Southern Copper Corporation (NYSE:SCCO) is one of the best commodity stocks to buy for the supercycle. On May 15, Scotiabank lifted the price target on Southern Copper Corporation (NYSE:SCCO) to $135 from $133, maintaining an Underperform rating on the shares. The firm told investors that it believes investors should find “attractive trading opportunities” with the industry facing increased volatility and scenarios of high metal price levels.

n

n

Southern Copper Corporation (NYSE:SCCO) also received a rating update from Wells Fargo on May 1, with the firm cutting the price target on the stock to $171 from $186 while maintaining an Equal Weight rating on the shares. The firm stated that fiscal Q1 benefited from solid byproduct credits, adding that energy cost risk was downplayed by management. It also cited the resolved Tia Maria permitting issues and believes that at about 13 times 2026 EV/EBITDA on $6/lb copper, near-term copper tightness appears largely priced in.

n

Southern Copper Corporation (NYSE:SCCO) is involved in the production, development, and exploration of zinc, copper, silver, and molybdenum. The company conducts its operations in the following segments: Peruvian Operations, Mexican Open-Pit Operations, and Mexican Underground Mining Operations.

n

n

While we acknowledge the potential of SCCO as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

n

n

n

READ NEXT: 15 Stocks That Will Make You Rich in 10 Years AND 12 Best Stocks That Will Always Grow.

n

Disclosure: None. Follow Insider Monkey on Google News.

MEXICO CITY, May 26, 2026 (GLOBE NEWSWIRE) — The following is a statement by PODER:

This information is related to the worst environmental disaster in the history of metal mining in Mexico: the 2014 spill of 40 million liters of toxic waste in the Sonora and Bacanuchi rivers by Buenavista del Cobre, a mine owned by Grupo Mexico, affecting more than 22 thousand people. Government authorities have yet to abide by court rulings to repair the damages caused and accumulated over time, and Grupo México has used legal obstacles to avoid taking preventive measures and paying for the damages.

According to the Ministry of the Environment (Semarnat) in Mexico, the total cost of the spill amounts to MORE THAN ONE BILLION (USD). The company alleges it agreed to an arrangement with the government to provide around 86,500 million USD. This amount will contribute to the installation of a hospital and a few water treatment plants that can separate heavy metals. There is NO public information to confirm this. The amount committed is the bare minimum to remediate the damages, and to prevent future disasters that could add to the current social and environmental damages. Accoridng to this source, the company has proposed confidentiality clauses on issues related to the communities’ rights, making reparations contingent on this.

This will continue to have repercussions for its investors.

In the context of the 2026 AGM of Grupo Mexico and Southern Copper Corporation, affected communities urge its investors to:

- Be vocal in linking executive compensation for the new CEO Leonardo Contreras Lerdo de Tejada to ensuring that the company operates in accordance with an assessment of risks and benefits for all workers, surrounding communities, value chains, and shareholders, including a preventative plan to identify, mitigate, communicate, and address current social, environmental, and climate negative impacts.

- Require a clear plan, with a concrete timeline and designated funds, to actively and efficiently repair the damages to the people, environment, biodiversity, land, and territory caused by the 2014 toxic spill, and ensure that these continue until reparation is achieved.

- Ensure that existing and new tailings dams meets the necessary safety standards to prevent it from overflowing, rupturing, or leaking into aquifers or rivers, and that all liquids discharged by the company are properly managed, leaving only clean, potable water.

We urge you to ensure that the company keeps its investors informed with transparency and accountability, that it transforms verbal commitments into concrete actions on this distressing, painful and shameful case, and to prevent further ones.

The affected communities have asked Grupo Mexico's investors to address the issue, be vigilant of greenwashing, and fulfill their obligation to respect human rights.

PODER is a corporate accountability and human rights NGO accompanying the affected communities. https://poderlatam.org

Contact Information: comunicacion@poderlatam.org

Make better investment decisions with Simply Wall St's easy, visual tools that give you a competitive edge.

The latest update to Teck Resources’ valuation lifts the fair value estimate to CA$83.06 from CA$79.35, signalling a modest reassessment of what the stock could be worth. That shift sits alongside a series of Street price target moves around CA$79 that are closely linked to expectations for the Anglo American merger and how execution risks are being weighed. As you read on, you will see how these evolving targets fit into the broader analyst narrative and what that means for tracking the story from here.

What Wall Street Has Been Saying 🐂 Bullish Takeaways

- Several firms, including Deutsche Bank, JPMorgan, Scotiabank, CIBC, TD Securities and Canaccord, have raised price targets in recent months, signalling a generally constructive stance on Teck Resources’ value.

- Deutsche Bank has lifted its target multiple times, most recently to US$62 from US$60, and maintains a Buy rating. This points to ongoing confidence in the stock at current levels.

- CIBC moved its target to C$79 from C$77 and shifted its rating to Tender after Canadian approval of the Anglo American merger, highlighting the role of the deal in the equity story.

- Scotiabank’s target moves, including an increase to C$80 with a Sector Perform rating, indicate that some analysts see support for the current valuation range even with more reserved ratings.

🐻 Bearish Takeaways

- Canaccord has both raised and lowered its Teck Resources target over this period, which underscores that not all analysts view the risk and reward profile as one way.

- CIBC’s Tender stance around C$79 ties part of the thesis to successful completion of the Anglo American merger. Delays or issues around remaining approvals in China and South Korea could weigh on sentiment.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there's more to the story. Head to the Simply Wall St Community to discover more perspectives!

TSX:TECK.B 1-Year Stock Price Chart

We've flagged 1 risk for Teck Resources. See which could impact your investment.

What's in the News

- Titan Mining and Teck Resources signed a cooperation agreement to evaluate recovering about 13,000 kg per year of contained germanium from Empire State Mines processing streams, using Teck's germanium recovery platform at Trail to assess feed specifications, volumes and potential long term offtake terms.

- Kodiak Copper, Teck Resources and Kay Copper announced a non binding letter of intent to combine Kodiak's Mohave project and Teck's Copper Hill project in Arizona into a new US focused copper exploration company. The new company is expected to seek a TSX Venture Exchange listing as Kay Copper Corp., with Teck set to hold about 28% and receive certain concentrate offtake rights, subject to approvals and financings.

- Copper Fox Metals outlined a planned CA$9.1 million program for 2026 at the Schaft Creek copper project in British Columbia, which is operated by Teck Resources with a 75% interest. The program targets work on the geological model, metallurgical testwork, tailings and mine plan options, road access studies and preparation for a potential Pre Feasibility Study.

How This Changes the Fair Value For Teck Resources

- Fair value estimate is CA$83.06, up from CA$79.35.

- Revenue growth assumption is 0.10%, reduced from 3.28%.

- Net profit margin assumption is 13.21%, down from 15.45%.

- Future P/E is 31.40x, up from 25.12x.

- Discount rate is 8.18%, slightly higher than the prior 8.00%.

Never Miss an Update: Follow The Narrative

Narratives link a company's real world projects, risks and milestones to a financial forecast and fair value that update as new information comes through. They help you see how individual data points fit into a bigger investment story.

Head over to the Simply Wall St Community and follow the Narrative on Teck Resources to stay up to date on:

- How copper growth projects like Highland Valley life extension, QB optimization and the Zafranal and San Nicolas pipeline are expected to reshape Teck Resources' production mix.

- The role of balance sheet strength, liquidity of about $8.9b and long running ESG focus in supporting project execution and access to capital.

- Key risks from project delays, cost inflation, permitting and commodity price weakness that could constrain margins and future earnings potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical datan and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or yourn financial situation. We aim to bring you long-term focused analysis driven by fundamental data.n Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.n Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include TECK-B.TO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Endeavour, Rio Tinto and Glencore lead rebounding miners as metals prices seesaw Proactive uses images sourced from Shutterstock

Mining stocks climbed on Tuesday as investors returned to metals after sharp gains in gold, silver and copper prices driven by hopes of easing geopolitical tensions in the Middle East.

n

Endeavour Mining PLC (LSE:EDV) led the FTSE 100 risers, up 3.5%, while Rio Tinto Ltd (LSE:RIO) gained 2.3%, Glencore PLC (LSE:GLEN) rose 2.2%, Antofagasta PLC (LSE:ANTO) 1.9%, Anglo American PLC (LSE:AAL) 1.4% and Fresnillo PLC (LSE:FRES) 0.8%.

n

The rally followed strong moves in metals markets on Monday after Donald Trump said a "memorandum of understanding" in talks to end the US and Israel's war on Iran "has been largely negotiated".

n

However, the US launched strikes on Iran overnight, targeting missile launch sites and vessels suspected of attempting to lay mines in what Washington described as “defensive” action.

n

Meanwhile, a senior delegation of Iranian negotiators is travelling to Qatar for fresh talks with the US over frozen financial assets and a possible wider deal.

n

Gold climbed from around $4,500 an ounce on Friday to about $4,570 on Monday before easing back to $4,535 on Tuesday morning. Silver followed a similar pattern, rising from $75.4 an ounce at the end of last week to above $78.5 before retreating to around $76.4.

n

Copper prices also surged, with US copper futures reaching $6.44 a pound and London Metal Exchange copper trading at $13,667.50 a tonne at one stage.

n

The moves helped lift both precious metal miners and diversified mining groups, with investors betting higher commodity prices could support earnings if geopolitical tensions remain elevated.

n

"For markets the message is straightforward: the peace trade is more fragile than Monday’s price action suggested," said market analyst Patrick Munnelly at Tickmill.

n

He said the latest round of strikes "complicates hopes for an interim deal to extend the ceasefire and reopen the Strait of Hormuz, even though Trump said talks were 'proceeding nicely' and Pakistan’s military chief Asim Munir reportedly told China that an agreement was close.

n

"Investors are still cautiously optimistic, but the risk premium has not disappeared. As long as military action and negotiations are running in parallel, energy markets will remain vulnerable to abrupt reversals."

Agnico Eagle Mines Limited (NYSE:AEM) is one of the cheap NYSE stocks to buy according to analysts. On May 20, Agnico Eagle Mines Limited announced a subscription agreement to acquire approximately 243.9 million common shares of Wallbridge Mining Company Limited for a total consideration of C$22.4 million. Expected to close around May 22, the transaction will increase Agnico Eagle’s stake in Wallbridge to approximately 19.62% on a non-diluted basis.

n

Upon closing, the companies will enter into an investor rights agreement, granting Agnico Eagle the right to maintain its pro-rata ownership in future equity financings and the option to nominate members to Wallbridge’s board of directors. This move aligns with Agnico Eagle’s broader corporate strategy of securing strategic interests in mining projects with high geological potential.

n

The investment is subject to standard closing conditions, including regulatory approval from the Toronto Stock Exchange. Agnico Eagle Mines Limited (NYSE:AEM) indicated that it may adjust its investment in Wallbridge in the future based on evolving market conditions, strategic priorities, and other relevant factors.

n

n

Agnico Eagle Mines Limited (NYSE:AEM) is a senior Canadian gold mining company and the world’s second-largest gold producer, focused on exploring, developing, and operating mines. It operates high-quality, low-risk assets primarily in Canada, Australia, Finland, and Mexico, with about 85% of its production coming from Canada.

n

n

While we acknowledge the potential of AEM as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

n

n

n

READ NEXT: 33 Stocks That Should Double in 3 Years and Cathie Wood 2026 Portfolio: 10 Best Stocks to Buy.

n

Disclosure: None. Follow Insider Monkey on Google News.

Teck Resources Limited (NYSE:TECK) is one of the 10 Best Performing Canadian Stocks So Far in 2026.

n

On May 15, 2026, Deutsche Bank raised the firm’s price target on Teck Resources Limited (NYSE:TECK) to $62 from $60 previously and maintained a Buy rating on the shares.

n

JPMorgan also increased its price target on Teck Resources Limited (NYSE:TECK) to $48 from $45 previously while keeping a Neutral rating on the shares.

n

Last month, Teck Resources Limited (NYSE:TECK) reported Q1 adjusted EPS of C$1.75, compared to C$0.60 in the prior-year period. Revenue rose to C$3.94B from C$2.29B a year earlier. President and CEO Jonathan Price said the company delivered a strong start to 2026, driven by record quarterly copper sales, favorable commodity pricing, and steady operational execution across the portfolio. Management highlighted particularly strong performance from the Quebrada Blanca operation, which achieved record quarterly copper sales alongside continued operating stability. Price added that the quarter underscored both the resilience of Teck’s asset portfolio and the strength of its balance sheet as the company continues working toward completing its proposed merger of equals with Anglo American.

n Pixabay/Public Domainn

Teck Resources Limited (NYSE:TECK) is a diversified mining company involved in the exploration, development, processing, refining, and reclamation of mineral properties globally.

n

n

While we acknowledge the potential of TECK as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

n

n

n

READ NEXT: 33 Stocks That Should Double in 3 Years and Cathie Wood 2026 Portfolio: 10 Best Stocks to Buy.

n

Disclosure: None. Follow Insider Monkey on Google News.

Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

Why Southern Copper Stock Is Back in Focus

Southern Copper (SCCO) is back on investors radar after a stronger earnings outlook, continued quarterly earnings beats and a new US$318.6 million upgrade plan for its Cuajone mine in Peru.

See our latest analysis for Southern Copper.

The US$179.12 share price has eased in recent months, with the 90 day share price return down 10%, even as the year to date share price return sits at 22.7% and the 1 year total shareholder return is 110.7%. This hints that recent volatility contrasts with a much stronger longer term experience for investors.

If this kind of copper exposure has your attention, it may be worth broadening your search using our screener of 8 top copper producer stocks

With earnings estimates moving higher, recent quarterly beats, and a US$179.12 share price that sits above the average analyst target, the key question now is clear: is there still an opportunity for investors here, or is the market already pricing in future growth?

Most Popular Narrative: 10.2% Overvalued

At a last close of $179.12, the most followed narrative puts Southern Copper’s fair value at $162.54, creating a clear gap investors are watching.

Southern Copper has announced substantial capital investments totaling over $15 billion, including projects in Mexico and Peru, which are expected to drive future production growth and potentially boost revenue significantly. The company’s Buenavista zinc concentrator is now operating at full capacity, anticipated to drive a 31% increase in zinc production in 2025, likely enhancing revenues and improving net margins due to efficient operations.

Curious what kind of growth, margin profile and future earnings multiple could still justify a premium price tag on a slow and steady expansion plan? The full narrative lays out a detailed earnings path, explains how profitability might shift, and specifies a valuation multiple for those projected results.

Result: Fair Value of $162.54 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this story can change quickly if cost pressures, community disruptions, or trade tensions between the U.S. and China weaken margins and project timelines.

Find out about the key risks to this Southern Copper narrative.

Next Steps

Given the mix of optimism and concern in this story, it makes sense to look at the figures yourself, consider both perspectives, and review the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Southern Copper has your attention, do not stop here. Broaden your watchlist now so you are not relying on a single story for future decisions.

- Spot potential upside early by scanning screener containing 20 high quality undiscovered gems that combine strong fundamentals with quieter market attention.

- Strengthen your portfolio core with solid balance sheet and fundamentals stocks screener (46 results) that can help support resilience when conditions get choppy.

- Target income-focused opportunities by reviewing 10 dividend fortresses built around higher yields with stability in mind.

This article by Simply Wall St is general in nature. We provide commentary based on historical datan and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or yourn financial situation. We aim to bring you long-term focused analysis driven by fundamental data.n Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.n Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SCCO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Friday, May 22, 2026The Zacks Research Daily presents the best research output of our analyst team. Today's Research Daily features new research reports on 16 major stocks, including Texas Instruments Inc. (TXN), Linde plc (LIN) and BHP Group Ltd. (BHP), as well as two micro-cap stocks Landmark Bancorp, Inc. (LARK) and Global Self Storage, Inc. (SELF). The Zacks microcap research is unique as our research content on these small and under-the-radar companies is the only research of its type in the country.These research reports have been hand-picked from the roughly 70 reports published by our analyst team today.You can see all of today’s research reports here >>>Ahead of Wall StreetThe daily 'Ahead of Wall Street' article is a must-read for all investors who would like to be ready for that day's trading action. The article comes out before the market opens, attempting to make sense of that morning's economic releases and how they will affect that day's market action. You can read this article for free on our home page and can actually sign up there to get an email notification as this article comes out each morning.You can read today's AWS here >>> Pre-Markets Up to Finish the Week Ahead of Memorial DayToday's Featured Research ReportsTexas Instruments’ shares have outperformed the Zacks Semiconductor – General industry over the past six months (+95.2% vs. +30.2%). The company is benefiting from solid data center demand, which is boosting its prospects in the enterprise systems market. A sustained focus on expanding its product portfolio across the Analog and Embedded Processing segments helps capture market share. Texas Instruments’ deepening focus on internal manufacturing and advanced technology infusion is another positive. Its robust cash flows and aggressive shareholder return policies instill confidence in its long-term prospects. However, its overall growth might be impacted by a slow recovery in the industrial market as customers are cautiously spending amid ongoing macroeconomic uncertainties. Rising manufacturing costs and the growing tech war between the United States and China are other concerns. Our model estimates indicate that revenues are likely to witness a CAGR of 12.1% through 2026-2028.(You can read the full research report on Texas Instruments here >>>)Shares of Linde have outperformed the Zacks Chemical – Specialty industry over the past six months (+28.5% vs. +12.7%). The company is a leading industrial gas supplier serving energy, healthcare, manufacturing, metals and electronics markets through long-term contracts with minimum purchase commitments that support stable cash flows during downturns. LIN has a $9.9B project backlog, including $7.1B of long-term Sale of Gas projects, providing durable earnings visibility and double-digit returns. Management expects operating margins to expand above its traditional 40–60 basis-point range via cost controls, automation and AI-driven efficiency initiatives. LIN reported strong first-quarter 2026 earnings on higher pricing and incremental project start-ups. However, Linde faces pressure in EMEA from weak industrial activity, softer chemicals demand, geopolitical disruptions and policy uncertainty, which could reduce volumes, delay investments and weigh on profitability.(You can read the full research report on Linde here >>>)BHP’s shares have outperformed the Zacks Mining – Miscellaneous industry over the past six months (+61.8% vs. +39.1%). The company remains a high-quality diversified miner with leadership in iron ore and growing leverage to copper and potash, supported by low-cost operations and disciplined capital allocation. Recent updates point to resilient iron ore volumes despite weather disruption, strong execution at Escondida and Copper South Australia. BHP’s strategic shift toward future-facing commodities like copper and potash positions it well to benefit from global decarbonization and trends. Strong cash generation, efforts to lower debt and portfolio actions support funding flexibility. However, weak steel demand, commodity price volatility and cost pressures in parts of the footprint remain headwinds. Large project delivery and capital intensity at Jansen, along with the suspended nickel business and regulatory uncertainty in Australia, remain key risks. (You can read the full research report on BHP here >>>)Shares of Landmark Bancorp have gained +5.9% over the past six months against the Zacks Financial – Savings and Loan industry’s gain of +17.9%. This microcap company with a market capitalization of $170.37 million benefits from a diversified community banking franchise across Kansas and Missouri, supporting balanced exposure to residential, commercial, agricultural, and municipal lending markets. The company is strengthening profitability through disciplined deposit pricing, improved loan yields, and expansion in net interest margin, creating a more resilient earnings profile. Credit quality remains manageable with stable reserves and limited charge-offs despite modest increases in delinquencies. Capital levels and tangible book value continue to improve, supported by consistent earnings generation and a long history of dividend payments.Management is also enhancing funding flexibility by emphasizing core relationship deposits while reducing reliance on brokered funding. In addition, liquidity management and active securities portfolio positioning help mitigate interest-rate volatility.(You can read the full research report on Landmark Bancorp here >>>)Global Self Storage’s shares have gained +6.8% over the past six months against the Zacks REIT and Equity Trust – Other industry’s gain of +11.9%. This microcap company with a market capitalization of $59.51 million has its investment thesis centered on targeting underserved secondary and tertiary markets, where supply growth is more rational and competition is lower than in major metropolitan areas. Global Self Storage’s focus on operational efficiency, customer retention and technology-enabled revenue management has supported strong occupancy and recurring cash-flow generation. Growth opportunities remain tied to selective acquisitions, JVs and redevelopment initiatives that can expand earnings without significant development risk. Investors should monitor margin pressure from rising labor and property-tax costs, which have recently limited profitability. SELF’s small scale also increases sensitivity to localized fluctuations. Current valuation levels suggest the market is discounting concerns around scale and margins, though continued growth could support upside and dividends.(You can read the full research report on Global Self Storage here >>>)Other noteworthy reports we are featuring today include Vertiv Holdings Co (VRT), Spotify Technology S.A. (SPOT) and Symbotic Inc. (SYM).Mark VickerySenior EditorNote: Sheraz Mian heads the Zacks Equity Research department and is a well-regarded expert of aggregate earnings. He is frequently quoted in the print and electronic media and publishes the weekly Earnings Trends and Earnings Preview reports. If you want an email notification each time Sheraz publishes a new article, please click here>>>

Today's Must Read

Texas Instruments (TXN) Gains From Robust Data Center Demand

Lincoln (LNC) rides on Premium Growth, Elevated Expenses Hurt

BHP Group (BHP) Bets on Growth Investments as Costs Hurt Margins

Featured Reports

Large User Base and Pricing Power Aid Spotify (SPOT), No Dividends AilPer the Zacks analyst, SPOT's Strong subscriber growth and improving pricing power ensure revenue growth, but the absence of cash dividends may deter income-focused shareholders.

Warehouse Automation Aids Symbotic (SYM), Customer Concentration AilsThe Zacks analyst is concerned about the customer concentration risk at Symbotic. The long-term push by retailers and wholesalers to automate warehouse operations is, however, a positive.

Insmed (INSM) Rides on Sales Uptake for Bronchiectasis DrugThe Zacks Analyst believes the demand for Insmed's Brinsupri, the first treatment for non-CF bronchiectasis, is strong. The drug is expected to achieve blockbuster status in 2026.

Increasing Adoption of Dragonfly Platform Aids Onto Innovation (ONTO)Per the Zacks analyst, Onto Innovation's top-line is gaining from higher demand for the Dragonfly platform. Momentum in both advanced packaging and advanced nodes is a tailwind.

Disciplined Investments and Customer Additions Aid OGE Energy (OGE)Per the Zacks analyst, OGE Energy will benefit from its systematic capital investment to upgrade its infrastructure. Rising customer base will further boost its performance.

Lincoln (LNC) rides on Premium Growth, Elevated Expenses HurtPer the Zacks analyst, Lincoln's growing premium is driven by new products and the enhancement of the existing ones, which keep driving its top line. However, escalating expenses remain a concern.

Wendy's (WEN) Gains on Project Fresh Momentum Amid Cost PressuresPer the Zacks analyst, Wendy's is benefiting from Project Fresh initiatives, digital engagement and international expansion. However, soft comparable sales and elevated costs remain headwinds

New Upgrades

Vertiv (VRT) Rides on Strong AI-Driven Data Center Power NeedsPer the Zacks analyst, Vertiv is benefiting from rising data center power and thermal needs as AI deployments drive higher infrastructure density and faster build cycles.

Higher Nitrogen Demand and Prices Drive CF Industries (CF)Per the Zacks analyst, CF Industries will gain from higher demand for nitrogen fertilizers in major markets. Higher nitrogen prices amid lower supply availability will also drive its margins.

Par Pacific Continues to Bank on Excess RINs and Low DebtThe Zacks analyst likes Par Pacific because Renewable Identification Number (RIN) monetization could free up working capital, and its low debt load supports investments and opportunistic buybacks.

New Downgrades

Whirlpool (WHR) Witnesses Operational Headwinds and Tariff PressuresPer the Zacks analyst, Whirlpool's performance is reflecting ongoing operational and market challenges. It has been witnessing tariff pressures, weak housing demand and promotional intensity.

Rising Net Outflows and Weak Liquidity Hurts Lazard (LAZ) FinancialsPer the Zacks analyst, rising net outflows continue to weigh on Lazard's assets under management (AUM) growth. Also, weak liquidity position remains a key concern for the company.

Prestige Consumer (PBH) Struggles With Supply VolatilityThe Zacks analyst is concerned with Prestige Consumer's ongoing supply pressures in eye care, uneven shipment, lean safety stocks and rising execution risks that could weigh on fiscal 2027 growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Texas Instruments Incorporated (TXN) : Free Stock Analysis Report

BHP Group Limited Sponsored ADR (BHP) : Free Stock Analysis Report

Linde PLC (LIN) : Free Stock Analysis Report

Landmark Bancorp Inc. (LARK): Free Stock Analysis Report

Global Self Storage, Inc. (SELF): Free Stock Analysis Report

Spotify Technology (SPOT) : Free Stock Analysis Report

Vertiv Holdings Co. (VRT) : Free Stock Analysis Report

Symbotic Inc. (SYM) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE.

- If you are wondering whether BHP Group at A$59.75 is still priced attractively after a strong run, the starting point is to understand what the current share price implies about its underlying value.

- The stock is up 30.6% year to date and 62.3% over the past year, although it has slipped 1.2% over the last week while still showing a 6.4% gain over the past month. These changes can affect how you think about both upside potential and downside risk.

- Recent coverage around BHP has focused on its position within global resources and how shifts in commodity demand and market sentiment are feeding into expectations for the stock. This context helps explain why shorter term price moves can look choppy, while the longer term chart shows a very different picture.

- Despite this share price performance, BHP currently records a valuation score of 1 out of 6. The next sections will break down what traditional valuation tools say about the stock and then finish with a broader way to think about value that goes beyond just the headline multiples.

BHP Group scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: BHP Group Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the cash the company might generate in the future and then discounting those cash flows back to today.

For BHP Group, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $10.33b. Analyst estimates and subsequent extrapolations point to projected Free Cash Flow of $11.36b in 2030, with a series of annual forecasts in between. Simply Wall St uses analyst inputs for the first years and then extends the trend to build a 10 year cash flow curve.

On this basis, the discounted projected cash flows result in an estimated intrinsic value of $40.75 per share. Compared with the current share price of A$59.75, the model suggests BHP is trading at a premium, with the DCF output indicating the stock is 46.6% overvalued on this measure.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests BHP Group may be overvalued by 46.6%. Discover 10 high quality undervalued stocks or create your own screener to find better value opportunities.

BHP Discounted Cash Flow as at May 2026

Approach 2: BHP Group Price vs Earnings

For profitable companies, the P/E ratio is a useful yardstick because it links what you pay for the stock directly to the earnings it currently generates. It is a quick way to see how much the market is paying for each dollar of profit.

What counts as a “normal” or “fair” P/E often reflects how the market views a company’s growth outlook and risk profile. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually points to a lower one.

BHP Group currently trades on a P/E of 21.11x. That sits above the Metals and Mining industry average P/E of 12.76x, but below the peer group average of 31.36x. Simply Wall St also calculates a proprietary “Fair Ratio” of 19.40x, which is the P/E it would expect for BHP given factors such as its earnings characteristics, industry, profit margin, market cap and risk profile.

This Fair Ratio aims to be more tailored than a simple comparison against peers or the broad industry because it accounts for company specific features rather than just grouping everything together.

Comparing the Fair Ratio of 19.40x with the current P/E of 21.11x suggests the stock is trading a little above that fair level.

Result: OVERVALUED

ASX:BHP P/E Ratio as at May 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 4 top founder-led companies.

Upgrade Your Decision Making: Choose your BHP Group Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring this to life by letting you attach a clear story about BHP Group to the numbers you care about, linking your view on its future revenue, earnings and margins to a forecast, a Fair Value and then a simple comparison with the current share price. All of this is available within an easy tool on Simply Wall St’s Community page that updates as new news or earnings arrive. The page already hosts very different perspectives, such as a lower fair value around A$31.79 that leans heavily on copper and project risks, and a higher fair value around A$121.48 that leans on scale, diversification and demand for critical commodities. This can help you see where your own view sits and how that might guide when you choose to act.

For BHP Group however we’ll make it really easy for you with previews of two leading BHP Group Narratives:

Fair value: A$121.48 per share

Implied discount to this fair value: about 50.8% below the narrative fair value

Revenue growth assumption: 28%

- Frames BHP as a large scale producer of iron ore, copper and metallurgical coal tied into long term infrastructure, steel and energy transition demand.

- Highlights FY2024 revenue of about US$55.7b and underlying profit of US$13.7b, with iron ore around 50% of revenue and copper about 33%.

- Sees BHP’s low cost operations and strong cash generation as key strengths, while flagging exposure to commodity price cycles and Chinese iron ore demand as the main risks.

Fair value: A$53.40 per share

Implied premium to this fair value: about 11.9% above the narrative fair value

Revenue growth assumption: 1.15%

- Sets out a view that BHP benefits from demand for critical minerals and steelmaking materials, supported by copper and potash projects and infrastructure spending in Asia and India.

- Notes analyst assumptions for modest revenue growth, higher profit margins over time and earnings of US$13.1b by about 2029, with a P/E of 19.1x applied to those earnings.

- Emphasizes risks around iron ore concentration, project execution, regulation, costs, and ESG pressures, and concludes that the current price sits close to the analyst consensus fair value.

If you find that your own expectations on growth, margins and risk line up with one of these narratives, that can help you decide whether today’s price feels stretched, conservative or somewhere in between, and whether BHP Group belongs on your watchlist or just on your radar for now.

Do you think there’s more to the story for BHP Group? Head over to our Community to see what others are saying!

ASX:BHP 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical datan and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or yourn financial situation. We aim to bring you long-term focused analysis driven by fundamental data.n Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.n Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include BHP.AX.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Company Executives Share Vision and Answer Questions Live at VirtualInvestorConferences.com

NEW YORK, May 22, 2026 (GLOBE NEWSWIRE) — Virtual Investor Conferences, the leading proprietary investor conference series, today announced the presentations from Precious Metals & Critical Minerals Hybrid Virtual Investor Conference held May 21st are now available for online viewing.

The company presentations will be available 24/7 for 90 days. Investors, advisors, and analysts may download investor materials from the company’s resource section.

May 21st

| Company | Ticker(s) |

| Keynote: Jeff Christian, Managing Partner of CPM Group “The Bullish Outlook for Precious Metals” | |

| Viva Gold Corp. | (OTCQB: VAUCF | TSXV: VAU) |

| Cygnus Metals Limited | (OTCQB: CYGGF | TSXV: CYG) |

| Eloro Resources Ltd. | (OTCQX: ELRRF | TSX: ELO) |

| Oreterra Metals Corp. | (OTCID: OTMCF | TSXV: OTMC) |

| Metals One plc. | (OTCQB: MTOPF| LSE: MET1) |

| Amaroq Ltd. | (OTCQX: AMRQF | LSE: AMRQ) |

| Midnight Sun Mining Corp. | (OTCQX: MDNGF | TSXV: MMA) |

| Star Gold Corp. | (OTCQB: SRGZ) |

| Sirios Resources Inc. | (OTCQB: SIREF | TSXV: SOI) |

| Canadian Phosphate Limited | (Pink: FTZZF | ASX: CP8) |

| Honey Badger Silver Inc. | (OTCQB: HBEIF | TSXV: TUF) |

| Renforth Resources Inc. | (Pink: RFHRF | CSE: RFR) |

To facilitate investor relations scheduling and to view a complete calendar of Virtual Investor Conferences, please visit www.virtualinvestorconferences.com.

About Virtual Investor Conferences®

Virtual Investor Conferences (VIC) is the leading proprietary investor conference series that provides an interactive forum for publicly traded companies to seamlessly present directly to investors.

Providing a real-time investor engagement solution, VIC is specifically designed to offer companies more efficient investor access. Replicating the components of an on-site investor conference, VIC offers companies enhanced capabilities to connect with investors, schedule targeted one-on-one meetings and enhance their presentations with dynamic video content. Accelerating the next level of investor engagement, Virtual Investor Conferences delivers leading investor communications to a global network of retail and institutional investors.

Media Contact: OTC Markets Group Inc. +1 (212) 896-4428, media@otcmarkets.com

Virtual Investor Conferences

Greg Young

VP Corporate Services

OTC Markets Group

(212) 652-5958

This article first appeared on GuruFocus.

Gina Rinehart is sharpening Hancock Prospecting's exposure to two very different corners of the market: US defense and global mining. During the first quarter, the closely held firm bought shares in RTX (NYSE:RTX), Northrop Grumman (NYSE:NOC), L3Harris Technologies (NYSE:LHX), and Lockheed Martin (NYSE:LMT), with those US weapons-maker stakes worth a combined $97 million as of March 31, according to a regulatory filing. The move puts nearly $100 million behind aerospace and defense names at a time when the broader defense index has been under pressure.

- Warning! GuruFocus has detected 9 Warning Signs with AMD.

- Is RTX fairly valued? Test your thesis with our free DCF calculator.

Mining, however, still looks like the deeper portfolio bet. Hancock added 1.35 million shares to its Hudbay Minerals (NYSE:HBM) position and also took a stake in Newmont (NYSE:NEM). Those holdings, together with Hancock's positions in Teck Resources (NYSE:TECK) and MP Materials (NYSE:MP), make up nearly half of the firm's roughly $3.3 billion stock portfolio, based on Bloomberg calculations. That positioning could be notable for investors because the MSCI World Metals & Mining Index has returned 19% this year through Friday's close, outpacing the S&P 500's 8.2% rise.

The split matters because Rinehart appears to be leaning into mining strength while also possibly building optionality in defense. The MSCI World Aerospace & Defense Index has fallen 3.5%, creating a sharp contrast with the rally in metals and mining. Rinehart, 72, built her fortune developing massive iron ore deposits in Western Australia and is currently worth $43.8 billion, according to the Bloomberg Billionaires Index.

Source: Getty Images

Written by Demetris Afxentiou at The Motley Fool Canada

n

When trade tensions rise, investors seek out the stocks that can provide some defensive appeal to offset that market volatility. Often, these stocks can continue to offer growth, even when the market gets choppy. That means picking companies that can offer strong essential demand and recurring, stable revenue streams, over more volatile picks.

n

Trade tensions often create volatility in supply chains, impact commodity prices, and tend to influence corporate spending. And while not every company is exposed equally, there are some that can benefit from that volatility.

n

Trade tensions also tend to amplify supply‑chain bottlenecks, which can create uneven performance across sectors and highlight the value of those companies with stable demand.

n

So then, what are the stocks that offer that defensive appeal needed and thus an opportunity? Several great options on the market can meet that goal, and here’s a look at four of them.

nOption #1: Teck Resourcesn

Teck Resources (TSX:TECK.B) is one of the better-known mining companies in Canada. Teck’s appeal to investors stems from its exposure to certain commodities that are tied to global demand trends.

n

One of those commodities is copper. Copper is an essential metal used in power grids, construction, manufacturing, and renewable energy transition. Teck also has exposure to steelmaking coal and zinc. The sheer necessity of those metals makes them ideal options for defensive portfolios, even when trade tensions rise.

n

More importantly, this demand backdrop should continue to support Teck’s earnings even when the market turns unpredictable.

nnOption #2: Waste Connectionsn

Irrespective of how trade tensions impact the entire market, there are some services that persist with consistency. Waste Connections (TSX:WCN) is the perfect example of that.

n

Waste Connections provides essential waste management services, which is arguably one of the most stable industries on the market. Its business model is built on recurring revenue, long-term contracts, and steady pricing power.

n

This steady cash‑flow profile is attractive during periods when the broader market sentiment becomes unpredictable.

n

These factors make Waste Connections one of the better defensive options to consider amid trade tensions, especially compared to more cyclical sectors. Speaking of defensive appeal, the company’s focus on secondary and exclusive markets bolsters that moat further and reduces competitive pressure.

n

In short, Waste Connections is a great example of how essential‑services companies can anchor a portfolio with defensive appeal.

nnOption #3: Fairfax Financialn

Fairfax Financial (TSX:FFH) is the third option for investors looking to navigate volatile markets stemming from trade tensions. Fairfax has built a reputation around that stability, primarily through its insurance operations and disciplined investment approach.

n

The company’s diversified insurance operations generate consistent underwriting income, while its investment strategy protects capital during periods of uncertainty.

n

Fairfax has historically positioned itself conservatively when risks rise, giving it the flexibility to take advantage of opportunities when markets eventually stabilize. This makes Fairfax a stabilizing presence in a market full of uncertainties and trade tensions.

nnOption #4: Nutrienn

Wrapping up the list of stocks that persist through trade tensions is Nutrien (TSX:NTR).

n

Nutrien is a key global player in agriculture, supplying potash, nitrogen, and phosphate products. Those products support crop production worldwide, making Nutrien a defensive pick.

n

Food security concerns often intensify during periods of trade tension. Nutrien’s global distribution network and scale give it a strong competitive position as countries work to secure stable agricultural inputs.

n

Even when trade dynamics shift, demand for crop nutrients tends to remain steady, helping Nutrien maintain its important role across market cycles.

nnThese TSX stocks will outlast trade tensionsn

No stock, even the most defensive, is immune to risk. Fortunately, the four stocks mentioned above represent a well-diversified mix of options from different sectors of the market.

n

In my opinion, one or all of these stocks should be a small position in a larger, well-diversified portfolio.

n

The post Trade Tensions Are Rising Again — These 4 TSX Stocks Look Built to Keep Delivering appeared first on The Motley Fool Canada.

nn

nShould you invest $1,000 in Fairfax Financial right now?n

Before you buy stock in Fairfax Financial, consider this:

n

The Motley Fool Canada team has identified what they believe are the top 10 TSX stocks for 2026… and Fairfax Financial wasn’t one of them. The 10 stocks that made the cut could potentially produce monster returns in the coming years.

n

Consider MercadoLibre, which we first recommended on January 8, 2014 … if you invested $1,000 in the “eBay of Latin America” at the time of our recommendation, you’d have over $18,000!*

n

Now, it’s worth noting Stock Advisor Canada’s total average return is 94%* – a market-crushing outperformance compared to 85%* for the S&P/TSX Composite Index. Don’t miss out on our top 10 stocks, available when you join our mailing list!

nGet the 10 stocks instantlynnn#start_btn6 {nbackground:#0e6d04 none repeat scroll;color:#fff;font-size:1.2em;font-family:’Montserrat’, sans-serif;font-weight:600;height:auto;margin:30px 0;max-width:350px;text-align:center;width:auto;}nn#start_btn6 a {ncolor:#fff;display:block;padding:20px;padding-right:1em;padding-left:1em;}nn#start_btn6 a:hover {nbackground:#FFE300 none repeat scroll;color:#000;}nnn@media (max-width:480px) {ndiv#start_btn6 {nfont-size:1.1em;max-width:320px;}n}nnmargin_bottom_5 {margin-bottom:5px;}nmargin_top_10 {margin-top:10px;}nn

* Returns as of April 20th, 2026

n

n

More reading

Fool contributor Demetris Afxentiou has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Fairfax Financial and Waste Connections. The Motley Fool recommends Nutrien. The Motley Fool has a disclosure policy.

n

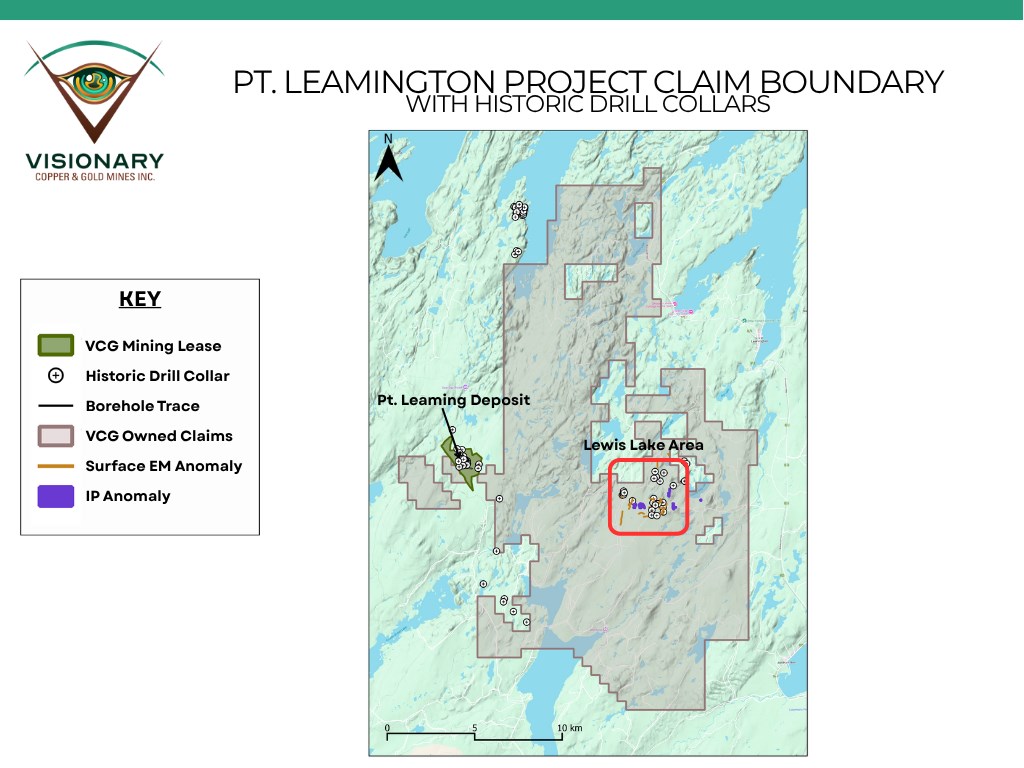

2026

Highlights

- District-scale land package expanded to ~30,000 hectares, covering the historic "Lewis Lake" area immediately east of the Pt. Leamington Deposit and a felsic volcanic-intrusive complex — geology that previous operators including Noranda, Billiton Exploration Canada Ltd. (now BHP), Altius Resources and Inmet Mining identified as prospective to host a volcanogenic massive sulphide ("VMS") deposit.

- Lewis Lake VMS thesis: Billiton/Rubicon defined the property target as a felsic volcanic-associated VMS deposit — comparable to other Wild Bight Group deposits including Pt. Leamington.

- Drill-confirmed permissive environment for a large VMS deposit: Billiton/Rubicon completed a 15-hole, 2,822 m Phase I diamond drilling program in 2000-2001 across six target areas and concluded that the drilling "established an environment that is permissive to host a large massive sulphide deposit".

- Multiple high-priority targets remain untested or partially tested, including undrilled Surface EM anomalies, strong off-hole EM conductors, IP Chargeability anomalies and untested airborne EM targets.

Vancouver, British Columbia–(Newsfile Corp. – May 21, 2026) – Visionary Copper and Gold Mines Inc. (TSXV: VCG) (OTCQB: VCGMF) (the "Company" or "Visionary") is pleased to announce that the Company has expanded its land package at its 100% owned Pt. Leamington Project (the "Project") located in central Newfoundland to nearly 30,000 hectares (300 km2). A portion of this newly staked ground covers the area historically referred to in assessment reports as "Lewis Lake," which was explored under a joint venture that included Billiton Exploration Canada Ltd. (now BHP) from 1999 to 2001, as well as adjacent ground previously worked by Noranda, Getty Canadian Metals, White Plains Resources, Altius Resources and Inmet Mining.

Max Porterfield, President & CEO of Visionary, stated, "Expanding our regional land package to ~30,000 hectares gives Visionary control over one of the most thoroughly studied — but most under-drilled — VMS districts in central Newfoundland. Billiton/BHP saw the same thing our team sees today: a felsic volcanic system with all the right ingredients to host a Pt. Leamington-scale, or larger, massive sulphide deposit. They did excellent work on very prospective ground which leaves us with the opportunity to quickly advance with our proven exploration model."

Dr. Stephen Piercey, Professional Geologist and Technical Advisor, added, "The Lewis Lake sequence is within similar rocks of the Wild Bight Group that hosts the Pt. Leamington deposit. Previous drilling by Billiton/Rubicon's drilling intersected sulphide mineralization and related VMS-style alteration coupled with multiple off-hole electromagnetic conductors that remain untested. These features, and presence in known VMS-hosting rocks of the Wild Bight Group warrant further drilling and testing of the Lewis Lake region."

Peter Dimmell, P.Geo., Visionary Director and Technical Advisor, who worked in the Wild Bight Group for Noranda Exploration and was on the drill for the discovery of the Pt. Leamington VMS deposit in 1971, over 50 years ago, commented, "Long after Noranda left the area, Billiton came in and confirmed the regional VMS potential with a 1,100-line-kilometre airborne survey. The survey identified fifteen conductive zones, some of which were drilled, but left behind undrilled priority targets which Visionary can systematically test with modern tools."

Regional VMS Opportunity – Lewis Lake

The Lewis Lake area lies within the Cambro-Ordovician Dunnage Zone of the Newfoundland Appalachians, specifically the Exploits Subzone, and is underlain by the Wild Bight Group. The Wild Bight Group is the host stratigraphy for the 100% owned Pt. Leamington VMS deposit (Pt. Leamington Project Area).

PT. LEAMINGTON PROJECT CLAIM BOUNDARYWITH HISTORIC DRILL COLLARS

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/3408/298362_61ca091b44672bab_001full.jpg

Billiton/Rubicon documented that the geology of the Lewis Lake area shares numerous characteristics with the host stratigraphy of the Pt. Leamington deposit, including (2001 Rubicon-Billiton Assessment Report, Property Geology, p. 4-5):

- A prevalence of massive and clastic (brecciated) quartz porphyritic rhyolite and high-level quartz porphyritic intrusive rocks (synvolcanic dyke swarm);

- Chert and jasper fragments and beds within heterolithic felsic-dominant volcaniclastic horizons;

- Areas of extensive hematite/magnetite (oxide-facies) volcanic and volcaniclastic rocks within and overlying the quartz porphyritic units – it is unknown if these oxide facies represent hydrothermal alteration or exhalative units and further work is required;

- An overall stratigraphic succession of footwall mafic volcanic rocks intruded by quartz porphyry, followed overlain by massive/brecciated quartz porphyritic rhyolite and heterolithic felsic-dominant volcaniclastic rocks — a similar stratigraphic sequence to the Pt. Leamington deposit; and

- Areas of extensive quartz-sericite (± biotite) plus pyrite alteration "typical of footwall alteration zones" (2001 Rubicon-Billiton Assessment Report, p. 5).

Between 1999 and early 2001, Billiton/Rubicon completed (2001 Rubicon-Billiton Assessment Report, Appendix II – Lewis Lake Project Status Report):

- A 1,100 line-kilometre Geoterrex airborne EM/Mag survey (1999) that identified 15 conductors or conductive zones across the property;

- 64.5 km of ground line cutting across seven grids with ground VLF/Mag and TEM (EM37) surveys (2000);

- 2.5 km of pole-dipole IP survey (2000) and an additional 19.9 km of pole-dipole IP and 34.4 km of ground magnetic surveys (2001);

- 115 prospecting and rock samples (2000), in addition to 67 samples collected during 1999 (1999 Rubicon Assessment Report, Executive Summary and p. 6-8); and

- A 15-hole, 2,822 m Phase I diamond drill program testing eight conductors and part of the large pole-dipole IP anomaly (2001 Rubicon-Billiton Assessment Report, p. 8-12, Table II).

Billiton/Rubicon concluded that this Phase I drilling had "established an environment that is permissive to host a large massive sulphide deposit" but recommended additional drilling of off-hole EM anomalies and untested surface and airborne EM anomalies that had not been tested (2001 Rubicon-Billiton Assessment Report, Conclusions and Recommendations, p. 12-14). No additional exploration was completed by Billiton/Rubicon following Phase I and no exploration drilling has been conducted in the area since.

Lewis Lake Target Areas

The following target inventory is a few of many opportunities drawn from Billiton/Rubicon's work in the Lewis Lake area:

Target Area One – Strong Off-Hole EM Conductors at JEN Grid

Billiton/Rubicon drilled four holes (LL2000-01 to LL2000-04) on the JEN grid to test three conductors (2001 Rubicon-Billiton Assessment Report, p. 6-7).

- LL2000-01 (152m) tested a strong shallow conductor and intersected several zones of sulphide-rich argillite and chert within mafic volcanics, potentially like the hanging wall/footwall contact at Pt. Leamington, from 88.85m to 99.60m, with a best interval of 0.50m of 480 ppm Cu and 460 ppm Zn at 93.20-93.70m (2001 Rubicon-Billiton Assessment Report, p. 6 and Table III, p. 12).

- LL2000-02 (490.7m) tested a strong deep 20-channel EM37 conductor and intersected a 50m sulphide-rich argillite/argillaceous tuff section from 393m to 443m within quartz porphyritic felsic volcanics. Best interval: 1.40m at 185 ppb Au (0.185 g/t Au), 0.84 g/t Ag, 178 ppm Cu, 459 ppm Zn from 392.60m (2001 Rubicon-Billiton Assessment Report, Table III, p. 12). Down-hole EM confirmed the in-hole sulphide source and identified a more highly conductive zone off-hole (2001 Rubicon-Billiton Assessment Report, p. 6).

- LL2000-03 (212m) intersected a 2.0m pyrrhotite-rich section with red-brown patchy sphalerite at 164.30-166.30m (best Table III interval 2.90m at 147 ppm Cu and 249 ppm Zn at 163.40-166.30 m). A down-hole Crone EM survey identified a strong off-hole anomaly at 170m, flagged as a "priority follow-up target for future drilling" (2001 Rubicon-Billiton Assessment Report, p. 7 and Table III, p. 12).

- LL2000-04 (220m) tested the eastern extension of the same deep conductor but was blocked before down-hole EM could be completed, leaving the strong deep conductor without an adequate explanation in this drill hole (2001 Rubicon-Billiton Assessment Report, p. 7).

Target Area Two – Strong, Undrilled 20-Channel Conductor at NBOG Grid

A single hole, LL2000-05 (100m), was drilled at the north end of the NBOG grid and intersected a 5.25m section of massive, very fine-grained laminated pyrrhotite with chert and jasper from 42.35m to 47.60m (best interval: 3.45m at 0.78 g/t Ag, 137 ppm Cu, 390 ppm Zn from 34.75m) (2001 Rubicon-Billiton Assessment Report, p. 7 and Table III, p. 12).

A separate strong 20-channel conductor in Northern Bog was proposed for drill testing in the vicinity of an old Noranda hole near 5500N/4000E but could not be drilled in 2000-2001 because of extremely wet bog conditions (2001 Rubicon-Billiton Assessment Report, p. 7 and p. 9).

Target Area Three – Multiple Untested Off-Hole EM Conductors at historic Fall Pond West

Five holes (LL2000-08 through LL2000-12) were drilled on the Fall Pond West grid. Several intersected variably altered and pyrrhotite/pyrite-mineralized basalts and chert-jasper horizons, with the conductor sources predominantly identified as off-hole by down-hole EM surveys (2001 Rubicon-Billiton Assessment Report, p. 8-9 and Table II, p. 9-10):

- LL2000-09 (143.4m): extensive bleached, pyrrhotite/pyrite-mineralized basalt; strong off-hole EM response at 75m correlating with strongest in-hole alteration; best interval 2.40m at 258 ppm Cu from 70.50m (2001 Rubicon-Billiton Assessment Report, p. 8-9 and Table III, p. 12).

- LL2000-10 (143.7m): chert-jasper section with pyrite/magnetite from 83.40m to 95.80m, with elevated gold values (158 ppb (0.158 g/t Au) and 182 ppb (0.182 g/t Au)) associated with arsenopyrite at/near the upper chert-jasper contact; down-hole EM identified an " off-hole response that is a priority follow-up target" (2001 Rubicon-Billiton Assessment Report, p. 9).

- LL2000-11 (128 m): lost in a fault zone at 127.30m, with the conductor still off the end of the hole (2001 Rubicon-Billiton Assessment Report, p. 9).

Target Area Four – Large IP Chargeability Anomaly

Target Area One hosts an IP chargeability anomaly that lies on the west edge of a large circular magnetic high (2001 Rubicon-Billiton Assessment Report, p. 12-13).

Drill hole LL2001-15 tested a limited area of this anomaly (2001 Rubicon-Billiton Assessment Report, p. 11-12):

- LL2001-15 (133.3m) was drilled after an expansion of the IP target through additional 2001 ground geophysics, intersected weakly mineralized quartz/quartz-feldspar porphyry with distinct chlorite-tremolite-biotite zones; best intersection 3.90 m of 341 ppm Cu (2001 Rubicon-Billiton Assessment Report, p. 12 and Table III).A weakly magnetic granodiorite body has been partially mapped within the northern part of the circular magnetic high (2001 Rubicon-Billiton Assessment Report, p. 13).Additionally, several chargeability anomalies associated with this larger IP grid remain untested.

Target Area Five – Surface Showings at Teddy's Barn

Rubicon's 1999 rock sampling discovered the Teddy's Barn showing: disseminated chalcopyrite in strongly chlorite-altered, quartz-phyric felsic rocks cut by mafic dykes, sampled over a 150 m strike length. Sourced samples include (1999 Rubicon Assessment Report, Tables 2 and 3, p. 7, and Appendix III ICP certificate 365-9233):

- RMR31262: 459 ppm Cu (chloritic quartz porphyry, trace to 1% chalcopyrite);

- RMR31263: 676 ppm Cu (quartz porphyry, strongly magnetic, possible native Cu);

- RMR31264: 535 ppm Cu (silicified quartz porphyry);

- RMR31266: 381 ppm Cu (pyritic quartz feldspar porphyry, 1-2% pyrite, 1% chalcopyrite); and

- Adjacent (~150 m to the east) grab samples returned 6,334 ppm Cu and 1,273 ppm Zn (RMR31316) and 2,687 ppm Cu (RMR31317) in banded fine-grained mafic/sedimentary rocks.

Future Exploration Plans

Visionary's regional exploration program at Lewis Lake is expected to incorporate:

- A property-wide geological re-interpretation incorporating the 2007 airborne EM/Mag, 2000 ground TEM/Mag/IP and 2001 expanded IP surveys (totalling more than 1,150 line-kilometres of geophysical coverage) together with all historic drill information where data is available;

- Detailed prospecting, soil geochemistry and ground geophysics over IP chargeability anomalies and untested airborne conductor areas;

- Modern Borehole Pulse Electromagnetic ("BPEM") surveys on historic Billiton/Rubicon drill holes (LL2000-03, LL2000-09, LL2000-10), if accessible, to vector towards undrilled off-hole conductors; and

- Drill testing of the untested Northern Bog conductor and the priority off-hole EM anomalies on the JEN and Fall Pond West grids.

Further details will be released in a separate news release in the near future.

QA / QC Protocols (Historic Data)

Historic Billiton/Rubicon drill core was sampled by saw-cut, with one-half submitted for assay and one-half retained for reference. Samples were prepared and analyzed by Eastern Analytical Ltd., Springdale, Newfoundland (Au by fire assay with AAS finish; multi-element ICP); with whole-rock analyses and check assays performed by ALS Chemex Laboratories (now ALS Global Labs), North Vancouver, British Columbia (2001 Rubicon-Billiton Assessment Report, Appendix I, p. 15 and Appendix IV analytical certificates).

All historic data discussed in this news release is sourced directly from publicly filed assessment reports lodged with the Geological Survey of Newfoundland and Labrador (Mineral Lands Division), including specifically:

- 1999 Rubicon Assessment Report – Assessment Report on the Lewis Lake Project, Licenses 5435M (2nd year), 6915M (1st year), Newfoundland (NTS 02E/3, 02E/4, 02E/5 & 02E/6): Prospecting and Rock Sampling, prepared by R. Bob Singh, Project Geologist, Rubicon Minerals Corporation, dated 12 June 2000;

- 2001 Rubicon-Billiton Assessment Report – Assessment Report on the Lewis Lake Project, Licenses 5435M, 6915M, 7206M, Newfoundland NTS 02E/3, 02E/4, 02E/5, 02E/6: Report on Diamond Drilling and Downhole Geophysical Surveys, prepared by Garfield MacVeigh, Project Geologist, Rubicon Minerals Corporation (operator for Billiton Exploration Canada Ltd.), dated 17 April 2001; and

- 2001 Rubicon-Billiton Assessment Report – Fifth Year Assessment Report on Linecutting, Geochemistry, Geology, Geophysics & Diamond Drilling for Mineral Licences 4782, 4783 & 7774M, New Bay Pond Area, Central Newfoundland, NTS Sheets 2E/04 & 2E/05, prepared by Dave Barbour, B.Sc., P.Geo., & Rodney A. Churchill, M.Sc., P.Geo., for Altius Resources Inc. and Inmet Mining, February 2001 (regional context only).

Pt. Leamington Project

The Pt. Leamington Project is located approximately 37 km by road and trails from the City of Grand Falls-Windsor and approximately 20 km from the provincial power grid. Pt. Leamington is a felsic-hosted VMS deposit that dips 70 degrees to the west, has a strike length of over 560 m and a maximum thickness of 85 m. Massive sulphides have been intersected to a depth of 360 m below surface from approximately 21,714 m of drilling in 72 holes. Regional government mapping and lithogeochemical sampling indicates that Pt. Leamington's host volcanic stratigraphy extends beyond the Deposit area.

The Deposit hosts a significant gold, copper, zinc, and silver resource, with a pit-constrained Indicated Mineral Resource of 5.0 Mt grading 2.5 g/t AuEq for 402 koz AuEq (145.7 koz gold, 60.0 Mlb copper, 153.5 Mlb zinc, 2.0 Moz silver, 1.5 Mlb lead), a pit-constrained Inferred Mineral Resource of 13.7 Mt grading 2.24 g/t AuEq for 986.5 koz AuEq (354.8 koz gold, 110.2 Mlb copper, 527.3 Mlb zinc, 6.2 Moz silver, 7.0 Mlb lead), and an out-of-pit Inferred Mineral Resource of 1.7 Mt grading 3.06 g/t AuEq for 168.5 koz AuEq (65.4 koz gold, 13.3 Mlb copper, 102.9 Mlb zinc, 1.4 Moz Ag, 2.6 Mlb lead) (see news release dated October 25, 2021).

Qualified Person

The technical and scientific information contained in this news release has been reviewed and approved by Aaryn Hutchins, P. Geo, a qualified person under National Instrument 43-101 Standards of Disclosure for Mineral Projects. Ms. Hutchins is a consultant for the Company and is independent of the Company. Historical information referenced in this news release, including all historic drilling, sampling and geophysical results from the Lewis Lake area, was verified from geological assessment reports filed with the Government of Newfoundland and Labrador by previous operators, as specifically cited above. The reader is cautioned that historical results have not been verified by the current operator beyond review of the publicly filed assessment reports and that historical sampling and analytical procedures may not meet current NI 43-101 standards. Visionary considers the historical data to be reliable for the purposes of describing the regional exploration opportunity and prioritizing follow-up work, but emphasizes that historic mineralized intersections on the regional ground are not currently part of a mineral resource estimate and that there is no guarantee that follow-up exploration will define a mineral resource on the regional targets discussed herein.

About Visionary Copper and Gold Mines Inc.

Visionary Copper and Gold Mines Inc. (TSXV: VCG) (OTCQB: VCGMF) is advancing its portfolio of base and precious metals rich deposits located in established Canadian mining jurisdictions. The focus of the portfolio is highlighted by the 100% owned Pt. Leamington Deposit in Newfoundland, located in one of the richest VMS and Gold Districts in Canada. The Company prepared a pit-constrained Indicated Mineral Resource of 5.0 Mt grading 2.5 g/t AuEq for 402 koz AuEq (145.7 koz gold, 60.0 Mlb copper, 153.5 Mlb zinc, 2.0 Moz silver, 1.5 Mlb lead), a pit-constrained Inferred Mineral Resource of 13.7 Mt grading 2.24 g/t AuEq for 986.5 koz AuEq (354.8 koz gold, 110.2 Mlb copper, 527.3 Mlb zinc, 6.2 Moz silver, 7.0 Mlb lead) and an out-of-pit Inferred Mineral Resource of 1.7 Mt grading 3.06 g/t AuEq for 168.5 koz AuEq (65.4 koz gold, 13.3 Mlb copper, 102.9 Mlb zinc, 1.4 Moz Ag, 2.6 Mlb lead) (see news release dated October 25, 2021). Additionally the Company is permitting the Rainbow deposit at its rich VMS Pine Bay Project located near existing infrastructure in the Flin Flon Mining District. The Company prepared an indicated mineral resource on the Rainbow deposit of 3.44 Mt grading 3.59% CuEq for 272.4 Mlb CuEq (238.3 Mlb Cu, 56.9 Mlb Zn, 37.6 koz Au, 692.8 koz Ag, 2.3 Mlb Pb), an inferred mineral resource on the Rainbow deposit of 1.28 Mt grading 2.95% CuEq containing 83.4 Mlb CuEq (72.1 Mlb Cu, 19.5 Mlb Zn, 11.1 koz Au, 222.2 Koz Ag, 0.8 Mlb Pb) and an inferred mineral resource at the Pine Bay deposit of 1.0 Mt grading 2.62% Cu containing 58.1 Mlb Cu (see news release dated July 10, 2023). Additionally, the portfolio includes the Nash Creek Project located in the VMS rich Bathurst Mining District of New Brunswick. A 2018 PEA generates a strong economic return with a pre-tax IRR of 34.1% (25.2% post-tax) and NPV8% of $230 million ($128 million post-tax) at $1.25 Zinc (see news release dated May 14, 2018).

For additional information, please contact:

Visionary Copper and Gold Mines Inc.

Max Porterfield, President and Chief Executive Officer

Phone: (604) 605-0885

E-mail: info@visionarycoppergold.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Some statements in this news release contain forward-looking information. These statements include, but are not limited to, statements with respect to future expenditures, the planning and timing of the exploration program at the Lewis Lake area, the prospectivity of the targets described herein, the ability to confirm the existence of a VMS deposit at Lewis Lake and the potential for the Lewis Lake area to host an economic mineral deposit. These statements address future events and conditions and, as such, involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the statements. Such factors include, among others, the ability to complete the proposed exploration program and the timing and amount of expenditures, receipt of all necessary permits and approvals, availability of qualified personnel and equipment, results of exploration activities, accuracy of historical data, and general market and economic conditions. The reader is cautioned that historic exploration results, geophysical interpretations and conceptual deposit-type targets discussed herein are not indicative of the presence of an economic mineral deposit on the regional land package. Except as required under applicable securities laws, Visionary does not assume the obligation to update any forward-looking statement.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/298362

Freeport-McMoRan Inc. FCX and Southern Copper Corporation SCCO are two heavyweights in the copper mining industry. Both operate on a global scale, extracting and processing copper and other metals. Also, both are navigating fluctuating copper prices and global economic uncertainties. Copper prices started 2026 on a strong note, underpinned by robust demand from China and the United States. Structural tailwinds, including electric vehicles (EVs), renewable energy projects, data center growth and grid modernization, continue to boost copper consumption. Worries about tightening supply amid rising EV and infrastructure demand also supported the red metal. These factors led to prices surging to roughly $6.4 per pound in late January. Prices of the red metal were mostly volatile during February, largely trading near $6 per pound. Copper prices came under pressure in March amid concerns about the impact of surging oil prices on the global economy due to the war in the Middle East, dragging down prices to a three-month low of around $5.3 per pound in late March. Prices rebounded in April on hopes of a de-escalation in the Iran war. Prices shot up to a record high of around $6.6 per pound last week amid robust demand in China and supply worries linked to the Middle East conflict. Prices have pulled back from that level amid war-related uncertainties and are currently hovering near $6.3 per pound. Let’s dive deep and closely compare the fundamentals of these two copper mining companies to determine which one is a better investment now.

The Case for Freeport

Freeport continues to leverage its portfolio of high-quality copper assets, emphasizing disciplined execution and organic growth initiatives to strengthen its production profile. It has completed the evaluation of a large-scale expansion at El Abra in Chile to define a large sulfide resource that could potentially support a major mill project similar to the large-scale concentrator at Cerro Verde, with an estimated resource of approximately 20 billion recoverable pounds of copper. In Arizona, FCX is progressing with pre-feasibility studies at its Safford/Lone Star operations, with completion targeted for 2026, to assess a sizable sulfide expansion opportunity. It has expansion opportunities at Bagdad in Arizona that can more than double the concentrator capacity of the operation. Technical and economic studies have revealed the potential to build concentrating facilities to boost copper production by 200-250 million pounds annually. PT Freeport Indonesia (PT-FI) is developing the Kucing Liar ore body within the Grasberg district with a targeted ramp-up to commence in 2030. FCX completed studies in 2025 that showed an opportunity to increase Kucing Liar’s design capacity to 130,000 metric tons of ore per day and reserves by roughly 20% at low costs. FCX has a strong liquidity profile and generates substantial cash flows, providing ample flexibility to fund expansion projects, reduce debt and enhance shareholder returns. It generated solid operating cash flows of $5.6 billion in 2025. Cash flows provided by operations surged 36% year over year to around $1.5 billion in the first quarter of 2026. Freeport ended the first quarter with strong liquidity, including $3.7 billion in cash and cash equivalents, $3 billion in availability under the FCX revolving credit facility, and $1.5 billion in availability under the PT-FI credit facility.At the end of the first quarter, Freeport had a net debt of $2.4 billion, excluding PTFI’s new downstream processing facilities. Its net debt is below its targeted range of $3-$4 billion. Freeport has a policy of distributing 50% of the available cash to its shareholders and the balance to either reduce debt or invest in growth projects. FCX has no significant debt maturities until 2027. FCX offers a dividend yield of roughly 0.5% at the current stock price. Its payout ratio is 14% (a ratio below 60% is a good indicator that the dividend will be sustainable). Backed by strong financial health, the company's dividend is perceived to be safe and reliable.Despite these positives, Freeport faces headwinds from higher costs. Its outlook for the second quarter of 2026 suggests higher costs on a sequential basis. It expects unit net cash costs to rise to $2.24 per pound, while projecting a full-year average of roughly $1.95 (compared with $1.65 in 2025). The projected second-quarter unit cost reflects a roughly 98% year over year and 17% increase from the prior quarter. The uptick in costs reflects higher costs of energy and other consumables due to the Middle East conflict and persistent pressure on volumes. Higher costs are expected to weigh on the company's margins. Freeport’s copper sales volumes tumbled approximately 25% year over year in the first quarter to 657 million pounds, and fell from 709 million pounds in the prior quarter. The downside primarily resulted from lower operating rates due to the temporary suspension of operations since the mud rush incident at the Grasberg Block Cave mine in Indonesia in September 2025. While the company’s outlook for copper sales volumes for the second quarter of 2026 of 690 million pounds indicates a sequential improvement, it still suggests a 32% year-over-year decline. For full-year 2026, consolidated sales volume projections were revised lower to around 3.1 billion pounds of copper from the prior view of 3.4 billion pounds due to an expected delay in achieving full ramp-up of the Grasberg Block Cave mine. Lower sales volumes are expected to weigh on its top line.

The Case for Southern Copper