There are more than a handful of things I can cite as leading indicators for the Gold price.

Ratios such as Gold against the stock market and Gold against foreign currencies are generally good leading indicators. The gold stocks and Silver can function as leading indicators at times.

The yield curve and bonds can also be leading indicators.

But there is one thing I’ve never mentioned, nor written about. It makes sense in the current context though. That’s Platinum.

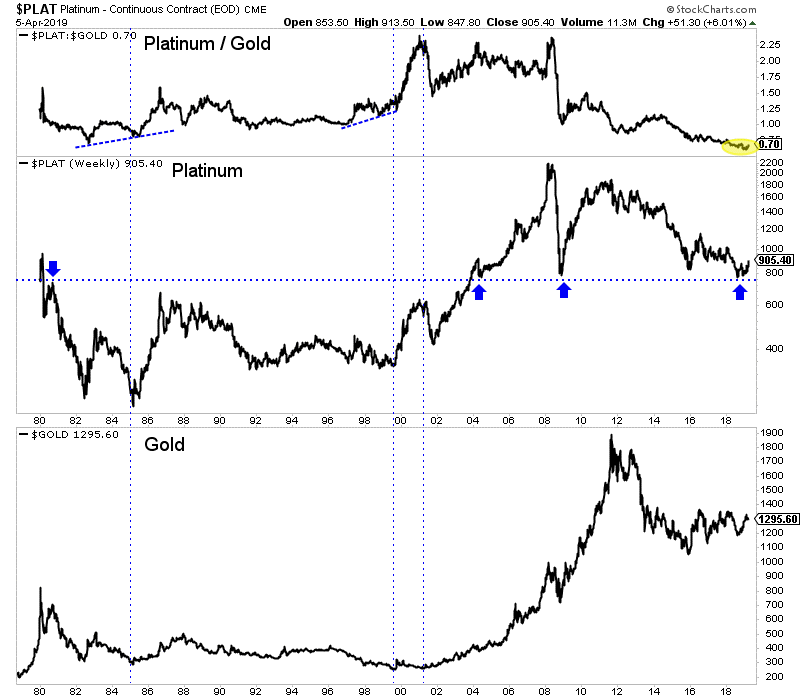

Platinum has a brief but clear history as a leading indicator for Gold.

Platinum outperformed and led Gold higher immediately after the two most recent major lows: 1985 and 1999-2001.

We also want to note the 1966-1968 period when Platinum tripled in price. Silver doubled and Gold of course was still fixed in price. In any event, Platinum’s huge move in the late 1960s was a leading indicator for Gold’s forthcoming surge.

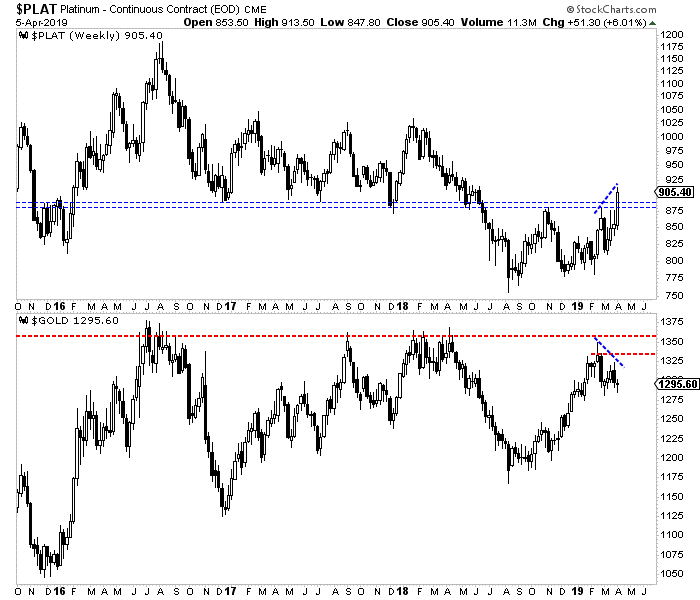

Since the February highs Platinum has made a higher high while Gold has corrected. Platinum looks like it has a reasonable shot to make a new 52-week high this year while Gold would need to fight through the wall of resistance to make a new 52-week high.

According to BMG Group, a study by Wainright Economics showed that Platinum is the leading indicator of inflation. While Gold and Silver lead by a year, Platinum leads by 16 months.

Whatever the reason, history is clear. Around major bottoms in precious metals, Platinum tends to outperform and lead Gold. Since February Platinum has strongly outperformed Gold while registering an important positive divergence.

We will certainly keep abreast of the other leading indicators such as relative performance of the miners, Fed policy, a steepening yield curve and precious metals performance against the stock market. We will also keep an eye on Platinum as continued outperformance would be a strongly bullish signal for Gold for 2020 and beyond.

The weeks and months ahead should continue to be an especially opportune time to position yourself in this sector. To learn what stocks we are buying and have 3x to 5x potential, consider learning more about our premium service.

April 11, 2019

Jordan Roy-Byrne

Recent activity in exploration and acquisitions in North America for the next supply of platinum reveals a troubling situation for South African platinum mining, which presents opportunities for platinum companies in safer jurisdictions.

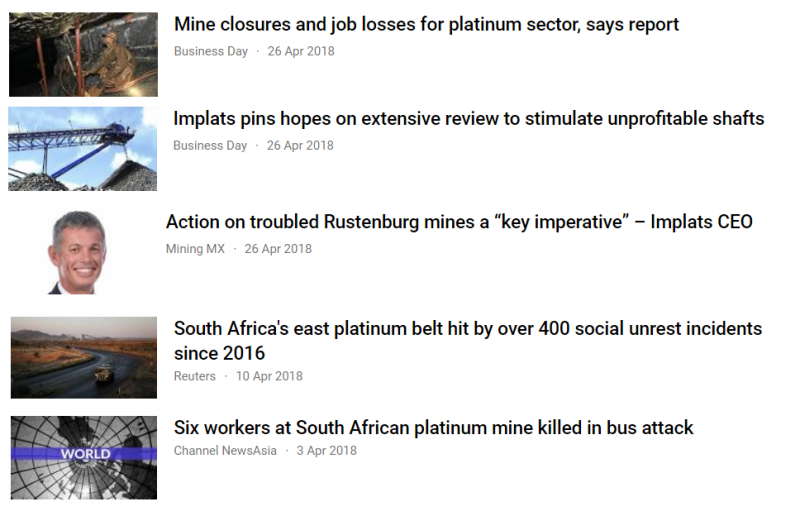

If you conduct a brief survey of headlines about platinum mining in South Africa, a stark picture is revealed.

JP Morgan Cazenove recently reviewed the SA platinum sector. South Africa accounts for 70 per cent of global mine supply and, at current prices, JP Morgan estimated about 60 per cent (2.6 million ounces) of South African mines are cash negative. The report commented “the outlook for the platinum price in 2018 to 19 is bleak.”

Part of this problem is that South Africa’s platinum miners resemble a “dysfunctional oligopoly” and are currently increasing supply despite depressed platinum prices with no significant improvement in the situation expected until 2020.

The report from JP Morgan Cazenove showed just how dire the situation is for SA miners and predicted that the year of change would be in 2020 as efforts to keep unprofitable mines going at enormous expense failed.

South African Mineral Resources Minister Gwede Mantashe said at a platinum conference there was no crisis in the sector. This comment nearly choked Northam Platinum CEO Paul Dunne with a breakfast sausage when hearing this willfully ignorant assessment at the conference.

The eastern limb of South Africa’s platinum belt has been hit by over 400 incidents of social unrest impacting mining operations since the start of 2016, according to data compiled by Anglo American Platinum and provided to Reuters.

The data does not provide estimates on production or revenue losses and does not compare with earlier periods. But it provides an alarming snapshot of a region in a perpetual state of unrest that has undermined the viability of some operations.

In response to this deteriorated operating environment, South African miners have been looking abroad and one acquisition has renewed Platinum exploration interest in North America.

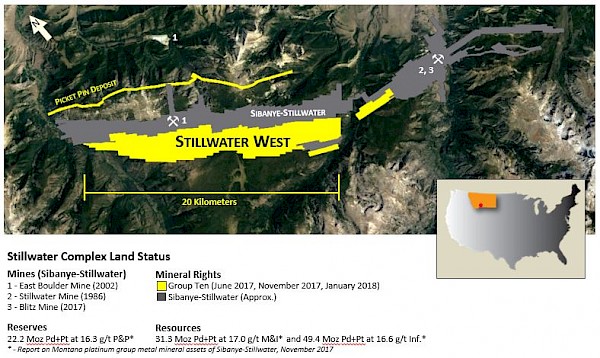

South African miner, Sibanye Gold Ltd. announced the $2.2-billion takeover of Stillwater back in 2017. The company has since changed its name to Sibanye-Stillwater to reflect this change of focus for the company.

One Canadian firm has agreed to buy 282 mining claims just west of the Stillwater Mining complex with the hope of expanding mining. Stillwater West PGE-Ni-Cu project, consists of 44-square kilometres adjacent to, and contiguous with, Sibanye-Stillwater’s high-grade Platinum PGE mining operations, in Montana, USA.

Group Ten’s (TSX-V: PGE) acquisition of the highly-prospective Stillwater West project positions the company as the second-largest landholder in the Stillwater ultramafic complex.

The company’s claims cover two groups in Custer National Forest on the East Boulder plateau in the Beartooth Mountain Range. It’s along the Johns-Manville, or J-M reef, which boasts some of the world’s richest deposits of platinum and palladium.

The high-grade J-M Reef deposit and other PGE-enriched Reef-type sulphide horizons in the Stillwater complex share many similarities with the highly prolific Merensky and UG2 Reefs in the Bushveld complex, while the lower part of the Stillwater complex shows the potential for much-larger-scale disseminated and high-sulphide PGE-nickel-copper-type deposits, such as the Platreef, Waterberg and Mogalakwena mines, that occur in the northern limb of the lower Bushveld complex.

Before any major new development occurs, Group Ten Metals must do additional geological work to determine the true extent and nature of the PGE mineralization as their ground is not directly analogous with the ultra high-grade reef style deposit of their neighbor, President and CEO Michael Rowley state in a telephone interview.

“There’s no question there is polymetallic mineralization there. It’s a question of how much, and, is it minable? It is a great time to answer these questions as it appears the market is in the process of a turnaround. Money has begun to come back in to the sector, and commodities are starting to get a lot of attention again.”

The company recently identified 12 major geophysical conductive anomalies from a 1,914 line kilometer magnetic survey of the property Michael Rowley stated:

“We are extremely encouraged by the size, strength and number of conductive targets identified at Stillwater West…our new insights into the geology of the Ultramafic and Basal Series of the complex. We see potential for multiple deposit types and indications of a much larger mineralized system than has been previously recognized in this under-explored part of the Stillwater Complex. We are especially excited about the similarities in the setting and style of mineralization at the Stillwater West Project to those seen in the world-class Platreef deposits of the lower Bushveld Complex.”

Rowley founded Group Ten in 2006. He said the company struggled to hold on during the commodity collapse but emerged in a good position on the other end.

Along with bringing on technical expertise with former employees of Sibanye-Stillwater, the company has acquired an extensive database on the property, including a significant drilling assays and core library which could yield important new information. This gives the company an in depth understanding of the property.

If conditions deteriorate as predicted by JP Morgan’s platinum report, Platinum miners are going to need to find news sources to mine. Group Ten Metals Stillwater property presents potential new source for platinum and palladium as well as a suite of other in demand metals..

The platinum group metals are composed of six noble, precious metallic elements: iridium, osmium, palladium, platinum, ruthenium, and rhodium. In mining, the most valuable PGMs are platinum and palladium, and rhodium to a lesser degree. Intuitively, the metals are correlated in terms of price movement, and often time track other precious metals, especially gold.

While platinum and gold are correlated (0.85), platinum has historically traded higher than gold, averaging 50% more since 2000. The platinum to gold ratio is currently 0.75, with gold consistently trading higher since the beginning of 2015.

If we shorten the timeframe from 2000 to 2009, the average decreases. However, it still implies that current platinum prices are undervalued relative to gold:

Using the current gold price of $1,300/oz. and the average ratio since 2000, platinum should rebound from its current price of $990/oz. to $1,950. Using the 2009 average of 1.03 still means a significant rebound to $1,360/oz., or a gain of 40% from current levels.

The PGM industry is dominated by the major South African platinum producers, and the largest palladium producer in the world, the Russian-based Norilsk Nickel. Just these two regions account for almost 90% of the World’s platinum and palladium production.

What makes PGM investing even more precarious is that in addition to operating in risky jurisdictions, there are only a handful of public companies. If you filter this to junior companies with a resource, you are down to less than ten.

New Age Metals (CVE:NAM, OTCMKTS:PAWEF)

Current Price: C$0.07

Shares Outstanding: 68.4 million

Market Capitalization: C$4.8 million

Cash: ~C$2.6 million

New Age Metals is one of the few PGM companies that operates in a safe jurisdiction, but is also the cheapest on a per platinum ounce basis. According to our analysis and current market prices, New Age Metal’s River Valley PGM Project hosts a total resource of 3.4 million ounces platinum equivalent. This gives New Age Metals a valuation of C$0.74/oz. Compare this to the average of its comp group, C$40.00/oz.

With platinum poised to return to its median, and New Age Metals trading at a substantial discount to its peers, the optionality in this play is enormous.

New Age Metals is an out of favor companies that has fallen through the cracks because of the decline of platinum. However, the company has raised C$2.6 million and is now more than halfway done its 2017 drilling campaign, focusing on the Dana North (T3) and Pine zone.

In addition, an induced polarization (IP) geophysical survey and borehole geophysics has been completed. The first portion of the drill program was concentrated on follow-up drill testing of the 2015/2016 PGM mineralization at the Pine zone. Drilling will now focus on the geophysical interpretation from the recently completed IP survey.

Six holes were completed at the Pine zone, which is open along strike and at depth. The first batch of assays has been sent to the lab. Results are expected any day now.

The current exploration program will be used to establish the resource base for a preliminary economic assessment (PEA), which the company plans to complete before the end of 2018.

Prior to the current program, the River Valley PGM Project has seen 671 holes drill holes for 152,394 metres and $40 million in total spending. Shares from its last financing became free-trading on August 28, and the stock has sold off in anticipation. In fact, share prices are down more than 50% from its recent high. This bargain price is a nice entry for new investors, especially with an imminent fall commodity rally, and the strong and catalytic news flow on the horizon.

No other PGM company has the torque NAM has, and that is why the company is one of largest holdings in our portfolio.

Cheers,

Sean

Platinum, among the rarest and costliest of metals, is also one of the most green. Platinum is so rare that all of the metal ever mined would fill a room measuring less than 25 feet on each side. The metal has many critical commercial uses, but the primary demand driver today is the automotive industry. Catalytic converters that control harmful automobile emissions now account for 60% of the annual demand for platinum. What makes platinum greener still is that its use as a catalyst is, in theory, all reclaimable and recyclable.

Catalytic converter legislation is spreading quickly. In the past five years both Brazil and Chile passed legislation mandating their use. Hong Kong, Malaysia, Singapore, Taiwan and Thailand are already on board. Higher North American, European, and Asian automobile emission standards are also expected to add pressure to automotive manufacturers to increase the use of platinum in catalytic converters.

Adam Collins, an analyst at Liberum Capital, estimates that the gradual roll-out of heavy duty diesel vehicle legislation alone could result in a 20 per cent boost to existing levels of platinum demand by as early as 2015.

Platinum catalysts are also a core component for fuel cells, a power generation technology that combines oxygen and hydrogen to form water and electricity. Fuel cells are an environmentally friendly power generation source and are viewed to be yet another key green source of future platinum demand.

Today, 75% of the world’s production of platinum comes from South Africa. It’s estimated that as much as 90% of all platinum deposits in the world are located there or in Russia. But output from South Africa has been relatively flat of late, for a variety of reasons. Closure of platinum mines, cutbacks on capital expenditures, inflation and cost pressures, ever-deepening depths of mining operations and lower grades of the ore produced have put a squeeze on the supply side of the equation. Industrial action by the labour unions has also had a negative effect on the level of production from South African producers. Platinum Australia (ASX: PLA) Managing Director John Lewins recently noted, “South Africa will obviously still dominate this area, but electricity, inflation, safety, depths and industrial unrest remaining as big issues.”

For all these reasons, the past decade has been very good for platinum, the price of the metal has increased from $588 to $1773 per troy ounce. And that premium has clearly spilled over into the equity markets.

Eastern Platinum (TSX:ELR), whose shares could be had for as little as $0.25 in 2008 have rebounded to the $1.40 mark. Late last year the company closed a massive $348 million financing and early returns suggest the money was invested wisely; Eastern Platinum recently announced a a net profit of $5,041,000 in the fourth quarter of 2010. Platinum Group Metals (TSX:PTM) closed a $125 million equity financing in late 2010 and is currently working towards putting their Western Bushveld Joint Venture platinum deposit into production. Anooraq Resources (TSXV:ARQ) is in the middle of an operational turnaround at their 51-per-cent-owned Bokoni platinum group mine in South Africa. The company reported sales of $148 million in 2010, up from $63 million in 2009. Although shares of Anooraq are trading well above 2008 lows the company’s stock has not fared well recently; it’s down roughly $0.75 from its 2010 high of $1.80. But some think Anooraq may, ultimately, shine bright. In October, 2010 Peter Grandich called the company a “sleeping giant” with “many of the ingredients needed to benefit greatly in a sector that looks like it has lots of upside.”

As society looks at better choices for the environment, long term, tighter emission regulations appear to be fueling momentum for catalytic converters. But bullish calls from equity analysts, which are appearing with increased frequency, have investors in platinum stocks thinking of a different kind of green.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |