NOT FOR DISTRIBUTION IN OR INTO OR TO ANY PERSON LOCATED OR RESIDENT IN AUSTRALIA, JAPAN, SOUTH AFRICA OR ANY OTHER JURISDICTION OR TO ANY PERSON LOCATED OR RESIDENT IN ANY JURISDICTION IN WHICH SUCH DISTRIBUTION IS UNLAWFUL

ENDEAVOUR ANNOUNCES PRICING OF US$500 MILLION

5-YEAR SENIOR NOTES

London, 7 October 2021 – Endeavour Mining plc (LSE:EDV, TSX:EDV, OTCQX:EDVMF) (the “Company”, together with its subsidiaries, the “Group”) is pleased to announce the pricing of its offering of US$500 million fixed rate senior notes due 2026 (the “Notes”) as part of its refinancing strategy.

The Company will pay interest on the Notes semi-annually at a rate equal to 5.00% per annum. The Notes will settle on or around 14 October 2021, subject to customary conditions, and the Notes will mature on 14 October 2026.

The proceeds of the Notes, together with cash available on the Group’s balance sheet, will be used: (i) to repay all amounts outstanding under the Group’s US$370 million bridge term loan facility, which was used to retire higher cost debt facilities acquired upon the acquisition of Teranga Gold Corporation (the “Bridge Facility”), (ii) to repay the US$130 million drawn under the Group’s existing revolving credit facility (the “Existing RCF”), and (iii) to pay fees and expenses in connection with the offering of the Notes.

As part of its Group refinancing strategy, the Company recently entered into a US$500 million unsecured revolving credit facility (the “New RCF”). The New RCF has a four-year tenor, with an interest rate ranging between 2.40 – 3.40% plus LIBOR (or SOFR) depending on leverage. The undrawn portion has a commitment fee of 35% of the applicable margin (0.84% based on currently applicable margin). The New RCF will replace the Bridge Facility and the Existing RCF, which will be cancelled upon settlement of the Notes offering. Effectiveness of the New RCF is conditioned upon the closing of the Notes offering.

The New RCF and the Notes will extend the maturities of the Company’s existing debt structure to 2025 and 2026 respectively, providing increased financial flexibility.

ABOUT ENDEAVOUR MINING PLC

Endeavour is one of the world’s senior gold producers and the largest in West Africa, with operating assets across Senegal, Cote d’Ivoire and Burkina Faso and a strong portfolio of advanced development projects and exploration assets in the highly prospective Birimian Greenstone Belt across West Africa.

A member of the World Gold Council, Endeavour is committed to the principles of responsible mining and delivering sustainable value to its employees, stakeholders and the communities where it operates. Endeavour is listed on the London Stock Exchange and the Toronto Stock Exchange, under the symbol EDV.

For more information, please visit www.endeavourmining.com.

Neither the Toronto Stock Exchange nor the Investment Industry Regulatory Organization of Canada accepts responsibility for the adequacy or accuracy of this press release.

IMPORTANT INFORMATION

This announcement is for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to buy the Notes or the guarantees thereof (the “Guarantees”), nor shall it constitute an offer, solicitation or sale in any jurisdiction in which, or to any person to whom, such offer, solicitation or sale would be unlawful. The Notes and the Guarantees have not been and will not be registered under the U.S. Securities Act of 1933 or the securities laws of any other jurisdiction. Securities may not be offered in the United States absent registration or an exemption from registration. No action has been or will be taken in any jurisdiction in relation to the Notes or the Guarantees to permit a public offering of securities. There is no assurance that any Notes offering will be completed or, if completed, as to the terms on which it is completed.

The Notes and the Guarantees are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the European Economic Area (“EEA”). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU (as amended, “MiFID II”) or (ii) a customer within the meaning of Directive 2016/97/EU, as amended (the “Insurance Distribution Directive”), where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II. Consequently, no key information document required by Regulation (EU) No 1286/2014 (as amended, the “EU PRIIPs Regulation”) for offering or selling the Notes or the Guarantees or otherwise making them available to retail investors in the EEA has been prepared and therefore offering or selling the Notes or the Guarantees or otherwise making them available to any retail investor in the EEA may be unlawful under the EU PRIIPs Regulation.

The Notes and the Guarantees are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the United Kingdom (the “UK”). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (8) of Article 2 of Regulation (EU) 2017/565 as it forms part of domestic law in the UK by virtue of the European Union (Withdrawal) Act 2018, as amended (the “EUWA”) or (ii) a customer within the meaning of the provisions of the Financial Services and Markets Act 2000, as amended (the “FMSA”), and any rules or regulations made under the FSMA to implement the Insurance Distribution Directive, where that customer would not qualify as a professional client, as defined in point (8) of Article 2(1) of Regulation (EU) 600/2014 as it forms part of domestic law in the UK by virtue of the EUWA. Consequently, no key information document is required by Regulation (EU) 1286/2914 as it forms part of domestic law in the UK by virtue of the EUWA (the “UK PRIIPs Regulation”) for offering or selling the Notes or otherwise making them available to UK retail investors in the UK has been prepared and therefore offering or selling the notes or otherwise making them available to any UK retail investor in the UK may be unlawful under the UK PRIIPs Regulation.

MiFID II professionals / ECPs-only / No PRIIPs KID – Manufacturer target market (MiFID II product governance) is eligible counterparties and professional clients only (all distribution channels). No EU PRIIPs key information document (“KID”) has been prepared as not available to retail in the EEA.

UK MiFIR professionals / ECPs-only / No UK PRIIPs KID – Manufacturer target market (UK MiFIR product governance) is eligible counterparties and professional clients only (all distribution channels). No UK PRIIPs key information document (“KID”) has been prepared as not available to retail in the UK.

This announcement is being distributed to, and is directed at, only persons who (i) are outside the UK; (ii) are “qualified investors” within the meaning of Article 2 of Regulation (EU) 2017/1129 (the “Prospectus Regulation”) as it forms part of retained EU law in the UK as defined in the EUWA (iii) have professional experience in matters relating to investments falling within the definition of “investment professionals” in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”), or (iv) are persons who are high net worth bodies corporate, unincorporated associations and partnerships and the trustees of high value trusts, as described in Article 49(2)(a) to (d) of the Order or (iii) are persons to whom this communication may otherwise be lawfully communicated (all such persons together being referred to as “Relevant Persons”). The investments to which this announcement relates are available only to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such investments will be available only to or will be engaged in only with, Relevant Persons. Any person who is not a relevant person should not act or rely on this announcement or any of its contents. Persons distributing this announcement must satisfy themselves that it is lawful to do so.

In any EEA Member State this communication is only addressed to and is only directed at “qualified investors” in that Member State within the meaning of Article 2(e) of the Prospectus Regulation.

The Notes have not been nor will they be qualified for sale to the public under applicable Canadian securities laws and, accordingly, any offer and sale of the Notes in Canada will be made on a basis which is exempt from the prospectus requirements of Canadian securities laws and the Notes will be subject to “hold period” resale restrictions under applicable Canadian securities laws.

The distribution of this announcement in certain jurisdictions may be restricted by law and therefore persons in such jurisdictions into which they are released, published or distributed, should inform themselves about, and observe, such restrictions. Any failure to comply with these restrictions may constitute a violation of the laws of any such jurisdiction.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

This announcement contains “forward-looking statements” within the meaning of applicable securities laws. All statements, other than statements of historical fact, are “forward-looking statements”, including but not limited to, statements with respect to the Group’s intentions with regards to any offering of the Notes and the Guarantees. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “will”, “can”, “could”, “would” and similar expressions.

Forward-looking statements, while based on management’s reasonable estimates, projections and assumptions at the date the statements are made, are subject to risks and uncertainties that may cause actual results to be materially different from those expressed or implied by such forward-looking statement. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Please refer to the Group’s most recent Annual Information Form filed under its profile at www.sedar.com for further information respecting the risks affecting Endeavour and its business.

These forward-looking statements speak only as of the date of this announcement. Except as required by applicable law and regulation, the Company does not undertake any obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

CONTACT INFORMATION

|

Endeavour Mining |

Brunswick Group LLP in London Vincic Advisors in Toronto |

Attachment

VANCOUVER, British Columbia, Oct. 07, 2021 (GLOBE NEWSWIRE) — Lupaka Gold Corp. ("Lupaka" or the “Company") (TSX-V: LPK, FRA: LQP) provides an update on progress with its international arbitration claim against the Republic of Peru.

Over the past months, the Company, its legal team and associates in Peru and Canada have been compiling background information, relevant documents and witness statements to support the arbitration case against the Republic of Peru. As part of its case, Lupaka contracted an independent Quantum Evaluator to assess the damages. As of October 1, 2021, the first round of comprehensive submissions supporting Lupaka’s claim have been submitted to the Arbitration Tribunal. The Republic of Peru and its legal team will now review the material and respond.

A few relevant points are as follows:

-

The police developed a comprehensive and detailed plan to remove the illegal blockade and restore the Company’s access to the mine. Permission to execute this plan was requested from senior authorities in Lima but permission was not provided.

-

Many meetings were held and correspondence traded between the Company’s representatives and multiple levels of the Peruvian government. Despite the evidence that the situation should be resolved by the authorities, this was not done.

-

The company that foreclosed on and now owns the Invicta Project expressed a high level of confidence that they would have the community issues resolved and full access to the mine in a very short time frame. To the best of our knowledge the illegal blockade remains in place today (now three years since the permanent blockade was put in place) and the group that erected the illegal blockade is currently exploiting the mine.

-

The Company had all key permits in place as well as valid agreements with the two communities owning the surface rights on which mining activities were to take place and was about to go into full production when the illegal and violent blockade occurred.

After reviewing ongoing and recently completed arbitration cases, the Company considers its case to be exceptionally strong and well justified.

For ongoing updates and more detail with respect to the arbitration, please refer to the Company’s website (www.lupakagold.com/projects/arbitration).

For background on the basis for the arbitration please refer to the Company’s previous news releases, also available on the website (www.lupakagold.com/news/#2020).

With respect to the arbitration proceedings, Lupaka is represented by the international law firm, LALIVE (www.lalive.law), and has the financial backing of Bench Walk Advisors (www.benchwalk.com).

Neither the TSX Venture Exchange nor its Regulation Service Provider (as the term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy of this news release.

About Lupaka Gold

Lupaka is an active Canadian-based company focused on creating shareholder value through identification and development of mining assets.

About Bench Walk Advisors

Bench Walk Advisors is a global litigation financier with over USD 250m of capital deployed across in excess of 100 commercial cases. Bench Walk and its principals have consistently been ranked as leading lawyers and litigation funders in various global directories.

About LALIVE

LALIVE is an international law firm with offices in Geneva, Zurich and London, that specializes in international dispute resolution. The firm has extensive experience in international investment arbitration in the mining sector, amongst others, and is currently representing investors and States as counsel worldwide.

FOR FURTHER INFORMATION PLEASE CONTACT:

Gordon Ellis, C.E.O.

gellis@lupakagold.com

Tel: (604) 985-3147

or visit the Company’s profile at www.sedar.com or its website at www.lupakagold.com

Just because a business does not make any money, does not mean that the stock will go down. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So, the natural question for Prairie Mining (ASX:PDZ) shareholders is whether they should be concerned by its rate of cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

View our latest analysis for Prairie Mining

Does Prairie Mining Have A Long Cash Runway?

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. When Prairie Mining last reported its balance sheet in June 2021, it had zero debt and cash worth AU$5.0m. Importantly, its cash burn was AU$2.2m over the trailing twelve months. So it had a cash runway of about 2.2 years from June 2021. That's decent, giving the company a couple years to develop its business. You can see how its cash balance has changed over time in the image below.

How Is Prairie Mining's Cash Burn Changing Over Time?

In our view, Prairie Mining doesn't yet produce significant amounts of operating revenue, since it reported just AU$298k in the last twelve months. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. Even though it doesn't get us excited, the 40% reduction in cash burn year on year does suggest the company can continue operating for quite some time. Admittedly, we're a bit cautious of Prairie Mining due to its lack of significant operating revenues. We prefer most of the stocks on this list of stocks that analysts expect to grow.

How Hard Would It Be For Prairie Mining To Raise More Cash For Growth?

While Prairie Mining is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Prairie Mining has a market capitalisation of AU$80m and burnt through AU$2.2m last year, which is 2.8% of the company's market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

So, Should We Worry About Prairie Mining's Cash Burn?

As you can probably tell by now, we're not too worried about Prairie Mining's cash burn. For example, we think its cash burn relative to its market cap suggests that the company is on a good path. And even though its cash burn reduction wasn't quite as impressive, it was still a positive. Looking at all the measures in this article, together, we're not worried about its rate of cash burn; the company seems well on top of its medium-term spending needs. On another note, we conducted an in-depth investigation of the company, and identified 3 warning signs for Prairie Mining (1 can't be ignored!) that you should be aware of before investing here.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

(Bloomberg) — If iron ore giant Vale SA decides to separate its base metals operations, it may look at the possibility of merging that business with the assets of another company.

Most Read from Bloomberg

-

How Singapore's $50 Billion Financial District Will Change After Covid-19

-

Left-Wing Rage Threatens a Wall Street Haven in Latin America

-

Amazon Delivery Partners Rage Against the Machines: ‘We Were Treated Like Robots’

-

Climate Scientists Created a SWAT Team for Weather Disasters

Chief Executive Officer Eduardo Bartolomeo opened the door to such a possibility during the Financial Times Mining Summit on Thursday.

The world’s second-largest producer of iron ore continues to weigh up the pros and cons of forming a seperate company with its copper and nickel mines in Canada, Brazil and Indonesia. The goal is to unlock value as the global transition toward clean energy gains momentum. A future merger would help Vale gain scale as new deposits get trickier and pricier to find and develop.

“When you have this vehicle you might find a way to merge with somebody who has synergies with you,” Bartolomeo said. “But this is a second step. First step is to look at yourself, fix yourself.”

Read More: Vale CEO Sees Iron Ore Market Staying ‘Relatively Tight’

Vale became the world’s biggest commercial producer of nickel after taking over Inco in 2006 for about $19 billion. The company calculates the nickel and copper business is worth about $25 billion, a value that’s not reflected in the current single structure.

“When people look at Vale, they look to iron ore,” he said.

The company sees an opportunity to grow in the electric-vehicle supply chain as the world tries to wean itself off fossil fuels.

Vale has faced setbacks in its base metals operations in the past week or so, with miners trapped in a Canadian underground mine, a fire at Brazil’s Salobo copper mine and a temporary halt of nickel mining at Onca Puma.

Most Read from Bloomberg Businessweek

-

As Louisianans Flee Hurricanes, Natural Gas Dollars and Jobs Flood In

-

‘Most Americans Today Believe the Stock Market Is Rigged, and They’re Right’

©2021 Bloomberg L.P.

(Reuters) -The chief executive of Vale SA said on Thursday the Brazilian iron ore miner is not looking into a near-term spin-off for its base metal, and the company later said the unit needs to be "transformed" before that longstanding plan can be carried out.

"We are not talking about a spin off yet. The problem here is the size of the business," said Eduardo Bartolomeo, Vale's Chief Executive Officer as part of the Financial Times' Mining Summit.

Vale had a longstanding plan to sell the unit, that was still being considered as recently as April of this year. The plan had first been developed in 2014, postponed to 2015, and then the idea was temporarily abandoned.

Bartolomeo said part of the problem was the value of the business, saying it brings in $3.5 billion in revenue a year, which would put a sale value at "more or less $25 billion."

To get to a spin-off, Vale said in a statement after the event, "the business still needs to be adjusted, transformed, and go through an internal transformation."

Vale, one of the world's largest iron ore miners, is still dealing with the consequences of a dam burst in 2019, which killed 270 in the town of Brumadinho.

Aside from the lives lost, the environmental damage, fines and complicated legal proceedings that targeted its top executives, the incident also depressed the company's value.

"We are perceived as a risky stock," Bartolometo said, adding however that "Vale did the homework. Now it's not a risky company."

(Reporting by Marcelo Rochabrun; Editing by David Gregorio)

Vale S.A VALE recently announced that it has temporarily suspended production of copper concentrate at its Salobo mine in Brazil after a fire partially affected a conveyor belt. The company stated that other activities, including mine and maintenance operations, are running as usual. The impacted site is currently undergoing an assessment, and the company expects to resume operations by the end of this month.

Vale’s Salobo mine, located in Marabá, in the southeast of Pará, is the largest copper deposit ever discovered in Brazil. The low-cost copper-gold mine began operating in 2012. In October 2018, the company announced the approval of the Salobo III mine expansion, which is currently in progress. Start-up is expected in 2022 and the expansion is expected to increase capacity by 30-40 kt per year.

In 2020, Vale produced 360.1 kt of copper with Salobo contributing 172.7 kt, or 48% of the total output. In the first half of 2021, the company produced 179 kt of copper. Of this, Salobo’s contribution was 83.5 kt. In the second quarter of 2021, copper production in Salobo was 38.7 kt, 13.5% higher than the first quarter, due to the ramp-up of mine maintenance activities. Movement at Salobo mine has been improving with increased availability of equipment as the ramp-up of the mine maintenance workshop continues. Total mine movement at Salobo has increased 31.2% in the second quarter compared to the first quarter. Improvement in mine movement is expected to have continued in the third quarter as well.

This news comes on the heels of Vale’s announcement that it has halted all activities at Onça Puma mine, Brazil, following the suspension of its operation license by a State Agency on allegations that the company has failed to comply with conditions for licensing. Vale is currently evaluating the direct impact of the shutdown on total production. Onca Puma accounted for 7.5% of the company's total nickel production in 2020.

Vale’s Base Metals business, which includes exploration efforts related to nickel, copper, cobalt, PGMs and gold and silver, has gone through a broad safety review of the operational process, resulting in comprehensive overhaul of maintenance standards, procedures, training and oversight. It anticipates improvements from maintenance activities to materialize throughout the business this year. The company anticipates to attain 500 ktpy (kilo tons per year) with projects — Salobo III, Alemao and Cristalino — already in pipeline. Carajas is expected to act as a key catalyst in copper growth. Vale uncovered 1.9 Mt of copper equivalent in the last two years that will support growth in the future. The long-term outlook for copper is positive as copper demand is expected to improve, partly driven by electric vehicles and renewable energy and infrastructure investments, while future supply growth remains challenged on account of declining ore grades and the lack of major discoveries.

So far this year, shares of Vale have fallen 16.2%, compared with the industry’s decline of 17.9%.

Image Source: Zacks Investment Research

The drop in Vale’s share price this year can primarily be attributed to the recent plunge in iron ore prices due to weak demand in China on account of its intensified curbs on steel production. In the third quarter of 2021, iron ore plummeted 49% — the first quarterly loss since the first quarter of 2020. Copper prices have dipped lately on a stronger dollar and easing supply disruption threat in Peru, the world's second largest producer of mined copper.

Zacks Rank & Key Picks

Vale currently carries a Zacks Rank #5 (Strong Sell).

Some better-ranked stocks in the basic materials space include Nucor Corporation NUE, Methanex Corporation MEOH and The Chemours Company CC. While Nucor and Methanex sport a Zacks Rank #1 (Strong Buy), Chemours carries a Zacks Rank #2 (Buy), at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Nucor has an estimated earnings growth rate of 537.4 % for the ongoing year. So far this year, the company’s shares have appreciated 82.9%.

Methanex has a projected earnings growth rate of 409.3 % for 2021. The company’s shares have gained 6% so far this year.

Chemours has an estimated earnings growth rate of 86.4% for the current year. The company’s shares have increased 23.7% year to date.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

VALE S.A. (VALE) : Free Stock Analysis Report

Nucor Corporation (NUE) : Free Stock Analysis Report

Methanex Corporation (MEOH) : Free Stock Analysis Report

The Chemours Company (CC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

(Reuters) – Fortescue Metals Group Ltd's green energy unit said on Thursday it bought a 60% stake in Dutch-based renewable firm High yield Energy Technologies (HyET) Group in a bid to cut costs and boost green energy production.

Fortescue Future Industries (FFI) is part of Fortescue Metals' plan to become the world's first major supplier of green iron ore, and aims to supply 15 million tonnes of green hydrogen globally by 2030.

Fortescue Metals, the world's No.4 iron ore producer, is pursuing some of the most ambitious green plans in the industry with its efforts to diversify into renewable energy and green hydrogen through FFI.

"HyET Hydrogen's technology will support FFI in reducing costs in other areas of the green hydrogen supply chain," said Julie Shuttleworth, chief executive officer of FFI.

FFI, which plans to spend between $400 million and $600 million in the year to June 2022 on developing green transport and decarbonisation technologies, expects to cut down costs at its Powerfoil factory in Australia from the acquisition.

As part of the deal, FFI will provide a majority share of financing for the expansion of HyET Solar's Dutch Solar photovoltaics factory. Financial terms of the stake acquisition were not disclosed.

(Reporting by Tejaswi Marthi in Bengaluru; Editing by Subhranshu Sahu)

Peel Mining (ASX:PEX) has had a rough three months with its share price down 5.9%. However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. Specifically, we decided to study Peel Mining's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for Peel Mining

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Peel Mining is:

4.2% = AU$3.7m ÷ AU$87m (Based on the trailing twelve months to June 2021).

The 'return' is the yearly profit. So, this means that for every A$1 of its shareholder's investments, the company generates a profit of A$0.04.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Peel Mining's Earnings Growth And 4.2% ROE

At first glance, Peel Mining's ROE doesn't look very promising. We then compared the company's ROE to the broader industry and were disappointed to see that the ROE is lower than the industry average of 13%. In spite of this, Peel Mining was able to grow its net income considerably, at a rate of 56% in the last five years. Therefore, there could be other reasons behind this growth. For instance, the company has a low payout ratio or is being managed efficiently.

Next, on comparing with the industry net income growth, we found that Peel Mining's growth is quite high when compared to the industry average growth of 24% in the same period, which is great to see.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Peel Mining is trading on a high P/E or a low P/E, relative to its industry.

Is Peel Mining Using Its Retained Earnings Effectively?

Peel Mining doesn't pay any dividend to its shareholders, meaning that the company has been reinvesting all of its profits into the business. This is likely what's driving the high earnings growth number discussed above.

Conclusion

Overall, we feel that Peel Mining certainly does have some positive factors to consider. Even in spite of the low rate of return, the company has posted impressive earnings growth as a result of reinvesting heavily into its business. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. You can see the 4 risks we have identified for Peel Mining by visiting our risks dashboard for free on our platform here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

Insiders who purchased PepinNini Minerals Limited (ASX:PNN) shares in the past 12 months are unlikely to be deeply impacted by the stock's 13% decline over the past week. Even after accounting for the recent loss, the AU$744k worth of stock purchased by them is now worth AU$989k or in other words, their investment continues to give good returns.

While we would never suggest that investors should base their decisions solely on what the directors of a company have been doing, logic dictates you should pay some attention to whether insiders are buying or selling shares.

See our latest analysis for PepinNini Minerals

PepinNini Minerals Insider Transactions Over The Last Year

The insider Peter Proksa made the biggest insider purchase in the last 12 months. That single transaction was for AU$506k worth of shares at a price of AU$0.54 each. That means that even when the share price was higher than AU$0.38 (the recent price), an insider wanted to purchase shares. It's very possible they regret the purchase, but it's more likely they are bullish about the company. We always take careful note of the price insiders pay when purchasing shares. As a general rule, we feel more positive about a stock if insiders have bought shares at above current prices, because that suggests they viewed the stock as good value, even at a higher price.

Happily, we note that in the last year insiders paid AU$744k for 2.60m shares. But they sold 128.50k shares for AU$57k. In the last twelve months there was more buying than selling by PepinNini Minerals insiders. Their average price was about AU$0.29. It is certainly positive to see that insiders have invested their own money in the company. However, we do note that they were buying at significantly lower prices than today's share price. The chart below shows insider transactions (by companies and individuals) over the last year. By clicking on the graph below, you can see the precise details of each insider transaction!

PepinNini Minerals is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Does PepinNini Minerals Boast High Insider Ownership?

Another way to test the alignment between the leaders of a company and other shareholders is to look at how many shares they own. A high insider ownership often makes company leadership more mindful of shareholder interests. PepinNini Minerals insiders own about AU$5.8m worth of shares. That equates to 34% of the company. While this is a strong but not outstanding level of insider ownership, it's enough to indicate some alignment between management and smaller shareholders.

What Might The Insider Transactions At PepinNini Minerals Tell Us?

It doesn't really mean much that no insider has traded PepinNini Minerals shares in the last quarter. But insiders have shown more of an appetite for the stock, over the last year. Overall we don't see anything to make us think PepinNini Minerals insiders are doubting the company, and they do own shares. So these insider transactions can help us build a thesis about the stock, but it's also worthwhile knowing the risks facing this company. Every company has risks, and we've spotted 4 warning signs for PepinNini Minerals (of which 2 don't sit too well with us!) you should know about.

Of course PepinNini Minerals may not be the best stock to buy. So you may wish to see this free collection of high quality companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions, but not derivative transactions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

VANCOUVER, British Columbia, October 06, 2021–(BUSINESS WIRE)–Fancamp Exploration Ltd. ("Fancamp" or the "Corporation") (TSX Venture Exchange: FNC) today announced the voting results at its annual general meeting ("AGM"), which was held earlier today in Montreal, Quebec.

A total of 126,670,684 million shares, representing approximately 71.76% of the Corporation’s issued and outstanding shares, were voted in connection with the meeting. The Corporation is pleased to announce that all resolutions put forward to shareholders in the Corporation’s management information circular ("Circular") dated June 2, 2021 were overwhelmingly approved, including the election of management nominees Mark Billings, Ashwath Mehra, Rajesh Sharma, Paul Ankcorn, H. Dean Journeaux, and Charles Tarnocai.

As announced on September 22, 2021, Mr. Greg Ferron has been appointed to Fancamp’s Board of Directors (the "Board"), replacing Mr. Paul Ankcorn, who has stepped down. Mr. Mathieu Stephens has also been appointed to the Board, replacing Mr. H. Dean Journeaux who has resigned.

The shareholders of Fancamp voted to re-appoint MNP LLP, Chartered Accountants as Fancamp’s auditors for the next ensuing year. The shareholders of Fancamp also re-approved the Corporation’s "rolling10%" stock option plan.

Fancamp thanks shareholders for their consistent strong support and looks forward to moving forward with its plan to create value for all shareholders.

Advisors

Lavery, de Billy, L.L.P. and Goodmans LLP are serving as legal advisor to Fancamp. Harris & Company LLP is serving as litigation counsel to Fancamp. Kingsdale Advisors is acting as strategic shareholder and communications advisor to Fancamp. Koffman Kalef LLP is serving as legal advisor to the Special Committee.

About Fancamp Exploration Ltd. (TSX-V: FNC)

Fancamp is a growing Canadian mineral exploration corporation dedicated to its value-added strategy of advancing mineral properties through exploration and development. The Corporation owns numerous mineral resource properties in Quebec, Ontario and New Brunswick, including gold, rare earth metals, strategic and base metals, zinc, chromium, titanium and more. Fancamp is also building on the industrial possibilities inherent in dealing with some of these materials, notable being the development of its Titanium technology strategy. The Corporation is managed by a new and focused leadership team with decades of mining, exploration and complementary technology experience.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

View source version on businesswire.com: https://www.businesswire.com/news/home/20211005006252/en/

Contacts

Rajesh Sharma, Chief Executive Officer

+1 (604) 434 8829

info@fancamp.ca

Debra Chapman, Chief Financial Officer

+1 (604) 434 8829

info@fancamp.ca

VANCOUVER, British Columbia, October 06, 2021–(BUSINESS WIRE)–Fancamp Exploration Ltd. ("Fancamp" or the "Corporation") (TSX Venture Exchange:FNC) is pleased to announce that it has successfully acquired a total of 2,348,485 common shares ("ScoZinc Shares") of ScoZinc Mines Ltd. ("ScoZinc") on October 5, 2021, further to Fancamp’s news release dated September 16, 2021. Of the 2,348,485 ScoZinc Shares, Fancamp acquired 1,969,697 ScoZinc Shares by way of private placement at $0.66 per share for a total purchase price of $1,300,000, of which a termination fee of $300,000 payable to ScoZinc was credited towards the purchase price and Fancamp paid the balance of $1,000,000 in cash, and 378,788 ScoZinc Shares at a deemed issue price of $0.66 per share in settlement of an outstanding loan of $250,000 to ScoZinc (the "Transaction"). The ScoZinc Shares are subject to a hold period expiring February 6, 2022.

Immediately prior to the closing of the Transaction, Fancamp had no beneficial ownership of any ScoZinc Shares. Upon closing of the Transaction, Fancamp currently has beneficial ownership of 2,348,485 ScoZinc Shares, representing 13.1% of the outstanding ScoZinc Shares, a total increase of 13.1% of Fancamp’s beneficial shareholding percentage in the ScoZinc Shares.

Fancamp has acquired the ScoZinc Shares for investment purposes. Fancamp may acquire additional ScoZinc Shares or dispose of ScoZinc Shares (through market or private transactions) from time to time.

A copy of the related early warning report may be obtained from the SEDAR website (www.sedar.com) or from Debra Chapman at Fancamp at +1 (604) 434 8829.

About Fancamp Exploration Ltd. (TSX-V:FNC)

Fancamp is a growing Canadian mineral exploration corporation dedicated to its value-added strategy of advancing mineral properties through exploration and development. The Corporation owns numerous mineral resource properties in Quebec, Ontario and New Brunswick, including gold, rare earth metals, strategic and base metals, zinc, chromium, titanium and more. Fancamp is also building on the industrial possibilities inherent in dealing with some of these materials, notable being the development of its Titanium technology strategy. The Corporation is managed by a new and focused leadership team with decades of mining, exploration and complementary technology experience.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

View source version on businesswire.com: https://www.businesswire.com/news/home/20211006005322/en/

Contacts

Rajesh Sharma, Chief Executive Officer

+1 (604) 434 8829

info@fancamp.ca

Debra Chapman, Chief Financial Officer

+1 (604) 434 8829

info@fancamp.ca

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Lynas Rare Earths (ASX:LYC) so let's look a bit deeper.

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Lynas Rare Earths:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets – Current Liabilities)

0.11 = AU$156m ÷ (AU$1.5b – AU$108m) (Based on the trailing twelve months to June 2021).

Thus, Lynas Rare Earths has an ROCE of 11%. On its own, that's a standard return, however it's much better than the 9.5% generated by the Metals and Mining industry.

Check out our latest analysis for Lynas Rare Earths

Above you can see how the current ROCE for Lynas Rare Earths compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

What Does the ROCE Trend For Lynas Rare Earths Tell Us?

Lynas Rare Earths has recently broken into profitability so their prior investments seem to be paying off. The company was generating losses five years ago, but now it's earning 11% which is a sight for sore eyes. In addition to that, Lynas Rare Earths is employing 103% more capital than previously which is expected of a company that's trying to break into profitability. We like this trend, because it tells us the company has profitable reinvestment opportunities available to it, and if it continues going forward that can lead to a multi-bagger performance.

The Bottom Line

To the delight of most shareholders, Lynas Rare Earths has now broken into profitability. Since the stock has returned a staggering 1,087% to shareholders over the last five years, it looks like investors are recognizing these changes. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

One more thing to note, we've identified 1 warning sign with Lynas Rare Earths and understanding this should be part of your investment process.

While Lynas Rare Earths may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

It is usually uneventful when a single insider buys stock. However, When quite a few insiders buy shares, as it happened in Dundee Precious Metals Inc.'s (TSE:DPM) case, it's fantastic news for shareholders.

While insider transactions are not the most important thing when it comes to long-term investing, logic dictates you should pay some attention to whether insiders are buying or selling shares.

See our latest analysis for Dundee Precious Metals

Dundee Precious Metals Insider Transactions Over The Last Year

In the last twelve months, the biggest single sale by an insider was when the President, David Rae, sold CA$304k worth of shares at a price of CA$7.60 per share. That means that even when the share price was below the current price of CA$7.90, an insider wanted to cash in some shares. When an insider sells below the current price, it suggests that they considered that lower price to be fair. That makes us wonder what they think of the (higher) recent valuation. However, while insider selling is sometimes discouraging, it's only a weak signal. This single sale was 100% of David Rae's stake. David Rae was the only individual insider to sell over the last year. Notably David Rae was also the biggest buyer, having purchased CA$337k worth of shares.

Over the last year, we can see that insiders have bought 85.27k shares worth CA$337k. But insiders sold 40.00k shares worth CA$304k. Overall, Dundee Precious Metals insiders were net buyers during the last year. The average buy price was around CA$3.95. It is certainly positive to see that insiders have invested their own money in the company. However, we do note that they were buying at significantly lower prices than today's share price. You can see a visual depiction of insider transactions (by companies and individuals) over the last 12 months, below. By clicking on the graph below, you can see the precise details of each insider transaction!

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Insider Ownership

Looking at the total insider shareholdings in a company can help to inform your view of whether they are well aligned with common shareholders. Usually, the higher the insider ownership, the more likely it is that insiders will be incentivised to build the company for the long term. Our data indicates that Dundee Precious Metals insiders own about CA$11m worth of shares (which is 0.7% of the company). Whilst better than nothing, we're not overly impressed by these holdings.

So What Do The Dundee Precious Metals Insider Transactions Indicate?

The fact that there have been no Dundee Precious Metals insider transactions recently certainly doesn't bother us. On a brighter note, the transactions over the last year are encouraging. Overall we don't see anything to make us think Dundee Precious Metals insiders are doubting the company, and they do own shares. So these insider transactions can help us build a thesis about the stock, but it's also worthwhile knowing the risks facing this company. While conducting our analysis, we found that Dundee Precious Metals has 2 warning signs and it would be unwise to ignore them.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions, but not derivative transactions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

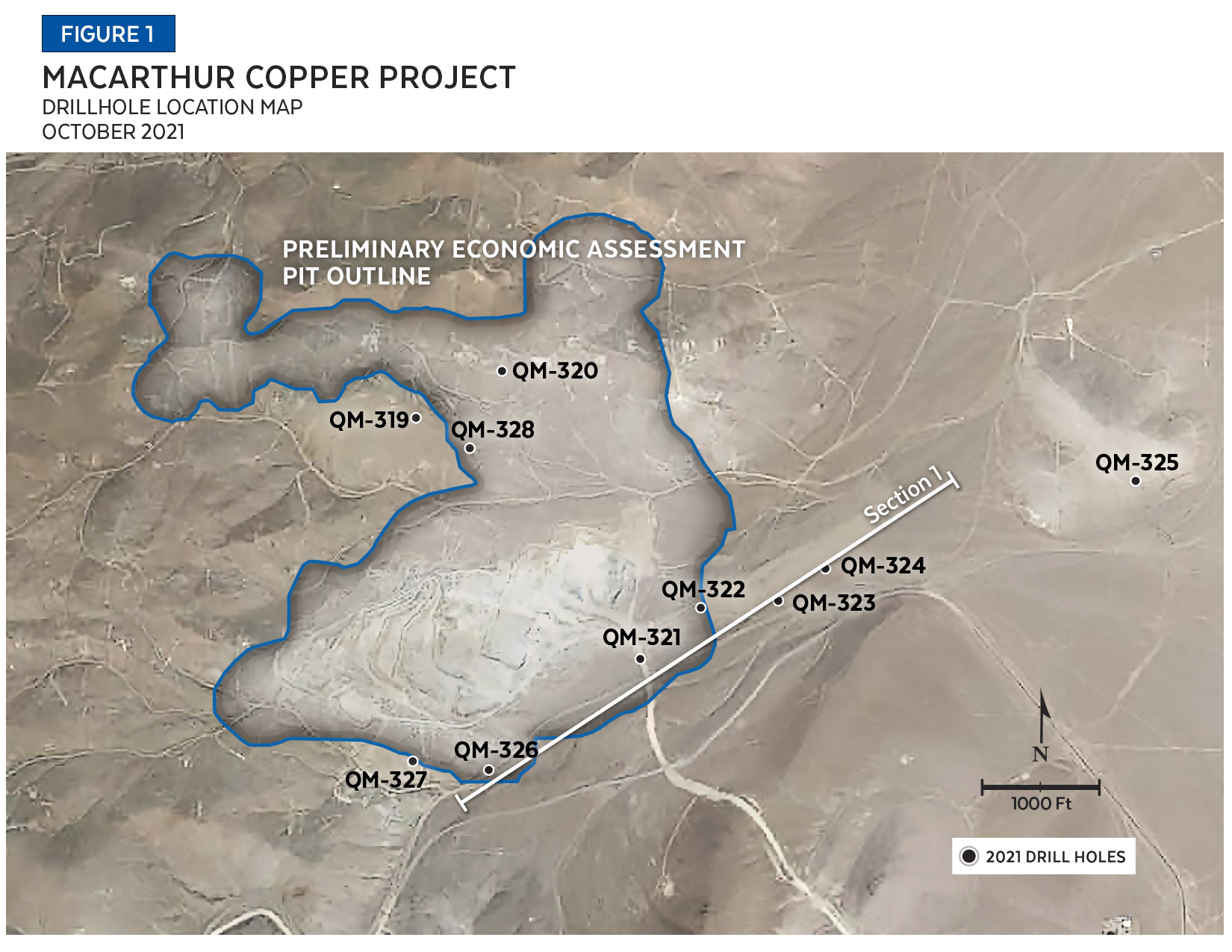

Vancouver, British Columbia–(Newsfile Corp. – October 6, 2021) – Quaterra Resources Inc. (TSXV: QTA) (OTCQB: QTRRF) (the "Company") today announced positive results from a ten-hole core drilling program totaling 5,147 feet (1,569 meters) that was recently completed. The ten-hole program was designed to assess the likelihood that further drilling would upgrade portions of the resource from Inferred to Indicated and expand the overall size of the current resource. Mr. Travis Naugle, CEO states, "We believe that additional drilling could accomplish these exciting objectives." These results are further discussed below and outlined in Table 1 below.

Three holes (QM-319, QM-320, and QM-328) were drilled on the north to northwestern edge of the current resource. Each hole intersected oxide and chalcocite mineralization. Significant intercepts include drill hole QM-320 (31.1 m @ 0.58% Cu, including 22.6 m @ 0.70% Cu); QM-328 (23.5 m @ 0.44% Cu); and QM-319 (10.8 m @ 0.14% Cu). Each drill hole contains additional acid soluble copper intercept (Table 1).

Holes QM-326 and QM-327, drilled on the southern edge of the current oxide resource (Figure 1), each intersected near surface oxide mineralization. Significant intercepts include 6.7 m @ 0.27% Cu and 7.3 m @ 0.70% copper from QM-326 and QM-327, respectively. Both holes also indicate the potential for additional oxide resource expansion to the south and southeast (Figure 2).

Drill holes QM-321 and QM-322 were drilled on the south/southeastern edge of the current oxide resource. Both drill holes intersected near surface oxide mineralization; QM-321 intersected 13.7 m @ 0.17% copper and QM-322 intersected 31.1 m @ 0.11% Cu. Both drill holes also indicate the potential for an additional oxide resource to the south. In addition, QM-322 was collared on a legacy MacArthur sub-grade stockpile, from which 12.3 m @ 0.13% copper was identified. The MacArthur sub-grade stockpile has not previously been sampled but based on these results, the Company may consider evaluating it for additional resource potential.

It is expected that the above results could increase the resource (Figure 2) and upgrade a portion of the current resource from inferred to measured/indicated status. The MacArthur resource estimate is in the process of being updated by Independent Mining Consultants (IMC); it is expected to be completed before the end of 2021.

Two additional drill holes (QM-323 and QM-324) were drilled to explore for additional oxide resource farther east and infill from previous oxide intercepts in this area. Each drill hole identified short, scattered oxide intercepts, and identified additional chalcocite and chalcopyrite mineralization. QM-323 includes 24.4 m @ 0.20% copper in the form of chalcopyrite and QM-324 includes 9.8 m @ 0.39% copper in the form of chalcocite and chalcopyrite. Please see Table 1 for additional intercepts. The potential for additional drilling in this area is under further evaluation.

Drill holes QM-319 and QM-320 were drilled to depths of 243.8 m and 362.3 m, respectively, to test under-drilled induced polarization geophysical anomalies. Both drill holes intersected zones of primary mineralization, occurring as wispy quartz-sericite-biotite-sulfide veinlets/vein haloes, which are commonly associated with porphyry-style mineralization in the Yerington District. These two drill holes provide important guidance for primary sulfide drilling in future programs.

|

TABLE 1. SIGNIFICANT INTERCEPTS |

||||||

|

Drill Hole |

From |

To |

Interval |

Interval |

% |

Mineralization |

|

HOLE QM-319 |

136 |

171.5 |

35.5 |

10.8 |

0.14 |

oxide |

|

221 |

269 |

48 |

14.6 |

0.13 |

chalcocite |

|

|

HOLE QM-320 |

62 |

115 |

53 |

16.2 |

0.17 |

oxide |

|

203.5 |

241 |

37.5 |

11.4 |

0.29 |

oxide & chalcocite |

|

|

272 |

378.5 |

106.5 |

32.5 |

0.58 |

oxide & chalcocite |

|

|

includes |

301 |

375 |

74 |

22.6 |

0.70 |

oxide & chalcocite |

|

955 |

1027 |

72 |

21.9 |

0.11 |

chalcopyrite |

|

|

HOLE QM-321 |

50 |

95 |

45 |

13.7 |

0.17 |

oxide |

|

135.5 |

166.5 |

31 |

9.4 |

0.19 |

oxide |

|

|

HOLE QM-322 |

11.5 |

40.5 |

29 |

8.8 |

0.13 |

MacArthur dump oxide |

|

338 |

450 |

112 |

34.1 |

0.11 |

oxide |

|

|

HOLE QM-323 |

255 |

272.6 |

17.6 |

5.4 |

0.32 |

chalcopyrite |

|

332.5 |

343.5 |

11 |

3.4 |

0.24 |

chalcopyrite |

|

|

353.5 |

376 |

22.5 |

6.9 |

0.11 |

chalcopyrite |

|

|

399 |

479 |

80 |

24.4 |

0.20 |

chalcopyrite |

|

|

HOLE QM-324 |

218 |

250 |

32 |

9.8 |

0.39 |

chalcocite & chalcopyrite |

|

264.5 |

275 |

10.5 |

3.2 |

0.20 |

chalcocite |

|

|

HOLE QM-326 |

17 |

39 |

22 |

6.7 |

0.27 |

oxide |

|

159 |

190.5 |

31.5 |

9.6 |

0.11 |

oxide |

|

|

312 |

327.5 |

15.5 |

4.7 |

0.19 |

chalcopyrite |

|

|

364 |

375 |

11 |

3.4 |

0.19 |

chalcopyrite |

|

|

HOLE QM-327 |

18.5 |

42.5 |

24 |

7.3 |

0.70 |

oxide |

|

96 |

128.5 |

32.5 |

9.9 |

0.13 |

oxide |

|

|

234.5 |

260 |

25.5 |

7.8 |

0.22 |

oxide |

|

|

HOLE QM-328 |

194 |

271 |

77 |

23.5 |

0.44 |

chalcocite |

*Drill intercepts are based on actual core lengths and may not reflect the true width of mineralization

Figure 1, Plan Map

To view an enhanced version of Figure 1, please visit:

https://orders.newsfilecorp.com/files/1020/98721_Figure%201%20Plan%20Map.jpg

Figure 2, Section 1

To view an enhanced version of Figure 2, please visit:

https://orders.newsfilecorp.com/files/1020/98721_Figure%202%20Section1.jpg

Quality Assurance and Control

All drilling described is from core, contracted to National EWP, Elko, Nevada. Core samples were either sawed or split by SPS personnel in Yerington, Nevada and shipped to Skyline Assayers and Laboratories in Tucson, Arizona for sample preparation. Copper analyses were assayed using their "SEA-Cu" (total copper) "SEACuSEQ" (sequential copper leach) procedure with a 50 ppm detection limit. Commercially prepared standards and blanks are inserted by SPS at 50-foot intervals to insure precision of results as a quality control measure. SPS has a chain of custody program to ensure sample security during all stages of sample collection, cutting, shipping, and storage.

Technical information in this news release was approved by Thomas Patton, Chairman to the Company and a qualified person as defined in NI 43-101.

About Quaterra Resources Inc.

Quaterra Resources Inc. is a copper-gold exploration company focused on projects with the potential to host large-scale mineral deposits attractive to major mining companies. It is advancing its Yerington copper project in the historic Yerington Copper District, Nevada and continues to investigate opportunities to acquire prospects in North America on reasonable terms and the partnerships with which to advance them.

On behalf of the Board of Directors,

Stephen Goodman,

President, Quaterra Resources Inc.

For more information please contact:

Karen Robertson

Corporate Communications

778-898-0057

Email: info@quaterra.com

Website: www.quaterra.com

Disclosure note:

Some statements in this news release are forward-looking statements under applicable United States and Canadian laws. These statements are subject to risks and uncertainties which may cause results to differ materially from those expressed in the forward-looking statements. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date thereof. The Company does not undertake to update any forward-looking statement that may be made from time to time except in accordance with applicable securities laws.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/98721

Shares Outstanding: 277,847,367

Trading Symbols: TSX: GGD

OTCQX: GLGDF

HALIFAX, NS, Oct. 6, 2021 /PRNewswire/ – GoGold Resources Inc. (TSX: GGD) (OTCQX: GLGDF) ("GoGold", "the Company") is pleased to report production for the year ending September 30, 2021 of 2,270,073 silver equivalent ounces ("AgEq"), consisting of 1,138,358 silver ounces, 13,447 gold ounces, and 470 tonnes of copper. Quarterly production at Parral was 526,044 silver equivalent ounces, consisting of 221,202 silver ounces, 3,437 gold ounces, and a record 138 tonnes of copper.

"Parral in 2021 proved to be a very stable operation, producing 2.3 million silver equivalent ounces similar to the prior year, and generated in excess of $US 22 million in free cash flow over the year," said Brad Langille, President and CEO. "We believe that the reinvestment of this free cash flow into the Los Ricos project is generating exceptional value growth for our shareholders."

Table 1: Quarterly Production Summary

|

Quarter Ended |

Jun 2020 |

Sep 2020 |

Dec 2020 |

Mar 2021 |

Jun 2021 |

Sep 2021 |

|

Silver Production (oz) |

270,044 |

300,740 |

298,591 |

302,933 |

315,632 |

221,202 |

|

Gold Production (oz) |

1,914 |

3,414 |

3,632 |

3,208 |

3,170 |

3,437 |

|

Copper Production (tonnes) |

104 |

128 |

125 |

86 |

120 |

138 |

|

Silver Equivalent Production (oz)1 |

504,444 |

605,287 |

614,149 |

551,207 |

575,302 |

526,044 |

|

1. |

"Silver equivalent production" include gold ounces and copper tons produced and converted to a silver equivalent based on a ratio of the average market metal price for each period. The gold:silver ratio for each of the periods presented was: Jun 2020 – 105, Sep 2020 – 79, Dec 2020 – 76, Mar 2021 – 69, Jun 2021 – 68, Sep 2021 – 73. The copper:silver ratios were: Mar 2020 – 340, June 2020 – 326, Sep 2020 – 274, Dec 2020 – 305, Mar 2021 – 320, June 2021 – 369, Sep 2021 – 383. |

Table 2: Annual Production Summary

|

Quarter Ended |

Sep 2019 |

Sep 2020 |

Sep 2021 |

|

Silver Production (oz) |

1,059,438 |

1,315,661 |

1,138,358 |

|

Gold Production (oz) |

9,149 |

10,089 |

13,447 |

|

Copper Production (tonnes) |

– |

260 |

470 |

|

Silver Equivalent Production (oz)1 |

1,847,835 |

2,295,416 |

2,270,073 |

|

1. |

"Silver equivalent production" include gold ounces and copper tons produced and converted to a silver equivalent based on a ratio of the average market metal price for each period. The gold:silver ratio for each of the periods presented was: Sep 2019 – 86, Sep 2020 – 89, Sep 2021 – 72. The copper:silver ratio for the periods presented was: Sep 2020 – 302, Sep 2021 – 348. |

Mr. Robert Harris, P.Eng. is the qualified person as defined by National Instrument 43-101 and is responsible for the technical information of this release.

About GoGold Resources

GoGold Resources (TSX: GGD) is a Canadian-based silver and gold producer focused on operating, developing, exploring and acquiring high quality projects in Mexico. The Company operates the Parral Tailings mine in the state of Chihuahua and has the Los Ricos South and Los Ricos North exploration projects in the state of Jalisco. Headquartered in Halifax, NS, GoGold is building a portfolio of low cost, high margin projects. For more information visit gogoldresources.com.

CAUTIONARY STATEMENT:

The securities described herein have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the "U.S. Securities Act"), or any state securities laws, and may not be offered or sold within the United States or to, or for the benefit of, U.S. persons (as defined in Regulation S under the U.S. Securities Act) except in compliance with the registration requirements of the U.S. Securities Act and applicable state securities laws or pursuant to exemptions therefrom. This release does not constitute an offer to sell or a solicitation of an offer to buy of any of GoGold's securities in the United States.

This news release may contain "forward-looking information" as defined in applicable Canadian securities legislation. All statements other than statements of historical fact, included in this release, including, without limitation, statements regarding production and cash flows of the Parral tailings mine, the ability of GoGold to self fund its ongoing exploration and administrative costs, future operating margins, future production and processing, and future plans and objectives of GoGold, constitute forward looking information that involve various risks and uncertainties. Forward-looking information is based on a number of factors and assumptions which have been used to develop such information but which may prove to be incorrect, including, but not limited to, assumptions in connection with the continuance of GoGold and its subsidiaries as a going concern, general economic and market conditions, mineral prices, the accuracy of mineral resource estimates, and the performance of the Parral project. There can be no assurance that such information will prove to be accurate and actual results and future events could differ materially from those anticipated in such forward-looking information.

Important factors that could cause actual results to differ materially from GoGold's expectations include exploration and development risks associated with GoGold's projects, the failure to establish estimated mineral resources or mineral reserves, volatility of commodity prices, variations of recovery rates, and global economic conditions. For additional information with respect to risk factors applicable to GoGold, reference should be made to GoGold's continuous disclosure materials filed from time to time with securities regulators, including, but not limited to, GoGold's Annual Information Form. The forward-looking information contained in this release is made as of the date of this release.

View original content:https://www.prnewswire.com/news-releases/parral-reports-annual-production-of-2-3m-ageq-oz-and-quarterly-production-of-526k-ageq-oz-301393880.html

SOURCE GoGold Resources Inc.

TORONTO, October 06, 2021–(BUSINESS WIRE)–Aquila Resources Inc. (TSX: AQA, OTCQB: AQARF) ("Aquila" or the "Company") is pleased to announce that it has entered into a definitive arrangement agreement (the "Arrangement Agreement") with Gold Resource Corporation ("GORO") (NYSE American: GORO) providing for the acquisition by GORO of all the issued and outstanding common shares of Aquila by way of a plan of arrangement under the Business Corporations Act (Ontario) (the "Transaction").

As announced by Aquila on September 7, 2021, pursuant to the Transaction GORO will, through a wholly-owned subsidiary, acquire all the issued and outstanding Aquila shares for 0.0399 of a GORO share per Aquila share (the "Exchange Ratio"). Based upon the 20-day volume-weighted average price ("VWAP") of GORO’s shares on the NYSE American stock exchange on September 3, 2021, being the last trading day prior to the date of the announcement of the Transaction, the Exchange Ratio represents a 29% premium to the 20-day VWAP of Aquila’s shares on the Toronto Stock Exchange as of such date.

Upon closing of the Transaction, the existing GORO and Aquila shareholders will own approximately 85.1% and 14.9%, respectively, of the combined company on a fully diluted basis.

Barry Hildred, Executive Chair of Aquila, commented, "We believe strongly that the Transaction outlined in the Arrangement Agreement provides significant benefits to Aquila shareholders. GORO has a strong balance sheet, it owns a consistently profitable mine in the Americas, and it has a highly accomplished technical and operating team. As such, this Transaction materially de-risks the financing and development of the Back Forty Project for the benefit of our stakeholders."

Guy Le Bel, President & CEO of Aquila, added, "The new Gold Resource Corporation will be a multi-jurisdictional, diversified precious and base metal producer with an attractive growth profile underpinned by the Back Forty Project. We look forward to closing the Transaction in short order."

Strategic Rationale for the Transaction

As previously announced on September 7, 2021, the benefits of the Transaction to GORO and Aquila shareholders include the following:

-

Enhanced Market Presence and Re-Rating Potential. GORO currently benefits from inclusion in the VanEck Junior Gold Miners ETF (the "GDXJ") and from an average daily trading volume of approximately 1 million shares, trailing three months. The Transaction is intended to result in the Back Forty Project being placed into production on a more accelerated basis, funded by cash flow generation, thus elevating the combined company to intermediate producer status. Following the completion of the Transaction, GORO is expected to continue to be included in the GDXJ and to benefit from an enhanced capital markets profile in the United States and Canada, as well as increased trading liquidity and broadened appeal to global index, resource, and generalist investors. This offers the potential for a re-rating to a multiple more in line with other intermediate gold producers.

-

Enhanced Project and Jurisdictional Diversification. Each of GORO and Aquila is currently a single-asset, single-jurisdiction company. Through the Transaction, GORO and Aquila shareholders will have the opportunity to participate in the ongoing growth of a multi-jurisdictional, diversified precious and base metal producer with exposure to gold, silver, zinc, copper and lead through GORO’s producing Don David Gold Mine in Oaxaca, Mexico and Aquila’s Back Forty Project in Menominee County, Michigan.

-

Growth Profile and Financial Strength of Combined Company. The combined company is expected to benefit from a peer leading growth profile, a robust balance sheet with no debt and cash of US$30.2 million at June 30, 2021, free cash flow generation from its Don David Gold Mine and the synergies that generally accrue from scale in the areas of general and administrative expenses, from less duplication of salaries, wages and other public company expenses, improved concentrate sales and marketing and supply chain efficiencies.

-

Materially De-Risks the Financing and Development of the Back Forty Project for Aquila Shareholders. Benefitting from the free cash flow generated by the Don David Gold Mine, Aquila shareholders will not be diluted by a near-term equity financing that would otherwise be required to advance the Back Forty Project through the final stages of permitting and engineering. GORO is supportive of Aquila’s project development plans including continuing working towards an optimized Feasibility Study. The combined Company’s position of financial strength is also expected to result in an improved ability to access required additional financing to fund the Back Forty Project’s construction capital expenditures.

-

All-Stock Transaction Enables Aquila Shareholders to Maintain Upside Exposure. Through their ownership in the combined company, Aquila shareholders will maintain exposure to the value that is expected to be unlocked as the Back Forty Project is advanced towards construction and production. Despite being a proven gold producer, GORO currently trades at only approximately 2.5 times free cash flow from operations. Aquila shareholders will participate in the anticipated re-rating of GORO from a one mine company in Mexico to a two-mine company with jurisdictional diversification.

-

Experienced Management Team. The combined company will benefit from GORO’s and Aquila’s technical and operational teams’ expertise in polymetallic open pit and underground mines. The GORO executive team has a demonstrated record of success in developing and operating mining projects in the Americas.

-

Demonstrated Consistent Dividend History. Post-Transaction, GORO intends to continue to pay dividends in accordance with its past practice. GORO has made consistent dividend payments to its investors for more than ten years.

Transaction Summary

The Transaction will require the approval of (i) 66⅔ percent of the votes cast by Aquila shareholders and (ii) a simple majority of the votes cast by the minority shareholders (excluding shareholders whose votes are required to be excluded pursuant to Multilateral Instrument 61 – 101) at a special meeting of shareholders (the "Aquila Shareholder Meeting"). The Aquila Shareholder Meeting is scheduled to be held on November 17, 2021. The Transaction is also subject to approval by the Ontario Superior Court of Justice (Commercial List) and applicable stock exchange approvals. The Transaction does not require the approval of GORO’s shareholders.

In addition to shareholder, court and regulatory approvals, the Transaction is also subject to the satisfaction of certain other closing conditions that are customary for a transaction of this nature, and each of GORO and Aquila has provided appropriate interim period covenants regarding the operation of its business in the ordinary course. The Arrangement Agreement includes customary deal protection provisions pursuant to which Aquila has agreed not to solicit any other acquisition proposal (subject to customary fiduciary out rights), has agreed to grant GORO the right to match any superior proposal, and will pay a termination fee of US$1,000,000 to GORO if the Arrangement Agreement is terminated in certain circumstances.

Details of the Transaction and the Arrangement Agreement will be set out in the management information circular to be prepared and mailed to Aquila shareholders in connection with the Aquila Shareholder Meeting.

Subject to all conditions precedent to completion of the Transaction being met, the Transaction is expected to close in late November 2021. In connection with the closing of the Transaction, Aquila will apply to have its shares delisted from the Toronto Stock Exchange.

Support for the Transaction from Key Aquila Stakeholders

Each of Orion Mine Finance and Hudbay Minerals Inc., which hold 28.3% and 10.4%, respectively, of the issued and outstanding Aquila shares, has entered into a voting support agreement with GORO pursuant to which they have agreed to vote their Aquila shares in favour of the Transaction. In addition, all of the directors and officers of Aquila holding approximately 1.9% of the issued and outstanding Aquila shares in aggregate have also executed a voting support agreement.

Osisko Bermuda Limited, which is a wholly-owned subsidiary of Osisko Gold Royalties Ltd, and a party to gold and silver stream agreements with Aquila relating to the Back Forty Project, has also reiterated that it considers GORO to be an approved purchaser under those agreements, and that it is supportive of the Transaction.

Board Approvals

The Arrangement Agreement has been unanimously approved by the boards of directors of both GORO and Aquila. The Aquila board’s approval of the Arrangement Agreement was based in part on the unanimous recommendation of a special committee of independent directors of Aquila which was appointed to consider the Transaction. The board of Aquila has received an opinion from PI Financial Corp. that based upon and subject to the assumptions, limitations, and qualifications set forth therein, the consideration to be received by Aquila shareholders pursuant to the Transaction is fair, from a financial point of view, to Aquila shareholders.

Advisors

Goodmans LLP is Aquila’s Canadian legal advisor and Scotiabank and PI Financial Corp. are Aquila’s financial advisors.

ABOUT AQUILA

Aquila Resources Inc. (TSX: AQA, OTCQB: AQARF) is a development‐stage company focused on high grade polymetallic projects in the Upper Midwest, USA. Aquila’s experienced management team is currently advancing pre-construction activities for its flagship 100%‐owned gold and zinc‐rich Back Forty Project in Michigan.

The Back Forty Project is a volcanogenic massive sulfide deposit with open pit and underground potential located along the mineral‐rich Penokean Volcanic Belt in Michigan’s Upper Peninsula. Back Forty contains approximately 1.1 million ounces of gold and 1.2 billion pounds of zinc in the Measured & Indicated Mineral Resource classifications, with additional exploration upside. An optimized Feasibility Study for the Project is underway.

Additional disclosure of Aquila’s financial statements, technical reports, material change reports, news releases and other information can be obtained at www.aquilaresources.com or on SEDAR at www.sedar.com.

ABOUT GOLD RESOURCE CORPORATION