Cypress Development Corp. (TSX-V: CYP) (OTCQB: CYDVF) (Frankfurt: C1Z1) owns 100% of a giant, leachable, lithium-bearing claystone-hosted resource, the Clayton Valley Lithium Project (“CVLP“), adjacent to Albemarle Corp.’s Silver Peak brine operations in Nevada. The Company has an Enterprise Value (“EV“) {market cap + debt – cash} of C$17.5 million.

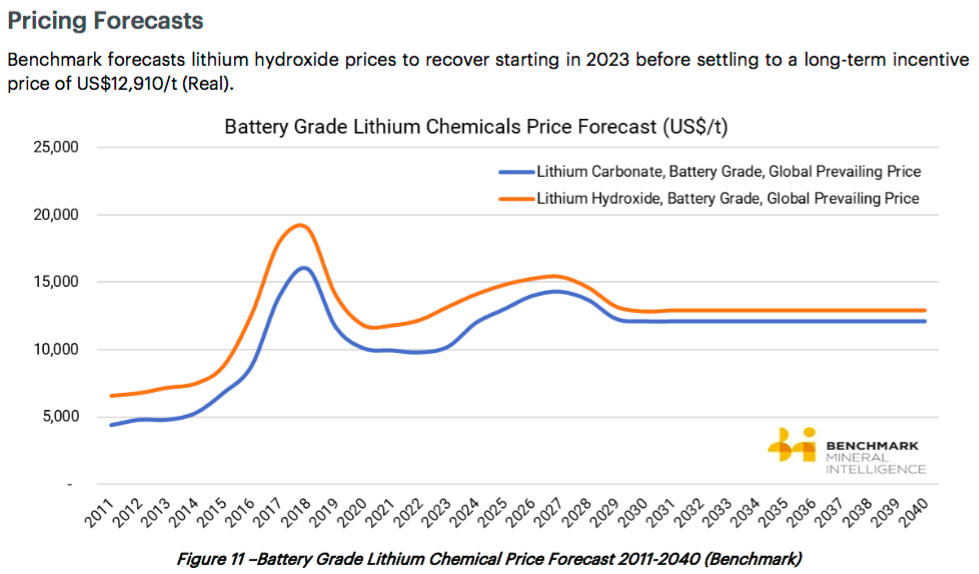

On May 19th, management delivered a highly-anticipated press release summarizing its Pre-Feasibility Study (“PFS“) on the CVLP. Let me start by saying…. It was worth the wait. Cypress adopted a low long-term price of US$9,500/tonne (“t“) of Lithium Carbonate Equiv. (“LCE“). The price used in a dozen other brine or clay-hosted (sedimentary) project reports (PEA, PFS or DFS) in the past three years ranged from US$11,000 to US$13,950/t and averaged US$12,558/t.

Cypress Development Corp. PFS a high-quality, serious report

Admittedly, lithium prices have been falling since 2018, but peer Nevada lithium + boric acid project developer ioneer ltd. announced, (20 days before Cypress), a Definitive Feasibility Study (“DFS“) with a US$13,200/t LCE price assumption.

Hard rock juniors are pursuing lithium hydroxide, but brine projects have lithium carbonate in their plans. Cypress plans to make battery-quality lithium hydroxide. In Cypress’ PFS, nameplate capacity is 27,400 tonnes LCE/yr. However, it takes less lithium to manufacture hydroxide than to make carbonate. If the CVLP project were to deliver 100% hydroxide, it would be operating at an average of 31,141 tonnes /yr.

Some investors might be wondering why management didn’t use a higher long-term lithium price. I believe there are two reasons. First, that’s not how CEO Bill Willoughby rolls. Dr. Willoughby is a PhD in Mine Engineering & Metallurgy, making him the polar opposite of a Vancouver promoter, and the best choice imaginable to be leading Cypress.

Second, I suspect that Cypress is in talks with entities led by serious engineers, metallurgists & experienced mining experts like Dr. Willoughby. A detailed, highly accurate PFS was called for. Please note, management has never revealed to me a name of anyone they’ve spoken with in the past or presently.

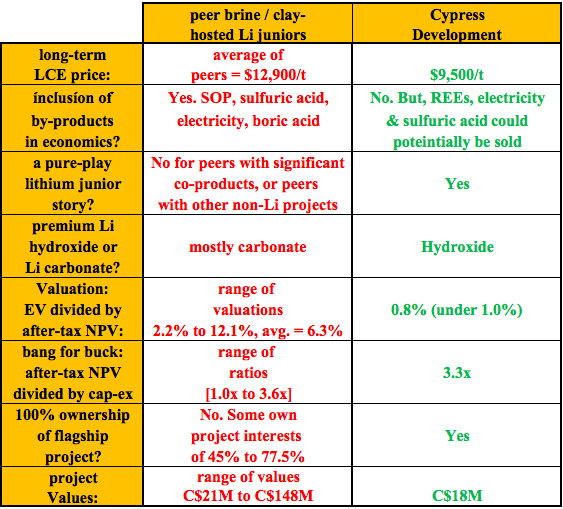

Cypress is very attractive in peer comparisons & in valuation

Unlike peers, Cypress did not incorporate by-/co-products in the economics. By contrast, Lithium Americas’ Thacker Pass project includes 11% of gross annual revenue from the sale of excess electricity & sulfuric acid. Cypress might also have excess sulfuric acid to monetize, but management did not use it in the model.

Rare Earth Elements (“REEs“) [scandium, dysprosium & neodymium] are present at the CVLP, but zero credit was ascribed to these potential cash flows. If recoverable, the un-discounted value of the REEs is in the hundreds of millions. REEs will be studied and reported on in the Definitive Feasibility Study (“DFS“).

By-/co-products are included in the economics of some peer company projects. I mentioned Thacker Pass (electricity + sulfuric acid). Bacanora proposes to produce potassium sulfate (“SOP“) alongside lithium carbonate.

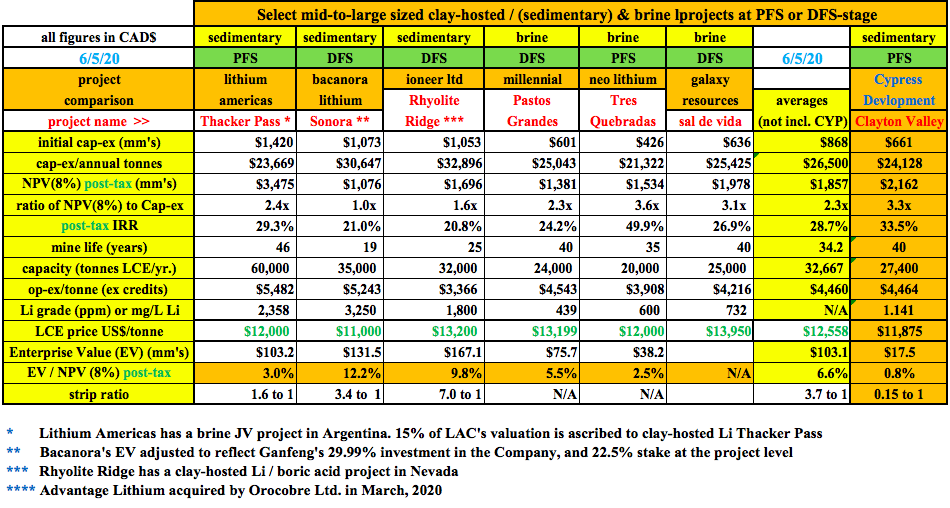

In order to more accurately compare projects, I adjusted the lithium price assumption in the CVLP PFS. Taking the midpoint between the base case of $9,500/t and the “upside” case of US$14,250/t, I interpolated key metrics at an implied LCE price of US$11,875/t, (5% lower than US$12,558/t peer average).

Cypress’ PFS compares quite well to the projects shown below. The average cap-ex was C$874M vs. C$661M for CYP.V, capital intensity; C$26,500/t vs. C$24,128/t for CYP.V, ratio of after-tax NPV(8%) to upfront capital; 2.3x vs. 3.3x for CYP.V., and IRR; 28.7% vs. 33.5% for CYP.V.

Again, these comparisons were done with a US$11,875/t price for Cypress. One last thing, the CVLP has a strip ratio of just 0.15 to 1. The other sedimentary projects have strip ratios ranging from 1.6 to 7.0 to 1, averaging 3.7 to 1.

Is Cypress a takeover candidate?

Could Tesla be looking at acquiring Cypress? With an EV of C$224.4B (12,824 times that of Cypress) it could easily afford to. However, I have no idea if Tesla is interested. I imagine that a few auto and/or Li-ion battery makers are kicking the tires. More importantly, I suspect that lithium & specialty chemicals giant Albemarle Corp. will be carefully reviewing the PFS.

Why would a C$15 billion company like Albemarle care about tiny Cypress? Simple. In a much larger company’s hands, the CVLP would be worth a lot more than C$17.5 million. A larger company could comfortably afford the initial cap-ex of C$661M. Financially strong players can borrow at low interest rates.

With substantial financial wherewithal and unrivaled, decades-long, expertise in specialty chemicals & lithium — Albemarle could bring a sedimentary project, one adjoining its own Silver Peak brine operations, to fruition faster than Cypress ever could. Silver Peak has been in operation since the mid-1960s. Assuming its current 6,000 tonnes LCE/yr. capacity, Albemarle says it has ~20 years of remaining mine life.

Think about the synergies that could be gained by adding the CVLP to Albemarle’s neighboring lithium complex. Silver Peak has all manner of industrial / chemical property, plant & equipment, and of course — lithium processing facilities. Equally important, it has 50+ years of expert knowledge & experience with lithium compounds and local / State permitting.

Adding 27,400 tonnes/yr. LCE (or 31,141 tonnes/yr. hydroxide) to Albemarle’s 6,000 tonnes LCE/yr. would move the needle for Albemarle. Cypress does not include EBITDA in the summary press release of its PFS, but the op-ex is US$3,329/t. So, at an interpolated lithium price of US$11,875/t, the operating margin before taxes would be $8,546/t.

Therefore, 31,141 tonnes hydroxide, multiplied by a US$8,546/t operating margin, equates to ~C$346 million in cash flow/yr. Compare that C$346 million to Albemarle’s trailing 12-month EBITDA of C$1.235 billion. All else equal, Albemarle’s EBITDA margin could jump from 27.1% to ~31.3% by acquiring Cypress. Can these two companies find a way to combine resources?

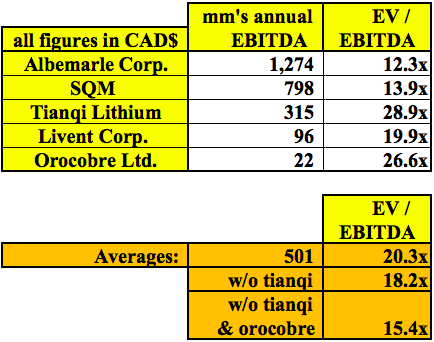

There are not that many lithium producers (of meaningful quantities), and SQM & Albemarle are not pure-play lithium investments. In the chart above, I show that EV/EBITDA multiples are fairly strong even with lithium prices at less than half 2018’s highs. Although there’s still a lot or execution risk, imagine what a potential cash flow stream of C$346 million/yr. for 40 years might be worth? A 15.4x multiple times C$346 million = C$5.3 billion. Discounting that figure back six years (from 2026) at a 20% discount factor, it’s still C1.78 billion.

Next Steps

The authors of the PFS recommend additional testing & studies be done in the areas of processing, mining, permitting & infrastructure. Further work is needed to confirm the flow sheet and determine recovery & reagent consumptions. A confirmation of the process & equipment in the leaching & filtration functions is sought and there’s further work to do to enhance solid-liquid separation to further reduce acid consumption.

Management must determine if there is any lithium or acid losses in the processing plant design and optimize lithium solution handling. Another important step will be to assess the economic viability of potassium, magnesium, REEs or other elements.

Drilling / limited test-mining is required to obtain material for metallurgical testing. Regarding permitting, a field program will be necessary to determine if any protected species of plants or animals are present, and to gather environmental & other data to prepare a mine Plan of Operations.

Finally, infrastructure — Feasibility-level designs for the mine, plant & tailings storage areas can now begin. A better understanding of power & water supply is needed. These are big ticket items that need to be sorted out over the next 12-18 months, before a DFS can be completed.

Capital will have to be raised to fund a pilot plant, various reports & studies and a DFS. Importantly, funding need not come solely from equity raises. I suspect that a farm out or JV is possible as soon as this year. Management is confident that these and other critical factors can be addressed. Readers should remember that first commercial production is probably not until 2025, there’s plenty of time to address any challenges.

CONCLUSION

There are simply not that many 25,000+ tonne/yr. lithium hydroxide projects in the world at PFS-stage or more advanced, that could be in production in 2025, or perhaps 2024 if a company like Albemarle were to get involved.

Once car & battery makers see lithium projects get acquired, or have their production capacities tied up by off-take agreements away from them, there might be a rush of M&A activity. Cypress Development Corp. (TSX-V: CYP) (OTCQB: CYDVF) (Frankfurt: C1Z1), with a world-class project in a world-class location, an EV of just C$17.5 million and a project with cap-ex < US$500 million, is a company that should be high on the lists of prospective suitors.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Cypress Development Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Cypress Development Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Cypress Development Corp. was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.