Three Valley Copper (TSXV:TVC) took an important step today in funding the advancement of the company’s flagship 91.1% owned Minera Tres Valles copper mining project. Initially, it entered into an agreement with co-lead underwriters and joint bookrunners PI Financial Corp. and Eight Capital for a C$10 million bought deal financing.

Then, shortly after, due to significant investor demand, PI Financial Corp and Eight Capital amended the agreement to increase the size of the deal. It now consists of 50,000,000 units at a price of C$0.32 per unit for gross proceeds of C$16,000,000.

The deal includes 50,000,000 units of common shares at a price of C$0.32, and one common share purchase warrant for each unit. These are exercisable into one common share of the company at a price of C$0.45 for a period of 30 months following the closing of this offering.

Advancing the MTV Mission

This will help fund the advancement of exploration and development at the company’s Minera Tres Valles project and for working capital and general corporate purposes. The offering is expected to close on or around November 19, 2021, subject to regulatory approvals including the approval from the TSX Venture Exchange where Three Valley is listed under the symbol “TVC”.

The underwriters also have the option, exercisable at the offering price for a period of 30 days following the closing, to purchase up to an additional 15% of the units or the components of the units to cover over-allotments and for market stabilization purposes.

Strategy Comes Into Focus

The announcement comes on the heels of the October 20 announcement that the company had initiated a strategic review to explore alternatives for the enhancement of shareholder value. The goal is to maximize production at Minera Tres Valles, and increase cash flows from its mining assets in Chile.

This will encompass a thorough evaluation of the development strategy, business plan, market valuation, and capital structure, and could bring into focus a number of new opportunities for the company going forward. While this financing is one of them, strategies could include mergers, strategic partnerships, acquisitions, restructuring, and refinancing of long-term debt.

Through the strategic review, Three Valley will be able to chart a clear path forward for the end of 2021 and into early 2022 as it looks to explore, develop, and produce at Minera Tres Valles. The property consists of 46,000 hectares, 95% of which are unexplored, presenting a large opportunity and potential for future development.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Pretivm Resources (TSX:PVG) (NYSE:PVG) has made a new high-grade gold discovery on its Brucejack property in British Columbia, Canada. The property is located approximately 3.5 kilometres north of the Valley of the Kinds deposit, and the discovery was made at the Golden Marmot Zone.

Assays have now been received for its first nine drills holes. Eight of the nine drill holes intersected gold with a highlight of 53.5m grading 72.5 grams per tonne gold; including 50cm grading 6,700g/t gold and 3,990g/t silver.

President and CEO of Pretium Resources, Jaques Perron said in a statement: “Initial results from Golden Marmot are exciting and affirm the district-scale potential of the Brucejack property.”

The property’s gold mineralization covers a zone about 150m by 250m and 275 in depth, and occurs in the same host rocks and with the same alteration signature as the Valley of the Kings deposit. The company has claimed that this may be an indication that it could also be a new high-grade deposit.

Anticipation for Q3 Results

The company also recently announced it will release third-quarter 2021 operational and financial results after the market close on Thursday, November 11, 2021. This is to be followed by a webcast and conference call on Friday, November 1, 2021. Investors will also be waiting to hear about the new discovery and more details on how the company interprets the discovery.

No doubt a positive development, the high-grade gold discovery could also change the drill program or accelerate the timeline if Pretium decides it is economically feasible and fits forward guidance.

Pretium’s Q2 2021 operating and financial results showed the company was on-track for annual guidance, and that its cash position had then exceeded its debt. Perron said in a statement: “The second quarter of 2021 started under some challenging circumstances, but thanks to the hard work of our team we made consistent improvements through the quarter and we remain on track to achieve our annual guidance. We accomplished another profitable quarter with $152.3 million in revenue, generated $50.7 million in free cash flow and we have reached a key turning point where our cash position now exceeds our debt.”

Production came in at 83,083 ounces of gold, revenue hit $152.3 million through the sale of 84,618 ounces of gold, and the company was on track to achieve the 2021 guidance of 325,000 to 365,000 ounces of gold produced at an AISC between $1,060 and $1,190 per ounce of gold sold.

Brucejack continues to be a focus for the company, and progresses consistently quarter after quarter. The company will likely extend the Valley of the Kings deposit further, and the fourth quarter of 2021 is likely to bring new drill results. The Brucejack Mine is a high-grade gold mine located in northwest British Columbia, about 65 kilometers south of Stewart.

Optimistic Outlook

Pretivm Resources isn’t the only company with an optimistic outlook for 2021. Despite the obstacles and challenges posed by the pandemic, 82% of global mining industry CEOs believe economic growth will improve in the next 12 months, according to PCW’s BC Mining Survey. The long tradition of discovery mining lays the foundations for the next generation of investment.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

This morning, Collective Mining (TSXV:CNL) has announced that is has made a significant grassroot discovery at the Pound target within the San Antonio project. This comes right on the heels of the recent discovery at the Donut target at its Guayabales property.

One of three targets generated at the San Antonio project, reported assay results are from the recently completed Phase 1 reconnaissance drill program which tested two of these targets.

Ari Sussman, Executive Chairman of Collective Mining commented in a press release: “The wide and continuous zones of mineralization intersected from surface at Pound are exciting and suggest we are either peripheral to or above a very large porphyry system. It is extremely pleasing that we have made brand new significant discoveries with the initial drill holes into grass root generated targets at both our Guayabales and San Antonio projects. With funding in place through 2022, the Company will become aggressive in the short-term with follow up drilling on our new discoveries and testing newly generated targets across the project portfolio.”

Highlights (Tables and Figures 1 to 5)

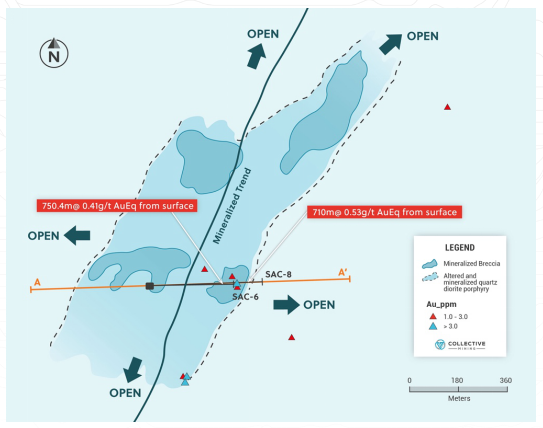

- Continuous gold (“Au”), silver (“Ag”) and base metal (copper and molybdenum) mineralization has been intersected from surface, over the full core lengths of two reconnaissance diamond drill holes at Pound as follows:

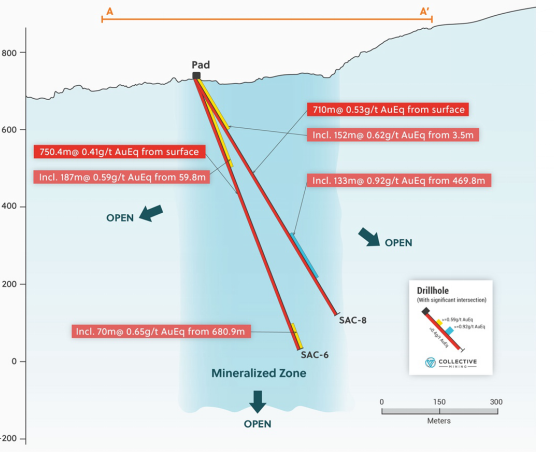

- 710 metres at 0.53 g/t gold equivalent from surface including 133 metres at 0.92 g/t gold equivalent from 470 metre depth (SAC-8); and

- 750 metres at 0.41 g/t gold equivalent from surface including 187 metres at 0.59 g/t gold equivalent from 60 metre depth (SAC-6).

- 710 metres at 0.53 g/t gold equivalent from surface including 133 metres at 0.92 g/t gold equivalent from 470 metre depth (SAC-8); and

- Importantly, both drill holes ended in mineralization with copper and molybdenum grades increasing at depth including:

- 70 metres at 0.12% copper and 89 ppm molybdenum from 681 metre depth (SAC-6); and

- 133 metres at 0.15% copper and 27 ppm molybdenum from 470 metre depth (SAC-8).

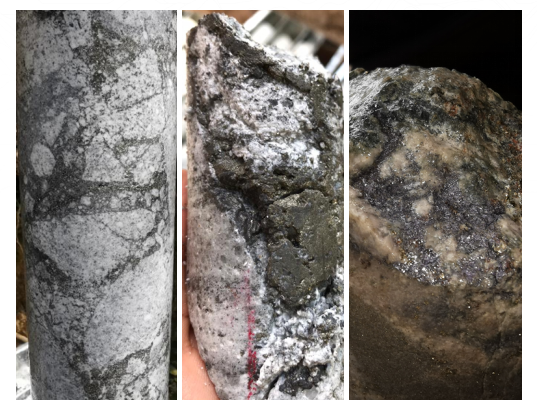

- Pound mineralization is related to hydrothermal breccia and highly altered, quartz diorite intrusive which have been overprinted by late stage, polymetallic veins. Pound is located within a NE-SW trending corridor, as defined by mineralized breccia and altered intrusive, which is open in all directions and has been mapped to date over a strike length of approximately 1.3 kilometres.

- The alteration system associated with Pound (advanced Argillic litho-cap) is related to the upper and peripheral portions of a porphyry system. The Company is currently reviewing its options for follow up exploration which would include initiating a Phase II diamond drill program and a high-resolution and deep penetrating IP survey as has recently and successfully been undertaken at the Guayabales project.

Table 1 Initial Diamond Drilling Results at the Pound Target

| Hole ID | From

(m) |

To

(m) |

Intercept

Interval (m)** |

Au

(g/t) |

Ag (g/t) | Zn

(ppm) |

Pb

(ppm) |

Cu % | Mo % | AuEq

(g/t)* |

| SAC-6 | 0 | 750 | 750 | 0.32 | 6 | 454 | 303 | 0.02 | 0.001 | 0.41 |

| Incl. | 60 | 247 | 187 | 0.50 | 9 | 274 | 63 | 0.00 | 0.000 | 0.59 |

| And | 681 | 750 | 70 | 0.41 | 2 | 79 | 11 | 0.12 | 0.009 | 0.65 |

| SAC-8 | 0 | 710 | 710 | 0.40 | 6 | 352 | 130 | 0.04 | 0.001 | 0.53 |

| Incl. | 4 | 156 | 152 | 0.50 | 11 | 281 | 65 | 0.01 | 0.000 | 0.62 |

| And | 470 | 603 | 133 | 0.61 | 6 | 504 | 307 | 0.15 | 0.003 | 0.92 |

* AuEq (g/t) = (Au (g/t) x 0.95) + (Ag g/t x 0.013 x 0.90) + (Cu (%) x 1.83 x 0.92) + (Mo (%) x 4.57 x 0.92), utilizing metal prices of Cu – US$4.00/lb, Mo – US$10.00/lb, Ag – $20/oz and Au – US$1,500/oz and recovery rates of 95% for Au, 90% for Ag, 92% for Cu and Mo.

** a 0.1 g/t AuEq cut-off grade was employed with no more than 10% internal dilution. True widths are unknown and grades are uncut.

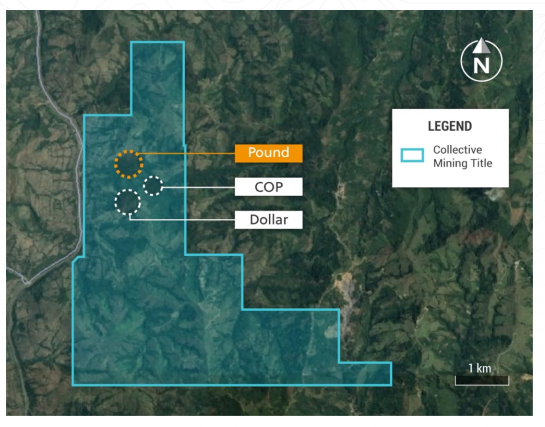

Geological Details of the San Antonio Project

The San Antonio (“SA”) Project is located in the Middle Cauca Gold Belt (“MCB”), 80 km south of Medellin and 50 km north of Manizales, Department of Caldas, Colombia. The MCB has been the most prolific belt for Miocene aged, porphyry and epithermal vein discoveries within Colombia and multi-million ounce discoveries in recent years include Buriticá, La Colosa, Nueves Chaquiro and Marmato.

The SA covers an area of 3,853 hectares and hosts multiple quartz diorite, diorite intrusive and breccia bodies of Miocene age which intrude basement schists and younger volcano-sedimentary packages.

Three specific grassroots exploration targets have been outlined by surface mapping, sampling, soil geochemistry, geophysical modelling, and shallow scout drilling. These are referred to as the Dollar, COP and Pound targets.

The Pound target is located in the northern portion of the project, is defined by multiple hydrothermal breccia bodies hosted within highly altered diorite and quartz diorite intrusive and overprinted by late stage, polymetallic veins. This zone of altered intrusive and breccia bodies trends NE-SW and has been mapped for a strike length of plus 1.3 kilometres. The zone is still open to the NE and SW. Outcrop exposures on the southern border of this target area include epithermal vein systems within a preserved lithocap of advanced argillic alteration which is superimposed on hydrothermal breccia bodies which grades laterally and downwards into intermediate argillic alteration assemblages. These rocks are interpreted to reflect preservation of the shallow levels of the porphyry system. The initial two reconnaissance diamond drill holes, SAC-6 and SAC-8, were drilled to respective downhole depths of 750 metres and 710 metres and intersected various hydrothermal breccia (pyrite matrix), altered quartz diorite intrusive and late-stage polymetallic veins. All the rock units have been hydrothermally altered with an earlier sericitic event overprinted by a strong, advanced argillic phase with various aluminosilicates. At depth, various diorite phases display disseminations and aggregates of chalcopyrite and molybdenite in contact with large blocks of metamorphic schist. The target remains open in all directions and further work is envisaged and will commence with a deep penetrating, high-resolution, induced polarization survey down to minimum depths of 900m below surface followed by a Phase II expanded diamond drilling program. Exploration targets include the mineralized breccia and a porphyry system postulated to occur below the lithocap.

The COP target is located 800 metres south of Pound and is defined by highly anomalous molybdenum (8 ppm to 108 ppm) and gold (up to 2.74 g/t) in soils in association with altered diorite porphyry and quartz veinlets over an area of 650 metres x 350 metres. The surface expression of the COP target is coincident with geophysical anomalies, at 200-300 metres depth which include a positive magnetic anomaly and IP chargeability and resistivity highs. COP has not been tested, other than a single historical borehole drilled just south of the target area, returned an intercept of 99 metres at 0.42 g/t gold and 4.9 g/t silver within unmineralized country rocks partially intruded by mineralized porphyry quartz veins at a depth of 608 meter downhole. The mineralization encountered in the drill-hole is interpreted to be leakage from the COP target directly to the north.

The Dollar target is located 400 metres south of COP. At surface various outcrop of quartz diorite porphyry host stockwork and sheeted quartz-magnetite vein systems associated with disseminated pyrite covering a 500-metre radius. Shallow scout drilling (6 holes) to cover the target area, identified the main mineralized porphyry. Holes SAC-1 to SAC-5 and SAC-9 returned gold intercepts of 0.1 to 0.3 g/t over various angled intercepts of 100 metres to 600 metres length within or across the various outcrops of the mineralized stockwork system. Based on the shallow intercepts a deeper hole was drilled into the mineralized stockwork and returned the intercepts outlined in Table 2 below. Gold, copper and molybdenum grades improve with depth and further deeper drilling is warranted, particularly as the project area is located approximately 300 metres above an accessible valley floor.

Table 2 Initial Deep Diamond Drilling Hole at the Dollar Target

| Hole ID | From

(m) |

To

(m) |

Intercept

Interval (m)** |

Au

(g/t) |

Ag

(g/t) |

Zn

(ppm) |

Pb

(ppm) |

Cu % | Mo % | AuEq

(g/t)* |

| SAC-7 | 0 | 621 | 621 | 0.22 | 3 | 207 | 49 | 0.01 | 0.001 | 0.26 |

| Incl. | 547 | 621 | 74 | 0.49 | 6 | 195 | 19 | 0.05 | 0.001 | 0.62 |

* AuEq (g/t) = (Au (g/t) x 0.95) + (Ag g/t x 0.013 x 0.90) + (Cu (%) x 1.83 x 0.92) + (Mo (%) x 4.57 x 0.92), utilizing metal prices of Cu – US$4.00/lb, Mo – US$10.00/lb, Ag – $20/oz and Au – US$1,500/oz and recovery rates of 95% for Au, 90% for Ag, 92% for Cu and Mo.

** a 0.1 g/t AuEq cut-off grade was employed with no more than 10% internal dilution. True widths are unknown, and grades are uncut.

The San Antonio project benefits from favorable topography with approximately 600 vertical metres of elevation change from the mountain peaks to the various flat lying valleys. Additionally, the topography is not overly steep, lending itself to multiple potential infrastructure development scenarios should an economic deposit be discovered in the future.

Source: Collective Mining

Figure 1: Plan View of the San Antonio Project and the Pound Target

Figure 2: Plan View of the Pound Target

Figure 3: Cross Section of Pound Drilling

Figure 4: Core Photos: Pound: SAC-6 and SAC-8

Figure 5: Core Photos: Dollar, SAC-7. Clay Alteration Overprint Decreases With Depth

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Sibanye-Stillwater (NYSE:SBSW), a South African precious metals mining company, has inked a deal with private equity firm Appian Capital Advisory for two nickel and copper mines in Brazil. The deal is valued at $1 billion. The transaction also includes a 5% net smelter return royalty (NSR), valued at approximately $218 million for future underground production from Santa Rita. CEO Neal Froneman has said it is one of the ten biggest open-pit nickel sulfide assets producers in the world.

Froneman said, “The transaction represents a unique opportunity for Sibanye-Stillwater to acquire significantly pre-developed and pre-capitalized, low-cost, producing nickel and copper assets.”

Appian will also keep its investment exposure to the upside potential of the two assets in question, through NSRs. These will be equal to a 35% stream on gross gold revenues in the case of Meracao Vale Verde. Appian will also retain 100% ownership of the Pereiro Velho gold exploration property after the acquisition.

The highly valuable project has long-term upside potential that Appian, a London-based firm, does not want to give up completely.

This is Sibanye’s fourth battery metal investment this year, following a recent transaction in September for 50% of ioneer Ltd’s lithium-boron project in Nevada. The deal spree comes as the company aims to boost its growing battery materials portfolio.

Battery Metals Battles

Miners are scrambling to acquire battery metals assets for nickel, copper, and lithium mining as the race for the decarbonization of the global economy heats up. Metals like these are used for batteries in electric vehicles and consumer products like laptops, smartphones, and more.

Countries aiming to hit their Paris Climate Accord agreements will need to expand their use of renewable energy and store that energy in high-density, high-efficiency batteries. Lithium-ion batteries are typically used and require the materials miners are exploring, developing, and producing now.

Appian had initially acquired Santa Rita when the previous operator, Australia’s Mirabela Nickel, went bankrupt and needed to sell off its assets. Its Atlantic Nickel unite resumed production at the mine in 2020.

The open-pit mine is expected to last until 2028, at which point it will be transitioned into an underground mining operation to extend the life of the mine from eight to 34 years. Annual production for the open-pit mine is estimated at 16,000 tonnes nickel-equivalent per year. Sibanye has another acquisition target, Mineracao Vale Verde, which has not finished construction of the Serrote copper-gold mine in easter Brazil. That target could product an additional 20,000 tonnes of copper-equivalent every year for the next 13 years. Both acquisitions would expand the Australian company’s presence in the battery metals space and allow it to command a larger footprint in the industry.

Nickel and copper in particular have been the commodity stories of the year, with prices rising month after month in what some are calling a “copper supercycle”. While the more traditional use of nickel is for processing stainless steel into kitchen appliances and utensils, some types of the material can be processed into battery precursor materials.

Those materials then find their way into EV batteries and other types of products needs for the storage and transfer of electricity. A shortage of copper, cobalt, nickel, and other battery metals is what is driving the market higher. Miners are now scrambling to invest in the space to bring supply to meet the demand that continues to grow every quarter.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Countries from the Western Hemisphere to the Eastern hemisphere are now focusing on economic recoveries from the pandemic. That means spending is up, manufacturing is up, and industry is refiring.

But some European leaders worry about a shortage of magnesium and what kind of effects that might have on an industrial recovery from the pandemic. The European Union gets 95% of its magnesium from China, and so talks have opened between the EU and China to ensure the supply of the silvery-white metal used to make aluminum.

One of the challenges facing Chinese magnesium smelters is the electricity shortages sweeping the nation. The power cuts due to challenges generating sufficient energy from current power sources mean that China has ordered some smelters to close.

Factories have had to be powered down, and rationing is in effect in many regions as the country tries to manage its electricity supply. The talks are of particular importance since China has ordered approximately 35 out of 50 magnesium smelters to close until the end of the year. The reason was to conserve electricity, but the effect has been a supply shift that has EU leaders worried.

A Fast-Approaching Deadline

Germany’s association of metals producers, WVM, warned that the current European inventories will be exhausted by the end of November – a fast-approaching deadline. The price of magnesium has spiked in recent months as uncertainty surrounding a supply dearth creates chaos in the markets.

It is also difficult to store, and this has been a worrying point of contention as well. It begins to oxidize after three months, and global stocks could run critically low before the end of 2021 if China does not restart production soon.

Magnesium is used to make aluminum, which has become a critical metal for the industrial sector, especially for the auto industry. Aluminum alloys are used in auto parts that include gearboxes, steering columns, fuel tank covers, and seat frames. Its lightweight nature means it can be formed into the necessary shapes while maintaining strength and lightness.

As a result of aluminum used in cars, fuel efficiency has skyrocketed in the past decade. The lighter, more efficient cars are also cheaper to produce thanks to affordable aluminum. However, with the price of magnesium up from approximately $2000 per tonne at the beginning of the year to approximately $4700 per tonne now, the certainty that affordable aluminum can continue to be made is in doubt as well. Industry groups have said that the remaining stocks in Europe are selling for $10,000-$14,000 per tonne in Europe.

The issue was raised on Thursday during an EU leaders’ summit, and a dialogue was opened with China by the European Commission.

On the other side of the world, North American is having its own issues with magnesium. Canada’s Matalco Inc. produces aluminum billet. Last week it had to tell clients that magnesium availability had “dried up” and if it continued then the company may have to cut output. Additionally, it may need to ration deliveries beginning in 2022 to ensure that some are prioritized and every client gets the minimum needed.

Magnesium as a Critical Metal

Magnesium is a light metal used as an alloy for hardening aluminum used in beverage cans and light car parts. The most commonly used magnesium castings do not contain more than 90 mg of alloyed aluminum. Magnesium compounds are used for various purposes.

Magnesium castings are used in the automotive industry, aerospace components, defense applications, and consumer goods (especially laptops, tablets, and mobile phones covers). Aluminum alloys contain an average of 0.8% magnesium and are used in a wide variety of industries with packaging (35% of magnesium used in aluminum alloys), transport (25%), and construction (21%) being the three most important.

China has a quasi-monopoly on the production of magnesium, which is a key component of the production of aluminum alloys. About 95% of the world’s magnesium production comes from China, most of it from the city of Yulin in Shaanxi Province. Worldwide production of magnesite (Sitmate) is 596 Mt, of which China is the largest producer.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

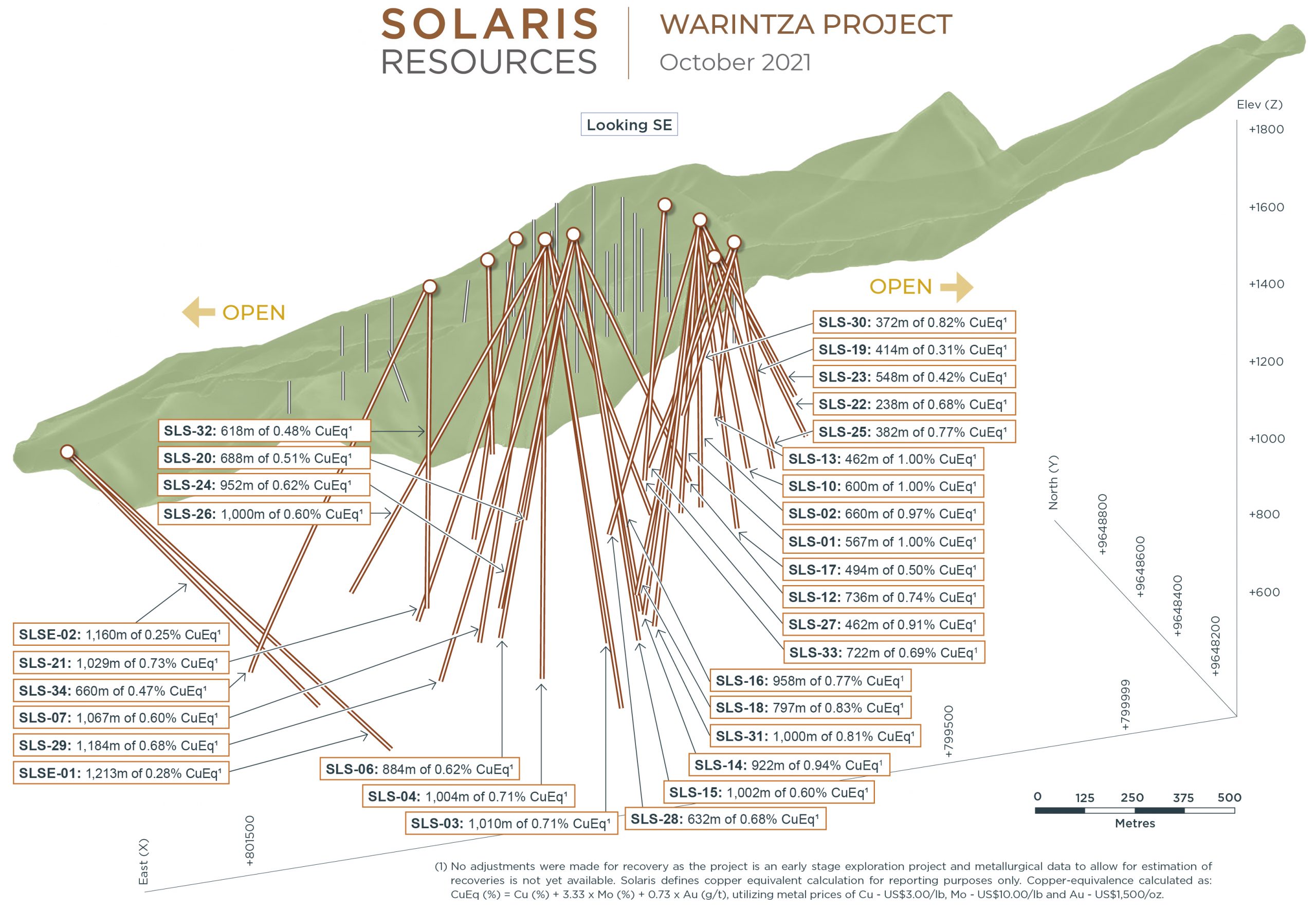

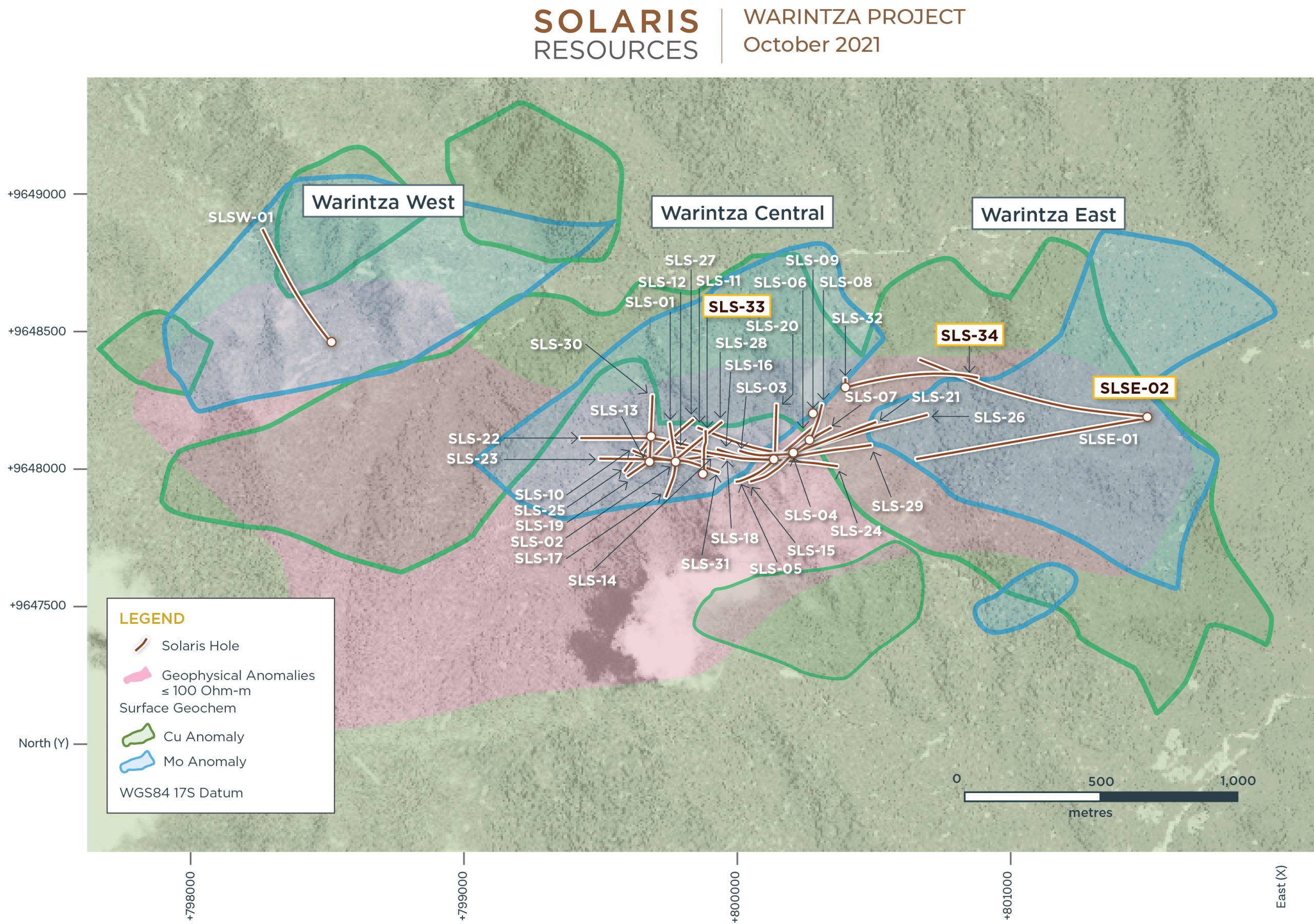

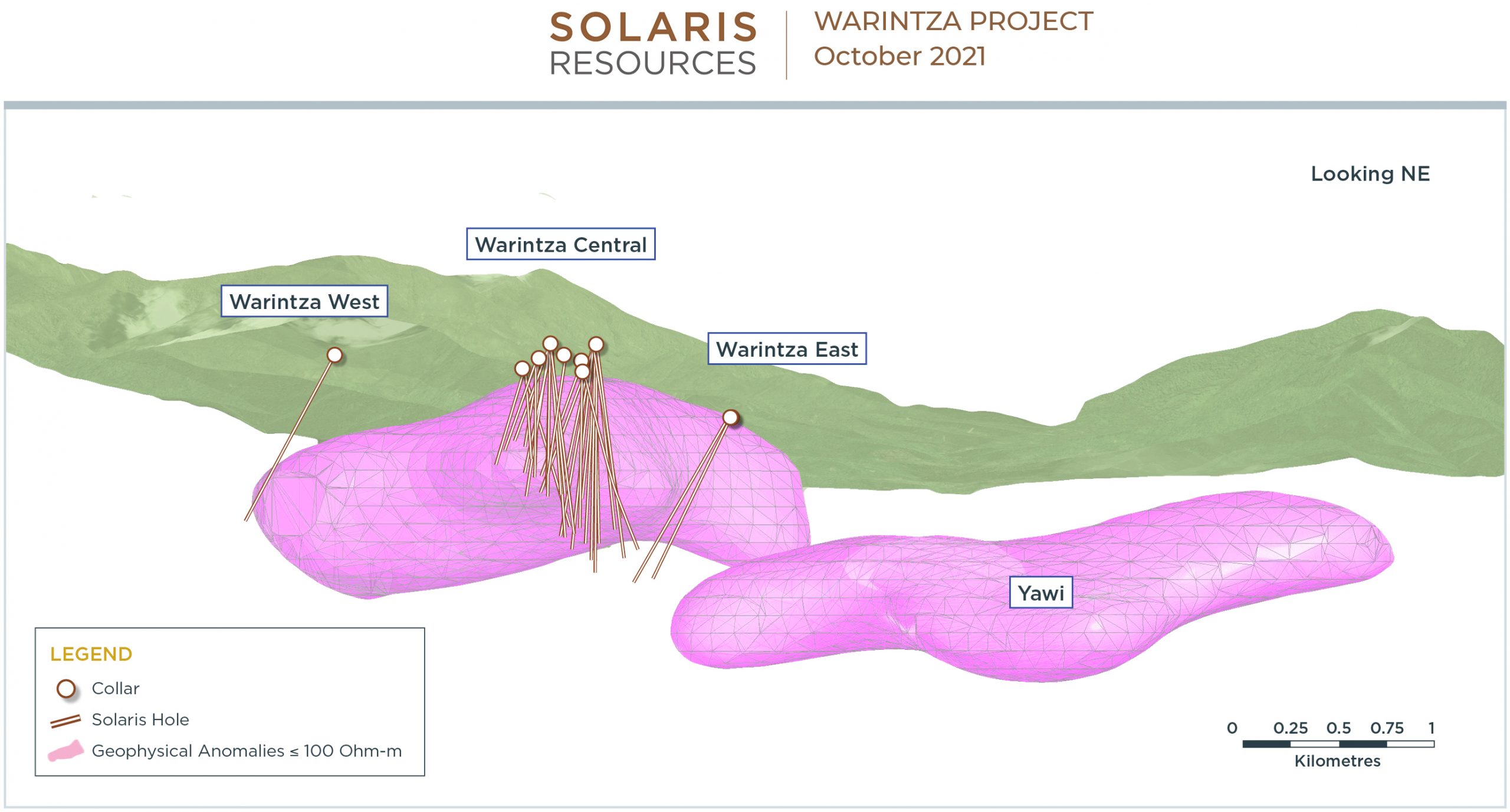

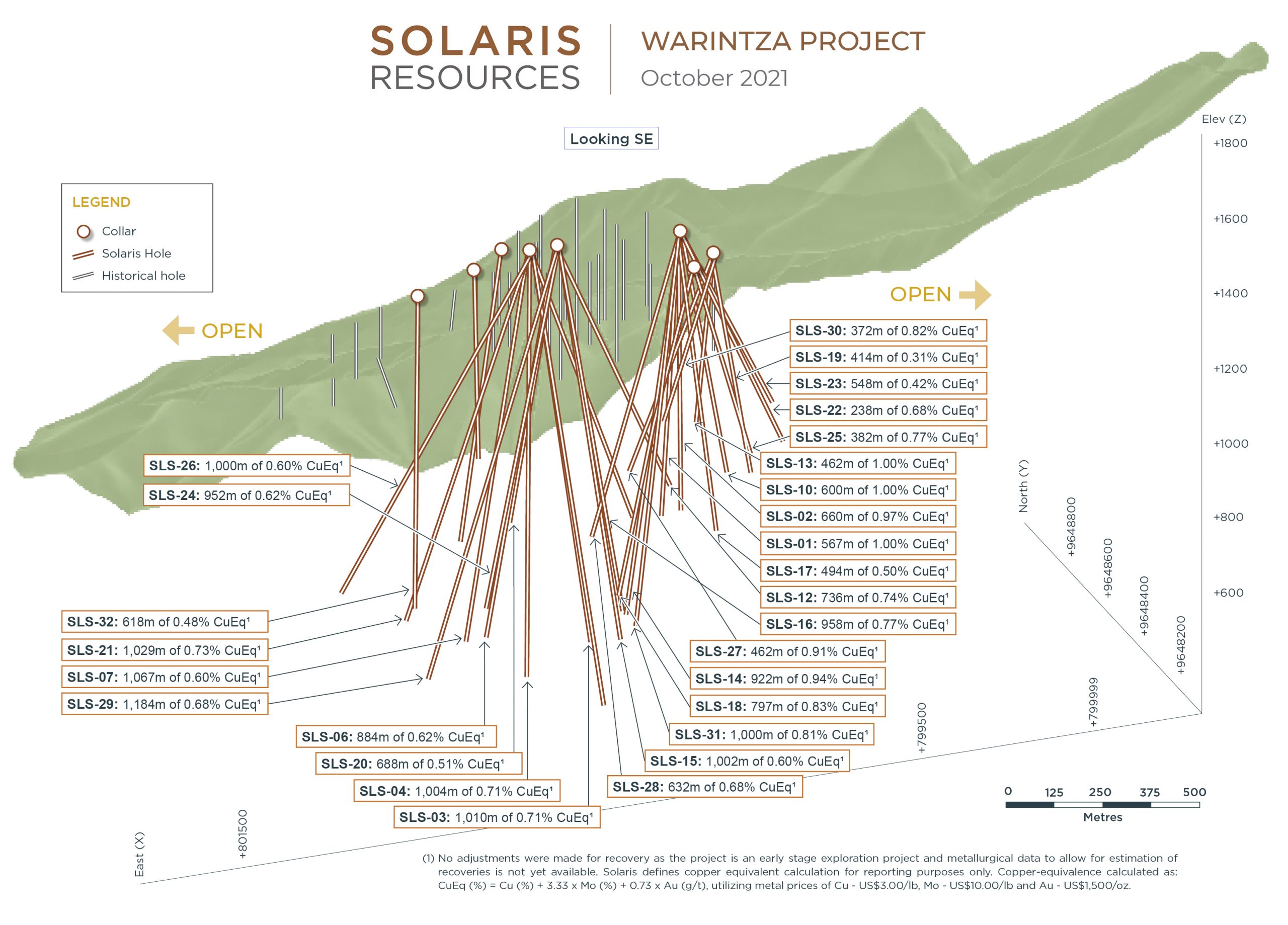

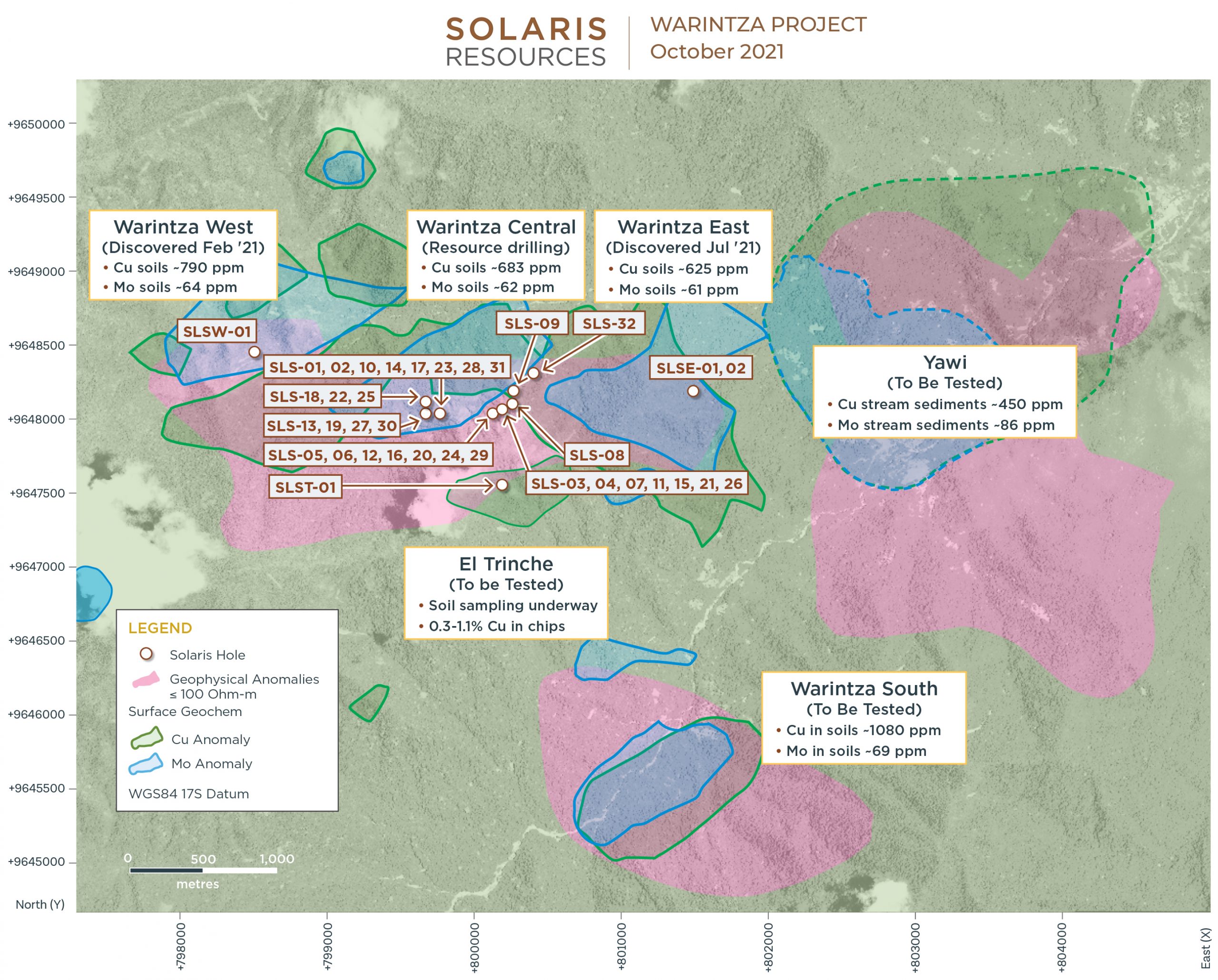

Solaris Resources (TSX:SLS) has reported new assay results from ongoing resource growth and discovery drilling at its flagship Warintza Project in Ecuador this morning. Warintza has now been extended, and now overlaps the Warintza East discovery.

Vice President of Exploration for Solaris Resource commented in a press release: “We are very proud to continue the great work of the late David Lowell with our first two holes confirming Warintza East as the third major copper porphyry discovery within the 7km x 5km Warintza porphyry cluster. Our drilling fleet has now been fully reoriented to pursue an aggressive growth strategy via step-out and extensional drilling as we prepare to test our next targets for further discoveries.”

Highlights are listed below, with corresponding images in Figures 1-3 and detailed results in Tables 1-2. A dynamic 3D model is available on the Company’s website and will be updated to incorporate the most recent results.

Highlights

- Eastern extension drilling has increased the strike length of Warintza Central to 1,350m where it now overlaps the western limits of Warintza East

- SLS-33 was drilled from Warintza Central into a partially open volume to the north, returning 722m of 0.69% CuEq¹, including 426m of 0.85% CuEq¹ from 46m depth, infilling and extending mineralization to the north in this area

- SLS-34 was collared at the northeastern limit of Warintza Central and drilled east into an entirely open volume, returning 660m of 0.47% CuEq¹, including 242m of 0.67% CuEq¹ from 52m depth, significantly extending mineralization to the east where it now partially overlaps Warintza East

- SLSE-02, the second hole at Warintza East, was collared approximately 1,300m east of Warintza Central and drilled northwest toward SLS-34, returning 320m of 0.48% CuEq¹ from surface within a broader interval of 1,160m assaying 0.25% CuEq¹, partially overlapping SLS-34

- SLSE-01 (previously reported September 27, 2021) was collared from the same platform as

SLSE-02 but drilled to the southwest, returning 396m of 0.42% CuEq¹ from surface within a broader interval of 1,213m assaying 0.28% CuEq¹ - Warintza East is the third major copper porphyry discovery within the Warintza cluster; each of the first two holes have returned long intervals of mineralization with the highest grades starting at or near surface reflecting the vertical zonation in the system

Figure 1 – Long Section of Warintza Central and Warintza East Drilling Looking Southeast

Figure 2 – Plan View of Warintza Drilling Released to Date

Figure 3 – Long Section of 3D Geophysics Looking Northeast

Note to Figure 3: Figure looks northeast and depicts high-conductivity geophysical anomaly (defined at 100 ohm-m) generated from 3D inversion of electromagnetic data, encompassing from left to right Warintza West, Central, East and the Yawi target (Warintza South lies off image to south).

Table 1 – Assay Results

| Hole ID | Date Reported | From (m) | To (m) | Interval (m) | Cu (%) | Mo (%) | Au (g/t) | CuEq¹ (%) | ||

| SLS-34 | Oct 25, 2021 | 52 | 712 | 660 | 0.36 | 0.02 | 0.06 | 0.47 | ||

| Including | 52 | 294 | 242 | 0.51 | 0.03 | 0.08 | 0.67 | |||

| SLS-33 | 40 | 762 | 722 | 0.55 | 0.03 | 0.05 | 0.69 | |||

| Including | 46 | 472 | 426 | 0.71 | 0.03 | 0.06 | 0.85 | |||

| SLSE-02 | 0 | 1160 | 1160 | 0.20 | 0.01 | 0.04 | 0.25 | |||

| Including | 0 | 320 | 320 | 0.39 | 0.02 | 0.04 | 0.48 | |||

| SLS-32 | Oct 12, 2021 | 0 | 618 | 618 | 0.38 | 0.02 | 0.05 | 0.48 | ||

| SLS-31 | 8 | 1008 | 1000 | 0.68 | 0.02 | 0.07 | 0.81 | |||

| SLS-30 | 2 | 374 | 372 | 0.57 | 0.06 | 0.06 | 0.82 | |||

| SLSE-01 | Sep 27, 2021 | 0 | 1213 | 1213 | 0.21 | 0.01 | 0.03 | 0.28 | ||

| SLS-29 | Sep 7, 2021 | 6 | 1190 | 1184 | 0.58 | 0.02 | 0.05 | 0.68 | ||

| SLS-28 | 6 | 638 | 632 | 0.51 | 0.04 | 0.06 | 0.68 | |||

| SLS-27 | 22 | 484 | 462 | 0.70 | 0.04 | 0.08 | 0.91 | |||

| SLS-26 | July 7, 2021 | 2 | 1002 | 1000 | 0.51 | 0.02 | 0.04 | 0.60 | ||

| SLS-25 | 62 | 444 | 382 | 0.62 | 0.03 | 0.08 | 0.77 | |||

| SLS-24 | 10 | 962 | 952 | 0.53 | 0.02 | 0.04 | 0.62 | |||

| SLS-19 | 6 | 420 | 414 | 0.21 | 0.01 | 0.06 | 0.31 | |||

| SLS-23 | May 26, 2021 | 10 | 558 | 548 | 0.31 | 0.02 | 0.06 | 0.42 | ||

| SLS-22 | 86 | 324 | 238 | 0.52 | 0.03 | 0.06 | 0.68 | |||

| SLS-21 | 2 | 1031 | 1029 | 0.63 | 0.02 | 0.04 | 0.73 | |||

| SLS-20 | April 19, 2021 | 18 | 706 | 688 | 0.35 | 0.04 | 0.05 | 0.51 | ||

| SLS-18 | 78 | 875 | 797 | 0.62 | 0.05 | 0.06 | 0.83 | |||

| SLS-17 | 12 | 506 | 494 | 0.39 | 0.02 | 0.06 | 0.50 | |||

| SLS-16 | Mar 22, 2021 | 20 | 978 | 958 | 0.63 | 0.03 | 0.06 | 0.77 | ||

| SLS-15 | 2 | 1231 | 1229 | 0.48 | 0.01 | 0.04 | 0.56 | |||

| SLS-14 | 0 | 922 | 922 | 0.79 | 0.03 | 0.08 | 0.94 | |||

| SLS-13 | Feb 22, 2021 | 6 | 468 | 462 | 0.80 | 0.04 | 0.09 | 1.00 | ||

| SLS-12 | 22 | 758 | 736 | 0.59 | 0.03 | 0.07 | 0.74 | |||

| SLS-11 | 6 | 694 | 688 | 0.39 | 0.04 | 0.05 | 0.57 | |||

| SLS-10 | 2 | 602 | 600 | 0.83 | 0.02 | 0.12 | 1.00 | |||

| SLS-09 | 122 | 220 | 98 | 0.60 | 0.02 | 0.04 | 0.71 | |||

| SLS-08 | Jan 14, 2021 | 134 | 588 | 454 | 0.51 | 0.03 | 0.03 | 0.62 | ||

| SLS-07 | 0 | 1067 | 1067 | 0.49 | 0.02 | 0.04 | 0.60 | |||

| SLS-06 | Nov 23, 2020 | 8 | 892 | 884 | 0.50 | 0.03 | 0.04 | 0.62 | ||

| SLS-05 | 18 | 936 | 918 | 0.43 | 0.01 | 0.04 | 0.50 | |||

| SLS-04 | 0 | 1004 | 1004 | 0.59 | 0.03 | 0.05 | 0.71 | |||

| SLS-03 | Sep 28, 2020 | 4 | 1014 | 1010 | 0.59 | 0.02 | 0.10 | 0.71 | ||

| SLS-02 | 0 | 660 | 660 | 0.79 | 0.03 | 0.10 | 0.97 | |||

| SLS-01 | Aug 10, 2020 | 1 | 568 | 567 | 0.80 | 0.04 | 0.10 | 1.00 | ||

| Notes to table: True widths cannot be determined at this time. | ||||||||||

Table 2 – Collar Location

| Hole ID | Easting | Northing | Elevation (m) | Depth (m) | Azimuth (degrees) | Dip (degrees) |

| SLS-34 | 800383 | 9648303 | 1412 | 1057 | 78 | -60 |

| SLS-33 | 799873 | 9648008 | 1632 | 764 | 0 | -80 |

| SLSE-02 | 801485 | 9648192 | 1170 | 1191 | 275 | -50 |

| Notes to table: The coordinates are in WGS84 17S Datum. | ||||||

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Freeport McMoran Inc. (NYSE:FCX) produced less copper than expected from its mines in the Americas in the last quarter, heightening concerns about a tight global market where prices have soared to record levels. Freeport produced 987 million pounds of the metal in the third quarter, the company said in a statement on Thursday, with production falling below Bloomberg analysts’ average estimate of 1 billion pounds. The slowdown was driven by lower-than-expected output at its mines in South America.

The stock has more than doubled in the last year, becoming one of the best performers among copper suppliers tracked by Bloomberg Intelligence. The production shortage at Freeport comes after the company posted a quarterly profit that beat analyst estimates as higher copper prices helped lift sales and operating profit to levels last seen in the same quarter a year ago. Adjusted earnings of 89 cents per share topped the average estimate of 82 cents. Freeport estimates that annual copper sales are 3.8 billion pounds this year, following sales of 1.03 billion pounds in July and September. Net cash costs for Freeport were $1.24 per pound in the third quarter, well above the average analyst estimate of $1.30 per pound. Rising costs are seen as one of the few headwinds to earnings growth for the copper mining giant.

Freeport’s results will be particularly interesting for traders navigating the wild swings in copper prices, with available stocks on the London Metal Exchange at their lowest level since 1974. The market had been banking on Freeport to ramp up underground production. The company said underground progress at its flagship Grasberg mine was progressing on schedule. While companies are moving quickly to bring more copper to market, growth in demand is seen to be outstripping supply over the next decade, with new projects needed to help balance the dynamic.

Global shipping bottlenecks and energy bottlenecks in China and Europe have clouded the demand outlook for the coming year. But the immediate outlook for copper, supported by lower inventories and a shift to low-carbon energy sources, is rosier in the longer term. Efforts to save electricity in China and to limit emissions have been a double-edged sword for mining companies with higher smelting fees wiping out some of the windfall.

The China Conundrum

Coal provides much of the country’s electricity, but a combination of factors has recently led to electricity shortages. China’s coal production in 2021 will be unable to keep pace with rising electricity demand due to tighter safety regulations and an additional focus on environmental issues in Beijing, tight global coal markets, rising prices, and other factors, including weather delays. China is working out of a coal-fired power crisis that has sent shockwaves through its economy, but efforts to move to a low-carbon future are bringing additional risks to the country’s supply-demand balance. The shift has been too great, too fast, and the country is having trouble balancing its power needs with generating sufficient electricity using cleaner fuels.

Copper is one of the desperately needed metals for that clean energy transition. It is used for energy storage which is critical to use with renewables that are not able to generate electricity consistently. China is and will be one of the biggest copper consumers in the coming years, and will contribute to how fast demand will be driven.

Solar power can only be generated for a certain period, and when the night sets in, countries will need to draw power from the excess generated and stored in batteries. The lithium-ion batteries used to store large amounts of power require copper to be manufactured, and copper is the primary material for electricity transportation as well. To get the electricity from the generation site to the storage site, copper wiring will be used. More will be necessary to deliver that electricity to homes and offices and the factories that need to keep running almost constantly.

As China tries to shift to renewable energy, a severe drought has hit hydropower, especially in central Yunnan province. According to the National Development and Reform Commission, the water production in July and August fell by more than 4% year-on-year. Freeport’s production miss is significant because the producer accounts for so much of the global production, but the copper market remains strong. If anything, the lower production may only contribute to the supply crunch and rising copper prices.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

According to a new report from S&P Global Market Intelligence, the annual global exploration budget will increase by 5% to 15% per year starting in 2022.

The 2021 global annual exploration budget shows that the exploration sector has rebounded from the recession caused by the COVID-19 pandemic. The prediction of a market study showed according to their data that the aggregate annual budget to annual global exploration has increased by 35% year over year. Compared to the $8.3 billion budget in 2020, this year it increased to $11.2 billion.

The large companies that continue to dominate the sector account for half of the global exploration budget with a total of $5.6 billion. However small company budgets have increased their planned allocations by 62% annually to a total of $4.1 billion.

The increase in the value of base metals such as gold which dominate the exploration target, and increased financing activity are the main drivers of the budget recovery in 2021.

“As we move into the final quarter of this year, metals prices and financings remain strong, and the risk of further pandemic-related closures has diminished,” Kevin Murphy of S&P Global Market Intelligence said in the report.

In terms of location, the report shows that Canada has brought in a large share of the global budget with an $800.5 million increase YoY to $2.1 billion, reaching its highest level since 2012. Conversely, Africa showed an underperformance with allocations.

Canada’s Mining Strength

Mining in Canada and gold mining, in particular, has long played a pivotal role in building and solidifying Canada’s economy today. The mining infrastructure that was built alongside cities in the 19th century has since grown to generate exports worth $21.6 billion for Canada by 2020.

The country’s favourable geological and technological characteristics enable and facilitate gold production. The discovery, mining, and production of gold have laid the foundation for many of Canada’s towns, cities, and regions.

Today, Canada has the geology, technology, political and regulatory stability to be a premier gold mining jurisdiction. Because of this, mining companies have great opportunities for gold exploration, development, and production in Canada.

Technology and Investment

Canada is the number one country in equity financing raised for mining and mineral exploration. Forty-seven percent of the world’s public mining companies are listed on the TSX and TSXV.

Mining companies raised $44 billion over the past five years on the TSX and TSXV, accounting for 52% of all global mining financing over the past five years.

In addition, the Canadian government also supports mining innovation. Investment funds such as Canada’s $155 million Clean Growth Canada program invest in clean technologies for more sustainable mining.

It’s no secret that the small country of just over 30 million pulls far above its weight when it comes to the mining industry:

- The Canadian mining industry, directly and indirectly, employs 719,000 people across the country. This accounts for 1 out of every 26 jobs in Canada.

- The Canadian mining industry has the highest average wage of all industrial sectors.

- The mining industry is the largest private-sector employer of Indigenous Canadians.

- Canadian gold mines produce more revenue than all other metal mines combined and account for more than half of 2019 exploration budgets.

- As the world’s fifth-largest gold producer, Canadian gold mining is a key part of international production.

- More than 75% of Canadian gold comes from Ontario and Québec.

Gold mining has played an essential role in Canada’s domestic and international economy and will continue to do so in the future.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Three Valley Copper (TSXV:TVC) is reviewing its development strategy, business plan, market valuation, and capital structure in a bid to deliver enhanced shareholder value and maximize production and cash flows.

The company’s 91.1% owned Minera Tres Valles property near Salamanca, Region de Coquimbo, Chile will be the focus of the evaluation, during which the company will consider mergers, strategic partnerships, acquisitions or disposition, restructuring or refinancing of its long-term debt, and any other options available to Three Valley to maximize shareholder value.

To complete the review, PI Financial has been retained. While the process does not guarantee a transaction or investment, the company looks to be aiming for the best strategies for maximizing results at its Papomono Masivo deposit. Papomono Masivo (PPM) has become a priority for Three Valley and the company is aiming to hit an increased production profile at Minera Tres Valles by ramping up production there.

Although the exploration program will be temporarily scaled back during the strategic review process, the review may reveal optimal paths forward for its exploration efforts to maximize drill programs. The review process will evaluate any and all alternative avenues for maximizing value, and the exploration program is a key pillar of shareholder value at Three Valley Copper.

Accelerating Investment, Revising 2022 Outlook and Guidance

PPM is a critical catalyst for Minera Tres Valles, and the successful development of this deposit continues to be a priority. For this reason, management has reviewed the preliminary development and mining plans at PPM and has decided to increase capital expenditures in 2022 instead of deferring some of those into the latter years of the mine life. This decision was made after a thorough review and concluded with a forecast from Three Valley that additional capital of approximately US$10 million in 2022 will be needed to achieve the recently announced production guidance. This decision will keep the program on track and keep the project on track for its timeline.

Don Gabriel

The Don Gabriel mine has experienced a lower head grade than initially forecasted, and as such, Three Valley Copper put a number of remedial measures in place in the third quarter. The delay between the implementation of those measures and the improved results may take a number of months to appear, due to the workflow of a heap leach operation. Initially, Three Valley had anticipated that copper production at Don Gabriel along with the recent drawdown of the remaining US$6 million of senior debt in September would support those operations and the ongoing PPM project. With production lower than expected and the Don Gabriel mine being the company’s primary source of ore to produce copper cathodes for 2021, Three Valley’s tight liquidity position has been amplified. Several factors are contributing to the liquidity crunch, including the company’s mostly fixed operating cost base, increased capital demands due to the PPM deposit 2022 development, and scheduled debt repayments due to begin March 2022.

A Path Forward

As such, Three Valley has announced that it does not expect to generate sufficient cash from operations to fully fund 2021 operations, planned investment activities, plus debt service obligations in March 2022 and the increased sustaining capital expenditures next year for PPM. To secure funding, Three Valley has initiated discussions with senior secured lenders and the company’s offtake provider.

This may allow the company to make changes to the existing loan agreement, inter alia, bridge loan financing, waivers of operating covenants, deferrals of or renegotiation of repayment terms, and/or renegotiation of the fixed-price portion of the offtake agreement. In the event of a successful strategic review and/or negotiations with the company’s senior secured lenders, Three Valley Copper will have the liquidity necessary to execute the planned production expansion at Minera Tres Valles.

Three Valley Copper (TSXV:TVC) stock was up 6% to CA$0.53 yesterday.

The Company’s revised preliminary operating outlook1 for 2022 at MTV is as follows:

| Revised | Original | ||

| Operating information | Year Ended | Year Ended | |

| Copper (MTV Operations) | Dec. 31, 2022 | Dec. 31, 2022 | |

| Cu Production (tonnes) | 8,000 – 10,000 | 8,000 – 10,000 | |

| Cu Production (pounds) | 17.6M – 22.0M | 17.6M – 22.0M | |

| Cash Cost per Pound Produced2 | $2.75 – $3.25 | $2.75 – $3.25 | |

| Capital Expenditures3 ($ millions) | $15 – $20 | $5 – $10 |

In the absence of a successful strategic review event and/or renegotiations with its senior secured lenders which will require financial liquidity solutions for MTV before the end of 2021, additional material changes to the Company’s revised preliminary outlook above will then be required.

- Preliminary guidance is based on certain estimates and assumptions, including but not limited to, mineral reserve estimates, grade and continuity of interpreted geological formations, metallurgical performance and foreign exchange rates. Please refer to the amended and restated technical report prepared by Wood Independent Mining Consultants, Inc., in respect of the Minera Tres Valles Copper Project (the “Technical Report”) dated May 27, 2021 and to the Company’s SEDAR filings for complete risk factors related to the Company and MTV.

- Cash Cost is a non-IFRS measure – Cash costs of production include all costs absorbed into inventory less non-cash items such as depreciation. Cash costs per pound produced are calculated by dividing the aggregate of the applicable costs by copper pounds produced.

- Planned capital expenditures (“CAPEX”) for 2022 are focused primarily on open pit expansion, plant CAPEX and sustaining CAPEX of PPM for the inclined block-caving mining project. It is expected that by early 2022, the underground operation at PPM will begin production and the resulting production growth is expected to lower per unit operating costs in 2022 and 2023 as the results of this CAPEX are realized.

Source: Three Valley Copper

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Lithium production is full-steam ahead this year, and companies like Rock Tech Lithium (TSXV:RCK) want to dominate. The company’s mission from the start has been to source raw material in Canada at its 100% owned Georgia Lake spodumene project in Ontario, Canada.

The company is developing the project while advancing plans in Germany for a battery-metals plant near the sites of key suppliers and customers. Those customers include Elon Musk’s TEsla Inc. and BASF SE.

This strategic location was also chosen due to its proximity to Gruenhide, which is the site of Tesla’s plant. The electric vehicle automaker is planning to start producing vehicles at the plant this year, but has not received approval for the project yet. The plant will be built in Brandenburg, a German state outside Berlin, and the same state that Tesla is completing its vehicle factory – its first in Europe.

To fund the battery-metals plants, Rock Tech may be preparing a Nasdaq listing. The company requires approximately $545 million to finance the new project and may require an equity raise next year.

Rock Tech is backed by billionaire venture capitalist Peter Thiel. The German-American entrepreneur believes that Germany will have a leading role to play as Europe and the US transition to electric vehicles in the coming years. The company is betting on hundreds of thousands of cars being put into production.

The plant could begin operating as soon as 2024. This will mark Europe’s first lithium converter, with a production capacity of 24,000 tonnes per year. That means the plant would be able to supply lithium-ion batteries for approximately 500,000 cars according to Rock Tech.

Rock Tech Lithium is already listed on the Toronto and Frankfurt exchanges, and the new listing would broaden its investor accessibility in the U.S. It could provide the financing needed for the project and more as it plans to expand.

The company’s mission has always focused on lithium. While it is developing a mining project in Canada, Rock Tech (TSXV:RCK) is positioning itself as a converted-lithium processor and supplier. This would make it a partner of the electric vehicle industry as well as the mining industry. By controlling extraction and processing, the company can keep costs lower and profits higher.

Rock Tech’s investor list is also impressive, with Peter Thiel holding a significant position, Christian Angermayer and hedge fund billionaire Alan Howard. The company also has retired BMW AG and Deutsche Bank finance head Stefan Krause in a top management position as CFO.

Li-Ion Takes Centre Stage

Lithium-ion batteries have a higher energy density than lead-acid batteries and nickel-metal hydroxide batteries, and it is possible to produce battery sizes smaller than others while maintaining the storage capacity. Li-ion battery cells contain electrodes of metal alloys and carbon-based materials such as graphite and their electrolyte contains lithium ions. Nissan’s lithium-ion battery technology uses materials that enable a higher density of lithium-ion.

Due to their high energy density, lithium batteries weigh less than a NIMH battery of the same capacity. Cheaper and safer battery models use lithium-nickel, manganese and cobalt oxide batteries that have the potential to charge a car in just ten minutes on a charge of up to 250 miles. These batteries are lighter and last much longer than previous battery technologies.

Different battery types differ in terms of the ion type, the electrode material, and the associated electrolyte. The individual batteries consist of a metal cathode of lithium mixed with other elements such as nickel, cobalt, manganese, iron, and graphite, an anode separator, and a liquid electrolyte made of lithium salts. Certain elements, including carbon, graphite metal oxide and lithium salts, form the positive and negative electrodes that connect to the electrolyte to generate the electric current that gets the battery going and powers your vehicle.

To power a car, thousands of cells are bundled into a series of modules that are wired to the battery pack and enclosed in a protective metal housing.

Batteries in electric vehicles are characterised by their high power-to-weight ratio and specific energy density (energy density). Small and lighter batteries are therefore desirable because they reduce the weight of the vehicle and improve its performance. Batteries can weigh thousands of pounds, with the F150 Lightning battery alone weighing more than 2,000 pounds. Compared to liquid fuels, most current battery technologies have lower specific energy, which affects the maximum electric range of a vehicle.

These features allow solid-state batteries to be lighter, have a higher energy density, and offer more range when recharged. The most common types of batteries for modern electric vehicles are lithium-ion and lithium-polymer, because they have a higher energy density compared to their weight. Other types of rechargeable batteries used in electric vehicles include lead-acid, flooded, low-cyclic, valve-controlled lead-acid, nickel-cadmium, nickel hydride, zinc-air, sodium-nickel chloride, and zebra batteries. However, companies like Rock Tech and Tesla are betting on a lithium-ion future for EVs.

Beyond Cars

Lithium-ion batteries are used in most portable consumer electronics, such as mobile phones and laptops, because they have high energy per mass unit compared to other electrical storage devices. They have a high power-weight ratio, high energy efficiency, good high-temperature performance, and low self-discharge. A major advantage of using nickel batteries is that they contribute to high energy density, greater storage capacity, and lower costs.

The market for lithium will continue to expand as more elements of the economy require energy storage and lithium-ion batteries. Rock Tech’s mission is primarily to supply the electric vehicle industry but has an open lane to supply other industries and sectors in the future.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

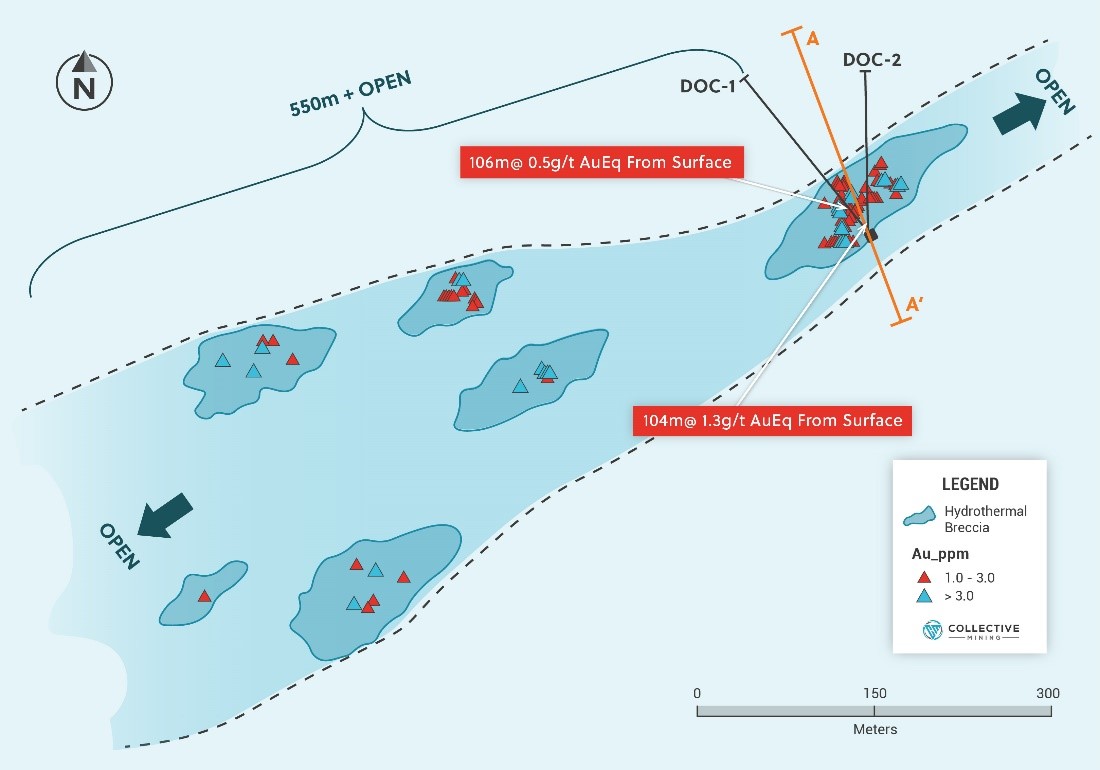

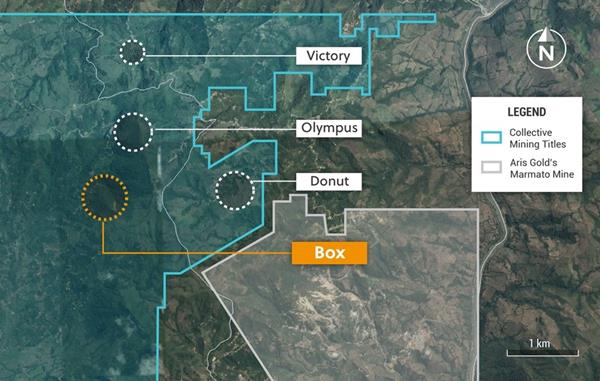

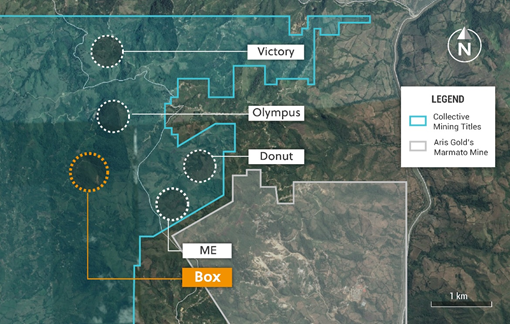

As the first of five outcropping and grassroot targets generated by Collective Mining (TSXV:CNL) at its Guayables project in Colombia, Donut has been the first to yield discoveries from the drill program. Collective Mining has announced that a significant discovery has been made at the Donut target.

This is the first drill hole at a grassroot target at the project, and it already has a new brand discovery. The company is aiming to increase its drill program from 7,500 metres to 10,000 and speed up plans to begin drilling the Olympus target. Collective will aim to begin drilling at the Olympus target in November 2021 instead of Q1 2022.

Currently, there is one diamond drill rig testing Donut. To accelerate the program, a second rig is expected to arrive at the target shortly and begin drilling the Box target before the end of the month.

Ari Sussman, Executive Chairman of Collective Mining, commented in a press release, “As a result of our team’s diligence and geological modelling prowess, we have accomplished the exceedingly arduous task of making a brand-new discovery on the very first drill hole into a grassroot target at the Guayabales project. We look forward to announcing additional drill hole assay results in the near term. As a result of this early success, we are increasing our initial drill program from 7,500 to 10,000 metres and are also accelerating our plans to drill the Olympus target to November 2021 from Q1, 2022.”

Highlights (Table 1 and Figures 1 to 4)

- Broad and continuous gold (“Au”) and silver (“Ag”) mineralization has been intersected from surface in the first two diamond drill holes at the Donut target as follows:

- 104 metres at 1.3 g/t gold equivalent from surface including 18 metres at 4.7 g/t gold equivalent from 16 metre depth (DOC-2);

- 106 metres at 0.5 g/t gold equivalent from surface (DOC-1).

- 104 metres at 1.3 g/t gold equivalent from surface including 18 metres at 4.7 g/t gold equivalent from 16 metre depth (DOC-2);

- Donut is located at the NW end of a SW trending zone hosting clusters of mineralized breccia bodies which can be traced along strike to the SW for 550 metres and remain open for further expansion.

- Drilling continues at Donut with holes DOC-3 through DOC-5 now complete and DOC-6 currently underway.

- DOC-3 and DOC-4 were drilled to the southwest and deeper within the mineralized system. Preliminary logging of both holes highlights continuity of the mineralized breccia and polymetallic vein system overprint with longer intercepts of mineralized breccia than was intersected in DOC-1 and DOC-2.

- DOC-05, which was drilled to the southeast, intersected a narrower interval of mineralized breccia before passing through a fault. Upon exiting the fault at approximately 80 metres down-hole, porphyry style alteration was encountered until the end of the hole at 327 metres.

- Assay results for DOC-3 to DOC-5 are anticipated in the near term and will be reported shortly thereafter.

- Due to the positive start to the drilling program, the Company is expanding its maiden drill program from 7,500 to 10,000 metres.

Table 1: Initial Diamond Drilling Results at the Donut Target

| Hole ID | From (m) | To (m) | Interval (m) | Au (g/t) | Ag (g/t) | AuEq* (g/t) |

| DOC-1 | 0.0 | 106.0 | 106 | 0.4 | 7 | 0.5 |

| Incl. | 55.0 | 70.2 | 15 | 0.6 | 23 | 0.9 |

| And | 89.7 | 106.0 | 16 | 0.6 | 5 | 0.7 |

| DOC-2 | 0.0 | 104.0 | 104 | 1.2 | 12 | 1.3 |

| Incl. | 16.0 | 58.1 | 42 | 2.5 | 8 | 2.4 |

| Incl. | 16.0 | 34.0 | 18 | 4.8 | 10 | 4.7 |

| Incl. | 20.0 | 22.0 | 2 | 33.3 | 41 | 32.2 |

Gold equivalent calculated based on a long-term 65:1 silver to gold ratio average and metallurgical recovery rate assumption of 95% for gold and 90% for silver based on similar projects globally. Readers should be cautioned that the Company has not yet performed any independent metallurgical test work on the deposit and as a result, recovery rates could ultimately be superior or inferior to the estimates used in the calculation.

Geological Details of the Donut Target

Underground mapping of artisanal workings covering a 100 metre x 100 metre area has exposed mineralized and oxidized porphyritic diorite in contact with hydrothermal breccia. The porphyry and the breccia display evidence of stockwork and sheeted, quartz-sulphide veinlets as well as later overprinting polymetallic veins. A total of one hundred and seventy-six two-metre channel samples were taken underground and returned an average of 2.1 g/t gold and 21.2 g/t silver (based on applying a statistical top-cut to three high-grade samples). Collective’s initial drilling has been focused on drill testing this mineralization at depth and in an array of different directions.

Review of the diamond drill core highlights a hydrothermal breccia with a sulphide matrix and hosting clasts of mineralized porphyry containing A and B veins and disseminated pyrite, chalcopyrite, and molybdenum. Breccia mineralization is associated with strong phyllic alteration (principally illite-sericite with some chlorite and epidote) whereas the diorite bodies intersected in the cores show potassic alteration (Biotite and K feldspar). The overprinting polymetallic veinlets contain quartz and pyrite associated with high grade gold values, sphalerite and occasional galena. Borehole DOC-5, drilled to the southeast, intersected mineralized breccia in a faulted contact with a potassic altered, porphyry body hosting disseminated chalcopyrite and molybdenum plus A and B porphyry veinlets.

In summary, mineralization at Donut is polyphase related to porphyry, hydrothermal breccia, and later polymetallic veining. At least three mineralization events are seen in the drill core. The presence of porphyry clasts and the mineralized porphyry intrusive intersected in DOC-5 highlight the potential for a large, mineralized porphyry body in the near vicinity.

Figure 1: Plan View of the Guayabales Project and the Donut Target is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/f9ee816f-ca94-4b43-8c82-fc466f2f7985

Figure 2: Plan View of the Donut Target Area (Gold Values (g/t)) is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/fb6daab3-fe64-40c2-9398-ec694f5d114b

Figure 3: Cross Section of Donut Drilling is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/1915efc3-8c65-47ba-ab07-63ef2de59cde

Figure 4: Core Photos (i) is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/0678467b-d64e-47a2-b32d-84d790c0e6be

Figure 4: Core Photos (ii) is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/3196635a-7415-45c8-ab0e-88f06f5449bf

Figure 4: Core Photos (iii) is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/26acf326-8613-4e81-9302-a210c364b1c7

Figure 4: Core Photos (iv) is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/e9f5f859-4b4f-4ba1-96d8-8c5694482b5d

Source: Collective Mining

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Chile holds the largest known lithium reserves, and miners have been clamoring for tenders consistently since the first discoveries and mapping were conducted. Now, the Latin American nation is opening a tender for the exploration and production of 400,000 tonnes of lithium.

This move by the Chilean government is an effort to reclaim market share from competitors like the Democratic Republic of Congo, Australia, and China, and fill some of the growing demand for lithium due to its use in electric vehicles and technology. Up until 2018, Chile was the world’s top lithium producer.

However, Australia displaced Chile, and China is fast approaching the point where it will be the second-largest lithium producer with a projected timeline of the end of this decade. For example, China’s Ganfeng Lithium is a majority shareholder in Argentina’s plant Cauchari-Olaroz. Production is scheduled to begin in mid-2022 and become one of the world’s leading lithium production mines.

Chile still produced approximately 29% of the world supply. No small feat for the smaller nation competing on the international stage. The government has ambitions set much higher though, and it looks to double production to 250,000 tonnes of lithium carbonate equivalent (LCE) by 2025.

Chile’s mining ministry projects show that global demand for lithium could quadruple by 2030 – a total of 1.8 million tonnes. Even if Chile doubles it production and new lithium projects come online, available supply is projected to be 1.5 tonnes, a significant deficit. This will likely drive prices higher and create a further wave of new projects and new tenders becoming available.

The tender is being prepared with rules that will make it available to local firms and foreign firms alike. The tender will split the 400,000 tonnes into five quotas of 80,000 tonnes each. Winning permits will mean companies have seven years to explore and develop projects. This is extendable by two years if needed. Following development, the tender will allow permit 20 years of production, according to the mining ministry.

Right now, there are two major lithium miners that dominate the market: Albemarle (NYSE:ALB) and SQM (NYSE:SQM). Their primary and most profitable location for extraction is in Chile’s Atacama Desert. The desert is one of the driest places on earth and creates ideal conditions for lithium extraction. The extraction process requires pumping brine from beneath surface and then concentrating the brine using evaporation pools.

They pump the brine from the vast salt plain of Salar de Atacama in Chile to 80 km2 basins. The salt flats and surrounding mountains have allowed rainfall to accumulate over millions of years, forming a salty brine that has become trapped in underground reservoirs. Lithium extraction in Chile is currently taking place in the Atacama Plain, but the Maricunga Plain is believed to hold the largest lithium reserves in the country.

The upcoming tender is designed to shift the dynamics of the global lithium market and help Chile compete with its global competitors. With the rise of China’s lithium mining giant, and the two dominant miners continuing to expand their footprints, Chile will open up the tender in the hopes of creating some of the biggest lithium projects of the next decade. This is all aimed at the mission of doubling production.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

In recent years, there has been much talk about the importance of helping women feel welcome, challenged in their skills, and finding opportunities in mining, an area traditionally dominated by men. Employers and an organisation called the Minerals Council of South Africa have conducted a survey on working conditions in the industry. They asked the respondents about their professional experience in the mining industry and whether it lured them into the mining industry or kept them there.

For the most part, respondents noted that the industry is constantly evolving, and never more than in the current moment. Inequality in the industry is at an all-time low and continues to drop as women take prominent positions at operational levels, middle-management, and the C-Suite.

North America Leading the Pack

A September 2019 report by international law firm Osler Hoskin Harcourt LLP & Co LLP found that in South Africa, the capital of African mining companies, a high percentage of female directors are driven by regulatory diversity standards. Whereas Latin America and the Caribbean have the lowest rates of women at the top of the mining sector. Canada and the United States are the countries making the most headway.

According to the US Bureau of Labor Statistics, women accounted for 15.8% of the labor force in the mining, quarrying, and oil and gas industries in the US in 2019. From the perspective of women with less than five years of work experience, women rank lower, while growth opportunities are higher for women with more than five years of work experience.

A report by PricewaterhouseCoopers in partnership with Women in Mining UK and Mining Talent shows that mining ranks third among global industries for women in leadership positions. Among the 500 largest mining companies in the world, 8% of directors are women.

A Prominent and Influential Executive

One of the executives breaking all barriers in their career in mining is Kylie Dickson. Kylie Dickson is a Canadian CPA with more than 14 years of experience working with listed commodity companies. She is also a Canadian auditor who has worked throughout the life cycle of the company’s growth and has played a key role in several financing and M & A transactions. Ms. Dickson is a board member of Fortuna Silver Mines Inc. and Star Royalties Ltd. and was appointed to the Board of Directors at Hillcrest Energy.

Other prominent positions have included her time as Chief Financial officer of Solaris Resources, which she resigned from in November of 2019. Before Solaris Resources was spun out of Equinox Gold, Ms. Dickson served as Vice President of Business Development at Equinox Gold.

Solaris Resources has made a deliberate effort to promote women’s empowerment in mining as the diversity of a workforce and management has been proven to lead to more innovation and profitability. Companies have adjusted expectations and seen that they do better with more women in the boardroom, and in particular, directing decisions in the C-suite.

Ms. Sunny Lowe, Chief Financial Officer of Solaris Resources Inc, states, “Solaris has embraced the Women’s Empowerment Principles established by UN Global Compact Office in an effort to advance gender equality and women’s empowerment in the workplace. We have made a deliberate effort to work towards developing a work environment that is barrier-free to developing women leaders in our organization and beyond. The Principles allow us to strengthen our commitment towards internationally proclaimed human rights and serve as a framework for us to create real impact on gender equality through commitment and action focused on seeing female representation in all our operations as well as within industry. Earlier this year, together with Women in Mining Ecuador, we launched the Soy Minera (Woman Miner) scholarship program that will finance undergraduate tuition for female engineering and/or undergraduate students in careers related to mining in Ecuador, supporting the mainstreaming of gender equality at our Warintza project, as well as the opportunity of the mining sector to incorporate actions, through investment, toward women empowerment in the industry.”

Kylie Dickson was on maternity leave for seven months after having her third child when the company she founded, Anthem United, Inc., entered into a merger with two other companies. Shortening maternity leave and hiring a nanny have been one of the toughest decisions of her career, she says.

Dickson grew up in Maple Ridge, British Columbia and earned a Bachelor of Business Administration from Simon Fraser University. During her studies, she worked at KPMG before getting a full-time job in 2003 and earning her Certificate of Accountancy. Using her skills and training, she has specialised as a manager in the mining sector.

A Track Record That Says it All

One of KPMG’s clients was Greg Smith, a mining entrepreneur who founded a company called Minefinders Corp. He hired Dickson as a financial controller and led partnerships in a series of successful mine mergers and acquisitions worth more than $2 billion. Dickson was Chief Financial officer of the subsequently acquired Esperanza Resources Corp. After leaving, Dickson co-founded Anthem United.

Her track record is an impressive one, and stands out as an example of a multi-faceted executive career in the mining industry. She was the Vice President of Business Development at Equinox Gold Corp. and, before that, VP, Business Development at Trek Mining. Kylie previously worked as Chief Financial Officer for JDL Gold Corp., Anthem United Inc. and Esperanza Resources, and served as the Corporate Controller of Minefinders Corporation.

The Latest Chapter

Most recently, Hillcrest Energy Technologies appointed Kylie Dickson to its Board of Directors.

Hillcrest is a partnership with Oropass Ltd., an Ontario-registered company that holds the U.S. license rights to a patented electrical generation technology. Through concept and commercialization, Hillcrest Energy Technologies Ltd. invests in the development of future-oriented energy solutions.

CEO Don Currie announced the appointment of Kylie Dickson to the company’s board of directors on April 9. Ms Dickson has worked throughout the life cycle of Hillcrest’s growth and has played a key role in several financing and M&A transactions. She will join the company’s Board of Directors, where she will bring experience, knowledge and involvement in areas such as audit and corporate governance committees.

Kylie Dickson also joined the Fortuna Silver Mines Inc. Board in 2017 and sits on the Audit Committee and Corporate Governance and Nominating Committee. Ms. Dickson is an executive with over 14 years of experience in the mining industry. She has worked with companies at various stages of the mining life cycle including exploration, mine development and operations, as well as playing a key role in multiple financings and M&A transactions. Kylie is currently the Vice President, Business Development of Trek Mining Inc. Kylie Dickson was the Chief Financial Officer of JDL Gold Corp. when JDL acquired Luna Gold Corp. to create Trek Mining in March 2017.

Previously, Kylie was a founding shareholder and Chief Financial Officer of Anthem United Inc. and was the Chief Financial Officer of Esperanza Resources which was acquired by Alamos Gold in 2013. She also served as the Corporate Controller of Minefinders Corporation from 2007 to 2012 prior to its acquisition by Pan American Silver. Kylie also currently serves on the Board of Directors at Hillcrest Energy Kylie began her career with KPMG LLP’s mining practice and is a Canadian CPA, CA with a BBA in Accounting from Simon Fraser University.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Collective Mining (TSXV:CNL) is pleased to announce that Steven Gold has been appointed Vice President of Corporate Development and Investor Relations, and granted 200,000 stock options, effective October 12, 2021. The stock options are exercisable for a period of five years from the date of grant to a common share of Collective Mining at a price of $2.40 per share and will vest at 25 percent every six months.

Mr. Gold has more than 20 years of capital market experience in the natural resource sector and has held various positions in the investment industry, both on the buy and sell side. More recently, he has held Senior Officer and Corporate Development roles at various junior and mid-level mining companies in the global mining sector.

Mr. Gold will now bring his valuable experience and expertise to the team at Collective Mining as it pursues exploration projects in Colombia, including its flagship Guayabales project.

Collective Mining Expecting Assay Results in Q4 2021

Collective Mining (TSXV:CNL) is an exploration and development company focused on identifying and exploring prospective mineral projects in South America. Founded by the team that developed and sold Continental Gold Inc. to Zijin Mining for approximately $2 billion in enterprise value, the mission of the Company is to repeat its past success in Colombia by making a significant new mineral discovery and advancing the projection to production. Management and insiders own approximately 41% of the outstanding shares of the Company and as a result are fully aligned with shareholders. Collective currently holds an option to earn up to a 100% interest in two projects located in Colombia: (i) the San Antonio project; and (ii) the Guayabales Project. With an aggressive grassroots exploration program in 2021 outlining five major targets at the Guayabales Project, the Company recently initiated a maiden 7,500 metre drill program with a sole purpose to make the next major discovery in Colombia. Initial assay results from this drill program are anticipated in Q4, 2021.

Source: Collective Mining

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Mining companies often need to contend with adverse factors and environments. Mining requires a complex infrastructure of mining equipment, transportation, and resource management. The last thing miners want to contend with is a dangerous or politically unstable jurisdiction.

However, some companies are finding that the risk far outweighs the reward and are willing to work in jurisdictions often avoided by most companies. This includes countries that contain deposits of metals and minerals gaining in value and demand, making the investment and risk worth the effort.

BHP (NYSE:BHP) is one of those companies, as CEO Mike Henry recently said that BHP is prepared to shift out of its usual operational comfort zone of advanced economies to work in “tougher jurisdictions”. Why would BHP take on more risk in countries that have politically volatile environments? To gain exposure to commodities like copper, nickel, or cobalt, for which demand is booming as they are needed for the green energy transition underway.

Investment in projects in these areas will require careful planning and understanding the political climate of areas typically avoided by mining companies. BHP’s scale and expertise will allow it to manage those risks to capitalize on the potential profits.

Henry commented, “But of course, the size of the opportunity needs to be commensurate with the increased management effort that is going to be required to pursue opportunities in jurisdictions that we may not currently be operating in,” Henry said.

Where and When?

The Democratic Republic of Congo (DRC) is host to Ivanhoe Mines’s (TSX:IVN) Kamoa-Kakula mine, also known as Western Foreland. This mine has been profitable for the company, and BHP is now holding talks with Ivanhoe over an exploration site adjacent to Kamoa-Kakula.

The DRC has also made it clear that it wants to open it doors wide for foreign investment, particularly for its copper and cobalt deposits. This would exploring outside of many companies’ “comfort zones”, but would also put companies who invest in these countries at an advantage in the future.

Besides the growing demand for these metals and minerals, there is also the probability that politically volatile jurisdictions could transform rapidly into stable ones, making it even more attractive for mining companies. But the miners who are first into these countries will have more attractive terms and a lower overall cost as incentives are higher and competition is lower.

While BHP is prepared to move into new areas, the company will be exploring opportunities in the “areas we like” as well. That may mean higher costs as some projects become less accessible, but BHP is prepared to invest in the effort to maximise returns in countries it has operational experience.

Henry continued, “I want to be clear we don’t see exploration success as being confined to moving into new jurisdictions. We know there is more copper to be found in the areas we like but it is going to be harder to find and perhaps deeper, which is going to bring different technological and financial challenges,” he said.

The Democratic Republic of Congo’s First Mover Advantage

In an effort to court more foreign investment, the DRC has paved the way for simpler and smoother deals to be made with lower taxes and support from local communities. This has made it a new focus for some miners.

Murray Hitzman, a former US Geological Survey scientist who spent more than a decade touring the southern Congo and advising mining projects, said the region’s rich cobalt and copper deposits began life at the bottom of shallow, ancient seas eight hundred million years ago. Over time, sedimentary rocks were buried under gentle hills, and salty liquids containing metals seeped into the earth and mineralized the rock.

A quarter of the world’s gold, tin and tantalum reserves are produced by artisanal and small miners. The artisanal miners are particularly interested in copper and cobalt; cobalt is a major attraction due to its high value-weight ratio, but efficient copper mining requires large-scale operations. A handful of mines provide semi-formal access for artisanal miners as part of the site, but industrial mining companies are in the default position of refusing to cooperate with them.

Africa Moving Rapidly

In recent decades, African governments have lifted restrictions and privatized their mining industries, attracting significant foreign direct investment. As a result, these industries have been dominated by transnational corporations such as Glencore, AngloAmerican, and Barrick Gold. These companies operate outside the formal reach and control of African governments and sit next to artisanal and small-scale mining sectors.