VANCOUVER, British Columbia, June 22, 2026 (GLOBE NEWSWIRE) — Teck Resources Limited (TSX: TECK.A and TECK.B, NYSE: TECK) (“Teck”) today announced the appointment of Edwin Shadeo as Acting Vice President, Investor Relations and Treasurer, effective immediately. Mr. Shadeo succeeds Emma Chapman, who is leaving Teck to pursue new professional opportunities.

“As Treasurer, Edwin has developed extensive relationships within the capital markets community, building on his deep understanding of our business. This, combined with his long-standing experience in investor relations, equips him well to lead our engagement with shareholders,” said President and CEO Jonathan Price. “I would also like to thank Emma for her leadership and outstanding contributions to Teck during her time as Vice President, Investor Relations.”

Mr. Shadeo joined Teck in 2005 as Strategic Analyst, Business Development, Coal, and has held progressively more senior and leadership roles in Investor Relations, Corporate Development, the Office of the President and CEO, and Treasury.

Mr. Shadeo holds a Bachelor of Commerce from the University of British Columbia, as well as the Chartered Alternative Investment Analyst (CAIA) and Certified Treasury Professional (CTP) designations.

About TeckTeck is a leading Canadian resource company focused on responsibly providing metals essential to economic development and the energy transition. Teck has a portfolio of world-class copper and zinc operations across North and South America and an industry-leading copper growth pipeline. We are focused on creating value by advancing responsible growth and ensuring resilience built on a foundation of stakeholder trust. Headquartered in Vancouver, Canada, Teck’s shares are listed on the Toronto Stock Exchange under the symbols TECK.A and TECK.B and the New York Stock Exchange under the symbol TECK. Learn more about Teck at www.teck.com or follow @TeckResources.

Investor Contact:Edwin ShadeoActing Vice President, Investor Relations604.699.4531edwin.shadeo@teck.com

Media Contact:Dale SteevesDirector, External Communications236.987.7405 dale.steeves@teck.com

Vancouver, British Columbia–(Newsfile Corp. – June 22, 2026) – Kay Copper Corporation (formerly Railtown II Capital Corp), currently an unlisted reporting issuer, is pleased to provide an update on the proposed transaction announced on April 29, 2026 (the "Transaction") with Teck Resources Limited (collectively with its subsidiary Teck American Incorporated, "Teck") and Kodiak Copper Corp. ("Kodiak").

Under the Transaction, Kodiak would vend its 100% owned Mohave project ("Mohave") and Teck would vend its 100% owned Copper Hill project ("Copper Hill"), both located in Arizona, into a subsidiary of Kay Copper to create a new US-focused copper exploration company that would apply to list its shares on the TSX Venture Exchange ("TSXV"). The Transaction is subject to ongoing negotiations, the execution of definitive agreements, due diligence, consents and regulatory approval, approval of the TSXV and the completion of the Newco Concurrent Financing (as defined below). There is no guarantee that the Transaction will be completed.

Transaction Progress

- The Transaction is advancing as planned and is expected to close in the third quarter of 2026;

- A new private company has been incorporated ("NewCo") for the purposes of the Transaction;

- NewCo has completed a non-brokered initial financing at $0.10 per share for gross proceeds of $830,000 (the "NewCo Initial Financing") to a broad group of investors, which is intended to support the distribution requirement for a listing on the TSXV;

- Mark Osterberg will join Kay Copper as Vice President, Exploration on closing of the Transaction. Other management and board appointments are being finalized and will be announced in due course; and

- The drafting of definitive agreements, due diligence and NewCo Concurrent Financing (as defined below) are under way in preparation for the application to list on the TSXV.

Management Appointment – VP Exploration

Further to the previously announced management and board appointments (see news release of April 29, 2026), Mark Osterberg has been named VP Exploration of Kay Copper. Mark is an exploration geologist with decades of base and precious metals mining experience, with a strong focus on porphyry copper deposits. He earned a PhD from the University of Arizona and spent the first half of his career working for Gold Fields Mining Corporation, Cyprus Mining Company, and BHP focused primarily on porphyry deposit exploration including Bagdad, Robinson, and Ok Tedi. Since 2001, he has worked as the founding principal for Mine Mappers, LLC, a geological consulting firm specializing in resource discovery and delineation, working for both major and junior mining and exploration companies.

Transaction Overview

The Transaction is anticipated to include the following steps:

- NewCo would acquire Mohave and Copper Hill from Kodiak and Teck respectively and issue to each of Kodiak and Teck 20 million common shares at a deemed price of $0.25 per share as consideration for Mohave and Copper Hill, respectively. The $0.25 share price is a deemed price for transaction purposes only and does not represent a valuation;

- NewCo would complete a three-cornered amalgamation with Kay Copper (the "Amalgamation"), whereby Newco would merge with a newly formed subsidiary of Kay Copper and the holders of shares of Newco would receive one share of Kay Copper for each Newco share held;

- Concurrently with the Amalgamation, Kay Copper would apply to list its shares for trading on the TSXV under the name of Kay Copper Corp; and

- Completion of the Transaction is subject to customary closing conditions including the completion of due diligence by each of Kodiak, Teck and Kay Copper, negotiating and executing definitive agreements, obtaining all necessary consents and regulatory approvals, TSXV acceptance and satisfaction of applicable listing requirements, the completion of the NewCo Concurrent Financing (as defined below) and other conditions.

Further details regarding the Transaction will be provided as the process continues to advance.

There can be no assurance that the Transaction or NewCo Concurrent Financing (as defined below) will be completed as proposed, or at all.

NewCo Concurrent Financing

In connection with the Transaction, NewCo intends to complete a subscription receipt financing at $0.25 per share for minimum gross proceeds of C$4.0 million (the "NewCo Concurrent Financing").

- Proceeds are intended to fund exploration work programs to materially advance both projects in 2026.

- Gross proceeds would be held in escrow and released concurrently with closing of the Transaction and upon satisfaction of specified escrow release conditions, including completion of the asset acquisitions, Amalgamation, and TSXV conditional approval, and all requisite corporate and regulatory approvals.

- If escrow release conditions are not satisfied, subscription receipt holders would be entitled to a return of funds in accordance with the terms of the subscription receipts.

See previous news release dated April 29th, 2026 for additional details concerning the proposed Transaction.

On behalf of the Board of DirectorsKay Copper Corp.

Cameron WhiteDirector

For further information, contact:Cameron White, Directorcam@caliber.vc+1 (604) 765-2601

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statement (Safe Harbor Statement): This press release contains forward-looking statements within the meaning of applicable securities laws. The use of any of the words "anticipate", "plan", "can", "could", "continue", "expect", "estimate", "objective", "may", "will", "would", "project", "shall", "should", "predict", "potential" and similar expressions are intended to identify forward-looking statements. In particular, this press release contains forward-looking statements concerning: the proposed creation of a new U.S.-focused copper exploration company expected to list on the TSXV; Kodiak vending Mohave to NewCo; Teck vending Copper Hill to NewCo; that NewCo will be positioned for meaningful growth; completion of the NewCo Concurrent Financing; completion of the Amalgamation; the successful negotiation and execution of a definitive agreement; the receipt of consents or regulatory approvals, including potential TSXV approval; the closing of the Transaction in the third quarter of 2026, or at all; the closing of the NewCo Concurrent Financing; that Mark Osterberg will join Kay Copper as Vice-President Exploration on closing of the Transaction; and the future investor rights of Teck and Kodiak and future offtake rights of Teck regarding NewCo. Although Kay Copper believes that the expectations and assumptions on which the forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because Kay Copper cannot give any assurance that they will occur or prove to be correct. Since forward-looking statements address future events and conditions, they involve inherent assumptions, risks and uncertainties. Actual results could differ materially from those currently anticipated due to a number of assumptions, factors and risks. These assumptions and risks include, but are not limited to, assumptions and risks associated with: the ability of the parties to execute their business objectives related to the Transaction; the ability of the parties to negotiate and execute definitive agreements; the parties expectations regarding future results from Mohave and Copper Hill; the ability to obtain necessary capital for the NewCo Concurrent Financing; conditions in the equity financing markets; receipt of regulatory and shareholder approvals; the impact of increasing competition; the regulatory framework regarding royalties, taxes and environmental matters; the ability to achieve potential synergies and unlock value from the Transaction; and the nature of the proposed business of NewCo, including the exploration and production of natural resources.

Management has provided the above summary of risks and assumptions related to forward-looking statements in this press release in order to provide readers with a more comprehensive perspective on Kay Copper's future operations. Kay Copper's actual results, performance or achievement could differ materially from those expressed in, or implied by, these forward-looking statements and, accordingly, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits Kay Copper will derive from them. These forward-looking statements are made as of the date of this press release, and, other than as required by applicable securities laws, Kay Copper disclaims any intent or obligation to update publicly any forward-looking statements, whether as a result of new information, future events or results or otherwise.

THIS NEWS RELEASE IS NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/302265

Kodiak Copper [TSXV:KDK] is moving closer to unlocking the value of its Arizona assets through the creation of a dedicated US-focused copper exploration company, as the proposed transaction with Teck Resources continues to advance towards an expected third-quarter completion.

n

The Canadian explorer said key milestones had been achieved in the formation of Kay Copper, the new company that is intended to combine Kodiak’s Mohave project with Teck’s Copper Hill project in Arizona, creating a focused vehicle positioned to capitalise on growing demand for copper in North America.

n

The transaction comes at a time when copper has become increasingly central to global industrial policy. Demand for the metal is expected to rise sharply over the coming decade, driven by electrification, renewable energy infrastructure, artificial intelligence-related power demand and grid modernisation.

n

Against that backdrop, investors have shown renewed interest in exploration companies with exposure to prospective projects in mining-friendly jurisdictions.

n

- Kodiak Copper advances Arizona spin-out with Teck

- Kodiak Copper and Teck Resources in project merger plan

- Kodiak Copper expands Arizona footprint

nMark Osterberg to join Kay Coppern

Kodiak chief executive Claudia Tornquist said the transaction remained on track and represented the best route to maximise the value of the company’s non-core Arizona assets.

n

“I am pleased to report that the previously announced transaction to create Kay Copper, a US-focused copper exploration company, is progressing well and important milestones have been achieved,” she said.

n

Among the latest developments is the completion of an initial financing by NewCo, the private company established to facilitate the transaction. The financing raised C$830,000 from a broad group of investors and is intended to support the shareholder distribution requirements associated with a future TSX Venture Exchange listing.

n

The project has also secured a key addition to its technical leadership team. Veteran exploration geologist Mark Osterberg has agreed to join Kay Copper as vice-president of exploration following completion of the transaction. Based in Arizona, he will oversee exploration programmes at both Mohave and Copper Hill.

n

Osterberg brings decades of experience in porphyry copper systems, including work with major mining groups such as BHP, Cyprus Mining and Gold Fields. His career has included involvement in exploration programmes at several well-known copper deposits, including Bagdad, Robinson and Ok Tedi.

n

His appointment is being viewed as an important step in building the management team required to advance the combined asset portfolio.

nWhat the Kodiak-Teck transaction looks liken

The proposed transaction would see Kodiak and Teck each contribute their respective Arizona projects into the new company in exchange for substantial equity stakes. Following completion of the deal and a planned concurrent financing, both companies are expected to own approximately 28 per cent of Kay Copper.

n

The structure provides strong alignment between the parties and ensures continued support from two experienced industry participants as the new company advances exploration.

n

Attention is now turning towards a planned C$4m financing, the proceeds of which are expected to fund exploration programmes aimed at materially advancing both projects during 2026. The funds will be held in escrow until the transaction closes and all regulatory and listing requirements have been satisfied.

n

For Kodiak, the transaction reflects a broader strategy of creating value through focused asset development while maintaining exposure to upside. The company will retain a significant ownership stake in Kay Copper, allowing shareholders to benefit from any exploration success while Kodiak continues to advance its flagship MPD copper-gold project in British Columbia.

n

As global competition for future copper supply intensifies, the emergence of a dedicated Arizona-focused explorer backed by both Kodiak and Teck is attracting increasing attention. While the transaction remains subject to final agreements and regulatory approvals, the progress achieved so far suggests momentum is building behind a venture designed to tap into one of mining’s most compelling long-term themes.

nn

n

Get free weekly UK company analysis from The Armchair Trader here

Vancouver, British Columbia–(Newsfile Corp. – June 22, 2026) – Kodiak Copper Corp. (TSXV: KDK) (OTCQX: KDKCF) (FSE: 5DD1) (the "Company" or "Kodiak") is pleased to provide an update on the proposed transaction announced on April 29, 2026 (the "Transaction", see news release here) with Teck Resources Limited (collectively with its subsidiary Teck American Incorporated, "Teck") and Kay Copper Corp. ("Kay Copper", formerly Railtown II Capital Corporation), currently an unlisted reporting issuer.

Under the Transaction Kodiak would vend its 100% owned Mohave project ("Mohave") and Teck would vend its 100% owned Copper Hill project ("Copper Hill"), both located in Arizona, into a subsidiary of Kay Copper to create a new US-focused copper exploration company that would apply to list its shares on the TSX Venture Exchange ("TSXV"). The Transaction is subject to ongoing negotiations, the execution of definitive agreements, due diligence, consents and regulatory approval, approval of the TSXV and the completion of the NewCo Concurrent Financing (as defined below). There is no guarantee that the Transaction will be completed.

Transaction Progress

- The Transaction is advancing as planned and is expected to close in the third quarter of 2026;

- A new private company has been incorporated ("NewCo") for the purposes of the Transaction;

- NewCo has completed a non-brokered initial financing at $0.10 per share for gross proceeds of $830,000 (the "NewCo Initial Financing") to a broad group of investors, which is intended to support the distribution requirement for a listing on the TSXV;

- Mark Osterberg will join Kay Copper as Vice President, Exploration on closing of the Transaction. Other management and board appointments are being finalized and will be announced in due course; and

- The drafting of definitive agreements, due diligence and NewCo Concurrent Financing (as defined below) are under way in preparation for the application to list on the TSXV.

Claudia Tornquist, President and CEO of Kodiak said, "I am pleased to report that the previously announced transaction to create Kay Copper, a US-focused copper exploration company, is progressing well and important milestones have been achieved, particularly the closing of the NewCo Initial Financing. Mark Osterberg, an accomplished geologist with extensive copper porphyry experience, has agreed to join Kay Copper as VP Exploration, based in Arizona, and lead the Company's exploration programs at the Mohave and Copper Hill projects. This is a key appointment for the Company, and we are glad to have found such an excellent candidate to strengthen our technical leadership team. I have no doubt that this transaction represents the best path to unlock the value of Kodiak's non-core Mohave project and will generate compelling returns for our shareholders."

Management Appointment – VP Exploration

Further to the previously announced management and board appointments (see news release of April 29, 2026), Mark Osterberg has been named VP Exploration of Kay Copper. Mark is an exploration geologist with decades of base and precious metals mining experience, with a strong focus on porphyry copper deposits. He earned a PhD from the University of Arizona and spent the first half of his career working for Gold Fields Mining Corporation, Cyprus Mining Company, and BHP focused primarily on porphyry deposit exploration including Bagdad, Robinson, and Ok Tedi. Since 2001, he has worked as the founding principal for Mine Mappers, LLC, a geological consulting firm specializing in resource discovery and delineation, working for both major and junior mining and exploration companies.

Transaction Overview

The Transaction is anticipated to include the following steps:

- NewCo would acquire Mohave and Copper Hill from Kodiak and Teck respectively and issue to each of Kodiak and Teck 20 million common shares at a deemed price of $0.25 per share as consideration for Mohave and Copper Hill, respectively. The $0.25 share price is a deemed price for transaction purposes only and does not represent a valuation;

- NewCo would complete a three-cornered amalgamation with Kay Copper (the "Amalgamation"), whereby Newco would merge with a newly formed subsidiary of Kay Copper and the holders of shares of Newco would receive one share of Kay Copper for each Newco share held;

- Concurrently with the Amalgamation, Kay Copper would apply to list its shares for trading on the TSXV under the name of Kay Copper Corp; and

- Completion of the Transaction is subject to customary closing conditions including the completion of due diligence by each of Kodiak, Teck and Kay Copper, negotiating and executing definitive agreements, obtaining all necessary consents and regulatory approvals, TSXV acceptance and satisfaction of applicable listing requirements, the completion of the NewCo Concurrent Financing (as defined below) and other conditions.

Further details regarding the Transaction will be provided as the process continues to advance.

There can be no assurance that the Transaction or NewCo Concurrent Financing (as defined below) will be completed as proposed, or at all.

NewCo Concurrent Financing

In connection with the Transaction, NewCo intends to complete a subscription receipt financing at $0.25 per share for minimum gross proceeds of C$4.0 million (the "NewCo Concurrent Financing").

- Proceeds are intended to fund exploration work programs to materially advance both projects in 2026.

- Gross proceeds would be held in escrow and released concurrently with closing of the Transaction and upon satisfaction of specified escrow release conditions, including completion of the asset acquisitions, Amalgamation, and TSXV conditional approval, and all requisite corporate and regulatory approvals.

- If escrow release conditions are not satisfied, subscription receipt holders would be entitled to a return of funds in accordance with the terms of the subscription receipts.

Expected Capital Structure of Kay Copper

Following completion of the Transaction and the NewCo Concurrent Financing, Kay Copper is expected to have approximately 70,300,000 common shares outstanding, on an undiluted basis, with ownership expected to be held approximately as follows:

- Kodiak: 28%

- Teck: 28%

- Kay Copper existing shareholders: 9%

- NewCo Initial Financing subscribers: 12%

- NewCo Concurrent Financing subscribers: 23%

Final capitalization will be determined upon negotiation and execution of definitive agreements and the NewCo Concurrent Financing.

Additional Terms

- In addition to receiving common shares of Kay Copper, each of Teck and Kodiak are expected to enter into separate Investor Rights Agreements with Kay Copper.

- Teck is expected to be granted offtake rights with respect to certain concentrate production from the Mohave and Copper Hill projects, subject to definitive documentation.

On behalf of the Board of DirectorsKodiak Copper Corp.

Claudia TornquistPresident & CEO

For further information contact:Nancy Curry, VP Corporate Developmentncurry@kodiakcoppercorp.com+1 (604) 646-8362

About Kodiak Copper

Kodiak is focused on advancing its 100%-owned MPD copper-gold porphyry project in the prolific Quesnel Terrane in south-central British Columbia, Canada, an established mining region with producing mines and existing infrastructure. MPD exhibits all the hallmarks of a large, multi-centered porphyry district with the potential for future economic development. The initial Mineral Resource Estimate, published in 2025, outlines seven substantial deposits and underscores the scale and potential of the project. All known deposits remain open to expansion, and numerous targets across the property have yet to be tested. Kodiak continues to systematically explore MPD's district-scale potential with the goal of delivering new discoveries and building further critical mass toward being the region's next mine.

Kodiak's founder and Chairman, Chris Taylor, is well-known for his gold discovery success with Great Bear Resources. Kodiak is also part of Discovery GroupTM led by John Robins, one of the most successful mining entrepreneurs in Canada.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statement (Safe Harbor Statement): This press release contains forward-looking statements within the meaning of applicable securities laws. The use of any of the words "anticipate", "plan", "can", "could", "continue", "expect", "estimate", "objective", "may", "will", "would", "project", "shall", "should", "predict", "potential" and similar expressions are intended to identify forward-looking statements. In particular, this press release contains forward-looking statements concerning: the proposed creation of a new U.S.-focused copper exploration company expected to list on the TSXV; Kodiak vending Mohave to NewCo; Teck vending Copper Hill to NewCo; that NewCo will unlock value of Kodiak's non-core Mohave project and will generate compelling returns for its shareholders; that NewCo will be positioned for meaningful growth; completion of the NewCo Concurrent Financing; completion of the Amalgamation; the successful negotiation and execution of a definitive agreement; the receipt of consents or regulatory approvals, including potential TSXV approval; the closing of the Transaction in the third quarter of 2026, or at all; the closing of the NewCo Concurrent Financing; that Mark Osterberg will join Kay Copper as Vice-President Exploration on closing of the Transaction; and the future investor rights of Teck and Kodiak and future offtake rights of Teck regarding NewCo. Although the Company believes that the expectations and assumptions on which the forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because the Company cannot give any assurance that they will occur or prove to be correct. Since forward-looking statements address future events and conditions, they involve inherent assumptions, risks and uncertainties. Actual results could differ materially from those currently anticipated due to a number of assumptions, factors and risks. These assumptions and risks include, but are not limited to, assumptions and risks associated with: the ability of the parties to execute their business objectives related to the Transaction; the ability of the parties to negotiate and execute definitive agreements; the parties expectations regarding future results from Mohave and Copper Hill; the ability to obtain necessary capital for the NewCo Concurrent Financing; conditions in the equity financing markets; receipt of regulatory and shareholder approvals; the impact of increasing competition; the regulatory framework regarding royalties, taxes and environmental matters; the ability to achieve potential synergies and unlock value from the Transaction; and the nature of the proposed business of NewCo, including the exploration and production of natural resources.

Management has provided the above summary of risks and assumptions related to forward-looking statements in this press release in order to provide readers with a more comprehensive perspective on the Company's future operations. The Company's actual results, performance or achievement could differ materially from those expressed in, or implied by, these forward-looking statements and, accordingly, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits the Company will derive from them. These forward-looking statements are made as of the date of this press release, and, other than as required by applicable securities laws, the Company disclaims any intent or obligation to update publicly any forward-looking statements, whether as a result of new information, future events or results or otherwise.

THIS NEWS RELEASE IS NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/302249

Find winning stocks in any market cycle. Join 7 million investors using Simply Wall St’s investing ideas for FREE.

BHP Group (ASX:BHP) continues to attract attention after recent share price moves, with the stock up about 7% over the past month and about 29% over the past 3 months.

See our latest analysis for BHP Group.

The recent move has come after a strong run over 3 months, but the 1-day and 7-day share price returns are both down. This suggests some of that momentum may be cooling even as the 1-year total shareholder return of 76.63% highlights how rewarding the stock has been for investors over a longer period.

If you are looking beyond BHP Group in the resources space, this could be a useful moment to scan other copper focused opportunities through the 8 top copper producer stocks.

With BHP Group posting a 76.63% total return over the past year and trading around A$61.40, investors now face a key question: is there still value on the table, or is the market already pricing in future growth?

Most Popular Narrative: 49.5% Undervalued

According to the most followed narrative for BHP Group, a fair value of A$121.48 sits well above the recent A$61.40 share price, raising questions about how much of the company’s scale and profitability is currently reflected in the market.

BHP Group is one of the world’s largest mining companies, producing key commodities such as iron ore, copper, and metallurgical coal that are essential for global infrastructure, steel production, and the energy transition. In FY2024, BHP reported revenue of approximately US$55.7 billion and underlying attributable profit of US$13.7 billion, highlighting the company’s strong profitability and scale in global resource markets.

Want to see what underpins such a big gap between narrative value and price? The core assumptions rest on large scale output, resilient margins and long term demand for copper and iron ore. Curious how those inputs combine into that A$121.48 figure and what kind of earnings profile they imply over time?

Result: Fair Value of A$121.48 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, BHP Group’s narrative could be tested if global steel demand weakens and iron ore prices soften, or if copper intensive projects are delayed or scaled back.

Find out about the key risks to this BHP Group narrative.

Another View on BHP Group Using Market Ratios

While the user narrative points to BHP Group as 49.5% undervalued at A$121.48 per share, the market’s own yardstick tells a different story. At a P/E of 21.4x, BHP trades well above the Australian Metals and Mining industry at 11.9x and above its fair ratio of 20.3x, which suggests less of a bargain and more valuation risk if earnings do not keep pace.

Compared with a peer average P/E of 30.2x, BHP does not look stretched across its wider peer set. However, the premium to its industry and to that 20.3x fair ratio invites a simple question for investors: is this pricing a quality premium you are comfortable paying at A$61.40?

See what the numbers say about this price — find out in our valuation breakdown.

ASX:BHP P/E Ratio as at Jun 2026

Next Steps

If the mix of optimism and caution around BHP Group has you weighing both sides, act quickly to review the numbers and risk indicators for yourself with the 1 key reward and 1 important warning sign.

Looking for more investment ideas beyond BHP Group?

If you are reassessing BHP Group, do not stop there. Use this moment to broaden your watchlist with fresh ideas that match your risk and income goals.

- Spot potential turnaround stories early by reviewing the 58 elite penny stocks with strong financials that already show stronger financial foundations than many investors expect.

- Zero in on quality at a price by scanning the 8 high quality undervalued stocks that combine solid cash flows with more conservative market expectations.

- Strengthen the core of your portfolio by assessing the solid balance sheet and fundamentals stocks screener (19 results) before other investors crowd into the same resilient stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical datan and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or yourn financial situation. We aim to bring you long-term focused analysis driven by fundamental data.n Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.n Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include BHP.AX.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Canadian National Railway Co (NYSE:CNI) is one of the best long-term stocks to invest in according to Bill & Melinda Gates Foundation Trust. Canadian National Railway shares have gone up more than 20% over the past six months.

n matthew siddons / Shutterstock.comn

Canadian National Railway Co (NYSE:CNI) has landed a deal to provide rail services to mining giant BHP, according to a June 4 press release. Canadian National Railway will transport potash from BHP’s Jansen mine in Saskatchewan to ports in Vancouver for export to the global markets.

n

In this arrangement, Canadian National Railway will operate unit trains between the mine and the export terminals using BHP-owned railcars. The initial contract will run for around four years and is focused on the Jansen Stage 1 production. The railroad operator may have a role in the next phases of the project. The Jansen mine is expected to begin production in mid-2027.

n

BHP said the rail transport deal with Canadian National Railway strengthens the reliability of its supply chain. It also said this arrangement ensures it’s well-positioned to deliver potash from Saskatchewan to global customers. Canadian National Railway said the Jansen project is a significant opportunity for Canada’s export industry.

n

Canadian National Railway Co (NYSE:CNI) is a freight rail company headquartered in Quebec, Canada. Its nearly 20,000-mile rail network serves Canada and the US, facilitating the movement of everything from resource materials and factory inputs to finished goods.

n

n

While we acknowledge the potential of CNI as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

n

n

n

READ NEXT: Billionaire Ken Fisher’s Top 12 High-Growth Stock Picks and 12 Best Tech Stocks to Invest In on the Dip.

n

Disclosure: None. Follow Insider Monkey on Google News.

This article first appeared on GuruFocus.

BHP Group (NYSE:BHP) will record a $2.3 billion writedown on its giant Jansen potash mine after another cost and timeline reset at the Canadian project. The latest review showed phase two will now cost $6.9 billion, up from the previous $4.9 billion estimate, adding fresh pressure to a project that has already tested investor patience.

- Warning! GuruFocus has detected 8 Warning Signs with BHP.

- Is BHP fairly valued? Test your thesis with our free DCF calculator.

The world's largest miner moved ahead with Jansen's expansion in 2023, before phase one had even started production, as fertilizer prices surged after Russia's invasion of Ukraine. Since then, potash prices have fallen, while costs across both phases have continued to rise, making the project more controversial among some investors.

BHP approved construction of the Saskatchewan mine in 2021 after years of debate over its large price tag. Phase one is expected to begin production next year, while phase two is now expected to start producing toward the end of 2031. BHP still views Jansen as a long-life potash business that could potentially operate for a century and scale toward the size of its flagship Australian iron ore operations.

This article first appeared on GuruFocus.

BHP Group (NYSE:BHP) shares fell sharply after the miner flagged a $2.3 billion write-down on its Jansen potash mine in Canada, driven by higher costs and delays tied to the project's expansion. The move marked BHP's biggest one-day share decline in 14 months, adding fresh pressure on a project that has already faced investor scrutiny over its scale, spending, and long development timeline.

- Warning! GuruFocus has detected 8 Warning Signs with BHP.

- Is BHP fairly valued? Test your thesis with our free DCF calculator.

The company said phase two of Jansen will now cost $6.9 billion, up from an earlier estimate of $4.9 billion, with production expected toward the end of 2031. BHP shares closed 5.6% lower in Sydney on Friday, while its UK-listed shares fell 4.4% in London on Thursday. Barclays analysts estimate BHP has spent $20.3 billion on the project so far, with $4.1 billion now impaired.

Barclays analysts including Amos Fletcher said expected internal rates of return have declined, and now estimate total returns of 7.1% across the first two development stages. BHP does not expect total capital expenditure to rise for the 2027 fiscal year, though it did not provide estimates for later years. First production from phase one is still expected next year, while the mine could possibly become a century-long business that BHP believes may eventually rival its Australian iron ore operations in scale.

USA Rare Earth, Inc. USAR and Teck Resources Limited TECK are key participants in the Zacks Mining – Miscellaneous industry. Both companies are engaged in the extraction, processing and development of minerals that are essential to modern technologies and industrial applications. USAR and TECK are well-positioned to benefit from the growing demand for critical materials used in electrification, clean energy technologies and advanced manufacturing.Both companies operate in capital-intensive mining industries that require extensive investments in infrastructure, advanced technologies and project development, while also navigating regulatory clearances and regulatory approval processes. At the same time, growing demand for minerals and metals critical to electric vehicles, renewable energy and other clean-energy technologies is creating favorable long-term growth opportunities for these companies.

The Case for USAR

USA Rare Earth has commissioned its hydrometallurgical demonstration facility in Wheat Ridge, CO, in June 2026, marking a key step in building an integrated rare earth supply chain outside China. The company expects to begin producing commercial-quality separated rare earth oxides, including NdPr, dysprosium and terbium, in the third quarter of 2026.The facility will process material from multiple sources, including the Round Top facility, third-party feedstocks and recycled magnet swarf, while supporting feasibility studies and future commercial-scale operations.Also, the successful commissioning of Phase 1a of USAR’s commercial magnet production line at its Stillwater, OK, facility marks an important milestone in USAR’s growth strategy. The development enables the company to begin supplying sintered NdFeB permanent magnets to customers starting in the second quarter of 2026.The commissioning demonstrates USA Rare Earth’s capability to operate a complex rare earth magnet manufacturing process at a commercial scale. At its Stillwater facility, USAR transforms rare earth materials into high-performance NdFeB permanent magnets through a series of production steps used in end markets such as defense, aerospace and automotive.The Phase 1a is expected to achieve an annual production run rate of 600 metric tons by the end of 2026, while the planned Phase 1b expansion is projected to double total capacity to 1,200 metric tons annually by the first quarter of 2027. Once fully operational, the Stillwater facility is expected to be among the first large-scale NdFeB magnet manufacturing facilities in the United States, supporting a more resilient domestic rare earth supply chain.USAR has strengthened its growth strategy through a combination of financing and acquisitions. In June 2026, the company secured access to up to $1.6 billion in government-backed funding under the CHIPS Program from the U.S. Department of Commerce. The package includes up to $277 million in federal funding and up to $1.3 billion in loan support as the company advances key development milestones.In May 2026, USA Rare Earth secured a $14.2 million grant from the Texas Semiconductor Innovation Fund to boost the development of its Round Top Mountain rare earth project in West Texas, aimed at supporting domestic supply chains for critical minerals used in defense, semiconductors, AI and advanced technologies.Also, in March 2026, USAR agreed to acquire Texas Mineral Resources Corp. in an all-stock transaction valued at approximately $73 million, giving it full ownership of the Round Top Project. The company expects commercial production at Round Top to begin in 2028, with a long-term goal of processing nearly 40,000 metric tons of rare earth and critical mineral feedstock per day by 2030. The November 2025 acquisition of Less Common Metals is expected to provide critical metal and alloy feedstock for the Stillwater plant.While USAR is making progress with its growth initiatives, it is still in the early stages of commercialization and continues to report losses as it scales its operations. While the acquisition of Less Common Metals has started contributing to revenues, profitability remains under pressure from higher operating expenses associated with expansion efforts, acquisitions and workforce additions.In the first quarter of 2026, selling, general and administrative expenses surged to $21.2 million from $7 million in the prior-year period, driven by higher legal, consulting and personnel-related costs. Research and development expenses also rose to $14.2 million from $1.7 million a year ago, reflecting increased investment in product development and growth initiatives.

The Case for TECK

As part of its long-term growth strategy, Teck Resources is increasing its focus on copper and other critical minerals that are essential for electrification and clean energy technologies. The company has agreed to merge with Anglo American plc to form the Anglo Teck group, creating one of the world's largest copper-focused mining companies. It will have more than 70% exposure to copper and is set to be among the top five global copper producers. The new company will consist of six world-class copper assets and premium iron ore and zinc operations with a combined annual copper production of 1.2 million tons. It is projected to grow 10% to 1.35 million tons by 2027, strengthening its position in the global copper market.Teck Resources is further strengthening its copper growth pipeline by advancing several development projects toward sanction readiness. The company is progressing with permitting activities, securing land access and refining the business cases for its Zafranal and San Nicolás projects.Zafranal is expected to have a mine life of 19 years and produce copper-gold concentrates through open-pit mining and conventional processing. The project is anticipated to generate an average of 126,000 tons of contained copper annually during its first five years of operation. Meanwhile, the San Nicolás project is advancing through the feasibility study stage and is expected to produce approximately 63,000 tons of copper and 147,000 tons of zinc annually during its first five years, on a 100% ownership basis.Also, the Highland Valley Mine Life Extension is expected to extend the mine’s life from 2028 to 2046. Expected average annual copper production will likely be 132,000 tons over the life of the mine. The company expects to increase copper production to around 800,000 tons before the end of this decade.However, the company’s zinc in concentrate production declined to 120 thousand tons in the first quarter of 2026 from 137 thousand tons a year earlier, reflecting lower grades at Red Dog in line with the mine plan. TECK expects zinc production to trend lower over the next three years as the mine approaches the end of its life. Full-year 2026 zinc production guidance is 410-460 thousand tons compared with 565 thousand tons produced in 2025.Operating costs at several assets increased year over year due to higher contractor, energy and maintenance expenses. The company highlighted exposure to fuel price volatility and higher freight and explosives costs linked to geopolitical developments. Even though there is currently no significant risk of fuel supply disruption, the company expects an impact on costs at its Chilean operations due to the requirement for diesel imports.

How Does the Zacks Consensus Estimate Compare for USAR & TECK?

The Zacks Consensus Estimate for USAR’s 2026 bottom line is pegged at a loss of 35 cents per share. Also, the company’s consensus estimate for the 2027 bottom line is pegged at a loss of 32 cents per share.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for TECK’s 2026 bottom line is pegged at $3.35 per share. Also, the company’s consensus estimate for 2027 bottom line is pegged at $2.89 per share.

Image Source: Zacks Investment Research

Price Performance and Valuation of USAR & TECK

In the past year, USAR’s shares have surged 103%, while TECK stock has gained 71.9%.

Image Source: Zacks Investment Research

USA Rare Earth is trading at a forward 12-month price-to-earnings ratio of negative 73.33X while Teck Resources’ forward earnings multiple sits at 21.39X.

Image Source: Zacks Investment Research

Final Take

USAR is benefiting from the ramp-up of its commercial magnet production line, along with strategic acquisitions and investments designed to build a fully integrated domestic rare earth supply chain. The acquisitions of Less Common Metals and Texas Mineral Resources are expected to enhance the company’s operational capabilities and support its long-term growth strategy. However, USAR remains in the early stages of commercialization and continues to incur losses as it invests in capacity expansion, technology development and other growth initiatives.In contrast, Teck Resources’ strong performance in the coming quarters is supported by its scale of operation, asset diversity and strategic transformation. The planned merger with Anglo American will create a global copper and critical minerals leader, with more than 70% exposure to copper. Though near-term zinc in concentrate production at Red Dog has been impacted by operational issues, TECK’s long-life assets and growth projects are expected to lower execution risk.Given these factors, TECK seems a better pick for investors than USAR currently. While TECK Materials carries a Zacks Rank #3 (Hold) at present, USA Rare Earth has a Zacks Rank #4 (Sell).You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Teck Resources Ltd (TECK) : Free Stock Analysis Report

USA Rare Earth Inc. (USAR) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Teck Resources Limited (NYSE:TECK) is one of the best copper stocks to buy for the AI and electrification boom. The company’s freshest relevant angle is tied to the planned Anglo-Teck merger. On May 18, 2026, Reuters reported that Anglo American agreed to sell its Australian steelmaking coal assets for up to $3.88 billion, a move aimed at simplifying the company and reducing debt ahead of its planned combination with Teck. The sale keeps investor attention on Anglo American’s portfolio reset before the merger closes.

n

For Teck investors, the update matters because the proposed combination would make copper the center of the future company’s investment case. Teck and Anglo American have said the combined Anglo Teck would become a top-five global copper producer and is expected to offer investors more than 70% exposure to copper. That gives Teck a cleaner link to electrification, grid expansion, and AI-related power demand, even without a direct data-center customer angle.

nn

Teck Resources Limited (NYSE:TECK) is a Vancouver-based resource company with copper and zinc operations across North and South America and a copper growth pipeline.

n

n

While we acknowledge the potential of TECK as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

n

n

n

READ NEXT: 33 Stocks That Should Double in 3 Years and Cathie Wood 2026 Portfolio: 10 Best Stocks to Buy.

n

Disclosure: None. Follow Insider Monkey on Google News.

Toronto, Ontario–(Newsfile Corp. – June 17, 2026) – Honey Badger Silver Inc. (TSXV: TUF) (OTCQB: HBEIF) (FSE: 1QA) (Tradegate: 1QA) ("Honey Badger" or the "Company") is pleased to announce the appointment of Tom Chep. PEng., as Innovation Advisor.

"Tom brings a rare combination of advanced engineering expertise, entrepreneurial vision, and real-world experience developing and commercializing transformative technologies," said Chad Williams, Executive Chairman of Honey Badger Silver. "We are extremely fortunate to have Tom on our team. He will evaluate many new technologies, such as the latest drone, robotic, AI, and energy generation/storage technologies, to ensure that the PC Silver Mine re-starts production as quickly, efficiently, and as ecologically sound as possible. Tom's experience includes a strong partnership with an Indigenous technology group, considering Indigenous Knowledge in emerging technologies, and looks forward to working in partnership with Honey Badger Silver's Indigenous partners who will benefit from the PC Silver Mine's re-start."

Mr. Chep is an accomplished technology entrepreneur, engineer, and product development leader with extensive experience in advanced energy systems, infrastructure development, electrification, and complex technical project execution. He is the founder of Arc Motor Company Inc., where he has led the development of modular vehicle platforms, integrated energy systems, and scalable charging and power infrastructure solutions.

Throughout his career, Mr. Chep has worked across electrified transportation systems, industrial technologies, energy infrastructure, critical infrastructure projects, and large-scale construction environments. His expertise spans systems engineering, infrastructure integration, commercialization strategy, product development, and the deployment of advanced technologies from concept through commercial scale.

Mr. Chep holds a degree in Electrical Engineering and is a licensed Professional Engineer (P.Eng.).

"I am excited to join Honey Badger Silver at such a pivotal stage in the Company's growth," said Mr. Chep. "The PC Silver Mine is one of the most compelling undeveloped silver assets in North America and represents a unique opportunity to apply innovative technologies to enhance future operations. I look forward to working with the team to evaluate solutions that can improve project performance, strengthen sustainability, and help position Honey Badger Silver as a modern, technology-enabled mining company."

As Honey Badger Silver re-starts the PC Silver Mine, Mr. Chep will focus on identifying opportunities across electrification, energy infrastructure, automation, advanced mining technologies, remote operations, and innovative transportation and logistics solutions. His mandate will include evaluating emerging technologies that could reduce capital requirements, lower operating costs, improve reliability, and strengthen the long-term sustainability of the Company's operations.

About Honey Badger Silver (TSXV: TUF) (OTCQB: HBEIF) (FSE: 1QA) (Tradegate: 1QA)

Silver is rare and valuable. Honey Badger Silver controls some of Canada's richest untapped silver potential. With the acquisition of the fully permitted, high-grade PC Silver Mine, the Company has become a leading North American silver and critical minerals company.

Backed by an impressive portfolio of 8 high-quality silver mineral projects in Canada, including the Sunrise Lake, Plata, and Nanisivik properties, Honey Badger Silver controls district-scale land positions in some of the most metal-rich jurisdictions on the continent.

What sets Honey Badger Silver apart is its strategic blend of real silver ownership and growth leverage: the Company holds 10,000 ounces of physical silver yielding 12% annually, reinforcing tangible asset value while advancing aggressive exploration and acquisition plans.

Led by a proven team of mine-builders and capital markets professionals, Honey Badger Silver is building a cash-generating, asset-backed platform for the bull cycle in precious and critical minerals.

More information is available at www.honeybadgersilver.com.

Chad WilliamsExecutive Chairman, Interim CEO

Investor Relationsinvestors@honeybadgersilver.com | +1 (647) 226-7315

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Cautionary Note Regarding Forward-Looking Information

This news release contains "forward-looking information" within the meaning of the applicable Canadian securities legislation that is based on expectations, estimates, projections and interpretations as at the date of this news release, including without limitation, the potential for Tom Chep to reduce costs and improve the PC Silver Mine. Any statement that involves discussions with respect to predictions, expectations, interpretations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as "expects", or "does not expect", "is expected", "interpreted", "management's view", "anticipates" or "does not anticipate", "plans", "budget", "scheduled", "forecasts", "estimates", "believes" or "intends" or variations of such words and phrases or stating that certain actions, events or results "may" or "could", "would", "might" or "will" be taken to occur or be achieved) are not statements of historical fact and may be forward-looking information and are intended to identify forward-looking information. This forward-looking information is based on reasonable assumptions and estimates of management of the Company at the time such assumptions and estimates were made, and involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Honey Badger to be materially different from any future results, performance or achievements expressed or implied by such forward-looking information.

Such factors include, but are not limited to, risks relating to capital and operating costs varying significantly from estimates; delays in obtaining or failures to obtain required governmental, environmental or other project approvals; uncertainties relating to the availability and costs of financing needed in the future; changes in equity markets; inflation; fluctuations in commodity prices; delays in the development of projects; other risks involved in the mineral exploration and development industry; and those risks set out in the Company's public documents filed on SEDAR+ (www.sedarplus.ca) under Honey Badger's issuer profile. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed timeframes or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/301839

Southern Copper (SCCO) ended the recent trading session at $193.22, demonstrating a +1.81% change from the preceding day's closing price. The stock's change was more than the S&P 500's daily gain of 1.65%. On the other hand, the Dow registered a gain of 0.92%, and the technology-centric Nasdaq increased by 3.07%.

Coming into today, shares of the miner had gained 7.36% in the past month. In that same time, the Basic Materials sector lost 4.3%, while the S&P 500 gained 0.48%.

Analysts and investors alike will be keeping a close eye on the performance of Southern Copper in its upcoming earnings disclosure. The company is forecasted to report an EPS of $1.85, showcasing a 51.64% upward movement from the corresponding quarter of the prior year. In the meantime, our current consensus estimate forecasts the revenue to be $4.23 billion, indicating a 38.73% growth compared to the corresponding quarter of the prior year.

Regarding the entire year, the Zacks Consensus Estimates forecast earnings of $7.25 per share and revenue of $16.54 billion, indicating changes of +38.36% and +23.22%, respectively, compared to the previous year.

Investors should also take note of any recent adjustments to analyst estimates for Southern Copper. These revisions typically reflect the latest short-term business trends, which can change frequently. As a result, we can interpret positive estimate revisions as a good sign for the business outlook.

Our research suggests that these changes in estimates have a direct relationship with upcoming stock price performance. To utilize this, we have created the Zacks Rank, a proprietary model that integrates these estimate changes and provides a functional rating system.

The Zacks Rank system, spanning from #1 (Strong Buy) to #5 (Strong Sell), boasts an impressive track record of outperformance, audited externally, with #1 ranked stocks yielding an average annual return of +25% since 1988. Over the past month, there's been a 4.05% rise in the Zacks Consensus EPS estimate. As of now, Southern Copper holds a Zacks Rank of #3 (Hold).

In terms of valuation, Southern Copper is presently being traded at a Forward P/E ratio of 26.17. This expresses a discount compared to the average Forward P/E of 26.42 of its industry.

It's also important to note that SCCO currently trades at a PEG ratio of 1.79. The PEG ratio bears resemblance to the frequently used P/E ratio, but this parameter also includes the company's expected earnings growth trajectory. Mining – Non Ferrous stocks are, on average, holding a PEG ratio of 1.55 based on yesterday's closing prices.

The Mining – Non Ferrous industry is part of the Basic Materials sector. This industry currently has a Zacks Industry Rank of 186, which puts it in the bottom 24% of all 250+ industries.

The Zacks Industry Rank gauges the strength of our industry groups by measuring the average Zacks Rank of the individual stocks within the groups. Our research shows that the top 50% rated industries outperform the bottom half by a factor of 2 to 1.

You can find more information on all of these metrics, and much more, on Zacks.com.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Southern Copper Corporation (SCCO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

How much a stock's price changes over time is important for most investors, since price performance can both impact your investment portfolio and help you compare investment results across sectors and industries.

FOMO, or the fear of missing out, also plays a role in investing, particularly with tech giants and popular consumer-facing stocks.

What if you'd invested in Teck Resources Ltd (TECK) ten years ago? It may not have been easy to hold on to TECK for all that time, but if you did, how much would your investment be worth today?

Teck Resources Ltd's Business In-Depth

With that in mind, let's take a look at Teck Resources Ltd's main business drivers.

Vancouver, Canada-based Teck Resources is committed to mining and mineral development with business units focused on copper and zinc. Teck is also a leading producer of lead and a significant producer of specialty metals such as germanium, indium and cadmium. It also produces gold dore and silver. Teck also produces industrial products and fertilizers, which are recovered from its zinc and lead smelting operations in Trail, B.C.

Teck Resources divested its Steelmaking Coal business or Elk Valley Resources (“EVR”) in July 2024. The company categorized it as discontinued operations and restated the revenue and EPS (in CAD) for all quarters of 2023 and for 2024.

Teck Resources is a significant copper producer in the Americas, with four operating mines in Canada, Chile and Peru, and development projects in North and South America. Its main projects are Highland Valley Copper in Canada and Antamina, Quebrada Blanca (QB) and Carmen de Andacollo in South America.

Teck Resources is one of the world's largest producers of mined zinc, with three operating mines in the United States and Peru, and it owns one of the world's largest fully integrated zinc and lead smelting and refining facilities located in Canada. Teck produces zinc concentrate from Red Dog Operations in Alaska. In addition to marketing its zinc concentrate around the world, the company’s concentrate team also purchases concentrate from other mines for processing at the Trail operations complex in British Columbia.In September 2025, Teck Resources entered the merger agreement with Anglo American to form the Anglo Teck group. The new company will boast an industry-leading portfolio, consisting of six world-class copper assets, and premium iron ore and zinc operations. The combined annual copper production of 1.2 million tons is projected to grow 10% to 1.35 million tons by 2027. The combined company will also be one of the world's largest zinc producers. Within four years of completion, the deal is expected to yield around $800 million in annual pre-tax synergies. It has been cleared by shareholders of both the companies.

Bottom Line

Anyone can invest, but building a successful investment portfolio requires research, patience, and a little bit of risk. So, if you had invested in Teck Resources Ltd, ten years ago, you're likely feeling pretty good about your investment today.

A $1000 investment made in June 2016 would be worth $5,687.72, or a 468.77% gain, as of June 15, 2026, according to our calculations. Investors should note that this return excludes dividends but includes price increases.

The S&P 500 rose 254.54% and the price of gold increased 214.85% over the same time frame in comparison.

Looking ahead, analysts are expecting more upside for TECK.

Teck delivered record copper sales and higher earnings in the first quarter of 2026, supported by elevated copper prices and improved performance at Quebrada Blanca and Trail. The balance sheet remains solid providing visibility on capital allocation. However, zinc production is set to decline as Red Dog matures, input cost volatility remains a risk and execution across large growth projects requires sustained discipline. The long-term prospects for copper remain positive, supported by the clean energy transition trend. Teck entered into a merger agreement with Anglo American plc to form the Anglo Teck group. The combined annual copper production of 1.2 million tons is projected to grow 10% to 1.35 million tons by 2027. Within four years of completion, the deal is expected to yield around $800 million in annual pre-tax synergies.

The stock has jumped 5.69% over the past four weeks. Additionally, no earnings estimate has gone lower in the past two months, compared to 14 higher, for fiscal 2026; the consensus estimate has moved up as well.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Teck Resources Ltd (TECK) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

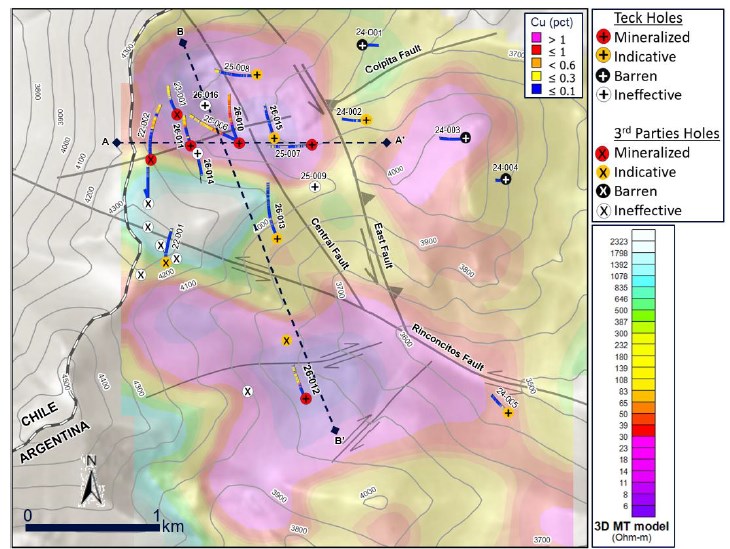

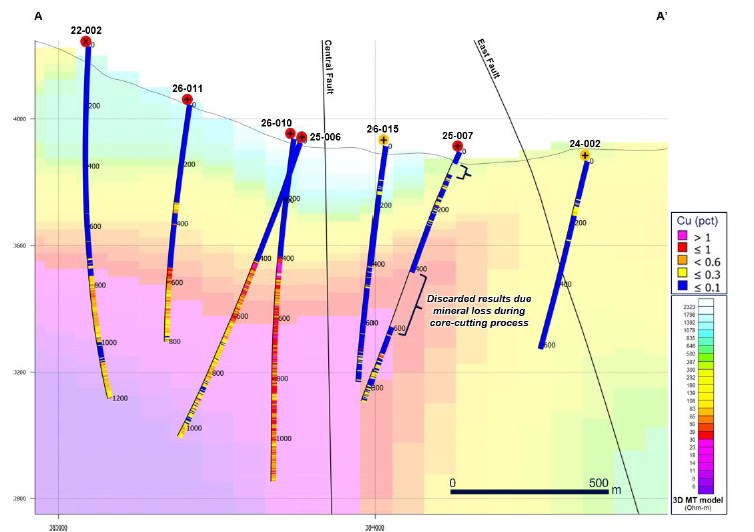

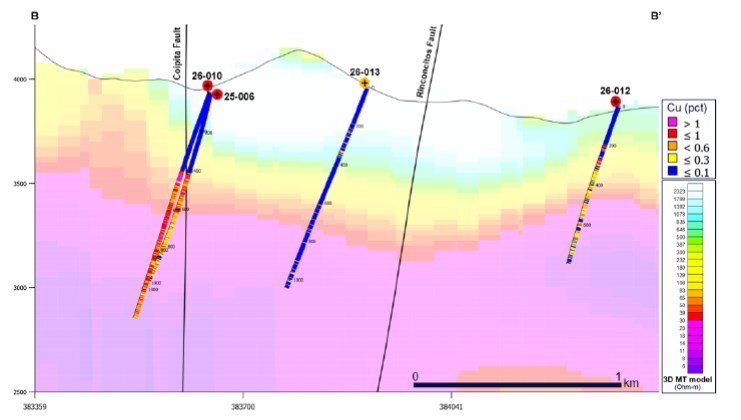

Drilling Confirms Continuity of Large-Scale Mineralized System & Delivers New Discovery

Toronto, Ontario–(Newsfile Corp. – June 15, 2026) – AbraSilver Resource Corp. (TSX: ABRA) (OTCQX: ABBRF) ("AbraSilver" or the "Company") is pleased to report assay results from the 2026 drill program at the La Coipita copper-gold-molybdenum project ("La Coipita" or the "Project") located in the San Juan Province of Argentina.

The drill program is fully funded and operated by a subsidiary of Teck Resources Limited ("Teck") under the terms of the earn-in and joint venture agreement, as per the Company's news release dated January 22, 2024.

The 2026 program comprised 5,248 metres ("m") of diamond drilling across seven holes (DDH-LC26-010 through DDH-LC26-016), designed to test the limits and vertical continuity of known mineralization at the Yaretas target and evaluate new targets generated by the first-ever magnetotelluric ("MT") geophysical survey completed across the property.

Key Highlights

- Hole DDH-LC26-010 returned the strongest drill intercept recorded to date at La Coipita: 747.5 m grading 0.69% Cu, 0.06 g/t Au and 142 ppm Mo, from 396 m to 1,143.5 m down-hole depth, confirming the presence of a robust and vertically extensive copper-gold-molybdenum system. Including:

- 108 m at 1.06% Cu, 0.10 g/t Au and 204 ppm Mo, from 396 to 504 m;

- 184 m at 0.78% Cu, 0.09 g/t Au and 123 ppm Mo, from 604 to 788 m

- Hole DDH-LC26-011 returned 250.6 m at 0.39% Cu, 0.07 g/t Au and 119 ppm Mo, from 550 to 800.6 m. This hole confirmed continuity of mineralization between previously reported holes DDHC-22-002 and DDH-LC25-006 (see Figures 1 and 2), further strengthening confidence in the scale and continuity of the Yaretas system.

- Hole DDH-LC26-012 resulted in a new, shallower discovery at the Yaretas Sur target, located approximately 1.9 km south of the main Yaretas drilling area (see Figures 1 and 3), intersecting multiple zones of copper-gold mineralization:

- 42 m at 1.03% Cu, 0.63 g/t Au and 41 g/t Ag, from 264 to 306 m, including 28 m at 1.45% Cu, 0.81 g/t Au and 45 g/t Ag

- Additional mineralized intervals that confirm a vertically extensive mineralized system at Yaretas Sur.

- The first-ever MT geophysical survey conducted during the 2026 season provides valuable new insights into the geometry of the mineral system and indicates potential extensions to the south, guiding target generation for future drill campaigns.

- Holes DDH-LC26-013 and DDH-LC26-015 intercepted indicative copper mineralization within the Yaretas zone, highlighting variability in the system; holes DDH-LC26-014 and DDH-LC26-016 were unable to reach planned target depths.

John Miniotis, President and CEO, commented, "The 2026 drill program delivered several important milestones at La Coipita. Most notably, hole DDH-LC26-010 returned the strongest intercept drilled on the property to date, while hole DDH-LC26-011 confirmed the continuity of mineralization across the core Yaretas system. Equally encouraging was the new, shallower discovery at Yaretas Sur, located nearly 2 km south of the main drilling area, which further demonstrates the district-scale potential of this project. We are pleased to have Teck, one of the world's leading mining companies, continuing to advance La Coipita, and we look forward to continued exploration success."

Stuart McCracken, Vice President, Exploration, Teck commented, "These results reinforce our commitment to responsible and sustainable exploration and our long-term interest in the geological potential of the region."

Table 1 – Summary of Key Drill Intercepts

Intercepts greater than 25%-metres copper shown in bolded text:

| Drill Hole | Area | From(m) | To(m) | Type | Interval (m) | Cu% | Au g/t | Moppm | Ag g/t |

| DDH-LC26-10 | Yaretas | 396.0 | 1,143.5 | – | 747.5 | 0.69 | 0.06 | 142 | 3 |

| Including | 396.0 | 504.0 | Secondary Enrichment | 108.0 | 1.06 | 0.10 | 204 | 6 | |

| Including | 604.0 | 788.0 | Hypogene & High Sulphidation ("HS") | 184.0 | 0.78 | 0.09 | 123 | 3 | |

| Including | 646.0 | 666.0 | Hypogene & HS | 20.0 | 1.05 | 0.13 | 147 | 4 | |

| Including | 724.0 | 742.0 | Hypogene & HS | 18.0 | 1.00 | 0.11 | 153 | 3 | |

| DDH-LC26-11 | Yaretas | 550.0 | 800.6 | – | 250.6 | 0.39 | 0.07 | 119 | 3 |

| including | 550.0 | 770.0 | HS | 220.0 | 0.42 | 0.08 | 127 | 3 | |

| DDH-LC26-12 | Yaretas Sur | 192.0 | 206.0 | HS | 14.0 | 0.67 | 0.28 | 1 | 6 |

| 264.0 | 306.0 | HS | 42.0 | 1.03 | 0.63 | 2 | 41 | ||

| including | 264.0 | 292.0 | HS | 28.0 | 1.45 | 0.81 | 2 | 45 | |

| 316.0 | 366.0 | HS | 50.0 | 0.29 | 0.12 | 1 | 4 | ||

| 398.0 | 464.0 | HS | 66.0 | 0.28 | 0.04 | 1 | 3 | ||

| 488.0 | 566.0 | HS | 78.0 | 0.39 | 0.24 | 1 | 4 | ||

| 584.0 | 604.0 | HS | 20.0 | 0.36 | 0.05 | 1 | 2 | ||

| 624.0 | 662.0 | HS | 38.0 | 0.28 | 0.02 | 1 | 3 |

Note: All results in this news release are rounded. Assays are uncut & undiluted. Widths are drilled widths, not true widths. True widths are unknown

La Coipita Project Overview

La Coipita is a district-scale property covering over 70,000 hectares in the western San Juan Province, adjacent to the Chilean border. Elevation across the property ranges between 3,500 and 4,500 MASL with moderate to high relief.

The property lies within the prolific Miocene porphyry-epithermal belt of Argentina and Chile, host to numerous world-class deposits, including Filo del Sol, Los Azules, El Indio, Veladero, Pascua Lama and El Pachon.

Since commencing the earn-in program in 2024, Teck has completed a total of 11,270 m of diamond drilling across 19 holes at La Coipita, representing approximately US$23 million in expenditures to date against the total earn-in commitment of US$20 million. In addition to Teck completing US$20 million in expenditures, certain cash payments defined in the earn-in and joint venture agreement remain to be completed by Teck. On completion of these obligations, it is anticipated the parties will form a Joint Venture (80% Teck, 20% AbraSilver).

The 2026 program successfully extended known mineralization at Yaretas, confirmed continuity between previously drilled areas and identified a new mineralized centre at Yaretas Sur. Together with the results of the MT survey, these findings support the potential for a large-scale mineralized system extending well beyond the currently drilled footprint.

The 2026 program, which included 5,248 metres of drilling and the first MT survey ever completed on the property, represents a significant step forward in defining the scale and geometry of the system as the project advances toward potential future Mineral Resource delineation.

Figure 1 – Plan Map – Drillhole Locations and Cu Results with MT-Resistivity Survey at 500 m Depth.

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/11792/301375_fd15b8c2a41daba3_001full.jpg

Figure 2 – A-A' Cross Section: Cu-Grade Results and MT-Resistivity

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/11792/301375_fd15b8c2a41daba3_002full.jpg

Figure 3 – B-B' Cross Section: Yaretas (left) and Yaretas Sur (right) Targets, Cu-Grade Results and MT-Resistivity

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/11792/301375_fd15b8c2a41daba3_003full.jpg

Collar Data

| Hole Number | UTM Coordinates | Elevation | Azimuth | Dip | Depth (m) | |

| DDH-LC26-10 | 383738 | 6615406 | 3937 | 340 | -70 | 1,143.5 |

| DDH-LC26-11 | 383408 | 6615329 | 4045 | 340 | -70 | 800.6 |

| DDH-LC26-12 | 384236 | 6613500 | 3870 | 340 | -70 | 794 |

| DDH-LC26-13 | 384027 | 6614707 | 3959 | 340 | -70 | 1,040 |

| DDH-LC26-14 | 383405 | 6615338 | 4044 | 160 | -70 | 639 |

| DDH-LC26-15 | 384026 | 6615398 | 3914 | 340 | -70 | 821 |

| DDH-LC26-16 | 383490 | 6615677 | 4025 | 340 | -70 | 9.7 |

Note: All results in this news release for La Coipita have been rounded. Assays are uncut and undiluted. Widths are drilled widths, not true widths. True widths cannot be determined due to the uncertain geometry of mineralization.

QA/QC and Core Sampling Protocols

Core samples were taken every 2m, sent to San Juan for cutting (where applicable), and submitted to ALS Labs for sample preparation and for four-acid digestion multi-element analysis with ICP-MS finish (method codes ME-MS61) and with AAS finish for overlimit of Cu, Pb, Ag, As, Zn, Mo (OG62), and for Au by fire assay with ICP-MS finish (Au-ICP21) and with gravimetry finish for overlimit (Au-GRA21). Steps taken to avoid copper loss from drill core of the supergene enrichment zone included: (1) drilling with triple tube core barrels; (2) sampling whole core in zones of supergene mineralization (retaining 15-20cm of representative skeleton core); (3) avoiding interaction with water or core saws; and (4) taking field duplicates with a hydraulic core splitter.

Qualified Persons

David O'Connor P.Geo., Chief Geologist for AbraSilver, is the Qualified Person as defined by National Instrument 43-101 Standards of Disclosure for Mineral Projects, and he has reviewed and approved the scientific and technical information in this news release.

About AbraSilver

AbraSilver is an advanced-stage exploration company focused on rapidly advancing its 100%-owned Diablillos silver-gold project in the mining-friendly Salta and Catamarca provinces of Argentina. The current Measured and Indicated Mineral Resource estimate for Diablillos (tank leach-only) consists of 102.0 Mt grading 65 g/t Ag and 0.62 g/t Au, containing approximately 213Moz of silver and 2.0Moz of gold, with significant further upside potential based on recent exploration drilling. The Company is led by an experienced management team and has long-term supportive shareholders. In addition, the Company has an earn-in option and joint venture agreement with Teck on the La Coipita project, located in the San Juan province of Argentina. AbraSilver is listed on the Toronto Stock Exchange under the symbol "ABRA" and in the U.S. on the OTCQX under the symbol "ABBRF."

The full Technical Report in respect of the updated MRE estimate is being prepared in accordance with NI 43-101 and will be available on SEDAR+ (www.sedarplus.ca) under the Company's issuer profile within 45 days from the news release dated May 06, 2026.

For further information please visit the AbraSilver Resource website at www.abrasilver.com, our LinkedIn page at AbraSilver Resource Corp., and follow us on X at www.x.com/abrasilver

Alternatively, please contact:

John Miniotis, President and CEOinfo@abrasilver.comTel: +1 416-306-8334

Cautionary Statements

This news release includes certain "forward-looking statements" under applicable Canadian securities legislation. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable, are subject to known and unknown risks, uncertainties, and other factors which may cause the actual results and future events to differ materially from those expressed or implied by such forward-looking statements. All statements that address future plans, activities, events or developments that the Company believes, expects or anticipates will or may occur are forward-looking information. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. When considering this forward-looking information, readers should keep in mind the risk factors and other cautionary statements in the Company's disclosure documents filed with the applicable Canadian securities regulatory authorities on SEDAR+ at www.sedarplus.ca. The risk factors and other factors noted in the disclosure documents could cause actual events or results to differ materially from those described in any forward-looking information. The Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Neither the TSX nor its Regulation Services Provider (as that term is defined in the policies of the TSX) accepts responsibility for the adequacy or accuracy of this news release

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/301375

MIAMI, June 10, 2026 (GLOBE NEWSWIRE) — EmergingGrowth.com a leading independent small cap media portal announces the schedule of the 93rd Emerging Growth Conference on June 10 & 11, 2026.

The Emerging Growth Conference identifies companies in a wide range of growth sectors, with strong management teams, innovative products & services, focused strategy, execution, and the overall potential for long-term growth.

Register for the Conference here.

Submit Questions for any of the presenting companies to: Questions@EmergingGrowth.com

For updates, follow us on Twitter

Presenting Today – Wednesday June 11, 2026