Hard rock lithium deposits are going to fill the demand as they are more evenly geographically distributed across the globe and are less dependant on a changing climate for production than lithium brine production. They are more and more filling the supply gap.

According the United State Geological Survey’s 2018 Mineral Commodity Summaries, Australia was the largest producer of lithium. It produced 18,700 MT of lithium last year, up 3,300 MT from the previous year. The 34-percent increase has been attributed to two new spodumene operations that ramped up production to meet strong demand.

Hard rock lithium mining relies on traditional methods of drilling and processing, and presents a more reliable method of mining and opens up deposits closest to major markets within. Hard rock mining is giving countries a competitive advantage over countries dependant on lithium brines for production, as it did with Australia.

Here are five exploration companies that are currently looking for the next hard rock deposit.

Azincourt Energy (TSX-V: AAZ)

The company controls 6,368 hectares of pegmatite-rich ground in Manitoba, with historical Li20 numbers & drill-ready targets. Crews are on the ground, beginning prep work for the 2018 work program. Mapping/sampling will get underway, then min 3000m of drilling. Azincourt’s Lithium Two project is adjacent to QMC’s Cat Lake Lithium Project

Quantum Minerals (QMC.V)

The company’s properties include the Irgon Lithium Mine project, a Rare-metal (Li-Ta-Cs) deposit within the Irgon pegmatite located immediately north of Cat Lake Manitoba. The deposit contains an estimated resource of more than 1.2M tonnes of spodumene-bearing pegmatite grading 1.5% Li2O.

https://qmcminerals.com/cat-lake-lithium-project/

Far Resources Ltd. (CSE: FAT)

Far Resources, an exploration and development company, will become a leader in the energy metals sector by defining a lithium resource with their Zoro project located in the Snow Lake region of Manitoba. In 1956, the lithium deposit was considered an historic “reserve” based on the drilling of 1.8 million tonnes grading 1.4% Li2O to a depth of 305 m.

https://www.farresources.com/lithium-projects/

MGX Minerals (CSE: XMG)

MGX Minerals Inc plans to drill the company’s Case Lake lithium project in May. Drilling will total 8,000 metres followed by an additional 7,000 metres of planned drilling in the fall. There have been 8,400 metres of drilling completed at Case Lake to date. Substantial spodumene mineralization intersections have included:

- PWM-17-34: 1.81 percent lithium oxide (Li2O) over 17.0 metres;

- PWM-17-33: 2.11 percent Li2O over 11.0 m;

- PWM-17-10: 1.74 percent Li2O over 15.06 m;

- PWM-17-08: 1.94 percent Li2O over 26.0 m.

The Case Lake property is located in Steele and Case townships, 80 kilometres east of Cochrane in Northeastern Ontario close to the Ontario-Quebec border. The Case Lake pegmatite swarm consists of five dikes. MGX currently has a paid-up 20-per-cent working interest in Case Lake and four other lithium hardrock properties in Ontario controlled by Power Metals

Power Metals (TSX-V: PWM)

The Cass spodumene pegmatite swarm is located 80 km east of Cochrane and 100 km north of Kirkland Lake, NE Ontario. It is accessible year-round by road via the Translimit Road which connects Ontario and Quebec.

https://www.powermetalscorp.com/

Argentinian lithium producer Orocobre (TSX: ORL) recently reported lower than expected lithium production in its third fiscal quarter because weather interfered with its evaporation rates of its lithium brines. This reveals two problems with lithium brine production: reliability and geography. Another source of lithium is rising to met these problems, hard rock lithium mining.

One analyst pointed out that Orocobre’s production problems “clearly demonstrate” that production is not a straightforward process. “Weather events are beyond the control of Orocobre, but this reaffirms that there is still room to improve on the robustness of operations and reduce production variability from we ather impacts,” the analyst stated.

The company reported a 25-per-cent lower evaporation rate compared with the same quarter in 2017 which caused production problems and lithium output to fall 29 percent to 2,802 tonnes of Lithium Carbonate equivalent, from 3,937 tonnes in the December quarter. Its February rates were the lowest since 2011.

Weather has clear impacts on the production at lithium brine operations and with global demand for lithium on the rise, more reliable and consistent methods of production will be required. Lithium brine operations are limited to select climates and regions that can support sufficient weather to ensure economic processing.

Demand for the metal is set to grow by 600,000-800,000 tonnes of lithium carbonate equivalent over the next 10 years, Daniel Jimenez, senior commercial vice president at SQM, said.

The global lithium industry will need $10 billion to $12 billion of investment over the next decade to meet surging demand amid the electric vehicle boom, Daniel Jimenez of Chilean miner SQM said.

Not all lithium is equal and not all lithium is mined the same way. There are two significant sources of lithium, Lithium Brines and Lithium-Cesium Tantalum Pegmatites (hard rock).

According the United States Geological Survey’s 2018 Mineral Commodity Summaries, Australia was the largest producer of lithium. It produced 18,700 MT of lithium last year, up 3,300 MT from the previous year. The 34-percent increase has been attributed to two new spodumene operations that ramped up production to meet strong demand.

Australia hosts the Greenbushes lithium asset, which is operated by Talison Lithium, a subsidiary jointly owned by Tianqi Lithium (SZSE:002466) and Albemarle (NYSE:ALB). Greenbushes is the longest continuously operating mining area in Western Australia, having been in operation for over 25 years.

These production figures helped to push Australia as the top lithium producing country and it shows how hard rock lithium mines have the potential to disrupt traditional sources of lithium from older operators of lithium evaporation ponds.

Hard rock lithium deposits are not limited to select climates and regions and are going to help fill the demand as they are more evenly geographically distributed across the globe and are less dependant on a changing climate for production.

The future is sealed; batteries will rule the automotive industry as more and more countries outlaw combustion engines. Lithium (Li) is the lightest metal with the highest energy density, allowing the metal to supply the maximum charge per kilogram, which, in turn, makes it excellent for battery use.

Current global lithium production is not enough to meet future demand and with countries around the world increasingly shunning fossil fuels, demand for a secure supply of lithium will drive growth of lithium mining companies.

One company is already on its way to commercial production of lithium.

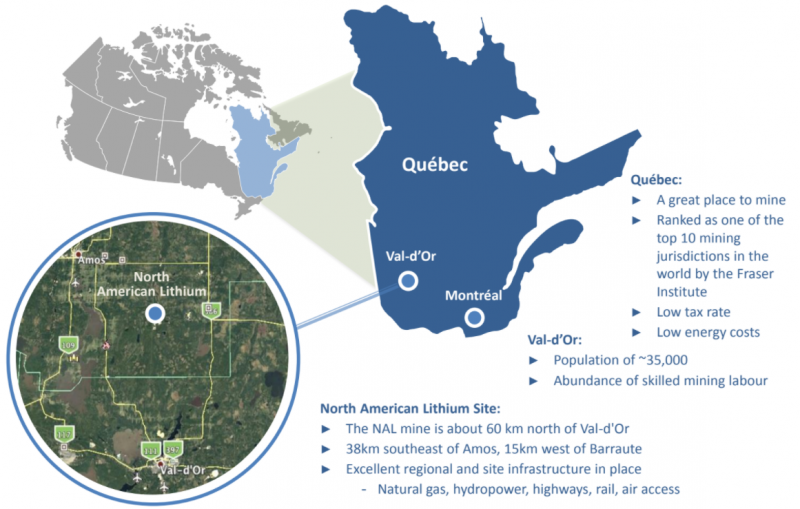

North American Lithium (NAL) acquired and is re-starting one of the only near-term viable hard rock lithium operations globally. North American Lithium is the 100-per-cent owner of the Québec Lithium Mine in Val-d’Or, Quebec, a mine site located within reach of North America’s largest markets and export terminals.

According to the 2016 Fraser Institute Annual Survey Mining Jurisdictions, Québec ranks as one of the top 10 mining jurisdictions in the world, with a low tax rate, low energy costs and a mining friendly government. NAL’s mine is situated about 60 kilometres north of Val-D’Or, a city with a population of 35,000 residents that provides an abundance of skilled mining labor for the region. The site also happens to be serviced by excellent regional and site-based infrastructure with access to natural gas, hydropower, highways, rail, and air. With security of supply a top priority for technology companies, businesses that require lithium will want to source their supply from safe and stable jurisdictions.

NAL’s lithium project is a past-producing mine with approximately $500 million already spent on the development of the property. Previous companies completed the necessary work to advance the project to the brink of commissioning. In addition, over $100 million has been invested by NAL shareholders over the last two years, shortening the timeline to production for a junior mining company.

Previous work at NAL’s mine site revealed significant mineral resource estimates for a long operating life. As of May 2017, the company has measured resources of 13.5 Mt tonnes at 1.08 %Li2, indicated 25.8 Mt at 1.02 %Li2 for a total of measured and indicated of 39.3 Mt tonnes at 1.04 %Li2. Also as of May 2017, the site proved 11.9 Mt at 0.94 %Li2 and probable reserves of 8.9 Mt at 93 %Li2. Infill-drilling confirmed previous drilling data and the 2016 drill campaign shows potential to extend reserve life from material within current mining lease. Currently, the project is fully permitted, in possession of all permits/licenses to restart the mine, processing facility and tailings.

The amount of previous work, in addition to the size of the resource and the improved market demand for lithium prompted NAL to acquire the asset in 2016. NAL is a joint investment venture between Jien International Investments Ltd. and Investissement Québec. Jien has a successful track record in Québec, having invested $1.6 billion in Northern Québec nickel, copper and PGM producer Canadian Royalties Inc. (CRI). The company has strong relationships with China and other Asian markets with an experienced, Canadian-based operational, technical and finance team. Management has experience with turning around mines in Québec and a unique access to Chinese lithium converter markets.

NAL is led by Chief Executive Officer and Director, James Xiang. James Xiang has had a successful track record as an entrepreneur, investor and savvy rescue artist since immigrating to Canada in 2001. In 2005, Xiang began pursuing a career in the resource sector and successfully brought a China-based nickel-copper project, GobiMin Inc, to list on the TSX. In less than one and a half years, GobiMin’s market cap grew by 10 times. Under his management during the financial crisis of 2008, GobiMin was able to sell its main project to a Chinese firm in an all cash-deal which proved his ability to take advantage of both North American market and Chinese markets.

James Xiang was also instrumental in the turnaround of Canadian Royalties Inc. As the company’s CEO, Xiang re-built the company’s senior management and corporate strategy, which was work that ultimately led to a company turnabout that caught the attention of the market, especially Investissment Québec, which partnered with Xiang at NAL.

Future plans for the company include developing and completing the improvement of its existing lithium processing facilities, becoming a commercial producer of lithium carbonate, and looking for expansion and acquisition in Québec and globally.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |