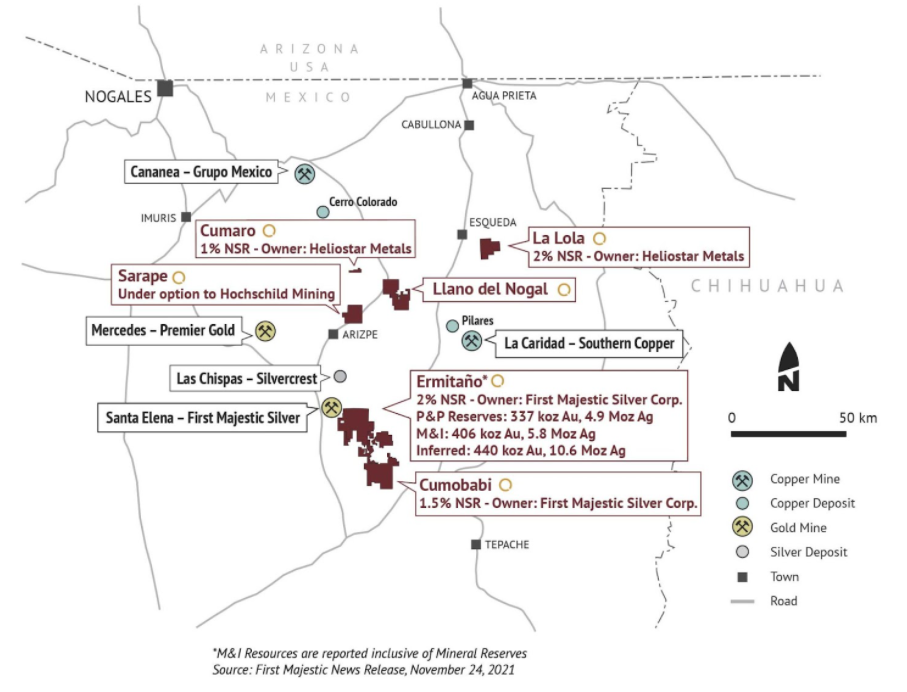

Orogen Royalties (TSX-V: OGN) will be on investors’ radar in the coming weeks with news about their Ermitaño and Silicon assets. Revenue from their 2% NSR on First Majestic’s Ermitaño project is forecasted to begin in Q1 2022. A NI 43-101 on Ermitaño is also expected to be released within weeks. Orogen’s other flagship royalty is a 1% NSR on the Silicon project in the Beatty District of Nevada, where AngloGold Ashanti’s activities have led to anticipation of drill results.

Organic royalty generator

Orogen was created in August 2020 from the merger of two established exploration companies: Evrim Resources and Renaissance Gold. The switch to a royalty model was seen as a way to unlock market value based on near-term production from Ermitaño and Silicon.

However, Orogen is entering a saturated royalty market and, relative to larger players, faces a high cost of capital for asset acquisition. For this reason, Orogen aims to leverage its geological talent and prospecting experience to generate new royalties organically.

As Lawrence Pryer, Orogen’s Exploration Manager states, “in a royalty market that is incredibly saturated, we believe the technical expertise that we have will allow us to continue to generate a pipeline of royalty assets…. We also have a royalty division searching out opportunities that might be overlooked by some of the larger companies.”

Ermitaño and Silicon

Among their flagship assets is a 2% NSR on Ermitaño, an epithermal gold and silver deposit in the Sonora State, Mexico, owned by First Majestic (FM). FM has invested about $80M developing the project and inferred resources are 10.6 Ag (M oz) and 440 Au (k oz) with continued research expansion potential. An updated 43-101 is soon expected for FM’s Santa Elena project. For the first time, the report will include the Ermitaño project, which FM CEO Keith Neumeyer has stated is “going to be pretty exciting for the market”.

Orogen’s current revenue estimate of US$12.5 million over a 7 year mine life is based on 35% of total resources presently converted to the defined P&P Reserve. Therefore, Orogen expects US$27-30 million revenue from Ermitaño over 10-12 years. With production ramping up in Q1 2022, Ermitaño could permit Orogen to move from a $600k (projected) cash burn in 2022, to profitability.

Orogen’s other main asset is Silicon, an epithermal gold play in southwest Nevada. AngloGold Ashanti purchased Silicon in 2020 for $3M plus 1% NSR covering 15,000 acres. AngloGold recently acquired Corvus, which owned the land surrounding Silicon, for US$370 million to consolidate assets in the Beatty District, one of the largest new gold districts in the state. They have also drilled over 70,000 meters in the area in recent years.

The acquisition and extent of drilling have led to much anticipation regarding drill results and resource estimates for Silicon. In an August 2020 presentation about the project, Orogen Chief Geoscientist Mark Coolbaugh said, “the AngloGold geologists are very anxious to tell their story…they have some interesting things to say about what should prove to be a very interesting gold deposit”.

AngloGold intends to initially develop the North Bullfrog project to production in the next 3-4 years, followed by Silicon. Therefore, compared to Ermitaño, Silicon is a medium-term development.

Other assets and valuation

With Silicon several years from production, Orogen will look to generate cash flow and unlock shareholder value elsewhere in their asset portfolio. Their recent sale of the Axe Project is one such example, where Orogen received 950,000 shares of Kodiak Copper.

Orogen currently has 12 active royalty assets which, aside from Ermitaño, are all in exploration or drilling stages. They also have 14 active joint ventures and 9 assets available for a joint venture.

Orogen’s current market cap. is about 80M. The near-term NSR from Ermitaño alone could be enough to put it within a 30 to 50 times earnings multiple range that is typical of royalty companies. As reports on Ermitaño and Silicon come in, a valuation picture for Orogen should become more clear, based on a discounted cash flow model from both projects.

The two flagship assets, together with the portfolio and technical expertise of the team, could be enough for investors to see Orogen as a way to combine solid valuation fundamentals with the upside potential of prospect generation.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

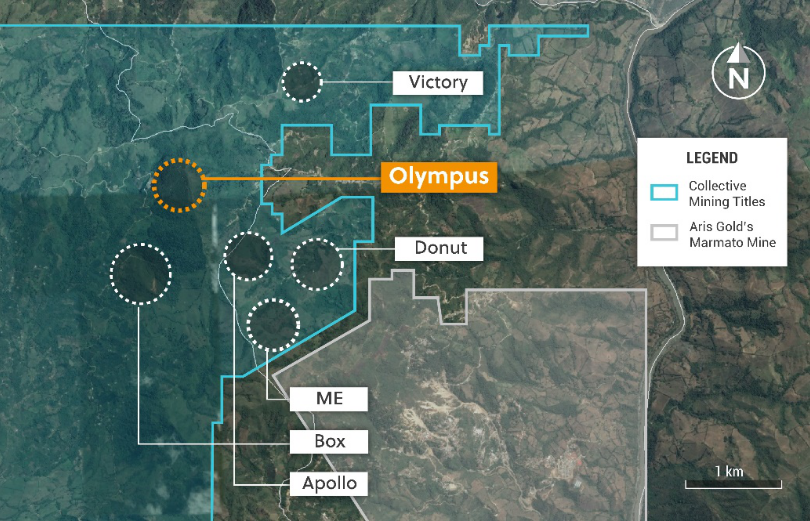

After a busy and successful 2021, Canada-based junior gold mining company Collective Mining (TSXV:CNL) is charting a path forward for 2022 that will highlight it’s Guayabales and San Antonio projects in Caldas, Colombia. After being listed on the TSX Venture Exchange through an RTO on May 28, 2021, the company went on to achieve a number of successful exploration campaigns at the Guayabales and San Antonio projects.

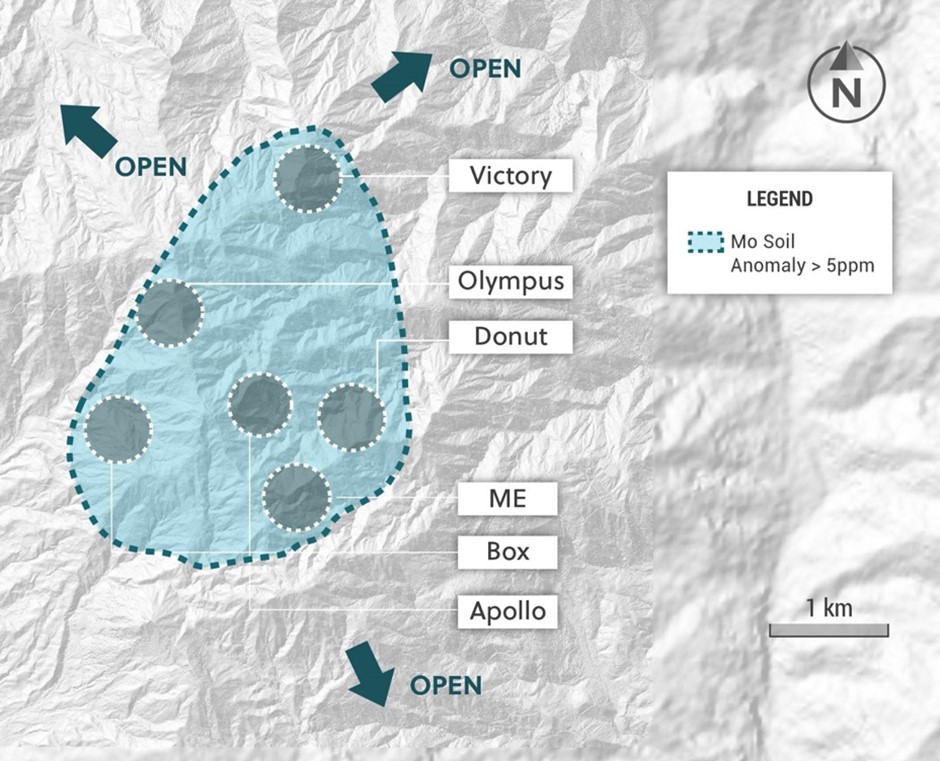

As a result of the success of the drill programs and discoveries, the company has decided to focus on some key targets in the new year. At Guayabales, the Olympus and Victory targets will be the focus of the drill campaign, but the company is also planning additional metres of drilling at the Donut and Box targets. The company has pushed up deadlines thanks to the success of the program so far and may do so again. If the exploration results in the first half of 2022 are successful, Collective could begin to test the earlier-stage Apollo and ME targets.

On the other side of the 20,000+ metre diamond drilling program, a deep penetrating ground IP survey will bein in January 2022 at San Antonio. Upon completion of the survey, the company will begin its follow-up drill program at the Pound target. Collective Mining is also looking at the possibility of testing the COP target at San Antonio for the first time during this period.

2022 is set to be an exciting year for the company, with an accelerated timeline in place for the 20,000+ metre drill program at Guayabales and San Antonio. If 2021 is anything to go by, then it could be another year of discoveries and advancing these two highly prospective properties in Colombia.

Some of the highlights from 2021 include:

Guayabales Project (Figure 1)

4,838 metres of diamond drilling has been completed at the project as of December 22, 2021.

Due to the operating team’s extensive Colombian experience, the Company was able to rapidly advance surface exploration at Guayabales, which in turn lead to the discovery of a 3.5 kilometre x 3 kilometre cluster encompassing six porphyry targets for diamond drilling.

Donut Target: The Company made a significant grassroots discovery with multiple broad drill intercepts in predominantly breccia beginning at surface. Highlights from holes completed to date are as follows:

* AuEq (g/t) is calculated as follows: (Au (g/t) x 0.95) + (Ag g/t x 0.016 x 0.90) + (Cu (%) x 1.83 x 0.92) + (Mo (%) x 4.57 x 0.92), utilizing metal prices of Cu – US$4.00/lb, Mo – US$10.00/lb, Ag – $24/oz and Au – US$1,500/oz and recovery rates of 95% for Au, 90% for Ag, 92% for Cu and Mo. Recovery rate assumptions are speculative as no metallurgical work has been completed to date.

** A 0.1 g/t AuEq cut-off grade was employed with no more than 10% internal dilution. True widths are unknown, and grades are uncut.

Assays for several completed drill holes remain outstanding and will be announced once received in Q1, 2022.

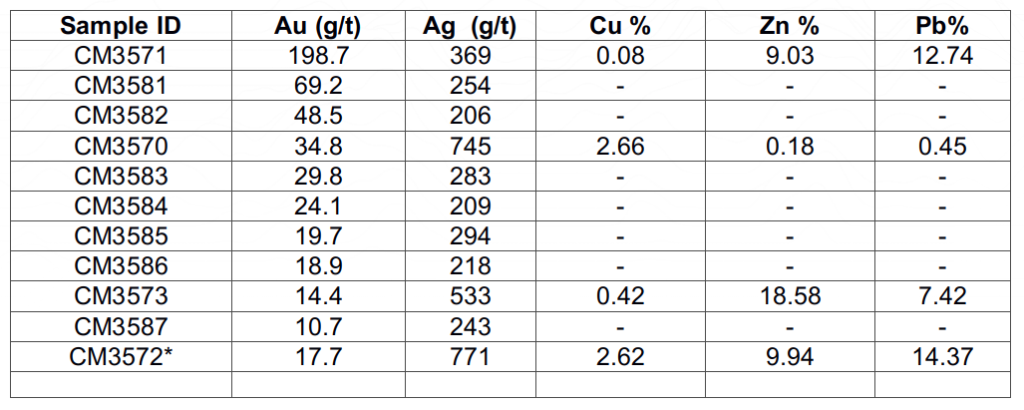

Olympus Target: A high-grade porphyry related, carbonate base metal (“CBM”) vein system, measuring 1,000 metres x 600 metres and open in all directions has been outlined through detailed surface sampling and geophysics. High-grade samples have been collected throughout the target area with highlights as follows:

*The reader should be cautioned that grab samples are selective in nature and as a result should not be relied upon as being representative of average grades anticipated in any future resource estimate or mining scenario.

** Only samples CM003570 and CM003571 reported above were analyzed for base metal grades.

A maiden diamond drilling program utilizing two rigs commenced at the Olympus target on December 1, 2021, and visual logging of the two completed holes to date highlights the discovery of multiple mineralized CBM veins hosted within intensely altered porphyry diorite and hydrothermal breccia units. Initial assay results are expected in January 2022.

Box Target: Three reconnaissance diamond drill holes were recently completed at the Box Target to test an altered and mineralized porphyry target with associated carbonate base metal veins. Visual inspection of the core for drill holes 1 and 3 indicates that multiple CBM veins and altered porphyry style mineralization were intercepted but appears to be distal to a potassic core of a porphyry system. Assay results are expected in mid to late Q1, 2022.

Victory Target: Extensive reconnaissance work is ongoing and has both significantly enhanced the 1000 metre x 600 metre porphyry target and has resulted in the discovery of a new carbonate base metal vein system directly flanking the eastern edge of the porphyry target. Multiple samples from both the porphyry and the Victory East vein target have been collected with results expected in Q1, 2022.

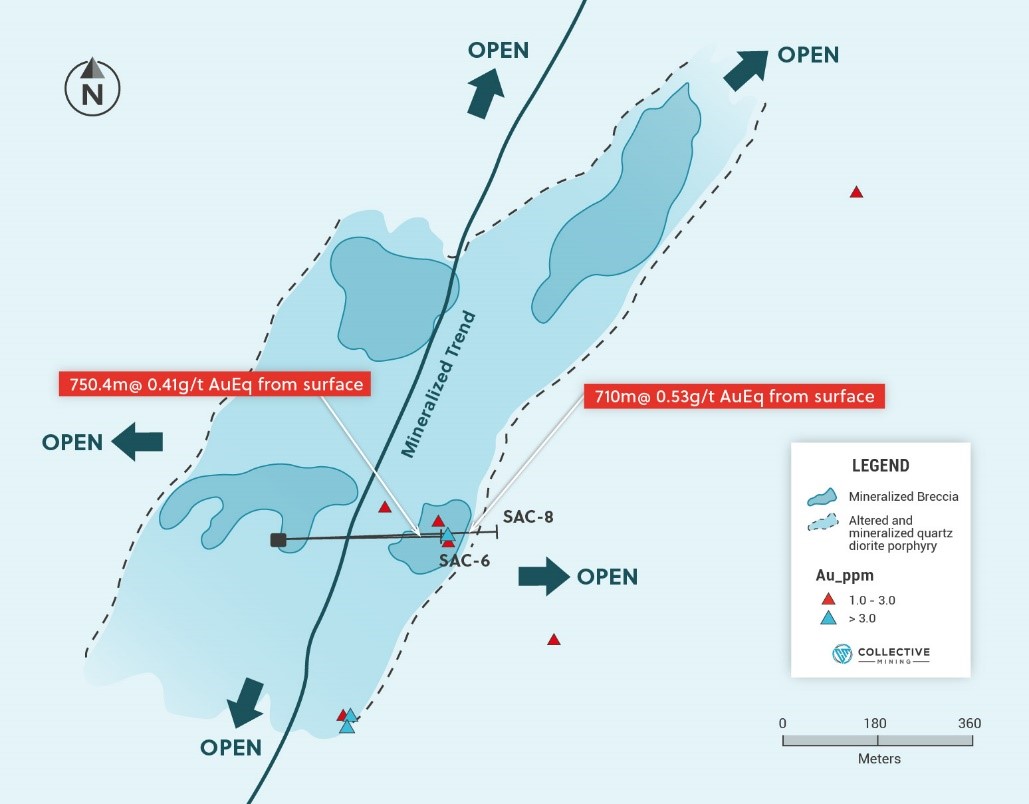

San Antonio Project (Figure 2)

4,310 metres of diamond drilling was completed at the project in 2021 resulting in a significant bulk tonnage grassroots discovery at the Pound Target. Mineralization at Pound, which begins from surface, is related to hydrothermal breccia and highly altered quartz diorite intrusive which have been overprinted by late stage, polymetallic veins. Subsequent follow up exploration has expanded the strike length of the target to at least 1.3 kilometres with assay results as follows:

* AuEq (g/t) = (Au (g/t) x 0.95) + (Ag g/t x 0.013 x 0.90) + (Cu (%) x 1.83 x 0.92) + (Mo (%) x 4.57 x 0.92), utilizing metal prices of Cu – US$4.00/lb, Mo – US$10.00/lb, Ag – $20/oz and Au – US$1,500/oz and recovery rates of 95% for Au, 90% for Ag, 92% for Cu and Mo.

** a 0.1 g/t AuEq cut-off grade was employed with no more than 10% internal dilution. True widths are unknown and grades are uncut.

Corporate and Sustainability

The Company successfully completed an RTO and was listed on the TSX Venture Exchange on May 28, 2021.

The Company raised C$28.5 million through a combination of a private placement financing and the exercise of warrants related to said financing.

As a result of successful exploration campaigns during the course of the year, the Company’s share price gained approximately 200% from the date of listing on the TSXVenture Exchange.

The Company’s multi-pronged and comprehensive ESG program for 2021 resulted in the recognition by local stakeholders as a transparent and trustworthy entity. Numerous programs were implemented throughout the year highlighted by the strategic alliance with the National Coffee Federation of Colombia and the Municipality of Supía to promote water utilities, infrastructure improvements, as well as to provide technical assistance for more than 400 coffee-growing families representing 6,000 people from 35 different communities.

Source: Collective Mining

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Vale (NYSE:VALE), the international mining giant, may be looking to buy a 30-40% in Anglo American’s (LSE:AAL) Minas-Rio iron ore project in Minas Gerias, Brazil, according to some reports. If the deal happens, Vale could look to acquire an operatorship stake in the project as well.

Located in the states of Minas Gerais and Rio de Janeiro in the south-eastern region of Brazil, Minas-Rio is an iron ore project 100% owned by Anglo American. The project is estimated to produce more than 26.5 million tonnes of iron ore per year.

The area is also known for hosting the world’s largest iron ore mine by reserves, Carajas, which belong to the Brazilian mining company Companhia Vale do Rio Doce (CVRD). Minas-Rio and Carajás work together in areas such as logistics and rail transportation. It also consists of a 529 kilometre pipeline, filtering plants, and export terminal location in the Atlantic port of Acu in Rio de Janeiro state.

Anglo American (LSE:AAL) bought the rights from MMX back in 2008. While annual production for phase one of operations is expected to be below 30 million tonnes, probable reserves have been estimated at 1.45 billion run-of-mine (ROM) tonnes back in February 2013. This would leave plenty of production capacity for Vale if the miner decides to acquire a stake in the project. Considering the billion-plus tonnes in probable reserves, this project could bring Vale much closer to its production target. It would also solidify the company’s position as a dominant global supplier of premium iron ore.

Vale’s (NYSE:VALE) Dominant Position in Iron Ore

Vale (NYSE:VALE) is one of the biggest mining companies in the world, and one of the most dominant suppliers in the global iron ore market. The company is set to produce close to 350 million tonnes of iron ore this year, making it by far the biggest producer of all top mining companies. Vale produces more than twice as much raw material in comparison to number two, Rio Tinto.

If the deal goes through in Minas Gerais, Vale could have access to a significant portion of Anglo American’s production at the project, with no signs of slowing down their expansion plans anytime soon. However, there are some concerns over how this would affect Vale’s own stock prices if they were actually buying another project at a time when commodity demand has been declining due to slower economic growth in China, which is also reducing volumes sold through major iron ore suppliers into that market.

The deal has not been confirmed yet and is subject to some speculation, but it could help Vale with its key production targets in the short term if they do sign off on a deal.

Vale buying Minas-Rio would certainly be good news for both companies involved, as Minas-Rio has proven reserves and an existing infrastructure so it’s easier and faster for Vale to get the product to market than starting from scratch.

Take an Operatorship Stake

When a mining company takes an operatorship stake in a project, it means the company is taking the responsibility for mining and selling all of the product from that project. The owner of a project with an operatorship agreement usually gives its partners access to a set amount of raw material each year depending on agreed-upon rates, but a mine under operatorship has 100% control of production and sales going forward.

This can be very profitable for both parties because the operator can control production and sales without having to pay the owner any additional fees for taking on operatorship. It’s also beneficial to both parties because the mining company is now able to focus on making money from its own mine instead of renting out part of it.

Iron Ore Gaining Traction

Iron ore production is gaining traction again after the pandemic slowed production due to a demand dearth. The largest importer of iron ore is China, and there was a significant reduction in China’s imports of iron ore as the country started importing less coal and steel to cope with the pandemic.

China has recently increased its coal and steel production, which means it will likely increase raw material demand as well. This is good news for Vale because increased demand from China should help push prices up significantly even if it doesn’t acquire Minas-Rio.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

A new merger between China’s largest rare earth producers is set to create one mammoth company in an industry that is becoming more critical and competitive every year. Minmetals Rare Earth Co. has said that it will be merging with two of the country’s other top rare earth producers to create a new company that will operate under the state assets regulator. The deal will see Minmetals Rare Earth, Chinalco Rare Earth & Metals Co, and China Southern Rare Earth Group merge into a new company. Two other companies will be included in the new entity: Jiangxi Ganzhou Rare Metal Exchange Co, a new bourse for spot transactions, and Ganzhou Zhonglan Rare Earth New Material Technology Co.

This will give the new company control over a wider range of assets, and might allow the company to control pricing. This could bring more tensions to the table between the United States and China.

China currently controls 85-90% of the rare earths processing industry, and there is a reliance on China by the United States as a result. The creation and announcement of the approval of the new larger company by the State-owned Assets Supervision and Administration Commission (Sasac) could intensify the competition in the space.

Light vs. Heavy

There is some competition for the rare earth smelting and separation (processing into a form used by manufacturers) industries. This is divided into the light rare earths and heavy rare earths. Light rare earths are easier to process and are viewed as the lesser rare earths. There is a division between China and Southeast Asia, versus Japan and North America. On the other hand, heavy rare earths are becoming more important in manufacturing technology because they have magnetic qualities that allow them to be used in electric cars, wind turbines, and hard drive components.

There is investment in separation in Australia, the United States, and Britain, but that separation is for light rare earths. Even if investment in the sector continues outside of China, for the foreseeable future, heavy rare earth separation would need to be done in China.

Heavy rare earths are more important than the light ones because they are used in many of the technologies that we depend on today. This is especially true for countries like Japan and South Korea that rely on manufacturing technology, and who could become less dependent on China if investment into heavy rare earth separation continued outside of China.

Some of the rare earths critical for magnets used in electric vehicles and wind turbines are dysprosium and terbium, and pricing for these has been up approximately 50% in 2021. Two factors have contributed to the price jump, as demand drives higher, and power disruptions for Chinese industry have forced production lower.

If the newly merged company can create a sufficient moat around pricing, then China could continue to dominate the rare earths separation industry globally. Now, industry watchers will be waiting to see what the combined production and coordination will mean for the rare earths industry.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

As the shift towards electric vehicles (EVs) gears up to full speed, rising opposition towards new mines in regards to the environment has started to become louder in recent months. The United States has plenty of reserves of copper, lithium, and other important metals to build millions of EVs, but looming concerns surrounding existing and future mines may end up delaying this transition.

The tension between environmentalists and miners won’t be going anywhere as we head into 2022, when US policymakers are expecting groundbreaking moves from big names such as Ford Motor Co, General Motors, and more.

Just earlier this year, President Joe Biden danced around the idea that he prefers to rely on outside allies to supply EV parts in an effort to calm down environmentalists. For U.S automakers, this choice could result in stressful competition with international suppliers as everyone seems to be ready to go electric. Biden also issued an executive order to ideally create half of all new vehicles electric in 2030.

Choosing to import metals rather than getting them from the US is somewhat counterproductive from an environmental standpoint. It could end up boosting greenhouse gas emissions when shipping overseas to the US processing facilities, which defeats the purpose of building EV’s in an effort to combat these climate issues.

An analysis done by Reuters found that “proposed U.S. mining projects could produce enough copper to build more than 6 million EVs, enough lithium to build more than 2 million EVs and enough nickel to build more than 60,000 EVs.”

Those estimates were made based on the volume of minerals used to make the world’s most popular EV, the Tesla Model 3, according to a study by Benchmark Mineral Intelligence. Other EV models and companies may use a different volume depending on their make and design.

James Calaway, executive chairman of Ioneer Ltd, a lithium-boron supplier, said “If we don’t start getting some mining projects under construction this coming year, then we will not have the raw materials domestically to support EV manufacturing.”

Many states have chosen to or are on the fence about opposing future mining projects and reversing decisions already made regarding building new mines. Washington is one of the places still figuring out how to balance regulating mining and the environment. For example, the U.S Fish and Wildlife are adamant about labelling a rare flower that lives on Ioneer’s Nevada lithium site as endangered. Simultaneously, The U.S Department of Energy is deciding if they are going to lend the company over $300 million to build the mine.

Conflicting Agendas

That is just one recent example of the confusion surrounding wanting to combat climate change while also not wanting to build new mines to create necessary materials to build EV’s in an effort to combat climate change.

In Minnesota, state regulators are debating whether or not to revoke or reissue permits to PolyMet Mining Corp, which is controlled by giant miner Glencore. In early 2022, judges will decide whether or not to reverse mines that were already approved by Former President Donald Trump to Lithium Americas (TSX:LAC) and Rio Tinto PLC (ASX:RIO).

Even Biden chose to block Antofagasta Plc’s (LSE:ANTO) Twin Metals copper and nickel mine project in Minnesota for 20 years this past October. The future underground mine would have been a major copper supplier towards EV’s in the US.

Despite that decision, the White House is working towards showing its support for the mining industry, including Lithium Americas’ proposed lithium mine, and a California geothermal lithium project funded in part by GM.

Biden’s EV goal “means good-paying union jobs for working people in responsible mining operations that will both supply battery minerals and protect the environment,” Tom Conway, head of the United Steelworkers recently said.

It will be a long-lasting challenge trying to balance what is best for the environment and what needs to happen for the economy in order to support the mining industry and green transition.

Gabriel Boric, a young leftist millennial was just elected as Chile’s new president on Sunday, and he is ready to make important changes for the nation and fellow Chileans.

Boric won 56% of the votes compared to his main opponent, lawmaker José Antonio Kast, who won 44% of the votes with more than 90% of polling stations releasing their data.

One of the first major changes of the young new leader will be drafting a new constitution, which will likely bring about updated legal and political changes surrounding environmental issues, gender inequality, Indigenous rights, just to name a few important issues.

One of those issues, mining, remains in the balance as some of the world’s biggest mining companies wait for decisions and the new president to set the tone through policy.

A Liberal Shift

Boric, who is 35, will be the youngest leader of Chile and most liberal since President Salvador Allende, who left behind a 17 year long excruciating dictatorship. Kast, who has a past of supporting the past military dictatorship, tweeted a photo of himself and Boric congratulating him on his “grand triumph,” saying “from now on, he is the president-elect of Chile and deserves all our respect and constructive collaboration.”

Outgoing President Sebastian Pinera also held a video conference call with Boric to congratulate him, and said “I am going to be the president of all Chileans,” in his brief TV appearance.

Boric will take over the office in March, and was able to win the majority of the votes from the public by committing to change the lasting effects from the 1973 to 1990 dictatorship. He plans to raise taxes on the “super-rich” in order to expand social services, fight inequality and focus on ways to help the economy into the green movement by implementing more environmentally friendly methods for production.

“We are a generation that emerged in public life demanding our rights be respected as rights and not treated like consumer goods or a business,” Boric said. “We know there continues to be justice for the rich, and justice for the poor, and we no longer will permit that the poor keep paying the price of Chile’s inequality.”

Mining Companies Wait for Decisions

As Chileans celebrate the young leader and his potential, important and necessary changes the country needs, it is somewhat unclear how the mining industry will adapt to new changes from the millennial president. As talks of a greener economy continue, Boric does not want to take away incentives to invest in the mining sector, according to Kracht, head of the mine engineering department at the University of Chile and a director at copper research center CESCO. However, Boric may find difficulty balancing his agenda with balancing the success of the country’s mining industry.

“There’s no intention to change the rules of the game, just to strengthen institutionality so that things function better,” Kracht said.

Chile is home to some of the biggest copper mining companies in the world, including state-owned Codelco, BHP Billiton (ASX:BHP), Glencore (LON:GLEN), Anglo American (LON:AAL) and Antofagasta (LON:ANTO). Having this many big miners in one country shows the work Boric has cut out for himself in the coming years.

The National Mining Society (Sonami) said in a statement that voters have “sent a clear message” about the need to maintain Chile’s economic and social development. “We trust that the spirit of programmatic convergence, moderation and openness to dialogue shown during the last week of the campaign will prevail,” it added.

However, an already alarming decision has already been made from Boric regarding future mining operations. He pledged to oppose the $2.5 billion iron-copper mine, known as the Dominga mine, which was just approved in August after years of legal battles back and forth.

“We don’t want more ‘sacrifice zones’ (areas of high pollution), we don’t want projects that destroy our country, destroy communities and we exemplify a case that has been symbolic: No to Dominga,” Boric said.

This is an environmentally controversial project that investors will be watching out for in the future. His pledge to oppose the mine could be seen as a warning shot for companies outside of ESG compliance. Besides such projects, the economic benefits of the mining industry and the large windfall taxes they produce for the country will be at the top of every discussion for Chile’s Constitutional Assembly.

Environmental reform is only one side of the agenda for the incoming President, and while some projects will need to adjust to regulations or shifts in the economic climate, the mining industry is prepared to deal with challenges from a shifting political climate.

Multiple Mineral Channels

Chile is also home to the world’s largest lithium reserves, the important metal that is being used around the world for mainly electric vehicle batteries. These EV batteries eliminate the need for gases and fossil fuels, which have a huge negative impact on the environment.

Boric in the past has criticized privatization in the mining sector and would like to see the state have its own lithium firm. The country is also debating raising taxes on mining firms, which Boric supports, along with a stalled bill to protect glaciers in the mineral-rich Andes. The mining industry fears this new bill could potentially “risk current mines and obstruct new ones.”

Firms affected by these potential changes include Codelco, as well as Anglo American’s Los Bronces, Los Pelambres of Antofagasta, and Caserones, linked to JX Nippon Mining. While major mining companies may see their tax bills rise, junior mining companies could remain largely unaffected as this only applies to certain larger thresholds for projects that exploration companies might not pass.

Boric is passionate about saving the environment, but also understands these changes need to be gradual in order to support its mining firms and economy.

“Not everything can be done at the same time and we will have to prioritize to make progress that allows us to improve, step by step, the lives of our people,” he said.

It is unclear how the decisions of the new, young president will pan out. The environment is an important and necessary aspect of life for everyone, and the mining sector is an important and crucial part of the economy. Mining companies will be anxiously watching for signs of a friend or foe in the Presidential Palace.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Wheaton Precious Metals (NYSE:WPM) announced just last week they will be acquiring the existing gold stream located in the Blackwater Gold Project in British Columbia, Canada. The gold stream is currently being held by New Gold Inc. (NYSE:NGD) and the company will acquire the stream for an upfront payment of $300 million.

Wheaton has also entered into a precious metals purchase agreement with Artemis Gold Inc. (CVE:ARTG) in regards to the silver streams within the Blackwater project. The precious metals company will pay Artemis approximately $141 million upfront, which will be paid in four equal installments during construction at the project. In total, Wheaton will pay $441 million for both streams.

New Gold did sell the Blackwater Gold Project to Artemis last year, except it retained the gold stream as partial consideration.

Randy Smallwood, Wheaton’s President and Chief Executive Officer, commented in a press release: “Artemis’s approach of disciplined, responsible resource development aligns well with our own focus on promoting industry-leading mining practices. We are proud to partner with Artemis in the advancement of the Blackwater Project, which we believe is on track to develop into a top-tier operation, producing socially and environmentally sound minerals, right in our own backyard.”

Under terms of the new gold stream, Wheaton is entitled to receive 8% of the payable gold production until 279,908 ounces have been delivered. Once that amount has been delivered, it will drop to 4% of payable gold production for the life of the mine.

Wheaton will also be entitled to receive 50% of the payable silver production until 17.8 million ounces have been delivered, and will then drop to 33% of payable silver production for the life of the mine.

Wheaton Precious Metals Continue to Hunt for Growth

“The acquisition of the gold and silver streams on the Blackwater Project further enhances and diversifies Wheaton’s existing portfolio of low-cost, high-quality, long-life mines. With strong ESG commitments at every stage of development, compelling economics and significant exploration upside potential, Blackwater incorporates many of the attributes we seek for accretive growth,” said Smallwood.

For the first five full years of production, gold production is expected to average approximately 26 koz per year, and grow up to 28 koz per year for the first ten full years.

Silver production is forecast to average over 480 koz per year for the first five full years of production, and over 670 koz per year for the first ten full years. Compared to Silver, gold’s numbers may seem small, but there is a fixed silver recovery of 61% that also attributes to these amounts.

Steven Dean, Chairman and CEO of Artemis commented in a press release, “The company is very pleased to have completed the Silver Stream Agreement with Wheaton. The purchase by Wheaton of the Gold Stream provides further endorsement of the quality and first-tier status of the Blackwater project. It also facilitates simplification of administration of such agreements through development and operations and magnifies the conviction of the technical and economic merits of the project by a top tier royalty and streaming company. We look forward to working with Wheaton as a trusted partner in the years to come”.

Wheaton has also agreed to make ongoing cash payments for gold and silver ounces delivered depending on the spot price. For gold, it will pay 35% of the spot price. For silver, it will pay equal to 18% of the spot price until the up-front deposit payment is reduced to zero, at which the payments will increase to 22% of the spot silver price.

Artemis is expected to start major construction works for the Blackwater project in the second quarter of next year, and is on track to begin production in the first quarter of 2024.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The global energy future is rapidly evolving due to the construction and high demand for electric vehicles, mass energy storage solutions, and nanotechnology. All require more technology-grade graphite than lithium and cobalt. If the shortage of lithium and cobalt has been a bit nerve-wracking, the shortage of graphite is even more frightening.

In addition to concerns about finding lithium, nickel, and cobalt resources for China to stay on top of the electric vehicle stakes, the country is even more concerned about the supply of a mineral closer to home: graphite.

Graphite is a mineral of high importance as it is naturally and synthetically used for the negative end of lithium-ion batteries. The negative end of batteries is known as the anode.

The vast majority of lithium-ion batteries use graphite powder as the anode material. Graphite materials are either produced synthetically (artificial graphite) or mined from the ground (natural graphite), then heavily processed before being baked into copper foil to serve as anodes.

Approximately 70% of the graphite used in battery anodes comes from China and to this day there are very few alternatives that can replace graphite in battery construction. Graphite is of paramount importance to the economy. This has led to graphite being declared a critical supply mineral.

Demand for graphite for lithium-ion batteries will soar more than 200 percent in the next four years driven by the rise of electric vehicles and energy storage alone. Chinese producers have their work cut out for them to have the capacity to meet global demand for graphite.

Prices are skyrocketing, with spot prices for graphite electrodes reaching $35,000 as Chinese exports dry up.

Benchmark Mineral Intelligence (BMI), a consulting firm, estimates a graphite deficit of approximately 20,000 tons in 2022, compared to a surplus of similar size last year.

Industry experts approximate that 20,000 tons of graphite is needed to build batteries for approximately 250,000 electric vehicles. Demand from electric car manufacturers such as Tesl is growing rapidly, and graphite supply is extremely tight.

Shandong province used to be the center of graphite mining in China, however, its production is declining due to depleting ore reserves and stringent environmental regulations that have been put in place lately. Mining has shifted to Heilongjiang province and it is now the leading producer.

With the approach of the Winter Olympics in Beijing, energy-intensive and carbon-intensive industries, such as graphite, have been asked to cut production as authorities seek to ensure a blue-sky backdrop for the main event.

This has caused the supply of graphite to become even scarcer.

George Miller, an analyst at BMI said, “Graphite consumers, whether inside or outside of China, are fighting for a limited stock of material” in addition, he said graphite mines in northwest China tend to close during the winter due to low temperatures, causing graphite producers to have to fulfill orders from their inventory stockpiles.

BMI has forecasted that global demand for battery anodes will increase by around 27% per year over the next 10 years, driven by the lithium-ion sector of batteries.

The market for large flake and XL graphite is much stronger because the production of expandable graphite is the fastest growing market along with lithium batteries. Expandable graphite is primarily made from large flakes. It is used in thermal management for consumer electronics and many industrial applications, including heat and corrosion-resistant gaskets and fire retardants.

Anode-grade graphite flake prices in the Chinese domestic market have risen nearly 40% so far this year to 4,500 yuan ($707) per ton, testing the all-time highs seen in 2018, according to BMI.

Fuel cells and flow batteries are also new and potentially large markets for expandable graphite. In addition, the steel industry is a major user of large flake and its recovery will put additional pressure on large flake prices.

China’s automotive sector, sold 2.99 million electric and plug-in hybrid vehicles in the first 11 months of 2021 which represents a 170% increase over the same period in 2020. This reflects the rapid growth in the electric vehicle market.

CATL is currently studying the use of the more natural form of graphite in battery anodes as an alternative to artificial graphite due to greater availability although not of the same performance.

In conclusion, graphite is an extremely important material in building our energy future. It is a wonder metal that behaves like a metal and conducts electricity, but also acts like a nonmetal and resists high temperatures.

Graphite is also used to make steel and glass, and to process iron because it is a common refractory material that resists high temperatures without changing chemically.

It is practically everywhere. Power tools, vacuum cleaners, bicycles, solar power, even the military uses it. Hence the urgency of supply is of global concern.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

European battery supplier Northvolt and energy company Galt have announced they will be working together to create a joint venture (JV) company called Aurora, which plans to develop the largest and most sustainable lithium plant in Europe.

The new lithium plant will be located in Portugal and plans to start operations by the end of 2025 and commercial operations by 2026. Galp and Northvolt will have an equal 50% stake each in Aurora, and it is set to have an annual production capacity of up to 35,000 tons of battery-grade lithium hydroxide. Included in the agreement, Northvolt secured an “offtake” of up to 50% of the plant’s capacity for its battery manufacturing.

The main goal of creating a new lithium plant is the fact it is going to be sustainable while also producing the necessary amount of lithium hydroxide. This follows suit with the Portuguese and European industrialization efforts to embrace the green energy transition.

“This is a once-in-a-generation opportunity to reposition Europe as a leader in an industry that will be vital to bringing down global CO2 emissions, in line with European and Portuguese climate-change priorities,” said Galp CEO Andy Brown. “To be successful in this drive, we must all work together, industry and decision makers, with a sense of urgency, because if we do not claim this role today, others will.”

Lithium hydroxide is a crucial material that is required to make lithium-ion batteries, and the new plant will be able to deliver enough lithium hydroxide sufficient for 50 GWh of battery production per year. This equals out to enough batteries for about 700,000 electric vehicles, which is one of the biggest markets that require lithium. The demand for lithium hydroxide alone is estimated to grow at least tenfold by the end of the decade.

The joint venture is still running technical and economic studies regarding the new plant, and is currently looking at several possible site locations for the building. Based on similar projects in the past, this new lithium plant could represent an investment estimated at around $700 million and create as many as 1,500 direct and indirect jobs.

Paolo Cerruti, Co-Founder and COO of Northvolt said in a statement “This joint venture represents a major investment into this area, and will position Europe with not only a path to the domestic supply of key materials required in the manufacturing of batteries, but the opportunity to set a new standard for sustainability in raw materials sourcing.”

The plant and joint venture are focused on making this plant as sustainable and in line with the green energy movement as much as possible. The plant will use a proven conversion process, using recent process improvements and technologies to their advantage to increase sustainability and efficiency.

As well, the joint venture is trying to power the conversion process using green energy, which minimizes and eventually will avoid the use of natural gas altogether. Both Galp and Northvolt are confident that Iberia hosts resources that can be recovered with a low greenhouse gas emission footprint, while complying with the highest standards for environmental and human rights.

“The development of a European battery manufacturing industry provides tremendous economic and societal opportunity for the region. Extending the new European value chain upstream to include raw materials is of critical importance,” said Cerruti.

Galp already has established themselves as a player in the green energy movement, along with being one of the largest solar power generation companies in Iberia, which makes them a good partner for Northvolt. The project is on course to fit within Galp’s decarbonisation path as well on its capital allocation guidelines, as per announcements at the Company’s latest Capital Markets Day.

Northvolt has also made big progress towards the green movement, with a goal to deliver the world’s greenest lithium-ion battery with a minimal CO2 footprint. The company has grown to more than 2,300 people from over 100 different nationalities. The company has also secured multi-million dollar contracts with big names in the car industry such as BMW, Fluence, Scania, Volkswagen, Volvo Cars and Polestar which support its future green plans.

Despite the two companies’ motivation for sustainability and environmentally friendly practices, some local folks are still skeptical of the operation.

Nik Völker of MiningWatch Portugal, a campaign group, said “It seems unlikely that the investment by Galp and Northvolt would benefit the Barroso region in Northern Portugal in the longer term, beyond ore sales during the 12 years of open-pit mine life.”

As the new plant is planned and built, the joint venture will continue to look for and explore other business opportunities along the value chain while maintaining environmentally friendly practices and methods.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

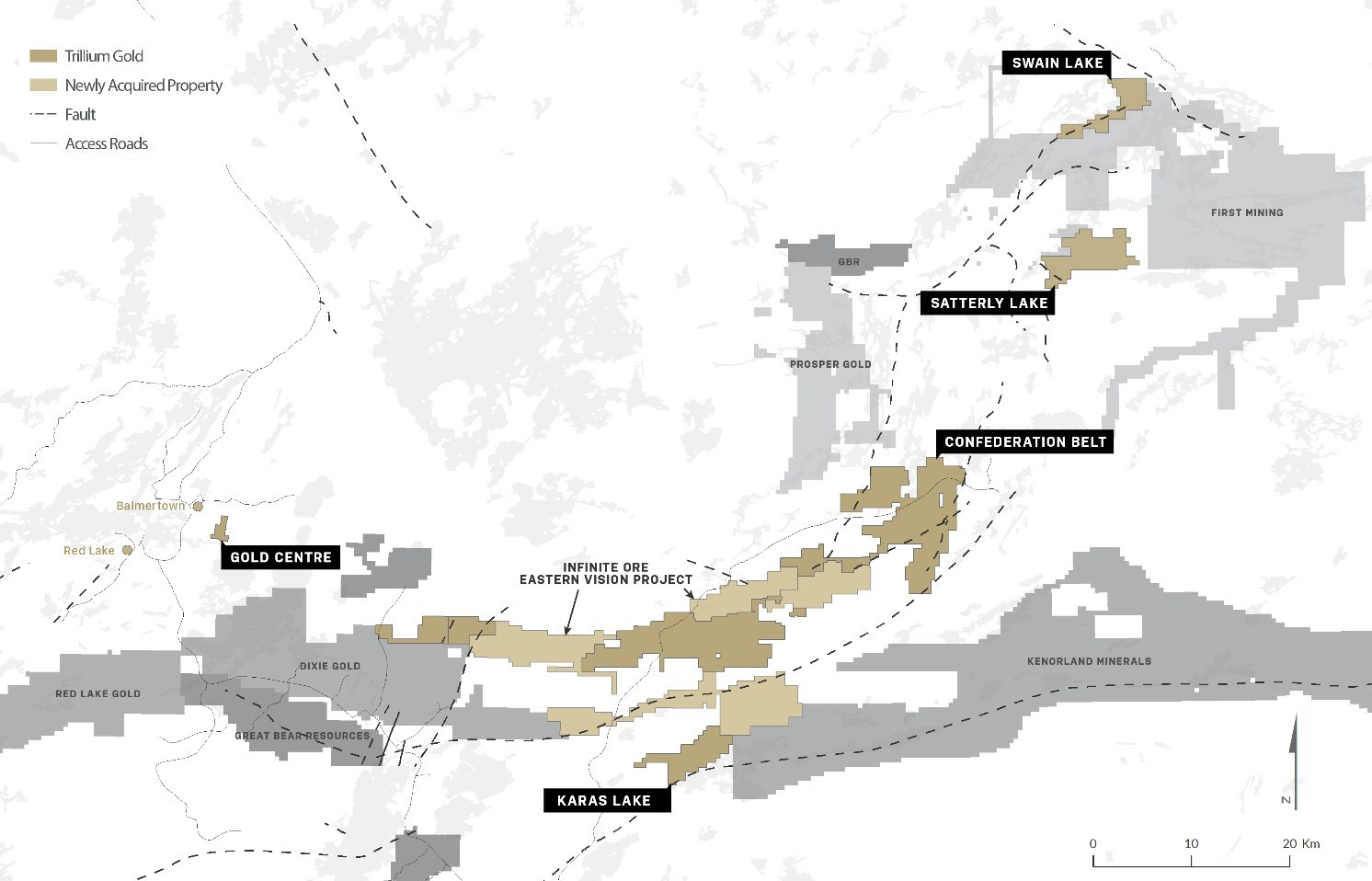

Trillium Gold Mines Inc. (TSXV:TGM) has announced this morning it has signed a definitive agreement to acquire all of Infinite Ore Corp.’s Eastern Vision property holdings in the Confederation lake assemblage of the Birch-Uchi greenstone belt in the Red Lake Mining District, Ontario.

The property holdings include 16,991 hectares between the Fredart, Garnet Lake, Confederation north, and Confederation South properties. Red Lake is the company’s focus, and this acquisition gives Trillium control over a significant portion of the Confederation Lake assemblage and creates a contiguous land package covering over 100 kilometers of favourable structure on trend with Great Bear Resources’ Dixie Deposit.

Red Lake Hotspot

Great Bear was recently acquired by Kinross for C$1.8 billion, a huge acquisition in the Red Lake Mining District. The key focus for the acquisition with the Dixie project, which has shown exciting recent discoveries and the characteristics of a top-tier deposit.

Trillium Gold’s acquisition is on trend with Dixie, placing it in good company in one of Canada’s premier gold mining districts.

The Dominant Exploration Company

Trillium Gold has is focused on properties in the Red Lake Mining District, in particular, its Newman Todd project being advanced toward open-pit mining. The company has assembled on the most extensive property packages in the Confederation Lake assemblage of the Birch-Uchi greenstone belt, and this latest acquisition adds an additional 16,991 hectares to its portfolio. This is a major step in strengthening the company’s strategic advantage to consolidate the greenstone belt and makes the company the most dominant exploration company in the Red Lake Mining District.

Beyond the Red Lake Mining District, Trillium Gold has interests in highly prospective properties in Larder Lake, Ontario, and the Matagami and Chibougamou areas of Quebec.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Collective Mining (TSXV:CNL) has announced new further high-grade, polymetallic vein grab sample results from the western side of the grassroot generated Olympus target at the Guayabales project in Colombia. These are additions to previous grab sample results from the eastern portion of Olympus that were announced on December 1, 2021.

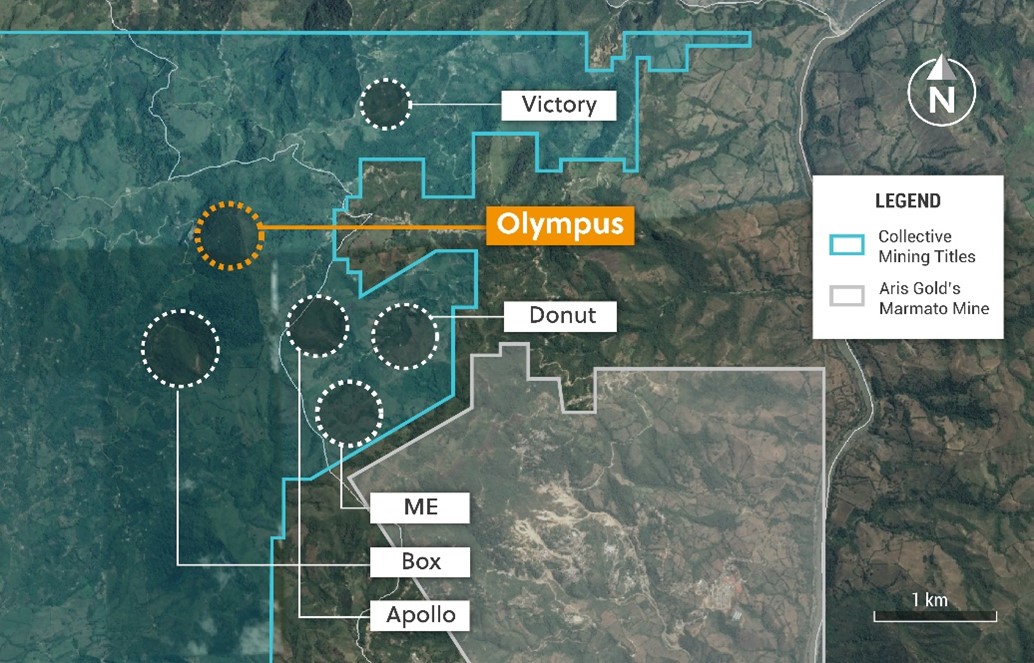

Figure 1: Plan View of the Guayabales Project and the Olympus Target

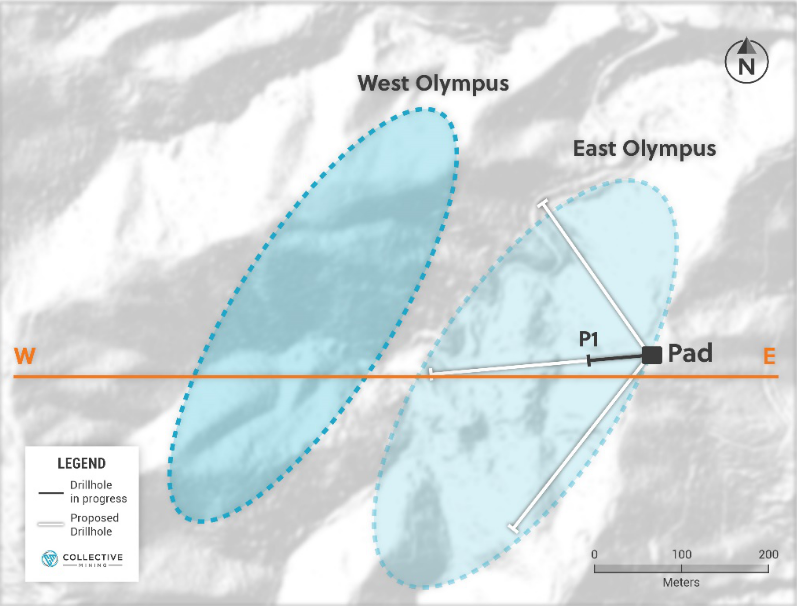

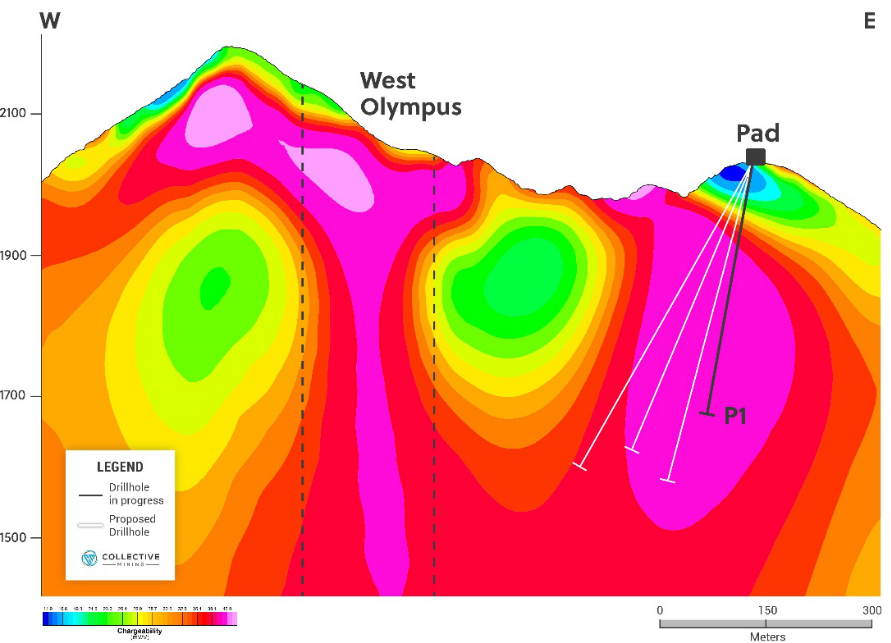

Ari Sussman, Executive Chairman of Collective Mining, commented in a press release: “Olympus is an extremely exciting grass roots discovery for the Company and locates in an area with no previous drilling or modern exploration work. High-grade polymetallic assay results to date are so compelling that we have prioritized Olympus for drilling in 2022 with a much expanded and fully funded drill program currently being finalized ahead of the new year. Olympus is a very large mineralized system measuring at least 1,000 metres X 600 metres on surface and the veins and porphyry are coincident with IP chargeability anomalies that can be followed to depths of up to 800 metres below surface.”

A third diamond drill rig is expected to be added at Guayabales in addition to the two rigs currently operating at part of Collective’s maiden 10,000 metre drill program. The third rig is anticipated to begin operating later in December.

Highlights (Table 1 and Figures 1 to 4)

- Assay results of grab samples taken from veins located within historical, shallow underground adits on the western side of Olympus continue to confirm the presence of a significant high-grade carbonate base metal (“CBM”) sheeted vein system. Four of the samples were also selected to be assayed for base metals with results as follows:

- Table 1: Grab Sample Assay Results from the Western Sector of Olympus**

- * Gold and Silver assays previously reported on December 1, 2021. Sample was collected from eastern side of Olympus.

**The reader should be cautioned that grab samples are selective in nature and as a result should not be relied upon as being representative of average grades anticipated in any future resource estimate or mining scenario.

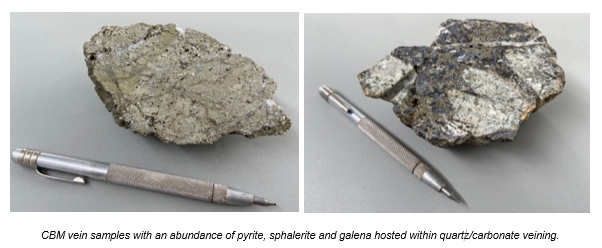

*** Only samples CM003570 through CM003573 were assayed for base metal grades. - Preliminary logging of the first completed hole into the eastern portion of Olympus highlights multiple CBM veins hosted with intensely altered porphyry diorite and hydrothermal breccia. The CBM veins contain pyrite, galena, chalcopyrite and sphalerite sulphides.

- As a result of the grab sample results and the visual logging of the first hole, the Company will commence diamond drilling with a second rig in December and will soon commence construction of a third drill pad in early January 2022.

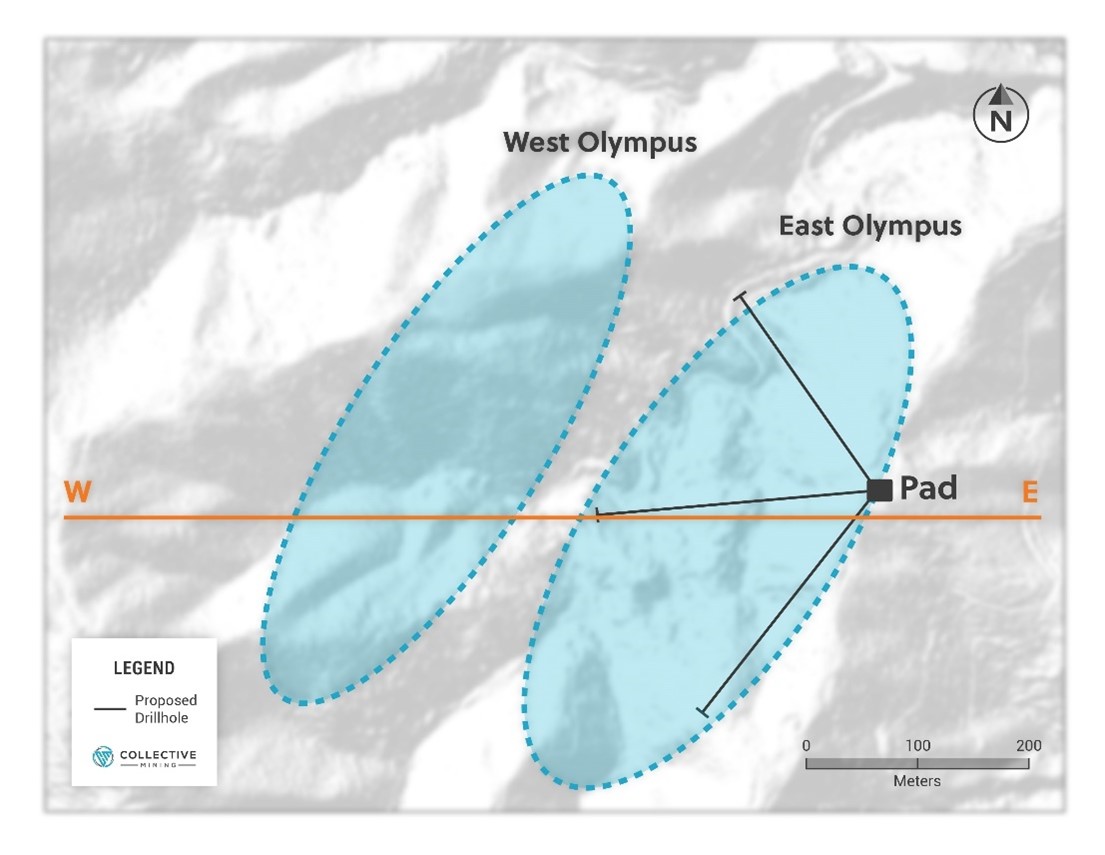

Figure 2: Plan View of Olympus with Proposed Drill Holes Traces Superimposed

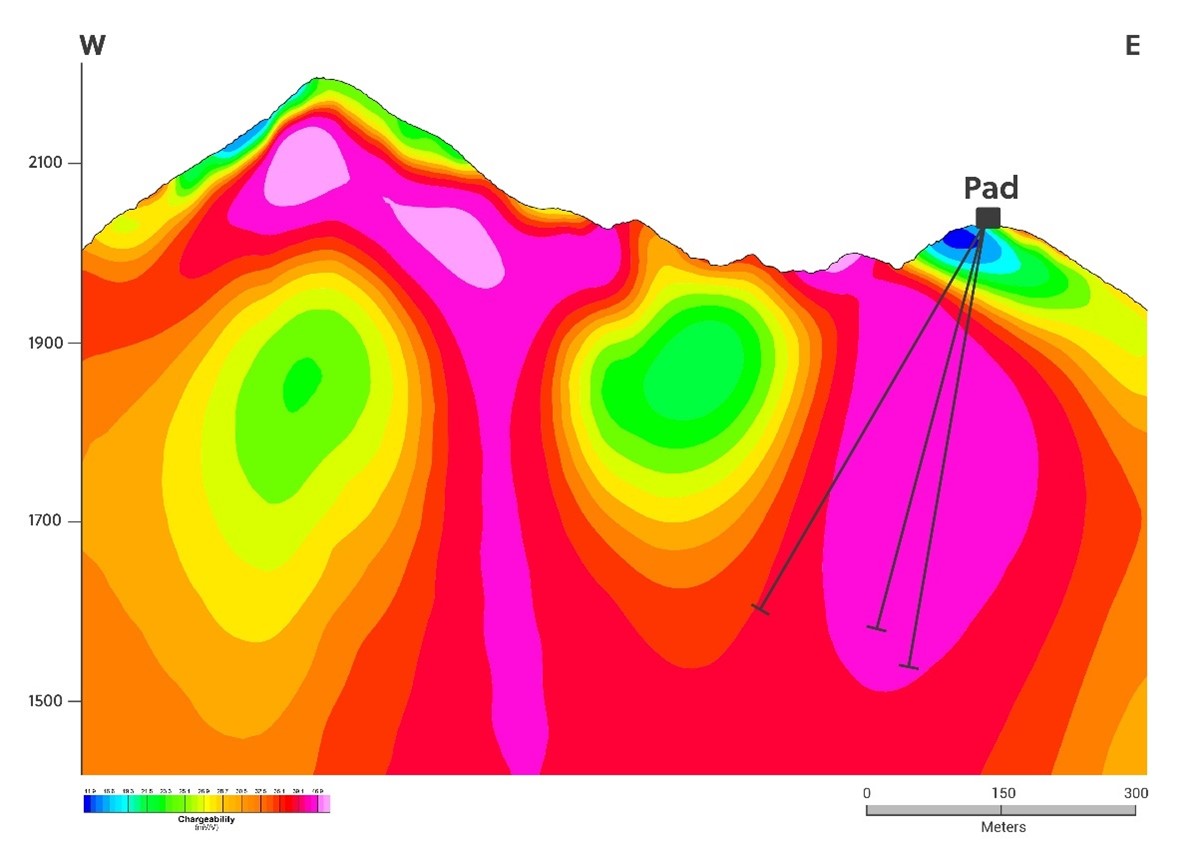

Figure 3: Olympus Section View Showing Drill Hole Traces into a Chargeability High

Figure 4: Photos of High-Grade Polymetallic Grab Samples Taken at Olympus

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

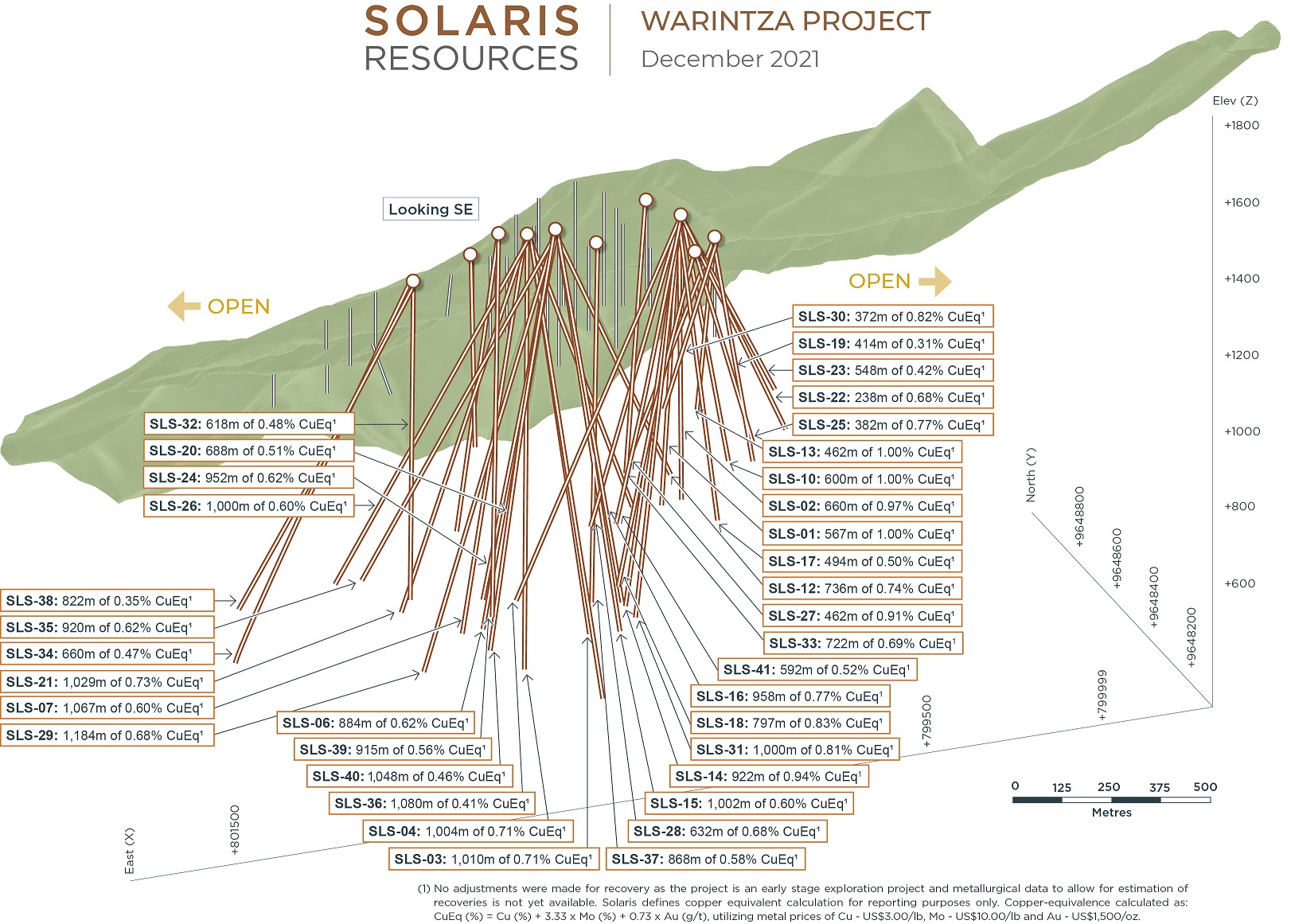

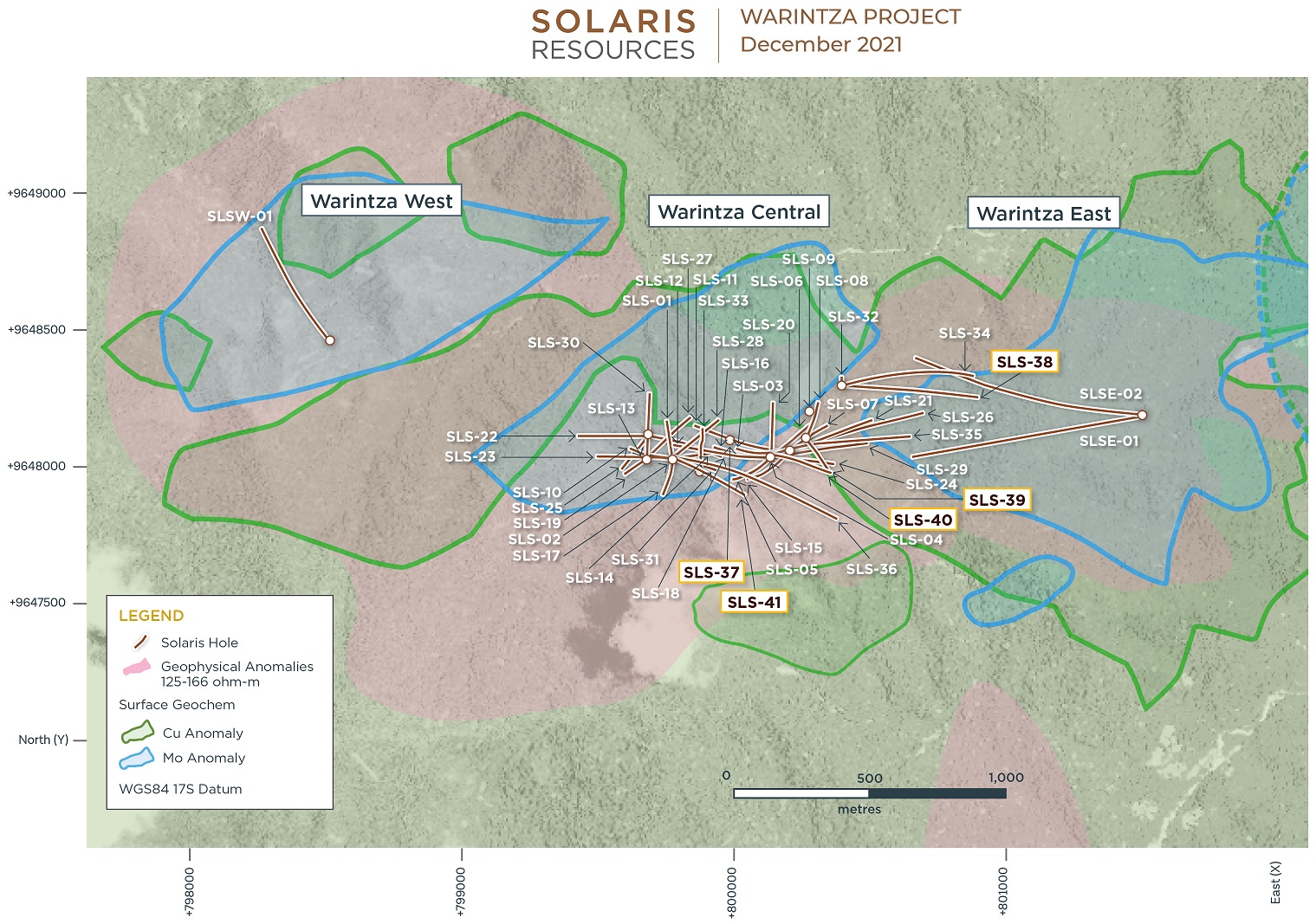

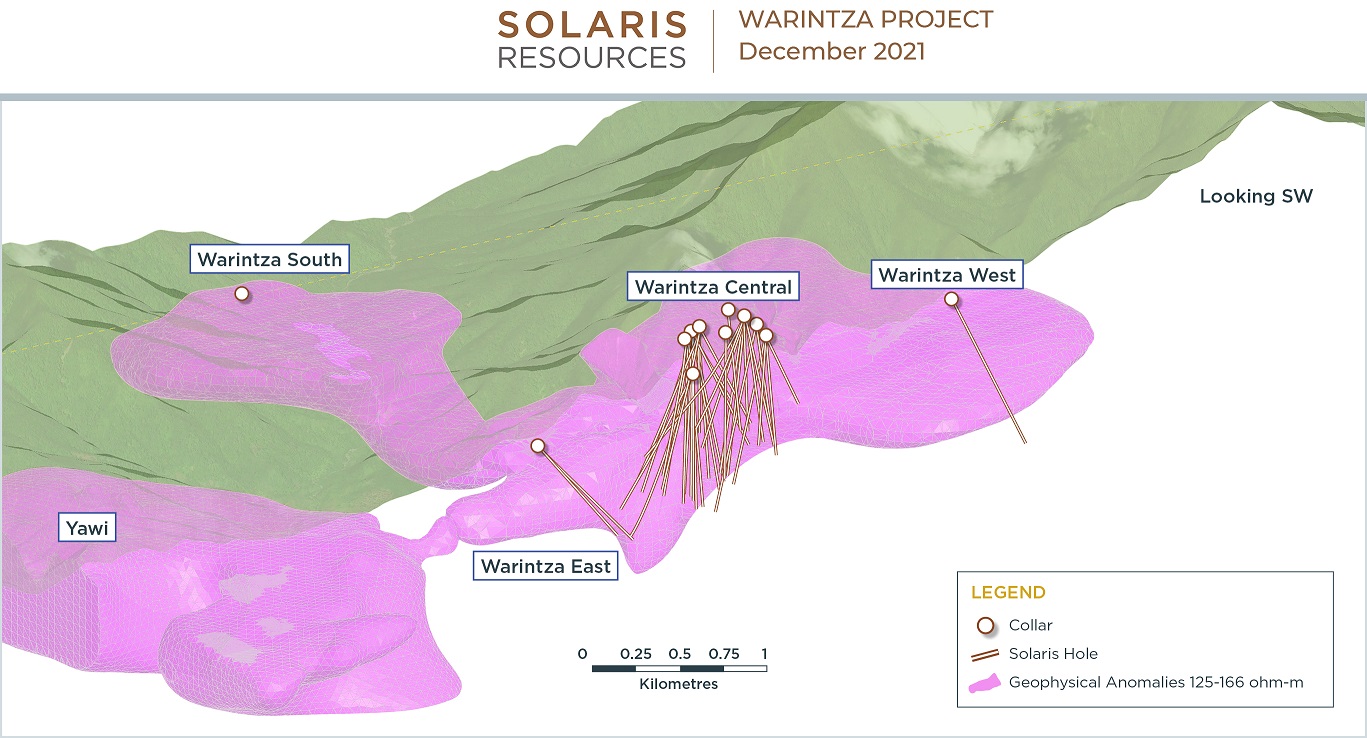

Solaris Resources (TSX:SLS) has reported assay results from its ongoing drill program at its Warintza Project in Ecuador. The company is currently operating discovery drill programs and aiming for mineral resource growth at the project.

Solaris announced this morning that it has extended Warintza Central to South, Southeast, and still open, while announcing that drill results from maiden drilling at Warintza South are now expected in January 2022.

Mr. Jorge Fierro, Vice President, Exploration, commented in a press release: “These latest results continue to expand the dimensions of Warintza Central to the south and southeast where it remains open. Our next series of holes will target extensions to the north and northeast. In January, we are looking forward to the results of the first-ever drilling at Warintza South, where we are targeting the fourth major discovery within the 7km x 5km cluster of copper porphyries on this property.”

Figure 1 – Long Section of Warintza Central Drilling Looking Southeast

Figure 2 – Plan View of Warintza Drilling Released to Date

Figure 3 – Long Section of 3D Geophysics Looking Southwest

Highlights

- Five additional holes reported in this press release have expanded the dimensions of Warintza Central to the south and southeast where it remains open, with the highest-grade intervals within each hole starting at or near surface (refer to Figures 1 & 2)

- SLS-37 was collared in the middle of the Warintza Central grid and drilled vertically into a partially open volume near surface, returning 868m of 0.58% CuEq¹ from 28m depth; further drilling from this platform will target northern and southern extensions of the zone

- SLS-38 was collared at the northeastern limit of the grid and drilled east into an open volume, returning 244m of 0.70% CuEq¹ from 58m depth, within a broader interval of 822m of 0.35% CuEq¹ that included dilution from a weakly-mineralized mafic intrusive

- SLS-39 was collared on the eastern side of the grid and drilled into a partially open volume to the southeast, returning 915m of 0.56% CuEq¹, including 368m of 0.73% CuEq¹ from 90m depth, with the last 10m of the hole grading 0.61% CuEq¹ suggesting further potential to the southeast

- SLS-40 was collared at the southeastern limit of the grid and drilled into a partially open volume to the southeast, returning 1,048m of 0.46% CuEq¹ from surface, including 382m of 0.64% CuEq¹ from 50m depth, extending mineralization to the southeast where it remains open

- SLS-41 was collared in the middle of the Warintza Central grid and drilled into an open volume to the southeast, returning 592m of 0.52% CuEq¹ from surface, including 496m of 0.58% CuEq¹, extending mineralization to the south where it remains open

- To date, 55 holes have been completed at Warintza Central with assays reported for 41 of these

- Maiden drilling results are expected in January from Warintza South, a target defined by a high conductivity anomaly measuring 2.5km x 2.0km x 0.7km and overlapping copper and molybdenum anomalies where exposed at surface

Table 1 – Assay Results

| Hole ID | Date Reported | From (m) | To (m) | Interval (m) | Cu (%) | Mo (%) | Au (g/t) | CuEq¹ (%) |

| SLS-41 | Dec 14, 2021 | 0 | 592 | 592 | 0.42 | 0.02 | 0.06 | 0.52 |

| Including | 8 | 504 | 496 | 0.48 | 0.02 | 0.06 | 0.58 | |

| SLS-40 | 8 | 1056 | 1048 | 0.39 | 0.01 | 0.03 | 0.46 | |

| Including | 50 | 432 | 382 | 0.56 | 0.02 | 0.04 | 0.64 | |

| SLS-39 | 28 | 943 | 915 | 0.49 | 0.01 | 0.04 | 0.56 | |

| Including | 90 | 458 | 368 | 0.65 | 0.02 | 0.04 | 0.73 | |

| SLS-38 | 58 | 880 | 822 | 0.28 | 0.01 | 0.05 | 0.35 | |

| Including | 58 | 302 | 244 | 0.58 | 0.02 | 0.06 | 0.70 | |

| SLS-37 | 28 | 896 | 868 | 0.39 | 0.05 | 0.05 | 0.58 | |

| SLS-36 | Nov 15, 2021 | 2 | 1082 | 1080 | 0.33 | 0.01 | 0.04 | 0.41 |

| SLS-35 | 48 | 968 | 920 | 0.53 | 0.02 | 0.04 | 0.62 | |

| SLS-34 | Oct 25, 2021 | 52 | 712 | 660 | 0.36 | 0.02 | 0.06 | 0.47 |

| SLS-33 | 40 | 762 | 722 | 0.55 | 0.03 | 0.05 | 0.69 | |

| SLSE-02 | 0 | 1160 | 1160 | 0.20 | 0.01 | 0.04 | 0.25 | |

| SLS-32 | Oct 12, 2021 | 0 | 618 | 618 | 0.38 | 0.02 | 0.05 | 0.48 |

| SLS-31 | 8 | 1008 | 1000 | 0.68 | 0.02 | 0.07 | 0.81 | |

| SLS-30 | 2 | 374 | 372 | 0.57 | 0.06 | 0.06 | 0.82 | |

| SLSE-01 | Sep 27, 2021 | 0 | 1213 | 1213 | 0.21 | 0.01 | 0.03 | 0.28 |

| SLS-29 | Sep 7, 2021 | 6 | 1190 | 1184 | 0.58 | 0.02 | 0.05 | 0.68 |

| SLS-28 | 6 | 638 | 632 | 0.51 | 0.04 | 0.06 | 0.68 | |

| SLS-27 | 22 | 484 | 462 | 0.70 | 0.04 | 0.08 | 0.91 | |

| SLS-26 | July 7, 2021 | 2 | 1002 | 1000 | 0.51 | 0.02 | 0.04 | 0.60 |

| SLS-25 | 62 | 444 | 382 | 0.62 | 0.03 | 0.08 | 0.77 | |

| SLS-24 | 10 | 962 | 952 | 0.53 | 0.02 | 0.04 | 0.62 | |

| SLS-19 | 6 | 420 | 414 | 0.21 | 0.01 | 0.06 | 0.31 | |

| SLS-23 | May 26, 2021 | 10 | 558 | 548 | 0.31 | 0.02 | 0.06 | 0.42 |

| SLS-22 | 86 | 324 | 238 | 0.52 | 0.03 | 0.06 | 0.68 | |

| SLS-21 | 2 | 1031 | 1029 | 0.63 | 0.02 | 0.04 | 0.73 | |

| SLS-20 | April 19, 2021 | 18 | 706 | 688 | 0.35 | 0.04 | 0.05 | 0.51 |

| SLS-18 | 78 | 875 | 797 | 0.62 | 0.05 | 0.06 | 0.83 | |

| SLS-17 | 12 | 506 | 494 | 0.39 | 0.02 | 0.06 | 0.50 | |

| SLS-16 | Mar 22, 2021 | 20 | 978 | 958 | 0.63 | 0.03 | 0.06 | 0.77 |

| SLS-15 | 2 | 1231 | 1229 | 0.48 | 0.01 | 0.04 | 0.56 | |

| SLS-14 | 0 | 922 | 922 | 0.79 | 0.03 | 0.08 | 0.94 | |

| SLS-13 | Feb 22, 2021 | 6 | 468 | 462 | 0.80 | 0.04 | 0.09 | 1.00 |

| SLS-12 | 22 | 758 | 736 | 0.59 | 0.03 | 0.07 | 0.74 | |

| SLS-11 | 6 | 694 | 688 | 0.39 | 0.04 | 0.05 | 0.57 | |

| SLS-10 | 2 | 602 | 600 | 0.83 | 0.02 | 0.12 | 1.00 | |

| SLS-09 | 122 | 220 | 98 | 0.60 | 0.02 | 0.04 | 0.71 | |

| SLSW-01 | Feb 16, 2021 | 32 | 830 | 798 | 0.25 | 0.02 | 0.02 | 0.31 |

| SLS-08 | Jan 14, 2021 | 134 | 588 | 454 | 0.51 | 0.03 | 0.03 | 0.62 |

| SLS-07 | 0 | 1067 | 1067 | 0.49 | 0.02 | 0.04 | 0.60 | |

| SLS-06 | Nov 23, 2020 | 8 | 892 | 884 | 0.50 | 0.03 | 0.04 | 0.62 |

| SLS-05 | 18 | 936 | 918 | 0.43 | 0.01 | 0.04 | 0.50 | |

| SLS-04 | 0 | 1004 | 1004 | 0.59 | 0.03 | 0.05 | 0.71 | |

| SLS-03 | Sep 28, 2020 | 4 | 1014 | 1010 | 0.59 | 0.02 | 0.10 | 0.71 |

| SLS-02 | 0 | 660 | 660 | 0.79 | 0.03 | 0.10 | 0.97 | |

| SLS-01 | Aug 10, 2020 | 1 | 568 | 567 | 0.80 | 0.04 | 0.10 | 1.00 |

| Notes to table: True widths cannot be determined at this time. | ||||||||

Table 2 – Collar Location

| Hole ID | Easting | Northing | Elevation (m) | Depth (m) | Azimuth (degrees) | Dip (degrees) |

| SLS-41 | 799765 | 9648033 | 1571 | 792 | 115 | -70 |

| SLS-40 | 800124 | 9648044 | 1568 | 1056 | 105 | -75 |

| SLS-39 | 800253 | 9648105 | 1576 | 943 | 145 | -80 |

| SLS-38 | 800383 | 9648303 | 1412 | 923 | 90 | -56 |

| SLS-37 | 799968 | 9648102 | 1510 | 929 | 0 | -90 |

| Notes to table: The coordinates are in WGS84 17S Datum. | ||||||

Source: Solaris Resources

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The major diversified Rio Tinto (ASX:RIO) and Canadian junior Star Diamond have terminated their long-standing and controversial dispute. As part of the resolution Rio Tinto and Star Diamond reached agreements that were jointly reviewed in order to advance the development of a diamond mining operation on the Fort a la Corne property in Saskatchewan, Canada.

The dispute originated in 2017 by virtue of Rio Tinto Exploration Canada (RTEC) spending $75 million to acquire 60% of what would be Saskatchewan’s first operating diamond mine, Star-Orion South. In addition Star diamond also claimed that RTEC overspent on the project while exercising its earn-in options prior to completing and delivering the results of its bulk sampling program.

When RTEC exercised its options, Star Diamonds objected claiming that RTEC, was attempting to increase its stake below market value. Thus the junior Star Diamond initiated legal action against RTEC.

Among the new points agreed in the dispute resolution are:

- All Fort å la Corne project expenditures incurred between November 9, 2019 and December 31, 2021 will be the sole responsibility of Rio Tinto Exploration Canada’s (RTEC) subsidiary.

- Star Diamond will have no obligation to fund or contribute to accrued interest costs until the commencement of commercial production, which will not occur until after the completion of construction of the diamond mine

- RTEC will own 75% of the project, and Star diamond will own the remaining 25%. In the event that Star Diamond sells more than 50% of its shares to any other person, RTEC will have five business days to match such proposed acquisition.

- Star Diamond will have six months to begin contributing to the costs and capital expenditures necessary to build the mine once a decision has been made to develop it.

- Star Diamond shares rose 58% to C$0.36, the highest level they have traded this year. This puts the company’s market capitalization at C$138.25 million.

A decision on whether or not to build the diamond operation will be made after the completion of a feasibility study. Next year’s investments will initially be advanced by RTEC.

Both parties to the agreement said Star Diamond will not be obligated to begin reimbursing RTEC for its share of the costs until commercial production has been achieved.

Ewan Mason, chairman of the board of Star Diamond said, “We are very pleased to have reached a constructive resolution with Rio Tinto that puts our differences in the past, fully aligns our interests, and allows both of us to focus singularly on moving forward together quickly.”

For his part, Rio Tinto’s Head of Exploration, Dave Andrews, said, “These new arrangements and our alignment with Star Diamond represent an important milestone in the continued development of the Fort à la Corne property. We are very pleased to now be working in cooperation with Star Diamond on a diamond project that we believe has the potential to be a significant contributor to both the local communities around the Fort à la Corne property and the broader Saskatchewan economy.”

A 2018 preliminary economic assessment estimated that 66 million carats can be recovered from the project, generating $3.3 billion ($2.6 billion) in revenue. This could be a huge project for both parties and illustrates the power of a major mining company taking a stake in a junior mining company’s project.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Canadian-based mining company Kinross Gold Corp. (NYSE:KGC) announced plans to acquire Great Bear Resources Ltd. for an upfront payment of $1.8 billion, a huge acquisition in the Red Lake Mining District in Ontario, Canada.

Kinross’s main focus in acquiring Great Bear is their Dixie project located in Red Lake. The project is said to have shown exciting recent gold discoveries and characteristics of a top-tier deposit.

Paul Rollinson, Kinross’ President, and CEO, said in a press release regarding the acquisition: “The Dixie project represents an exciting opportunity to develop a potentially top-tier deposit into a large, long-life mine complex. In addition to the prospect of developing a quality, high-grade open pit mine, we also believe that a significant portion of the asset’s value is its longer-term potential, which includes the view of a sizable underground operation.”

Great Bear is a junior gold mining company, and purchased the Red lake property from Newmont Mining back in 2017. Within the four years of owning the Dixie project, the Vancouver-based company has made outstanding discoveries. To date, Great Bear has completed more than 340,000 metres of drilling in 794 drill holes and has identified five high-grade gold discoveries.

Chris Taylor, Great Bear’s president and CEO said: “Kinross first set foot on the Dixie property three years ago, and has closely monitored the discovery and growth of each successive gold discovery Great Bear has made. With extensive drilling now completed at Dixie, both companies have a shared vision of the clear potential for a multi-deposit mine complex consisting of a potential high-grade open-pit mine and a long-life underground mine. As Great Bear’s track record of continuous discovery shows, the Dixie project hosts a prolific gold system that remains completely unconstrained and open to extension. In the near-term, with over 80% of the property unexplored, our shareholders will continue to have exposure to ongoing advanced project development and extensive exploration upside in the lead-up to planned production.”

The Dixie project is 91 square kilometres of contiguous claims and 25 kms southeast of the town of Red Lake. Only 20% of the property has actually been explored, which leaves high potential for many more high-grade discoveries. Some analysts speculate that the property could contain up to 20 million ounces of gold, which would raise its status to one of the largest gold mines in Canada.

Kinross President J. Paul Rollinson commented, “the Dixie project has multiple high-potential mineralized zones which remain open along strike and at depth, and we are confident that the asset has strong untapped upside with numerous avenues for growth.”

The most well-known and significant discovery at Dixie is known as the “LP Fault” zone. This area has continuous wide, moderate grade mineralization along with subparallel high-grade gold lenses which forms a 200 to 400 metre wide envelope of stacked zones. Drilling in the LP Fault zone concluded there is gold mineralization down to a depth of 786 metres along 10.8 kilometres of strike. The LP Fault zone also is said to have similar geological features to the Hemlo deposit, which has been a successful operation for more than 30 years.

200,000 metres of drilling is planned for 2022 for the LP Fault zone, with expected long-term potential and value.

Red Lake is also home to multiple Indigenous communities, the Wabauskang and Lac Seul First Nations, in which Great Bear and Kinross recognize the important territorial claims they have within the area.

The company has already had a meeting with the chiefs of both First Nations and looks forward to maintaining and growing their relationships with both Indigenous communities. The company is committed to ensuring its operations leave a positive and lasting legacy, and that they develop the area in a way that honours Indigenous rights and brings long-term socio-economic benefits to the region.

Not only is Kinross dedicated to respecting the importance of the Indigenous community, they also have a goal of being a net-zero greenhouse gases emissions company by 2050. Dixie is located in a low carbon energy grid which supports this goal. Kinross is planning to incorporate energy-efficient initiatives as it develops the Dixie project, including evaluating electric and hydrogen fuel fleets.

The project is also located in an established mining camp, making skilled labour and infrastructure easily accessible resources. Dixie also offers the potential for long-term tax benefits.

“We are pleased to achieve our goal of adding a high-quality asset in our home jurisdiction that further bolsters our global portfolio and can potentially provide long-term tax benefits,” said Kinross’ Rollinson. The deal is likely to close in the first quarter of 2022.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Canadian-based Solaris Resources (TSX:SLS) has announced its plans to focus on advancing its 100%-owned flagship Warintza copper and gold project in southeastern Ecuador, while transferring its non-core assets into a new private company called Solaris Exploration Inc.

The company will be transferring its noncore assets in Ecuador, Chile, Mexico, and Peru to the new company following an internal reorganization from the company. It is expected that 100% of the common shares of Solaris Resources will be spun out to shareholders relative to their shareholdings.

In order for the spin-out to be approved, at least two-thirds of Solaris Resources shareholders have to vote and agree on the future plans. The spin-out and reorganization are also subject to other approvals, including approval by the Supreme Court of British Columbia.

After the proposed spin-out has been approved, Solaris will continue trading on the Toronto Stock Exchange in Canada under the symbol “SLS”, and on the OTCQB Venture Market in the United States under the symbol “SLSSF”. Solaris Exploration will not be listed on any stock exchange post-spin-out approval, and will remain a private company for the time being.

Warintza Stands on Its Own

As the company bundles its non-core assets, Solaris plans to focus on rapidly growing and advancing its Warintza project. The 268-sq.-km property is adjacent to the San Carlos-Panantza copper and gold mine, along with the Mirador copper and gold mine about 40 km south of the property. The Mirador mine is one of the world’s lowest-cost copper operations and largest mines in Ecuador; it started production in 2019 and is expected to produce 94,000 tonnes of copper concentrate per year.

The low cost of operation at Waritnza and the surrounding mines is due to easy-to-access roads and highways, access to freshwater, and access to low-cost hydroelectric energy.

The property is also adjacent to a highway nearby that allows access to Pacific ports, transmission lines, and an airport. It is connected to grid power which supplies the company with inexpensive hydroelectric power, as well as access to fresh water, and low-cost skilled labour. This is the ideal situation for the exploration company and its flagship asset. Ultimately, the capital cost savings for the project have been lowered immensely due to the opportune placement of the project.

A 2019 mineral resource estimate for Warintza Central estimated 123.8 million inferred tonnes grading 0.56% copper, 0.03% molybdenum, and 0.06 gram gold per tonne (0.7% copper-equivalent) for 1.5 billion lb. contained copper, 77.5 million lb. molybdenum, and 238,600 oz. gold. The estimate was based on about 7,000 metres of historical drilling to an average depth of approximately 200 metres.

Warintza was first discovered by David Lowell over 20 years ago in 2000. After the discovery, the property was left alone for almost two decades as social acceptance of the property began to break down within the local communities. Through extensive communication and understanding of why operating this project would affect the community so immensely, the two parties came to a resolution in 2019.

Beyond Business, To Community Development

Now, Solaris has a strategic alliance in place with the Shuar communities of Warintza and Yawi to overlook and engage in direct and transparent dialogue regarding all Warintza project-related activities. This alliance also led to the decision to create a CSR program promoting trust, cooperation, and reciprocal support. Solaris now employs over 450 personnel, which represents full employment from the local communities.

In September 2020, the company signed an Impacts & Benefits Agreement with the Shuar communities of Warintza and Yawi for the Warintza project. This agreement provides certainty to Solaris that the communities will continue to support the company through the development and production stages of the project.

Warintza has 12 drill rigs on the property, mostly focused on Waritnza Central, currently open to the north, east, and south. Results from ongoing exploration are expected in the near-term as well, and 2022 is set to bring further big developments.

Most Exciting Year Yet?

An updated mineral resource estimate is expected to be published within the first quarter of 2022, as well as a preliminary economic assessment set to be released later in the year. Those updates could establish Warintza as a premier copper project, and reset investor expectations for how big the Warintza project – and Solaris Resources – could be.

With the new move to make it clear that Warintza is a world-class asset on its own, this could mean the start of the next chapter for the project and Solaris Resources.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Three Valley Copper (TSXV:TVC) has announced that it has increased its ownership of Minera Tres Valles to 95.1%, following the closing of the previously announced bought deal financing. This increases the company’s share of MTV from the previous 91%. About $9 million of the previously announced bought deal financing was used to subscribe to the newly issued shares of Minera Tres Valles.

The closing of the bought deal financing on November 25 gave the minority shareholder, and SRH Chile SpA the opportunity subscribe for newly issued shares of MTV. Since the minority shareholder declined to participate, their shares were diluted from an 8.9% stake to 4.9%. Critically, Three Valley Copper expects that the minority shareholder’s position will likely be diluted further if they decline to participate in any future anticipated MTV share issuances.

The increased ownership of MTV will give Three Valley Copper better operational control over production and future exploration at the property.

Minera Tres Valles is in the process of expanding its capacity in order to increase copper production in 2022 through to 2023. The company is targeting 13-000 to 16,000 tonnes of copper cathode production in 2023. Ultimately all Three Valley Copper shareholders will benefit from the increased copper production at Minera Tres Valles. As the majority shareholder of MTV, Three Valley Copper, and its shareholders stand to gain significantly from the future advancement of the project as well as planned exploration at the property. MTV is still 10% unexplored, with potential future discoveries waiting in the 46,348 hectares of exploratory lands.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Ecuador’s constitutional court ruled Wednesday that mining in the country’s protected rainforest violates nature’s constitutional rights. The landmark decision was reached after a lawsuit filed by environmental organizations, which argued that mining activities threatened Ecuador’s constitutional provisions granting rights to ecosystems and protection from degradation or pollution. In their ruling, Ecuadorian justices found that the state mining company Enami and Cornerstone Capital Resources, its Canadian partner violated constitutional protections granted to natural resources in the Los Cedros Protected Area.

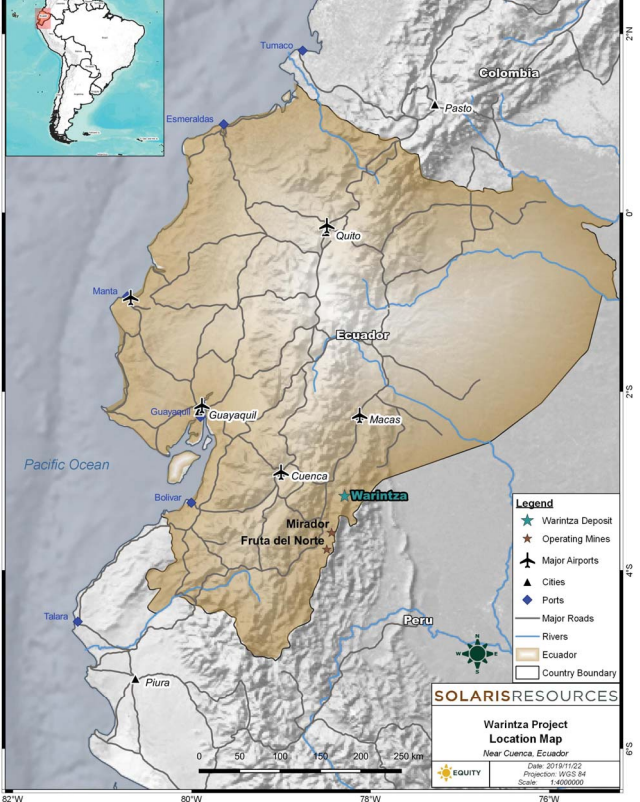

Solaris Resources (TSX:SLS) is exploring its Warintza property in southeastern Ecuador, which lies east of Cuenca. The project is not located in any of the biologically sensitive areas mapped out by the government, and does not lie within or near the rainforest.

This is good news for the junior mining company that has made significant progress in its drill program, making back-to-back discoveries at multiple targets. With several hundred kilometres between the Warintza project and the nearest protected forest, Sangay, Solaris should be able to avoid much of the risk that other mining companies will need to deal with.

The ruling creates uncertainty for other junior mining companies through this new precedent that could threaten their projects if they lie within or around the protected rainforest or other environmentally sensitive areas.

This could also be harmful to the country’s tax base and economic prosperity as the mining industry has been an important source of economic growth and contributes to Ecuador’s GDP.

With this latest constitutional court decision on protecting nature’s rights, it looks like Ecuador could be witnessing a shift towards greater environmental protections at the expense of foreign investment which could impact future economic development initiatives by President Guillermo Lasso’s administration.

The ruling is a landmark victory for the rights of nature movement, which has been growing in popularity as more countries adopt constitutional amendments and legislation recognizing the legal rights of ecosystems to exist and flourish. Ecuador is one of the first countries to recognize constitutional rights for nature, doing so in 2008 with Article 71-A of its Constitution.

Good for Nature, Harmful to Business

This week’s ruling by Ecuador’s constitutional court follows another groundbreaking verdict that granted the Vilcabamba River constitutional rights and recognized it as an entity with legal interests in the protection against pollution or degradation. The watershed of this Andean river spans across six provinces through Peru and three more provinces in southern Colombia before reaching its mouth at the Amazonian city of Iquitos, where approximately 500,000 people reside. This unprecedented ruling was also decided by seven justices voting unanimously for nature’s right to exist and flourish under Article 71A of Ecuador’s Constitution.

An Infringement of Rights?

However, the most recent ruling from the constitutional court is seen by some as an infringement of mining rights that were granted to two companies authorized to operate on those lands. According to Ecuador’s Ministry of Mines and Metal Resources, mining is the second most important source of income for the country after oil.

This places the country’s interests directly in contention with the legal ruling made by the constitutional court, which is expected to set a precedent for future constitutional protections on nature. Ultimately, this could open the country up to more litigation in the future as companies with projects in protected lands that have worked to protect those regions while maintaining operations are shut down or have their licenses revoked.

Miners may also consider the risk of doing business in Ecuador to be too high if the constitutional court continues to hand down rulings in this way, evoking images of overreach in some cases. Foreign investment from the mining industry in Ecuador is important because it boosts the country’s economy through royalties, taxes, and job creation.

If nature’s rights begin to impede economic progress, the constitutional court may have to begin to weigh that into its decision-making process. It is likely that eventually, Ecuador’s constitutional court will be forced to make definitive rulings on these issues in order for them not to continue being brought before it with each new instance of violation of pollution taking place within ecosystems protected by constitutional rights.

This ruling sets a public global precedent as well, which could lead other countries around the world where nature also has constitutional protections – such as Colombia and Bolivia – to follow suit if they are seeing similar environmental degradation from mining activities there.

For now, mining companies and investors will be watching very closely for the progress in Ecuador and any future news on this case and others.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Cadillac lithium property located approximately 40 km west of Val-d’Or. Source: Vision Lithium