Galantas Gold (TSX:GAL) has announced it will restart commercial operations at the Omagh gold mine in June. The Northern Ireland mine is a past-producing mine with ongoing refurbishing.

The company delayed any completion of the secondary egress and installation of the manway, to mid-May. If this had been completed earlier, production could have begun earlier, however, it is necessary for the start of production. The extra time was needed for rehabilitation of the ramp access and ore headings due to safety reasons.

However, the Canada-based junior miner reported that it had made significant progress in rebuilding the underground workings and tunnels, refurbishing, and acquiring vital mining equipment, among other things.

In 2017, Northern Ireland was hit by a wave of insecurity. The police (PSNI) had to increase the availability of anti-terrorism cover so that Omagh’s subterranean development could be resumed. Other limitations imposed by the PSNI again delayed blasting activities in 2019, with ore production suspended the following year because of insufficient funds and the global health pandemic disrupting operations.

The company said in January that preliminary production is anticipated to reach 4,500 to 5,500 ounces through the end of the year and rise to 17,800 ounces in gold concentrate by 2023. A second stage of the operation would increase annual gold production to 35,000 ounces.

Northern Ireland

Galantas is not the only Canadian miner in Ireland, with Dalradian Resources (TSX:DNA) also working on a proposed gold project since early 2010 in the Tyrone region. Since Northern Ireland holds the seventh richest gold resource in the world, but for decades a string of violence and safety concerns have kept investors away from the country.

In September 2021, the gold mining companies operating in Northern Ireland were able to secure an agreement granting them free policing linked to the handling of explosives at mines. This requires special police services, which Galantas had required during operations. The company will be reimbursed for over $200,000 in costs that it paid for these services as part of the agreement.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Collective Mining (TSXV:CNL) announced yesterday it had intercepted a broad zone of mineralization at the second diamond drill hole at the Apollo target. A second rig has been mobilized, and the company expects assay results from the first hole at Apollo to be ready in the near term. Collective has three drill rigs at Guayabales, with ongoing drilling at Apllo and Olympus. The goal for the drilling is to expand on the announced Olympus Central discovery hole (302 metres @ 1.11 g/t gold equivalent).

Ari Sussman, Executive Chairman of Collective Mining, commented in a press release: “The Guayabales project continues to demonstrate that it has been blessed with a remarkable mineral endowment. We are early in the first inning of unlocking the potential of this asset and already we have drilled three potentially significant discoveries characterized by broad zones of mineralization. Assay results are expected from both Olympus and Apollo in the near term and our fully funded drill program will continue unabated through the balance of 2022.”

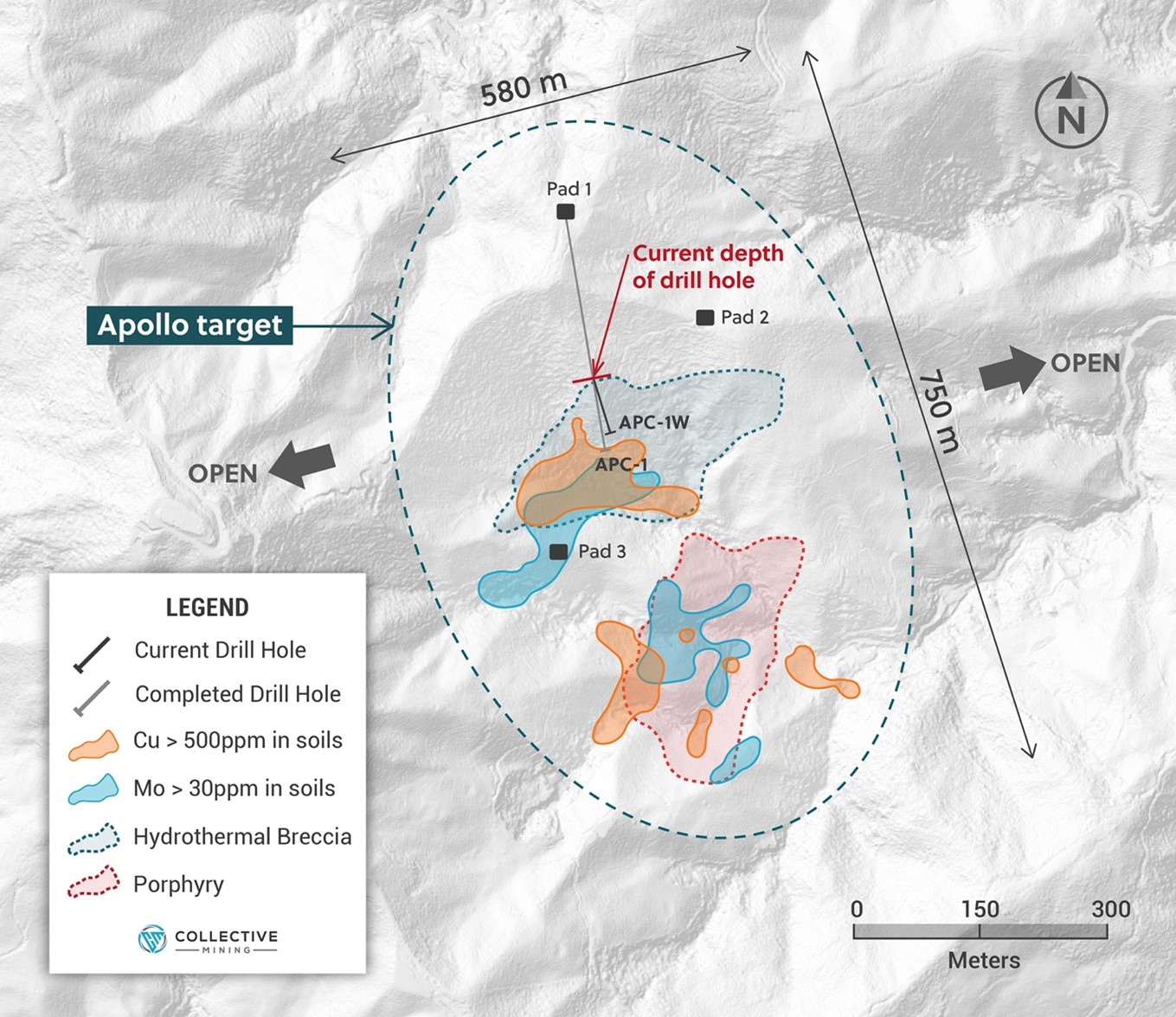

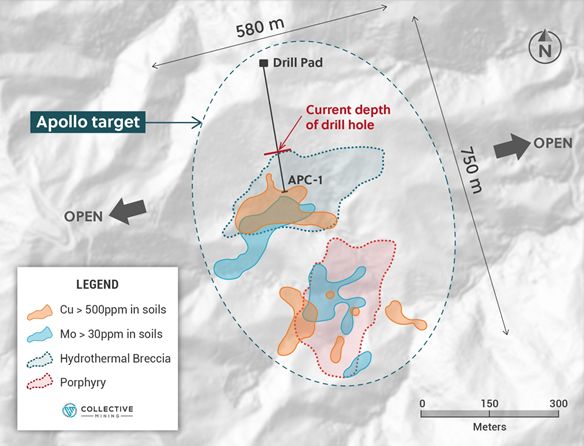

A porphyry target in the south and a porphyry-related hydrothermal breccia target flanking the north side have been outlined at Apollo through surface mapping and soil and rock chip sampling. The porphyry and breccia targets are characterized by coincidental high-grade copper and molybdenum soil anomalies measuring greater than 500 parts per million (“ppm”) and 30 ppm, respectively. Apollo spans 750 metres X 580 metres and remains open to the east, west and south for further expansion.

Figure 2: Plan View of the Apollo Target Area Outlining Porphyry and Breccia Targets Overprinted by High-Grade Coincidental Copper and Molybdenum Soil Anomalies

Highlights from the results are as follows:

- A maiden diamond drill program at Apollo began in April 2022 with the initial hole (“APC-1”) now complete to a final length of 438.7 metres. Beginning at 280 metres down hole, APC-1 intercepted favorable porphyry related hydrothermal breccia mineralization over a core length totalling between 85-90 metres. Core from this hole has been sent to the lab and assay results are expected shortly.

- Given the significant distance from the drill pad and to expedite drilling at Apollo, the Company is currently drilling at wedge hole (“APC-1W”), which was kicked-off from APC-1 at 213 metres down-hole. Drilled at a slightly steeper angle and to the east, APC-1W is currently at 85 metres and is still drilling within favorable visual breccia mineralization. Drilling of the hole will continue until the hole exits from the breccia mineralization.

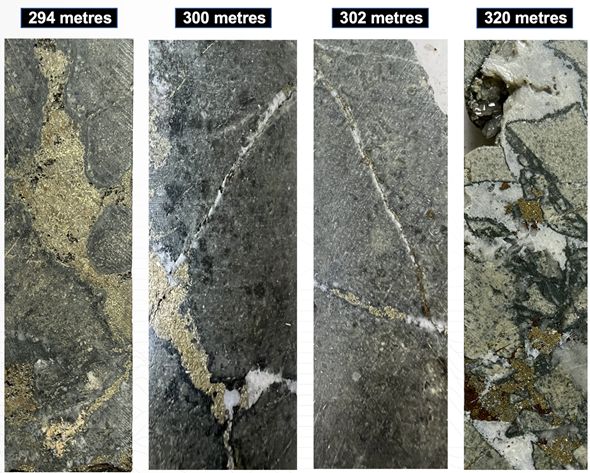

- The breccia matrix consists of approximately 4-5% pyrite and 1-1.5% chalcopyrite with overprinting carbonate base metal (“CBM”) veins in places (see press release dated April 12, 2022, for further details).

- Considering the encouraging visual mineralization over broad widths intersected in both drill holes, the Company has initiated construction of two additional drill pads at Apollo (“Pad 2” and “Pad 3”), which will provide the Company with significantly better locations to test the full extent of the potential at Apollo. The rig that is currently drilling APC-1W will be moved to Pad 2 shortly and a second diamond drill rig will mobilize to Pad 3 shortly thereafter.

- Importantly, the mineralized breccia intercepts in APC-1 and APC-1W does not correspond with the coincidental high-grade copper and molybdenum soil anomalies covering both breccia and porphyry targets at Apollo. As a result, drill holes from Pad 2 and Pad 3 will also be designed to test both anomalies.

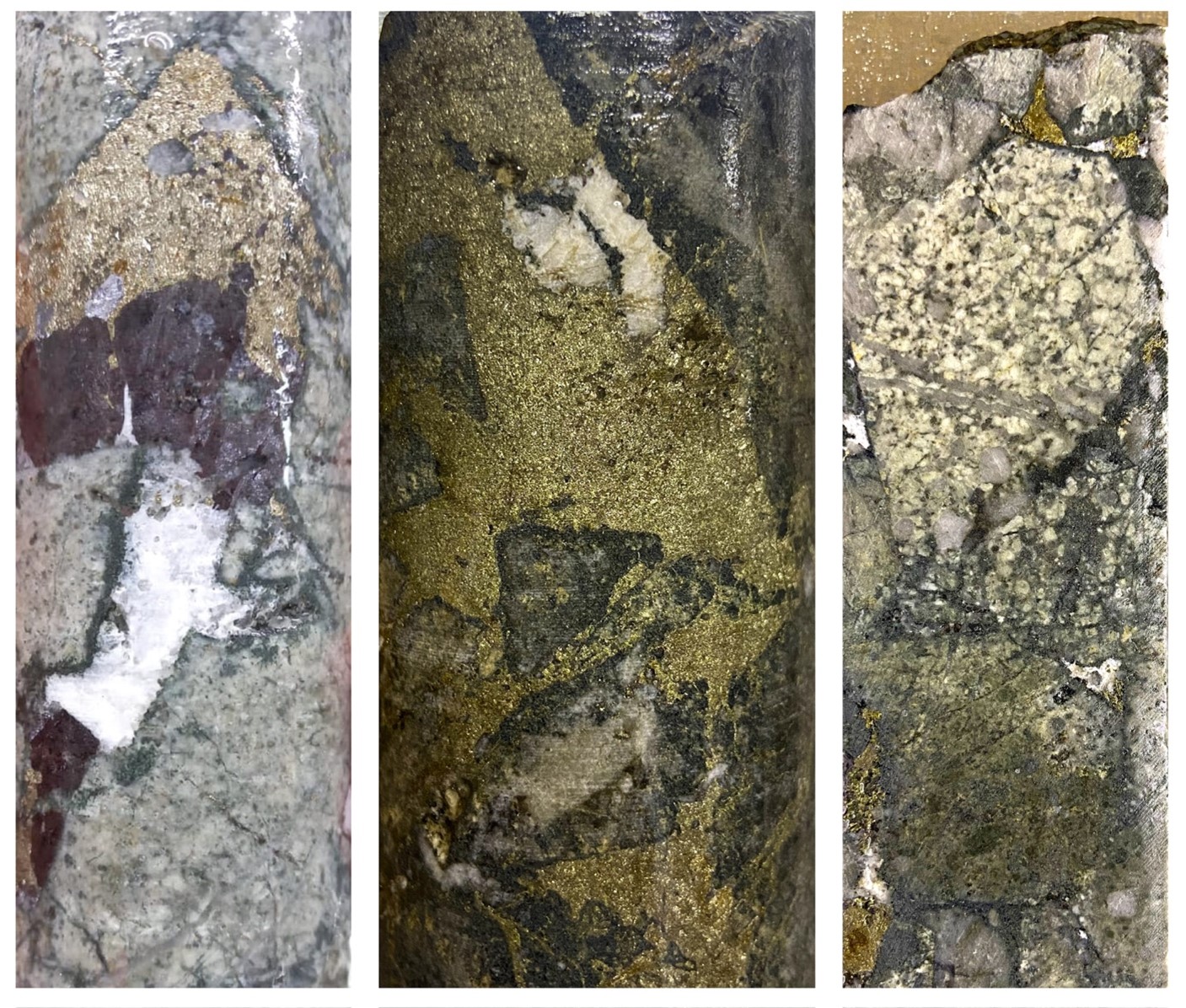

- The reader should be cautioned that only assay results from a certified third-party laboratory can confirm whether any amounts of precious or base metals are present in the breccia matrix currently being intersected in the drill hole. As such, visual core inspection presented herein should be viewed as speculative in nature.

Source: Collective Mining

Figure 3: Core Photos from Drill Hole APC-1W

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

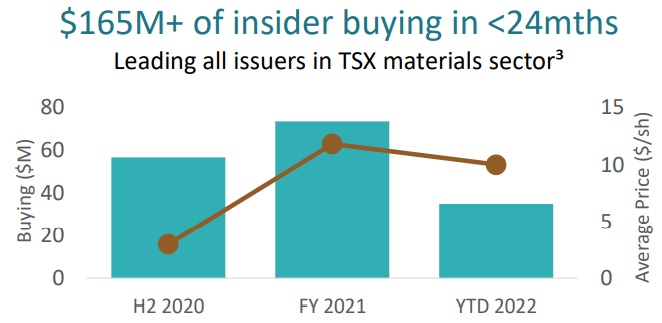

Insider buying at Solaris Resources (TSX:SLS) continues to show a large amount of stock being purchased throughout the last two years. On April 20, 2022, Richard Warke, Executive Chairman, bought C$35 million of Solaris stock through the exercise of 3,500,000 warrants. Warrants were set at $10 to buy 5 million shares of Solaris Resources from Equinox Gold. The warrants would have expired on April 26th, 2022.

Christian Milau, CEO of Equinox Gold, stated: “As a strategic and supportive shareholder, Equinox Gold is pleased to accommodate Solaris in this transaction, which benefits both companies. The proceeds from this sale will further strengthen Equinox Gold’s already solid balance sheet as we continue to execute on our expansion and growth objectives.”

A recent mineral resource update and the ongoing success of the drill program at Warintza may have insiders optimistic about the future of the company since they have been net buyers of shares since the IPO. The total insider shareholding of any given company gives investors an overall view of whether management and other inside investors are aligned with other shareholders.

Sunny Lowe, CFO of Solaris Resources (TSX:SLS), also purchased approximately C$100K in Solaris shares on the open market on Monday, April 25th, 2022. Total insider investment has reached over C$165 million in less than 24 months now, demonstrating a significant amount of confidence in the company by those in charge of its success. In the TSX materials sector, this places Solaris Resources (TSX:SLS) in the lead for insider buying. The company has seen strong interest in the stock since its IPO, up nearly 700%.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Bear Creek Mining (TSXV:BCM), based in Canada, has completed the purchase of a 100 percent stake in the Mercedes gold-silver mine in Mexico from Equinox Gold (TSX:EQX) of Toronto, Canada. The Mercedes mine is located in the northern, mineral and metal-rich state of Sonora. The mine consists of 43 mineral concessions spread across an area of 69,285 hectares. Equinox Gold gained ownership and control of the mine in 2021 when it acquired Premier Gold Mines.

Bear Creek Mining will pay $75 million as part of the agreement, which was signed in December 2021. On closing of the deal, Bear Creek Mining will pay a 2% net smelter return on production from the Mercedes mine. Equinox Gold has shifted its focus to larger production and development assets, and as such sees the sale as part of this strategy.

Bear Creek Mining president and CEO Anthony Hawkshaw commented in a press release: “We are extremely pleased to have acquired a producing gold-silver mine with a strong operating team, underlying assets with a replacement cost exceeding our purchase price and what we believe to be exciting “blue sky” exploration potential.”

Equinox Gold CEO Christian Milau also commented: “As a significant shareholder of Bear Creek Mining, we look forward to participating in the success of Mercedes and future development of Bear Creek Mining’s Corani silver-lead-zinc deposit, one of the largest, fully-permitted silver deposits in the world.”

Mexican Mining Industry A Mixed Bag of Uncertainty

Mexico is seen as a favourable jurisdiction for mining, with a long history of both large and small-scale mining operations. The country is the world’s largest producer of silver and gold and is also a major producer of copper, zinc, lead and other minerals.

However, recent events resulted in the Mexican government’s nationalization of lithium, meaning that companies can no longer mine the metal without a government concession, and production will be owned exclusively by the state.

This has led to some uncertainty in the Mexican mining industry, with a number of companies put off by the new rules. It also throws into question the future of lithium mining in the country and whether the government might aim to nationalize other resources as it has oil at the beginning of the prior century. Nevertheless, the country still presents a number of opportunities for miners, especially given its rich mineral resources.

Gold mining in particular has a long history in Mexico, with some of the first mines dating back to the 16th century. The country is thought to have the world’s second-largest gold reserves, after Russia. In 2019, Mexican gold production reached a record high.

The vast majority of Mexico’s gold is produced by large-scale mines, with just a small number of artisanal and small-scale miners operating in the country. Many of Mexico’s gold mines are located in the northwestern state of Sonora, which is also home to the Mercedes mine.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Elon Musk has made public appeals to boost mining in the past, most notably for nickel. Most recently, the Tesla (NASDAQ:TSLA) boss made it clear that he is looking for more lithium for electric vehicles (EVs). One of the problems the company faces right now, is that very few places can supply lithium consistently right now.

Tesla CEO Elon Musk has repeatedly said that the company would begin mining lithium following years of comments indicating it would do so. He first stated this nearly two years ago although steps have not yet been taken.

While demand for the commodity is set to rise in the coming years, the necessity to have a steady supply of it has become all the more pressing. Major producers such as Albemarle Corp. (NYSE:ALB) are increasing capacity and launching new projects, but growth in supply is still insufficient owing to a lack of investment following the lithium boom-bust from 2017 to 2019.

For the present, lithium production is concentrated in a few nations, with Chile and Australia accounting for 81% of global output. Few suppliers imply greater uncertainty about delivery, and often price volatility.

Recent Price Moves

In April, rising lithium carbonate and hydroxide prices in China slowed their rise, according to Benchmark Mineral Intelligence, but for chemical processors and battery manufacturers trying to keep up with price increases so far in 2022, the lull is unlikely to last. The first half of April has seen lithium hydroxide prices (the kind used in batteries with nickel cathodes) rise further though. This is the particular kind of lithium that Tesla requires for its vehicles.

A Dry Spell and Price Slump

For some time, there was a price slump for lithium as the market was still deciding what the demand might be from the coming changes in the auto and energy industries. Now that it is clear that the direction toward clean energies is certain, prices have been more bullish.

At the time of the pause, a lot of lithium capacity was being built, driven by the electric vehicle craze when Tesla and non-hybrid vehicles arrived five years ago. Now, prices have caught up to the reality of the demand and expected demand growth in the coming decade.

There is an industry of startups and junior miners attempting to tackle the challenge of developing new lithium projects. However, the process of going from exploration to production takes several years, which has contributed to today’s undersupply. None have been able to achieve commercial scale yet either. For now, Tesla has relied on and will continue to rely on traditional lithium mining countries like Australia and Chile.

Mexico Nationalizes Its Lithium Industry

In other lithium news, the Mexican government has nationalized the country’s lithium industry after the Senate passed a mining reform bill proposed by President Andres Manuel Lopez Obrador. The president now has 90 days to establish a new, decentralized organization to deal with all aspects of lithium in the country.

The president declared that his administration will conduct an audit of all lithium contracts, casting a cloud over projects already in development, and all but assuring a lack of new projects in the near future. The law may also likely deter foreign investment not just for lithium mining but for other mining as investors weigh the risks of the populist government proposing similar changes to other areas of the industry.

The law, according to reports, would violate the United States-Mexico-Canada Agreement (USMCA) and jeopardize trade frictions with Mexico’s northern neighbours. Most of the world’s current lithium production is stashed away in long-term deals because downstream chemicals producers, battery manufacturers, and electric vehicle makers are all trying to lock down future supply. While the law will change the industry within Mexico, it may not change much for the lithium mining industry globally.

According to data from the US Geological Survey, Mexico’s lithium reserves place it in just 10th place among the world’s top producers.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Ivanhoe Mines (TSX:IVN), a Canada-based mining company, reported from its Kamoa copper mine in the Democratic Republic of Congo (DRC) that it had achieved record production numbers in Q1 2022 at the Kamoa copper mine. The mine recorded production o f55,602 tonnes of copper, which the company attributed the increase in production to improved mining operations and higher grades.

Mark Farren, Kamoa Copper’s CEO, commented in a press release: “The Phase 2 concentrator has been successfully commissioned in record time. We can expect to see a doubling of copper output for the remainder of this year, as well as further increases into 2023 as the de-bottlenecking program is executed. It has been wonderful to see how quickly Phase 2 reached commercial production, as our team leveraged prior learnings and experience from Phase 1.”

In May 2021, the Kamoa-Kakula project began producing copper concentrates, and commercial production began on July 1st, 2021. Kamoa-Kakula is well positioned to be one of the world’s major copper producers through planned phased expansions.

On April 7, 2022, the Kamoa-Kakula Phase 2, a 3.8 million tonne per day concentrator facility, achieved commercial production. Kamoa-Kakula also established a new daily production record on April 8 with 25,126 tonnes milled and 1,202 metric tons of copper produced.

Considering that copper is one of the battery metals playing a key role in the green energy transition, Ivanhoe’s goal of producing the industry’s “greenest” copper is key.

Ivanhoe is working to be the first net-zero carbon emitter in the world’s top copper producers’ ranks. Kamoa-Kakula will be powered by clean, renewable hydroelectric energy and is expected to have one of the lowest global greenhouse gas outputs per unit of metal produced.

Kamoa-Kakula

The Kamoa-Kakula copper deposit is a collaboration between Ivanhoe Mines (39.6%), Zijin Mining Group (39.6%), Crystal River Global Limited (0.8%), and the Government of the Democratic Republic of Congo (20%). According to international mining consultant Wood Mackenzie, it has been independently ranked as the world’s largest undiscovered high-grade copper discovery.

Higher Production

The higher production numbers come at a time when the industry is clamoring for more copper. The pandemic-fueled surge in demand for copper has caused a global shortage of the metal, leading to higher prices.

In 2021, the price of copper reached an all-time high of $10,000 per tonne on the London Metal Exchange. The rally was attributed to a combination of strong Chinese demand, constrained supply, and a weaker US dollar.

Copper is an essential metal for industries such as electric vehicles, renewable energy, and 5G technology. The global pandemic has caused a surge in demand for these products and has led to a shortage of copper. A shortage of new projects coming online on time to meet the demand has also pushed prices higher amid a general commodities supercycle.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

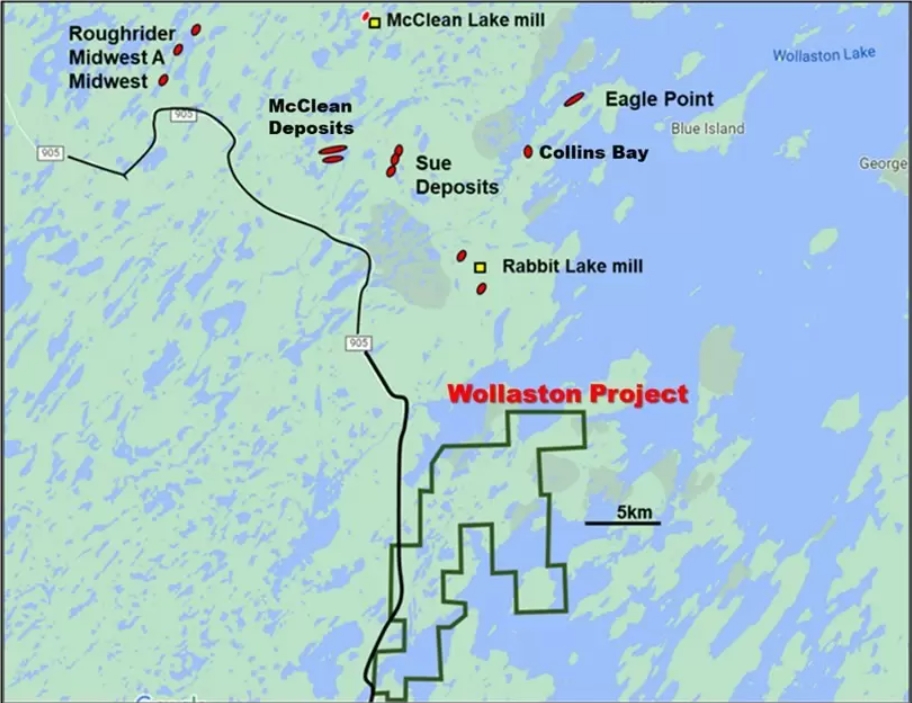

Forum Energy Metals (TSXV:FMC) has announced that drilling has been completed at eight holes for a total of 2,062 metres at the Wollaston uranium Project. The 100%-owned project is located 10 kilometres southeast of the Cameco Rabbit Lake mill, plus 30 kilometres southeast of the Orano/Denison McClean Lake mill.

Ken Wheatley, Vice President of Exploration at Forum Energy Metals commented in a press release: “This is a tremendous start on this project in an area of the Athabasca Basin that is prolific with several uranium deposits in close proximity to two uranium mills. To intersect uranium mineralization in an area of very strong alteration in the first pass drill program confirms that this property has much potential for a near surface, basement hosted unconformity deposit with rich grades of uranium.”

Forum has uranium, copper, nickel, and cobalt projects located in Saskatchewan, Canada. It also holds a uranium land position in the northern province of Nunavut as well as a strategic cobalt land position in the Idaho Cobalt Belt, United States. Forum is currently exploring its multiple properties with a focus on the Wollaston uranium project in Saskatchewan.

Figure 1: Location of Forum’s Wollaston Uranium Project.

Highlights from drilling are as follows:

- Anomalous radioactivity in four holes on one of three targets drilled.

- Weak uranium mineralization was seen in core with associated bleaching, secondary hematite and minor uranium oxides in 4 holes.

- Follow-up drilling and further gravity surveys strongly recommended.

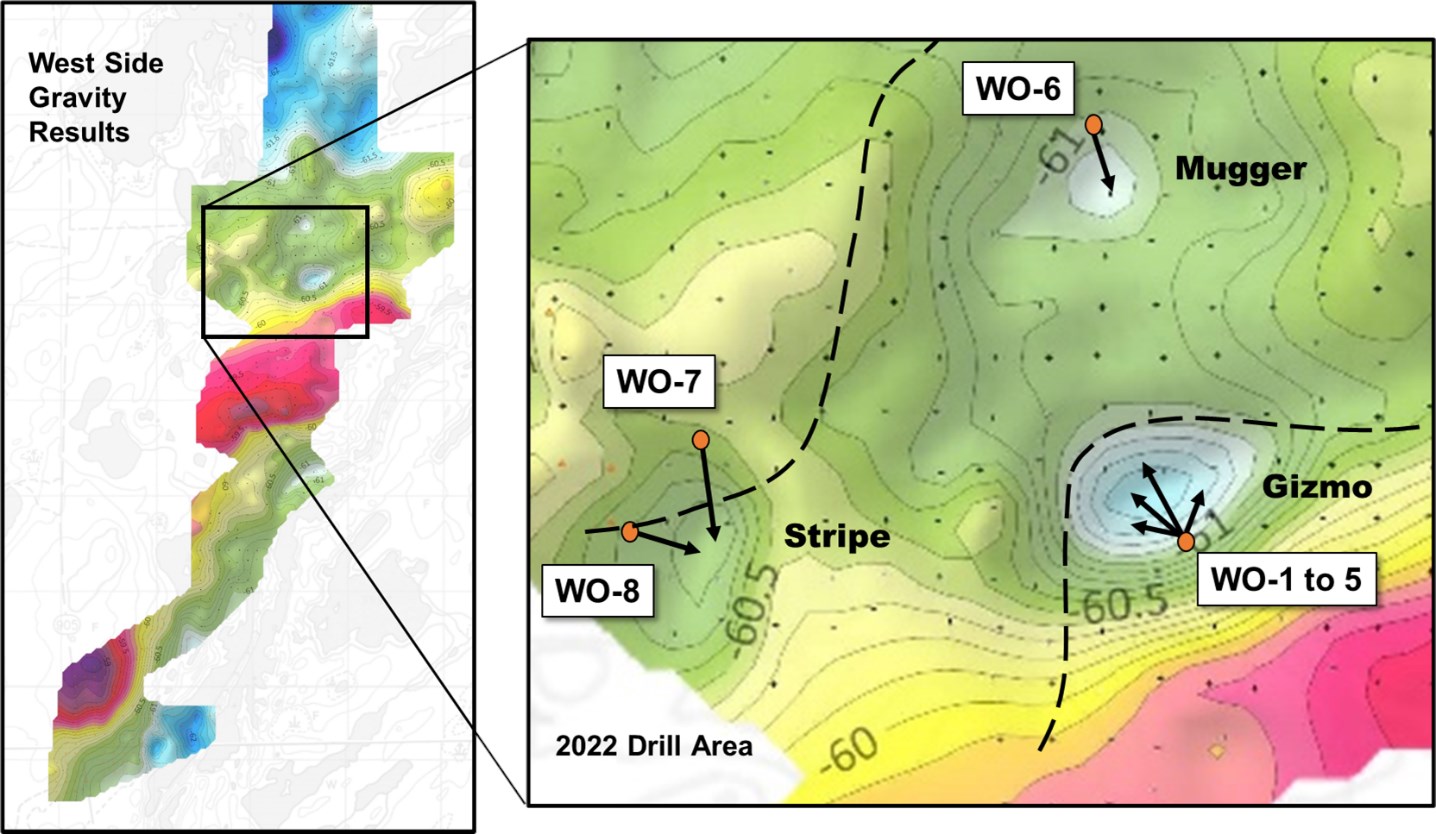

First Target – Gizmo

The drill program tested 3 zones of gravity lows, two of them in combination with EM conductors. The first gravity low (Gizmo) measuring 300 metres long and 200 metres wide was tested by 5 holes and returned very strong alteration of the rocks immediately beneath the overburden at 40m and continuing to about 150m depth (Figure 2). Weak uranium mineralization was seen in core with associated bleaching, secondary hematite and minor uranium oxides in several of the holes (Figure 3). A downhole radiometric probe* detected anomalous radioactivity in 4 out of the 5 holes:

- 1,540 counts per second (cps) at 187.8 metres (m) in DDH WO-1

- 1,752 cps at 128.1m in DDH WO-2

- 4,620 cps at 161.2m in DDH WO-2

- 2,002 cps at 105.3m in DDH WO-3

- 3,320 cps at 111.2m in DDH WO-4

* a Mount Sopris down-hole logging system (5MXA-1000 matrix, 4MXA-1000 winch and 2PGA-1000 gamma probe) was used for the radiometric probing.

Further drilling is recommended on this target in areas that could not be reached this winter, testing an EM conductor that crosses the northwest part of the gravity low (see Figure 2).

Second and Third Targets – Mugger and Stripe

The sixth hole tested a weak gravity anomaly (Mugger) that returned relatively fresh calc-silicates and has been eliminated. The final two holes tested a third gravity anomaly (Stripe), also with an associated EM conductor that intersected a series of faulted units with associated gouges and local alteration. These holes have been heavily sampled and sent for assay.

Future Plans

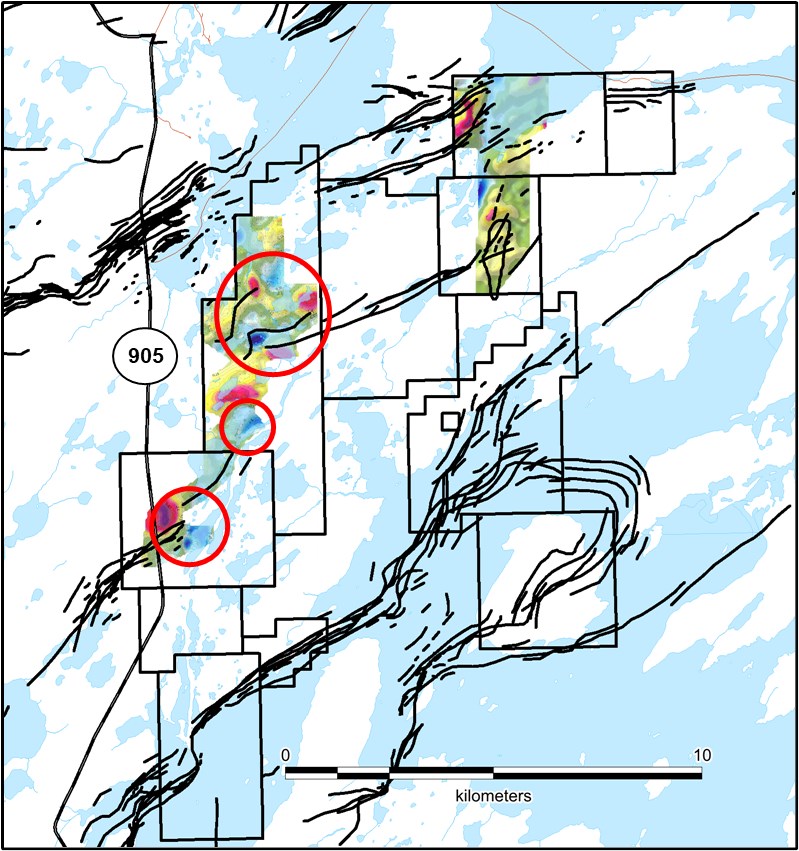

Forum sent 393 samples of the drill core to the Saskatchewan Research Council for geochemical analysis and results are expected in a month. The Company is reviewing its plans for further exploration of the property, including drilling of the Gizmo target. Figure 4 illustrates areas that have had gravity surveys completed this past year. Excellent targets remain on the west side close to the highway, which will be investigated first before moving to the eastern targets. Further airborne and ground geophysical surveys are being considered to fully test the regional potential of the property.

Figure 2: Drill Hole Locations on Gravity Background.

Figure 3: Uranium mineralization on core returned from WO-2 and WO-4

Figure 4: Gravity surveys completed over structural zones and EM conductors

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

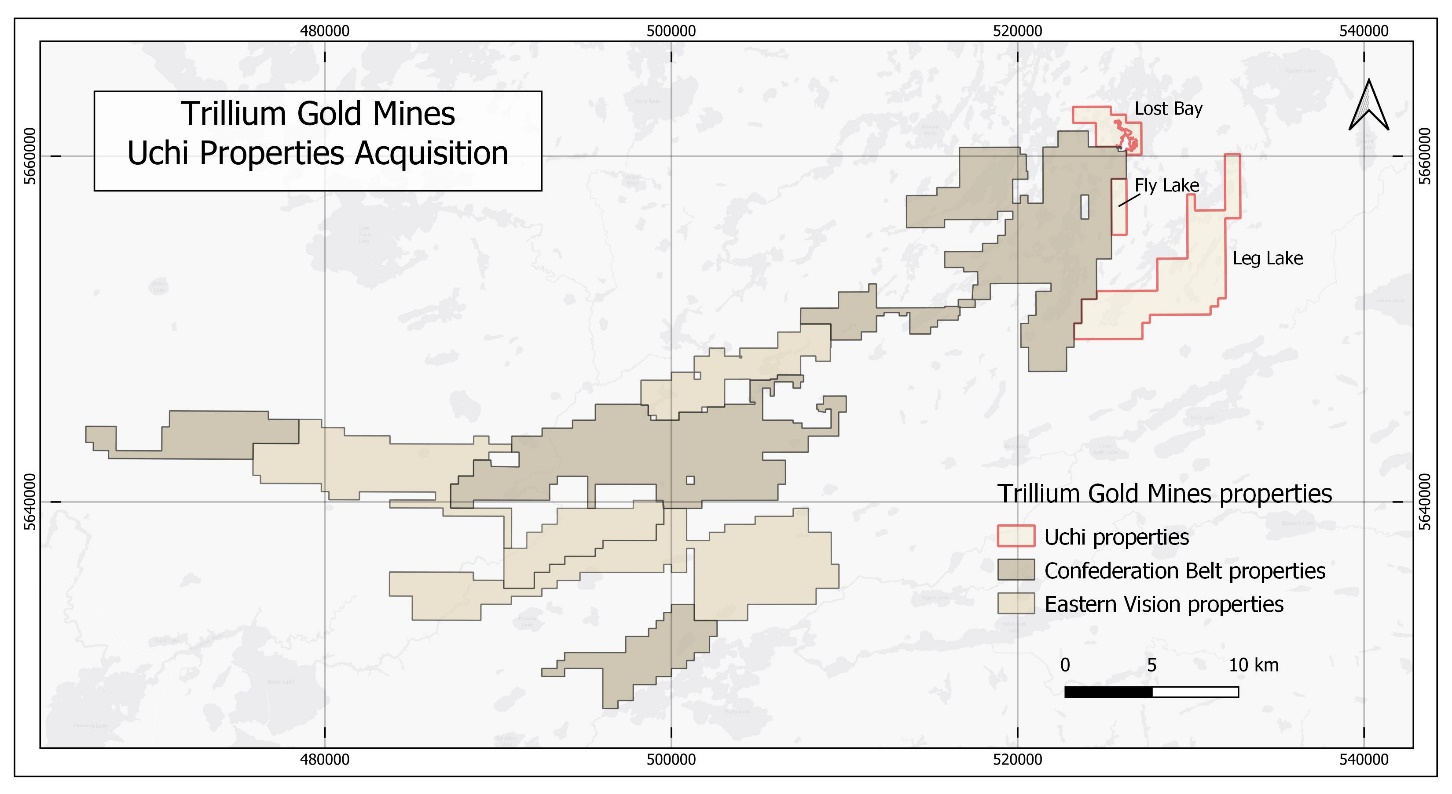

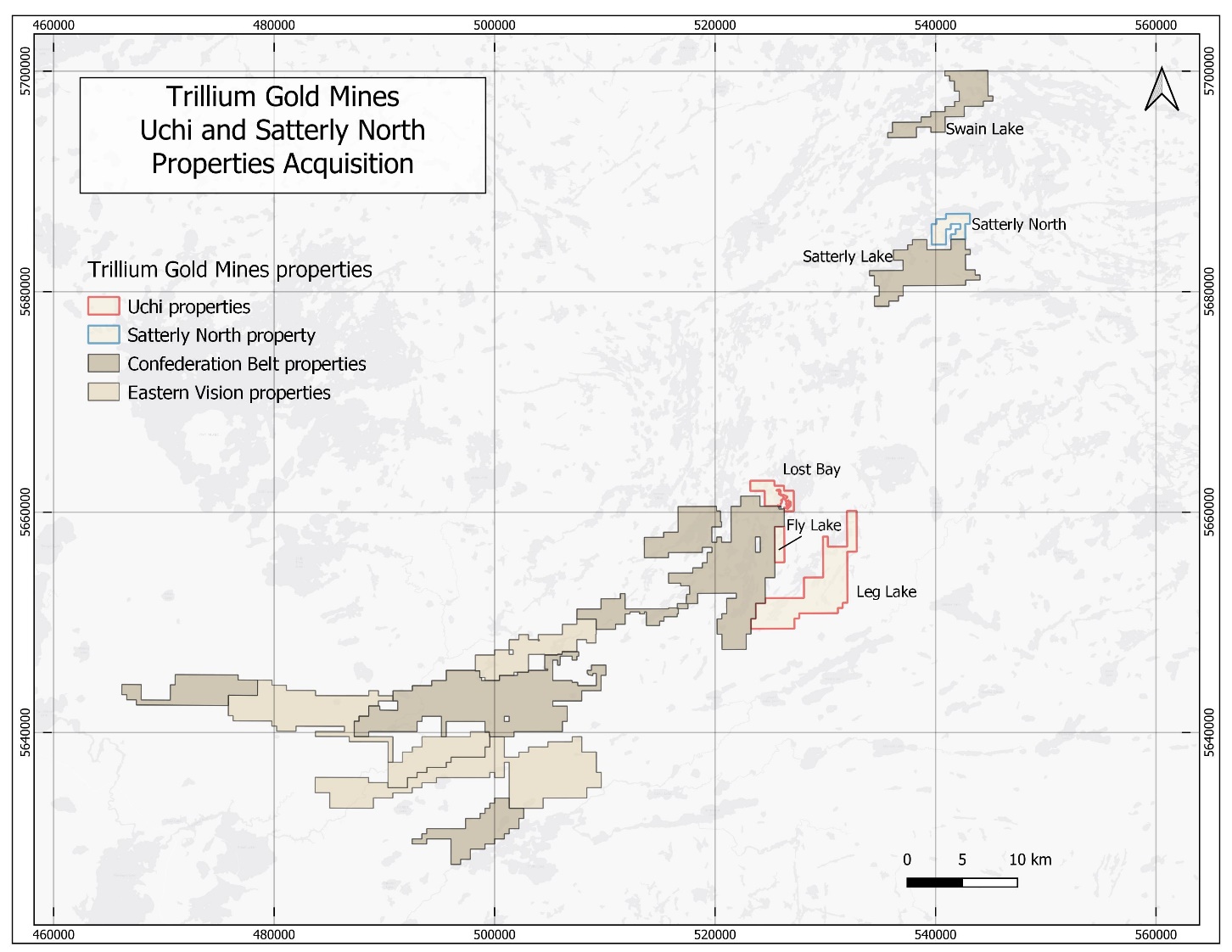

Trillium Gold Mines Inc. (TSXV:TGM) (OTCQX:TGLDF) announced that it has entered into two purchase option agreements for the Uchi Gold Project and Satterly Gold Project, to acquire a 100% undivided interest in each area within the Confederation greenstone belt. The agreements further Trillium Gold’s strategic objective to consolidate the Confederation belt and Birch-Uchi greenstone belt, positioning it as the dominant exploration company in the Red Lake Mining District.

Uchi Gold

Figure 1: Uchi Gold Option Properties

The Uchi Gold Agreement covers 4,189 hectares of unpatented mining claims immediately adjacent to and adjoining the Company’s Confederation belt properties which already stretch over 100km of favourable structure on trend with Kinross Gold’s Dixie deposit.

The Uchi Gold agreement brings a whole other set of favourable mining claims into the company’s portfolio. Properties include the contiguous and complementary Lost Bay, Fly East, and Leg Lake mining claims. By adding these properties, Trillium extends its Confederation belt property assemblage to the northeast towards its Satterly Lake property. Most notably, the deal boosts Trillium Gold’s foothold in a contiguous land position along the same structural trend that has attracted major mining companies.

Vast, Untapped Potential

The new properties also hold a vast amount of untapped potential, considering how underexplored they are. The Fly East and Leg Lake properties have previously seen limited reconnaissance type exploration, with the majority of exploration having focused on base metals in the 1970s and 1980s. Only eight drill holes were conducted over the properties during that time period.

Then in the early 2000s, platinum group mineralization was targeted, with results of up to 1g/t PGMs and 1.8% copper. At Fly East, some minor gold exploration took place but only indirectly. Considering that both of these properties contain favourable structures and lithologies for both gold and base metals, Trillium Gold has snapped up a strategic package that could be more prospective than envisioned.

To top it off, as part of the Uchi agreement, the company gains the Lost Bay property. This is particularly significant being located close to the historic Bobjo Mine, which in 1929 produced 362 ounces of gold.

The Lost Bay property contains felsic and mafic volcanic rocks with gold mineralization that appears to follow a preferred west-northwest orientation. In the mid-1930s some gold and base metal exploration was performed, targeting South Bay Mine analogues, but these structures were not deemed to be important in the base metal context. Today Trillium Gold has the opportunity to unlock the potential of these structures prospective for gold, base metals (copper/zinc) and PGMs.

Satterly Gold

Figure 2: Uchi and Satterly Gold Option Properties

The Satterly Gold Agreement consists of 5 unpatented mining claims covering 565 hectares adjoining the company’s existing Satterly Lake properties located to the northeast of the Confederation belt land package.

Like the other properties, this area has seen sporadic exploration in the 1930s, recommencing gold exploration in the 1990s, and then again in 2009.

The region is underlain by a variety of rock types, including mafic volcanics and intrusives, sediments, and lamprophyre dykes. In the northeast corner of the property, Cominco carried out a local basal till sampling program, which revealed several anomalous results.

These aforenoted purchase option agreements have effectively furthered Trillium Gold’s regional-scale consolidation strategy which has resulted in a dominant land position in the Confederation and Birch-Uchi belts. The potential of the combined property is vast, and the company is ideally positioned to explore and unlock that potential in 2022 and beyond.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

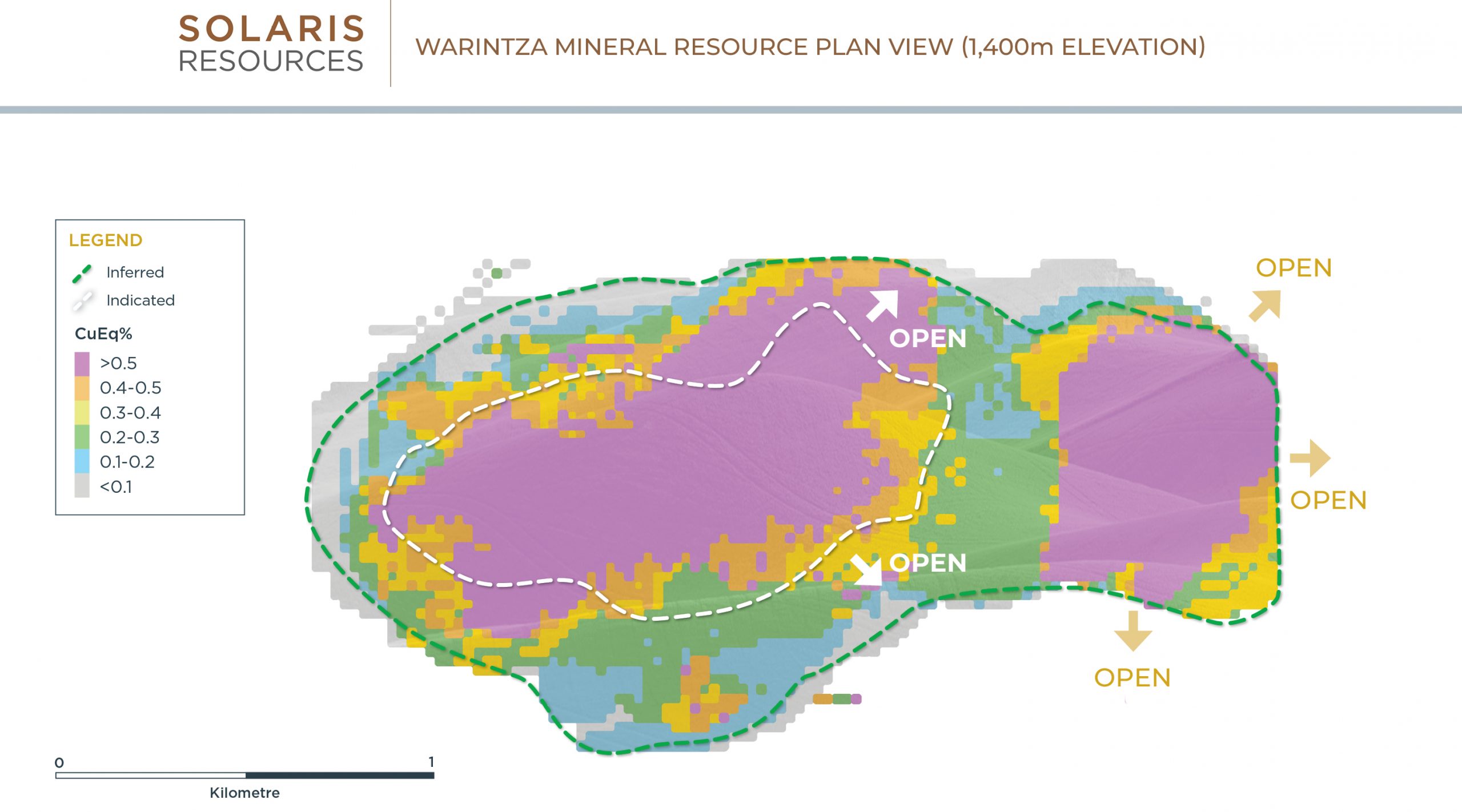

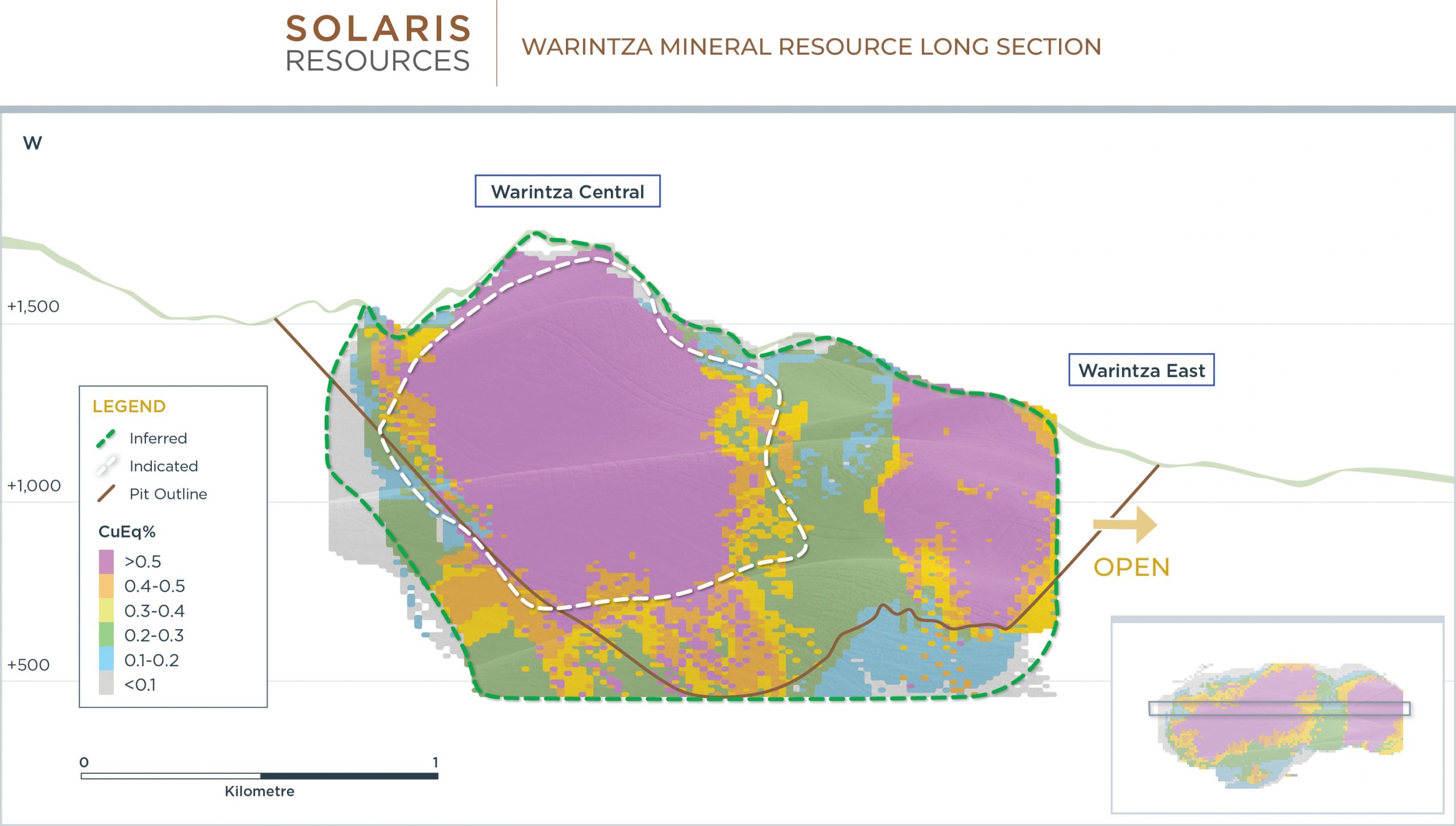

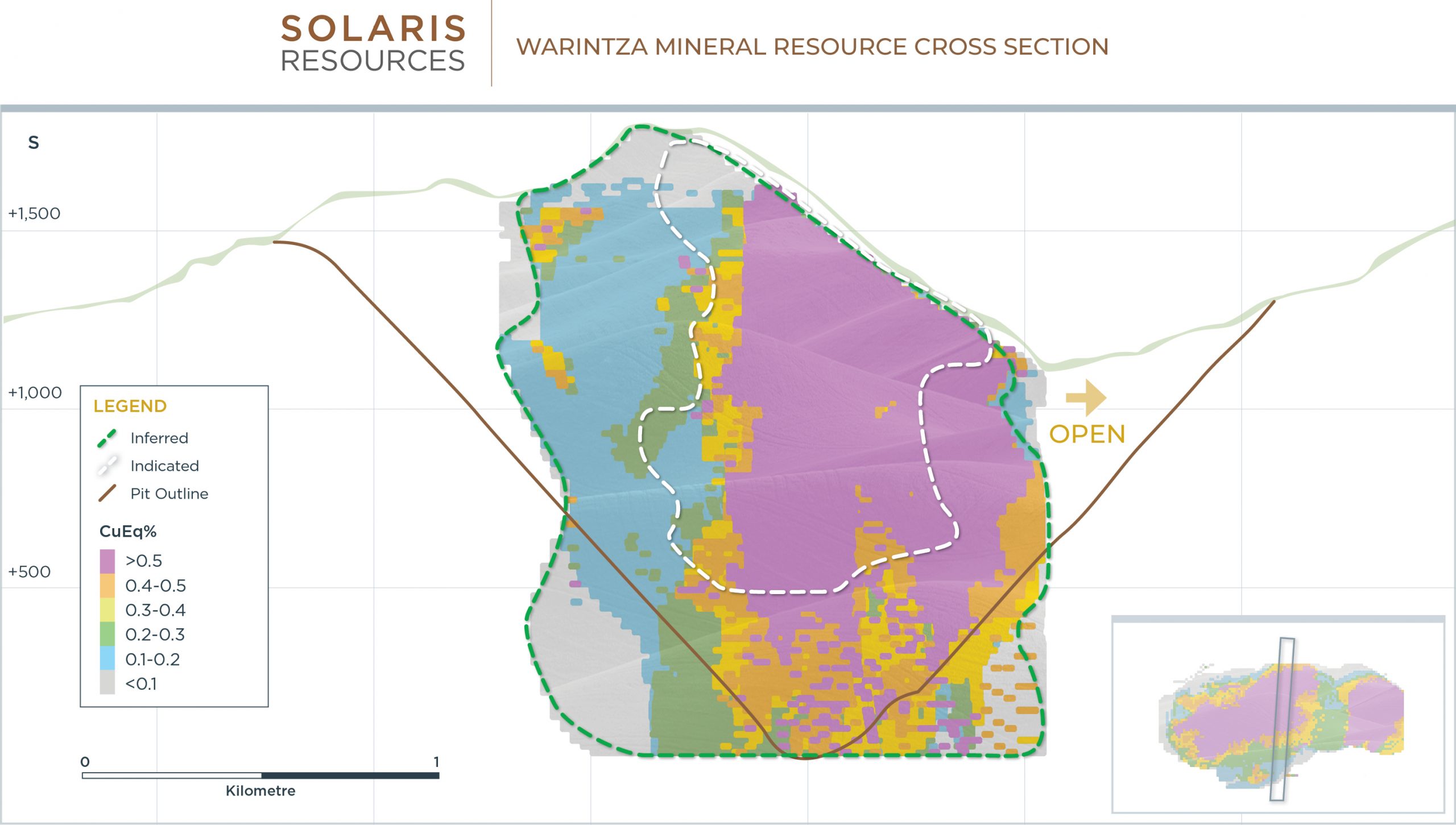

Solaris Resources (TSX:SLS) (OTC:SLSSF) has announced a highly-anticipated mineral resource update to Warintza Central at the Warintza Project in Ecuador. The company reported in-pit resources of 579 Mt at 0.59% CuEq (Ind) & 887 Mt at 0.47% CuEq (Inf). This also includes an ‘indicative starter pit’ of 180 Mt at 0.82% CuEq (Ind) & 107 Mt at 0.73% CuEq (Inf). Additionally, the company is now targeting high-grade extensions and major growth in cluster.

Daniel Earle, President & CEO of Solaris Resources, commented in a press release: “After only eighteen months of drilling, primarily in Warintza Central, one of the four major discoveries made on the property to date, the MRE establishes baseline credentials for the Project of hosting a robust inventory, featuring a high-grade indicative starter pit and low strip ratio, within a mining district offering major structural advantages from highway access, abundant and low-cost hydroelectric power, fresh water, labour and low elevation. Ongoing drilling is targeting further rapid growth, with an emphasis on the open extensions of near surface, high-grade mineralization at Warintza Central and expanding our recent Warintza East discovery to include it within a shared pit, while testing the further potential within the cluster.”

Highlights from the mineral resource update are as follows:

Highlights

- In-Pit Indicated mineral resources of 579 million tonnes (“Mt”) at 0.59% copper equivalent¹ (“CuEq”) and Inferred mineral resources of 887 Mt at 0.47% CuEq¹ above a 0.3% CuEq cut-off grade

- Includes ‘Indicative Starter Pit’ comprised of Indicated mineral resources of 180 Mt at 0.82% CuEq² and Inferred mineral resources of 107 Mt at 0.73% CuEq² above 0.6% CuEq cut-off grade

- High Quality – Expected low strip ratio ‘Indicative Starter Pit’ and ultimate pit, zoned from high-grade at surface to low grade at depth, consistent, clean sulphide mineralogy free of deleterious elements

- High-Grade Growth – Ongoing drilling focused on open extensions of near surface, high-grade mineralization to the northeast and southeast of Warintza Central

- ‘Super Pit’ Growth – Warintza Central pit shell includes overlapping portion of Warintza East, discovered mid-2021, a target wide open for major growth potential within a shared pit

- Cluster Potential – Warintza Central forms part of a 7km x 5km cluster of porphyry deposits, where in addition to East, recent discoveries at West and South offer major growth potential

- Structural Advantages – Set within mining district featuring access to highway, abundant and low-cost hydroelectric power, fresh water, labour and low elevation

Table 1: Warintza Mineral Resource Estimate Summary and Cut-Off Grade Sensitivity

| Cut-off | Category | Tonnage | Grade | Contained Metal | |||||||

| CuEq (%) |

(Mt) | CuEq (%) |

Cu (%) |

Mo (%) |

Au (g/t) |

CuEq (Mt) |

Cu (Mt) |

Mo (Mt) |

Au (Moz) |

||

| 0.2 | % | Indicated | 736 | 0.52 | 0.40 | 0.02 | 0.05 | 3.84 | 2.95 | 0.18 | 1.11 |

| Inferred | 1,558 | 0.37 | 0.31 | 0.01 | 0.03 | 5.80 | 4.80 | 0.19 | 1.63 | ||

| 0.3% (Base) | Indicated | 579 | 0.59 | 0.47 | 0.03 | 0.05 | 3.45 | 2.70 | 0.15 | 0.93 | |

| Inferred | 887 | 0.47 | 0.39 | 0.01 | 0.04 | 4.17 | 3.48 | 0.13 | 1.08 | ||

| 0.4 | % | Indicated | 442 | 0.67 | 0.54 | 0.03 | 0.05 | 2.97 | 2.38 | 0.12 | 0.77 |

| Inferred | 539 | 0.55 | 0.47 | 0.01 | 0.04 | 2.96 | 2.53 | 0.08 | 0.71 | ||

| ‘Indicative Starter Pit’ | |||||||||||

| 0.6 | % | Indicated | 180 | 0.82 | 0.67 | 0.03 | 0.07 | 1.49 | 1.20 | 0.06 | 0.38 |

| Inferred | 107 | 0.73 | 0.64 | 0.02 | 0.05 | 0.79 | 0.69 | 0.02 | 0.17 | ||

Notes to Table 1:

- The mineral resource estimates are reported in accordance with the CIM Definition Standards for Mineral Resources & Mineral Reserves, adopted by CIM Council May 10, 2014.

- Reasonable prospects for eventual economic extraction assume open-pit mining with conventional flotation processing and were tested using NPV Scheduler™ pit optimization software with the following assumptions: metal prices of US$3.50/lb Cu, US$15.00/lb Mo, and US$1,500/oz Au; operating costs of US$1.50/t + US$0.02/t per bench for mining, US$4.50/t milling, US$0.90/t G&A; recoveries of 90% Cu, 85% Mo, and 70% Au.

- Resource includes grade capping and internal dilution. Grade was interpolated by ordinary kriging populating a block model with block dimensions of 25m x 25m x 15m.

- The ‘Indicative Starter Pit’ is based on the same assumptions as the Resource except utilized metal prices of US$1.00/lb Cu, US$7.50/lb Mo, and US$750/oz Au. No economic analysis has been completed by the Company and there is no guarantee than an ‘Indicative Starter Pit’ will be realized or prove to be economic.

- Mineral resources that are not mineral reserves do not have demonstrated economic viability.

- Copper equivalent assumes recoveries of 90% Cu, 85% Mo, and 70% Au based on preliminary metallurgical testwork, and metal prices of US$3.50/lb Cu, US$15.00/lb Mo, and US$1,500/oz Au. CuEq formula: CuEq (%) = Cu (%) + 4.0476 × Mo (%) + 0.487 × Au (g/t).

- The Qualified Person is Mario E. Rossi, FAusIMM,RM-SME, Principal Geostatistician of Geosystems International Inc.

- All figures are rounded to reflect the relative accuracy of the estimate.

- The effective date of the mineral resource estimate is April 1, 2022.

The corresponding Technical Report disclosing the MRE in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) will be prepared by Mr. Rossi and available on SEDAR under the Company’s profile at www.sedar.com within 45 days of this news release.

- Copper equivalent assumes recoveries of 90% Cu, 85% Mo, and 70% Au based on preliminary metallurgical testwork, and metal prices of US$3.50/lb Cu, US$15.00/lb Mo, and US$1,500/oz Au. CuEq formula: CuEq (%) = Cu (%) + 4.0476 × Mo (%) + 0.487 × Au (g/t).

- The Company anticipates that a near surface, high grade portion of the Resource may form the basis of an ‘Indicative Starter Pit’ once an economic analysis of the Project is complete. No economic analysis has been completed by the Company and there is no guarantee an ‘Indicative Starter Pit’ will be realized or prove to be economic. The ‘Indicative Starter Pit’ is based on the same assumptions as the Resource except utilized metal prices of US$1.00/lb Cu, US$7.50/lb Mo, and US$750/oz Au.

Resource Estimation Methodology and Parameters

Indicated mineral resources were defined where the nominal drill hole spacing is 120m. The classification reflects not only the drill spacing, but the confidence level in the continuity of the grade and the geometry of the deposit. Inferred mineral resources were defined by blocks which were estimated with less stringent requirements within search ellipses defined for each domain to a maximum distance of 350m. Resources include grade capping and internal dilution. Grade was interpolated by ordinary kriging populating a block model with block dimensions of 25m x 25m x 15m. The Indicated and Inferred mineral resources are classified in a manner that is consistent with the May 10, 2014 CIM Definition Standards for Mineral Resources and Mineral Reserves. Mineral resources that are not mineral reserves do not have demonstrated economic viability. In Mr. Rossi’s opinion, there are currently no relevant factors or legal, political, environmental, or other risks that could materially affect the potential development of the mineral resources.

Source: Solaris Resources

Figure 1 – Warintza Mineral Resource Plan View (1,400m Elevation)

Figure 2 – Warintza Mineral Resource Long Section

Figure 3 – Warintza Mineral Resource Cross Section

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Barrick Gold (TSX:ABX) (NYSE:GOLD) has revealed plans to develop the Reko Diq copper-gold deposit in Balochistan, Pakistan, in two stages. The first stage will be an almost 40Mtpa plant. The company will look to double the capacity of the plant in the next five years.

If everything goes as planned, Barrick Gold predicts that the mine’s first output will arrive within five to six years. The two-phase construction of the mine is said to optimize profits, reduce execution risks, manage upfront capital, and provide cash flows in the long run for the miner.

The development is expected to result in 7,500 employment opportunities during the peak construction period and over 4,000 long-term positions after it begins operating. Furthermore, Barrick was considering solar, wind, and battery systems to boost the renewable power generation at the operation.

Barrick Gold has a 50 percent stake in the project and will act as the operator. The remaining share is owned by Pakistani state-owned companies which have 25%, and the Balochistan government which holds a 25% stake.

Barrick CEO Mark Bristow said on an investor call: “Offering a unique combination of large scale, low strip and good grade, Reko Diq will be a multi-generational mine, with a life of at least 40 years. The contemplated mine plan is based on four porphyry deposits within our land package and our exploration licence area holds additional deposits with future upside potential.”

The project was put on hold in 2011 owing to a long-running dispute with Pakistan over the licensing procedure the jobs. However, Barrick Gold agreed to resume work on the project and get the mine back on track after reaching an out-of-court settlement, under which the previous $11 billion penalty against Pakistan was forgiven.

Bristow continued: “At Barrick, we know that our long-term success depends on sharing the benefits we create equitably with our host governments and communities. That’s why we wanted Balochistan’s share of the venture to be fully funded, 10% by the project and 15% by the Government of Pakistan.

2022 Inflationary Headwinds

Barrick Gold Corp. has far outpaced the rest of the bullion industry in surviving a soaring costs dilemma in 2021 and 2022, but it is now facing inflationary headwinds for the first time.

Barrick announced a preliminary statement Thursday, in which it said gold production for the first quarter was lower than the previous quarter, according to its earlier forecast. At the same time, all-in sustaining costs per ounce are anticipated to be 19-21% greater than in the fourth quarter. Apart from a 20% decrease in gold ounces produced and sold, the company didn’t provide further guidance.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The nickel shortage and growing demand is pushing miners to expand exploration and production. This also comes on the heels of companies like Tesla (NASDAQ:TSLA), that have announced plans to source more nickel for their electric vehicle batteries from environmentally sound projects.

Talon Metals (TSX:TLO) is one of the latest miners to announce expansion plans at their Minnesota-based nickel project. Tesla is a client of Talon’s and the Tamarack nickel-copper-cobalt project is one of the company’s major projects, of which is holds a 51% interest. Rio Tinto (ASX:RIO) holds the remaining 49%.

The Tamarack North and South projects are located in an 18-kilometer stretch of strike length with a significant land position (18 kilometers of strike length) and numerous high-grade intercepts outside the current resource area. The new rigs will be utilized outside of the main resource zone. If Talon chooses, it has an earn-in option to increase its interest to 60%.

The goal is for the firm to make staggered payments worth $22.5 million in cash and shares to partner Rio Tinto, invest $10 million in exploration and development, and complete a feasibility study in order to reach it.

The Supply Race is On

Rising demand from EV companies is driving automakers to secure steady supply of battery metals which include nickel, cobalt, and lithium. While most of the world’s nickel is used in stainless steel production, an increasing amount is being gobbled up by the battery sector as the production of EVs ramps up.

The market for electric vehicles is expected to grow rapidly in coming years, alongside the demand for these metals.

Nickel is beneficial to the development of lithium-ion batteries, which are increasingly being used in automobiles. It allows EVs to charge faster and farther between plug-ins by increasing the energy density of battery packs.

The price of nickel has increased to previously unseen heights in recent months, not surprisingly. In March, the price rose by an unprecedented 250 percent in a day, forcing the London Metal Exchange (LME) to halt trading in the metal.

EV Giants Scramble

Tesla CEO Elon Musk has noted that nickel supply is one of the company’s top concerns because of the amount used in each battery pack. The company is also eying a move into more direct control of raw materials, which would give it more control over its supply chain.

For now, however, miners are benefiting from the electric vehicle boom as they race to increase exploration and production. Talon Metals is just one of the many firms looking to take advantage of the perfect climate for them.

The sanctions against Russia resulting from the invasion of Ukraine have further heightened the need for nickel, which it holds about 17% of global capacity for refined Class 1 nickel, the type used for EVs.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

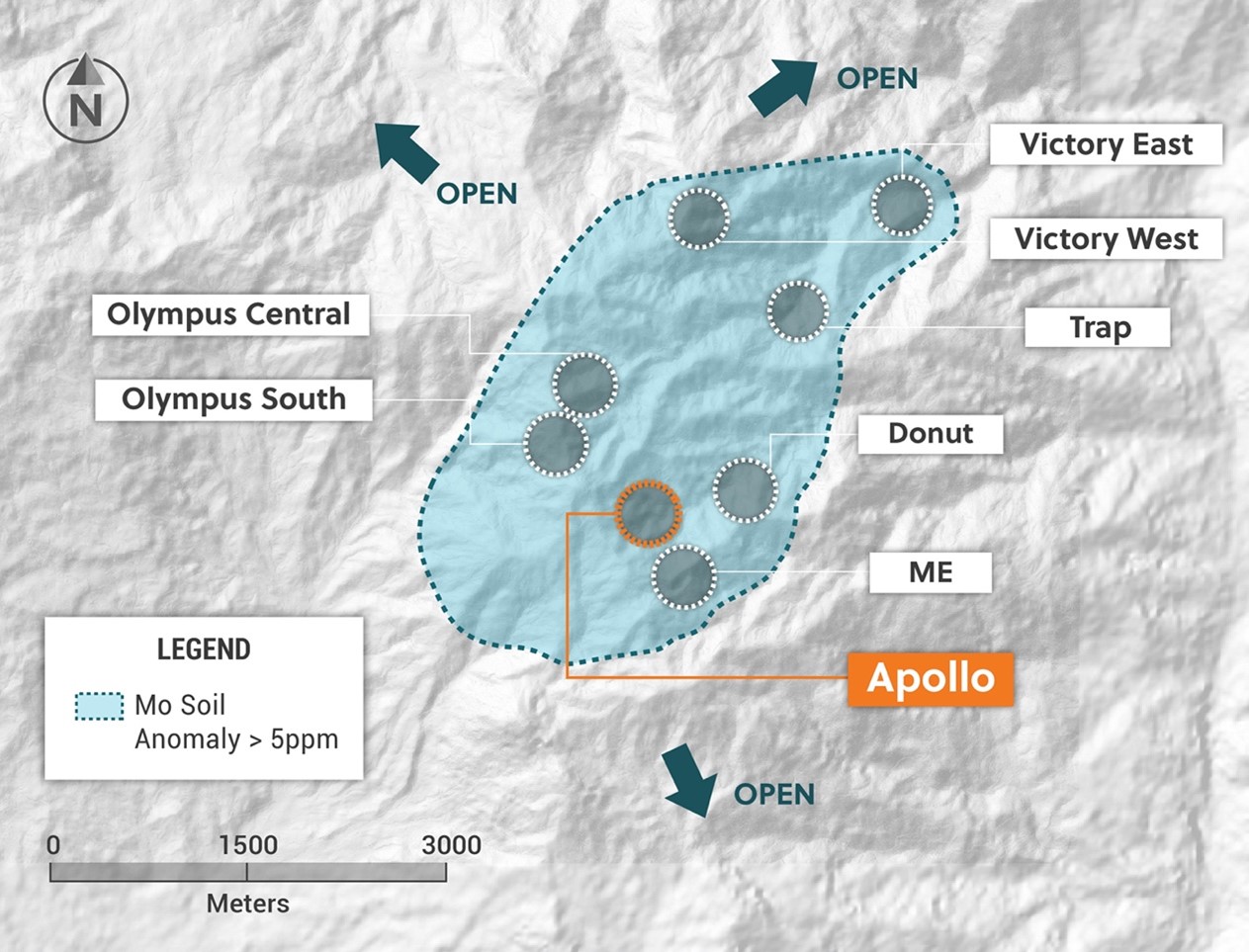

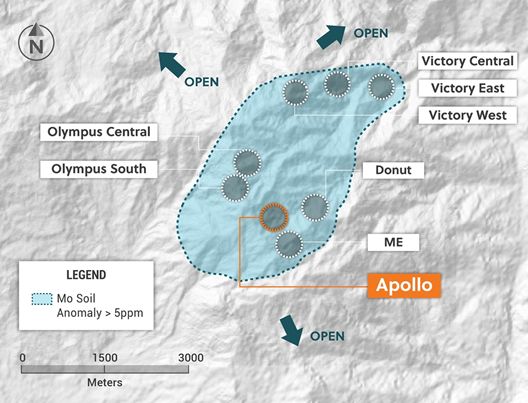

Collective Mining (TSXV:CNL) has announced this morning that it has begun drilling at its maiden drill at the Apollo target. Collective recently announced an Olympus Central discovery hole of 302 metres @ 1.11 g/t gold equivalent, and has drills operating at the Apollo and Olympus Central targets. These are part of the four diamond drill rigs currently operating at Guayabales. These two targets are located approximately 600 metres apart, with the Apollo target sitting to the southeast of Olympus Central.

Ari Sussman, Executive Chairman, Collective Mining, commented: “Our shotgun approach for 2022 of testing multiple targets at the Guayabales project with reconnaissance drilling has provided us with spectacular returns. The latest potential discovery at Apollo is currently at 70 metres in down hole length and remains in strongly mineralized breccia as the hole continues to advance. We now plan to accelerate exploration at Apollo and look forward to receiving assay results from this intercept in the coming weeks.”

Figure 1: Plan View of the Guayabales Project Highlighting the Apollo Target

Highlight from the news are as follows:

A maiden diamond drill program at Apollo recently began with the initial 500-metre-long hole (APC-1) well underway. Beginning at 280 metres down hole, the Company has intersected a porphyry related, hydrothermal breccia with the matrix consisting of approximately 5% pyrite and 1.5% chalcopyrite (according to core logging). The pyrite has potential to contain gold and chalcopyrite is sulphide mineral containing copper and iron. Additionally, a late overprint of carbonate base metal (“CBM”) veins is present in places and as a result and based on previous similar intercepts, could introduce additional gold and silver into the system.

- Drill hole APC-1 is currently at 350 metres in length and continues to intersect strongly mineralized breccia (70 metres total thus far). Assay results for this hole are expected over the coming weeks.

- Surface mapping, soil and rock sampling at Apollo has outlined a target area measuring at least 750 metres x 580 metres open to the east, west and south.

- The main target at Apollo is a porphyry system with a porphyry related breccia system flanking the porphyry veining on its northern side. Both systems outcrop at surface.

- Soil sampling at Apollo has outlined two coincidental high-grade copper and molybdenum in soil anomalies measuring more than 500 parts per million (“ppm”) copper and 30 ppm molybdenum and covering the target area.

- The current hole will only test the northern portion of this mineralized system with both soil anomalies remaining largely untested for future drilling.

- The Company plans to immediately begin constructing additional drill pads to the south of the current pad to better attack the target area from closer range.

- The reader should be cautioned that only assay results from a certified third-party laboratory can confirm whether any amounts of precious or base metals are present in the breccia matrix currently being intersected in the drill hole. As such, visual core inspection presented herein should be viewed as speculative in nature.

Source: Collective Mining

Figure 2: Plan View of the Apollo Target Area Outlining Porphyry and Breccia Targets Overprinted by High-Grade Coincidental Copper and Molybdenum Soil Anomalies

Figure 3: Core Photos from Drill Hole APC-1 Labeled with the Down Hole Depth Where Mineralization was Encountered

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Solaris Resources (TSX:SLS) (OTC:SLSSF) has reported assay results from additional holes at Warintza Project as part of its mineral resources growth drilling. The company also recently added to near-surface, high-grade northeast and southeast extension. Solaris has said that the extension to the northeast and southeast are not priority targets and therefore will be targeted for further growth through step-out drilling.

Highlights from drilling are as follows:

Key Takeaways

Since the discovery of Warintza East in mid-2021, approximately 1km east of Warintza Central, limited drilling has been completed on the open area between the two deposits that would fall into the eastern sector of the conceptual pit design for Warintza Central as uncategorized waste – these results now establish continuity of mineralization between the two deposits with Warintza East remaining entirely open and undrilled to the north, south and east for future potential growth

- SLSE-06 was collared from the original platform in the middle of Warintza East and drilled west-northwest into an entirely open volume, returning 484m of 0.42% CuEq¹ from surface

- SLSE-08 was collared from the same platform and drilled northwest into an open volume, returning 142m of 0.65% CuEq¹ from near surface within a broader interval of 536m of 0.43% CuEq¹ from surface

- SLSE-04 was collared between Warintza Central and Warintza East and drilled west-southwest into a partially open volume, returning 616m of 0.63% CuEq¹ from 276m depth within a broader interval of 892m of 0.50% CuEq¹ from surface, establishing the overlap of the two deposits within the Warintza Central pit shell

- SLSE-03 was collared from the same platform and drilled west-northwest into a partially open volume, returning 326m of 0.62% CuEq¹ from 276m depth within a broader interval of 818m of 0.38% CuEq¹ from 38m depth, further confirming the overlap of the two deposits

- SLSE-05, collared from the same platform, was drilled north-northwest into a partially open area, returning 268m of 0.53% CuEq¹ from 446m depth within a broader interval of 714m of 0.32% CuEq¹ from surface

Updated Warintza Central Mineral Resource Estimate expected to be issued in April

To date, 62 holes have been completed at Warintza Central with assays reported for 54 of these and 8 holes have been completed at Warintza East with results reported for all holes

Mr. Jorge Fierro, Vice President, Exploration, commented: “Following the final Warintza Central results released April 4, these results represent the final holes from Warintza East to be included in the forthcoming mineral resource update, and serve to convert what would otherwise be uncategorized waste within the expected pit shell in the area where Warintza Central and Warintza East overlap.”

Table 1 – Assay Results

| Hole ID | Date Reported | From (m) | To (m) | Interval (m) | Cu (%) | Mo (%) | Au (g/t) | CuEq¹ (%) | ||

| SLSE-08 | Apr 11, 2022 | 8 | 544 | 536 | 0.35 | 0.02 | 0.04 | 0.43 | ||

| Including | 18 | 160 | 142 | 0.56 | 0.01 | 0.06 | 0.65 | |||

| SLSE-07 | 632 | 1069 | 437 | 0.29 | 0.02 | 0.04 | 0.37 | |||

| SLSE-06 | 0 | 484 | 484 | 0.33 | 0.02 | 0.04 | 0.42 | |||

| SLSE-05 | 0 | 714 | 714 | 0.26 | 0.01 | 0.05 | 0.32 | |||

| Including | 446 | 714 | 268 | 0.42 | 0.02 | 0.08 | 0.53 | |||

| SLSE-04 | 0 | 892 | 892 | 0.43 | 0.01 | 0.04 | 0.50 | |||

| Including | 276 | 892 | 616 | 0.54 | 0.02 | 0.04 | 0.63 | |||

| SLSE-03 | 38 | 856 | 818 | 0.29 | 0.02 | 0.03 | 0.38 | |||

| Including | 276 | 602 | 326 | 0.48 | 0.03 | 0.05 | 0.62 | |||

| SLS-54 | Apr 4, 2022 | 0 | 1093 | 1093 | 0.45 | 0.02 | 0.04 | 0.56 | ||

| Including | 50 | 406 | 356 | 0.62 | 0.02 | 0.05 | 0.73 | |||

| SLS-53 | 10 | 967 | 957 | 0.39 | 0.01 | 0.03 | 0.46 | |||

| Including | 16 | 192 | 176 | 0.65 | 0.03 | 0.04 | 0.78 | |||

| SLS-52 | 42 | 1019 | 977 | 0.39 | 0.01 | 0.03 | 0.45 | |||

| Including | 96 | 578 | 482 | 0.55 | 0.01 | 0.03 | 0.62 | |||

| SLS-51 | 36 | 1048 | 1012 | 0.38 | 0.01 | 0.06 | 0.47 | |||

| Including | 130 | 1048 | 918 | 0.41 | 0.01 | 0.05 | 0.50 | |||

| SLS-50 | 336 | 458 | 122 | 0.14 | 0.04 | 0.03 | 0.30 | |||

| SLS-49 | Feb 28, 2022 | 50 | 867 | 817 | 0.50 | 0.02 | 0.04 | 0.60 | ||

| SLS-48 | 50 | 902 | 852 | 0.45 | 0.02 | 0.05 | 0.56 | |||

| SLS-47 | 48 | 859 | 811 | 0.41 | 0.02 | 0.05 | 0.51 | |||

| SLS-46 | 48 | 680 | 632 | 0.27 | 0.01 | 0.03 | 0.31 | |||

| SLS-45 | 44 | 608 | 564 | 0.37 | 0.01 | 0.03 | 0.41 | |||

| SLS-44 | 6 | 524 | 518 | 0.16 | 0.05 | 0.03 | 0.35 | |||

| SLS-43 | 138 | 350 | 212 | 0.17 | 0.03 | 0.03 | 0.30 | |||

| SLS-42 | 52 | 958 | 906 | 0.42 | 0.02 | 0.06 | 0.53 | |||

| SLSS-01 | Jan 18, 2022 | 0 | 755 | 755 | 0.28 | 0.02 | 0.02 | 0.36 | ||

| SLS-41 | Dec 14, 2021 | 0 | 592 | 592 | 0.42 | 0.02 | 0.06 | 0.52 | ||

| SLS-40 | 8 | 1056 | 1048 | 0.39 | 0.01 | 0.03 | 0.46 | |||

| SLS-39 | 28 | 943 | 915 | 0.49 | 0.01 | 0.04 | 0.56 | |||

| SLS-38 | 58 | 880 | 822 | 0.28 | 0.01 | 0.05 | 0.35 | |||

| SLS-37 | 28 | 896 | 868 | 0.39 | 0.05 | 0.05 | 0.58 | |||

| SLS-36 | Nov 15, 2021 | 2 | 1082 | 1080 | 0.33 | 0.01 | 0.04 | 0.41 | ||

| SLS-35 | 48 | 968 | 920 | 0.53 | 0.02 | 0.04 | 0.62 | |||

| SLS-34 | Oct 25, 2021 | 52 | 712 | 660 | 0.36 | 0.02 | 0.06 | 0.47 | ||

| SLS-33 | 40 | 762 | 722 | 0.55 | 0.03 | 0.05 | 0.69 | |||

| SLSE-02 | 0 | 1160 | 1160 | 0.20 | 0.01 | 0.04 | 0.25 | |||

| SLS-32 | Oct 12, 2021 | 0 | 618 | 618 | 0.38 | 0.02 | 0.05 | 0.48 | ||

| SLS-31 | 8 | 1008 | 1000 | 0.68 | 0.02 | 0.07 | 0.81 | |||

| SLS-30 | 2 | 374 | 372 | 0.57 | 0.06 | 0.06 | 0.82 | |||

| SLSE-01 | Sep 27, 2021 | 0 | 1213 | 1213 | 0.21 | 0.01 | 0.03 | 0.28 | ||

| SLS-29 | Sep 7, 2021 | 6 | 1190 | 1184 | 0.58 | 0.02 | 0.05 | 0.68 | ||

| SLS-28 | 6 | 638 | 632 | 0.51 | 0.04 | 0.06 | 0.68 | |||

| SLS-27 | 22 | 484 | 462 | 0.70 | 0.04 | 0.08 | 0.91 | |||

| SLS-26 | July 7, 2021 | 2 | 1002 | 1000 | 0.51 | 0.02 | 0.04 | 0.60 | ||

| SLS-25 | 62 | 444 | 382 | 0.62 | 0.03 | 0.08 | 0.77 | |||

| SLS-24 | 10 | 962 | 952 | 0.53 | 0.02 | 0.04 | 0.62 | |||

| SLS-19 | 6 | 420 | 414 | 0.21 | 0.01 | 0.06 | 0.31 | |||

| SLS-23 | May 26, 2021 | 10 | 558 | 548 | 0.31 | 0.02 | 0.06 | 0.42 | ||

| SLS-22 | 86 | 324 | 238 | 0.52 | 0.03 | 0.06 | 0.68 | |||

| SLS-21 | 2 | 1031 | 1029 | 0.63 | 0.02 | 0.04 | 0.73 | |||

| SLS-20 | April 19, 2021 | 18 | 706 | 688 | 0.35 | 0.04 | 0.05 | 0.51 | ||

| SLS-18 | 78 | 875 | 797 | 0.62 | 0.05 | 0.06 | 0.83 | |||

| SLS-17 | 12 | 506 | 494 | 0.39 | 0.02 | 0.06 | 0.50 | |||

| SLS-16 | Mar 22, 2021 | 20 | 978 | 958 | 0.63 | 0.03 | 0.06 | 0.77 | ||

| SLS-15 | 2 | 1231 | 1229 | 0.48 | 0.01 | 0.04 | 0.56 | |||

| SLS-14 | 0 | 922 | 922 | 0.79 | 0.03 | 0.08 | 0.94 | |||

| SLS-13 | Feb 22, 2021 | 6 | 468 | 462 | 0.80 | 0.04 | 0.09 | 1.00 | ||

| SLS-12 | 22 | 758 | 736 | 0.59 | 0.03 | 0.07 | 0.74 | |||

| SLS-11 | 6 | 694 | 688 | 0.39 | 0.04 | 0.05 | 0.57 | |||

| SLS-10 | 2 | 602 | 600 | 0.83 | 0.02 | 0.12 | 1.00 | |||

| SLS-09 | 122 | 220 | 98 | 0.60 | 0.02 | 0.04 | 0.71 | |||

| SLSW-01 | Feb 16, 2021 | 32 | 830 | 798 | 0.25 | 0.02 | 0.02 | 0.31 | ||

| SLS-08 | Jan 14, 2021 | 134 | 588 | 454 | 0.51 | 0.03 | 0.03 | 0.62 | ||

| SLS-07 | 0 | 1067 | 1067 | 0.49 | 0.02 | 0.04 | 0.60 | |||

| SLS-06 | Nov 23, 2020 | 8 | 892 | 884 | 0.50 | 0.03 | 0.04 | 0.62 | ||

| SLS-05 | 18 | 936 | 918 | 0.43 | 0.01 | 0.04 | 0.50 | |||

| SLS-04 | 0 | 1004 | 1004 | 0.59 | 0.03 | 0.05 | 0.71 | |||

| SLS-03 | Sep 28, 2020 | 4 | 1014 | 1010 | 0.59 | 0.02 | 0.10 | 0.71 | ||

| SLS-02 | 0 | 660 | 660 | 0.79 | 0.03 | 0.10 | 0.97 | |||

| SLS-01 | Aug 10, 2020 | 1 | 568 | 567 | 0.80 | 0.04 | 0.10 | 1.00 | ||

| Notes to table: True widths cannot be determined at this time. | ||||||||||

Table 2 – Collar Location

| Hole ID | Easting | Northing | Elevation (m) | Depth (m) | Azimuth (degrees) | Dip (degrees) |

| SLSE-08 | 801485 | 9648192 | 1170 | 959 | 305 | -70 |

| SLSE-07 | 800749 | 9648146 | 1282 | 1069 | 84 | -50 |

| SLSE-06 | 801485 | 9648192 | 1170 | 1078 | 285 | -55 |

| SLSE-05 | 800749 | 9648146 | 1282 | 737 | 330 | -65 |

| SLSE-04 | 800749 | 9648146 | 1282 | 893 | 257 | -45 |

| SLSE-03 | 800749 | 9648146 | 1282 | 909 | 270 | -45 |

| Notes to table: The coordinates are in WGS84 17S Datum. | ||||||

(1) No adjustments were made for recovery as the project is an early-stage exploration project and metallurgical data to allow for estimation of recoveries is not yet available. Solaris defines copper equivalent calculation for reporting purposes only. Copper-equivalence calculated as: CuEq (%) = Cu (%) + 3.33 × Mo (%) + 0.73 × Au (g/t), utilizing metal prices of Cu – US$3.00/lb, Mo – US$10.00/lb and Au – US$1,500/oz.

Source: Solaris Resources

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Copper prices have pulled back since a recent spike above $11,000 per tonne in March, but Goldman Sachs says that the ride higher isn’t over in 2022. Dramatic inventory shortages are to blame. In a note to clients, Goldman analysts said that they see a convincing case for prices to return to record highs by the end of the year. The bank has now revised its number higher to $13,000 per tonne.

Back in February 2022, Goldman indicated that a serious “scarcity episode” was occurring when stocks declined to about 200,000 tonnes. That amount was just enough to cover three days of global consumption, an extremely tight supply that could create chaos if not replenished fast enough.

The analysts boosted the anticipated deficit of refined metal for this year from previous forecasts by a factor of two, to 374,000 tonnes, and increased the shortfalls predicted over the following two years.

The investment bank’s three, six, and 12-month price targets are now all higher. Importantly, the bank sees a new price record in the next three months. That $13,000 price target? Analysts expect copper to climb to that level in just one year.

Another key indicator of the troubles ahead was what happened in March when stocks again declined on exchanges around the world. This is the first time in a decade this has happened considering this is usually the time that copper has a “…seasonal surplus phase.”

Goldman Sachs has historically been the biggest bull for copper, and it’s not the only one. JPMorgan increased its price target for the red metal, also due to a supply crunch.

The world is on an unprecedented path of growth and industrialization, and that is good news for copper bulls as demand continues to surge. Electric vehicles, batteries, 5G technology, and other factors are all working in favor of those who see higher prices ahead.

Beyond those macro factors, the supply crunch felt around the world is not expected to get any better. Factors such as coronavirus-related production delays, China’s crackdown on environmental violations, and a lack of new mines coming online are all working against those who need copper.

Inventories on the LME, the world’s largest copper market, have declined sharply since February, and are now at the lowest level in a decade. Inventories in China, the world’s largest copper consumer, have also been drawn down to extremely low levels.

While a surge in prices could be bad news for companies and consumers who need the metal for various reasons, it would be good news for producers. Companies such as Freeport-McMoRan (NYSE:FCX), Southern Copper (NYSE:SCCO), and Antofagasta (OTC:ANFGY) would all benefit if prices were to continue moving higher.

New copper projects are also scarce, and the explorers bringing new projects to fruition are finding valuations are soaring in the current climate.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

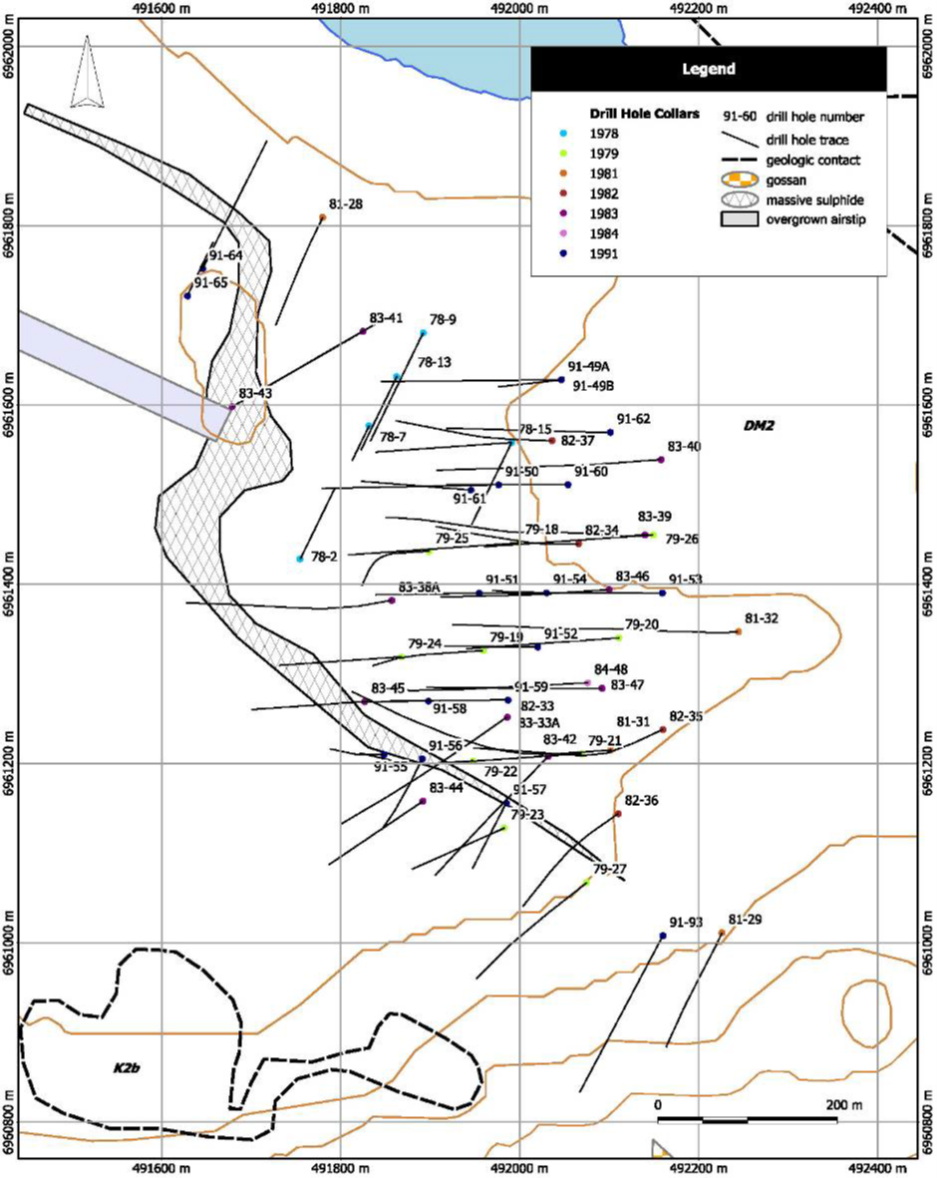

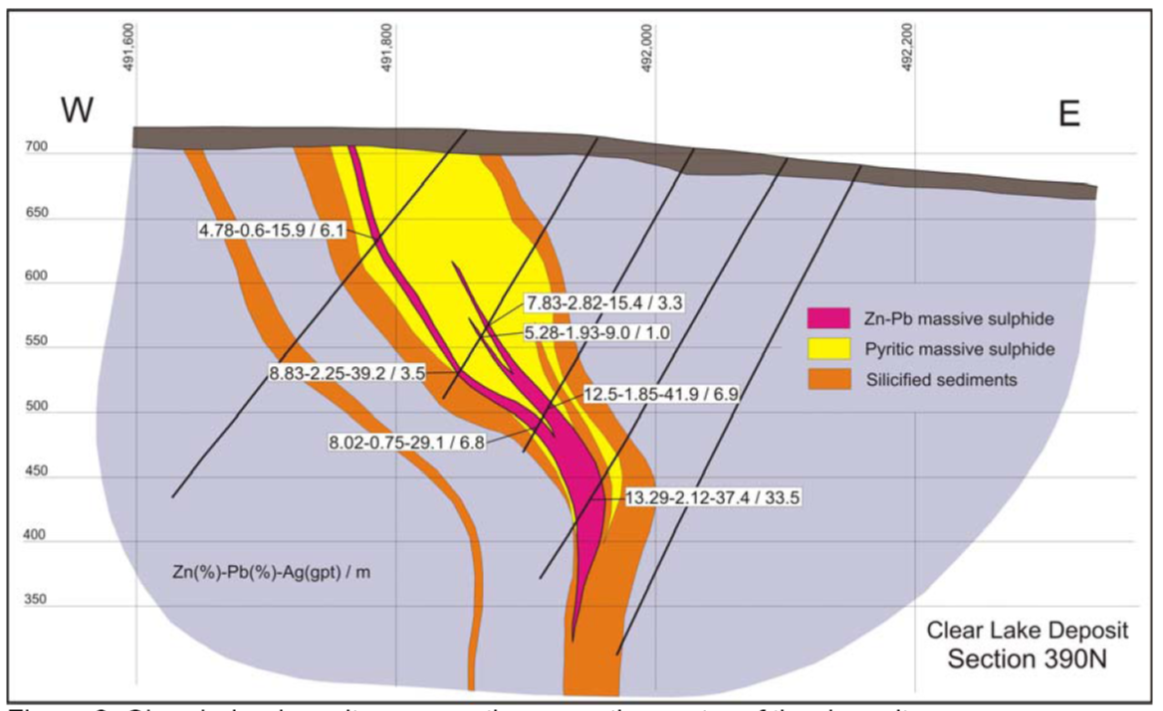

Honey Badger Silver Inc. (TSXV:TUF) announced on Tuesday, March 29 that it had acquired a 100% interest in the Clear Lake deposit in the Whitehorse Mining District of the Yukon.

The transaction is subject to a 1% net smelter return royalty on all metals except silver. The Clear Lake deposit is known to be an important source of zinc and lead but holds mostly silver. With the acquisition Honey Badger Silver Inc. is becoming the owner of a historic resource of 5.5 million ounces of silver.

Honey Badger Chairman Chad Williams said: *The Clear Lake acquisition represents a milestone as we acquire, on an extremely value-accretive basis, a quality asset with in-situ silver resources in one of the best mining jurisdictions in the world, where we are currently active at our higher-grade Plata silver project. This acquisition demonstrates our stated strategy of identifying and executing highly accretive targeted silver acquisitions. Clear Lake not only provides our shareholders with exposure to silver resources but also offers the possibility of unlocking value from the significant zinc and lead endowment, which is not of primary interest to Honey Badger, in a royalty/stream spin-off or even potentially other innovative instruments, such as a commodity-linked non-fungible token (“NFT”) – watch for more news on this front.”

This acquisition represents an important step in fulfilling the company’s strategy of entering more silver properties at different stages of production that will allow it to offer investors high exposure to silver prices. As part of the strategy. Honey Badger continues to conduct asset evaluations.

The historical resources were reported in a NI-43-101 technical report dated February 23, 2010 and were 43-101 compliant at the time the agreement was signed.

Inferred historical resource prepared by SRK Consulting in 2010 in accordance with National Instrument 43-101 (“NI 43-101”) of 5.5 million ounces of silver at 22 grams per tonne, plus 1.3 billion pounds of zinc grading 7.6% zinc and 185 million pounds of lead grade 1.08%(A)(B);

Figure 2: Cross-Section of Clear Lake Deposit, SRK Technical Report, 2010(A)

Being a silver deposit but also a zinc and lead deposit, the company is exploring different options to make the best use of the historic Clear Lake resource.

The Clear Lake deposit includes 1.3 billion pounds of zinc and 185 million pounds of lead so Honey Badger is considering the possible sale of royalties on the zinc and lead or other means. It also presents potential to gradually expand existing resources and discover additional mineralization on the property.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

As the war in Ukraine continues, and sanctions against Russian business continue to expand, mining companies have been exiting businesses in the country. Rio Tinto (ASX:RIO), BHP (NYSE:BHP), and more have been selling assets in Russia as they mak their exit.

Canada’s Kinross Gold (NYSE:KGC) is the latest company to dump holdings there, selling the Kupol and Dvoinnoye operating mines; exploration assets, including the Chulbatkan project; and related infrastructure to Highland Gold Mining and other associates in a $680 million cash deal. Under the agreement, Kinross will receive $400 million in cash for the Kupol mine and surrounding exploration rights.

When the transaction closes, Kinross will receive $100 million, with another $150 million to be paid out before the end of 2023, an additional $100 million before the end of 2024, and a final payment of $50 million before the end of 2025.

Highland Gold CEO Vladislav Sviblov commented in a press release: “Our largest mining hubs are located in the Khabarovsk and Chukotka regions, precisely where these mines are located, and we, therefore, anticipate operational, logistical and management synergies. We also intend to maintain the high operating standards of the previous owner, and to invest in employee development.”

Deals in the country are tightly linked with government approval and oversight considering the stakes, and the Russian Federation Ministry of Industry and Trade, Denis Manturov, commented: “Kinross Gold followed the second of the three options proposed by the government for foreign investors with choosing a civilised way out of Russian projects. Therefore, we support the execution of such a deal: the result will be a stable flow of tax revenues, save of working places and support for social projects in the regions of presence.”

A Civilized Way Out

For mining companies with assets in Russia, the path out of the country has been swift. The largest mining companies in the world have all pulled out or are in the process of selling assets, and while the reasons behind it vary, sanctions and political risk are the primary drivers.

Kinross Gold is the latest company to sell its Russian assets, with the sale totaling $680 million, and many other companies are in discussions to exit their businesses in the country.

The European Union has likewise stated that in response to Russia’s invasion of Ukraine, the European Commission will impose a ban on Russian coal and other items. A potential EU ban on Russian coal import, according to a Reuters source, would be worth around €4bn per year.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

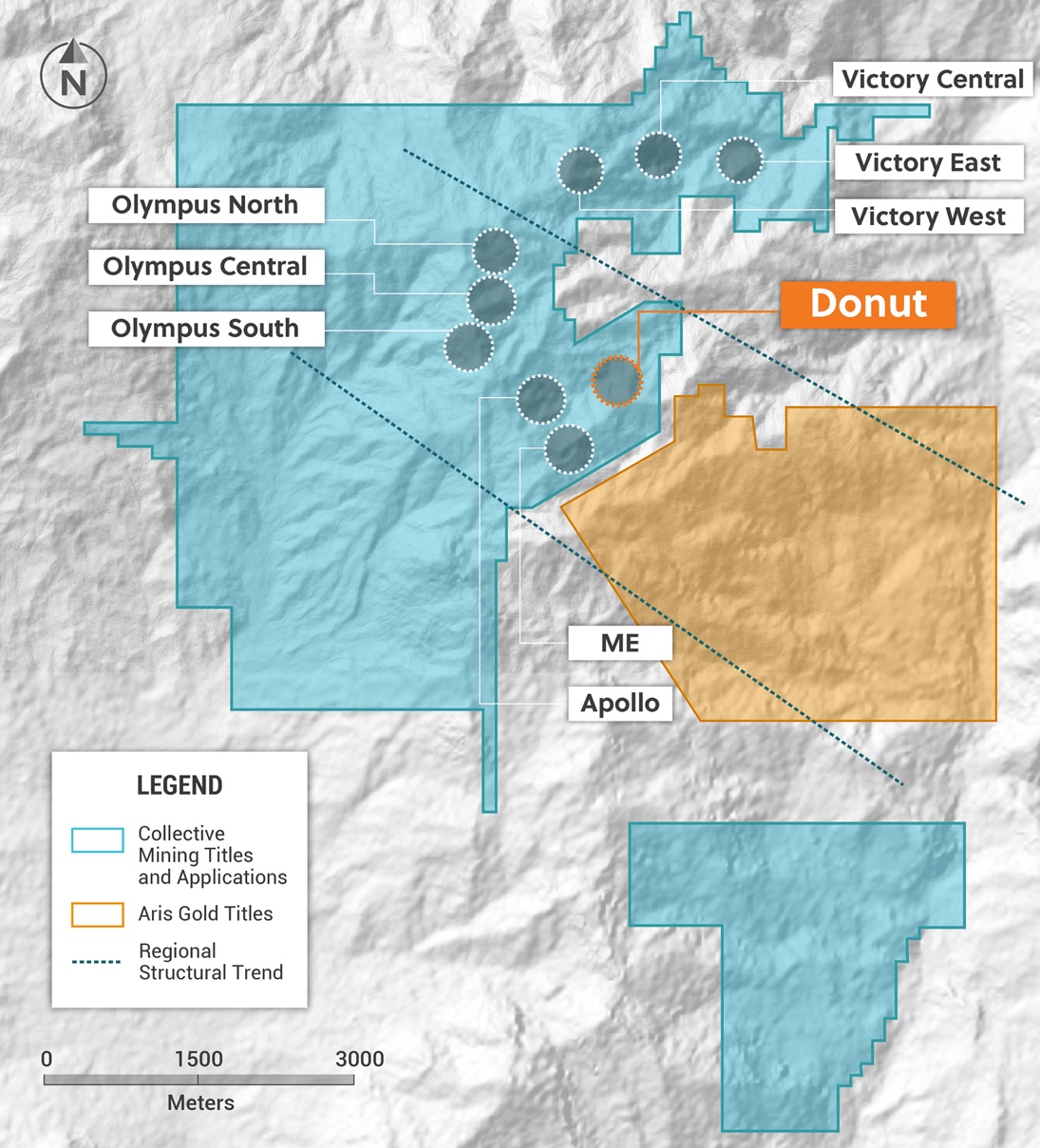

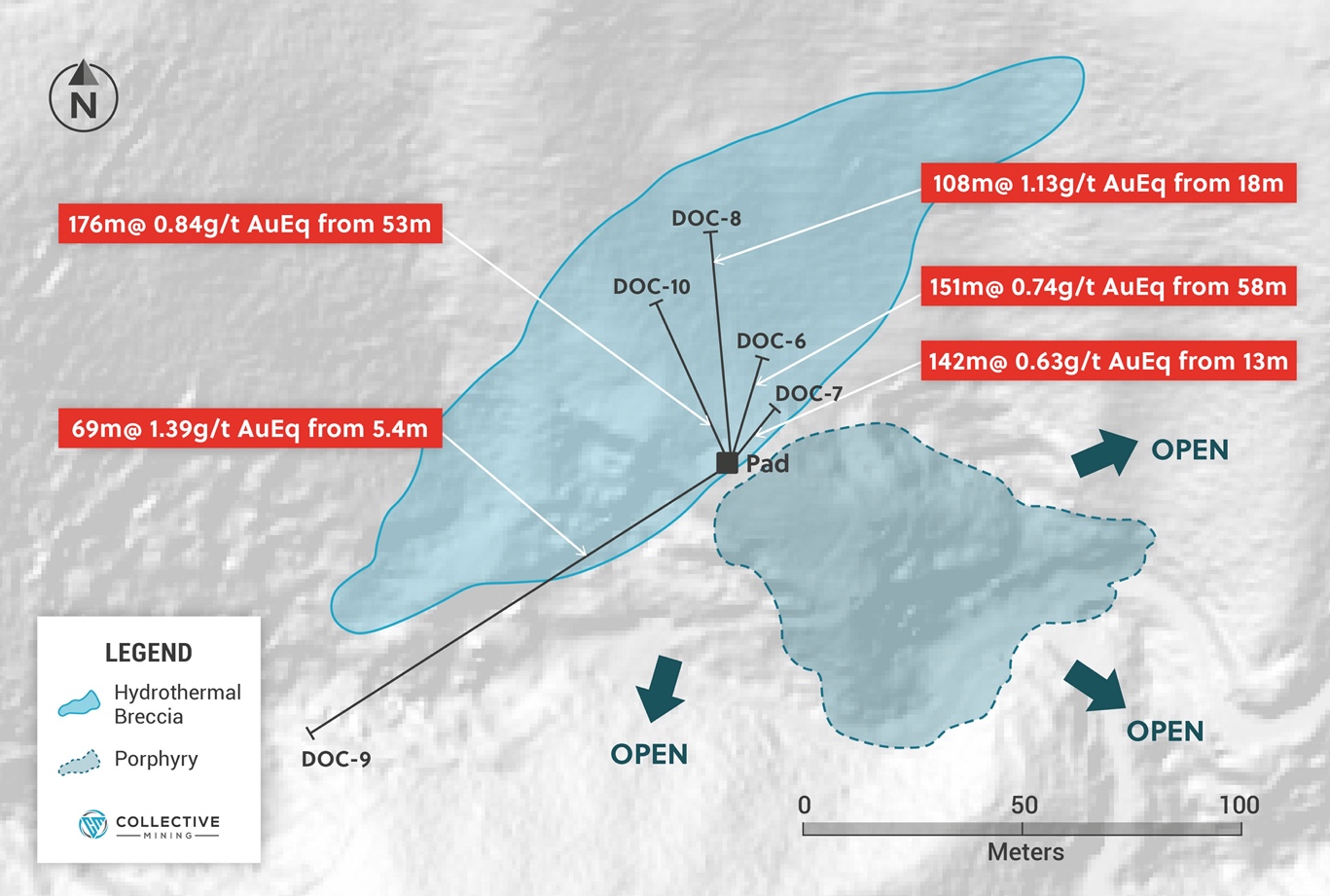

Collective Mining (TSXV:CNL) has published assay results for the final five diamond drill holes completed at the Donut Target in late 2021 as part of its maiden drill program at the Guayabales project, located in Caldas, Colombia. 2022’s drill plan of completing a minimum of 20,000 metres is already underway, with Collective currently operating four diamond drill rigs at the Guayabales Project.

A recent discovery at Olympus Central has directed the program’s focus toward expanding the discovery hole of 302 metres @1.11 g/t gold equivalent. At the same time, the company plans to test for the first suite of new targets: Victory East, Victory West, Olympus South, and Apollo. The expansion of the discovery hole as well as the first tests on the new targets will aim to deliver further results in the coming quarters.

Ari Sussman, Executive Chairman of Collective Mining, commented: “Over the course of the past year, Collective has drilled five grassroots generated targets and made three significant new discoveries, two of which are at the Guayabales project and one at the San Antonio project. In my career, I have never been involved in projects as prospective as our current portfolio. We plan on remaining aggressive for the balance of 2022 and will focus on expanding the mineralization at Olympus Central, where we recently drilled the discovery hole yielding 302 metres from near surface at 1.11 g/t gold equivalent.

“Additionally, over the next two weeks we will begin drilling at the Apollo target, which is characterized by coincidental copper and molybdenum soil anomalies blanketing outcropping porphyry related veins and breccias. By the middle of Q2, 2022 maiden drill programs will begin at the Victory East and Victory West targets, both of which are large scale copper and gold porphyry targets. Finally, drill programs to test the high-grade vein system at Olympus South and the porphyry potential at Donut will commence in early Q3, 2022.”

Figure 2: Plan View of the Donut Target Area

Table 1: Assay Results for drill holes DOC-6 – DOC-10

| Hole ID | From (m) | To (m) | Intercept (m) |

Au (g/t) |

Ag (g/t) |

Cu % | Mo % | AuEq (g/t)* |

| DOC-6 | 58.0 | 209.1 | 151.1 | 0.54 | 11 | 0.03 | 0.002 | 0.74 |

| Incl. | 58.0 | 88.6 | 30.60 | 0.83 | 10 | 0.03 | 0.002 | 1.02 |

| DOC-7 | 13.0 | 155.2 | 142.2 | 0.36 | 13 | 0.03 | 0.002 | 0.63 |

| DOC-8 | 18.0 | 125.7 | 107.7 | 0.78 | 21 | 0.02 | 0.001 | 1.13 |

| Incl. | 27.9 | 30.4 | 2.50 | 15.62 | 6 | 0.03 | 0.001 | 14.99 |

| DOC-9 | 5.4 | 74.3 | 68.9 | 0.97 | 24 | 0.03 | 0.002 | 1.39 |

| DOC-10 | 53.5 | 229.7 | 176.2 | 0.44 | 22 | 0.03 | 0.002 | 0.84 |

| Incl | 53.5 | 99.6 | 46.10 | 0.44 | 34 | 0.04 | 0.002 | 1.06 |

* AuEq (g/t) is calculated as follows: (Au (g/t) x 0.95) + (Ag g/t x 0.017 x 0.95) + (Cu (%) x 2.06 x 0.95) + (Mo (%) x 6.86 x 0.95), utilizing metal prices of Cu – US$4.50/lb, Mo – US$15.00/lb, Ag – $25/oz and Au – US$1,500/oz and recovery rates of 95% for Au, Ag, Cu and Mo. Recovery rate assumptions are speculative as no metallurgical work has been completed to date.

** A 0.1 g/t AuEq cut-off grade was employed with no more than 10% internal dilution. True widths are unknown, and grades are uncut.

Source: Collective Mining

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

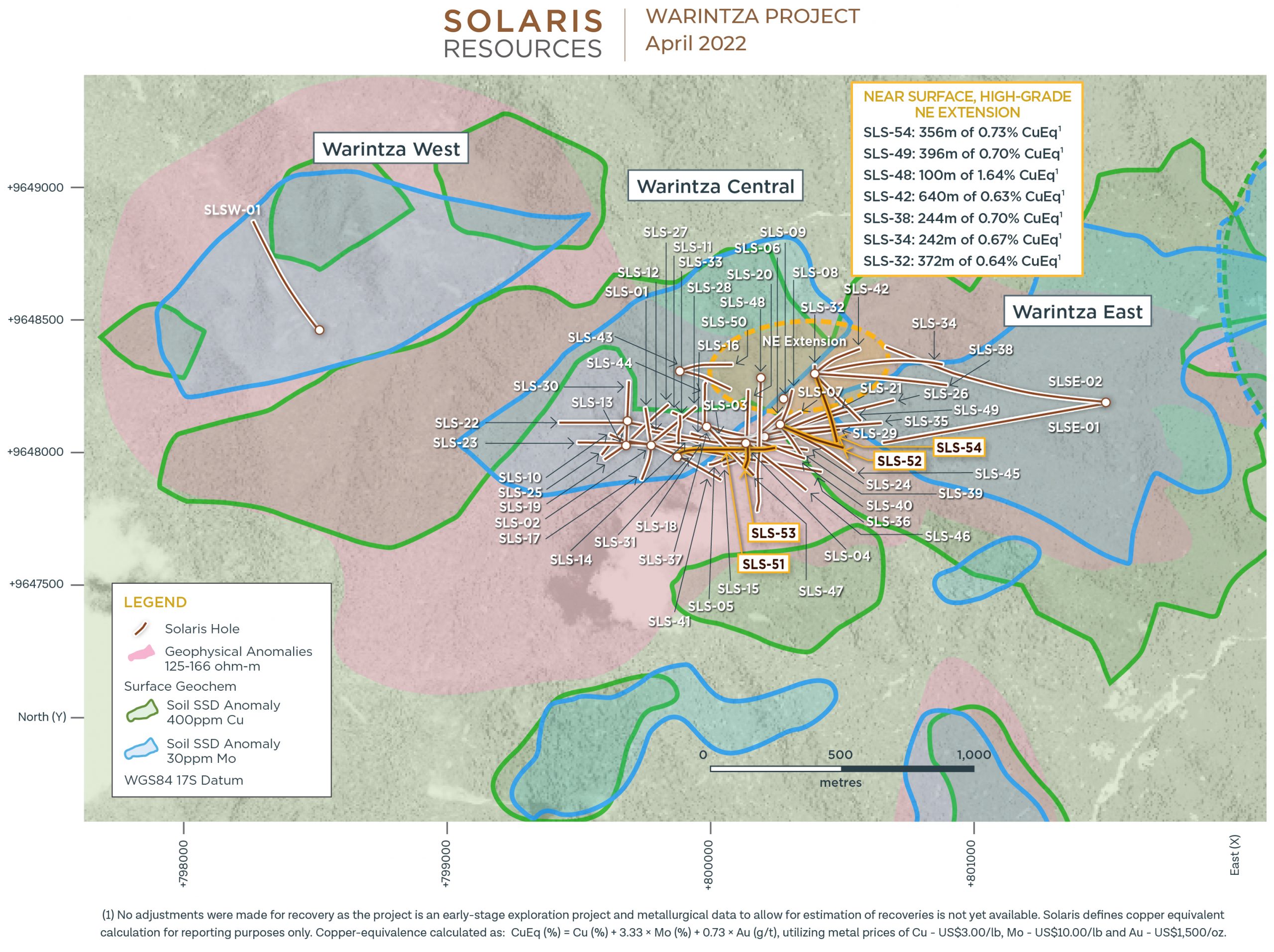

Solaris Resources (TSX:SLS) has reported assay results from a series of additional holes from mineral resource growth drilling at its Warintza Project in southeastern Ecuador. The results highlighted expansion of the growing northeastern extension area, and that drilling has expanded the southeastern extension area. The southeastern extension remains open in near surface, high-grade mineralization.

Mr. Jorge Fierro, Vice President of Exploration for Solaris, said in a press release: “These final holes expand on two key growth areas with near surface, high-grade mineralization on the edge of resource drilling that remains open. These holes will be included in the forthcoming resource update; further extensions to the northeast and southeast represent priority targets for further growth with step-out drilling commencing shortly.”

On top of the exciting assay results, the company has noted that an updated Warintza Central Mineral Resource Estimate is expected to be issued in April. This is a highly anticipated catalyst for the company and the Warintza Project.

Highlights

Additional drilling has expanded the growing northeast extension area, which remains open with follow-up and step-out drilling underway. This zone is characterized by near surface, high-grade mineralization, as detailed below, at the northeastern limit of drilling at Warintza Central and represents a priority target for further growth.

- SLS-54 was collared at the northeastern limit of the grid and drilled into an open volume near surface, returning 356m of 0.73% CuEq¹ from 50m depth within a broader interval of 1,093m of 0.56% CuEq¹ from surface

- This follows from near surface, high-grade mineralization previously reported (refer to press releases dated February 28, 2022, December 14, 2021 and October 25 & 12, 2021) from:

- SLS-49 – 396m of 0.70% CuEq¹ from 50m depth within 817m of 0.60% CuEq¹

- SLS-48 – 100m of 1.64% CuEq¹ from 50m depth within 852m of 0.56% CuEq¹

- SLS-42 – 740m of 0.60% CuEq¹ from 52m depth within 906m of 0.53% CuEq¹

- SLS-38 – 244m of 0.70% CuEq¹ from 58m depth within 822m of 0.35% CuEq¹

- SLS-34 – 242m of 0.67% CuEq¹ from 52m depth within 660m of 0.47% CuEq¹

- SLS-32 – 372m of 0.64% CuEq¹ from 46m depth within 618m of 0.48% CuEq¹

- Follow-up drilling from existing platforms is underway, with a 260m northeast step-out platform recently completed and a second platform stepping out further to the northeast under construction

Additional drilling has expanded the growing southeast extension area, which remains open in near surface, high-grade mineralization.

- SLS-52 was collared on the eastern side of the grid and drilled southeast into an open volume near surface, returning 482m of 0.62% CuEq¹ from 96m depth, within a broader interval of 977m of 0.45% CuEq¹ from near surface that infilled drilling at depth

- SLS-53 was collared from a southeastern platform and drilled south into an open volume near surface, returning 176m of 0.78% CuEq¹ from 16m depth, within a broader interval of 957m of 0.46% CuEq¹ from 10m depth that infilled drilling at depth

- This follows from near surface, high-grade mineralization previously reported (refer to press releases dated February 28, 2022, December 14, 2021 and November 15, 2021) from:

- SLS-45 – 236m of 0.56% CuEq¹ from 44m depth within 564m of 0.41% CuEq¹

- SLS-39 – 368m of 0.73% CuEq¹ from 90m depth within 915m of 0.56% CuEq¹

- SLS-35 – 326m of 0.80% CuEq¹ from 50m depth within 920m of 0.62% CuEq¹

- Additional platform construction to support follow-up and step-out drilling to test the further southeast extension of near surface, high-grade mineralization is planned, following the release of the updated mineral resource estimate

- SLS-51 was collared from the south-central portion of the grid and drilled east into an open volume at surface, returning 918m of 0.50% CuEq¹ from 130m depth within a broader interval of 1,012m of 0.47% CuEq¹ from near surface that infilled drilling at depth

Updated Warintza Central Mineral Resource Estimate expected to be issued in April.

To date, 62 holes have been completed at Warintza Central with assays reported for 54 of these.

Table 1 – Assay Results

| Hole ID | Date Reported | From (m) | To (m) | Interval (m) | Cu (%) | Mo (%) | Au (g/t) | CuEq¹ (%) | ||

| SLS-54 | Apr 4, 2022 | 0 | 1093 | 1093 | 0.45 | 0.02 | 0.04 | 0.56 | ||

| Including | 50 | 406 | 356 | 0.62 | 0.02 | 0.05 | 0.73 | |||

| SLS-53 | 10 | 967 | 957 | 0.39 | 0.01 | 0.03 | 0.46 | |||

| Including | 16 | 192 | 176 | 0.65 | 0.03 | 0.04 | 0.78 | |||

| SLS-52 | 42 | 1019 | 977 | 0.39 | 0.01 | 0.03 | 0.45 | |||

| Including | 96 | 578 | 482 | 0.55 | 0.01 | 0.03 | 0.62 | |||

| SLS-51 | 36 | 1048 | 1012 | 0.38 | 0.01 | 0.06 | 0.47 | |||

| Including | 130 | 1048 | 918 | 0.41 | 0.01 | 0.05 | 0.50 | |||

| SLS-50 | 336 | 458 | 122 | 0.14 | 0.04 | 0.03 | 0.30 | |||

| SLS-49 | Feb 28, 2022 | 50 | 867 | 817 | 0.50 | 0.02 | 0.04 | 0.60 | ||

| SLS-48 | 50 | 902 | 852 | 0.45 | 0.02 | 0.05 | 0.56 | |||

| SLS-47 | 48 | 859 | 811 | 0.41 | 0.02 | 0.05 | 0.51 | |||

| SLS-46 | 48 | 680 | 632 | 0.27 | 0.01 | 0.03 | 0.31 | |||

| SLS-45 | 44 | 608 | 564 | 0.37 | 0.01 | 0.03 | 0.41 | |||

| SLS-44 | 6 | 524 | 518 | 0.16 | 0.05 | 0.03 | 0.35 | |||

| SLS-43 | 138 | 350 | 212 | 0.17 | 0.03 | 0.03 | 0.30 | |||

| SLS-42 | 52 | 958 | 906 | 0.42 | 0.02 | 0.06 | 0.53 | |||

| SLSS-01 | Jan 18, 2022 | 0 | 755 | 755 | 0.28 | 0.02 | 0.02 | 0.36 | ||

| SLS-41 | Dec 14, 2021 | 0 | 592 | 592 | 0.42 | 0.02 | 0.06 | 0.52 | ||

| SLS-40 | 8 | 1056 | 1048 | 0.39 | 0.01 | 0.03 | 0.46 | |||

| SLS-39 | 28 | 943 | 915 | 0.49 | 0.01 | 0.04 | 0.56 | |||

| SLS-38 | 58 | 880 | 822 | 0.28 | 0.01 | 0.05 | 0.35 | |||

| SLS-37 | 28 | 896 | 868 | 0.39 | 0.05 | 0.05 | 0.58 | |||

| SLS-36 | Nov 15, 2021 | 2 | 1082 | 1080 | 0.33 | 0.01 | 0.04 | 0.41 | ||

| SLS-35 | 48 | 968 | 920 | 0.53 | 0.02 | 0.04 | 0.62 | |||

| SLS-34 | Oct 25, 2021 | 52 | 712 | 660 | 0.36 | 0.02 | 0.06 | 0.47 | ||

| SLS-33 | 40 | 762 | 722 | 0.55 | 0.03 | 0.05 | 0.69 | |||

| SLSE-02 | 0 | 1160 | 1160 | 0.20 | 0.01 | 0.04 | 0.25 | |||

| SLS-32 | Oct 12, 2021 | 0 | 618 | 618 | 0.38 | 0.02 | 0.05 | 0.48 | ||

| SLS-31 | 8 | 1008 | 1000 | 0.68 | 0.02 | 0.07 | 0.81 | |||

| SLS-30 | 2 | 374 | 372 | 0.57 | 0.06 | 0.06 | 0.82 | |||

| SLSE-01 | Sep 27, 2021 | 0 | 1213 | 1213 | 0.21 | 0.01 | 0.03 | 0.28 | ||

| SLS-29 | Sep 7, 2021 | 6 | 1190 | 1184 | 0.58 | 0.02 | 0.05 | 0.68 | ||

| SLS-28 | 6 | 638 | 632 | 0.51 | 0.04 | 0.06 | 0.68 | |||

| SLS-27 | 22 | 484 | 462 | 0.70 | 0.04 | 0.08 | 0.91 | |||

| SLS-26 | July 7, 2021 | 2 | 1002 | 1000 | 0.51 | 0.02 | 0.04 | 0.60 | ||

| SLS-25 | 62 | 444 | 382 | 0.62 | 0.03 | 0.08 | 0.77 | |||

| SLS-24 | 10 | 962 | 952 | 0.53 | 0.02 | 0.04 | 0.62 | |||

| SLS-19 | 6 | 420 | 414 | 0.21 | 0.01 | 0.06 | 0.31 | |||

| SLS-23 | May 26, 2021 | 10 | 558 | 548 | 0.31 | 0.02 | 0.06 | 0.42 | ||

| SLS-22 | 86 | 324 | 238 | 0.52 | 0.03 | 0.06 | 0.68 | |||

| SLS-21 | 2 | 1031 | 1029 | 0.63 | 0.02 | 0.04 | 0.73 | |||

| SLS-20 | April 19, 2021 | 18 | 706 | 688 | 0.35 | 0.04 | 0.05 | 0.51 | ||

| SLS-18 | 78 | 875 | 797 | 0.62 | 0.05 | 0.06 | 0.83 | |||

| SLS-17 | 12 | 506 | 494 | 0.39 | 0.02 | 0.06 | 0.50 | |||

| SLS-16 | Mar 22, 2021 | 20 | 978 | 958 | 0.63 | 0.03 | 0.06 | 0.77 | ||

| SLS-15 | 2 | 1231 | 1229 | 0.48 | 0.01 | 0.04 | 0.56 | |||

| SLS-14 | 0 | 922 | 922 | 0.79 | 0.03 | 0.08 | 0.94 | |||

| SLS-13 | Feb 22, 2021 | 6 | 468 | 462 | 0.80 | 0.04 | 0.09 | 1.00 | ||

| SLS-12 | 22 | 758 | 736 | 0.59 | 0.03 | 0.07 | 0.74 | |||

| SLS-11 | 6 | 694 | 688 | 0.39 | 0.04 | 0.05 | 0.57 | |||

| SLS-10 | 2 | 602 | 600 | 0.83 | 0.02 | 0.12 | 1.00 | |||

| SLS-09 | 122 | 220 | 98 | 0.60 | 0.02 | 0.04 | 0.71 | |||

| SLSW-01 | Feb 16, 2021 | 32 | 830 | 798 | 0.25 | 0.02 | 0.02 | 0.31 | ||

| SLS-08 | Jan 14, 2021 | 134 | 588 | 454 | 0.51 | 0.03 | 0.03 | 0.62 | ||

| SLS-07 | 0 | 1067 | 1067 | 0.49 | 0.02 | 0.04 | 0.60 | |||

| SLS-06 | Nov 23, 2020 | 8 | 892 | 884 | 0.50 | 0.03 | 0.04 | 0.62 | ||

| SLS-05 | 18 | 936 | 918 | 0.43 | 0.01 | 0.04 | 0.50 | |||

| SLS-04 | 0 | 1004 | 1004 | 0.59 | 0.03 | 0.05 | 0.71 | |||

| SLS-03 | Sep 28, 2020 | 4 | 1014 | 1010 | 0.59 | 0.02 | 0.10 | 0.71 | ||

| SLS-02 | 0 | 660 | 660 | 0.79 | 0.03 | 0.10 | 0.97 | |||

| SLS-01 | Aug 10, 2020 | 1 | 568 | 567 | 0.80 | 0.04 | 0.10 | 1.00 | ||

| Notes to table: True widths cannot be determined at this time. | ||||||||||

Table 2 – Collar Location

| Hole ID | Easting | Northing | Elevation (m) | Depth (m) | Azimuth (degrees) | Dip (degrees) |

| SLS-54 | 800383 | 9648303 | 1412 | 1093 | 160 | -74 |

| SLS-53 | 800126 | 9648032 | 1566 | 967 | 170 | -82 |

| SLS-52 | 800258 | 9648097 | 1559 | 1019 | 110 | -75 |

| SLS-51 | 799873 | 9648008 | 1632 | 1048 | 85 | -70 |

| SLS-50 | 799870 | 9648315 | 1414 | 768 | 80 | -75 |

| Notes to table: The coordinates are in WGS84 17S Datum. | ||||||

(1) No adjustments were made for recovery as the project is an early-stage exploration project and metallurgical data to allow for estimation of recoveries is not yet available. Solaris defines copper equivalent calculation for reporting purposes only. Copper-equivalence calculated as: CuEq (%) = Cu (%) + 3.33 × Mo (%) + 0.73 × Au (g/t), utilizing metal prices of Cu – US$3.00/lb, Mo – US$10.00/lb and Au – US$1,500/oz.

Source: Solaris Resources

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Among President Joe Biden’s plans at the moment are the potential use of Cold War powers to achieve increased domestic production of essential minerals for batteries and electric vehicles.

Throughout history, the Defense Production Act of 1950 has been used rarely. Today, the White House is preparing to add battery materials to the list of items covered by this Act. Just as Harry Truman used it to manufacture steel for the Korean War and Donald Trump to encourage the production of facemasks to deal with the coronavirus pandemic.

Shares of MP Materials Corp., being the only U.S. company that produces metals needed for the production of electric vehicles, rose 4.7% on the day of the news. Lithium Americas Corp. which heads a project in Nevada posted its biggest gain in several weeks. And Piedmont Lithium Inc. rebounded from losses in recent weeks by gaining as much as 8.7% on the day of the announcement.

Huge Funding Available

If minerals such as lithium, nickel, cobalt, cobalt, manganese and cobalt are added to the list mining companies could be boosted and have access to $750 million for production under the fund titled III Defense Production Act. This could also help the recycling of materials needed for batteries.

The funding from the directive would be encouraging improvements to current production such as productivity and safety improvements as well as funding reliability studies in order to avoid loans or outright purchases. It would also encourage the manufacture of high-capacity batteries.