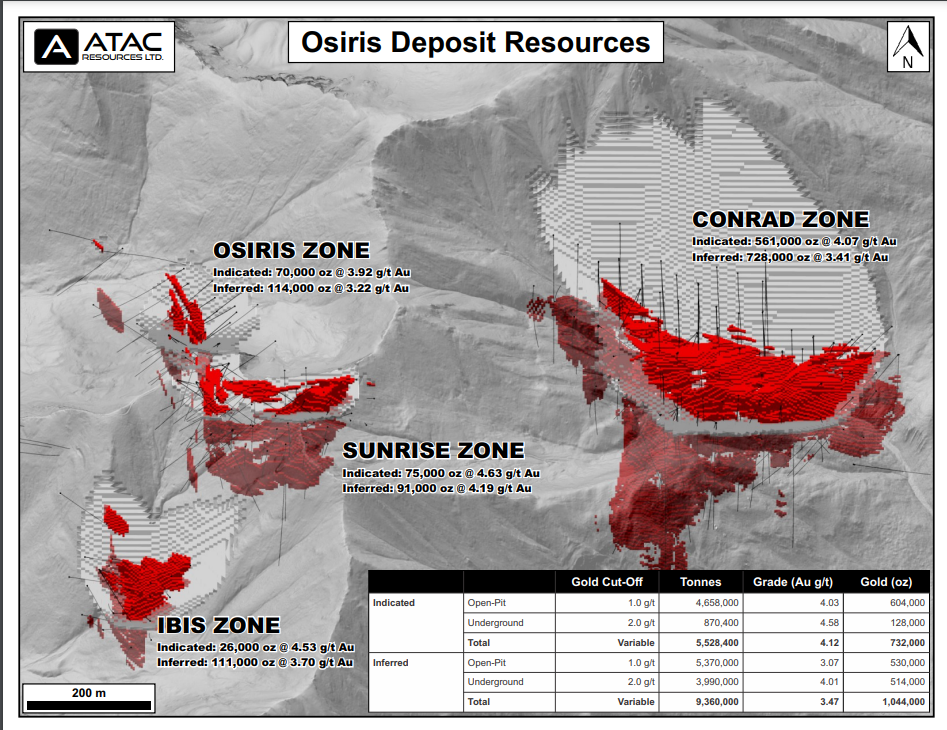

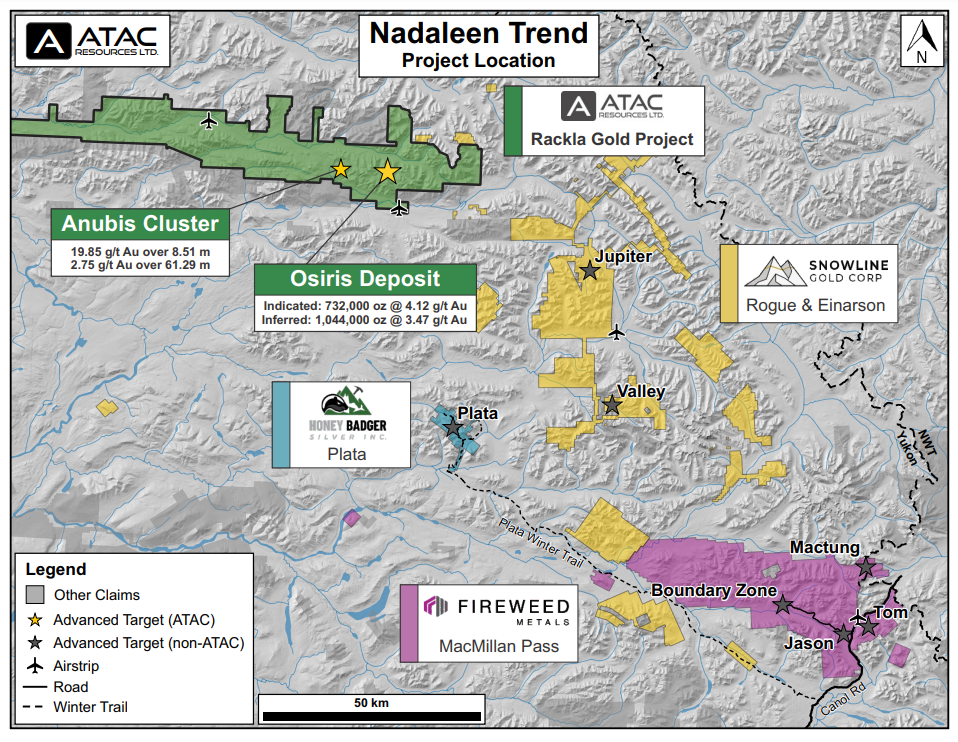

ATAC Resources (TSXV:ATC) has announced it has completed an updated mineral resource estimate at the Osiris Deposit at the Rackla Gold Property in Yukon, Canada. The 100%-owned property demonstrates a significant conversation of resources from the Inferred to Indicated category at the Osiris Deposit. This mineral resource estimate updates data from the previously released 2018 Osiris Resources. The company has since done additional geological modelling, geotechnical studies, and metallurgical test work since then. The cut-off grades for the deposit have also been modified to reflect current gold prices.

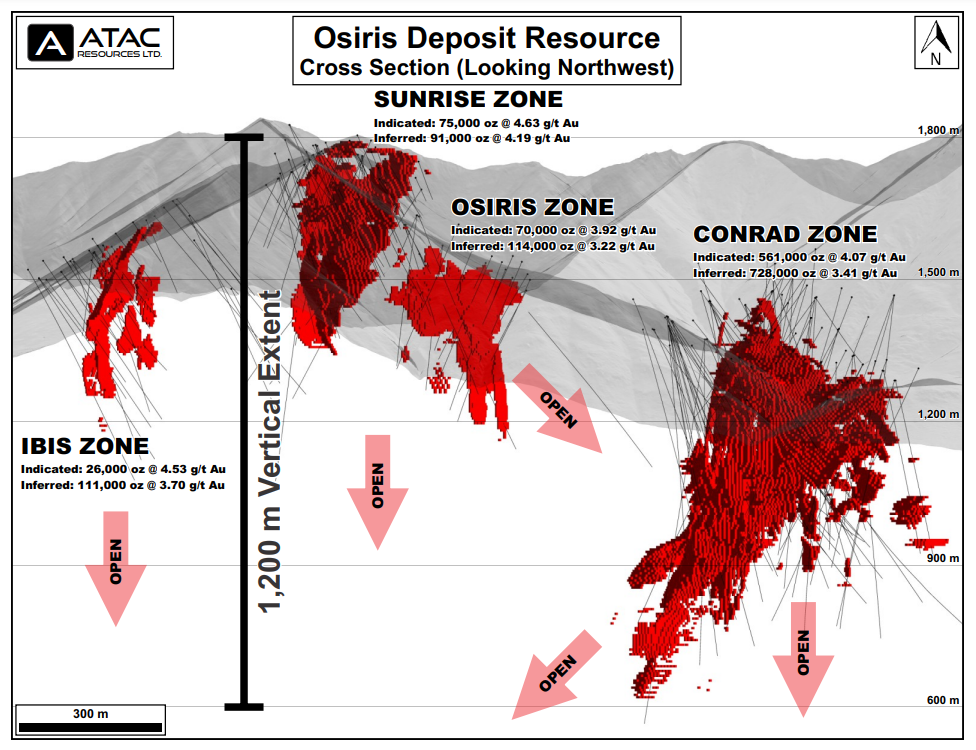

The Osiris Deposit is located at the eastern end of ATAC Resources’ Nadaleen Project. The deposit has four zones: Conrad, Sunrise, Osiris, and Ibis. All four of the zones remain open in multiple directions. The company also has additional targets at the pre-resource stage.

Graham Downs, President and CEO of ATAC Resources, commented in a press release: “We are very pleased to demonstrate significant conversion of resources from the Inferred to Indicated category at Osiris. This continues to demonstrate the confidence we have in this extensive, high-grade Carlin-style system that hosts some of the best gold intervals ever reported in Yukon. Work over the past two years has focused on technical studies and modeling, leading to growth of the deposit and improved classification of part of the resources at Osiris. We have recently completed 1,500 m of drilling stepping out on open near-surface parts of the resource and look forward to releasing those results when available.”

Highlights from the Deposit Resource Update include:

- Indicated Mineral Resource of 732,000 ounces gold at an average grade of 4.12 g/t (in 5.5 Mt), including pit-constrained resources of 604,000 ounces gold at 4.03 g/t (in 4.7 Mt);

- Inferred Mineral Resource of 1,044,000 ounces gold at an average grade of 3.47 g/t (in 9.4 Mt), including pit-constrained resources of 530,000 ounces gold at 3.07 g/t (in 5.4 Mt);

- Conversion of 43% of the 2018 maiden Inferred Resource (1,685,000 ounces at 4.23 g/t) to the Indicated category;

- All zones remain open to extension along strike and at depth; and

- Metallurgical testwork confirms >80% gold recoveries, and viable processing paths with flotation, pre-treatment by either pressure oxidation or roasting, and cyanide leaching.

Osiris Deposit – Mineral Resource Estimate Summary1,2,3

| Classification | Type | Gold Cut-off

(Au g/t) |

Tonnes | Grade

(Au g/t) |

Gold (ounces) |

| Indicated | Open-Pit3 | 1.0 | 4,658,000 | 4.03 | 604,000 |

| Underground | 2.0 | 870,400 | 4.58 | 128,000 | |

| Total | Variable | 5,528,400 | 4.12 | 732,000 | |

| Inferred | Open-Pit3 | 1.0 | 5,370,000 | 3.07 | 530,000 |

| Underground | 2.0 | 3,990,000 | 4.01 | 514,000 | |

| Total | Variable | 9,360,000 | 3.47 | 1,044,000 |

| 1. | CIM definition standards were used for the Mineral Resource. The Qualified Person is Steven Ristorcelli, C.P.G., associate of MDA. |

| 2. | Numbers may not add due to rounding. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. |

| 3. | Open-Pit material was constrained using a Whittle™ optimization at US$1,800/oz gold price. |

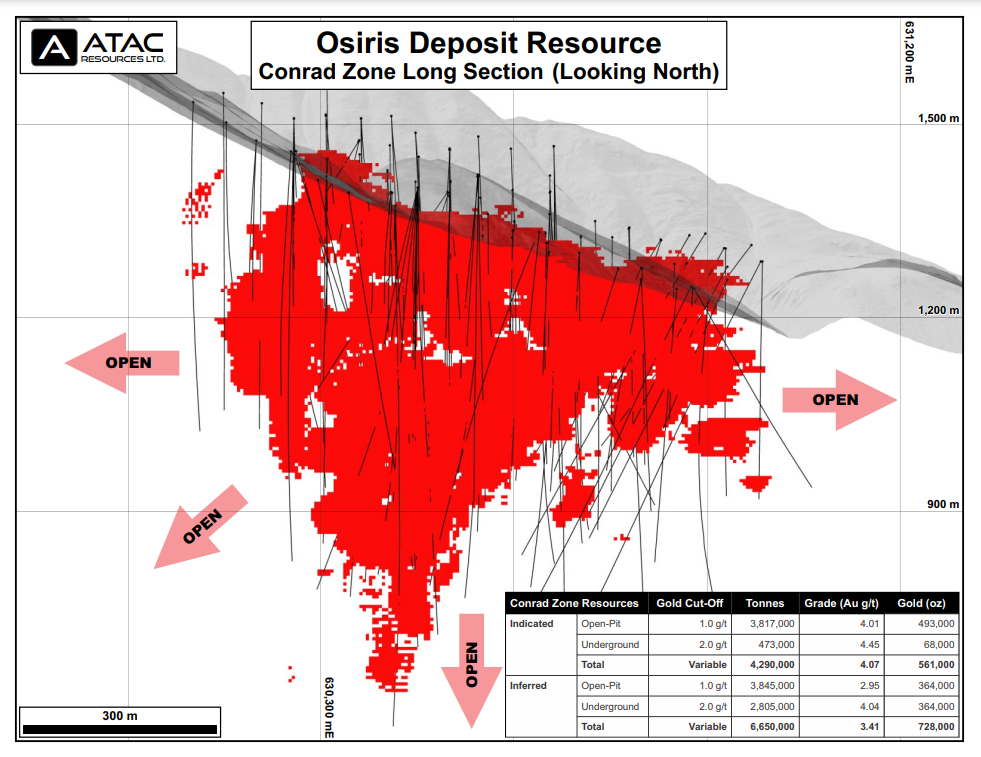

Figure 2 – Conrad Long Section

Figure 3 – Osiris Long Section

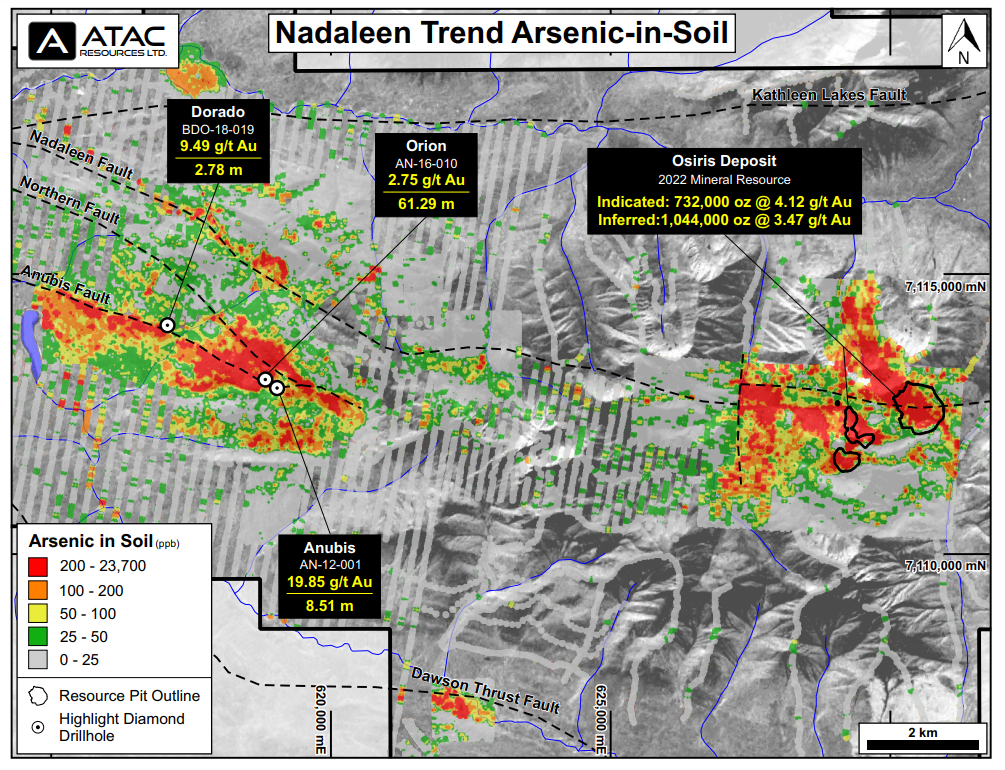

Figure 4 – Nadaleen Trend

Figure 5 – Nadaleen Project Location

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Aris Gold (TSX:ARIS) and GCM Mining have announced a signed merger deal that will make the combined company the largest gold mining company in Colombia. GCM will acquire Aris Gold for all of the remaining shares it does not already own. The company will purchase the remaining outstanding shares at an exchange ratio of 0.5 of a GCM share for every Aris Gold share. The merged company anticipates a balance sheet of $397 million in cash and $260 million in additional committed funding. Once the transaction is completed, it will become a large-scale gold mining company that the companies have said will be “top-of-the-class” among the junior producers in the Americas. The deal is currently scheduled to close following the companies’ shareholder meetings which are scheduled in mid-September 2022.

Once combined, it will also be Colombia’s biggest company and will continue to operate under the Aris Gold name, headquartered in Vancouver, Canada. The total consolidated business will have a mix of exploration, development, and production assets across the Americas and will be led by Neil Woodyer as CEO and director. The company’s project portfolio will ultimately span Soto Norte, Marmato Mine, and Segovia operations in Colombia, the Juby project in Ontario, Canada and in Guyana, the Toroparu project. The final merged company expects to have proven and probable mineral reserves of 3.8Moz of gold and 18.3Moz of measured and indicated mineral resources of gold.

In a press release, Aris Gold chairman Ian Telfer commented: “The combined group creates a top-in-class company with multiple tier one assets. After Aris Gold became the operator of the Soto Norte joint venture, joining forces with GCM became a logical next step. Our increased scale will also broaden our future opportunities to continue building a +1 million ounce (oz) producer over the next few years.”

GCM executive chair Serafino Iacono commented: “Each team has unique strengths with GCM being the Colombian leader for responsible, sustainable mining practices. Together with Aris Gold’s Board and management, the combined group brings a track record of building sizable and successful mining companies; this transaction further diversifies the company’s portfolio and reaffirms Colombia as an area of focus. While I am stepping down from a day-to-day executive role, I will remain a director and adviser on matters in Colombia, as well as an enthusiastic security holder.”

Highlights of the transaction are as follows:

- Creates the top-of-the-class company among junior producers and the largest gold company in Colombia, with diversification in Guyana and Canada.

- Experienced Board of Directors and management team with a track record of building value in the gold sector

- Brings together teams with unmatched experience in Colombia and extensive project development and mine building expertise

- Strong financial position to de-risk growth projects, with combined cash and committed funding of US$657 million2 and free cash flow generation from the Segovia Operations (US$84 million on a 12-month trailing basis to March 31, 2022)3

- Estimated G&A cost savings of US$10 million per year through the reduction of duplicative public company expenses and rationalizing other expenses

- No premium transaction that simplifies the ownership structure within a single company

- Substantial long-term re-rating potential, with share price upside from enhanced market visibility, trading liquidity, access to capital, and reduced cost of capital

- Segovia Operations (Antioquia, Colombia): a high-grade underground mining district that produced 206,389 ounces of gold in 2021. Operations at Segovia have been ongoing for over 150 years and there is a well-established history of mineral resource and reserve replacement. The Segovia Operations include the purchase of mined material from small-scale miners, which are described in the Segovia Technical Report[5] and represented about 16% of 2021’s gold production, as part of an industry-leading Colombian program for the integration of informal small-scale miners into the supply chain, with added environmental, social and security benefits.

- Marmato Mine (Caldas, Colombia): a historic producing underground gold mine currently undergoing a modernization and expansion program, which includes the construction of a new decline, mine workings, 4,000 tpd carbon in pulp processing plant and dry stack tailings facilities. The Pre-Feasibility Study disclosed in the Marmato Technical Report estimates production of 175,000 ounces per year (oz/yr) from the optimized Upper Mine and the Lower Mine expansion project.5

- Toroparu Project (Cuyuni-Mazaruni, Guyana): an advanced stage open pit and underground gold project with estimated average gold production of 225,000 oz/yr over a 24-year mine life, as described in the Preliminary Economic Assessment (PEA) disclosed in the Toroparu Technical Report.6 Located approximately 50 kilometres southwest of the recently constructed Aurora gold mine, Toroparu is one of the largest undeveloped gold projects in the Americas and provides the combined company with a foothold in the emerging and highly prospective Central Guiana Shear Zone.5

- Soto Norte Project (Santander, Colombia): a large-scale feasibility-stage underground gold project undergoing permitting and licensing. In April 2022, Aris Gold became the operator of the Soto Note joint venture and is leading a new and reframed environmental permitting process. The Feasibility Study disclosed in the Soto Norte Technical Report estimates average gold production of 450,000 oz/yr over the steady state production years. Upon exercising its option to increase its joint venture ownership interest from 20% to 50%, the attributable gold production to Aris Gold would be 225,000 oz/yr.5

- Juby Project (Ontario, Canada): an advanced stage gold project with an open pit mineral resource located in the Abitibi greenstone belt.

Source: Aris Gold Corporation

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

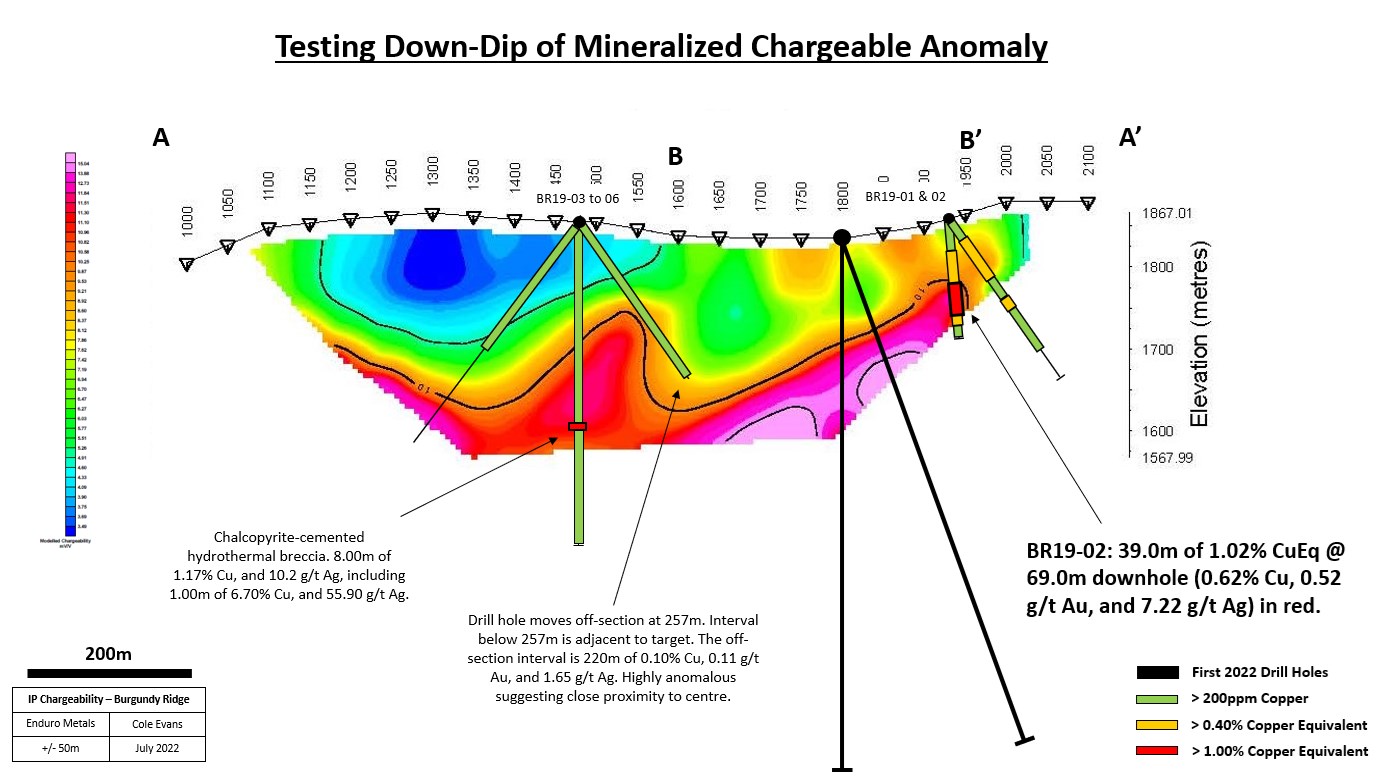

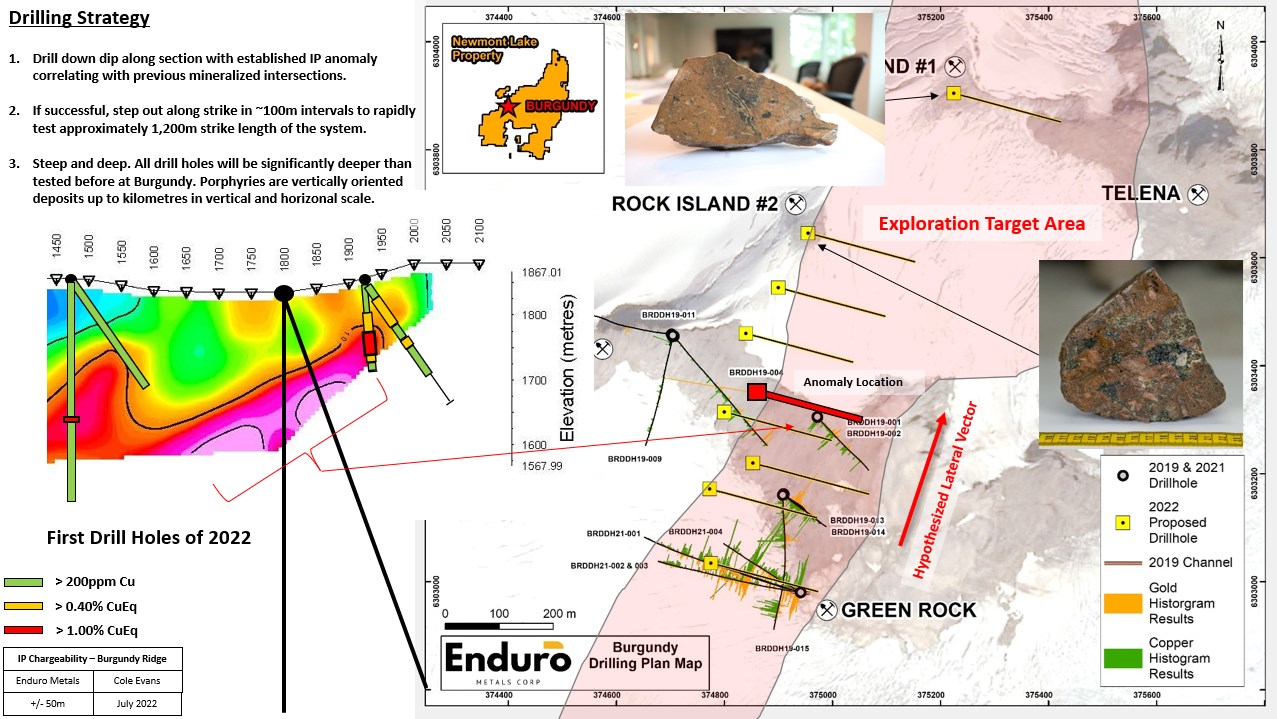

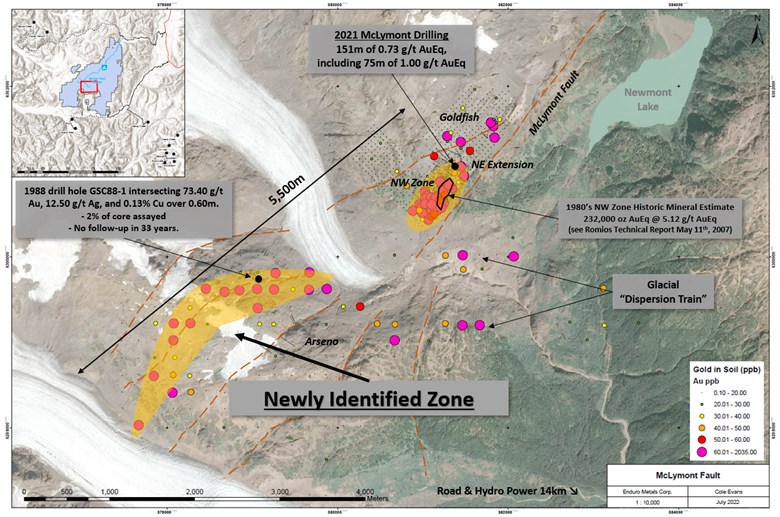

Enduro Metals (TSXV:ENDR) has announced the fully-funded 2022 exploration program at the Newmont Lake Project has begun. Located in British Columbia’s Golden Triangle, the goals of the drilling focus on the Burgundy Ridge and McLymont Fault Projects.

The goal of the 2022 exploration program is to expand the mineralized footprint of the alkalic porphyry system discovered at Burgundy Ridge in 2021. The second aim will be to continue the geochemical sampling effort at McLymont Fault and extend the potential mineralized footprint from 700m to 5,500m.

President, CEO, and Director of Enduro Metals Cole Evans commented in a press release: “The company is in a fortunate position to be fully funded for its 2022 exploration program following the C$10m private placement undertaken in May. Burgundy represents a top-tier porphyry exploration target, and we are looking forward to a very exciting year with a greater understanding of the scale and significance of this mineralized system which shows many similarities to Galore Creek, some 35km to our northwest. While Burgundy is truly exciting, we must not forget that we have an excellent project in the McLymont Fault. The results of the recent geochemical sampling program suggest that we have a gold-rich project which has the size and scale needed to be economic in the Golden Triangle. I would like to extend our thanks to the entire field team whose combined efforts have allowed us to commence drilling earlier than ever before on the property despite the fact that the snow base has been substantially higher than average.”

At Burgundy Ridge, a two-rig diamond drill program has begun testing the extent of the copper and gold mineralization at the site along a 1,2000m strike length. The company is preparing multiple drill locations and the first drill has already commenced with the second rig ready to begin drilling soon. The Burgundy Ridge program is designed to zone in on the centre of the porphyry system. It will also test the mineralization deeper than previously drilled at the site since porphyries usually form as vertically oriented deposits up to many kilometres in vertical and horizontal scale.

At the McLymont Fault, Enduro is finalizing a detailed exploration program following up on the geochemical soil sampling program from 2021. It’s anticipated that one of the two rigs working at Burgundy Ridge will be moved to test the new zone and follow up on drill hole GSC88-1, which revealed 73.40g/t Au, 12.5g/t Ag, and 0.13% Cu over 0.60m in 1988. If this is successful, the project would expand the footprint of the McLymont Fault mineralized zone to 5,500 meters, comparable to other large bulk-tonnage gold deposits adjacent to Newmont Lake like KSM.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Nickel is one of the most important metals in the world, and the refined nickel supply and demand situation has a big impact on the market. Recently, two major players, Russia and China, have been able to control the market due to their large holdings of nickel.

The two heads of Norilsk in Russia and Tsignshan in China hold significant control of the refined nickel market. The past has seen nickel prices being artificially low due to oversupply from these two nickel companies. However, this is no longer the case as both companies have been cutting back on production. At the same time, the war in Ukraine has pushed the supply strain higher.

This has caused the refined nickel market to become much tighter, with prices now rising in response to the reduced supply. This has led to a situation where the market is even further controlled by these two large nickel companies.

At the same time, Tsignshan’s head, Xiang, initiated a big short bet on nickel in March. That trade sent nickel above $100,000 during the short squeeze. While other countries have attempted to control nickel prices and Russia has been sanctioned, there has been little change in the balance of power in this important market.

Australia and Canada both placed sanctions on Potanin, Russia’s richest man, who owns 37% of Norilsk. This has done little as the market reaction to the sanctions did not affect the company. The company has continued to sell its product and the nickel price has moved below $20,000 per tonne this week, the first drop below that level in 2022.

Broader actions on Russian nickel may have a further effect on the market, but for now, nothing has changed. The nickel market is small, marking only a little more than 2.2 million tonnes in all of 2021, but it is growing extremely quickly. Driving demand is the growing market for electric vehicles, as nickel is a key component in batteries. The rise of nickel demand has been so great that it has caused a massive increase in prices, with the metal more than quadrupling in price over the past two years.

Stainless steel demand is also growing, as nickel is a key component of stainless steel. This has driven prices even higher. The market may have seen a small correction since then with levels dropping below $20,000, but nickel prices are still very high by historical standards.

Battery-grade nickel is made into nickel sulphate and used in electric vehicle batteries. More than three-quarters of new nickel demand is coming from the battery sector as the world moves to electrify its vehicles. As this trend continues, the world’s biggest nickel players will continue to dominate a market that is increasingly becoming more important to the global economy.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The Lithium Americas Corporation (TSX:LAC) has announced the opening of its new Technical Development Center in Nevada. The new center was built to demonstrate the chemical process designed for the company’s Thacker Pass lithium project. Last month, initial production successfully produced 5 kg of battery-quality lithium carbonate. This is a major step forward for Lithium Americas, as it continues to move towards the production of its lithium carbonate product.

Lithium carbonate is a key ingredient in the production of lithium-ion batteries, which are used in a wide range of applications including electric vehicles, laptops, and cell phones. The new Technical Development Center will allow Lithium Americas to further optimize the process flowsheet for the Thacker Pass project and produce larger quantities of lithium carbonate product.

This is not the only U.S. initiative to advance battery metal tech for the supply chain. Ford and Rio Tinto (ASX:RIO) announced an initiative to build out a mining and battery metals supply chain for electric vehicles that could help the automaker secure supplies at a time when demand is expected to surge. The two companies will work together to develop battery minerals including lithium, cobalt, and nickel in the United States and around the world.

The official opening of the Lithium Technical Development Center marks the beginning of a new period of test work and production. The facility is 2800m2 and the company will use it to test new target ores and brines. The Center has a state-of-the-art analytical laboratory which can analyze ultra-pure lithium compounds. For the commercial work done at the facility, Lithium Americas will work with UNV Reno.

The processing facility is fully commissioned and operational, with state and federal permits already in place, and so the company will move ahead with planned construction on the Nevada lithium operation. Jonathan Evans, president and CEO of Lithium Americas stated: “As we prepare to break ground on Thacker Pass, we have never lost sight of our broader responsibility in developing the largest and most advanced new source of lithium in the U.S.”

Thacker Pass is moving toward the feasibility phase of the project with a target initial production capacity of 40,000 tonnes of lithium carbonate per year. The project will then move to a second stage expansion with an annual production capacity target of 80,000 tonnes. The second half of 2022 should see the release of feasibility study results from the project.

Highlights from the Lithium Technical Development Center are as follows:

- Official opening of Lithium Technical Development Center. Inauguration of the Company’s 30,000 ft2 lithium process testing facility in Reno, Nevada.

- Facility commissioned and operating as planned. Production commenced in June 2022 to replicate Thacker Pass’ flowsheet from raw ore to final product in an integrated process.

- Lithium carbonate samples achieve battery-quality. Facility achieving battery-quality specifications with product samples being produced for potential customers and partners.

- Early-works construction on track to commence in 2022. Federal appeal moving forward with briefings scheduled to be complete August 11, 2022, and oral arguments and a final decision expected shortly thereafter. The Company has all permits to commence construction. During construction, Thacker Pass is expected to employ over 1,000 workers.

- Process underway to appoint engineering construction contractor. The Company has issued a request for proposal (“RFP”) from short-listed engineering, procurement and construction management firms (“EPCM”) to perform detailed engineering, execution planning and manage Thacker Pass’ construction.

- Cultural assessment work was successfully completed in mid-July. Members of the Fort McDermitt Paiute and Shoshone Tribe (“Tribe”) were hired as cultural monitors to perform archeological mitigation work in collaboration with Far Western Anthropological Research Group.

- Completing carbon intensity and water utilization analysis. Analysis prepared with a leading international environmental engineering consulting firm indicates Scope 1 and Scope 2 carbon emission intensity per tonne of lithium carbonate produced from Thacker Pass’ process is expected to be competitive to South American-based brine operations and substantially lower than US and Australian-based spodumene operations.

- Continuing to advance Thacker Pass financing discussions. Formal application submitted to U.S. Department of Energy (“DOE”) in April 2022 through the Advanced Technology Vehicles Manufacturing (“ATVM”) loan program which is expected to fund the majority of Thacker Pass’ capital costs.

Source: Lithium Americas

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

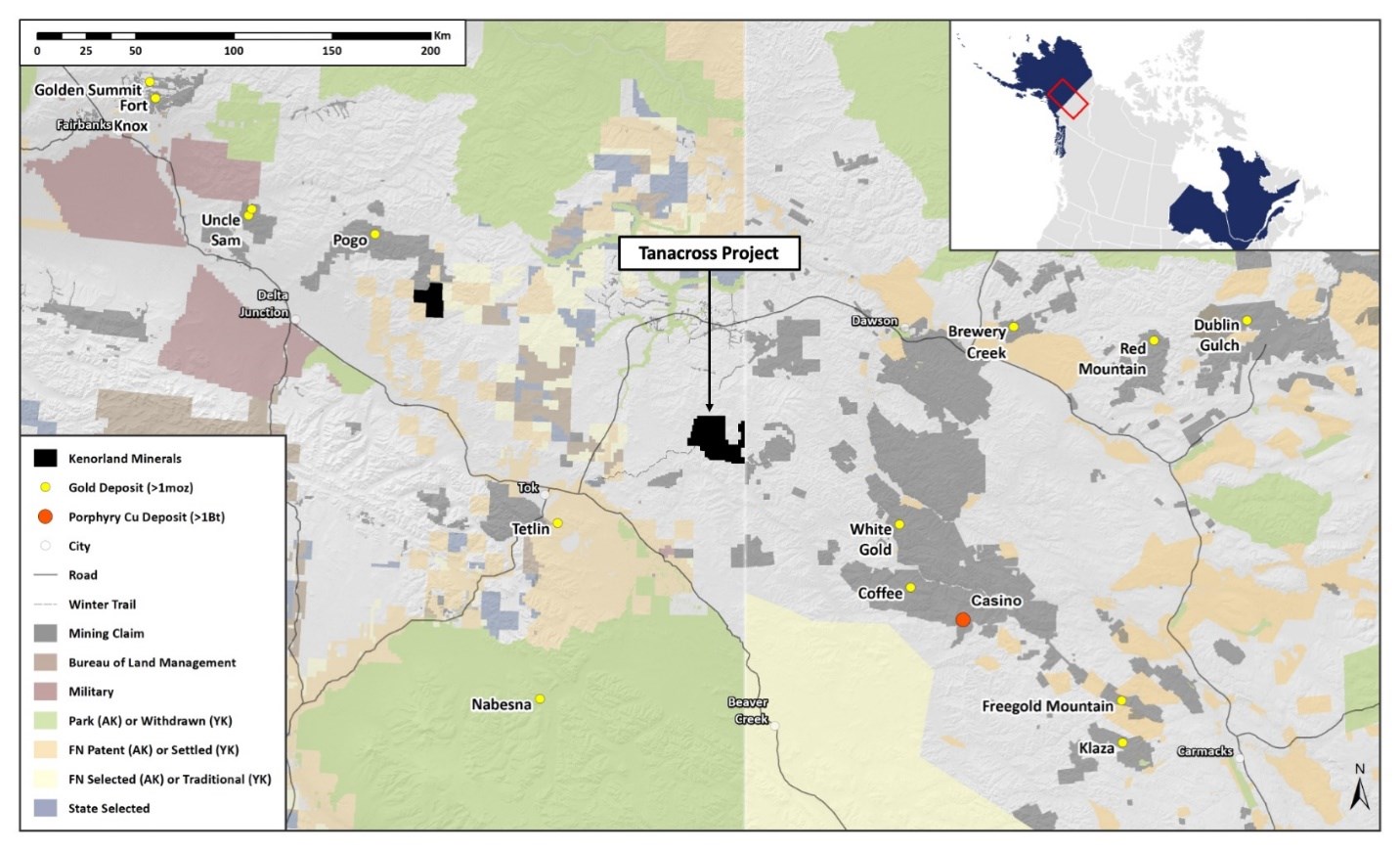

Kenorland Minerals (TSXV:KLD) has announced that an earn-in agreement with Antofagasta (LSE:ANTO) has been signed for the Tanacross copper-gold project in eastern Alaska. Antofagasta is granted the option to acquire a 70% interest in the Tanacross project by spending US$30,000,000 over 8 on exploration. As part of the agreement, the company will need to deliver a NI 43-101 compliant preliminary economic assessment report for the project.

The Tanacross project is 45,000 hectares of Alaskan state-owned land roughly 70 kilometres northeast of Tok. Located near the Alaska Highway, Tanacross hosts a cluster fo late Cretaceous porphyry coper occurrences. These are spread out across West Taurus, East Taurus, and Bluff. The region is known for similar systems, locating the project in an advantageous zone. Tanacross has already had 17,076 metres of drilling over 67 drill holes since 1971 when the initial discovery of East Taurus was made by the Duval Corporation.

Zach Flood, CEO of Kenorland, commented in a press release: “We’re very excited to be working with Antofagasta on the Tanacross Project. The property, which covers numerous mineralised systems and target areas, warrants significant exploration to unlock the discovery potential that we believe exists. We look forward to getting back on the ground as soon as possible to begin work which will lead towards drill-target definition.”

Agreement Terms

Antofagasta can earn a 70% interest in Tanacross by making cash payments in an aggregate amount of US$1,000,000 plus a success payment of US$4,000,000 upon exercise of the option and spending US$30,000,000 on exploration over eight years, with a firm commitment to spend US$1,000,000 in year one, and delivering the Report. During the option period, Antofagasta will fund all exploration and Kenorland will be the initial operator.

Once Antofagasta has earned its 70% interest, Kenorland and Antofagasta will form a 30:70 joint venture. If either party’s interest in the joint venture falls below 10%, that party’s interest will be converted to a 2% NSR, one quarter of which can be purchased by the other party for US$2,000,000.

Source: Kenorland Minerals

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

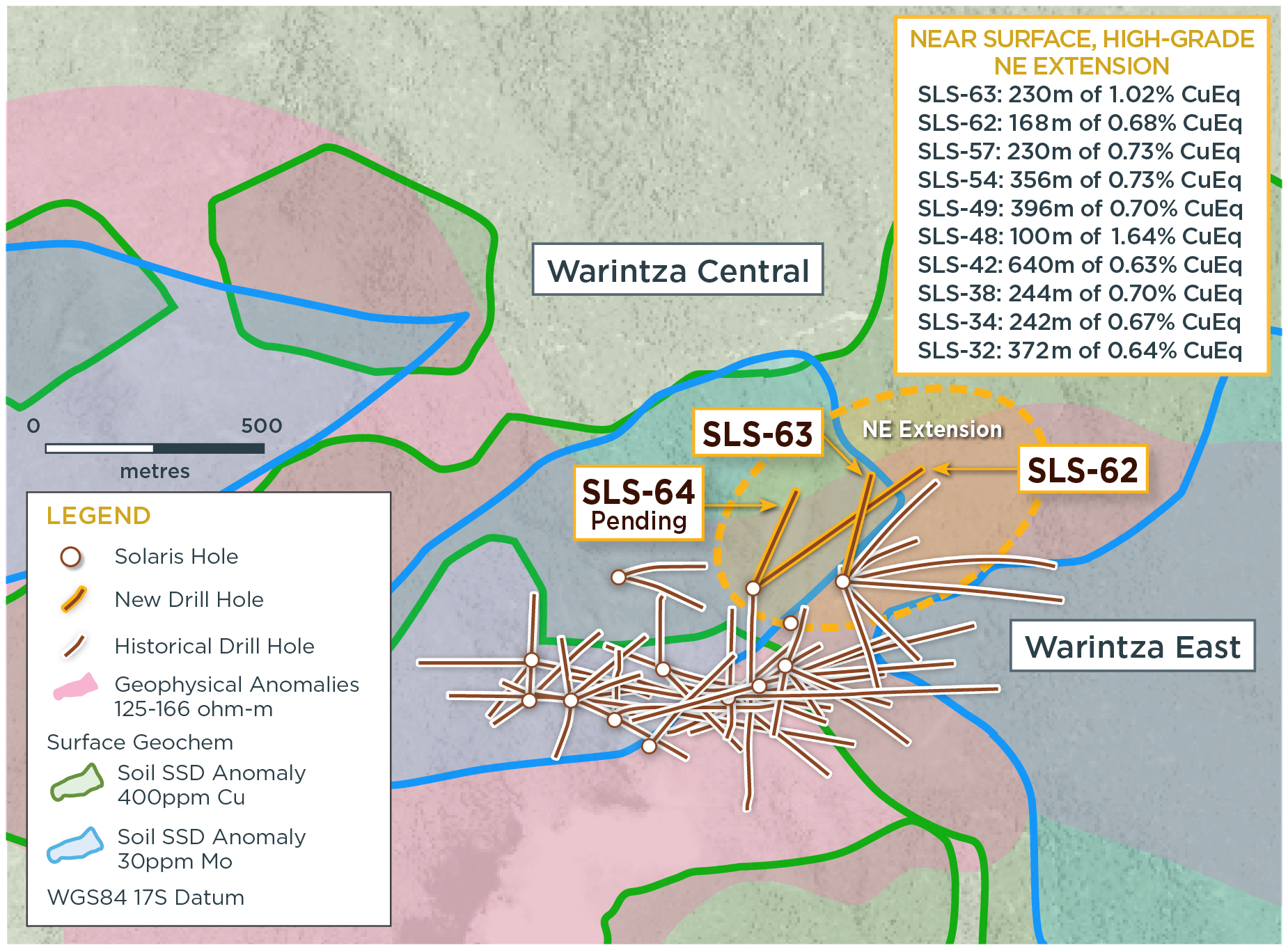

Solaris Resources (TSX:SLS) (OTCQB:SLSSF) has announced this morning new assay results from a series of holes aimed at growing the Northeast Extension of the “Indicative Starter pit” at the Warintza Project. The “Indicative Starter Pit” was noted in an April 18, 2022 announcement from the company in a mineral resource estimate for the Warintza Central Deposit, in which the company reported in-pit resources of 579 Mt at 0.59% CuEq (Ind) and 887 Mt at 0.47% CuEq (Inf), and 180 Mt at 0.82% CuEq (Ind) and 107 Mt at 0.73% CuEq (Inf) for the “Indicative Starter Pit”. The company has been targeting high-grade extensions and major growth in cluster at the project, with ongoing drilling focused on open extensions of near surface, high-grade mineralization to the northeast and southeast of Warintza Central.

Mr. Jorge Fierro, Vice President, Exploration, commented in a press release: “Ongoing drilling from existing and newly constructed platforms aims to expand on the Northeast Extension zone, which is one of the key target areas for the expansion of the ‘Indicative Starter Pit,’ along with higher grade, near surface mineralization being targeted at Warintza East, where results are pending.”

Highlights from the results are as follows:

Additional drilling has expanded the Northeast Extension of the ‘Indicative Starter Pit’ recently estimated at 180 Mt at 0.82% CuEq1 (Indicated) and 107 Mt at 0.73% CuEq1 (Inferred) within the Warintza Mineral Resource Estimate² (“MRE”). This zone is characterized by near surface, high-grade mineralization and remains open for further growth with follow-up and step-out drilling underway.

- SLS-62 was collared at the northern limit of Warintza Central and drilled northeast into an open volume, returning 168m of 0.68% CuEq¹ from 102m depth within a broader interval of 900m of 0.45% CuEq¹ from surface, expanding on prior drilling further to the east

- This hole represents the first follow-up to SLS-48, collared from the same pad but drilled to the south, which returned 100m of 1.64% CuEq³ from 50m depth within a broader interval of 852m of 0.56% CuEq³ (refer to press release dated Feb 28, 2022)

- SLS-63 was collared at the northeastern limit of the Warintza Central grid approximately 200m to the east and drilled into an open volume to the north-northeast, returning 230m of 1.02% CuEq¹ from 118m depth within a broader interval of 472m of 0.76% CuEq¹ from surface

- This hole follows on SLS-57, which was drilled northeast from the same pad, returning 230m of 0.73% CuEq¹ from 56m depth within a broader interval of 926m of 0.61% CuEq¹ from surface and SLS-54, drilled to the south and returning 356m of 0.73% CuEq³ from 50m depth within a broader interval of 1,093m of 0.56% CuEq³ from surface (refer to press releases dated May 26 and Apr 4, 2022)

- Follow-up drilling is underway and aims to test the Northeast Extension zone further to the north and northeast, with assays expected shortly for SLS-64, representing a follow-up hole from the same pad as SLS-62 and SLS-48

Table 1 – Assay Results

| Hole ID | Date Reported | From (m) | To (m) | Interval (m) | Cu (%) | Mo (%) | Au (g/t) | CuEq¹ (%) |

| SLS-63 | Jul 20, 2022 | 0 | 472 | 472 | 0.60 | 0.02 | 0.12 | 0.76 |

| Including | 118 | 348 | 230 | 0.87 | 0.02 | 0.12 | 1.02 | |

| SLS-62 | 10 | 910 | 900 | 0.33 | 0.02 | 0.07 | 0.45 | |

| Including | 102 | 270 | 168 | 0.51 | 0.03 | 0.07 | 0.68 |

Table 2 – Collar Location

| Hole ID | Easting | Northing | Elevation (m) | Depth (m) | Azimuth (degrees) | Dip (degrees) |

| SLS-63 | 800383 | 9648303 | 1412 | 498 | 17 | -61 |

| SLS-62 | 800178 | 9648285 | 1439 | 943 | 55 | -60 |

| Notes to table: The coordinates are in WGS84 17S Datum. | ||||||

Endnotes

- Copper-equivalence calculated as: CuEq (%) = Cu (%) + 4.0476 × Mo (%) + 0.487 × Au (g/t), utilizing metal prices of US$3.50/lb Cu, US$15.00/lb Mo, and US$1,500/oz Au, and assumes recoveries of 90% Cu, 85% Mo, and 70% Au based on preliminary metallurgical test work.

- Refer to Solaris press release dated April 18, 2022, stating updated Warintza Mineral Resource Estimate.

- Copper-equivalence calculated as: CuEq (%) = Cu (%) + 3.33 × Mo (%) + 0.73 × Au (g/t), utilizing metal prices of US$3.00/lb Cu, US$10.00/lb Mo, and US$1,500/oz Au. No adjustments were made for recovery prior to the updated Warintza Mineral Resource Estimate, as the metallurgical data to allow for estimation of recoveries was not yet available. Solaris defined CuEq for reporting purposes only.

Source: Solaris Resources

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Barrick Gold’s (TSX:ABX) proposed framework agreement with the Pakistani government over the Reko Diq copper-gold deposit to develop and bring it to production is nearing conclusion, the company says. Barrick plans to develop the project in phases, the first of which would include a plant with a capacity of 40 million tonnes per year. The company says that capacity has the potential to double within just five years. Reko Diq is located close to the borders of Iran and Afghanistan and is said to be one of the largest undeveloped deposits of copper-gold in the world. The Pakistani Government and the provincial government of Balochistan signed an agreement in principle with Barrick earlier in 2022 to restart the project.

All told, the project could cost $7 billion, with a $4 billion investment for the initial crush development, including a milling and flotation circuit. Barrick Gold has a 50% stake and is the planned project operator. Both governments will own a quarter of the project. Now, the definitive agreements that will underlie the framework agreement are being finalized, at which point the company can move forward with a feasibility study. Barrick Gold commented in a statement on the project: “Once this has been completed and the necessary legalization steps have been taken, Barrick will update the original feasibility study, a process expected to take two years. Construction of the first phase will follow that with the first production of copper and gold expected in 2027/2028.”

Once operational the operational life of the mine should be at least 40 years and is expected to create 7,500 jobs during the construction phase alone, plus 4,000 more long-term jobs once the project is commissioned.

New copper projects are rare, and one of this size could have a significant impact on the copper market. While commodity prices have temporarily pulled back in the wake of some market jitters, analysts say there is still plenty of room for copper prices to move higher. This is due to low supply, high demand, and a lack of new projects in the pipeline. This project aims to change that.

The expected production at Reko Diq would make it one of the world’s largest copper mines. It is also a very significant project for Pakistan, which has been trying to woo international investors and increase its mining output in an effort to boost growth and development. The country’s Prime Minister, Shehbaz Sharif, has made mining one of his government’s key priorities.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

GCM Mining (TSX:GCM) has announced production updates for the second quarter and first half of 2022 reflecting increased output from the same period a year ago. The company reported production of 16,370 ounces gold for June 2022 at the Segovia Operations to create a total of 53,198 ounces for 2Q2022 versus 52,198 ounces for the same quarter in 2021. 2Q2022 also saw silver production of 85,741 ounces silver, 294,000 pounds of zinc, and 345,000 pounds of lead.

GCM Mining’s first half of 2022 production was also higher than the same period in 2021. At the Segovia Operations, the company produced 103,149 ounces of gold, compared to 101,256 in the first half of 2021. Consolidated gold production in 2021’s first half was 103,684 including 2,428 ounces from the Marmato mine up to the date of the loss of control of Aris Gold Corporation on February 4, 2021. Trailing 12-months’ total gold production ended June 2022 totalled 208,282 ounces, approximately 1% more than the previous year. GCM has stated that it is currently on track to meet the 2022 production guidance of 210,000 to 225,000 ounces of gold this year. The completion of the Maria Dama plant extension will aid this goal by adding 2,000 tonnes per day of capacity sometime in the third quarter of 2022.

The plant is the cornerstone of its operations, processing 44,047 tonnes in June 2022 alone, with a daily average processing rate of 1,468 tpd at an average head grade of 12.8 g/t. Operations at the plant in June also reflected a scheduled 120-hour stoppage to change the linings of the mill on top of the company’s routine repairs and improvements.

With the operational update, GCM Mining also declared its next monthly dividend slated for August 15, 2022, which will be paid to all shareholders of record as of the close of business on July 29, 2022. The Board of Directors for the company approved a dividend of CA$0.015 per common share to be paid on that date.

Other highlights from the Segovia Operations update include:

For the second quarter of 2022, a total of 147,580 tonnes, equivalent to 1,622 tpd, were processed at Segovia at an average head grade of 12.4 g/t compared with a total of 143,910 tonnes, equivalent to 1,581 tpd, at an average head grade of 12.6 g/t in the second quarter last year. This brings the daily average processing rate for the first half of 2022 to 1,604 tpd at an average head grade of 12.3 g/t compared with 1,526 tpd and 12.7 g/t in the first half last year.

The Company’s polymetallic plant at Segovia processed an average of approximately 97 tpd of tailings in the first half of 2022 resulting in the production of approximately 645 tonnes of zinc concentrate and approximately 547 tonnes of lead concentrate which have been stockpiled and are expected to start shipping in the next few weeks under an offtake agreement with an international customer that was executed in June. Payable production from the concentrates in the first half of 2022 is estimated to total approximately 546,000 pounds of zinc, 683,000 pounds of lead, approximately 57,600 ounces of silver and approximately 200 ounces of gold. Actual payable quantities are subject to change and will be finalized once the concentrates are shipped.

Source: GCM Mining

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

While some analysts continue to lean bearish when it comes to gold lately, Goldman Sachs is not one of them. In fact, they’ve recently raised their year-end gold price target to $2500/oz, signalling a strong finish to the year for the precious metal.

This latest move comes after gold prices ended 2021 down approximately 4% despite a strong economic recovery and growth throughout the year. Many investors moved towards riskier assets, but concerns of a potential US recession in the coming year could lead to increased demand for gold.

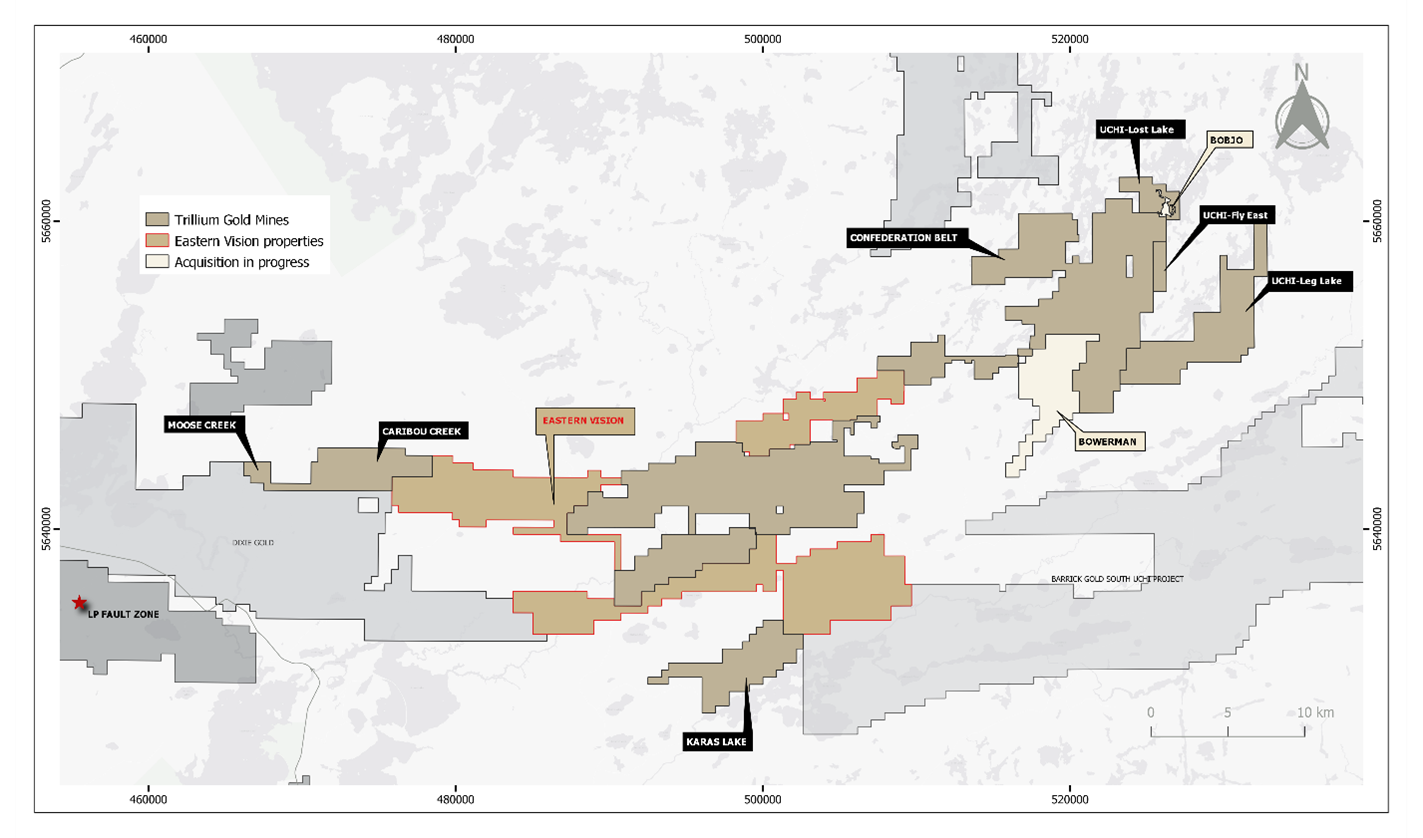

Mining companies will also benefit from a higher gold price, with more attention swinging to companies in the industry as gold becomes more valuable. Trillium Gold Mines (TSXV:TGM) is a Canadian gold exploration company with highly prospective properties in the Red Lake Mining District, Ontario. The company recently announced that it had closed the acquisition of the Eastern Vision property holdings in the Confederation Lake assemblage, acquired from Imagine Lithium.

The total land package is 13,958 hectares between the Fredart, Confederation North and Confederation South properties. Trillium Gold now has a dominant contiguous land package over more than 100 kilometres of favourable structure on trend with Kinross Gold’s Great Bear Project and Evolution Mining’s Red Lake Mine. The company has built a dominant land position in the Red Lake Mining District when asset values have continued to climb, and future gold prices could be set to move far higher.

The strong recovery in 2021 meant that gold prices slumped for some time, losing some of the momentum gained in the first year of the pandemic. Investors moved to riskier assets as the vaccine rollout continued and economies reopened.

However, the coming year has investors worried about a recession, which would lead to higher gold prices if the case. The other side of this dynamic is a rising inflation rate that has consumers, investors, and central banks concerned. Goldman Sachs believes those fears are exaggerated and that inflation will ultimately remain contained.

Risk appetite is often influenced by several global factors that can be difficult to predict. One of them is the strength of the jobs market in the United States.

Currently, the US job market is looking strong with unemployment at a pandemic low. This has been the case for some time now, showing strength in the real economy. At the same time, asset prices have taken quite a haircut, spooking some investors into safer havens, including gold. The other ongoing risk is the Russian invasion of Ukraine, which has created supply chain issues inflating food and energy prices, and presenting significant challenges for the European bloc and North America.

Russia is a major exporter of food and commodities, so the situation is especially being scrutinized by those in the industry. A new plan to contain some of the risks of the sanctions placed on the Russian economy may not protect the U.S. or Canadian economies in perpetuity, and that has sparked a selloff in equities, trimming gains from 2021.

If the slide continues, or buyers prove apathetic to ease some of the pressure, investors will assuredly turn their attention to gold and particularly those gold mining companies with assets that offer discovery and development potential.

Overall, Goldman Sachs’ bullish stance on gold is predicated on global factors that continue to generate uncertainty. With a higher gold price target, mining companies are poised to benefit from growing attention and investment. Trillium Gold Mines is one company that is ideally positioned to benefit from a higher gold price.

The stock has sold off with a range of other mining stocks and may present a compelling buying opportunity for deep value investors with a keen eye. And even as the share price has drifted precipitously from its two-year highs, the company has forged ahead in consolidating strategic holdings under the radar; a sign that investors may not be seeing the whole picture yet.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Trillium Gold Mines (TSXV:TGM) has announced that it has closed the previously announced acquisition of Imagine Lithium’s Eastern Vision property holdings in the Confederation Lake assemblage. The properties lie within the Birch-Uchi greenstone belt in the Red Lake Mining District where Kinross’ Dixie Deposit is located.

Some of the properties have been acquired directly and the company has assumed option agreements as optionee for others. Trillium Gold’s total land package covers 13,958 hectares between the Fredart, Confederation North and Confederation South properties. The company now has control over a significant portion of the Confederation Lake assemblage, creating a contiguous land package over greater than 100km of favourable structures on trend with Kinross Gold’s Dixie Deposit and Evolution Mining’s Red Lake Operation.

Transaction Details

As part of the transaction, Trillium Gold issued 2,800,000 common shares in the capital of the Company together with a cash payment of $175,000 to Imagine Lithium. In addition, the Company has agreed to assume Imagine Lithium’s cash payment commitments under its existing option agreements, while Imagine Lithium retains its original share issuance obligations.

Concurrent with the closing, Trillium Gold paid $20,000 in cash to Pegasus Resources Inc. (“Pegasus”), together with 100,000 common shares in the capital of the Company, to earn into certain option agreements that Trillium has agreed to assume as optionee from Imagine Lithium. The cash consideration represented the remaining option payments under said option agreements, while the equity consideration purchased Pegasus’ carried interest in the relevant properties such that 100% of those properties are now held by Trillium Gold.

Pursuant to the remaining option agreements that it is assuming as optionee, Trillium Gold must pay a total of $186,000 in option payments over approximately two years in order to earn in to and exercise the options.

Also concurrent with the closing, Trillium Gold purchased a 2.0% NSR royalty on the Fredart property from prospector Perry English in consideration for the issuance of 60,000 common shares in the capital of the Company and $50,000 in cash.

Source: Trillium Gold Mines

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Ganfeng Lithium, China’s largest lithium compounds producer, has announced it is buying Lithea Inc. for up to $962 million. Lithea’s Argentina-focused property portfolio which includes the rights to two lithium salt lakes in the mineral-rich Salta province will help Ganfeng secure access to lithium and more resources for battery metal production. Lithea Inc. is privately owned.

Securing lithium resources has become a priority for China’s top producer, but also for the country as a whole. As worries about electric vehicle battery supply chains grow, Beijing has been stockpiling the metal and investing in mines and chemical plants around the world. China consumes about two-thirds of the world’s lithium, according to estimates. It is also expected to be a major competitive player in the electric vehicle market, beginning with a strong domestic market.

Argentina is one of the countries included in what is called the “lithium triangle”, and is looking to attract more foreign investors through accessible mining infrastructure and favourable tax cuts. However, the country is not without its risks as political instability in Latin America can be a deterrent to some companies.

Ganfeng’s move is the latest in a series of acquisitions by Chinese firms looking to gain a foothold in Argentina’s growing lithium industry. From the western hemisphere, U.S.-based Lithium Americas Corp. has a lithium project in the same area as Lithea’s, and Rio Tinto (ASX:RIO) has announced that it will buy the Rincon lithium project in the same Salta province for $825 million. Rio Tinto has also begun to build its battery materials division, investing in new projects and preparing for a future where demand remains high for these minerals and metals.

Lithium prices have risen even while production has increased. In 2021, lithium products increased 21%, mainly from the demand for industry-standard lithium-ion batteries. According to the U.S. Geological Survey, this increase can be attributed to these batteries which are used in electric vehicles and energy storage systems, as well as consumer electronics.

As the world moves away from fossil fuels and towards renewable energy sources, demand for lithium is only expected to increase. Companies like Ganfeng Lithium are positioning themselves to be at the forefront of this transition.

The battle is also playing out on a geopolitical level, as countries jockey for position in a market that is expected to be worth hundreds of billions of dollars. The United States has put forth a plan to secure the electric vehicle battery supply chain and has been investing in domestic mines and chemical plants. Japan and South Korea, two other major players in the industry, have also been working to increase their share of the lithium market.

Major automakers and EV-focused companies like Tesla have noted the dire need for more lithium, and Tesla has not ruled out building or buying its own mines and chemical plants.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

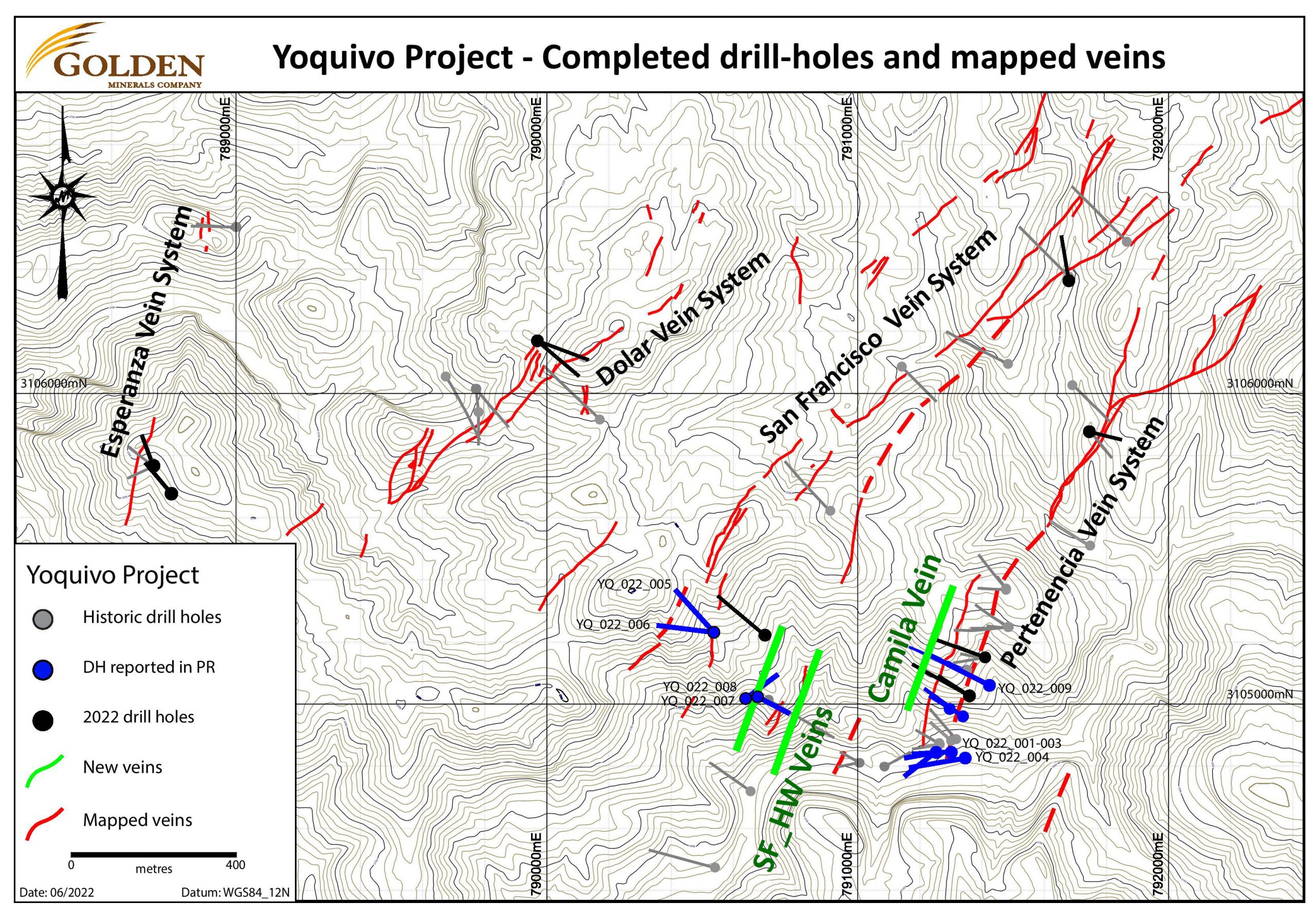

Golden Minerals (TSX:AUMN) has announced new results from the first nine holes in the third drill program being conducted at its Yoquivo gold-silver project in northwest Chihuahua state, Mexico. The 2022 drill program began back in May 2022 and a total of 17 holes of 4,033 metres have been drilled to-date. This is following up on high-grade intercepts reported during Golden Minerals’ 2021 drill activity, and to drill several new holes to explore other vein systems on the property.

Warren Rehn, President and Chief Executive Officer of Golden Minerals commented in a press release: “This most recent drilling has focused on testing the Pertenencia vein system to extend the known mineralized strike length into previously untested areas. The Pertenencia vein has continued to return strong gold-silver grades, and the vein remains open to depth and to the north. The discovery of multiple, previously unknown, high-grade gold-silver structures, particularly the Camila vein, demonstrates that there is also significant potential at Yoquivo to discover additional high-grade structures on the property. The current drill program is expected to allow us to report an initial gold-silver resource on the property later this year.”

Highlights from the drill results are as follows:

- 2.2m @ 10.21 g/t Au and 138.8 g/t Ag

- 0.4m @ 30.80 g/t Au and 5260.0 g/t Ag

- 4.2m @ 0.16 g/t Au and 229.2 g/t Ag

- 80.1m @ 0.89 g/t Au and 64.5 g/t Ag

- 1.7m @ 0.13 g/t Au, 354.6 g/t Ag

Significant results are summarized in the table below, with complete results available on the Company website.

| Hole ID | From (m) | To (m) | Interval (m) | True Width (m) | Au g/t | Ag g/t | Target |

| YQ_022_001 | No Significant results | ||||||

| YQ_022_002 | 49.3 | 50.3 | 1.0 | 0.8 | 1.82 | 297.0 | Tajitos Vein |

| YQ_022_003 | 71.9 | 73.2 | 1.3 | 1.1 | 1.03 | 219.8 | Tajitos Vein |

| YQ_022_004 | 154.9 | 155.2 | 0.3 | 0.3 | 0.59 | 131.0 | Pertenencia Vein |

| YQ_022_004 | 163.4 | 163.7 | 0.3 | 0.2 | 0.91 | 112.0 | Pertenencia Vein |

| YQ_022_005 | 9.0 | 10.3 | 1.3 | 1.1 | 0.09 | 214.0 | SF Vein |

| YQ_022_005 | 232.5 | 233.3 | 0.8 | 0.69 | 180.3 | SF_FW Vein # 1 | |

| YQ_022_006 | 6.6 | 10.8 | 4.2 | 3.7 | 0.16 | 229.2 | SF Vein |

| YQ_022_006 | 199.0 | 200.3 | 1.3 | 0.55 | 189.0 | SF_FW Vein # 1 | |

| YQ_022_007 | 69.1 | 70.8 | 1.7 | 2.09 | 10.0 | New Vein | |

| including | 70.6 | 70.8 | 0.2 | 16.90 | 57.2 | New Vein | |

| YQ_022_008 | 47.2 | 47.9 | 0.8 | 0.6 | 0.20 | 128.0 | San Francisco HW # 1 |

| YQ_022_008 | 141.5 | 141.9 | 0.4 | 0.3 | 30.80 | 5260.0 | San Francisco HW # 2 |

| YQ_022_008 | 153.2 | 157.3 | 4.1 | 3.3 | 0.44 | 103.1 | San Francisco HW # 3 |

| YQ_022_009 | 128.7 | 130.4 | 1.7 | 1.4 | 0.13 | 354.6 | Pertenencia Vein |

| including | 128.7 | 129.0 | 0.3 | 0.2 | 0.51 | 1735.0 | Pertenencia Vein |

| YQ_022_009 | 225.9 | 306.0 | 80.1 | 0.89 | 64.5 | Vein Stockwork Zone | |

| including | 231.9 | 237.4 | 5.5 | 4.7 | 0.67 | 130.7 | Pert FW Vein |

| including | 281.3 | 290.7 | 9.5 | 8.2 | 3.93 | 120.0 | Camila Vein |

| which also includes | 284.6 | 286.8 | 2.2 | 2.0 | 10.21 | 138.8 | Camila Vein |

Drill hole collar location table:

| Hole ID | Easting | Northing | Elevation (m) | Azimuth | Inclination | Length (m) |

| YQ_022_001 | 791250 | 3104845 | 1996 | 260 | -45 | 180 |

| YQ_022_002 | 791250 | 3104845 | 1996 | 232 | -45 | 180 |

| YQ_022_003 | 791300 | 3104848 | 2001 | 265 | -46 | 261 |

| YQ_022_004 | 791350 | 3104825 | 2007 | 259 | -45 | 265 |

| YQ_022_005 | 790538 | 3105230 | 2214 | 278 | -46 | 261 |

| YQ_022_006 | 790537 | 3105231 | 2214 | 318 | -45 | 175 |

| YQ_022_007 | 790641 | 3105023 | 2116 | 53 | -44 | 162 |

| YQ_022_008 | 790681 | 3105026 | 2122 | 118 | -45 | 306 |

| YQ_022_009 | 791422 | 3105230 | 2115 | 296 | -46 | 143 |

Coordinates are in WGS84 datum, zone 12N

Source: Golden Minerals

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

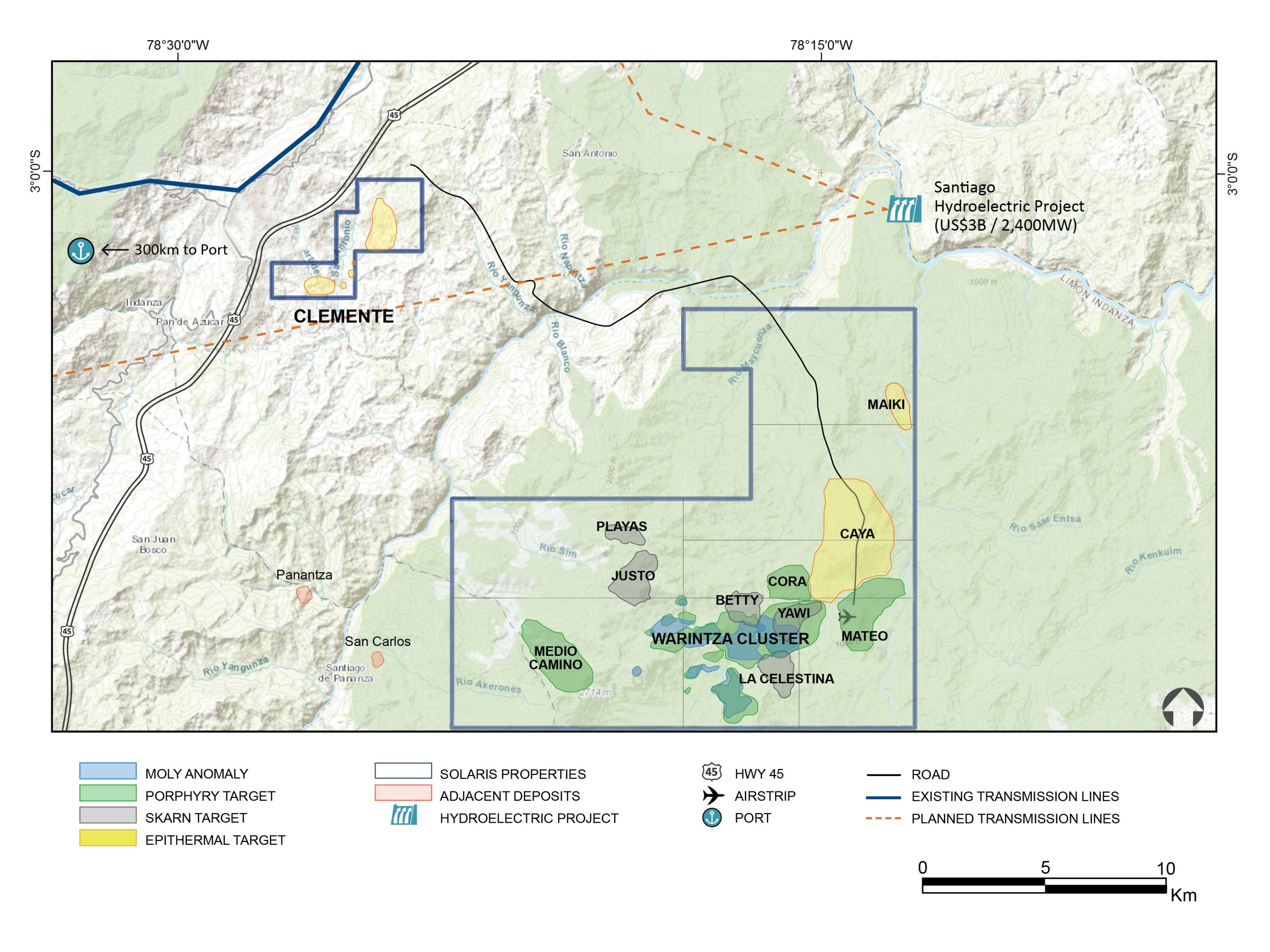

Solaris Resources (TSX:SLS) has provided an update for the Warintza Project in southeastern Ecuador, and announced that it has identified a number of new targets for further exploration in the support of the drill program. The company also provided a report on the progress of the proposed asset spin-out to create Solaris Exploration Inc. Ecuador’s recent protests concluded on June 30, and the company’s samples have now been able to flow from the core processing facility to the prep lab, which has resumed operations. The samples are continuing on for final assays in Lima, Peru, although there is a considerable backlog of assays still pending.

The company is continuing its regional exploration program and identified new porphyry, skarn, and epithermal targets. A large high sulphidation epithermal target was identified adjacent to the Warintza porphyry cluster where overlapping mineralized porphyries have intruded a layered sequence of carbonate and volcanic rocks. This has given the mineralization a very fertile setting to be able to develop.

Solaris also provided an update of the proposed Solaris Exploration spin-out, and when completed, it is expected that 100% of the common shares of Solaris Exploration will be spun out to shareholders of Solaris relative to their current shareholdings. Details of the corporate update are as follows:

Corporate Update on Proposed Solaris Exploration Spin-Out

Solaris continues to advance the proposed spin-out and has made considerable progress with the internal re-organization of the Company, its subsidiaries and mineral concessions including the transfer of its non-core assets held in Ecuador outside of the Warintza porphyry cluster (involving the authorization of the Ministry of Energy and Mines), Peru, Chile and Mexico into a newly incorporated wholly-owned subsidiary of Solaris named Solaris Exploration Inc. Following the internal re-organization, it is expected that 100% of the common shares of Solaris Exploration Inc. will be spun out to shareholders of Solaris relative to their shareholdings (refer to press release dated December 6, 2021).

Source: Solaris Resources

A full update from Warintza and the regional exploration program is as follows:

Warintza Update

Exploration activities at the Warintza Project continue with seven drill rigs targeting high value growth of the recently reported Warintza Mineral Resource Estimate (refer to press release dated April 18, 2022), with drilling at Warintza Central targeting extensions to near surface, high-grade mineralization, and major growth targeted from the expansion of drill coverage at Warintza East within a largely undrilled footprint. With the protests in Ecuador having concluded on June 30, the flow of samples from the Company’s core processing facility to its prep lab, which has now resumed operations, and onward for final assay in Lima has restarted, with a considerable backlog of assays pending.

Regional Exploration Update

Solaris has undertaken the first significant program of regional exploration at Warintza since the original stream sediment sampling program that identified the Warintza porphyry cluster in the 1990s. This work has identified additional porphyry targets (refer to Figure 1), potentially expanding the footprint of the cluster to the northeast, and possibly a new area of porphyry emplacement to the west, approximately halfway to the adjacent San Carlos copper porphyry deposit.

In addition, this work has established a series of skarn targets, as well as a large high sulphidation epithermal target adjacent to the Warintza porphyry cluster where overlapping mineralized porphyries have intruded a layered sequence of carbonate and volcanic rocks that have provided a fertile setting to develop these styles of mineralization.

Porphyry Targets:

- Mateo: 3km x 1.4km area of copper-molybdenum enrichment in soil samples located approximately 5km to the east of Warintza East. A program of detailed mapping and sampling is underway to refine the target in support of drilling.

- Cora: 1.2km x 1.4km copper-molybdenum-gold soil anomaly in andesitic volcanic sequences cut by porphyry dikes approximately 3km to the northeast of Warintza East. This anomaly resembles those that defined the Warintza East and Warintza South discoveries. Detailed mapping and sampling are planned to refine the target in support of drilling.

- Medio Camino: 3.5km x 1.5km area of porphyry-related alteration, and copper-molybdenum veining 5km to the west of Warintza West and 7km east of the adjacent San Carlos copper porphyry deposit. An extensive program of soil and rock chip sampling has been completed to refine the large target area, with results pending.

Skarn Targets:

Five skarn targets have been identified with three of these forming a partial arc on the northeastern side of the Warintza porphyry cluster, which is typical of skarn mineralization related to porphyry systems.

- Playas and Justo: Extensive mineral alteration typical of skarn systems has been identified in an area of copper mineralization concentrated in a permeable horizon 3.5km northwest of Warintza West. Soil sampling of the 10km2 area surrounding the Justo target has been completed in an effort to refine the target, with results pending. Soil sampling is also planned at the Playas target, along with detailed mapping at both targets based on the results of soil sampling.

- Betty and Yawi: Betty, a 1.2km x 1.4km skarn and potential carbonate replacement target located 0.5km north of Warintza Central, features significant copper values in rock samples in carbonate horizons within volcano-sedimentary sequences. Within the Yawi target, a 2km x 1km skarn/carbonate replacement target features strongly anomalous zinc values in limited soil sampling within a high conductivity anomaly interpreted from ZTEM. Additional soil sampling is planned at both targets.

- La Celestina: Marble exposed in streams in this 1.7km x 1.2km area host copper-zinc veinlets that may represent leakage from a mineralized zone below, with soil geochemistry showing enrichment of pathfinder elements and anomalous copper. Two windows of garnet-bearing skarn containing copper mineralization are exposed through the marble. Detailed mapping and sampling of marble and exposed skarn are underway to help define drill targets.

High Sulphidation Epithermal Gold Target

- Caya: Large 5km x 3km gold anomaly in stream sediments, 6km to the northeast of Warintza East, where recent follow-up soil and rock sampling in the southern part of the anomaly has identified a flat-lying volcano-sedimentary layer that has a high permeability over at least 300m in thickness. In this portion of the anomaly, an area of 0.7km x 1.3km features anomalous gold, copper and pathfinder element values in soil and rock samples, and a concentration of dickite clay and vuggy silica, characteristic of high sulphidation systems.

Figure 1 – Regional Map of Solaris Land Package in Ecuador

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Honey Badger Silver (TSXV:TUF) announced on June 10, 2022, that it had entered into a non-binding term sheet to acquire a 100% interest in the Cachinal De La Sierra Silver-Gold Project from Aftermath Silver Ltd. The Cachinal Project is located in the Cachinal de la Sierra areas in the Antofagasta region of Chile. The proposed transaction includes an exclusivity period that ends on August 15, 2022, and the companies are working to finalize a definitive agreement on or before this date.

Chad Williams, Director and Non-Executive Chair of Honey Badger Silver, commented in a press release: “We are very pleased to announce a further accretive addition to our growing portfolio of silver assets. Cachinal is a significant known silver resource located in a favorable jurisdiction. Moreover, its proximity to Austral’s Guanaco mine and mill complex may offer substantial synergies to advancing Cachinal to production in a timely manner. We believe Cachinal will be transformational for Honey Badger. We were also greatly encouraged and inspired by a recent speech delivered by H.E. Gabriel Boric, President of the Republic of Chile, at an event hosted by the Canadian Council for the Americas. During this event, Mr. Boric strongly signalled his commitment to property rights, and the rule of law in addition to welcoming direct foreign investment. Chile’s long-standing partnership with Canada to generate economic growth and jobs for all was reiterated in meetings with Prime Minister Trudeau during his visit.”

Cachinal Project Highlights

- Open-pit Indicated Resource of 15.03 Moz of silver grading 97 g/t of silver and 20.05Koz of gold grading 0.13 g/t gold;

- Open-pit Inferred Resource of 0.41 Moz of silver grading 73 g/t of silver and 0.43Koz of gold grading 0.07 g/t gold;

- Underground Indicated Resource of 1.29 Moz of silver grading 182 g/t of silver and 1.65Koz of gold grading 0.22 g/t gold;

- Underground Inferred Resource of 2.07 Moz of silver grading 180 g/t of silver and 2.18Koz of gold grading 0.19 g/t gold;

- Proximity to Austral Gold Limited’s (“Austral Gold”) operating Guanaco Mine and Mill complex, located just 16 km to the south;

- Good potential to confirm and incrementally expand existing resources and discover additional mineralization on the property and in the region.

The mineral resource was independently prepared by SRK Consulting (Canada) Inc. in a technical report filed on Aftermath’s SEDAR profile at www.sedar.com, with an effective date of August 10, 2020 and prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators (“NI 43-101”).

Transaction Summary

The Term Sheet contemplates that Honey Badger or an affiliate will acquire all of the issued and outstanding shares of Minera Cachinal S.A., a wholly-owned subsidiary of Aftermath, according to the following terms:

- Share Payment: C$1,000,000 in shares of Honey Badger payable at closing and priced at the greater of: (i) the volume weighted average share price of the Honey Badger common shares on the TSXV for a period of thirty (30) trading days immediately preceding the date of announcement of the transaction and (ii) the maximum discounted price allowed under the policies of the TSXV.

- Cash Payments: a) C$400,000 payable at closing, b) C$452,000 six months after closing, c) C$400,000 on May 21, 2023 and d) C$400,000 eighteen months after closing.

- Royalty: Honey Badger shall grant a 1% Net Smelter Return Royalty with a complete buyback option at Honey Badger’s sole discretion for a purchase price of C$8,500,000;

- Production Payments: Upon commencement of commercial production, Honey Badger shall pay in cash or shares at Aftermath’s option, C$0.50 per payable silver ounce produced at the Cachinal Project, capped at C$2,000,000 in payments.

The detailed terms and conditions of the proposed transaction will be set out in definitive documentation to be negotiated between the parties, which will contain customary representations, warranties and covenants of the parties as well as customary indemnities and closing conditions. There can be no assurance that the proposed transaction will be completed on the terms contemplated, or at all. Readers are referred to the section below entitled: “Cautionary Note Regarding Forward-Looking Information”.

While the Term Sheet is non-binding, the parties have agreed to a mutual break fee of C$250,000 in the event a definitive agreement is not entered into prior to the expiry of the exclusivity period due to a party’s action or inaction, subject to certain exceptions outside the control of the parties. The proposed transaction will be subject to regulatory approval, including the approval of the TSX Venture Exchange (the “TSXV”).

Cachinal Asset Overview

Cachinal is a low-sulphidation epithermal deposit located in the Paleocene Gold Belt of northern Chile, which hosts several significant gold and silver deposits, including Yamana Gold’s El Penon Low Sulfidation Epithermal gold–silver mine and Austral Gold’s Guanaco gold-silver mine-complex, just 16 kilometers to the south. Shallow drilling at Cachinal has defined the current mineral resources principally to a depth of 150 metres below surface and provides sufficient evidence to interpret the presence of high-grade shoots within the vein system extending below the base of a potential open pit.

Cachinal Location

The Cachinal silver-gold project is located in Chile’s Antofagasta region (Region II). The project is located about 40 km east of the Pan American Highway, in a nearly flat plain at an elevation of around 2,700 metres above sea level, 16 km north of Austral Gold’s Guanaco gold-silver mine and mill complex.

Cachinal NI 43-101 Resource Estimate

The Cachinal Mineral Resource was documented in a technical report prepared following the guidelines of NI 43-101 and Form 43-101F1, and in conformity with the generally accepted CIM “Estimation of Mineral Resources and Mineral Reserves Best Practice Guidelines” (2019) by SRK Consulting (Canada) Inc., authored by independent qualified persons Glen Cole, P.Geo of SRK Consulting, and Sergio Alvarado Casas, CMC of Geoinvest SAC E.I.R.L. (Chile), on behalf of Aftermath Silver Ltd., with an effective date of August 10, 2020.

| RESOURCE CLASSIFICATION |

MATERIAL TYPE | TONNES (MT) |

SILVER (G/T) |

GOLD (G/T) |

SILVER (MOZ) |

GOLD (KOZ) |

| Indicated | Open Pit | 4.83 | 97 | 0.13 | 15.03 | 20.05 |

| Underground | 0.22 | 182 | 0.22 | 1.29 | 1.65 | |

| TOTAL | 5.05 | 101 | 0.13 | 16.32 | 21.70 | |

| Inferred | Open Pit | 0.17 | 73 | 0.07 | 0.41 | 0.43 |

| Underground | 0.36 | 180 | 0.19 | 2.07 | 2.18 | |

| TOTAL | 0.53 | 145 | 0.15 | 2.48 | 2.61 |

Notes on the Cachinal Mineral Resource Estimate:

- For complete details on the Cachinal Mineral Resource estimate, please refer to the NI 43-101 technical report titled “Independent Technical Report for the Cachinal Silver-Gold Project, Region II, Chile”, by Qualified Persons G. Cole, (P.Geo) of SRK Consulting (Canada) Inc. and S. Alvarado Casas, of Geoinvest SAC E.I.R.L. (Chile), dated September 11, 2020 with an effective date of August 10, 2020, filed on the Aftermath Silver SEDAR profile.

- Cachinal mineral resources were classified according to the CIM Definition Standards for Mineral Resources and Mineral Reserves (May 2014).

- Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

- All figures have been rounded to reflect the relative accuracy of the estimates.

- Cut-off grades are based on metal price assumptions of US$22.00 / ounce of silver and US$1,550 / ounce of gold, and metallurgical recoveries of 85% for both silver and gold using milling and cyanide leaching.

- The portion of the Mineral Resources that has been determined to be amenable to extraction through open-pit methods was reported to a cut-off of 30 g/t silver equivalent.

- The open-pit Mineral Resource is constrained within Lerchs-Grossman optimised pit shells that assume mining dilution & losses of 2.5%, 50-degree overall slope angles, mining costs of $2/t rock, general and administrative costs of $2/t rock, processing costs of US$15/t for processing using milling and cyanide leaching.

- The portion of the Mineral Resources deemed to be amenable to extraction through underground methods are reported at a cut-off of 150 g/t silver equivalent. This assumes a mining cost of US$90/t, general and administrative costs of $2/t and a processing costs of US$15/t.

Past Work at Cachinal

The Cachinal deposit was mined from underground workings during the 20th century. Drilling by previous owners of the project since 2005 has delineated near-surface silver mineralization associated with a network of steeply dipping, north-to-northwest trending low-sulphide quartz veins.

The epithermal veins and breccias have been recognized by trenching and drilling over a strike length of at least 2 kilometers and are known to have been mined to a depth of at least 300 meters. They range in thickness from a few centimetres to 2 meters, reaching up to 20 meters locally at the intersection of two structures. The main veins trend north-northwest and northwest with a secondary set trending east-northeast to east-west, best developed at the southern end of the deposit.

Technical information in this news release has been approved by Glen Cole, P.Geo., a Principal Consultant (Resource Geology) with SRK Consulting (Canada) Inc. and qualified person for the purposes of National Instrument 43-101.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

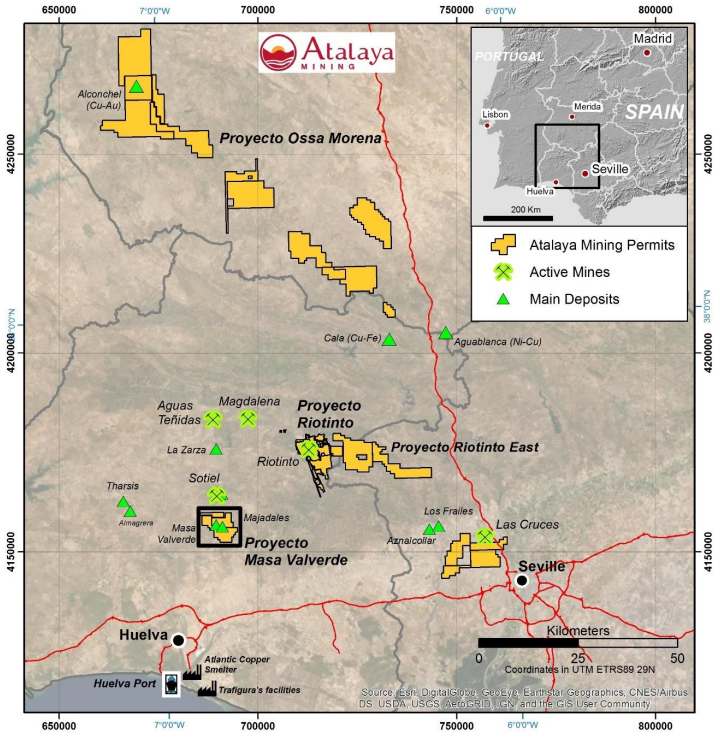

Atalaya Mining (TSX:AYM) has announced results from the first 22 exploration drill holes completed to date at the Campanario Trend. This is one of several mineralized zones comprising Proyecto Masa Valverde, located in Southern Spain. It is roughly 28 kilometres south of Atalaya’s 15 Mtpa mill at Proyecto Riotinto.

CEO of Atalaya Mining Alberto Lavandeira commented in a press release: “We are pleased with these initial drilling results from the Campanario Trend which confirm the expectations we had on the exploration potential of PMV. We continue working on defining the potential shallow mineral resource in the short term which to date has only been drill tested in approximately 10% of the entire mineralised structure. In addition, we have several coincident geochemical and geophysical targets pending for drill testing indicating that we are still far from knowing the ultimate exploration potential of PMV. We believe that these initial results will not only have a positive impact on future development scenarios and project economics, but they also highlight the significant exploration potential of the Iberian Pyrite Belt.”

Figure 1: Proyecto Masa Valverde Location

Highlights from the drill results are as follows:

- Initial drilling results confirm PMV’s continued exploration potential and the possibility to quickly define a shallow mineral resource

- Shallow polymetallic mineralisation includes:

- CA15: 35.20m at 0.70% Cu, 1.53% Zn, 1.39% Pb and 62.50 g/t Ag (1.71% CuEq) from 77.80m from surface

- CA21: 18.10m at 1.19% Cu, 0.08% Zn, 0.32% Pb and 36.66 g/t Ag (1.40% CuEq) from 43.20m from surface

- Drilling to date has focused around the historical Campanario workings, which only represents approximately 10% of the entire strike length of the mineralised structure

- Intersected mineralisation includes massive and semi-massive sulphides as well as stockwork-type material, consistent with the Masa Valverde and Majadales deposits

- Initial drilling results demonstrate the significant exploration potential of Atalaya’s strategic land package in the world-class Iberian Pyrite Belt

About Proyecto Masa Valverde

PMV consists of several volcanogenic massive sulphide (“VMS”) type deposits including Masa Valverde, Majadales, the Campanario Trend and other drill ready targets. Atalaya’s exploration team discovered the Majadales deposit and in 2020 acquired a 100% interest in PMV. The project is strategically located approximately 28 km from Proyecto Riotinto, therefore future development scenarios are expected to utilise the Company’s existing 15 Mtpa processing plant.

In April 2022, Atalaya announced a new independent resource estimate for PMV that was prepared in accordance with CIM guidelines and disclosure requirements of NI 43-101, including:

- Masa Valverde Indicated Mineral Resource of 16.9 Mt at 0.66% Cu, 1.55% Zn, 0.65% Pb, 27 g/t Ag and 0.55 g/t Au (1.51% CuEq)

- Masa Valverde Inferred Mineral Resource of 73.4 Mt at 0.61% Cu, 1.24% Zn, 0.61% Pb, 30 g/t Ag and 0.62 g/t Au (1.37% CuEq)

- Majadales Inferred Mineral Resource of 3.1 Mt at 0.94% Cu, 3.08% Zn, 1.43% Pb, 54 g/t Ag and 0.32 g/t Au (2.55% CuEq)

Atalaya expects to complete a PEA for PMV by the end of the year.

Four rigs are currently operating at PMV, as part of the Company’s €10 million exploration programme for 2022. Two rigs are devoted to the Campanario Trend and the rest are drill testing the Fix Loop Electromagnetic (“FLEM”) anomalies west of the Masa Valverde deposit. So far, three holes were completed at two of the FLEM anomalies. The results of that programme will be released in a future announcement.

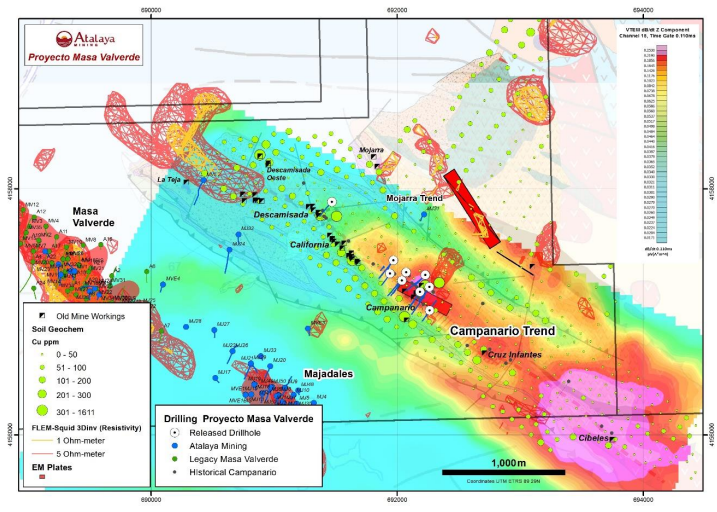

About the Campanario Trend

The Campanario Trend is a five kilometre north-west trending mineralised corridor, located one kilometre north of the Masa Valverde and Majadales VMS deposits. Campanario is characterised by the presence of numerous small historical workings and coincident soil geochemical and geophysical anomalies (see Figure 2 in the Website Announcement).

Figure 2: Campanario Trend Anomalies

Historical mining activity (from 1876 – 1917) along the Campanario Trend was at a small scale and focused on narrow zones of massive sulphides. Near-surface oxidation of the massive sulphides, mainly pyrite, generated gossans which were also investigated for gold potential.

Total historical mine production is estimated to be 0.22 million tonnes at 1.5% Cu from six main mining areas situated from the east to the west: Cruz Infante, Cibeles, Campanario, California, Descamisada and Descamisada Oeste. Drilling to date by Atalaya has focused around the historical Campanario workings which, by size, are the most important along the Campanario Trend.

Notably, immediately to the west of the historical Descamisada Oeste mine, the FLEM geophysical survey delineated a significant conductor (Loop 14 in Figure 2 in the Website Announcement) which is interpreted to be the potential west extension of the main mineralised corridor. To the east of the historical Campanario workings and coincident with the Cruz Infantes and old Cibeles mines, a previous VTEM (“Versatile Time Domain Electromagnetic”) survey delineated a zone of elevated conductivity which could be related with the presence of massive sulphides at depth.

Despite the numerous historical workings, the semi-continuous outcropping mineralisation and the proximity to the large Masa Valverde deposit, the Campanario Trend remained under-explored for many years. The last drilling campaign was carried out in 1995 by the Spanish state-owned company Adaro.

Campanario Trend Initial Drilling Results

Atalaya has completed 22 drill holes at the Campanario Trend with assay results produced by the certified laboratory at Proyecto Riotinto. In addition, assays including gold were produced by an independent external laboratory (ALS) up to hole CA-13.

Drilling was focused around the historical Campanario workings, located in the central part of the five kilometre long Campanario Trend (see drill hole map in Figure 3 in the Website Announcement). Assay results received to date included intersections that are the best so far in terms of “grade x thickness” factor.

Local stratigraphy consists of black shales with varying graphite content, coherent acid rocks of rhyodacitic composition and, to a lesser extent, volcanic tuffs. Mineralised zones are mainly hosted in the black shale levels which are intensely folded and sheared and often show zones of sericitic, chloritic and silicic alteration.

Except near surface where it is oxidised (gossans), the main mineralisation styles are massive and semi-massive sulphides and stockwork-type. Pyrite is the predominant sulphide mineral with subordinate chalcopyrite, sphalerite, galena and sulphosalts. Mineralisation is polymetallic with elevated As, Sb, Hg and Bi values, therefore Atalaya believes the E-LIX System has strong potential to unlock value from any future mined material from the Campanario Trend.

The geometry of the mineralised zones varies down dip from steeply dipping to moderately dipping to the north-north-east and may include several parallel lenses of massive and semi-massive sulphides, with individual true thicknesses varying from 1-2 metres up to 20-25 metres. Two representative cross sections are included in Figure 4 in the Website Announcement.

The mineralised system remains completely open laterally but seems to get thinner at depth in some sections. Pinch and swell geometry is evident, quite likely due to syn/late deformation.

Source: Atalaya Mining

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

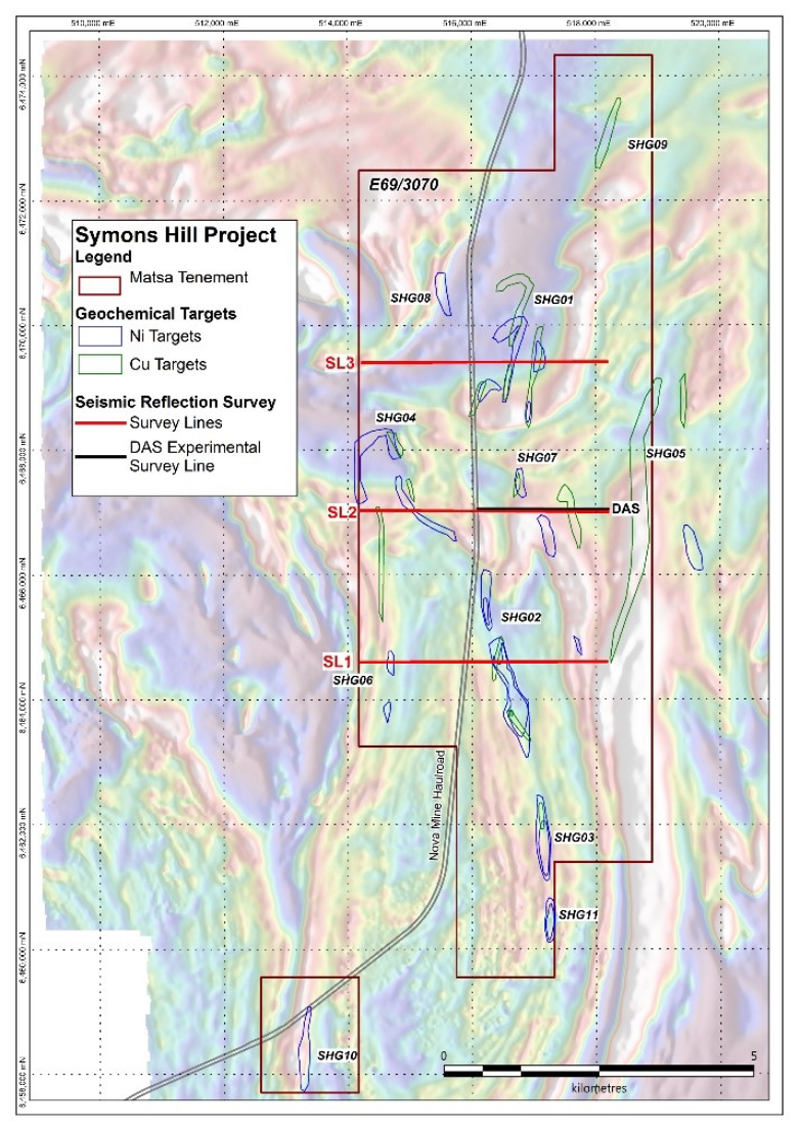

IGO Newsearch has announced that it has signed an agreement to acquire a 70% interest in Matsa Resources’ (ASX:MAT) Fraser Range Tenements. As part of the deal, the company will also buy the stake in the Symons Hill copper/nickel project. Matsa will still keep a 30% free carried interest in all of the tenements. This will be held until a feasibility study is finished or any decision is final for the development and mining of a deposit on each of the tenements in question.

Both companies are also planning to end existing commitments, and instead continue with one single agreement that covers Matsa’s stake in the Fraser Range tenements.

Matsa Resources chairman Paul Poli commented in a press release: “This transaction enables IGO to have unfettered access to any part of Matsa’s Fraser Range landholding and explore the tenements to the fullest extent without a specific time or cost demands. It provides Matsa with a cash boost, as well as receiving the expert knowledge and exploration experience of the IGO team which is second to none. Matsa welcomes IGO’s exploration know-how and capabilities throughout its Fraser Range tenement holdings.”

Highlights of the agreement are as follows:

- Matsa has entered in to an agreement whereby IGO will purchase a 70% interest in all of Matsa’s Fraser Range tenements

- Matsa will retain a 30% free carried interest in each of the tenements until the completion of a feasibility study or a decision to proceed to development and mining of a deposit on each of the tenements

- IGO will pay $600,000 cash and free carry Matsa for the 70% interest in the tenements

- The disposal of the non-core Fraser Range tenements allows Matsa to focus on its Lake Carey project but retain an interest in the potential upside at no cost.

Source: Matsa Resources

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |