If you are weighing your next move with BHP Group stock, you are far from alone. The stock has been on a steady climb lately, gaining 1.3% over the past week, 4.5% for the last month, and an impressive 8.3% in the past year. Looking back even further, BHP Group has rewarded patient investors with an 80.8% gain over five years. This naturally draws attention when deciding whether to buy more, hold, or perhaps even take some profit off the table. There is plenty of recent news impacting investor sentiment. On the positive side, BHP is taking a leadership role in an ambitious consortium exploring carbon capture initiatives across Asia. This is a strategic play that could enhance the company's future prospects and its alignment with cleaner industry trends. Of course, there have been challenges, too. Legal headlines about longstanding settlements related to the Mariana dam disaster put a spotlight on risk, which can sway opinions on what is already a closely watched stock. So, is BHP Group undervalued? According to the standard six-check valuation score, the company clocks in at 2 out of 6. This indicates that while it is undervalued by some measures, investors may want a closer look before making a move. Next, we will break down how these different valuation approaches stack up, and keep an eye out for a more insightful way to cut through the noise at the end of the article. BHP Group scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: BHP Group Cash Flows

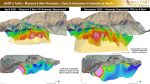

A Discounted Cash Flow (DCF) model estimates what a company is really worth by projecting its future cash flows and then discounting them back to today. This helps investors judge if the current stock price is attractive.

For BHP Group, the company reported a Last Twelve Months Free Cash Flow of $10.4 billion. Analysts project that annual free cash flow will decrease slightly over the coming years, with estimates dropping to $7.2 billion by 2028 and, based on extrapolations, reaching around $6.4 billion in 2035.

Based on these projections, the DCF calculation produces an estimated intrinsic value of $37.35 per share. When compared to BHP Group's share price, the model suggests the stock is trading at a 14.2% premium. This means it is 14.2% overvalued by this approach.

Result: OVERVALUED

BHP Discounted Cash Flow as at Aug 2025

Our DCF analysis suggests BHP Group may be overvalued by 14.2%. Find undervalued stocks based on DCF analysis or create your own screener to find better value opportunities.

Approach 2: BHP Group Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most widely used valuation multiples, especially for profitable companies like BHP Group. It offers a straightforward way to compare how much investors are willing to pay for each dollar of earnings. Generally, companies with better growth prospects and lower risk trade at higher PE ratios, while those facing uncertainty or slower growth are valued at lower multiples.

Currently, BHP Group trades at a PE ratio of 15.56x. This is slightly higher than the industry average of 14.42x for the Metals and Mining sector but below its peer average of 17.60x. These benchmarks provide helpful context but do not tell the whole story, as they overlook unique growth rates, risk profiles, and company fundamentals.

That is where Simply Wall St's "Fair Ratio" comes in. The Fair Ratio (20.01x) is tailored for BHP by considering its earnings growth forecasts, profitability, industry landscape, company size, and risk factors. By taking these important factors into account, the Fair Ratio gives a more nuanced and accurate reflection of what a fair valuation multiple should be, rather than relying solely on industry peers or averages.

With BHP's current 15.56x PE trailing the 20.01x Fair Ratio, the stock appears to be undervalued using this approach.

Result: UNDERVALUED

ASX:BHP PE Ratio as at Aug 2025

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your BHP Group Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. Simply put, a Narrative is your personal story or perspective on a company, brought to life by linking your assumptions about BHP Group's future revenue, profit margins, and fair value to a forecast that you can track.

Narratives allow you to connect the company's broader story with concrete financial forecasts and a resulting fair value, all within an easy-to-use tool on Simply Wall St's Community page, which is used by millions of investors worldwide.

With Narratives, you can quickly see how your view of BHP’s prospects compares to others. You can make buy or sell decisions by comparing your Fair Value to the current share price.

As new news or earnings are released, Narratives are automatically refreshed, giving you real-time context to adjust your view.

For example, one investor might believe BHP’s ambitious copper growth justifies a Fair Value above A$41. Another may see risks from debt or commodity price swings and set their Fair Value much lower. Ultimately, Narratives help you make sense of what really matters to you as an investor.

Do you think there's more to the story for BHP Group? Create your own Narrative to let the Community know!

ASX:BHP Community Fair Values as at Aug 2025

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include BHP.AX.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.