The silver miners’ stocks have mostly drifted sideways this year, looking vexingly comatose. Such dull price action repels speculators and investors, so they’ve largely abandoned this lackluster sector. That weak trader participation has led to silver stocks’ responsiveness to silver price moves decaying. What can shock silver stocks out of their zombified stupor? And how soon is such an awakening catalyst likely?

Silver stocks’ flatlined behavior so far in 2017 is surprising and odd. Silver-stock prices are ultimately driven by silver-mining profits, which are overwhelmingly driven by prevailing silver price levels. Silver in turn is slaved to gold’s fortunes, the yellow metal is the white metal’s dominant primary driver. With gold faring quite well this year despite the euphoric record stock markets, silver and its miners’ stocks should be shining.

Since silver is a tiny market compared to gold, silver’s moves tend to leverage gold’s. The best global silver and gold supply-and-demand fundamental data available comes from the Silver Institute and World Gold Council respectively. According to them, worldwide silver and gold demand last year ran 1027.8m ounces and 4337.4 metric tons. Along with average prices, these can be used to approximate market sizes.

Silver and gold averaged $17.12 and $1250 last year. Run these numbers, and 2016’s total global silver and gold markets were worth about $17.6b and $174.3b. This latest-available data shows silver’s market is literally an order of magnitude smaller than gold’s! With silver only enjoying 1/10th the capital flows of gold, silver tends to be far more responsive. Any dollar of buying or selling is 10x more impactful for silver.

The silver market’s small size is one of this metal’s greatest strengths. Compared to the vastly-larger broader markets, it doesn’t take much new buying to catapult silver dramatically higher. Speculators and investors alike usually get interested in shifting capital into silver when gold is already rallying. Silver then tends to rally much more than gold, leveraging its upside, because silver inflows are relatively larger.

Given gold’s good performance this year, silver and the stocks of its miners should’ve surged. Year-to-date gold is up 11.3%, well ahead of full-year 2016’s 8.5% gain. But instead of amplifying gold’s 2017 advance by 2x to 3x like usual, silver is only up 6.7% YTD as of this week. This makes for really poor leverage to gold of 0.6x. Last year silver rallied 15.1%, yielding still-weak-but-more-normal 1.8x upside leverage.

Silver’s serious underperformance relative to gold this year has greatly retarded traders’ interest in the silver miners’ stocks. The leading silver miners’ trading vehicle and sector-index proxy is the SIL Global X Silver Miners ETF. Because of the great profits leverage to silver inherent in the silver miners, their stocks usually amplify silver’s upside. But YTD SIL is only up 4.0%, for extremely-poor 0.6x leverage!

Gold stocks aren’t having a great year either, with their leading GDX ETF only up 11.5% YTD compared to gold’s 11.3% gains. Like silver stocks, their gains tend to multiply their underlying metal’s gains by 2x to 3x. But the gold stocks’ weak in-line performance so far in 2017 highlights just how bad silver stocks’ lagging performance is. They have been largely drifting comatose this year, hardly even responding to silver.

Silver stocks have serious problems, and they certainly aren’t fundamental. Every quarter I analyze the latest operating and financial results from the top silver miners of SIL. They will soon start reporting their new Q3’17 results, but the prior quarter’s are the latest now available. In Q2’17 SIL’s elite top silver miners reported average all-in sustaining costs of $11.66 per ounce, well below average silver prices of $17.18.

That implies hefty industrywide silver-mining profits of $5.52 per ounce. While the average silver price did slump 2.0% sequentially in Q3 to $16.84, that’s certainly no fundamental threat. Assuming flat mining costs, the silver miners still should’ve been able to earn $5.18 per ounce last quarter. That’s down 6.2% quarter-on-quarter, but is still very profitable. Fundamentals can’t explain silver stocks’ vexing malaise this year.

That narrows down the suspect list to technicals and sentiment. This first chart looks at the price action in SIL and silver over the past couple years or so. Silver miners’ responsiveness to silver moves was excellent last year, but is decaying dramatically this year. With speculators and investors abandoning this sector, it’s barely budging. That has spawned a vicious circle convincing other traders to avoid silver stocks.

Silver stocks’ troubling lethargy is new this year. Back in December 2015 two days before the Fed’s first rate hike of this cycle, silver slumped to a major 6.4-year secular low in concert with gold. Silver stocks bottomed just over a month later in January 2016 paralleling the gold stocks. SIL fell to an all-time low in split-adjusted terms that day. A couple months earlier, Global X had executed a 1-for-3 reverse split in SIL.

Silver stocks were so deeply out of favor in late 2015 that this leading ETF’s managers feared SIL’s price would collapse low enough to risk delisting! Out of that very despair, strong new bull markets in silver and its miners’ stocks were born. In just 6.9 months from mid-January to mid-August 2016, SIL rocketed 247.8% higher on a 40.6% silver rally! That made for outstanding 6.1x upside leverage to silver prices.

Naturally silver and its miners’ stocks were soon sucked into gold’s correction following its own new bull’s initial upleg. Those silver and SIL corrections ballooned to monstrous proportions, thanks to gold-futures stops being run then Trump’s surprise election victory unleashing stock-market euphoria. So over the next 4.2 months, silver and SIL plunged 20.1% and 42.5%. SIL’s downside leverage to silver of 2.1x was modest.

2016’s behavior is the way silver stocks normally react to silver-price moves. The blue SIL and red silver lines above were closely intertwined last year. Silver stocks generally rallied and fell sharply in lockstep with silver itself. This normal behavior carried over into the first couple months of 2017, when SIL surged 33.6% between late December 2016 and early February 2017 on a mere 12.5% parallel rally in silver itself.

Silver stocks were leveraging silver’s upside by 2.7x, near the high end of their usual 2x to 3x range. So back in late January the silver stocks’ 2017 prospects looked really bullish. Things started going awry in February and March. The silver stocks corrected hard, plunging 21.1% in a month on a relatively-small 4.5% silver pullback. That made for big 4.7x downside leverage that was quite excessive, scaring traders.

So they started to flee silver miners’ stocks, a trend that’s continued ever since. With each subsequent silver rally since March, silver stocks have become less and less responsive to silver upside. This year’s blue SIL line above is no longer mirroring and amplifying the underlying volatility in the red silver line. It’s as if silver stocks are flatlining relative to silver, which is very strange. I can’t recall seeing anything like this.

Thus silver stocks have been stuck in a descending-triangle consolidation pattern for much of this year. They finally enjoyed breakouts from this triangle’s upper resistance and SIL’s 200-day moving average in August, mirroring similar major breakouts in gold stocks. But silver stocks’ responsiveness to silver continued decaying. In a month leading into early September, SIL only climbed 11.3% on an 11.5% silver rally.

Technically it looks like silver stocks have largely disconnected from silver. They’ve lapsed into this super-weird zombified comatose state. Speculators and investors alike aren’t the least bit interested in silver miners today, because they’re performing so poorly. And the resulting lack of participation in this sector scares away other traders, exacerbating the problem. Silver stocks have effectively been left for dead.

After decades studying and actively trading silver stocks, I’ve pondered this strange anomaly quite a bit in recent months. It’s certainly not fundamentally-driven, as silver miners’ earnings are looking good. It’s likely not technical either. While silver stocks are really underperforming, they haven’t suffered a serious selloff. SIL’s triangle support around $33 has held rock solid all year long, so this is a consolidation not a correction.

That leaves sentiment as the culprit behind silver stocks’ vexing stupor this year. Traders’ psychology is important in all markets, but disproportionately so in silver. Silver is a tiny highly-speculative market, exceptionally sensitive to shifting winds of sentiment. While weak technicals breed bearish sentiment and that becomes self-reinforcing, there had to be some root causes poisoning silver psychology earlier this year.

I suspect multiple factors are to blame. Once again silver sentiment is heavily dependent on gold. In the wake of Trump’s election win almost a year ago, stock markets soared in Trumphoria on hopes for big tax cuts soon. That hammered gold, which is hostage to stock-market fortunes. Gold is an anti-stock trade that usually moves counter to stock markets, so gold investment demand collapsed after the election.

Gold’s own psychology was utterly miserable late last year, exceedingly bearish. When gold fell to $1128 right after the Fed’s second rate hike of this cycle last December, Wall Street forecasts calling for a plunge under $1000 exploded. Traders don’t get interested in silver until gold is already rallying, so the extreme gold gloom and doom late last year certainly tainted silver sentiment. It has yet to recover from that.

Though gold bounced sharply and has enjoyed a good 2017, silver oddly didn’t join in. Gold itself likely played a major role. Despite gold’s gains this year, gold sentiment has remained pretty bearish. With the stock markets magically levitating in Trumphoria on those fervent big-tax-cuts-soon hopes, gold was flying under traders’ radars. With virtually no enthusiasm for gold, silver psychology had nothing to feed on.

The speculative traders who flock to silver for its sharp rallies and big gains were finding greener pastures elsewhere. Throughout the year various mainstream stock-market sectors have surged, so traders could find strong gains outside the precious metals. I’m certain this year’s extraordinary bitcoin bubble diverted interest away from silver too. The stratospheric skyrocketing of bitcoin prices has captivated traders.

Bitcoin’s value is hyper-speculative, as bitcoins are a synthetic virtual construct given perceived worth by software creating artificial scarcity. Having been in the financial-newsletter business for almost a couple decades now, I hear and read endless market anecdotes. This year I’m seeing the same types of traders who are usually interested in speculative silver raving about bitcoin instead. Bitcoin is a speculative mania!

Both in my own private feedback from countless traders around the world, and on the Internet’s popular gold and silver forums, the usual gold and silver conversations have shifted to gold and bitcoin this year. There’s no doubt bitcoin has stolen some limelight from silver, and almost certainly sucked away some of the capital that would’ve flowed into silver in 2017 too. Bitcoin is this year’s alternative speculation of choice.

But bitcoin’s meteoric rise won’t eclipse silver forever. Silver investment has been around for millennia, but bitcoin was just introduced in January 2009. As of this week bitcoin is up an astounding 485% YTD in 2017 alone! Such extreme vertical gains are never sustainable, as history has abundantly proven. So bitcoin’s epic competition this year for mindshare and capital from traditional silver speculators won’t last.

While bitcoin is definitely a factor in the lack of interest in silver and silver stocks this year, these record-high Trumphoria-goosed stock markets are far more important. As long as gold psychology is bearish as stocks seemingly do nothing but rally forever, silver’s speculative appeal will languish. Once these lofty stock markets inevitably roll over, gold and therefore silver investment will return to favor just like in early 2016.

Gold and silver slumped to brutal 6.1-year and 6.4-year secular lows in December 2015, everyone hated the precious metals. But the US stock markets finally succumbed to their first corrections in 3.6 years, an extreme near-record span. As the S&P 500 fell 12.4% in 3.2 months in mid-2015 followed by another 13.3% in 3.3 months into early 2016, long-neglected gold and silver demand returned with a vengeance.

Gold and silver surged 29.9% and 50.2% higher over the next half-year or so, igniting their first new bull markets in years! The next correction-grade stock-market selloff, over 10% on the S&P 500, will spark another renaissance in gold and silver investment demand. After being miraculously delayed for so long, that next major stock-market selloff is overdue and imminent. The risk factors stacking against stocks are legion.

The US stock markets are literally trading in bubble territory, over 28x earnings on the traditional trailing-twelve-month basis. They’ve rallied so long and so high that euphoria is extreme, with all measures of sentiment showing dangerous bull-slaying levels. And the Fed just birthed quantitative tightening for the first time in history, which is exceedingly bearish for these quantitative-easing-inflated artificial stock markets.

The stock markets finally decisively rolling over is the most-likely catalyst to shock silver and the stocks of its miners out of their comatose malaise. The silver stocks are perfectly poised for a first-half-of-2016-like scenario, where SIL rocketed 247.8% higher in just 6.9 months. The driver will be silver’s next major bull-market upleg. Silver remains radically undervalued relative to gold, thus enjoying colossal upside potential.

This next chart looks at the Silver/Gold Ratio, which simply divides the daily silver close by the daily gold close. Technically that results in little decimals that are hard to parse mentally, so I prefer using a scale-inverted gold/silver ratio which is the same thing. It yields more-meaningful whole numbers like 75.5 where the SGR stands today. This is way too low based on historical precedent, an unsustainable anomaly.

This week it took over 75 ounces of silver to equal the value of one ounce of gold. That’s a really-high SGR historically, meaning silver prices are really low relative to gold. Silver’s extreme undervaluation is a key reason speculators and investors aren’t interested in silver stocks today. That will change dramatically as silver inevitably resumes mean reverting higher relative to gold. Silver will outperform for a long time.

Before 2008’s stock panic, the SGR averaged 54.9. After the stock panic between 2009 to 2012, the SGR averaged 56.9. So outside of the extreme SGR anomalies driven by the stock panic and later the Fed’s QE3-conjured stock-market levitation from 2013 on, a mid-50s SGR is normal. This has proved true all throughout modern history due to geological and relative silver-and-gold supply-and-demand reasons.

During late 2008’s stock panic, the SGR briefly averaged an extremely-low 75.8. That soon gave way to a sharp mean reversion higher to reestablish silver’s usual relationship with gold. That mean reversion overshot dramatically, as is often the case with silver after an SGR extreme. In April 2011 when silver was enjoying mania-like popularity the SGR briefly peaked at 31.7! Silver’s upside is extreme after low SGRs.

Incredibly since Q4’15, when silver and gold hit their major 6-year secular lows, the SGR has averaged just 73.6. That’s not much better than late 2008’s stock-panic levels! So silver is long overdue to mean revert relative to gold, rallying much faster than gold for months on end until this relationship is restored. We don’t need to assume a likely overshoot, as a simple mean reversion alone would drive huge silver gains.

Assuming a 56 normal SGR, at this week’s $1280 gold price silver should be trading over $22.75. That’s 35% above prevailing price levels. But with gold itself readying to rally, silver’s mean-reversion targets climb much higher with gold prices. Another 30% gold upleg like in early 2016, which is modest by gold’s historical standards, would take it to $1665. At a 56 SGR, silver would have to soar 75% to around $29.75!

Since silver prices remain so depressed relative to their primary driver gold’s, the silver upside potential from here is enormous. This overdue silver mean reversion higher is what will shock silver stocks back to life. Once speculators and investors see silver starting to run, they are going to flood back into beaten-down silver stocks with reckless abandon. That will catapult this small sector radically higher like in early 2016.

The trigger reigniting silver will be gold powering higher, and again that will likely result from these crazy stock markets rolling over. Once these bubble-valued stock markets start decisively weakening, traders will rush to return to gold, silver, and their miners’ stocks to prudently diversify their stock-heavy portfolios. The Fed’s QT juggernaut ramping up over the next year will likely set this chain of events in motion.

Recent months’ comatose silver stocks are largely the product of general-stock euphoria leaving silver radically undervalued relative to gold. Silver psychology is very bearish, so traders aren’t the least bit interested in owning its miners. Sprinkle in the extreme allure of the bitcoin mania for the speculative traders who crave silver’s normal volatility, and that explains 2017’s serious anomaly in silver and silver stocks.

When this all changes, silver will move fast. This restless and volatile metal has a long history of drifting sideways and doing little. But occasionally the winds of sentiment shift enough to ignite enormous bull markets and uplegs generating fortunes. Traders who have the discipline to wait out silver’s sometimes-vexing consolidations are greatly rewarded when capital really flows into silver again, catapulting it far higher.

The greatest gains in this next major silver upleg won’t be won in silver-stock ETFs like SIL. They are burdened with too many companies that aren’t primary silver miners, the majority of their revenues come from other metals. So they aren’t very responsive to silver’s upside. But the purer individual silver miners with superior fundamentals will enjoy massive gains trouncing the ETFs. They are the best way to play silver.

The key to riding any silver-stock bull to multiplying your fortune is staying informed, both about broader markets and individual stocks. That’s long been our specialty at Zeal. My decades of experience both intensely studying the markets and actively trading them as a contrarian is priceless and impossible to replicate. I share my vast experience, knowledge, wisdom, and ongoing research through our popular newsletters.

Published weekly and monthly, they explain what’s going on in the markets, why, and how to trade them with specific stocks. They are a great way to stay abreast, easy to read and affordable. Walking the contrarian walk is very profitable. As of the end of Q3, we’ve recommended and realized 967 newsletter stock trades since 2001. Their average annualized realized gain including all losers is +19.9%! That’s hard to beat over such a long span. Subscribe today and get invested before silver stocks power way higher!

The bottom line is silver stocks have largely drifted comatose this year, with decaying responsiveness to silver moves. The extreme stock-market euphoria has left gold psychology bearish, bleeding into silver sentiment. And the spectacular bitcoin bubble has diverted speculative traders’ interest and capital away from silver as well. All this has led traders to largely abandon silver miners, condemning their stocks to consolidate.

But the likely catalyst to shock silver stocks from their zombified stupor is nearing with each passing day. Once these QE-inflated stock markets inevitably succumb to QT, gold and silver investment demand will return. The tiny silver market will rapidly surge on major capital inflows, with lots of room to mean revert far higher relative to gold. Then speculators and investors alike will rush to buy the cheap silver miners’ stocks.

Adam Hamilton, CPA

October 20, 2017

Copyright 2000 – 2017 Zeal LLC (www.ZealLLC.com)

The silver miners’ stocks have largely languished this year, grinding sideways near lows for months on end. This vexing consolidation has fueled near-universal bearishness, leaving silver stocks deeply out of favor. But once a quarter when earnings season arrives, hard fundamentals pierce the obscuring veil of popular sentiment. The silver miners’ recently-reported Q2’17 results reveal today’s silver prices remain profitable.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. These are generally due by 45 days after quarter-ends in the US and Canada. They offer true and clear snapshots of what’s really going on operationally, shattering the misconceptions bred by the ever-shifting winds of sentiment. There’s no silver-miner data that is more highly anticipated than quarterlies.

Silver mining is a tough business both geologically and economically. Primary silver deposits, those with enough silver to generate over half their revenues when mined, are quite rare. Most of the world’s silver ore formed alongside base metals or gold, and their value usually well outweighs silver’s. So typically in any given year, less than a third of the global mined silver supply actually comes from primary silver mines!

The world authority on silver supply-and-demand fundamentals is the Silver Institute. Back in mid-May it released its latest annual World Silver Survey, which covered 2016. Last year only 30% of silver mined came from primary silver mines, a slight increase. The remaining 70% of silver produced was simply a byproduct. 35% of the total mined supply came from lead/zinc mines, 23% from copper, and 12% from gold.

As scarce as silver-heavy deposits supporting primary silver mines are, primary silver miners are even rarer. Since silver is so much less valuable than gold, most silver miners need multiple mines in order to generate sufficient cash flows. These often include non-primary-silver ones, usually gold. More and more traditional elite silver miners are aggressively bolstering their gold production, often at silver’s expense.

So the universe of major silver miners is pretty small, and their purity is shrinking. The definitive list of these companies to analyze comes from the most-popular silver-stock investment vehicle, the SIL Global X Silver Miners ETF. This week its net assets are running 6.0x greater than its next-largest competitor’s, so SIL really dominates this space. With ETF investing now the norm, SIL is a boon for its component miners.

While there aren’t many silver miners to pick from, major-ETF inclusion shows silver stocks have been vetted by elite analysts. Due to fund flows into top sector ETFs, being included in SIL is one of the important considerations for picking great silver stocks. When the vast pools of fund capital seek silver-stock exposure, their SIL inflows force it to buy shares in its underlying companies bidding their prices higher.

Back in mid-August as the major silver miners finished reporting their Q2’17 results, SIL included 29 “silver miners”. This term is used loosely, as SIL includes plenty of companies which can’t be described as primary silver miners. Most generate well under half their revenues from silver, which greatly limits their stock prices’ leverage to silver rallies. Nevertheless, SIL is today’s leading silver-stock ETF and benchmark.

The higher the percentage of sales any miner derives from silver, naturally the greater its exposure to silver-price moves. If a company only earns 20%, 30%, or even 40% of its revenues from silver, it’s not a primary silver miner and its stock price won’t be very responsive to silver itself. But as silver miners are increasingly actively diversifying into gold, there aren’t enough big primary silver miners left to build an ETF alone.

Every quarter I dig into the latest results from the major silver miners of SIL to get a better understanding of how they and this industry are faring fundamentally. I feed a bunch of data into a big spreadsheet, some of which made it into the table below. It includes key data for the top 17 SIL component companies, an arbitrary number that fits in this table. That’s a commanding sample at 93.2% of SIL’s total weighting.

While most of these top 17 SIL components had reported on Q2’17 by mid-August, not all had. Some of these major silver miners trade in the UK or Mexico, where financial results are only required in half-year increments. If a field is left blank in this table, it means that data wasn’t available by the end of Q2’s earnings season. Some of SIL’s components also report in gold-centric terms, excluding silver-specific data.

In this table the first couple columns show each SIL component’s symbol and weighting within this ETF as of mid-August. While most of these silver stocks trade in the States, not all of them do. So if you can’t find one of these symbols, it’s a listing from a company’s primary foreign stock exchange. That’s followed by each company’s Q2’17 silver production in ounces, along with its absolute year-over-year change.

After that comes this same quarter’s gold production. Pretty much every major silver miner in SIL also produces significant-if-not-large amounts of gold. While gold stabilizes and augments the silver miners’ cash flows, it also retards their stocks’ sensitivity to silver itself. Naturally investors and speculators buy silver stocks and their ETFs because they want leveraged upside exposure to silver’s price, not gold’s.

So the next column reveals how pure the elite SIL silver miners are. This is mostly calculated by taking a company’s Q2 silver production, multiplying it by Q2’s average silver price, and then dividing that by the company’s total quarterly sales. If miners didn’t report Q2 revenues, I approximated them by adding the silver sales to gold sales based on their quarterly production and these metals’ average second-quarter prices.

Then comes the most-important fundamental data for silver miners, cash costs and all-in sustaining costs per ounce mined. The latter determines their profitability and hence ultimately stock prices. Those are also followed by YoY changes. Finally comes the YoY changes in cash flows generated from operations and GAAP profits. But an exception is necessary for companies with numbers that crossed zero since Q2’16.

Percentage changes aren’t relevant or meaningful if data shifted from negative to positive or vice versa. Plenty of major silver miners suffered net losses in Q2’17 after earning profits in Q2’16. So in cases where data crossed that zero line, I included the raw numbers instead. This whole dataset offers a fantastic high-level fundamental read on how the major silver miners are faring today, and it’s reasonably well.

That’s reassuring given silver’s serious under-performance relative to gold this year. As a far-smaller market, silver usually amplifies gold’s advances by at least 2x. But as of the end of Q2, silver was only up 4.5% YTD compared to 7.9% for gold. That’s dismal 0.6x leverage. And by mid-August as Q2’s earnings season wrapped up, silver’s YTD gain of 4.6% fell even further behind gold’s 10.6%. That’s horrible 0.4x leverage!

Production is the lifeblood of mining companies, and thus the best place to start fundamental analysis. In Q2’17, these top 17 SIL components collectively produced an impressive 78.6m ozs of silver. If 2016’s world-silver-mining run rate is applied to this year’s second quarter, that implies 221.5m ozs of silver mined. Thus these top SIL silver miners would account for over 35% of that total, they truly are major silver players.

But these elites still weren’t able to significantly grow their collective silver production, it was up just 0.9% YoY. Instead they invested heavily in expanding their gold production, which surged 6.4% YoY to 1354k ounces. Interestingly 10 of these top 17 SIL components, a majority representing 45.3% of SIL’s total weighting, are also included in the leading GDX gold miners’ ETF. SIL is mostly made up of primary gold miners!

Many of these elite major silver miners don’t just mine gold as a silver byproduct, but actually operate at least one primary gold mine. The silver miners have collectively decided to diversify into gold due to its superior economics. Consider hypothetical mid-sized silver and gold miners, which might produce 10m and 300k ounces annually. What would those cash flows look like at last quarter’s average metals’ prices?

In Q2’17, silver and gold averaged $17.18 and $1258. Silver was up 2.3% YoY, while gold slipped by a slight 0.1% YoY. At 10m ounces, that silver miner would generate $172m in sales. But the similar-sized gold miner’s sales of $377m more than doubles that. At recent years’ prevailing prices, the cash flows from gold mining are much more robust than those from silver mining. That makes it easier to pay bills and expand.

Silver mining is often as capital-intensive as gold mining, requiring similar large expenses for planning, permitting, and constructing mines and mills to process ore. Similar heavy excavators and haul trucks are necessary to dig and haul the ore, along with similar staffing levels to run mines. So silver’s lower cash flows to support all this activity make silver mining harder than gold mining, which isn’t lost on silver miners.

Silver-mining profits do skyrocket when silver soars occasionally in one of its massive bull markets. But during silver’s long intervening drifts at relatively-low price levels, the silver miners often can’t generate sufficient cash flows to finance expansions. So the top silver miners are increasingly looking to gold, a trend that isn’t likely to reverse given the relative economics of silver and gold. Primary silver miners are getting rarer.

Technically a company isn’t a primary silver miner unless it derives over half its revenues from silver. In Q2’17, the average sales percentage from silver of these top SIL components was just 37.6%! That is right on trend over this past year, with Q2’16, Q3’16, Q4’16, and Q1’17 weighing in at 46.3%, 38.5%, 40.5%, and 37.9%. In Q2’17, only 5 of the top SIL component companies qualified as primary silver miners!

While I understand this, as a long-time silver-stock investor it saddens me primary silver miners have apparently become a dying breed. When silver starts powering higher in one of its gigantic uplegs and way outperforms gold again, this industry’s silver percentage will rise. But unless silver not only shoots far ahead but stays there while gold lags, it’s hard to see major-silver-mining purity significantly reversing.

Unfortunately SIL’s mid-August composition was such that there wasn’t a lot of Q2 cost data reported by its top component miners. 3 of its top 4 companies trade in the UK and Mexico, where reporting only comes in half-year increments. Lower down the list there are more half-year reporters, an explorer with no production, and primary gold miners that don’t report silver costs. So silver cost data was fairly scarce.

Nevertheless, it’s always useful to look at the data we have. Industry wide silver-mining costs are one of the most-critical fundamental data points for silver-stock investors. As long as the miners can produce silver for well under prevailing silver prices, they remain fundamentally sound. Cost knowledge helps traders weather this sector’s fear-driven plunges without succumbing to selling low like the rest of the herd.

There are two major ways to measure silver-mining costs, classic cash costs per ounce and the superior all-in sustaining costs. Both are useful metrics. Cash costs are the acid test of silver-miner survivability in lower-silver-price environments, revealing the worst-case silver levels necessary to keep the mines running. All-in sustaining costs show where silver needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of silver, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q2’17, these top 17 SIL-component silver miners that reported cash costs averaged $6.34 per ounce. That surged a major 19.1% YoY from Q2’16’s $5.32, which seems like a troubling omen.

But it’s not. Flighty silver-stock investors are always on the verge of panicking, fleeing this volatile and psychologically-challenging sector. But the only event worthy of such extreme bearishness would be prevailing silver prices falling near cash costs. And even at $6.34-per-ounce cash costs and today’s low silver, a vast buffer exists. There’s no way silver is going to plummet down under $7 in any conceivable scenario!

These high cash costs are actually an anomaly mainly driven by two companies. First, SSR Mining (TSX: SRR) is now winding down its rapidly-depleting silver mine as planned. It produced 10.4 million ounces of silver in 2016, but only 5.5m is forecast this year! As silver throughput drops each quarter, the per-ounce costs are rising. Without SSRM’s outlying super-high cash costs, the rest of these top SIL miners averaged just $5.51.

Another company Silvercorp Metals (TSX: SVM) had slid out of SIL’s top 17 components as of mid-August. It was the 18th one, removing it from this particular calculation. Due to SVM’s enormous lead and zinc byproducts, its costs are the lowest in the industry. In Q2’16 it reported cash costs of $0.08 per ounce, which really dragged down that comp-quarter average. So the major silver miners’ collective cash costs were just fine in Q2.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain a silver mine as an ongoing concern. AISC include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current silver-production levels.

These additional expenses include exploration for new silver to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee silver mines. All-in sustaining costs are the most-important silver-mining cost metric by far for investors, revealing silver miners’ true operating profitability.

In Q2’17, these top 17 SIL components reporting AISC averaged $11.66 per ounce. That was up 16.0% YoY from Q2’16s $10.05. Coeur Mining was a big factor, with AISC surging 19% to a lofty $15.90 per ounce! That was due to lower-grade ore on the way to better zones. Ex-CDE, this average ran $10.96 which was closer to year-ago levels. SVM was also a factor, with low $7.06 AISC feeding into Q2’16 comps.

Two other elite silver miners suffered major production problems in Q2’17, resulting in big production drops. With fewer ounces to spread mining’s heavy fixed costs across, all-in sustaining costs soared. First Majestic Silver (TSX: FR), the purest major silver miner at 65.4% of Q2 revenues, saw production fall 20% YoY which forced AISC 33% higher. Unprecedented labor unrest in Mexico temporarily halted 3 of its 6 silver mines.

Those issues have since been resolved, so AG’s production should bounce back in Q3 which will push its AISC back down. Meanwhile Tahoe Resources (TSX: THO) saw its Q2 production plunge 28% YoY forcing its own AISC 23% higher. It got sucked into a legal battle between anti-mining activists and the government of Guatemala where its silver mine is. That mining license was temporarily suspended for an unmerited lawsuit.

The activists allege the government shouldn’t have granted Tahoe its Escobal mining license in the first place because it didn’t consult with a particular indigenous tribe first. But those people don’t even live anywhere near the mine site, it’s ridiculous! Tahoe doesn’t know when Escobal operations will be allowed to resume, but estimates a range between a couple months from now out to 18 months for a full resolution.

Tahoe’s large gold production from its two other gold mines in Peru, 110k ounces in Q2’17, ensures it won’t have any serious problems weathering this Guatemalan nightmare. But the point for our purposes today is that anomalous special situations fed the steep jump in the major silver miners’ all-in sustaining costs in Q2. But even at these elevated levels, this industry is still enjoying hefty silver-mining margins.

At $11.66 AISC, the major silver miners still earned big profits in the second quarter. Once again silver averaged $17.18, implying fat profit margins of $5.52 per ounce or 32%! Most industries would kill for such margins, yet silver-stock investors are always worried silver prices are too low for miners to thrive. That’s why it’s so important to study fundamentals, because technical price action fuels misleading sentiment!

Today’s silver price remains really low relative to prevailing gold levels, which portends huge upside as it mean reverts higher. The long-term average Silver/Gold Ratio runs around 56, which means it takes 56 ounces of silver to equal the value of one ounce of gold. Silver is really underperforming gold so far in 2017, with the SGR averaging just 72.6 YTD as of mid-August. So silver is overdue to catch up with gold.

At a 56 SGR and $1300 gold, silver is easily heading near $23.25. That’s 35% above its Q2 average. Assuming the major silver miners’ all-in sustaining costs hold, that implies profits per ounce soaring 110% higher! Plug in a higher gold price or the typical mean-reversion overshoot after an SGR extreme, and the silver-mining profits upside is far greater. Silver miners’ inherent profits leverage to rising silver is incredible.

Still Q2’17’s relatively-weak silver price weighed on miners’ cash flows generated from operations and GAAP accounting profits. Despite their big gold production, operating cash flows plunged 28.4% YoY to $1038m for these top SIL components. That’s not quite a righteous comparison though, because only 13 of this year’s top 17 had reported Q2 financial results by mid-August. Last year that number totaled 15.

And one of the silver miners not reporting OCF by the usual Q2 deadline this year was the Mexican silver giant Fresnillo (NASDAQ: FNLPF). Its OCF last year was fully 1/6th of these top SIL components’ total! So their operating-cash-flows situation in Q2’17 is nowhere near as bad as the drop implies. The same is true on the GAAP-earnings front. Last year Fresnillo contributed nearly 22% of the profits of these top 17 SIL components.

Another huge Mexican silver miner, the conglomerate Industrias Penoles (NASDAQ: IPOAF), saw its profits plunge about $140m YoY. These two Mexican silver giants alone account for the entire drop in these top SIL miners’ profits in Q2’17, which plummeted 57.5% YoY or $221m. Without them, silver-mining profits were flat. That’s pretty darned good considering all the super-anomalous company-specific problems that plagued Q2 results.

Silver miners’ earnings power and thus stock-price upside potential will only grow as silver mean reverts higher. In mining, costs are largely fixed during the mine-planning stages. That’s when engineers decide which ore bodies to mine, how to dig to them, and how to process that ore. Quarter after quarter, the same numbers of employees, haul trucks, excavators, and mills are generally used regardless of silver prices.

So as silver powers higher in coming quarters, silver-mining profits will really leverage its advance. And that will fundamentally support far-higher silver-stock prices. The investors who will make out like bandits on this are the early contrarians willing to buy in low, before everyone else realizes what is coming. By the time silver surges higher with gold so silver stocks regain favor again, the big gains will have already been won.

While investors and speculators alike can certainly play the silver miners’ ongoing mean-reversion bull with this leading SIL ETF, individual silver stocks with superior fundamentals will enjoy the best gains by far. Their upside will trounce the ETFs’, which are burdened by companies that don’t generate much of their sales from silver. A handpicked portfolio of purer elite silver miners will yield much-greater wealth creation.

At Zeal we’ve literally spent tens of thousands of hours researching individual silver stocks and markets, so we can better decide what to trade and when. As of the end of Q2, this has resulted in 951 stock trades recommended in real-time to our newsletter subscribers since 2001. Fighting the crowd to buy low and sell high is very profitable, as all these trades averaged stellar annualized realized gains of +21.2%!

The key to this success is staying informed and being contrarian. That means diligently studying and buying great silver stocks before they grow popular again, when they’re still cheap. An easy way to keep abreast is through our acclaimed weekly and monthly newsletters. They draw on our vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. For just $10 per issue, you can learn to think, trade, and thrive like contrarians. Subscribe today and get deployed in great silver stocks before they surge far higher!

The bottom line is the major silver miners fared fine in Q2 despite some real challenges. A combination of silver continuing to seriously lag gold, along with anomalous company-specific problems, weighed on miners’ collective results. Yet they continued to produce silver at all-in sustaining costs way below Q2’s low prevailing silver prices. And their accelerating gold-production growth leaves them financially stronger.

With silver-stock sentiment remaining excessively bearish, this sector is primed to soar as silver itself continues mean reverting higher to catch up with gold’s current upleg. The silver miners’ profits leverage to rising silver prices remains outstanding. After fleeing silver stocks so aggressively this year, investors and speculators alike will have to do big buying to reestablish silver-mining positions. That will fuel major upside.

Adam Hamilton, CPA

September 1, 2017

Copyright 2000 – 2017 Zeal LLC (www.ZealLLC.com)

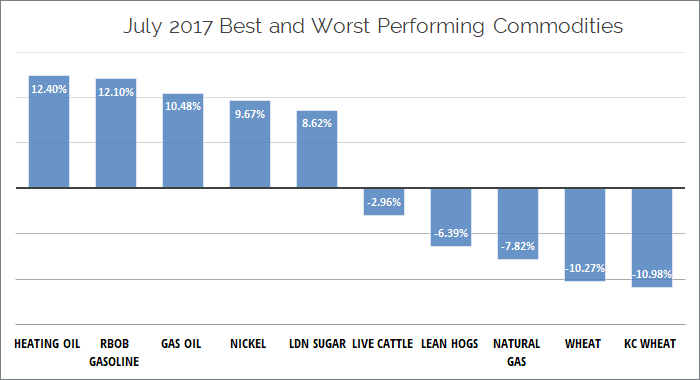

In July, the Rogers International Commodity Index (RICI) had its best month since September, 2016, according to Price Asset Management, a US-based firm that manages a commodity fund based on the RICI index.

The index was up 3.13%, slightly ahead of the benchmark Bloomberg Commodity Index (BCOM) which was up 2.26%.The RICI is a composite, US dollar-based index designed by legendary commodity investor Jim Rogers Jr. in the late 1990’s. Metals continue to be the leading sector as both precious and industrial metals are showing strength as a result of continued strong fundamentals and global disturbances supporting precious metals.

For the year, the RICI was down 2.82% versus a 3.12-per-cent downturn in the BCOM. July was the first month of 2017 where commodities outperformed US Equities, with the S&P 500 Index up 2.06%. The increase in the RICI was very broad based as 29 of the 37 components were positive for the month. The index was led by the energy sector which was up 6.68%, followed by metals up +2.51% and agriculture down a slight 0.42%, For the year so far, metals continue to be the leading sector as both precious and industrial metals are showing broad strength as a result of continued strong fundamentals and global unrest supporting precious metals. Tin was the only metal in the negative at 1.46% for the year.

According to Alan Konn, Managing Director of Price Asset Management LLC, commodities, after an extensive bear market, are now up over +15% from a low in February of 2016. Prices of the RICI components are on average still 50% below their highs. He notes that the recovery has started with tremendous pressure on producers due to the prolonged downturn which has caused marginal production and capital expenditures to be cut. With the possibility of rising interest rates, increased inflation expectations, and fiscal stimulus in the form of global infrastructure spending replacing quantitative easing; the global macro outlook appears decidedly positive. These global macro forces that should be positive for some commodities but may also cause problems in other asset classes.

About the Rogers International Commodity Index:

The Rogers International Commodity Index® (RICI®) was developed by Jim Rogers to be an international, diversified, investable raw materials index. The RICI® currently has thirty-seven commodities representing the energy, metals, and agricultural sectors. The index is a basket of commodities consumed in the global economy. The index’s weightings attempt to balance consumption patterns worldwide (in developed and developing countries) with specific future contract liquidity. The value of this basket is tracked via futures contracts on 37 different exchange-traded physical commodities, quoted in four different currencies, on nine exchanges in four countries.

About Price Asset Management LLC:

Price Asset Management, LLC (PAM) has been registered with the CFTC as a Commodity Trading Advisor (CTA) and a Commodity Pool Operator (CPO) since 2000, and has been managing its main commodities fund since 2007. PAM is an SEC Registered Investment Advisor, a member of the National Futures Association (NFA), and has adopted the Global Investment Performance Standards (with independent verification) and the CFA Institute Asset Manager Code of Professional Conduct. PAM operates with robust compliance and risk management, offsite IT redundancy, business continuity and disaster recovery planning, with external audit and fund administration.

(Sources: Price Asset Management, July 2017 Update)

Yesterday evening, Tahoe Resources Inc. (T:THO) reported its second quarter 2017 financial results of US$33.48-million. Daniel Earle of TD Securities found the results mixed. Earnings per share (EPS) beat on lower costs and the company suspended its dividend, which TD securities believes is prudent. Q2/17 adjusted EPS of $0.11 were above TD estimates of $0.08 (street consensus: $0.09) due to lower costs and expenses generally. Operating Cash Flow of $0.26 was above TD’s estimate of $0.22 (consensus: $0.23) and Haywood Securities estimate of ~US$0.20. However, the company suspended its multi-year guidance given the uncertainty at the Escobal silver mine.

On July 5, the company reported that the Supreme Court of Guatemala had issued a provisional decision to suspend the company’s Escobal mining license. The company has appealed the decision to the Constitutional Court and a ruling could come within the next three months. The company is are seeking to have its Escobal mining license reinstated during this period. TD securities is accounting for no production from Escobal for one year. The Casillas road block that is still in place, and reportedly shows no sign of immediate resolution. In a note to clients today, Geordie Mark of Haywood Securities notes that both the road block and the provisional decision to suspend the Escobal mining licence need to be resolved prior to operations returning. The Casillas road block is still in place, and there are reportedly no signs of immediate resolution to this situation.

Preliminary production results were released, with the company having reported production greater than 4 Moz Silver (Ag) and greater than 110 koz Au. Q2/17 total cash costs were not previously reported and were better than we anticipated. Until further clarity is obtained at Escobal, the company’s 2017 and multi-year guidance has been suspended and certain exploration and capital spending programs are being reviewed. 2017 gold guidance remained unchanged at 375-425 koz Au at total cash costs of $700-$750/oz.

The company has also deferred the La Arena II PEA and an investor day that was planned for mid-September. La Arena produced 48 koz gold at a cash cost of US$579/oz. Gold production was higher than our estimates (46 koz gold) on placing less (3.2 Mt vs 3.7 Mt) higher grade (0.46 g/t vs 0.43 g/t gold) on the leach pads. Cash costs bettered our forecast of US$670/oz.

Management reported that it views its expansion plans at the Shahuindo and Timmins mines as budgeted and required and that these projects are on track for completion in mid-2018. Shanuindo produced 21 koz gold, which was higher than Haywood Securities estimates of 15.4 koz gold, by placing more (1.3 Mt vs 0.98 Mt) tonnes of lower grade (0.65 g/t vs 0.73 g/t gold) on the leach pad. Reported cash costs of US$590/oz were much lower than their expectations of US$845/oz. Timmins Mines produced 41 koz gold that was lower than expectations (44 koz gold) on processing slightly more (356 kt vs 314 kt) lower grade (3.75 g/t vs 4.56 g/t gold) ore. Gold recoveries of 97% were slightly higher than the Haywood estimate of 96%. Cash cost of US$633/oz were marginally higher than Haywood’s estimates of US$632/oz

The company generated positive free cash flow (FCF) of $17 million in the second quarter of 2017, after spending $63 million in total capital expenditures. Haywood expects capex to increase in the second half of 2017. As at June 30, the company had cash and equivalents of $191 million and $35 million of debt due in April 2018. The company currently has access to $75 million from its undrawn credit facility.

On the year, shares in Tahoe Resources (T:THO) are down from a 12-month high of $22.11 and at time of publication, shares were trading down 25 cents to $6.35 on 3.6 million shares traded for the day, near 12-month lows. TD Securities provided a recommendation of hold and a high risk rating with a 12-month price target of $8.50. However, TD Securities may want to revise its price target given the uncertainty at Escobal and other brokerages price targets. Haywood Securities in a note to clients today maintained its hold rating with a price target of $6.75 (revised down from $7.25) with a high risk rating for shares of Tahoe. Significant upcoming catalysts will be any updates at the Escobal mine which should be expected in the second half of 2017.

With money markets and Treasuries yielding next to nothing these days, investors are finding income in new places. One area those investors should consider is gold mining. With gold rising in value, mining companies are reaping record profit margins, yet the stock prices are depressed due to lack of investor interest. A solution for both gold companies and investors may be dividends, specifically gold-linked dividends.

Several top-tier gold producers that are benefiting from higher gold prices have begun to share a portion of their profits with shareholders via a dividend payout. Thirteen of the world’s largest gold producers are expected to pay nearly $2 billion in dividends this year, according to MineFund, making it the largest payment in gold stock history. The Financial Post also reported that miners’ dividend payments are up 75 percent on a year-over-year basis, compared to a 26 percent increase in 2010.

Yamana Gold (TSX:YRI) is just one of several large producing miners to report increased revenues, expanding cash flows and record adjusted earnings. Because of the company’s strong balance sheet, Yamana increased its dividend for the second time this year to $0.20 per share annually. When discussing the enhanced payouts, CEO Peter Marrone cited that the company “continued to focus on delivering growth across all measures, enhancing shareholder value and generating significant cash flow in the third quarter.”

The latest payout represents a 67 percent increase over the past 12 months and the second increase this year.

Other miners, such as Newmont Mining (NYSE:NEM), have implemented a gold-linked dividend, which means that the amount of the dividend the shareholder receives will be linked to the average price of gold. As the yellow metal trades higher, the company would increase dividends paid out to its investors. Conversely, if gold falls in value, dividend payouts would decrease.

Eldorado Gold (TSX:ELD) has also come out with a similar dividend policy, linking dividends to the price of gold. As shown in the chart below, Eldorado Gold anticipates its next dividend payout will be 67 percent higher than the previous quarter.

Barrick Gold (TSX:ABX) also announced a third quarter dividend increase during its earnings release. Over the past five years, the company has increased its dividend by more than 170 percent on a quarterly basis. The company’s latest dividend—$0.15 per share— represents a 25 percent increase from the prior quarter.

Barrick estimates its third quarter gold cash margins have increased by 55 percent on a year-over-year basis, driven by the company’s leverage to higher gold prices. The company says it will continue to offer its shareholders a rising income stream while also expanding operations in Pueblo Viejo, Pascua-Lama and Nevada.

While the share prices of these miners have been punished in 2011, increasing dividends allow investors to get “paid to wait” for the market to turn around. The dividends are a cash incentive for investors to hold shares of the company and allow them to participate in rising earnings. We like that idea.

From the article entitled, “Get Paid to Play Gold” by Frank Holmes. Frank Holmes is chief executive officer of U.S. Global Investors – a registered investment adviser that manages approximately $2.8 billion. The information provided herein has been provided to MiningFeeds.com by the author and, as such, is subject to our disclaimer: CLICK HERE.

Here are your “Movers and Shakers” for the week ending September 16th, 2011 on the TSX and TSX-V Exchanges. In no particular order, these are the 10 mining companies that caught our eye this week.

Here are your “Movers and Shakers” for the week ending September 16th, 2011 on the TSX and TSX-V Exchanges. In no particular order, these are the 10 mining companies that caught our eye this week.

1. Dalradian Resources Inc. (TSX: DNA)

Dalradian Resources was this week’s top TSX-listed mining stock percentage gainer posting a gain of 27.8%. Dalradian will be added to the S&P/TSX SmallCap Index on Monday, September 19th. Earlier this month, the company announced intersecting 3.2m grading 5.34g/t Au at its Curraghinalt Deposit in Northern Ireland.

2. TerraX Minerals Inc. (TSX-V: TXR)

On the TSX Venture board, TerraX Minerals posted a weekly gain of 37.9% which made it the number one mover this week. On Wednesday, September 14th, the company announced it intersected a porphyry-style alteration with significant sulphides at its Stewart gold-copper property in Newfoundland.

3. Aura Minerals Inc. (TSX: ORA)

Aura Minerals chalked up an 11.6% loss this week which marked the largest decline for a TSX-listed mining stock. Aura closed down $0.20 on Friday to end the week at $1.53. The company has faced a host of operational problems and the loss of its chief executive officer. In July, Dundee Capital Research analyst Ron Stewart noted, “No question in our mind, Aura has had the proverbial stuffing knocked out of it in the market.” At the time, Aura was trading at $2.13 and Stewart issued a $3.00 target on the company’s stock.

4. Copper One Inc. (TSX-V: CUO)

Copper One was off 17.5% this week which marked the biggest drop for any widely traded TSX-V listed mining stock. Volume was up considerably on Friday with over 1.4 million shares traded. The company’s stock was off $0.07 on the day to close at $0.33 on no news. On July 8th, Copper One annouced that exploration work on the Rivière Doré project in Quebec was being put on hold. At the time, the company’s shares were trading at $0.70.

5. Avion Gold Corp. (TSX: AVR)

Avion Gold was the most actively traded issuer on the TSX Exchange on Friday with over 33 million shares trading hands. The company was up $0.08 on the week to close at $2.54. Avion Gold is being added to the TSX Global Gold and Global mining Indexes effective Monday, September 19th, 2011.

6. Silver Wheaton Corp. (TSX: SLW)

Silver Wheaton was the second most actively traded stock on Friday on the TSX Exchange with almost 24 million shares traded. On Monday, September 19, 2011 Silver Wheaton will be added to the TSX 60 Index. Also upcoming, third quarterly cash dividend payment for 2011 of US$0.03 per common share will be paid to holders of record of its common shares as of the close of business on September 20, 2011.

7. Allana Potash Corp. (TSX:AAA)

This week marked the first full week of trading on the TSX for Allana Potash. The company graduated to the TSX on Friday, September, 9th. On Thursday, September 15, Allana Potash announced drill results from the company’s potash project in Ethiopia which included 8 meters of 18.54% KCl. About the news, Company President & CEO Farhad Abasov stated, “Allana management believes that the potash in this region may be amenable to mining by open pit methods and future studies will focus on this potential.”

8. Silvercorp Metals Inc. (TSX: SVM)

Silvercorp Metals was in the headlines all week after the B.C. Securities Commission announced last Friday it was conducting a regulatory investigation into anonymous allegations against the company. A second set of allegations were published on the internet this week and the company’s Chairman Dr. Rui Feng invited the authors responsible for the accusations to “come out of the shadows and participate with the regulators in their investigations“. This week the company bought back over $31 million of its own shares through a normal course issuer bid.

9. Copper Fox Metals Inc. (TSX-V: CUU)

B.C. copper miner Copper Fox intends to raise an additional $2-million via a private placement bringing the total private placement proceeds of its recently announced financing to $5-million. The offering is expected to consist of 3,333,334 units at a purchase price of $1.50 per unit. Each unit consists of one common share of Copper Fox and one-half common share purchase warrant of Copper Fox. Each whole warrant entitles the holder to acquire one common share of Copper Fox at an exercise price of $1.75 for one year.

10. Passport Potash Inc. (TSX-V: PPI)

Passport Potash was also in the B.C. Securities Commission spotlight this week when, on Monday, the regulator expressed concern that the company may be in possession of the results of an economic analysis for the Holbrook project that had not been disclosed through a news release and material change report. The company’s shares are down $0.09 on the week closing at $0.47.

The British Columbia Securities Commission said on Friday it’s conducting a regulatory investigation into anonymous allegations against Silvercorp Metals (TSX: SVM), a Vancouver-based company with silver mines in China.

The regulator said that certain allegations were made against the company in an anonymous letter dated August 29th, 2011 addressed to the Ontario Securities Commission and various media outlets.

“This is a departure from the BCSC’s usual policy of keeping investigations confidential, but we feel it is necessary in order to conduct a balanced and thorough review to publicly ask the author of the complaint to come forward,’’ said Lang Evans, Director of Enforcement for the BCSC. The news of the investigation came after Silvercorp shares fell 6% on Friday to $8.39. In the past year, the stock has traded between $15.60 and $6.92.

On September 2nd, the company issued a statement saying it had received the anonymous letter which was also addressed to the company’s auditors. The company said the central allegation is that while Silvercorp reported a net profit of US$66 million to the U.S. Securities & Exchange Commission in calendar 2010, financials purportedly available from the Chinese State Administration of Industry and Commerce shows Silvercorp reporting a loss of US$500,000 for calendar 2010. The letter also alleges that the company’s cash position is grossly overstated.

“This type of manipulative scheme is baseless and which depresses our share price and harms our shareholders,’’ said Silvercorp Chief Executive Officer Rui Feng. Silvercorp noted there has been a dramatic increase in the short position of its shares over the past two months, approximately 23 million, or 13% of the total outstanding shares.

This is not the first case of questionable accounting to hit a Chinese TSX-listed company. On June 8th, 2011, Sino Forest Corporation (TSX:TRE) confirmed that the Ontario Securities Commission opened an investigation concerning the company and the unusual trading activity and volatility associated with the company’s stock in response to a report issued by Muddy Waters Research.

With three projects in Asia’s leading economy, the company reportedly accounts for roughly 5% of the China’s silver output. The BCSC is asking the author of the complaint, or anyone else who may have information related to the allegations, or the identity of the author, to contact them.

CLICK HERE – for our Silver Issue where Silvercorp Metals was profiled in 10 Most Interesting Silver Stocks.

World production of the gray precious metal rose again in 2010. Silver, unlike gold, has seen production levels increase since 2003. This difference in production between gold and silver is not a coincidence due to geology and the history of their production.

World production of silver in 2010 was 713 million ounces. Silver production increased by 1.8% since 2009, 59.7% since its low in 1994 and 161.9% since 1968. In comparison, gold production increased by 8.7% since 1994 and 70% since 1968. World production of silver in 2010 has naturally increased with the increase in the combined production of copper, zinc and gold. This increase has resulted, somewhat mechanically, from the increased production of other metals around the world. Over two thirds of the production of silver is not from primary silver mines but from mine bi-products that produce zinc, copper, lead and gold.

World production of silver by country.

In 2010 Peru remains the world’s number one producer of silver. Silver production in Peru was 123.7 million ounces this past year, down by 1.3% when compared to 2009. The main silver mine in Peru produced 14.9 million ounces (12% of silver production in Peru). The mine is a primary copper mine which also produces silver. The second largest silver mine in Peru produced 10 million ounces (8% of silver production in Peru) and the third 8.6 million ounces (7% of silver production in Peru). The first three mines produce a quarter of the country’s silver, the rest is supplied by more than 140 mines.

Mexico is the second largest producer of silver in 2010. Production declined slightly from 114.1 to 112.5 million ounces of silver. The first number one mine in Mexico produced 35.9 million ounces of silver in 2010, one third of the country’s production and 5% of world production of silver in 2010. This mine is the second biggest silver mine in the world and also produces gold, lead and zinc.

China, number one in zinc, lead and gold, is the third largest producer of silver. China’s silver production continues to grow in 2010, up from 93.2 to 96.4 million ounces of silver. The largest silver mine in China (limited information available so no assurances on this data) is also a wealth of zinc and lead and accounts for only 4-5% of national production and 0.6% of world production.

Australia, number two in lead and gold, is the fourth largest producer of silver with 54.6 million ounces produced in 2010. Australia has the largest silver mine in the world. The mine also produces zinc and lead but is primarily a silver mine. Australia’s largest silver mine produces two thirds of the silver the country and accounts for 5.2% of world production of silver.

Chile, number one in copper, is the fifth largest producer of silver with 48 million ounces of silver produced in 2010. The leading silver mine in the country is also the world’s largest producer of copper, it extracts a quarter of silver production in Chile.

Russia is the sixth largest producer of silver in the world with 45 million ounces of silver produced in 2010. One third comes from a single mine that also produces gold with silver.

Bolivia is the seventh largest producer of silver with 43.7 million ounces of silver in 2010. The main silver mine in Bolivia produced 6.7 million ounces of silver in 2010.

The USA ranks eighth in silver production with 41.1 million ounces of silver produced in 2010. The largest U.S. silver mine, located in Alaska, is also the eighth largest silver mine in the world. It represents 17% of the silver from the U.S. and also produces zinc and lead.

Poland is the 9th largest producer of silver with 38.5 million ounces of silver. 100 percent of Polish production comes from from one mine that also produces copper.

Of these nine countries, the only leading silver mine that produces exclusively silver is from Bolivia. For all the other top silver producing countries, the largest silver mine also produces either copper, zinc, lead, molybdenum or gold.

As noted above, two-thirds of silver production is not derived from primary silver mines, rather from mine bi-products that produce silver along with copper, zinc, gold, lead, molybdenum, or even uranium (in Australia).

It is for this reason that the future of silver production depends to a large degree, almost half, on the production of zinc and copper. While the price of silver is often put in parallel with that of gold, its production depends primarily on the production of base metals. Therefore, the peak production of silver will probably happen at the same time as copper and zinc.

From the article entitled, “World Production of Silver” by Dr. Thomas Chaize author of the Mining and Energy Newsletter. The information provided herein has been provided to MiningFeeds.com by the author and, as such, is subject to our disclaimer: CLICK HERE.

In the early 1970s two brothers from Texas, William Herbert and Nelson Bunker Hunt, began accumulating silver. By 1979, the pair had effectively cornered the silver market. From September, 1979 to January, 1980 the price of an ounce of silver leapt from $11 to $54. Before the collapse a few months later, it is estimated the brothers were up almost $4 billion.

For the Hunt brothers, the silver market’s unraveling hit its nadir on March 27th, 1980, a day that came to be known as Silver Thursday. On that day, the Hunt brothers received a $100 million margin call on futures contracts that they were unable to meet. Facing a potential $1.7 billion loss, the ensuing panic rocked commodities and futures markets and the financial markets in general. The price of silver experienced a 50% one day decline, from $21.62 to $10.80.

Government officials feared that if the Hunts were unable to meet their debts some of the large Wall Street brokerage firms they dealt with might collapse. To save the situation, a consortium of US banks provided a $1.1 billion line of credit to the brothers secured against the majority of their remaining assets.

In late April, with silver approaching the historical record highs attributed to the Hunt brothers, investors and money managers alike were enthusiastically debating the value of an ounce of silver. Silver, it seems, is developing a cultish following similar to gold. “Silver bugs” worldwide are quick to point out that investment and consumption demand is increasing while supply is constrained. Moreover, they advocate that the silver to gold price ratio is forty to one, far from its historical 16 to 1 ratio, so a realignment, by some, is thought to be inevitable. With silver in the headlines on a daily basis we focused our efforts this month on the volatile precious metal and the Canadian listed companies that are exploring, developing and mining silver around the world. We present, in no particular order, 10 companies that we found interesting for various reasons.

1. Silver Wheaton Corp. (TSX:SLW)

Silver Wheaton was established in 2004. It was previously controlled by Goldcorp until December 7, 2006 when the gold miner reduced its ownership to 48%. On February 14, 2008 Goldcorp divested itself completely of Silver Wheaton, selling 108 million shares to net a healthy $1.566 billion.

Today, Silver Wheaton is reportedly the largest silver streaming company in the world. Silver streaming, the process of securing silver from mining companies through long term price contacts, exists because silver is often produced as a by-product of gold and base metals. It is estimated that roughly 70% of the world’s annual supply of silver is produced from secondary sources. The primary benefits associated with silver streaming is that acquiring silver through contracts, as opposed to mining the element, means that growth doesn’t require significant capital expenditure.

Silver Wheaton sells over 19 million ounces of silver annually – silver that’s mined by other companies including Barrick Gold and Goldcorp. In all, the company has 14 silver purchase agreements and expects attributable production to reach 27 million ounces in 2011. As a silver streamer Silver Wheaton enjoys another benefit, its sales are routed through a tax advantageous Cayman Islands subsidiary. In 2010, the company reported revenue of $423.4 million and earnings of $0.83 per share.

Because a large percentage of the company’s revenue is derived from low-cost, long-life mining operations and it does not sell forward its silver sales the rise in the price of silver has been beneficial to Silver Wheaton. In an interview with CNBC, Silver Wheaton’s CEO, Peter Barnes said he believes silver prices could go through $50 in the next two to three years, and that hedging the company’s silver is not on the horizon.

2. First Majestic Silver Corp. (TSX:FR)

Mexico is a country rich in history and in silver. During the European conquest of the Americas, silver was discovered in Mexico in 1546 in what is now the state of Zacatecas. Vast amounts of the shiny white metal were brought into the possession of the crowns of Europe from the area. The Fresnillo mine in Zacatecas, owned by the Mexican silver producer that bares its name, is considered to be one of the world’s largest primary silver mines and it has been in near continuous operation since 1550. And today, Mexico is one of the world’s biggest producers of silver.

An early mover into silver-rich Mexico has proven to be a good strategy for First Majestic Silver. The company has three producing mines in three different states including Durango, Jalisco and Coahulia. First Majestic’s soon-to-be fourth producing asset, the Del Toro Silver Mine, is located in the state of Zacatecas. But the company faced some challenges along the way. In late 2008, during the height of the financial crisis, the company’s shares traded down to a low of $0.88. But since then First Majestic’s comeback has been nothing short of amazing. The company now trades on the NYSE, and its shares are being exchanged of late for $20.00. Today, the company has a market capitalization of over $2 billion.

On May 13th, 2011 First Majestic Silver reported revenue of $55.3 million for the first quarter of 2011, an increase of 211% compared to $17.7 million in the first quarter of 2010 and an increase of 38% or $15.2 million compared to the fourth quarter of 2010. These results were spurred on by a 95% increase in the average realized price of silver, combined with a 13% increase in production. The appreciation in the price of silver went straight to the company’s bottom line. The company, which is considered to be the purist mid-tier silver producer, generated net earnings of $23.9 million for the first quarter of 2011 compared to net earnings of $0.4 million in the first quarter of 2010 and net earnings of $13.7 million in the fourth quarter of 2010. First Majestic Silver currently reports a cash balance of $97.1 million and the company doesn’t carry any long term debt.

With an income statement that might make the most conservative accountant crack a smile and a balance sheet that could even make Jim Flaherty blush we connected with the President & CEO of First Majestic Silver, Keith Neumeyer, to find out what’s on the horizon for the company – CLICK HERE – for the interview.

For 10 Most Interesting Silver Stocks – Part 2 – CLICK HERE.

3. Alexco Resource Corp. (TSX:AXR)

Alexco Resource is Canada’s newest silver producer. The company is focused on the Yukon Territory of Northern Canada. Renowned silver bug Sprott Asset Management is a significant shareholder, reportedly owning a 12.1% stake in the company.

Alexco entered into production at its Bellekeno mine in January 2011. Management forecasts 2.8 million ounces of silver, 18 million pounds of lead and 8 million pounds of zinc production in 2011. In 2008, Alexco reached a financing arrangement with Silver Wheaton to provide the capital necessary to develop the Bellekeno deposit through to production in order to avoid a dilutive equity financing. That call now looks prescient, as in December, 2010 just before the Bellkeno mine was about to enter production, Alexco completed a financing at a price of $8.20, for gross proceeds of $41 million.

Interestingly, Alexco also has an environmental services business in Canada and the United States. The company provides mine-related environmental consulting services, reclamation and mine closure services, and environmental remediation technologies to clients in both the public sector and the private sector.

Alexco’s President & CEO Clynton Nauman attributes the relatively short time frame associated with putting the Bellekeno mine into production to the strategic structure of the organization. “One of the reasons we were able to permit the Bellekeno Mine in a timely manner was the fact that we utilized our expert in-house environmental services team to permit the project.” he said. “As a result, we confidently constructed the mine and mill and related facilities in tandem with permitting stages, enabling fast-track project execution in a modern environmental regulatory regime.”

On the exploration front, Alexco’s primary objective is the Keno Hill silver district in the Yukon Territory in properties near their production facility. Although the Yukon is famous for its Klondike gold rush, the Keno Hill silver deposit, discovered in 1918, actually produced more pay-dirt than the Klondike. This lesser known but very rich precious metals district made the Yukon one of the world’s leading silver producers for decades – Keno Hill reportedly produced more than 217 million ounces of silver between 1921 and 1988. To purchase a copy of Dr. Aho’s book, “Hills of Silver, The Yukon’s Mighty Keno Hill Mine” – CLICK HERE.

4. Silver Standard Resources Inc. (TSX:SSO)

According to the company, Silver Standard possesses the largest in-ground silver resource of any publicly-traded primary silver miner. With a pipeline of 13 projects, ranging from early-stage exploration to production in various countries including Argentina, Peru, Mexico, Canada, Chile, the United States and Australia, the company’s portfolio is impressive.

Silver Standard’s first mine, the Pirquitas Mine in Argentina, achieved commercial production in December, 2009. In 2010 production from the Argentinean mine was 6.3 million ounces of silver and sold 5.94 million ounces at a weighted average price of $20.92 per ounce for total revenues of $112 million. The Pirquitas operation milled 1.26 million tonnes of ore in 2010 with silver grades of 233 grams per tonne at recoveries of 65.2%. Cash production cost per ounce declined throughout 2010 as production volumes and efficiencies increased to $9.47 per ounce in the fourth quarter net of by-product credits. Average cash production cost per ounce of silver, net of by-product credits, are projected to be $9 per ounce of silver in 2011. Factoring out by-products, the average cash production costs per ounce of silver is estimated to be $15.00

But what seems to have captured the interest of investors is not what Silver Standard is doing today but what they might do in the future. The speculative jewel in the Silver Standard crown appears to be the Pitarrilla project in Durango, Mexico. Pitarrilla, a grassroots discovery made by Silver Standard in 2002, now ranks as one of the largest silver discoveries in the world. Currently, estimated silver reserves are 91.7 million ounces, measured and indicated silver resources total 552 million ounces, plus 82 million ounces of inferred silver resources. And as they say in Mexico, eso es grande! A feasibility study on the project is expected to be completed this year.

In January of this year in a note to clients, BMO Capital Markets analyst Andrew Kaip wrote that the Vancouver-based miner boasts an “unrivalled pipeline of projects.” With three development projects in Latin America including the Pitarrilla project in Mexico, Mr. Kaip believes Silver Standard has the potential “to evolve into the fastest growing intermediate silver producer.”

5. Revett Minerals Inc. (TSX:RVM)

The justice system. An endless fount of interest. On March 29th, 2010, a federal judge rejected the U.S. Forest Service’s approval of a mining operation on the edge of the Cabinet Mountains Wilderness Area in Montana. That project was the Rock Creek mine owned by Revett Minerals.

The court ruled that the Forest Service violated the National Environmental Policy Act and the Forest Service Organic Act in approving the Rock Creek Mine, which would have bored under the Cabinet Mountain Wilderness Area and into the midst of popular recreational areas and key habitat for bull trout, grizzly bears and other environmentally sensitive wildlife species.