ATAC Resources (TSXV:ATC) has commenced its maiden drill program at the Catch Property in Yukon, Canada, and has announced surface exploration results. The company has received prospecting, soil sampling, and Induced Polarization (IP) results from the 2022 Phase 1 exploration and commencement of a Phase 2 maiden drill program.

The results from the Catch Property have allowed ATAC to identify and define multiple drill-ready targets that can be included in the campaign. Additionally, there are numerous soil anomalies that the company has yet to follow up on, which indicate that Catch could be a significant new grassroots copper-gold discovery. Planned drilling for the campaign is expected to begin in the coming days.

Highlights from the initial exploration are as follows:

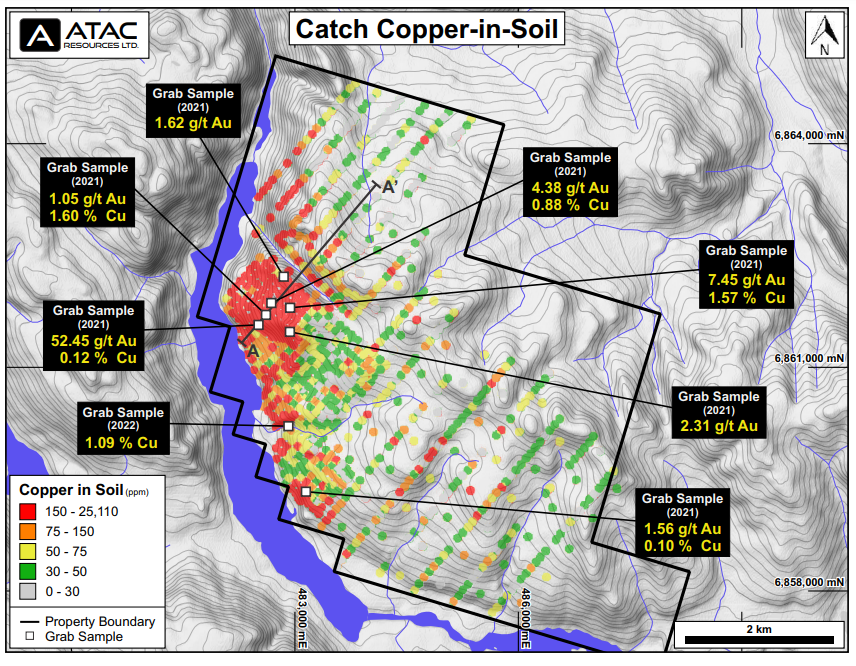

- Primary copper-in-soil anomaly extended by 1.5 km to total of 5 km x 500 m, with multiple additional target areas identified (figures 1 & 2);

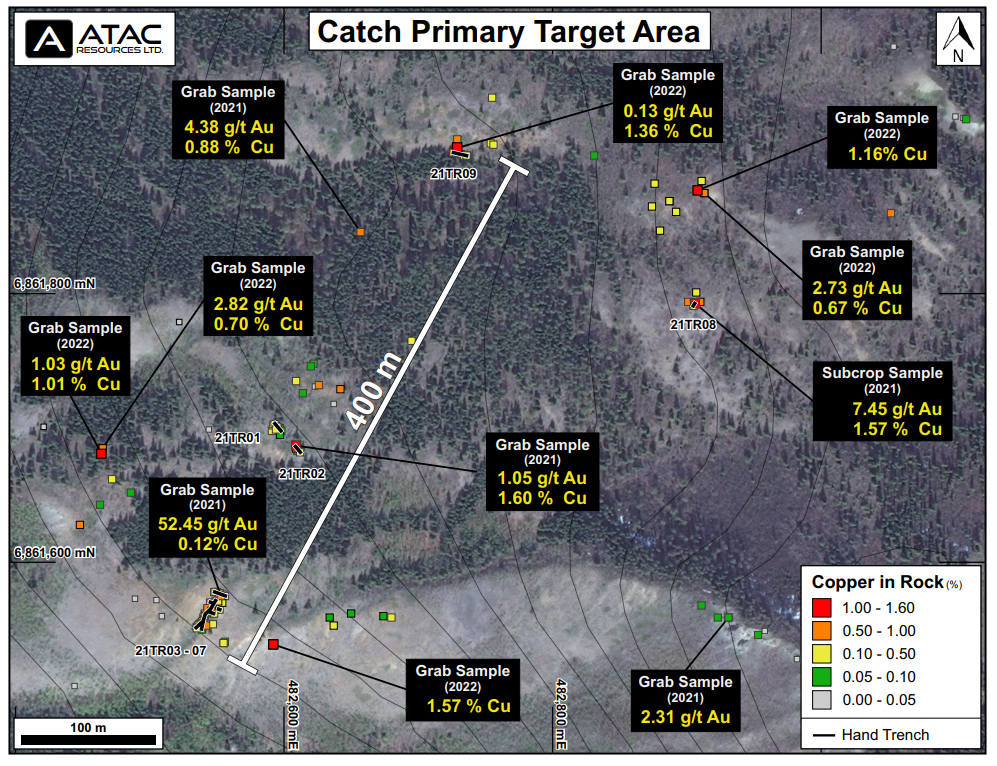

- Widespread copper mineralization observed at surface in the primary target area, with grab samples (figure 3) returning values including:

- 1.57% copper;

- 1.01% copper with 1.03 g/t gold; and

- 0.70% copper with 2.82 g/t gold;

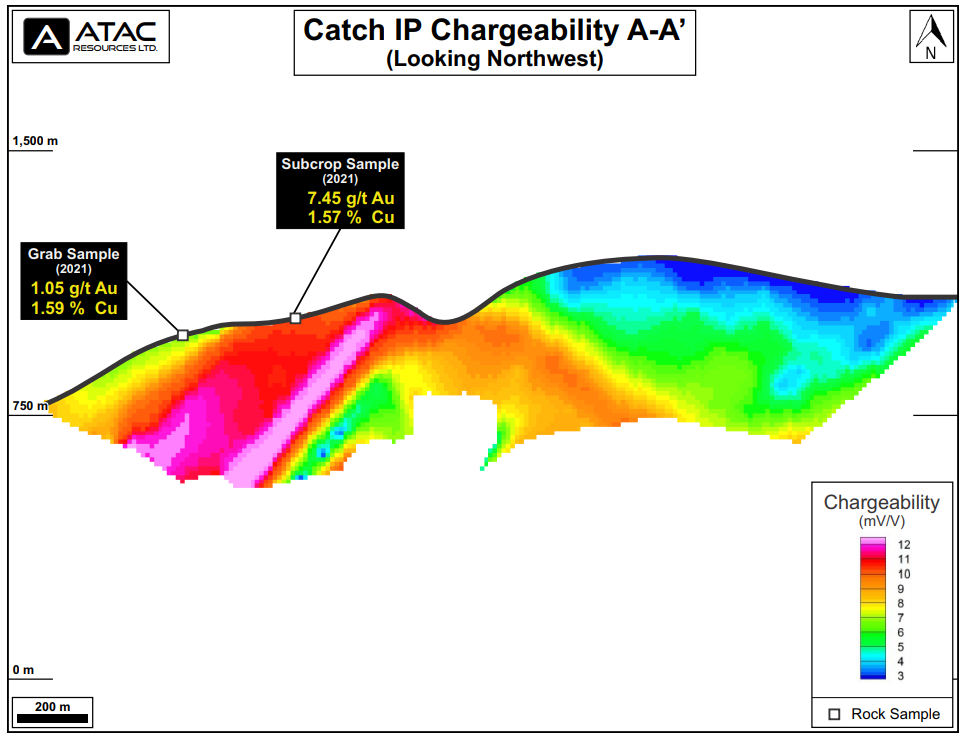

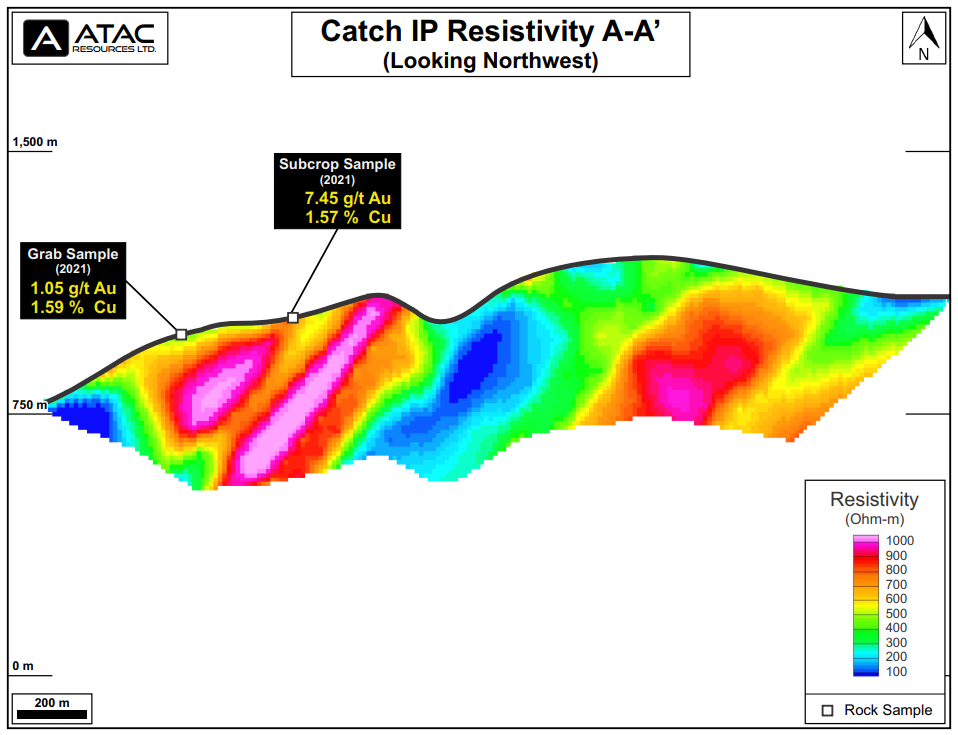

- IP surveys returned a 1,000 x 600 x 400 m chargeability and resistivity high coincident with high-grade surface samples (figures 4 & 5);

- Phase 2 maiden drill program at the Catch property has commenced, with up to 1,500 m of reverse circulation (“RC”) drilling to test priority coincident geochemical and geophysical targets; and

- Outcrop sampling 1.5 km south of the primary target area returned 1.09% copper in an area that has seen minimal sampling (figures 1 & 2).

Graham Downs, ATAC president and CEO, commented in a press release: “We are very impressed with the results we have seen from Catch so far. We’ve already defined multiple drill-ready targets, with numerous soil anomalies yet to be followed-up. This has all the hallmarks of a significant new grassroots copper-gold discovery, and we look forward to drilling the first ever holes on this property in the coming days.”

Exploration Summary

Phase 1 exploration at Catch consisted of prospecting, mapping, soil sampling and geophysical surveys. A total of 50 rock samples and 359 soil samples were collected. 10.1 line-km of IP and 49.3 line-km of ground magnetics and very low frequency surveys were completed.

Broad-spaced soil sampling (100 x 500 m) extended the primary copper-in-soil anomaly by 1.5 km to the north, to a total of 5 km x 500 m in size. Additional areas of anomalous copper-in-soil were identified outside the main target area and provide compelling targets for Phase 2 prospecting work.

Figure 1 – Catch Copper-in-soil

Rock sampling extended areas of known mineralization at surface. Hand pitting 100 m north of Trench 8 yielded a sample returning 1.16% copper. Follow-up sampling at Trench 9 yielded a sample returning 1.36% copper with 0.13 g/t gold. Sampling 135 m west of Trench 1 returned 1.01% copper with 1.03 g/t gold from a hand pit. Sampling 50 m east of Trench 7 returned 1.57% copper. Apart from the follow-up sampling at Trench 9, all of these samples are from new mineral occurrences within the main target area, significantly extending known mineralization at surface. The primary anomaly area remains underexplored and numerous additional targets will be evaluated in Phase 2 work.

A separate copper-in-soil anomaly located 1.5 km south of the trenching area returned 1.09% copper from outcrop in an area that remains underexplored. This area and additional soil anomalies located further south and east will be evaluated in Phase 2 and future work.

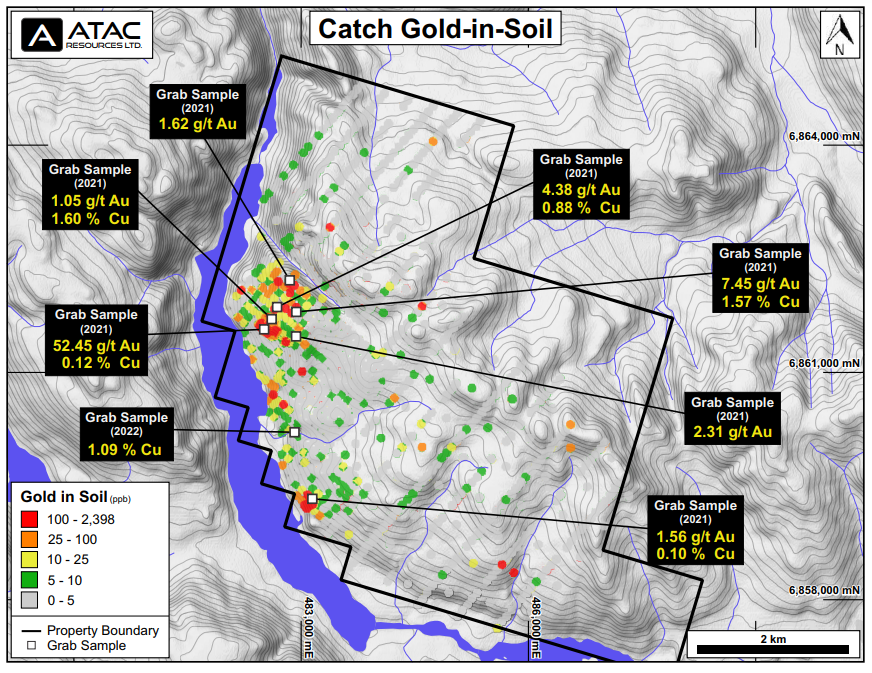

Figure 2 – Catch Gold-in-soil

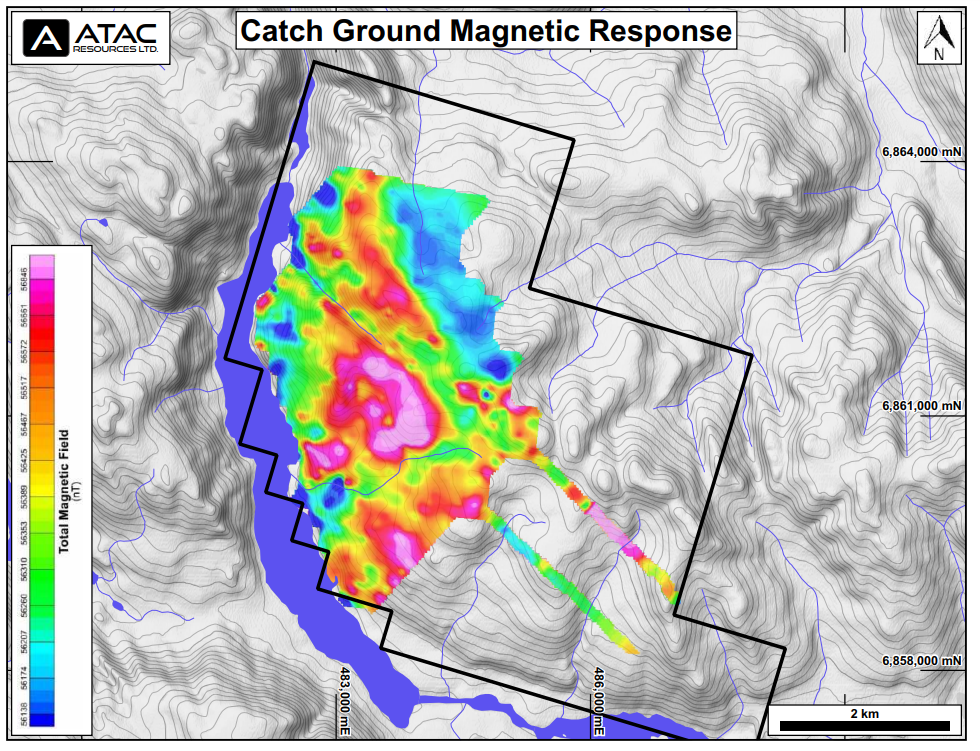

The IP survey returned an open ended (NW-SE), 1,000 x 600 x 400 m coincident chargeability and resistivity high coincident with the primary zone of copper-gold mineralization (figure 4 & 5). This area lies within a moderate magnetic high and is immediately adjacent to a 1.5 x 1.2 km circular magnetic high (figure 6).

Based on the highly encouraging results from this Phase 1 work, crews have recently returned to the Catch property to initiate a Phase 2 program, with additional prospecting, mapping and sampling underway. Crews and equipment are currently being mobilized to site for a maiden RC drill program, with drilling scheduled to begin in the coming days. This property has never been drilled, and all targets represent new grassroots discoveries.

Figure 3 – Catch Rock Highlights

Property Geology and Mineralization

The Property lies within the Quesnel Terrane and is juxtaposed against the Stikine Terrane by the 1,000+ km long, deep seated, crustal scale strike-slip Teslin-Thibert fault approximately 3 km west of the Property boundary. The Quesnel and Stikine Terranes are characterized by similar Late Triassic to early Jurassic volcanic-plutonic arc complexes that are well-endowed with copper-gold-molybdenum porphyries including the Mt. Milligan, KSM, Red Chris, Mt. Polley, Highland Valley Copper deposits.

Figure 4 – Catch IP Section Chargeability

The Property is underlain by augite phyric basalt of the Semenof Formation, centered on a 7 x 3 km regional magnetic high. Bedrock exhibits strong propylitic and sericitic alteration and intense localized oxidation, brecciation and malachite staining.

The geology, alteration and mineralization observed throughout the Property are all indicative of a nearby copper-gold±molybdenum bearing porphyry system.

The Property is under option from a Yukon prospector, and ATAC can earn up to a 100% interest in the Property. For more information, see ATAC news release dated January 25, 2022.

Figure 5 – Catch IP Section Resistivity

Figure 6 – Catch Ground Magnetics

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

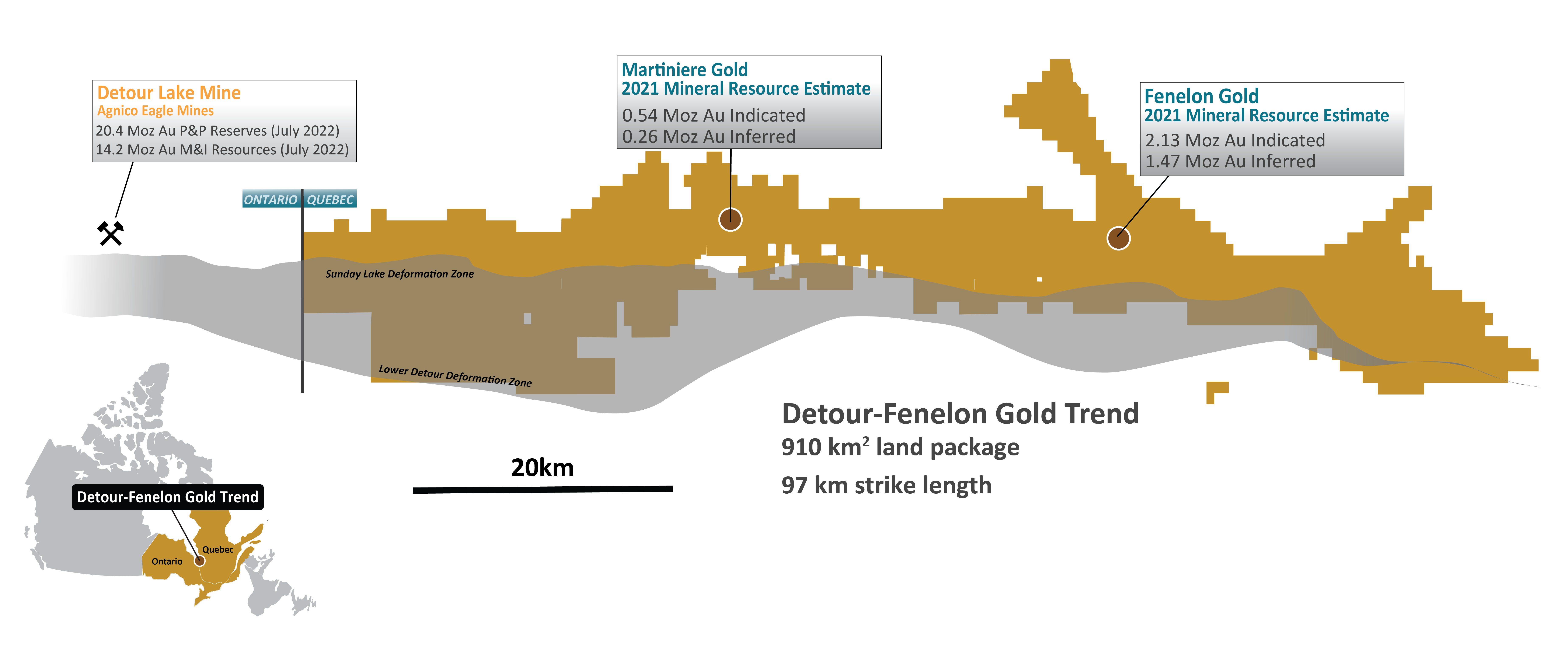

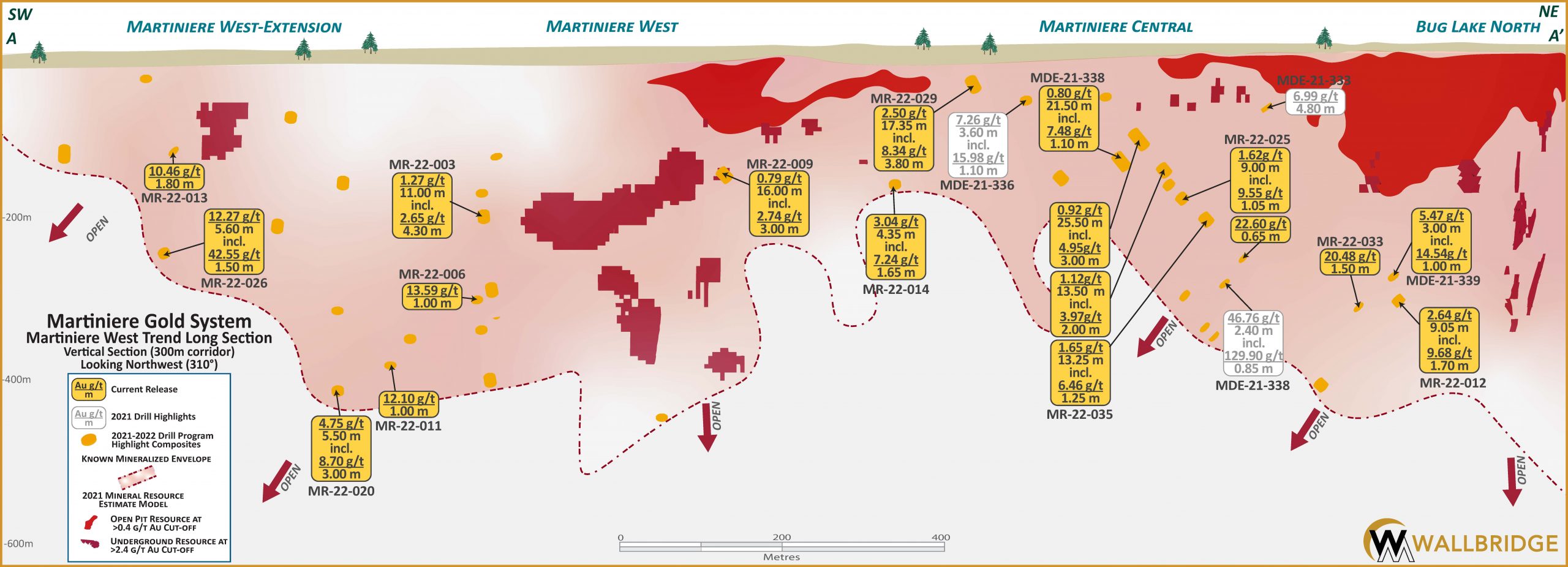

Wallbridge Mining (TSX:WM) has announced new assay results from its Martiniere Gold Property. The results validate resource growth at the property, located 30 kilometres and within trucking distance of the company’s Fenelon Gold Project. Fenelon is located on the Detour-Fenelon Gold trend in Northern Abitibi, Quebec.

Figure 1. Detour Fenelon Gold Trend

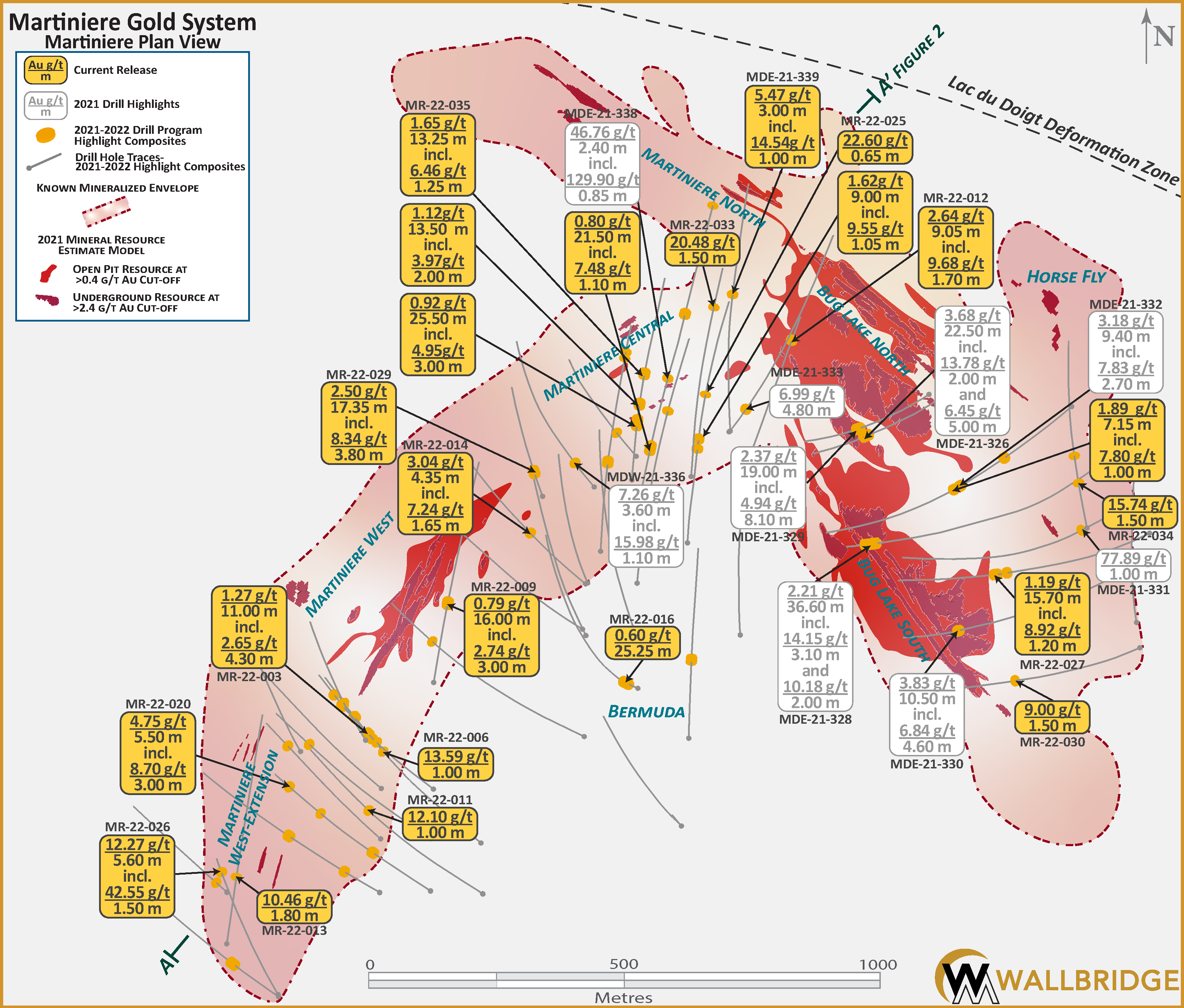

Attila Péntek, Wallbridge’s Vice President of exploration, commented in a press release: “Our 2021-2022 exploration program at Martiniere has provided essential geologic information on the orientation of the gold zones and their host rocks and has demonstrated resource expansion potential in multiple directions. We see excellent opportunities to add to the existing resource, including at shallow depths, as in hole MR-22-029, and the deposit remains largely untested below 400 metres from the surface. We will use the remainder of the year to incorporate this new data, along with pending assays from three more exploration holes, into our geology models, in preparation for an updated Mineral Resource Estimate and planning for our 2023 exploration program at the property.”

The results included 12.27 g/t Au over 5.60 metres in holes MR-22-026, extending the Martiniere West zone along strike by over 400 metres to the southwest; 4.75 g/t Au over 5.50 metres in hole MR-22-020, extending the Martiniere West zone down-plunge by over 300 metres; and 2.50 g/t Au over 17.35 metres, near-surface in hole MR-22-029 in the area between the Martiniere West and Central zones.

The property contains 544,000 ounces of indicated gold resources along with 256,000 ounces of inferred gold resources. Martiniere holds all of this within a large mineralized footprint spanning four square kilometres. A lot of potential remains for the deposit as drilling has only been done to a depth of 400 metres, with mineralized shoots remaining open down-plunge.

Highlights from the drill results are as follows:

| Martiniere West Zone | |

| MR-22-026 | 12.27 g/t Au over 5.60 metres, including |

| 42.55 g/t Au over 1.50 metres; | |

| MR-22-020 | 4.75 g/t Au over 5.50 metres, including |

| 8.70 g/t Au over 3.00 metres; | |

| MR-22-013 | 10.46 g/t Au over 1.80 metres; |

| Martiniere Central Zone | |

| MR-22-029 | 2.50 g/t Au over 17.35 metres, including |

| 8.34 g/t Au over 3.80 metres; | |

| MDE-21-338 | 0.80 g/t Au over 21.50 metres, including |

| 7.48 g/t Au over 1.10 metres; | |

| These intersections are in addition to an interval of 46.75 g/t Au over 2.40 metres announced previously in the Wallbridge press release dated February 2, 2022. | |

| MR-22-033 | 20.48 g/t Au over 1.50 metres; |

| MR-22-035 | 0.92 g/t Au over 25.50 metres, including |

| 4.95 g/t Au over 3.00 metres; | |

| 1.12 g/t Au over 13.50 metres; | |

| 1.65 g/t Au over 13.25 metres; | |

| MR-22-012 | 2.64 g/t Au over 9.05 metres, including |

| 9.68 g/t Au over 1.70 metres; | |

| Bug Lake North | |

| MR-22-027 | 1.19 g/t Au over 15.70 metres; |

| MR-22-034 | 15.74 g/t Au over 1.50 metres; |

| MDE-21-339 | 5.47 g/t Au over 3.00 metres; |

Assay results from 40 drill holes of the 2021-2022 Martiniere drill program are reported in the Table and Figures below. Further assays results are pending for three drill holes of the 2022 program. All figures and a table with drill hole information of recently completed holes are posted on the Company’s website under “Current Program”.

Figure 2. Martiniere Gold, Plan View

Figure 3. Martiniere Gold, Martiniere West Trend Long Section

| Table 1. Regional Gold Property, Recent Drill Assay Highlights (1) | |||||||

| Drill Hole | From | To | Length | Au | Au Cut(2) | VG(3) | Zone/Corridor |

| (m) | (m) | (m) | (g/t) | (g/t) | |||

| MDE-21-332 | 267.50 | 276.00 | 8.50 | 0.68 | 0.68 | Bug Lake North | |

| MDE-21-332 | 457.00 | 464.15 | 7.15 | 1.89 | 1.89 | Bug Lake North | |

| Including… | 458.00 | 459.00 | 1.00 | 7.80 | 7.80 | Bug Lake North | |

| MDW-21-335 | 89.50 | 91.00 | 1.50 | 3.66 | 3.66 | Martiniere Central | |

| MDE-21-338 | 182.00 | 203.50 | 21.50 | 0.80 | 0.80 | Martiniere Central | |

| Including… | 182.00 | 183.10 | 1.10 | 7.48 | 7.48 | Martiniere Central | |

| MDE-21-338 | 572.00 | 583.00 | 11.00 | 0.54 | 0.54 | Martiniere Central | |

| MDE-21-338 | 863.70 | 864.55 | 0.85 | 7.80 | 7.80 | Martiniere Central | |

| MDE-21-339 | 389.00 | 392.00 | 3.00 | 5.47 | 5.47 | Bug Lake North | |

| Including… | 390.00 | 391.00 | 1.00 | 14.54 | 14.54 | Bug Lake North | |

| MR-22-001 | No Significant Mineralization (4) | ||||||

| MR-22-002 | No Significant Mineralization (4) | ||||||

| MR-22-003 | 227.50 | 229.00 | 1.50 | 3.67 | 3.67 | Martiniere West | |

| MR-22-003 | 260.00 | 271.00 | 11.00 | 1.27 | 1.27 | Martiniere West | |

| Including… | 260.00 | 264.30 | 4.30 | 2.65 | 2.65 | Martiniere West | |

| MR-22-003 | 375.70 | 388.00 | 12.30 | 1.02 | 1.02 | Martiniere West | |

| Including… | 380.55 | 385.65 | 5.10 | 1.81 | 1.81 | Martiniere West | |

| MR-22-003 | 420.40 | 426.50 | 6.10 | 1.49 | 1.49 | Martiniere West | |

| Including… | 421.00 | 423.65 | 2.65 | 2.92 | 2.92 | Martiniere West | |

| MR-22-004 | 43.50 | 44.70 | 1.20 | 4.32 | 4.32 | Martiniere West- Extension | |

| MR-22-005 | 158.85 | 177.70 | 18.85 | 0.63 | 0.63 | Martiniere West- Extension | |

| Including… | 172.80 | 177.70 | 4.90 | 1.09 | 1.09 | Martiniere West- Extension | |

| MR-22-006 | 403.80 | 404.80 | 1.00 | 13.59 | 13.59 | Martiniere West | |

| MR-22-006 | 452.30 | 454.50 | 2.20 | 4.55 | 4.55 | VG | Martiniere West |

| Including… | 453.00 | 453.50 | 0.50 | 15.24 | 15.24 | VG | Martiniere West |

| MR-22-006 | 530.00 | 541.15 | 11.15 | 0.72 | 0.72 | Martiniere West | |

| MR-22-007 | No Significant Mineralization (4) | ||||||

| MR-22-008 | 575.40 | 576.30 | 0.90 | 5.64 | 5.64 | Martiniere West | |

| MR-22-009 | 213.00 | 229.00 | 16.00 | 0.79 | 0.79 | Martiniere West | |

| Including… | 226.00 | 229.00 | 3.00 | 2.74 | 2.74 | Martiniere West | |

| MR-22-010 | 203.60 | 215.75 | 12.15 | 0.45 | 0.45 | Bermuda | |

| MR-22-011 | 475.00 | 476.00 | 1.00 | 12.10 | 12.10 | Martiniere West- Extension | |

| MR-22-012 | 427.70 | 436.75 | 9.05 | 2.64 | 2.64 | VG | Martiniere Central |

| Including… | 432.90 | 434.60 | 1.70 | 9.68 | 9.68 | VG | Martiniere Central |

| MR-22-013 | 178.50 | 180.30 | 1.80 | 10.46 | 10.46 | Martiniere West- Extension | |

| MR-22-014 | 224.80 | 229.15 | 4.35 | 3.04 | 3.04 | Martiniere West | |

| Including… | 227.50 | 229.15 | 1.65 | 7.24 | 7.24 | Martiniere West | |

| MR-22-015 | 112.25 | 119.75 | 7.50 | 1.52 | 1.52 | Martiniere West- Extension | |

| MR-22-015 | 295.00 | 307.00 | 12.00 | 0.50 | 0.50 | Martiniere West- Extension | |

| MR-22-016 | 35.00 | 60.25 | 25.25 | 0.60 | 0.60 | Bermuda | |

| MR-22-017 | 464.00 | 467.00 | 3.00 | 1.72 | 1.72 | Martiniere West- Extension | |

| MR-22-018 | 403.90 | 407.00 | 3.10 | 3.67 | 3.67 | Martiniere West- Extension | |

| Including… | 406.00 | 407.00 | 1.00 | 10.39 | 10.39 | Martiniere West- Extension | |

| MR-22-019 | No Significant Mineralization (4) | ||||||

| MR-22-020 | 207.50 | 218.50 | 11.00 | 0.74 | 0.74 | Martiniere West | |

| MR-22-020 | 413.85 | 415.15 | 1.30 | 6.03 | 6.03 | Martiniere West | |

| MR-22-020 | 538.50 | 544.00 | 5.50 | 4.75 | 4.75 | Martiniere West | |

| Including… | 541.00 | 544.00 | 3.00 | 8.70 | 8.70 | Martiniere West | |

| MR-22-021 | 233.50 | 247.00 | 13.50 | 0.85 | 0.85 | Martiniere Central | |

| Including… | 233.50 | 238.00 | 4.50 | 1.20 | 1.20 | Martiniere Central | |

| MR-22-021 | 513.90 | 515.30 | 1.40 | 7.62 | 7.62 | Martiniere Central | |

| MR-22-021 | 529.50 | 532.70 | 3.20 | 2.75 | 2.75 | Martiniere Central | |

| MR-22-022 | 156.15 | 157.20 | 1.05 | 6.70 | 6.70 | Martiniere Central | |

| MR-22-023A | No Significant Mineralization (4) | ||||||

| MR-22-024 | 458.15 | 462.00 | 3.85 | 1.67 | 1.67 | Martiniere Central | |

| MR-22-025 | 250.00 | 256.00 | 6.00 | 1.73 | 1.73 | Martiniere Central | |

| Including… | 253.00 | 254.00 | 1.00 | 7.58 | 7.58 | Martiniere Central | |

| MR-22-025 | 274.00 | 283.00 | 9.00 | 1.62 | 1.62 | Martiniere Central | |

| Including… | 274.00 | 275.05 | 1.05 | 9.55 | 9.55 | Martiniere Central | |

| MR-22-025 | 392.05 | 392.70 | 0.65 | 22.60 | 22.60 | Martiniere Central | |

| MR-22-026 | 357.90 | 363.50 | 5.60 | 12.27 | 10.25 | Martiniere West- Extension | |

| Including… | 360.50 | 362.00 | 1.50 | 42.55 | 35.00 | Martiniere West- Extension | |

| MR-22-027 | 473.00 | 478.90 | 5.90 | 1.77 | 1.77 | Bug Lake North | |

| MR-22-027 | 504.50 | 520.20 | 15.70 | 1.19 | 1.19 | Bug Lake North | |

| Including… | 519.00 | 520.20 | 1.20 | 8.92 | 8.92 | Bug Lake North | |

| MR-22-028 | No Significant Mineralization (4) | ||||||

| MR-22-029 | 62.65 | 80.00 | 17.35 | 2.50 | 2.50 | Martiniere Central | |

| Including… | 68.50 | 72.30 | 3.80 | 8.34 | 8.34 | Martiniere Central | |

| MR-22-030 | 428.50 | 430.00 | 1.50 | 9.00 | 9.00 | Bug Lake South | |

| MR-22-031 | No Significant Mineralization (4) | ||||||

| MR-22-032 | No Significant Mineralization (4) | ||||||

| MR-22-033 | 173.50 | 176.50 | 3.00 | 1.72 | 1.72 | Martiniere Central | |

| MR-22-033 | 464.50 | 466.00 | 1.50 | 20.48 | 20.48 | Martiniere Central | |

| MR-22-034 | 124.50 | 126.00 | 1.50 | 15.74 | 15.74 | Bug Lake North | |

| MR-22-034 | 199.00 | 200.00 | 1.00 | 5.60 | 5.60 | Bug Lake North | |

| MR-22-035 | 151.00 | 176.50 | 25.50 | 0.92 | 0.92 | Martiniere Central | |

| Including… | 173.50 | 176.50 | 3.00 | 4.95 | 4.95 | Martiniere Central | |

| MR-22-035 | 209.50 | 223.00 | 13.50 | 1.12 | 1.12 | Martiniere Central | |

| Including… | 221.00 | 223.00 | 2.00 | 3.97 | 3.97 | Martiniere Central | |

| MR-22-035 | 294.75 | 308.00 | 13.25 | 1.65 | 1.65 | Martiniere Central | |

| Including… | 294.75 | 296.00 | 1.25 | 6.46 | 6.46 | Martiniere Central | |

| MR-22-037 | No Significant Mineralization (4) | ||||||

| (1) Table includes only assay results received since the latest press release dated February 02, 2022. | |||||||

| (2) Au cut at: 0.35 g/t Au. | |||||||

| (3) Intervals containing visible gold (“VG”). | |||||||

| (4) Metal factor of at least 5 g/t*m and minimum weighted average composite grade of 0.40 g/t Au within the 2021 MRE open pit shell and 2.4 g/t Au for outside open pit shell.

Note: True widths are estimated to be 50-80% of the reported core length intervals. |

|||||||

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Brazil Potash recently presented its flagship Autazes Potash Project to students in the Technical Surveying Course at the Centro Tecnológico do Amazonas (CETAM). The centre trains professionals in mapping which is fundamental to engineering projects. This was an opportunity for students to learn about the project, an important potash project in Brazil, currently in the licensing phase.

Lúcio Rabelo, the director of ESG at Brazil Potash, said the presentation demonstrated to students the influence of the Autazes Potash Project on society, the economy, and the environment. According to Rabelo, CETAM students will have an opportunity to apply what they learned in the course when they participate in the Project.

Lucio Rabelo commented: “These are young people who are graduating, receiving a qualification, who will have the opportunity to apply the knowledge they are receiving. They verified that, indeed, many opportunities will arise to help, in the great project that is being implemented here, so that the municipality can develop.”

At the moment, the Autazes Potash Project is in the environmental licensing stage. It has a prior license (LP) and is waiting for an installation license (LI) as a result of a legal agreement, at the Federal Court, between the firm and the Mura People, which was launched in 2019. The enterprise continues to be open to discussion with society about how the Autazes Potash Project can serve as one of Amazonas’ future development models.

The project will create 2,600 direct jobs every year during implementation Then, once the Potassium Chloride factory is operational, working from the soil of the Autazes Potash Project, 1,300 direct jobs will be created, as well as 17,000 indirect positions.

The finalist students were in attendance and the presentation was part of the last module of the course: Practices II, led by professor and engineer Márcio Góes. Professionals who will be responsible for mapping are educated during the Surveying course.

Mr. Góes commented: “I think this is something magical for us because we live in a region of magnitude, when it comes to geography, gigantic, with little investment. When we see a project like Autazes Potash Project, we are sure that the Amazon is here to make a difference in the world, with all our trees standing. And we come to believe when we know a project like this, that it is possible, yes, to bring progress keeping our forest, our fauna and our flora intact.”

The professor noted that it’s nice to see a project that improves the region, in addition to offering tremendous possibilities and infrastructure. He also said he has two perspectives on the Autazes Potash Project: one as a teacher and one as a riverside caboclo.

After the conclusion of the Project presentation, Fabiana Oliveira, coordinator of CETAM in Autazes, stated that she was satisfied. “I leave here with my heart overflowing with joy to know that we are included and that it is going to have a wonderful impact. We really need to know. When we know, our hearts are calmer, knowing we are on the right path,” she said.

The presentation of the Autazes Potash Project is vital for student Adriano Gomes since it gives him direction in his professional future and transforms people’s perception of the Project. “I arrived here and heard many people talking about the Potassium issue. And, today, we leave here with another mentality, which is really something that comes to add to our municipality, to our community. For us, who are leaving now, graduating, it is something very hopeful, where we will have our share of contribution”, he explained.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Brazil Potash Corp. has announced the closing of its Regulation A, Tier 2 offering of common shares, no par value per share, as of the end of July 2022. The company raised over US$40 million, and is well capitalized for ongoing operations as it prepares to increase output at its flagship Autazes Project.

Brazil Potash is an extraction company currently preparing for the implementation of the Autazes Potash Project 120 km southeast of Manaus. The company will serve customers in the agricultural sector of Brazil and intends to produce more than 20% of potash consumed by Brazil annually. Brazil Potash is still in the pre-revenue development stage and has not commenced mining operations yet.

Brazil Potash is aiming to reduce the strain of the global demand for potash amid record prices and global demand. The current record prices of potash are the result of a combination of increased global demand for potash and sanctions against Russia and Belarus, which hinder their ability to export potash. Since Russia and Belarus historically supply approximately 40% of the world’s potash, the current sanctions have further reinforced the need for domestic potash production in Brazil to help ensure global food security.

Potash prices have remained above $1,100 USD per tonne and Brazilian demand is currently robust, with imports of potash increasing 42% year over year to 3.1 million tonnes in the first quarter of 2022, according to Reuters.

The company’s management team, backed by a group of third-party experts, also recently finalized Brazil Potash’s Environmental, Social and Governance (ESG) report. The report confirms management’s beliefs that the Autazes Project will be one of the most environmentally clean potash projects in the world, emitting 79% less greenhouse gas emissions than existing potash producers. The report will be made available on the company’s website soon.

The Autazes Project is making a huge impact in the fight against climate change by reducing greenhouse gas emissions. The project will get 85% of its energy from renewable sources, and the company will avoid unnecessarily long distances when transporting its produced potash.

Autazes has support from all levels of the Brazilian government. The Brazilian Minister of Agriculture recently visited Canada to meet with fertilizer companies including Brazil Potash. The minister asked what the country could do to help accelerate the construction of the Autazes Project while offering support for the companies present and the industry in Brazil.

Beyond this visit, the Governor of Amazon, Wilson Lima, met with Adriano Espeschit, President in Brazil, and it´s ESG Director Lucio Rabelo to get an update on the project. The engagement and support from the Brazilian government reflect a strong initiative to bring new potash projects online in the country and reduce Brazil’s reliance on imports as soon as possible.

Brazil Potash has also engaged ERCOSPLAN, a German engineering firm, to update the company’s technical report and feasibility study for Autazes. The initial technical report and feasibility study were done by WORLEY in 2016 with strong support and participation from ERCOSPLAN.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

On Wednesday, Rio Tinto (ASX:RIO) upped the ante in its attempt to acquire the entire Turquoise Hill Resources it does not already own, offering an additional $400 million in cash.

With the intention of gaining direct ownership of the large Oyu Tolgoi copper-gold mining project in Mongolia, Rio Tinto’s new offer means Turquoise Hill’s minority shareholders would receive $40 per share. The board of Turquoise Hill, a company that owns 66% of one of the world’s largest copper and gold deposits 550 km south of Mongolia’s capital Ulaanbaatar, said the company’s board is reviewing the proposal now.

After appointing an independent committee to determine if the offer was in the best interests of minority shareholders, last week the Canadian company rejected it as too low. They had received an offer of $26.57 per share back in March. Rio’s first offer was met with dissent from some of its largest shareholders, Turquoise Hill, including activist investor Pentwater Capital Management (with a 10% stake) and SailingStone Capital Partners (2.2% stake).

Copper’s demand is projected to increase as the world transitions away from fossil fuels. This is because copper wiring is necessary for electric vehicles, charging stations, and other renewable energy infrastructure. The increased bid reflects this potential value.

Turquoise Hill’s stock shot up in trading Wednesday on news of the increased bid.

Rio’s improved offer is contingent on Turquoise Hill not raising more than $1 billion in equity to pay for the project. Rio has committed to providing interim debt financing worth up to $400 million for the project.

Rio Tinto’s offer also reflects an M&A environment that is trying to keep up with demand through acquisitions. One of the biggest factors affecting the industry right now is the lack of new projects when demand is growing. This has created an environment of rising prices, which is encouraging consolidation.

It is also encouraging companies to increase production by any means necessary, even if it means reopening old mines or taking on more debt. In the case of Rio Tinto’s offer for Turquoise Hill, the company is willing to take on more debt to increase its ownership stake in a project with high potential. This is a sign that companies are becoming increasingly desperate to secure resources and output for the future.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

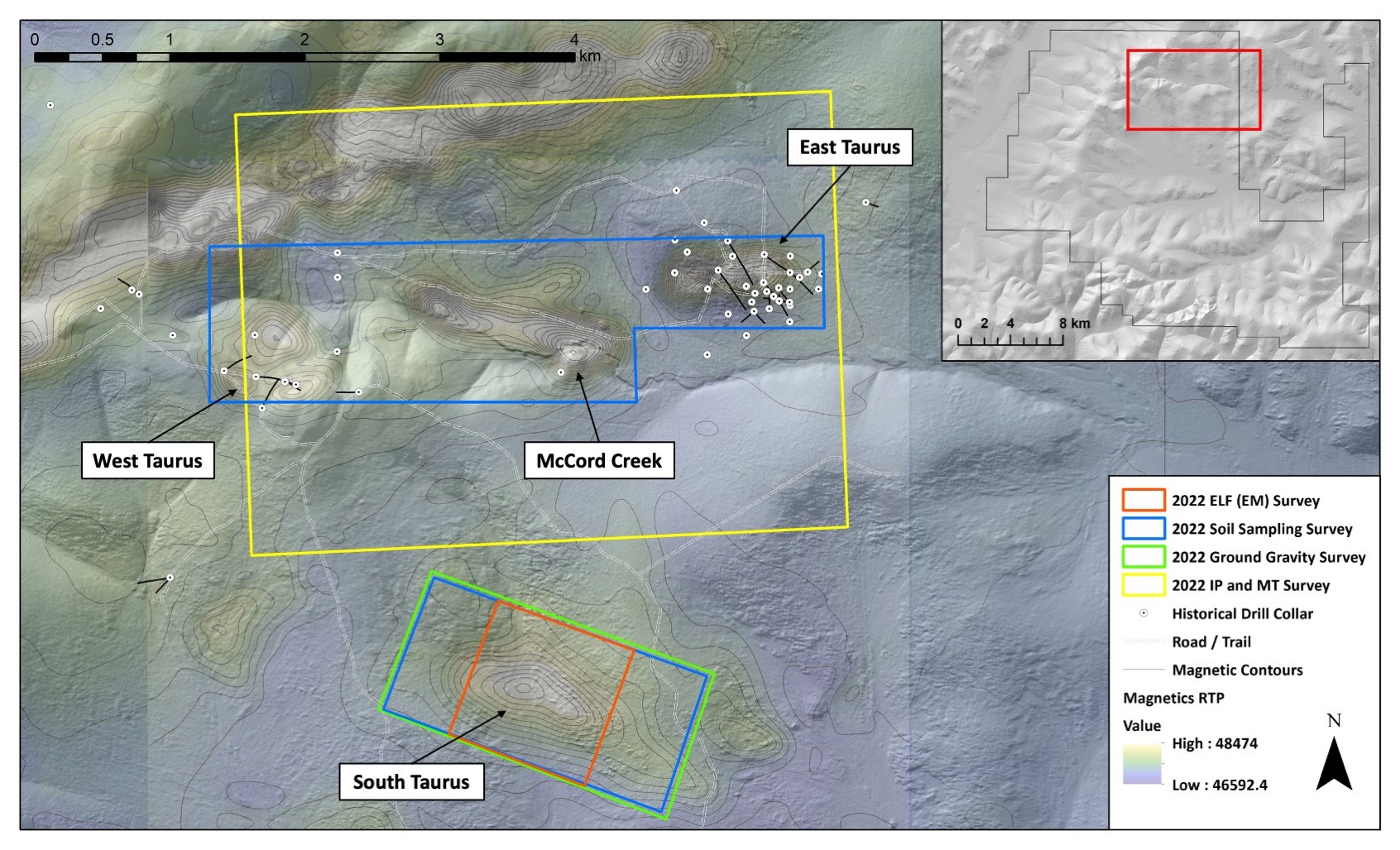

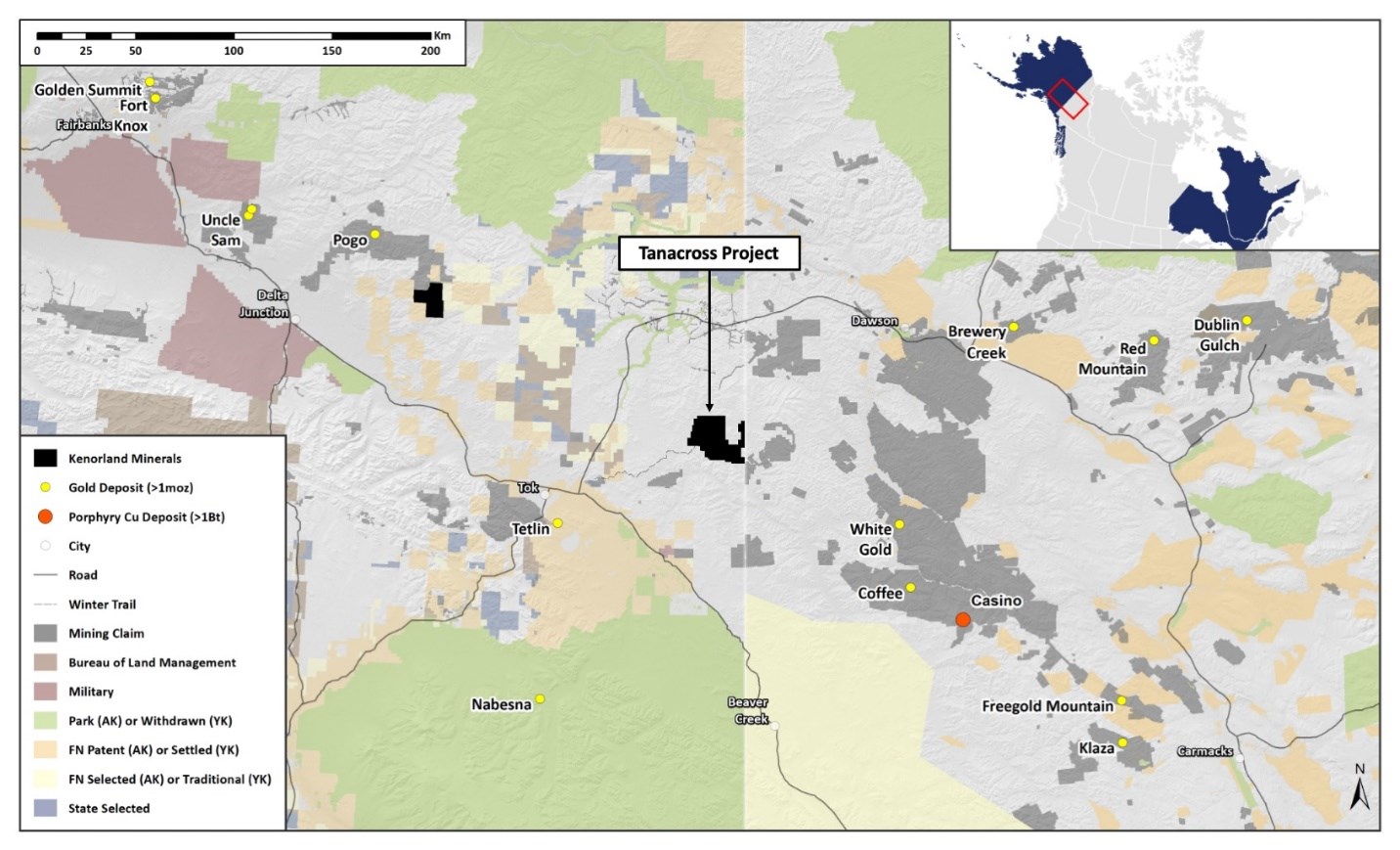

Kenorland Minerals (TSXV:KLD) has commenced exploration activities as part of the 2022 exploration program at the Tanacross Project in Eastern Alaska. The project is held under an earn-in agreement with Antofagasta Minerals. The company’s 2022 field program includes geophysical, geological, and geochemical surveys. This work will cover the McCord Creek, East Taurus, West Taurus, and South Taurus targets.

Figure 1: Location of exploration surveys conducted at the Tanacross Project in 2022

At the East Taurus-McCord Creek-West Taurus complex, a 42-kilometre induced polarization and magneto telluric survey will be done with detailed mapping and soil sampling. The complex hosts many mineralized intrusions and alteration systems which are enriched with copper, gold, and molybdenum.

Figure 2: Location map of the Tanacross Project

Zach Flood, CEO of Kenorland commented in a press release: “We are very excited to be back in Alaska, with Antofagasta, advancing the Tanacross Project towards discovery. This comprehensive exploration program will create a strong foundation for future drill targeting. We believe there’s incredible potential in this fertile and target-rich environment.”

The program includes work at South Taurus of a detailed ground gravity and extremely low-frequency electromagnetic survey and soil sampling that have already been completed. The target is still an untested coincident magnetic and conductive feature associated with anomalous soil geochemistry. Surveys done in 2022 in combination with historical datasets give the company the fundamental information for drill targeting across all areas.

The approved budget for this year’s summer exploration program combined with fixed costs in 2023 totals US$2,000,000. Exploration has already begun and will continue through August and September 2022. Another update will be provided by the end of the year.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

A projected shortage of sulfuric acid could have a major impact on green technology advancement and global food security, according to a paper published in The Geographical Journal. The paper’s authors warn that without enough sulfuric acid, the development of new technologies like carbon capture and storage (CCS) and solar energy will be stalled. They also say that the world’s food supply could be at risk if this shortage continues.

Sulfuric acid is needed for a variety of industrial processes, including the production of fertilizer and other chemicals. It is also used in CCS, which is a process that captures carbon dioxide from power plants and stores it underground. Solar energy also requires sulfuric acid to create the silicon wafers that are used in solar panels.

Right now, most of the sulfur in the world comes from waste created when fossil fuels are processed to reduce emissions that cause acid rain. But as we work to decarbonize the economy to combat climate change, production of fossil fuels will go down, and so will the supply of sulfur.

Researchers from the University College of London released a paper that suggests unless we take action now to reduce our dependency on this chemical, we will need to mine exponentially more resources than we do currently.

Mining companies currently produce about 80 million tons of sulfur each year. But by 2050, the paper’s authors say we will need to mine hundreds of million tons to meet demand. This is sure to boost prices for the chemical, and could make it inaccessible for many countries.

The paper’s authors say that we need to find alternative sources of sulfur, or find ways to use less of it. They also warn that if we don’t act now, the world’s food supply could be at risk. This unique situation also presents an opportunity for the mining industry to develop new technologies that can extract sulfur from other sources, like seawater.

Lead researcher Mark Maslin stated: “Sulfur shortages have occurred before, but what makes this different is that the source of the element is shifting away from being a waste product of the fossil fuel industry. What we’re predicting is that as supplies of this cheap, plentiful, and easily accessible form of sulfur dry up, demand may be met by a massive increase in direct mining of elemental sulfur. This, by contrast, will be dirty, toxic, destructive, and expensive.”

Co-author Simon Day stated: “Our concern is that the dwindling supply could lead to a transition period when green tech outbids the fertilizer industry for the limited more expensive sulfur supply, creating an issue with food production, particularly in developing countries.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

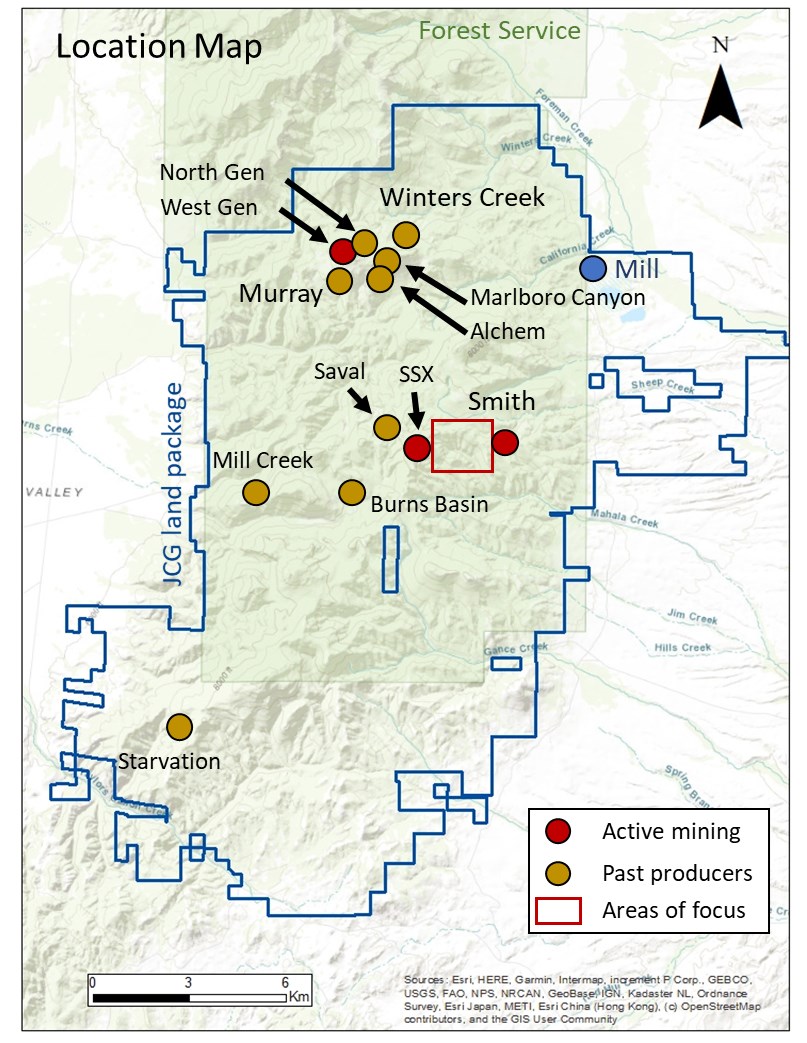

First Majestic Silver (TSX:FR) announced this morning new drill results from the ongoing exploration program at the Jerritt Canyon Gold Mine in Nevada. Roughly 120,000m of drilling is planned at Jerritt Canyon in 2022. Drilling will focus on the Smith and SSX mines, Winters Creek, Murray, Wheeler, and Waterpipe areas. The campaign is focused on short-term underground core drilling testing extensions for known ore controls. These are near active mining.

Other mid-term focused drilling is focused on validating and testing the presence of mineralized volumes near historic workings. Finally, the long-term drilling of the program will aim to make new gold discoveries in this important district.

Keith Neumeyer, President and CEO of First Majestic, commented in a press release: “Today’s exploration results continue to validate our thesis that the area between the operating SSX and Smith mines is favourable for new, near-mine gold discoveries. Hole-1102 intersected what looks like a new high-grade area on the north side of the SSX/Smith connection drift. Nine follow up drill holes are being planned to further define this potential new zone. In addition, follow up drilling at Zone 10 in the Smith mine has confirmed the presence of a high-grade pod of gold mineralization approximately 90 metres southeast from the connection drift. Over the past few months, we advanced the mine development towards this high-grade pod in anticipation of initial ore extraction in early October. Furthermore, ore production from the West Gen mine is also planned to begin in October and expected to increase the amount of fresh ore production at Jerritt to over 3,000 tonnes per day by the end of 2022.”

Highlights from the Company’s ongoing exploration program are as follows:

Drilling at Smith Zone 10:

- Follow up drilling to hole SMI-LX-1112 (8.39 grams of gold per tonne (g/t Au) over 29.7m, reported May 2022) delineated a new gold mineral zone located above the water table, approximately 90m southeast of the new connection drift between the SSX and Smith mines. Geologic interpretation and modeling of the drilling results determined that the gold zone is flat-lying, similar to nearby deposits. Results from Smith Zone 10 include:

- SMI-LX-1067: 6.98 g/t Au over 17.6m

- SMI-LX-1068: 8.61 g/t Au over 12.8m

- SMI-LX-1069: 8.61 g/t Au over 24.4m

- SMI-LX-1071: 14.60 g/t Au over 13.2m

Drilling from the SSX/Smith Mine connection drift:

- SMI-LX-1102: 19.35 g/t Au over 23.2m: the intercept is approximately 75m north and 40m above the connection drift (above the current water table). The geometry of the mineralization appears to be sub-horizontal with the drilling intersecting at a low angle.

- SSX-SR-612: 10.27 g/t Au over 14.7m and 9.53 g/t Au over 13.7m: the intercepts are approximately 300m SE and 75m below the connection drift. The drill hole likely intercepted the mineralization at a low angle and may be correlated to results from hole SSX-SR-608 reported in May 2022.

Drilling at Smith:

- SMI-LX-799: 32 g/t Au over 13.7m: identified gold mineralization approximately 150m north and 15m below active mine workings. Geologic interpretation suggests that this intercept is stratigraphically controlled (sub-horizontal) and drilling has intersected it at a low angle.

Drilling at SSX Zone 5:

- Intersected mineralization approximately 100m from active mining and above the water table. The geometry of the mineralization is not yet known, a combination of sub horizontal controls along stratigraphy (for low angle intersects) and vertical controls are under investigation.

- SSX-SR-486: 6.53 g/t Au over 11.3m

- SSX-SR-490: 11.22 g/t over 35.3m

Table 1: Summary of Significant Gold Intercepts:

| Drillhole | Target | Drill type | Intercept | |||

| From (m) | To (m) | Length (m) | Au (g/t) | |||

| SMI-LX-1067 | Smith | DDH | 126.6 | 138.0 | 11.4 | 5.30 |

| SMI-LX-1067 (2) | Smith | DDH | 149.4 | 167.0 | 17.6 | 6.98 |

| SMI-LX-1068 | Smith | DDH | 127.1 | 134.7 | 7.6 | 9.13 |

| SMI-LX-1068 (2) | Smith | DDH | 151.5 | 164.3 | 12.8 | 8.61 |

| SMI-LX-1069 | Smith | DDH | 120.7 | 145.1 | 24.4 | 8.61 |

| SMI-LX-1071 | Smith | DDH | 93.3 | 106.5 | 13.2 | 13.76 |

| SMI-LX-1071 (2) | Smith | DDH | 110.0 | 116.1 | 6.1 | 3.60 |

| SMI-LX-1071 (3) | Smith | DDH | 119.2 | 132.9 | 13.7 | 14.60 |

| SMI-LX-1071 (4) | Smith | DDH | 137.5 | 143.7 | 6.2 | 8.88 |

| SMI-LX-1102 | Smith | DDH | 91.7 | 114.9 | 23.2 | 19.35 |

| SMI-LX-799 | Smith | DDH | 171.3 | 185.0 | 13.7 | 32.00 |

| SSX-SR-486 | SSX | DDH | 116.7 | 128.0 | 11.3 | 6.53 |

| SSX-SR-490 | SSX | DDH | 81.7 | 90.8 | 9.1 | 13.03 |

| SSX-SR-490 (2) | SSX | DDH | 98.5 | 133.8 | 35.3 | 11.22 |

| SSX-SR-612 | SSX | DDH | 266.6 | 281.3 | 14.7 | 10.27 |

| SSX-SR-612 (2) | SSX | DDH | 284.5 | 298.2 | 13.7 | 9.53 |

DDH is abbreviation for Diamond Drill Hole;

From, To and Length indicated in metres, true width of the mineralized intercepts is unknown at this time.

Source: First Majestic Silver

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Copper bounced back over $8,000 a tonne last week on hopes that the worst of China’s economic downturn was behind it, but the bellwether metal is now flirting with a bear market once again — with a nearly 20% decline so far in 2022.

On Tuesday, while releasing its full-year results, BHP based on 2021’s total production of just over 1 million tonnes, warned that prices might significantly weaken in the next few years. That trend could then reverse in the second half of the decade.

Short-term supply gains may be possible thanks to new output from projects and expansion in central Africa, Chile, Peru, and Mongolia. These should come on stream through 2024 and keep the market well-supplied. The company’s guidance for a 4%-16% increase in copper production in the next 12 months and rising primary supply should dovetail with the higher scrap levels supported by increasing end-of-life pool size out of China.

Electrification is the major factor driving projections for a spike in demand from the mid-to-late 2020s. Renewable power generation, electric vehicles, and energy storage are all expected to grow exponentially, with copper an essential input.

Grade declines, water constraints, resource depletion, and increasing complexity at known developments all have an effect on costs. This is why companies have been reluctant to invest in new copper projects, even as the price of the metal has more than tripled since early 2016

Grade decline is the natural result of the depletion of easy-to-find, high-grade ore deposits. This has been a factor in the rising costs of copper production for a number of years.

Water constraints are an increasingly important issue for the copper industry, especially in Chile, the world’s largest producer. Record low rainfall in many parts of the world have created challenges for both mines and smelters that require large volumes of water to operate.

BHP also noted that capital spending and demand in the space are disconnected right now. For an upside case for demand by 2030, the industry’s capex could hit $250 billion. However, S&P Global notes that spending in 2024 for most copper producers in the list of the 80 largest miners (excluding diversified miners) could be roughly half that of the calendar year 2014.

Uncertainty in the copper market due to fluctuating demand from China, the world’s largest consumer, has been a key factor weighing on prices in recent years. While Chinese demand is expected to continue to grow in the long term, it is unlikely to do so at the same breakneck pace as in previous years.

China’s economic growth is expected to slow in the coming years as the country grapples with structural problems such as high levels of debt. This could lead to weaker demand for copper in the short term but a continued upward trend through the rest of the decade, coinciding with BHP’s overall outlook.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

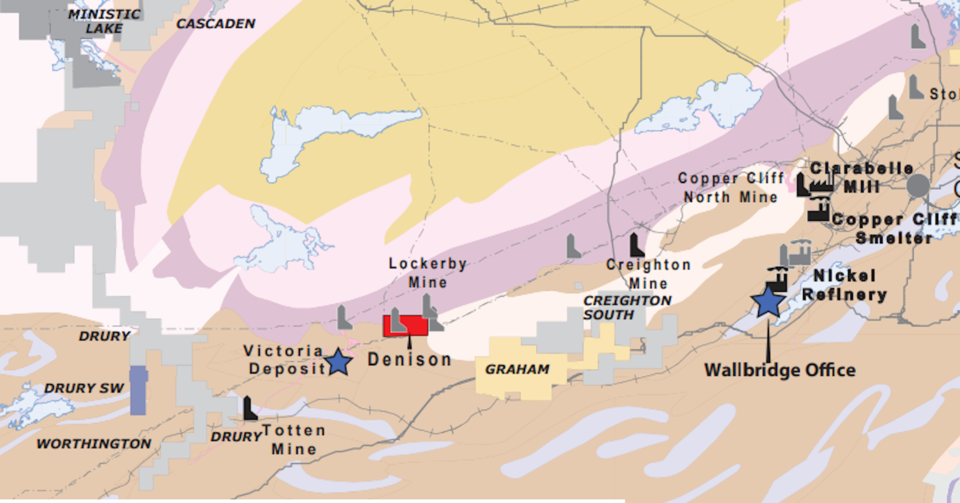

Magna Mining (TSXV: NICU) has agreed to buy 100% of Lonmin Canada Inc.’s (Loncan) assets, which include the Denison project and the inactive Crean Hill nickel-copper-PGM mine, both located in Ontario’s Sudbury basin.

Magna’s CEO Jason Jessup stated to investors: “We believe that this is, in every sense of the word, a transformational acquisition, and it is a key milestone in our vision to become the next mid-tier nickel producer in Canada.”

The Denison project, which includes the old Crean Hill mine, is 37 kilometers east of the company’s advanced-stage Shakespeare operation. From 1906 to 2002, Crean Hill was dug over three periods and yielded 20.3 million tonnes of ore containing 1.3% nickel, 1.1% copper, and 1.6 g/t platinum-palladium-gold. Loncan announced an agreement with Vale Canada regarding the transfer and development of the Denison project in 2018 after the mine closed.

After the operations were halted, several PGM-rich regions were investigated. Recent drilling has revealed 1.69% nickel, 2.28% copper, and 2.37 g/t platinum-palladium-gold over 8.23 meters in the 99 Shaft zone, and 1.87% nickel, 0.95% copper, and 3.14 g/t platinum-palladium-gold over 6.16 meters in the 109 West zone.

According to the share purchase agreement between Magna, Loncan and current Loncan shareholders – which consists of Sibanye UK (formerly known as Lonmin Ltd., a subsidiary of Sibayne Stillwater), Wallbridge Mining (with 16.5% ownership) and other minority shareholders – the total cost for all outstanding shares of Loncan will be C$16 million. This includes a closing payment of C$13 million in cash as well as a deferred payment amounting to $3 million.

Magna has proposed to issue approximately 74 million subscription receipts of the firm at a price of C$0.27 each in a private placement, raising aggregate gross proceeds of up to C$20 million, in order to finance the purchase of Loncan and exploration and development of the Denison project.

Jessup commented further in a press release: “The Crean Hill mine was a significant producer in the Sudbury basin for more than 80 years, and we believe the Denison project has potential to add tremendous value through development of the remaining historical mineral resources and additional exploration on the property. The successful closing of this transaction will be transformative for Magna and has several potential synergies with Magna’s fully permitted, advanced-stage Shakespeare project.”

The Shakespeare property is a past-producing nickel-copper-PGM mine located 70 km southwest of Sudbury. The project has an existing NI 43-101 resource (20.3 million tonnes in the indicated category grading 0.33% nickel, 0.36% copper, 0.32 g/t platinum, 0.35 g/t palladium and 0), permits for both the construction of a 4,500 t/d mill and recommencement of open pit mining activities recommend this surrounding 180 km² land package as being highly prospective for additional discoveries of nickel, copper and PGM deposits.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

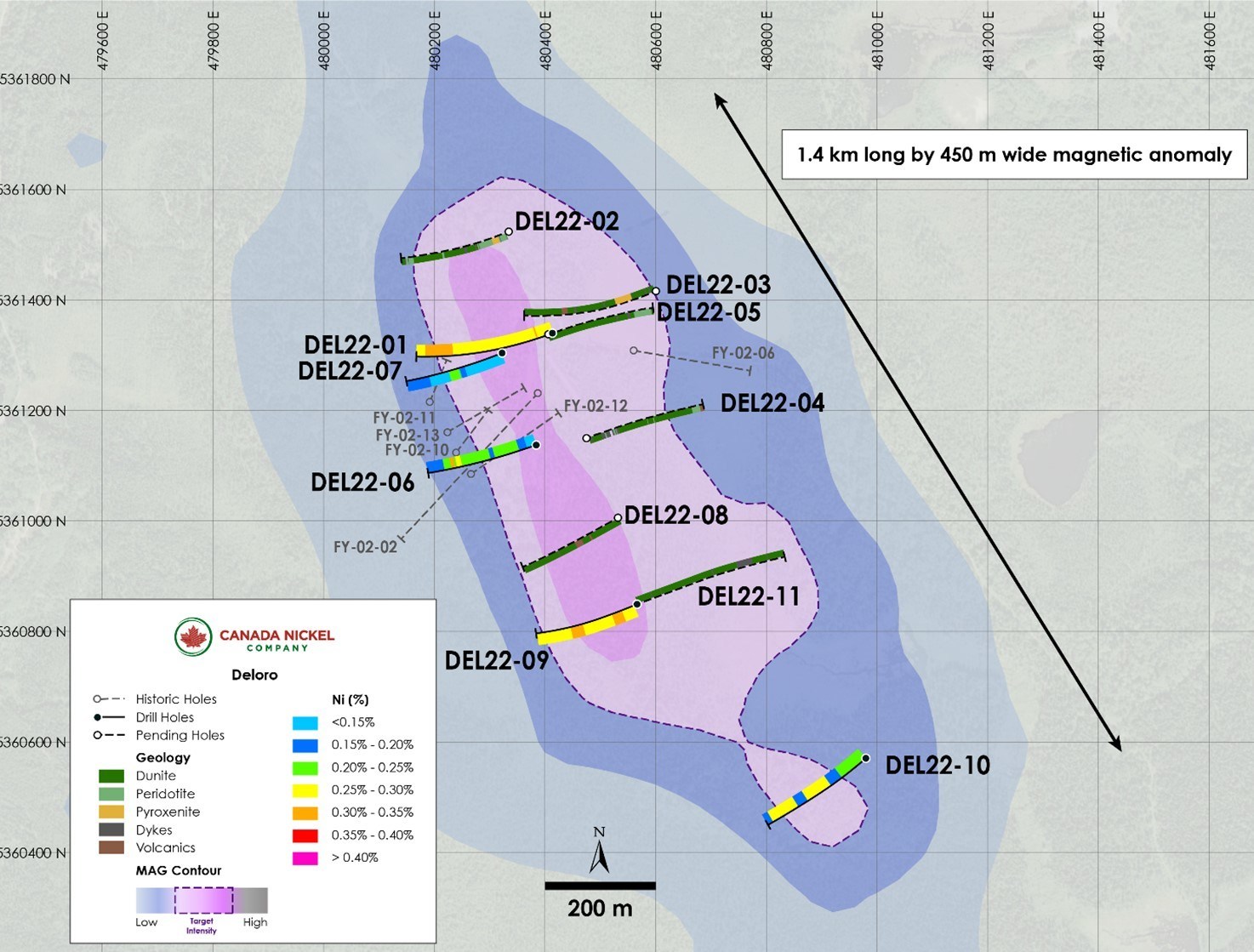

Canada Nickel Company (TSXV:CNC) recently acquired the Deloro property and has already reported a new discovery at the property. This is the second discovery at one of its two recently acquired properties, the other one being the Reid property. Drill intersected 487 metres of 0.25% nickel with a high-grade section close to the bottom of the hole where 0.28% nickel over 91 metres was intersected. At hole DEL 22-09, 393 metres of 0.26% nickel was intersected. The company has now released assays from 5 of the 11 holes.

In November 2021, Canada Nickel announced that it had acquired 13 properties – including Deloro and Reid. By consolidating its district-scale mining potential in the Timmins area, the company created a stronger presence for itself. These projects are located within close proximity of the company’s flagship Crawford nickel sulphide project; all falling within a 95 km radius.

Following a fresh assessment, the Crawford deposit is purported to have the fifth-largest nickel sulphide resource worldwide, weighing 1.4 billion tonnes and containing 0.24 percent nickel in the measured and indicated category and 0.23 percent nickel in the inferred category. The economic assessment of the project, based on former resource estimates, showed a 25-year operation would result in 842,000 tonnes of nickel.

Mark Selby, Canada Nickel Chair and Chief Executive Officer commented in a press release: “We are very pleased with the results from Deloro where we successfully delineated our target mineralization and grades throughout the intended geophysical target. Deloro now joins Reid as another significant, sizeable nickel discovery and we look forward to continued success as we continue exploration around our regional properties, developing what we believe has the potential to be one of the world’s leading nickel districts. We will provide further updates on drilling and our regional plans in September.”

Highlights from the assays are as follows:

- Second significant discovery from newly acquired regional properties – Reid and Deloro.

- Assay results at Deloro confirmed expected grades over entire core length of 487 metres of 0.25% nickel including 91 metres of 0.28% nickel.

- Mineralization successfully defined over 1.1 kilometres of strike length by 100 – 400 metres wide to a depth of 420 metres.

Hole DEL22-01 collared in dunite on the northern half of the target and was drilled to the southwest. The hole remained largely in dunite for a total length of 487 metres grading 0.25% nickel, with a higher-grade section near the bottom of the hole intersecting 0.28% nickel over 91 metres.

DEL22-09 collared in dunite and the hole intersected 393 metres of 0.26% nickel, including 51 metres of 0.28% nickel. The hole finished in peridotite.

DEL22-06 collared in peridotite and transitioned in composition from dunite to peridotite and intersected a total of 227 metres of mineralization – 74 metres grading 0.20% nickel starting at 54 metres and 141 metres grading 0.21% nickel starting at 140 metres including a 12-metre core length of 0.33% nickel and 0.15 g/t Pt+Pd from 248 to 260 metres. This higher-grade Pt+Pd in dunite has similar characteristics to the high-grade core in Crawford’s East Zone.

DEL22-07 collared in dunite, on section with DEL22-01, 100 metres to the west. DEL22-10 collared in dunite and remained in dunite for the majority of the hole except for minor pyroxenite and mafic dykes. The hole intersected 79 metres of 0.25% nickel 124 metres downhole, and 87 metres of 0.25% nickel at 235 metres, before intersecting intermediate volcanics at the contact.

Source: Canada Nickel Company

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

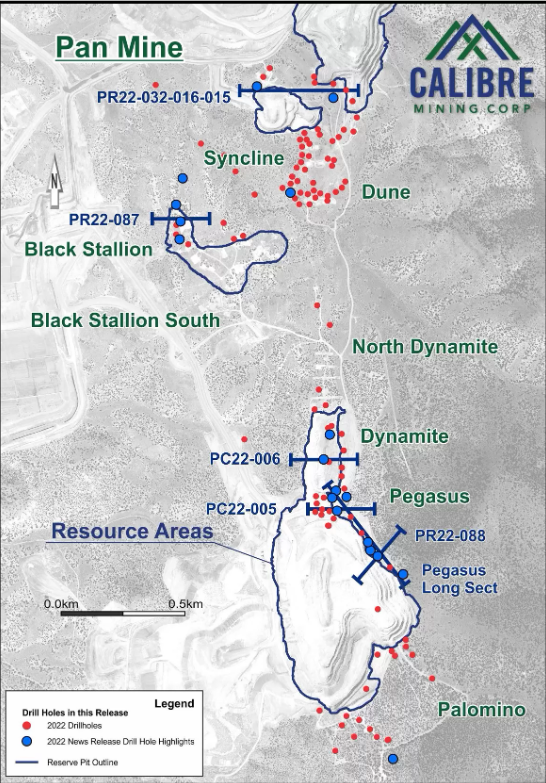

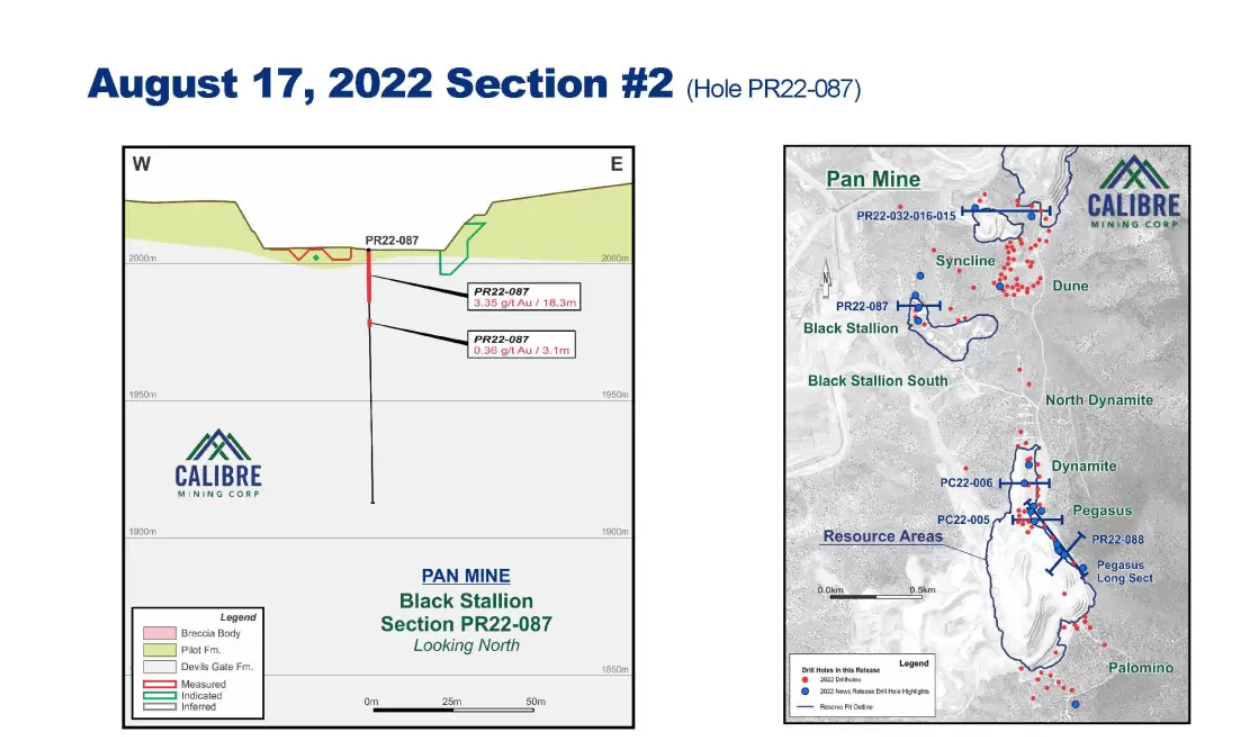

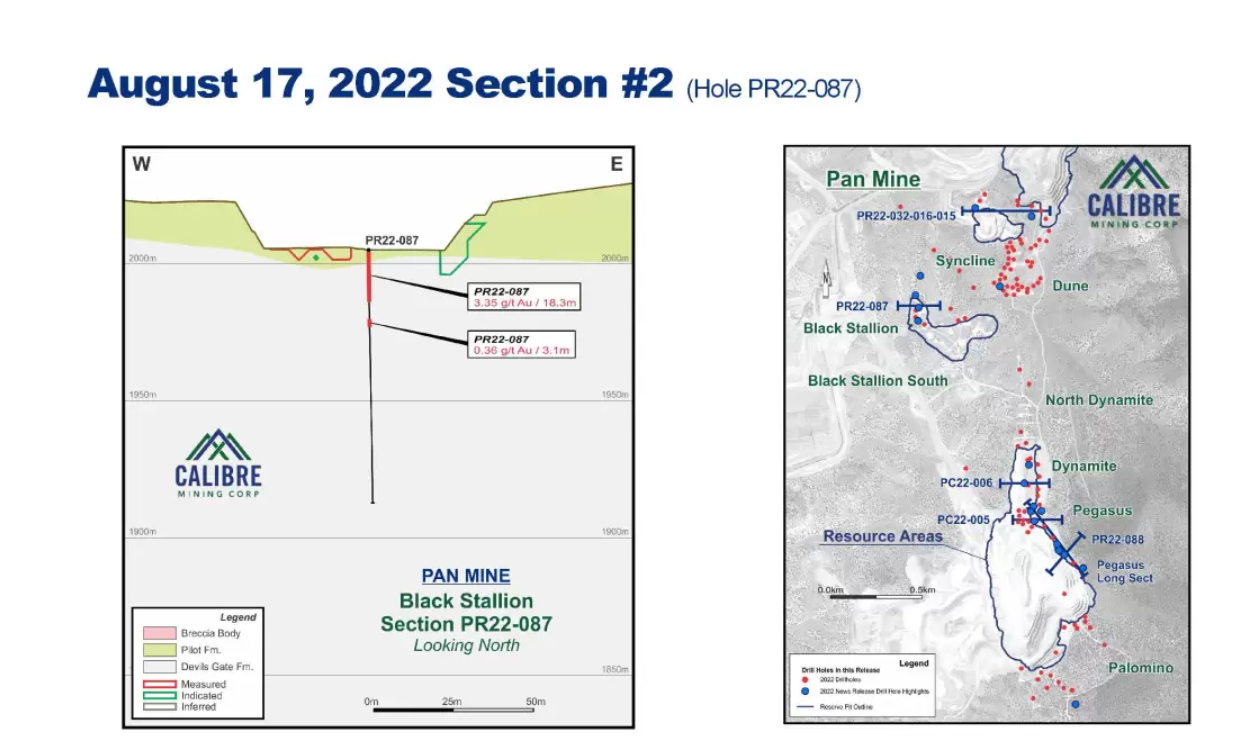

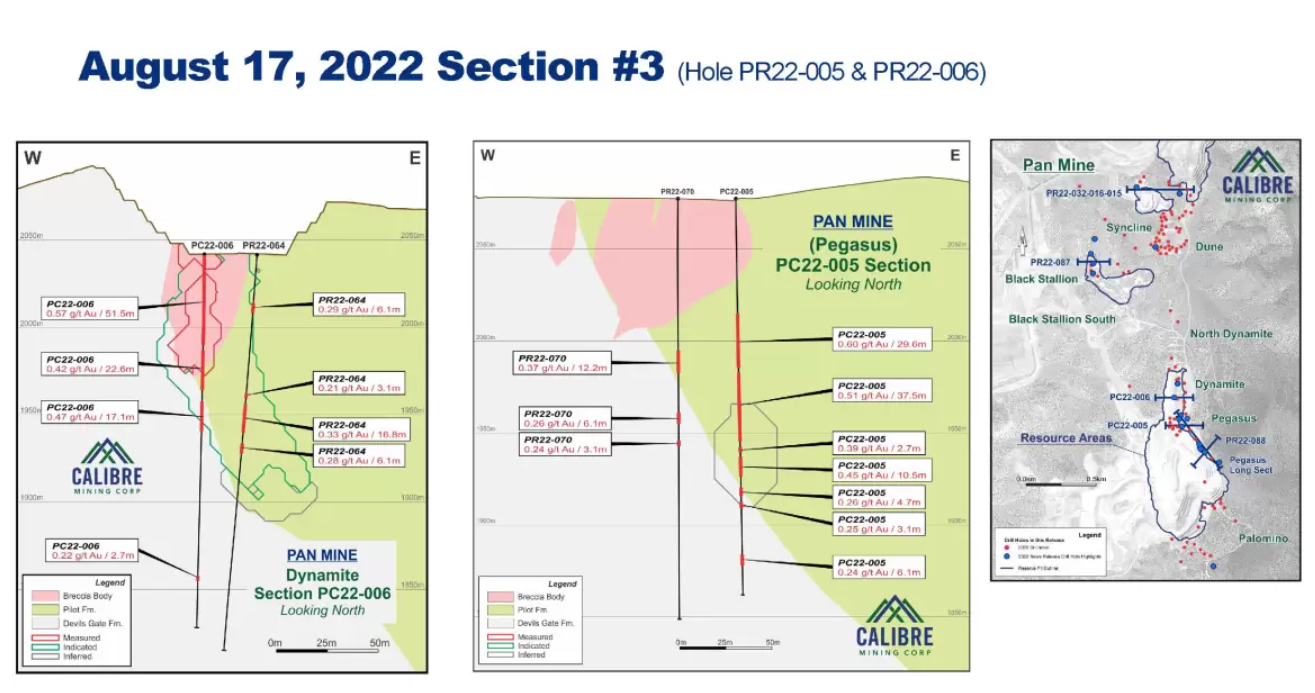

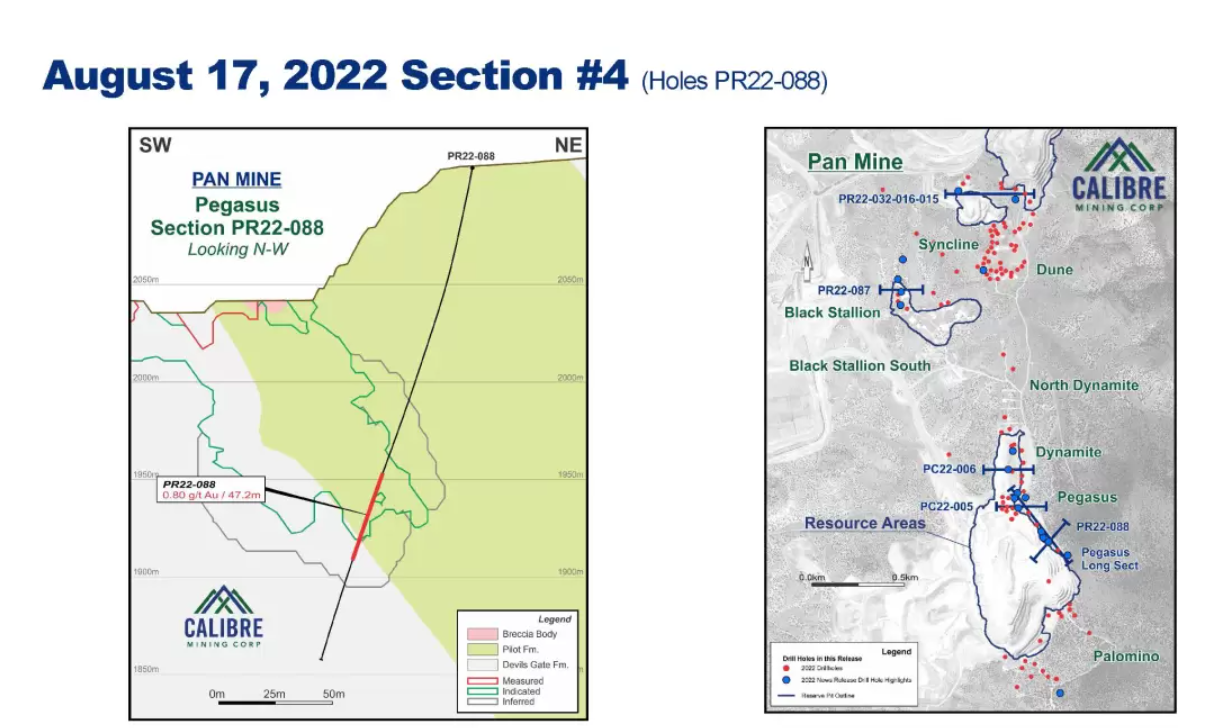

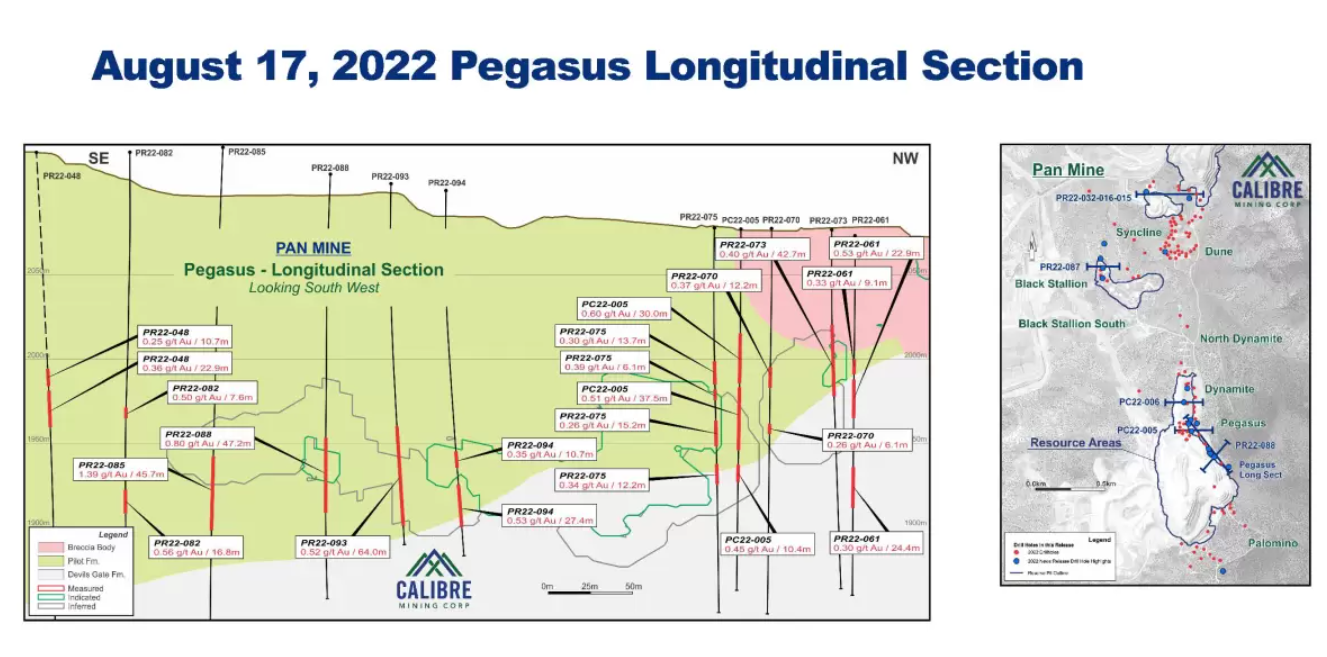

Calibre Mining (TSX:CXB) has announced new assay results from the 100%-owned Pan Mine in Nevada. Located in the prolific Battle Mountain – Eureka gold trend, ongoing resource conversion and expansion drilling has delivered promising new results. Shown below, the company believes there is a high potential for resource expansion while it focuses on converting known zones of mineralization. Calibre is currently advancing a multi-rig 85,000 metre drill program in 2022 including 50,000 metres of the drilling focused at the Pan Mine.

Darren Hall, President, and Chief Executive Officer of Calibre Mining, commented in a press release: “The recent drilling at Pan has focused on expanding mineralization along trends of known targets. Today’s results confirm our initial interpretation that numerous resource expansion and discovery opportunities exist. We continue to see excellent opportunities for growth and in some cases are seeing shallow, higher-grade zones open for further expansion. Since acquiring Fiore Gold in January, 2022 we have announced positive results and anticipate this year’s results will expand resources and lead to additional mine life.”

Highlights from the Pan Resource expansion and discovery drill program are as follows:

Black Stallion Target

- 3.35 g/t Au over 18.3 metres in Hole PR22-087; 0.93 g/t Au over 12.2 metres in Hole PR22-116; 0.82 g/t Au over 10.7 metres in Hole PR22-100; 0.50 g/t Au over 15.2 metres in Hole PR22-083; and

- Significant intercepts outside existing resources remain open to the north, east and west.

Pegasus Target

- 0.53 g/t Au over 27.4 metres in Hole PR22-094; 0.56 g/t Au over 16.8 metres in Hole PR22-082

- 0.80 g/t Au over 47.2 metres in Hole PR22-088; 0.52 g/t Au over 64.0 metres in Hole PR22-093;

- 0.60 g/t Au over 29.6 metres and 0.51 g/t Au over 37.5 metres in Hole PC22-005; and

- Several intercepts extend mineralization down-dip and along strike and are open for further expansion.

Palomino Target

- 1.06 g/t Au over 10.7 metres and 0.96 g/t Au over 10.7 metres in Hole PR22-055.

Dune Target

- 0.90 g/t Au over 22.9 metres in Hole PR22-015; 0.51 g/t Au over 15.2 metres in Hole PR21-062; and

- Near surface mineralization trending and open to the northwest confirming mineralized zones.

Syncline Target

- 1.41 g/t Au over 24.4 metres in Hole PR22-032; and

- Encountered higher grade mineralization to the northwest, outside the Syncline pit and open for expansion.

Dynamite Target

- 0.57 g/t Au over 51.1 metres in Hole PC22-006; 0.53 g/t Au over 22.9 metres in Hole PR22-061;

- 0.54 g/t Au over 15.3 metres in Hole PR22-045; 0.44 g/t Au over 30.5 metres in Hole PR22-077;

- 0.40 g/t Au over 42.7 metres in Hole PR22-073; and

- Mineralization remains open to the east where follow-up drilling is planned.

Note: All holes were drilled at angles of -45 to -90 degrees at azimuths designed to intersect targeted structures as nearly as possible to perpendicular when possible. Some drill holes and intercepts reported here did not cross mineralization perpendicularly, and do not represent exact ‘true widths’.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

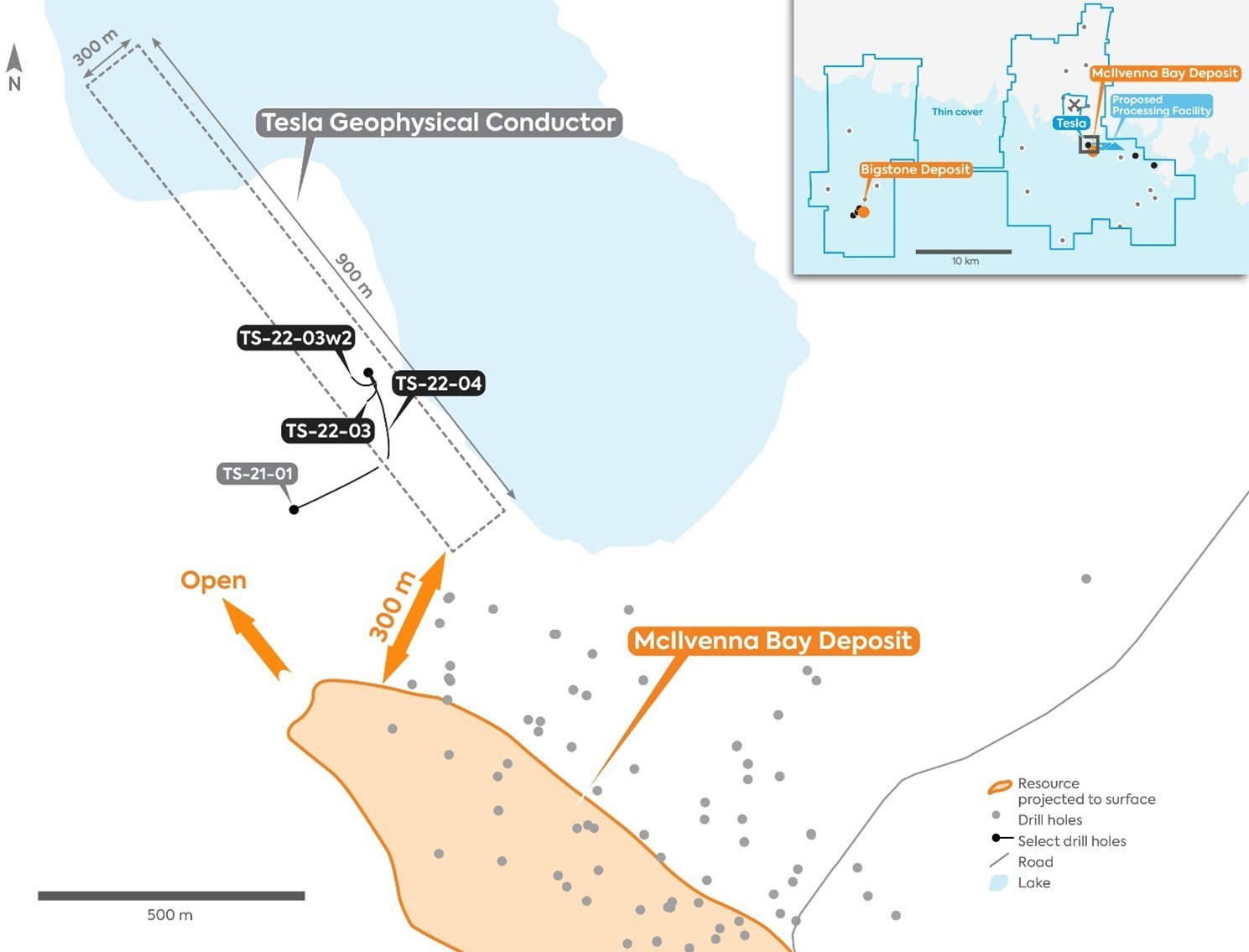

Foran Mining (TSXV:FOM) has announced additional results from ongoing drilling at its recently discovered Tesla Zone on the McIlvenna Bay Project in Saskatchewan. The results include the remaining intercepts from the initial discovery hole and initial assays from a wedge hole testing up-dip potential.

Dan Myerson, Foran Mining Executive Chairman & CEO, commented in a press release: “To achieve these success rates and intercept these robust zones, at such an early stage in a new discovery, is truly remarkable. These results demonstrate the growing potential at the near-mine newly discovered Tesla Zone, and further illustrates the rarity of this tremendous scalable discovery. Additionally, and what is even more exciting, is that we have encountered high-temperature alterations at Tesla, which could correlate with higher-grade gold and copper values, similar to other base and precious metal deposits within the Flin Flon Terrane. Our exploration team and strategy are working, and we are successfully unlocking this prolific district on our path towards building Canada’s next great mining camp, we look forward to sharing more exciting exploration results later this year, throughout 2023, and beyond.”

The complete assay results for the Tesla Zone discovery hole (TS-22-03) have been received, and the company has created a significant expansion of the mineralized intervals. Foran also received results for the first wedge hole (TS-22-03w2) which were completed as follow-up on the discovery. This wedge hole intersected the Tesla mineralization to the north of the original drill hole.

Highlights from the results are as follows:

- Assay results from wedge hole 30m up-dip (TS-22-03w2) include:

- 11.9 metres (“m”) grading 6.2% Copper Equivalent (“CuEq”), including 5.4m at 10.2% CuEq;

- 17.2m at 1.0% CuEq, including 3.9m at 1.4% CuEq; and

- 3.9m at 4.1% CuEq, including 2.2m at 5.9% CuEq.

- Assays from initial discovery hole (TS-22-03) now complete:

- Expanded preliminary intersection (12.4m at 1.8% CuEq) to 31.4m (from 12.4m), at 1.3% CuEq, including 1.2m at 8.5% CuEq; and

- Also expanded preliminary intersection of 3.1m at 2.2% CuEq to 7.1m at 1.5% CuEq, including 1.6m at 3.8% CuEq.

- Up-dip step-out hole TS-22-04 testing 200m strike appears to have intersected the Tesla Zone, with assays pending.

- Drilling provides further validation of the original geophysical modelling of a 900m strike x 300m wide conductor with true widths estimated to be ~25-50m (Figure 1).

The full assay results from TS-22-03 indicate that the Tesla Zone consists of continuous disseminated and fracture filling sulphide mineralization containing significant copper and zinc over approximately 100m of core length with several high-grade intervals of semi-massive to massive sulphide mineralization (Figure 2). Results from TS-21-01 have also been received, which contained a narrow zone of anomalous zinc mineralization near the bottom of the hole (Table 1) which appears to be located stratigraphically below the Tesla zone mineralization in TS-22-03. Additional drilling will be required to determine the significance of this mineralization.

Since the initial discovery of mineralization in the Tesla Zone, the Company has continued with follow up drilling to better understand the controls on the mineralization and the potential geometry of the zone. To date, one wedge (TS-21-03w2) has been completed from the original discovery hole and a second hole (TS-22-04) has been drilled from surface from the same drill pad, oriented to obtain a larger spacing of the intersections along the mineralized horizon. Both holes appear to have intersected the Tesla Zone.

TS-22-03w2 intersected the Tesla Zone approximately 30m northwest of TS-22-03, further validating the proposed geophysical model (Figure 3). Mineralization is of the same style as TS-22-03 with significant copper and zinc over approximately 80m before terminating at the boundary of the geophysical model.

TS-22-04 was completed from surface from the same drill pad at a shallower angle than the original hole in an attempt to obtain a spread of the intersections along the mineralized horizon. The hole intersected the mineralized horizon approximately 100m up-dip from the discovery hole and approximately 200m away from TS-22-03w2, where it encountered a zone of significant alteration and several zones of disseminated and fracture fill sulphide mineralization, indicating that the intersection lies on the periphery of the mineralization. Assays are pending from the laboratory, but it is currently interpreted that this drill hole intersected the upper margin of the Tesla Zone which is consistent with the geophysics model and helps to confirm the northeast dipping geometry of the mineralization.

Geophysical surveys outline a conductor with potential dimensions of ~900m (strike) by 300m (depth) associated with the Tesla Zone (Figure 1). The results herein confirm that this conductor is, in part at least, a well mineralized zone of copper and zinc sulphides. In order to properly test the conductor, given its geometry and location adjacent to the shoreline, future drill holes will need to be completed from Hanson Lake. An application is being finalized for a winter exploration permit that will allow for a large winter drill program to be completed targeting expansion of the Tesla zone.

Table 1 – Updated Tesla Assay Results1 (* Denotes previously released values)

| Hole | From_m | To_m | Interval_m | Cu % | Zn % | Ag g/t | Au g/t | CuEq % |

| TS-21-01 | 947.3 | 949.3 | 2.0 | 0.05 | 1.27 | 1.21 | 0.01 | 0.5 |

| TS-22-03 | 822.7 | 824.3 | 1.5 | 0.68 | 1.35 | 7.5 | 0.36 | 1.4 |

| TS-22-03 | 866.1* | 897.4 | 31.4 | 1.05 | 0.20 | 8.5 | pending | 1.3 |

| Including | 872.2* | 873.4* | 1.2* | 7.80* | 0.64* | 42.3 | 0.61* | 8.5 |

| TS-22-03 | 910.2 | 917.3* | 7.1 | 1.41 | 0.06 | 9.9 | 0.08 | 1.5 |

| Including | 915.7* | 917.3* | 1.6* | 3.57* | 0.12* | 26.8 | 0.12 | 3.8 |

| TS-22-03 | 927.1* | 928.9* | 1.8* | 1.39* | 8.99* | 17.0 | 0.13* | 4.9 |

| Including | 927.9* | 928.9* | 1.0* | 1.49* | 15.88* | 18.4 | 0.17* | 7.6 |

| TS-22-03 | 933.0* | 940.7* | 7.7* | 0.98* | 1.50* | 17.4 | 0.29* | 1.8 |

| Including | 939.2* | 940.7* | 1.6* | 0.35* | 4.16* | 14.5 | 0.32* | 2.1 |

| TS-22-03 | 948.2* | 953.1* | 5.0* | 0.71* | 2.62* | 21.8 | 0.32* | 1.9 |

| Including | 948.2* | 950.2* | 2.0* | 1.36* | 1.58* | 26.1 | 0.45* | 2.3 |

| And | 950.2* | 953.1* | 3.0* | 0.28* | 3.31* | 18.9 | 0.23* | 1.7 |

| TS-22-03 | 955.1* | 960.5* | 5.4* | 2.29* | 1.66* | 19.2 | 0.96* | 3.4 |

| Including | 959.1* | 960.2* | 1.1* | 7.19* | 3.62* | 44.2 | 3.63* | 10.4 |

| TS-22-03 | 973.4 | 974.5 | 1.1 | 0.54 | 0.06 | 4.6 | 0.16 | 0.7 |

| TS-22-03 | 977.9 | 978.6 | 0.7 | 0.74 | 0.08 | 5.2 | 0.13 | 0.9 |

| TS-22-03 | 983.2 | 984.7 | 1.5 | 1.03 | 0.13 | 9.0 | 0.12 | 1.2 |

| TS-22-03w2 | 808.1 | 812.0 | 3.9 | 3.00 | 2.72 | 20.3 | pending | 4.1 |

| Including | 809.4 | 811.6 | 2.2 | 4.23 | 3.99 | 28.1 | pending | 5.9 |

| TS-22-03w2 | 831.5 | 834.9 | 3.4 | 1.44 | 1.09 | 11.4 | 0.29 | 2.0 |

| Including | 833.8 | 834.3 | 0.6 | 3.25 | 0.60 | 23.7 | 0.86 | 4.0 |

| TS-22-03w2 | 847.0 | 849.0 | 2.0 | 2.17 | 1.19 | 30.0 | 0.74 | 3.1 |

| TS-22-03w2 | 860.9 | 871.0 | 10.1 | 1.39 | 0.32 | 12.8 | 0.29 | 1.7 |

| Including | 861.4 | 863.8 | 2.4 | 2.21 | 0.36 | 15.5 | 0.46 | 2.6 |

| TS-22-03w2 | 875.5 | 887.4 | 11.9 | 1.18 | 13.04 | 16.9 | 0.20 | 6.2 |

| Including | 882.0 | 887.4 | 5.4 | 1.66 | 22.50 | 18.7 | 0.05 | 10.2 |

| TS-22-03w2 | 887.4 | 904.5 | 17.2 | 0.86 | 0.26 | 8.2 | 0.03 | 1.0 |

| Including | 900.6 | 904.5 | 3.9 | 1.13 | 0.43 | 10.2 | 0.07 | 1.4 |

| TS-22-02w2 | 919.4 | 921.8 | 2.4 | 2.47 | 1.33 | 20.7 | pending | 3.1 |

| Including | 920.2 | 920.7 | 0.6 | 6.50 | 3.02 | 51.9 | pending | 7.9 |

| TS-22-03w2 | 957.7 | 960.0 | 2.3 | 0.01 | 1.80 | 13.4 | 0.08 | 0.8 |

| Including | 957.7 | 958.5 | 0.8 | 0.01 | 2.38 | 26.0 | 0.13 | 1.2 |

| TS-22-03w2 | 977.0 | 979.0 | 2.0 | 0.07 | 2.04 | 6.5 | 0.19 | 1.0 |

| TS-22-03w2 | 1017.8 | 1021.8 | 4.0 | 0.02 | 1.04 | 4.3 | 0.10 | 0.5 |

Note: Intersections are not true width. Intervals generally composited using a 0.5% Cu cut-off grade. 1Copper Equivalent values calculated using metal prices of $4.00/lb Cu, $1.50/lb Zn, $20.00/ounce Ag and $1,800/ounce Au.

Summer Drill Program Underway

Additional follow-up drilling at Tesla is planned for later in the year after the winter freeze. Foran’s helicopter-supported 7,000m summer drill program is currently underway at the Marconi Prospect located on the Bigstone Property, 25km west of McIlvenna Bay. It is currently anticipated that the summer program will continue into the fall and also include further testing of the Flinty Prospect, located 7km to the southeast of McIlvenna Bay, and other regional target areas in the Hanson Lake District as the Company continues to build on its exploration pipeline to support the potential development of a central milling facility envisioned for the McIlvenna Bay deposit.

Source: Foran Mining Corporation

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Fuse Cobalt (TSXV:FUSE) announced that it has reached an agreement in principle (AIP) as a first step toward supplying cobalt raw material to Electra Battery Materials in Canada.

The non-binding MoU, which was signed by Fuse Cobalt and the Electra-owned cobalt sulfate plant in Temiskaming Shores, Ontario, will see Fuse Cobalt provide the raw material for the operation.

The transaction is contingent on the two firms signing a final agreement, which will be subject to Fuse satisfying certain conditions. There are several items that must be addressed in order to produce cobalt material suitable for further processing to battery-grade cobalt sulphate at Electra’s refinery, as well as the completion of a bankable feasibility study.

The cobalt raw material will most likely come from one of Teledyne or Glencore Bucke’s Ontario discovery operations, which are both located near Electra’s cobalt plant.

The MoU is also expected to set the groundwork for future transactions between the two Canadian firms. Electra will purchase up to two kilo-tonnes per year (KTA) of raw cobalt material from Fuse Cobalt’s “Glencore Bucke” and/or “Teledyne” operations for its cobalt camp refinery. The two companies might also work together to explore means of extracting copper by-products on a profit-sharing basis.

Fuse CEO Robert Setter commented in a press release: “This MOU is the first step towards a potential Definitive Agreement to supply cobalt raw material for Electra’s nearby cobalt refinery and sets out the terms by which we will exchange information with Electra to advance a potential transaction involving the supply of cobalt raw materials. The end result of this collaboration will be the execution of a Definitive Agreement to provide cobalt feedstock to the Electra Cobalt Refinery, which is roughly a stone’s throw away from our two cobalt exploration properties in Ontario.”

Electra CEO Trent Mell commented in the press release: “Having a domestic source of cobalt raw material produced ethically and with low-carbon emissions will help us to better address the demand for onshore EV battery materials.”

In a statement, Fuse Cobalt also commented: “The transaction is expected to provide a ‘Made in North America’, low greenhouse gas emissions cobalt sulfate solution, capable of supplying the continent’s growing lithium-ion battery supply capacity.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

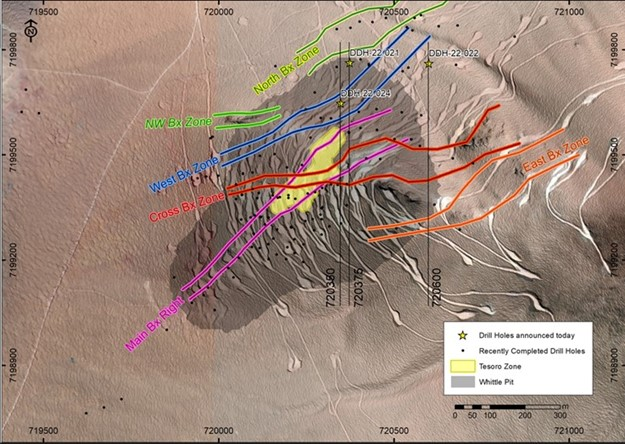

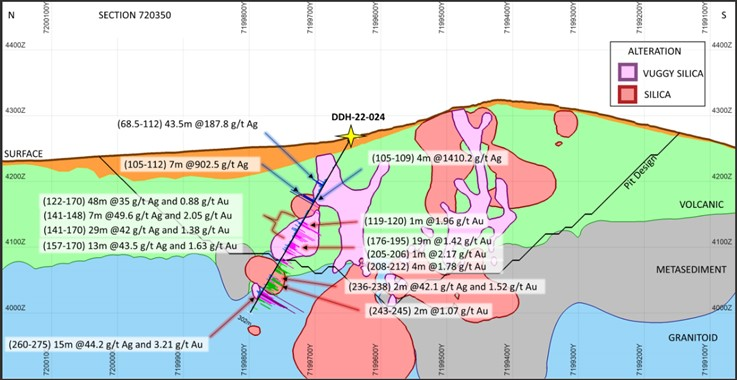

AbraSilver Resource Corp. (TSXV:ABRA) has announced new assay results from three of its new diamond drill holes at the Phase II drill program at the company’s Diablillos property in Salta Province, Argentina. The near-surface intercept includes silver grades of 1,423 g/t AgEq (20.3 g/t AuEq) over 4 metres.

The 80 km2 Diablillos property is in the Puna region of Argentina, and was originally acquired from SSR Mining in 2016. The property is located in the southern extension of the Altiplano of southern Peru, Bolivia, and northern Chile, a notable silver mining region. The Oculto mineral zone is the most advanced on the property with over 100,000 metres drilled to date.

John Miniotis, President and CEO, commented in a press release: “We are very encouraged by the numerous near-surface, high-grade silver results intersected in the Northeast zone by these latest drill holes, as well as the underlying high-grade gold intercepts. These results will be included in the updated Mineral Resource estimate which will be announced later this year. It is evident that the multiple zones of mineralisation being encountered in the Northeast zone should add substantially to our overall Mineral Resource estimate which continues to grow rapidly.”

Dave O’Connor, Chief Geologist, also commented: “These new results, drilled in the Oculto Northeast zone, help clearly demonstrate the continuity of numerous mineralized breccia zones in this highly prospective area. What is particularly encouraging is the newly discovered shallow, high-grade silver mineralization encountered in holes 21 and 24, which is expected to allow for a substantial expansion of the conceptual open pit towards the northeast.

Highlights from the results are as follows:

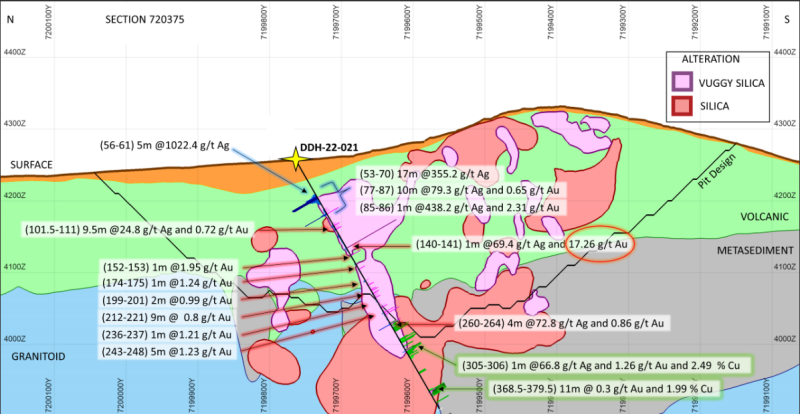

- DDH 22-021 intersected a near-surface, high-grade silver interval of 17m at 365 g/t AgEq (5.2 g/t AuEq – comprised of 355 g/t Ag and 0.14 g/t Au) in oxides starting at a down-hole depth of only 53 metresThis included a bonanza-grade 5m interval of 1,037 g/t AgEq (14.8 g/t AuEq – comprised of 1,022 g/t Ag 0.21 g/t Au);

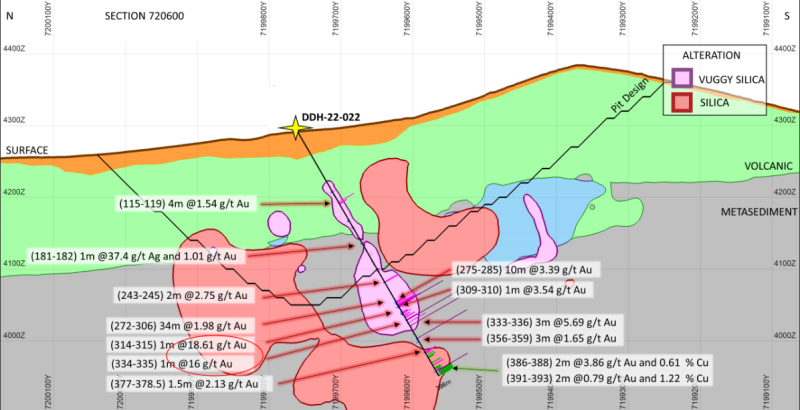

- DDH 22-022 intersected multiple zones of high-grade gold mineralization, including a broad intercept of 34m at 156 g/t AgEq (2.2 g/t AuEq – comprised of 18 g/t Ag and 1.98 g/t Au);

- DDH 22-024 intersected near-surface, high-grade silver mineralization including a broad intercept of 43.5m grading 196 g/t AgEq (2.8 g/t AuEq – comprised of 188 g/t Ag and 0.11 g/t Au) in oxides starting at a down-hole depth of only 68.5 metres. The hole included a bonanza-grade interval of 4m at 1,423 g/t AgEq (20.3 g/t AuEq – comprised of 1,410 g/t Ag 0.18 g/t Au);

Figure 1 – Plan View of Drill Results

Table 1 – Diablillos Drill Result Highlights

(Intercepts greater than 2,000 gram-metres AgEq shown in bold text):

| Drill Hole | From (m) | To (m) | Type | Interval (m) | Ag

g/t |

Au g/t | Cu % | AgEq1 g/t | AuEq1 g/t | ||

| DDH-22-021 | 53 | 70 | Oxides | 17.0 | 355.2 | 0.14 | – | 365.0 | 5.21 | ||

| DDH-22-021 | Includes | 56 | 61 | Oxides | 5.0 | 1,022.4 | 0.21 | – | 1,037.1 | 14.82 | |

| DDH-22-021 | 77 | 87 | Oxides | 10.0 | 79.3 | 0.65 | – | 124.8 | 1.78 | ||

| DDH-22-021 | Includes | 85 | 86 | Oxides | 1.0 | 438.2 | 2.31 | – | 599.9 | 8.57 | |

| DDH-22-021 | 101.5 | 111 | Oxides | 9.5 | 24.8 | 0.72 | – | 75.2 | 1.07 | ||

| DDH-22-021 | 119 | 131 | Oxides | 12.0 | 24.0 | 0.10 | – | 31.0 | 0.44 | ||

| DDH-22-021 | 140 | 141 | Oxides | 1.0 | 69.4 | 17.26 | – | 1,277.6 | 18.25 | ||

| DDH-22-021 | 212 | 221 | Oxides | 9.0 | 11.0 | 0.80 | – | 67.0 | 0.96 | ||

| DDH-22-021 | 243 | 248 | Oxides | 5.0 | 20.4 | 1.23 | – | 106.5 | 1.52 | ||

| DDH-22-021 | 260 | 264 | Oxides | 4.0 | 72.8 | 0.86 | – | 133.0 | 1.90 | ||

| DDH-22-021 | 305 | 306 | Sulphides | 1.0 | 66.8 | 1.26 | 2.49 | 359.9 | 5.14 | ||

| DDH-22-022 | 115 | 119 | Oxides | 4.0 | 5.4 | 1.54 | – | 113.2 | 1.62 | ||

| DDH-22-022 | 243 | 245 | Oxides | 2.0 | 26.1 | 2.75 | – | 218.6 | 3.12 | ||

| DDH-22-022 | 272 | 306 | Oxides | 34.0 | 17.5 | 1.98 | – | 156.1 | 2.23 | ||

| DDH-22-022 | Includes | 275 | 285 | Oxides | 10.0 | 26.1 | 3.39 | – | 263.4 | 3.76 | |

| DDH-22-022 | 309 | 310 | Oxides | 1.0 | 23.0 | 3.54 | – | 270.8 | 3.87 | ||

| DDH-22-022 | 314 | 315 | Oxides | 1.0 | 5.6 | 18.61 | – | 1,308.3 | 18.69 | ||

| DDH-22-022 | 333 | 336 | Oxides | 3.0 | 17.8 | 5.69 | – | 416.1 | 5.94 | ||

| DDH-22-022 | Includes | 334 | 335 | Oxides | 1.0 | 17.5 | 16.00 | – | 1,137.5 | 16.25 | |

| DDH-22-022 | 356 | 359 | Oxides | 3.0 | 17.0 | 1.65 | – | 132.5 | 1.89 | ||

| DDH-22-022 | 377 | 378.5 | Oxides | 1.5 | 0.9 | 2.13 | – | 150.0 | 2.14 | ||

| DDH-22-022 | 386 | 388 | Sulphides | 2.0 | 24.4 | 3.86 | 0.61 | 344.8 | 4.93 | ||

| DDH-22-022 | 391 | 393 | Sulphides | 2.0 | 8.4 | 0.79 | 1.22 | 164.1 | 2.34 | ||

| DDH-22-024 | 68.5 | 112 | Oxides | 43.5 | 187.8 | 0.11 | – | 195.5 | 2.79 | ||

| DDH-22-024 | Includes | 105 | 112 | Oxides | 7.0 | 902.5 | 0.31 | – | 924.2 | 13.20 | |

| DDH-22-024 | Includes | 105 | 109 | Oxides | 4.0 | 1,410.2 | 0.18 | – | 1,422.8 | 20.33 | |

| DDH-22-024 | 122 | 170 | Oxides | 48.0 | 35.0 | 0.88 | – | 96.6 | 1.38 | ||

| DDH-22-024 | Includes | 141 | 170 | Oxides | 29.0 | 42.0 | 1.38 | – | 138.6 | 1.98 | |

| DDH-22-024 | 176 | 195 | Oxides | 19.0 | 31.8 | 1.42 | – | 131.2 | 1.87 | ||

| DDH-22-024 | 208 | 212 | Oxides | 4.0 | 29.8 | 1.78 | – | 154.4 | 2.21 | ||

| DDH-22-024 | 236 | 238 | Oxides | 2.0 | 42.1 | 1.52 | – | 148.5 | 2.12 | ||

| DDH-22-024 | 243 | 245 | Oxides | 2.0 | 32.8 | 1.07 | – | 107.7 | 1.54 | ||

| DDH-22-024 | 260 | 275 | Oxides | 15.0 | 44.2 | 3.21 | – | 268.9 | 3.84 | ||

Note: All results in this news release are rounded. Assays are uncut and undiluted. Widths are drilled widths, not true widths. True widths are estimated to be approximately 80% of the interval widths.

1AgEq & AuEq calculations for reported drill results are based on USD $1,750/oz, $25.00/oz Ag & $3.00/lb Cu. The calculations assume 100% metallurgical recovery and are indicative of gross in-situ metal value at the indicated metal prices.

Source: AbraSilver Resource Corp.

Figure 2 – Cross Section (Looking Northeast) with Highlighted Intercepts in Hole DDH 22-021

Figure 3 – Cross Section (Looking Northeast) with Highlighted Intercepts in Hole DDH 22-022

Figure 4 – Cross Section (Looking Northeast) with Highlighted Intercepts in Hole DDH 22-024

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Ned Goodman, a driving force in the Canadian mining industry, has passed away and left an indelible legacy. He was known for his geological expertise and business acumen, which he applied to build several successful mining companies. In addition to being an outstanding member of the philanthropic community, Montreal-born Goodman was considered one of the leading architects of Canada’s investment management industry. We would like to take this opportunity to remember all that he has done for Canadian mining and reflect on his remarkable career.

Goodman began his career by studying for a BSc in geology at McGill University in Montreal. However, after being laid off in 1960 from Noranda, he went on to attain an MBA from the University of Toronto. Following his designation as a Chartered Financial Analyst in 1967, Goodman founded Beutel, Goodman & Company, Ltd., and began offering pension funds and private client investment advice, specializing in mining and oil investment. Goodman and his partner Seymour Schulich became experts at finding junior companies with good management and prospective mineral resource projects, and raising funds for them.

His career coincided with and helped boost the booming 1980’s gold-mining industry in Canada, and Goodman ultimately became the largest shareholder and chairman of International Corona. He was an early investor in Kinross, and had leadership roles in Repadre (renamed IAMGOLD), Dundee Precious Metals, FNX Mining Company (renamed Quadra FNX Mining), and that company’s nickel deposit discovery and development in Ontario’s Sudbury camp.

A leading figure in the mining industry, he was the driving force behind making Canada’s mining industry into the international powerhouse it is today, and leaves a legacy of success in the industry. His legacy was such that Brock University in Canada renamed its business school the Goodman School of Business in 2012, the first time the university changed the name of one of its faculties in its history.

Friends, family, and colleagues remember him fondly, as Ned Goodman was a man with a major presence in the lives of those around him. Friends refer to him as a “titan” in their dealings with him, with Douglas McCorkle noting: “Ned touch my life in so many ways as an advisor at Dundee. He was quick to smile, offer advice and to stop and say hello. The amazing thing to me was that he always remembered my name. The world has lost a titan among men and he will be greatly missed. To his family I offer my deepest condolences and prayers that Jehovah will bring you peace in this time. To Ned I say, Shalom my friend.”

His character was never lost on those who knew him best, and was something he brought to every aspect of his life: “I was honoured to know Ned Goodman. He was a remarkable man. Ned had great energy and insight into many businesses, from mining to financial services and innovation. His legendary business acumen allowed him to create massive success with his many ventures, including Dundee Corp., Dundee Wealth, International Corona and many other ventures. He always showed up early and worked late. He told me he remained particularly proud of his contributions to Canadian law and business with his leadership in the International Corona Resources v. Lac Minerals case, which stands as the leading case by the Supreme Court of Canada on fiduciary duties and confidential relationships to this day. However, Ned’s most striking features were his outstanding work-ethic, character and deep courage of his convictions. Ned will be missed and remembered for his many profound contributions, his love of family, countless kindnesses to friends and his great business successes. Please accept my family’s sincere condolences to his family on this profound loss,” wrote Jon Aikman in a memorial message.

Yesterday, the expansion of the Timmins regional land holdings and the presentation of an exploration update on the Timmins properties were announced by HighGold Mining (TSXV:HIGH). The Company’s commanding land position has been increased by 25% thanks to recent claim staking and acquisition, bringing it to 335 square kilometres.

The new acquisition comprises of 255 strategically located mining claims covering 56 square kilometres (22 square miles), which connect to HighGold’s existing Timmins South mining claims and border Newmont’s Dome mine property, located seven kilometres to the northwest.

The Timmins South property is home to several high-grade gold occurrences. In the 1930s, a 12-meter shaft was sunk into a 1.37m wide quartz vein at the Bay Lake gold display, which produced composite samples of 150.8 g/t Au, 43.2 g/t Au and 35.17 g/t Au as well as historical grab specimens of 766.2 g/t Au and 229.7 g/t Au.

Drilling will be planned at a later date once the company’s exploration plans for the Timmins projects include low-cost field surveys to create and perfect drill targets. Under present market conditions, HighGold is taking a methodical capital expenditure approach with the goal of significantly advancing its understanding of prospects in preparation for drilling at a future date.

Geology mapping, prospecting, and rock sampling have been done at the Munro-Croesus and Timmins South projects. The emphasis has been on prospects with known historical exploration shafts and possible stratigraphy, as well as the findings achieved during the winter Munro Croesus drilling program.

At Munro-Croesus, a 63-line km DCIP ground geophysical survey was done during the winter, with modelling, inversion, and data interpretation continuing. Preliminary findings indicate numerous chargeability and resistivity anomalies that need to be investigated further, including chargeability highs that are close to, and in line with, the new Argus Zone.

An 85-line kilometre overwater seismic survey was recently completed on Frederickhouse Lake to map the depth of the sediment and bedrock, which will aid drill planning and interpretation of bedrock geology and structures. Frederickhouse Lake is a big, shallow (2-4 meters deep on average) man-made lake that straddles several promising geology prospects at the intersection of the Pipestone Fault and Timmins Mine trend. In summer or winter, drilling may be done by barge.

CEO of HighGold Darwin Green commented in a press release: “This acquisition builds on HighGold’s vision of creating one of the most dominant land positions in the Timmins gold camp. Our focus is underexplored portions of this world-class gold environment underpinned by high-potential geology. The Timmins assets provide shareholders with exposure to low-cost greenfield exploration in the shadow of headframes that is complimentary to the Company’s flagship Johnson Tract high-grade gold project, Alaska.”

Recap of 2022 Munro-Croesus Winter Drill Program and Final Drill Results

The 2022 Winter Drill Program at Munro-Croesus was completed in early April with a total of 7,401 meters drilled in 33 holes. Highlights include the discovery of near-surface bulk tonnage style gold mineralization at the new Argus Zone and the intersection of new high-grade quartz veins near the historic Croesus Gold Mine.

Argus Zone

- 136m at 0.54 g/t Au, starting at a vertical depth of 70 meters, including 62.8m at 0.79 g/t Au, and including 4.5m at 4.88 g/t Au in MC22-110 (see Company news release dated May 9, 2022).

- Five of six drill holes drilled at the Argus Zone intersected significant intervals of mineralization which is open to expansion in multiple directions, including to the west toward the intersection of the Argus Zone trend with the regional Pipestone Fault.

Croesus Vein Extension

- 13.40 g/t Au over 0.5m within a broader 4.80m interval grading 3.60 g/t Au (hole MC22-96) from an intersection of the Croesus Vein, 100m northeast of the Croesus Mine (See Company new release dated March 20, 2022).

- 14.00 g/t Au over 0.6m within a broader 2.60m interval grading 3.42 g/t Au (hole MC22-92) from a new quartz vein zone intersected 370m northwest of the Croesus Mine.

- These discoveries are a ‘proof of concept’ of the Company’s geological and structural models which highlight the potential for the Croesus Vein system to continue to the northeast along a major regional structure, and also that the prospective Croesus Flow could host multiple analogues to the Croesus Vein along strike.

The Company has received all final assay results from the remaining 19 holes from the 2022 Munro-Croesus Winter Drill Program with encouraging results from the first-pass drilling of four other prospects. Highlights include:

Walhart Prospect

- 0.29 g/t Au over 26.30m (hole MC22-99)

- 6.00 g/t Au over 0.60m (hole MC22-100)

JM Prospect