![]()

Copper prices are on track for their strongest monthly gain in a year, driven by significant supply disruptions even as economic data from China points to ongoing weakness in manufacturing. On Tuesday, copper futures eased on the London Metal Exchange, falling 0.6% to $10,347 a ton by 12:53 p.m. local time. Despite the dip, the metal remains up 4.5% for September, placing it close to a 16-month high. Prices are also up 18% so far in 2024, with levels briefly topping $11,000 a ton in May. Other base metals, including aluminum, zinc and nickel, showed little movement on the day.

The sharp rise in copper prices has been supported by growing supply concerns. Freeport-McMoRan Inc. recently declared force majeure at its massive Grasberg mine in Indonesia after about 800,000 tons of mud inundated underground tunnels. The incident killed at least two workers and forced the company to lower production guidance for both this year and next.

Societe Generale analysts noted that the outage could prolong copper’s rally, calling the commodity “on fire.” They added that if the Grasberg halt persists alongside steady consumption, the global copper market could be heading toward its largest annual deficit since 2004. As part of its longer-term operations, Freeport has also reached a deal to divest a 12% stake in its Indonesian unit to the government at no cost. According to CNBC Indonesia, the divestment forms part of an agreement that extends Freeport’s license to operate Grasberg through 2041.

Demand Trends and Trade Policy Impacts

The surge in prices comes after a turbulent year marked by both supply outages and policy developments. The Trump administration’s trade measures—including country-specific levies and targeted tariffs on certain U.S. copper-product imports—have added uncertainty to the market.

At the same time, expectations of stronger demand remain. Analysts point to two structural drivers: the ongoing global energy transition, which relies heavily on copper for renewable power and electrification, and the rapid expansion of artificial-intelligence data centers, which require significant amounts of the metal for power infrastructure.

Weak Economic Signals From China

Balancing the supply-side disruptions are signals of softening demand from the world’s largest consumer of copper. New economic data released Tuesday showed China’s factory activity contracted for a sixth consecutive month, the longest downturn since 2019.

The official manufacturing purchasing managers’ index registered at 49.8 in September, below the 50-point threshold that separates growth from contraction. The reading offered the first indication that industrial weakness extended through the end of the third quarter.

With prices near multi-year highs, the copper market remains caught between short-term volatility and long-term structural pressures. Analysts stress that the pace of recovery in China’s manufacturing sector will play a critical role in determining whether demand can offset the widening gap in global supply. For now, supply snarls such as the Grasberg disruption appear to be dominating investor sentiment. Whether this trend continues may depend on how quickly output can be restored and how effectively policymakers in Beijing address the slowdown in industrial activity.

Nevada Lithium Resources (TSXV:NVLH) saw its shares surge on Wednesday following the announcement of a partnership with South Korea’s Hydro Lithium aimed at advancing extraction of critical minerals from its flagship Bonnie Claire project in Nevada. The stock gained as much as 23% by midday, pushing the Vancouver-based company’s market capitalization to C$46.8 million ($33.7 million).

Partnership Details

The collaboration was formalized through a letter of intent signed on September 7. The agreement outlines the potential use of Hydro’s proprietary technologies, developed by CEO Dr. Uong Chon, for the recovery of lithium and other elements designated as critical minerals in the United States. The framework also extends beyond Bonnie Claire, with provisions for joint work on additional North American projects.

Hydro Lithium currently operates a facility in Geumsan-gun, South Korea, with an annual production capacity of 3,600 tonnes of battery-grade lithium hydroxide and lithium carbonate. At Hydro, Dr. Chon has developed technologies including CULH, which produces battery-grade lithium chemicals, and CULX, designed to extract lithium from natural resources.

In a statement accompanying the partnership news, Dr. Chon emphasized the significance of applying CULX to the U.S. market: “The US hosts numerous potential sources of critical minerals, including lithium, many of which may pose challenges to economically viable extraction. Our proprietary technology, CULX, addresses these challenges.”

Bonnie Claire Project Economics

Nevada Lithium CEO Stephen Rentschler said the company will evaluate Hydro’s technologies alongside the economic projections recently updated for Bonnie Claire. The project, a sediment-hosted lithium-boron deposit, has undergone extensive study in the past three years, including the discovery and expansion of a deeper mineralized zone.

A preliminary economic assessment (PEA) released in early August outlines an underground mining operation using a hydraulic borehole method. Production is projected at 2.92 million tonnes of lithium-bearing material annually, grading 4,500 parts per million. From this, the operation could generate 62,354 tonnes of lithium carbonate equivalent and 129,533 tonnes of boric acid each year.

The PEA estimates a 61-year mine life, with pricing assumptions of $24,000 per tonne for lithium carbonate and $950 per tonne for boric acid. Under these conditions, Bonnie Claire would deliver an after-tax net present value (at an 8% discount rate) of $6.83 billion, marking a fourfold improvement compared to a 2021 assessment. The study also projects an internal rate of return of 32.3% and payback on the $2.1 billion initial capital investment in less than three years.

Rentschler also highlighted the scale of the Nevada deposit, noting in an August 6 press release that “Bonnie Claire has emerged as one of the world’s largest and highest-grade sedimentary-hosted lithium and boron deposits, and remains open for expansion. The potential for even higher grades and volumes could positively impact the PEA economics already demonstrated.”

The CEO also drew attention to Dr. Chon’s earlier role in developing PosLX, a lithium extraction technology now used by South Korea’s POSCO, underscoring the technical experience being brought into the Nevada project.

Nevada Lithium gained full control of Bonnie Claire in 2023 after previously holding it under a 50/50 joint venture with Iconic Minerals (TSXV: ICM). With ownership consolidated, the company is pursuing partnerships and technology collaborations to accelerate development.

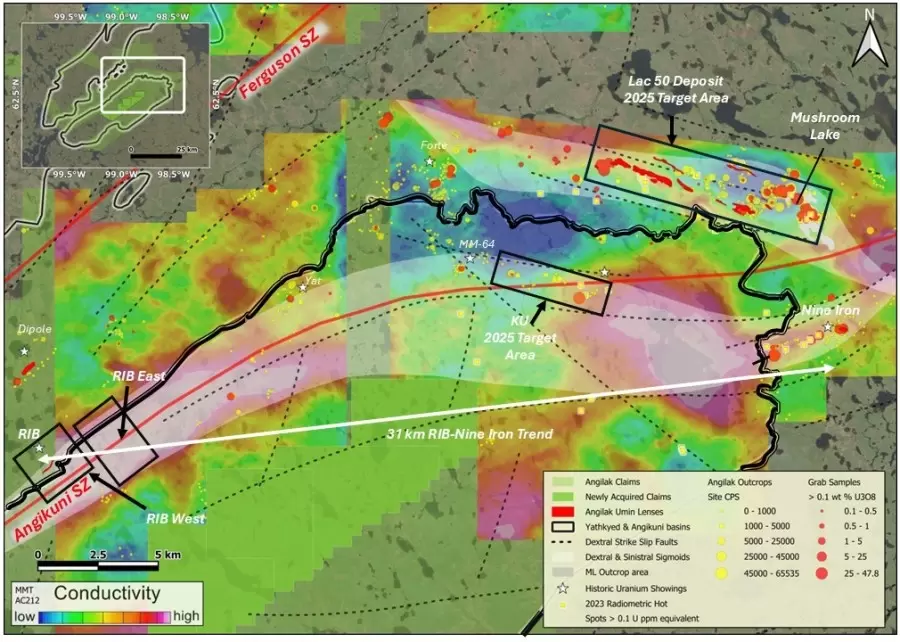

Atha Energy (TSX.V: SASK; FRA: X5U; OTCQB: SASKF) has announced its third uranium discovery of the year following maiden drilling at the RIB West target within the company’s 100%-owned Angilak Uranium Project in Nunavut, Canada. The update comes alongside news that the company has completed an oversubscribed financing, raising $11,499,928.30 through an underwritten private placement of special warrants.

Troy Boisjoli, CEO commented in a press release: ” The newest discovery along the 31 km long RIB-Nine Iron Trend – at RIB West – is the Company’s third discovery of the 2025 Angilak Exploration Program. This is an unprecedented feat from a greenfield exploration program targeting uranium discovery and speaks to the metal endowment at the Angilak Project area, beyond the Lac 50 Deposit area and ATHA’s top tier technical teams’ ability to plan and execute on its thesis. We continue to see the hallmarks of a generational bull market for uranium and based on ATHA’s continued exploration success over the last two years, the Company is well positioned to accelerate uranium discovery and build value for this cycle .”

Cliff Revering, VP Exploration also commented in a press release: ” We are very excited about the results emerging from the RIB regional target area, including another discovery along the RIB West trend and the continued expansion of the mineralized strike length along the RIB East trend. To date, we have drill-tested only a relatively small proportion of the prospective trends within the RIB area, with all completed holes intersecting uranium mineralization associated with graphitic structural corridors. All prospective trends remain open along strike and at depth. We are also very encouraged by the accuracy of the EM inversion model provided by Expert Geophysics in locating graphitic structural corridors associated with uranium mineralization. This model has been highly valuable in guiding our targeting strategy in the RIB area, and in highlighting numerous additional prospective trends that have yet to be drill-tested. “

Highlights from the results are as follows:

- ATHA closes previously announced CAD $11.5 Million Over-Subscribed Bought Deal (See detail below, “Underwritten Private Placement”);

- First two drill holes completed at the RIB West Discovery successfully intersected uranium mineralization, including high-grade, over a strike length of ~340 m (Figure 2);

- Results represent the third new discovery of uranium mineralization – beyond the Lac 50 Deposit Trend – during the 2025 Angilak Exploration Program, within the Angikuni Basin along the 31 km RIB-Nine Iron Trend (Figure 1);

- RIB East Discovery is currently defined by eight mineralized drill holes, intersecting shallow uranium mineralization (<275 m depth), the five latest holes extend mineralization from 400 m to a strike length of ~750 m (Figure 2). Based on EM Inversion modelling (see below), RIB East now has prospective strike length of more than 5 km, which remains largely untested by drilling;

- In August 2025, Expert Geophysics Ltd. utilized the MMT survey data acquired in 2024 to complete Advanced Electromagnetic Inversion modelling (“EM Inversion”) across 12 km of the 31 km long RIB-Nine Iron Trend, focused on the RIB East and West Discovery areas. The EM Inversion has proved successful in mapping out multiple stacked conductors, including numerous interpreted north-south and east-west trending cross cutting structures. Drilling at both RIB East and West has demonstrated the EM Inversion is accurately mapping graphitic structural corridors which are associated with uranium mineralization To date the Company has only explored a small proportion of the 12 km long prospective EM Inversion model at RIB East and West. The Company will be completing additional EM inversion modelling over the remaining 62% of the RIB-Nine Iron Trend where MMT data was acquired in 2024;

- Through the end of the 2025 Angilak Exploration Program, the Company will be focused on targeting newly derived EM Inversion anomalies, including the newly identified north-south and east-west cross cutting trends;

- The 2025 Angilak Exploration Program is on-going, to date, only ~55% of expected diamond drillhole results have been announced.

Financing Completed

The $11.5 million offering was conducted by a syndicate of underwriters led by Stifel Canada, which acted as lead underwriter and sole bookrunner. Red Cloud Securities Inc. and Paradigm Capital Inc. also participated in the syndicate. The financing included the full exercise of the underwriters’ option. Proceeds are expected to support Atha’s ongoing exploration efforts at Angilak and related projects.

Third Discovery of 2025 at RIB West

The latest drilling results confirm a new discovery at RIB West, making it the third discovery from Atha’s 2025 Angilak Exploration Program. Two drill holes have been completed at this target, located about 1.5 kilometers west of the previously defined RIB East Discovery.

-

RIB_W-DD-001 intersected 2.1 meters of composite mineralization. Within this interval, 0.5 meters contained high-grade uranium with a peak response of 18,485 counts per second (CPS).

-

RIB_W-DD-002, drilled roughly 340 meters northeast along strike from the first hole, intersected 8.5 meters of composite mineralization over a broad interval between 204.8 and 269.5 meters depth. The mineralization was associated with a graphitic structural zone.

Together, the two drill holes demonstrate uranium mineralization potential continuity across at least 340 meters of strike length at RIB West. The majority of this prospective corridor remains untested.

Expansion of Mineralization at RIB East

Exploration has also advanced at RIB East, where the company has now completed eight drill holes in total. All holes have intersected uranium mineralization. With the latest results, the potential strike length of mineralization has been extended from approximately 400 meters to about 750 meters.

The RIB East Discovery remains open both along strike and at depth. Large sections of the conductive trend associated with this discovery have not yet been drill-tested.

Geophysics Modelling Results

In addition to drilling, Atha Energy received results in mid-August from advanced electromagnetic (EM) inversion modelling performed by Expert Geophysics Ltd. The modelling covered 12 kilometers of the 31-kilometer-long RIB–Nine Iron Trend, concentrating on the RIB East and West discovery areas.

The EM Inversion work was based on magnetotelluric (MMT) survey data collected in September 2024. According to the company, the modelling successfully mapped multiple stacked conductors, with both north-south and east-west cross-cutting trends identified. Drilling at both RIB East and RIB West has confirmed that the EM Inversion accurately outlines graphitic structural corridors associated with uranium mineralization.

2025 Exploration Context

The RIB West discovery marks the third new discovery of Atha’s 2025 exploration program at Angilak. Alongside the expansion of mineralization at RIB East, the results highlight the broader potential of the RIB–Nine Iron Trend. With large portions of the trend still untested, further drilling and geophysical analysis are expected to guide additional exploration targets.

Copper markets held their ground on Monday and early this weee, as traders are watching the latest developments at one of the world’s largest copper mines against ongoing supply constraints and firm demand. Three-month copper futures on the CME traded above $10,000 per ton ($4.6125 per pound), slipping 0.3% on the day. In London, prices hovered just under $10,000 per ton, maintaining most of Friday’s advance. Market participants attributed the stability to uncertainty surrounding the future of Freeport McMoRan’s Grasberg mine in Indonesia, which has been shuttered since a mud flow accident earlier this month.

The incident at Grasberg, the second-largest copper producer globally, occurred two weeks ago when seven workers were trapped underground. Freeport confirmed on Monday that the bodies of two workers have been recovered, while five remain unaccounted for. The company stated that operations will remain suspended while search and recovery efforts continue.

The prolonged shutdown raises questions about the near-term balance of global copper supplies. Analysts noted that an extended suspension at Grasberg could significantly tighten the market, which has already been constrained by disruptions and underinvestment in new projects. Supply limitations have played a central role in supporting copper prices throughout 2025.

Citigroup analysts recently projected that copper is likely to close out this year with cautious stability before potentially making a more pronounced push toward $12,000 per ton in 2026. That outlook assumes that demand, particularly from electrification and infrastructure projects, will remain resilient while supply challenges persist.

The Grasberg mine, a critical component of global copper output, has been at the center of market attention since Freeport announced the temporary suspension. With uncertainty over the timeline for resuming production, traders are closely monitoring developments to gauge the potential impact on inventories and pricing trends.

For now, prices remain elevated compared to historical levels, reflecting the market’s sensitivity to supply shocks. Whether the Grasberg situation evolves into a longer-term disruption may prove decisive for copper’s trajectory heading into next year.

Trident Resources (TSXV:ROCK, OTCQB: TRDTF) has announced an expansion of its inaugural drill exploration program at the company’s 100%-owned Contact Lake Gold Project in Saskatchewan.

The program, originally designed for 5,000 metres of diamond drilling, has been increased to more than 6,500 metres across 18 to 20 drill holes. According to the company, the decision was based on both drilling progress and visual indications of mineralization observed so far. Trident confirmed it has over C$11 million in treasury and is fully funded for the expansion.

Jonathan Wiesblatt, Chief Executive Officer of Trident, commented in a press release: “Due to the early visual indications of mineralization and cost-effective execution of the ongoing drilling program, Trident is adding an additional ~1,500 metres of drilling, bringing the total initial diamond drilling program to ~6,500 meters. The additional metres will be focused on the following:

- Expanding the known footprint of the deposit by drilling underneath the old mine workings, following up on historical drill holes which intersected high grade gold, and

- Closing the gap between the current known mineralization and its extension both down dip and laterally. The Company believes this program has the potential to add to the current know geological model with a minimal amount of additional drilling and positively impact the resource potential of the project.

Further, we expect ample news flow in the coming months from this drill program, technical report updates, and continued consolidation of properties in this prolific gold district.”

Highlights from the results are as follows:

- Excellent progress is being made with the drilling and costs are coming in lower than expected with nearby infrastructure helping to make the drilling more cost-efficient

- Encouraging visual mineralization has been seen in numerous drill holes prompting an expansion in the drilling program

- Additional ~1,500m drilling (~30%) increase to the current 5,000m program for a total over 6,500m in 18-20 drill holes planned

- The program remains fully funded with core samples being split and sent for analytical geochemical testing; assays are pending

Focus of the Drill Program

Exploration work at Contact Lake is aimed at confirming historical gold grades while also testing for new mineralized zones adjacent to and beneath historical underground mine workings. The additional 1,500 metres of drilling will specifically target:

-

Expanding the footprint of the deposit beneath old mine workings by following up on earlier drill holes that intersected high-grade gold.

-

Closing gaps in known mineralization, both laterally and at depth.

Company executives stated that the extra metres are intended to enhance the geological model of the project with minimal additional drilling. Trident also expects the results to potentially improve resource potential and generate steady news flow over the coming months, including technical report updates and ongoing property consolidation in the gold district.

Geological Context

Several drill holes in the program are designed to test continuity between the historical underground mine workings and the unmined BK3 Gold Zone, which lies about 50 metres to the northeast of current drilling. These holes intersected the Bakos shear at the predicted location, cutting through a broad zone of alteration and veining that extended from the hanging wall through the shear zone into the footwall.

The company indicated that the remainder of the drill program will also investigate shallow targets and test for deeper extensions of the Main Zone beneath the old underground mine.

Oversight and Standards

Cornell McDowell, P.Geo., reviewed and approved the technical information under National Instrument 43-101 standards. McDowell, who is not independent, visited the property multiple times in 2025 to assess historical infrastructure and assist with drill hole planning.

The drill program is being managed by Terralogic Exploration and incorporates a quality assurance and quality control system. Health and safety protocols mandated by the province are being followed, with participation from members of the Lac La Ronge Indian Band in the field program.

Marketing Arrangements

In addition to exploration updates, Trident also clarified details of a marketing arrangement originally disclosed in May. The company engaged Resource Stock Digest (RSD) for two investor relations and marketing programs, both starting May 28, 2025.

-

The first program is a three-month awareness campaign costing USD $115,000, paid upfront.

-

The second is a featured company sponsorship with an initial three-month term at USD $10,000 per quarter, set to run for 18 months unless terminated with 30 days’ notice.

The total upfront payment for both programs was USD $125,000.

Trident Resources said upcoming updates will include results from the expanded drill program, revisions to technical reports, and further property consolidation efforts in the Contact Lake area, a region historically known for gold mining activity.

Glencore (LON:GLEN) has held discussions over the potential sale of a stake in its flagship Kamoto Copper Company (KCC) mine in the Democratic Republic of Congo (DRC), showing a potential change in strategy for the commodities trader that has long considered the project a cornerstone of its African operations. KCC, one of the world’s largest combined copper and cobalt producers, yielded 191,000 tons of copper and 27,000 tons of cobalt in 2024. Despite those figures, the mine has been hindered by operational difficulties, falling cobalt prices, and a protracted dispute with Congolese authorities over billions of dollars in royalties and taxes.

While Glencore has not launched a formal sales process, it has signaled to companies including Rio Tinto Group that it is open to selling a controlling stake, according to people familiar with the matter. The Swiss-based company previously rejected an unsolicited bid from New York-based Orion Resource Partners, which was working in partnership with Abu Dhabi’s ADQ, but sources said recent talks with Orion and others have intensified.

U.S. Strategic Interests

The possible sale of KCC is unfolding against the backdrop of broader negotiations between the United States and the DRC over a minerals and infrastructure partnership. Washington has made access to critical minerals — particularly cobalt, copper, and rare earths — a policy priority amid growing concern about China’s dominant role in the sector.

The U.S. International Development Finance Corp. (DFC) is in talks to establish a mining investment fund with Orion, Bloomberg reported this week. Three people familiar with the matter said the DFC could participate in a potential KCC deal through that partnership. A senior State Department official declined to address the specifics of any sale but emphasized Washington’s commitment to encouraging U.S. investment in Congo and strengthening cooperation with African partners in the critical minerals sector.

Congo is the world’s second-largest copper source and accounts for about 75% of global cobalt production. Glencore remains the only major Western company with substantial cobalt operations in the country, while Chinese firms and Kazakhstan’s Eurasian Resources Group dominate the industry. Overproduction has weighed heavily on cobalt prices, but demand from the defense and energy industries has prompted the U.S. to consider stockpiling supplies as a safeguard.

Glencore’s decision to explore options for KCC also comes at a time when the company faces investor frustration over its performance. KCC has failed to reach its full production potential, while Glencore’s overall copper output has been declining. Compounding the situation, the group has seen its coal revenues fall and has struggled with a crisis in metals processing and refining, contributing to a nearly 20% drop in its share price over the past year. The company holds a 70% stake in KCC. The remainder belongs to Congo’s state-owned Gecamines and the Congolese government.

Royalties Dispute and Sanctions Issues

Another complication in any sale is the royalty arrangement tied to sanctioned Israeli businessman Dan Gertler. Gertler, who has long-standing ties in Congo’s mining sector, is entitled to a 2.5% royalty on KCC’s net revenues, as well as payments from Glencore’s Mutanda mine and ERG’s Metalkol operations. The U.S. Treasury sanctioned him in 2017, alleging he accumulated wealth through opaque and corrupt mining and oil deals, charges Gertler denies. He has never been charged with a crime.

Western investors have been hesitant to commit capital to Congolese projects partly due to the risk of indirectly engaging with a sanctioned individual. Several options are being discussed to resolve the matter, including a lump-sum buyout of Gertler’s royalties, transferring them back to Gecamines, or leaving Glencore with a large enough stake to continue paying the royalties without involving new buyers. Gertler has shown a willingness in principle to divest his Congolese royalties, participate in an audit, and accept a U.S. license that could lift sanctions under certain conditions. The value of his royalties could amount to hundreds of millions of dollars.

Despite ongoing talks, apparently some people close to the negotiations cautioned that there is no guarantee of a deal. The outcome may depend not only on price but also on resolving disputes with the Congolese government and addressing the sanctions-related complications.

The United States has deepened its push to secure critical minerals outside Chinese control by supporting an expansion project at a copper and cobalt mine in Zambia.

On Thursday, the US Trade and Development Agency (USTDA) awarded a $1.4 million grant to Metalex Africa, a subsidiary of US-based Metalex Commodities, to fund a feasibility study at the Kazozu mine in Zambia’s North-Western Province. The study will evaluate the potential to increase production by up to 25,000 metric tonnes of copper and cobalt concentrates annually. The grant is part of a broader collaboration between Washington and Lusaka to strengthen mining output and infrastructure links. USTDA officials said the project is expected to create opportunities for US companies to supply materials, equipment, and expertise while also connecting Metalex with American buyers.

“USTDA’s partnership with Metalex will help ensure that US industries can reliably access the inputs they need to remain secure, competitive, and prepared to meet the challenges of the future,” acting director Thomas R. Hardy said in a statement. Metalex chief executive Ayo Sopitan described the award as a milestone. According to Sopitan, the funding will help define project phases, expand resource estimates, and establish the feasibility of scaling up the Kazozu operation. The initiative is being carried out in partnership with Zambian firm Terra Metals.

Strategic Context

The move comes as the United States positions itself against China’s long-standing dominance in Africa’s mining sector. Beijing controls nearly all global processing and refining capacity for copper and cobalt, key inputs for electric vehicles and renewable energy technologies. In Zambia specifically, Chinese companies have steadily increased their footprint, most recently through JCHX Mining’s acquisition of an 80% stake in the Lubambe copper mine.

Washington has responded by promoting alternatives such as the Lobito Corridor, a transport and trade initiative spanning Angola, Zambia, and the Democratic Republic of Congo (DRC). The corridor revolves around a 1,700-kilometre railway stretching from Angola’s Atlantic port of Lobito to the DRC’s mining hub in Kolwezi, with plans for an extension into Zambia’s Copperbelt Province.

US Commitments in Africa

The investment in Kazozu is one piece of a larger US-backed effort to secure mineral supply chains and diversify Africa’s trade routes. During President Joe Biden’s term, the US International Development Finance Corporation committed around $550 million for railway and port upgrades tied to the Lobito Corridor. The Millennium Challenge Corporation has also directed funding toward rural road construction and agricultural improvements in Zambia.

Private US investment has been part of the strategy as well. KoBold Metals, supported by investors such as Bill Gates and Jeff Bezos, has pledged to develop its Mingomba copper and cobalt project as a key anchor along the Lobito rail line.

Shifting the Global Supply Chains

By investing in feasibility studies and infrastructure, Washington is working to establish a secure supply of critical minerals for US industries while offering an alternative to Chinese-backed projects. The Kazozu expansion, if found viable, could strengthen Zambia’s mining output and provide a new source of copper and cobalt for international markets. For both countries, the project is an effort to combine resource development with infrastructure investment, linking Zambia more directly to global buyers while advancing US ambitions to reduce dependence on China’s mineral supply chain.

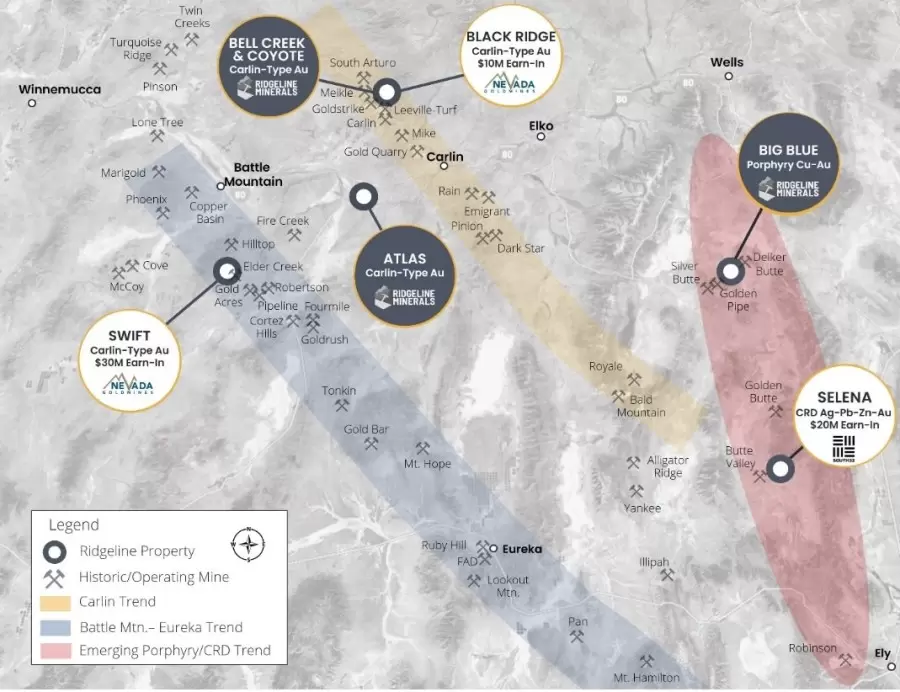

Ridgeline Minerals (TSXV: RDG; OTCQB: RDGMF; FSE: 0GC0) has provided detailed updates on its ongoing exploration drill programs at three projects in north-central Nevada: Swift, Black Ridge, and Selena. These projects are being advanced under separate earn-in agreements with major industry partners Nevada Gold Mines (NGM) and South32 Limited.

Chad Peters, Ridgeline’s President, CEO & Director commented in a press release: “Drilling is progressing smoothly across our three partner projects with both Swift and Selena close to finishing up the first deep core tails of their respective programs. NGM has also recently completed a single framework drill hole at Black Ridge, which is on-trend of NGM’s Leeville Mine and Fallon Deposit1 to the south. We expect drilling to continue at Swift and Selena through the end of 2025 with steady news flow and assay results throughout the end of the year.”

The company confirmed that the 2025 partner-funded exploration budget totals US $9.5 million, the largest in Ridgeline’s history. The drilling programs are ongoing, with results pending at all three sites into Q4 2025 and Q1 2026.

Selena Project – Drilling Targets Sulfide CRD System

The Selena project, located in White Pine County, is being explored under an earn-in agreement with a wholly owned subsidiary of South32 Limited, with up to US $20 million in potential expenditures. Ridgeline remains the operator of the project.

Drilling at Selena began in June 2025, with the first core tail initiated in late July. The current phase includes plans to drill up to three deep core holes, totaling 4,500 meters, with a US $3.45 million budget. The holes are targeting a highly conductive Magnetotellurics (MT) anomaly identified at the Chinchilla Sulfide CRD (carbonate replacement deposit) target earlier in the year.

South32 has reported US $573,758 in qualifying expenditures through June 30, 2025. To earn an initial 60% interest, South32 must spend a minimum of US $10 million in qualifying work expenditures by August 21, 2029.

Swift Project – Targeting High-Grade Gold Intersections

At the Swift gold project, located in Lander County, Nevada Gold Mines (NGM) is the operator under a US $30 million earn-in agreement. As of June 30, 2025, NGM has spent US $10.87 million in qualifying expenditures. The agreement requires NGM to spend at least US $20 million by December 31, 2026 to earn an initial 60% interest in the property.

Drilling is currently underway, with the first of up to five planned holes being drilled. This hole is positioned along the projected strike of a previously reported high-grade gold intercept: 1.1 meters grading 10.4 g/t gold in hole SW24-006. The current drilling focuses on a geological setting where cross-cutting fault zones intersect a modeled fold hinge located in the hanging wall of the Mill Creek thrust fault, a potential structural trap for mineralized fluids.

Details of this program were initially outlined in a company news release dated July 30, 2025.

The Black Ridge project, also in Lander County, is the second project being advanced under an earn-in agreement with Nevada Gold Mines, with up to US $10 million in potential qualifying expenditures. As of June 30, 2025, NGM has spent US $586,904 toward the agreement. NGM must spend a minimum of US $4.5 million by July 14, 2028, to earn an initial 60% interest in the property.

In August 2025, NGM completed one deep core hole targeting the lower-plate carbonate host rocks—a geological sequence associated with numerous past and current gold deposits on the northern Carlin Trend. This drill hole is the first major test of this target at Black Ridge, with assays currently pending and expected in Q4 2025.

Ridgeline noted that the Qualified Person (QP) has not verified the Fallon and Ren resources located on nearby properties and that mineralization on those sites may not be indicative of potential mineralization at Black Ridge.

Ridgeline Minerals Corp. is a mineral exploration company headquartered in Vancouver, British Columbia. The company manages a 200 km² exploration portfolio in Nevada and operates under a hybrid business model, combining wholly owned assets with strategic partnerships through earn-in agreements.

In total, these partnerships represent up to US $60 million in potential partner-funded expenditures.

With drilling underway across all three projects and results expected in the coming months, the next phase of exploration could further define the mineral potential of Ridgeline’s Nevada portfolio. The company has stated that all results will be publicly disclosed following internal review and verification, in accordance with regulatory standards.

Gold extended its historic rally on Tuesday, climbing to unprecedented levels as expectations for a Federal Reserve rate cut intensified and a weaker US dollar provided further support. Spot prices briefly touched $3,702.84 per ounce in morning trading, setting a new all-time high before easing back to around $3,685. That still placed bullion above Monday’s previous record. US gold futures saw a similar surge, reaching $3,739.90 per ounce before also retreating.

The rally came as the dollar dropped to its lowest point since July, adding momentum to an upward trend already fueled by speculation that the Fed will begin lowering interest rates this week. Market participants have largely priced in the prospect of a rate cut, a move that could strengthen gold’s appeal by reducing the opportunity cost of holding the non-yielding metal.

A Year of Record Gains

Gold has risen approximately 41% since the start of the year, outperforming the S&P 500 and even surpassing its inflation-adjusted peak from 1980. Analysts attribute the surge to several overlapping factors: strong central bank purchases, growing safe-haven flows, and a shift by some investors away from the US dollar.

Investment demand has been significant enough that major banks have revised their forecasts higher. UBS, for instance, recently raised its year-end price target for gold to $3,800.

Goldman Sachs issued an even more striking projection earlier this month, suggesting that prices could approach $5,000 per ounce if just 1% of privately held US Treasuries were reallocated into the metal.

Fed Policy in Focus

Traders are not only betting on a rate cut in September but also anticipating further reductions before year-end. A series of US economic reports has pointed to a softening labor market while showing no major surprises on inflation, reinforcing expectations of looser monetary policy. Gold tends to benefit in such environments, as lower interest rates diminish the relative attractiveness of yield-bearing assets while boosting the safe-haven case for bullion.

The combination of structural factors such as central bank accumulation and cyclical drivers like monetary easing has pushed gold into uncharted territory. Whether the metal can sustain its momentum may depend on the scale of the Fed’s rate decisions in the coming months and the extent of investor appetite to continue reallocating capital toward precious metals.

First Atlantic Nickel (TSXV: FAN; OTCQB: FANCF; FSE: P21) has announced a substantial expansion of its RPM Zone within the Atlantic Nickel Project, following new drill results that confirm increased width and scale of awaruite mineralization.

Highlights from the results are as follows:

- AN-25-07 Expands RPM Zone to 750 Meters in Width: The second hole of the Phase 2 drill program confirms a drilled width up to 750 meters wide of mineralization, with visibly disseminated awaruite grains observed throughout a 495-meter intersection.

- 400-Meter Step-Out Success: AN-25-07 was drilled on Line S2, a 400-meter step-out north from Line S1, demonstrating strong continuity of awaruite mineralization along strike.

- RPM Zone Now Measures 750 Meters Wide x 400 Meters Long: Every hole drilled at the RPM Zone has intersected large grain visibly disseminated awaruite, with mineralization now traced to depths of up to 495 meters downhole.

- Phase 2 Expansion Targeting 1 km+ Strike Length: Holes AN-25-08 and AN-25-09, drilled on Line S3, have extended the tested north-south strike length to 800 meters. The Phase 2 program is designed to test beyond 1 kilometer.

- Consistent Metallurgical Performance: To date, drilling at the RPM Zone has returned magnetically recoverable nickel averaging 1.38% in magnetic concentrate, with a mass pull of 9.08%. This results in an average DTR nickel grade of 0.12% and overall recovery of 51.59% from an average starting grade of 0.24% over 1,763 meters of continuously sampled core.

- Multiple Updates Expected: The Company anticipates providing additional updates on Phase 2 drilling and other project developments in the coming weeks.

As noted by the United States Geological Survey (USGS) in 2012: “The development of awaruite deposits in other parts of Canada may help alleviate any prolonged shortage of nickel concentrate. Awaruite, a natural iron-nickel alloy, is much easier to concentrate than pentlandite, the principal sulfide of nickel.”

“We congratulate our geological team on the breakthrough discovery at the RPM Zone” stated Adrian Smith, CEO of First Atlantic Nickel. “Prior operators conducting exploration at the Pipestone Ophiolite Complex missed the awaruite mineralization in the southern parts of the property, where our team’s systematic approach and unique experience recognized both the geological controls and the distinction between surface expressions and underlying mineralization. Thanks to Newfoundland’s streamlined permitting process, we have advanced from discovery to Phase 2 drilling significantly faster than would have been possible in many other jurisdictions. Our geological team’s expertise has been instrumental in understanding this 30-kilometer awaruite system – a rare nickel alloy that offers the potential to provide a nickel source while eliminating the energy consumption, environmental impacts, and capacity constraints associated with conventional smelting, roasting and acid leaching processes of nickel sulfide or laterite ores.”

The most recent drill hole from the company’s ongoing Phase 2 drill program, designated AN-25-07, intersected 495 meters of visibly disseminated awaruite—a naturally occurring nickel-iron-cobalt alloy. The results extend the known mineralized zone to 750 meters in width, a 50% increase from the previously established 500-meter width during Phase 1 drilling.

The RPM Zone is part of First Atlantic’s 100%-owned Atlantic Nickel Project, a 30-kilometer district-scale initiative located in central Newfoundland. AN-25-07 was drilled approximately 400 meters north of the original discovery holes and ended in mineralization, indicating the potential for further lateral and depth extensions.

Details of the Drill Hole and Mineralization

Drill hole AN-25-07 was collared on survey line S2, north of the initial discovery on line S1. The hole intersected serpentinized peridotite hosting disseminated awaruite over a 495-meter section. Geological logging and microscope analysis confirmed the presence of awaruite grains throughout the core, with grain sizes visually consistent with those identified in previous holes.

Photographs of the core at multiple depths (97m, 245m, and 354m) display visibly disseminated awaruite grains, ranging in size up to 647 microns. These observations further support the continuity of mineralization within the RPM Zone and the geological consistency of the host rock.

The drill core also supports the theory that the mineralized zone extends westward and to depth, as the hole terminated within mineralized rock.

Phase 2 Drilling Progress

The Phase 2 program aims to test both the north-south strike and the width of the mineralized body. Following the success of AN-25-07, two additional drill holes, AN-25-08 and AN-25-09, have been completed on line S3. With these additions, the company has now tested over 800 meters of north-south strike length within the RPM Zone.

Together, these drill holes support the presence of a potentially continuous zone of awaruite mineralization over more than one kilometer. The expansion enhances the geological model for the RPM Zone and supports the idea of a bulk-tonnage nickel target.

RPM Zone: Overview and Geological Context

The RPM Zone lies 10 kilometers south of the Super Gulp Zone and 26 kilometers south of the historical Atlantic Lake Zone. It represents a new discovery within the Pipestone Ophiolite Complex, a 30-kilometer-long belt of ultramafic rocks considered prospective for nickel mineralization.

The RPM Zone has grown rapidly in scale since its initial discovery and now measures approximately 750 meters wide by 400 meters long. The mineralization remains open in all directions, with no current geological constraints on its full extent.

Early metallurgical testing, including Davis Tube Recovery (DTR), has returned an average nickel grade of 1.38% in magnetic concentrate across all RPM drill holes. This supports the suitability of awaruite for magnetic separation, a process that does not require smelting, roasting, or acid leaching.

Mineralogical and Environmental Considerations

Awaruite (Ni₃Fe) is a sulfur-free nickel-iron-cobalt alloy that occurs in metallic form, allowing it to bypass traditional nickel processing methods. Unlike sulfide and laterite ores, which often require energy-intensive processes and present environmental challenges, awaruite can be processed through magnetic separation alone.

This characteristic avoids the need for smelting capacity—currently a bottleneck in the North American nickel supply chain—and eliminates risks such as acid mine drainage (AMD), which often complicate the permitting of sulfide ore projects.

The average nickel grade of awaruite (~76%) significantly exceeds that of common sulfide minerals like pentlandite, which typically contain around 25% nickel. This high-grade potential, combined with its favorable processing profile, continues to position awaruite as a strategic mineral for clean energy and battery metals supply chains.

Ongoing Exploration Across Pipestone Ophiolite Complex

In parallel with drilling at RPM, Phase 2 includes district-scale prospecting across the broader 30-kilometer Pipestone Ophiolite Complex. Numerous surface rock samples containing visible awaruite have been collected and are undergoing both assay and DTR metallurgical testing.

This regional work is intended to identify additional mineralized zones beyond RPM and evaluate the broader potential of the Atlantic Nickel Project area.

Next Steps and Anticipated Updates

With three drill holes completed in Phase 2 and visible awaruite confirmed over a wide area, First Atlantic Nickel expects to provide additional updates in the coming weeks. Ongoing drill results, surface sampling data, and metallurgical testing are expected to further refine the understanding of the RPM Zone and the overall potential of the Atlantic Nickel Project.

No resource estimate has yet been published for the RPM Zone, and further drilling will be required to define the scale and grade of mineralization before any economic assessments can be made.

Solaris Resources (TSX:SLS) (NYSEAmerican:SLSR) has signed a landmark agreement with the Pueblo Shuar Arutam (PSHA), completing formal partnerships with every Indigenous organization surrounding its Warintza copper project in southeastern Ecuador.

The PSHA, representing nearly 10,000 people in 47 Shuar centers, approved a joint working group with Solaris in January 2025. A Letter of Intent followed in February, leading to the new formal agreement. Solaris already has an Impacts and Benefits Agreement with the Warints and Yawi Shuar Centres, signed in 2020 and updated in 2022 and 2024.

“This agreement reflects the strong collaboration between PSHA and Solaris, as well as our shared commitment to strengthening the communities and families of Morona Santiago. The agreement seeks to generate concrete and sustainable benefits, and we remain committed to ensuring that future generations enjoy the lasting advantages of responsible mining. We are confident that the next stages of this alliance will continue to demonstrate the broad and sustainable benefits that large-scale mining can deliver,” said Marcelo Unkuch, PSHA president.

Matthew Rowlinson, Solaris CEO and president, said, “With this signing, we have now established formal relationships with all Indigenous organisations surrounding Warintza, in addition to our ongoing collaboration with local authorities. These agreements generate strong momentum for the continued advancement of the project and reinforce our long-term commitment to inclusive, community-led development.”

The company said the PSHA deal adds to an earlier trilateral agreement with the Interprovincial Federation of Shuar Centers, Ecuador’s largest Shuar organization, and a partnership with the Alliance for Entrepreneurship and Innovation of Ecuador.

Regulatory and Technical Progress

Regulatory steps are also moving ahead. Solaris submitted a final Technical Environmental Impact Assessment in August 2024 and said it has addressed all government questions. The report is now under review by Ecuador’s Ministry of Environment and Energy.

In July 2025, ministry and Sub-Secretary of Mines officials visited the site and met Indigenous and local stakeholders to evaluate readiness for Ecuador’s Free, Prior and Informed Consultation process, which is required for large resource projects. Solaris expects the consultation to begin in the coming months.

“We are advancing every facet of project de-risking with discipline and determination.” added Matthew Rowlinson. “Warintza is a uniquely positioned asset, long-life, near-term, and aligned with the world’s future resource needs. We remain committed to delivering exceptional value for all stakeholders through responsible development.”

On the technical side, Solaris continues to work on a Pre-Feasibility Study with consultants Ausenco, Knight Piésold and AMC. The study will include an updated Mineral Resource Estimate incorporating Warintza West for the first time and is scheduled for completion in the second half of 2025.

The company said it is working toward a Final Investment Decision for the project. It also plans further exploration within the broader Warintza district and noted that a recent transaction with Royal Gold secures long-term liquidity.

Solaris described these steps; completing Indigenous agreements, advancing environmental review and pushing technical studies—as key milestones for Warintza’s development.

Q2 Metals (TSXV:QTWO | OTCQB: QUEXF | FSE: 458) has expanded its exploration and drilling activities at the Cisco Lithium Project, located in the Eeyou Istchee James Bay region of Quebec, following the completion of a $26 million flow-through private placement financing on August 14, 2025. The project area falls within the greater Nemaska traditional territory and comprises a total of 801 claims across 41,253 hectares.

Alicia Milne, President & CEO of Q2 Metals, commented in a press release: “Strong institutional support enabled us to complete the $26 million financing in August, which has allowed us to significantly ramp-up activities at Cisco. These funds have enabled Q2 to greatly accelerate our drill program, continue regional mapping and sampling programs, and expand on metallurgical test work. With three drill rigs now operating, our immediate focus is to advance the Cisco Project towards an initial inferred Mineral Resource estimate.”

Highlights from the results are as follows:

- $26 million flow-through financing completed in August 2025.

- Drilling at the Cisco Project has been ongoing since June 2025, and a total of 46 holes for 20,138 metres has been drilled to date. Assays are pending on all drill holes completed this summer.

- Three (3) drill rigs are currently operating at Cisco with a fourth expected to commence operation in November.

- Current drilling is focused on infill scale spacing of the main mineralized zone as the Company works towards an initial inferred Mineral Resource estimate at Cisco.

- Additional metallurgical test work is ongoing.

- Regional geological sampling and mapping work continues.

The Cisco Project, which Q2 describes as having district-scale potential, has become the focal point of a significantly expanded summer 2025 exploration campaign, particularly around a known northeast-southwest trending mineralized zone stretching approximately 1.5 kilometers. This zone has been under active investigation since June 2025 and is now being tested more intensively with three drill rigs on-site. A fourth drill rig is expected to commence operations in November 2025.

Drilling Program and Exploration Target

The summer drilling program was initially launched using a single drill rig, with a primary focus on infill drilling along the mineralized strike length. As of early September, three rigs are active on-site, increasing the intensity and density of drilling aimed at tightening the existing drill spacing. This work is intended to support an initial inferred Mineral Resource estimate under National Instrument 43-101 Standards of Disclosure for Mineral Projects (NI 43-101).

The project’s mineralized zone is being evaluated based on an Exploration Target prepared by independent consultant BBA Inc., which estimates a potential range of 215 to 329 million tonnes of lithium-bearing material grading between 1.0% and 1.38% lithium oxide (Li₂O). Q2 Metals notes that this estimate is conceptual in nature. The company also emphasized that there has been insufficient exploration to define a Mineral Resource at this time, and it remains uncertain whether future work will support a formal resource delineation.

In addition to infill drilling, the company’s expanded program includes testing of additional outcrop zones, aided by geophysical targeting. Orientation-style geophysical surveys have already been conducted over a section of the Mineralized Zone to evaluate the effectiveness of these methods in guiding exploration. Further geophysical work may be expanded based on the results of these preliminary surveys.

Metallurgical Testing

In parallel with drilling, Q2 is conducting metallurgical testing to assess the recoverability of lithium from core samples. Preliminary results from the first phase of test work, carried out by SGS Canada Inc. on samples collected during the 2024 drill program, have confirmed that strong recoveries are possible using a dense media separation (DMS) circuit.

A second phase of metallurgical testing is now in the planning stage and is expected to begin in September 2025. This next phase will build upon the initial findings and is intended to provide more comprehensive data on processing characteristics.

Q2’s geology team is also continuing with a regional mapping and rock sampling initiative across the broader Cisco Project area. The objective of the regional work is to identify additional zones of interest within the 41,253-hectare land package. Rock samples from these newly assessed areas have been submitted to a laboratory, and results are currently pending.

The mapping work is aimed at refining exploration targets that could be incorporated into future drilling campaigns. The company has indicated that if the orientation-style geophysical surveys currently underway prove effective, they may be extended to other parts of the project.

The Cisco Project is located approximately 6.5 kilometers from the Billy Diamond Highway, which runs through the project area, providing direct road access. The town of Matagami, which serves as the railhead of the Canadian National Railway, lies about 150 kilometers to the south. This proximity to infrastructure may have implications for future development potential, although the project remains in early-stage exploration.

Q2 Metals is continuing its exploration activities with an eye toward completing an initial inferred Mineral Resource estimate. Rolling assay results from the ongoing drill campaign are expected in the coming weeks and months. The company has indicated that mineralization at the Cisco Project remains open at depth and along strike, suggesting the potential for further expansion.

Smackover Lithium, a joint venture between Standard Lithium (TSX-V, NYSE-A: SLI) and Norway’s state-owned oil and gas company Equinor (NYSE: EQNR), has released the results of its definitive feasibility study (DFS) for the South West Arkansas (SWA) lithium project. The findings suggest what the company refers to as “robust economics” for a proposed lithium extraction and chemicals production facility in the Smackover Formation, located in the southwestern region of Arkansas.

The SWA project, if completed as planned, would become the first commercial lithium production site in the Smackover Formation, a geologic formation containing lithium-rich brine that extends from Florida to Texas. Analysts estimate that the formation could hold over 4 million tonnes of lithium, positioning it as a potentially significant domestic resource for the U.S. battery supply chain.

“The robust economics from our SWA project DFS confirm what we’ve known for a long time – that this is a world-class asset and opportunity,” Standard Lithium’s president and COO Andy Robinson said in a news release.

“Through years of extensive testing and development we have substantially de-risked the process technology and increased our confidence in project execution,” Robinson added. “We are well-positioned to move the project towards a final investment decision and are excited by the prospect of being a domestic champion for securing critical minerals production in the United States.”

The SWA project is a greenfield development that aims to produce battery-quality lithium carbonate (Li₂CO₃) from underground brine. The joint venture received a $225 million grant from the U.S. Department of Energy in January 2025 to support the construction of Phase 1 of the project. The funding aligns with broader federal efforts to secure domestic supply chains for critical minerals such as lithium, which is used extensively in electric vehicles (EVs), energy storage systems, and portable electronics.

According to the DFS, the project’s initial design targets production capacity of 22,500 tonnes per annum (tpa) of lithium carbonate. The facility would extract lithium from brine with an average concentration of 481 milligrams per liter (mg/L), supporting an operating life of at least 20 years, with room for significant expansion depending on further development and demand.

The project’s estimated capital expenditure (capex) stands at $1.45 billion. This figure is based on an 18-month front-end engineering design (FEED) process, which, according to the company, provides a higher degree of capital definition than is typical in DFS-level studies. The capex estimate incorporates learnings from pilot operations, with the company noting potential for improved capital efficiency in future project phases.

These figures are based on the planned production scenario over the 20-year project life.

The project’s measured and indicated resources are reported at 1,177,000 tonnes of lithium carbonate equivalent (LCE), with an average brine concentration of 442 mg/L across a 0.5 km³ brine volume. Proven reserves are estimated at 447,000 tonnes LCE, drawn from a brine volume of 0.2 km³ and a higher average concentration of 481 mg/L.

Since the completion of the project’s prefeasibility study (PFS), Smackover Lithium has undertaken additional exploration activity, including the re-entry of existing wells and the drilling of a new infill well. These efforts were conducted to support upgrading the resource classification and improve modeling of proven and probable reserves.

For the initial phase of lithium extraction, the joint venture will license Koch Technology Solutions’ lithium selective sorption process. This technology, categorized under direct lithium extraction (DLE) methods, is designed to extract lithium more efficiently and with lower environmental impact than traditional evaporation pond systems. The process includes performance guarantees and is expected to contribute to the project’s economic and technical viability.

Smackover Lithium has secured regional exclusivity for the licensed technology within the Smackover Formation under a joint development agreement. According to the company, this exclusivity presents an opportunity for future cost optimization and scalability across other portions of the formation.

The release of the DFS comes at a time when global demand for lithium continues to rise. With the growth of electric vehicle markets and increasing investment in renewable energy infrastructure, lithium has emerged as one of the most strategically important elements in the clean energy transition. However, the U.S. currently relies heavily on imported lithium, much of it from South America and Australia.

If the SWA project proceeds to construction and operation, it could mark a significant step toward developing a domestic lithium supply chain. Industry analysts and government officials have previously cited the Smackover Formation’s potential to support this goal, but until now, there has been no commercial-scale lithium extraction from the formation.

Puma Exploration (TSXV: PUMA, OTCQB: PUMXF) has resumed its 2025 exploration drilling program at the Williams Brook Project in northern New Brunswick following a temporary halt due to a provincial ban on mineral exploration on Crown land. The company reports that drilling has continued at the Lynx Gold Zone, where a recent hole (WB25-181) intersected multiple grains of visible gold at a depth of 355 metres downhole — the deepest visible gold intersection recorded to date at the project.

Ongoing drilling program highlights:

- Six holes completed for a total of 1,343 metres.

- Visible gold (VG) observed in hole WB25-181 at 355 metres downhole depth.

- Drilling successfully intersected fresh rock beneath the oxide zone, confirming continuity of the targeted mineralized horizon.

- Quartz-carbonate veins with traces of pyrite, sphalerite, chalcopyrite and galenaintersected in multiple holes.

- Fully funded $2M exploration program in collaboration with Kinross Gold is ongoing.

Deepest Gold Intercept to Date at Lynx Gold Zone

Hole WB25-181 intersected fine to very fine grains of visible gold within a brecciated quartz-carbonate vein at a vertical depth of approximately 250 metres. This occurrence represents a potential 100-metre extension of known gold mineralization along the favourable geological contact.

The mineralized contact zone intersected in the hole was characterized by discontinuous quartz-carbonate veins with a stockwork texture, and minor sulphide mineralization including pyrite, sphalerite, chalcopyrite, and galena. The hole targeted the hanging wall and the key lithological horizon beneath the oxide zone, where vein sets in fresh rock were successfully intersected.

Drilling Resumed After Fire Ban Suspension

The 2025 exploration campaign at Williams Brook had been temporarily suspended on August 10 following a wildfire-related provincial ban on exploration activities on Crown land. Prior to the halt, six drill holes totaling 1,343 metres had been completed. Drilling resumed this week as restrictions were lifted.

A total of 3,500 metres of drilling is planned at the Lynx Gold Zone as part of a fully funded $2 million exploration program developed in collaboration with Kinross Gold Corporation. The program is focused on identifying new mineralized zones, defining geological contacts, and enhancing understanding of structural controls on mineralization.

Surface Sampling and Channel Work at Lynx

In parallel with drilling activities, channel sampling was completed at Lynx, with 410 samples collected to investigate various vein systems. Assay results for these samples, as well as those from the drilling program, are pending and will be released once received.

Upcoming Work at Jaguar Gold Zone

The Joint Technical Committee overseeing exploration activities has also announced plans for a 1,500-metre drilling campaign at the Jaguar Gold Zone (JGZ), located approximately 5 kilometres northeast of the Lynx zone. The upcoming drill program will follow up on historical data and recent trenching results.

Historical drilling at the JGZ, conducted in 2008, recorded grades of 0.52 g/t Au over 55 metres, 0.68 g/t Au over 42 metres, and 0.21 g/t Au over 64 metres, according to a 2009 report by Arthur Hamilton, P.Geo., for Blue Note Mining Inc. More recently, Puma’s 2022 trenching work at the JGZ yielded higher values, including grab samples returning up to 34.70 g/t Au. In total, 306 samples were collected during that campaign, with an average grade of 1.72 g/t Au. Notably, 31% of the samples (95 out of 306) assayed above 1.00 g/t Au. However, the company notes that grab samples are selective by nature and may not represent the overall grade of the mineralized zone.

Currently, the mineralized area at JGZ spans 80 metres by 50 metres and remains open in all directions.

In addition to activities at Lynx and JGZ, ongoing exploration continues across the broader Williams Brook Project. Puma has collected 570 samples from prospecting, trenching, and excavating operations targeting high-priority areas identified by the technical committee. A total of 2,265 metres of trenching has been completed to date.

Exploration has also commenced at the Jonpol and Portage properties, which are included in the Williams Brook land package.

The Williams Brook Project, spanning 40,225 hectares, includes the Williams Brook, Jonpol, and Portage properties. Under an option agreement signed in 2024, Kinross Gold Corp. can earn a 65% interest in the project by funding a minimum of $16.75 million in exploration expenditures over five years. This includes a firm commitment of $2 million and at least 5,000 metres of drilling within the first 18 months (2025–2026).

Puma Exploration holds a portfolio of gold-focused properties in northern New Brunswick, strategically situated near infrastructure and roads. These include the Williams Brook and McKenzie Gold Projects, both located near the Rocky Brook Millstream Fault — a significant structural feature formed during the Appalachian Orogeny and believed to control gold deposition in the region.

While the Williams Brook Project remains the company’s flagship asset, early-stage exploration work on other properties has also identified zones of interest with potential for further gold mineralization.

Global iron ore markets rose sharply following a fatal incident at Rio Tinto’s (ASX:RIO) Simandou project in Guinea, prompting the company to suspend operations. The event pushed iron ore prices to their highest level in over a week amid concerns about supply disruptions and broader market factors influencing demand.

“All activity at the SimFer mine site is currently suspended, and support is in place for colleagues affected by this event,” the company said.

Fatal Incident at SimFer Mine Site

The rise in prices followed an announcement from Rio Tinto that it had suspended all activity at the SimFer mine site, part of the larger Simandou iron ore project located in Nzérékoré, southeastern Guinea. The suspension was triggered by a fatal incident involving a contract worker. Details surrounding the circumstances of the incident have not yet been released.

In a statement, Rio Tinto confirmed the suspension and said, “All activity at the SimFer mine site is currently suspended, and support is in place for colleagues affected by this event.”

Simon Trott, who took over as Rio Tinto’s chief executive officer on Monday, is expected to visit the site. Trott also confirmed that the company will conduct a full investigation into the incident.

Project Overview and Timeline Disruption

Simandou is widely regarded as one of the largest undeveloped high-grade iron ore deposits in the world. Rio Tinto operates two of the four mining blocks through its SimFer joint venture, which includes China’s Chalco Iron Ore Holdings (CIOH) and the government of Guinea. The company had previously indicated that it expected first shipments from the site to begin in November 2025.

At full capacity, the mine is projected to produce nearly 120 million tonnes of high-quality iron ore annually, making it one of the most significant new sources of global supply. Initial shipments were expected to be modest as operations gradually ramp up.

The temporary shutdown of activity at SimFer has raised concerns about potential delays to this timeline, though no revised production schedule has yet been announced.

The fatality adds to a series of safety-related incidents involving Rio Tinto operations over the past two years. This is the seventh recorded death at Rio’s sites in that timeframe. Notably, a contractor was killed last October at the SimFer port site. In January of the same year, four employees died in a charter flight crash en route to the Diavik diamond mine in Canada. These incidents have interrupted what had previously been a five-year period without any fatalities at Rio Tinto’s managed operations.

Despite the operational setback in Guinea, broader market conditions are contributing to the current support for iron ore prices. In China, the top global consumer of iron ore, demand has remained firm, even amid environmental restrictions affecting steel production.

In the steelmaking hub of Tangshan, authorities have implemented temporary production curbs aimed at improving air quality in Beijing ahead of an upcoming military parade commemorating the end of World War Two. However, these restrictions have not significantly impacted consumption. According to consultancy firm Mysteel, average daily hot metal output — a key indicator of iron ore demand — remained steady at 2.41 million tonnes for the week ending August 21.

As of now, there is no confirmation on when operations at the SimFer site will resume. The pending investigation, to be led by Rio Tinto with expected collaboration from joint venture partners and local authorities, will be a determining factor.

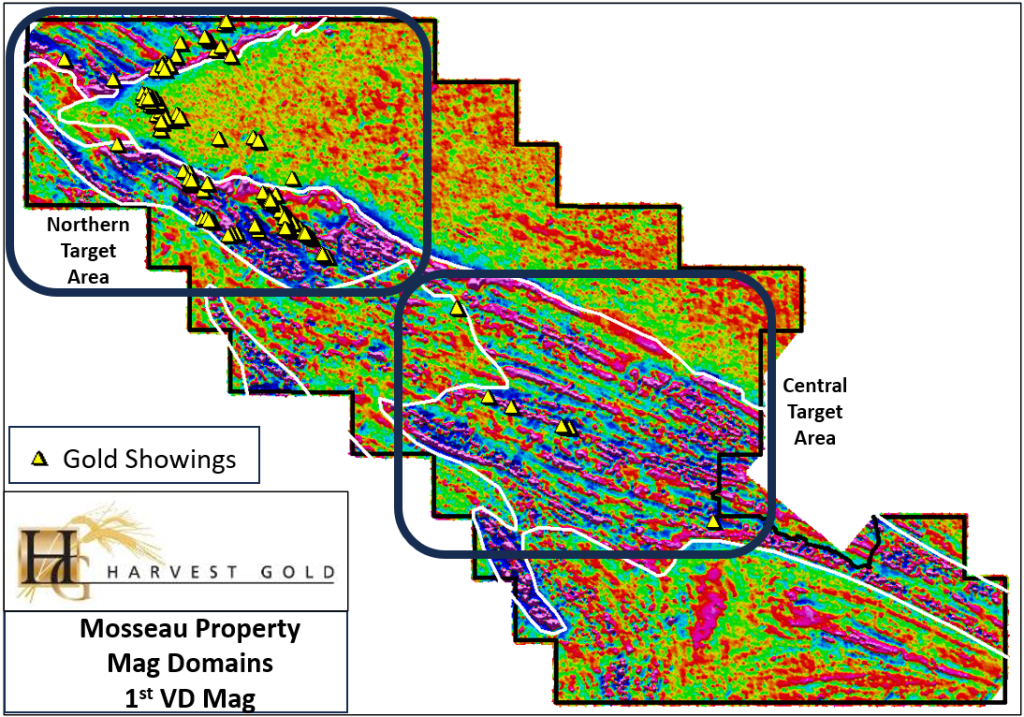

Harvest Gold (TSXV: HVG) has released a detailed update on its ongoing exploration activities, confirming significant progress on two of its key gold projects in Quebec. According to the company, its diamond drilling campaign at the Mosseau Gold Project is proceeding as scheduled, while a regional till sampling program at its Urban-Barry property has been completed ahead of time and under budget.

Mosseau Drill Program Advances in Northern Corridor

The company announced that five diamond drill holes have been successfully completed at the Mosseau Gold Project. Drilling is taking place in the northern section of the property, an area characterized by historical gold showings and favorable geological conditions. This segment of the mineralized corridor is a central focus of the current exploration effort, aimed at identifying new mineralized zones and expanding the known footprint of gold occurrences.

Harvest Gold stated that drilling operations are on schedule and on budget. The company highlighted the performance of its contractors, citing steady drilling progress by Forage Rouillier and technical support from Explo-Logik. The latter is responsible for field logistics, core logging, and drill core sampling. According to the update, all operational protocols are being followed, and daily progress reports are being submitted to the company’s management team to ensure safety and efficiency throughout the project.

No analytical or assay results from the completed drill holes were disclosed as part of this update. These results are expected to play a critical role in determining future exploration decisions and delineating potential mineralized zones within the property.

Urban-Barry Till Sampling Program Completed

In addition to developments at Mosseau, Harvest Gold confirmed the successful completion of its regional till sampling program at the Urban-Barry property. The purpose of this geochemical survey was to identify new exploration vectors that could signal the presence of gold mineralization below surface.

The sampling campaign was originally designed to include 145 sample sites distributed along a grid system. Sampling lines were oriented in a northwest-southeast direction and spaced roughly 1,000 to 1,500 metres apart. Individual sampling locations were positioned approximately every 250 metres along each line. In total, 137 usable till samples were collected.

According to the company, the majority of samples were taken from depths exceeding one metre, in an effort to reach the lodgment till layer. Lodgment till is a type of glacial deposit that is considered significant for geochemical exploration due to its higher likelihood of containing material derived from nearby mineralized sources. Each collected sample weighed approximately 10 kilograms and was manually gathered to avoid contamination from larger debris like cobbles and pebbles.

Harvest Gold has not yet released geochemical assay results from the till survey but indicated that the data will be used to define and prioritize exploration targets across the broader Urban-Barry project area.

Company’s Regional Exploration Portfolio

Harvest Gold holds three active gold exploration properties in the Urban Barry region of Quebec: Mosseau, Urban-Barry, and LaBelle. Combined, the projects span over 50 kilometers of mineralized shear zones and include 377 claims covering a total area of 20,016.87 hectares. These properties are located approximately 45 to 70 kilometers west of the Windfall deposit, a major gold asset owned by Gold Fields Limited.

The Mosseau property, where drilling is currently ongoing, is situated along the boundary of the Eeyou Istchee-James Bay and Abitibi territories. The company reiterated its commitment to building respectful and transparent relationships with Indigenous communities in the region.

Harvest Gold is engaged in the exploration of near-surface gold deposits and copper-gold porphyry systems. The company operates within jurisdictions considered to be politically stable, with its leadership team and technical advisors bringing a combined experience of more than four centuries in geology, mineral exploration, and financing.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |