Trillium Gold Mines Inc. (TSXV:TGM), a gold mining company focused on acquisition, exploration, and development at the Red Lake Mining District of Northern Ontario, has been busy in 2021.

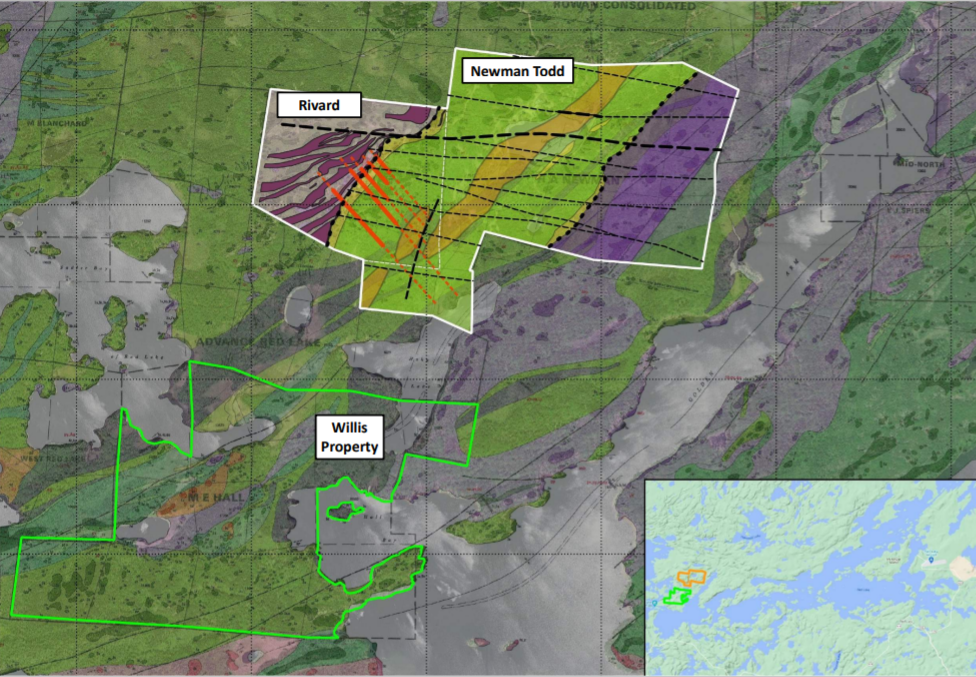

Trillium has assembled the largest prospective land package in and around the Red Lake mining district in Northern Ontario. Red Lake has many major mines and deposits, and the greenstone belts of Confederation Lake and Birch-Uchi. The company is advancing drill programs at multiple properties including Willis, Newman Todd, a significant portion of the Confederation Lake Greenstone Belt, and properties in Larder Lake, Ontario, and Matagami and Chibougamou areas of Quebec.

New Results Continue to Pour In

The company announced on September 8 that the majority of assays from drilling at the Newman Todd Complex had been received, with assay reporting over two months. The company was able to process and summarize samples representing 6,708 metres across 15 drill holes at the property.

The Rivard and Newman Todd properties were explored in isolation and not systematically drilled for an integrated structural understanding.

Highlights

| Newman Todd | ||

| NT21-185: | 17.6m @ 1.35 g/t Au | |

| 13.2m @ 1.24 g/t Au incl. 0.5m @ 20.5 g/t Au | ||

| NT21-187: | 6.97m @ 7.5 g/t Au incl. 1m @ 45.9 g/t Au | |

| 4.75m @ 4.95 g/t Au incl. 0.65m @ 33.88 g/t Au and 0.35m @ 54.7 g/t Au | ||

| 6.2m @ 5.4 g/t Au incl. 0.3m @ 61.9 g/t Au | ||

| NT21-188: | 52.3m @ 1.07 g/t Au incl. 0.7m @ 11.5 g/t Au | |

| NT21-190: | 3.3m @ 8.06 g/t Au incl. 0.4m @ 61.9 g/t Au | |

| NT21-192: | 21.3m @ 3.55 g/t Au incl. 4.3m @ 13.8 g/t Au (includes 1m @ 35.15 g/t Au) | |

| Rivard | ||

| RV21-31: 0.3m @ 28.0 g/t Au | ||

| RV21-32: 0.3m @ 15.9 g/t Au | ||

| RV21-33: 0.7m @ 54.49 g/t Au incl. 0.4m @ 95.3 g/t Au | ||

| RV21-34: 2.2m @ 25.23 g/t Au incl. 0.3m @ 116 g/t Au and 0.3m @ 67.7 g/t Au | ||

Source: Trillium Gold Mines

Expanding the Property Portfolio

Trillium Gold (TSXV:TGM) also announced on October 26 that it had closed the acquisition of the of the Willis Property. Willis consists of thirteen patented mineral claim totalling 229 hectares. The company now holds a 100% interest in the Willis property, which is subject to a 2% net smelter returns royalty, half of which Trillium Gold has retained the right to repurchase for $1.2 million. If the holders of the royalty decide to sell the royalty in the future, Trillium also holds the right of first refusal.

MiningFeeds will begin covering news and insights from Trillium Gold (TSXV:TGM) as it continues to advance its drill programs in some of the best gold mining districts in the world, in one of the best mining jurisdictions in the world, Canada.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Three Valley Copper (TSXV:TVC) has announced its financial results for the three months and nine and months periods ended on September 30, 2021. As the company has closed its bought deal financing and looks to explore its huge property in Chile, the company is moving quickly in multiple areas of the business.

The multi-pronged approach to the project includes increasing copper production and furthering exploration of the property. The Minera Tres Valles property is 91.1% owned by Three Valley Copper, and is located in Salamanca, Chile. The property consists of 46,000 hectares of exploratory lands, of which 95% are still unexplored. The company’s position as a producer of 99.99% copper cathodes and an explorer of this large property puts it in a unique position in a copper market that is contnually clamoring for more.

Michael Staresinic, President and Chief Executive Officer of Three Valley Copper (TSXV:TVC), commented in a press release: “This past quarter showed a marked improvement with our flagship project, the construction and development of our underground mine, Papomono. Since the renegotiation of this contract in August, the contractor has performed much better than we previously experienced with multi 200-meter month advancements. We are approaching 90% completion of the required meters to begin producing and expect our first caving of ore to begin in January 2022.”

“As we continued our assessment of Papomono during the quarter given its paramount importance to the Company, it was concluded that to further ensure its successful ramp-up during 2022 and maximize its economic benefit, we decided to bring forward sustaining capital expenditures originally planned for later years to 2022. This decision came at a time when our open pit operations at Don Gabriel continued its underperformance delivering less ore at a lower grade that will lead to cathode production at the lower end of our 2021 revised guidance. The Company’s original plan for 2021 included reinvesting the cash flows delivered by Don Gabriel to fund development of Papomono but unfortunately, this has not happened and we foresaw near-term capital stresses to the business. Our announced strategic review in October was, in part, to help address this and quickly led to a required near-term financing raising gross proceeds of C$18.2 million.”

“With this financing we eliminated the short-term liquidity issue that was on the horizon allowing us to continue completing Papomono in January 2022 and increasing production in 2022. The completion of Papomono continues to be our focus and any deviation or delay would be value destructive to stakeholders. Our senior lenders agreed with us and as a condition of the financing, continued their strong partnership by agreeing to forbear on the debt repayments due in the first three quarters of 2022 while we together continue to renegotiate new repayment terms of the senior debt facility.”

“This new capital also allows the strategic review process to move forward without undue pressure. This new capital secures a better future for the MTV project and assists the strategic review process underway which ultimately we believe will increase shareholder value.

“Our exploration program continues and with over 46,000 hectares available to explore with highly prospective exploration targets including the 100 outcrop copper occurrences identified and 170,000 meters of diamond drilling performed by previous owners, we expect to provide preliminary results from this campaign in the first half of 2022. We hope this is the beginning of a multi-year exploration program and expansion of the copper resources contained in our land tenure.

“We are very proud of our health and safety record with every health and safety statistic reporting below the country averages and specific to COVID-19, our initiated on-site vaccination program has resulted in approximately 94% of the workforce receiving both doses of the vaccine and nearly 100% of the workforce has opted to participate. We have already begun a booster shot program to supplement this.

“Much has been accomplished by the team in Chile during 2021 through a restart of mining operations all complicated by the complexities of COVID-19. The copper price has remained above $4 per pound for almost all of 2021 and we see this level of support continuing. And the longer this trend continues, the more capital and attention the industry will attract. Three Valley Copper will not be overlooked. TVC is uniquely positioned among junior copper companies to take advantage of this coming cycle – fully built infrastructure, producing operations with defined deposits and, a rich land package in a very good neighborhood.”

Highlights from the press release are as follows:

Corporate

- The Company, through its indirectly held subsidiary (SRH Chile SpA), subscribed for additional common shares of MTV for approximately $1.0 million, resulting in the Company’s indirect holding of MTV increasing from 90.3% to 91.1% effective August 16, 2021.

- On October 4, 2021, the Company delivered to the minority shareholder of MTV (the “Minority Shareholder“) the required written notice of its intention to acquire the remaining interest in MTV held by the Minority Shareholder as per the call option notice requirements of the MTV shareholders’ agreement.

- On October 20, 2021, the Company engaged an independent financial advisor to review and evaluate potential alternatives that may further maximize value for the shareholders of the Company. These alternatives may include, inter alia, potential mergers, strategic partnerships, acquisition or dispositions of assets and/or refinancing or amending terms of the Company’s long-term debt.

- On November 25, 2021, the Company successfully closed a bought-deal offering (the “Bought-Deal Financing“) and issued a total of 56,681,000 units (the “Units”) and 819,000 additional common share purchase warrants (each, an “Additional

Warrant”) at an offering price of CAD$0.32 per Unit, for gross proceeds of CAD$18.2 million. Each Unit consists of one common share in the capital of the Company and one common share purchase warrant (each a “Warrant”). Each Additional Warrant and each Warrant is exercisable into one common share of the Company at an exercise price of CAD$0.45 for a period of 30 months from the closing of the Bought-Deal Financing. - Prior to closing the Bought-Deal Financing, the Company and its subsidiaries executed an undertaking agreement (the “Undertaking”) with the MTV senior secured lenders (the “Lenders“) to amend the loan repayment terms of the secured prepayment facility entered into with the Lenders and amended as part of MTV’s Judicial Reorganization Agreement (the “Amended Facility“). The Company and the Lenders have undertaken to execute a binding agreement to amend the loan repayment terms of the Amended Facility on or prior to September 30, 2022. Under the terms of the Undertaking the Lenders have agreed not to accelerate or enforce their rights or remedies under the Amended Facility should MTV fail to (i) make scheduled loan repayments on March 31, 2022, June 30, 2022 and September 30, 2022 and/or (ii) replenish the operating reserve account to reestablish the minimum reserve as required under the Amended Facility (each, a “Specific Event of Default“). As per the terms of the Undertaking, the forbearance period is from November 22, 2021 to October 1, 2022. The Undertaking also provides that the net proceeds of the Bought-Deal Financing that closed on November 25, 2021 will not be used to repay any of the loans outstanding under the Amended Facility during the forbearance period. The Lenders will cease to be bound by the Undertaking (i) should the Company not invest the net proceeds received on CAD$16 million of the Bought-Deal Financing into MTV between the closing of the financing on November 25, 2021 and April 30, 2022, (ii) if an event of default occurs under the Amended Facility other than a Specified Event of Default, or (iii) if the Company and the Lenders fail to enter into a definitive agreement by September 30, 2022, pursuant to which the loan repayment schedule in the Amended Facility is revised.

Operations

- The Company continued to further advance the development of Papomono during the third quarter of 2021. MTV completed the critical ventilation shaft and the ore pass, which will further accelerate the speed of its continued advance. As at October 31, 2021, the development of Papomono is approximately 77% complete and 87% of the required meters to begin producing have been completed.

- In August 2021, MTV negotiated an extension of its underground development contractor’s contract to include the remaining development work following the initial construction and development phase of the block caving project. This has enabled the contractor to have more success with their recruiting efforts of skilled workers, and as a result, performance improved significantly in August, September, and October with over 200 meters of advancement each month, a rate not seen since the construction began. The block caving construction project is on track for completion in early 2022 with the planned ramp-up of production during 2022.

- Effective August 1, 2021 MTV entered into an amendment to the offtake agreement (the “Offtake“) specific to the fixed price sales component with Anglo American Marketing Limited (“AAML“). Under the terms of the amendment, the remaining monthly deliveries of copper cathodes due under the fixed price portion of the Offtake are deferred until May 1, 2022 and all sales of copper cathodes commencing August 1, 2021 until April 30, 2022 will be sold at the prevailing spot price for copper cathode, less a nominal amount.

- Copper cathode production was 1,138 tonnes at an average grade of 0.52%, increasing production 10% from 1,035 tonnes at an average grade of 0.53% for the three months ended June 30, 2021, mainly due to a higher average grade of ore purchased from third-party small miners and Empresa Nacional de Minera (“ENAMI“) compared to the second quarter of 2021.

- For the nine months ended September 30, 2021, capital expenditures of $9.3 million were incurred related to the construction and development of the incline block caving mine at the Papomono Masivo deposit.

Financial

- Reported gross loss of $0.9 million on a realized average copper price2 of $3.58 compared to $2.82 in Q3 2020.

- Adjusted EBITDA from continuing operations1 of negative $0.4 million compared to negative $0.9 million in Q3 2020.

- Net loss per share attributable to owners of the Company of $0.02 compared to $0.01 in Q3 2020.

- During September 2021, the Company drew down the remaining $6 million loan facility available to it under the terms of the Amended Facility. This additional senior secured debt has substantially the same security and terms as defined in the Amended Facility but with a fixed annual interest rate of 11%.

Operational Results Summary

| Three months ended | Nine months ended | |||||||||||

| Operating information | Sept. 30, 2021 | Sept. 30, 2020 | Sept. 30, 2021 | Sept. 30, 2020 | ||||||||

| Copper (MTV Operations) | ||||||||||||

| Total ore mined (thousands of tonnes) | 178 | 49 | 550 | 351 | ||||||||

| Grade of ore mined (% Cu) | 0.52 | % | 0.88 | % | 0.54 | % | 0.86 | % | ||||

| Total waste mined (thousands of tonnes) | 739 | 118 | 1,358 | 853 | ||||||||

| Ore Processed (thousands of tonnes) | 231 | 90 | 680 | 474 | ||||||||

| Cu Production (tonnes) | 1,138 | 1,077 | 3,073 | 3,789 | ||||||||

| Cu Production (thousands of pounds) | 2,509 | 2,374 | 6,775 | 8,353 | ||||||||

| Change in inventory ($000s) | $ | 3,563 | (11 | ) | $ | 10,427 | (4,421 | ) | ||||

| Cash cost of copper produced 1 (USD per pound) | $ | 3.40 | $ | 2.44 | $ | 3.49 | $ | 2.75 | ||||

| Realized copper price 2 (USD per pound) | $ | 3.58 | $ | 2.82 | $ | 3.48 | $ | 2.46 | ||||

1 Cash cost per pound of copper produced includes all costs absorbed into inventory including inventory write-downs less non-cash items such as depreciation and non-site charges. It is a non-IFRS performance measure. Refer to Non-IFRS Performance Measures.

2 Realized copper price is a non-IFRS performance measures. Refer to Non-IFRS Performance Measures.

Ore Production

- Ore mined of 165,222 tonnes at a grade of 0.47% from Don Gabriel representing 93% of ore mined.

- 73% of ore processed from Don Gabriel; 22% from third-party small miners and ENAMI; 5% from Papomono Masivo.

- Produced 2.5 million pounds of 99.99% pure copper cathodes at a cash cost per pound produced1 of $3.40.

- Sold 2.3 million pounds of copper cathodes at an average realized copper price2 of $3.58 per pound.

- High unit costs expected throughout 2021 and into 2022 as the Company expects to operate below capacity until Papomono Masivo is in full production.

Construction and Development of Papomono Masivo

- Mineral reserve estimate for Papomono Masivo is 3,067kt of proven and probable mineral reserves (at a copper grade of 1.51%).

- Block caving construction 77% complete and 87% of the required meters to begin producing have been completed as at October 31, 2021 with 19 opened construction fronts.

- High grade ore being extracted as part of construction process.

- In August 2021, MTV negotiated an extension of the underground contractor, Aura, contract to include the remaining development work following the initial construction and development phase of the block caving project. This has enabled Aura to have more success with their recruiting efforts of skilled workers.

- Aura delivered significantly improved performance since August 2021 with over 200 meters of advance per month from August to October. October 2021 was the best month since commencement of the project with 220 meters of advance. The block caving construction project is on track for completion in early 2022.

Exploration

- In September 2021, the Company commenced its 2021 near mine exploration drilling program on MTV focused on testing high-potential copper targets located between Don Gabriel and Papomono, which sit approximately 3 kilometers apart.

- On September 28, 2021, the Company announced that it has identified a new porphyry target in its license area. The identified central core has dimensions of approximately 2km by 1km. This target is an example of the broader potential of this property as copper porphyry deposits are associated with some of the largest long life copper mines in the world, with Chile hosting the greatest concentration of these deposits.

- Dr. John Mortimer, senior exploration geologist, is leading the Company’s explorations activities and executing the exploration program at MTV.

- Significant strategic land package of over 46,000 hectares.

- Property in the well-known copper producing Coquimbo region which has Antofogasta Minerals’ Los Pelambres mine located approximately 50 kilometers to the east of MTV.

- With more than 100 copper outcrop occurrences and 70 artisanal mining sites with geological characteristics similar to that of the Papomono and Don Gabriel orebodies, together with near-term infill drilling opportunities, the Company believes there is significant exploration potential.

COVID-19

- Beginning in March 2021 and in conjunction with the Chilean Ministry of Mining, the Ministry of Health and the Regional Mining Secretary of Coquimbo, MTV initiated an on-site vaccination program by offering vaccinations to all MTV employees and contractors. To date, 2021, approximately 94% of the workforce have received both doses of the vaccine and nearly 100% of the workforce has opted to participate.

- MTV continued its vaccination campaign in October 2021, offering booster shots on site to all workers.

- In the third quarter of 2021, COVID-19 restrictions eased in Chile as cases trended downward, resulting in little impact on the Company’s operations during this period. Should these restrictions reappear in the future, the effect of the COVID-19 pandemic on the Company’s business activities will create elevated uncertainty and may further impact production and previous guidance.

- The Company continues its preventative, mitigating and containment measures to actively minimize the spread of COVID-19.

Financial Results Summary

| Three months ended | Nine months ended | |||||||||||

| Financial information (in thousands) | Sept. 30, 2021 | Sept. 30, 2020 | Sept. 30, 2021 | Sept. 30, 2020 | ||||||||

| Revenue | $ | 8,362 | $ | 5,610 | $ | 22,873 | $ | 17,700 | ||||

| Gross loss | $ | 881 | $ | 552 | $ | 3,070 | $ | 9,546 | ||||

| Net loss from continuing operations | $ | 1,474 | $ | 335 | $ | 9,407 | $ | 21,167 | ||||

| Net loss from discontinued operations | $ | — | $ | — | $ | — | $ | 2,241 | ||||

| Net loss for the period | $ | 1,474 | $ | 335 | $ | 9,407 | $ | 23,408 | ||||

| Net loss per share attributable to owners of the Company | $ | 0.02 | $ | 0.01 | $ | 0.16 | $ | 0.48 | ||||

| EBITDA from continuing operations 1 | $ | 2,254 | $ | 1,873 | $ | 1,347 | $ | (12,695 | ) | |||

| Adjusted EBITDA from continuing operations 1 | $ | (392 | ) | $ | (926 | ) | $ | 440 | $ | (4,529 | ) | |

| Gain (loss) on portfolio investments | $ | — | $ | 1,038 | $ | 107 | $ | (1,294 | ) | |||

| Impairment of non-current assets | $ | — | $ | — | $ | — | $ | (7,628 | ) | |||

| Reversal (write-down) of inventory | $ | — | $ | 665 | $ | (2,474 | ) | $ | (3,441 | ) | ||

| Gain on modification of debt | $ | — | $ | 3,487 | $ | — | $ | 3,487 | ||||

| Cash used in operating activities before working capital changes | $ | (1,229 | ) | $ | (1,097 | ) | $ | (103 | ) | $ | (4,412 | ) |

1 Refer to Non-IFRS Performance Measures

Financial Results

Revenues of $8.4 million for the three months ended September 30, 2021 were generated predominantly from the sale of copper cathodes. Finished goods inventory at September 30, 2021 was approximately $2.9 million. Copper cathodes sold for the three months ended September 30, 2021 of 1,060 tonnes was higher than the comparative quarter in 2020 of 858 tonnes with their respective revenues based on an average realized copper price of $3.58 per pound and $2.82 per pound.

The Company reported a gross loss of $0.9 million for the three months ended September 30, 2021, mainly due to higher operating costs resulting from lower-than-expected grades of the ore mined from Don Gabriel. A reversal of previous write-down of inventory of $0.7 million that was recorded as a decrease to cost of sales offset the gross loss of $0.6 million for the comparable quarter.

Revenues of $22.9 million for the nine months ended September 30, 2021 were generated predominantly from the sale of copper cathodes. Copper cathodes sold for the nine months ended September 30, 2021 of 2,975 tonnes was lower than the comparative period in 2020 of 3,068 tonnes. The decrease in tonnes of the copper cathodes sold in 2021 was more than offset by the average realized copper price of $3.48 per pound, which increased by 41% from $2.46 per pound in the nine months ended September 30, 2020.

The Company reported a gross loss of $3.1 million for the nine months ended September 30, 2021 that includes a write-down of inventory, net of reversals of $2.5 million that is recorded as an increase to cost of sales. Included in the gross loss of $9.5 million for the comparable period, is a write-down of inventory, net of reversals of $3.4 million that is recorded as an increase to cost of sales.

In accordance with the Offtake with AAML, MTV sold 46% of its copper cathode production at $2.89 per pound for the three months ended September 30, 2021. This percentage is higher than the expected 40% as copper cathode production was lower during the nine months ended September 30, 2021 than was anticipated when the fixed priced portion of the contract was entered into.

Effective August 1, 2021 MTV entered into an amendment to the Offtake specific to the fixed prices sales component with AAML. Under the terms of the amendment, the remaining monthly deliveries of copper cathodes due under the fixed price portion of the Offtake are deferred until May 1, 2022 and all sales of copper cathodes commencing August 1, 2021 until April 30, 2022 will be sold at the prevailing spot price for copper cathode, less a nominal amount. The remaining 12 months of contracted delivery amounts of the fixed price portion of the contract will resume on May 1, 2022 at the previous agreed fixed price of $2.89 per pound.

The increasing copper price together with MTV’s obligation to sell a set amount of its production at $2.89 per pound affected the economics of purchasing ore from third-party small miners at market until July 31, 2021, but thereafter, the amendment to the Offtake significantly benefited ore supply from third-party small miners. The amendment allowed the Company to purchase ore from third-party miners at more competitive rates driving a progressive increase in ore supply up to October 2021, when MTV purchased over 21,000 tonnes of ore from third-party miners, which was 17% above the expected 18,000 tonnes.

The Company’s general and administrative expense for the three and nine months ended September 30, 2021 was $1.3 million and $3.2 million compared to $0.8 million and $3.2 million, respectively, in the comparative periods, showing an increase in marketing expenses in the three months ended September 30, 2021, compared to the same period of 2020.

Finance expenses for the three and nine months ended September 30, 2021 totaled $2.4 million and $6.8 million compared to $1.2 million and $4.5 million, respectively, in the comparative periods, as the average balance of the Company’s long-term debt grew. Given the current grace period achieved for the long-term debt under MTV’s restructuring in 2020, cash interest payments made during the three and nine months ended September 30, 2021 amounted to $1.1 million and $1.8 million, respectively.

The Company reported a quarterly net loss attributable to owners of the Company of $1.3 million or $0.02 per share. Adjusted EBITDA (see Non-IFRS Financial Measures ) from continuing operations for the three months ended September 30, 2021 was negative $0.4 million or $0.01 per share. For the comparable quarter in 2020, the Company reported a net loss attributable to owners of the Company of $0.3 million or $0.01 per share and Adjusted EBITDA from continuing operations of negative $0.9 million or $0.03 per share.

In the first three quarters of 2021, the Company reported a net loss attributable to owners of the Company of $7.6 million or $0.16 per share. Adjusted EBITDA (see Non-IFRS Financial Measures ) from continuing operations for the nine months ended September 30, 2021 was $0.4 million or $0.01 per share. For the comparable quarters of 2020, the Company reported a net loss attributable to owners of the Company of $16.2 million or $0.48 per share and Adjusted EBITDA from continuing operations of negative $4.5 million or $0.14 per share.

In the first three quarters of 2021, cash used in operating activities was $9.8 million (cash used of $0.1 million before changes in non-cash components of working capital), compared with 2020 when cash used in operating activities was $2.4 million (cash used of $4.4 million before changes in non-cash components of working capital).

Cash Position, Working Capital and Net Debt

Cash and cash equivalents decreased to $6.7 million at September 30, 2021 from $12.0 million at December 31, 2020 mainly due to $9.8 million used in operating activities, $7.7 million of disbursed capital expenditures mainly related to the construction and development of Papomono Masivo and $1.8 million of interest payments; all partially offset by $8.3 million of net proceeds from the April 2021 bought deal financing, $6.2 million of net proceeds from loans and borrowings and $0.4 million of net proceeds from the exercise of warrants.

The Company has working capital (see Non-IFRS Financial Measures ) of $3.1 million at September 30, 2021 and approximately $27.5 million as at the date hereof. Cash position as at the date hereof is approximately $17.8 million.

The Company is substantially leveraged. The Company’s net debt (see Non-IFRS Financial Measures ) at September 30, 2021 was $67.1 million. The Company’s debt position continues to increase as it capitalizes interest and remains in a grace period for the majority of its debt (see the Undertaking in Recent Highlights previously).

Health and Safety

For the three months ended September 30, 2021, there was no Lost-Time Incident. MTV’s annual injury frequency index continues to remain below the average of the mining industry in Chile. The Company and MTV devote considerable time and effort to ensure that workers and contractors return safely to their families after each shift. Safety statistics are monitored and compared to the country and peer averages, and MTV pro-actively engages in education and assessment to achieve a goal of zero lost-time incidents.

Community and Environment

MTV continues to actively work with local communities and stakeholders and for the three months ended September 30, 2021, the MTV Foundation continued the funding of projects agreed to by the MTV Foundation board, which is largely composed of community representatives to help MTV understand the true needs of its neighbors, such as starting an eco-friendly cooperative at a local school. MTV’s ore purchase program also ensures support from local miners, buying ore from over 26 providers and supporting the development of over 300 small-scale miners through local mining unions.

Ongoing Arbitration

As previously disclosed, the Company is involved in an arbitration proceeding with the Minority Shareholder of MTV. The arbitration proceeding is continuing and no further material developments have occurred. The Company remains confident in its position and is monitoring the arbitration proceeding and its process closely.

Qualified Persons

The scientific and technical content contained in this news release is taken from the technical report (the “ Technical Report “) entitled “Minera Tres Valles Copper Project, Salamanca, Coquimbo Region, Chile NI 43-101 Technical Report” prepared by Dr Antonio Luraschi, RM CMC, Manager of Metallurgic Development and Senior Financial Analyst, Wood, Mr Alfonso Ovalle, RM CMC, Mining Engineer, Wood, Mr Michael G. Hester, FAusIMM, Vice President and Principal Mining Engineer, Independent Mining Consultants, Inc., Mr Enrique Quiroga, RM CMC, Mining Engineer, Q&Q Ltda, Mr Gabriel Vera, RM CMC, Metallurgical Process Consultant, GVMetallurgy, and Mr Sergio Alvarado, RM CMC, Consultant Geologist, General Manager and Partner, Geoinvestment Sergio Alvarado Casas E.I.R.L. all of whom were independent qualified persons as defined by NI 43-101 at the time the Technical Report was prepared. The Technical Report was filed by TVC on SEDAR (www.sedar.com) on December 14, 2018 and subsequently amended and restated on May 27, 2021. Readers are encouraged to read the Technical Report in its entirety except for certain sections withdrawn by the Company in relation to disclosure regarding the Preliminary Economic Assessment appearing in the Technical Report (see press release dated April 12, 2021).

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Lucara Diamond (TSX:LUC), a leading independent producer of exceptional quality type IIa diamonds, said on wednesday that the global market for diamond jewelry and rough diamonds is at one of the healthiest places it has been in several years.

The Vancouver-based miner believes it is a trend it can expect to see continue into 2022 as targets are being set accordingly. These positive market changes were spurred on by an improvement in global supply and demand fundamentals, Lucara said in a statement.

Lucara anticipates producing up to 340,000 carats which are planning to be sold through its multi sales channel approach and could generate revenues up to between $185 and $215 million. The following 2022 year also marks the tenth year their 100% owned Karowe mine in Botswana has been in operation.

These figures do not include any estimated contributions of revenue from large, exceptional diamonds that have historically formed a regular part of Karowe’s production profile, the company said.

The Karowe mine, which actually means precious stone in the local Botswana language, began operations in 2012. It is one of world’s most well known producers of large, high quality, Type IIA diamonds, mostly 10.8 carats, including the famous and historic 1,758 Sewelô, the 1,109 carat Lesedi La Rona and the 813 carat Constellation.

The only other major diamond ever unearthed at that site was discovered in South Africa in 1905, the Cullinan Diamond. The huge diamond was then cut into smaller stones, and some were even placed in the British royal family’s crown.

“The business environment for diamonds and diamond jewelry is the healthiest we’ve seen in several years,” CEO Eira Thomas said in the statement.

Big Names With Big Prices

The diamond market faced some difficulties over the last year due to the global COVID-19 pandemic, with some folks having increasing concerns that the market may take years to recover. However, intermediaries who polish, cut and trade stones seem to be purchasing every miner’s supply, even as big names such as Alrosa and Anglo American’s De Beers raise their prices.

According to the company website, over 6,900 diamonds of +10.8 carats have been discovered, as well as 25 +300 carat diamonds and three huge +1000 carat diamonds. The forecast for 2022 revenue assumes that 100% of the stones and carats recovered will come from the higher value M/PK(S) and EM/PK(S) units within the South Lobe, which is in accordance with their mine plan.

Diamonds that have a higher value than +10.8 will continue to enter the manufacturing pipeline at HB, allowing the company to gain exposure to polished prices and regular cash flow as these larger diamonds are of the highest value.

Open-pit operations will finish by 2026 at Karowe, however, Lucara also has an underground mining expansion project that was supported by the completion of a supplemental debt financing package in 2021. The company says it was a “significant de-risking milestone” for themselves and the mine.

“The underground expansion at Karowe provides access to the richest portion of the orebody and will extend mine life to at least 2040. The project remains on schedule and budget, with a forecasted spend of up to $110 Million in 2022,” Thomas said in the statement.

The underground expansion will focus on the commencement of shaft sinking activities, the commissioning of power, and detailed engineering for the underground development. Sustaining capital and project expenditures are expected to be up to $17 million with a focus on completion of a community sports facility, dewatering activities, and an expansion of the tailings storage facility, the company said.

BMO Capital Markets analyst Ray Raj touched on the importance of the future of the expansion, saying “the continued recovery of the significant high-value stones from the South Lobe further highlights the importance of the Karowe underground expansion.”

Thomas touched on the underground expansion updates in a previous press release, saying “These developments have significantly de-risked Lucara’s outlook on growth and has positioned the Company to benefit from a stronger, more stabilized diamond price environment as global rough diamond supply remains constrained.”

The decision to move the Karowe mine underground comes after Botswana renewed Lucara’s mining license in early January for another 25 years. The total cost of moving the mine is around $514 million and will take about five years to complete and extend the mine’s life up to 20 more years.

Next year, Lucara expects to process 2.6 million to 2.8 million tonnes of ores, which should yield between 300,000 and 340,000 carats.

Lucara owns 100% of the Karowe mine in Botswana and owns 100% interest in Clara Diamond Solutions, a sales platform designed to bring the existing diamond supply chain digital and more accessible in the modern era.

Pushing Digital First

The company highlighted its digital sales platform in the statement as it continues to help the company grow and expand in terms of volumes traded and customer participation. Lucara plans to continue platform trials and discussions with third-party suppliers of rough diamonds to build supply.

“The rationale for a web-based digital sales platform for the transaction of rough diamonds has never been stronger, sparked by industry’s need for increased transparency, global restrictions on travel, and a new openness to the use of innovation and technology to create a more efficient supply chain,” Thomas said.

Quarterly tenders and regular sales through Clara, primarily for stones less than 10.8 carats in size will continue, consistent with the practise from previous years, the company said.

Although Lucara is optimistic about the diamond market going into 2022, DeBeer’s is experiencing the opposite of what Lucara is claiming. The world’s largest diamond miner by value reported on Wednesday it has sold $430 million worth of rough diamonds this month, compared to the $492 million in sales obtained in the previous cycle.

Lucara’s shares fell 4.6% in early trading in Toronto to C$0.62. The company has a market capitalization of about C$287 million ($226m).

The diamond miner is based out of Vancouver and was originally incorporated in 1981. In 2018, Lucara completed the acquisition of Clara, their digital sales platform that “uses proprietary analytics together with cloud and blockchain technologies to revolutionize and modernize the diamond sales process.”

Lucara issued 13.1 million shares to the former shareholders of Clara upfront along with equity payments totaling 13.4 million shares which become payable upon the achievement of performance milestones related to total revenues generated by Clara.

The company agreed to a profit-sharing mechanism whereby the founders and facilitators of the Clara technology, and management of Clara, will retain 13.33% and 6.67%, respectively, of the annual EBITDA generated by the platform, to a maximum of US$25 million per year, for 10 years.

Full Ownership Acquired by Rio Tinto

In other recent diamond news, Rio Tinto (ASX:RIO) just became the sole owner of the Diavik Diamond Mine in the Northwest Territories in Canada. The transaction follows a 19-month process prompted in April 2020 by Dominion Diamond Mines ULC filing for insolvency protection under the Canadian Companies’ Creditors Arrangement Act. The mine employs over 1100 employees, of which 17% are Northern Indigenous people, and in 2020 it produced 6.2 million carats of rough diamonds. Production is expected to finish in 2025.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Three Valley Copper (TSXV:TVC) announced this morning that it had closed the previously announced bought-deal offering and exercise of the over-allotment option. The financing will help the company advance the Minera Tres Valles copper project in Chile, and fund exploration at the site. Additionally, funds will be used for working capital and general corporate purposes as Three Valley Copper explores, develops, and produces 99.99% copper cathodes at its flagship property.

Initially, the company entered into an agreement with co-lead underwriters and joint bookrunners PI Financial Corp. and Eight Capital for a C$10 million bought deal financing.

Then, shortly after, due to significant investor demand, PI Financial Corp and Eight Capital amended the agreement to increase the size of the deal.

Details of the financing are as follows:

The Company issued a total of 56,681,000 units (the “Units”) on a bought deal basis, at an offering price of C$0.32 per Unit (the “Offering Price”), which included 6,681,000 Units issued pursuant to the exercise of the over-allotment option, and issued 819,000 additional Common Share purchase warrants (each, a “Warrant”) pursuant to the exercise of the over-allotment option at an offering price of C$0.08 per Warrant, for gross proceeds of approximately C$18.2 million. Each Unit consists of one Class A common share (a “Common Share”) in the capital of the Company and one Warrant. Each Warrant entitles the holder thereof to purchase one Common Share at a price of C$0.45 for a period of 30 months following the closing of the Offering.

Source: Three Valley Copper

Michale Staresinic, CEO of Three Valley Copper (TSXV:TVC) commented in a press release: “This new equity capital coupled with the concessions provided by our senior lenders provide a roadmap for the Company to complete its flagship project at MTV, Papomono is on schedule to begin its first caving operations in January 2022 followed by an increasing production profile during 2022 and ultimately reach near production capacity in 2023. In parallel, we continue the strategic review process announced by the Company in October and welcome our new shareholders with the closing of this equity raise, and thank our existing shareholders for their ongoing support.

“With copper prices firmly above US$4 per pound for the majority of 2021, we continue to believe this level of price support for copper will continue in the long-run. The electric vehicle revolution, infrastructure stimulus spending, and world consensus on decarbonization back our strong conviction that our pure-play copper project with 46,000 hectares of underexplored lands will produce strong results for shareholders once we are able to reach production capacity. Our new shareholders see this too and we welcome their support through this Offering.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Novo Resources (TSX:NVO) announced last Friday that it will begin its brownfield exploration programs at its highly prospective Nullagine gold project located in the East Pilbara District of Western Australia.

The new exploration programs will focus on oxide opportunities at the Nullagine gold project with a 15,000 m reverse circulation drilling program which started at the Parnell-Vulture trend, also known as Parnell, during the first week of November 2021. This will take the company into the first quarter of 2022 as well.

Gold assay results from the new drill program are expected to be released by December 2021. Novo Resources has a priority arrangement with Intertek1 to provide PhotonAssay gold results.

Parnell-Vulture

Parnell is located about 45 kms from the Golden Eagle processing facility and can be accessed by an existing reliable haul road with surrounding infrastructure attached. Parnell covers a strike length of approximately 2 kms and contains a series of vein-hosted targets with historical drill intercepts.

The Parnell and Vulture reverse circulation programs are the first programs at the Nullagine gold project as things begin to ramp up, with forward programs currently being generated at several priority basement targets.

Novo has already conducted detailed mapping and gridded soil sampling at Parnell and Vulture to determine the mineralization potential, but has yet to acquire the necessary details to validate historical data. Once this information is acquired, it will serve as further confirmation and guidance for targets. However, significant rock samples from both Parnell and Vulture highlight the presence of high-grade gold targets, and further confirm the prospectivity of this area.

Multiple Projects on the Go

Novo’s primary focus is exploring and developing gold projects in the Pilbara region of Western Australia. It has several ownership interests across its 13,000 sq km land package, and has several different projects on the go.

Novo Resources’ main focus is its Egina gold project, where it is currently exploring and testing innovative exploration techniques under a JV with Japan’s Sumitomo Corporation. The company also has a 100% interest in the Purdy’s Reward gold project and a 100% interest in the production-ready Beatons Creek gold project.

The new drilling programs follow other recent news from Novo Resources (TSX:NVO) as its Golden Eagle processing facility or “Golden Eagle Mill” had restarted production at the beginning of November. The faculty underwent opportunistic maintenance as the company repaired its main crushing unit, which is now back online.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

It was announced yesterday that Three Valley Copper Corp (TSXV:TVC) has entered into an undertaking between itself and its secured lenders of Minera Tres Valles, the Company’s primary asset that is 91.1% owned and located near Salamanca, Region de Coquimbo, Chile.

The company, with its direct and indirect wholly-owned subsidiaries including MTV and the lenders, have agreed to create a definitive binding agreement to revise the loan repayment schedule as set forth in the loan facility agreement.

Michael Staresinic, President and CEO of Three Valley Copper, said in a press release: “Our senior lenders continue to work as partners with us. This is an important first step in restructuring MTV’s debt obligations to improve cash flow from MTV in 2022 as we complete the development of the Papomono mine and ramp up production in 2022. Papomono is nearing completion and we remain on schedule to complete our first caving of ore in January 2022.”

Terms and conditions of the undertaking include the lenders agreeing not to accelerate or enforce their rights or remedies under the Facility Agreement if MTV were to fail to make scheduled loan repayments on March 31, 2022, June 30, 2022 and September 30, 2022 and/or replenish the operating reserve account to reestablish the Minimum Reserve as required under the Facility Agreement.

Also included in the conditions, the proceeds of the recently announced bought-deal financing of C$16 million will not be used to repay any of the loans outstanding under the Facility Agreement during the Forbearance Period. The Forbearance period is from November 22, 2021, to October 1, 2022. That financing was upsized from C$10 million after significant investor interest was expressed.

This undertaking follows the recent announcement to increase the size of the previously announced bought deal financing to an aggregate of 50,000,000 units of the Company at a price of C$0.32 per Unit. This is an excellent step forward with TVC’s partners and helps to secure financing that is expected to close later this week.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Mining royalty generator Altus Strategies has entered into an agreement to sell its 100% owned subsidiary Aterian Resources Ltd to Eastinco Mining and Exploration. Altus Strategies is a mining royalty generator based in the UK that focuses on generating a diverse portfolio of precious metals.

Altus has agreed to sell 100% of the Morocco-focused subsidiary to Eastinco, along with receiving up to 10% of additional warrants in Eastinco. It was also included in the agreement that Altus will be a shareholder of up to 25% of Eastinco, as well as having the option to let an Altus member join the Eastinco board. In addition, Altus will own 15 new royalties including a royalty on the Musasa tantalum mine in Rwanda.

Steven Poulton, Chief Executive of Altus said in a statement, “We are delighted to announce the proposed divestment to Eastinco of our 100% owned Moroccan focused exploration subsidiary, Aterian, as part of Eastinco’s proposed LSE Standard Listing and subsequent name change to Aterian Plc. The enlarged entity will have a strong and unique portfolio of strategic metal exploration and development projects in Morocco and Rwanda.”

Through this new agreement, Eastinco is planning to transform into a pan-African strategic metals development company, including a subsequent name change to Aterian Plc upon completion of the transaction.

Eastinco currently owns tantalum exploration and development projects in Rwanda. It is an investment company whose focus is on acquiring assets for the ethical exploration, development and trading of critical minerals across the African continent.

Charles Bray, Executive Chairman of Eastinco said in a press release: “I am delighted to report on this proposed acquisition of a significant portfolio of 15 copper, silver and other base metal exploration projects strategically positioned close to existing mining projects in Morocco. Upon completion, Altus will become a strategic shareholder of the Company, demonstrating Altus’ confidence in the projects, and providing us with an alignment of interest and the support of a well-respected industry player.”

Bray continued “Previous exploration undertaken by Altus on the Moroccan assets highlight the strong potential for the discovery of deposits of strategic metals in particular, copper and silver. We believe the market fundamentals for copper are excellent, specifically linked to the anticipated growing demand for renewable energy and the related electrification of transportation globally.”

The agreement still remains subject to certain conditions including the admission to trading of Eastinco’s entire issued share capital to the Official List of the FCA and to trading on the London Stock Exchange’s Main Market for listed securities.

“We consider this to be the optimal time to broaden and strengthen our asset portfolio across Africa, adding to our established tantalum mining and exploration projects in Rwanda. Our working relationship with Altus will also guarantee a smooth transition to ensure exploration continues in Morocco without interruption. Our proposed LSE Standard Listing will provide us with exposure to a wider investor profile and greater liquidity in our shares and, therefore, a solid platform from which we can continue to grow,” Bray said.

Charles Bray believes this is a key step to becoming a leading strategic metal exploration and development company in Africa.

“We look forward to the completion of the acquisition, the successful Admission of Eastinco, and to supporting the Eastinco team going forward,” Poulton concluded.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Canada Nickel announced that through 18 separate and concluded transactions, it has acquired or been granted earn-in to 13 additional target properties within a radius of 95 km of the company’s flagship Crawford Nickel-Sulfide Project in Ontario.

The acquisition consolidates Canada Nickel’s position in the Timmins area, as the company sees high potential for future endeavours in the region.

“The acquisition of these highly prospective target properties represents a transformational milestone for Canada Nickel, on par with the initial discovery of our flagship property, Crawford. The consolidation of these properties underscores our strong belief in the district-scale potential of the Timmins region and in our journey to become a leader of the Next Generation of Nickel Supply – large, scalable, low carbon nickel supply,” said Mark Selby, Chair & CEO of Canada Nickel in the statement.

Each of the properties is said to contain one or more ultramafic targets based on combinations of historical geophysical work and drilling over the past 65 years. The 13 new properties have a combined target surface of 37.7 square km, which is 40 times larger than the current Crawford Main Zone resource of 0.85 square km.

Ten of the target properties have a larger footprint than Crawford and nine are confirmed to contain the same host mineralization as Crawford, a proposed open-pit mine and mill that will produce both nickel and magnetite concentrates.

The Sothman target property was highlighted by Canada Nickel for having a historical higher grade, with a shallow resource of approximately 190,000 tons of 1.24% nickel. Sothman is a property of approximately 1,000 ha located 70 km south of Timmins and was acquired by Glencore.

They also highlighted that four target areas have yielded drill intersections of nickel including Sothman, Deloro, Midlothian, and Mann Southeast.

“We’re talking district-scale potential that would make this the largest base metal mine in Canada once it’s ramped up,” Selby said in an interview back in May. “We’d be the largest single nickel sulphide mine in the world outside Russia. We’ll be bigger than [Vale’s] Voisey’s Bay. This is a pretty significant project.”

The 18 properties were negotiated through all separate agreements and Canada Nickel will pay a combined $371,500 in cash and 2,044,000 shares, in which $25,000 has already been paid and 125,000 shares have already been issued.

One of the main goals of the company is working towards developing a process for production of net-zero carbon nickel, cobalt, and iron products using technology from its wholly-owned subsidiary NetZero Metals.

The plan is to use existing methods and alternatives to help reach this goal rather than creating new tools and equipment, such as electric rope shovels and trolley trucks that use electricity rather than diesel whenever they can. A natural mineral carbonation approach for the deposition of waste rock and tailings during mining to allow material to absorb CO2 is another alternative they plan on implementing.

Turning into a zero-emissions nickel producer could also grab the attention of Elon Musk, co-founder and CEO of Tesla. The electric vehicles maker claimed last year that he would give any big firm that can extract the metal in an environmentally friendly manner a giant contract for a long period.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

On November 18, 2021 Solaris Resources (TSX:SLS) traded above average volume by hundreds of thousands of shares at nearly 1.7 million in daily volume. Solaris’ share structure has one of the highest insider ownerships for a junior miner, begging the question of why exactly did volume spike on that day?

Could it have been that insiders are shifting positions ahead of upcoming drill results? Or is something else happening with retail investors to draw such high volume?

It would first help to understand what a breakout above regular price action and traded volume can mean for investors. Often higher volume will drive prices higher or lower depending on the bid-ask spread, but in this case, shares traded only 2% higher on the day.

The stock was not outside of its normal bounds, and closed just below C$14, at $13.90. The uptick in volume is notable for how it didn’t accompany a significantly different price action, but potentially foreshadows new price action coming down the line.

For this reason, it could be inferred that the expectation of news coming down the pipeline could be the reason for the higher than average daily volume. The company has had a run of successful assay results as part of its ongoing exploration at the Warintza Project in Ecuador.

An expansion of the Warintza Porphyry Cluster, multiple back-to-back discoveries, the commencement of maiden drilling at Warintza South, and positive preliminary results at Warintza Central have seen shares climb consistently month after month.

The stock is up over 1000% since the company’s IPO in 2020, and the bullish sentiment indicated by multiple breaks above the 50-day moving average would seem to indicate that buyers are always present.

Whether the larger than average trade volume is indicative of insiders moving shares ahead of news or higher investor interest due to the company’s performance and the drill program is yet to be seen. For now, investors will be watching closely whether Solaris (TSX:SLS) continues to climb higher.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Evolution Mining (ASX:EVN), based in Australia, is a globally recognized gold miner. On October 5, 2021, the company acquired the Ernest Henry Mining (EHM) copper and gold mine in Queensland, Australia, from Glencore (LON:GLEN) for $729.60 million (A $1 billion).

Ernest Henry includes an underground mine that produces copper and gold concentrate that is transported to Mount Isa Mines for smelting.

Evolution acquired the company $582 million (A$800 million). After completion of 12 months, a further A$200 million will be paid. Evolution had previously acquired an economic interest in Ernest Henry in 2016 through a joint structure, with the asset managed and operated by Glencore. This new deal brings the Ernest Henry Mine under Evolution’s control and ownership. Evolution is now the sole owner of the asset so it will assume full ownership of its operations as well.

An Exit for One of the World’s Largest Natural Resource Companies

Glencore is one of the world’s largest diversified natural resource companies, as well as a major producer and marketer of more than 60 commodities. In Australia, Glencore produces coal, copper, cobalt, nickel, zinc, lead, silver, and gold between 26 mining operations. Glencore is also one of the country’s biggest employers.

Glencore employs approximately 17,700 people in Australia (including around 600 at the Ernest Henry Mine) and in 2020 the company contributed more than $13.8 billion to the regional, state, and national economies.

Glencore CEO Gary Nagle said in a statement, “Evolution has been a strong partner at Ernest Henry Mine for five years. They share our way of working and our commitment to operating responsibly in all aspects of the business.”

Glencore’s commitment to northwest Queensland will continue with the Mount Isa Mines copper and zinc complex, copper smelter, and Townsville copper refinery. Glencore will also pivot from this mine and increase its focus on lower-cost, long-life copper assets in its global portfolio, such as those in Africa and South America.

Shares of Evolution Mining Ltd (ASX: EVN) were up nearly 8% on the day of the announcement.

An Effort to Boost Production

The company advised that the acquisition will increase its copper production from its previous forecast to between 34,000 and 38,000 tons and reduce its all-in sustaining cost (AISC) to around A$90 to A$100 per ounce. This will help cement it as one of the lowest-cost gold producers in the world.

The recent acquisition aligns with Evolution’s strategy of investing in assets with immediate material increase in cash flow generation.

Once the initial $800 million round of the transaction is completed, Evolution will have about $900 million in liquidity available at settlement, the release noted.

Evolution Mining’s CEO said, “We have long coveted ownership of Ernest Henry. It is a world-class asset, in Australia, and one we know extremely well due to our successful investment in the asset in 2016 and we are proud that it will once again be 100% Australian. The acquisition is consistent with our strategy, substantially improves the quality of our portfolio and offers both strong cash flow and life-of-mine extension opportunities.”

He continued, “The site management team has an outstanding track record of operational delivery and we are delighted to have them join Evolution and look forward to working with them to make this an even better operation. We are also pleased to continue our strong relationship with Glencore and that product will continue to be treated in the local region at their Mt Isa smelter and Townsville refinery.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Rio Tinto (ASX:RIO), the world’s second-largest miner, just became the sole owner of the Diavik diamond mine in Canada’s Northwest Territories on Thursday. Despite saying in the past the Company was not interested in taking full control of the aging arctic mine, Rio Tinto ended up buying the 40% share held by Dominion Diamond Mines for a total stake of 100%.

Part of the transaction includes Rio Tinto releasing Dominion and its lenders from any outstanding liabilities or obligations involving funding the operation or the closure of the joint venture. On the other end, Rio Tinto will receive all remaining Diavik assets held by Dominion including a security cash collateral for the potential future closure for the mine and unsold production.

Why the Buyout Now?

Dominion, which used to be the fourth-largest diamond producer, suffered some financial troubles which played out in court over several months last year. These troubles ultimately led Dominion to sell its other Canadian mine, Ekati in December 2020. In 2017, The Washington Companies ended up buying the Company for $1.2 billion.

This deal follows a 19 month long process beginning in April 2020 by Dominion Diamond Mines filing for insolvency protection under the Canadian Companies’ Creditors Arrangement Act.

Diavik has been in production since 2003 and is eventually facing closures in 2025 which will cost hundreds of millions of dollars to fully clean up. Diavik is Canada’s largest diamond mine, and yielded 6.2 million carats of rough diamonds in 2020.

Rio Tinto Minerals boss Sinead Kaufman said in a statement, “Diavik will now move forward with certainty to continue supplying customers with high quality, responsibly sourced Canadian diamonds.”

Worries and concerns began to surround the diamond market due to production coming to a

halt during the global COVID-19 pandemic, with some people worried the market would never recover. However, Alrosa, the world’s top diamond miner by output, claims the market has fully recovered from the effects of the global pandemic, and sales of jewelry and rough diamonds are up 23% this year compared to 2020.

Rio Tinto Invests US$87 Million to Boost Low-Carbon AP60 Aluminum Production

In other recent news, Rio Tinto (ASX:RIO) decided to invest US$87 million in order to increase capacity at its Canadian low-carbon aluminum production project. The company is creating 16 new smelting cells in the Saguenay-Lac-Saint-Jean region of Quebec at its AP60 smelter in the which will increase the production by about 45%, or 26,500 metric tonnes of primary aluminum per year.

This will increase capacity up to 86,500 metric tonnes. Not only will production increase, but this upgrade will secure the futures of up to approximately 100 employees who work at the smelter by extending the life of the project.

Rio Tinto Aluminium chief executive Ivan Vella commented: “Rio Tinto is committed to strengthening its position as a leader in low-carbon, hydro-powered aluminum production to meet the clear demand from our customers in North America and Europe. Our AP60 technology is one of the most energy-efficient, environmentally friendly and cost-effective systems in commercial production today. It produces some of the world’s lowest carbon aluminum with renewable hydropower here in Quebec. We are assessing options for further investments, as we progress development of the ELYSIS zero-carbon smelting technology with our partners.”

Rio Tinto predicts the aluminum market will grow at an average rate of about 3.3% per annum over the next decade as strong demand for the metal comes from green energy transition and decarbonization.

The AP60 technology building generates seven times fewer greenhouse gases than the average building in the industry and was created by Rio Tinto’s research and development teams. Since 2013, the initial AP60 technology pots have produced more than 465,000 tonnes of low-carbon aluminum.

The new work will begin in 2022 and should be completed by the end of 2023. The new pots will be built in the existing building of the Complexe Jonquière’s AP60 technology centre, which currently has 38 pots. As the new pots are being built, Rio Tinto will also be looking into potentially installing AP60 cells at the site in the future.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

U.S. President Joe Biden and President Xi Jinping of China held a virtual summit, and the leaders of the world’s two largest economies faced tensions over trade, cyber threats, climate, and human rights.

Investors applauded the meeting between U.S. President Joe Biden, and Chinese leader, Xi Jinping, due to positive developments that favored the rise in copper prices.

Copper prices rose as the dollar weakened, leading to an improved risk sentiment among investors.

Three-month copper on the London Metal Exchange was up 0.4% at $9,711.50 a tonne at the same time as the most-traded December copper contract on the Shanghai Futures Exchange rose 0.2% to 71,070 yuan (11,154.01) a tonne.

The dollar retreated broadly against riskier currencies in early trading. It recovered slightly to hold near a 16-month high against the euro ahead of U.S. retail sales data, which could influence the outlook for interest rates.

A weaker dollar makes dollar-priced metals cheaper for other currencies.

Meanwhile, thanks to traders welcoming a dialogue between the U.S. and Chinese presidents, the yuan rose to a five-month high as the conversation between the two presidents appeared to be off to an amicable start.

“Old Friend”

Biden and Xi emphasized their responsibility to the rest of the world to avoid conflict. During the conference held via a virtual phone call, Xi called Biden an “old friend” emphasizing improved communication and cooperation between the two countries.

The two leaders have agreed to hold talks on their nuclear arsenals, having discussed their need for “strategic stability.” The move suggests that the United States is taking the nuclear threat posed by China more seriously.

The U.S. and China also reportedly discussed during their call a coordinated action to release strategic oil reserves in order to lower prices.

U.S. officials have been pressing their Chinese counterparts to close the gap on promised purchases of U.S. energy, agricultural products, and medical devices to improve other areas where China has not lived up to its trade commitments to respect intellectual property provisions.

A Rising Tide

While commodities were up broadly across the market, copper was up significantly more than the rest. While President Xi Jinping did not join other world leaders for the COP26 conference, it is clear that China’s participation in the summit with President Biden is a step in the right direction.

China has attempted to cool copper and other commodity prices by releasing state reserves to the market, to no avail. Prices continued to rise even after the reserves were released, following a slight drop in prices as traders adjusted.

Inventories on the LME are low, and shipping and other logistical backlogs are creating problems for deliveries for key metals and minerals. For now, the inventory issue will need to be solved in the short term, with future copper projects brought online faster than currently forecasted to keep up with demand.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Collective Mining (TSXV:CNL) announced on Monday that their follow-up drilling on the recent grassroots discovery at the Donut target intercepted long and continuous zones of mineralization from the surface. The Donut target is at the Guayabales project in Colombia and is the first out of five outcropping and grassroot targets generated by the Company to be drill tested.

The company currently has two diamond drill rigs on site as part of its maiden 10,000 metre drill program with a third rig to be added in early Q1, 2022.

Ari Sussman, Executive Chairman of Collective Mining, commented: “We are absolutely thrilled with the results of the first five drill holes into Donut, which is a complete virgin grassroots discovery. Importantly, the results mark an important step in our vision of once again untapping the enormous geological potential of Colombia by discovering the next large-scale deposit in the country. The first ever drill hole is now advancing in the Box target and later this month, we will begin drilling our maiden hole into the Olympus target.”

Highlights from the press release are as follows:

- Broad and continuous gold (“Au”) and silver (“Ag”) mineralization hosted predominately in breccia has been intersected from surface in diamond drill holes DOC-3 and DOC-4 at the Donut target as follows:

- Drilled to the north, DOC-3 intercepted 163 metres at 1.3 g/t gold equivalent from surface including 2 metres at 83.2 g/t gold and 37 g/t silver from 155.6 metres depth; and

- Drilled steeply to the southwest, DOC-4 intercepted 260 metres at 0.6 g/t gold equivalent from surface including 69 metres @ 0.9 g/t gold and 8 g/t silver from 183 metres depth (DOC-4).

- DOC-5, which was drilled to the southeast, intersected a narrower interval of mineralized breccia before passing through a fault. Upon exiting the fault at 81 metres down-hole, late phase (lower grade) porphyry style mineralization was encountered over a significant interval as follows:

- 275 metres at 0.2 g/t gold, 5 g/t silver, 0.07% copper from surface.

- Donut is located at the NW end of a SW trending zone of outcropping breccia mineralization which, to date, has been traced to the SW for 550 metres along strike and remains open for further expansion to the SW.

“Potassic altered diorite porphyry overprinted by phyllic assemblages and sulfide cemented breccia dominate Donut drill holes. Banded quartz-magnetite veins cutting diorite porphyry at depth and as common clasts in breccia at shallower levels indicates excellent potential to discover a large porphyry system nearby the existing new breccia discovery at Donut,” commented Dick Tosdal, Special Advisor to Collective Mining and world-renowned expert on porphyry systems.

This intercept confirms that a porphyry system exists in the Donut target area. In order to better pinpoint a potential location for a concealed well-mineralized porphyry, a special survey is planned and once that is completed there will be follow-up additional diamond drilling.

Drilling was recently completed for holes DOC 6 through DOC 10 and samples were sent to the lab for analysis. Additional assay results are expected in Q4, 2021.

Figure 1: Plan View of the Guayabales Project and the Donut Target is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/73fc402b-5fb4-451b-85d0-e3ae439b457d

Figure 2: Plan View of the Donut Target Area is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/45408cf8-9286-4069-a56a-e7e73836c984

Figures 3: Drill Core Photos are available at:

DOC-3: https://www.globenewswire.com/NewsRoom/AttachmentNg/c796b708-f7c3-44f9-99fb-524f1eba9b9b

DOC-4: https://www.globenewswire.com/NewsRoom/AttachmentNg/e386c984-4141-4fc7-811f-e39c728c87d4

DOC-5: https://www.globenewswire.com/NewsRoom/AttachmentNg/9c3290f1-f9cf-4c16-8855-d5e1ba0be905

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

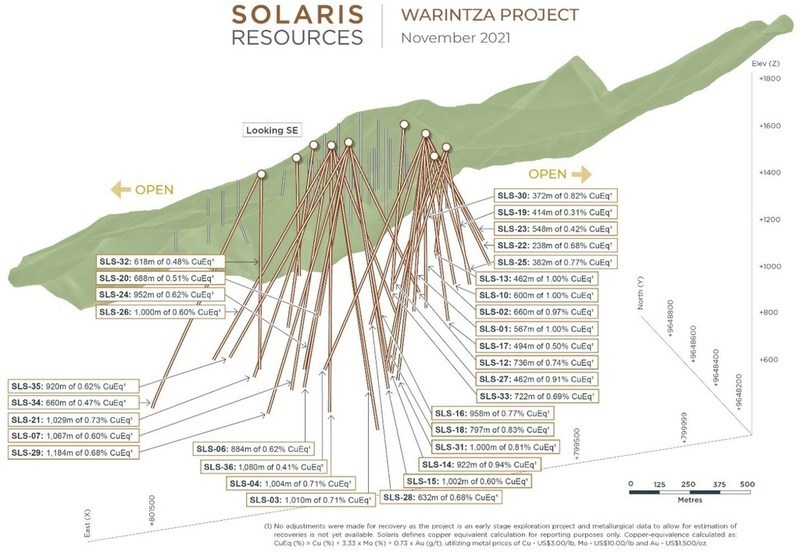

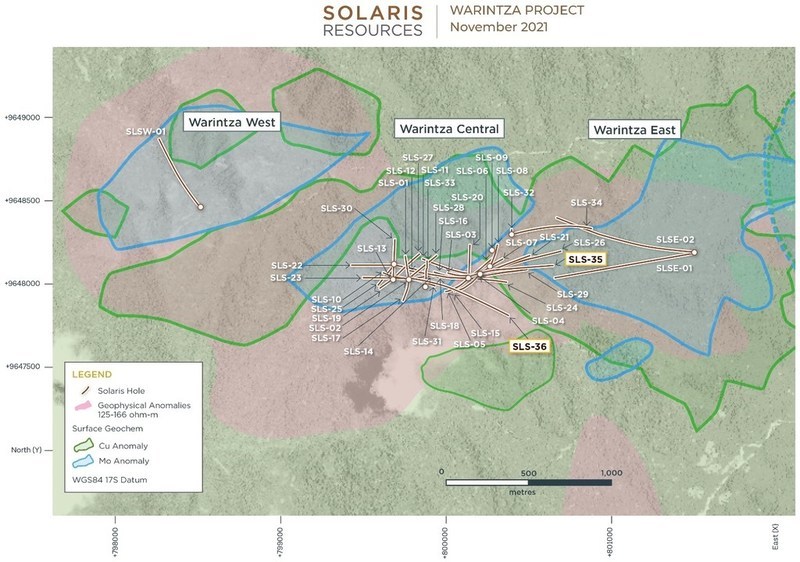

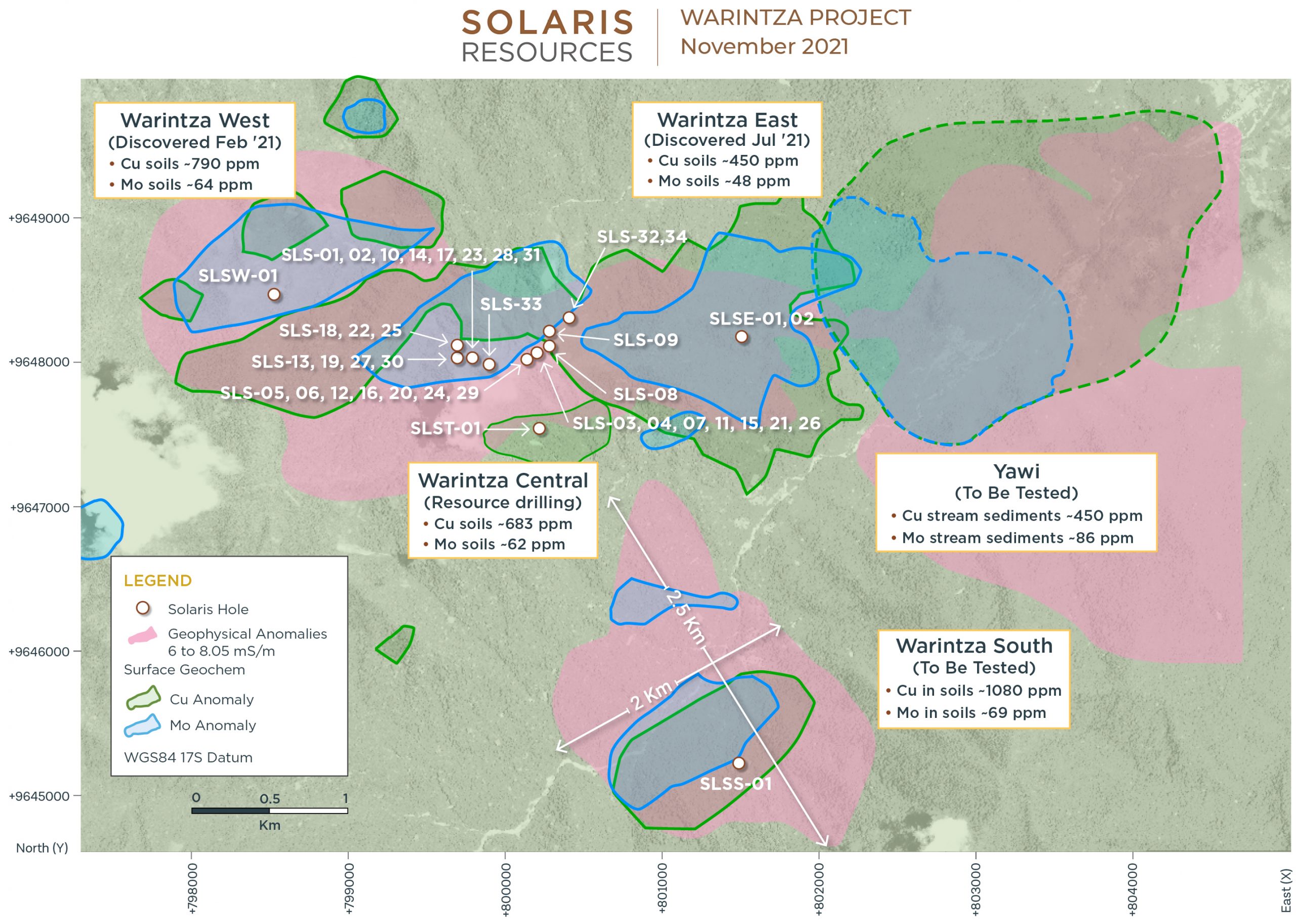

Solaris Resources (TSX:SLS) announced this morning its assay results from a set of additional holes from ongoing resource growth and discovery drilling programs at the Warintza Project in southeastern Ecuador.

Vice President, Exploration Mr. Jorge Fierro, commented: “We are pleased to see the continued growth of the Warintza Central zone, with every hole drilled having hit significant mineralization and the dimensions of the zone open and growing to the east, and broadening to the north and south where additional assays are expected soon. Our drilling fleet has now been fully reoriented to pursue aggressive growth and discovery drilling over the balance of the year and into 2022.”

The highlights from the project are as follows:

- Two additional holes reported in this press release have extended the dimensions of Warintza Central zone to the south and east, with the highest-grade intervals in each hole starting at or near surface

- Southern extension drilling in SLS-36 together with northern step-out drilling previously reported on October 12 in SLS-32, which returned 618m of 0.48% CuEq¹ from surface, including 372m of 0.64% CuEq¹ from 46m depth, have widened the Warintza Central zone

- SLS-35 was collared at the southeastern limit of the Warintza Central grid and drilled into a partially open volume to the east, returning 920m of 0.62% CuEq¹, including 326m of 0.80% CuEq¹ from 50m depth, extending mineralization to the east where it partially overlaps Warintza East

- SLS-36 was collared in the middle of the Warintza Central grid and drilled into an open volume to the southeast, returning 1,080m of 0.41% CuEq¹ from surface, including 290m of 0.81% CuEq¹ from 46m depth, extending mineralization by at least 200m to the south where it remains open

- To date, 50 holes have been completed at Warintza Central with assays reported for 36 of these

Source: Solaris Resources

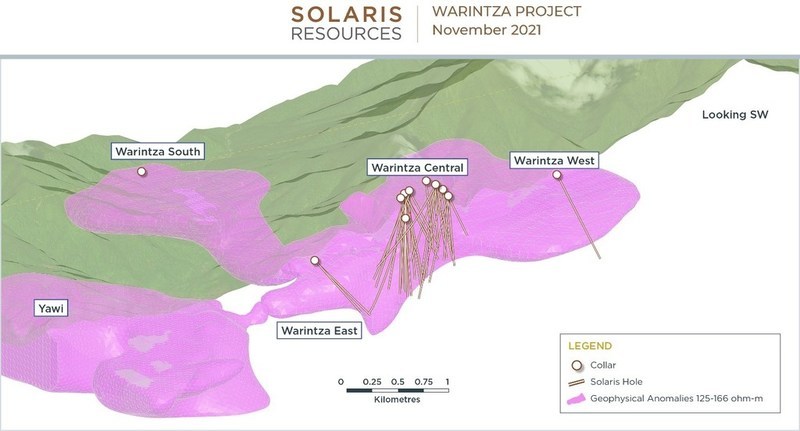

Future drilling will be focused on extensional and step-out drilling. This includes establishing the potential link to the Warintza East zone, discovery drilling at the other well-defined targets within the 7km x 5km Warintza cluster of copper porphyries, and focusing on the untested gold potential.

Drilling Continues in Harmonious Alliance

A strategic alliance was made between Solaris and the Shuar communities of Warints and Yawi in 2019 to overlook and engage in direct and transparent dialogue regarding all Warintza Project-related activities. This alliance allows the people of the community to build and promote trust, reciprocal support, cooperation and strengthen the decision-making capacity of the community. It allows them to have a voice in their community when direct change is taking place.

The company states the mandate will include but not be limited to positive results including employment, business development opportunities, appropriate health care, and emergency care services, development of community infrastructure, and education and skills training.

The Warintza Project is situated in southeastern Ecuador, in the same belt as the Fruta del Norte and Mirador mines, adjacent to San Carlos – Panantza copper deposits. Solaris Resources also has four other current gold and copper projects, including La Verde in Mexico in which Solaris has earned a 60% interest via JV with Teck Resources.

There is also the Tamarugo in Chile which is an undrilled, grassroots copper porphyry exploration target in the Chilean copper belt, and the Capricho Paco Orco in Peru which is a Grassroots exploration project. The final project is Ricardo in Chile, it is a brownfield copper porphyry exploration project immediately contiguous and on the same structure as Chuquicamata, one of the largest copper mines in Chile.

Table 1 – Assay Results

|

Hole ID |

Date Reported |

From (m) |

To (m) |

Interval (m) |

Cu (%) |

Mo (%) |

Au (g/t) |

CuEq¹ (%) |

||

|

SLS-36 |

Nov 15, 2021 |

2 |

1082 |

1080 |

0.33 |

0.01 |

0.04 |

0.41 |

||

|

Including |

46 |

336 |

290 |

0.67 |

0.03 |

0.08 |

0.81 |

|||

|

SLS-35 |

48 |

968 |

920 |

0.53 |

0.02 |

0.04 |

0.62 |

|||

|

Including |

50 |

376 |

326 |

0.69 |

0.02 |

0.05 |

0.80 |

|||

|

SLS-34 |

Oct 25, 2021 |

52 |

712 |

660 |

0.36 |

0.02 |

0.06 |

0.47 |

||

|

SLS-33 |

40 |

762 |

722 |

0.55 |

0.03 |

0.05 |

0.69 |

|||

|

SLSE-02 |

0 |

1160 |

1160 |

0.20 |

0.01 |

0.04 |

0.25 |

|||

|

SLS-32 |

Oct 12, 2021 |

0 |

618 |

618 |

0.38 |

0.02 |

0.05 |

0.48 |

||

|

SLS-31 |

8 |

1008 |

1000 |

0.68 |

0.02 |

0.07 |

0.81 |

|||

|

SLS-30 |

2 |

374 |

372 |

0.57 |

0.06 |

0.06 |

0.82 |

|||

|

SLSE-01 |

Sep 27, 2021 |

0 |

1213 |

1213 |

0.21 |

0.01 |

0.03 |

0.28 |

||

|

SLS-29 |

Sep 7, 2021 |

6 |

1190 |

1184 |

0.58 |

0.02 |

0.05 |

0.68 |

||

|

SLS-28 |

6 |

638 |

632 |

0.51 |

0.04 |

0.06 |

0.68 |

|||

|

SLS-27 |

22 |

484 |

462 |

0.70 |

0.04 |

0.08 |

0.91 |

|||

|

SLS-26 |

July 7, 2021 |

2 |

1002 |

1000 |

0.51 |

0.02 |

0.04 |

0.60 |

||

|

SLS-25 |

62 |

444 |

382 |

0.62 |

0.03 |

0.08 |

0.77 |

|||

|

SLS-24 |

10 |

962 |

952 |

0.53 |

0.02 |

0.04 |

0.62 |

|||

|

SLS-19 |

6 |

420 |

414 |

0.21 |

0.01 |

0.06 |

0.31 |

|||

|

SLS-23 |

May 26, 2021 |

10 |