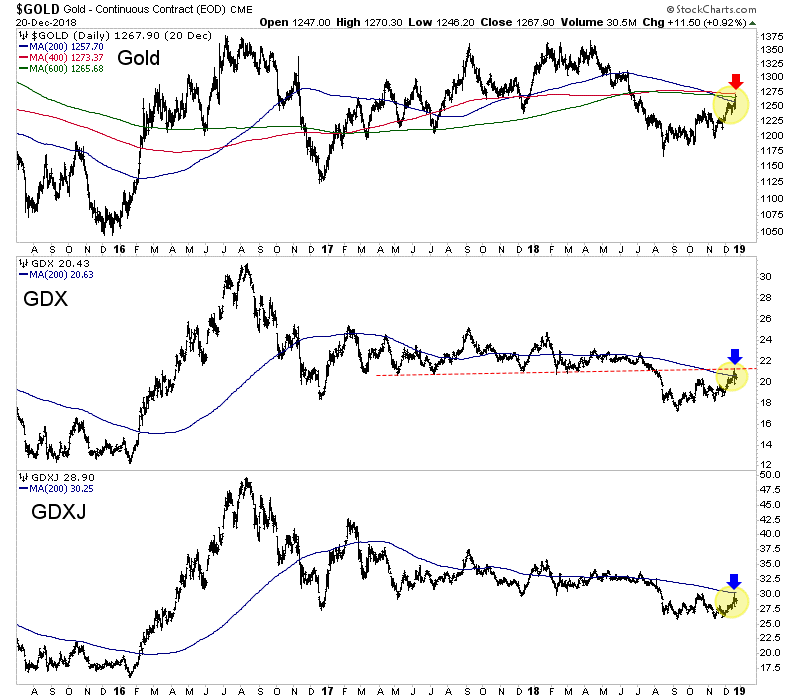

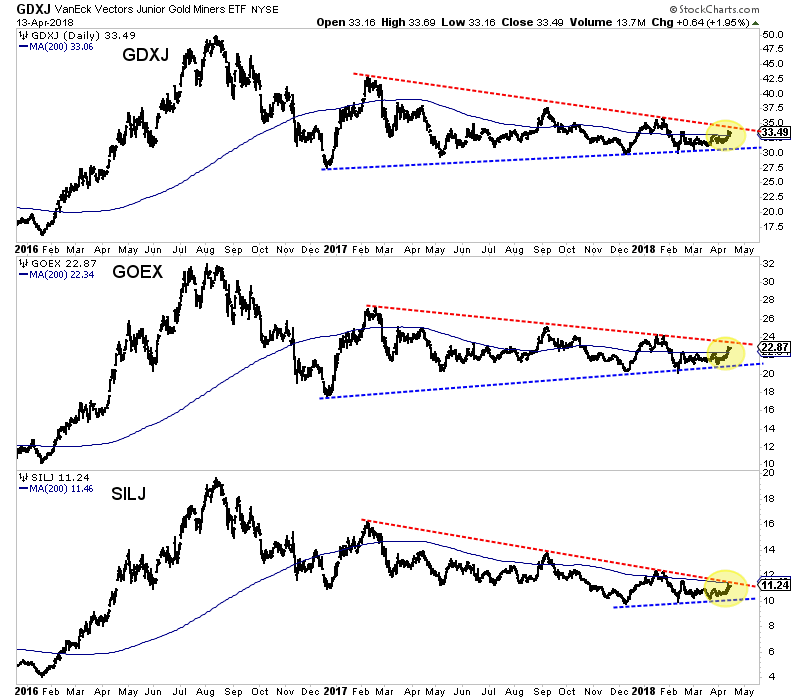

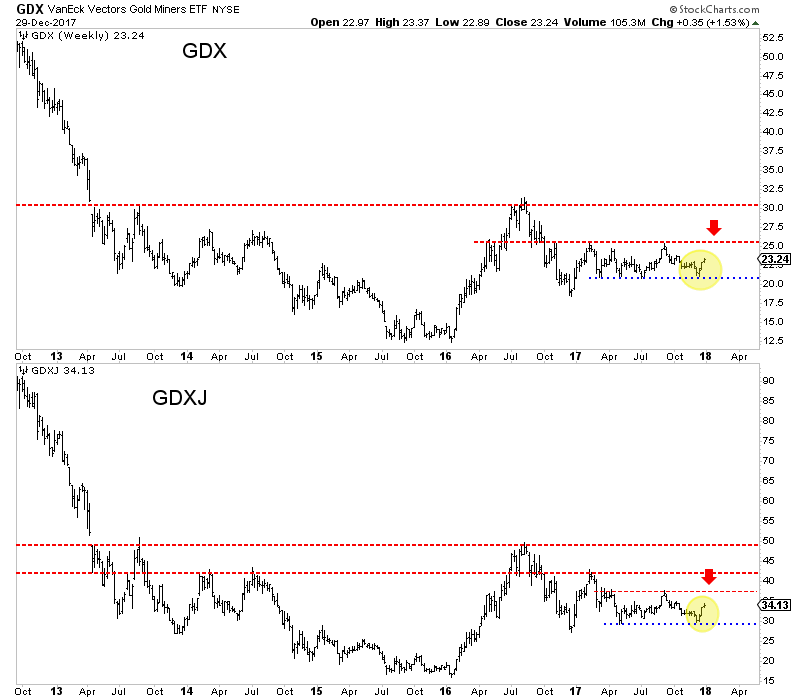

Last week we discussed the difference between a rally and bull market.

Gold stocks have been in a rally.

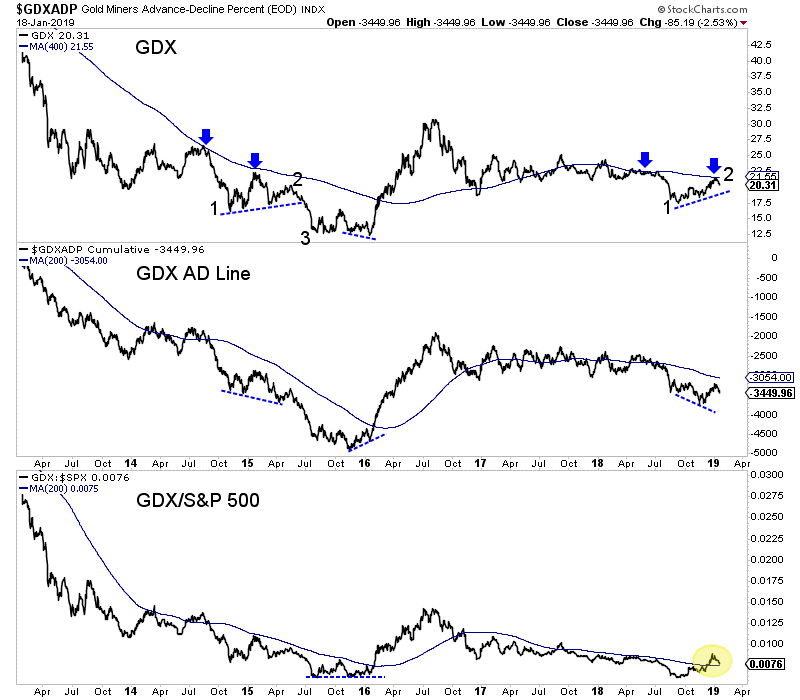

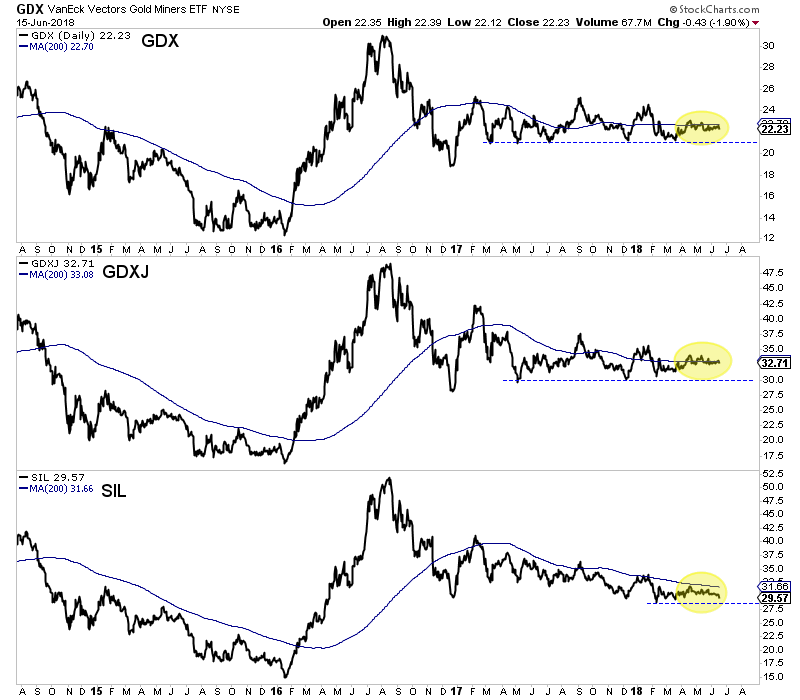

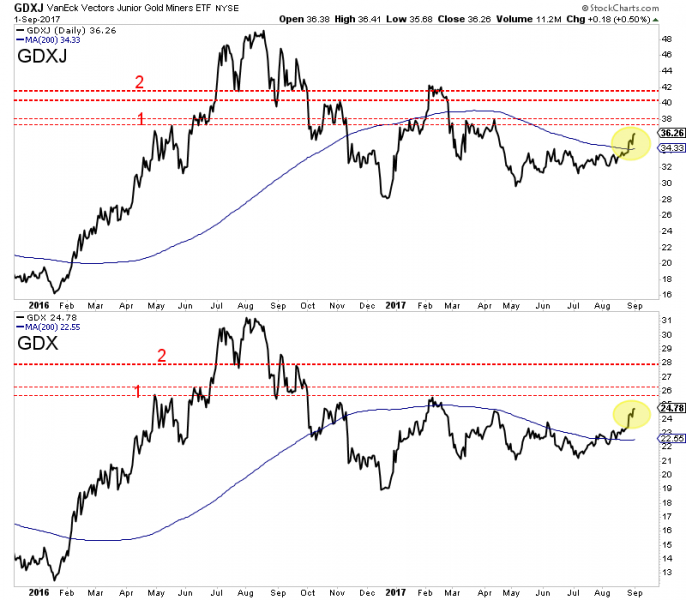

That rally is now over as gold stocks peaked at their 400-day moving averages days ago and sliced through their 200-day moving averages Friday.

Take a look at the charts of any gold stock index (GDX, GDXJ, HUI) and it’s clear they are in a downtrend.

Go back two to three years. You’ll see lower highs and lower lows. That’s a downtrend!

Until that changes, we have to respect that.

The change will come when the market knows the Fed is done hiking and anticipates the start of rate cuts.

Going back 65 years, I counted 13 times when the Fed went from rate hikes to rate cuts. The average gain in gold stocks during 11 of those periods was 172%.

The moves higher began an average and median of three to four months after the time of the last hike.

If the final hike is in March or June then the bull run should begin around the average time frame. If December 2018 was the final hike, then obviously the move higher could begin after the average or median period.

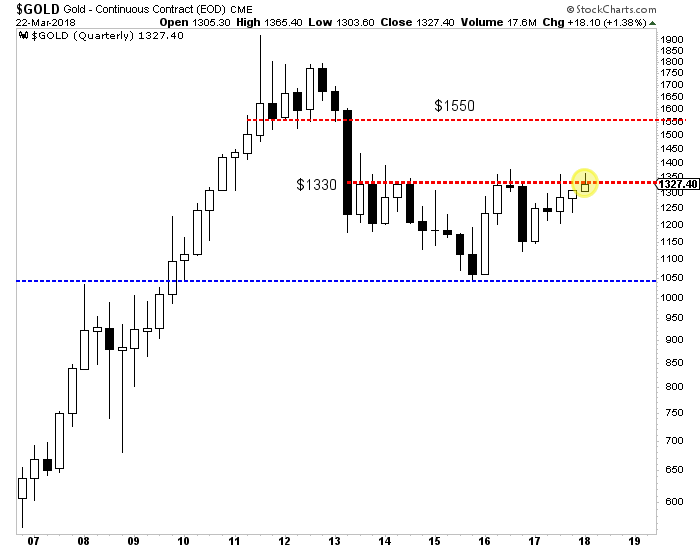

The immediate risk is the gold stocks could be starting another leg lower. In the chart below, we see similarities between GDX today and where it was in Q2 2015.

At both junctures the market had finished rallying after breaking down from a long consolidation. Note the points 1,2,3 and also the similarities in the advance-decline line. One positive difference is GDX relative to the stock market has surpassed its 200-day moving average.

In summation, we are looking for one more leg lower before a potential historic buying opportunity in precious metals. How much lower and for how long could depend on how soon the market is certain the Fed is done hiking.

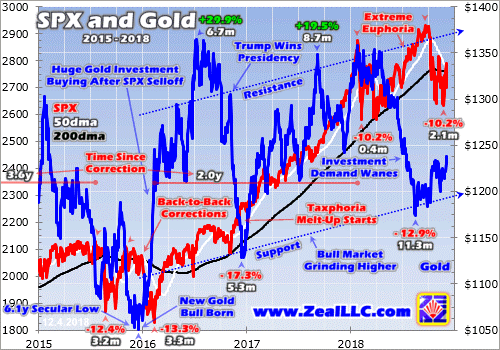

Gold investment demand reversed sharply higher in recent months, fueling a strong gold rally. The big stock-market selloff rekindled interest in prudently diversifying stock-heavy portfolios with counter-moving gold. These mounting investment-capital inflows into gold are likely to persist and intensify. Both weaker stock markets and higher gold prices will continue to drive more investment demand, growing gold’s upleg.

Early in Q4’18, gold reached a major inflection point. It languished during the first three quarters of 2018, down 8.5% year-to-date by the end of Q3. Investors wanted nothing to do with alternative investments with the stock markets powering to new record highs. The flagship S&P 500 broad-market stock index (SPX) had rallied 9.0% in the first 3/4ths of last year. That left gold deeply out of favor heading into Q4.

But a critical psychological switch was flipped as the SPX started sliding last quarter. After long years with little material downside, stock traders had been lulled into overpowering complacency. They were shocked awake as the SPX plunged 14.0% in Q4, its worst quarter since Q3’11. They poured back into gold as stocks burned, driving it a strong 7.6% higher in Q4! Rekindled investment demand was the driver.

Unfortunately gold investment demand is rather murky. Gold is bought and sold every day all over the world, in countless venues ranging from major exchanges to tiny third-world merchants. Tracking even the majority of this in real-time is impossible. The best-available data on global gold investment comes from the World Gold Council. But it is only published once per quarter, about a month after quarter-ends.

I can’t wait to see the WGC’s new Q4’18 Gold Demand Trends report due out in early February. These quarterly GDTs are very well done and essential reading for all investors. But while detailed and informative, their resolution is really low only being released 4 times per year. Investors need alternative data sources to understand and game what’s going on with gold investment demand between the GDTs, like now.

Thankfully there’s an excellent proxy of investors’ capital flows into and out of gold published daily, a high-resolution read. It is the physical gold bullion held in trust for the shareholders of the world’s dominant gold exchange-traded fund. That of course is the American GLD SPDR Gold Shares. GLD was created and launched by the World Gold Council way back in November 2004, and has grown into a gold juggernaut.

As part of the WGC’s GDT work each quarter, it tracks the world’s top 10 physically-backed gold ETFs. At the end of Q3’18 when you could hardly give away gold to American investors, GLD’s holdings still accounted for nearly 32% of the world’s top-10 gold-ETF total. Add in the 2nd-largest ETF which is also American, the IAU iShares Gold Trust, and these two leading ETFs control over 3/7ths of the global top-10 total.

The primary constituency for American gold ETFs is American stock investors. So what they are doing in terms of capital flows through GLD especially is exceedingly important for gold. In recent years most of the major quarterly moves in gold prices are nearly fully explainable by GLD’s holdings alone! They must be watched daily, as changes in them have proven the key to gold’s fortunes. It’s important to understand why.

The American stock markets are the biggest in the world, and American investors’ capital is vast beyond compare. At the end of Q3’18, the collective market capitalization of the 500 elite SPX stocks alone was a staggering $26,141.4b. By comparison, GLD’s total physical-gold-bullion holdings of 742.2 metric tons were only worth $28.4b. That’s less than 1/9th of a single percent, which for all intents and purposes is zero.

Thus if even the tiniest fraction of U.S. stock-market capital migrates into or out of GLD shares, gold itself moves big. This dominant gold ETF effectively acts as a conduit between stock-market capital and gold. But as these colossal pools of capital slosh into and out of GLD, it is always at risk of failing its mission of tracking the gold price. The supply and demand of GLD shares and gold are independent of each other.

So differential buying or selling of GLD shares by American stock investors must be directly equalized into the underlying global gold market. This mechanism is simple in concept. When GLD shares are being bought faster than gold itself, this ETF’s price threatens to decouple from gold’s price to the upside. To prevent this, GLD’s managers need to shunt that excess GLD-share demand directly into gold in real-time.

They issue enough new GLD shares to offset that excess demand, and then use the proceeds to buy physical gold bullion held in trust for GLD’s shareholders. So when GLD’s daily holdings are rising, that reveals American stock-market capital is flowing into gold. This GLD capital pipeline into gold also works similarly on the downside, when American stock investors dump GLD shares faster than gold is being sold.

GLD’s share price will soon disconnect from gold’s price to the downside. This ETF’s managers avoid that by buying back GLD shares to sop up the excess supply. They raise the capital to do this by selling some of GLD’s physical-gold-bullion holdings. So when GLD’s daily holdings are falling, American stock-market capital is being pulled back out of gold. These holdings closely mirror world gold-investment trends.

My chart this week compares GLD’s daily gold holdings in metric tons with the gold price over the past several years or so. After falling to a major 6.1-year secular low in December 2015, gold started powering higher in a new bull market. Since gold hasn’t retreated 20%+ from its bull-to-date peak in July 2016, this bull remains alive and well. It has been overwhelmingly driven by American stock-market capital flows via GLD.

Let’s start in the middle of 2018, when GLD’s holdings were stable above 800t which has proven major support for this bull market. In much of the first half of last year, the stock markets were largely grinding sideways after the SPX suffered a sharp-yet-shallow-and-short correction in early February. The SPX finally started climbing decisively again in early Q3, ultimately achieving 5 new all-time record highs in that quarter.

That stoked incredible euphoria, convincing investors these amazing stock markets could rally indefinitely. By late September the SPX had skyrocketed 333.2% higher over 9.5 years, making for the 2nd-largest and 1st-longest stock bull in U.S. history! With general stocks looking invincible, there was little incentive to prudently diversify stock-heavy portfolios with gold. American stock investors were actually fleeing it.

In Q3 they sold GLD shares so aggressively that it forced a serious 76.8t or 9.4% draw in GLD’s holdings! All that selling pressure pushed world gold prices 4.9% lower that quarter. And GLD alone was mostly responsible. The WGC’s Q3 GDT showed total global gold demand actually grew a slight 0.6% year-over-year that quarter to 964.3t. Every major demand category grew considerably with a lone exception.

Global investment demand plunged 20.8% YoY to 194.9t. The WGC breaks it out into two major sub-categories, physical bar-and-coin demand and gold-ETF demand. The former was very strong, surging 28.0% YoY to 298.1t. But the latter plummeted from +13.2t in Q3’17 to -103.2t in Q3’18! Gold would’ve rallied nicely that quarter if not for GLD, which accounted for a commanding 2/3rds of that total world ETF drop.

When American stock investors are sustaining selling GLD shares faster than gold is being sold, it forces the world gold price lower. That serious Q3’18 GLD-holdings draw was the worst by far since back in Q4’16. That was when Trump’s surprise election victory with Republicans controlling both chambers of Congress ignited a major stock-market rally on hopes for big tax cuts soon. The resulting euphoria hammered gold.

While the SPX only climbed 3.3% in Q4’16, 8 new all-time record highs were achieved. American stock investors jettisoned gold with reckless abandon, both to chase that stock surge and out of relief that the political uncertainty didn’t trigger a stock selloff as feared. The differential GLD-share selling proved so intense that this ETF suffered a colossal 125.8t or 13.3% holdings draw, which crushed gold 12.7% lower!

Total world gold demand per the latest WGC GDT dropped 103.4t or 9.0% YoY that quarter. That huge GLD draw alone was 122% of that! Overall global gold-ETF demand fell 107.0t from -66.4t in Q4’15 to -173.4t in Q4’16. GLD’s draw was 118% of that. So literally the only reason gold plunged in Trump’s election quarter was American stock investors pulling big capital out of GLD forcing it to sell physical gold bullion.

Compared to that extreme dump, gold was relatively resilient in Q3’18. While GLD’s draw ran 61% of that Q4’16 episode, gold only declined 39% as much. There were hints the stock markets were ready to roll over into a long-overdue new bear. On Q3’s final trading day with the SPX just under its recent record peak, I published an essay explaining why Q4’s first-ever full-speed Fed QT was this stock bull’s death knell.

Indeed within a week of Fed QT ramping up to $50b per month of monetary destruction, the SPX started to falter. Its first serious down day erupted on October 10th when this leading stock-market benchmark plunged 3.3%. That triggered a major sentiment shift in gold. GLD enjoyed a large 1.2% holdings build that day on heavy differential GLD-share buying. Those were its first capital inflows at all since late July.

That very day American stock investors’ faith in perpetually-levitating stock markets started to crack, they started remembering gold. As Q4 wore on and that SPX selloff snowballed into a 4%+ pullback, a 10%+ correction, and narrowly missed new-bear-market territory at -19.8% on Christmas Eve, gold investment demand continued growing. Tending to rally when stocks fall, gold is essential for wisely diversifying portfolios.

By the time the dust settled on Q4, American stock-market capital sloshing back into gold via that GLD conduit had fueled a 45.4t or 6.1% holdings build. That was the biggest by far since way back in Q2’16 soon after this latest gold bull was born. All that differential GLD-share buying forced gold 7.6% higher in Q4 as the SPX plunged 14.0%. The WGC’s coming Q4’18 GDT will likely prove GLD largely drove gold’s gains.

The last time American stock investors started returning to gold after stock-market corrections spooked them was in the first half of 2016. Remember gold had just slumped to a major 6.1-year secular low, so it was deeply out of favor suffering incredibly-bearish sentiment. Yet in Q1’16 GLD’s holdings skyrocketed an epic 176.9t of 27.5% higher, which catapulted gold up 16.1%. Nothing else mattered per the WGC.

Overall world gold demand soared 188.1t or 17.1% YoY that quarter. GLD’s enormous build driven by American stock investors returning to gold accounted for an amazing 94% of that! If their vast pools of capital hadn’t sloshed back into gold via GLD that quarter, this bull never would’ve been born. And that utter dominance of American stock-market-capital inflows through GLD persisted in the subsequent quarter.

In Q2’16 gold surged another 7.4% higher on a 130.8t or 16.0% GLD-holdings build. The WGC reports that total world gold demand climbed 123.5t or 13.2% YoY that quarter. GLD’s huge build alone was responsible for 106% of that. So again without American stock-market capital moving into gold through that leading GLD conduit, that initial gold-bull upleg wouldn’t even exist. GLD dominates the gold world.

There have been 13 quarters since Q4’15 when today’s gold bull was born. 8 of them have seen major gold moves higher or lower. In all but one of these cases, GLD’s builds or draws accounted for the vast majority of the overall yearly change in total world gold demand. In the remaining 5 quarters where gold ground sideways or moved comparatively modestly, GLD’s holdings didn’t change very much either.

So there’s no doubt GLD’s strong build in Q4’18 ignited and fueled by this new SPX selloff is an important omen for gold. Once American stock investors start buying gold again via GLD shares in a big way, the resulting major gold uplegs tend to become self-feeding. Investors love chasing performance. The higher gold rallies, the more stock investors want to own GLD. And the more GLD they buy, the faster gold climbs.

And while correction-grade 10%+ stock-market selloffs are the catalysts that trigger renewed investment demand for gold, it usually persists well after the SPX bottoms and bounces. In essentially the first half of 2016, gold blasted 29.9% higher in just 6.7 months. That was totally fueled by an epic 351.1t or 55.7% build in GLD’s holdings as American stock investors rushed back into gold. That upleg peaked in early July.

But the 13.3% SPX correction that spawned it actually bottomed in mid-February. Over the following 4.9 months leading into gold’s top, the SPX blasted 16.4% higher! Nearly 3/4ths of gold’s upleg duration came after the stock selloff that ignited it, and just over 3/4ths of GLD’s upleg build also happened after the SPX had bottomed. Major gold uplegs take on a life of their own after being triggered by stock selloffs.

So even if today’s stock selloff ended at a severe correction on Christmas Eve and this record bull still has farther to run, gold investment demand should remain strong on upside momentum. But far more likely the long-overdue young new stock bear is being born. The SPX’s enormous and violent surge since that deep Christmas Eve low looks exactly like a classic bear-market rally technically, an ominous sign.

Bear-market rallies are the biggest and fastest ever witnessed in all of stock-market history. They soar out of major lows in sharp V-bounces on frantic short covering, then gradually run out of momentum over a couple to few weeks. If the stock markets are indeed rolling over into a new bear, far more weakness is guaranteed over the next couple years or so. That will fuel sustained gold-investment-demand growth.

Bear markets in stocks following major bulls are nothing to be trifled with. The last couple bears in the early and late 2000s saw the SPX fall 49.1% over 2.6 years and 56.8% over 1.4 years! 50% bears are common and expected after large bulls. And if we are early in the next bear, gold will likely be the top-performing asset class while it runs its course. American stock investors buying GLD shares will lead the way.

So far in January 2019, this huge apparent bear-market rally in the SPX has stalled investment demand for gold. Like many bear rallies, it has rekindled great greed and complacency. So GLD hasn’t experienced many significant builds yet in this young new year. But those capital inflows will return with a vengeance once the SPX starts rolling over and weakening again, likely driving gold sharply higher like in early 2016.

Again that sustained investment demand in H1’16 catapulted the yellow metal 29.9% higher pretty much exclusively on differential GLD-share buying. A mere 20% upleg off gold’s recent mid-August low driven by record gold-futures short selling would catapult it back up over $1400. Anything above the bull-to-date peak of $1365 in July 2016 is going to unleash a flood of new investor excitement in gold and big demand.

So this gold bull is likely to grow a lot larger in coming quarters. The greatest beneficiaries will be the gold miners’ stocks, as their profits leverage gold’s gains. Roughly during that mostly-H1’16 major gold upleg, the leading GDX and GDXJ gold-stock ETFs rocketed 151.2% and 202.5% higher! The better gold stocks with good fundamentals are going to soar again during gold’s next upleg, which is already well underway.

The earlier you get deployed, the greater your gains will be. That’s why the trading books in our popular weekly and monthly newsletters are currently full of better gold and silver miners mostly added in recent months. The gains we won in 2016 were amazing the last time American stock investors returned to gold. Our newsletter stock trades that year averaged +111.0% and +89.7% annualized realized gains respectively!

The gold-stock gains should be similarly huge in this next major gold upleg. The gold miners are the last undervalued sector in these still-very-expensive stock markets, and rally with gold during stock-market bears unlike anything else. To multiply your wealth in the stock markets you have to do your homework and stay abreast, which our newsletters really help. They explain what’s going on in the markets, why, and how to trade them with specific stocks. You can subscribe today for just $12 per issue!

The bottom line is gold investment demand began surging again in Q4, ignited by that major stock-market selloff. American stock investors started remembering gold, returning to GLD to diversify their portfolios which drove gold sharply higher. Once gold begins returning to favor after such major inflection points, its uplegs tend to grow large. Investment buying is self-feeding, with higher gold prices enticing in ever more capital.

Gold buying begets gold buying long after stock markets bounce, as investors love chasing performance. But odds are these lofty stock markets are now rolling over into a major new bear, portending much more weakness to come. Gold investment demand will thrive for years in that scenario, catapulting both gold and the stocks of its miners far higher. There’s no better place to multiply wealth during bear markets.

“Some analysts believe China could deliver 2 trillion yuan ($296.21 billion) worth of cuts in taxes and fees, and allow local governments to issue another 2 trillion yuan in special bonds largely used to fund key projects.” – CNBC News, Jan 15, 2019.

China’s economy is likely to grow in the 6.2%-6.5% range for 2019 and the stimulus is inflationary. While that growth is the slowest pace in almost thirty years, it’s still “head and shoulders” above the horrifying meltdown in growth that the United States is likely about to experience.

Please click here now. Goldman is predicting a meltdown in U.S. earnings growth from 20%+ in 2018 to just 3% to 6% for 2019!

Goldman’s heavyweight analysts are also predicting that US GDP growth melts towards 1% by the third quarter of this year. This, while Morgan Stanley is predicting an “earnings recession”.

Germany’s economy is already slipping towards 1% GDP growth and EU earnings are unlikely to grow more 5% in 2019.

Interestingly, most big bank economists are predicting an uptick in inflation will accompany the slide in Western earnings and GDP growth. Clearly, all roads lead to…gold!

On that note, please click here now. Double-click to enlarge. Gold continues to perform remarkably well at a time when a substantial pullback would be expected.

Conspiracy buffs are waiting for the “banksters” to smash the gold price. Where is the smash? Well, it doesn’t exist. All that’s happening is mild consolidation.

A pullback to key Fibonacci retracement lines in the $1250-$1260 area would be healthy but even that may not happen. Current technical action indicates a very healthy gold market.

Please click here now. Gold has raced to an all-time high against the Australian dollar. There’s a loose triangle pattern in play. The target of that pattern is well above $2000.

It’s very important for gold stock enthusiasts to make some effort to own at least a few Australian gold stocks that trade on Australian markets. Many of these stocks have been in powerful uptrends for years and are likely in a new acceleration phase.

Gold is also doing well against the British Pound and the Cbone (Canadian dollar). Most of the world’s gold stocks trade on the Canadian stock market and a lot of them are beginning to show good technical action.

Please click here now. Double-click to enlarge. The paint is barely dry on the Barrick-Rangold merger, and now Newmont is buying Goldcorp!

When mergers or takeovers happen, I like to see the new entity prove itself technically, with momentum. In the case of Barrick (GOLD-NYSE), I’ve suggested that investors need to see a weekly close of $14 for that to happen.

For Newmont, I need to see a weekly close of $36. That would suggest institutional money managers are endorsing the new entity. Once that happens I would be a buyer of every dollar of price weakness in the stock.

Both Barrick and Newmont are key GDX components. I’m impressed with the relative strength of GDX in the face of the softness in both those stocks.

Please click here now. Double-click to enlarge. While GDX “should” pull back to about $20 from the current price zone, the technical action is superb.

Note the fade in volume as price drifts sideways in the $21.50 resistance area. That’s extremely positive. Eager accumulators should be buyers of every ten cents of price weakness between $21 and $20.

Once the current consolidation ends, I’m anticipating a surge to the $23 price area… on strengthening volume.

Goldman’s influential gold market analyst Jeff Currie has a new $1425 target for gold in 2019. That’s an important number, because most gold and silver miners have made a significant effort to reduce their AISC (all-in sustaining cost) numbers.

A gold price in the $1400+ area would turn many of these companies into “cash cows”… and do so at a time when most companies in America face an earnings and revenue meltdown.

An institutional stampede into gold stocks in this new and emerging situation is not a pipe dream. It’s becoming more of a probable event than just a potential scenario.

Please click here now. Double-click to enlarge. My weekly gold chart shows that $1300 resistance is merely a pitstop on the road to the inverse H&S bottom neckline at about $1392.

If Goldman’s $1425 target price is achieved in 2019, it would mean gold has traded well above the neckline, ushering in a new target zone of about $1750. That $1750 price would turn most gold miners into not just cash cows, but cash cow superstars!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Golden Sweet Spot” report. I highlight six gold stocks trading the $3 to $7 price range that give investors an ideal mix of managed risk and potentially enormous reward! I include key buy and sell points for each stock.

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

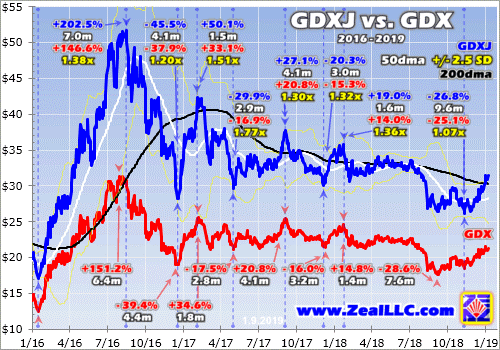

Gold miners’ exchange-traded funds are surging with gold powering higher. These mounting gains are naturally fueling growing interest in the leading gold-stock investment vehicles. Traders looking to deploy capital are wondering which major gold-stock ETF is superior, offering the best balance between upside potential, component fundamentals, and risks. GDXJ takes the crown, besting its larger big brother GDX.

By my count, there are currently 14 gold miners ETFs trading in U.S. markets. But that’s not authoritative, as the broader ETF industry is constantly in flux. These gold-stock ETFs collectively held $17.5b in net assets as of the middle of this week. And two major ETFs utterly dominated, commanding fully 85.1% of all those gold-stock investments! They are of course GDX and GDXJ, which dwarf everything else in this sector.

The GDX VanEck Vectors Gold Miners ETF and GDXJ VanEck Vectors Junior Gold Miners ETF hold net assets of $10.6b and $4.4b, or 60.2% and 24.9% of American gold-stock ETFs’ total. They have a huge and likely-insurmountable first movers’ advantage, being birthed way back in May 2006 and November 2009 respectively. They’ve gradually built great brand recognition, even being viewed as primary sector indexes.

When hedge funds report their equity holdings every quarter, if they have any gold-stock exposure GDX or GDXJ often top those lists. When gold miners are discussed on CNBC, GDX and to a lesser extent GDXJ are used in charts as sector benchmarks. VanEck’s popular pair of leading gold-miners ETFs are well-known to investors and speculators interested in this sector. They are effectively the only game in town.

With one company managing both GDX and GDXJ, and actively marketing them as a “Gold Miners ETF” and a “Junior Gold Miners ETF”, you’d think they are as different as their names imply. But unfortunately that’s not really the case. GDX and GDXJ hold many of the same component gold miners, with massive overlap in their holdings. And GDXJ’s definitely aren’t junior gold stocks, but actually larger mid-tier gold miners.

I’ve researched and written extensively on this. Every quarter I wade through the latest results from the top 34 component stocks of both GDX and GDXJ. The latest-available data is still Q3’18’s, as the full-year reports including Q4 aren’t due until 60 to 75 days after year-end depending on companies’ market capitalizations. As the recent Q3 earnings season wrapped up, GDXJ’s components were a subset of GDX’s.

GDXJ’s top 34 stocks accounted for 82.9% of its total weighting. And fully 31 of these components were also GDX components. These common gold miners across both ETFs weighed in at a massive 79.2% of GDXJ’s total weighting, and 31.7% of GDX’s. So nearly 4/5ths of this “Junior Gold Miners ETF” is made up by nearly 1/3rd of the major “Gold Miners ETF”. GDXJ is now a mid-tier gold miners ETF, not a junior one!

It wasn’t always this way, with GDXJ staying true to its advertised mission in its early years. But GDXJ became a victim of its own success in the first half of 2016. A young gold bull fueled skyrocketing gold-stock prices as traders flooded in to chase their rallies. GDXJ quickly grew so large that it risked running afoul of Canadian securities laws, where most of the world’s smaller gold miners’ and explorers’ stocks trade.

In the Canadian stock exchanges which are the centre of the junior-gold universe, an antiquated rule severely hobbles ETFs. Once any investor including ETFs acquires a 20%+ stake in any Canadian stock, it is legally deemed a takeover offer that must be extended to all shareholders! American stock-market capital flooding into GDXJ in early 2016 pushed many of its Canadian-junior ownership percentages near 20%.

Obviously hundreds of thousands of investors buying ETF shares have no intention of taking over gold-mining companies, no matter how big their collective stakes. That’s a totally-different scenario than a single corporate investor buying 20%+. Instead of lobbying Canadian regulators to exempt ETFs, GDXJ’s managers chose to unilaterally redefine what junior gold miners are. Stakes in Canadian juniors were slashed.

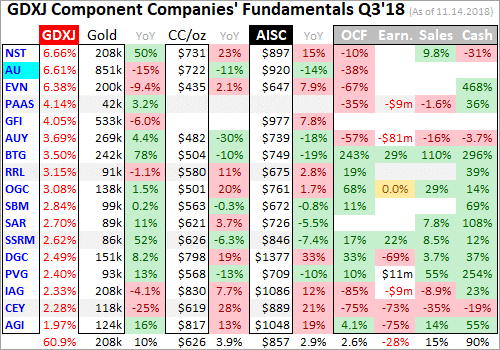

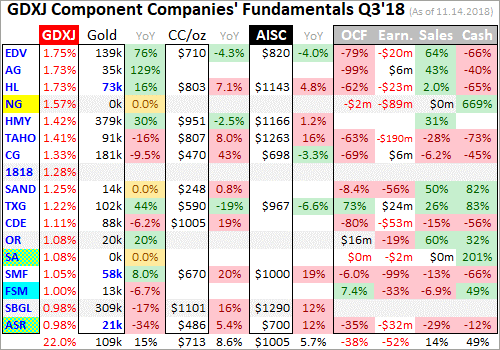

For decades juniors were often considered to be gold miners producing less than 200k ounces annually. To give GDXJ the benefit of the doubt, I conservatively expand that to 300k. That works out to 75k per quarter. In Q3’18, only 3 of the top 34 GDXJ component stocks were primary gold miners that met this junior threshold! The rest were mid-tier miners between 300k to 1m ounces per year, and even 1m+ majors.

GDXJ made these mission changes stealthily, knowing they would be controversial. It took me quarters to piece this all together, and I was an outspoken critic of the “Junior Gold Miners ETF” no longer being what it was billed as. But if you ignore the deceptive title, GDXJ has grown into an amazing mid-tier gold-miners ETF. It owns lots of the world’s best gold miners, which are given much-higher weightings than in GDX.

The mid-tier gold miners producing between 300k to 1m ounces per year are in the sweet spot for stock-price upside. Unlike the majors over 1m which are struggling with production declines, the mid-tiers are expanding existing mines and building new ones to boost their output and earnings. The mid-tier gold miners have smaller market caps too, making it much easier for capital inflows to bid up their stock prices.

Production is the lifeblood of the gold-mining industry, so traders often prize growth there above anything else when picking gold stocks. In Q3’18, the top 34 GDX gold miners including all the majors saw their total production decline 2.9% year-over-year to 9.5m ounces! That was stunning compared to the World Gold Council’s read on overall global gold mined that quarter, which actually grew a healthy 1.9% YoY.

GDX is heavily burdened by giant gold miners with shrinking production and high market caps, retarding its upside potential. GDXJ has some similar problems but to a lesser extent. Inexplicably GDXJ includes the major South African gold miners which are the worst in this industry for falling production and high mining costs. In Q3 four of them weighing in at 13.1% of GDXJ’s weighting suffered sizable production declines.

Excluding them and a fast-growing mid-tier gold miner that was oddly removed from GDXJ over the past year, the rest of the top 34 GDXJ gold miners achieved strong 3.4% YoY production growth in Q3! All the growth in the gold-mining industry is now coming from the mid-tier miners. GDXJ not only holds the best mid-tiers, but they have much-higher weightings than in the major-dominated GDX. GDXJ is the place to be.

In addition to the mid-tier gold miners’ growing production and lower market capitalizations, their mining costs are in line with the majors. In Q3 the top 34 GDX gold miners averaged all-in sustaining costs of $877 per ounce. The difference between that and prevailing gold prices shows industry profitability. The top 34 GDXJ gold miners had similar $911 AISCs in Q3. Without those South African majors, it was $877 too.

So if you can get past the fact GDXJ certainly isn’t a “Junior Gold Miners” ETF, it is superior to GDX in every way. The top 34 GDX stocks averaged 288.8k ounces mined in Q3, while GDXJ’s top 34 came in 43% lower at 163.3k. That’s still far above the 75k conservative junior threshold, but this mid-tier gold-miner range is where the vast majority of world production growth is happening. GDXJ action reflects this.

I’ve been writing about GDXJ outperforming GDX in my quarterly-results essays and newsletters for the better part of several years now. But until this week I hadn’t done the work to formally quantify GDXJ’s superior upside. I’ve been curious about it for some time, and have received more questions on it with gold stocks powering higher again. So I dug into this gold-stock bull’s GDXJ and GDX performances so far.

Since gold miners’ stocks are exceedingly volatile, bulls and bears in them are often delineated instead by gold itself. Today’s gold bull was born in December 2015 before surging in a powerful upleg in the first half of 2016. While gold has suffered a couple of serious corrections since, it never crossed that -20% new-bear threshold. So with gold in a continuous bull market for 3.1 years now, so too are the gold stocks.

They are effectively leveraged plays on gold since gold-mining profits directly amplify underlying moves in gold. The major gold stocks of GDX generally leverage gold uplegs and corrections by 2x to 3x. So if gold rallies 10%, GDX usually climbs 20% to 30%. Since GDX has become the leading benchmark for this entire sector, GDXJ’s performance is best considered relative to GDX’s. This chart summarizes it all.

GDX and GDXJ were both hammered to fundamentally-absurdall-time lows back in mid-January 2016 soon after gold’s own 6.1-year secular low. Ever since gold stocks have meandered in a series of bull-market uplegs and corrections. The performances of GDXJ and GDX in these recent years are rendered in blue and red below. Key stats are shown for each major gold ETF’s uplegs and corrections during that span.

The vertical light-blue lines divide up GDXJ’s uplegs and corrections, which generally match GDX’s but sometimes see major lows or highs out of sync. Each GDXJ upleg or correction shows GDXJ’s total gain or loss, the time that move took in months, GDX’s corresponding move over that identical span, and GDXJ’s leverage to GDX in yellow. The actual full GDX uplegs and corrections are also shown below in red.

Even in today’s young, delayed, mostly-unpopular, and weak gold-stock bull, GDXJ has outperformed GDX by a wide margin. And that’s despite GDXJ morphing from being a true junior-gold-miner ETF in the first half of 2016 to a mid-tier gold-miner ETF over the subsequent year. Even holding bigger gold miners, their superior fundamentals to the struggling majors have enabled GDXJ to keep the performance crown.

In just 6.4 months in largely the first half of 2016, gold stocks as measured by GDX skyrocketed 151.2% higher on a 29.9% gold upleg. GDXJ well-outperformed GDX in roughly that same span, blasting 202.5% higher in 7.0 months! GDX actually rallied 146.6% within GDXJ’s exact upleg, showing the mid-tier gold-stock ETF leveraged the major gold-stock ETF’s massive upleg by a solid 1.38x. GDXJ’s upside bested GDX’s.

Gold’s powerful initial upleg was followed by a massive correction in the second half of 2016, where it plunged 17.3% after Trump’s surprise election victory unleashed a huge stock-market surge on hopes for big tax cuts soon. The gold-stock carnage as gold plunged was great, with GDXJ plummeting 45.5% in just 4.1 months. Interestingly that leveraged GDX’s downside by 1.20x, much less than in the preceding upleg.

Ever since, the gold stocks have been mostly stuck in a big consolidation trading range. Enthusiasm for this sector waned to nothing as general stocks kept powering higher in recent years which relegated gold to drift sideways as well. While this extraordinary gold-stock-bull disruption was highly unusual, it was the result of record U.S. corporate tax cuts levitating the stock markets. That one-off event finally passed in 2018.

If you go through all this gold-stock bull’s uplegs, GDXJ’s gains outpaced GDX’s by an average of 1.39x! Ranging from 1.30x on the low side to 1.51x on the high side, there was not a single gold-stock upleg in recent years where GDXJ didn’t majorly outperform GDX. Taking GDX’s usual 2x to 3x leverage to gold and adding another 39% of marginal GDXJ gains on top of that is impressive. What trader wouldn’t want that?

GDXJ’s much-superior upside in this young bull is also accompanied by outsized downside relative to GDX during gold-stock corrections. That’s logical, as bigger mid-tier gold-stock gains in preceding uplegs leave more room to sell off in subsequent corrections. Interestingly though, GDXJ’s downside leverage averaging 1.34x is a bit lower than its upside leverage in uplegs. That is skewed to the high side as well.

It ranged from a low of 1.07x in the latest gold-stock selloff last summer and autumn to a staggering 1.77x in spring 2017. That outlier was the result of GDXJ’s gold miners surging far faster than GDX’s in early 2017. Without that anomaly, GDXJ’s downside leverage to GDX during corrections averages only 1.20x. That is merely about half its upside leverage, so GDXJ’s added risks are disproportionally smaller than its better upside.

Given all this, there is really no reason to bother with GDX at all if you are deploying capital in major gold-stock ETFs. GDXJ has better mid-tier gold miners growing their production while trading at lower market caps than the struggling majors. GDXJ has demonstrated much-better upside during gold-stock uplegs throughout this young bull, yet its downside during corrections isn’t proportional. GDXJ is far superior.

That being said, investors and speculators are much better off avoiding these major gold ETFs entirely! While GDXJ is nowhere near as bad as GDX, both are still burdened by major gold miners with declining production and rising costs. It doesn’t make any sense to own such laggards when they can be avoided entirely in favor of mid-tiers and true juniors with great fundamentals like growing production and stable costs.

The best strategy for riding this reaccelerating gold bull to wealth-multiplying gains in gold stocks is to carefully handpick the best mid-tier gold miners mostly included in GDXJ. Every quarter I break out this ETF’s top 34 and look at their production, costs, operating cash flows, earnings, and sales trends among others. That exercise helps separate the gold miners with better fundamentals from the lagging weaker ones.

So instead of just settling and owning GDXJ, even-better gains are highly probable by sticking to mid-tiers and juniors with superior fundamentals. They rank lower in GDXJ’s weightings and are usually growing their production organically or through new mine builds that recently came online or will soon be live. With plenty of great gold miners in this sector, there’s simply no need to hold the laggards retarding even GDXJ.

With gold stocks now enjoying a major upside breakout, massive new investment buying is coming. And the best gains by far will be won in smaller mid-tier and junior gold miners with superior fundamentals. While GDXJ itself will power dramatically higher despite some deadweight in its holdings, the better gold miners will generate much-greater wealth creation. Finding and owning these better gold-mining stocks is essential.

That’s one of my important missions at Zeal, relentlessly studying the gold-stock world to uncover the stocks with the greatest upside potential. The trading books in both our weekly and monthly newsletters are currently full of these better gold and silver miners. Most of these trades are relatively new, added in recent months as gold stocks recovered from deep lows. So it’s not too late to get deployed ahead of big gains!

To multiply your wealth in stocks you have to do some homework and stay abreast, which our popular newsletters really help. They explain what’s going on in the markets, why, and how to trade them with specific stocks. Walking the contrarian walk is very profitable. As of Q3, we’ve recommended and realized 1045 newsletter stock trades since 2001. Their average annualized realized gain including all losers is +17.7%! That’s double the long-term stock-market average. Subscribe today for just $12 per issue!

The bottom line is GDXJ’s upside easily bests GDX’s. While GDXJ is now really a mid-tier gold miners ETF instead of the junior one advertised, it holds some of the world’s best gold miners. Unlike struggling majors which dominate GDX, plenty of mid-tiers are still growing their production. They enjoy superior fundamentals and are weighted much more heavily in GDXJ than GDX, giving it much-better potential gains.

Throughout this entire young gold bull of recent years, GDXJ has well-outperformed GDX during gold-stock uplegs. While that has also led to bigger downside during corrections, it is disproportionally small compared to the upleg gains. GDXJ simply offers superior gold-stock sector exposure than GDX. But both these major gold-stock ETFs are still burdened with laggards dragging down their overall performances.

As we’ve been saying, the stock market will have great influence on Gold. It has been easy to see in recent months.

The S&P 500 has cracked, losing both its 200-day and 400-day moving averages. Gold and gold stocks have benefitted and gained in recent months even with a stable to rising U.S. Dollar.

The past 65 years of history shows us that in almost any context (but not all) the time between the Fed’s last rate hike and first rate cut is exactly when you want to buy gold stocks.

We don’t know if December is the last rate hike. No one does.

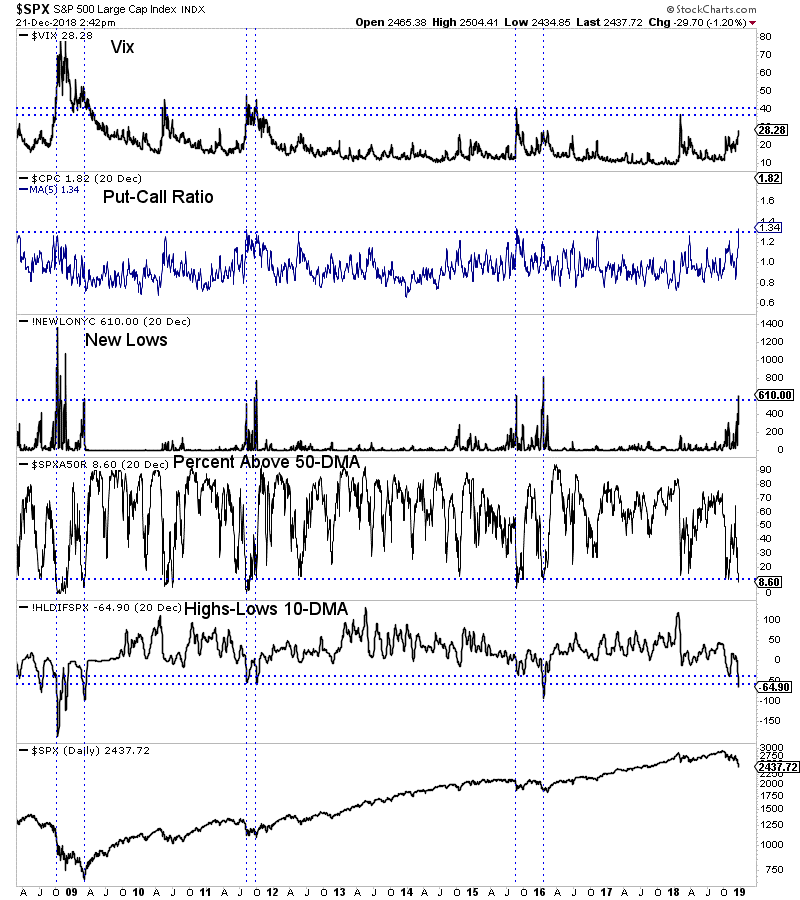

What we do know is the stock market is approaching an extreme oversold condition and is likely to begin a counter trend rally very soon.

In the chart below we plot five indicators that can help define an extreme oversold condition. These include the Vix, the put-call ratio and several breadth indicators. All but the Vix are in extreme oversold territory.

As we pen this article, the S&P 500 is trading at 2436.

The 40-month moving average, which has provided key support and resistance over the past 20 years (including the 2016 and 2011 lows) is at 2395 while the 50% retracement of the 2016 to 2018 advance is at 2380.

The setup for a bullish reversal is in place.

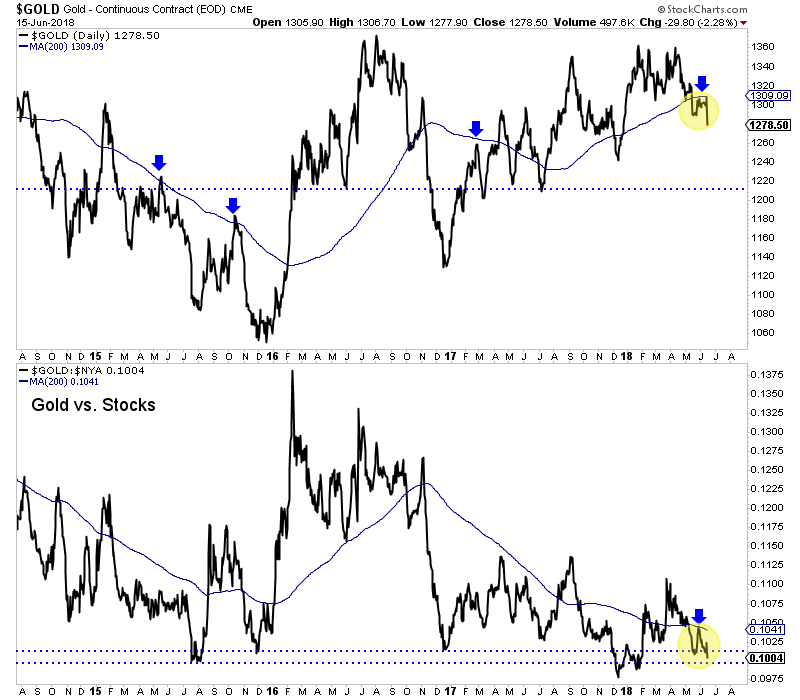

Meanwhile, despite the recent carnage in stocks, precious metals have been unable to surpass resistance.

Gold is set to close the week right below a confluence of resistance at $1260-$1270. Perhaps it will close right on its 200-day moving average at $1258.

The gold stocks (GDX, GDXJ) have been strong since Thanksgiving but appear to have been turned back at their 200-day moving averages.

So in recent days the selloff in the S&P 500 accelerated but precious metals (at least to this point) failed to capitalize in a bullish fashion.

If the S&P 500 is within one or two days of a rally then we should not expect much more upside in Gold and GDX in particular. Those were the markets that benefited most from weakness in the S&P 500.

As we noted last week, the weakness in the stock market (and the economy) has not done enough to change Fed policy yet.

Over the past 65 years, the start of bull markets and big rallies in gold stocks coincided with the start of rate cuts. When the market sniffs the first rate cut, we will know precious metals are beginning a sustained advance and not another false start.

The recent stock-market selloff is persisting, fueling mounting worries among investors. The intensifying volatility and lack of a quick rebound higher is strangling euphoric sentiment, spawning self-reinforcing selling pressure. Scoffed at a few months ago, the notions that a young bear market is underway and a recession looms are gaining traction. The great beneficiary of this ominous stock-market downturn will be gold.

Gold has always been an essential asset class for prudently diversifying investment portfolios. Uniquely it tends to rally when stock markets weaken, offsetting some of the losses in typical stock-heavy portfolios. Gold acts like portfolio insurance, usually soaring when stock markets plunge on unforeseen news. All throughout history, wise investors have recommended everyone have 5% to 10% of their portfolios in gold.

But like insurance in general, the important role gold plays in portfolios is gradually forgotten when it isn’t needed. Just a few months ago, the U.S. stock markets seemed invincible. The flagship S&P 500 broad-market stock index (SPX) had powered 333.2% higher over 9.5 years by late September. That made for the 2nd-largest and 1st-longest stock bull in U.S. history! Investors were convinced that would last indefinitely.

The SPX had surged 9.6% year-to-date by that latest peak, while gold had slumped 7.3%. Thus investors felt no need to allocate virtually any capital to gold, they were and are radically underinvested in it. This is especially true of American stock investors, who were wildly optimistic after long years of big stock-market gains. Their effective portfolio exposure to gold was vanishingly small back in late September.

The 500 elite stocks of the SPX had an extreme collective market capitalization way up at $26,141.4b as that topping month waned. It is interesting contrasting that with the physical gold bullion holdings of the world’s dominant gold exchange-traded fund, the American GLD SPDR Gold Shares. GLD has long been the go-to destination for American stock investors looking to allocate capital for gold exposure in their portfolios.

At the end of September as stock euphoria peaked, GLD’s total holdings were merely worth $28.4b. That implies American stock investors were running trivial gold allocations around 0.11%! That’s on the order of only 1/50th the minimum 5% that’s been universally advised for centuries if not millennia. So it’s not much of a stretch to argue American stock investors had zero gold exposure, they were effectively all-out.

The sharp stock-market selloff in the few months since those halcyon all-time record highs has surprised most, but it shouldn’t have. As Q4’18 dawned, something ominous happened that was unprecedented in stock-market history. The US Federal Reserve upped its quantitative-tightening campaign necessary to start unwinding its $3625b of quantitative-easing money creation over 6.7 years to its terminal velocity.

October 2018 would be the first month ever to see the Fed’s monetary destruction ramp to a staggering $50b-per-month pace. And even to unwind just half of the Fed’s radical QE, QT would have to keep on destroying $50b per month of QE-conjured money for 30 months! At the end of September when the SPX was just 0.6% off its all-time record high, I explained all this in depth warning it was this bull’s death knell.

And indeed within a week of Fed QT going full-throttle, the SPX started to slide. There was no way QE-levitated stock markets could ignore QT obliterating that QE money. Every daily selloff since had its own unique story and specific drivers, which I discussed and analyzed in our subscription newsletters. These all added up to enough selling to spawn an ongoing stock-market correction, an SPX selloff exceeding 10%.

Blame it on Fed QT, stock-market bubble valuations, mounting US-China trade-war threats, Republicans losing the House, or whatever you want, but by Black Friday the SPX had fallen 10.2% over 2.1 months since that euphoric record peak. The stock markets staged some sharp rallies within that span, but they quickly fizzled proving to be dead-cat bounces. This recent action is ominously looking very bear-market like.

We can’t know for sure whether the long-overdue new bear market driven by epic record Fed tightening is indeed upon us until the SPX falls 20%+ on a closing basis. This recent correction would still have to double to hit that bear-market threshold. But gold has certainly been the main beneficiary of the recent stock-market weakness. Investors are starting to remember the ages-old wisdom of diversifying into gold.

This week’s chart looks at the US-dollar gold price superimposed over the SPX during the past 4 years or so. Despite gold being forgotten in recent years as the stock markets surged ever higher, it remains in a young bull market. And that was spawned by the last set of back-to-back corrections in the SPX, which catapulted gold sharply higher. We’re likely on the verge of another stock-selloff-driven major gold upleg!

GLD’s physical-gold-bullion holdings held in trust for its shareholders reveal how American stock investors feel about gold. This past spring they started slumping as gold was sold to move even more capital into the lofty US stock markets. For 5 months in a row ending in September, GLD’s holdings retreated as investors dumped GLD shares faster than gold was falling. By early October GLD’s holdings hit a 2.6-year low.

I penned a whole essay on this stock-euphoria-driven gold exodus in late September, explaining why it was happening and why it was likely to soon reverse. And that shift in gold-investment sentiment began the very day the SPX started plunging in mid-October! Up until October 9th the stock markets looked totally normal, the SPX had only drifted a trivial 1.7% lower from its peak. Everyone remained wildly bullish.

But something snapped on October 10th, that fateful day the SPX plunged 3.3% out of the blue on no catalyst at all. Heavy technically-motivated selling accelerated led by the market-darling mega tech stocks. For years investors had believed them bulletproof, their businesses so good they could weather any stock selloff or economic slowdown. Fears surged on the worst SPX down day since back in early February.

That very day American stock investors started returning to gold. They poured capital into GLD shares so aggressively they forced a major 1.2% holdings build. GLD’s mission is to track the gold price, but it has its own supply-and-demand profile independent from gold’s. So when GLD shares are being purchased faster than gold is bought, GLD’s share price threatens to decouple to the upside on that excess demand.

So GLD’s managers must vent that differential buying pressure directly into the physical gold market in order to equalize it and maintain tracking. They do this by issuing enough new GLD shares to satisfy all the excess demand, and then plow the cash proceeds into gold bullion. Thus rising GLD holdings show American stock-market capital is flowing into gold. That proved to be GLD’s biggest build in 6.7 months.

That fateful day proved a major inflection point for both near-record US stock markets and the extremely-unpopular gold. As the SPX continued to weaken over the next couple months, GLD continued to enjoy modest builds on investment gold buying. By late November GLD’s holdings had climbed a considerable 4.5% over 6 weeks. That has helped push gold 5.5% higher since its mid-August lows, a solid young upleg.

Odds are that gold buying via GLD by American stock investors is only beginning. The longer this stock-market weakness persists, the deeper their worries will grow. And the more their stock-heavy portfolios bleed, the quicker they will remember they should’ve allocated 5% to 10% to gold. Once gold investment demand is kindled by falling stock markets, it tends to balloon dramatically and take on a life of its own.

Gold’s young bull market today that was forgotten this summer began as 2016 dawned. Much like this year, in the first half of 2015 the US stock markets were powering to dazzling new record highs. Since it seemed like stocks could do nothing but rally indefinitely, gold was forgotten and shunned. It slumped to a brutal 6.1-year secular low by mid-December 2015, with investors really wanting nothing to do with it.

But their ironclad euphoria started to crack soon after the stock markets corrected. In mid-2015 the SPX finally suffered its first correction in an incredibly-extreme 3.6 yearsafter being levitated by relentless Fed money creation from its third quantitative-easing campaign. Gold caught a bid on that 12.4% SPX selloff over 3.2 months, but then faded again into the expected first Fed rate hike in 9.5 years in mid-December.

Then the SPX fell into another 13.3% correction over 3.3 months into early 2016. Seeing menacing back-to-back corrections after long years without one really deflated gold-suppressing stock-market euphoria. So in early 2016 American stock investors began prudently rediversifying their stock-dominated portfolios into gold. That birthed today’s gold bull, and the gold-buying momentum fed on itself to drive a powerful upleg.

Gold went from being left for dead in mid-December 2015 to surging 29.9% higher in just 6.7 months solely on American stock investors returning! This is no generalization, the hard numbers prove it without a doubt. The world’s best gold fundamental supply-and-demand data comes from the venerable World Gold Council. It releases fantastic quarterly reports detailing the global buying and selling happening in gold.

Gold blasted higher on SPX weakness in Q1’16 and Q2’16. According to the latest data from the WGC, total world gold demand climbed 188.1 and 123.5 metric tons year-over-year in those key quarters. That was up 17.1% and 13.2% YoY respectively! But the real stunner is exactly where those major demand boosts came from. It wasn’t from jewelry buying, central-bank buying, or even physical bar-and-coin investment.

In Q1’16 and Q2’16, GLD’s holdings alone soared 176.9t and 130.8t higher on American stock investors redeploying into gold after back-to-back SPX corrections. Incredibly this one leading gold ETF accounted for a staggering 94% of overall global gold demand growth in Q1’16 and 106% in Q2’16! So there’s no doubt without American stock investors fleeing into gold via GLD this gold bull never would’ve been born.

Gold was holding those sharp gains throughout 2016 until Trump’s surprise presidential victory unleashed a monster stock-market run on hopes for big tax cuts soon. Gold was pummeled in Q4’16 as American stock investors pulled capital back out to chase the newly-soaring SPX. That quarter total global gold demand per the WGC fell 103.4t YoY or 9.0%. GLD’s 125.8t Q4’16 holdings draw accounted for 122% of that!

Gold’s fortunes are being driven by American stock investors’ collective buying and selling of GLD shares. And nothing motivates them to redeploy capital into gold to diversify their stock-heavy portfolios like major SPX selloffs. Recent months’ one has already proven serious enough to rekindle differential GLD-share buying. And as H1’16 proved, once investors start driving gold higher its rallies tend to become self-feeding.

The more physical gold bullion American stock investors buy via GLD shares, the more gold climbs. The higher gold rallies, the more investors want to buy it to ride the momentum and chase its gains. So buying begets buying, driving gold higher fairly rapidly. And when stock markets are sliding, gold is often the only asset class rallying. That makes it even more attractive to investors getting pounded by sliding stocks.

This latest SPX correction is even more damaging to sentiment because it is 2018’s second one. Back in early February the SPX plunged 10.2% in 0.4 months, which started to crack sentiment. Back when this gold bull was born it was the second of back-to-back SPX corrections that proved the coup de grâce in hurting stock-market sentiment enough to unleash a reallocation into gold. This scenario is playing out again.

Provocatively seeing the three major US stock indexes suffer two 10%+ corrections within any single calendar year is itself a super-bearish omen. 2018 joined 1973, 1974, 1987, 2000, 2001, 2002, and 2008 as the SPX’s only other dual-correction years. Those coincided with a 48.2% SPX bear, a 20.5% single-day SPX crash, another 49.1% SPX bear, and a third 56.8% SPX bear! All three bears triggered recessions.

This stock-market weakness isn’t only likely to persist, but the odds really favor it snowballing into another major SPX bear market. Gold investment demand will naturally surge as stocks burn, fueling a strong bull market. Gold’s 29.9% gain over 6.7 months at best so far in this bull is nothing. Gold’s last secular bull from April 2001 to August 2011 saw it soar 638.2% higher! Gold’s gains as the SPX rolls over should be massive.

With a trivial 0.1% portfolio allocation to gold, what happens to gold prices if American stock investors just return to a still-immaterial 1.0%? That’s still way under the 5% to 10% recommended in normal times, and plenty of great investors believe 20% gold allocations are necessary during stock bears. Gold’s upside from here with virtually-zero US-stock-market capital allocated to it is vast. And it could accelerate rather fast.

The timing of this current SPX correction is likely to magnify bearish psychology. It has occurred entirely within Q4’18. The SPX exited Q3’18 just 0.6% off its record peak from a week earlier. So I suspect a lot of American retirement investors have no idea just how much carnage their precious capital has suffered. When they get their quarterly statements from their money managers in January, they could really freak out.

Even worse, far too much of this retirement capital was allocated to the market-darling mega techs which were the biggest holdings across most funds. Their losses have far outpaced the SPX’s. As of that latest correction low on Black Friday when the SPX was down 10.2%, Apple, Amazon, Microsoft, Alphabet, Facebook, and Netflix had collapsed 25.8%, 26.4%, 10.8%, 19.9%, 39.4%, and 38.2% from their all-time highs!

The mega techs that nearly single-handedly pushed the SPX higher for years averaged 26.8% losses, or 2.6x the SPX’s! When investors who don’t closely follow the stock markets figure that out next month, the investment demand for rallying gold ought to explode. The first half of 2019 has a setup much like H1’16, where gold essentially powered 30% higher. A similar upleg from mid-August’s lows isn’t a stretch at all.

Another 30% run from $1174 would leave gold at $1525. And once gold climbs decisively back over its bull-to-date high of $1365 from early-July 2016, investment interest and demand will soar. Just like the mega tech stocks, the higher gold prices the more investors want to buy it. A mere 16% gold upleg off August’s lows, or another 10% higher from this week’s levels, would near that psychologically-huge bull breakout!

All investors should always have 5% to 10% of their investable capital allocated to gold. But almost none do today as a long-overdue bear market fueled by epic record Fed QT looms. If you don’t have that core gold allocation, you need to get it in place before stocks fall much farther and gold surges much higher. The gold miners’ stocks will greatly leverage gold’s gains too, their leading index soared 182.2% largely in H1’16!

Absolutely essential in bear markets is cultivating excellent contrarian intelligence sources. That’s our specialty at Zeal. After decades studying the markets and trading, we really walk the contrarian walk. We buy low when few others will, so we can later sell high when few others can. While Wall Street will deny the coming stock-market bear all the way down, we will help you both understand it and prosper during it.

We’ve long published acclaimed weekly and monthly newsletters for speculators and investors. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. As of Q3, we’ve recommended and realized 1045 newsletter stock trades since 2001. Their average annualized realized gain is +17.7%! That’s double the long-term stock-market average. Subscribe today and take advantage of our 20%-off holidays sale!

The bottom line is this stock selloff is boosting gold. Flagging gold investment demand turned on a dime when the stock markets started plunging in mid-October. Gold has rallied on balance since as American stock investors start redeploying capital. Their buying alone via GLD shares was fully responsible for gold’s sharp 30% upleg in 2016’s first half. That followed the last back-to-back corrections in US stock markets.

And between record Fed tightening running full-throttle, continuing dangerous bubble valuations, and the mounting trade wars, this recent stock selling is likely to persist on balance. So gold investment will look far more attractive. Coming from virtually-zero gold portfolio allocations, investors have massive buying to do. The higher they push gold, the more other investors will chase it. Especially as US stock markets weaken.

The junior gold miners’ stocks have spent recent months mostly languishing near major multi-year lows. That spawned a sentiment wasteland riddled by bearishness and bereft of bids. But these companies’ battered stock prices aren’t fundamentally righteous, as proven yet again by their latest earnings season. Faring far better in a challenging third quarter than stock prices imply, they need to mean revert way higher.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the U.S. Securities and Exchange Commission by 40 calendar days after quarter-ends. Canadian companies have similar requirements at 45 days. In other countries with half-year reporting, many companies still partially report quarterly.

The definitive list of elite “junior” gold stocks to analyze comes from the world’s most-popular junior-gold-stock investment vehicle. Mid-month the GDXJ VanEck Vectors Junior Gold Miners ETF reported $4.1b in net assets. Among all gold-stock ETFs, that was second only to GDX’s $9.0b. That is GDXJ’s big-brother ETF that includes larger major gold miners. GDXJ’s popularity testifies to the great allure of juniors.

Unfortunately this fame created serious problems for GDXJ a couple years ago, resulting in a stealthy major mission change. This ETF is quite literally the victim of its own success. GDXJ grew so large in the first half of 2016 as gold stocks soared in a massive upleg that it risked running afoul of Canadian securities laws. And most of the world’s smaller gold miners and explorers trade on Canadian stock exchanges.

Since Canada is the centre of the junior-gold universe, any ETF seeking to own this sector will have to be heavily invested there. But once any investor including an ETF buys up a 20%+ stake in any Canadian stock, it is legally deemed to be a takeover offer that must be extended to all shareholders! As capital flooded into GDXJ in 2016 to gain junior-gold exposure, its ownership in smaller components soared near 20%.

Obviously hundreds of thousands of investors buying shares in an ETF have no intention of taking over gold-mining companies, no matter how big their collective stakes. That’s a totally-different scenario than a single corporate investor buying 20%+. GDXJ’s managers should’ve lobbied Canadian regulators and lawmakers to exempt ETFs from that 20% takeover rule. But instead they chose an inferior, easier fix.

Since GDXJ’s issuer controls the junior-gold-stock index underlying its ETF, it simply chose to unilaterally redefine what junior gold miners are. It rejiggered its index to fill GDXJ’s ranks with larger mid-tier gold miners, while greatly demoting true smaller junior gold miners in terms of their ETF weightings. This controversial move defying long decades of convention was done quietly behind the scenes to avoid backlash.

There’s no formal definition of a junior gold miner, which gives cover to GDXJ’s managers pushing the limits. Major gold miners are generally those that produce over 1m ounces of gold annually. For decades juniors were considered to be sub-200k-ounce producers. So 300k ounces per year is a very-generous threshold. Anything between 300k to 1m ounces annually is in the mid-tier realm, where GDXJ now traffics.

That high 300k-ounce-per-year junior cutoff translates into 75k ounces per quarter. Following the end of the gold miners’ Q3’18 earnings season in mid-November, I dug into the top 34 GDXJ components’ results. That’s simply an arbitrary number that fits neatly into the tables below. Although GDXJ included a staggering 70 component stocks mid-month, the top 34 accounted for a commanding 82.9% of its total weighting.

Out of these top 34 GDXJ companies, only 3 primary gold miners met that sub-75k-ounce-per-quarter qualification to be a junior gold miner! Their quarterly production is rendered in blue below, and they collectively accounted for just 3.8% of this ETF’s total weighting. GDXJ is inarguably now a pure mid-tier gold-miner ETF, not a junior one. But its holdings include the world’s best gold miners with huge upside potential.

I’ve been doing these deep quarterly dives into GDXJ’s top components for years now. In Q3 2018, fully 31 of the top 34 GDXJ components were also GDX components! These are separate and distinct ETFs, a “Gold Miners ETF” and a “Junior Gold Miners ETF”. So they shouldn’t have to own many of the same companies. In the tables below I highlighted the symbols of rare GDXJ components not also in GDX in yellow.

These 31 GDX components accounted for 79.2% of GDXJ’s total weighting, not just its top 34. They also represented 31.7% of GDX’s total weighting. Thus nearly 4/5ths of this “Junior Gold Miners ETF” is made up by nearly 1/3rd of the major “Gold Miners ETF”! These GDXJ components also in GDX are clustered from the 11th- to 30th-highest weightings in that latter larger ETF. GDXJ is mostly smaller GDX stocks.

In a welcome change from GDXJ’s vast component turmoil of recent years, only 4 of its top 34 stocks are new since Q3 2017. Their symbols are highlighted in light blue below. Thus the top GDXJ components’ collective results are finally getting comparable again in year-over-year terms. Analyzing ETFs is much easier if their larger components aren’t constantly in flux. Hopefully changes going forward are relatively minor.

Despite all this, GDXJ remains the leading “junior-gold” benchmark. So every quarter I wade through tons of data from its top components’ latest results, and dump it into a big spreadsheet for analysis. The highlights make it into these tables. Most of these top 34 GDXJ gold miners trade in the US and Canada, where comprehensive quarterly reporting is required by regulators. But others trade in Australia and the UK.

In these countries and most of the rest of the world, regulators only mandate that companies report their results in half-year increments. Most do still issue quarterly production reports, but don’t release financial statements. There are wide variations in reporting styles, data presented, and release timing. So blank fields in these tables mean a company hadn’t reported that particular data for Q3 2018 as of mid-November.

The first couple columns of these tables show each GDXJ component’s symbol and weighting within this ETF as of mid-November. While just over half of these stocks trade on US exchanges, the other symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each gold miner’s Q3’18 production in ounces, which is mostly in pure-gold terms excluding byproduct metals often found in gold ore.

Those are usually silver and base metals like copper, which are valuable. They are sold to offset some of the considerable costs of gold mining, lowering per-ounce costs and thus raising overall profitability. In cases where companies didn’t separate out gold and lumped all production into gold-equivalent ounces, those GEOs are included instead. Then production’s absolute year-over-year change from Q3’17 is shown.

Next comes gold miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated, hard GAAP earnings, sales, and cash on hand with a couple exceptions.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. This whole dataset together offers a fantastic high-level read on how the mid-tier gold miners as an industry are faring fundamentally. They actually did relatively well in Q3.

While this new mid-tier GDXJ is generally excellent, some decisions by its managers are utterly baffling. Out of all the world’s gold miners they could’ve added over this past year, they inexplicably decided on the giant largely-African AngloGold Ashanti. It produced an enormous 851k ounces of gold last quarter, the largest in GDXJ by far. It and the rest of the South African majors definitely don’t belong in GDXJ!

Remember that major-gold-miner threshold has long been 1m+ ounces per year. AU’s production is annualizing to well over 3x that, making this company the world’s 3rd-largest gold miner last quarter. Why on earth would managers running a “Junior Gold Miners ETF” even consider AngloGold Ashanti? It is as far from junior-dom as gold miners get. The same is true with the rest of the troubled South African gold miners.

AU, Gold Fields, Harmony Gold, and Sibanye-Stillwater mined 851k, 533k, 379k, and 309k ounces in Q3’18, all are majors. Yet they accounted for 13.1% of GDXJ’s total weighting. They are riddled with all kinds of problems too, from shrinking production to high costs to increasing stealth expropriations from South Africa’s openly-Marxist anti-white-investor government. Their inclusion heavily skews and taints GDXJ.

These South African majors’ Q3 production of 2.1m ounces was a whopping 41% of the GDXJ top 34’s total! And it still fell 7.0% YoY due to South Africa’s tragic death spiral. Excluding them and the amazing Kirkland Lake Gold which has grown so fast it was moved exclusively into GDX over this past year, the rest of the GDXJ top 34 grew production 3.4% YoY in Q3. The South African majors’ cost impact is even worse.

Mining in that country is very expensive thanks to very-old very-deep mines and endless new government interference via stifling regulations. In Q3 the South African majors’ cash and all-in sustaining costs came in really high averaging $925 and $1088 per ounce. The rest of GDXJ’s top 34 averaged $629 and $877, a massive 32.0% and 19.4% lower! The South African majors are really retarding GDXJ’s performance.

As struggling majors far larger than mid-tiers and juniors, they need to get kicked out of GDXJ posthaste. They can be left in GDX where they belong. AU effectively took KL’s place, which makes no sense at all fundamentally. Kirkland Lake produced 180k ounces of gold in Q3 at $351 cash costs and $645 AISCs. So unlike AU, KL remains solidly in the mid-tier realm and has been performing incredibly well operationally.

While GDXJ’s managers really dropped the ball including those South African majors, they deserve big praise for upping the weighting of the outstanding Australian miners. They are Northern Star Resources, Evolution Mining, Regis Resources, St Barbara, and Saracen Mineral. Their collective weighting in GDXJ grew to 21.7% at the end of Q3’s earnings season, nearly 2/3rds higher from their 13.3% a year earlier.

Unlike AU’s dumbfounding inclusion, the Australians’ rise is well-deserved. Their production surged 8.9% YoY to 686k ounces, or 23% of the GDXJ top 34’s total excluding those South African majors. And the Australian miners are masters at developing great gold deposits and controlling costs, as their cash costs and AISCs in Q3 averaged just $586 and $724! It’s fantastic GDXJ offers American investors this Aussie exposure.

GDXJ’s component list and weightings are a work in progress, and are gradually getting better. For years I’ve pointed out things like the South African majors that weren’t right, and GDXJ’s managers eventually seem to come around and change things for the better. Greatly helping that process is investors buying the better individual stocks like KL and shunning laggards like AU, readjusting their relative market capitalizations.

GDXJ and GDX are essentially market-cap weighted, with larger companies rightfully commanding larger weightings. These leading gold-stock ETFs’ managers can override this by deciding which gold miners to include in each ETF. So they can easily purge GDXJ of the deteriorating South African majors and add real mid-tier gold miners. But the true core problem is having so many of the same stocks in GDX and GDXJ.

Such massive overlap between these two ETFs is a huge lost opportunity for VanEck. It owns and manages GDX, GDXJ, and even the MVIS indexing company that decides exactly which gold stocks are included in each. With one company in total control, there’s no need for any overlap in the underlying companies of what should be two very-different gold-stock ETFs. Inclusion ought to be mutually-exclusive.

VanEck could greatly increase the utility of its gold-stock ETFs and thus their ultimate success by starting with one big combined list of the world’s better gold miners. Then it could take the top 20 or 25 in terms of annual gold production and assign them to GDX. Based on Q3’18 production, that would run down near 139k or 93k ounces per quarter. Then the next-largest 40 or 50 gold miners could be assigned to GDXJ.

Getting smaller gold miners back into GDXJ would be a huge boon for the junior-gold-mining industry. Most investors naturally assume this “Junior Gold Miners ETF” owns junior gold miners, which is where they are trying to allocate their capital. But since most of GDXJ’s funds are instead diverted into much-larger mid-tiers and even some majors, the juniors are effectively being starved of capital intended for them.

That’s one of the big reasons smaller gold miners’ stock prices are so darned low. They aren’t getting enough capital inflows from gold-stock-ETF investing. So their share prices aren’t bid higher. They rely on issuing shares to finance their exploration projects and mine builds. But when their stock prices are down in the dumps, that is heavily dilutive. So GDXJ is strangling the very industry its investors want to own!

Back to these mid-tier gold miners’ Q3’18 results, production is the best place to start since that is the lifeblood of the entire gold-mining industry. These top 34 GDXJ gold miners that had specifically reported Q3 production as of mid-November produced 5063k ounces. That surged by a massive 18.8% YoY, implying these miners are thriving. But that is heavily distorted by that huge 851k-ounce boost from AU’s addition.

Without the world’s 3rd-largest gold miner, the rest of the GDXJ top 34 saw their production slip 1.2% YoY to 4212k ounces. That reflected the peak-gold challenges the gold-mining industry is facing, as I discussed a couple weeks ago while reviewing the GDX majors’ Q3’18 results. The GDXJ top 34 are still outperforming the GDX top 34, which saw their gold production retreat 2.9% YoY in Q3 bucking historical trends.

Sequentially quarter-on-quarter from Q2’18 the GDXJ top 34’s production surged a dramatic 13.3%! And AU was already one of GDXJ’s top components then. That partially came from new mines ramping up at the world’s best mid-tier gold miners. It is far easier for them to grow production off lower bases than it is for the majors off high bases. That’s a key reason why the mid-tiers’ upside potential trounces that of the majors.

For all GDXJ’s faults, it does still offer investors exposure to much-smaller gold miners. The average quarterly production of all the top 34 GDXJ miners reporting it in Q3 was 163.3k ounces. That is 43% smaller than the 288.8k averaged by the top 34 GDX miners last quarter. And again AU’s crazy inclusion really skews this. Ex-AU, the GDXJ average falls to 140.4k. Without all the South African majors, it is 110.8k.

These annualize to 562k and 443k, both solidly in the mid-tier realm. Analyzing GDXJ’s production and costs requires breaking out those heavily-distorting South African majors that have no place in a mid-tier gold-miner ETF. Again their production fell 7.0% YoY in Q3, while the rest of the GDXJ top 34’s ex-KL grew 3.4%! Production and costs tend to be proportionally inversely related because of how mining works.

Gold-mining costs are largely fixed quarter after quarter, with actual mining requiring the same levels of infrastructure, equipment, and employees. The tonnage throughputs of the mills that process the gold-bearing ore are also fixed. So gold produced varies with ore grades each quarter. The more gold that is recovered, the more ounces to spread gold mining’s big fixed costs across. That lowers per-ounce costs.

There are two major ways to measure gold-mining costs, classic cash costs per ounce and the superior all-in sustaining costs per ounce. Both are useful metrics. Cash costs are the acid test of gold-miner survivability in lower-gold-price environments, revealing the worst-case gold levels necessary to keep the mines running. All-in sustaining costs show where gold needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of gold, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q3’18, the overall cash costs of the GDXJ top 34 surged 8.4% higher YoY to $663 per ounce. That was still largely in line with the past four quarters’ $612, $618, $692, and $631 averaging $638.

But that sharp jump was mostly the result of the South African majors’ deepening troubles. Again their average cash costs last quarter were a whopping $925! Without them, the rest of the GDXJ top 34 averaged $629 per ounce which was only up 2.8% YoY and below the rolling-four-quarter mean. So the mid-tier gold miners of GDXJ are holding the line on cash costs, a sign their operations are fundamentally sound.