Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE.

Recent Performance Context for Lundin Mining

Lundin Mining (TSX:LUN) has drawn fresh attention after a period of strong share performance, with the stock showing gains over the past week, month, and past 3 months that outpaced its single day decline.

For investors tracking longer trends, total returns over the past year and past 3 years are very large multiples of the starting value. The past 5 years also show a sizeable gain, putting the current CA$34.22 share price into sharper focus.

See our latest analysis for Lundin Mining.

The recent 60.28% three-month share price return on Lundin Mining, together with a very large one-year total shareholder return of 178.33%, suggests momentum has been building into the current CA$34.22 level despite a one-day share price decline of 1.10%.

If you are scanning for other opportunities in the resources space, this could be a good moment to broaden your search with fast growing stocks with high insider ownership.

With Lundin Mining now at CA$34.22 and trading above the average analyst price target of CA$30.14, the key question is whether recent momentum leaves upside on the table or if the market is already pricing in future growth.

Most Popular Narrative: 21% Overvalued

With Lundin Mining last closing at CA$34.22 against a narrative fair value of about CA$28.28, the gap between price and modelled worth is clear and sets up an interesting valuation debate.

The fair value estimate has risen slightly from US$27.52 to US$28.28, reflecting a modest adjustment to the model inputs.

The net profit margin has risen slightly from 15.98% to 16.67%, suggesting a somewhat higher assumed earnings efficiency over time.

Curious what justifies paying up for Lundin Mining here? The narrative leans heavily on future profitability, modest growth assumptions, and a premium earnings multiple. Want to see how those ingredients are combined into that fair value?

Result: Fair Value of $28.28 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the heavy tilt to South American copper and the ongoing Candelaria legal overhang could easily challenge today’s upbeat profitability assumptions.

Find out about the key risks to this Lundin Mining narrative.

Build Your Own Lundin Mining Narrative

If you look at the numbers and reach a different conclusion, or simply want to test your own assumptions against the data, you can build a personalised Lundin Mining narrative in just a few minutes, starting with Do it your way.

A great starting point for your Lundin Mining research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Lundin Mining has caught your attention, do not stop here. You could miss opportunities that better match your goals and risk comfort.

- Scan for potential value by checking out these 868 undervalued stocks based on cash flows that trade at prices below what their cash flows might suggest.

- Ride big technology shifts by reviewing these 24 AI penny stocks that are tied to artificial intelligence themes.

- Add income-focused ideas to your watchlist by assessing these 12 dividend stocks with yields > 3% offering yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LUN.TO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

- If you are looking at Lundin Mining and wondering whether the current share price offers value or stress, this article walks through what the numbers actually say about the stock.

- The share price closed at C$34.22, with returns of 9.9% over 7 days, 22.6% over 30 days, 15.2% year to date and 178.3% over the past year, which naturally raises questions about what is already priced in.

- Recent attention on Lundin Mining has centred on the stock’s strong share price performance and how it fits into investor interest in materials companies more broadly. These moves have put valuation front and centre for anyone trying to decide whether to initiate or adjust a position.

- Against this backdrop, Lundin Mining currently scores 0 out of 6 on our valuation checks for being undervalued. In what follows, we look at what different valuation methods say about the stock and then finish with a way to tie those models into a more complete view of value.

Lundin Mining scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Lundin Mining Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model takes estimates of future cash flows and discounts them back to today to reach an implied value for the company on a per share basis.

For Lundin Mining, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is $471.03 million. Analyst estimates and extrapolations suggest free cash flow of $743.55 million in 2026 and $402 million in 2030, with interim years including both positive and negative projected figures. Beyond the analyst horizon, Simply Wall St extrapolates additional years of free cash flow using its own assumptions.

When all of these projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of $16.37 per share. Compared to the current share price of C$34.22, the DCF output implies the stock is 109.1% overvalued based on these inputs and assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Lundin Mining may be overvalued by 109.1%. Discover 868 undervalued stocks or create your own screener to find better value opportunities.

LUN Discounted Cash Flow as at Jan 2026

Approach 2: Lundin Mining Price vs Earnings

For profitable companies, the P/E ratio is a useful gauge because it links what you pay for each share to the earnings that business is currently generating. Investors usually look for a P/E level that reflects both how quickly earnings might change over time and how risky those earnings are, with higher expected growth or lower risk often justifying a higher P/E, and the opposite also being true.

Lundin Mining is currently trading on a P/E of 99.20x. That sits well above the Metals and Mining industry average of 25.01x and the peer group average of 22.31x. Simply Wall St’s Fair Ratio for Lundin Mining is 25.53x, which is its proprietary estimate of what a reasonable P/E could be for this company given factors such as earnings growth profile, profit margins, industry, market cap and identified risks.

The Fair Ratio is more tailored than a simple comparison with peers or the industry average, because it adjusts for company specific characteristics rather than assuming every business in the group deserves the same multiple. Comparing Lundin Mining’s current 99.20x P/E to the Fair Ratio of 25.53x indicates that the shares are trading well above what this framework suggests.

Result: OVERVALUED

TSX:LUN P/E Ratio as at Jan 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Lundin Mining Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St’s Community page you can use Narratives, where you set a story for Lundin Mining that ties your view on its projects, risks and metals cycles to specific forecasts for revenue, earnings and margins. This then produces a Fair Value you can compare with the current price. It updates automatically when news or earnings land and can look very different from other investors’ views. For example, one investor might build a bullish Lundin Mining Narrative closer to the upper analyst price target of about C$21.08, while another might anchor their assumptions nearer the C$14.04 lower target.

Do you think there’s more to the story for Lundin Mining? Head over to our Community to see what others are saying!

TSX:LUN 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LUN.TO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

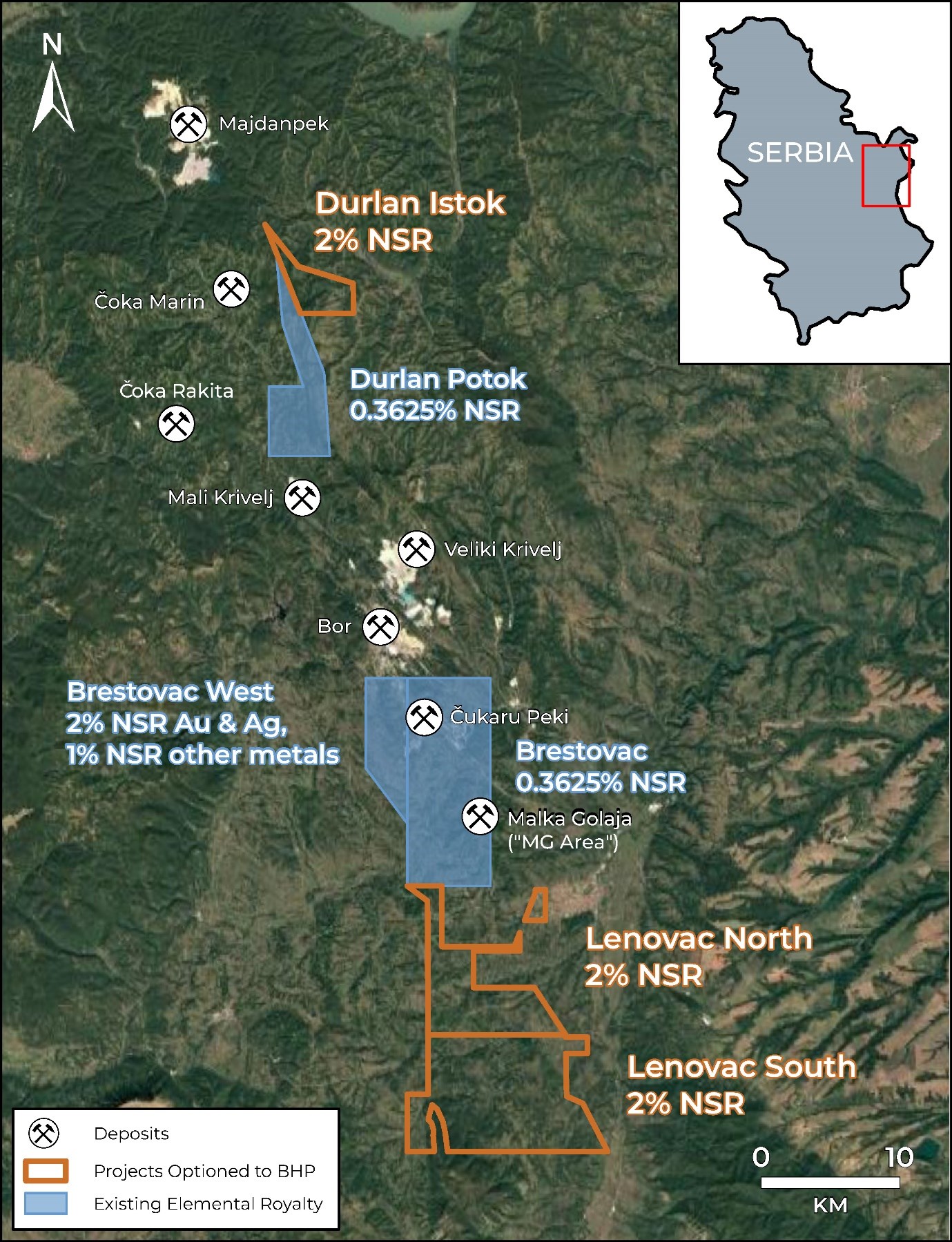

Vancouver, British Columbia–(Newsfile Corp. – January 16, 2026) – Elemental Royalty Corporation (TSXV: ELE) (NASDAQ: ELE) ("Elemental" or the "Company") is pleased to announce the execution of a definitive option and earn-in agreement (the "Agreement") covering three exploration licenses in the Bor Mining District of Serbia to a wholly owned subsidiary of BHP Group Limited ("BHP"). The three exploration-stage projects are currently held by Elemental's wholly owned Serbian subsidiary Magma Resources doo ("Magma") and BHP will have the option to acquire Magma in exchange for cash payments and by satisfying work commitments. Elemental will retain 2% NSR royalties on the projects as well as other considerations (see discussion of Commercial Terms below).

The Projects nicely complement Elemental's other royalty interests in the Bor District, which include the Brestovac, Brestovac West, and Jasikovo East-Durlan Potok properties (see Figure 1). Brestovac is one of Elemental's flagship royalties, covering Zijin Mining Group Co., Ltd's producing Čukaru Peki copper-gold mine and recently discovered Malka Golaja copper-gold deposit. Zijin has been rapidly expanding its Čukaru Peki operations, increasing capacity at its current mill while continuing to add infrastructure for the development of the "Lower Zone" porphyry copper-gold deposit. Zijin's published mineral resources and reserves for Čukaru Peki have also continued to grow rapidly, as shown in Zijin's recent annual reports. The Lenovac projects, included in the BHP Agreement, cover the extension of the geologic trend that hosts the Čukaru Peki and Malka Golaja copper-gold deposits to the south.

Commercial Terms Overview. (all terms in USD)Pursuant to the Agreement, BHP can acquire and retain a 100% interest in Magma and the Projects by satisfying each of the following conditions: (a) making a payment of $200,000 to the Company on the six-month anniversary of the Agreement, (b) annual payments of $200,000 to the Company on every anniversary of the Agreement until the earn-in is complete, and (c) completing $5,000,000 in cumulative exploration expenditures on the Projects within five years.

Upon BHP's option exercise and earn-in, Elemental will retain a 2% NSR royalty interest on each Project. BHP may buy back up to a total of half a percent (0.5%) of the royalty in quarter percent (0.25%) increments; 0.25% can be purchased for $5,000,000 before the eighth anniversary of the agreement and 0.25% can be purchased for $5,000,000 before the 11th anniversary of the agreement. BHP will also make annual advance royalty payments of $200,000 to the Company until the commencement of commercial production.

Overview of the Projects.The Bor Mining District in eastern Serbia has been one of Europe's largest copper producers for over a century, where historic and current mining operations have been developed within a cluster of porphyry Cu-Au, high-sulfidation epithermal and skarn systems (including Bor, Veliki Krivelj, Majdanpek and Čukaru Peki; see Figure 1). The Elemental projects (the "Projects") were originally acquired in 2023 and 2024 and are positioned along trend of Zijin Mining's Bor and Čukaru Peki operations. Although there are still near-surface deposits being identified in the area, several recent discoveries have been made at relatively deep levels (such as Zijin's Čukaru Peki and Dundee Precious Metals' Čoka Rakita deposits) and require deep drilling. BHP's deep-sensing geophysical capabilities and existing regional interest make them an ideal exploration partner for the Projects.

Elemental has acquired over 150 square kilometres of mineral rights along trend of the major copper and gold deposits within the Bor Mining District (see Figure 1). Previous exploration in the Bor District has typically targeted Upper Cretaceous andesite units, which host the majority of the epithermal and porphyry systems at the Bor Copper Complex and Čukaru Peki mine. However, new discoveries such as Dundee Precious Metals' Čoka Rakita skarn deposit highlights that the different geologic settings and older Jurassic and Paleozoic host rocks are also prospective for additional discoveries. The Elemental Projects include both the traditionally prospective Upper Cretaceous andesite units of the Timok Magmatic Complex, as well as deeper host rock packages where several recent discoveries have been made.

The Lenovac North and South licenses lie directly south of the Zijin's Brestovac license, which hosts the Čukaru Peki and the recently discovered Malka Golaja copper-gold deposits. Elemental's Lenovac licenses cover the southern extension of this trend where a regional fault displaces the trend of mineralization and favorable host rocks to the southwest. The licenses are largely comprised of prospective Cretaceous volcanic and sedimentary units with some areas of Miocene cover.

The Durlan Istok license is located to the southeast of Zijin's Majdanpek porphyry copper-gold mine and east of Čoka Marin, a high-grade polymetallic volcanogenic/epithermal deposit. The Durlan Istok license contains the stratigraphic sections that hosts Čoka Marin and the Čoka Rakita skarn further to the southwest.

Comments on adjacent or nearby Districts, Mines, and Deposits.The districts, mines, and deposits discussed in this news release provide context for Elemental's projects, which occur in similar geologic settings, but this is not necessarily indicative that the Company's projects host similar tonnages or grades of mineralization.

North American Investor RelationsElemental has retained the services of Renmark Financial Communications Inc. to handle its investor relations activities in North America. In consideration of the services to be provided, the monthly fees incurred by Elemental will be a cash consideration of up to C$9,000, starting January 1, 2026, for a period of seven months ending on July 31, 2026, and monthly thereafter. Renmark Financial Communications does not have any interest, directly or indirectly, in Elemental or its securities, or any right or intent to acquire such an interest.

David M. ColeCEO and Director

For more information, please contact:

|

David M. Cole |

|

|

CEO |

|

|

Tara Vivian-Neal |

|

|

Investor Relations |

(TSXV: ELE) (NASDAQ: ELE) | ISIN: CA28620K1066 | CUSIP: 28620K

About Elemental Royalty Corporation.Elemental Royalty is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 16 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus's track record of accretive royalty acquisitions with EMX's strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental Royalty trades on the TSX Venture Exchange under the ticker symbol "ELE", and on the NASDAQ Stock Market under the ticker symbol "ELE".

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Qualified PersonDr. Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

Cautionary note regarding forward-looking statementsThis news release contains certain "forward looking statements" and certain "forward-looking information" as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "intend", "estimate", "anticipate", "believe", "continue", "plans" or similar terminology.

Forward-looking statements and information include, but are not limited to, the Company's ability to deliver a materially increased revenue profile with a lower cost of capital, the future growth, development and focus of the Company, and the acquisition of new royalties and streams. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies.

Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of Elemental Royalty to control or predict, that may cause Elemental Royalty' actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the impact of general business and economic conditions, the absence of control over the mining operations from which Elemental Royalty will receive royalties, risks related to international operations, government relations and environmental regulation, the inherent risks involved in the exploration and development of mineral properties; the uncertainties involved in interpreting exploration data; the potential for delays in exploration or development activities; the geology, grade and continuity of mineral deposits;; the possibility that future exploration, development or mining results will not be consistent with Elemental Royalty' expectations; accidents, equipment breakdowns, title matters, labour disputes or other unanticipated difficulties or interruptions in operations; fluctuating metal prices; unanticipated costs and expenses; uncertainties relating to the availability and costs of financing needed in the future; the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses, commodity price fluctuations; currency fluctuations; regulatory restrictions, including environmental regulatory restrictions; liability, competition, loss of key employees and other related risks and uncertainties. For a discussion of important factors which could cause actual results to differ from forward-looking statements, refer to the annual information form of Elemental Royalty for the year ended December 31, 2024. Elemental Royalty undertakes no obligation to update forward-looking statements and information except as required by applicable law. Such forward-looking statements and information represents management's best judgment based on information currently available. No forward-looking statement or information can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Figure 1. Elemental Royalty interests and projects in the Bor Mining District of Serbia.

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/8358/280566_3dabfe0184c6bbcd_001full.jpg

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/280566

Morgan Stanley (MS)

Morgan Stanley (MS) jumped nearly 6% on Thursday and rose again in pre-market trading on Friday after reporting upbeat fourth-quarter results, which exceeded Wall Street expectations on the back of strong revenue from wealth management.

Fourth-quarter net income rose to $4.40bn, or $2.68 per share, from $3.71bn, or $2.22 per share, a year ago. Revenue increased to $17.89bn from $16.22bn a year ago.

The wealth management unit posted $8.4bn in net revenue in the most recent quarter, up from $7.5bn a year earlier. For the full year, the division generated a record $31.8bn in net revenue.

Total client assets in the wealth and investment management business climbed to $9.3tn, fuelled by more than $350 billion in net new assets.

“Morgan Stanley delivered outstanding performance in 2025,” Ted Pick, the bank’s chief executive and chairman, said in a statement. “Our performance reflects multi-year investments which have contributed to growth and momentum across the integrated firm.”

Morgan Stanley shares have gained more than 43% over the past 12 months.

Anglo American (AAL.L)

London’s listed miners were among the worst performers in the city this morning, with the likes of Anglo American down as much as 1.8% after opening.

It comes as copper prices are down around 2% morning amid reports that Chinese regulators have ordered exchanges to remove servers operated by high-frequency traders from their datacentres.

The Shanghai Futures Exchange, a major metals trading platform, has told brokers they need to get equipment for high-speed clients out by the end of the month, according to a report by Bloomberg. Other clients will need to do so by the end of April, it reported.

Endeavour Mining (EDV.L), Rio Tinto (RIO.L), Antofagasta (ANTO.L), and Glencore (GLEN.L) also lost ground in London on Friday.

Read more: Stocks that are trending today

Genus (GNS.L)

Shares in the biotech business Genus surged as much as 10% this morning, to the top of the FTSE 250 (^FTMC), up around 8% at the time of writing, as it beat expectations for its half-year trading update.

The animal genetics company has forecasted about £50m in actual currency for its adjusted pre-tax profit.

The London-listed business said it had performed strongly in the six months to 31 December, and expects adjusted pre-tax profits to come in around £50m in actual currency, ahead of internal forecasts.

Last September, the company struck a deal to accelerate its 49%-owned porcine joint venture with BCA in China. Genus confirmed that it had received approval from the relevant authorities in China, trigging the $7.5m milestone payment.

Analysts at the broker Peel Hunt credited its earnings beat to strong performance in its pig breeding business.

The Basingstoke-based firm helps farmers breed animals with certain traits such as disease resistance and faster growth. It operates in more than 25 countries, with research laboratories in Wisconsin.

BAE Systems (BA.L)

BAE Systems rose on Friday, up 1.6% at the time of writing, along with other defence-related firms such as Babcock (BAB.L) and Rolls-Royce (RR.L).

It came as Nato personnel from a number of European countries landed in Greenland for an exercise after Trump seeks to own the country, which is a semi-autonomous part of Denmark.

He doubled down on his bid to bring Greenland under US control, telling reporters in the Oval Office, "we need Greenland for national security". Although he did not rule out the use of force, he said late on Wednesday that he thought something could be worked out with Denmark.

"The problem is there's not a thing that Denmark can do about it if Russia or China wants to occupy Greenland, but there's everything we can do. You found that out last week with Venezuela."

Speaking to reporters on Thursday, White House press secretary Karoline Leavitt said she didn't think the deployment of additional European troops to Greenland would impact the president's decision-making process on the Arctic territory. She added: "Nor does it impact his goal of the acquisition of Greenland at all."

Neil Wilson, UK investor strategist at Saxo Markets, said it was "hardly a show of force, but a reminder of what's at stake here".

Download the Yahoo Finance app, available for Apple and Android.

The FTSE 100 (^FTSE) and European stocks had moved lower on Friday, while tech was a bright spot among US indices, as a volatile week comes to a close.

Chipmakers TSMC (TSM) and Nvidia (NVDA) eyed more gains, thanks in part to a US-Taiwan trade deal that promises a $250bn boost to American chip and tech manufacturing.

On Thursday, shares in TSMC popped following a strong quarterly report that revived AI enthusiasm to buoy related stocks more widely.

Meanwhile in Europe, commodities prices have been on a rollercoaster this week as investors looked to precious metals to retreat from risk.

"Copper has been signalling strong economic growth in 2026 — in nominal terms at least," said Neil Wilson, UK investor strategist at Saxo Markets.

"Apparently, China has moved to clamp down on some high frequency traders at the Shanghai Futures Exchange, which has knocked prices down from record highs, while nickel and tin were also lower."

The world has also been watching to see if president Donald Trump will make orders to send troops to Iran amid widespread and violent anti-government protests. While he said earlier in the week that he had been told the killing had stopped, more than 2,400 people have lost their lives in the unrest, according to human rights groups.

Oil prices were higher on Friday afternoon as the chance of increased US presence in Iran cooled, with brent crude futures (BZ=F) trading up more than 1% and West Texas Intermediate (CL=F) rising 1.1%.

Market movers

-

The FTSE 100 (^FTSE) pulled back from all-time highs, dragged 0.1% lower by commodity stocks as precious metal prices lost momentum.

-

Miners Antofagasta (ANTO.L), Glencore (GLEN.L), Anglo American (AAL.L) and Rio Tinto (RIO.L) were among the top fallers in the index by the closing bell

-

Germany's DAX (^GDAXI) dipped 0.3% as its consumer price index data came in in line with expectations.

-

The CAC 40 (^FCHI) in Paris dropped 0.8%.

-

The pan-European STOXX 600 (^STOXX) lost 0.1%.

-

The pound rose slightly against the dollar (GBPUSD=X) to trade below the $1.34 mark.

-

The tech-heavy Nasdaq Composite (^IXIC) was just above the flatline, while the S&P 500 (^GSPC) added nearly 0.1%. The Dow Jones Industrial Average (^DJI) nudged 0.1% lower after stocks reversed a two-day losing streak on Thursday.

Download the Yahoo Finance app, available for Apple and Android.

Rio Tinto Group RIO reported solid growth in iron ore production in the third quarter of 2025. During the quarter, Pilbara iron ore shipments reached 84.3 million tons, increasing 6% from the previous quarter. The company’s total Pilbara iron ore production stood at 84.1 million tons, reflecting robust output despite weather-related disruptions earlier in the year.The robust performance was primarily supported by Rio Tinto’s Pilbara operations in Western Australia. The Gudai-Darri project achieved its highest-ever quarterly production in the third quarter, operating at a run rate of 51 million tons per annum, while shipments rose on a sequential basis despite planned maintenance and infrastructure works. The successful rollout of the new Pilbara Blend product strategy also contributed to improved product mix, with lower SP10 volumes as planned.Also, several major growth projects of the company are progressing. In December 2025, RIO’s Rhodes Ridge joint venture approved a $191 million feasibility study to develop one of the world’s major undeveloped iron ore deposits in Western Australia, aiming for an initial annual production of 40-50 million tons. The study is expected to conclude in 2029. In October 2025, at the Simandou iron ore project in Guinea, the first ore was loaded and transported, marking the start of commissioning across the mine, rail and port infrastructure.The strong quarterly performance, supported by record output at the Gudai-Darri facility and improved system efficiency across the Pilbara, highlights Rio Tinto’s operational strength in iron ore. Major growth projects, such as Rhodes Ridge and Simandou, are advancing steadily, positioning the company well for long-term growth.

Snapshot of RIO’s Peers

Among its major peers, Vale S.A.’s VALE Iron Solutions segment generated net operating revenues of around $8.42 billion in the third quarter of 2025, which marked 5.7% growth from last year’s comparable quarter. Vale’s total iron ore shipments were up 5% from the year-ago quarter. Vale’s average realized iron ore fines price increased 4% year over year to $94.40 per ton.Its other peer, BHP Group Limited BHP, produced a record 263 Mt of iron ore in fiscal 2025. This came within BHP Group’s guidance of 255-265.5 Mt and was up 1% year over year. Production at BHP Group’s Western Australia Iron Ore was a record of 257 Mt (290 Mt on a 100% basis).

RIO's Price Performance, Valuation & Estimates

Shares of Rio Tinto have gained 43.8% in the past six months compared with the industry’s growth of 27.3%.

Image Source: Zacks Investment Research

From a valuation standpoint, RIO is trading at a forward price-to-earnings ratio of 12.13X, below the industry’s average of 17.56X. Rio Tinto carries a Value Score of B.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for RIO’s 2026 earnings has been on the rise over the past 60 days.

Image Source: Zacks Investment Research

Rio Tinto currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BHP Group Limited Sponsored ADR (BHP) : Free Stock Analysis Report

VALE S.A. (VALE) : Free Stock Analysis Report

Rio Tinto PLC (RIO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

An updated edition of the November 25, 2025 article.Nuclear energy is gaining renewed recognition as a vital solution for meeting the world’s rising demand for clean electricity. As utilities transition toward low-carbon power sources, nuclear plants stand out for their ability to provide reliable, carbon-free generation. Unlike solar and wind, which are dependent on weather conditions, nuclear power delivers stable, round-the-clock output. The recent restart of a previously shuttered U.S. nuclear facility underscores the sector’s revival and reflects growing investor interest in nuclear energy stocks.The nuclear energy sector is gaining traction as updated regulations and R&D advance microreactors and small modular reactors. Growing 24/7 clean energy demand from AI data centers, manufacturing reshoring, and electric vehicles is driving new opportunities, while government efforts to bolster domestic uranium supply further support the industry’s momentum.Nuclear power plant operators began the year on a strong footing. Meta Platforms META has entered into long-term nuclear power agreements with Vistra Corp. VST, TerraPower and Oklo Inc. OKLO to secure up to 6.6 gigawatts of nuclear capacity by 2035. Previously, META also signed a long-term agreement with Constellation Energy to procure 1.12 GW of clean nuclear power.With this increasing importance, nuclear energy-related stocks, such as NextEra Energy NEE, Vistra and Oklo, are becoming attractive investment options. Unlike other clean energy sources affected by intermittency, nuclear power plants provide a consistent and stable energy output, operating around the clock except during planned maintenance intervals.Compared with other clean energy sources, nuclear power requires significantly less land to generate the same amount of clean electricity. Additionally, while all traditional energy sources produce waste, nuclear energy stands apart for its highly regulated, secure and systematic approach to waste management and storage. Increasing adoption of electric vehicles, rising demand from the power grids and development of large artificial intelligence-powered data centers are increasing the importance of nuclear power plants.Nuclear Energy stocks have huge potential in the energy space and can offer significant growth opportunities for investors. Our Nuclear Energy Screen makes it easier for investors to locate high-potential stocks at any given time. Apart from the stocks mentioned above, investors can also explore stocks like Ameren Corporation AEE and BHP Group Limited BHP for a stable return in the nuclear energy space.Ready to uncover more transformative thematic investment ideas? Explore 36 cutting-edge investment themes with Zacks Thematic Investing Screens and discover your next big opportunity.NextEra Energy operates several nuclear generation units through its subsidiary, NextEra Energy Resources. NEE’s nuclear assets form a cornerstone of its clean energy strategy, delivering steady, carbon-free baseload power that complements its leading wind and solar portfolio. This diverse generation mix strengthens grid reliability and underpins sustainable long-term earnings growth.Ongoing investments in the upkeep and modernization of its nuclear facilities ensure top-tier operational performance, safety and regulatory adherence. These plants offer long service lives, low operating costs and protection from swings in fossil fuel prices.Last year, NextEra Energy announced two major agreements with Google aimed at strengthening U.S. nuclear leadership and supplying the rising energy needs of AI with clean, reliable nuclear power.This Zacks Rank #2 (Buy) company has a very disciplined capital investment plan, targeting more than $74 billion through 2029, which is expected to fund the expansion of its renewable and storage capacity. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.Vistra Corp. offers a strong long-term investment case, supported by its diversified generation portfolio and expanding leadership in nuclear energy. The acquisition of Energy Harbor meaningfully scaled its nuclear capacity, while long-term power purchase agreements, including a 2,600 megawatt (MW), 20-year nuclear supply deals with Meta, position the company to capitalize on growing demand for reliable, clean power from data centers and AI-driven infrastructure.Vistra’s six nuclear reactors have received a license extension, ensuring continued reliable generation of emission-free electricity in key markets. These six nuclear reactors have the capacity to generate more than 6,500 MW of emission-free energy, enough to power about 3.25 million homes.This Zacks Rank #3 (Hold) stock has a comprehensive hedging program, which lessens the impact of short-term price fluctuations. Oklo Inc.’s small-scale nuclear reactors are gaining traction as an effective solution to address the rapidly growing energy demands of industries like data centers. These small modular reactors are based on liquid-metal-cooled, metal-fueled fast-reactor technology. Oklo has deliberately selected this established technology to lower technical risk, prioritizing systems with proven performance over untested designs.OKLO also signed a long-term power supply agreement with META. Per the agreement, OKLO will supply nearly 1.2 gigawatts to meet the energy demand from Meta’s large-scale data centers. This Zacks Rank #3 stock has developed the Aurora Powerhouse reactor, having a maximum power generation capacity of 75 MW.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ameren Corporation (AEE) : Free Stock Analysis Report

NextEra Energy, Inc. (NEE) : Free Stock Analysis Report

BHP Group Limited Sponsored ADR (BHP) : Free Stock Analysis Report

Vistra Corp. (VST) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report

Oklo Inc. (OKLO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

This article first appeared on GuruFocus.

Rio Tinto (NYSE:RIO) and BHP (NYSE:BHP) are coming together for one of their biggest collaborations in years, agreeing to jointly tap up to 200 million tonnes of iron ore in Western Australia's Pilbara region.

The two miners signed non binding agreements to look at developing neighboring deposits and sharing infrastructure across their Yandicoogina and Yandi operations. Instead of spending heavily on new projects, the focus is on getting more out of what's already there, including potentially developing Rio Tinto's Wunbye deposit and processing ore from BHP's Yandi Lower Channel through Rio's existing wet plants.

- Warning! GuruFocus has detected 9 Warning Signs with RIO.

- Is RIO fairly valued? Test your thesis with our free DCF calculator.

Executives from both companies framed the move as a practical response to rising costs and declining ore grades across the Pilbara. Rio Tinto iron ore chief Matthew Holcz said the partnership allows both sides to unlock extra production with minimal capital spending, while BHP's Tim Day called it a clear example of productivity gains through cooperation.

The Pilbara remains one of the world's most important iron ore regions, supplying steelmakers across Asia. The tie up also builds on a 2023 agreement that opened up mining along a shared boundary that was previously off limits, showing how rivals are finding common ground as industry pressures grow.

Coeur Mining, Inc. CDE has gained 235.7% over the past year compared with the Zacks Mining-Non Ferrous industry’s 85.9% increase and the S&P 500’s 20% rise.

Among its peers, Southern Copper Corporation SCCO and Lundin Mining Corporation LUNMF have risen 85.1% and 188.1%, respectively.

Price Performance CDE vs. Industry, S&P 500, SCCO & LUNMFZacks Investment Research

Image Source: Zacks Investment Research

Technical indicators show that CDE has been trading above its 50-day and 200-day simple moving averages (SMA). The 50-day SMA is reading higher than the 200-day SMA, indicating a bullish trend.

Zacks Investment Research

Image Source: Zacks Investment Research

Let’s look at the CDE’s fundamentals to analyze the stock better.

CDE’s Multi-Mine Strength Drives Strong Q3

Coeur Mining reported consolidated revenues of roughly $555 million for the third quarter of 2025, which represented a substantial 77 % year-over-year increase. This jump was driven by higher realized metal prices, increased sales volumes and balanced contributions from each of the company’s five wholly owned North American gold and silver operations.

Coeur Mining’s diversified North American portfolio, which spans the Las Chispas silver-gold mine in Sonora, the Palmarejo gold-silver complex in Chihuahua, the Rochester silver-gold mine in Nevada, the Kensington gold operation in Alaska and the Wharf gold mine in South Dakota, was a key driver of its strong quarterly results. The company noted that revenue contributions were evenly spread across these five assets, with Palmarejo generating about 23%, Kensington 22%, Rochester 20%, Wharf 18% and Las Chispas roughly 17% of total third-quarter revenues.

This balanced operational mix allowed Coeur Mining to fully capitalize on higher metal prices and robust production levels across multiple regions, leading to better operational execution, reduced reliance on any single asset and reinforced the company’s overall growth trajectory across its North American footprint.

Cash Surge and Deleveraging Fuel Coeur Mining’s Momentum

The company’s financial transformation underpins a more resilient business model, deleveraging rapidly while still funding growth and returning capital. Coeur Mining ended the third quarter with a significantly strengthened financial footing, holding $266.3 million in cash and equivalents, more than double its previous quarter's balance.

Coeur Mining generated $237.7 million in cash flow from operating activities during the third quarter, a strong increase from $206.95 million in the previous quarter. This robust operating cash flow forms a foundation for Coeur’s capital deployment strategy, supporting capex, debt repayment and its shareholder return initiatives.

CDE repaid more than $228 million of debt during the first nine months of 2025, reducing its total debt to $363.5 million and bringing its net-leverage ratio down to a very conservative 0.1X.

Coeur Mining invested $49 million in capital expenditures in the third quarter, of which about 70% was allocated to sustaining capex and 30% toward development projects. On the exploration front, the company spent $30 million, with $25 million expensed and $5 million capitalized, signaling a dual focus on reserve maintenance and future growth.

The cash cushion not only provides flexibility for further expansion but also reduces risk in a volatile commodity price environment.

CDE’s Growth Projects Set Up Next Revenue Expansion

The Rochester silver-gold mine in Nevada remains one of Coeur Mining’s most important growth engines. A major expansion project completed over the past few years has significantly increased the mine’s throughput capacity, with the new Stage VI leach pad and enhanced crushing circuit now in commercial production.

Coeur Mining’s acquisition of Las Chispas brought a high-grade, low-cost silver-gold asset into its portfolio early in 2025, contributing meaningfully to production and top-line results, including in the third quarter. Las Chispas’ strong performance has enhanced the overall production mix and cash flow and is expected to continue supporting revenue growth as the asset is fully integrated and optimized.

Coeur Mining is executing one of its largest exploration programs to date, with substantial drilling underway at Palmarejo, Kensington, Wharf, Rochester and Las Chispas, aimed at extending mine lives, improving grades and expanding reserves. The company announced a commitment of $67-$77 million for the same.

At the Silvertip project in British Columbia, Coeur Mining has more than tripled its land position and is undertaking expanded drilling programs aimed at increasing understanding of this polymetallic deposit. Early indicators suggest the potential for significant future resource additions.

What CDE’s Estimate Revisions Indicate

The Zacks Consensus Estimate for 2025 and 2026 for CDE has been revised lower and higher, respectively, over the past 60 days.

Zacks Investment Research

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CDE’s 2025 earnings is currently pegged at 76 cents per share, suggesting year-over-year growth of 322.2%.

Zacks Investment Research

Image Source: Zacks Investment Research

Coeur Trading Above Industry

Coeur Mining is currently trading at a forward 12-month price-to-sales multiple of 4.96X, above the industry’s average of 4.84X.

Zacks Investment Research

Image Source: Zacks Investment Research

The forward 12-month price-to-sales multiples for Southern Copper and Lundin Mining are 10.14X and 5.16X, respectively. CDE, SCCO and LUNMF currently have a Value Score of D, each.

Final Thought: Buy CDE Shares

Coeur Mining is transitioning into a breakout phase marked by accelerating revenue, surging cash flow and one of the industry’s fastest deleveraging cycles. Balanced contributions from strong-performing mines and a cash balance that has more than doubled in the last reported quarter signal a business firing on all cylinders. Rochester’s ramp-up, Las Chispas’ high-grade boost and a large exploration push position Coeur Mining for meaningful production and cash-flow growth, reinforced by better fundamentals, rising metal prices and a much stronger balance sheet. CDE is emerging as one of the most compelling high-upside plays in the North American mining sector, a standout pick for investors looking for powerful leverage to the next surge in gold and silver.

CDE currently carries a Zacks Rank of #1 (Strong Buy) You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Southern Copper Corporation (SCCO) : Free Stock Analysis Report

Coeur Mining, Inc. (CDE) : Free Stock Analysis Report

Lundin Mining Corp. (LUNMF) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Southern Copper (SCCO) closed the most recent trading day at $182.97, moving +1.5% from the previous trading session. This change outpaced the S&P 500's 0.26% gain on the day. Meanwhile, the Dow experienced a rise of 0.6%, and the technology-dominated Nasdaq saw an increase of 0.25%.

Heading into today, shares of the miner had gained 27.44% over the past month, outpacing the Basic Materials sector's gain of 8.62% and the S&P 500's gain of 1.57%.

The upcoming earnings release of Southern Copper will be of great interest to investors. The company is expected to report EPS of $1.44, up 42.57% from the prior-year quarter. Alongside, our most recent consensus estimate is anticipating revenue of $3.62 billion, indicating a 30.11% upward movement from the same quarter last year.

Regarding the entire year, the Zacks Consensus Estimates forecast earnings of $5.3 per share and revenue of $13.17 billion, indicating changes of +22.4% and 0%, respectively, compared to the previous year.

It's also important for investors to be aware of any recent modifications to analyst estimates for Southern Copper. Such recent modifications usually signify the changing landscape of near-term business trends. Therefore, positive revisions in estimates convey analysts' confidence in the business performance and profit potential.

Based on our research, we believe these estimate revisions are directly related to near-term stock moves. To take advantage of this, we've established the Zacks Rank, an exclusive model that considers these estimated changes and delivers an operational rating system.

The Zacks Rank system, ranging from #1 (Strong Buy) to #5 (Strong Sell), possesses a remarkable history of outdoing, externally audited, with #1 stocks returning an average annual gain of +25% since 1988. Within the past 30 days, our consensus EPS projection has moved 1.83% higher. Southern Copper presently features a Zacks Rank of #3 (Hold).

From a valuation perspective, Southern Copper is currently exchanging hands at a Forward P/E ratio of 28.85. This represents a premium compared to its industry average Forward P/E of 27.92.

Investors should also note that SCCO has a PEG ratio of 1.51 right now. Comparable to the widely accepted P/E ratio, the PEG ratio also accounts for the company's projected earnings growth. The Mining – Non Ferrous was holding an average PEG ratio of 0.74 at yesterday's closing price.

The Mining – Non Ferrous industry is part of the Basic Materials sector. With its current Zacks Industry Rank of 20, this industry ranks in the top 9% of all industries, numbering over 250.

The Zacks Industry Rank evaluates the power of our distinct industry groups by determining the average Zacks Rank of the individual stocks forming the groups. Our research shows that the top 50% rated industries outperform the bottom half by a factor of 2 to 1.

Don't forget to use Zacks.com to keep track of all these stock-moving metrics, and others, in the upcoming trading sessions.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Southern Copper Corporation (SCCO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Thursday, January 15, 2026The Zacks Research Daily presents the best research output of our analyst team. Today's Research Daily features new research reports on 16 major stocks, including American Express Co. (AXP), Intuitive Surgical, Inc. (ISRG) and Booking Holdings Inc. (BKNG), as well as two micro-cap stocks Daily Journal Corp. (DJCO) and Star Group, L.P. (SGU). The Zacks microcap research is unique as our research content on these small and under-the-radar companies is the only research of its type in the country.These research reports have been hand-picked from the roughly 70 reports published by our analyst team today.You can see all of today’s research reports here >>>Ahead of Wall StreetThe daily 'Ahead of Wall Street' article is a must-read for all investors who would like to be ready for that day's trading action. The article comes out before the market opens, attempting to make sense of that morning's economic releases and how they will affect that day's market action. You can read this article for free on our home page and can actually sign up there to get an email notification as this article comes out each morning.You can read today's AWS here >>> Pre-Markets Positive on Healthy Economic PrintsToday's Featured Research ReportsAmerican Express’ shares have outperformed the Zacks Financial – Miscellaneous Services industry over the past six months (+15.4% vs. -16%). The company is benefiting from sustained revenue growth driven by new product launches, strategic partnerships and a rebound in travel and entertainment spending. Revenues rose 9% YoY in the first nine months of 2025. Strong cash generation and disciplined capital returns underscore its financial strength. Its ROE of 33.4% lies above the industry average. It returned $2.9 billion in 3Q alone, through dividends and buybacks. Its focus on increasing tech-savvy customers positions it for long-term growth. However, persistently rising expenses continue to weigh on margins. Loan loss provisions remain elevated due to macro uncertainty. It is less agile in capitalizing on emerging non-card-based payment trends. AXP carries a heavy debt load, which induces the incurrence of high interest expenses. As such, the stock warrants a cautious stance.(You can read the full research report on American Express here >>>)Shares of Intuitive Surgical’s have gained +6.6% over the past six months against the Zacks Medical – Instruments industry’s gain of +11.6%. The company delivered a strong third-quarter, beating revenue and EPS estimates. The da Vinci 5 system gained momentum with 240 U.S. placements, raising its installed base to 929, alongside approvals in Europe and Japan for phased rollout. Utilization surpassed the Xi platform, supported by force feedback and Case Insights, while rising trade-ins highlighted upgrade demand. Global procedures grew 19% year over year, with 16% growth in the U.S. and 24% OUS, driven by benign general and non-urology surgeries in India, Korea, and distributor markets. System placements totaled 427, showing strong demand. However, gross margin slipped on higher costs and tariffs, while OUS markets remain pressured by budget constraints. Medicaid policy uncertainty is a risk, but ISRG raised 2025 growth guidance to 17–17.5% and margins to 67–67.5%.(You can read the full research report on Intuitive Surgical here >>>)Booking’s shares have gained +7.1% over the past year against the Zacks Internet – Commerce industry’s gain of +11.1%. The company benefits from its global footprint, strong brands and growing shift toward direct-channel bookings, which support margins and customer loyalty. Expansion into alternative accommodations, transport and attractions, alongside the Connected Trip strategy and increased GenAI integration, boosts engagement and cross-selling. Strong liquidity, solid cash generation and deep partner relationships further reinforce its position. Additionally, its focus on automating partner tools and traveler interactions enhances operational efficiency and satisfaction. However, softness in U.S. travel trends, elevated marketing spend and rising competitive pressure pose challenges. Its limited domestic presence may also restrict growth as affordability trends impact pricing power, and it faces strong competition from online travel agencies.(You can read the full research report on Booking here >>>)Shares of Daily Journal have outperformed the Zacks Publishing – Newspapers industry over the past six months (+61.8% vs. +35.5%). This microcap company with a market capitalization of $894.14 million has its shareholder value anchored by a $493 million marketable securities portfolio, which delivered $134.3 million in unrealized gains in FY25. Despite the passing of Charles Munger, the board continues to conservatively manage these assets, providing liquidity without external capital needs. Journal Technologies is accelerating, with FY25 revenues rising 32% YoY to $69.9 million and pretax income rising to $12.7 million, fueled by demand for e-filing and milestone-based contracts. The company’s capital-light model, $500.4 million in working capital, and positive $13.3 million operating cash flow support reinvestment. While growth is robust, risks include government revenue timing, rising competition in justice tech, and legal ad revenue headwinds from legislative changes. Underutilized real estate also weighs on efficiency. DJCO trades at 4.57X EV/sales and 2.29X P/B, below sector medians. (You can read the full research report on Daily Journal here >>>)Star Group’s shares have gained +9.4% over the past six months against the Zacks Electronics – Miscellaneous Products industry’s gain of +25.9%. This microcap company with a market capitalization of $403.63 million is a consolidator in a fragmented Northeast/Mid-Atlantic heating oil and propane market, using tuck-in M&A to build route density, lift efficiency and strengthen margins. Management has shown an ability to protect profitability through pricing discipline, cost control and effective integration, while expanding HVAC services to diversify revenues, deepen customer relationships and provide a counter-seasonal earnings buffer. Capital allocation remains shareholder-friendly, yet flexible, and selective tech/AI adoption should improve service productivity and retention over time. Key risks center on persistent customer attrition and limited organic growth, weather-driven earnings volatility, rising fixed costs and financing burden tied to acquisitions, tighter cash-flow flexibility amid seasonal working-capital swings, and longer-term regulatory and electrification pressures in core markets.(You can read the full research report on Star Group here >>>)Other noteworthy reports we are featuring today include Southern Copper Corp. (SCCO), Fastenal Co. (FAST) and Take-Two Interactive Software, Inc. (TTWO).Mark VickerySenior EditorNote: Sheraz Mian heads the Zacks Equity Research department and is a well-regarded expert of aggregate earnings. He is frequently quoted in the print and electronic media and publishes the weekly Earnings Trends and Earnings Preview reports. If you want an email notification each time Sheraz publishes a new article, please click here>>>

Today's Must Read

AmEx (AXP) Aided by Strong Card Member Spending Amid High Costs

Intuitive Surgical's (ISRG) da Vinci System Helps Offset Risks

Booking Holdings Benefits From Strong Leisure Travel Demand

Featured Reports

High Prices Aid Southern Copper (SCCO), Lower Production AilThe Zacks analyst believes Southern Copper is poised well to gain on high copper and silver prices and its expansion actions. However lower production levels due to lower grades might impair results.

Sales Boosting Initiatives Aid Fastenal (FAST) Amid High CostsPer the Zacks analyst, Fastenal's prospects are gaining from accretive sales boosting initiatives and cost control efforts. However, a tepid macro scenario, high costs and seasonality return hurt.

TEVA's New Drugs and Generic Stability Are Reviving GrowthThe Zacks analyst believes newer drugs, Austedo and Ajovy as well as a stable generics business are reviving its top-line growth.

CardFree Acquisition Aids Fiserv (FISV) Amid High CompletionPer the Zacks Analyst, Fiserv's CardFree buyout improves Clover's capabilities to support small businesses as they grow into larger merchants. Rising competition from other players is an overhang.

SWP Demand, Buyouts, AUM Aid SEI Investments (SEIC), High Costs AilPer the Zacks analyst, rising demand for the SWP, solid assets under management balance, strategic buyouts and global presence will support SEI Investments' growth, while mounting expenses are a woe.

Expanding Customer Base, Steady Investment Aid Spire (SR)Per the Zacks analyst, Spire is seeing stronger demand from its increasing customer base. Infrastructure investments are enhancing service capacity and supporting improved profitability.

Product Refreshes Aid Sonos (SONO) Amid Weak Macro BackdropPer the Zacks analyst, Sonos is poised to gain from new product launches in the global audio market, while cautious consumer discretionary spending amid a weak macroeconomic environment is a woe.

New Upgrades

Strong Portfolio Aids Take Two (TTWO) Amid Stiff CompetitionPer the Zacks analyst, Take-Two's popular franchises including NBA 2K26 and Grand Theft Auto V is helping it to counter stiff competition from the likes of EA and Activision Blizzard.

Rapid Project Execution and Volume Growth Aids Cenovus Energy (CVE)Per the Zacks analyst, CVE's rapid project executions are expected to accelerate future cash flows. Its targeted upstream production growth through 2028 should further enhance profitability.

Diversified Business and SMBs Expansions Aid BILL Holdings (BILL)Per the Zacks Analyst, BILL Holdings is likely to gain from its diversified business model, expansions into the SMB ecosystem and the adoption of its AI-powered financial operations platform.

New Downgrades

Home Depot (HD) Pressured by Weak Discretionary Unit and High CostsPer Zacks analyst, Home Depot sees softness in big-ticket and discretionary categories. It witnesses margin pressures driven by operating expense deleverage and costs related to the GMS acquisition.

China's slowdown and tariff risks hurt Philips (PHG) prospectsPer the Zacks analyst, Philips suffers from a sharp China slowdown and tariff uncertainties, which are affecting segment growth and limiting near-term upside.

Bath and Body Works (BBWI) Faces Demand Weakness and Margin PressurePer the Zacks analyst, BBWI continues to grapple with broad demand softness, heavier promotions and tariff pressures, signaling prolonged margin and growth challenges.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fastenal Company (FAST) : Free Stock Analysis Report

American Express Company (AXP) : Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG) : Free Stock Analysis Report

Take-Two Interactive Software, Inc. (TTWO) : Free Stock Analysis Report

Southern Copper Corporation (SCCO) : Free Stock Analysis Report

Star Group, L.P. (SGU): Free Stock Analysis Report

Daily Journal Corp. (S.C.) (DJCO): Free Stock Analysis Report

Booking Holdings Inc. (BKNG) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Investors interested in Mining – Miscellaneous stocks are likely familiar with Nexa Resources S.A. (NEXA) and Teck Resources Ltd (TECK). But which of these two companies is the best option for those looking for undervalued stocks? Let's take a closer look.

We have found that the best way to discover great value opportunities is to pair a strong Zacks Rank with a great grade in the Value category of our Style Scores system. The Zacks Rank is a proven strategy that targets companies with positive earnings estimate revision trends, while our Style Scores work to grade companies based on specific traits.

Currently, Nexa Resources S.A. has a Zacks Rank of #2 (Buy), while Teck Resources Ltd has a Zacks Rank of #3 (Hold). This system places an emphasis on companies that have seen positive earnings estimate revisions, so investors should feel comfortable knowing that NEXA is likely seeing its earnings outlook improve to a greater extent. However, value investors will care about much more than just this.

Value investors are also interested in a number of tried-and-true valuation metrics that help show when a company is undervalued at its current share price levels.

The Style Score Value grade factors in a variety of key fundamental metrics, including the popular P/E ratio, P/S ratio, earnings yield, cash flow per share, and a number of other key stats that are commonly used by value investors.

NEXA currently has a forward P/E ratio of 10.74, while TECK has a forward P/E of 28.43. We also note that NEXA has a PEG ratio of 0.31. This figure is similar to the commonly-used P/E ratio, with the PEG ratio also factoring in a company's expected earnings growth rate. TECK currently has a PEG ratio of 0.57.

Another notable valuation metric for NEXA is its P/B ratio of 1.25. The P/B ratio is used to compare a stock's market value with its book value, which is defined as total assets minus total liabilities. For comparison, TECK has a P/B of 1.34.

Based on these metrics and many more, NEXA holds a Value grade of A, while TECK has a Value grade of D.

NEXA sticks out from TECK in both our Zacks Rank and Style Scores models, so value investors will likely feel that NEXA is the better option right now.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Nexa Resources S.A. (NEXA) : Free Stock Analysis Report

Teck Resources Ltd (TECK) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

How much a stock's price changes over time is important for most investors, since price performance can both impact your investment portfolio and help you compare investment results across sectors and industries.

Another factor that can influence investors is FOMO, or the fear of missing out, especially with tech giants and popular consumer-facing stocks.

What if you'd invested in Teck Resources Ltd (TECK) ten years ago? It may not have been easy to hold on to TECK for all that time, but if you did, how much would your investment be worth today?

Teck Resources Ltd's Business In-Depth

With that in mind, let's take a look at Teck Resources Ltd's main business drivers.

Vancouver, Canada-based Teck Resources is committed to mining and mineral development with business units focused on copper and zinc. Teck is also a leading producer of lead and a significant producer of specialty metals such as germanium, indium and cadmium. It also produces gold dore and silver. Teck also produces industrial products and fertilizers, which are recovered from its zinc and lead smelting operations in Trail, B.C.

Teck Resources divested its Steelmaking Coal business or Elk Valley Resources (“EVR”) in July 2024. The company categorized it as discontinued operations and restated the revenue and EPS (in CAD) for all quarters of 2023 and for 2024.

Teck Resources is a significant copper producer in the Americas, with four operating mines in Canada, Chile and Peru, and development projects in North and South America. Its main projects are Highland Valley Copper in Canada and Antamina, Quebrada Blanca and Carmen de Andacollo in South America.

Teck Resources is one of the world's largest producers of mined zinc, with three operating mines in the United States and Peru, and it owns one of the world's largest fully integrated zinc and lead smelting and refining facilities located in Canada. Teck produces zinc concentrate from Red Dog Operations in Alaska. In addition to marketing its zinc concentrate around the world, the company’s concentrate team also purchases concentrate from other mines for processing at the Trail operations complex in British Columbia.Teck Resources recently announced a structure in two regional business units – The North America business and The Latin America (LATAM) business.

The North America business unit, includes Highland Valley Copper, Red Dog and Trail operations, and the Galore Creek, Schaft Creek, and New Range copper projects. The LATAM unit, includes Carmen de Andacollo and Quebrada Blanca operations, Teck’s interest in Antamina, and the Zafranal, San Nicolas, and NuevaUnión copper growth projects.In September 2025, Teck Resources entered the merger agreement with Anglo American to form the Anglo Teck group. The new company will boast an industry-leading portfolio, consisting of six world-class copper assets, and premium iron ore and zinc operations.

Bottom Line

Anyone can invest, but building a successful investment portfolio takes a combination of a few things: research, patience, and a little bit of risk. So, if you had invested in Teck Resources Ltd a decade ago, you're probably feeling pretty good about your investment today.

According to our calculations, a $1000 investment made in January 2016 would be worth $17,335.55, or a gain of 1,633.55%, as of January 15, 2026, and this return excludes dividends but includes price increases.

Compare this to the S&P 500's rally of 260.42% and gold's return of 313.45% over the same time frame.

Going forward, analysts are expecting more upside for TECK.

Teck Resources reported third-quarter 2025 copper output of around 104,100 tons, a 9.5% decline year over year due to lower-than-expected results at QB and HVC. Ongoing TMF development work is expected to impact production at QB. The company lowered the 2025 copper production guidance to 415,000-465,000 tons, suggesting a 1% dip at the midpoint. Also, due to the outage of the shiploader at QB's port facility, net cash unit costs at QB are expected to be higher than before. Copper prices have gained lately on supply concerns amid solid demand. The long-term prospects for copper remain positive, supported by the clean energy transition trend. Teck Resources entered into a merger agreement with Anglo American plc to form the Anglo Teck group, with a combined annual copper production of 1.2 million tons.

The stock has jumped 17.92% over the past four weeks. Additionally, no earnings estimate has gone lower in the past two months, compared to 6 higher, for fiscal 2025; the consensus estimate has moved up as well.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Teck Resources Ltd (TECK) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Vancouver, British Columbia–(Newsfile Corp. – January 15, 2026) – Corcel Exploration Inc. (CSE: CRCL) (OTCQB: CRLEF) (the "Company" or "Corcel") today announced that Grant Tanaka has been appointed Chief Financial Officer of the Company to replace Kyle Nazareth. Corcel thanks Mr. Nazareth for his contributions and dedication to the Company and wishes him continued success in his future endeavors.

Mr. Tanaka brings over 15 years of financial leadership experience in the mining industry. Grant is the Chief Financial Officer of Vizsla Royalties Corp. and Vizsla Copper Corp. and was a Director, Finance Operations, of Ma'aden Gold & Base Metals Co. Prior to this, he held senior financial positions at Teck Resources Limited, New Gold Inc., Copper Mountain Mining Corporation, and Bisha Mining Share Company, an operating subsidiary of Nevsun Resources Ltd. He has experience at both the corporate and operational levels, having worked throughout North America, Africa and the Middle East in gold, base metals and coal operations.

"We are excited to welcome Grant as our new Chief Financial Officer," commented Corcel CEO, Jon Ward. "Grant brings strong financial leadership and public company experience that will be instrumental as we continue to advance our exploration strategy and position the Company for future growth."

Stock Option Grant

Corcel has granted a total of 2,220,000 stock options ("Options") to directors, officers, employees and consultants of the Company, with each Option exercisable at a price of $0.265 to acquire one common share of the Company until January 15, 2031 and having vested immediately.

About Corcel Exploration Inc.

Corcel is a mineral resource company engaged in the acquisition and exploration of precious and base metals properties throughout North America. The Company has entered a long-term lease agreement to acquire the Yuma King Copper-Gold project in Arizona, which spans a district-scale land position of 3,200 hectares comprising 515 unpatented federal mining claims in the Ellsworth Mining District, including the past-producing Yuma Mine which saw underground production of copper, lead, gold and silver between 1940 and 1963. The Company also holds an option to acquire a 100% undivided right, title, and interest in and to the Peak gold exploration project and holds a 100% interest in the Willow copper project. For more information, please visit our website at https://corcelexploration.com/.

For further information contact:

Jon Ward, CEOEmail: info@corcelexploration.comTel: (604) 355-0303

Caution Regarding Forward-Looking Information

This news release contains "forward‐looking information" and "forward-looking statements" under applicable Canadian and U.S. securities laws (collectively, "forward‐looking statements"). These statements relate to future events or the Company's future performance, business prospects or opportunities that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management made in light of management's experience and perception of historical trends. Assumptions may prove to be incorrect and actual results and future events may differ materially from those anticipated. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives or future events or performance (often, but not always, using words or phrases such as "seek", "anticipate", "plan", "continue", "estimate", "expect", "may", "will", "project", "predict", "forecast", "potential", "target", "intend", "could", "might", "should", "believe" and similar expressions) are not statements of historical fact and may be "forward‐looking statements".

Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause actual results to materially differ from those expressed or implied by such forward-looking statements, including but not limited to: material adverse changes, unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts with the company to perform as agreed; social or labour unrest; changes in commodity prices; and the failure of exploration programs or studies to deliver anticipated results or results that would justify and support continued exploration, studies, development or operations. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. The Company believes that the expectations reflected in these forward‐looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward‐looking statements included herein should not be unduly relied upon. These statements speak only as of the date hereof. The Company does not intend, and does not assume any obligation, to update these forward-looking statements, except as required by applicable laws.

Neither the Canadian Securities Exchange nor the Market Regulator (as that term is defined in the policies of the Canadian Securities Exchange) accepts responsibility for the adequacy or accuracy of this release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/280478

How much a stock's price changes over time is important for most investors, since price performance can both impact your investment portfolio and help you compare investment results across sectors and industries.

FOMO, or the fear of missing out, also plays a role in investing, particularly with tech giants and popular consumer-facing stocks.

What if you'd invested in Southern Copper (SCCO) ten years ago? It may not have been easy to hold on to SCCO for all that time, but if you did, how much would your investment be worth today?

Southern Copper's Business In-Depth

With that in mind, let's take a look at Southern Copper's main business drivers.

Phoenix, AZ-based Southern Copper Corporation engages in mining, exploring, smelting, and refining copper and other minerals. The company conducts exploration activities in Argentina, Chile, Ecuador, Mexico and Peru.

Southern Copper has the largest copper reserves in the industry and operates high-quality, world-class assets in investment grade countries, such as Mexico and Peru.

Southern Copper reports results under three reportable segments. Each consist of a groups of mines with similar economic characteristics, type of products, processes and support facilities, regulatory environments as well as employee bargaining contracts.Peruvian operations (around 36% of the company's revenues) includes the Toquepala and Cuajone mine complexes and the smelting and refining plants, industrial railroad and port facilities that service both mines. The Peruvian operations produce copper, with significant by-product production of molybdenum, silver and other materials.Mexican Open-Pit (58% of revenues) includes La Caridad and Buenavista mine complexes, the smelting and refining plants and support facilities, which service both mines. The Mexican open pit operations produce copper, with significant by-product production of molybdenum, silver and other materials.Mexican underground operations (6% of revenues) (IMMSA unit) includes five underground mines that produce zinc, lead, copper, silver and gold, a coal mine which produces coal and coke, and several industrial processing facilities for zinc, copper and silver.

The geographic breakdown of the company’s sales is as follows – Americas (50% of revenues), Europe (32%) and Asia (18%).Approximately 80% of the company’s revenue come from the sale of copper, 6% from molybdenum and 10% from silver and zinc.

Bottom Line

Putting together a successful investment portfolio takes a combination of research, patience, and a little bit of risk. For Southern Copper, if you bought shares a decade ago, you're likely feeling really good about your investment today.

According to our calculations, a $1000 investment made in January 2016 would be worth $7,775.00, or a gain of 677.50%, as of January 14, 2026, and this return excludes dividends but includes price increases.

Compare this to the S&P 500's rally of 268.40% and gold's return of 309.27% over the same time frame.

Analysts are anticipating more upside for SCCO.

Southern Copper's performance is set to benefit from ongoing strength in metal prices. Increased output of silver, zinc and molybdenum is expected to largely offset a modest decline in copper production, although elevated operating costs remain a concern. Copper demand continues to be robust, supported by U.S. infrastructure spending and the global shift toward clean energy. An anticipated supply deficit should provide additional price support. The recent designation of copper and silver as critical minerals further highlights their strategic importance. Backed by extensive copper reserves and more than $15 billion in investments across Peru and Mexico over the decade, Southern Copper is well positioned for long-term growth. Its initiatives to reduce debt are also encouraging. The earnings estimates for the company have moved up lately.

Shares have gained 24.31% over the past four weeks and there have been 2 higher earnings estimate revisions for fiscal 2025 compared to none lower. The consensus estimate has moved up as well.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Southern Copper Corporation (SCCO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).