MELBOURNE, Australia, August 19, 2021–(BUSINESS WIRE)–Rio Tinto is partnering with the Western Australian Government to launch a COVID-19 vaccination blitz targeting communities in the Pilbara and the fly-in fly-out workforce.

Following positive discussions between Rio Tinto and the WA Department of Health, vaccination hubs will be established in the Pilbara and at a trial clinic at Perth Airport to make vaccinations more accessible.

Starting with Tom Price, planning is underway for hubs at several locations in the Pilbara, with vaccines available to members of the local community, Indigenous communities, Rio Tinto employees, contractors and their families.

Rio Tinto is working with the Department of Health and the Shire of Ashburton and is close to finalising a location for the proposed Tom Price hub. The facility could potentially offer vaccines to the entire adult population of Tom Price and surrounding communities.

Rio Tinto’s COVID-19 screening facilities at Perth Airport (T2 and T3) will also be modified to include ‘pop-up’ vaccination hubs to target workers returning to Perth. The hubs will initially be available to Rio Tinto’s FIFO workforce, who regularly travel to and from the Pilbara, with the option to expand the vaccination service to the wider FIFO community.

The initial vaccination blitz is expected to commence in September, subject to availability of vaccines. Rio Tinto will work with the WA Government to finalise details in the coming weeks.

Rio Tinto Iron Ore chief executive Simon Trott said the company stood ready to support the WA Government’s vaccination rollout in any way it can.

"We are pleased to work in partnership with the WA Government on this industry-first vaccination blitz, which we expect will help boost vaccination rates in the Pilbara.

"This is an important development in our state’s effort to combat COVID-19. We know vaccinations are our best way out of this pandemic and we are very happy to convert our existing screening facilities, which have helped keep COVID-19 out of our operations and vulnerable communities for almost 18 months, to include vaccination hubs.

"Given Rio Tinto’s large operational footprint in the Pilbara, we are well positioned to support the WA Government’s vaccination rollout in the region, ensuring the vaccine is more accessible to remote and vulnerable communities.

"Plans are being developed to establish additional hubs in places like Paraburdoo, Pannawonica and Dampier, following the Tom Price vaccine blitz.

"While the initial vaccine blitz at Perth Airport will target Rio Tinto’s FIFO workforce, we will work with the WA Government to make our facilities available to others in the industry and community.

"Throughout the COVID-19 pandemic, the resources sector has worked hard to continue to operate in a COVID-safe way. The next step in is to play our part in making the vaccine accessible to as many Western Australians as possible."

View source version on businesswire.com: https://www.businesswire.com/news/home/20210818005863/en/

Contacts

Please direct all enquiries to

Media.enquiries@riotinto.com

Media Relations, Australia

Jonathan Rose

M +61 447 028 913

Matt Chambers

M +61 433 525 739

Jesse Riseborough

M +61 436 653 412

Jamie Macdonald

M +61 467 725 517

Rio Tinto plc

6 St James’s Square

London SW1Y 4AD

United Kingdom

T +44 20 7781 2000

Registered in England

No. 719885

Rio Tinto Limited

Level 7, 360 Collins Street

Melbourne 3000

Australia

T +61 3 9283 3333

Registered in Australia

ABN 96 004 458 404

Category: General

TSX-V: GBR

VANCOUVER, BC, Aug. 19, 2021 /CNW/ – Great Bear Resources Ltd. (the "Company" or "Great Bear") (TSXV: GBR) (OTCQX: GTBAF) today provides an update regarding its ongoing fully funded $45 million 2021 exploration program at its 100% owned flagship Dixie Project in the Red Lake district of Ontario.

Significant improvements in the forest fire situation in Northwestern Ontario have allowed the Ministry of Northern Development, Mines, Natural Resources and Forestry (MNRF) of Ontario to remove a work suspension order which was originally issued on July 21st, which had restricted industrial activities over a large area of the Province. With the work suspension rescinded on August 18th, Great Bear will now commence Phase 2 drilling, consisting of:

-

Ongoing expansion drilling of the LP Fault below 450 metres depth, and along strike beyond the 4 kilometre long Phase 1 grid drilling area,

-

Any additional infill drilling of the Phase 1 LP Fault grid drilling area that may be required,

-

Expansion and infill drilling of the Hinge, Limb and Arrow zones, and

-

Testing of new regional targets at Dixie.

Drills are expected to be active on the Dixie property as of Monday, August 23rd.

About the Dixie Project

The Dixie Project is 100% owned, comprised of 9,140 hectares of contiguous claims that extend over 22 kilometres, and is located approximately 25 kilometres southeast of the town of Red Lake, Ontario. The project is accessible year-round via a 15 minute drive on a paved highway which runs the length of the northern claim boundary and a network of well-maintained logging roads.

The Dixie Project hosts two principal styles of gold mineralization:

-

High-grade gold in quartz veins and silica-sulphide replacement zones (Dixie Limb, Hinge and Arrow zones). Hosted by mafic volcanic rocks and localized near regional-scale D2 fold axes. These mineralization styles are also typical of the significant mined deposits of the Red Lake district.

-

High-grade disseminated gold with broad moderate to lower grade envelopes (LP Fault). The LP Fault is a significant gold-hosting structure which has been seismically imaged to extend to 14 kilometres depth (Zeng and Calvert, 2006), and has been interpreted by Great Bear to have up to 18 kilometres of strike length on the Dixie property. High-grade gold mineralization is controlled by structural and geological contacts, and moderate to lower-grade disseminated gold surrounds and flanks the high-grade intervals. The dominant gold-hosting stratigraphy consists of felsic sediments and volcanic units.

About Great Bear

Great Bear Resources Ltd. is a well-financed gold exploration company managed by a team with a track record of success in mineral exploration. Great Bear is focused in the prolific Red Lake gold district in northwest Ontario, where the company controls over 200 km2 of highly prospective tenure across 4 projects, all 100% owned: The flagship Dixie Project, the Pakwash Property, the Sobel Property, and the Red Lake North Property, all of which are accessible year-round through existing roads.

Qualified Person and NI 43-101 Disclosure

Mr. R. Bob Singh, P.Geo, VP Exploration, and Ms. Andrea Diakow P.Geo, VP Projects for Great Bear are the Qualified Persons as defined by National Instrument 43-101 responsible for the accuracy of technical information contained in this news release.

ON BEHALF OF THE BOARD

"Chris Taylor"

Chris Taylor, President and CEO

Cautionary note regarding forward-looking statements

This release contains certain "forward looking statements" and certain "forward-looking information" as defined under applicable Canadian and U.S. securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "intend", "estimate", "anticipate", "believe", "continue", "plans" or similar terminology. The forward-looking information contained herein is provided for the purpose of assisting readers in understanding management's current expectations and plans relating to the future. Readers are cautioned that such information may not be appropriate for other purposes.

Forward-looking information are based on management of the parties' reasonable assumptions, estimates, expectations, analyses and opinions, which are based on such management's experience and perception of trends, current conditions and expected developments, and other factors that management believes are relevant and reasonable in the circumstances, but which may prove to be incorrect.

Such factors, among other things, include: impacts arising from the global disruption caused by the Covid-19 coronavirus outbreak, business integration risks; fluctuations in general macroeconomic conditions; fluctuations in securities markets; fluctuations in spot and forward prices of gold or certain other commodities; change in national and local government, legislation, taxation, controls, regulations and political or economic developments; risks and hazards associated with the business of mineral exploration, development and mining (including environmental hazards, industrial accidents, unusual or unexpected formations pressures, cave-ins and flooding); discrepancies between actual and estimated metallurgical recoveries; inability to obtain adequate insurance to cover risks and hazards; the presence of laws and regulations that may impose restrictions on mining; employee relations; relationships with and claims by local communities and indigenous populations; availability of increasing costs associated with mining inputs and labour; the speculative nature of mineral exploration and development (including the risks of obtaining necessary licenses, permits and approvals from government authorities); and title to properties.

Great Bear undertakes no obligation to update forward-looking information except as required by applicable law. Such forward-looking information represents management's best judgment based on information currently available. No forward-looking statement can be guaranteed and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

View original content to download multimedia:https://www.prnewswire.com/news-releases/great-bear-begins-phase-2-drilling-at-dixie-project-301358592.html

SOURCE Great Bear Resources Ltd.

View original content to download multimedia: http://www.newswire.ca/en/releases/archive/August2021/19/c9216.html

VANCOUVER, August 19, 2021–(BUSINESS WIRE)–Capstone Mining Corp. ("Capstone" or the "Company") (TSX:CS) announces that Mr. Richard N. Zimmer has retired from the Board of Directors of the Company effective August 17, 2021.

Prior to Capstone, Mr. Zimmer was Chief Executive Officer of Far West Mining Ltd. ("Far West"), the previous owner and operator of the Santo Domingo project. He joined the Company’s Board of Directors in 2011 following Capstone’s acquisition of Far West. At Capstone, Mr. Zimmer served as the Chair of the Technical, Health, Environmental, Safety and Sustainability Committee from June 2011 until April 2019, and most recently served as Chair of the Corporate Governance & Nominating Committee.

Darren Pylot, President & CEO commented, "Rick was instrumental in the integration and advancement of the Santo Domingo project and contributed his invaluable expertise to our Board through the years. We thank him for his significant contributions and dedication to Capstone over his ten years of service on our Board."

ABOUT CAPSTONE MINING CORP.

Capstone Mining Corp. is a Canadian base metals mining company, focused on copper. We are committed to the responsible development of our assets and the environments in which we operate. Our two producing mines are the Pinto Valley copper mine located in Arizona, US and the Cozamin copper-silver mine in Zacatecas State, Mexico. In addition, Capstone owns 100% of Santo Domingo, a large scale, fully permitted, copper-iron-gold project in Region III, Chile, as well as a portfolio of exploration properties. Capstone's strategy is to focus on the optimization of operations and assets in politically stable, mining-friendly regions, centred in the Americas. Our headquarters are in Vancouver, Canada and we are listed on the Toronto Stock Exchange (TSX). Further information is available at www.capstonemining.com.

View source version on businesswire.com: https://www.businesswire.com/news/home/20210818005834/en/

Contacts

Jerrold Annett, SVP, Strategy and Capital Markets

647-273-7351

jannett@capstonemining.com

Kettina Cordero, Director, Investor Relations & Communications

604-262-9794

kcordero@capstonemining.com

Teck Resources Ltd TECK recently announced that the wildfire evacuation order issued by the District of Logan Lake has been lifted for the company’s Highland Valley Copper Operations (HVC). HVC has resumed operations and is on track to ramp up to full production. On Aug 14, Teck temporarily suspended its British Columbia-based HVC operations in response to the forest fire incident.

Earlier this month, Teck reported smoke from wildfires in southwestern British Columbia that impacted its Trail Operations metallurgical facility. Trail’s oxygen plant was closed down due to poor air quality. While Zinc and Lead refining operations continue to operate normally, lead smelting operations were temporarily idled.

On Aug 13, Trail’s oxygen plants restarted following an improvement in air quality. Operations at the Trail metallurgical facility are ramping back up to full capacity.

The company is focused on safeguarding the health and safety of employees and contractors, and continues to monitor wildfire and regional air quality conditions.

Last month, the company reported second-quarter 2021 results, wherein earnings beat the Zacks Consensus Estimate but sales missed the same. Both the bottom-and top-line figures increased year over year.

Teck Resources expects steelmaking coal production between 25 million tons and 26 million tons in 2021. Copper production is anticipated within 275,000-290,000 tons. Zinc production is projected between 605,000 tons and 630,000 tons. The company estimates Bitumen production for 2021 between 6.6 million barrels and 8.1 million barrels.

For the third quarter, at Red Dog, the company projects sales of zinc in concentrate to be 180,000-200,000 tons. Steelmaking coal sales are projected to be 5.7-6.1 million for the quarter.

Price Performance

The company’s shares have soared 83.9% over the past year, outperforming the industry’s rally of 25.9%.

Image Source: Zacks Investment Research

Zacks Rank & Stocks to Consider

Teck Resources currently carries a Zacks Rank #3 (Hold).

Better-ranked stocks in the basic materials space include Avient Corporation AVNT, Veritiv Corporation VRTV and Commercial Metals Company CMC. While Avient and Veritiv flaunt a Zacks Rank #1 (Strong Buy), Commercial Metals carries a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Avient has a projected earnings growth rate of 75% for 2021. The company’s shares have soared 92% in the past year.

Veritiv has an estimated earnings growth rate of 215% for the current year. Over the past year, the company’s shares have soared 340%.

Commercial Metals has an expected earnings growth rate of 32.8% for the current fiscal year. The company’s shares have gained 54% in a year’s time.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Commercial Metals Company (CMC) : Free Stock Analysis Report

Veritiv Corporation (VRTV) : Free Stock Analysis Report

Teck Resources Ltd (TECK) : Free Stock Analysis Report

Avient Corporation (AVNT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

PERTH, Australia, Aug. 19, 2021 (GLOBE NEWSWIRE) —

Wyloo Metals Pty Ltd (“Wyloo Metals”) provides the following update regarding its intentions in relation to the offer by BHP Western Mining Resources International Pty Ltd ("BHP") to acquire all of the outstanding common shares of Noront Resources Ltd (TSXV:NOT) ("Noront").

Response to BHP’s offer

Noront’s Ring of Fire land package hosts some of the most prospective mineral deposits in the world. These deposits have the potential to become Canada’s next great mineral district, supporting the production of future-facing commodities for multiple generations. Wyloo Metals continues to firmly believe in the immense potential of the Ring of Fire and therefore does not intend to support or tender its Noront shares to BHP's offer.

Wyloo Metals was disappointed that the Noront Board did not seek to meaningfully engage or negotiate with it prior to accepting the BHP offer. Given Wyloo Metals’ cornerstone interest of approximately 37.5% (partially diluted) of Noront, the minimum mandatory tender condition for BHP's bid is unlikely to be satisfied without Wyloo Metals' support and a second step acquisition transaction is impossible.

Superior offer by Wyloo Metals

Wyloo Metals would consider proposing a superior offer to acquire the outstanding common shares of Noront it does not already own, should it be provided with access to due diligence. Despite numerous attempts to date, the Noront Board has denied Wyloo Metals from obtaining access to due diligence on reasonable terms for a shareholder with a cornerstone position.

Unfortunately, the total value of any superior offer contemplated by Wyloo Metals must accommodate the Cdn$13 million break fee payable to BHP, which was agreed to by the Noront Board to the direct detriment of Noront’s shareholders.

ABOUT WYLOO METALS

Wyloo Metals is the metals and mining subsidiary of Tattarang, one of Australia’s largest private investment groups. Led by a multidisciplinary team of geologists, engineers and financial professionals, Wyloo Metals manages a diverse portfolio of exploration and development projects and cornerstone interests in a number of public and private companies. Wyloo Metals seeks to work closely with all stakeholders to accelerate projects through the development cycle while meeting the highest international environmental, social and governance standards. See more at: www.wyloometals.com.

Wyloo Canada Holdings Pty Ltd (“Wyloo Canada”), a wholly owned subsidiary of Wyloo Metals, currently holds an aggregate of 111,815,458 common shares of Noront, representing approximately 24.4% of the outstanding common shares of Noront. As previously announced on July 23, 2021, Wyloo Metals intends to convert its US$15 million convertible loan (“Convertible Loan”) into common shares of Noront at or before the September 30, 2021 maturity date. At an exchange rate of 0.792 US Dollars per Canadian Dollar1, Wyloo Canada would acquire an additional 94,702,494 common shares of Noront upon conversion of its Convertible Loan, following which it would hold 206,517,952 common shares of Noront, representing approximately 37.3% of the outstanding common shares of Noront on a partially diluted basis.

Wyloo Canada also holds warrants (“Noront Warrants”) to acquire 1,774,664 common shares of Noront at an exercise price of Cdn$0.35 per share. If the Noront Warrants are also fully exercised, Wyloo Canada would hold 208,292,616 common shares of Noront, representing approximately 37.5% of the outstanding common shares of Noront on a partially diluted basis.

DISCLAIMER

Some of the statements in this press release may be forward looking statements or statements of future expectations based on currently available information. Such statements are naturally subject to risks and uncertainties. Factors such as the development of general economic conditions, future market conditions, unusual catastrophic loss events, changes in the capital markets and other circumstances may cause the actual events or results to be materially different from those anticipated by such statements. Wyloo Metals does not make any representation or warranty, express or implied, as to the accuracy, completeness or updated status of such statements. Therefore, in no case whatsoever will Wyloo Metals and its affiliate companies be liable to anyone for any decision made or action take in connection with the information and/or statements in this press release or for any related damages.

This press release is issued pursuant to National Instrument 62-103 – The Early Warning System and Related Take-Over Bid and Insider Reporting Issues, which requires a report to be filed under Noront’s profile on SEDAR (www.sedar.com) containing additional information with respect to the foregoing matters. A copy of such report may be obtained by contacting Wyloo Metals at info@wyloometals.com. The address of Wyloo Metals is PO Box 3155, Broadway Nedlands, WA 6009 Western Australia.

1 At August 18, 2021.

Vancouver, British Columbia–(Newsfile Corp. – August 19, 2021) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the "Company" or "EMX") announces that pursuant to the Company's Stock Option Plan, incentive stock options (the "Options") to purchase an aggregate of 500,000 common shares, exercisable at a price of $3.66 per share for a period of five years, has been granted to certain directors, and a consultant of the Company.

About EMX. EMX is a precious, base and battery metals royalty company. EMX's investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company's common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol "EMX"; and on the Frankfurt exchange under the symbol "6E9". Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole

President and Chief Executive Officer

Phone: (303) 979-6666

Dave@EMXroyalty.com

Scott Close

Director of Investor Relations

Phone: (303) 973-8585

SClose@EMXroyalty.com

Isabel Belger

Investor Relations (Europe)

Phone: +49 178 4909039

Ibelger@EMXroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/93798

Shares of United States Steel (X) have been strong performers lately, with the stock up 27.7% over the past month. The stock hit a new 52-week high of $30.57 in the previous session. United States Steel has gained 75.6% since the start of the year compared to the 9.6% move for the Zacks Basic Materials sector and the 56.9% return for the Zacks Steel – Producers industry.

What's Driving the Outperformance?

The stock has an impressive record of positive earnings surprises, as it hasn't missed our earnings consensus estimate in any of the last four quarters. In its last earnings report on July 29, 2021, U.S. Steel reported EPS of $3.37 versus consensus estimate of $3.16.

For the current fiscal year, U.S. Steel is expected to post earnings of $11.92 per share on $18.98 billion in revenues. This represents a 355.25% change in EPS on a 94.87% change in revenues. For the next fiscal year, the company is expected to earn $4.66 per share on $16.35 billion in revenues. This represents a year-over-year change of -60.87% and -13.88%, respectively.

Valuation Metrics

U.S. Steel may be at a 52-week high right now, but what might the future hold for the stock? A key aspect of this question is taking a look at valuation metrics in order to determine if the company has run ahead of itself.

On this front, we can look at the Zacks Style Scores, as they provide investors with an additional way to sort through stocks (beyond looking at the Zacks Rank of a security). These styles are represented by grades running from A to F in the categories of Value, Growth, and Momentum, while there is a combined VGM Score as well. Investors should consider the style scores a valuable tool that can help you to pick the most appropriate Zacks Rank stocks based on their individual investment style.

U.S. Steel has a Value Score of B. The stock's Growth and Momentum Scores are B and F, respectively, giving the company a VGM Score of B.

In terms of its value breakdown, the stock currently trades at 2.5X current fiscal year EPS estimates. This isn't enough to put the company in the top echelon of all stocks we cover from a value perspective.

Zacks Rank

We also need to consider the stock's Zacks Rank, as this supersedes any trend on the style score front. Fortunately, U.S. Steel currently has a Zacks Rank of #1 (Strong Buy) thanks to rising earnings estimates.

Since we recommend that investors select stocks carrying Zacks Rank of 1 (Strong Buy) or 2 (Buy) and Style Scores of A or B, it looks as if U.S. Steel meets the list of requirements. Thus, it seems as though U.S. Steel shares could have a bit more room to run in the near term.

How Does U.S. Steel Stack Up to the Competition?

Shares of U.S. Steel have been soaring, and the company still appears to be a decent choice, but what about the rest of the industry? Some of its industry peers are also impressive, including Commercial Metals (CMC), Ternium (TX), and Nucor (NUE), all of which currently have a Zacks Rank of at least #2 and a VGM Score of at least B, making them well-rounded choices.

The Zacks Industry Rank is in the top 5% of all the industries we have in our universe, so it looks like there are some nice tailwinds for U.S. Steel, even beyond its own solid fundamental situation.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

United States Steel Corporation (X) : Free Stock Analysis Report

Nucor Corporation (NUE) : Free Stock Analysis Report

Ternium S.A. (TX) : Free Stock Analysis Report

Commercial Metals Company (CMC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

ST. JOHN’S, Newfoundland and Labrador, August 19, 2021–(BUSINESS WIRE)–Altius Minerals Corporation (ALS:TSX) (ATUSF: OTCQX) ("Altius" or the "Corporation") is pleased to announce that it has renewed its Normal Course Issuer Bid ("NCIB") and may purchase at market price up to 1,642,612 common shares ("Shares"), being approximately 3.96% of the 41,504,497 common shares issued and outstanding as of August 18, 2021, by way of an NCIB through the facilities of the Toronto Stock Exchange ("TSX") or a Canadian alternative trading system. The NCIB is subject to regulatory approval. The NCIB will commence August 22, 2021 and will end no later than August 21, 2022. Any Shares purchased pursuant to the NCIB will be cancelled and returned to treasury.

The TSX rules permit Altius to purchase daily, through TSX facilities or approved alternative trading systems, a maximum of 30,870 Shares under the NCIB. From August 22, 2020 to August 21, 2021 Altius purchased a total of 477,400 Shares through market purchases on the TSX and alternative trading systems at a weighted average price of $15.55 per Share, while its approval allowed for it to purchase a maximum number of 1,622,920 Shares. The reason for the NCIB is that, in the opinion of the board of directors, the value of Altius Shares, based on anticipated cash flows and underlying asset values, is from time to time greater than the market price of the Shares and accordingly the acquisition of Shares under the NCIB represents an appropriate use of funds. Altius has had an active NCIB program every year since 2010.

About Altius

Altius’s strategy is to create per share growth through a diversified portfolio of royalty assets that relate to long life, high margin operations. This strategy further provides shareholders with exposures that are well aligned with sustainability-related global growth trends including the electricity generation transition from fossil fuel to renewables, transportation electrification, reduced emissions from steelmaking and increasing agricultural yield requirements. These macro-trends each hold the potential to cause increased demand for many of Altius’s commodity exposures including copper, renewable based electricity, several key battery metals (lithium, nickel and cobalt), clean iron ore, and potash. In addition, Altius runs a successful Project Generation business that originates mineral projects for sale to developers in exchange for equity positions and royalties. Altius has 41,504,497 common shares issued and outstanding that are listed on Canada’s Toronto Stock Exchange. It is a member of both the S&P/TSX Small Cap and S&P/TSX Global Mining Indices.

Forward-looking information

This news release contains forward‐looking information. The statements are based on reasonable assumptions and expectations of management and Altius provides no assurance that actual events will meet management's expectations. In certain cases, forward‐looking information may be identified by such terms as "anticipates", "believes", "could", "estimates", "expects", "may", "shall", "will", or "would". Although Altius believes the expectations expressed in such forward‐looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those projected. Readers should not place undue reliance on forward-looking information. Altius does not undertake to update any forward-looking information contained herein except in accordance with securities regulation.

View source version on businesswire.com: https://www.businesswire.com/news/home/20210819005068/en/

Contacts

Flora Wood

Email: Fwood@altiusminerals.com

Tel: 1.877.576.2209

Direct: +1(416)346.9020

Ben Lewis

Email: Blewis@altiusminerals.com

Tel: 1.877.576.2209

(Bloomberg) — Iron ore extended its rout as BHP Group warned it sees an increasing likelihood of “stern cuts” to China’s steel output this year.

The prospect of much lower steel production in the second-half is “testing the bullish resolve of the futures markets,” BHP wrote in a commodities outlook report on its website. Iron ore in Singapore has plunged by a third since spiking to an all-time high in May.

China’s steel industry is under pressure after pledging to reduce output this year, a goal that requires huge second-half curbs to offset booming output earlier in 2021. Production in July was more than 8% lower year-on-year, data on Monday showed.

Futures in Singapore fell 6.5% to $147.95 a ton by 6:49 p.m. local time, and were heading for a fifth weekly loss. In China, futures dropped 2.5% to close at the lowest level since November.

While investor attention is very focused on China’s output curbs in the second half, the nation’s demand trends will also be critical. Beijing is pushing a range of measures to control the property sector, which accounts for big chunk of steel usage and has traditionally helped drive surges in iron ore prices.

“Policymakers are clearly concerned about over-investment and concentrated credit risk in the property sector,” Commonwealth Bank of Australia wrote in an emailed note. And even if China swings to more pro-growth policies to battle recent weakness, “there’s a good chance that the property sector is left out”.

Shanghai steel futures also dropped, with hot-rolled coil down 3.3% and rebar down 3.8%.

More stories like this are available on bloomberg.com

Subscribe now to stay ahead with the most trusted business news source.

©2021 Bloomberg L.P.

BHP Group BHP reported underlying attributable profit of $17.1 billion in the fiscal 2021 (ended Jun 30, 2021), which was up 88% year over year, reflecting higher commodity prices and strong operational performance. Earnings per American Depositary Share (ADS) was $6.75 in fiscal 2021, up from $3.58 in fiscal 2020 but missed the Zacks Consensus Estimate of $6.93. Underlying earnings per share was $3.38, compared with $1.79 in fiscal 2020. The company’s each American Depositary Shares represents two fully-paid ordinary shares. It also made a flurry of announcements — to exit its oil and gas operations as it strikes a merger deal with Woodside Petroleum Ltd, approval of $5.7 billion in capital expenditure in Jansen Potash Mine in Canada and its decision to unify its dual-listed structure.

The company’s attributable profit amounted to $11.3 billion in fiscal 2021, including an exceptional loss of $5.8 billion. The exceptional loss was related to the impairments of potash and energy coal assets as well as the current year impact of the Samarco dam failure. Attributable profit in fiscal 2020 was $7.9 billion, which included an exceptional loss of $1.1 billion.

Revenues & Margin Performance

Revenues for fiscal 2021 totaled $60.8 billion, which beat the Zacks Consensus Estimate of $60.2 billion. It marked an improvement of 42%from revenues of $42.9 billion in the prior fiscal. The Iron ore segment’s revenues surged 66% year over year to $34 billion on higher prices and record production achieved at WAIO. Revenues in the Copper segment rose 47% to $15.7 billion, reflecting higher prices. Revenues in the Petroleum fell 3% year over year to $3.9 billion. The Coal segment’s revenues slumped 17% to $5 billion.

Adjusted profit from operations in fiscal 2021 soared 91% year over year to $30.3 billion owing to higher commodity prices and strong underlying operational performance, lower deferred stripping depletion at Escondida, lessened fuel and energy costs, and savings from the company’s cost reduction initiatives. Unfavorable impacts of exchange rate movements, copper grade decline, natural field decline in Petroleum, inflation, adverse weather and planned maintenance somewhat mitigated these impacts. Underlying earnings before interest, taxes, depreciation, and amortization (EBITDA) were $37.4 billion for fiscal 2021, up 69% year over year.

Balance Sheet & Cash Flow

Net operating cash flow for fiscal 2021 was $27.2 billion compared with $15.7 billion in fiscal 2020. This marked 15th consecutive year of generating net operating cash flow above the $15 billion mark. The company reported record free cash flow of $19.4 billion, courtesy of higher iron ore and copper prices, and a strong operational performance.

Cash and cash equivalents as of Jun 30, 2021 amounted to $15.2 billion, up from $13.4 billion at the end of fiscal 2020. Capital and exploration expenditure totaled $7.1 billion, down 7% from the prior fiscal. The company provided capital and exploration guidance at $7.1 billion for fiscal 2022. As of the end of fiscal 2021, net debt was $4 billion, substantially lower than $12 billion reported as of fiscal 2020. Backed by strong fiscal 2021 results, BHP Group’s board announced a record final dividend of $2.00 per share.

Other Updates

In fiscal 2021, the company successfully achieved first production at four major development projects — on or ahead of schedule and on budget. It acquired an additional 28% working interest in Shenzi in November 2020. The Shenzi North development, a two-well subsea tie-in to the Shenzi platform, was approved in August 2021. At the end of fiscal 2021, BHP Group had two major projects under development — Mad Dog Phase 2 in petroleum and Jansen mine shafts in potash.

Significant Announcements

BHP Group approved $5.7 billion in capital expenditure for the Jansen Stage 1 potash project. First ore is expected in 2027. Once operational, Jansen S1 is expected to produce approximately 4.35 million ton of potash per year. This will provide the company exposure to a commodity with a strong demand outlook and immense growth potential.

The company has agreed to pursue a merger of its Petroleum business with Woodside Petroleum Ltd, which will create a global top 10 independent energy company by production. The combined business will have a high margin oil portfolio and long life LNG assets. Woodside would issue new shares to be distributed to BHP Group’s shareholders. Woodside shareholders will own 52% of the merged group, while BHP Group’s shareholders owning the remaining 48%. Woodside and BHP Group have estimated annual synergies in excess of $400 million per year. The Petroleum segment generated 6% of BHP Group’s fiscal 2021 revenues.

BHP Group intends to unify its corporate structure under its existing Australian parent company to realize simplification and enhanced strategic flexibility benefits.

Fiscal 2022 Production & Cost Guidance

In fiscal 2022, the company expects to produce between 249 Mt and 259 Mt of iron ore compared with 254 Mt produced in fiscal 2021 as WAIO continues to focus on incremental volume growth through productivity improvements. The petroleum production guidance is 99-106 MMboe. BHP Group anticipates copper production between 1,590 kt and 1,760 kt. Production guidance of Metallurgical coal for fiscal 2022 is at 39-44 Mt, while the same for energy coal is at 13-15 Mt. Nickel production is expected between 85 kt and 95 kt.

Conventional Petroleum unit cost is projected at $11-$12 per barrels of oil equivalent (boe) for fiscal 2022. Escondida unit cost is anticipated at $1.20-$1.40 per pound. Queensland Coal unit cost for the fiscal is expected at $80-$90 per ton. WAIO unit cost guidance is projected to be $17.50-$18.50 per ton.

The company expects demand for energy, metals and fertilizers to remain strong in the years to come, fueled by global economic growth, population growth and rising living standards. The near-term outlook, however, remains cloudy due to the uncertainties associated with the COVID-19 pandemic.

Price Performance

Image Source: Zacks Investment Research

BHP Group’s shares have gained 22.7% over the past year compared with the industry’s growth of 21%.

Zacks Rank & Other Key Picks

BHP Group currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Some other top-ranked stocks in the basic materials space include Avient Corporation AVNT, Veritiv Corporation VRTV and Commercial Metals Company CMC. While Avient and Veritiv flaunt a Zacks Rank #1, Commercial Metals carries a Zacks Rank #2.

Avient has a projected earnings growth rate of 75% for 2021. The company’s shares have soared 92% in the past year.

Veritiv has an estimated earnings growth rate of 215% for the current year. Over the past year, the company’s shares have soared 340%.

Commercial Metals has an expected earnings growth rate of 32.8% for the current fiscal year. The company’s shares have gained 54% in a year’s time.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BHP Group Limited Sponsored ADR (BHP) : Free Stock Analysis Report

Commercial Metals Company (CMC) : Free Stock Analysis Report

Veritiv Corporation (VRTV) : Free Stock Analysis Report

Avient Corporation (AVNT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

By Sonali Paul

(Reuters) – Australia's Woodside Petroleum Ltd shares fell more than 4% on Wednesday in the market's first verdict on a merger with BHP Group's petroleum business that will turn it into a global top 10 oil and gas producer.

The deal, announced after the market closed on Tuesday, involves Woodside doubling its share base to acquire BHP's oil and gas arm in a nil-premium merger to create a roughly A$40 billion ($29 billion) company.

Woodside shareholders will own 52% of the merged group, with BHP shareholders owning 48%.

The merger, expected to be completed in mid-2022, will double Woodside's output and market capitalisation.

Some analysts praised the deal, saying the share price drop reflected worries about a stock overhang as many BHP shareholders who want out of fossil fuels may dump the shares.

"The price of all this funding headroom is a huge share overhang, which … could leave the better part of A$10 billion of Woodside's stock to change hands," CLSA analysts said in a note which maintained an underperform rating on the stock.

"However, we emphasise Woodside 2.0 will be more attractive fundamentally, and our recommendation could become significantly more positive once the market digests the new deal and the new shares," CLSA said.

Others, however, were more negative.

Fund manager Van Eck Australia questioned the value of the merger and said it may have difficulty winning approval from Woodside shareholders.

"While the merger offers Woodside increased diversification, it is also forcing the company to take on aging oil fields and remediation issues," said Jamie Hannah, deputy head of investments at fund manager Van Eck Australia.

The shares partly recovered in morning trade to be down 2.1% in a flat broader market. The stock had already fallen 5% since speculation started swirling in July about a potential merger with BHP petroleum involving a huge issue of shares.

Woodside earlier reported a 17% rise in first-half underlying profit on a rebound from last year's pandemic-hit oil prices, but missed broker forecasts and trimmed its annual production outlook.

Woodside's underlying net profit rose to $354 million for the six months to June 30 from $303 million a year earlier. That was well short of broker forecasts around $413 million on Visible Alpha.

The company trimmed the top end of its annual production outlook to 93 million barrels of oil equivalent (mmboe) from 95 mmboe, implying a drop of at least 7% from last year's record output.

Most of the decline is due to falling output at its ageing, mainstay North West Shelf LNG project. Woodside, the operator, will be doubling its stake to one-third of North West Shelf with the BHP merger.

($1 = 1.3782 Australian dollars)

(Reporting by Sonali Paul; Additional reporting by Soumyajit Saha and Shashwat Awasthi in Bengaluru; Editing by Aditya Soni, Stephen Coates and Richard Pullin)

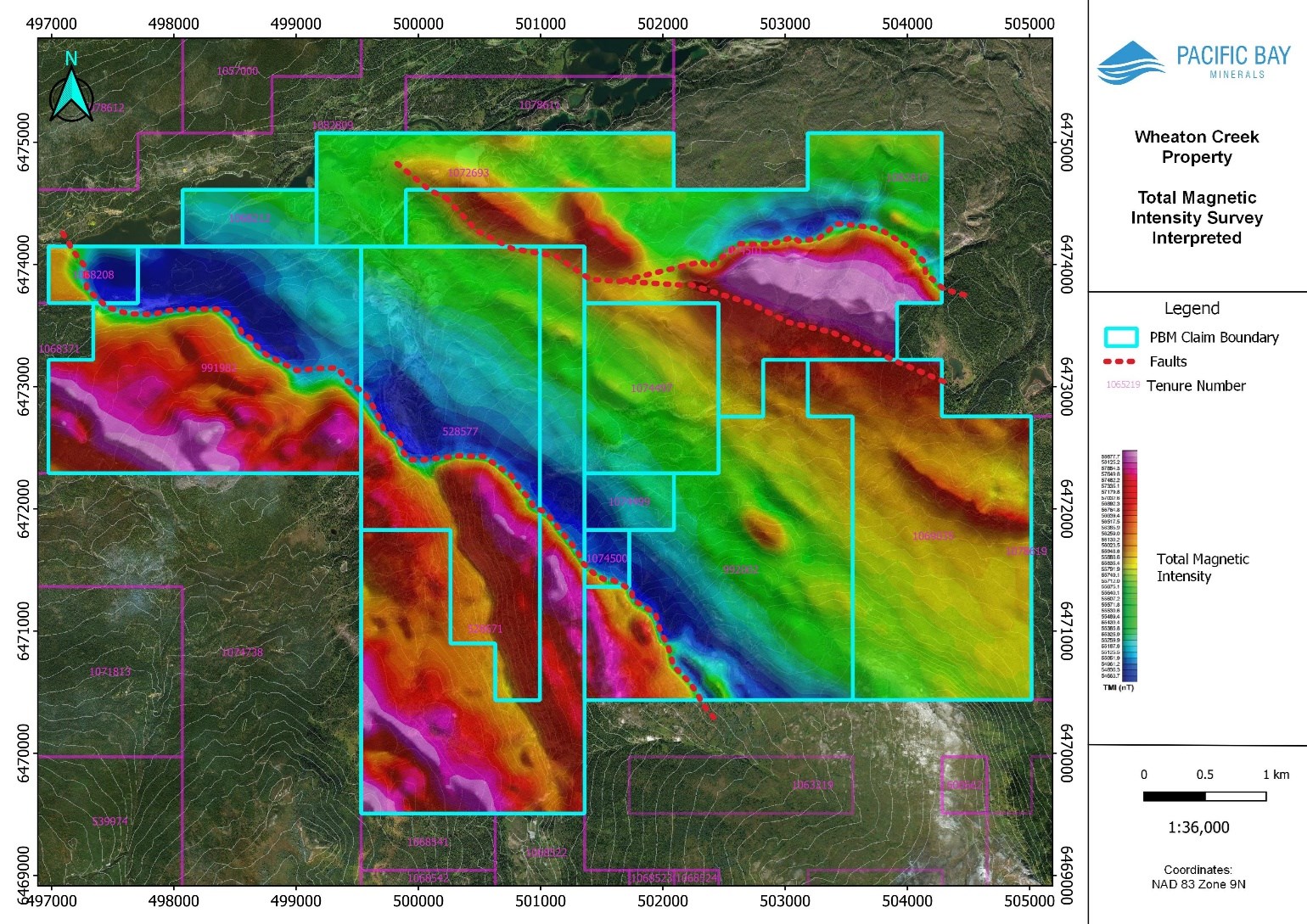

Vancouver, British Columbia–(Newsfile Corp. – August 18, 2021) – David H. Brett, President and CEO, Pacific Bay Minerals Ltd. (TSXV: PBM) ("Pacific Bay" or the "Company") is pleased to announce that Precision GeoSurveys Inc. ("Precision") has completed the airborne magnetic survey (the "Survey"), announced on June 16, 2021, over the Company's 100% owned Wheaton Creek Gold property (the "Property") in Northern British Columbia. The survey has successfully outlined distinctive magnetic features that will assist the drill targeting in the upcoming program.

From the Company's VP of Exploration, Sebastien Ah Fat, "We are very pleased to find that the Survey has successfully confirmed our initial theory that a well-defined ultramafic contact boundary exists on the Property. The discovery of thick zones of magnetic lows that abruptly transition from magnetic highs may be associated with liswanite mineralization. Listwanite, being formed by the carbonization of serpentinized ultramafic rock, is a key alteration indicator commonly associated with mesothermal quartz carbonate gold deposits and we hope to confirm this via our future drilling programs at Wheaton Creek Gold."

The Survey successfully identified magnetic high anomalies of the Cache Creek Ultramafic Complex and distinctive contact fault boundaries which are prospective for hydrothermal deposition. Furthermore, a thick, northwest-trending, magnetic low anomaly adjoining the Cache Creek Ultramafic Complex to the east may correlate with carbonization of serpentinized ultramafic rock known as liswanite. Listwanite is a distinctive alteration feature commonly associated with lode gold, quartz carbonate gold deposits. These findings reinforce the thesis that Wheaton Creek bears many geologic similarities to the Atlin Mining Camp where the source of the placer gold was found to be at or near fault boundaries of ultramafic and sedimentary rock.

Figure 1: Wheaton Creek Gold, Total Magnetic Intensity Survey Results with Interpreted Fault Boundaries

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3362/93395_c890000fe49298fd_002full.jpg

Figure 2: Wheaton Creek Gold, Calculated Vertical Gradient Survey Results with Interpreted Carbonization Alteration Zone.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3362/93395_c890000fe49298fd_003full.jpg

Pacific Bay's Vice President of Operations, Antonio Vespa, explains, "We want to take a data driven approach for our exploration programs. Now that we have completed our initial site visit and the airborne magnetic survey, we have increased confidence in our proposed drill targets. We are very excited to receive further interpretation of the data gathered so far and continue with exploration later this year."

Mr. Vespa and Mr. Ah Fat, completed a site visit on the 17th of June, 2021. The site visit was successful in gathering information about the current state of the Property, including:

-

Accessibility to the site

-

Condition of infrastructure, including camp availability, in the area

-

Location of previous drillholes

-

Drone photogrammetry

The Company plans to proceed with the diamond drilling of 3-5 drillholes in September/October of 2021, subject to drill contractor availability and permit amendments with new drill sites.

Wheaton Creek Highlights:

-

3,019 hectares of mineral tenures 100% owned by the Company

-

1986 drillhole 86-01 intercepted 5.38 grams per tonne of gold over 3.05 metres with visible gold

-

5-year multi-year area based (MYAB) permit in good standing

-

Notice of work (NOW) application approved

Note: all above reported intercepts are core lengths only as the true width of the structures has not yet been determined.

Sebastien Ah Fat, P.Geo., a Qualified Person as defined by National Instrument 43-101, approved the technical information in this release.

On Behalf of the Board of Directors

David Brett, CEO

dbrett@pacificbayminerals.com

(604) 682-2421

Helder Carvalho, Vice President, Corporate Development

hcarvalho@pacificbayminerals.com

pacificbayminerals.com / Twitter / LinkedIn

This news release contains "forward‐looking statements" within the meaning of Canadian securities legislation. Forward‐looking statements include, but are not limited to, statements with respect to the expected use of proceeds of the Financing. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which Pacific Bay will operate in the future. Certain important factors that could cause actual results, performances or achievements to differ materially from those in the forward‐looking statements include, amongst others, the global economic climate, dilution, share price volatility and competition. Although Pacific Bay has attempted to identify important factors that could cause actual results to differ materially from those contained in forward‐looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward‐looking statements. Pacific Bay does not undertake to update any forward‐looking statements, except in accordance with applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR RELEASE, PUBLICATION, DISTRIBUTION OR DISSEMINATION DIRECTLY, OR INDIRECTLY, IN WHOLE OR IN PART, IN OR INTO THE UNITED STATES.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/93395

(Bloomberg) — BHP Group’s go-ahead to spend $5.7 billion on a giant Canadian potash mine is shining a spotlight on a commodity vital to feeding the world.

Prices of the nutrient essential to producing food for growing populations soared after a crop rally helped farmers boost fertilizer purchases. Unlike oil or most metals and grains, potash trade is focused on annual contracts or in the spot market, rather than on a futures exchange — and supplies are mostly controlled by just a handful of producers.

The fertilizer is part of mining giant BHP’s shift toward commodities of the future as it exits fossil fuels, though production won’t start for another six years. For now, much of the focus will be on how U.S. sanctions on Belarus’s state-owned producer affect supply.

Here’s why potash is important and what’s driving the market:

Market Rally

Grains output jumped about 25% in almost a decade on rising global food demand, while a crop rally in the past year encouraged farmers to expand planting and use more fertilizers. That’s seen spot potash prices in Brazil and the U.S. hit the highest in at least eight years.

Nutrien Ltd., the biggest fertilizer company, earlier this year said it will raise potash production amid a tightening market. Last week, the Canadian company revised its forecast for global potash shipments to a record on strong demand.

Miners Join Party

BHP on Tuesday finally approved spending on the Jansen potash mine in Canada, after years of wavering over the huge cost. Potash offers the world’s top mining company a long-term future profit driver as it retreats from fossil fuels and focuses on commodities that should benefit from rising populations or the green-energy transition.

Jansen could operate for a century, and is a scalable business that could grow to rival BHP’s Pilbara iron ore operations and its copper mines in Chile in importance, Ragnar Udd, president of BHP’s Minerals Americas business, said on a media call on Wednesday. BHP isn’t the only miner moving into fertilizers — Anglo American Plc took over a $4 billion U.K. mine in 2020 as it shifts from coal to more environmentally-friendly commodities.

There are other big projects in the works. Russia’s Acron Group is speeding up construction of Talitsky potash mine and targets the first supplies in 2025. In Belarus, Slavkali plans to start a 2 million tons-a-year mine in 2023.

Supply Uncertainty

Output is mostly concentrated in North America and former Soviet nations like Russia and Belarus, from underground deposits formed by evaporated sea beds millions of years ago. Nutrien, Mosaic Co., Belaruskali OAO and Uralkali PJSC are among the main producers.

The U.S. last week sanctioned Belaruskali as it targeted companies with ties to President Alexander Lukashenko, though it’s not clear how that will affect supply. Counterparts have until December to wind down transactions with Belaruskali, while Belarusian Potash Co., which handles all of the country’s potash exports, wasn’t itself sanctioned.

Still, BPC told RIA Novosti the sanctions will lead to higher potash prices and less availability on the world market.

Potash Trade

Unlike say crude, copper or wheat, benchmark prices are largely derived from annual deals between producers and buyers, rather than on a futures exchange. The nutrient is also traded in spot markets.

Prices at multiyear highs “revived projects like Jensen or Talitsky in Russia, even as the market is still in oversupply,” said VTB Capital analyst Elena Sakhnova. “It’s not clear how long potash price dynamics will sustain, as it is driven by speculative factors and uncertainty over Belarusian shipments.”

BHP’s Udd said he was confident the market could absorb the extra supply from Jansen, with first production targeted for 2027. “The feedback we’re getting from customers at this point is that they will really relish the competition this will induce in the market.”

(Adds comments from BHP’s Udd throughout.)

More stories like this are available on bloomberg.com

Subscribe now to stay ahead with the most trusted business news source.

©2021 Bloomberg L.P.

(Expressed in United States dollars except where otherwise indicated)

MONTREAL, Aug. 18, 2021 (GLOBE NEWSWIRE) — (TSXV: GMN) GobiMin Inc. (“GobiMin” or the “Company”, together with its subsidiaries collectively the “Group”) reports its financial and operating results for the second quarter of 2021. The unaudited condensed interim consolidated financial statements along with quarterly highlights of management’s discussion and analysis have been filed with SEDAR (www.sedar.com) and are also available at the website of the Company (www.gobimin.com).

Financial Highlights

|

Three months ended June 30, |

Year ended |

||

|

2021 |

2020 |

December 31, 2020 |

|

|

$’000 |

$’000 |

$’000 |

|

|

Revenue |

220 |

202 |

891 |

|

(Loss)/gain on disposal of financial assets |

(22) |

124 |

266 |

|

Fair value (loss)/gain on financial assets |

(26) |

194 |

(106) |

|

Net loss for the period/year |

(479) |

(70) |

(3,349) |

|

Loss attributable to shareholders of the Company |

(402) |

(30) |

(3,057) |

|

Basic and diluted loss per share (in $) |

(0.008) |

(0.001) |

(0.062) |

|

(LBITDA)/EBITDA (1) |

(415) |

10 |

(3,002) |

|

(LBITDA)/EBITDA per share (in $) (1) |

(0.008) |

0.0002 |

(0.061) |

|

As at June 30, |

As at |

||

|

2021 |

2020 |

December 31, 2020 |

|

|

$’000 |

$’000 |

$’000 |

|

|

Cash and cash equivalents |

18,636 |

17,886 |

19,471 |

|

Cash and cash equivalents per share (in $) (1) |

0.38 |

0.36 |

0.40 |

|

Working capital |

20,528 |

21,190 |

21,306 |

|

Total current liabilities |

2,512 |

2,272 |

2,536 |

|

Total assets |

74,266 |

73,296 |

74,985 |

Note:

(1) As non-IFRS measurements, (LBITDA)/EBITDA ((loss)/earnings before interest income and expense, income taxes, depreciation and amortization), (LBITDA)/EBITDA per share and Cash and cash equivalents per share are not mandatorily required by IFRS and, therefore, the amounts presented in the above table may not be comparable to similar data presented by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

Business Summary and Development

1. Gold Project in Xinjiang

The Company owns 70% equity interests in Xinjiang Tongyuan Minerals Limited which operates the Sawayaerdun Gold Project (“Gold Project”) in Xinjiang. Its exploration licence had been renewed with expiry date on June 15, 2023. Upon the settlement of the mining royalties of $1,481,000 (equivalent to RMB9,560,000) in July 2021, the mining licence had been renewed with expiry date on March 22, 2023.

The on-site industrial test on applying bio-tech methodology on extraction of metals from large-scale samples of gold ores was running behind schedule attributable to the COVID-19 pandemic. According to the analysis results on the ore samples and the immersion gold tests conducted by the Research Institute, arsenic and iron in the ore samples have been successfully removed by oxidation. It is almost the end of the pre-oxidation stage. Upon the satisfaction in maintaining the alkali balance, the industrial test would enter into the final stage of gold immersion process in late 2021.

For the six months ended June 30, 2021, there was no addition to exploration and evaluation assets. As at June 30, 2021, the Group had a contractual commitment of $1,653,000 for the future development of the Gold Project.

2. Financial Assets

(i) Listed Securities

As at June 30, 2021, the fair value of listed securities held by the Group amounted to $313,000 (December 31, 2020: $247,000) which include investments in listed stock, futures and options of $252,000 (December 31, 2020: $127,000) trading through registered brokerage firms in Hong Kong and a listed stock in Canada of $61,000 (December 31, 2020: $120,000). For the six months ended June 30, 2021, the loss on disposal of listed stock, indexes, futures and options amounted to $137,000 (six months ended June 30, 2020: gain of $84,000) and fair value loss on listed securities was $88,000 (six months ended June 30, 2020: $76,000).

(ii) Unlisted Investments

The Group holds 670,000 shares of Dragon Silver Holdings Limited (“Dragon Silver”) representing 9.90% of its total issued capital at an investment cost of $1,121,000 (equivalent to HK$8,710,000). Dragon Silver is a Hong Kong based company which mainly engaged in trading, production, processing and investment in precious metals and non-ferrous metals and related products. In consideration of the continuous difficult market conditions and the impact of COVID-19, the Group agreed to waive further the profit guarantee compensation for the years ended June 30, 2021 and 2022 as requested by the guarantor. There were no material fair value changes for the investments in Dragon Silver for the six months ended June 30, 2021 (six months ended June 30, 2020: nil).

As at June 30, 2021, unlisted investments held by the Group other than Dragon Silver amounted to $268,000 (December 31, 2020: $257,000). During the period under review, the fair value gain on other unlisted investments was $4,000 (six months ended June 30, 2020: gain of $5,000).

(iii) Debentures and Certificate of Deposit

As at June 30, 2021, the Group held debentures of $2,551,000 (December 31, 2020: $2,741,000) with coupon rates ranged from 4.250% to 7.375% (December 31, 2020: 4.250% to 7.375%) per annum and maturities ranged between November 30, 2026 and perpetual (December 31, 2020: May 31, 2021 and perpetual).

For the six months ended June 30, 2021, interest income from debentures was $79,000 (six months ended June 30, 2020: $98,000) and fair value gain on debentures amounted to $10,000 (six months ended June 30, 2020: loss of $138,000). No gain or loss on disposal of debentures (six months ended June 30, 2020: gain of $4,000) was recorded for the six months ended June 30, 2021.

3. Liquidity and Capital Resources

As at June 30, 2021, working capital of the Group was amounted to about $20,528,000 (December 31, 2020: $21,306,000), which is computed by netting off its current assets of $23,040,000 (December 31, 2020: $23,842,000) with its current liabilities of $2,512,000 (December 31, 2020: $2,536,000).

Taking into account of its financial position, management of the Group considered that its cash and cash equivalents will be more than sufficient to finance its operation, including the contractual commitments of the Gold Project of approximately $1,653,000 (December 31, 2020: $1,633,000) as at June 30, 2021.

For further information, please contact:

Felipe Tan, Chief Executive Officer

Tel: (852) 3586-6500

Email: felipe.tan@gobimin.com

Certain statements contained in this press release constitute forward-looking information. Such statements are based on the current expectations of management of GobiMin. You are cautioned that such statements are subject to a multitude of risks and uncertainties that could cause actual results, future circumstances or events to differ materially from those projected in the forward-looking information. Forward looking information includes without limitation, statements regarding the size and quality of the Company’s mineral resources, progress in development of mineral properties, the prospective mineralization of the properties, and planned exploration programs. The reader should not place undue reliance on the forward-looking information included in this press release given that (i) actual results could differ materially from a conclusion, forecast or projection in the forward-looking information, and (ii) certain material factors or assumptions were applied in drawing a conclusion or making a forecast or projection as reflected in the forward-looking information could prove to be inaccurate. These statements speak only as of the date they are made, and GobiMin assumes no obligation to revise such statements as a result of any event, circumstance or otherwise, except in accordance with law.

“Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.”

To receive GobiMin press releases by email, send a message to info@gobimin.com and

specify “GobiMin press releases” on the subject line

To unsubscribe GobiMin press releases, please send a message to unsubscribe@gobimin.com

VANCOUVER, BC / ACCESSWIRE / August 18, 2021 / Strategic Metals Ltd. (TSXV:SMD) ("Strategic" or the "Company") announces results from a recently completed program comprising geological mapping and soil geochemical sampling at its Nikki copper-gold porphyry project, which is located in the Kluane belt where the Company's research and exploration has recognized a string of promising high-level porphyry copper-gold prospects.

The Nikki project is situated in southwestern Yukon, 25 km northwest of the Mint project (see Company news release dated August 11, 2021) and 16 km west of the Alaska Highway (Figure 1). Both Nikki and Mint are 100% owned by Strategic and neither is subject to underlying royalty interests. The Nikki project comprises 40 mineral claims, encompassing 800 hectares (8 km2), and is located within the Traditional Territory of the White River First Nation.

The Nikki area was first staked in 1910, making it one of the oldest mineral occurrences in western Yukon, but little exploration was done on it prior to Strategic staking its claims in 2004 despite the fact that it was recognized as a porphyry target in the late 1960s soon after Western Copper and Gold's Casino deposit was discovered 120 km to the northeast.

The Nikki porphyry system is hosted in a northwesterly-elongated, early Cretaceous intrusive complex composed of tabular bodies of fine grained diorite and younger porphyritic granodiorite, which intrude a section of Paleozoic argillites with minor limestone lenses. A system of Miocene porphyry dykes cut the older intrusions and sedimentary wallrocks. The target is marked by very strong copper and gold stream sediment anomalies, a magnetic high and a large gossan.

Work by Strategic has defined a 2000 m long by up to 1100 m wide soil geochemical anomaly that is cored by high copper values with scattered anomalous values for lead, zinc and silver on the northern and eastern flanks. Gold-in-soil values are strong within the porphyry but are also high on the flanks where mineralized skarns and veins have been noted. Peak soil values are 3060 ppm copper, 1590 ppb gold, 45.5 ppm silver, 4970 ppm lead and 3950 ppm zinc, as illustrated on Figures 2-6.

The Nikki project has also responded well to geophysical surveys (magnetic, radiometric and induced polarization). A pronounced magnetic high that coincides with the diorite/granodiorite complex (Figure 7) is locally accompanied by strong radiometric highs that are attributed to potassic alteration (Figure 8), and areas of moderate chargeability. The geological setting, soil geochemical patterns and geophysical response are all consistent with a high-level alkalic porphyry system.

A total of seven shallow diamond drill holes have tested the upper portion of the porphyry target, with two holes in 1971 totalling 290 m, four holes in 2010 totalling 1308 m and one hole in 2012 reaching 298 m. All of the holes contain porphyry style alteration and mineralization. The 1971 holes were not analyzed for gold but return promising copper values, with one hole averaging 0.15% over 150 m and the other 0.12% over 140 m. The best results from the 2010 and 2012 drilling came from the bottom of hole 10-02, which averaged 0.13 % copper and 0.076 g/t gold over the last 64 m (Figure 9). Nearby hand trenches also produced encouraging results with chip samples from one trench grading 0.38% copper and 0.364 g/t gold over its entire 6 m length and those from the other trench averaging 0.47% copper and 0.194 g/t gold over its 8 m length.

Little effort has been directed towards evaluating precious metal mineralization in skarns and veins on the fringes of the porphyry system. Most of the gold-enriched rock samples taken on the property were collected up-slope to the northeast of the drill holes (Figure 10). The best gold-in-rock result came from a chip sample across part of a copper-bearing skarn exposure, located about 500 m north of the historical drill holes, which returned 11.95 g/t gold over 2 m. The strongest gold-in-soil values approximately coincide with a broad area characterized by high potassium radiometrics and moderately strong magnetics.

"Historical work has identified a broad zone of copper-enriched porphyry mineralization within the diorite/granodiorite complex, but recent work at Nikki and elsewhere in the Kluane belt suggests that the younger dykes may have played an important role in localizing mineralization, particularly gold." states Doug Eaton CEO of Strategic. "The best results from soils and rocks are mostly located up-slope to the north of the historical drill holes in an area with elevated radiometric and magnetic response. This signature suggests that potassic alteration may have occurred in wallrocks above deeper porphyry mineralization."

Rock sample preparation and multi-element analyses were carried out at ALS in Whitehorse, YT and North Vancouver, BC, respectively. Each sample was dried, fine crushed to better than 70% passing 2 mm and then a 250 g split was pulverized to better than 85% passing 75 microns. The fine fractions were analyzed for 35 elements using aqua regia digestion followed by inductively coupled plasma (ME-ICP41). An additional 50 g charge was further analysed for gold by fire assay and atomic absorption spectroscopy finish (Au-AA24). Samples with overlimit values were further analyzed by four-acid digestion for silver and zinc using Ag-OG46 and Zn-OG46.

Technical information in this news release has been approved by Heather Burrell, P.Geo., a senior geologist with Archer, Cathro & Associates (1981) Limited and qualified person for the purpose of National Instrument 43-101.

About Strategic Metals Ltd.

Strategic is a project generator with 11 royalty interests, 8 projects under option to others, and a portfolio of more than 100 wholly owned projects that are the product of over 50 years of focussed exploration and research by a team with a track record of major discoveries. Projects available for option, joint venture or sale include drill-confirmed prospects and drill-ready targets with high-grade surface showings and/or geochemical anomalies and geophysical features that resemble those at nearby deposits.

Strategic has a current cash position of over $8 million and large shareholdings in a number of active mineral exploration companies including 38.9% of GGL Resources Corp., 33.5% of Rockhaven Resources Ltd., 19.9% of Honey Badger Silver Inc., 19.2% of Precipitate Gold Corp. and 18.7% of Silver Range Resources Ltd. All of these companies are well funded and are engaged in promising exploration projects. Strategic also owns 21.9% of Terra CO2 Technologies Holdings Inc., a private Delaware corporation which recently completed a US$9.2 million financing to advance its environmentally-friendly, cost-effective alternative to Portland cement. The current value of Strategic's stock portfolio is approximately $22 million.

ON BEHALF OF THE BOARD

"W. Douglas Eaton"

President and Chief Executive Officer

For further information concerning Strategic or its various exploration projects please visit our website at www.strategicmetalsltd.com or contact:

Corporate Information

Strategic Metals Ltd.

W. Douglas Eaton

President and C.E.O.

Tel: (604) 688-2568

Investor Inquiries

Richard Drechsler

V.P. Communications

Tel: (604) 687-2522

NA Toll-Free: (888) 688-2522

rdrechsler@strategicmetalsltd.com

http://www.strategicmetalsltd.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release may contain forward looking statements based on assumptions and judgments of management regarding future events or results that may prove to be inaccurate as a result of exploration and other risk factors beyond its control, and actual results may differ materially from the expected results.

SOURCE: Strategic Metals Ltd.

View source version on accesswire.com:

https://www.accesswire.com/660211/Strategic-Metals-Updates-Results-from-Its-Nikki-Project-Located-in-the-Newly-Recognized-Kluane-Porphyry-Cu-Au-Belt-SW-Yukon

(Corrects to A$40 billion from $40 billion in first paragraph)

MELBOURNE (Reuters) -Shares in BHP Group Ltd. and Woodside Petroleum fell on Wednesday as investors digested details of the Perth-based oil and gas group's A$40 billion ($29 billion) merger with BHP's petroleum arm, with some questioning the value of the deal for Woodside.

While a 6% fall in BHP's share price was linked to a decision to end its UK dual listing, where its shares have traditionally traded at a large discount, a fall of up to 4% in Woodside reflected concerns about the expansion, they said.

"It may be difficult to get a vote across the line, with Woodside shareholders likely to question the value of the merger," said Jamie Hannah, deputy head of investments at Van Eck Australia, a shareholder in both BHP and Woodside.

"Woodside is one of the worst-performing companies within the energy sector globally post-COVID; the company doesn't yet have a strong mandate to enter a deal of such questionable value and this could further drag on Woodside's shares," he said.

BHP agreed to hive off its petroleum business to Woodside in a nil-premium merger, in return for new Woodside shares which will go to BHP shareholders, who will own 48% of the enlarged group.

The deal will make Woodside a top 10 global independent oil and gas producer, giving it oil assets in the Gulf of Mexico, gas in Trinidad and Tobago and ageing assets in Australia's Bass Strait, while doubling its stake in North West Shelf LNG.

However, it has raised concerns about the strategic sense of expanding in oil and taking on ageing gas assets with big decommissioning costs.

Investors said the fall in Woodside shares was also partly due to worries about an overhang of stock as BHP investors who want to get out of fossil fuels would look to dump the shares.

The stock was down 0.7% in afternoon trade, underperforming local rivals Santos and Oil Search, which were both up 1%.

Woodside's new chief executive, Meg O'Neill, said while investors were very familiar with BHP's Australian oil and gas assets, they did not appreciate the value of its Gulf of Mexico oil stakes – Mad Dog, Atlantis and Shenzi.

"Those are just first-class top-tier assets that will be very cash accretive to the merged company," O'Neill told Reuters.

Analysts were more upbeat about the long term, saying the deal would give Woodside more growth options, beyond its $12 billion Scarborough gas project and Pluto LNG expansion, and the company would benefit from strong cash generation at BHP's debt-free assets.

"It's a logical deal between the parties," said Argo Investments portfolio manager Andy Forster. "I do think ultimately shareholders will vote for it."

Woodside aims to put the deal to a vote in the second quarter of 2022.

Credit Suisse analyst Saul Kavonic said Woodside shareholders may be painted into a corner, noting that, as part of the deal, Woodside gave BHP an option to give up its stake in the Scarborough project for $1 billion if Woodside makes a final investment decision on the project by Dec. 15.

Woodside would then be the sole owner of Scarborough and have to fund the whole project by itself, which it currently cannot afford.

"Shareholders may have little choice but to vote the merger through because it would pose a serious balance sheet overhang," Kavonic said.

($1 = 1.3770 Australian dollars)

(Reporting by Sonali Paul; editing by Richard Pullin)

VANCOUVER, British Columbia, Aug. 18, 2021 (GLOBE NEWSWIRE) — Teck Resources Limited (TSX: TECK.A and TECK.B, NYSE: TECK) (“Teck”) today announced that the wildfire evacuation order for Highland Valley Copper Operations (HVC) issued by the District of Logan Lake previously announced on August 15 has been lifted. HVC has resumed operations and is now in the process of ramping back up to full production.

Teck is focused on protecting the health and safety of employees and contractors and we are continuing to closely monitor wildfire and regional air quality conditions.

Teck’s copper production guidance will be updated as necessary after the risk of further effect on operations from wildfires subsides.

About Teck

As one of Canada’s leading mining companies, Teck is committed to responsible mining and mineral development with major business units focused on copper, zinc, and steelmaking coal, as well as investments in energy assets. Copper, zinc and high-quality steelmaking coal are required for the transition to a low-carbon world. Headquartered in Vancouver, Canada, Teck’s shares are listed on the Toronto Stock Exchange under the symbols TECK.A and TECK.B and the New York Stock Exchange under the symbol TECK. Learn more about Teck at www.teck.com or follow @TeckResources.

Teck Media Contact:

Chris Stannell

Public Relations Manager

604.699.4368

chris.stannell@teck.com

Teck Investor Contact:

Fraser Phillips

Senior Vice President, Investor Relations & Strategic Analysis

604.699.4621

fraser.phillips@teck.com

By Sonali Paul and Melanie Burton

MELBOURNE (Reuters) -Shares in BHP Group and Woodside Petroleum fell on Wednesday as investors on both sides raised questions about the value of the Perth-based oil and gas group's proposed $29 billion merger with BHP's petroleum arm.

While a 6% fall in BHP's share price was linked to a decision to end its UK dual listing, where its shares have traditionally traded at a large discount, a fall of up to 4% in Woodside reflected concerns about the expansion, they said.

"Woodside is one of the worst-performing companies within the energy sector globally post-COVID; the company doesn't yet have a strong mandate to enter a deal of such questionable value and this could further drag on Woodside's shares," said Jamie Hannah, deputy head of investments at Van Eck Australia, a shareholder in both companies.

BHP agreed to hive off its petroleum business to Woodside in a nil-premium merger, in return for new Woodside shares which will go to BHP shareholders, who will own 48% of the enlarged group.

The deal will make Woodside a top 10 global independent oil and gas producer, giving it oil assets in the Gulf of Mexico, gas in Trinidad and Tobago and ageing assets in Australia's Bass Strait, while doubling its stake in North West Shelf LNG.

However, it raised concerns about the strategic sense of expanding in oil and taking on ageing gas assets with big decommissioning costs.

Investors said the fall in Woodside shares was also partly due to worries about an overhang of stock as BHP investors who want to get out of fossil fuels would look to dump the shares.

The stock was down 1.2% in afternoon trade, underperforming a 1% rise in local rivals Santos and Oil Search.

Woodside's new chief executive, Meg O'Neill, said while investors were very familiar with BHP's Australian oil and gas assets, they did not appreciate the value of its Gulf of Mexico oil stakes – Mad Dog, Atlantis and Shenzi.

"Those are just first-class top-tier assets that will be very cash accretive to the merged company," O'Neill told Reuters.

Analysts and two BHP investors said Woodside got the BHP assets relatively cheaply.

"I'd much rather have just hung on to them and harvested the capital because demonstrably the returns from the growth parts of those projects are much higher than Jansen," said a Sydney-based fund manager, referring to the $5.7 billion Jansen potash project BHP approved on Tuesday.

Tribeca Investment Partners CEO Ben Cleary, a BHP shareholder, said what BHP lost with the discount on its petroleum assets would be offset by a higher valuation multiple for no longer holding oil and gas.

"Long term the deal makes sense. I think BHP looks more attractive for a wider audience," said Matt Haupt, portfolio manager at Wilson Asset Management, a BHP shareholder.

Analysts were upbeat about the long term for Woodside, saying the deal would give it more growth options, beyond its $12 billion Scarborough gas project and Pluto LNG expansion, funded by strong cash generation at BHP's debt-free assets.

"It's a logical deal between the parties," said Argo Investments portfolio manager Andy Forster. "I do think ultimately shareholders will vote for it."

Woodside aims to put the deal to a vote in the second quarter of 2022.

Credit Suisse analyst Saul Kavonic said Woodside shareholders may be painted into a corner, noting that, as part of the deal, Woodside gave BHP an option to hand over its stake in the Scarborough project for $1 billion if Woodside makes a final investment decision on the project by Dec. 15.

Woodside would then be the sole owner of Scarborough and have to fund the project by itself, which it cannot afford.

"Shareholders may have little choice but to vote the merger through because otherwise it would pose a serious balance sheet overhang," Kavonic said.

($1 = 1.3770 Australian dollars)