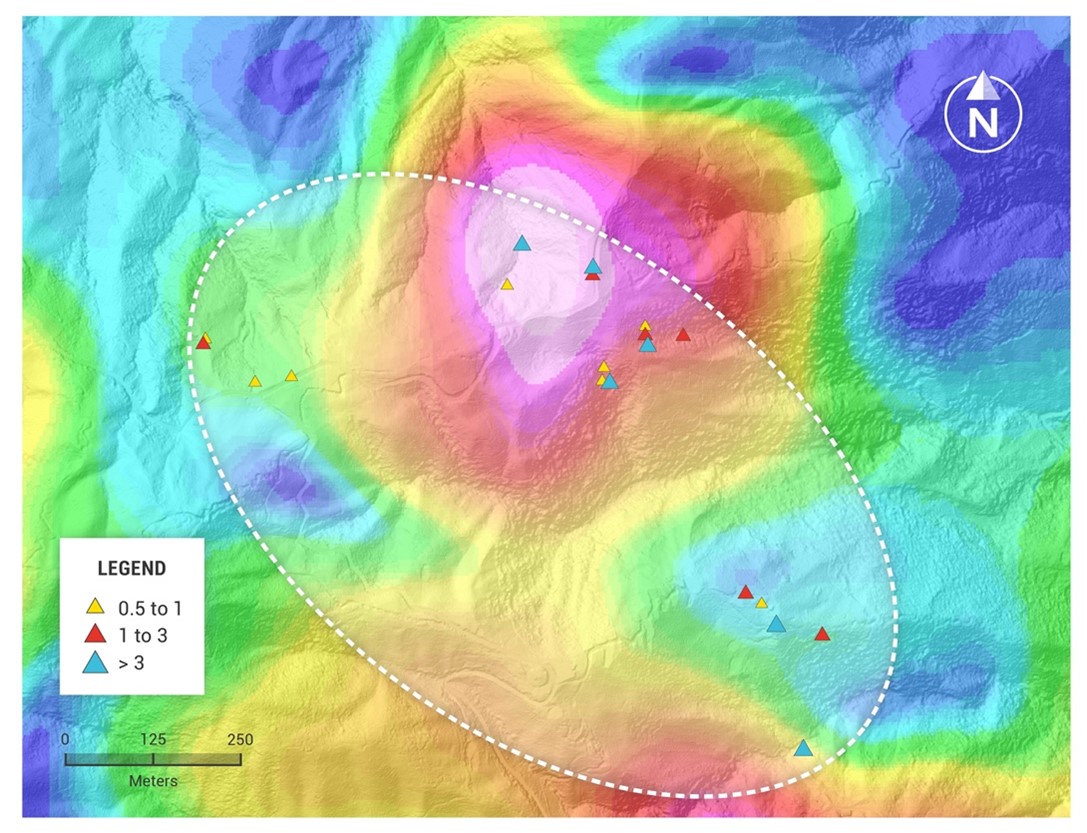

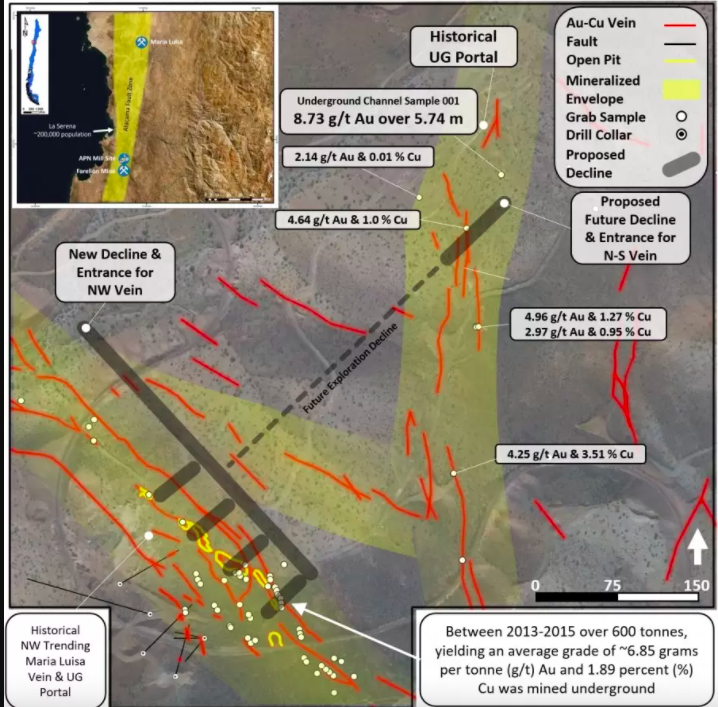

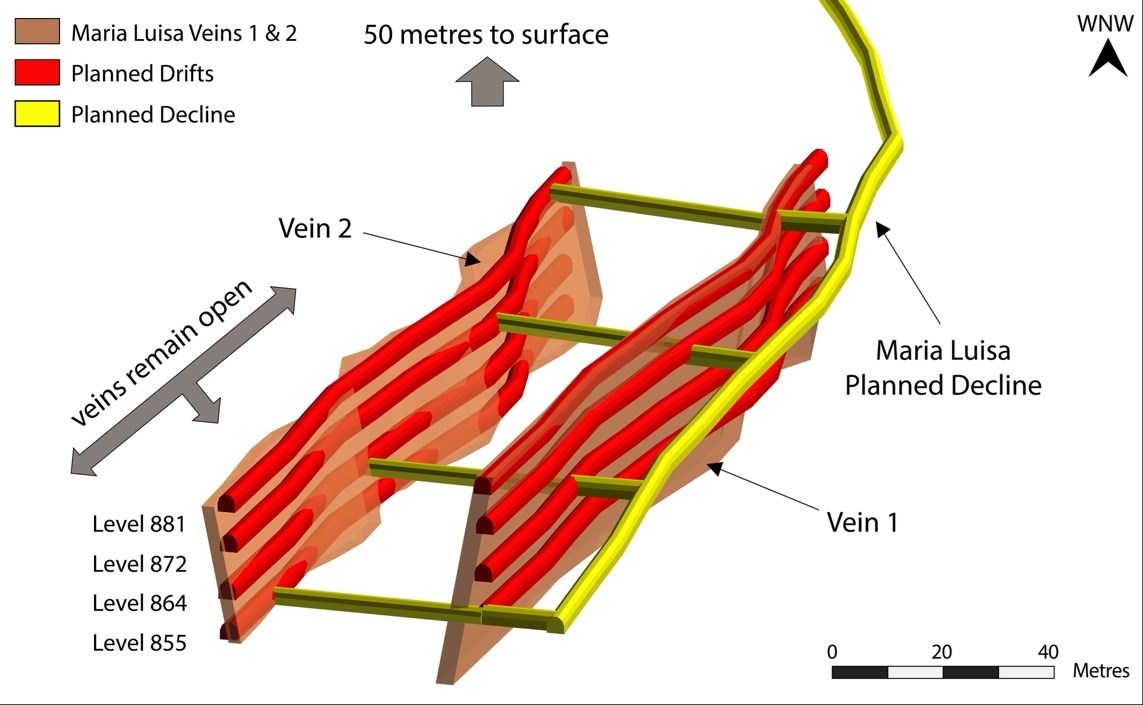

Altiplano Metals Inc. (TSXV:APN) is proud to announce that the mining application has been approved by the Chilean Mining Authority (Servicio Nacional de Geologia y Mineria) for the historic Maria Luisa Gold-Copper Mine . The permit gives Altiplano permission to commence underground exploration and development of the mine.

The project, known as the “Maria Luisa Mine,” is located in the Atacama region, about 100 km south of La Serena, Incahuasi, Chile. Altiplano (TSXV:APN)plans to establish an underground waste system designed to reach mineralized veins through multiple access points at various levels with this permit.

Design and Development

The design process involves access to the northwest and southeast mineralized Au and Cu veins by intersecting four separate levels designed to create 8 mining areas (Figure 2). The initial decay system will penetrate into the southwest corner of the property and advance 350 meters southeast to intersect mineralized zones within historical mining areas.

The development work will be led by surface and underground drilling programs to support future grade control. The Company intends to mine approximately 3,000 tonnes of mineralized gold and copper material at this stage, with future opportunities to expand to 5,000 tonnes.

Construction is expected to take approximately 6 months and Phase 1 funding is estimated at approximately $600,000. During the construction and development phases, the company will have the opportunity to extract mineralized bulk samples from Au and Cu, which will be sold to a nearby processing plant to offset the development costs before full capital improvements. The Company is in the process of completing the review process to select a contracted miner to build and/or develop the project. The review process is expected to be completed in the next few weeks and work will begin.

Altiplano (TSXV:APN) is a Canadian mining company focusing on the acquisition and development of short-term cash flow assets and exploration projects of considerable size. The aim of Companys is to grow into a medium-sized producer of copper, gold and silver, with an immediate plan to generate profits from three cash flow projects by 2021.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Teck Resources Ltd. (NYSE:TECK) is exploring options for its metallurgical coal business including a sale or spin-off that could mark the unit up to $8 billion, sources with knowledge of the matter said. Teck is working with consultants to explore strategic alternatives for the coal block, insiders said to Bloomberg News, citing confidential information.

Teck isn’t the only company to reconsider its assets. Major commodity producers are under increasing pressure to reduce fossil fuels in response to investor concerns about climate change. BHP Group (ASX:BHP) recently agreed to sell its oil and gas assets to Australian company Woodside Petroleum Ltd last month and is attempting to exit the coal business.

This is a recurring and growing trend in the industry as coal mining falls out of favour for the critical tech and other metals needed for a carbon-neutral economy. Copper, aluminum, lithium, nickel, and cobalt are some of the preferred business units that are seeing investment from mining companies.

Each of them is critical to the battery supply chain, electric vehicle (EV) manufacturing, or energy industries and will be required in massive amounts. This is also driving the need for clean steel and other metals while simultaneously reducing the size of coal divisions.

Anglo American PLC (LSE:AAL) produced more than 21 million tonnes of steel coal last year at four sites in western Canada. The company spun off its South African coal division in a separate IPO in June. Consultations are still at an early stage and the company has yet to decide whether to retain the South African unit, it said.

Anglo American accounted for about 35% of gross profit before depreciation and amortization in 2020, according to its website. An exit from coal would free up resources for Anglo American (LSE:AAL) to accelerate its plans for commodities like copper for which demand is accelerating on the powerful tailwind of a coming electrified global economy.

Metallurgical coal, a key raw material for steel production, remains one of the world’s most polluting industries and is under considerable pressure from policymakers to clean up their act. China, the world’s largest metal producer, has even hinted at curbing steel production to reduce carbon emissions. Still, metallurgical coal prices have continued to rise this year as investors fuel steel demand on a global economic recovery and sustained needs as the transition to cleaner sources continues.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Precious metal miner Sibanye-Stillwater (NYSE:SBSW) has bought a 50% stake in the pioneer Ltd. Rhyolite Ridge mine in Nevada. The lithium-boron project has the potential to become the largest lithium mine in the US, according to Sibanye’s CEO.

This is Sibanyes’ third investment this year, after Eramet acquired a 30% stake in the Cone Lithium mine in Finland and Eramet’s purchase of a nickel processing plant in Normandy. The deal, one of the largest lithium deals in the US, and comes amid growing concerns about more investment as demand for the metal outstrips supply and efforts to combat climate change could be delayed. The companies say they will form a joint venture to develop Rhyolite Ridge lithium mine 355 km north of Las Vegas.

ioneer will remain the operator of the project, leveraging Sibanye’s (NYSE:SBSW) experience as the world’s largest platinum group metals (PGM) miner to develop the project. Silbanye-Stillwater has agreed to underwrite a strategic placement of new common shares of Ioneer for $70 million, representing 7.1% of the share capital after the placement.

The miner said it had already begun securing debt financing to finance the remainder of the $850 million project. According to the company, the full funding and necessary permits are expected by the end of next year and the project is expected to start by the end of 2024. This would bring a critical project online at just the right moment with rising prices and a lack of supply converging into some of the most favourable conditions for lithium miners in history.

Sibanye-Stillwater chief executive Neal Froneman, commented: “Rhyolite Ridge is a world-class lithium project and we recognize its strategic value, with the potential to become the largest lithium mine in the US,”

Perfect Timing

Once operational, the Nevada mine is expected to produce 2,200 tons of lithium hydroxide, which is used in most Tesla batteries and will fuel the electric vehicle boom for other automakers as well.

Auto giants such a Volkswagen Group, Toyota, Mercedes-Benz, and BMW all have plans to develop their electric vehicle lines further. The need for high-density batteries is one of the critical points of concern for the supply chain, and miners will be a large part of stabilizing supply.

The deal also includes the rights for ioneer to expand operations at nearby lithium deposits, in which case the company has the option to pay an additional $50 million to secure a 50% interest in the project. The project is at an advanced stage and is the largest and most durable lithium project near Tesla’s Gigafactory in the nearby Port of California. The proximity of the project to the Gigafactory and the battery production facilities housed there is a good setup for simple infrastructure and distribution in the future.

The proposed mine is intended to boost local lithium supplies to U.S. automakers and battery manufacturers. In June, ioneer signed an agreement to supply lithium carbonate units to South Korean battery manufacturer Ecopro. This is likely to be just the tip of the iceberg for the sector as it is heating up quickly with new deals announced regularly and M&A a pivotal part of many lithium miners’ strategies.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

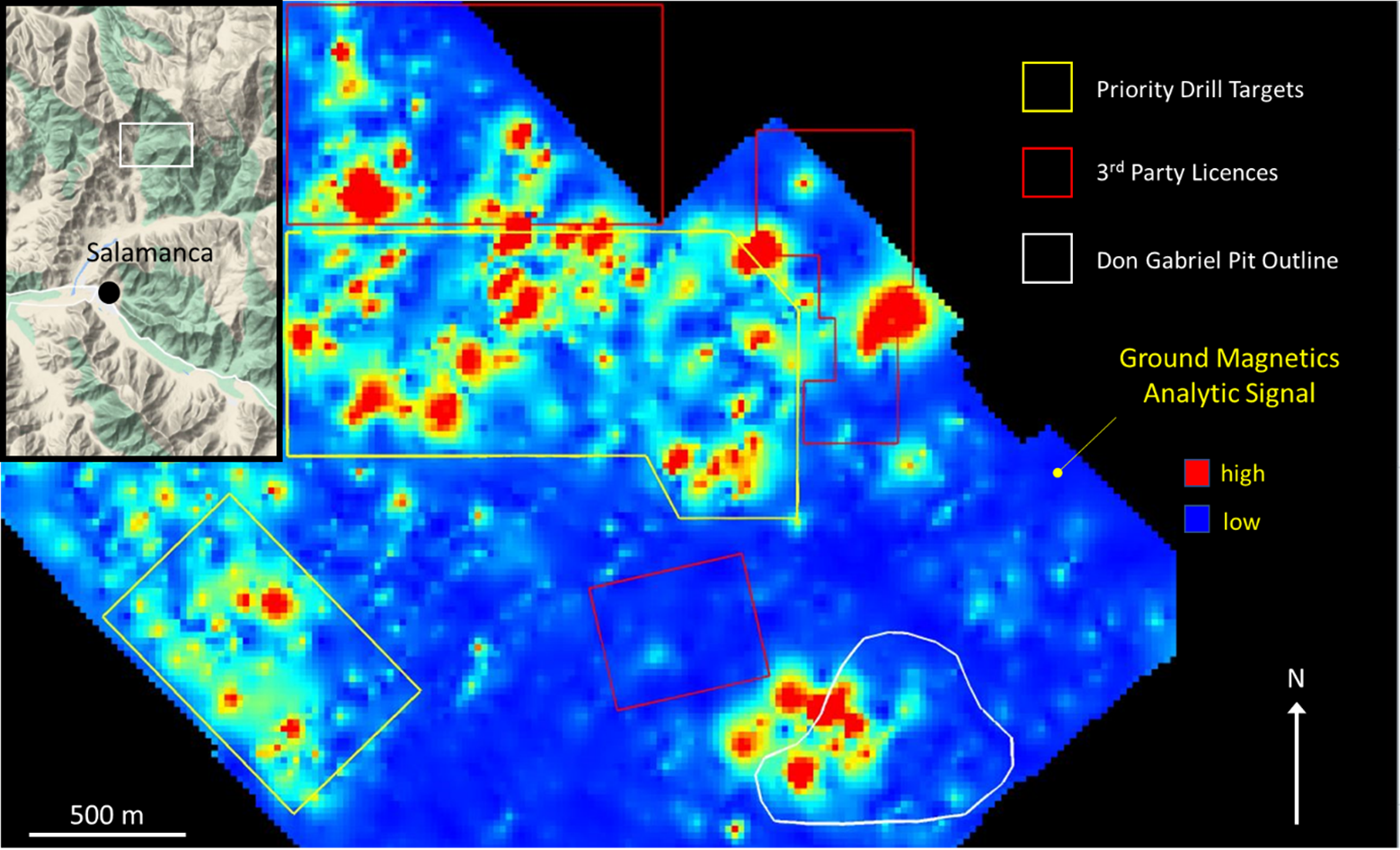

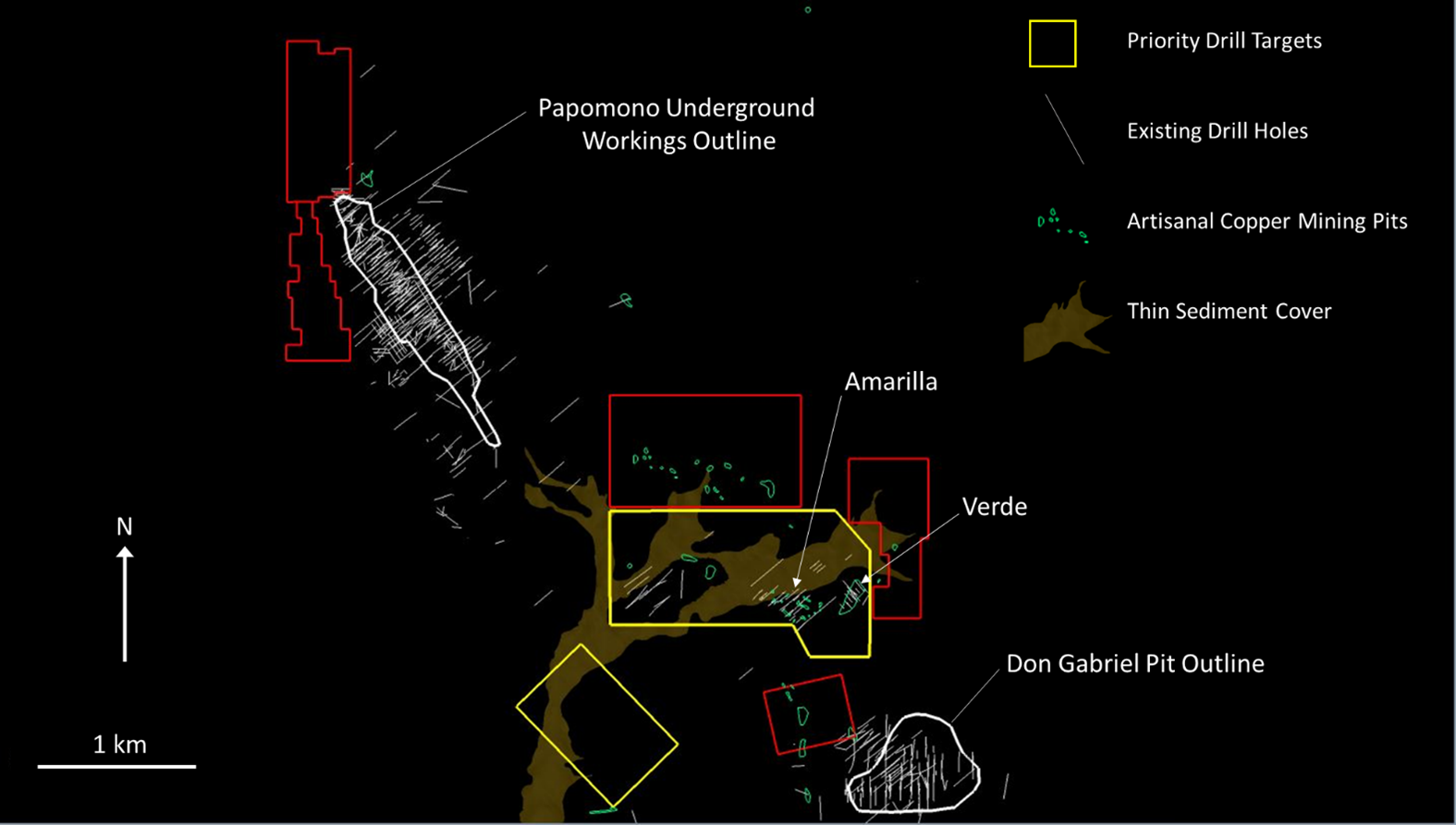

Three Valley Copper (TSXV:TVC) announced this morning the start of its near mine exploration drilling program at its Minera Tres Valles project in the Salamanca region of Coquimbo, Chile. A geophysical survey of the area was conducted by Zonge Ingenieria y Geofisica Chile (SA) under the previous ownership of Compania Minera Latino Americano (LTDA), a subsidiary of Vale, in 2005. This information was used by the exploration team to plan the 2021 exploration program at the property, including geophysical, magnetic, and IP chargeability anomalies and similarity anomalies related to the Papomono and Don Gabriel mines.

Kickoff

The commencement of the exploration drilling program marks the beginning of a critical prong of Three Valley Copper’s business model. As a company exploring, developing, and producing copper, Three Valley is in a unique position to unlock the value of the assets it explores. Minera Tres Valles could be one of those assets.

Michael Staresinic, President and CEO of Three Valley Copper (TSXV:TVC) had this to say about the news: “Since Vale first staked the property and found our two deposits named Don Gabriel and Papomono in 2005/2006, little further exploration has been performed on the property.

“A majority of Vale’s 170,000 meters of diamond drilling was focused on defining these two deposits. Multiple targets were identified elsewhere on the 46,000-hectare land package although detailed follow-up was postponed while delineation of Don Gabriel and Papomono was prioritized.

“Our drill program will test high-potential copper targets located between Don Gabriel and Papomono, which sit approximately 3 kilometers apart. This initial area of focus represents less than 5 square kilometers or approximately 1% of our land package. We believe this is an excellent opportunity to identify new near-surface copper occurrences close to our existing mines and mineral processing plant.”

The Site

The Papomono and Don Gabriel mines are TVC’s two main ore sources but the exploration campaign looks to explore areas where two of the largest and longest third-party miners on the property operate, containing oxide-rich capsthat MTV facilities develop and process. It is also noteworthy that between the Papomono and Don Gabriel mine where Verde is located, there is a collection of artisanal pits. MTV believes similar geophysical features of the District and maps of similar copper mineralized rocks will help determine drilling targets for the upcoming program.

The possibility of being part of a larger mineralized system is consistent with available geophysical soil data. The initial drilling is expected to be between 6,000 and 8,000 meters, with a budget of $2.5 million for the drilling. Drilling will be carried out with existing surface infrastructure and current environmental approvals. The exploration team will evaluate the results of the new drill holes as they become available and incorporate them into a dynamic design and management program.

Mining, The Right Way

Minera Tres Valles is also a symbol of what Three Valley Copper (TSXV:TVC) is aiming for. The mine received visitors from the surrounding communities at the site for a demonstration of an in-situ controlled blasting event. The purpose of the event was to teach the protocols required by the regulatory authorities to the community representatives and show correct compliance with regulations. Now, TVC will put its ESG plan into action with the drill program.

The company produces Electrolytic Copper Cathodes (Grade A) of 99.99% purity. That copper is often used in electric equipment like technology, battery parts, and the copper can easily be drawn and formed into wires.

With the current focus on global decarbonization efforts, this particular type of copper is seeing massive demand growth. Electrolytic copper undergoes refining or purification through the process of electrolysis. That purification is by far the simplest method of achieving purity levels 99.99% in copper and makes Three Valley Copper’s product particularly valuable in a world that is rapidly going electric.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

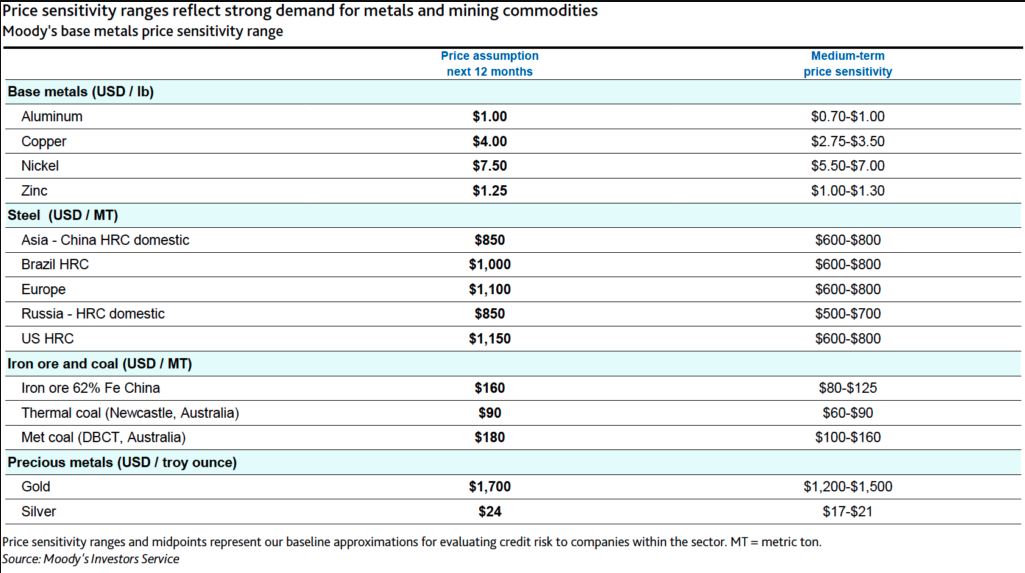

The outlook for the global metal mining industry has changed from positive to stable, with a new report from Moody’s Investors Service concluding that while most metal prices surpass historical highs, this does not mean that they will improve from current levels. Moody’s predicts in the report that most prices will pass historic highs.

The company also sees signs that most commodity prices will remain stable through 2022, reaching historic highs later this year. However, peaks above current price levels are expected to fade while the expected higher aggregate demand for metals and mining is still expected to increase over this period.

The Green Metals

Aluminum prices are expected to remain elevated until at least mid-2022. Aluminum prices will continue to rise in early 2022, after surpassing $2,600 a tonne, or $118 a pound, in mid-2101, the highest level in more than a decade. Copper prices are expected to remain strong relative to historical averages until at least the end of 2022, as long-term structural deficits will keep copper prices high.

Moody’s sees copper prices in the third quarter in the $250 to $300 a pound range compared with the start of the year before the devastating March 2020 pandemic affected many of the world’s economies.

Efforts by governments and industries to reduce carbon emissions have benefited copper production, but copper supply is struggling to keep pace with demand in certain regions, including Chile. Copper prices have remained above $400 a pound since February, after demand rebounded from a peak above $500 a pound and an early retreat when China risked a COVID-19 delta variant that could slow its production and copper imports.

Nickel in the Driver’s Seat

Global industrial activity remains strong, with manufacturing purchasing manager indices above 60% in the US and Europe and above 50% in China. If production recovers to pre-pandemic levels, nickel will be abundant. Moody’s believes that high nickel prices in the first half of 2021 will not be sustainable in 2022 and will remain high at least until the beginning of the year.

Analysts also point out that the supply of nickel pig iron (NPI), an inferior ferronickel that is a cheaper alternative to pure nickel for stainless steel production, will continue to increase as additional plants boost activity in Indonesia. The rise in NPI should offset reduced production in China, which is facing lower ore availability and rising ore prices.

Heavy Metal

While production at the large zinc mines in Peru, Mexico, Bolivia, and other countries is recovering, the global zinc market is shifting from deficit to surplus. This prompted Fitch Solutions to publish a report stating that the global zinc production will grow at the fastest rate of 4.3% between 2012 and 2021 as the disruption caused by COVID-19 subsides. Due to strong demand in the steel sector and reduced zinc production in China, prices will continue to rise in the second half of 2021. Zinc prices will show strength until mid–2021, but in the long run, they will fall to the lower end of the price range as long-term output growth outstrips lower demand growth.

According to Moody’s, prices will retreat from their peak this year as supply increases and demand growth slows. Coal prices are expected to remain high despite easing supply problems as geopolitical disputes ease.

Iron ore prices are likely to return to their average level of $70-80 a tonne between 2016-2019 and 2022. The tight iron ore supply is likely to keep prices below their historic norm in 2022.

Moody’s expects market uncertainty, low real interest rates, and inflation in 2022 to keep gold prices near historic levels and predicts that prices will fall below $1,800 an ounce by the third quarter of the year owing to an ongoing economic recovery, a strong US dollar, and a gradual increase in earnings. Global supply and demand imbalances in steel will return in 2022 and prices will fall to their historical average after unusual highs earlier this year.

What happens next will remain to be seen as investors hold on for the ride of their lives on what has so far been a commodity price rocket ship.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

With funding closed and planning completed, Collective Mining (TSXV:CNL) has announced this morning that its maiden 7,500 metre diamond drilling program is not underway at its Guayabales Project. The project, located immediately along strike and northwest of Aris Gold’s Marmato gold mine, is the company’s flagship project in the country.

After encountering abundant precious metal mineralization throughout the property during exploration, Collective moved quickly to begin the drill program. This includes identifying the five unique grassroots targets at Guayabales which include Donut, Box, Olympus, Victory, and ME. The five targets make up this 7,500 metre maiden drilling program which has now begun.

The program will consist of short, fanned holes measuring up to 300 metres from a single drill pad. The pad will cover various depths beneath the shallow underground workings to define the potential grade and extent of the mineralized system. Some drilling has already been completed, and the visual observation of that drilling has intersected porphyry breccia with a pyrite matrix overprinted by a quartz-carbonate-sphalerite vein stockwork associated with intense sericite alternation over intersection lengths of up to 250 metres.

Donut is of particular interest to Collective and remains a first priority for the program. It has been traced along strike and to the west for at least 600 metres and is open in all directions. To test the strike extent of the target, the company will construct additional drill pads.

Ari Sussman, Executive Chairman of Collective Mining, commented on the news: “The commencement of drilling activities within the Guayabales project represents another important and exciting milestone in the Company’s evolution from early-stage explorer to outlining multiple large, continuous and mineralized porphyry, breccia, and high-grade vein systems. In total, we now have five distinct targets defined for first-pass drill testing over the next six months with more to come as we continue to explore and evaluate our highly prospective land package.”

As an exploration and development company working to identify and explore prospective gold projects in South America, this is Collective’s kickoff drill program that will begin the road ahead to discovery. The stock has remained steady since its IPO, and now investors will be looking to results from this maiden drill program for further guidance.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

A US House committee voted to include the language in a broader budget reconciliation package that would prevent Rio Tinto Ltd from building its Resolution copper mine in Arizona. Elected officials in nearby Superior, Arizona, have said the mine is crucial to the region’s economy. The tribe of San Carlos Apaches and other Indians say the mine would destroy the sacred land where they hold religious ceremonies. Conflict has stalled a decision until now, but the committee’s vote finalizes the language that will determine the future of the mine.

The House Natural Resources Committee on Thursday passed the Save Oak Flat Act, a $3.5 trillion compensation measure. Should the House reverse the move, the measure faces an uncertain fate in the US Senate. Approval of the measure would reverse a 2014 decision by former President Barack Obama that Congress began a complex process to hand over more than 40 billion pounds of copper owned by Rio Tinto in exchange for acreage Rio owns nearby. Former President Donald Trump gave final approval to the process before leaving office in January, but his successor Joe Biden could reverse it and leave the project in limbo.

A final reconciliation budget should also include funds for solar, wind, and other renewable energy projects that require tremendous amounts of copper. Electric vehicles consume much of the metal, as do internal combustion engines. The Resolution mine would cover about 25% of the demand for U.S. copper.

Mayor Mila Besich, a Democrat, said the project appeared stuck in “bureaucratic purgatory”. She hopes the House will not allow the language to remain in the final bill. The move “seems contradictory to what the Biden administration is trying to do to address climate change”, Besich said.

Rio said it would continue consultations with local communities and tribes. Rio Tinto chief executive Jakob Stausholm plans to visit Arizona later this year.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

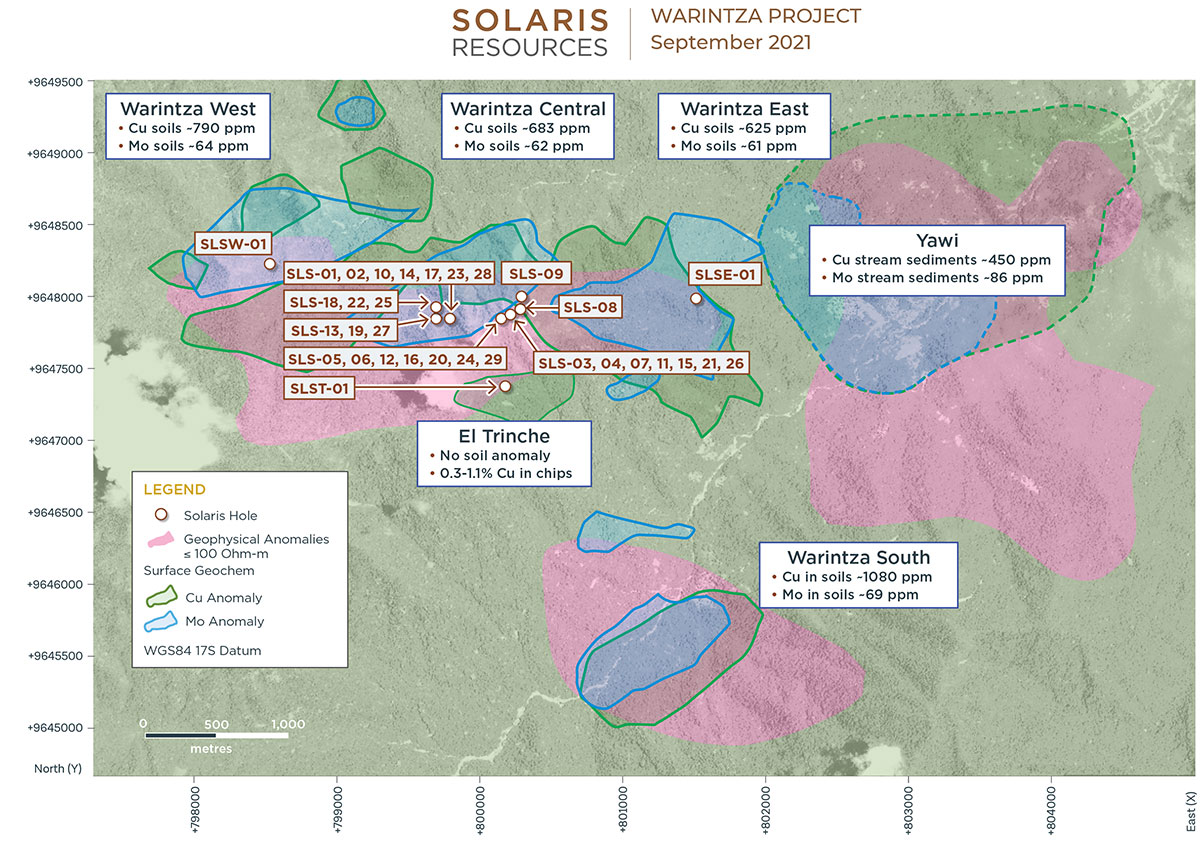

Solaris Resources has just announced its latest assay results from ongoing resource expansion drilling at its Warintza Project in southeastern Ecuador.

Mr. Jorge Fierro, Vice President, Exploration, commented “Drilling at Warintza Central continues to expand the dimensions of the zone beyond its original footprint. The strike length of Central now measures over 1,250m, with ongoing drilling aiming to extend the zone further to the east, broaden the zone to the north, and test the potential for a southern extension of at least 500m at El Trinche. At the same time, we await additional assays for our recent Warintza East discovery, where we have just added a second rig to accelerate drilling.”

The highlights from the results are as follows:

- Three additional holes at Warintza Central have unfilled gaps within the drilling pattern and extended the envelope of high-grade mineralization to the east, with high-grade mineralization encountered in all holes starting at or near the surface.

- SLS-27 was collared in the southwestern part of Warintza Central and drilled into a partially-open volume to the northeast, returning 462m of 0.91% CuEq¹ from near surface, including 372m of 1.02% CuEq¹ from 36m depth, infilling and extending mineralization in this area.