Every day, we come across the news that a new electronic device has been released and users are wondering if the battery performance will be sufficient for their daily use. Battery durability has become an important buying motive as users expect the batteries in their devices to offer them optimal performance for all-day use over an extended period of time. Undoubtedly, the need for much lighter and longer-lasting batteries is increasing and meeting this demand is a major challenge for manufacturers.

The batteries we know today derive their energy from liquid lithium and it has been difficult to find materials that match or exceed the conductivity, electrode potential and charging flexibility offered by batteries built from this alkaline element. Now, researchers are also turning to gold for use in high-capacity batteries with better energy density. It might be up to mining companies to fill in the supply gaps to fuel further research, and potentially production for gold use in batteries.

Trillium Gold Mines Inc.(TSXV:TGM) is a mining company engaged in the exclusive exploration and development of high-grade gold. The company has the second largest land holdings in the Red Lake District, one of the world’s most prolific and concentrated gold mining areas. Mines in the region have produced a cumulative total of 29.5 million ounces of gold at an average grade of 15.41 grams of gold per tonne of resource (g/t).

The company recently announced the acquisition of the Willis Property, which consists of thirteen contiguous patented mining concessions covering a total of 229 hectares located southwest, contiguous to Trillium’s flagship property, Newman Todd (NT) in Todd Township, Red Lake Mining District, Ontario.

Trillium Gold acquired a 100% interest in the property, subject to a 2% net smelter return royalty, completing payments totaling $420,000 and a total of 400,000 common shares in the capital of the company.

Trillium Gold CEO, Russell Star commented “The Willis property represents a significant addition to Trillium’s suite of properties in the western Red Lake area. It covers both the southwest extension of the NT Zone and other ground that has proven to be highly prospective for gold with visible gold observed in outcrop sampling. As with the NT Property, the Willis Property shows many similarities to the major gold mines to the east. Despite these attributes, the property has seen very little exploration since the 1930s and is one of the few remaining unexplored properties in the Red Lake greenstone belt.”

Gold Battery Rush?

In the battery industry, gold has not been given prominence as a candidate material for battery construction but now the importance of gold for this purpose has come to the forefront. The gold rush is here to stay.

The University of California, Irvine has been looking for a way to replace liquid lithium in batteries with a more robust and safer alternative. Now, researchers have found a way to create batteries with higher capacities than lithium with the use of gold nanowires to see if they can extend the lifespan of batteries as we know them.

Mya Le Thai, a study leader, as an experiment, added an additional layer of polymethyl methacrylate (PMMA) and charged and discharged it numerous times to test its durability. To their surprise, the researchers found that these batteries withstood more than 200,000 charge cycles. Reginald Penner, an advisor in the chemistry department at the University of California irvine said, “This is incredible because these things typically die dramatically after 5,000 or 6,000 cycles, 7,000 at the most.”

The research results are a strong indication of the importance of gold not only as an essential material for battery construction but also as an indispensable element in being able to take battery performance to the next level.

Although these super batteries require very little gold to build them, it is extremely expensive to meet the enormous demand. The mining industry will be the number one source for this material that might be the key in advanced battery performance for EVs, mobile devices, and more.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

BHP’s (NYSE:BHP) copper operation, Spence, located in northern Chile, has begun its journey to autonomy by inaugurating its first drilling rig. This event marks the beginning of the implementation of many other projects that seek autonomy and safer, more competitive and sustainable mining practices.

The equipment used is the Pit Viper 351 model, which is operated remotely from the Spence control room located approximately 2 kilometres from the mine pit. The use of this equipment will significantly reduce the exposure to operational health and safety risks of the workforce, which is a strategy that will continue to be implemented throughout the current year.

Five Rigs to be Commissioned

Five autonomous drilling rigs will be commissioned gradually over time. The plan is that in the future 100% of the drilling fleet will be autonomous. Similarly, it is planned that during 2022 the operation will make a strong decision regarding the autonomy of its truck fleet.

Regarding the implementation of these changes Pedro Hidalgo, the head of Autonomy at BHP Minerals Americas said, “Spence’s first autonomous drilling rig is the spearhead of a broader program that we are implementing at BHP’s main operations in Chile. We are not only working on drills but also on autonomous trucks. We are very pleased to meet this first milestone that will allow us to advance in the Autonomy Program at both Spence and Escondida”.

The active participation of Spence workers has been fundamental for the development of the project. From the study stage, which began two years ago, to date.

Spence Copper Mine

For the project, Spence opened 16 new job categories such as autonomous drill controllers and autonomous drill yard operators. The selected employees underwent an arduous training and special training with a duration of approximately 200 hours divided into practical and theoretical learning.

BHP built a US$2.46 billion concentrator plant for the Spence project last year, capable of generating 95,000 tons of material per day. The plant is expected to extend the life of the Spence mine by producing 300,000 tons per year until at least 2026. Spence’s first copper sales are expected to take place in the first quarter of the year.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

De Beers has extensive experience in diamond exploration, mining and trading and produces 40% of the world’s diamonds at its mines in Botswana, Canada, Namibia and South Africa and is considered the world’s largest diamond producer by value.

De Beers’ diamond production increased significantly to meet the recently recovering demand. Its production increased by 15% to7.7 million carats during the last quarterly period of 2021. De Beers said Namibian production was up 16% y/y at 400 000 carats for the fourth quarter, reflecting shorter scheduled maintenance for the marine fleet.

South African production reached 1.29 million carats in the quarter and production from the Canadian mine on the other hand was little changed due to planned plant maintenance. Canadian production fell from 776 000 carats in the fourth quarter of 2020 to 771 000 in the same period of 2021.

As a result of planned processing of higher grade ore at the Jwaneng mine, the Anglo American (LSE:AAL) unit’s diamond production increased by 23% to 5.2 million carats in the months to December 31. Which was partially offset by lower production at Orapa due to the plant’s closure at the end of 2020.

De Beers increased overall diamond production by 29% to 32.3 million carats in 2021. The producer is expected to achieve production of between 30 million and 33 million carats during 2022.

During much of 2021, De Beers increased the price of its rough diamonds in order to recover from the industry’s lull during the first year of the pandemic. Prices for its diamonds increased by 23% in “just over a year” said Mark Cutifani, CEO of Anglo American. This strategy allowed De Beers a steady recovery during the year. The price increase applied to stones over 1 carat.

Russia’s Alrosa, the world’s largest diamond producer by production, like De Beers, increased its prices, which prompted complaints in the industry. Some industry players claim that the price increase has gotten out of control mainly because polished prices must also increase in order to justify the higher prices of rough stones.

The global fine jewelry market is dominated by gem-quality diamonds, however, demand for diamonds has been driven by other sectors including computer chip production, construction and natural resource drilling, and machinery manufacturing.

A Resource-Rich Nation

South Africa is a resource-rich nation for which copper is also abundant. This metal is critical for much of the electrification happening in the economy right now, and South Africa may see further developing of its copper mines and assets. One of the companies named for the mine it operates is Palabora Mining Company Ltd.

Palabora is a copper mine based in the town of Phalaborwa in the Limpopo province of South Africa. The mine also operates a smelting and refinery complex. Its origin is associated with a unique rock formation in the region known as the Palabora Igneous Complex.

Palabora Copper is South Africa’s sole producer of refined copper, supplying mainly the local market and exporting the remainder. Palabora has been in operation since its incorporation in 1956 and is the country’s leading refined copper producer, producing approximately 45,000 tonnes of copper per year.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Canadian mining giant Barrick Gold (NYSE: GOLD) announced Tuesday that its North Mara and Bulyanhulu gold mines in Tanzania, which were ”moribund” mines are now qualifying Tier 1 assets.

Barrick, who took over management of the mines in 2019 after reacquiring Acacia Mining announced that the mines generated combined production of more than 500,000 ounces in 2021. Barrick explained that to be considered in a higher category, the assets must have reserve potential that offer a minimum mine life of 10 years, as well as annual production of at least 500,000 ounces of gold and octal cash costs per ounce over the life of the mine.

North Mara is expected to become a fully integrated mine with the planned implementation of the Nyabirama pit during the current quarterly period and the commissioning of the Nyabigena pit which, the company stated, is scheduled to commence operations in the third quarter of 2022. This could add substantial resources and greater flexibility to the mine’s plan.

Meanwhile, Bulyanhulu, having achieved steady production with the successful ramp-up of its mining and metallurgical operations in December last year, has established itself as a world-class, low-cost, long-life subway mine.

Mark Bristow, Barrick’s chief executive officer stated that the mines’ strong performance is supported by protocols and implementation of vaccinations for its workforce. The company reported that 26.45% of the workforce has already been partially vaccinated and 20.25% are already on the full vaccination schedule.

Toronto-based Barrick Mining signed an agreement with Tanzania last year that established a model for negotiations with other companies, ending a long-standing tax controversy. The deal allowed the government to acquire stakes in three gold mines.

Barrick has increased its presence around Bulyanhulu through the acquisition of six highly prospective licenses surrounding the mine. In addition, its operating teams are also on the lookout for new opportunities elsewhere in Tanzania.

Tanzanian nationals now account for 96% of the workforce and the mines continue to recruit and train people from surrounding villages. Since re-entering Tanzania, Barrick has invested more than $1.8 billion in taxes, wages and payments to local businesses. It has also invested $6.7 million in community infrastructure, health and education.

Regarding the environmental problems inherited from previous operators reported in Barrick’s Human Rights report, Bristow mentioned that these problems have been successfully addressed.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

A collective sigh of relief was heard from markets and investors on Friday as newly elected Chile president Gabriel Boric just revealed his cabinet members, picking the current head of central bank Mario Marcel as finance minister.

Boric announced his cabinet members at an event in Santiago and will be taking office March 11, during which he will only be 36, one of the youngest presidents Chile has seen. Many markets and investors, including the mining sector, had increasing concerns surrounding the young leftist president as he has made claims in past weeks prioritizing the environment and social changes over proceeding with expansions and building new mining projects.

Boric’s decision of choosing lawmaker Marcela Hernando for the key role of mining minister and Marcel for finance minister looks to be a sign of gradual rather abrupt changes for the economy, especially the mining sector. Markets and investors feel hopeful these experienced individuals will lead the country towards economic stability and an agreeable balance between environmental needs and mining enough copper and lithium to help meet the current high demand.

Diversity

Boric’s new government is made up of a politically and socially diverse group, choosing to give 14 out of the 24 positions to women as well as several former student protest leaders. The young president and inclusive cabinet reflect the desire to change outdated laws and regulations the country has, as Boric has previously announced one of his major steps as president is to draft a new constitution changing laws surrounding the environment, the lqtbq+ community, gender inequality and more.

“This Cabinet’s mission is to lay the foundations for the great reforms that we have proposed in our program,” Boric said after unveiling his ministers, adding that it would look to drive economic growth while cutting out “structural inequalities.”

Copper and Lithium

Chile is the world’s largest copper producer, and home to some of the biggest copper mining companies in the world, including state-owned Codelco, BHP, Glencore, Anglo American and Antofagasta. 2022 and onward is seeing a huge demand for both lithium and copper as many companies head towards using green energy sources and infrastructure. A huge demand for both metals comes from the electric vehicle movement, in which both are used to make batteries for the vehicles so they do not have to rely on fossil fuels, and to generate energy from sources such as solar and wind power.

“One of Boric’s biggest challenges will be cooling down the economy and retaining popular support,” Oxford Economics said in a report, adding that the young leader would face pressure to increase social spending while meeting tighter budget targets.

This is especially true within the mining industry as Boric already made several remarks in the past about not following through with certain mining operations. One example of this is when Boric pledged to oppose the $2.5 billion iron-copper mine, known as the Dominga mine, which was just approved in August after years of legal battles back and forth.

Although no further update has been given regarding the Dominga mine, markets and investors are hopeful Boric and his new cabinet members will guide the country to more economically stable grounds and continue to support the mining sector as the demand for copper and lithium continues to remain high.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Canadian mining company Trillium Gold Mines Inc. (TSXV:TGM) recently reported that it has identified numerous gold pathfinder anomalies on its Confederation Belt properties, one of the 10 different projects it has on the go within the Red Lake Mining District. The company believes these anomalies establish the “great gold potential” for the 39,300 hectares of Confederation Belt properties, and will serve as priority targets for Trillium’s second phase of exploration work in 2022.

This follow up field work is expected to generate multiple drill targets, which will “effectively launch Trillium Gold’s Confederation belt properties into a new era in gold exploration,” said the company’s VP of Exploration William Paterson in a recent press release.

Trillium Gold has catapulted into the consciousness of many mining industry watchers and investors with its latest land acquisition.

Trillium also recently announced the approval of all the items presented at its annual general and special meeting of shareholders, including the re-election of the Directors of the Company being Robert Schafer, Russell Starr, David Velisek, Robert Kang and Krisztian Toth, which was held on December 21, 2021.

The company is advancing projects in the Red Lake Mining District, which is located in Northern Ontario and known to be one of the most premier gold mining districts in the world. There has been over 60,000 meters of historical drilling performed on the district, including multiple targets that have yet to be tested, and access to essential infrastructure.

Just last December Trillium’s project list grew even more as it acquired all of Infinite Ore Corp.’s Eastern Vision property holdings in the Confederation Lake assemblage of the Birch-Uchi greenstone belt in the Red Lake Mining District. The agreement will also include the issuance of 4,000,000 common shares in the capital of Trillium Gold including payment of $175,000 in cash to Infinite Ore.

The property covers 16,991 hectares between the Fredart, Garnet Lake, Confederation North and Confederation South properties, and will give the company control over a significant portion of the Confederation Lake assemblage.

Other operations the company runs include the Gold Centre located in “the heart of the highest-grade gold camp in North America,” Shining Tree in Matachewan -Kirkland Lake mining district, and multiple properties including the Fenelon property in Quebec.

Throughout all of their operations, Trillium Gold stands by their socially and environmentally responsible values, including creating employment opportunities, boosting the communities economical performance, and making an overall positive impact on the community. Energy and the use of emissions are monitored closely, along with proper waste management in place to help preserve the ecosystem and biodiversity, which the company recognizes as a top priority.

Out of all of the projects the company operates, one of the most highlighted projects is the Newman Todd project, which the company is just scratching the surface of in terms of the future potential. Early exploration back in the 1930’s and 1940’s was carried out with little information recorded from these explorations, and until now it has only been sparsely drilled or tested at depths below 400 meters.

Some drilling that has been completed on the project has concluded excellent potential with over 40% of the holes intercepted greater than 10g/t Au over various interval lengths. 56 holes drilled in 2011 identified zones of high-grade gold mineralization along the northeast of the project, and as of November 15, 2021 the total drilling stands at 15,927 meters on both the Newman Todd and Rivard Projects combined.

Future updates will be watched closely as the new land acquisition opens tens of thousands of available hectares to the company, and investors watch to see whether Trillium Gold might be the next Great Bear Resources, and a potential takeout target for the future.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

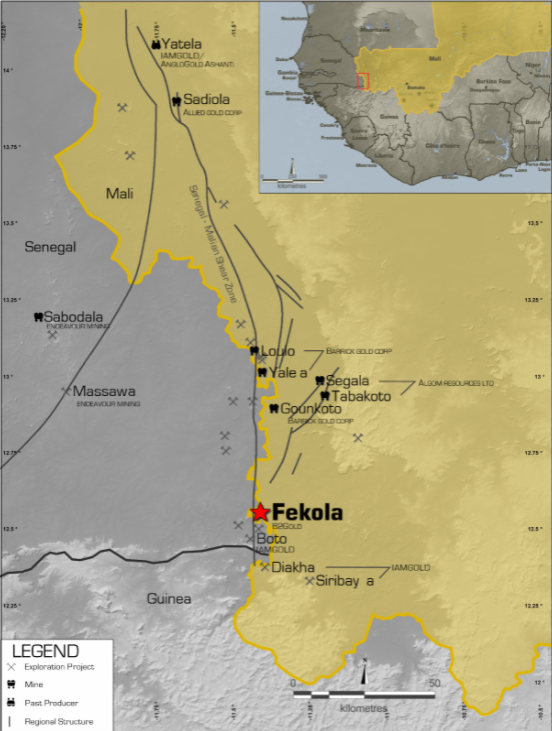

B2Gold’s (NYSE:BTG) strong 2021 production numbers are overshadowed by its underperforming Gold Miners Index (GDX) by nearly 20%.

The drop was partly due to a record comparative earnings year in 2020 as well as perceived risk in Mali. If recent sanctions do not impact mining operations, B2Gold’s price could start to better reflect its solid fundamentals.

Low cost producer with strong cash position

Annual production for FY2021 was 1.04M oz. with all-in sustaining costs (AISC) between $870 and $910. AISC for FY2022 are projected to be $1,010-$1,050 due to inflationary pressures. Even so, B2G is poised to remain among the lowest cost producers in the industry.

2021 cash flow from operations is estimated at $650M. The strong cash position with virtually no debt gives the company options for exploration and M&A. $29M has been allocated to grassroots exploration for 2022, highlighting their ambition to continue to grow by drilling.

In the words of chief executive Clive Johnson, “we’ve always been very entrepreneurial, yet we’re very good at the bricks and mortar of our business…. We’ll do deals that other companies may not do.”

Perceived Mali risks but no impact on production

Over half of B2Gold’s production comes from the Fekola Mine in Mali, where regulatory and geopolitical events have been an ongoing theme.

There was a military coup in May which, while not impacting operations, created some negative investor sentiment regarding one of Africa’s biggest gold producers. The government’s revocation of an exploration permit for B2Gold’s Menankoto property also caused negative market reaction. Although a permitting agreement was reached in December, recent sanctions on the country imposed by the Economic Community of West African States (ECOWAS) raise the possibility of supply disruptions.

Nonetheless, Fekola exceeded 2021 production estimates with 567,795 oz. and CEO Clive Johnson maintains that it will withstand supply disruptions and meet 2022 targets.

Image source: b2gold.com

Underexplored jurisdictions

Part of B2Gold’s strategy is to operate and develop in jurisdictions which, while relatively underexplored, are often perceived as higher risk compared to, for instance, Canada, Nevada, or Australia. As Clive Johnson states, “a core part of our strategy is to go where others fear to tread.”

Aside from core operations in Mali, The Philippines, and Namibia, the company has exploration projects in Uzbekistan and Finland as well as a JV development in Colombia. In July 2021, they signed exploration contracts in Egypt.

In the face of perceived geopolitical risks, Johnson highlights the solid economic foundation gold miners brought to countries during COVID and anticipates B2Gold’s experience and reputation will set it apart.

Valuation fundamentals

B2Gold offers one of the highest dividends in the industry (4.38%). It is trading at 8.67 times earnings and has healthy current and quick ratios of 4.89 and 2.90, respectively. Price to forward earnings and price to cash flow are both below industry averages.

If perceived Mali risks begin to ease and gold continues to show a strong hand in volatile markets, B2Gold’s value could start to be better reflected in the price.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is an insider or shareholder of one or more of the companies mentioned above.

Three Valley Copper (TSXV:TVC) is a company committed to environmental compliance with ESG criteria at the highest levels of compliance. TVC carries out best environmental practices in its operations, thus providing great value to shareholders in the long term. At the same time, the company is committed to maintaining strong community relations through actions that reduce environmental impact.

Three Valley Copper builds strong relationships with the community under the policy of an open and permanent dialogue based on generating results that bring benefits to those involved. In this way, TVC achieves conflict resolution in an efficient manner.

In May 2021, The Valley Copper received some neighbors from the community to show them the protocols in an in situ controlled blasting event. During the visit, community members were able to verify that the protocols required by regulatory authorities are applied on a daily basis at the operations. The event took place in an atmosphere of mutual respect and concern with the Sustainability Manager and other TVC executives.

These are some of the points that visitors and members of the community confirmed:

- Compliance with the protocols and procedures required for blasting to reduce dust emissions as much as possible.

- TVC’s commitment to the measures in place to control dust from the Don Gabriel mine and the Manquehua road.

- It was agreed with the community to maintain an open and constructive dialogue.

- It was communicated that an on-site inspection of the shock monitoring station will be carried out by an expert in order to verify and inform the community of the station’s operating methodology.

The contributions made by TVS are based on emphasizing the ability to work in community. This method not only helps to establish relationships with the community but also favors community involvement, resulting in better project management and, therefore, better results. This synergy allows the development of the territory to be boosted.

Social Responsibility, and a Foundation to Back it Up

The Three Valley Foundation was created in 2014 and its main distinctive feature is that it is made up of members of the community, representing the valleys of Chalinga, Cárcamo and Chuchiñi. It is through this foundation that Three Valley Copper channels its investment and carries out the financing of various social projects related to education, social infrastructure, rural health posts and more.

The Environmental Aspect

Three Valley Copper is in a continuous search for process improvement and total openness of its operations to the external community. It is also committed to caring for the environment through strict compliance with environmental legislation.

Three Valley has had a comprehensive Environmental Qualification Resolution in place for its operations since 2009. The Environmental Qualification Resolution provides companies with the fundamental instructions and permits necessary to execute operations in a sustainable manner in order to guarantee respect for the environment in a physical and social way.

Some of the environmental obligations that Three Valley Copper has in the EQR are:

- Uninterrupted monitoring of air and water quality.

- Reforestation of 250 hectares with native species.

- Construction of a petroglyph park at Quimenco.

The Minera Tres Valles project operates with renewable biomass energy that was contracted to reduce the carbon footprint, as one of its priorities is the constant care of the environment. As another measure for environmental care, Three Valley Copper keeps its water consumption to a minimum, which has earned it several awards for its efficient use of this invaluable resource.

Cultural Appreciation and Protection

Three Valley Copper’s project territory is characterized by its social and cultural heritage. As its name indicates, it is located in the heart of three surrounding valleys called Chalinga, Chuchiñi and Cárcamo.

The value of its social and cultural heritage is reflected in the traditions coming from this land.

One of the typical traditions of the region is the transhumance which is a type of seasonal grazing in continuous movement where cattle are taken from the valleys and lowlands to the Andes mountains and vice versa.

Pilgrims celebrate the Virgin Mary with dances, songs and praises, which is one of the most important religious festivities in the Chuchiñí and Manquehua valleys.

In this region you can also find petroglyph art made by the pre-Columbian cultures that inhabited the valleys, generally following the watercourses.

The people have left traces of their culture that later generations will have the opportunity to know and continue to enjoy.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Investors in the mining sector are preparing for what should be another strong year for the industry by adding a total of $86.3 billion of market capital to the top mining companies in the Top 50 ranking in 2021.

The overall value of the Top 50 ended 2021 at just under $1.4 trillion after peaking a little above that. This amount represents an increase of about $100 billion since the beginning of the year and double the market capitalization they had during March and April 2020, i.e., the peak of the pandemic.

Coal Doesn’t Go Cold

With no exposure to iron ore other than trading, Glencore (OTC:GLNCY) and its investors bucked the trend by closing the year with $25 billion.

The Swiss multinational company, Glencore, a commodity trading and production company, has not abandoned coal mining. Like its peers, its coal, gas and oil trading arm is benefiting from rising energy prices.

The performance of coal miners in 2021, especially in China, is the clearest evidence of the volatility of commodity markets. Although only a short time ago, towards the end of the year coal miners and their coal divisions in the diversifieds were threatening to drop out of the ranking altogether.

The rest of the three remaining coal companies (the ranking excludes power companies that operate their own mines such as Shenhua Energy) rose and Coal India halted its decline. The world’s largest coal miner, Coal India was number 4 in the rankings four years ago.

Lithium on the Rise

The high demand for electric cars has caused lithium prices, used for the motors and battery technology, to remain high, and their rebound has been prolonged. At the moment, the top three lithium producers, listed in the Top 50 ranking, have a global value of more than $66 billion.

Tianqi Lithium briefly dropped its position in the rankings in 2019, due to its market value being below $5 billion. However, China’s Shenzhen-listed Lithium producer is now ranked in the top 20 of the majors, with a value of about $25 billion surpassing SQM.

For its part, Albemarle (NYSE:ALB), the world’s number one producer, has risen 59% since the year began which made its investors $10 billion richer. Charlotte, North Carolina-based Albemarle announced that it intends to buy, with the aim of expanding downstream, a Chinese lithium producer.

Ganfeng, the leading manufacturer of lithium chemicals (a company not ranked as mining is not a major part of its business) is striving to secure investment in that sector of production. For its part, copper producer Codelco is advancing work on its lithium project. However, concessions in Chile could become scarce or disappear altogether in the decades to come.

Pilbara Minerals is currently ranked 54th but Pilbara is expected to enter the top 50 mining rankings very soon, as the company continues to post record highs and operations at the Pilgangoora project are ramping up to supply the huge demand for spodumene for Chinese transformers.

Rio Tinto’s (ASX:RIO) Jadar project is not off to a good start in Serbia. The Anglo-Australian company’s lithium business is likely to start to look up in the rankings in the next few years as well as Sibanye’s entry into battery metal with an acquisition in Nevada.

Iron Ore, and More

Falling iron ore prices and the decline of copper in the market in the last months of 2021 affected the ranking position of the big three companies, BHP (NYSE:BHP), Rio Tinto (ASX:RIO) and Vale (NYSE:VALE). Over the course of last year, they lost a total of $56 billion.

Last year, BHP had a valuation of almost $200 billion being worth slightly more than oil company Royal Dutch Shell for some time. This made it the most valuable stock in the UK.

A sign of the belief investors have in the effect on mining for the green energy transition is the fact that BHP has lost almost $50 billion despite activating the search for nickel for battery manufacturing. Rio Tinto, for its part, has lost $43 billion since its peak. These losses are indicators that iron ore mining remains central to the sector.

The fall in iron ore caused South Africa’s Kumba Iron Ore to have its worst valuation of the year, plummeting 30%. Australia’s Fortescue Metals, the world’s fourth largest iron ore producer, plunged by $13 billion over the year. While its ranking fell six places as its trading arm, Fortescue Future Industries, got off to a slow start.

CSN Mineração, one of the biggest mining IPOs since Glencore’s in 2011, dropped out of the 50 ranking in its first quarter debut. But thanks to last year’s 87% rise, the Cleveland-Cliffs company is ranked in the top 50 after spending years in obscurity.

Uranium

For the first time after many years, the value of uranium producers is once again ranked in the top 50.

Kazakhstan’s Kazatomprom expanded its stock exchange listing beyond Almaty. As a result, the company has doubled in value this year. Kazakhstan, responsible for about 40% of uranium production, despite the turmoil in the country, has not affected the fortunes of the state-controlled company.

AngloGold Ashanti, Cameco’s main rival, has been overtaken by Cameco leaving Cameco out of the rankings at the end of the year. However, the stock’s performance since the Dec. 31 close would see the Saskatoon-based company move back up the rankings in the hope that it can take advantage of the revival of uranium mining and the problems in Kazakhstan.

A Banner Year

Overall, the mining industry had a banner year with record investor inflows. The bullishness of 2021 is likely to continue as the pandemic recedes and producers get back to normal with production targets as well as a more balanced and predictable supply chain.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

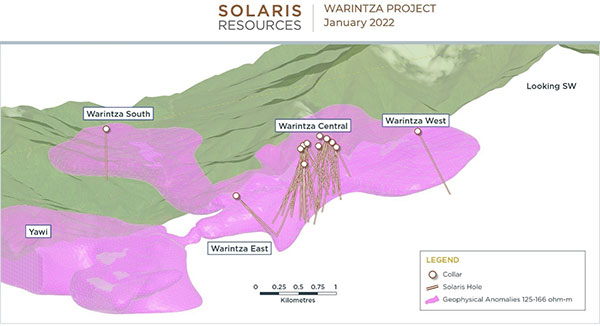

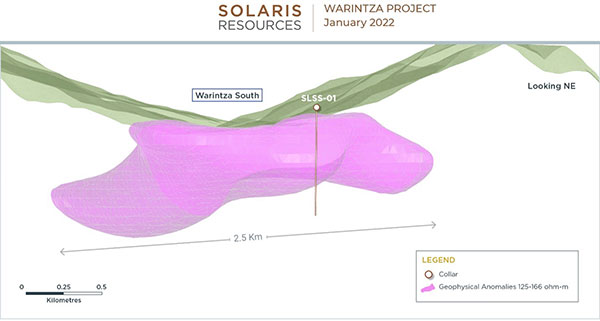

This morning, Solaris Resources (TSX:SLS) announced a huge new discovery at the Warintza South target at the Warintza Project. Ongoing exploration has revealed multiple high-grade targets, and Warintza South is the latest in a string of discoveries at the project.

Mr. Jorge Fierro, Vice President, Exploration, Solaris Resources, said in a press release, “We are delighted to have made a significant new discovery at Warintza South, with the firstever hole returning a long interval of well mineralized copper porphyry. The multi-km dimensions of the target present a large-scale opportunity. Interpretation of the drill core together with recent mapping and sampling provide important vectors for follow-up drilling to be completed once additional access and infrastructure are established.”

The high-grade resource at Warintza has been the source of excitement for investors, as Solaris’ stock price has continued to rise throughout 2021 and 2022. The company recently spun out its non-core assets to focus on drilling at Warintza in Ecuador, but placed other projects in another entity including projects in Chile, Peru, and Mexico.

Solaris (TSX:SLS) is up 133% in the trailing twelve-month period ended January 18, 2022. The company continues to gather interest as a prime takeout target for a major mining company as the copper mining industry struggles to keep up with growing demand due to the green energy transition. For Solaris Resources’ Warintza project, that means high potential for a producer to direct its interest toward the company in the future as it continues toward an updated resource in 2022.

Highlights from Warintza South:

- SLSS-01 was the first hole ever drilled at Warintza South, which is an entirely separate porphyry deposit, located approximately 3kms south of the Warintza Central zone that has been the focus of the Company’s resource expansion drilling efforts to date

- SLSS-01 was drilled vertically and returned 606m of 0.41% CuEq¹ of continuous porphyry copper mineralization from near surface, within a broader interval of 755m of 0.36% CuEq¹, marking a significant new discovery on the Project

- Warintza South is reflected by a high conductivity anomaly over twice the size of Warintza Central, illustrating the very broad proportions of this newly discovered porphyry system, with approximate dimensions of 2.5km x 2.0km x 0.7km

- SLSS-01 targeted an exposure of leached capping within this anomaly; an ongoing program of detailed sampling, including an additional 265 soil samples and 131 rock samples, significantly expanded the geochemical anomaly and shifted its core to the northeast (Figure 1)

- Follow-up drilling targeting the interpreted core of the porphyry system is set to commence after additional drill platforms are prepared based on this recent mapping and sampling work refining the target and a dedicated exploration camp is set up to support a ramp-up in activities

- Warintza South marks the fourth major copper discovery within the 7km x 5km Warintza porphyry cluster, with the adjacent Yawi and Caya targets still to be tested, as well as other recently generated targets within the broader land package to be revealed in a forthcoming update

Mr. Jorge Fierro, Vice President, Exploration, commented: “We are delighted to have made a significant new discovery at Warintza South, with the first ever hole returning a long interval of well mineralized copper porphyry. The multi-km dimensions of the target present a large-scale opportunity. Interpretation of the drill core together with recent mapping and sampling provide important vectors for follow-up drilling to be completed once additional access and infrastructure are established.”

Figure 1 – Plan View

Figure 2 – Long Section of 3D Geophysics Looking Southwest

Figure 3 – Long Section of Warintza South 3D Geophysics Looking Northeast

Figure 4 – SLSS-01 Drill Core

Notes to Figure 4: SLSS-01 core interval from 377.03 to 379.15m, averaging 0.74% Cu, 0.04% Mo and 0.05g/t Au. Quartz-diorite intermineral dike is cutting andestic volcanics. Alteration and mineralization is mainly composed of early-stage, halo-type associations with quartz, anhydrite, chlorite, biotite, epidote, pyrite, chalcopyrite, and magnetite cut by A- and B-type Mo-bearing quartz veinlets.

Table 1 – Warintza South Results

| Hole ID | Date Reported | From (m) | To (m) | Interval (m) | Cu (%) | Mo (%) | Au (g/t) | CuEq¹ (%) |

| SLSS-01 | Jan 18, 2022 | 0 | 755 | 755 | 0.28 | 0.02 | 0.02 | 0.36 |

| Including | 42 | 648 | 606 | 0.32 | 0.02 | 0.02 | 0.41 | |

| Including | 188 | 512 | 324 | 0.35 | 0.02 | 0.02 | 0.45 | |

| Notes to Table 1: True widths cannot be determined at this time. | ||||||||

Table 2 – Collar Location

| Hole ID | Easting | Northing | Elevation (m) | Depth (m) | Azimuth (degrees) | Dip (degrees) |

| SLSS-01 | 801494 | 9645194 | 1215 | 755 | 0 | -89 |

| Notes to Table 2: The coordinates are in WGS84 17S Datum. | ||||||

Source: Solaris Resources

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

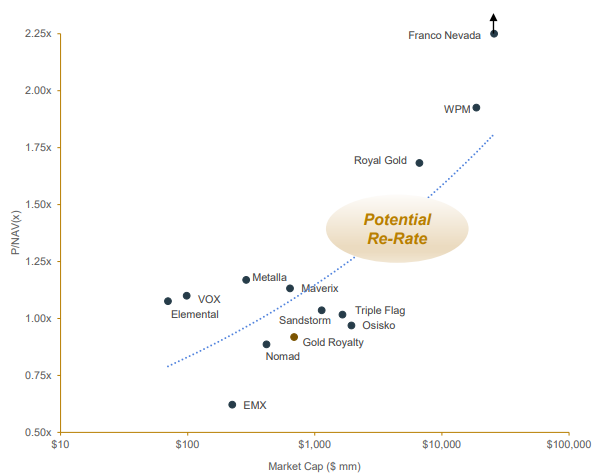

Gold Royalty Corp (NYSE:GROY) is down over 9% YTD, significantly underperforming GDXJ. The poor performance could be attributed to arbitrage shorts and sentiment that the premium being offered for Elemental (OTCQX:ELEMF) is too high.

The high premium and aggressive M&A posture of Gold Royalty can be viewed in light of CEO David Garafelo’s thesis that there will be strong investor appetite for a mid-cap in the space.

Elemental’s superior cash position

Gold Royalty announced its intent to acquire Elemental on Dec. 20, 2021. The offer of 0.27 GROY per share of Elemental was a 37% premium at the time. Since the value of GROY has fallen, the current premium is closer to 28%.

Elemental’s Board rejected the offer as “opportunistic”, stating it “substantially undervalues the company’s portfolio of revenue-generating royalties”. Gold Royalty is taking the offer directly to shareholders in a hostile bid.

The initial offer would value Elemental at just over $100 million with a P/NAV of about 1.4, well above the average for small-cap peers, which is closer to 1.0x. The transaction rationale highlights Elemental’s cash flowing assets. Elemental had revenue over $4 million for the first three quarters of 2021 versus Gold Royalty’s $192,000 (despite GRC having ~6 times the market cap). Also notable is Elemental’s relatively favourable cash position of $5.6 million (Q3 2021) versus $9.9 million for Gold Royalty.

As CEO David Garofalo states, “one of the key factors that drew us to Elemental is its attractive mix of cash flowing and near-term development assets”.

Seeking a Re-Rate

Despite negative market reaction, the bid is consistent with Garofalo’s capitalization strategy.

Garofalo reiterates the common value proposition in the space: the macro outlook for gold is positive; operating cost inflation and the need for capital investment on the part of miners will mean that royalty companies are a better leverage on the price of the metal.

However, investors face a market saturated with small-cap players who have entered the space anticipating the need for producers to use their strong cash positions to invest back into the ground. For Garofalo, the question is one of scale, where “the bigger you are, the more liquid you are, the higher valuation you get in the marketplace”.

There is a large gulf between the few large, $20-30 billion players (e.g. Wheaton, Franco Nevada) trading above NAV 2x, and the plethora of sub $1-2B small-caps trading closer to 1x. Gold Royalty sees re-rate opportunity somewhere in between: a $4-5 billion market cap that gets a 1.5x NAV valuation. Garofalo is anticipating that fundamentals will mean a larger pool of investors will be attracted to a NYSE listed gold royalty company with the liquidity and cash flow that small-caps don’t have, while maintaining a growth rate that exceeds the large caps. Part of this strategy is adding a dividend, which would explain why Elemental’s cash position would be attractive even though it does not add much breath to Gold Royalty’s portfolio.

The Canadian Malartic mine is a potential company building asset for Gold Royalty that could get it into the mid-cap category, but it is still at least 5 years from cash flowing. Meanwhile, Gold Royalty is walking a line between adding shareholder value or diluting it in the pursuit of growth.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is an insider or shareholder of one or more of the companies mentioned above.

Yorkton Ventures has announced that it has acquired the Sirmac East Lithium Project, which consists of 12 mining concessions divided into five blocks, in a total area of 656 hectares. The project is located in the James Bay area of Quebec, approximately 170 km northwest of Chibougamau.

Sirmac East Lithium Project is contiguous to the Sirmac property of Vision Lithium, an exploration company focused on high-grade battery mineral assets such as lithium and copper in secure jurisdictions in Canada.

Lithium does not exist on its own in nature. It is derived primarily from two main sources, hard rock and brine. The Sirmac project is a source of hard rock lithium found in pegmatites containing spodumene.

The Sirmac East Project is located within the Sirmac lithium deposit. The Sirmac property consists of 155 mining concessions with an area of approximately 7,670 hectares. Forest roads run alongside the property and to access the project, a network of highways must be traversed. In addition, the area is crossed by a 700kV power line.

The Sirmac property hosts at least two mapped historical lithium occurrences in the western part of the region, making it a highly prospective project for lithium (Sirmac Lithium and Clapier Lithium). In the northwestern part of the region, at least one lithium-bearing boulder has been found on land with Provincial Park status although the position of this boulder indicates that the area has great potential for new discoveries.

The deposit type associated with the lithium mineralization on the Sirmac property is a granitic pegmatite containing rare elements due to the presence of spodumene in an amount ranging from 5 to 30% by volume. The crystals are generally slightly altered as they contain rounded quartz inclusions. In 1994, Wrightbar Mine Ltd. conducted a historical resource estimate on the deposit which resulted in a total of 314,328 tonnes grading 2.04% Li2O.

Geologically, the Sirmac East Lithium project is located in the northwestern part of the Superior geological province in the Frote-Evans volcano-sedimentary belt. The structural trend is approximately east-west trending.

Four lithologies occur within the project area which include quartz-biotite-hornblende schists, amphibolite flows or mafic sills, spodumene-bearing pegmatites and a syenite pluton measuring about 6 km in diameter. Lithium mineralization is associated with granitic pegmatites with spodumene-bearing elements. The Sirmac East Lithium Project is also contiguous to Winsome Resources’ Sirmac-Clapier property and Troilus Gold’s Troilus Gold Project.

The seller will retain a 2% NSR (Net Smelter Return) of which Yorkton venture may acquire one-half by paying C$1 million in cash at any time. For an undisclosed sum, Yorkton also acquired last month a group of three non-contiguous lithium properties in the James Bay area of Quebec. The acquired project is known as the Cyr-Kapiwak Project comprising 42 mineral concessions over a total area of 220 hectares.

The project includes the Key Lithium, Amisk West lithium and Amisk East Lithium properties and is located 100 km east of Eastmain and 170 km south of Radisson.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

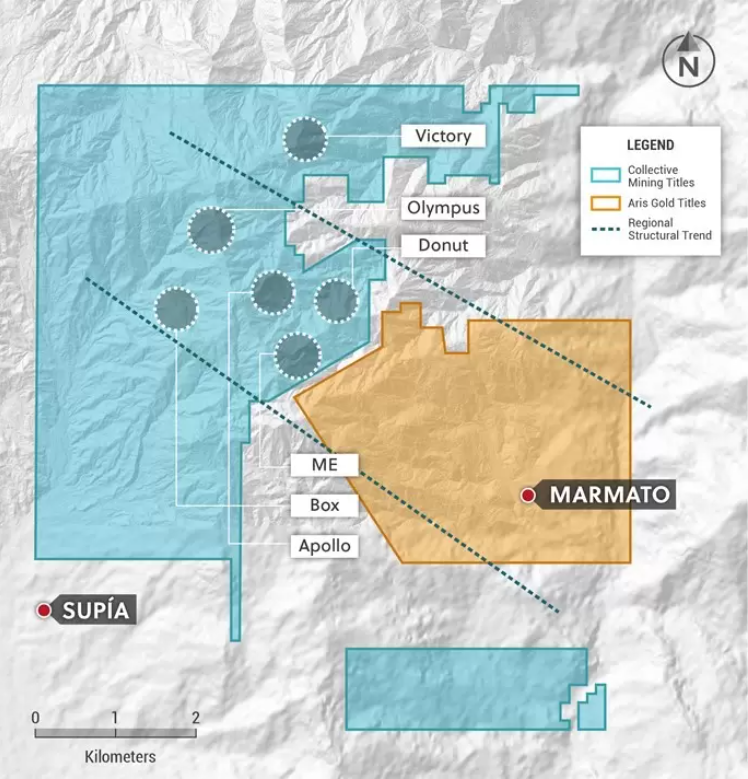

Colombia focused Collective Mining Ltd announced further high-grade gold and silver vein grab sample assay results from it’s grassroot generated Olympus target located within the Guayabales project in Colombia in a recent press release.

The company currently has two diamond drill rigs operating at Olympus with a third rig anticipated to commence drilling in approximately one week. The company has a minimum 20,000 metre program for 2022, in which all three drills are a part of.

Ari Sussman, Executive Chairman of Collective commented “Olympus continues to deliver in terms of high-grade veins and porphyry potential. The recent IP work has now considerably extended the target. This extremely exciting grass roots discovery will be a priority area for drilling in 2022 and the company is committed to constructing enough drill pads to test the full potential extent of the mineralized system.”

The highlights from the results are as follows:

Assay results of grab samples taken from veins located within historical, shallow underground adits from the northwestern region to the Olympus target confirm the continuation of the high-grade carbonate base metal (“CBM”) sheeted vein system with results as follows:

Table 1: Grab Sample Assay Results from the Northwestern Sector of Olympus

| Sample ID | Au g/t | Ag g/t |

| CM3350 | 112.3 | 544 |

| CM3516 | 57.1 | 634 |

| CM3341 | 55.4 | 439 |

| CM3351 | 25.4 | 521 |

| CM3334 | 10.9 | 268 |

| CM3349 | 7.3 | 206 |

| CM3336 | 7.2 | 179 |

| CM3339 | 7.0 | 474 |

| CM3345 | 5.7 | 144 |

| CM3346 | 4.5 | 107 |

| CM3347 | 3.3 | 68 |

- Multiple CBM vein systems were sampled, where possible, over a 250-metre-wide area from limited and partial exposures of rock. These new high-grade samples now extend the known CBM vein exposure at Olympus to an area measuring more than 600 metres by 600 metres. The CBM veins are sulphide rich and coincident with IP chargeability anomalies. Recently revised interpretation of the IP data by the Company has now expanded the surface area of Olympus to 1,250 metres north-south by 750 metres east-west.

- Preliminary logging of the first completed holes into the eastern portion of Olympus indicates that the Company has intersected multiple CBM veins hosted within intensely altered porphyry diorite and hydrothermal breccia.

- Collective has made the Olympus target a 2022 priority area for drilling due to its grade, potential size, and multiple mineralization styles, including porphyries, high-grade carbonate base metal veins and breccias.

Source: Collective Mining

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

On January 10, Three Valley Copper, (TSXV:TVC), a junior gold exploration, development, and production company based in Toronto, Canada, began trading on the OTCQB under the symbol “TVCCF”. Shares of Three Valley Copper continue to trade on the TSX Venture Exchange.

The move will expand the company’s accessibility across the border in the biggest capital market available, and allow U.S.-based investors to have more efficient access to trading TVC shares. This will ultimately broaden the company’s investor base.

Three Valley Copper’s primary asset, Minera Tres Valles in Salamanca, Chile, is the focus of the company’s efforts and the primary asset of interest for investors. It is a producing mine with 46,348 hectares at the property, with approximately 90% of the property remaining unexplored. The potential for new discovery is high at MTV, and a new exploration drilling program will begin shortly.

The company recently increased its ownership in Minera Tres Valles from 91.1% to 95.1%, gaining further operational control. The company is now in the process of expanding capacity at the site to increase copper production in 2022 and 2023. Planned exploration will continue in 2022, and shareholders on both sides of the border stand to gain significantly from the advancement of this project.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

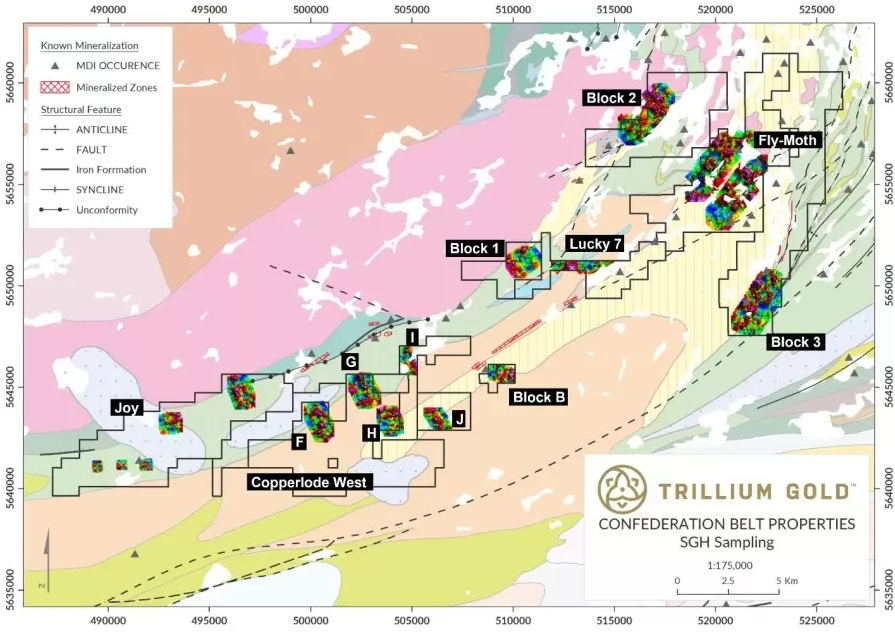

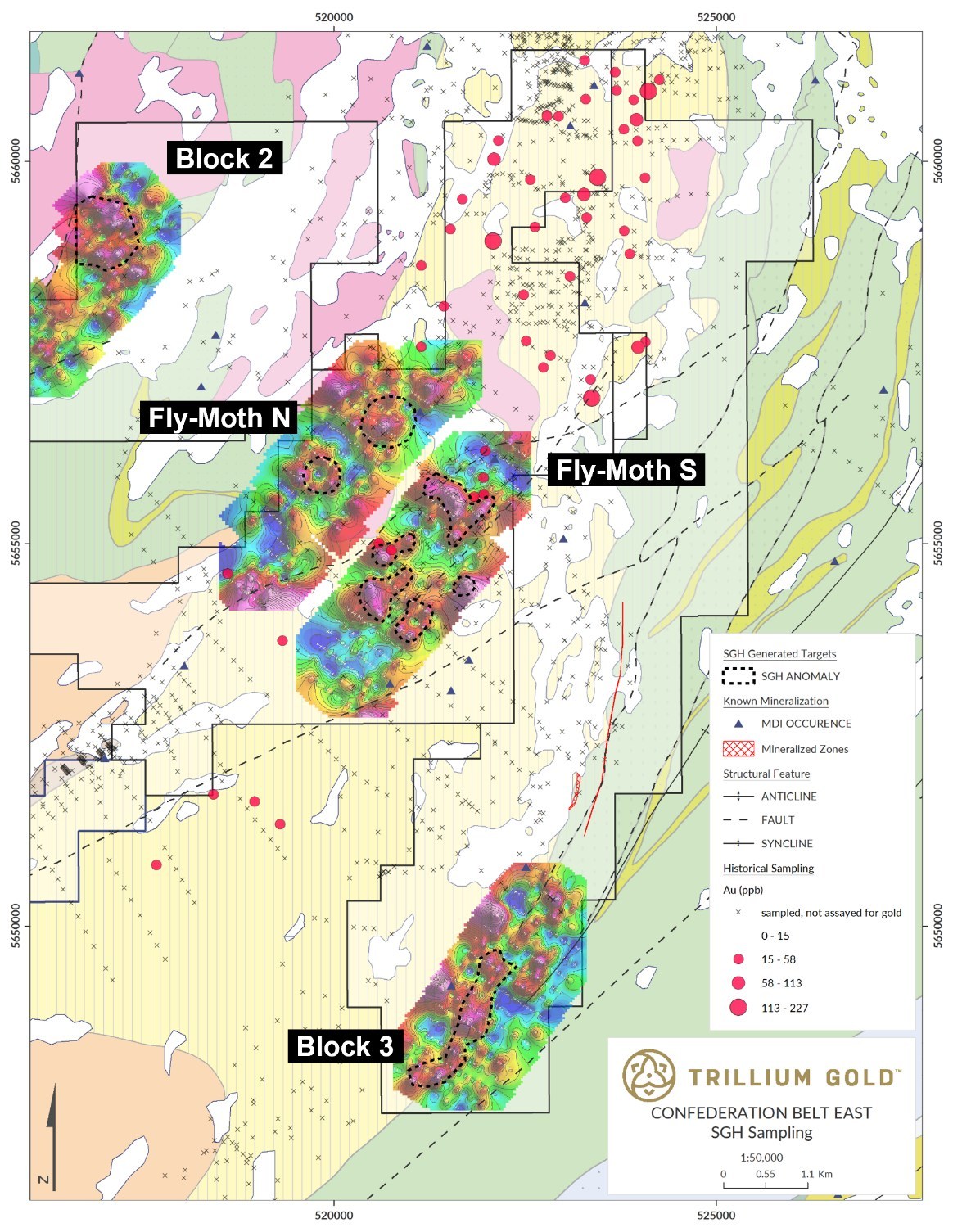

After acquiring a significant land package and consolidating its position in the Red Lake Mining District in Canada, Trilliium Gold Mines Inc (TSXX:TGM) (OTC:TGLDF) has announced this morning it has discovered multiple gold anomalies along its Confederation Belt Properties in Red Lake.

A spaciotemporal geochemical hydrocarbon sampling program was completed during the summer of 2021 at the Confederation Belt properties. This survey unveiled numerous gold pathfinder anomalies with rating categories ranging from 1-6. This has now confirmed and established the gold exploration potential of Trillium’s properties. These properties form a 39,300 hectare contiguous land position directly on trend with other discoveries currently unfolding in the district and therefore makes Trillium Gold’s position highly valuable.

The gold pathfinder anomalies identified by the survey conducted by Activation Laboratories will now serve as the priority targets for the company’s second for of exploration work in the 2022 field season. Trillium can use the sampling and concurrent prospecting program to generate multiple drill targets.

Red Lake Mining District has already produced 29 million ounces of high-grade gold. Red Lake is one of the country’s premier mining districts, and has infrastructure, million, and roads in place for efficient drilling and exploration. The survey focused on some key blocks at the properties, to focus on known base metal and minor gold mineralization intersected in historical drilling, including the Joy Block. A significant portion o the Joy-Copperlode Blocks are covered by variably conductive outwash and deglaciation sediments.

Information from the surveys according to the press release includes:

The three smaller grids in the southwest of the Joy Block were designed as orientation surveys over known base metal and minor gold mineralization intersected in historical drilling. A large portion of the Joy-Copperlode Blocks are covered by variably conductive outwash and deglaciation sediments (not locally derived) and despite no outcrop identified in these areas, all three returned anomalies, the western-most two confirming the method over known drill hole results.

Based on a synthesis of previous work reviewed to date by Company geologists, these anomalies appear likely spatially associated with more than one type of control (i.e., late-stage structural, lithological, as well as possible earlier structures (syn-volcanic?), as previously interpreted in historical work). The location of the anomalies is directly on trend with regional-scale faults (as at Great Bear’s Dixie Project) and provide a new framework on which to focus gold exploration in the belt and region.

Several new target areas have also been confirmed where historically very little exploration work has been conducted (e.g., the northern-most anomaly on the Copperlode property, I-anomaly, Figure 1). These new discoveries provide exciting new targets for follow-up work.

On the Copperlode West block, the F-anomaly is a highly-rated anomaly cut by a NW-SE trending magnetic lineament (possibly D2 orientation?) and represents one of the more encouraging targets in the area. Also of high-rating is the I–anomaly which lies on the western extension of an EM conductor in an area with no known historical geological, geochemical or geophysical surveys. The J-anomaly was identified as a potential Redox zone by Actlabs, similar to that at the Dixie Hinge and Limb zones sampled by Great Bear Resources (news release August 1, 2019).

The Block B anomaly is also highly rated and shows parallel responses coincident with a magnetic high trend, and coincident with or flanking a NE trending EM conductor.

The Block 1 anomalies lie within stratigraphy representing the eastern extension of that hosting the copper-molybdenum mineralization near Fredart Lake. The two geochemical signatures appear to be on strike from one another, hosted by iron formation or ferruginous sediments. There has been very little historical work in this area. The Lucky 7 anomaly lies within an EM conductor trend that has been drilled, off-property, intersecting gold values up to 4 g/t over 1.5ft. Grab samples in the drilled area also ran up to 13 g/t gold.

The Block 2 anomaly, among the highest rated by Actlabs, shows a significant number of high contrast peaks over a large, 600m x 450m area. Actlabs identify it as a segmented nested-halo anomaly coincident to that of the Redox zone. The potential for gold mineralization here is believed to possibly exist directly below this anomaly.

The Fly-Moth N and S grids serve as extensions to exploration work on known prospective and mineralized trends associated with the past-producing South Bay Mine. There are anomalous gold values in historical lithogeochemical samples in the general area around the mine; however, samples further towards the southwest were not assayed for gold. The SGH grids fill in the data gaps and successfully highlight new gold anomalies. These anomalies are highly rated and show characteristics of Redox Zones as well.

Here, the controls on processes responsible for the development of these anomalies likely reflect a complex interplay between lithology and structure. There appears to be some, but not exclusive, spatial lithological control locally (e.g., near Triangle Lake) as the anomalies are associated with minor intrusive rocks which themselves were previously interpreted as fault controlled. However, one anomaly coincides directly with a previously mapped rhyolite tuff unit suggesting the possibility of lithologically hosted gold.

Equally, the geometry of elevated gold in this package of rocks could be suggestive of syn-volcanic fault-controlled mineralization. At the southern edge of Triangle Lake, historical work identified anomalous gold that coincides with a previously mapped fault. These types of relationships bear investigating for refinement or confirmation of ideas with follow-up exploration work planned for 2022.

The Block 3 anomaly coincides with several important features: a regional-scale fault trace, a major volcanic break (cf. Thurston et al, 1980), and a property scale transition from felsic to mafic volcanic rocks. Historical work on the property identified several sulphide zones and/or geophysical conductors. The few historical drill holes in the general area, inconsistently sampled for base metals and even more infrequently for precious metals, do show elevated copper, zinc and gold in these sulphide horizons.

Conversely, in the direct vicinity of the anomaly, virtually no geochemical work has been performed, and there are only two known drill holes, the locations of which remain uncertain.

Source: Trillium Gold Mines

After recently acquiring the Confederation Lake assemblage from Infinite Ore Corp., the company has become one of the dominant explorers in the Red Lake Mining District. The Eastern Vision property holdings at Confederation Lake include 16,991 hectares, and give Trillium control over a large portion of the assemblage. Most importantly, it gives the company control over a contiguous land package that now covers over 100 km of favourable structure on trend with Great Bear Resources’ Dixie Deposit.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Richard Ryan Penn and Roman Reuven Rubin, chief executive officer and former chief financial officer and secretary of Black Tusk, were fined for insider trading over a three-year period. Both executives were fined by the BC Securities and Exchange Commission for failing to disclose information regarding their insider share sales to the authorities.

Black Tusk Resources is a Canadian mining company with six gold and palladium projects in Canada, although most of the projects are located in Quebec, one is in BC 145 kilometers south of Smithers. In a settlement with the BC Securities Commission, executives admitted to failing to report most of their transactions to authorities with respect to internal share sales.

A notice issued Jan. 6 by the Securities Commission reported, “As corporate insiders, Penn and Rubin were required to report transactions in their securities on the Electronic Disclosure System by publicly available insiders.” However, for the period between January 2018 and December 2021, Penn and Rubin did not report their securities transactions for the period between January 2018 and December 2021.

Richard Ryan Penn reportedly failed to report 87% of transactions valued at $1,155,947 million. For his part, Roman Reuven Rubin omitted information on 96% of the transactions made in the same period, such transactions were valued at $646,566.

According to the agreements reached by the BC Securities and Exchange Commission with Penn and Rubin, the current CEO of the company must pay a fine of $75,000 dollars as well as complete an educational course on how to be a responsible director of a public company. Rubin, on the other hand, decided to resign from his position as CFO of Black Tusk Resources and was ordered to pay a $65,000 fine and complete the same course.

Misrepresentation of Holdings

The executives were held responsible for Black Tusk’s misrepresentation of the number of shares held by the company because Penn and Rubin did not issue press releases when they reduced their holdings of Black Tusk common stock, thereby misrepresenting the number of shares they each owned. However, the executives are estimated to have taken home cash salaries of $120,000 in 2021, according to the latest management documents.

In October 2019, the company had stated that Penn held 2,924,500 shares of Black Tusk stock when it actually held only 1,093,725; and in November 2020, the company had misleadingly stated that Penn held 5,014,500 shares when it actually owned only 505,075.

Although Penn and Rubin made the required filings, paid late fees, and the company issued press releases correcting the disclosure of their holdings, it is unclear how much profit the company executives may have made by selling their shares during that time period.

Since Penn took over as CEO of Black Tusk in 2017, the company has had no revenue, limited resources, and no sources of operating cash. According to its 2021 annual audit, the company reported a net loss of $3.28 million.

Black Tusk’s Multiple Projects

Black Tusk Resources Inc. is a Canadian mineral exploration company focused on gold and precious metals mining and drilling. The company currently conducts exploration and development activities on 6 separate gold and PGE projects: McKenzie East Gold Project, Golden Valley Project, Lorraine Property, PG Highway Property, MoGold Property, and South Rim Gold Project. The company has offices in Vancouver and Montreal, with six gold and palladium projects, the majority of which are located in Quebec, and the other located in British Columbia.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Kazakhstan, the world’s number one uranium producer, continues to produce and output uranium despite the ongoing protests currently happening within the Central Asian State. Risks remain, but the industry has remained largely unaffected by the unrest. Protests began due to fuel prices rising, and as a result of the unrest in the streets of Kazakhstan, uranium prices have also risen to the highest they have been since November 30., no there have not been any stoppages.

The price for the metal has been up and down over the past year, sitting around $30 per pound in August, then rising again towards the end of the year at $45 per pound in November before falling to $42 per pound by December. Currently, the price sits at 45.50 per pound, and could continue to rise on the basis of supply uncertainty.

Analysts at Canaccord Genuity commented in a note that they expect the market could see further upward pressure on uranium prices and equities until the situation in Kazakhstan starts to subdue and come to a stop.

The widespread uproar initially started as the price of liquefied petroleum gas (LPG), which many Kazakhs use to fuel their cars and get to where they need to go, began to rise. As time went on, politics were included in the protests such as criticizing Kazakhstan’s long autocratic rule.

The largest uranium producer in the world and Kazakhstan itself, Kazatomprom, has remained unaffected throughout the entirety of the protests, and output of uranium has continued as usual. Uranium mines in Kazakhstan are located in remote regions of Turkestan oblast, far enough away from the turmoil and protests that production is unaffected. As of January 6, there were no reports of the uranium workers joining the disruptions.

“Uranium mining is going according to plan there have been no stoppages. The company is fulfilling its export contracts,” a Kazatomprom spokesperson said.

Since the protests have begun, around 1,000 people have been injured, and dozens of anti-government protesters have reportedly been killed in Kazakhstan’s largest city Almaty. In order to help calm the protest, BBC news reported that president Jomart Toqayev dismissed his and Nursultan Nazarbayev cabinet, while also calling upon the Russian-led regional security organization CSTO to help restore order to the country.

Uranium from Kazakhstan accounts for 40% of the global uranium output, just under half of the entire world’s uranium supply comes from this Central Asian state. According to Kazatomprom’s website, the company’s production represented about 23% of global primary uranium output in 2020.

Uranium is mainly used for powering nuclear reactors which are used at nuclear power plants in order to generate electricity. It is a naturally radioactive element, is very heavy and is a silvery-grey colour. Uranium is such an important metal because it provides nuclear fuel which generates electricity in nuclear power plants. The power is generated by using heat to boil water and create steam, which turns huge turbines creating energy. A chemical process called nuclear fission creates the heat for the water to boil.

The continued unrest resulted in a hasty selloff of uranium stocks in Toronto on January 6, halting uranium equities rallying up until Wednesday. Canadian uranium companies also fell between 5 and 7% in the early morning trading on Thursday, including Cameco (TSX:CCO), Denison Mines (TSX:DML), and NexGen Energy (TSX:NXE).

Shares differ between uranium producers, for example Kazatomprom’s London-listed shares were down almost 5% on Thursday, while Cameco’s shares were up Wednesday, and have been on an upward trend of 12% in the year to date.

There have been no reported actions or sightings of the protests slowing or stopping, and as long as the disruptions refrain from spreading or include uranium plant workers, uranium output should continue as normal. If fuel prices begin to lower, protests could potentially slow down, and prices could start to slowly decrease.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Due to drops in copper output from state-owned Codelco and BHP’s Escondida mine, Chile saw its total copper production drop in November by 0.6% year-on-year down to 481,800 tonnes, according to the Chilean Copper Commission (Cochilco) report published on Tuesday.

When compared to the previous year during the same period, Codelco experienced an output drop of 7.4% in November, decreasing to 153,800 tonnes. This was a total 0.4% drop in production in 2021 so far for the copper company. Codelco is approaching its 50th year since it was created in 1976, and mainly focuses on the exploration, development, and refining process of copper.

The world’s largest copper mine, BHP’s Escondida, also experienced an output drop in November. Extraction fell 11.6% compared to last year, totaling 80,300 tonnes for the month. In 2021 through November, the mine recorded a 14.5% drop in output.

BHP’s Escondida is the world’s biggest producer of copper concentrates and cathodes. The copper deposit is located in the Atacama Desert in Northern Chile, 170km southeast of Antofagasta. The name ‘Escondida’ actually means ‘hidden’ in Spanish because it is hidden by hundreds of meters of overburden. Oppositely, the Collahuasi copper mine, which is a joint venture by Glencore and Anglo American, reported a 5.1% year-on-year rise in production to 50,700 tonnes, according to Cochilco.

Shifting Politics

The biggest recent change for Chile was the election of a new president, Gabriel Boric. Many in the mining and copper industry have concerns regarding new rules and regulations surrounding the mining sector that Boric has already begun to discuss.

Boric has already pledged to oppose the $2.5 billion iron-copper mine known as the Dominga mine, after years of legal battles back and forth. He is passionate about the environment and believes the high pollution that would come from this mine would not be worth what it could produce and create.

Boric, who is 35, will be the youngest leader in the history of Chile since President Salvador Allende, and plans to make a plethora of changes to the nation, including drafting a new constitution. The 2022 year will be a time of change and adaptation for the entire mining industry under his new environmentally focused changes and rules. While Boric will be aiming for an environmentally friendly and ESG mining environment, there may be compromises to be found yet, as slowing down an industry that is so critical to the Chilean economy would not be feasible without serious consequences.

Models Prove the Chilean Upward Trend

Chile is the world’s largest copper producer, from January until August 2021, Chile’s copper production totaled 3.73 million metric tons. In 2020, Chile’s copper production was about 5.7 metric tons, accounting for approximately 28.5 % of the global copper production that year.

According to trading economics models, Chilean copper production is projected to trend around 540.00 thousands of tonnes in 2023.

Not only is Chile the world’s largest copper producer, but they also have some of the biggest lithium reserves in the world. Boric in the past has criticized privatization in the mining sector and would like to see the state have its own lithium firm, but has not touched on these plans again since pledging to create one.

As the global pandemic and supply and demand continue to change and update, and Boric takes his place as president in March, Chile can expect to see lots of changes in the upcoming 2022 year.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

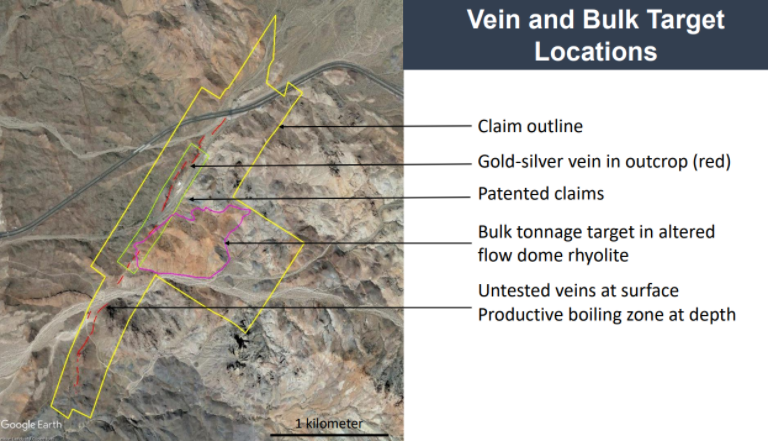

Assay results released by Arizona Silver (TSXV: AZS) last month indicate a larger than expected bulk tonnage target on their Philadelphia property. Deeper diamond drilling across the high-grade vein is needed to confirm the extent of the mineable system.

New potential in a historic mining district

Arizona Silver is a junior explorer focused on the southwest US. Their current drilling is on the Philadelphia property, a high-grade gold and silver vein in Mohave County in northwestern Arizona. The property is at the north end of the historic Oatman Mining District where the Oatman Mines produced over 1.5M oz. Au, and where the Moss and Gold Road mines are currently operating.

The district was mined most heavily from the 1890s until 1942 when area operations were deemed unessential to the war effort. This history, combined with Arizona having been less explored than neighboring Nevada, has led some to believe the district may host unexplored resources while still having solid infrastructure.

Arizona Silver began exploration in 2019/20. Drilling intersected a high-grade vein (Au: 41.6 gpt across 0.76m, 23.5 gpt over 2.3m, 33.6 gpt over 2.4m, 9.3 gpt over 10.8m), with a strike length extending 3km. A drilling campaign completed in summer 2021 discovered bulk tonnage above the vein, which the latest results suggest extends to a depth of over 100m.

According to Greg Hahn, VP of Exploration, “the Philadelphia Property is one of the few gold systems remaining in the Western USA that has never been evaluated using modern exploration concepts…. Discovering the bulk tonnage target answered my question as to why we see such a remarkable alteration feature at surface. All this project needs is drilling to demonstrate its real potential.”

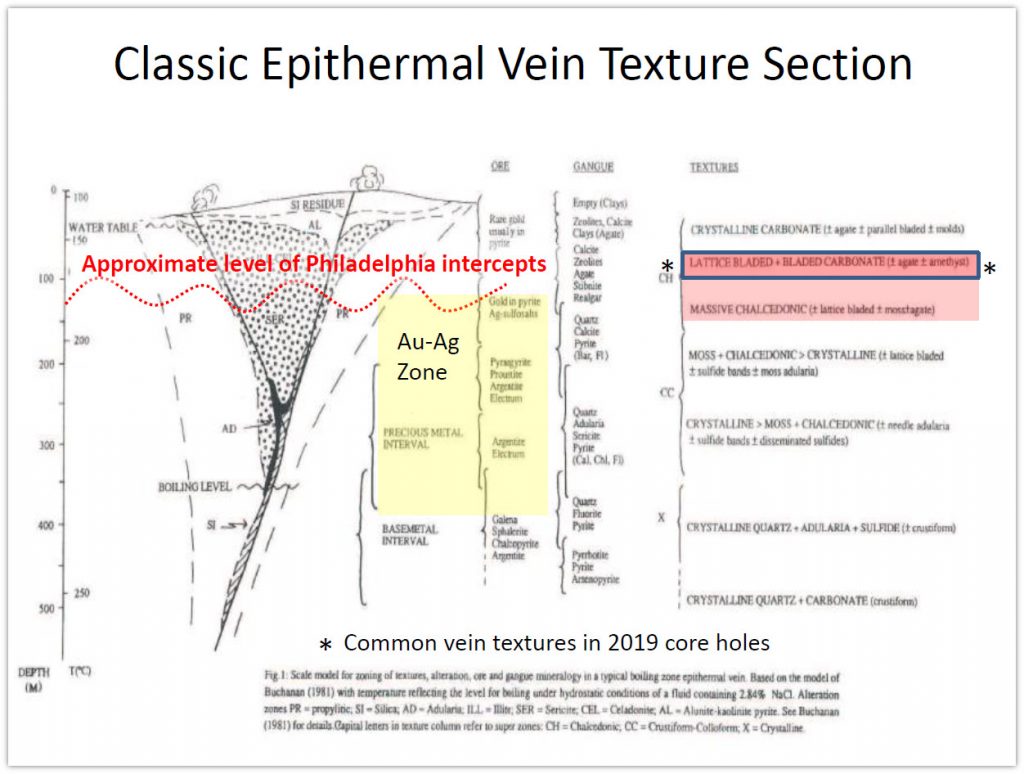

Estimating the extent of the epithermal system

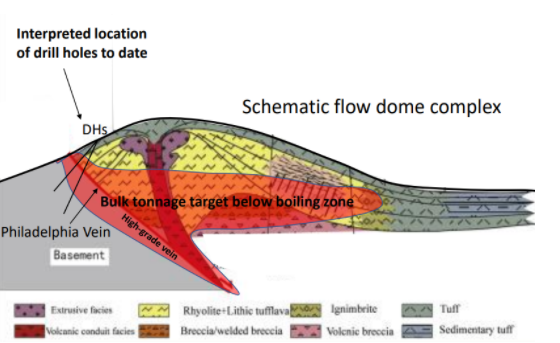

The initial exploration focus was based on historical production in the region, characterized by veins as opposed to bulk zones. The orebody at the Oatman Mine, for instance, assayed less than 1 gpt at narrow widths up to the boiling zone at about 65m. Beyond the boiling zone, grade went up dramatically to a depth of 300m at +1 oz/ton over a 10m width.

Arizona believes drilling to date has been only at the top of the boiling zone. Drilling results are consistent with classic epithermal veins, with a large breccia extending above the high-grade system. “We just need to go deeper down into the system to get into the heart of the boiling zone”, says Hahn.

The schematic of the epithermal system at Philadelphia depicts a high-grade vein, separating basement from the rhyolite complex which hosts the bulk tonnage target.

Schematic of bulk tonnage target. (Source: Arizona Silver)

Arizona estimates the size of the initial vein target block resource area as 400m x 200m x 5m. The average vein grade has been just over 8 gpt Au but, based on the Oatman epithermal model, the expectation is that both grade and thickness will increase as they continue to drill at depth.

When initially targeting the vein, Arizona didn’t expect a mineable grade in the bulk material. The initial bulk target is estimated in the range of 400m x 200m x 100m with +1 gpt Au. Arizona cites the potential total bulk zone size as 600m x 600m x 100m.

What to expect moving forward

Targets for continued drilling include the high-grade vein system, the bulk tonnage stockwork zone, and an undrilled southern extension to the vein system.

To date, the RC drill has been limited to points on the northern and southern edges of the initial 600m strike. Roads and access pads will need to be completed before samples along the full high-grade zone can be drilled.

Meanwhile, recently completed financing will provide the budget to drill step-out holes and continue along the down dip of the main vein. Assay sections and proposed holes can be found here.

Philadelphia Project Presentation Video

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Adventus mining Corporation, the copper and gold exploration company, together with Ecuadorian Salazar Resources (TSXV:SRL), have formed a joint venture (JV), with the objective of developing the Curipamba copper-gold project in Ecuador. In 2017, Adventus Mining agreed together with Salazar Resources, that by funding exploration and development expenditures of US$25 million over five years, the company could earn a majority interest in the Curipamba project located in central Ecuador.

The agreement required the company to fulfill certain development obligations, including the completion of the reliability study for the development of the high grade El Domo volcanic massive sulfide (VMS) copper-gold massive sulfide deposit, which was completed last year.

Adventus is also obligated to fund 100% of the project’s production capital costs upon completion of the reliability study. The company will receive 95% of the free cash flows until all of its investments made since 2017, are recovered. Once expenditures and capital costs have been reimbursed to Adventus, the cash flows will be shared between Adventus and Salazar Resources with 75% and 25% respectively.

Through September 2021, Adventus earned $44.1 million of total earn-in expenditures on the Curipamba project and the company plans to continue to advance further exploration in new areas within the Curipamba project and complete an investment agreement with the Ecuadorian government by the first quarter of 2022.

The Curipamba project, located approximately 150 km from the port city of Guayaquil, consists of seven concessions covering 215 km2 including the El Domo advanced high-grade copper-gold deposit. El Domo is a flat tabular VMS deposit with dimensions of approximately 800 x 400 meters. Three gravel roads provide direct access to El Domo and most of the Curipamba project area.

After systematic exploration work was carried out over the entire Curipamba property, and after El Domo was discovered in 2008, the partners completed a MobileMT airborne geophysical survey in 2019 for a total of 2,142 line kilometers. With this, the partners succeeded through a target generation initiative (TGI) in processing and integrating all geoscience data collected from surface geochemistry, geological mapping, prospecting, drilling and ground geophysical surveys at Curipamba. These data were compiled for a target ranking that drove the 2020- 2021 exploration planning.