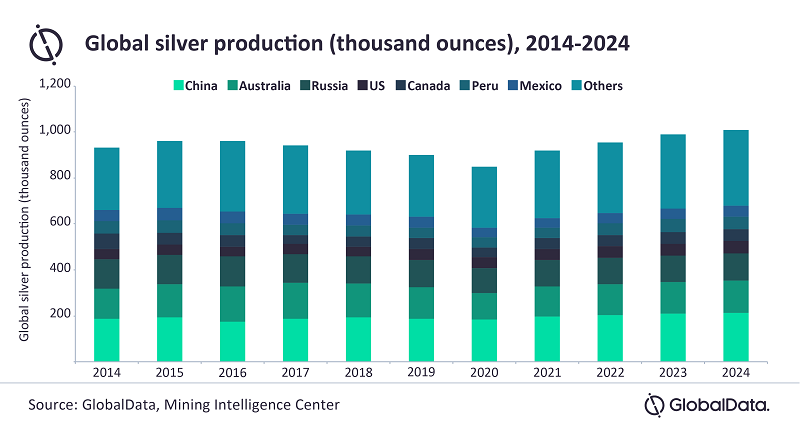

The last four years haven’t been kind to silver production, with four consecutive years of annual decline. 2021 is finally bringing an increase of 8.1% to 918.3 million ounces (Moz), and ultimately silver production should exceed one billion ounces by 2024, according to a report from GlobalData. This notable bump would be a 3.2% compound annual growth rate (CAGR).

Where in the World?

The top contributors to this growth will be Peru, Mexico, and China, with a combined production increase forecast at 393.9Moz in 2021 to 443.9 Moz in 2024. The countries have ramped up their efforts to allow new projects to move forward, and companies have had it easier as these countries either recover from the pandemic (China) or refuse to put more restrictions in place (Mexico and Peru) due to struggling economies.

Hit Hard

2020 saw an estimated global silver mine production decline of 2.4% to 849.7 million ounces, as the lockdown and restrictions in some of the top silver-producing countries hit hard. While those restrictions did crimp growth and production overall, those countries seem to be intent on avoiding any form of lockdown again as fumbling economies in the developing world struggle to regain traction.

The first nine months of 2020 were the hardest, as eight of the top ten silver producers reported a collective 13.9% YoY decrease in output. This had an outsize effect and resulted in lower global production numbers.

According to Vinneth Bajaj, associate project manager at GlobalData: “In Mexico, output was estimated to have fallen by 1.8% in 2020, with mining activities suspended for almost two months through to the end of May. Major silver producers in the country temporarily suspended their mining operations during this period, and production losses were registered at Pan American’s La Colorada and Dolores mines, Fortuna Silver’s San Jose mine, Industria Penoles’ Saucito mine, and Hecla Mining Company’s San Sebastian project, among others. However, these COVID-19-related production losses were partially offset by high production from other key mines, including the Penasquito, Guanacevi, Zimapan, and Ocampo projects, as well as from the commencement of projects in 2020 such as the Red de Plata, Capire, and Tahuehueto projects.”

Depleted Supply

According to the report, depleting ore reserves are also weighing on production and is a major industry concern. As miners work to increase production over the next three years, discovery and exploration will continue to be a prime driver of activity for the sector.

Top Silver Miners 2020

Although 2020 was a challenging year for silver production and the companies mining it, some miners continued to work steadily. The rankings of the top 10 silver producing companies in 2020 based on output reported last year worldwide prove that while production was down globally, some companies could increase production.

| Rank | Company | 2020 Ag output, Moz | 2019 Ag output, Moz | Change, % |

| 1 | Fresnillo | 53.1 | 54.6 | -3 |

| 2 | KGHM | 43.4 | 45.5 | -5 |

| 3 | Glencore | 32.8 | 32 | 2 |

| 4 | Newmont | 27.8 | 15.9 | 75 |

| 5 | CODELCO | 27 | 17.9 | 51 |

| 6 | Vedanta (Hindustan Zinc) | 23.7 | 22.3 | 6 |

| 7 | Southern Copper | 21.5 | 20.3 | 6 |

| 8 | Polymetal | 18.8 | 21.6 | -13 |

| 9 | Pan American Silver | 17.3 | 25.9 | -33 |

| 10 | Hecla | 13.5 | 12.6 | 7 |

Source: Vladimir Basov, Kitco News

The rankings bear out a story that while silver production suffered in 2020, not every company did. Some of them went on to increase production. The most significant gain in production came from Newmont, with a 75% increase YoY from 2019. With the expected production increases of the coming years, these companies will all be maneuvering for market dominance and gains like those seen last year from companies like Newmont.

The silver miners’ stocks have largely languished this year, grinding sideways near lows for months on end. This vexing consolidation has fueled near-universal bearishness, leaving silver stocks deeply out of favor. But once a quarter when earnings season arrives, hard fundamentals pierce the obscuring veil of popular sentiment. The silver miners’ recently-reported Q2’17 results reveal today’s silver prices remain profitable.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. These are generally due by 45 days after quarter-ends in the US and Canada. They offer true and clear snapshots of what’s really going on operationally, shattering the misconceptions bred by the ever-shifting winds of sentiment. There’s no silver-miner data that is more highly anticipated than quarterlies.

Silver mining is a tough business both geologically and economically. Primary silver deposits, those with enough silver to generate over half their revenues when mined, are quite rare. Most of the world’s silver ore formed alongside base metals or gold, and their value usually well outweighs silver’s. So typically in any given year, less than a third of the global mined silver supply actually comes from primary silver mines!

The world authority on silver supply-and-demand fundamentals is the Silver Institute. Back in mid-May it released its latest annual World Silver Survey, which covered 2016. Last year only 30% of silver mined came from primary silver mines, a slight increase. The remaining 70% of silver produced was simply a byproduct. 35% of the total mined supply came from lead/zinc mines, 23% from copper, and 12% from gold.

As scarce as silver-heavy deposits supporting primary silver mines are, primary silver miners are even rarer. Since silver is so much less valuable than gold, most silver miners need multiple mines in order to generate sufficient cash flows. These often include non-primary-silver ones, usually gold. More and more traditional elite silver miners are aggressively bolstering their gold production, often at silver’s expense.

So the universe of major silver miners is pretty small, and their purity is shrinking. The definitive list of these companies to analyze comes from the most-popular silver-stock investment vehicle, the SIL Global X Silver Miners ETF. This week its net assets are running 6.0x greater than its next-largest competitor’s, so SIL really dominates this space. With ETF investing now the norm, SIL is a boon for its component miners.

While there aren’t many silver miners to pick from, major-ETF inclusion shows silver stocks have been vetted by elite analysts. Due to fund flows into top sector ETFs, being included in SIL is one of the important considerations for picking great silver stocks. When the vast pools of fund capital seek silver-stock exposure, their SIL inflows force it to buy shares in its underlying companies bidding their prices higher.

Back in mid-August as the major silver miners finished reporting their Q2’17 results, SIL included 29 “silver miners”. This term is used loosely, as SIL includes plenty of companies which can’t be described as primary silver miners. Most generate well under half their revenues from silver, which greatly limits their stock prices’ leverage to silver rallies. Nevertheless, SIL is today’s leading silver-stock ETF and benchmark.

The higher the percentage of sales any miner derives from silver, naturally the greater its exposure to silver-price moves. If a company only earns 20%, 30%, or even 40% of its revenues from silver, it’s not a primary silver miner and its stock price won’t be very responsive to silver itself. But as silver miners are increasingly actively diversifying into gold, there aren’t enough big primary silver miners left to build an ETF alone.

Every quarter I dig into the latest results from the major silver miners of SIL to get a better understanding of how they and this industry are faring fundamentally. I feed a bunch of data into a big spreadsheet, some of which made it into the table below. It includes key data for the top 17 SIL component companies, an arbitrary number that fits in this table. That’s a commanding sample at 93.2% of SIL’s total weighting.

While most of these top 17 SIL components had reported on Q2’17 by mid-August, not all had. Some of these major silver miners trade in the UK or Mexico, where financial results are only required in half-year increments. If a field is left blank in this table, it means that data wasn’t available by the end of Q2’s earnings season. Some of SIL’s components also report in gold-centric terms, excluding silver-specific data.

In this table the first couple columns show each SIL component’s symbol and weighting within this ETF as of mid-August. While most of these silver stocks trade in the States, not all of them do. So if you can’t find one of these symbols, it’s a listing from a company’s primary foreign stock exchange. That’s followed by each company’s Q2’17 silver production in ounces, along with its absolute year-over-year change.

After that comes this same quarter’s gold production. Pretty much every major silver miner in SIL also produces significant-if-not-large amounts of gold. While gold stabilizes and augments the silver miners’ cash flows, it also retards their stocks’ sensitivity to silver itself. Naturally investors and speculators buy silver stocks and their ETFs because they want leveraged upside exposure to silver’s price, not gold’s.

So the next column reveals how pure the elite SIL silver miners are. This is mostly calculated by taking a company’s Q2 silver production, multiplying it by Q2’s average silver price, and then dividing that by the company’s total quarterly sales. If miners didn’t report Q2 revenues, I approximated them by adding the silver sales to gold sales based on their quarterly production and these metals’ average second-quarter prices.

Then comes the most-important fundamental data for silver miners, cash costs and all-in sustaining costs per ounce mined. The latter determines their profitability and hence ultimately stock prices. Those are also followed by YoY changes. Finally comes the YoY changes in cash flows generated from operations and GAAP profits. But an exception is necessary for companies with numbers that crossed zero since Q2’16.

Percentage changes aren’t relevant or meaningful if data shifted from negative to positive or vice versa. Plenty of major silver miners suffered net losses in Q2’17 after earning profits in Q2’16. So in cases where data crossed that zero line, I included the raw numbers instead. This whole dataset offers a fantastic high-level fundamental read on how the major silver miners are faring today, and it’s reasonably well.

That’s reassuring given silver’s serious under-performance relative to gold this year. As a far-smaller market, silver usually amplifies gold’s advances by at least 2x. But as of the end of Q2, silver was only up 4.5% YTD compared to 7.9% for gold. That’s dismal 0.6x leverage. And by mid-August as Q2’s earnings season wrapped up, silver’s YTD gain of 4.6% fell even further behind gold’s 10.6%. That’s horrible 0.4x leverage!

Production is the lifeblood of mining companies, and thus the best place to start fundamental analysis. In Q2’17, these top 17 SIL components collectively produced an impressive 78.6m ozs of silver. If 2016’s world-silver-mining run rate is applied to this year’s second quarter, that implies 221.5m ozs of silver mined. Thus these top SIL silver miners would account for over 35% of that total, they truly are major silver players.

But these elites still weren’t able to significantly grow their collective silver production, it was up just 0.9% YoY. Instead they invested heavily in expanding their gold production, which surged 6.4% YoY to 1354k ounces. Interestingly 10 of these top 17 SIL components, a majority representing 45.3% of SIL’s total weighting, are also included in the leading GDX gold miners’ ETF. SIL is mostly made up of primary gold miners!

Many of these elite major silver miners don’t just mine gold as a silver byproduct, but actually operate at least one primary gold mine. The silver miners have collectively decided to diversify into gold due to its superior economics. Consider hypothetical mid-sized silver and gold miners, which might produce 10m and 300k ounces annually. What would those cash flows look like at last quarter’s average metals’ prices?

In Q2’17, silver and gold averaged $17.18 and $1258. Silver was up 2.3% YoY, while gold slipped by a slight 0.1% YoY. At 10m ounces, that silver miner would generate $172m in sales. But the similar-sized gold miner’s sales of $377m more than doubles that. At recent years’ prevailing prices, the cash flows from gold mining are much more robust than those from silver mining. That makes it easier to pay bills and expand.

Silver mining is often as capital-intensive as gold mining, requiring similar large expenses for planning, permitting, and constructing mines and mills to process ore. Similar heavy excavators and haul trucks are necessary to dig and haul the ore, along with similar staffing levels to run mines. So silver’s lower cash flows to support all this activity make silver mining harder than gold mining, which isn’t lost on silver miners.

Silver-mining profits do skyrocket when silver soars occasionally in one of its massive bull markets. But during silver’s long intervening drifts at relatively-low price levels, the silver miners often can’t generate sufficient cash flows to finance expansions. So the top silver miners are increasingly looking to gold, a trend that isn’t likely to reverse given the relative economics of silver and gold. Primary silver miners are getting rarer.

Technically a company isn’t a primary silver miner unless it derives over half its revenues from silver. In Q2’17, the average sales percentage from silver of these top SIL components was just 37.6%! That is right on trend over this past year, with Q2’16, Q3’16, Q4’16, and Q1’17 weighing in at 46.3%, 38.5%, 40.5%, and 37.9%. In Q2’17, only 5 of the top SIL component companies qualified as primary silver miners!

While I understand this, as a long-time silver-stock investor it saddens me primary silver miners have apparently become a dying breed. When silver starts powering higher in one of its gigantic uplegs and way outperforms gold again, this industry’s silver percentage will rise. But unless silver not only shoots far ahead but stays there while gold lags, it’s hard to see major-silver-mining purity significantly reversing.

Unfortunately SIL’s mid-August composition was such that there wasn’t a lot of Q2 cost data reported by its top component miners. 3 of its top 4 companies trade in the UK and Mexico, where reporting only comes in half-year increments. Lower down the list there are more half-year reporters, an explorer with no production, and primary gold miners that don’t report silver costs. So silver cost data was fairly scarce.

Nevertheless, it’s always useful to look at the data we have. Industry wide silver-mining costs are one of the most-critical fundamental data points for silver-stock investors. As long as the miners can produce silver for well under prevailing silver prices, they remain fundamentally sound. Cost knowledge helps traders weather this sector’s fear-driven plunges without succumbing to selling low like the rest of the herd.

There are two major ways to measure silver-mining costs, classic cash costs per ounce and the superior all-in sustaining costs. Both are useful metrics. Cash costs are the acid test of silver-miner survivability in lower-silver-price environments, revealing the worst-case silver levels necessary to keep the mines running. All-in sustaining costs show where silver needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of silver, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q2’17, these top 17 SIL-component silver miners that reported cash costs averaged $6.34 per ounce. That surged a major 19.1% YoY from Q2’16’s $5.32, which seems like a troubling omen.

But it’s not. Flighty silver-stock investors are always on the verge of panicking, fleeing this volatile and psychologically-challenging sector. But the only event worthy of such extreme bearishness would be prevailing silver prices falling near cash costs. And even at $6.34-per-ounce cash costs and today’s low silver, a vast buffer exists. There’s no way silver is going to plummet down under $7 in any conceivable scenario!

These high cash costs are actually an anomaly mainly driven by two companies. First, SSR Mining (TSX: SRR) is now winding down its rapidly-depleting silver mine as planned. It produced 10.4 million ounces of silver in 2016, but only 5.5m is forecast this year! As silver throughput drops each quarter, the per-ounce costs are rising. Without SSRM’s outlying super-high cash costs, the rest of these top SIL miners averaged just $5.51.

Another company Silvercorp Metals (TSX: SVM) had slid out of SIL’s top 17 components as of mid-August. It was the 18th one, removing it from this particular calculation. Due to SVM’s enormous lead and zinc byproducts, its costs are the lowest in the industry. In Q2’16 it reported cash costs of $0.08 per ounce, which really dragged down that comp-quarter average. So the major silver miners’ collective cash costs were just fine in Q2.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain a silver mine as an ongoing concern. AISC include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current silver-production levels.

These additional expenses include exploration for new silver to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee silver mines. All-in sustaining costs are the most-important silver-mining cost metric by far for investors, revealing silver miners’ true operating profitability.

In Q2’17, these top 17 SIL components reporting AISC averaged $11.66 per ounce. That was up 16.0% YoY from Q2’16s $10.05. Coeur Mining was a big factor, with AISC surging 19% to a lofty $15.90 per ounce! That was due to lower-grade ore on the way to better zones. Ex-CDE, this average ran $10.96 which was closer to year-ago levels. SVM was also a factor, with low $7.06 AISC feeding into Q2’16 comps.

Two other elite silver miners suffered major production problems in Q2’17, resulting in big production drops. With fewer ounces to spread mining’s heavy fixed costs across, all-in sustaining costs soared. First Majestic Silver (TSX: FR), the purest major silver miner at 65.4% of Q2 revenues, saw production fall 20% YoY which forced AISC 33% higher. Unprecedented labor unrest in Mexico temporarily halted 3 of its 6 silver mines.

Those issues have since been resolved, so AG’s production should bounce back in Q3 which will push its AISC back down. Meanwhile Tahoe Resources (TSX: THO) saw its Q2 production plunge 28% YoY forcing its own AISC 23% higher. It got sucked into a legal battle between anti-mining activists and the government of Guatemala where its silver mine is. That mining license was temporarily suspended for an unmerited lawsuit.

The activists allege the government shouldn’t have granted Tahoe its Escobal mining license in the first place because it didn’t consult with a particular indigenous tribe first. But those people don’t even live anywhere near the mine site, it’s ridiculous! Tahoe doesn’t know when Escobal operations will be allowed to resume, but estimates a range between a couple months from now out to 18 months for a full resolution.

Tahoe’s large gold production from its two other gold mines in Peru, 110k ounces in Q2’17, ensures it won’t have any serious problems weathering this Guatemalan nightmare. But the point for our purposes today is that anomalous special situations fed the steep jump in the major silver miners’ all-in sustaining costs in Q2. But even at these elevated levels, this industry is still enjoying hefty silver-mining margins.

At $11.66 AISC, the major silver miners still earned big profits in the second quarter. Once again silver averaged $17.18, implying fat profit margins of $5.52 per ounce or 32%! Most industries would kill for such margins, yet silver-stock investors are always worried silver prices are too low for miners to thrive. That’s why it’s so important to study fundamentals, because technical price action fuels misleading sentiment!

Today’s silver price remains really low relative to prevailing gold levels, which portends huge upside as it mean reverts higher. The long-term average Silver/Gold Ratio runs around 56, which means it takes 56 ounces of silver to equal the value of one ounce of gold. Silver is really underperforming gold so far in 2017, with the SGR averaging just 72.6 YTD as of mid-August. So silver is overdue to catch up with gold.

At a 56 SGR and $1300 gold, silver is easily heading near $23.25. That’s 35% above its Q2 average. Assuming the major silver miners’ all-in sustaining costs hold, that implies profits per ounce soaring 110% higher! Plug in a higher gold price or the typical mean-reversion overshoot after an SGR extreme, and the silver-mining profits upside is far greater. Silver miners’ inherent profits leverage to rising silver is incredible.

Still Q2’17’s relatively-weak silver price weighed on miners’ cash flows generated from operations and GAAP accounting profits. Despite their big gold production, operating cash flows plunged 28.4% YoY to $1038m for these top SIL components. That’s not quite a righteous comparison though, because only 13 of this year’s top 17 had reported Q2 financial results by mid-August. Last year that number totaled 15.

And one of the silver miners not reporting OCF by the usual Q2 deadline this year was the Mexican silver giant Fresnillo (NASDAQ: FNLPF). Its OCF last year was fully 1/6th of these top SIL components’ total! So their operating-cash-flows situation in Q2’17 is nowhere near as bad as the drop implies. The same is true on the GAAP-earnings front. Last year Fresnillo contributed nearly 22% of the profits of these top 17 SIL components.

Another huge Mexican silver miner, the conglomerate Industrias Penoles (NASDAQ: IPOAF), saw its profits plunge about $140m YoY. These two Mexican silver giants alone account for the entire drop in these top SIL miners’ profits in Q2’17, which plummeted 57.5% YoY or $221m. Without them, silver-mining profits were flat. That’s pretty darned good considering all the super-anomalous company-specific problems that plagued Q2 results.

Silver miners’ earnings power and thus stock-price upside potential will only grow as silver mean reverts higher. In mining, costs are largely fixed during the mine-planning stages. That’s when engineers decide which ore bodies to mine, how to dig to them, and how to process that ore. Quarter after quarter, the same numbers of employees, haul trucks, excavators, and mills are generally used regardless of silver prices.

So as silver powers higher in coming quarters, silver-mining profits will really leverage its advance. And that will fundamentally support far-higher silver-stock prices. The investors who will make out like bandits on this are the early contrarians willing to buy in low, before everyone else realizes what is coming. By the time silver surges higher with gold so silver stocks regain favor again, the big gains will have already been won.

While investors and speculators alike can certainly play the silver miners’ ongoing mean-reversion bull with this leading SIL ETF, individual silver stocks with superior fundamentals will enjoy the best gains by far. Their upside will trounce the ETFs’, which are burdened by companies that don’t generate much of their sales from silver. A handpicked portfolio of purer elite silver miners will yield much-greater wealth creation.

At Zeal we’ve literally spent tens of thousands of hours researching individual silver stocks and markets, so we can better decide what to trade and when. As of the end of Q2, this has resulted in 951 stock trades recommended in real-time to our newsletter subscribers since 2001. Fighting the crowd to buy low and sell high is very profitable, as all these trades averaged stellar annualized realized gains of +21.2%!

The key to this success is staying informed and being contrarian. That means diligently studying and buying great silver stocks before they grow popular again, when they’re still cheap. An easy way to keep abreast is through our acclaimed weekly and monthly newsletters. They draw on our vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. For just $10 per issue, you can learn to think, trade, and thrive like contrarians. Subscribe today and get deployed in great silver stocks before they surge far higher!

The bottom line is the major silver miners fared fine in Q2 despite some real challenges. A combination of silver continuing to seriously lag gold, along with anomalous company-specific problems, weighed on miners’ collective results. Yet they continued to produce silver at all-in sustaining costs way below Q2’s low prevailing silver prices. And their accelerating gold-production growth leaves them financially stronger.

With silver-stock sentiment remaining excessively bearish, this sector is primed to soar as silver itself continues mean reverting higher to catch up with gold’s current upleg. The silver miners’ profits leverage to rising silver prices remains outstanding. After fleeing silver stocks so aggressively this year, investors and speculators alike will have to do big buying to reestablish silver-mining positions. That will fuel major upside.

Adam Hamilton, CPA

September 1, 2017

Copyright 2000 – 2017 Zeal LLC (www.ZealLLC.com)

On April 24th, the price of silver reached nearly $50 an ounce before a hasty retreat to $32.32. Ask some, and silver’s impressive move from under $20 an ounce just eight months earlier was a predictable bubble ready to pop. Others, however, say the move was inevitable considering market forces and the devaluation of global currencies.

On April 25th, the day silver began its sharp correction, Hakan Kaya, a commodities portfolio manager at Neuberger Berman an international asset management company with almost $200 billion on the books said, “At current prices, we find it (silver) highly overvalued with no fundamental reasons backing it up.” This sentiment, shared by many, set the stage for a staggering 35% correction in less than three weeks.

But since the dramatic pullback in early May silver has recovered over $5.50 an ounce trading at $38.00. Eric Sprott, the founder of Sprott Asset Management is not surprised. Sprott calls silver “the best recommendation anyone could make this decade”, and sees silver going to $100 an ounce within the next 3 to 5 years. Recently, MiningFeeds.com featured Eric Sprott in, “Sprott still bullish on Silver” – CLICK HERE – to read the article.

MiningFeeds.com

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |