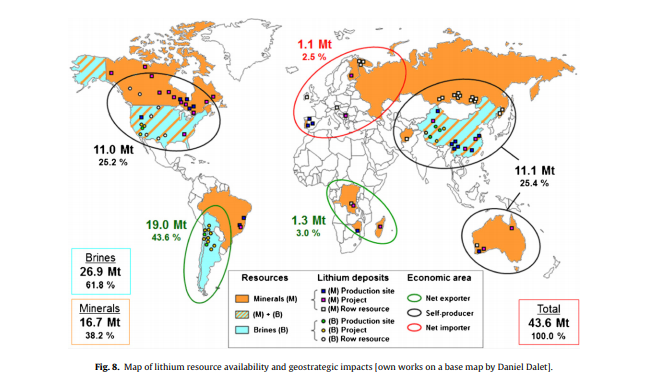

Chile holds the largest known lithium reserves, and miners have been clamoring for tenders consistently since the first discoveries and mapping were conducted. Now, the Latin American nation is opening a tender for the exploration and production of 400,000 tonnes of lithium.

This move by the Chilean government is an effort to reclaim market share from competitors like the Democratic Republic of Congo, Australia, and China, and fill some of the growing demand for lithium due to its use in electric vehicles and technology. Up until 2018, Chile was the world’s top lithium producer.

However, Australia displaced Chile, and China is fast approaching the point where it will be the second-largest lithium producer with a projected timeline of the end of this decade. For example, China’s Ganfeng Lithium is a majority shareholder in Argentina’s plant Cauchari-Olaroz. Production is scheduled to begin in mid-2022 and become one of the world’s leading lithium production mines.

Chile still produced approximately 29% of the world supply. No small feat for the smaller nation competing on the international stage. The government has ambitions set much higher though, and it looks to double production to 250,000 tonnes of lithium carbonate equivalent (LCE) by 2025.

Chile’s mining ministry projects show that global demand for lithium could quadruple by 2030 – a total of 1.8 million tonnes. Even if Chile doubles it production and new lithium projects come online, available supply is projected to be 1.5 tonnes, a significant deficit. This will likely drive prices higher and create a further wave of new projects and new tenders becoming available.

The tender is being prepared with rules that will make it available to local firms and foreign firms alike. The tender will split the 400,000 tonnes into five quotas of 80,000 tonnes each. Winning permits will mean companies have seven years to explore and develop projects. This is extendable by two years if needed. Following development, the tender will allow permit 20 years of production, according to the mining ministry.

Right now, there are two major lithium miners that dominate the market: Albemarle (NYSE:ALB) and SQM (NYSE:SQM). Their primary and most profitable location for extraction is in Chile’s Atacama Desert. The desert is one of the driest places on earth and creates ideal conditions for lithium extraction. The extraction process requires pumping brine from beneath surface and then concentrating the brine using evaporation pools.

They pump the brine from the vast salt plain of Salar de Atacama in Chile to 80 km2 basins. The salt flats and surrounding mountains have allowed rainfall to accumulate over millions of years, forming a salty brine that has become trapped in underground reservoirs. Lithium extraction in Chile is currently taking place in the Atacama Plain, but the Maricunga Plain is believed to hold the largest lithium reserves in the country.

The upcoming tender is designed to shift the dynamics of the global lithium market and help Chile compete with its global competitors. With the rise of China’s lithium mining giant, and the two dominant miners continuing to expand their footprints, Chile will open up the tender in the hopes of creating some of the biggest lithium projects of the next decade. This is all aimed at the mission of doubling production.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Argentinian lithium producer Orocobre (TSX: ORL) recently reported lower than expected lithium production in its third fiscal quarter because weather interfered with its evaporation rates of its lithium brines. This reveals two problems with lithium brine production: reliability and geography. Another source of lithium is rising to met these problems, hard rock lithium mining.

One analyst pointed out that Orocobre’s production problems “clearly demonstrate” that production is not a straightforward process. “Weather events are beyond the control of Orocobre, but this reaffirms that there is still room to improve on the robustness of operations and reduce production variability from we ather impacts,” the analyst stated.

The company reported a 25-per-cent lower evaporation rate compared with the same quarter in 2017 which caused production problems and lithium output to fall 29 percent to 2,802 tonnes of Lithium Carbonate equivalent, from 3,937 tonnes in the December quarter. Its February rates were the lowest since 2011.

Weather has clear impacts on the production at lithium brine operations and with global demand for lithium on the rise, more reliable and consistent methods of production will be required. Lithium brine operations are limited to select climates and regions that can support sufficient weather to ensure economic processing.

Demand for the metal is set to grow by 600,000-800,000 tonnes of lithium carbonate equivalent over the next 10 years, Daniel Jimenez, senior commercial vice president at SQM, said.

The global lithium industry will need $10 billion to $12 billion of investment over the next decade to meet surging demand amid the electric vehicle boom, Daniel Jimenez of Chilean miner SQM said.

Not all lithium is equal and not all lithium is mined the same way. There are two significant sources of lithium, Lithium Brines and Lithium-Cesium Tantalum Pegmatites (hard rock).

According the United States Geological Survey’s 2018 Mineral Commodity Summaries, Australia was the largest producer of lithium. It produced 18,700 MT of lithium last year, up 3,300 MT from the previous year. The 34-percent increase has been attributed to two new spodumene operations that ramped up production to meet strong demand.

Australia hosts the Greenbushes lithium asset, which is operated by Talison Lithium, a subsidiary jointly owned by Tianqi Lithium (SZSE:002466) and Albemarle (NYSE:ALB). Greenbushes is the longest continuously operating mining area in Western Australia, having been in operation for over 25 years.

These production figures helped to push Australia as the top lithium producing country and it shows how hard rock lithium mines have the potential to disrupt traditional sources of lithium from older operators of lithium evaporation ponds.

Hard rock lithium deposits are not limited to select climates and regions and are going to help fill the demand as they are more evenly geographically distributed across the globe and are less dependant on a changing climate for production.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |