Unfortunately, investing is risky – companies can and do go bankrupt. But if you pick the right business to buy shares in, you can make more than you can lose. For example, the Metals X Limited (ASX:MLX) share price has soared 188% return in just a single year. Also pleasing for shareholders was the 70% gain in the last three months. On the other hand, longer term shareholders have had a tougher run, with the stock falling 73% in three years.

See our latest analysis for Metals X

Because Metals X made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually expect strong revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

In the last year Metals X saw its revenue grow by 3.2%. That's not a very high growth rate considering it doesn't make profits. In contrast, the share price took off during the year, gaining 188%. We're happy that investors have made money, though we wonder if the increase will be sustained. We're not so sure that revenue growth is driving the market optimism about the stock.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

A Different Perspective

It's good to see that Metals X has rewarded shareholders with a total shareholder return of 188% in the last twelve months. Notably the five-year annualised TSR loss of 9% per year compares very unfavourably with the recent share price performance. This makes us a little wary, but the business might have turned around its fortunes. It's always interesting to track share price performance over the longer term. But to understand Metals X better, we need to consider many other factors. Even so, be aware that Metals X is showing 2 warning signs in our investment analysis , you should know about…

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

KELOWNA, BC, April 19, 2021 /CNW/ – Metalex Ventures Ltd. (TSXV: MTX) (the "Company") is pleased to report that exceptionally anomalous amounts of ilmenite as well as highly anomalous scandium analyses of ilmenite-rich concentrates have been received for 22 of the 24 heavy mineral samples tested and collected on its 100% owned gold-scandium claims located 100km southeast of Chibougamau, Quebec.

These results are consistent with the claims being underlain by an extensive massive ilmenite horizon highly anomalous in scandium. Rio Tinto are presently mining an extensive massive ilmenite horizon near Allard Lake, Quebec. The ilmenite ore is railed 42km and then shipped about 900km along the St. Lawrence River to their Fer et Titane metallurgical complex near Montreal where titanium oxide, iron, steel and metal powders are recovered from the ilmenite ore. A plant to recover scandium from the ilmenite tailings is presently being constructed that is expected to produce 20% of the global scandium supply. Scandium is used primarily in the aerospace, automotive, military and 3D printing industries.

The Metalex claims are located adjacent to Highway 167, 520 kilometres by road from the Rio Tinto metallurgical complex.

Table 1, below, presents the results from the 0.25mm to 0.5mm sized heavy (> 3.27 specific gravity), weakly magnetic, conductive concentrate recovered from the sample. This concentrate should contain the vast majority of the ilmenite grains of this size fraction. For each sample, a representative split of the concentrate was picked, with the number of ilmenites within the sample extrapolated from this. The table contains the number of ilmenites (normalized to a 10kg sample size) along with the scandium content of the concentrate as determined by neutron activation analysis at Activation Laboratories.

Table 1. Ilmenite counts and scandium content of the 0.25mm to 0.5mm heavy, weakly magnetic, conductive concentrate.

|

Sample Name |

Picked ilmenites |

Scandium |

|

Normalized |

ppm |

|

|

RQ0571 |

7,694 |

41.3 |

|

RQ0722 |

127,702 |

19.6 |

|

RQ0723 |

13,446 |

26.8 |

|

RQ0724 |

46,007 |

31.0 |

|

RQ0725 |

154 |

53.1 |

|

RQ0751 |

83,629 |

29.1 |

|

RQ0752 |

8,609 |

32.4 |

|

RQ0753 |

6,213 |

25.6 |

|

RQ0754 |

9,299 |

56.4 |

|

RQ0755 |

8,382 |

34.4 |

|

RQ0756 |

68,668 |

22.9 |

|

RQ0757 |

26,022 |

29.5 |

|

RQ0760 |

43 |

57.8 |

|

RQ0765 |

56,726 |

27.4 |

|

RQ0766 |

402 |

49.8 |

|

RQ4076 |

275 |

39.1 |

|

RQ4077 |

84,010 |

31.9 |

|

RQ4078 |

142,754 |

24.2 |

|

RQ4079 |

2,243,805 |

31.9 |

|

RQ5046 |

81 |

53.5 |

|

RQ5047 |

56,564 |

28.3 |

|

RQ5048 |

17,375 |

33.0 |

|

RQ5049 |

2,627 |

42.3 |

|

RQ5050 |

60,157 |

30.0 |

According to Alexandsandrovsky et al., Ores and Metals Publishers, Moscow, 2004, about 2 million tons per year of ilmenite containing 10 to 20ppm scandium yields about 20 to 40 tons of scandium oxide. As seen in the table above, the ilmenite rich concentrates exceed these global ppm values.

Upon review of the Company's proprietary 8,698 regional heavy mineral samples database covering central Quebec ten samples were selected that also yielded anomalous scandium in the -0.25mm sized heavy, non-magnetic concentrates of these +/- 10kg samples. 0.25mm to 0.5mm, weakly magnetic, conductive concentrates (which would contain the bulk of the ilmenite grains) were prepared. Picking at CF Minerals using a binocular microscope of a portion of each concentrate yielded abundant ilmenites from seven of ten samples. These concentrates have also been submitted for neutron activation analysis for scandium and 33 other elements. Metalex awaits these results to see whether other areas in Quebec could also host scandium rich ilmenite.

Metalex directors are optimistic that an extensive ilmenite-rich body high in scandium will be discovered within the claims. A combined magnetic-electromagnetic survey is expected to commence over the claims within the next month which should provide drill targets.

The technical information and results reported here have been reviewed by Mr. Chad Ulansky P.Geol., a Qualified Person under National Instrument 43-101, who is responsible for the technical content of this release.

Signed,

Charles Fipke

Charles Fipke

Chairman

Forward Looking Statements

Some of the statements contained herein may be forward-looking statements which involve known and unknown risks and uncertainties. Without limitation, statements regarding potential mineralization and resources, exploration and financing results, and future plans and objectives of the Company are forward looking statements that involve various risks. The following are important factors that could cause the Company's actual results to differ materially from those expressed or implied by such forward looking statements: changes in the world wide price of mineral commodities, general market conditions, risks inherent in mineral exploration, risks associated with development, construction and mining operations, the uncertainty of future profitability and the uncertainty of access to additional capital. There can be no assurance that forward-looking statements will prove to be accurate as actual results and future events may differ materially from those anticipated in such statements. In particular there is no assurance that the Offering detailed herein will complete in full or at all. Metalex undertakes no obligation to update such forward-looking statements if circumstances or management's estimates or opinions should change. The reader is cautioned not to place undue reliance on such forward-looking statements.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

SOURCE Metalex Ventures Ltd.

View original content: http://www.newswire.ca/en/releases/archive/April2021/19/c6116.html

SUDBURY, ON / ACCESSWIRE / April 19, 2021 / Northern Superior Resources ("Northern Superior" or the "Company") (TSXV:SUP)(OCTQB:NSUPF) is pleased to announce that it has expanded its previously announced 10,000 meter ("m") core drill program on its 100% owned Lac Surprise property (see Northern Superior press release, March 15, 2021). The expanded Phase II drill program has been increased to a minimum of 13,000m, and will consist of two stages.

Stage 1, expanded to 8,000m, is designed to better define and expand the newly discovered Falcon Gold Zone, believed to be the western extension of the neighboring IAMGold/Vanstar's Nelligan gold deposit located approximately 2.4 kilometers ("km") to the east with an inferred resource* of 3.2 million ounces at 1.02 g/t gold ("Au") (see Figure 1).

Stage 2, consisting of approximately 5,000m, is designed to test three early-stage gold targets west of Target 1; Target 3; the Fox Gold showing and the Confluence Area (see Figure 2).

Stage 1: Target 1, Better Defining the Falcon Gold Zone

Based on the progress of the drill program to date the board has approved an expansion of the Stage 1 drill program on the Falcon Zone to 27 holes over 8,000m from its prior 16 holes over 5,000m. Eight holes (2,591m) of the now expanded 8,000m Stage 1 program have been completed. Five of the first eight holes have been processed with 1,134 samples submitted for assays, with material from another two holes expected to be delivered to the lab by the end of next week. These first eight holes cover a strike length of 450m from the property boundary near the first discovery hole of the Falcon Gold Zone (LCS20-13, 1.07 g/t gold equivalent ("AuEq")** over 35.5m with a high-grade interval of 8.22 g/t AuEq over 2.6m) to 150m west of the second discovery hole (LCS19-005ext., 1.55 g/t AuEq over 44.9m, including 3.82 g/t AuEq over 15m). Although most of these holes are relatively shallow (~250m), one deep hole has been completed (375m) while a second deep hole of (350m) is in progress currently. The expanded 27 hole program will test a potential strike length of approximately 900m.

Dr. T.F. Morris, President and CEO states: "We are very pleased with the drill progress made to date at Target 1, having learned much about the Falcon Gold Zone from the Fall 2020 drill program we have been able to apply this knowledge to the current program. The expanded Phase II drill program of 13,000 meters will allow us to fully define the full potential of this exciting new discovery for our shareholders.

We are also very excited to share details of our plans for Stage 2 of this program, having completed a thorough evaluation of highly prospective targets at Target 3, the Fox Gold Zone and the Confluence Area. In addition, initiating a drone magnetic survey over the central part of the property will provide high quality magnetic data, the same type of magnetic data used to assist in discovering the Falcon Gold Zone at Target 1 and defining the geophysical parameters associated with Target 3. This data will go a long way to refining drill targets in the Confluence area and the area directly to the south and west.

We look forward to sharing the progress and the results of these various initiatives on the Lac Surprise property as assays become available."

Stage 2: Target 3, Falcon Showing and the Confluence Area

Target 3

Target 3 is a compelling, large geophysical target located 7km west of the Nelligan gold deposit (see Figure 2). The geophysical signature of this target consists of a number of similarities to the Nelligan geophysical signature that led to the discovery of the Falcon Gold Zone. The geophysical attributes include:

-

A large, deeply rooted intrusion;

-

Associated with 60° faults; and

-

Associated large areas magnetic lows suggesting areas of silicification and alteration leading to magnetic destruction. There are three such large areas identified to the southeast (~4.0 x 1.0kms), northeast (~2.0 x 2.0kms) and northwest (~1.0km x 1.0km) of the proposed intrusion (Figure 3).

Our Initial Drilling on Target 3 will focus on the largest target to the southeast (4.0 x 1.0 kms) and will be tested with 3 core drill holes, each 400m long.

Fox Gold Showing

The Fox gold showing is located along the southwest part of the southeast area of Target 3. Unlike the targets associated with Target 3, the Fox showing is associated with a high magnetic signature suggesting an association with a more iron-rich environment. Gold-bearing material associated with this showing was collected from two channel samples (up to 6.76 g/t Au over 1.0m: Fox North showing; up to 2.95 g/t Au over 1.0m: Fox Showing) and grab samples from SOQUEM trenches (up to 900 ppb Au; ref. GM49908)(see Figure 4).

Four drill holes for a total of approximately 1,000m is currently proposed to test this target.

Confluence Area

The Confluence is an area where two prominent deformation zones converge (Remick and Doda: the "Confluence Area"; see Figure 2). This area contains a prominent gold grain dispersal train (maximum 49 gold grains, 10 kilogram ("kg") till sample). A 10kg stream sediment sample just west and at the intersection of two faults yielded 107 gold grains. This area also has a gold showing with a grab sample that assayed 1.35 g/t Au.

To test the prospectivity for gold mineralization in this area, three targets were selected based on a careful evaluation of the Company's Induced Polarization geophysical data, distribution of gold grain data and historical drilling (see Figure 5).

These targets will be tested with 5 drill holes, each 300m in length.

Drone Magnetic Survey

Northern Superior is also pleased to announce that it has initiated a 954 line-kilometer, 50m spaced, drone magnetic survey over the central part of the property (see Figure 6). The geophysical product derived from this program will be the same high-quality data used to identify the geophysical properties associated with the Falcon Gold Zone discovered in Target Area 1 and the geophysical properties associated with Target 3. The data will also be used to refine targets in the Confluence Area and the area to the south and southwest of the Confluence Area.

* Reference for IAMGOLD/Vanstar's Nelligan 3.2MM Inferred Gold Resource: "Carrier, Alain (M.Sc., P.Geo); Nadeau-Benoit, Vincent (P.Geo); Fauvre, Stéphane (PhD., P.Geo). October 22, 2019. NI 43-101 Technical Report and Initial Resource Estimate for the Nelligan Project, Québec, Canada."

** Gold equivalent grades calculated based on a 75 Au:Ag factor ratio.

Qualified Person

Michel Leblanc (P.Geo.) is a Qualified Person ("QP") within the meaning of National Instrument 43-101. Mr. Leblanc has reviewed, and approved information disclosed in this press release. Michael Leblanc, who is also a Qualified Person ("QP") will be overseeing the core drill program.

Note to readers: Mineralization hosted on adjacent and/or nearby properties is not necessarily indicative of mineralization hosted on the Company's property.

About Northern Superior Resources Inc.

The Lac Surprise gold property is one of three key mineral properties 100% owned by Northern Superior Resources. The other two properties (TPK and Croteau Est) also represent regional scale exploration opportunities (see Northern Superior Corporate Presentation, www.nsuperior.com).

Northern Superior is a reporting issuer in British Columbia, Alberta, Ontario and Québec, and trades on the TSX Venture Exchange under the symbol SUP, and the OTCQB Venture Market under the symbol NSUPF.

For Further Information

Please refer to Northern Superior news available on the Company's website (www.nsuperior.com) and on SEDAR (www.sedar.com) or contact:

Thomas F. Morris P.Geo., PhD., FGAC

President and CEO

Tel: (705) 525 ‐0992

Fax: (705) 525 ‐7701

e‐mail: info@nsuperior.com

Cautionary Note Regarding Forward-Looking Statements

This Press Release contains forward-looking statements that involve risks and uncertainties, which may cause actual results to differ materially from the statements made. When used in this document, the words "may", "would", "could", "will", "intend", "plan", "anticipate", "believe", "estimate", "expect" and similar expressions are intended to identify forward-looking statements. Such statements reflect our current views with respect to future events and are subject to such risks and uncertainties. Many factors could cause our actual results to differ materially from the statements made, including those factors discussed in filings made by us with the Canadian securities regulatory authorities. Should one or more of these risks and uncertainties, such actual results of current exploration programs, the general risks associated with the mining industry, the price of gold and other metals, currency and interest rate fluctuations, increased competition and general economic and market factors, occur or should assumptions underlying the forward looking statements prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, or expected. We do not intend and do not assume any obligation to update these forward-looking statements, except as required by law. Shareholders are cautioned not to put undue reliance on such forward-looking statements.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Figure 1: Phase II Stage I core drill plan, Target Area 1.

Figure 2: Location of Target 3, the Fox Showing and the Confluence area.

Figure 3: Target Area 3, surface expression. Note the three deep blue areas representing the large areas of potential alteration zones in addition to the large intrusive complex (potential heat source) and structural environment.

Figure 4: Geophysical signature and gold showings associated with the Fox Gold Showing.

Figure 5. Three target areas to be tested associated with the Confluence Area, drill collars and traces. Each drill hole will be ~300m long.

Figure 6. Areas covered by the ongoing Drone magnetic survey, total of 954km of flight lines at 50m spacing. Data will be the same high-quality data derived from the drone survey completed in 2019 used to help define the Falcon Gold Zone, target Area 1 and the geophysical properties associated with target Area 3. Same data will also refine targeting in the Confluence Area and the area to the south and south west.

SOURCE: Northern Superior Resources Inc.

View source version on accesswire.com:

https://www.accesswire.com/640777/Northern-Superior-Announces-Progress-Update-and-Expansion-of-Phase-II-Drill-Program-at-Lac-Surprise-to-a-Minimum-of-13000-Meters

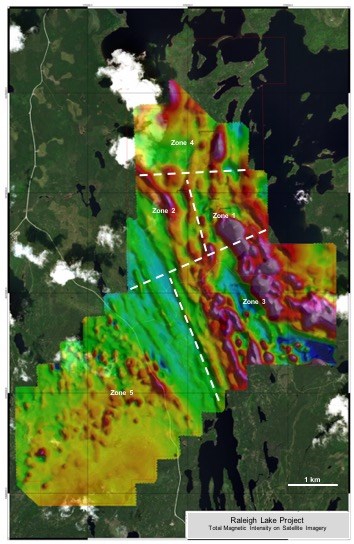

Vancouver, British Columbia–(Newsfile Corp. – April 19, 2021) – International Lithium Corp. (TSXV: ILC) (the "Company" or "ILC") is pleased to announce that the Company has completed a maiden diamond drilling program on the Raleigh Lake Lithium project near Ignace, Ontario, Canada. A total of 1,504 metres of NQ core drilling were completed in eight holes to test the continuity of spodumene bearing pegmatites and their associated lithium, tantalum and cesium mineralization down dip and along strike from outcrop and previous operators' drilling.

The royalty-free, 100-percent-owned Raleigh Lake project comprising a total of 3,027 hectares hosts a number of outcropping pegmatite bodies. The recent drilling focused on what the Company now refers to as Zone 1 (Figure 1), an area of approximately one square kilometre (100 hectares) that hosts Pegmatites 1 and 3. The two shallow dipping pegmatite dykes have been mapped at surface with Pegmatite 1 exposed along strike for at least 300 metres and intersected 400 metres downdip by drilling conducted prior to ILC's drilling campaign. Seven of ILC's eight widely dispersed holes, covering an area approximately 600 x 300 metres, intersected pegmatite.

The core has been logged and cut with samples submitted for chemical analysis. Assay results are expected by mid-May.

Logistics of the drill program were excellent as the project is road accessible and is just a short distance from the Trans-Canada Highway. The Raleigh project is located less than 20 kilometres directly west of the Township of Ignace, Ontario. It distinguishes itself from other lithium projects in Canada by being very well situated near to major public infrastructure; the Trans-Canada Highway, with direct access to Thunder Bay on Lake Superior, is less than six kilometres north of the project as is the mainline of the Canadian Pacific Railway, natural gas pipelines, and the hydro power line junction at Raleigh Lake. By having relatively easy access to public services coupled with no need to spend significant sums of money on building new roads or electric power lines to service the site nor buildings to house contractors, the Raleigh project posesses a substantial advantage over more remote mining projects.

With the drilling taking place exclusively in Zone 1, which is within one kilometre of the historic drilling, there are no results yet for Zones 2 to 5. These additional zones include claims acquired by ILC in 2016 and 2018 and include some with surface pegmatite exposures. ILC intends to carry out wider drilling in various phases on Zones 2 to 5 as targets are prioritized in these areas.

John Wisbey, Chairman and CEO of International Lithium Corp. commented "This was an encouraging drilling program for ILC with what appear to be good and solid results in Raleigh Lake Zone 1 that build significantly on our confidence of the project's potential. If the chemical analysis received over the next few weeks is favourable, that may well be sufficient to warrant follow-up with some preliminary economic analyses prior to further drilling in Zone 1. The board also believes that investment in further drilling in Zones 2 to 5 is highly warranted and remains hopeful, based on earlier geological analysis, that it could deliver even greater potential than we are defining at Zone 1."

Quality assurance/quality control procedures

International Lithium Corp. has implemented a rigorous quality assurance/quality control program to ensure best practices in sampling and analysis of diamond drill core. All assays are performed by Activation Laboratories Ltd. (ActLabs), with sample preparation and analysis carried out in their full-service facility in Dryden, Ontario. Sample preparation involves crushing the entire sample to 80% passing 2 mm, riffle split 250g and pulverize to 95% passing 105 µm.

Primary analysis method: Peroxide (Total) Fusion, ICP-OES & ICP-MS with 55 elements including Li (3ppm – 5%). Sodium peroxide fusion provides total metal recovery and is effective for the decomposition of sulphides and refractory minerals.

Over limit analysis method: If Li >5%, then re-analyse by Assay Grade, Peroxide (Total) Fusion, including Li from 0.01%.

The drill program was under the control of a Professional Geoscientist, registered with The Association of Engineers and Geoscisntists of the Province of British Columbia.The Company and its contractors carried out the program under full compliance with COVID-19 protocols based on guidelines issued by the Provincial Health Officer (PHO) of British Columbia to ensure the safety and health, for all personnel.

Qualified person

Patrick McLaughlin, P.Geo, a "Qualified Person" as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects has reviewed and approved the technical information in this press release.

Figure 1: Total magnetic intensity image over the mineral claim outline divided into five Zones for various staged exploration activities at the Raleigh Lake Lithium project.

To view an enhanced version of Figure 1, please visit:

https://orders.newsfilecorp.com/files/3232/80715_8c2d9e82c48ab894_003full.jpg

About International Lithium Corp.

International Lithium Corp. believes that the '20s will be the decade of battery metals, at a time that the world faces a major turning point in the energy market's dependence on oil and gas and in the governmental and public view of climate change. Our key mission in the new decade is to make money for our shareholders from lithium and battery metals while at the same time helping to create a greener, cleaner planet. This includes optimizing the value of our existing projects in Canada, Argentina and Ireland as well as finding, exploring and developing projects that have the potential to become world class lithium and rare metal deposits. In addition, we have seen the clear and growing wish by the USA and Canada to safeguard their supplies of critical battery metals, and our Canadian properties are strategic in that respect.

A key goal in the new decade is to become a well funded company to turn our aspirations into reality.

International Lithium Corp. has a significant portfolio of projects, strong management, and strong partners. Partners include Ganfeng Lithium Co. Ltd., ("Ganfeng Lithium") a leading China-based lithium product manufacturer quoted on the Shenzhen and Hong Kong stock exchanges (A share code: 002460, H share code: 1772) and Essential Metals Limited, quoted on the Australian Stock exchange.

The Company's primary strategic focus is now on the Mariana project in Argentina and on the Raleigh Lake project in Canada.

The Company has a strategic stake in the Mariana lithium-potash brine project located within the renowned South American "Lithium Belt" that is the host to the vast majority of global lithium resources, reserves and production. The Mariana project strategically encompasses an entire mineral rich evaporite basin, totalling 160 square kilometres, that ranks as one of the more prospective salars or 'salt lakes' in the region. Current ownership of the project is through a joint venture company, Litio Minera Argentina S. A., a private company registered in Argentina, now owned 89.0% by Ganfeng Lithium and 11.0% by ILC (percentages are estimates and subject to audit). In addition, ILC has an option to acquire a further 10% in the Mariana project through a back-in right.

The Raleigh Lake project, now consisting of 3,027 hectares of adjoining mineral claims in Ontario, is regarded by ILC management as ILC's most significant project in Canada. It is 100% owned by ILC, is not subject to any encumbrances, and is royalty free.

Complementing the Company's lithium brine project at Mariana and rare metal pegmatite property at Raleigh Lake, are interests in two other rare metal pegmatite properties in Ontario, Canada known as the Mavis Lake and Forgan Lake projects, and the Avalonia project in Ireland, which encompasses an extensive 50-km-long pegmatite belt.

The ownership of the Mavis Lake project is now 51% Essential Metals Limited and 49% ILC. In addition, ILC owns a 1.5% NSR on Mavis Lake. ESS has an option to earn an additional 29% by sole-funding a further CAD $8.5 million expenditures of exploration activities, at which time the ownership will be 80% ESS and 20% ILC.

The Forgan Lake project will, upon Ultra Resources Inc. meeting its contractual requirements pursuant to its agreement with ILC, become 100% owned by Ultra Resources, and ILC will retain a 1.5% NSR on Forgan Lake.

The ownership of the Avalonia project is currently 55% Ganfeng Lithium and 45% ILC. Ganfeng Lithium has an option to earn an additional 24% by either incurring CAD $10 million expenditures on exploration activities or delivering a positive feasibility study on the project, at which time the ownership will be 79% Ganfeng Lithium and 21% ILC.

With the increasing demand for high tech rechargeable batteries used in electric vehicles and electrical storage as well as portable electronics, lithium has been designated "the new oil", and is a key part of a "green tech" sustainable economy. By positioning itself with solid strategic partners and projects with significant resource potential, ILC aims to be one of the lithium and battery metals resource developers of choice for investors and to continue to build value for its shareholders in the '20s, the decade of battery metals.

On behalf of the Company,

John Wisbey

Chairman and CEO

For further information concerning this news release please contact +1 604-449-6520

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Cautionary Statement Regarding Forward-Looking Information

Except for statements of historical fact, this news release contains certain "forward-looking information" within the meaning of applicable securities law. Forward-looking information or forward-looking statements in this or other news releases may include: the effect of results of the preliminary economic assessment of the Mariana Joint Venture Project, timing of publication of the PEA technical report, anticipated production rates, the timing and/or anticipated results of drilling on the Raleigh Lake or Mavis Lake projects, the expectation of feasibility studies, lithium recoveries, modeling of capital and operating costs, results of studies utilizing membrane technology at the Mariana Project, budgeted expenditures and planned exploration work on the Avalonia Joint Venture, satisfactory completion of the sale of mineral rights at Forgan Lake, satisfactory completion of the purchase of additional mineral rights at Raleigh Lake, increased value of shareholder investments, and continued agreement between the Company and Jiangxi Ganfeng Lithium Co. Ltd. regarding the Company's percentage interest in the Mariana project. Such forward-looking information is based on a number of assumptions and subject to a variety of risks and uncertainties, including but not limited to those discussed in the sections entitled "Risks" and "Forward-Looking Statements" in the interim and annual Management's Discussion and Analysis which are available at www.sedar.com. While management believes that the assumptions made are reasonable, there can be no assurance that forward-looking statements will prove to be accurate. Should one or more of the risks, uncertainties or other factors materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in forward-looking information. Forward-looking information herein, and all subsequent written and oral forward-looking information are based on expectations, estimates and opinions of management on the dates they are made that, while considered reasonable by the Company as of the time of such statements, are subject to significant business, economic and competitive uncertainties and contingencies. These estimates and assumptions may prove to be incorrect and are expressly qualified in their entirety by this cautionary statement. Except as required by law, the Company assumes no obligation to update forward-looking information should circumstances or management's estimates or opinions change.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/80715

Figure 1

Grace Shear Zone with the 2017 RPX Diamond Drilling intercept and the War Eagle Showing

Figure 2

Location of the War Eagle Claims

TORONTO, April 19, 2021 (GLOBE NEWSWIRE) — Red Pine Exploration Inc. (TSX-V: RPX) (“Red Pine” or the “Company”) announces that it has entered into a definitive property purchase agreement with 2533258 ONTARIO CORP. (the “Vendor”), dated April 16th, 2021 to acquire 100% interest in additional mining claims located in the McMurray Township, Michipicoten region of Ontario. This acquisition aligns with the Company’s strategy of consolidation of the Wawa Gold Project land package.

The acquisition of these properties, covering a total area of 50.2 hectares located East of Mountain Lake, is an integral part of Red Pine’s exploration strategy to increase the Company’s interests and developments in the region. Red Pine is pleased to secure this claim block surrounded by and adjacent to the Company’s flagship 100% owned Wawa Gold Project. The acquisition remains subject the receipt of TSX Venture Exchange approval.

Quentin Yarie, President and CEO of Red Pine, stated, “We are excited with the successful acquisition of these strategically located claims with gold showings exhibiting similar characteristics to our highly prospective Grace Darwin structures. Grace Darwin is a high priority, high grade exploration target planned for drilling in 2021.”

These additional properties sit on the projected Southern extension of the Grace Shear Zone in which intermittent historic mining between 1901 and 1944 in the Darwin-Grace Mine produced 17,634 ounces of gold at 13.27 g/t. Of the newly acquired claims, significant gold mineralization is known to occur at the War Eagle showing located along the strike of the projected southern extension of the Grace Shear Zone (see Figure 1). The best historic channel samples taken at the showing contained 15.43 g/t Au over 0.82 metre, and grab samples contained up to 16.32 g/t gold (Simson, W.E., Synopsis of Report on the Grace Mine, October 1, 1924). The reader is cautioned that the qualified person has not done sufficient work to independently verify the reported historic results, and that grab samples are selective by nature and may not represent the true grade or style of gold mineralization.

Figure 1: Grace Shear Zone with the 2017 RPX Diamond Drilling intercept and the War Eagle Showing is available at

https://www.globenewswire.com/NewsRoom/AttachmentNg/aa5f3771-38fc-4224-a5be-0c9cf0fcfc34

Previous Red Pine drilling conducted in 2017 in the Grace Shear Zone confirmed that high-grade gold mineralization extends beyond the known footprints of the Darwin-Grace mine and defined the Grace Shear Zone as a significant exploration target of the Wawa Gold Project (see Red Pine’s news release of March 3, 2017 for drilling results in the Grace Shear Zone and Figure 1). Notable results from Red Pine’s 2017 drilling are 57.31 g/t gold over 3.14 metres.

Pursuant to this agreement, Red Pine will purchase from 2533258 ONTARIO CORP. all the rights, titles and interests in and to the mineral properties located in the Sault Ste. Marie Mining Division, for a sale price of CAD$240,000 in cash and the issuance of 83,000 common shares at closing. The common shares issued in connection with the purchase agreement are subject to a standard 4 month hold period.

The description of mineral properties subject to this agreement are noted below and displayed in Figure 2:

-

PIN: 31169-0293 (MLAS ID: PAT-775): PCL 1785 SEC AWS; MINING CLAIM SSM3492 MCMURRAY; MICHIPICOTEN

-

PIN: 31169-0302 (MLAS ID: PAT-776 and PAT-777): PCL 1833 SEC AWS; MINING CLAIM SSM3809 MCMURRAY; MINING CLAIM SSM3810 MCMURRAY; MICHIPICOTEN

Figure 2: Location of the War Eagle Claims is available at

https://www.globenewswire.com/NewsRoom/AttachmentNg/0e297e02-194d-42e9-8511-eadad2c98509

The information is not necessarily indicative of the mineralization on the property. The Company will need to conduct an exploration program to confirm historical mineralization reported on the property and there is no guarantee that significant discovery will be made as a result of its exploration efforts.

Qualified Person

Quentin Yarie, P.Geo. and Chief Executive Officer of Red Pine and the Qualified Person, as defined by National Instrument 43-101, has reviewed and approved the news release’s technical information.

COVID-19 Precautions

Red Pine has developed and implemented compliant precautions and procedures according to guidelines for the Province of Ontario. Protocols were put in place to ensure our employees’ and contractors’ safety, thereby reducing the potential for community contact and spreading of the virus.

About Red Pine Exploration Inc.

Red Pine Exploration Inc. is a gold exploration company headquartered in Toronto, Ontario, Canada. The Company's common shares trade on the TSX Venture Exchange under the symbol "RPX".

For more information about the Company, visit www.redpineexp.com

Or contact:

Quentin Yarie, President and CEO, (416) 364-7024, qyarie@redpineexp.com

Or Tara Asfour, Investor Relations Manager, (514) 833-1957 tasfour@redpineexp.com

1National Instrument 43-101 Technical Report for the Wawa Gold Project, Brian Thomas P.Geo. Golder Associates Ltd, effective July 16, 2019

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This News Release contains forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as "may", "should", "expects", "plans", "anticipates", "believes", "estimates", "predicts", "potential" or "continue" or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors that may cause our or our industry's actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

Merger creates the 5th largest global lithium chemicals company with a diversified production base and exciting growth platform, with potential to unlock significant synergies and realise value to be shared by all shareholders.

BRISBANE, Australia, April 19, 2021 (GLOBE NEWSWIRE) — Orocobre Limited (ASX:ORE, TSX:ORL) (Orocobre) and Galaxy Resources Limited (ASX:GXY) (Galaxy) are pleased to announce that they have entered into a binding Merger Implementation Deed (MID) under which the two companies will merge via a Galaxy Scheme of Arrangement (Scheme) pursuant to which Orocobre will acquire 100% of the shares in Galaxy.

Galaxy shareholders will receive 0.569 Orocobre shares for each Galaxy share held at the Scheme record date. Upon implementation of the Scheme, Orocobre shareholders will own 54.2% of the fully diluted share capital of the combined entity and Galaxy shareholders will own the remaining 45.8%.

The Scheme is unanimously recommended by the Board of Galaxy and each Galaxy Director intends to vote all the shares that they hold in Galaxy in favour of the Scheme (in both cases, subject to no superior proposal emerging and the Independent Expert concluding (and continuing to conclude) that the Scheme is in the best interests of Galaxy shareholders).

The Scheme is endorsed and supported by the Board of Orocobre, subject to no proposal for Orocobre emerging.

As part of the proposed Scheme, Martin Rowley would become Non-Executive Chairman, Robert Hubbard would become Deputy Chairman, and Martín Pérez de Solay would remain CEO and Managing Director of the group, with a highly experienced and complementary Board and management team drawn from the combined group.

A new name for the merged entity will be selected in due course representing the global reach of the new entity, which will have its head office in Buenos Aires, Argentina, a corporate headquarters on the Australian East Coast and an office in Perth.

Highlights Summary

-

Creating a Top 5 global lithium chemicals company1

-

Highly complementary portfolio of assets delivering geographical and product diversification across brine, hard rock and vertical integration across the supply chain

-

Industry leading growth profile with enhanced financial position to optimise and potentially accelerate development with the ability and intent to capture further downstream value

-

Compelling industrial logic with significant value creation opportunities unique to this merger

-

Highly experienced and complementary Board and senior management teams to drive growth

-

Potential to generate significant shareholder value with enhanced scale and financial capacity

Galaxy Chairman Martin Rowley commented: “This transaction has the potential to be a significant value-creating opportunity for Galaxy and Orocobre shareholders. The Scheme provides shareholders of Galaxy with the opportunity to share in the significant benefits of being part of a larger diversified group and the synergies expected to be available to help enhance and progress our portfolio of world class assets. The merged entity's growth opportunities in both brine and hard rock position it uniquely to take advantage of expected rising EV demand for lithium.”

Orocobre Chairman Robert Hubbard commented: “The logic of this merger is compelling. Both Orocobre and Galaxy shareholders, will benefit from the diversification, growth and scale of a top 5 global lithium chemicals company. I take this opportunity to re-iterate the group's ongoing commitment to the principles of delivering the highest level of transparency of our environmental, social and governance performance, the foundations upon which our assets have and will continue to be developed.”

Orocobre CEO and Managing Director Martín Pérez de Solay commented: “The merger brings together assets and teams with highly complementary skills and knowledge, with a unique opportunity to create a leading independent lithium company. The merger consolidates the combined group’s position in Argentina and will give us significant operational, technical and financial flexibility to deliver the full value of our combined portfolio.”

Galaxy CEO Simon Hay commented: “The merger with Orocobre represents an exciting opportunity for both Orocobre and Galaxy shareholders to consolidate and realise the full potential of our asset portfolios and technical capabilities. The transaction will allow the group to materially accelerate the development of our combined growth projects.”

Orocobre and Galaxy will be hosting a joint investor call at 10.30am AEST (8.30am AWST) today, 19 April 2021. Orocobre and Galaxy are announcing their respective quarterly results today.

The call can be accessed via the following link:

https://services.choruscall.com.au/webcast/ubs-210419.html

Transaction Summary

Orocobre Limited (ASX:ORE, TSX:ORL) and Galaxy Resources Limited (ASX:GXY) have entered into a binding Merger Implementation Deed (MID) under which the two companies will merge via a Galaxy Scheme.

Under the Scheme, Galaxy shareholders will receive 0.569 Orocobre shares for each Galaxy share held on the record date for the Scheme. Orocobre shareholders will own 54.2% of the fully diluted share capital of the combined entity and Galaxy shareholders will own the remaining 45.8%.

The Galaxy Board of Directors unanimously recommends that Galaxy shareholders vote in favour of the Scheme and each Galaxy Director intends to vote all the shares that they hold in Galaxy in favour of the Scheme (in both cases, subject to the Independent Expert opining that the Scheme is in the best interests of Galaxy shareholders and in the absence of a superior proposal).

The Orocobre Board endorses and supports the transaction in the absence of a proposal for Orocobre.

Under the Scheme, Galaxy Chairman Martin Rowley would become Non-Executive Chairman, Orocobre Chairman Robert Hubbard would become Deputy Chairman, Martín Pérez de Solay would remain CEO of the group and Simon Hay will would become President of International Business reporting to the CEO. The CEO together with the Board will commence an integration process to determine the optimal management team drawing from employees from both companies based on a best fit basis.

On implementation of the Scheme, the Board of Directors will comprise four Independent Directors from Orocobre (including Mr Hubbard), four Independent Directors from Galaxy (including Mr Rowley), and the CEO Mr Pérez de Solay. It is agreed that both Mr Rowley and Mr Hubbard will retire from their roles within 12 months of implementation. They will lead a process to ensure that the longer-term Board composition is ideally placed to lead the merged entity going forward.

Strategic Rationale

-

Creating a Top 5 global lithium chemicals company

-

Creates the leading ASX lithium company and a top 5 global lithium chemicals company2

-

One of the world’s largest, most geographically diversified producers of lithium chemicals

-

Vertically integrated and able to service multiple markets and customers

-

-

Highly complementary portfolio of assets delivering diversification of production and vertical integration

-

Diversified across geography, lithium source and end products

-

Combines two complementary, large scale tier-one assets

-

Vertically integrated product strategy for all key assets

-

-

Industry leading growth profile with enhanced financial position to optimise and potentially accelerate development with the ability and intent to capture further downstream value

-

Significant portfolio of upstream and downstream growth projects

-

Growth pipeline evenly balanced between production optimisation, construction, advanced projects, brownfield expansions and early-stage projects

-

Unique platform of expertise, capacity and geographic presence to consider further inorganic growth opportunities

-

-

Compelling industrial logic with potentially significant value creation unique to this merger

-

Ability to apply combined management and technical expertise across the merged group and shared IP to further de-risk Sal de Vida and optimise Olaroz

-

Potential for substantial savings in Argentina from expertise sharing, employee and contractor sharing and procurement savings

-

Marketing synergies expected from expanded customer relationships and a broader product base

-

-

Highly experienced and complementary Board and senior management teams to drive growth

-

Global team with significant technical expertise to deliver brine projects in Argentina

-

Proven track record of successfully delivering projects across brine, hard rock, and processing

-

Extensive experience within Argentina shared across the combined board and senior management team

-

-

Potential to generate significant shareholder value with enhanced scale and financial capacity

-

Combined entity expected to be included in the ASX 200 index and approach ASX 100 index thresholds

-

Significantly enhanced liquidity and capital markets profile

-

Strengthened balance sheet with pro forma gross cash of US$487m3 well placed to deliver a world class project pipeline

-

Conditions

Key conditions to the implementation of the Scheme include:

-

Galaxy shareholder approval;

-

Approval by the Court;

-

The Independent Expert concluding that the Scheme is in the best interests of Galaxy shareholders and not changing, withdrawing or qualifying that conclusion;

-

No material adverse effect or prescribed event (as each defined in the MID) occurring in relation to either Orocobre or Galaxy (as applicable); and

-

Other conditions customary for a transaction of this nature.

The MID includes reciprocal exclusivity arrangements (including “no shop”, “no talk” and “no due diligence” restrictions and notification obligations) in favour of both parties, a matching right regime in favour of Orocobre and break fees in favour of both parties. The exclusivity arrangements are subject to customary exceptions that enable the directors of Galaxy and Orocobre to comply with their respective fiduciary and / or statutory duties.

Full details of the terms and conditions are set out in the MID, a copy of which is set out in Annexure A.

Timetable and next steps

Galaxy shareholders do not need to take any action in relation to the Scheme at this stage.

A scheme booklet containing information in relation to the Scheme, including the basis for the Galaxy Board’s unanimous recommendation, an Independent Expert Report and details of the Scheme is expected to be circulated to all Galaxy shareholders in late June 2021.

An indicative timetable (which remains subject to change) is set out below:

|

Event |

Estimated date |

|

First Court Hearing |

Late June 2021 |

|

Dispatch scheme booklet to Galaxy shareholders |

Late June 2021 |

|

Scheme Meeting |

Late July 2021 |

|

Second Court hearing |

Late July – Early August 2021 |

|

Effective Date |

Late July – Early August 2021 |

|

Record Date |

Early – Mid August 2021 |

|

Implementation Date |

Mid August 2021 |

Advisers

Orocobre’s financial adviser is UBS AG, Australia Branch and its legal adviser is Jones Day.

Galaxy’s financial adviser is Standard Chartered Bank and its legal adviser is Ashurst.

Conference Call

Orocobre and Galaxy will host a joint investor call at 10.30am AEST (8.30am AWST) today, 19 April 2021. The call can be accessed via the following link:

https://services.choruscall.com.au/webcast/ubs-210419.html

This release was authorised by the Board of Galaxy Resources Limited and the Board of Orocobre Limited.

Investor Relations Enquiries

|

Andrew Barber |

Phoebe Lee |

Media Enquiries

|

Justin Kirkwood |

Scott Rochfort |

IMPORTANT NOTICES

This announcement is a joint announcement by Galaxy Resources Limited ACN 071 976 442 (Galaxy) and Orocobre Limited ACN 112 589 910 (Orocobre).

This presentation has been prepared in relation to the proposed merger between Galaxy and Orocobre by way of scheme of arrangement under Part 5.1 of the Corporations Act 2001 (Cth) (Scheme). Under the Scheme, Orocobre would acquire 100% of the fully paid ordinary shares in Galaxy in exchange for the issue of new fully paid ordinary shares in Orocobre. The Scheme is subject to the terms and conditions described in the merger implementation deed entered into between Galaxy and Orocobre on or about the date of this announcement (Merger Implementation Deed). A copy of the Merger Implementation Deed is attached to this announcement and available on the ASX website (at www.asx.com.au).

Galaxy and Orocobre have jointly prepared this announcement based on information available to them as at the date of this announcement. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this announcement. To the maximum extent permitted by law, none of Galaxy or Orocobre, their respective directors, employees, agents or advisers, or any other person, accepts any liability, including, without limitation, any liability arising from fault or negligence on the part of any of them or any other person, for any loss arising from the use of this announcement or its contents or otherwise arising in connection with it.

Forward Looking Statements

This announcement contains forward looking statements concerning Galaxy, Orocobre and the merged group which are made as at the date of this announcement (unless otherwise indicated), including statements about intentions, beliefs and expectations, plans, strategies and objectives of the directors and management of Galaxy and Orocobre for Galaxy, Orocobre and the merged group, the anticipated timing for and outcome and effects of the Scheme (including expected benefits to shareholders of Galaxy and Orocobre), indications of and guidance on synergies, future earnings or financial position or performance, anticipated production or construction or development commencement dates, costs or production outputs, capital expenditure and future demand for lithium, expectations for the ongoing development and growth potential of the merged group and the future operation of Galaxy and Orocobre.

Forward looking statements are not statements of historical fact and actual events and results may differ materially from those contemplated by the forward looking statements as a result of a variety of risks, uncertainties and other factors, many of which are outside the control of Galaxy, Orocobre and the merged group. Such factors may include, among other things, risks relating to funding requirements, lithium and other commodity prices, exploration, development and operating risks (including unexpected capital or operating cost increases), production risks, competition and market risks, regulatory restrictions (including environmental regulations and associated liability, changes in regulatory restrictions or regulatory policy and potential title disputes) and risks associated with general economic conditions. Any forward-looking statements, as well as any other opinions and estimates, provided in this announcement are based on assumptions and contingencies which are subject to change without notice and may prove ultimately to be materially incorrect, as are statements about market and industry trends, which are based on interpretations of current market conditions.

There can be no assurance that the Scheme will be implemented or that plans of the directors and management of Galaxy and Orocobre for the merged group will proceed as currently expected or will ultimately be successful. You are strongly cautioned not to place undue reliance on forward looking statements, including in respect of the financial or operating outlook for Galaxy, Orocobre or the merged group (including the realisation of any expected synergies), particularly in light of the current economic climate and the significant volatility, uncertainty and disruption caused by the ongoing COVID-19 pandemic.

Except as required by law or the ASX listing rules, Galaxy and Orocobre assume no obligation to provide any additional or updated information or to update any forward looking statements, whether as a result of new information, future events or results, or otherwise. Nothing in this announcement will, under any circumstances (including by reason of this announcement remaining available and not being superseded or replaced by any other presentation or publication with respect to Galaxy, Orocobre or the merged group, or the subject matter of this announcement), create an implication that there has been no change in the affairs of Galaxy or Orocobre since the date of this announcement.

Mineral Resources and Ore Reserves reporting (by Galaxy and Orocobre)

Any information in this announcement that relates to Sal de Vida Project Mineral Resources and Ore Reserves is extracted from the ASX announcement entitled “Sal de Vida Resource and Reserve Update” dated 14 April 2021 which is available to view on www.gxy.com and www.asx.com.au. Galaxy confirms that it is not aware of any new information or data that materially affects the information included in the original market announcements and that all material assumptions and technical parameters underpinning the Mineral Resources and Ore Reserves estimates in the relevant market announcement continue to apply and have not materially changed. Galaxy confirms that the form and context in which the Competent Person’s findings are presented have not been materially modified from the original market announcement.

Any information in this announcement that relates to James Bay Mineral Resources is extracted from the ASX announcement, entitled “James Bay Resource Update” dated 4 December 2017 which is available to view on www.gxy.com and www.asx.com.au. Galaxy confirms that it is not aware of any new information or data that materially affects the information included in the original market announcement and that all material assumptions and technical parameters underpinning the Mineral Resources in the relevant market announcement continue to apply and have not materially changed. Galaxy confirms that the form and context in which the Competent Person’s findings are presented have not been materially modified from the original market announcement.

Any information in this announcement that relates to Mt Cattlin Mineral Resources and Ore Reserves is extracted from the report entitled “2020 Resource & Reserve Update” dated 17 March 2021 which is available to view on www.gxy.com and www.asx.com.au. Galaxy confirms that it is not aware of any new information or data that materially affects the information included in the original market announcement and that all material assumptions and technical parameters underpinning the Mineral Resources and Ore Reserves estimates in the relevant market announcement continue to apply and have not materially changed. Galaxy confirms that the form and context in which the Competent Person’s findings are presented have not been materially modified from the original market announcement.

Orocobre is not in possession of any new information or data relating to historical estimates that materially impacts on the reliability of the estimates or Orocobre's ability to verify the historical estimates as mineral resources, in accordance with the JORC Code. The supporting information provided in the initial market announcement on 21/08/12 continues to apply and has not materially changed. Additional information relating to Orocobre's Olaroz Lithium Facility is available on Orocobre's website in “Technical Report – Salar de Olaroz Lithium-Potash Project, Argentina” dated May 13 2011, which was prepared by John Houston, Consulting Hydrogeologist, together with Mr. Michael Gunn, Consulting Processing Engineer, in accordance with NI 43-101.

The information in this report that relates to exploration reporting at the Cauchari project has been prepared by Mr. Murray Brooker. Mr. Brooker is a geologist and hydrogeologist and is a Member of the Australian Institute of Geoscientists. Mr. Brooker is an employee of Hydrominex Geoscience Pty Ltd and is independent of Orocobre. Mr. Brooker has sufficient relevant experience to qualify as a competent person as defined in the 2012 edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves. He is also a “Qualified Person” as defined in NI 43-101. Mr. Brooker consents to the inclusion in this announcement of this information in the form and context in which it appears.

Note on synergies

Please also refer to the investor presentation (including slides 7, 8, 13, 14 and 15) released by Galaxy and Orocobre to ASX simultaneously with this announcement for further information about the basis and assumptions underlying any statements about expected synergies in this announcement.

Not for release or distribution in the United States

This announcement has been prepared for publication in Australia and may not be released to U.S. wire services or distributed in the United States. This announcement does not constitute an offer to sell, or a solicitation of an offer to buy, securities in the United States or any other jurisdiction, and neither this announcement or anything attached to this announcement shall form the basis of any contract or commitment. Any securities described in this announcement have not been, and will not be, registered under the U.S. Securities Act of 1933 and may not be offered or sold in the United States except in transactions registered under the U.S. Securities Act of 1933 or exempt from, or not subject to, the registration of the U.S. Securities Act of 1933 and applicable U.S. state securities laws.

TSX matters

Orocobre is an “Eligible Interlisted Issuer” for purposes of the TSX and intends to rely on the exemptions set forth in Section 602.1 of the TSX Company Manual in respect of the Scheme. The issuance of shares by Orocobre pursuant to the Scheme is subject to acceptance by the TSX.

___________________

1 Based on market capitalisation as at ASX market close on 16 April 2021.

2 Based on market capitalisation as at ASX market close on 16 April 2021.

3 As at 31 March 2021 and includes restricted cash of US$108m.

Whilst it may not be a huge deal, we thought it was good to see that the Oklo Resources Limited (ASX:OKU) MD, CEO & Director, Simon Taylor, recently bought AU$109k worth of stock, for AU$0.14 per share. That purchase might not be huge but it did increase their holding by 13%.

View our latest analysis for Oklo Resources

The Last 12 Months Of Insider Transactions At Oklo Resources

In fact, the recent purchase by Simon Taylor was the biggest purchase of Oklo Resources shares made by an insider individual in the last twelve months, according to our records. So it's clear an insider wanted to buy, at around the current price, which is AU$0.14. Of course they may have changed their mind. But this suggests they are optimistic. If someone buys shares at well below current prices, it's a good sign on balance, but keep in mind they may no longer see value. The good news for Oklo Resources share holders is that an insider was buying at near the current price. Simon Taylor was the only individual insider to buy during the last year.

Simon Taylor bought a total of 1.60m shares over the year at an average price of AU$0.18. The chart below shows insider transactions (by companies and individuals) over the last year. By clicking on the graph below, you can see the precise details of each insider transaction!

Oklo Resources is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Insider Ownership

Looking at the total insider shareholdings in a company can help to inform your view of whether they are well aligned with common shareholders. We usually like to see fairly high levels of insider ownership. From our data, it seems that Oklo Resources insiders own 11% of the company, worth about AU$7.0m. But they may have an indirect interest through a corporate structure that we haven't picked up on. Whilst better than nothing, we're not overly impressed by these holdings.

So What Does This Data Suggest About Oklo Resources Insiders?

It is good to see the recent insider purchase. We also take confidence from the longer term picture of insider transactions. However, we note that the company didn't make a profit over the last twelve months, which makes us cautious. We would certainly prefer see higher levels of insider ownership but analysis of the insider transactions suggests that Oklo Resources insiders are expecting a bright future. So these insider transactions can help us build a thesis about the stock, but it's also worthwhile knowing the risks facing this company. For example, Oklo Resources has 6 warning signs (and 3 which are concerning) we think you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions, but not derivative transactions.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Antofagasta plc (LON:ANTO) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Antofagasta

What Is Antofagasta's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Antofagasta had US$3.55b of debt, an increase on US$2.51b, over one year. But it also has US$3.67b in cash to offset that, meaning it has US$126.2m net cash.

How Strong Is Antofagasta's Balance Sheet?

We can see from the most recent balance sheet that Antofagasta had liabilities of US$1.63b falling due within a year, and liabilities of US$4.90b due beyond that. On the other hand, it had cash of US$3.67b and US$1.07b worth of receivables due within a year. So its liabilities total US$1.78b more than the combination of its cash and short-term receivables.

Given Antofagasta has a humongous market capitalization of US$25.9b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Antofagasta also has more cash than debt, so we're pretty confident it can manage its debt safely.

And we also note warmly that Antofagasta grew its EBIT by 17% last year, making its debt load easier to handle. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Antofagasta's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Antofagasta may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Antofagasta produced sturdy free cash flow equating to 52% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

We could understand if investors are concerned about Antofagasta's liabilities, but we can be reassured by the fact it has has net cash of US$126.2m. And we liked the look of last year's 17% year-on-year EBIT growth. So is Antofagasta's debt a risk? It doesn't seem so to us. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Antofagasta is showing 1 warning sign in our investment analysis , you should know about…

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

Vancouver, British Columbia–(Newsfile Corp. – April 16, 2021) – Margaret Lake Diamonds Inc. (TSXV: DIA) (FSE: M85) (OTC: DDIAF) ("MLD" or the "Company") is pleased to announce Arctic Star Exploration Corp. ("Arctic Star" or the "Company") (TSXV: ADD) (FSE: 82A2) (WKN: A2DFY5) (OTC Pink: ASDZF) has made a new discovery on the Diagras project in the Lac de Gras kimberlite field, Northwest Territory 380km north of Yellowknife. The discovery has been named the Birch Kimberlite.

It was discovered by drilling a vertical hole into a EM and gravity anomaly. The anomaly also occupies a distinct gap in an otherwise continuous Mackenzie diabase dyke in the magnetic data.

Kimberlite was discovered after drilling 28m through 11m of water and 17m of overburden (glacial till). The drill exited the kimberlite at 71m. A second hole from the same drill setup is underway to obtain more kimberlite for caustic fusion.

The drill collar is 220m SE of the known Black Spruce kimberlite discovered in the 1990s. The Black Spruce kimberlite was discovered by drilling a discrete magnetic low. In contrast, the Birch kimberlite has no magnetic signature.

Buddy Doyle, VP Exploration of Arctic, said, "We are all elated to strike kimberlite so early in our 2021 exploration program. It proves our exploration concept, we expect more discoveries as we proceed." Mr. Doyle continued, "After completing the current drill hole we will move from the Birch discovery to test other similar targets. The priority is to make as many discoveries as we can before the ice melts. Material from each discovery will be sent for caustic fusion. We will return to those kimberlites with the highest micro-diamond counts and give them further attention."

The Diagras project is a Joint Venture with Margaret Lake Diamonds Inc. Arctic is the manager and operator of this joint venture.

Qualified Person

The Qualified Person for this news release is Buddy Doyle, AUSIMM, a Geologist of over 30 years' experience in diamond exploration, discovery, and evaluation. A Qualified Person under the provisions of National Instrument 43-101.

Contact Information

Neil Foran

Chief Executive Officer

(604) 681-7735

neil@margaretlakediamonds.com

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This press release contains forward-looking information or forward-looking statements (collectively "forward-looking information") within the meaning of applicable securities laws. Forward-looking information is typically identified by words such as: "believe", "expect", "anticipate", "intend", "estimate", "potentially" and similar expressions, or are those, which, by their nature, refer to future events. The Company cautions investors that any forward-looking information provided by the Company is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to the Company's public filings for a more complete discussion of such risk factors and their potential effects, which may be accessed through the Company's profile on SEDAR at www.sedar.com.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/80724

Vancouver, British Columbia–(Newsfile Corp. – April 16, 2021) – InZinc Mining Ltd. (TSXV: IZN) ("InZinc" or the "Company") is pleased that, further to the news release of December 22, 2020, it has entered into an agreement (the "Option Agreement") with American West Metals Limited ("American West"), a private Australian company, pursuant to which InZinc granted to a wholly-owned subsidiary of American West an option ("Option") to earn a 100% interest in InZinc's West Desert project ("West Desert") located in Utah, USA. The Option Agreement is subject to, among other things, shareholder and regulatory approval.

"The proposed option agreement will benefit InZinc with improved financial flexibility and exposure to a broader, active portfolio of North American zinc and copper projects. The proposed shareholding in American West will provide InZinc continuing leverage at West Desert as a planned multi-year drill campaign to advance to prefeasibility is undertaken as well as exposure to activities at the Storm copper project, which American West recently optioned from Aston Bay Holdings Ltd. The financial terms offered by the proposed agreement will further provide InZinc the flexibility to advance, including drilling, the near surface discoveries and large untested targets at the prospective Indy Sedex project in BC, and assess new opportunities," said Wayne Hubert, CEO of InZinc.

The principal terms of the Option Agreement include:

1) An initial cash payment of US$500,000 to InZinc on the effective date (the "Effective Date") of the Option Agreement.

2) Required payments to InZinc during the 24 months following the effective date of the Option Agreement to comprise:

-

CDN$1,000,000 within 30 days of American West listing its shares on the Australian Securities Exchange ("ASX") through an initial public offering or other going public transaction ("IPO") or 12 months after the Effective Date, whichever is earlier;

-

US$1,500,000 upon the announcement by American West to the ASX of a completed Prefeasibility Study for West Desert or 24 months after the Effective Date, whichever is earlier; and

-

CDN$2,500,000 by way of shares of American West ranking equally with the shares of American West issued under the IPO (the "Consideration Shares"). If American West has not completed the IPO on the ASX within 12 months of the Effective Date, InZinc may elect to receive CDN$1,250,000 in cash from American West in lieu of Consideration Shares. If American West has not completed the IPO on the ASX within 24 months of the Effective Date, InZinc may elect to receive CDN$2,500,000 in cash in lieu of Consideration Shares.

3) Exercise of Option and Indium Revenue Share

Upon American West having paid the cash payments above and either having delivered the Consideration Shares or having paid the applicable cash payment in lieu of delivering Consideration Shares, American West may exercise the Option and acquire West Desert. InZinc will receive 50% of the revenue from the sale of indium mined from West Desert determined on a Net Smelter Return basis in accordance with generally accepted industry practice ("NSR"). American West will have the right to reduce the NSR to 25% by paying InZinc US$5,000,000 in cash at any time prior to the first sale of indium from the project.

4) Termination of Option

During the Option period, American West will be the operator of West Desert. If payments referred to above are not paid when due and American West does not rectify the failure within 45 days, InZinc would have the right to terminate the Option Agreement and American West shall surrender West Desert promptly to InZinc.

A meeting of InZinc shareholders to consider and, if thought fit, approve the Option Agreement and other matters is expected to be held in May 2021. An Information circular will be filed with regulatory authorities and mailed to InZinc shareholders.

American West Metals Ltd.

American West is targeting to be listed on the ASX in Q3 2021.

About InZinc