Vancouver, British Columbia–(Newsfile Corp. – October 4, 2021) – Philippine Metals Inc. (TSXV: PHI) (the "Company") announces that a total of 150,000 incentive stock options have been granted to an independent director of the Company pursuant to the Company's stock option plan. The options have an effective grant date of September 29, 2021 and are exercisable on or before July 7, 2022 at a price of $0.075 per share.

ON BEHALF OF THE BOARD

"Craig T. Lindsay"

Chief Executive Officer

For additional information, please contact:

Craig Lindsay

Tel: (604) 218-0550

Email: craig@agcap.ca

Neither TSX Venture Exchange nor its Regulation Services Provider (as defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/98535

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. However, after investigating Sociedad Química y Minera de Chile (NYSE:SQM), we don't think it's current trends fit the mold of a multi-bagger.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Sociedad Química y Minera de Chile is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets – Current Liabilities)

0.084 = US$456m ÷ (US$6.0b – US$581m) (Based on the trailing twelve months to June 2021).

Therefore, Sociedad Química y Minera de Chile has an ROCE of 8.4%. In absolute terms, that's a low return but it's around the Chemicals industry average of 9.8%.

View our latest analysis for Sociedad Química y Minera de Chile

Above you can see how the current ROCE for Sociedad Química y Minera de Chile compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Sociedad Química y Minera de Chile.

What Does the ROCE Trend For Sociedad Química y Minera de Chile Tell Us?

In terms of Sociedad Química y Minera de Chile's historical ROCE movements, the trend isn't fantastic. To be more specific, ROCE has fallen from 11% over the last five years. However, given capital employed and revenue have both increased it appears that the business is currently pursuing growth, at the consequence of short term returns. And if the increased capital generates additional returns, the business, and thus shareholders, will benefit in the long run.

The Bottom Line On Sociedad Química y Minera de Chile's ROCE

In summary, despite lower returns in the short term, we're encouraged to see that Sociedad Química y Minera de Chile is reinvesting for growth and has higher sales as a result. And the stock has done incredibly well with a 127% return over the last five years, so long term investors are no doubt ecstatic with that result. So should these growth trends continue, we'd be optimistic on the stock going forward.

If you want to know some of the risks facing Sociedad Química y Minera de Chile we've found 2 warning signs (1 can't be ignored!) that you should be aware of before investing here.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

FRANKLIN, Ind., Oct. 04, 2021 (GLOBE NEWSWIRE) — IBC Advanced Alloys Corp. (“IBC” or the “Company”) (TSX-V: IB; OTCQB: IAALF) is pleased to announce it has entered into a new master lease agreement (the “Lease”) among Utica Leaseco LLC and Utica Equipment Finance, LLC (collectively, “Utica”) and certain of the Company’s U.S. subsidiaries (the “Subsidiaries”) in support of the Company’s ongoing expansion and consolidation of its Copper Alloys production facility in Franklin, Indiana.

“This equipment leasing arrangement allows us access to capital necessary to continue to execute on our expansion and consolidation of the Copper Alloys division’s state-of-the-art foundry facility at our North American headquarters in Franklin, Indiana,” said Mark A. Smith, CEO and Chairman of IBC. “Construction of the new facility is well underway now, and we look forward to completing this effort and achieving the cost savings and expanded production capacity it is expected to provide.”

Pursuant to the Lease, the Subsidiaries will grant a security interest in certain equipment located on the Lessees’ premises in exchange for US$900,000 in connection with a capital lease facility for a four-year term. IBC intends to use the proceeds of the Lease to advance the Copper Alloys consolidation and expansion and for working capital purposes.

The Subsidiaries will make lease payments in 51 monthly installments of approximately US$24,389.80, with monthly lease payments increasing by 1.0% for every 0.25% increase to the prime rate of Comerica Bank.

Pursuant to the terms of the Lease, the Subsidiaries will pay aggregate fees and expenses consisting of an approximately US$18,000 origination fee + US$43,200 for legal, appraisal, and title expenses at close, and an annual lease administration fee of US$5,000. The Lease is also subject to an early termination fee ranging from 5%-1% of the total funding amount, which decreases over the term of the Lease. The Lease is further subject to customary terms for similar lease arrangements in the United States manufacturing sector.

For more information on IBC and its innovative alloy products, go here.

On Behalf of the Board of Directors:

"Mark Smith”

Mark Smith P.E., Esq. , Chairman

Contact:

Mark A. Smith, Chairman

Jim Sims, Director of Investor and Public Relations

+1 (303) 503-6203

Email: jsims@policycom.com

Website: www.ibcadvancedalloys.com

@IBCAdvanced $IB $IAALF #Beryllium #Beralcast

About IBC Advanced Alloys Corp.

IBC is a leading beryllium and copper advanced alloys company serving a variety of industries such as defense, aerospace, automotive, telecommunications, precision manufacturing, and others. IBC's Copper Alloys Division manufactures and distributes a variety of copper alloys as castings and forgings, including beryllium copper, chrome copper, and aluminum bronze. IBC's Engineered Materials Division makes the Beralcast® family of alloys, which can be precision cast and are used in an increasing number of defense, aerospace, and other systems, including the F-35 Joint Strike Fighter. IBC has production facilities in Indiana, Massachusetts, Pennsylvania, and Missouri. The Company's common shares are traded on the TSX Venture Exchange under the symbol "IB" and the OTCQB under the symbol "IAALF".

Cautionary Statements

The TSX Venture Exchange has not reviewed and does not accept responsibility for the adequacy of this news release. Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Certain information contained in this news release may be forward-looking information or forward-looking statements as defined under applicable securities laws. Forward-looking information and forward-looking statements are often, but not always identified by the use of words such as "expect", "anticipate", "believe", "foresee", "could", "estimate", "goal", "intend", "plan", "seek", "will", "may" and "should" and similar expressions or words suggesting future outcomes. This news release includes forward-looking information and statements pertaining to, among other things, the use of proceeds of the Lease. Forward-looking statements involve substantial known and unknown risks and uncertainties, certain of which are beyond the Company's control including: the impact of general economic conditions in the areas in which the Company or its customers operate, including the semiconductor manufacturing and oil and gas industries, risks associated with manufacturing activities, changes in laws and regulations including the adoption of new environmental laws and regulations and changes in how they are interpreted and enforced, increased competition, the lack of availability of qualified personnel or management, limited availability of raw materials, fluctuations in commodity prices, foreign exchange or interest rates, stock market volatility and obtaining required approvals of regulatory authorities. As a result of these risks and uncertainties, the Company's future results, performance or achievements could differ materially from those expressed in these forward-looking statements. All statements included in this press release that address activities, events or developments that the Company expects, believes or anticipates will or may occur in the future are forward-looking statements. These statements are based on assumptions made by the Company based on its experience, perception of historical trends, current conditions, expected future developments and other factors it believes are appropriate in the circumstances.

Please see “Risks Factors” in our Annual Information Form available under the Company’s profile at www.sedar.com, for information on the risks and uncertainties associated with our business. Readers should not place undue reliance on forward-looking information and statements, which speak only as of the date made. The forward-looking information and statements contained in this release represent our expectations as of the date of this release. We disclaim any intention or obligation or undertaking to update or revise any forward-looking information or statements whether as a result of new information, future events or otherwise, except as required under applicable securities laws.

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

Given this risk, we thought we'd take a look at whether Iron Road (ASX:IRD) shareholders should be worried about its cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

View our latest analysis for Iron Road

How Long Is Iron Road's Cash Runway?

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. In June 2021, Iron Road had AU$4.8m in cash, and was debt-free. In the last year, its cash burn was AU$3.3m. Therefore, from June 2021 it had roughly 18 months of cash runway. That's not too bad, but it's fair to say the end of the cash runway is in sight, unless cash burn reduces drastically. Depicted below, you can see how its cash holdings have changed over time.

How Is Iron Road's Cash Burn Changing Over Time?

Although Iron Road reported revenue of AU$50k last year, it didn't actually have any revenue from operations. That means we consider it a pre-revenue business, and we will focus our growth analysis on cash burn, for now. Over the last year its cash burn actually increased by 39%, which suggests that management are increasing investment in future growth, but not too quickly. That's not necessarily a bad thing, but investors should be mindful of the fact that will shorten the cash runway. Iron Road makes us a little nervous due to its lack of substantial operating revenue. We prefer most of the stocks on this list of stocks that analysts expect to grow.

How Easily Can Iron Road Raise Cash?

While Iron Road does have a solid cash runway, its cash burn trajectory may have some shareholders thinking ahead to when the company may need to raise more cash. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of AU$139m, Iron Road's AU$3.3m in cash burn equates to about 2.3% of its market value. So it could almost certainly just borrow a little to fund another year's growth, or else easily raise the cash by issuing a few shares.

Is Iron Road's Cash Burn A Worry?

Even though its increasing cash burn makes us a little nervous, we are compelled to mention that we thought Iron Road's cash burn relative to its market cap was relatively promising. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Iron Road's situation. On another note, Iron Road has 3 warning signs (and 1 which is significant) we think you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

Looking at Astro Resources NL's (ASX:ARO ) insider transactions over the last year, we can see that insiders were net buyers. That is, there were more number of shares purchased by insiders than there were sold.

While insider transactions are not the most important thing when it comes to long-term investing, logic dictates you should pay some attention to whether insiders are buying or selling shares.

Check out our latest analysis for Astro Resources

The Last 12 Months Of Insider Transactions At Astro Resources

In the last twelve months, the biggest single purchase by an insider was when Non-Executive Chairman Jacob Khouri bought AU$103k worth of shares at a price of AU$0.0052 per share. That means that even when the share price was higher than AU$0.005 (the recent price), an insider wanted to purchase shares. While their view may have changed since the purchase was made, this does at least suggest they have had confidence in the company's future. We always take careful note of the price insiders pay when purchasing shares. As a general rule, we feel more positive about a stock when an insider has bought shares at above current prices, because that suggests they viewed the stock as good value, even at a higher price. Jacob Khouri was the only individual insider to buy during the last year.

You can see the insider transactions (by companies and individuals) over the last year depicted in the chart below. If you want to know exactly who sold, for how much, and when, simply click on the graph below!

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Does Astro Resources Boast High Insider Ownership?

Looking at the total insider shareholdings in a company can help to inform your view of whether they are well aligned with common shareholders. A high insider ownership often makes company leadership more mindful of shareholder interests. It appears that Astro Resources insiders own 33% of the company, worth about AU$6.3m. This level of insider ownership is good but just short of being particularly stand-out. It certainly does suggest a reasonable degree of alignment.

So What Do The Astro Resources Insider Transactions Indicate?

There haven't been any insider transactions in the last three months — that doesn't mean much. But insiders have shown more of an appetite for the stock, over the last year. Insiders do have a stake in Astro Resources and their transactions don't cause us concern. So these insider transactions can help us build a thesis about the stock, but it's also worthwhile knowing the risks facing this company. To help with this, we've discovered 4 warning signs (3 are a bit unpleasant!) that you ought to be aware of before buying any shares in Astro Resources.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions, but not derivative transactions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

MELBOURNE, October 02, 2021–(BUSINESS WIRE)–Rio Tinto is supporting iron ore rail car manufacturing in Western Australia with a commitment to use local suppliers to build ore rail cars for its Pilbara mining operations.

A tender will soon be released to the local market for an initial purchase of 50 ore rail cars, followed by an ongoing commitment of 10 ore cars a year for the next five years.

The tender will be released through the Rio Tinto Buy Local portal, a resource dedicated to making local suppliers aware of opportunities to partner with Rio Tinto and be part of our supply chain.

Western Australia has been an important part of Rio Tinto’s history for more than 50 years as the company built a world-class iron ore business. In 2020, the company spent AUD$7.5 billion with more than 2,000 local businesses based in Western Australia.

Rio Tinto is also part of the WA Government’s iron ore rail car action group, launched as part of the WA Recovery Plan to develop a competitive iron ore rail car manufacturing industry in Western Australia.

Rio Tinto’s commitment to bring ore rail car manufacturing back to WA supports the action group’s vision to develop WA’s ore rail car manufacturing capability and support the State’s economic recovery.

Rio Tinto Iron Ore chief executive Simon Trott said: "Building Rio Tinto’s ore rail cars here in WA will support local manufacturing and create jobs for West Australians.

"Rio Tinto is proud to lead the way in building iron ore rail cars in WA, in line with the vision of State Government’s iron ore rail car action group.

"I look forward to partnering with local businesses to support and grow the local manufacturing industry in WA.

"Ore cars are a critical part of our mining operations and building capacity to manufacture ore cars locally in WA will deliver significant benefits for Rio Tinto and the WA economy."

Premier Mark McGowan said: "This is a pleasing outcome and I commend Rio Tinto for taking the first step and committing to our local steel manufacturing industry which will support more jobs for Western Australians.

"Rio Tinto’s commitment is a positive result off the back of the State Government’s independent pre-feasibility study, which identified initiatives for the manufacture, refurbishment and maintenance of iron ore railcar wagons.

"This was about securing an ongoing pipeline of work for the long term manufacture of iron ore wagons and critical rail wagon parts, which will deliver jobs and economic benefit for the State into the future.

"Rio Tinto’s purchase of Western Australian made railcars that will be used right here in our State is something I encourage other iron ore companies operating in WA to get on board with and increase local content and local jobs."

riotinto.com

View source version on businesswire.com: https://www.businesswire.com/news/home/20211002005001/en/

Contacts

Please direct all enquiries to Media.enquiries@riotinto.com

Media Relations, Australia

Jonathan Rose

M +61 447 028 913

Matt Chambers

M +61 433 525 739

Jesse Riseborough

M +61 436 653 412

Jamie Macdonald

M +61 467 725 51

Rio Tinto plc

6 St James’s Square

London SW1Y 4AD

United Kingdom

T +44 20 7781 2000

Registered in England

No. 719885

Rio Tinto Limited

Level 7, 360 Collins Street

Melbourne 3000

Australia

T +61 3 9283 3333

Registered in Australia

ABN 96 004 458 404

Category: Pilbara

(Bloomberg) — The global energy crisis is intensifying, hammering the shares of companies that consume a lot of power and sending the stocks of those that produce it soaring.

Most Read from Bloomberg

-

An Unapologetic Old Boys’ Network Is Costing Australia Billions

-

Christmas at Risk as Supply Chain ‘Disaster’ Only Gets Worse

Economic recovery from the pandemic has boosted demand for gas and coal but their supplies have not been able to keep up. With the northern hemisphere winter on the horizon and China — the world’s biggest electricity user — ordering state-owned energy firms to secure supplies at all costs, investors are in a race to pick the winners and losers.

A key measure of international energy producers, led by names including Cabot Oil & Gas Corp. and ConocoPhillips, has rallied almost 10% over the past month. Utilities stocks have gone into reverse, wiping out this year’s gains, with materials companies joining them among the biggest laggards on the MSCI World Index.

“The energy crisis can exist for the next several years. I think a super cycle in energy has started and will continue for several years,” said Sumeet Rohra, a fund manager at Smartsun Capital Pte. in Singapore. “Energy stocks are very well poised to generate big returns.”

China’s factory sector contracted in September for the first time since the pandemic began, thanks to power cuts that have affected regions making up more than two-thirds of the nation’s gross domestic product. The energy crunch has also reportedly halted production at suppliers of global tech giants such as Apple Inc. and Tesla Inc.

Meanwhile, European inventories of natural gas are running low as economies come out of the pandemic lockdown and the White House has expressed concern about the jump in oil prices.

Here is a guide to how the crisis is playing out in equities market:

Energy Producers

Companies that produce gas, oil and coal are set to continue benefiting as winter approaches and demand rises.

Royal Dutch Shell Plc, TotalEnergies SE, Eni SpA, and BP Plc are among big European names that may rally further. In Asia, traders have their eyes on companies including Woodside Petroleum Ltd., Petronas Gas Bhd., Inpex Corp., Oil and Natural Gas Corp. and Reliance Industries Ltd.

“It is not just about a short term supply-demand imbalance,” said Gary Dugan, chief executive officer of the Global CIO Office. “The energy crunch is very concerning as it leads to the worst case scenario for markets — that of stagflation,” he said, referring to a situation in which economic growth stalls while inflation and unemployment rise.

If the current tightness in the gas market endures into next year, then Total could see 2022 earnings boosted by 18% and Eni by 12%, Goldman Sachs Group Inc. analysts including Lilia Peytavin wrote in a note last week.

Bloomberg Intelligence analyst Talon Custer said U.S. exporters of liquefied natural gas, such as Cheniere Energy Inc. and Sempra Energy, appear well positioned in an LNG market that should stay extremely tight through the winter.

Exxon Mobil Corp. said on Sept. 30 that elevated gas prices will boost its third quarter profit by about $700 million.

A three-year-high in oil prices also helps Exxon, and should keep others such as Schlumberger Ltd., ConocoPhillips and Halliburton Co. on the radar of traders.

In contrast, gas distributors such as China Gas Holdings Ltd., Hong Kong and China Gas Co., Kunlun Energy Co, and Indraprastha Gas Ltd. may face margin pressure if they are not allowed to pass on rising input costs.

Amid surging prices of coal, key stocks to watch are Arch Resources Inc. and Peabody Energy Corp. in the U.S., Glencore Plc. in Europe, and China Shenhua Energy Co., China Coal Energy Co., Adaro Energy Tbk, Whitehaven Coal Ltd. as well as Coal India Ltd. in Asia.

Materials & Metals

While rising power prices hurt all users, it is particularly acute for energy-intensive materials and metal companies.

In Asia, these stocks include Aluminum Corporation of China Ltd., Baoshan Iron & Steel Co., Angang Steel Co., China National Chemical Engineering Co. and Zhejiang Longsheng Group Co.

European construction material maker Sika AG also fits the mold, as does steelmaker ArcelorMittal and cement producer Holcim Ltd. In the U.S., steel producer Nucor Corp. and paint maker Sherwin-Williams Co. may be focus.

Bank of America Corp. analysts see input-cost headwinds for Indian cement makers such as UltraTech Cement, Shree Cement Ltd. and companies in the paint sector.

Power Utilities

Many government-backed electricity providers are likely to face margin pressure while those that are less regulated or independent have a better chance profiting from higher electricity prices.

Barclays Plc.’s analysts including Peter Crampton expect further strength in power prices to create winners in less heavily regulated northern Europe. They identified Electricite de France, Engie SA, Fortum Oyj and RWE AG. The analysts expect significant earnings-per-share upgrades, particularly for EDF, and raised their 2021 and 2022 estimates by 82% and 61%, respectively.

The most visible signs of stock market distress so far have been in southern Europe’s heavily regulated utilities. Iberdrola SA and Endesa SA shares are both trading at their lowest levels in more than last year.

In Asia, potential losers include Korea Electric Power Co., Tokyo Electric Power Co. and India’s NTPC Ltd. In the U.S., companies such as Southern Co., American Electric Power Co. and Duke Energy Corp. could face pressure.

Green Stocks

Higher energy prices and efforts to cut carbon emissions are also flowing through into the share prices of renewable power and nuclear stocks.

Bloomberg Intelligence’s Laurent Douillet sees large nuclear and hydro electricity companies as potential winners over those that rely on gas and coal.

READ: China’s Energy Crunch Sends Coal Shares Up, Renewable Firms Down

Key stocks to monitor are Europe’s Scatec ASA, Azelio AB and Orsted A/S, North America’s First Solar Inc. and SolarEdge Technologies Inc., and Asia’s LONGi Green Energy Co., Trina Solar Co., Sungrow Power Supply Co. and Adani Green Energy Ltd.

“There hasn’t been a confluence of so many factors happening at the same time in energy and commodity markets since at least the 1980s,” said Robert Ryan, chief commodity and energy strategist at BCA Research.

Most Read from Bloomberg Businessweek

©2021 Bloomberg L.P.

Vancouver, British Columbia–(Newsfile Corp. – October 1, 2021) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the "Company", or "EMX") is pleased to announce that it intends to carry out a private placement of up to 5,000,000 units at C$ 3.30 each for gross proceeds of up to C$ 16,500,000. Members of the Sprott Group have agreed to act as finders in connection with the sale of some of the units.

The units will consist of one common share of the Company and one-half of one transferable warrant. Each whole warrant will entitle the purchase for two years of one common share at C$ 4.00 in the first year and C$ 4.50 in the second year.

Eligible finders will be paid a 6.0% cash commission and issued that number of non-transferable compensation warrants equal to 6.0% of the number of units sold to investors introduced by them. Each compensation warrant will entitle the purchase for one year of one common share of the Company for C$ 3.50.

The placement is subject to stock exchange approval.

This news release does not constitute an offer to sell or a solicitation of an offer to buy any of the securities in the United States. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the "1933 Act"), or any U.S. state securities laws and may not be offered or sold within the "United States" or to "U.S. Persons" (as such terms are defined in Regulation S under the 1933 Act) unless registered under the 1933 Act and applicable U.S. state securities laws, or an exemption from such registration is available.

About EMX. EMX is a precious, base and battery metals royalty company. EMX's investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company's common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol EMX, as well as on the Frankfurt exchange under the symbol "6E9". Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole

President and Chief Executive Officer

Phone: (303) 979-6666

Dave@EMXroyalty.com

Scott Close

Director of Investor Relations

Phone: (303) 973-8585

SClose@EMXroyalty.com

Isabel Belger

Investor Relations (Europe)

Phone: +49 178 4909039

Ibelger@EMXroyalty.com

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain "forward-looking statements" that reflect the Company's current expectations and projections about its future results. These forward-looking statements may include statements regarding completion of the transaction, perceived merits of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as "estimate," "intend," "expect," "anticipate," "will", "believe", "potential", "upside" and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company's future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company's actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors. It is possible EMX may not complete the transaction, as a result of failure to fulfill conditions of closing, unavailability of financing or for other reasons EMX cannot anticipate at this time.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company's MD&A for the quarter ended June 30, 2021 and the year ended December 31, 2020 (the "MD&A"), and the most recently filed Revised Annual Information Form (the "AIF") for the year ended December 31, 2020, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC's EDGAR website at www.sec.gov.

Not for distribution to United States newswire services or for dissemination in the United States.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/98219

VANCOUVER, BC / ACCESSWIRE / October 1, 2021 / CMC Metals Ltd. (TSXV:CMB)(FSE:ZM5N)(OTC PINK:CMCZF); (the "Company") is pleased to announce that it has adopted an advance notice policy (the "Advance Notice Policy"), establishing a framework for advance notice of nominations of directors by shareholders of the Company.

The Advance Notice Policy, among other things, seeks to fix a deadline by which holders of record of common shares of the Company must submit director nominations to the Company prior to any annual or certain special meetings of shareholders and sets forth the information required to be provided by a nominee director that a shareholder must include in the notice to the Company for the notice to be in proper written form.

The Advance Notice Policy is intended to, among other things: (i) facilitate an orderly and efficient Annual General or Special Meeting process; (ii) ensure that shareholders receive adequate notice of director nominations and sufficient information regarding all director nominations; and (iii) allow shareholders to cast an informed vote after having been afforded reasonable time for consideration.

The following notice requirements will apply for all Annual General or Special Meetings of shareholders of the Company:

-

In the case of an annual meeting of shareholders, notice of a director nomination must be given to the Company not less than 30 nor more than 65 days prior to the date of the annual meeting of shareholders; provided, however, that in the event that the annual meeting of shareholders is called for a date that is less than 50 days after the date (the "Notice Date") on which the first public announcement of the date of the annual meeting was made, notice by the nominating shareholder may be made not later than the tenth (10th) day following the Notice Date.

-

In the case of a special meeting of shareholders (which is not also an annual meeting) called for the purpose of electing directors (whether or not called for other purposes), notice of a director nomination must be given to the Company no later than the fifteenth (15th) day following the day on which the first public announcement of the date of the special meeting of shareholders was made.

-

The Advance Notice Policy is effective immediately and will be placed before shareholders for ratification and approval at the Company's next annual general and special meeting of shareholders (scheduled for December 7, 2021). In the event that shareholders determine not to ratify the Advance Notice Policy by ordinary resolution, the Advance Notice Policy shall terminate and be void and of no further force and effect following the termination of the Meeting.

A copy of the Advance Notice Policy, in its entirety, is available under the Company's profile at www.sedar.com and included in www.cmcmetals.ca.

About CMC Metals.

CMC Metals Ltd. is a growth stage mineral exploration company focused on opportunities in Yukon, British Columbia and Newfoundland. Our silver-lead-zinc projects include Silver Hart, Blue Heaven and the Rancheria South Properties (Rancheria South, Silverknife and Amy). Our polymetallic projects with gold potential include Logjam, Bridal Veil and Terra Nova.

On behalf of the Board:

John Bossio

John Bossio,

Chairman CMC METALS LTD.

For Further Information and Investor Inquiries:

Kevin Brewer, P. Geo., MBA, B.Sc Hons, Dip. Eng

President, CEO and Director

Tel: (604) 670 0019

kbrewer80@hotmail.com

Suite 110-175 Victory Ship Way

North Vancouver, BC

V7L 0B2

To be added to CMC's news distribution list, please send an email to info@cmcmetals.ca. Also please visit our website at www.cmcmetals.ca for more up-to-date news and information on our projects.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

"This news release may contain certain statements that constitute "forward-looking information" within the meaning of applicable securities law, including without limitation, statements that address the timing and content of upcoming work programs, geological interpretations, receipt of property titles and exploitation activities and developments. In this release disclosure regarding the potential to undertake future work comprise forward looking statements. Forward-looking statements address future events and conditions and are necessarily based upon a number of estimates and assumptions. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks, including the ability of the Company to raise the funds necessary to fund its projects and, accordingly, may not occur as described herein or at all. Actual results may differ materially from those currently anticipated in such statements. Factors that could cause actual results to differ materially from those in forward looking statements include market prices, exploitation and exploration successes, the timing and receipt of government and regulatory approvals, and continued availability of capital and financing and general economic, market or business conditions. Readers are referred to the Company's filings with the Canadian securities regulators for information on these and other risk factors, available at www.sedar.com. Investors are cautioned that forward-looking statements are not guarantees of future performance or events and, accordingly are cautioned not to put undue reliance on forward-looking statements due to the inherent uncertainty of such statements. The forward-looking statements included in this news release are made as of the date hereof and the Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by applicable securities legislation."

SOURCE: CMC Metals Ltd.

View source version on accesswire.com:

https://www.accesswire.com/666369/CMC-Metals-Ltd-Adopts-Advanced-Notice-Policy

NOT FOR DISTRIBUTION IN OR INTO OR TO ANY PERSON LOCATED OR RESIDENT IN AUSTRALIA, JAPAN, SOUTH AFRICA OR ANY OTHER JURISDICTION OR TO ANY PERSON LOCATED OR RESIDENT IN ANY JURISDICTION IN WHICH SUCH DISTRIBUTION IS UNLAWFUL

ENDEAVOUR ANNOUNCES OFFERING OF $500 MILLION SENIOR NOTES DUE 2026

London, 1 October 2021 – Endeavour Mining plc (LSE:EDV, TSX:EDV, OTCQX:EDVMF) (the “Company”, together with its subsidiaries, the “Group”) announces the launch of an offering of fixed rate senior notes due 2026 (the “Notes”) as well as the entry into a new revolving credit facility.

The proceeds of the Notes will be used (i) to repay all amounts outstanding under the Group’s $370 million bridge term loan facility, which was used to retire higher cost debt facilities acquired upon the acquisition of Teranga Gold Corporation (the “Bridge Facility”), (ii) to repay the $130 million drawn under the Group’s existing revolving credit facility (the “Existing RCF”), and (iii) to pay fees and expenses in connection with the offering of the Notes.

The Company has entered into a $500 million revolving credit facility (with a 4-year tenor, which may increase in accordance with its terms up to an aggregate amount of $650 million) with borrowing availability in US dollars for the general corporate purposes of the Company and certain of its subsidiaries. This new revolving credit facility will replace the Bridge Facility and the Existing RCF, which will be cancelled upon completion of any Notes offering.

Effectiveness of the new revolving credit facility is conditioned upon the closing of any Notes offering.

ABOUT ENDEAVOUR MINING PLC

Endeavour is one of the world’s senior gold producers and the largest in West Africa, with operating assets across Senegal, Cote d’Ivoire and Burkina Faso and a strong portfolio of advanced development projects and exploration assets in the highly prospective Birimian Greenstone Belt across West Africa.

A member of the World Gold Council, Endeavour is committed to the principles of responsible mining and delivering sustainable value to its employees, stakeholders and the communities where it operates. Endeavour is listed on the London Stock Exchange and the Toronto Stock Exchange, under the symbol EDV.

For more information, please visit www.endeavourmining.com.

Neither the Toronto Stock Exchange nor the Investment Industry Regulatory Organization of Canada accepts responsibility for the adequacy or accuracy of this press release.

IMPORTANT INFORMATION

This announcement is for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to buy the Notes or the guarantees thereof (the “Guarantees”), nor shall it constitute an offer, solicitation or sale in any jurisdiction in which, or to any person to whom, such offer, solicitation or sale would be unlawful. The Notes and the Guarantees have not been and will not be registered under the U.S. Securities Act of 1933 or the securities laws of any other jurisdiction. Securities may not be offered in the United States absent registration or an exemption from registration. No action has been or will be taken in any jurisdiction in relation to the Notes or the Guarantees to permit a public offering of securities. There is no assurance that any Notes offering will be completed or, if completed, as to the terms on which it is completed.

The Notes and the Guarantees are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the European Economic Area (“EEA”). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU (as amended, “MiFID II”) or (ii) a customer within the meaning of Directive 2016/97/EU, as amended (the “Insurance Distribution Directive”), where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II. Consequently, no key information document required by Regulation (EU) No 1286/2014 (as amended, the “EU PRIIPs Regulation”) for offering or selling the Notes or the Guarantees or otherwise making them available to retail investors in the EEA has been prepared and therefore offering or selling the Notes or the Guarantees or otherwise making them available to any retail investor in the EEA may be unlawful under the EU PRIIPs Regulation.

The Notes and the Guarantees are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the United Kingdom (the “UK”). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (8) of Article 2 of Regulation (EU) 2017/565 as it forms part of domestic law in the UK by virtue of the European Union (Withdrawal) Act 2018, as amended (the “EUWA”) or (ii) a customer within the meaning of the provisions of the Financial Services and Markets Act 2000, as amended (the “FMSA”), and any rules or regulations made under the FSMA to implement the Insurance Distribution Directive, where that customer would not qualify as a professional client, as defined in point (8) of Article 2(1) of Regulation (EU) 600/2014 as it forms part of domestic law in the UK by virtue of the EUWA. Consequently, no key information document is required by Regulation (EU) 1286/2914 as it forms part of domestic law in the UK by virtue of the EUWA (the “UK PRIIPs Regulation”) for offering or selling the Notes or otherwise making them available to UK retail investors in the UK has been prepared and therefore offering or selling the notes or otherwise making them available to any UK retail investor in the UK may be unlawful under the UK PRIIPs Regulation.

MiFID II professionals / ECPs-only / No PRIIPs KID – Manufacturer target market (MiFID II product governance) is eligible counterparties and professional clients only (all distribution channels). No EU PRIIPs key information document (“KID”) has been prepared as not available to retail in the EEA.

UK MiFIR professionals / ECPs-only / No UK PRIIPs KID – Manufacturer target market (UK MiFIR product governance) is eligible counterparties and professional clients only (all distribution channels). No UK PRIIPs key information document (“KID”) has been prepared as not available to retail in the UK.

This announcement is being distributed to, and is directed at, only persons who (i) are outside the UK; (ii) are “qualified investors” within the meaning of Article 2 of Regulation (EU) 2017/1129 (the “Prospectus Regulation”) as it forms part of retained EU law in the UK as defined in the EUWA (iii) have professional experience in matters relating to investments falling within the definition of “investment professionals” in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”), or (iv) are persons who are high net worth bodies corporate, unincorporated associations and partnerships and the trustees of high value trusts, as described in Article 49(2)(a) to (d) of the Order or (iii) are persons to whom this communication may otherwise be lawfully communicated (all such persons together being referred to as “Relevant Persons”). The investments to which this announcement relates are available only to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such investments will be available only to or will be engaged in only with, Relevant Persons. Any person who is not a relevant person should not act or rely on this announcement or any of its contents. Persons distributing this announcement must satisfy themselves that it is lawful to do so.

In any EEA Member State this communication is only addressed to and is only directed at “qualified investors” in that Member State within the meaning of Article 2(e) of the Prospectus Regulation.

The distribution of this announcement in certain jurisdictions may be restricted by law and therefore persons in such jurisdictions into which they are released, published or distributed, should inform themselves about, and observe, such restrictions. Any failure to comply with these restrictions may constitute a violation of the laws of any such jurisdiction.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

This announcement contains “forward-looking statements” within the meaning of applicable securities laws. All statements, other than statements of historical fact, are “forward-looking statements”, including but not limited to, statements with respect to the Group’s intentions with regards to any offering of the Notes and the Guarantees. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “will”, “can”, “could”, “would” and similar expressions.

Forward-looking statements, while based on management’s reasonable estimates, projections and assumptions at the date the statements are made, are subject to risks and uncertainties that may cause actual results to be materially different from those expressed or implied by such forward-looking statement. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Please refer to the Group’s most recent Annual Information Form filed under its profile at www.sedar.com for further information respecting the risks affecting Endeavour and its business.

These forward-looking statements speak only as of the date of this announcement. Except as required by applicable law and regulation, the Company does not undertake any obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

CONTACT INFORMATION

|

Endeavour Mining |

Brunswick Group LLP in London Vincic Advisors in Toronto |

Attachment

Here are five stocks added to the Zacks Rank #5 (Strong Sell) List today:

Kirby Corporation KEX operates domestic tank barges. The Zacks Consensus Estimate for its current year earnings has been revised 4.8% downward over the last 30 days.

BHP Group BBL engages in the natural resources business. The Zacks Consensus Estimate for its current year earnings has been revised 22.9% downward over the last 30 days.

AB Electrolux ELUXY manufactures and sells household appliances. The Zacks Consensus Estimate for its current year earnings has been revised 4.3% downward over the last 30 days.

TDK Corporation TTDKY manufactures and sells electronic components. The Zacks Consensus Estimate for its current year earnings has been revised 34.1% downward over the last 30 days.

Weichai Power Co., Ltd. WEICY manufactures and sells diesel engines, automobiles, and other major automobile components. The Zacks Consensus Estimate for its current year earnings has been revised 8.3% downward over the last 30 days.

View the entire Zacks Rank #5 List.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Electrolux AB (ELUXY) : Free Stock Analysis Report

BHP Billiton PLC (BBL) : Free Stock Analysis Report

Weichai Power Co. (WEICY) : Free Stock Analysis Report

Kirby Corporation (KEX) : Free Stock Analysis Report

TDK Corp. (TTDKY) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

VANCOUVER, British Columbia, Oct. 01, 2021 (GLOBE NEWSWIRE) — Aton Resources Inc. (AAN: TSX-V) ("Aton" or the "Corporation") announces the following operations and corporate updates.

Operations Update

Aton signed a drilling contract with Energold Drilling Ltd. in June to complete a minimum of 4,250 metres of diamond drilling at the Corporation’s Abu Marawat Concession (see news release dated June 14, 2021). At the time of signing the contract it was expected that drilling would commence in September 2021. Due to export clearance and shipping delays caused by the COVID-19 pandemic, the scheduled delivery date of the drill rig to the port in Egypt is now October 9, 2021. As a result, Aton expects to commence drilling during the month of November 2021. A summary of the drill program is provided below.

The program will commence at Rodruin with 3,350 metres of drilling, with the objective of following up on the successful 2018 reverse circulation percussion drill program, as well as testing for the first time the high-grade veins sampled at surface on the North Ridge, which returned assays of up to 321 g/t Au (see news release dated February 6, 2018). Drilling will also further test and delineate the distribution of the near-surface oxide mineralisation identified on the South Ridge, which returned intercepts including 36m @ 12.47 g/t Au (see news release, dated October 1, 2018) and 20m @ 5.36 g/t Au (see news release, dated December 10, 2018). The program will also follow up on the deeper sulphide mineralisation which returned wide intersections including 61m @ 1.55 g/t Au, 8.9 g/t Ag and 0.86% Zn (see news release dated January 29, 2019).

The drilling program at Hamama will consist of 900 metres of drilling with the objective of delineating additional oxide and transitional resources at the Hamama East and Central areas, which have not been effectively drill tested to date. Channel sampling of surface trenches has indicated the potential for relatively high grade oxide mineralisation, and has returned intercepts including 84m @ 1.13 g/t Au, 49.7 g/t Ag and 7.29% Zn and 42.8m @ 1.28 g/t Au, 55.5 g/t Ag and 10.37% Zn (see news release dated May 3, 2018).

During the last six months the Corporation has completed all the necessary work required to commence the above noted drill program, including the acquisition of capital items, construction of a new camp at the Rodruin project, road construction and drill pad preparation.

Aton’s exploration team has also resumed field activities, continuing with the surface channel sampling program at Rodruin, and have also undertaken further sampling, mapping and ionic leach sampling at the Abu Gaharish prospect. Samples have been dispatched to the ALS Minerals for analysis, and results will be released when they become available.

Corporate Update

Due to other professional commitments, Mr. Bill Koutsouras has resigned from his position as Director and Interim CEO of the Corporation, effective immediately. Mr. Koutsouras will continue to be available to provide ongoing support to the Corporation in the future as an advisor.

Mr. Tonno Vahk will assume the role of Interim CEO, effective immediately and until such time as a permanent CEO is recruited by the Board of Directors. Mr. Vahk has been a director of Aton since 2017 and is a significant shareholder of the Corporation with his current shareholding (held indirectly in OU Hektik) representing 12.97% of the issued and outstanding shares of Aton.

|

About Aton Resources Inc. Aton Resources Inc. (AAN: TSX-V) is focused on its 100% owned Abu Marawat Concession (“Abu Marawat”), located in Egypt’s Arabian-Nubian Shield, approximately 200 km north of Centamin’s world-class Sukari gold mine. Aton has identified numerous gold and base metal exploration targets at Abu Marawat, including the Hamama deposit in the west, the Abu Marawat deposit in the northeast, and the advanced Rodruin exploration prospect in the south of the Concession. Two historic British gold mines are also located on the Concession at Sir Bakis and Semna. Aton has identified several distinct geological trends within Abu Marawat, which display potential for the development of a variety of styles of precious and base metal mineralisation. Abu Marawat is 447.7 km2 in size and is located in an area of excellent infrastructure; a four-lane highway, a 220kV power line, and a water pipeline are in close proximity, as are the international airports at Hurghada and Luxor. |

Qualified Person The technical information contained in this News Release was prepared by Javier Orduña BSc (hons), MSc, MCSM, DIC, MAIG, SEG(M), Exploration Manager of Aton Resources Inc. Mr. Orduña is a qualified person (QP) under National Instrument 43-101 Standards of Disclosure for Mineral Projects. For further information regarding Aton Resources Inc., please visit us at www.atonresources.com or contact: TONNO VAHK Interim CEO |

|

Note Regarding Forward-Looking Statements Some of the statements contained in this release are forward-looking statements. Since forward-looking statements address future events and conditions; by their very nature they involve inherent risks and uncertainties. Actual results in each case could differ materially from those currently anticipated in such statements. Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release. |

|

After a long slumber, bears have finally awakened. Their wrath is being felt across all risk assets, and we’re officially in the midst of the biggest correction in the S&P 500 for the year. Granted, we’re still only down 5% from the peak, but in as low a volatility environment as we’ve seen this year, that qualifies as the worst whack of 2021. And yet, despite the mayhem, I’m sharing three stocks to buy.

When the market backdrop gets as ugly as it is now, I get extremely selective on new trades. Only the best setups make the cut, and even then, I sometimes pass until the S&P 500 starts to show signs of bottoming.

Today’s trio all boast relative strength and uptrends that remain intact. What’s more, they all saw increasing momentum on the last advance, despite a sinking market.

InvestorPlace – Stock Market News, Stock Advice & Trading Tips

That’s the pitch. Here are the picks:

Let’s take a closer look at each chart to chronicle the recent muscle-flexing. Then, we’ll map out a path to profit.

Stocks to Buy: Cameco (CCJ)

Source: The thinkorswim® platform from TD Ameritrade

If you’re going to buy something while the sky is falling, it certainly helps if it doesn’t have a strong correlation to the stock market. Lately, shares of Canadian uranium producer, Cameco Corp, have been moving to the beat of their own drum. Sometimes CCJ stock moves with the S&P 500; sometimes it doesn’t. As a result of the mixed relationship, CCJ has a 10-week correlation to the market near zero.

This is the type of stock I’d be willing to buy in large part because further market weakness doesn’t automatically mean CCJ will suffer. But that’s not all. The price chart looks bullish. We just saw nearly a month of rising prices that took CCJ from $15 to $26. Volume surged, adding legitimacy to the move. And now, we have our first pullback. It’s been deep, yes, but we’re still above the rising 50-day moving average.

I like selling puts to bet CCJ will stay above $17 for the next month.

The Trade: Sell the November $17 naked put for 50 cents.

Uber Technologies (UBER)

Source: The thinkorswim® platform from TD Ameritrade

Three weeks ago, I wouldn’t have touched Uber with a 10-foot pole. But much has changed.

The primary reason for my about-face was the massive gap on Sept. 21 that single-handedly reversed the downtrend. Volume eclipsed 100 million shares, marking the highest volume session of the year. This wasn’t some retail-driven micro-rally but an institutional-led influx.

Given the strength of the ramp, I’m inclined to believe the new uptrend will have staying power. And that makes me a buyer of dips.

Over the past three days, UBER stock has retreated three sessions, ending with a doji on Thursday. This morning’s gap higher is confirming a new upswing is beginning. I would build a directional play in a healthier environment, but to respect the broader market correction, we’re taking the higher probability route with a naked put play.

If you think UBER can stay above $37.50 for the next month, enter the following play.

The Trade: Sell the November $37.50 puts for 50 cents.

Stocks to Buy: Marathon Oil (MRO)

If there’s one sector that has shone brightest during the recent drama, it’s energy. And that makes it an obvious place to look for stocks to buy.

You can thank the strength in crude oil for the sector’s spunk. Oil prices are back to testing major resistance near $75 and haven’t budged in recent days, despite the thrashing suffered by equities.

There are a lot of good-looking energy stocks right now, but I’d suggest taking a good look at Marathon Oil. Its share price is flirting with a major breakout over $14. This zone has provided stiff resistance for the past five months. Once we take it out, I suspect buyers will come running.

Additionally, the cheap price tag of MRO stock makes it a great candidate for selling puts. The margin requirement is low, and the potential return is juicy.

The Trade: Sell the November $12 naked put for 36 cents.

On the date of publication, Tyler Craig did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

For a free trial to the best trading community on the planet and Tyler’s current home, click here!

More From InvestorPlace

The post 3 Stocks to Buy Despite the Market Mayhem appeared first on InvestorPlace.

Just because a business does not make any money, does not mean that the stock will go down. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So should Alliance Resources (ASX:AGS) shareholders be worried about its cash burn? For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

Check out our latest analysis for Alliance Resources

Does Alliance Resources Have A Long Cash Runway?

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. As at June 2021, Alliance Resources had cash of AU$3.3m and no debt. In the last year, its cash burn was AU$3.6m. That means it had a cash runway of around 11 months as of June 2021. That's quite a short cash runway, indicating the company must either reduce its annual cash burn or replenish its cash. You can see how its cash balance has changed over time in the image below.

How Is Alliance Resources' Cash Burn Changing Over Time?

In the last year, Alliance Resources did book revenue of AU$56k, but its revenue from operations was less, at just AU$6.0k. We don't think that's enough operating revenue for us to understand too much from revenue growth rates, since the company is growing off a low base. So we'll focus on the cash burn, today. It's possible that the 13% reduction in cash burn over the last year is evidence of management tightening their belts as cash reserves deplete. Admittedly, we're a bit cautious of Alliance Resources due to its lack of significant operating revenues. So we'd generally prefer stocks from this list of stocks that have analysts forecasting growth.

Can Alliance Resources Raise More Cash Easily?

While Alliance Resources is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of AU$34m, Alliance Resources' AU$3.6m in cash burn equates to about 10% of its market value. As a result, we'd venture that the company could raise more cash for growth without much trouble, albeit at the cost of some dilution.

Is Alliance Resources' Cash Burn A Worry?

On this analysis of Alliance Resources' cash burn, we think its cash burn relative to its market cap was reassuring, while its cash runway has us a bit worried. We don't think its cash burn is particularly problematic, but after considering the range of factors in this article, we do think shareholders should be monitoring how it changes over time. On another note, Alliance Resources has 4 warning signs (and 2 which are concerning) we think you should know about.

Of course Alliance Resources may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

Vancouver, British Columbia–(Newsfile Corp. – October 1, 2021) – Thesis Gold Inc. (TSXV: TAU) (WKN: A2QQ0Y) ("Thesis" or the "Company") is pleased to announce the appointment of Dr. Thomas Mumford as a Director of the Company. In addition, Mr. Xiang has stepped down from the Board of Directors effective September 30, 2021 but will remain as an advisor to the Company.

Dr. Mumford is an exploration geologist with over 15 years experience. He has extensive technical and project management experience in Au, REE, Cu-porphyry, and U deposits. He is a registered professional geologist and professional engineering licensee with Engineers and Geoscientists British Columbia (EGBC), and currently acts as the Vice President, Exploration for Scottie Resources Corp. He is a director for the Association for Mineral Exploration (AME) and has served as a lecturer at Carleton University and British Columbia Institute of Technology. He holds a B.Sc. and M.Sc. from University of New Brunswick, and a Ph.D. from Carleton University which focused on magmatic controls of the Nechalacho REE deposit in the NWT.

"We would like to thank James for his contributions to Thesis over the past year and we look forward to continuing working with him in his new role as an advisor to the Company," Ewan Webster, President and CEO commented.

"I am delighted to welcome Thomas to the board. His extensive exploration experience will be invaluable to the Company as we continue to advance our Ranch Gold project."

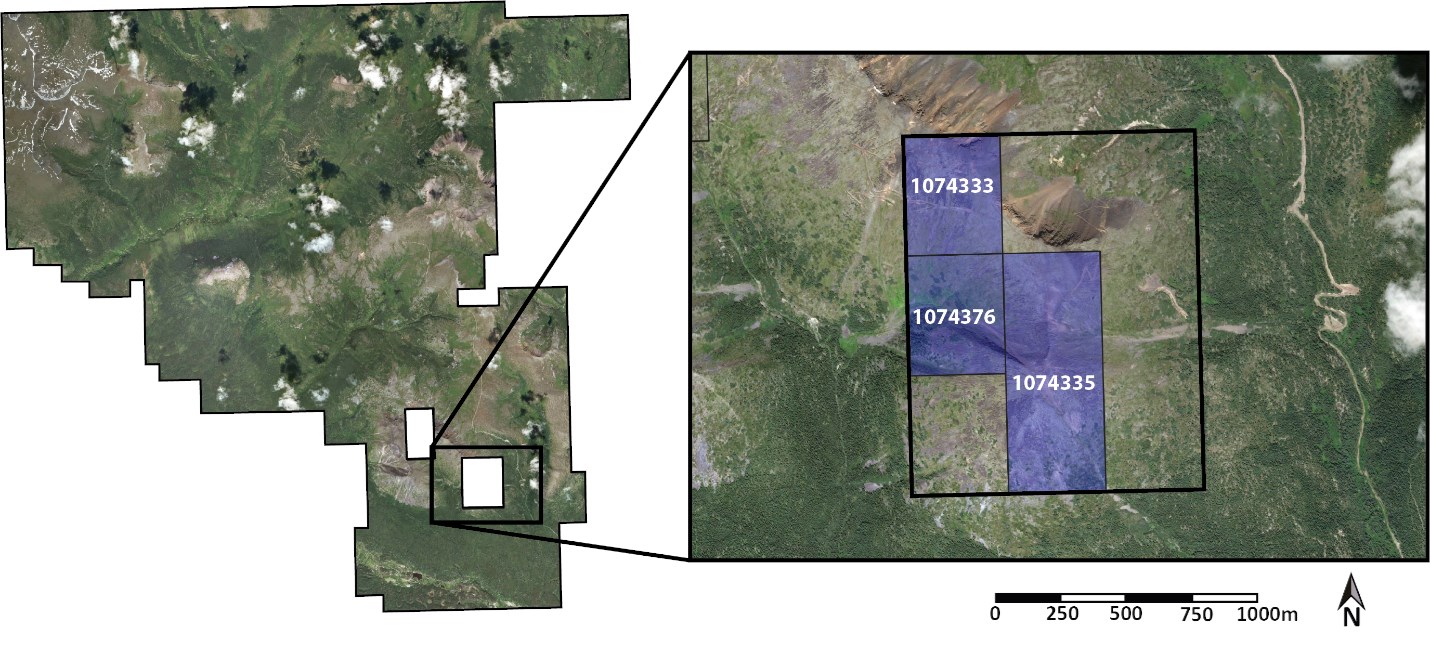

The Company is also pleased to announce it has entered into a letter agreement (the "Letter Agreement") dated September 15, 2021 with Steven Scott, pursuant to which the Company acquired British Columbia mineral claim numbers 1074376, 1074335 and 1074333 (the "Acquisition") (Figure 1). The mineral claims are all British Columbia mineral claims that were originally staked and are owned by an arm's length third party, Mr. Scott (the "Vendor"). Under the terms of the Letter Agreement, the Company paid cash consideration the amount of $5,000 plus the cost of transferring the title of the mineral claims to the Company. No finder's fees were paid in connection with the Acquisition.

Figure 1: Ranch project outline and inset showing the acquired claims.

To view an enhanced version of Figure 1, please visit:

https://orders.newsfilecorp.com/files/2191/98200_e9261cc5e4b709a0_001full.jpg

On behalf of the Board of Directors

Thesis Gold Inc.

"Ewan Webster"

Ewan Webster Ph.D., P.Geo.

President, CEO and Director

About Thesis Gold Inc.

Thesis Gold is a mineral exploration company focused on proving and developing the resource potential of the 17,832-hectare Ranch Gold Project located in the "Golden Horseshoe" area of northern British Columbia, approximately 300 km north of Smithers, B.C. For further details about the Ranch Gold Project, please refer to the Company's current geological Technical Report dated September 18, 2020 available under the Company's profile on SEDAR at www.sedar.com.

For further information or investor relations inquiries, please contact:

Dave Burwell

Vice President

The Howard Group Inc.

Email: dave@howardgroupinc.com

Tel: 403-410-7907

Toll Free: 1-888-221-0915

Nick Stajduhar

Director

Thesis Gold

Telephone: 780-701-3216

Email: nicks@thesisgold.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this press release.

Cautionary Statement Regarding Forward-Looking Information

This press release contains "forward-looking information" within the meaning of applicable Canadian securities legislation. Forward-looking information includes, without limitation, statements regarding the use of proceeds from the Company's recently completed financings, and the future plans or prospects of the Company. Generally, forward-looking information can be identified by the use of forward-looking terminology such as "plans", "expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates" or "does not anticipate", or "believes", or variations of such words and phrases or state that certain actions, events or results "may", "could", "would", "might" or "will be taken", "occur" or "be achieved". Forward-looking statements are necessarily based upon a number of assumptions that, while considered reasonable by management, are inherently subject to business, market and economic risks, uncertainties and contingencies that may cause actual results, performance or achievements to be materially different from those expressed or implied by forward-looking statements. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking information. Other factors which could materially affect such forward-looking information are described in the risk factors in the Company's most recent annual management's discussion and analysis which is available on the Company's profile on SEDAR at www.sedar.com. The Company does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/98200

DENVER, CO / ACCESSWIRE / October 1, 2021 / Gold Resource Corporation (NYSE American:GORO) (the "Company") will issue a news release providing a summary of its financial and operating results for the third quarter ended September 30, 2021 on Wednesday, October 27, 2021 after the market close, file its 10Q with the financial and operating results for the period ended September 30, 2021 with EDGAR and host a conference call on Thursday, October 28, 2021 at 11:00 a.m. Eastern Time.

The conference call will be recorded and posted to the Company's website later in the day following the conclusion of the call. Following prepared remarks, Allen Palmiere, President and Chief Executive Officer, Kim Perry, Chief Financial Officer and Alberto Reyes, Chief Operating Officer will host a live question and answer (Q&A) session. There are two ways to join the conference call.

To join the conference via webcast, please click on the following link:

https://www.webcaster4.com/Webcast/Page/2361/43124.

To join the call via telephone please use one of the following dial-in details:

Participant Toll Free: 888-506-0062

International: 973-528-0011

Entry Code: 552947

Please connect to the conference call at least 10 minutes prior to the start time using one of the connection options listed above.

About GRC:

Gold Resource Corporation is a gold and silver producer, developer, and explorer with its operations centered on the Don David Gold Mine in Oaxaca, Mexico. Under the direction of a new board and senior leadership, the Company focus is to unlock the significant upside potential of its existing infrastructure and large land position surrounding the mine, to close our acquisition of Aquila Resources Inc., and to develop the Back Forty Project in Michigan, USA. For more information, please visit GRC's website, located at www.goldresourcecorp.com and read the Company's 10-K for an understanding of the risk factors involved.

Contacts:

Ann Wilkinson

Vice President, Investor Relations and Corporate Affairs

Ann.Wilkinson@GRC-USA.com

www.GoldResourcecorp.com

SOURCE: Gold Resource Corporation

View source version on accesswire.com:

https://www.accesswire.com/666381/Gold-Resource-Corporation-to-Hold-Q3-2021-Conference-Call-on-October-28-2021

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. But as Warren Buffett has mused, 'If you've been playing poker for half an hour and you still don't know who the patsy is, you're the patsy.' When they buy such story stocks, investors are all too often the patsy.

If, on the other hand, you like companies that have revenue, and even earn profits, then you may well be interested in Anglo American (LON:AAL). Even if the shares are fully valued today, most capitalists would recognize its profits as the demonstration of steady value generation. In comparison, loss making companies act like a sponge for capital – but unlike such a sponge they do not always produce something when squeezed.

View our latest analysis for Anglo American

How Quickly Is Anglo American Increasing Earnings Per Share?

If a company can keep growing earnings per share (EPS) long enough, its share price will eventually follow. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. It certainly is nice to see that Anglo American has managed to grow EPS by 32% per year over three years. As a general rule, we'd say that if a company can keep up that sort of growth, shareholders will be smiling.

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. Anglo American shareholders can take confidence from the fact that EBIT margins are up from 18% to 36%, and revenue is growing. That's great to see, on both counts.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Anglo American's forecast profits?

Are Anglo American Insiders Aligned With All Shareholders?

Like standing at the lookout, surveying the horizon at sunrise, insider buying, for some investors, sparks joy. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

It's good to see Anglo American insiders walking the walk, by spending US$153k on shares in just twelve months. And when you consider that there was no insider selling, you can understand why shareholders might believe that lady luck will grace this business. Zooming in, we can see that the biggest insider purchase was by James Rutherford for UK£144k worth of shares, at about UK£24.30 per share.

The good news, alongside the insider buying, for Anglo American bulls is that insiders (collectively) have a meaningful investment in the stock. Notably, they have an enormous stake in the company, worth US$92m. This suggests to me that leadership will be very mindful of shareholders' interests when making decisions!

Does Anglo American Deserve A Spot On Your Watchlist?