Collective Mining (TSXV:CNL) had a big day last Friday, May 28, with a blockbuster IPO that saw the stock pop 205% on the first day of trading. The company’s common shares began trading at the market open on May 28, on the TSX Venture Exchange under the symbol CNL.

As part of its reverse takeover of shell company POCML5, Collective Mining (TSXV:CNL) had raised C$15 million at $1 per subscription receipt. With the share price hitting $3.05 on Friday, the company saw a valuation of C$30.9 million.

Collective’s executive chairman Ari Sussman said, “With the funds from our $15 million subscription receipt financing now released from escrow, we are embarking on an aggressive exploration programme and are excited to unlock the potential of our project over the next 12 months.” The exploration and development company is currently focused on exploring prospective gold projects in South America.

Colombia’s mines minister stated that it was great news to have a new Colombian-focused company listed on the TSX Venture Exchange. The high-level strong support from Colombia is a promising sign of the exciting times to come for Collective, with the minister saying in a joint statement that, “This is yet another endorsement of investors’ trust in the Colombia mining sector.”

Collective’s main directive is to realize its ability to earn a 100% interest in two projects located in Colombia (San Antonio, and Guayabales). With an assembly of superstar management with a track record of successfully selling Continental Gold to Zijin Mining for C$1.4 billion, the company is focused on bulk tonnage porphyry-related systems as opposed to high-grade gold.

This new approach to exploration is not the only change for the group. Collective Mining was founded with environmental, social, and governmental (ESG) principles embedded in the fabric of the company’s guiding philosophy and operational standards. The name of the company is a strong indication of the company’s commitment to collaborative and inclusive management, and a collective commitment to the values that investors prioritize for both stakeholders and investors.

Colombia’s mining sector is well-developed, with strong ancillary mining services, agriculture, and tourism industries helping form a well-rounded economy. As Collective builds strong and profitable porphyry gold projects, the economy and country stand to benefit from the strategic alliance across a myriad of industries.

Collective Mining’s (TSXV:CNL) management track record puts it in a good position to grow over the coming years. As the stock follows suit, investors will likely continue to add more of it to their portfolios as they look for ESG-compliant and focused mining companies. The fact that Collective’s team had such a massive success with the past buyout of Continental Gold also raises the possibility that the company could see a huge payday in the future as it develops it’s projects and revenue streams.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Mining companies are some of the biggest and most productive economic machines in the world. Mining produces important minerals and metals that are essential to the smooth functioning of society. Without mining, there would be no technology, no buildings, no electricity, and no global economy. For most, mining brings to mind some misconceptions about the industry and how it operates. It’s time to explore some of the positive effects of mining and get into the transformatively powerful effects of responsible mining around the world.

Kinross (NYSE:KGC) (TSX:K) Harvests Water From Snow in Chile

The Maricunga and La Coipa mines, located in the Atacama Desert approximately 4,000 metres above sea level, are some of the driest places on earth. Like everywhere else, water is critical to the ecosystems and wetlands that play host to wildlife including vicuna, flamingo, and guanaco. To ensure those habitats can thrive, Kinross Gold Corporation has implemented measures to improve the area’s water efficiency.

In 2011, the company installed 100-metre lines of wooden snow fencing. The fencing’s goal is to ensure that snowmelt infiltration into the groundwater is more efficient. This is helping to bring meaningful contribution to the local water supply. On top of that, Kinross and the Chilean National Irrigation Commission are exploring a joint research project. The project will investigate and test the snow harvesting tactic for potential use in other water-stress areas of Chile. The mining company is contributing resources and people to the job, and making a serious contribution to the country and the regions they operate in beyond the jobs and economic stimulus that their projects create.

Golden Star Resources (TSX:GSC) Builds a Health Centre

Golden Star Resources (TSX:GSC) has been a busy member of the Ghanaian community, particularly when it comes to healthcare. The company provides National Health Insurance Scheme coverage for every single employee as well as their immediate families. Golden Star was the winner of the PDAC 2018 Environmental and Social Responsibility Award, so it may come as no surprise that the company goes far beyond what is asked. The company has upgraded local clinic to provide services to all of its employees, and even built a health centre at Nsadweso, an Outpatients Department at the Prestea Government Hospital, nurses quarters at Bogoso, a mini-clinic at Brakwaline, and a community health post a Bondaye.

On top of all of the health infrastructure development Golden Star Resources (TSX:GSC) is doing, the company is also a supporter of Project C.U.R.E.. The project has delivered 29 containers of medical equipment, serving over 18 million people since 2003. Golden Star is a great example of how healthcare and wellbeing are integral to positive contributions for stakeholder communities and a company’s employees.

Solaris Resources (TSX:SLS) Flies in To Save a Child

Mining companies often need to operate in remote locations, where they are usually responsible for building and maintaining infrastructure and other services. Companies can be a powerful partner in these areas. Solaris Resources (TSX:SLS), a copper mining company with significant operations at its flagship Warintza Project in Ecuador, was exactly the kind of community partner needed in times of trouble for one 10-year-old patient.

When a child became ill and needed an emergency evacuation to a hospital in the border community of Banderas, near Peru, Solaris allowed for the air transfer of that child immediately and helped coordinate the rest of the transfer once the helicopter landed at Edmundo Carvajal airport in Macas. Since the location was so difficult to access, a helicopter was the only option, and Solaris (TSX:SLS) was able to coordinate the transport quickly, demonstrating that a powerful community partner from the mining industry could make a major difference in the lives of all stakeholders.

A statement from the Integrated Security Service and Lenin Moreno, Ecuadorian president at the time, read, “The work coordinated between security forces, citizens, and private enterprise made it possible to provide assistance at the right moment.”

Miners Continue to Be Strong Allies

While it may not always be obvious what private industry and communities can accomplish together, the results are clear. When government, citizens, and private enterprises in the mining industry come together for a common purpose, the industry is able to consistently demonstrate its ability to step up to the plate and hit home runs.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Vancouver-based Solaris Resources (TSX:SLS) is hitting a regular stride as the company continues to report positive assay results, expands its drill holes at its flagship Warintza Project, and continues to see strong stock growth.

Yesterday saw Canaccord Genuity analyst Michael Pettingell maintain a Buy rating for Solaris Resources (TSX:SLS) with a price target of C$12.50. As of May 27 12:16 EST, that target has already been broken.

How High Could It Go?

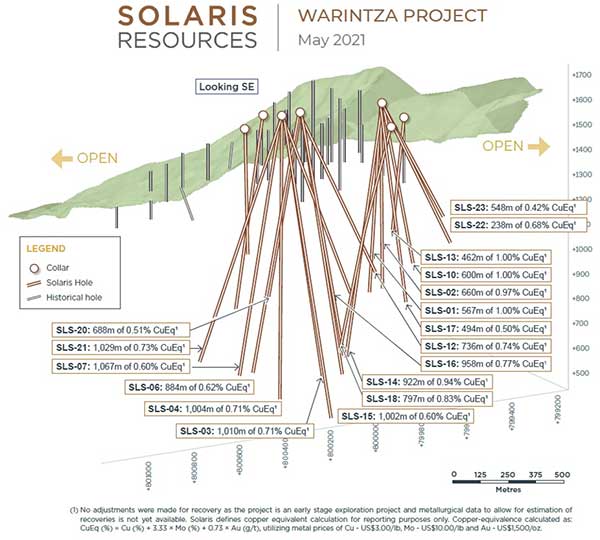

The stock has seen a steady, uninterrupted climb as it moves from strength to strength. With a strong balance sheet, the company has been able to move forward on all of its projects, with a particular emphasis on its Warintza Project in Ecuador. The project has seen strong results, and has reported for 22 of 31 holes drilled so far at the site.

The company continues to expand the project, and has begun with its first drill hole at Warintza East, sitting east of the Warintza Central site. The target has returned positive results already, and the stock is reflecting the optimism the results are setting. As more results are reported, the trend is likely to continue and possibly accelerate. The stock is also a value play considering the current trendline that could see it rise to $25 or higher.

As Solaris (TSX:SLS) continues to set new all-time highs, investors might be wondering when they should get in. However, it’s clear from the chart that any moment since the first day of trading would have been a good time to buy.

Positive Results Driving Positive Investor Returns

Solaris Resources (TSX:SLS) has released new assay results from new drill holes at the company’s Warintza Project in south-eastern Ecuador. The company announced results from three additional drill holes at Warintza Central, for a total of 31 holes drilled at the site. Results have been reported for 22 of them, with results looking very promising:

- Three additional holes at Warintza Central, as detailed below, have extended the drill defined envelope of high-grade mineralization to the east and west over a strike length of over 1,100m and open and to a depth up to 1,200m, with the highest-grade mineralization starting at surface

- SLS-21 was collared on the eastern side of Warintza Central and drilled into an open volume to the east, returning 1,029m of 0.73% CuEq¹, including 420m of 0.83% CuEq¹ from surface, extending the limits of mineralization to the east, with the hole terminating prematurely in mineralized porphyry

- SLS-22 was collared on the north-western side of Warintza Central and drilled into an open volume to the west, returning 238m of 0.68% CuEq¹, including 100m of 0.77% CuEq¹, extending the limits of mineralization in this direction

- SLS-23 was collared on the south-western side of Warintza Central and drilled to the west, returning 548m of 0.42% CuEq¹, including 352m of 0.46% CuEq¹ from surface, extending the limit of mineralization in this direction

- Maiden drilling is set to commence at Warintza East, which is one of the five main targets within the 5km x 5km cluster of copper porphyries identified on the property and has a similar geochemical and geophysical expression as Warintza Central

- To date, 31 holes have been drilled at Warintza Central with results reported for 22 of these. Unusually heavy rain in Ecuador has significantly impacted the pace of drilling productivity and platform construction over recent months, however weather conditions are now sporadically improving and the planned ramp-up of drilling activities is expected to resume

Source: Solaris Resources

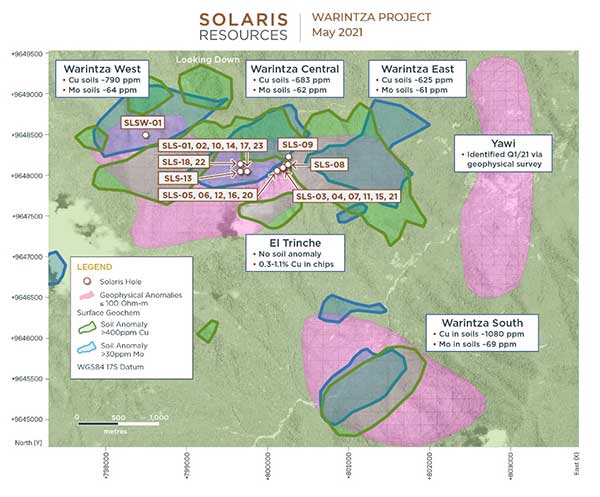

Solaris has ventured into its new site, Warintza East with the first hole (SLSE-01) being collared in weathered porphyry stockwork mineralization. The mineralization was first discovered by earthworks during drilling platform construction.

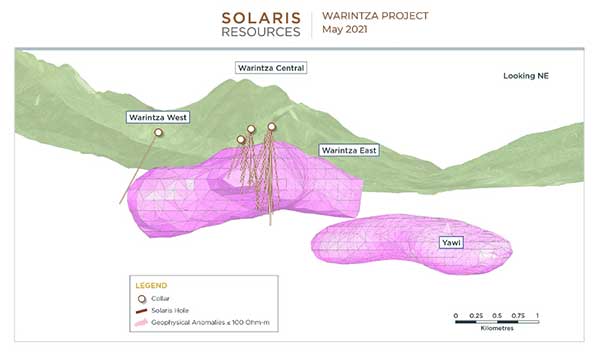

The target located at the site is defined by overlapping and molybdenum anomalies that hold similar values to Wartinza Central. With approximately 1,200 m in diameter, the high-conductivity anomaly extends continuously from Warintza Central to the target in the east.

Figure 1 – Long Section of 3D Geophysics Looking Northeast

Note to Figure 1: Figure looks northeast and depicts high-conductivity geophysical anomaly (defined at 100 ohm-m) generated from 3D inversion of electromagnetic data, encompassing from left to right Warintza West, Central, East and the newly-discovered Yawi target (Warintza South lies off image to south).

Figure 2 – Long Section of Warintza Central Drilling Looking Southeast

Figure 3 – Plan View

Source: Solaris Resources

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Foran Mining Corp. (TSXV:FOM) (OTCQX:FMCXF) has announced that Fairfax Financial Holdings Limited has entered into a letter agreement for a CA$100 million investment in Foran Mining Corp. (TSXV:FOM) (OTCQX:FMCXF) in exchange for common shares, non-voting common shares, and warrants. Divided into multiple tranches, the deal will allow Foran Mining Corp. (TSXV:FOM) (OTCQX:FMCXF) to rapidly advance its McIlvenna Bay project and centralized mill for the Hanson Lake district.

The company has been eyeing exploration in the district as it continues to expand operations in the region. The letter highlights that the funding will also enable investment in key technological and operational research and equipment and general corporate purposes.

A Major Vote of Confidence

The significant private placement is a decisive vote of confidence in the company and its business model and will be subscribed in two tranches:

- Tranche 1 – CAD$50 million gross proceeds, comprised of 27,777,778 voting common shares (the “Common Shares”) at a price of CAD$1.80 per Common Share, along with warrants to purchase an aggregate of 8,000,000 million Common Shares (the “Warrants”). The Warrants have an exercise price of CAD$2.09 per Common Share and an exercise period of five years.

- Tranche 2 – CAD$50 million gross proceeds, comprised of 27,777,778 non-voting common shares (the “Non-Voting Shares”) at CAD$1.80 per Non-Voting Share, along with 8,000,000 Warrants.

Source: Foran Mining Corp.

Foran shareholders know that the advantages the company holds are numerous including its 100% owned McIlvenna Bay deposits and the broader Hanson Lake district. Foran Mining Corp. (TSXV:FOM) (OTCQX:FMCXF) plans to build the world’s first carbon-neutral copper mine. The company has stiff competition, though, with companies like Solaris Resources (TSX:SLS.TO) and Rio Tinto (NYSE:RIO) setting carbon-neutral goals for their projects as well.

Creating a True Partnership Through Investment

For now, the expansion of its exploration efforts and current projects could continue to deliver substantial shareholder value, and efforts should be significantly strengthened by Fairfax’s global network of business partners. Foran Mining Corp. (TSXV:FOM) (OTCQX:FMCXF) has strong established ties with banking partners to support the exploration of potential ESG products; the goal of these initiatives is to enhance the overall investment return for all stakeholders, from shareholders to the communities in which the company operates.

The financing is still subject to TSX Venture Exchange approval and Foran Mining Corp. (TSXV:FOM) (OTCQX:FMCXF) shareholder approvals, plus some other standard closing procedures. For now, Fairfax will not be granted any Foran Mining Corp. (TSXV:FOM) (OTCQX:FMCXF) board seats as part of the deal.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

There are a few key mining regions that always seem to be the most industry-friendly as well as mineral-rich. South America, Eastern Russia, and North America have always stood out as top producers for their ability to put together a robust mining sector and boost their economies overall.

Serbia’s government wants to place the country closer to the top of the world’s mining hotspots. The country announced that the mining and energy sector is set to contribute 10% of the country’s GDP within 10 years. “This year, we are drafting an important legislative framework in the field of energy and mining, but we are also making very important decisions and embarking on a new, green and sustainable path of energy and mining,” Serbia’s Minister of Mining and Energy, Zorana Mihajlovic, said.

The new Law on Energy Efficiency and Rational Use of Energy is designed to help citizens improve insulation in their apartments. With a smaller population and less energy-intensive lifestyles, Serbia still consumes approximately four times more energy than the EU average.

The country has begun taking steps to make the energy sector more efficient for citizens and profitable for the country. Serbia has adopted a package of legislation for the energy and mining sectors, with two new laws – the Law on the Use of Renewable Energy Sources and the Law on Energy Efficiency and Rational Use of Energy – being adopted on April 12. Two existing laws – the Law on Energy and the Law on Mining and Geological Research – have been amended as well to reflect the new direction the country is looking to take with the sector.

Local and state governments will facilitate the first signing of contracts with citizens regarding the improvement of energy efficiency at the end of summer. This will help further the country’s agenda and bring mining companies to the forefront of the driving forces behind the country’s economy. The project is to be financed by local self-governments and state budgets, but Serbia expects that international institutions step in and become stakeholders in the project by next year. “We expect to have an average of around 150 million euros per year for such projects,” Mihajlovic said.

Serbia has a rich mineral portfolio with deposits of coal, iron ore, gold, silver, copper, zinc, and lithium sitting within the country’s borders. In an interview with Happy TV, Mihajlovic claimed the estimated value of mineral reserves in Serbia to exceed 200 billion euros.

Major miners are planning investments in the country and are developing new projects immediately. Chinese company Zijin announced plans to invest $408 million in production and projects in Bor and Majdenapek mining sites in easter Serbia, and plans for a total of $1.1 billion in investments in the country in three years.

Rio Tinto (NYSE:RIO) is developing their Jadar lithium-borates project following a 2004 discovery in the Jadar river valley. That particular site could hold 10% of the world’s deposits of lithium. With the world moving to greener, more sustainable forms of energy production and lithium being needed for technology and battery storage, this could be a major project for the company and a huge win for Serbia. A maiden ore reserve was reported last December by Rio Tinto (NYSE:RIO), signalling that the Jadar project could have the potential to produce battery-grade lithium carbonate (the most valuable version) and boric acid.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

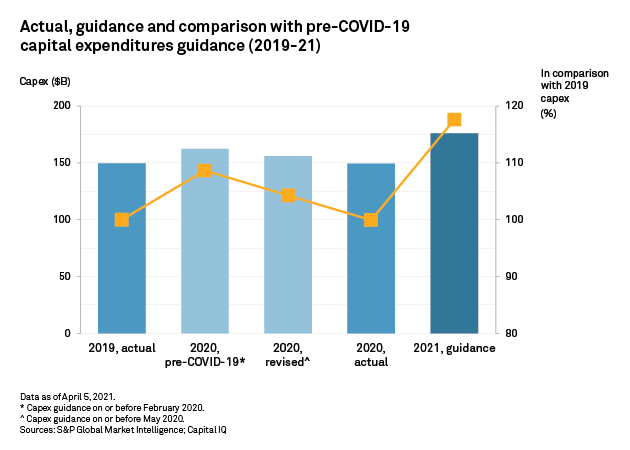

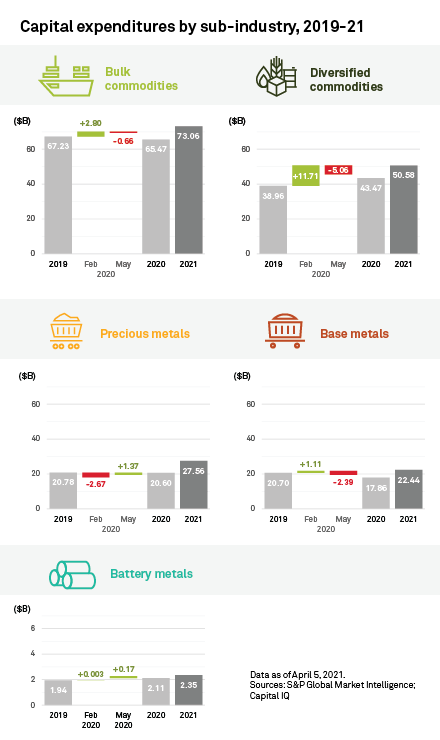

S&P Global Market Intelligence’s new report highlights the significant impact the pandemic has had on capital expenditure in 2020. The year was a complicated one, with projects shutting down temporarily, and licenses for new mines suspended until the lockdowns began to ease around the world.

Despite it all, the mining industry has fared well and continues to forge ahead with minimal disruption. However, the report found that among more than 400 mining companies examined, capital expenditures dropped 8% in 2020 when lockdown forced projects to stop work, and global supply chains began to crack under the dual pressures of shifting demands and lower production.

Feeling Better

The first quarter of 2020 held some optimism for the year. The miners’ group forecasted a capex YoY increase of 9% to $162 billion. By the beginning of the second quarter, expectations had been revised and the spending plans reduced 4% lower to reflect the coming changes. Still, this would represent an increase for the year before, as no one had anticipated the length of the lockdowns or the severity of the pandemic.

In the end, total capex for 2020 came in at $149.5 billion well below forecasts, but arguably strong considering the harsh mining environment of the year and the fact that global economic confidence was sucked out of the air faster than an airlock for a spaceflight.

A Realistic and Optimistic Outlook for 2021

S&P has set a positive tone for 2021, with a forecast of global gross domestic product growth of 5.5% in 2021, boosting capex and numbers across every. The company is forecasting a mining industry capex of $176 billion, up a substantial 18% fom 2020 and 2019.

As projects were put on hold last year and confidence dropped off a cliff, mining companies needed to revise their expectations. Now that the situation is improving rapidly, companies are ramping-up their activity. Positive outlooks are not hard to come by for miners as strong prices for metals and minerals continue to push commodity prices higher, boosting profits.

The Rich Get Richer

The Eastern Hemisphere is leading the recovery right now, particularly China and Australia. The influx of capital expenditures won’t be balanced across metals companies or metals either. Precious metals companies are expected to spend the most, and increase their capex by over a third compared to 2019. The biggest spenders will likely be the usual suspects including Newmont (NYSE: NEM) (TSX:NGT) and Gold Fields (JSE:GFI) (NYSE:GFI).

Large cap mining companies are always the first to jump into new projects with high capitalization levels and strong cash balances on hand. Most of these companies will recover stronger and faster, and S&P expects that companies with a $50 billion+ market cap will surpass their smaller peers for both forward guidance and spending. This would exacerbate the trend of the winners taking all, and the biggest players consolidating their gains and building on them. The largest market cap group is expected to spend 51% in 2021 compared to 2019, and the next three groups of companies expected to keep similar levels to 2019, averaging 12%, although they would be increasing their spending from 2020.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Copper’s continued rise seems to be without barriers right now, even after China ramped up efforts to cool the commodities surge that may be building fears of global inflation. Worries on the other side of the planet are also fueling concerns about the long-term supply outlook.

Chile’s proposed tightening of regulations in the country and higher taxes on royalties and other profits may not come to pass, but until a resolution is made by vote, miners and traders will continue to haggle over the direction of copper. For now, the bias has been a solid upward trend that is showing no signs of abating.

The world’s biggest copper-producing country (Chile) has just elected an assembly that had put the writing and signing of a new constitution mostly in control of the left-wing. With social and environmental concerns at the forefront of their political agenda, there isn’t much room for error as opponents of the new policies work to prevent them from being signed into law.

Compromise Will Be Necessary

In the end, some regulations could be coming down the pipeline, with miners facing more rigid rules around environmentally-friendly operations and mineral rights. That regulation would ultimately pave the way for one of the heaviest taxes on the mining industry in the world. Royalties and profits from mining activities in the country could be taxed at higher rates than ever before, possibly leading some miners to shift focus to other regions.

For some companies, risks are minimized. Canadian miner Teck Resources (NYSE:TECK) has a stability agreement in place with the country that will shield its massive Quebrada Blanca Phase 2 copper project from higher tx levels for 15 years, according to Chief Executive Don Lindsay. Many countries south of the equator have shifted tone on mining, with Peru’s socialist presidential candidate Pedro Castillo claiming he would raise taxes and royalties on Peru’s all-important mining sector and move to quickly renegotiate with large companies over their tax contracts. This is a big if, as he has not been elected, and opposition is strong.

Lobby groups, politicians, mining companies, and their workers will look to maintain operations as they are, with job creation and economic growth a key pillar for the countries in which the mining industry operates. As one of the most significant sectors for many of these countries, the jobs they rely on and the tax income generated are essential to the nations and the politicians who run them.

There’s No Stopping This Train, Even if it Slows

For now, China continues to maneuver to try to find ways to contain costs and keep prices low or at least stable. Citigroup analysts recently recommended buying the dips since Beijing could “easily run out of options” for tamping down price growth. Analyst Tracy Liao wrote in a note that, “We do not foresee such a U-turn any time soon given the strategic priority of these agendas.”

The coming decade is likely to see consistent growth for copper prices, regardless of intervention as the global economy pivots to an electrified format with EVs and batteries driving much of the transition.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

China’s output data has put some pep in the step of iron ore prices as low inventory levels around the world could potentially contribute to a supply dearth.

The most-traded iron ore contract by volume for September delivery was up 5.5% to $195.26 per tonne at one point on the Dalian Commodity Exchange. As construction ramps up on projects around the world, steel demand is likely to keep rising over the coming months.

The demand could push iron ore prices higher for the foreseeable future until a more balanced supply is established and inventories are refilled. Analysts with Huatai Future wrote in a note that, “Steel consumption is still at seasonal peak in the short term…mills are actively producing, driven by high profits, which support raw materials.”

China’s reopening from the pandemic has been a significant driver of both supply and demand, and the country’s output hit a record high even though the government has pledged to curb annual production in a bid to reduce pollution and keep costs high for raw materials. The global steel output continues to inch up, rising to 97.9 million tonnes. This crossed month and daily run-rate records.

Analysts at Morgan Stanley agree that China will continue to drive the market in the short term, writing, “As China’s steel production still continues to expand, its steel margins remain elevated and seaborne iron ore supply remains constrained, we think that the iron ore price can stay around the current level through 2Q, but is likely to remain highly volatile.”

5% daily moves may not be a regular occurrence, but risks loom as demand from Latin America remains low, and supply from Brazil could pick up in the coming months to supply local needs. Global iron production growth is expected to accelerate this year with Brazil driving much of that growth.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Monday, May 17 saw Newmont (NYSE:NEM) (TSX:NGT) complete its acquisition of GT Gold by scooping up the outstanding 85.1% of common shares of the Canadian exploration company in a C$393 million cash deal. Announced two months ago in March, the deal allows Newmont (NYSE:NEM) (TSX:NGT) to take control of the Tatogga gold-copper project in the Traditional Territory of the Tahltan Nation.

Tatogga sits about 14km west of Imperial Metal’s Red Chris copper-gold mine in British Columbia. For Newmont (NYSE:NEM) (TSX:NGT), the acquisition gives the US-based gold mining company a major advantage in the region, and further consolidates its position as the world’s number one gold producer.

Bigger and Better

By adding the copper-gold project to Newmont’s (NYSE:NEM) (TSX:NGT) portfolio, the company will add significant gold and copper annual production to its overall output. It also expands the company’s foothold in the area by adding to its existing interest through the company’s 50% ownership in the Galore Creek project; the acquisition includes the Saddle North asset. The company has also opened up opportunities for further exploration beyond the deposits at Saddle North with this acquisition.

Newmont (NYSE:NEM) (TSX:NGT) president and CEO Tom Palmer commented in a statement: “With the acquisition of GT Gold and the Tatogga project in the highly sought-after Golden Triangle district of British Columbia, Canada, Newmont continues to strengthen our world-class portfolio. We will partner with the Tahltan Nation at all levels, and with the Government of B.C to ensure a shared path forward as the company understands and acknowledges that Tahltan consent is necessary for advancing the Tatogga project.”

M&A Optimism Picks Up

M&A activity has picked up again after a sluggish rut in 2020 for the entire mining industry, but beautiful British Columbia’s volume has been higher than the average. Many of the deals in the last six months have involved deals with Vancouver-headquartered companies or companies with projects in the province.

In 2020, there was the sale of the New Gold (NYSE:NGD) (TSX:NGD) Blackwater property south of Prince George to Artemis Gold (TSX.V:ARTG) for a total of $190 million. The snowfield project operated by Pretium Resources (TSX:PVG) was bought by Seabridge Gold Inc. (TSX:SEA) in December 2020 for $100 million in cash, a 1.5% net smelter royalty on all production, and a future contingent payment of $20 million. Those deals began to foreshadow a pickup in M&A activity as miners’ optimism rose with the lifting of restrictions and business operations in some parts of the economy.

In early 2021, Eldorado Gold (NYSE:EGO) (TSX:ELD) made a neat and tidy acquisition of QMX Gold Corp. (TSX.V:QMX) for $132 million to kick off the new year.

More activity is likely with higher volume as well as bigger buyouts as a dearth of exploration projects or development projects makes anything operating or of a higher-quality worth even more. With everything scrambling to scoop up the same properties and projects, the competition is fierce, and it is driving bidding wars and competition not unlike the red-hot Canadian housing market.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Ethiopia’s mines ministry, in an effort to encourage production, has issued warnings to companies operating idle mines. Many mines sit unused or without active operations for years. The ministry was quoted: “Following a re-investigation, 27 mining companies that had been licensed to operate in the mining sector but failed to enter operation have had their licenses revoked, and three miners have been immediately warned to correct their mistakes.” Takele Uma, Ethiopian mines minister, was reported by Reuters as saying that the licenses will now be opened up to international tender.

The country has revoked 90 mining licenses, with 63 of those being revoked in December 2020. The mining companies involved failed to renew their licenses, or had not made royalty payments. Ethiopia would like to expand and develop its mineral and metal resources and needs committed partners to reach its goals. Mining will be a key sector for the country moving forward as it aims for economic growth and reform across every sector.

Trying to Revive an Economy on Life-Support

A large trade deficit and lack of regular foreign exchange have left the country in an untenable position with stagnant growth for most parts of the country and recession for others. Ethiopia relies on many artisanal miners, but would like to lure more international miners into the region. Larger companies will be allowed to bid on the licenses available for international tender to build a more robust and consistent mining industry.

The nation so far has exported gold valued at over $504.73 million in the last ten months. The metal accounts for the vast majority of the country’s mining exports, with over 90% being attributed to the yellow metal. Unfortunately, official figures and royalty payments have been on the decline for the past eight years as illegal trade and the closure of big plants have plagued the industry.

There is Hope for the Patient

December 2020 saw the government take its economic future in a new and more determined direction with a 10-year plan directed at bringing more foreign exchange through imports and exports. The goal is to grow the current import and export substitution of minerals from $265 million to $17 billion by 2030. The ambitious plan has its roadblocks, but the cancelling of the licenses is a solid first step in the right direction.

Investors may also be enticed by a 25% corporate tax rate and a 10-year loss carry-forward, royalties of 4% on industrial minerals, 5% on metallic minerals, and 7% for the all-important gold production. Mining companies obtaining licenses will also be pleased with their exemptions from customs duties and taxes for machinery, equipment, and vehicles that can be considered essential to operations.

Some big companies already have a foothold in the country and will benefit from this accommodating 10-year roadmap. Kefi Gold and Copper, as well as US-based Newmont (NYSE:NEM) (TSX:NGT) have assets in Ethiopia, with ongoing operations.

With change comes risk and disruption, and the mining industry is no exception. The coming changes in the green revolution sweeping the global economy will disrupt the balance of demand for metals and materials around the world. A new report published by Fitch Solutions forecasts some of the most significant changes to the energy and mining environment since the industrial revolution.

Miners and investors should be paying attention because the change is here, now. Major companies such as Equinor (NYSE:EQNR), Shell (AMS:RDSA), Total (NYSE:TOT), Repsol (BME:REP), ENI (BIT:ENI), and BP (NYSE:BP) have begun to shift their focus to the most in-demand metals and materials of the coming green revolution in technology, transportation, batteries, energy storage, and manufacturing.

Big Winners

Copper, tin, nickel, aluminum, and rare earths, together with lithium and cobalt, stand to benefit the most as a massive demand surge over the coming decades is driven by batteries, energy storage, and the general electrification of the global economy will drive prices and demand through the roof.

Traditional base metals like copper, nickel, tin, and aluminum will continue to be in demand, but the growth or decline for lithium and cobalt will be most acute. The next 20 years, in particular, will likely see the largest amount of growth, according to the report. Some conventional commodities should get an added boost over the next 20 years, as they take centre stage in the green and digital transitions.

While the coming demand growth will be spread widely across a variety of metals and materials, some are still at risk for a fall in demand. Coking coal thermal coal and nitrogen fertilizers, in particular, have a more downbeat outlook with risk of decline on the horizon. Coal has fallen out of favour for most energy producers now, as clean energy becomes the priority. There is also a PR issue for producers as the public image of coal has become that of an antiquated and dirty energy source.

Nitrogen fertilizers are effective, but they are not safe for the environment and do not have the right image for the coming green revolutions. Some other older commodities that might struggle over the coming decades include oil, iron, steel, zinc, lead, sugar, beef, and potash/phosphate fertilizers, according to the report.

These elements are essential to much of the global economy. Still, they may see a decline as shifting consumer tastes and an economy moving toward a greener image and processes moves away from the high demand for these metals.

Efficiency, Cost, and Sustainability

The commodities of the future, according to Fitch Solutions, include copper, nickel aluminum, lithium, cobalt, tin, rare earths, and even metal scraps due to the increase in recycling and high-quality green steel. As mentioned, steel is at risk of a decline in demand, but if producers can clean up steel mining and processing, it may be possible to keep it circulating along with recycled scrap metals. This will form part of the foundation of the construction and infrastructure economy.

The keys over the coming decades will be efficiency, cost, and sustainability for batteries, which will require Innovation and development in the types of battery chemistries being used. One of the materials at risk of a drop-off in demand for batteries is cobalt. Many companies along the battery supply chain want to reduce or entirely phase out cobalt from batteries. Because of the issues with sustainability and environmental, social, and governmental risks associated with it, it is beginning to lose some of its shine.

Mining conditions for cobalt are in dire straits in some parts of the world, with child labour and underpaid workforces being used in the Democratic Republic of Congo. The recycling process for Cobalt is so complicated that it ends up polluting rivers and streams, as well as natural ecological areas. The metal could also experience some supply vulnerabilities due to a concentration in production and geopolitical hotspots or sustainability issues. Investors will struggle to attract and retain Capital if cobalt is not able to clean up its process and image.

What Will Happen to Steel?

Digitalisation and modernization initiatives for infrastructure as well as the commercial economy, along with the decarbonization of the manufacturing sector, will require higher quality, lighter, and lower carbon steel.

Demand for high-quality and green steel is expected to be strong amid the likely multiplication of decarbonization policies in the next 10 to 20 years; steel and iron ore demand, as well as zinc demand, is expected to slow as a result. These two critical materials will likely record the most subdued growth among all of the metals. Consumption is highest in countries like China experiencing construction growth. Any reduced consumption would likely be caused by China recording more lackluster growth or any rise in efficiency in the steel sector.

Carbon credits will be a large part of driving the transition and will reduce risk and disruption for the industry. Carbon credits are not a commodity in the traditional sense, but in the Fitch report, they are treated as such because they have some similarities with commodities markets. The carbon trading mechanisms currently in place multiply with accelerated decarbonization strategies by both States and corporations. As this accelerates and grows, it is forecasted that this will become a booming and robust market.

First-Mover Advantage for the EU

The EU, with its emission trading schemes directive phase 4 set to be implemented over 2021-2030, is seen as the leader of such growth. The European Union will be a large driver of the carbon swap market. Carbon swaps and trading as a commodity in the future is likely, the report reads, and this shift in thinking has already had a large impact on the power sector. Analysts believe this will continue to be a core driver of the energy transition in the region.

“We, therefore, expect the European Union ETS Market is actually likely to see a sharp increase in EUA trading volumes and prices as existing and new industries compete in a shrinking pool,” the report reads. “China is introducing its own ETS in 2021, and its remit will grow significantly in the coming years.”

Hydrogen’s Place in the Family

Another unlikely addition to the commodity story is hydrogen. Fitch expects green hydrogen, which comes from renewable resources, to become more prominent in the power industry and production to rise from less than 1% of the current global market supply to 10% by 2030. This will likely be at the expense of traditional fossil fuels or even gray hydrogen.

Green hydrogen’s acceleration is happening on the coattails of declining renewable costs, broad geographical scope, shorter development times, and its completely zero carbon footprint. One of the effects of this is that natural gas-based or blue hydrogen production growth will remain highly focused in several key markets, and market share gains will be slower due to long development times. Resource dependency and high levels of capital investment require a highly developed market.

Highly developed markets such as the US, China, Western Europe, and Canada will be the focus of markets for green hydrogen demand, which will be most concentrated in these areas because there is enough investment capital and state support to push projects along. Green hydrogen should be expected to not only power operations across the economy and reduce emissions, but could create massive opportunities for revenue streams in the mining, energy, and metal sectors.

Big Names Are Leading the Charge

Major companies such as Equinor (NYSE:EQNR), Shell (AMS:RDSA), Total (NYSE:TOT), Repsol (BME:REP), ENI (BIT:ENI), and BP (NYSE:BP) are already driving the support for low-carbon hydrogen, particularly blue hydrogen, and aim to be major producers and suppliers in the market.

No matter what path the mining industry takes, things will likely shake out the same. Cleaner, more environmentally, socially, and governmentally (ESG) friendly metals and materials will gain market share, and demand will outstrip supply for years to come. The major miners with a foothold in those sectors will benefit the most. Still, there are numerous opportunities for junior miners and even brokers to take advantage of the favourable climate.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

McEwen Mining (TSX:MUX) (NYSE:MUX), a gold mining company based in Canada, reported new assays from its Stock West target within the Fox Complex. The site, situated about 45 km east of Timmins, has been the flagship project for the company for some time, and comprises multiple drill testing sites.

This venture aims to expand the company’s reach in the project and create new drill sites for future production. The reported assays are the result of drilling less than 500 metres west of the mill.

Highlights at Stock West Drilling 2020-2021:

- 8.43 g/t Au over 14.3 m, including 23.68 g/t Au over 1.1 m – hole S20-138a

- 6.76 g/t Au over 15.6 m, including 43.00 g/t Au over 0.4 m – hole S20-148

- 6.08 g/t Au over 25.7 m including 28.30 g/t Au over 0.6 m – hole S20-149

- 6.21 g/t Au over 19.0 m – hole S20-154

- 3.80 g/t Au over 7.3 m – hole S21-157

The company’s modeling efforts have shown that there is continuous mineralization, hinting at a potentially attractive mineable area.

Discovered in late 2019, Stock West is now being drill tested in a fully funded $20 million program at the Fox Complex that includes exploration and delineation. Seven drills are active at the Fox Complex, with four of them being at Stock West, Stock Main hosting one (500 east of Stock West), and two at Grey Fox. Due to its potentially high mineralization results and ease of integration into other operations at the Fox Complex, Stock West is being seriously evaluated as a potential mining operation along with the Grey Fox deposit at the Fox Complex, about 32 km east of the site.

The company acquired the Fox Complex in 2017 from Primero Mining for US$35 million. At the time, it included the Black Fox underground gold mine, producing 2,400 tonnes per day, Stock gold mine (producing in the past), a tailings facility, and Grey Fox and Froome (two development projects). Exploration was launched at Stock in 2018, during which it identified and defined deposits east and west of the mine.

McEwen Mining (TSX:MUX) (NYSE:MUX) has also committed $5 million toward drilling at its Gold Bar project in central Nevada, about 48 kilometres northwest of Eureka. RGM044M intersected 24.3 metres, grading 3.4 grams gold from 68 metres. The investment in the project will be used to delineate new resources, replace mining depletion, and further de-risk the geological and metallurgical models that will form the basis on which to build for future production planning.

With a $716.3 million market capitalization, McEwen Mining (TSX:MUX) (NYSE:MUX) continues to grow and consolidate much of the gains of the investments being poured into exploration right now. Its joint venture partner Hochschild Mining is beginning a $9.3 million drill program in 2021 at its San Jose mine in Argentina. The majority of that investment is earmarked for exploration drilling of priority targets, including the mine’s Escondida Vein and the Telken target. With a 49% interest in the project, McEwen Mining (TSX:MUX) (NYSE:MUX) is set up to see continued growth in its gold portfolio, share price, and market cap.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

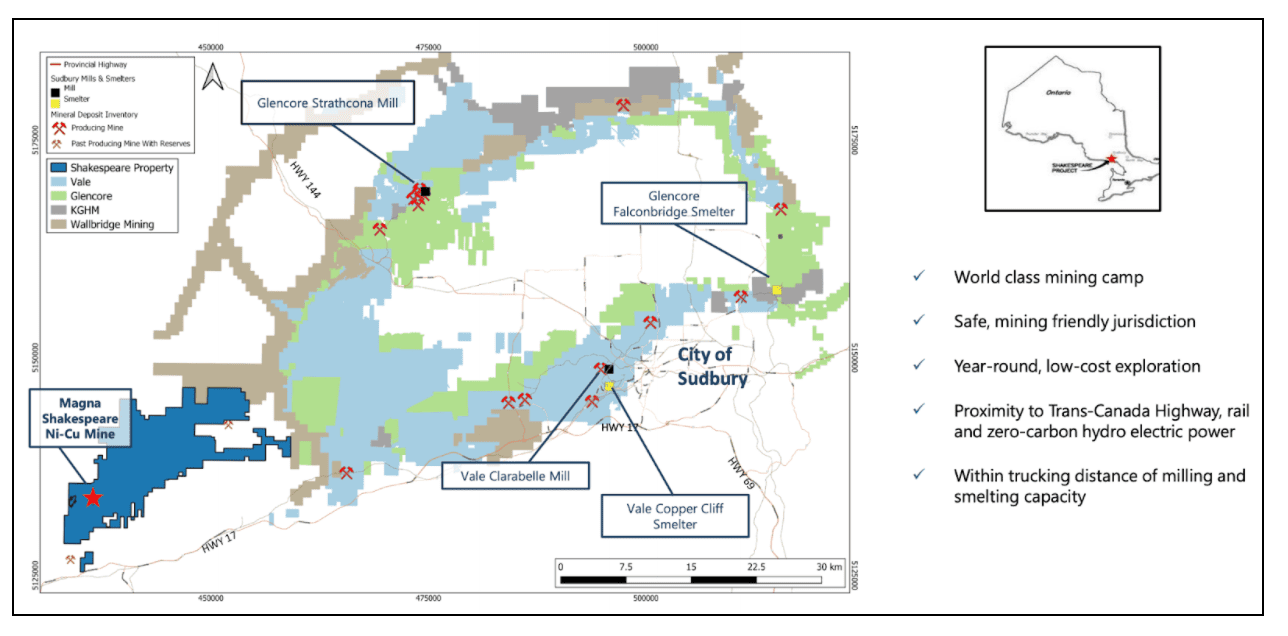

Sudbury, Canada, is a great place to mine nickel. The region has been home to some of the world’s largest nickel deposits, and the Sudbury Basin has eight producing mines. When production started over 125 years ago, it was little more than a frontier town in a country that was still finding its footing. Now, however, the area has produced over 11 million tonnes of nickel since that inaugural group of miners decided to put down roots and explore the land.

Companies like Vale (NYSE:VALE), KGHM, and Glencore (LON:GLEN), have control of most of the land packages in the region. These major players dominate the area and produce most of the nickel coming out of the Sudbury Basin. However, some junior miners are getting in on the action as well. Magna Mining (TSXV:NICU) has made its mark with a 100% stake in the Shakespeare mine, its flagship project. The mine could be a profitable one for the smaller miner with an indicated open pit resource of 14.4 million tonnes at 0.37% nickel, 0.37% copper, and 0.9g/t total precious metals. Today, Magna Mining begins trading on the TSX Venture Exchange, under the ticker NICU.

After going public, Magna Mining will have the capital to expand and advance its operations at the mine at a faster clip. The first area of focus will be expanding the exploration program to find more of the all-important nickel deposits sitting under the surface. Multiple drill targets have been set near the company’s existing deposit. This expansion of the project and the plan is really the first serious capital expenditure for the region in a long time. Additionally, the property package the company acquired includes more than 180km2 of prospective adjacent land, providing the opportunity for exploration in a section of the area that has seen little exploration in the past.

The company seems to be in the right place at the right time, with nickel fast becoming one of the critical metals for the green and digital transformations taking over the global economy. Elon Musk, CEO of Tesla, mentioned in an earnings call in 2020, “Well, I’d just like to re-emphasize, any mining companies out there, please mine more nickel.”

The Tesla boss’s call for more nickel mined in an environmentally conscious and socially responsible way was a wake-up call that the industry needs to step up to the plate and get more of the metals required for batteries, energy storage, and digital devices. Musk also later shared the company’s goal of implementing a battery supply model in North America to facilitate the production of zero high-cost cobalt and more low-cost nickel. It is rare that a company has a client wanting more than they can provide, but this is the state of play for the nickel miners out there right now.

As demand continues to pick up, projects in the Sudbury basin and beyond will also need to accelerate their timelines and invest more into existing nickel projects to keep up. New projects will also be necessary, both from major mining companies and the junior miners entering the field.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

November 2020 marked an inflection point for uranium stocks, which have been rising ever since. The two leading US-listed uranium miners are both up about 150% over the past three months. Even smaller miners like Western Uranium & Vanadium Corp. (CSE: WUC)(OTCQX:WSTRF) and Fission Uranium Corp. (TSX: FCU)(OTCQX: FCUUF) have seen gains of around 70% over the past 3 months.

The trend for some of the uranium miners mentioned above is difficult to explain at the levels we are seeing. Uranium prices have picked up since about mid-March, but not enough to justify the more than 150% we have seen for some of these stocks.

Shifting Tides and Opinions

Much of the talk in the past around uranium has been lukewarm at best. The world backed off of nuclear power after a few accidents caused disasters in Japan, Russia, and a few more regions. The public perception of nuclear power was that of a dangerous and violent power, because of the shocking images those reactor explosions produced. The risk seemed high even though they were rare events. The reason was the impact. The probability is low, but the stakes are so high. Our radar was pinging off the charts because of the kind of destruction those accidents caused.

However, for the coming change in renewable energy, we will need to wean ourselves off of the fossil fuels that have powered the world for the past few hundred years. As we advance, it will be imperative for countries and companies to rally behind the transition to green energy. One of the tools we can use to get there is uranium for nuclear power generation. Currently, nuclear reactors could feasibly replace much of the US power grid if done correctly. While the public relations nightmare of an accident could cost us any progress, the technology is modernized and safer, and the risk of an accident much lower.

For nuclear power to be an appropriate aid in a rapid transition to green energy, uranium will be needed in much larger quantities. Mining will need to begin and expand in domestic markets to keep steep prices at bay. According to Jack Lifton, host of The Technology Metals Show, “The USA imports 95% of the uranium it needs to operate its 25% of the worlds civilian nuclear reactors that provide almost 30% of American baseload (available at any time) electricity needs and accounts for more than half of all carbon-free power generation in the USA. It’s imperative, therefore, that America produces uranium domestically for its security of supply of carbon-free electric power. The US Congress has recognized this need and recently funded a program to buy domestic uranium.”

A Budding Bull Market Begins

Industry insiders and mining company executives agree that a bull market is building, and the forward guidance for spot uranium prices and mining companies extracting the material is upward, to say the least.

At least part of uranium’s pickup has been due to the Biden victory. The US President set a target of 100% carbon-free electricity by 2035, an ambitious one. Part of his strategy will likely include subsidies and investment in companies that can help reach that goal; this includes companies in the nuclear power space. Markets believe and are beginning to price in the fact that Biden will probably need to support nuclear energy as a way of reaching that target in just fourteen years.

The lack of domestic production and plans has also meant supply issues. As demand continues to rise and supply constricts, prices have risen to match the situation. This is primarily a domestic issue, as the Uranium Committee of the Energy Minerals Division of the American Association of Petroleum Geologists commented in their released 2020 Annual Report that prices and supplies of uranium worldwide look good. There is no shortage of uranium in the market around the world, but without domestic production, many countries will be caught out buying abroad for higher prices. It is essential that governments continue to expand their uranium plans and ensure that miners have the resources and clearance to expand their uranium production now.

Risks of Underdeveloped Domestic Uranium Production

After the pandemic exposed some of the flimsiness of global supply chains, the realisation that the rare metals supply issues need to be addressed now. Metals like lithium, cobalt, vanadium, and neodymium are often not produced in the US but imported from other countries like China. Being dependent on other countries isn’t just a logistical issue when governments can’t get stocks to fill demand, but potentially a national security risk.

When countries control the supply of a resource, it can become a bargaining tool. Monopolies or strong control of a market means a company or country can often dictate prices, particularly when demand begins to rise.

Painting a Rosier Picture

Positive strength and a turning tide in the public perception of nuclear power have benefited the United States, and the country is the world’s largest producer of nuclear power. Of the total share of global nuclear generation for electricity, the US accounts for more than 30%. It seems that uranium supply isn’t the crisis we are likely to deal with in the nuclear industry. Right now, the main problems are a lack of a large domestic market for new reactors and the costs of keeping the plants that are operating now at profitable levels.

Globally, the picture is rosier, with the most recently released World Nuclear Association’s Fuel Report noting that “…there are 53 new reactors under construction, more than 100 reactors in the planning stage, and another 320 in the proposal stage.” Production has fallen, though, with only 123 million lbs. produced last year, according to UxC, a nuclear-fuel data and research company.

Expanding projects and starting new ones will be essential to meeting the domestic demand in North American in the coming years as the electrification of the economy accelerates. Right now, efforts are not hitting the mark. A 33 million lb. uranium is forecast for 2021 by BMO Capital Markets, representing 18% of current demand. That gap needs to be filled, but there also needs to be a surplus goal to keep prices under control.

Three Top Uranium Miners

For the miners extracting and producing uranium, this is a golden moment. They have a confluence of events and plans that are lining up for their benefit and putting them in a position to profit for decades. Even when the transition is mostly complete, there will be an ongoing need for uranium for energy production. Here are the three companies poised to win in this clean energy game:

1. Cameco (NYSE:CCJ)

As the world’s largest publicly traded uranium company, Cameco is uniquely positioned to expand its control over the market. First-mover advantage and size means that its footprint in Kazakhstan, Canada, and the US will only grow. The company holds 455 million pounds of proven and probable mineral reserves, with a licensed capacity to produce upwards of 53 million pounds of uranium concentrates. As demand increases, Cameco (NYSE:CCJ) will be one of the biggest winners.

2. Ur-Energy (NYSE:URG)

Ur-Energy is a junior miner, and as such, has a lot of room to grow. The company’s latest project, Shirley Basin, was acquired in 2013. As progress continues on assessments and planning, up to 6.3 million pounds of U3O8, a uranium compound, might be produced by this up-and-comer. Its main Lost Creek uranium facility in Wyoming has a capacity of two million pounds per year, limited by physical design. This may be a good value play if the company can scale up in preparation for the demand increases for uranium around the world.

3. Uranium Energy Corp. (NYSE:UEC)

With a wide footprint and reach, Uranium Energy Corp. has projects in Wyoming, Texas, New Mexico, Paraguay, Colorado, Arizona, and Canada. The benefit of this diversification is that the company can more easily avoid geopolitical risks over the long term while setting itself up for success no matter where it operates. By spreading risks around to different regions, this company may be more stable than many of the junior uranium mining companies out there. Its other unique quality may be that it is entirely unhedged. The company holds zero contracts at pre-set prices and is massively leveraged to uranium’s price as a result. Compared to most other uranium mining companies, Uranium Energy Corp. is more likely to be able to take advantage of a rising price for spot uranium if supply is not expanded quickly.

The Future

Nuclear energy is still a tiny portion of energy production in the US. In recent years, it reached up to 20% of total energy production. Compared to countries like France that use nuclear energy for about 70% of total energy production, this is a pretty low number. There is plenty of room to grow for the industry. More nuclear projects continue to be approved, and governments are realising that nuclear energy is a better, cleaner option for the transition to renewables. It is a powerful, dense energy that could ease the way from fossil fuels to solar and wind energy.

Uranium stocks will be an attractive option for investors looking for a middle ground and something to gain exposure to this transition and the lofty decarbonisation goals set by the US government, as well as other developed economies around the world.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

For countries to reap the rewards of their natural resources, they need to make sure there is a favourable climate for miners and businesses operating within their borders. For Ecuador’s new president Guillermo Lasso, that means welcoming mining companies with open arms as they work to build a sector that is critical to Ecuador’s national economy. Chile hosts some of the biggest mining companies in the world, including BHP Group Ltd. (NYSE:BHP), Anglo American Plc (LSE:AAL.L), Glencore Plc (GLNCY), Antofagasta Miners (LSE:ANTO.L), and Freeport-McMoRan Inc. (NYSE:FCX).

Walking a Tightrope

Recent discussions by lawmakers in Chile could throw the country’s status as a mining hotspot into question. If investors or companies get spooked by the new tax, it could hamper efforts to invest in new projects or expand the ones currently operating in the region. Particularly for proposed royalty deals on copper and lithium sales, the ongoing discussions now could throw a wrench into the works of years of planning and investment.

Foreign investment in the country is an essential source of stimulus and job creation. The mining industry contributes massively to the national economy, and it has made Chile the biggest copper-producing nation in the world. With the new bill approved just last week imposing higher taxes on sales, and cash generated based on the current running price of copper, those contributions could begin to dry up.

A Painful Tax

Initially, lawmakers wanted to impose a 3% flat royalty for mining companies extracting copper and lithium. The valuable metals have seen steady price increases over the years, and with the coming electrification of the global economy, this trend shows no signs of abating.

A new version of the bill proposes a marginal rate of 15% on sales with copper prices between $2 and $2.50 per pound and up to 75% on any revenue generated from fees about 4%. This sliding scale has miners concerned about the future of their operations in the country, as copper’s price seems to have no slowdown in sight. If the bill were approved today, with current copper prices, the royalty rate would be 21.5%. Miners would be able to discount refining costs and some other tax write-offs for any copper sold as refined cathode, but the cut would be almost prohibitive for them.

“You can absolutely try and take more from the golden goose…”

This proposed tax would hit the biggest mining companies the hardest, with the bill affecting miners that produce more than 12,000 tonnes of copper and 50,000 tonnes of lithium per year. One of the companies that would be affected is speaking out against the proposed bill, as it would cut into the country’s status as a mining partner for some of the largest mining companies in the world. According to Ragnar Udd, President of BHP Minerals Americas, “You can absolutely try and take more from the golden goose but you just need to be very clear on what the implications are on that long term. The sort of reforms that are being put forward at the moment will be really quite damaging to the industry.”

“These are tax levels akin to expropriation…”

Even though the proposed tax has miners worried for the future of their operations, it is unlikely that the bill will be passed, especially in its current form. He believes the current system is fine, under which miners are charged a variable rate of up to 14% on operating profit. This rate only applies to large producers and does not affect the less competitive mines, giving them a shot at growth and keeping the country competitive for international investors.

For now, worry and outright opposition are the state of play, as one prominent mining group president has already touched on. Resistance is strong, and this is unlikely to let the bill pass as is. Sonami president Diego Hernandez issued a statement calling the project unconstitutional. He made it clear that the consequences of the proposed bill on the industry and the country would be severe and damaging. With this bill, Sonami (an organization representing copper miners in Chile) predicts that 12 of the 15 biggest miners operating in the country would end up operating at a loss.

Diego Hernandez himself has made it clear that the bill is unacceptable: “These are tax levels akin to expropriation and this is going to inhibit investment immediately.”

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

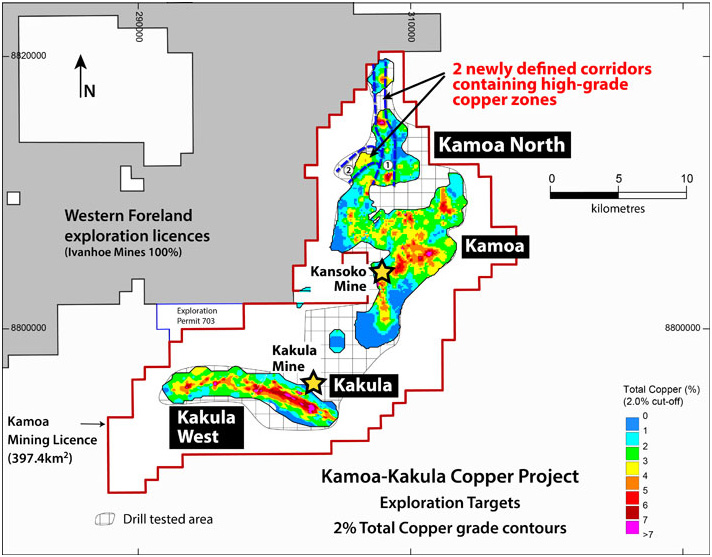

The world continues to watch the mining industry for signs of a serious commitment to the decarbonisation efforts sweeping the global economy. Company after company continues to put their effort and money where their mouth is. The latest company to jump onto the net-zero train is Ivanhoe Mines (TSX:IVN), committing to net-zero greenhouse gas emissions at its Kamoa-Kakula Copper Mine.

The company’s CEO, Robert Friedland, will be speaking today at the 2021 Goldman Sachs Copper Day and made the announcement before his speech.

The mine is expected to be the world’s highest-grade major copper mine and should begin producing its first copper concentrates soon. The Phase 1 mining rate is expected to be 3.8 million tonnes per year, with an approximate feed grade of more than 6%. Phase 2 should see a ramp-up to 7.6 million tonnes per year, and with the proposed expansion to 19 million tonnes, Kamoa-Kakula could end up being the world’s second-largest copper mining complex.

The company’s ambitions don’t stop at production. The way Ivanhoe plans to mine is focused on support from a green electricity grid and a plan to reduce the use of fossil fuels until the net-zero emissions goal is reached. Electric, hybrid, and even hydrogen technologies are proposed for trucks and transportation. While the upfront investment will cut into the cash on Ivanhoe’s balance sheet, the costs down the road from reduced fuel costs, lower ventilation costs, and even lower health and safety costs as the healthier and cleaner technologies pose less of a risk to workers will more than make up for those initial investments.

The Canadian company is not just following but leading the way when it comes to large-scale net zero emissions projects. Its Kamoa-Kakula copper discoveries in the Democratic Republic of Congo (DRC) have opened the opportunity for the project to become one of the world’s largest and make the company one of the world’s largest copper producers.

Pushed along by the Paris climate agreement and the Canadian government’s initiatives in reducing emissions to zero by 2050, copper mining companies like Ivanhoe (TSX:IVN), Solaris Resources (SLS.TO), and Glencore (LON:GLEN) are pledging their efforts to the critical cause. This is not just because of the ethical and environmental benefits, but because investors also demand these commitments now. Without a plan for the environmental, social, and governmental (ESG) principles in the planning stages of projects, investors may be hesitant to commit capital.

This year’s virtual Canadian Institute of Mining (CIM) Convention and Expo is seeing some positivity in forward-looking projections, and an undeniable confidence in the mining industry. One of the convention’s major speakers, Anglo-American CEO Mark Cutifani cut right to the chase in explaining that the mining sector is absolutely essential to both modern life and the global economy. According to him, “the simple fact is that the world cannot survive without mining and our contribution to literally every aspect of modern life.”

Mining activity is a significant driver of economic activity on its own, but the true reach of the industry is seen and felt in the other industries that rely on mining to not only thrive, but survive. Food production, construction, transportation, renewable energy infrastructure, and the all-important sectors of communications and energy all rely on mining in some way, shape, or form.

Perception vs. Reality

The convention, and Anglo American’s CEO, in particular, are quick to note that the disconnect between the reality and the public’s perception of mining is significant: “Even with all the contributions we make, people tend to see us as an industry that takes more than it gives. One of the things we don’t do well as an industry is talk about what we do.”

For example, the agriculture industry has a much larger footprint than the mining industry but doesn’t get half the criticism or attention. Agriculture takes up approximately half the world’s habitable land, with mining taking up a comparatively minuscule 0.04% of the habitable land available. The attention, however, is usually on the fact that the mining industry requires extraction for production, almost always of natural resources.

The industry and Anglo-American have begun to shift the narrative to highlight the good the industry does and the economic activity it generates around the world. On top of that, the industry is making a conscious and significant effort to join the global decarbonisation efforts underway now to plan for a future of cleaner mining and more responsible operational practices. Mining companies like Anglo-American plan to pivot to a new reality in which it becomes a “materials solutions company” delivering a more circular business model to include more recycling, efforts to slow or stop climate change, and a social responsibility approach that aligns with the needs of societies in every region in which they operate.

Part of the disconnect between the efforts and solutions being implemented in the mining industry and the public perception of the industry is a lack of communication. The industry has not conveyed the changes made in the past ten years, and the acceleration happening now that is so critical. The changes made now will also have significant ripple effects, as the mining industry is moving much faster than most other industries to get on board with the new, cleaner, and more sustainable reality.

An Important Convention for an Important Industry

The virtual convention will continue through tomorrow (May 6), with some of the biggest companies and CEOs in mining contributing to panels and discussions throughout the convention. Mark Cutifani spoke on a panel moderated by Jerrod Downey, president of Crownsmen Partners, and included Jody Kuzenko, president and CEO of Torex Gold Resources (TSX: TXG), David Cataford, president and CEO of Champion Iron (TSX: CIA) (ASX: CIA), and Denise Johnson, group president of Caterpillar.

The theme of the session was “resilient and thriving”, mirroring the results of 2021 as the mining industry continues to expand at full force. The 2020 pandemic hit the industry in some regions as lockdowns restricted mining activity, but growth is in the air now as companies press forward with current projects and expand into new ones.

Streaming and royalty contracts bring to mind a particular industry immediately: entertainment. Musicians are paid royalties for their music when it is played, and streaming services push music to listeners as the streaming services pay musicians for their share of total plays. The other business streaming services bring to mind is video streaming, from videos (YouTube) to movies and television (Netflix).

There is, however, another kind of streaming that may not be as well-known as the entertainment versions but has a similar profitable business model and a continued increase in interest around the world: metal streaming and royalty deals.

A Simple Strategy

Metal streaming-and-royalty contracts are essentially transactions that allow mining companies to sell future production or revenues in return for an up-front cash payment. The payment funds discovery, exploration, or production and a portion of either the physical metal or the revenue generated by selling it.

Streaming deals focus on specific commodities produced by a particular project. In return for an up-front cash payment (deposit balance), the streaming partner is given the rights to a share of the future production at an agreed-upon discounted price. The price might be fixed, or it might be a floating percentage of the prevailing spot price. This allows streaming partners to pay when they receive instead of taking on more risk and paying without conditions. The miners receive payment on delivery for streamed physical volumes, raising the incentive to produce.

Royalty deals are ultimately indifferent to the commodity they represent and instead are based on overall project revenues. The royalty company never really touches or “sees” the commodities produced but receives a share of the revenue from sales (royalty). To settle a royalty deal, the miner must use cash, while a miner would need to settle with physical metal in the case of a streaming deal.

Gaining In Popularity

There has been a big bump in investor interest for royalty and streaming deals in the mining industry over the past ten years. Still, these deals make up just 1%-3% of overall debt and equity financing. The past ten years have seen a 700% growth for the streaming and royalty market, reaching more than $15 billion in 2019. The result is an enthusiasm that seems ready to drive the next ten years faster and higher.

Streaming deals are the most popular format for investors right now and should see the most growth. Gold and silver make up 96% of the streaming market, and palladium, cobalt, and copper comprising the rest of the 4%. Even though the gold and silver streaming market is well-developed, these deals only cover about 14% of total gold by-product output and less than 6% for silver.

The current expansion for streaming deals in cobalt, nickel, and copper is driving investor interest in mining for new investors largely because of the increased demand for these tech metals. Electric vehicles, batteries, and all of the green technologies powering the decarbonization of the global economy are supporting high demand and growth for streaming deals at the same time.

Low Risk, High Reward

Streaming is also a great way to gain exposure to the commodities investors are interested in, without the exposure to the risks involved. Investors do not need direct investment to be involved in the deals, and issues related to environment, social, governance, or operations are minimized.

The concentration of streaming deals is also likely to change, as right now, 50% of all deals are done with mines in Canada, the U.S., Mexico, and Peru. That lack of regional diversity has largely been due to lower barriers for cross-border transactions and investment in the Americas. It leaves the door open for regional expansion in the future.

The Experts Agree

McKinsey’s recent report on mining streaming and royalty deals concludes that the trend is on an upswing for the next decade that will likely fuel more mining and better flexibility for investors. As the streaming dealbook continues to grow, this will be a favourite play for anyone looking for exposure to the valuable commodities of the future like copper and cobalt, without gaining too much exposure to the risks of mining in such a competitive market.

Glencore (GLEN:LN), one of the world’s largest producers and marketers of copper, produced 1.26 million tonnes and sold 3.4 million tonnes through its marketing business in 2020. Their copper production is so large that the company is also a major producer of cobalt, a byproduct of copper. Most of their cobalt product comes from the Democratic Republic of Congo.

The Start of an Upward Trend

While 2020 was a good year for Glencore (GLEN: LN), 2021 began to set the trend for production increases. On Thursday, the company reported 301,200 tonnes produced in the first quarter of 2021, 3% higher YoY from Q1 2020. While the reopening of production and the lifts of restrictions for miners contributed to this bump, productivity improvements also lent a hand to the increase.

“The group’s overall production was broadly in line with our expectations for the first quarter. Production in Q1 2021 reflects that many of our operations continue to maintain thorough Covid-safe working practices, as appropriate for each specific country and region. Full-year production guidance has been maintained for our key commodities,” according to CEO Ivan Glasenberg.

Big Influence

Glencore’s business is one of the most diversified, comprising more than 60 commodities. The company has operations at approximately 150 mining and metallurgical sites in more than 35 countries. Employing 135,000 employees and contractors, where Glencore goes, significant employment number improvement often follows, and the company holds so much sway in many commodities that it is often responsible for price changes as a direct result of supply and demand.

Copper’s in-demand status continues to increase, and Glencore’s production increase is just a piece of what will be necessary over the coming years to meet the massive demand coming. As one of the largest producers and marketers of copper in the world, Glencore (GLEN: LN) will need to take a lead position in the market and help balance the supply issues facing the industry right now.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |