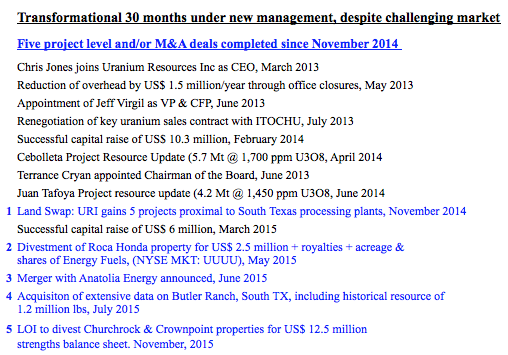

Uranium Resources Inc. “URI” (Nasdaq:URRE) (URI:ASX) has delivered a string of good news, but the Company’s stock is down nearly 60% since the June 2015 announcement of its acquisition of Anatolia Energy. Since Chris M. Jones took the helm as CEO in March 2013, URI has proactively executed a number of key initiatives, 14 in fact. Nothing short of transformational changes have been made over the past 32 months. These successes demonstrate ongoing efforts to bolster liquidity, reduce risk, diversify assets and pull forward cash flow. Achievements include; cost cutting & cost containment, new hires, positive project & resource updates, asset sales / acquisitions and importantly, the renegotiation of a key sales contract. Mr. Jones’ abbreviated bio is as follows:

Christopher M. Jones, President, CEO & Director: Joined in March 2013. More than 30 years experience in positions of increasing responsibility in the Mining & Energy industries. Mr. Jones was most recently President & CEO of Wildcat Silver Corporation, where his team quadrupled the size of the resource. He’s a licensed Professional Engineer in the US & Canada, has a B.S. in Mining Engineering from South Dakota School of Mines and an MBA from Colorado State University. Mr. Jones is a member of the American Institute of Mining, Metallurgical & Petroleum Engineers.

Clearly, the Company is run by a highly skilled, experienced and committed team, including 4 in new roles subsequent to CEO Jones’ arrival.

Select Management & Board members [Corporate Presentation]

Terence J. Cryan, Chairman of the Board: Director since October 2006, Chairman since June 2014. Mr. Cryan has over twenty years of international experience as an investment banker in the US & Europe. He served as Director of a number of international companies and is a frequent lecturer at Finance & Energy industry gatherings. He holds a Master of Science degree in Economics from the London School of Economics and a BA from Tufts University.

Tracy A. Stevenson, Director: Has served as Director since December 2013. Mr. Stevenson, CPA, is a Founding member of Bedrock Resources, a financial advisory firm focused on natural resources. He was Global Head of Business Process Improvement at Rio Tinto, and Executive VP, CFO & Director of Comalco Ltd. Prior, Mr. Stevenson served as CFO / Director of Kennecott Corp. and as Director of Ivanhoe Mines.

Mark K. Wheatley, Director: Has served as Director of Uranium Resources Inc. since 1q 2013 Mr. Wheatley’s independent, non-executive Board roles have included Chair of Gold One International, Norton Goldfields & Goliath Gold Mining, as well as directorships at St. Barbara Mines & Uranium One Inc. Mr. Wheatley was Chairman & CEO of Southern Cross Resources when it merged to create Uranium One in 2005.

Jeffrey L. Vigil, VP & CFO: Appointed VP & CFO in June 2013, responsible for financial & management reporting including tax, compliance, treasury, risk management & capital raising functions. Has served in various financial positions including CFO at Energy Fuels Inc. Mr. Vigil has more than 30 years financial management experience, 8 in the uranium sector, including serving as a mill cost analyst for Energy Fuels’ White Mesa Uranium Processing Facility.

URI’s market position has strengthened, yet its stock has plunged

Please look at the exhibit – 14 significant developments, 5 of which highlighted by management as transformational. Since March 2013, CEO Jones has led a new management team & Board in executing a well thought out, forward looking plan. The Company enjoys stronger liquidity, now trading on both the NASDAQ & Australian markets. The Anatolia acquisition closed on November 8th, eliminating deal risk. And, an asset sale was announced the following day. URI’s largest shareholder, Resource Capital Fund V L.P. “RCF” is reported to be, “evaluating project [the Temrezli ISR project] financing options.”

Balance sheet liquidity is solid, supporting a valuation that should be moving higher, not lower. As of September 30, 2015, non-restricted cash was $3.8 million. Since then, the Company signed a Binding Letter of Intent to sell 2 non-core assets for $12.5 million, of which $5.5 million is cash. To be clear, closing this transaction is not a sure thing. However, the buyer, Laramide Resources, recently obtained a $5 million loan and raised $1.5 million of equity. URI has $8 million in convertible debentures held by RCF. In December, URI closed a small equity raise, 2.5 million shares @ $0.40 (with no warrants). Existing warrants & options are well out of the money.

Therefore, URI’s pro forma Enterprise Value, “EV” is [54 mm shares x $0.53/share (Jan. 4th close) = $28.5 mm market cap, plus $8 mm convertible debt, minus ~ $9.5 mm pro forma cash, (including the prospective $5.5 million from sale of assets) is roughly $27 million (or $32.5 million without $5.5 million of cash proceeds). A pro forma EV of just $27 million for a company that’s produced over 8 million pounds of uranium in Texas, owns a world-class ISR project in Turkey, a standby processing facility in the U.S. and maintains strong exploration upside in Texas, New Mexico & Turkey, seems exceedingly cheap. [Corporate Presentation]

New & improved Uranium Resources Inc, trading at unwarranted discount to peers

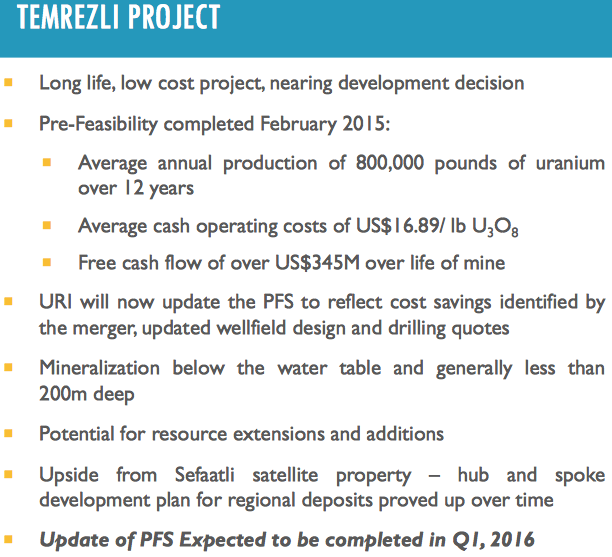

The nearest and most valuable asset possibly into production is the Temrezli ISR Project. Temrezli’s post-tax NPV of $126 million is based on upfront capital of $41 million. However, URI is on track to potentially reduce that figure trough synergies and the relocation of its Rosita processing plant to Turkey. If anticipated synergies can be extracted, the capital requirement could be in the low-to-mid $30’s million, which would boost the project’s already impressive IRR of 65%. As per the PFS sensitivities found in this press release, slashing initial cap-ex from $41 million to $35 million, if possible, would generate an after-tax IRR of ~77%.

URI’s entire pro forma EV is trading at roughly a quarter of Temrezli’s NPV alone! An investor at $0.53/share effectively gets Temrezli for FREE. That’s if one believes as I do that the valuation of the Company’s standby processing mill (2 mills, but Rosita mill headed to Turkey), plus advanced & earlier-stage exploration / development assets in Turkey, New Mexico & Texas, is worth at least $27 million. Hardly a stretch given that URI had an EV of $45 million the day before the Anatolia transaction was announced. Notably, in the months preceding Japan’s Fukushima incident, URI (without Anatolia) had a market cap as high as $300 million, 10x that of today’s market cap (including Anatolia).

Proactive corporate initiatives de-risk world-class Temrezli Project

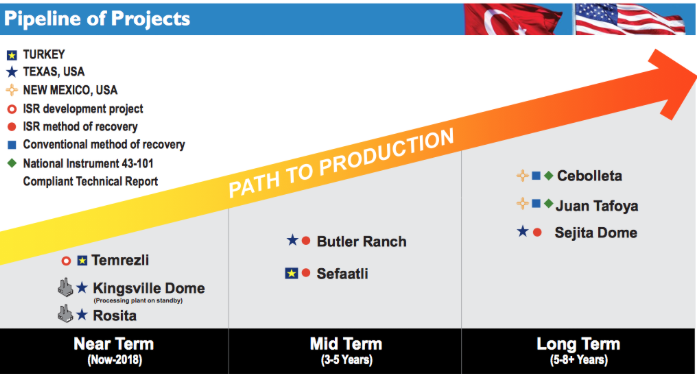

More detail on the Company’s non-Temrezli assets — URI holds a 100% interest in 9 licenses covering over 44,479 acres, including several advanced exploration opportunities in the central Anatolian region of the country. URI controls three production properties and several exploration targets in South Texas. The Company also has substantial historical, non-reserve mineralized material and a NRC license to produce up to 3 million pounds per year. URI controls mineral rights encompassing approximately 190,000 acres in the prolific Grants Mineral Belt of New Mexico, one of the foremost sandstone-hosted uranium basins in the world. Finally, the Company has expanded its feeder pipeline of high-potential ISR projects in Texas, near its processing infrastructure.

Enhanced liquidity would deliver more than a comfortable margin for error, it would be used to partially fund URI’s low-cost, world-class Temrezli ISR Project. Anatolia’s Pre‐Feasibility Study indicated an after-tax NPV(8%) of $126 million based on a uranium price of $65/lb. At a long-term uranium price of $55/lb., (currently $44/lb.) the after-tax NPV is roughly $85 million, still 3x that of the entire Company’s pro forma EV! Recall that the Temrezli project is squarely in the lowest cost quartile in the industry, making it solidly profitable at a price as low as $40/lb. I believe that an upfront capital call in the $30’s of millions, for a top-tier ISR project, is achievable even in this challenging funding environment.

Conclusion

I strongly believe that the new Uranium Resources Inc. (Nasdaq:URRE) (URI:ASX) is demonstrably undervalued. URI is without question in a stronger position today then it was six months ago. Importantly, URI’s lower risk profile should facilitate project financing. URI’s stock is ~ 70% below its 52-week high. Compared to ISR peers Energy Fuels, UR-Energy, Uranium Energy Corp. & Peninsula Energy, URI is trading at close to a 55% discount on an EV/lb. basis (giving zero credit to historical non-reserve mineralized, “lbs. in the ground”). In my opinion the sell off is unwarranted, offering a compelling risk-adjusted opportunity to buy shares. [Please see my prior article on URI]

Reiterating the analysis, the Company’s pro forma cash balance is about $9.5 million (including the prospective $5.5 million from sale of assets). The pro forma EV is just $27 million, 40% below URI’s EV before the Anatolia acquisition. Investors are arguably getting Temrezli’s Pre-Feasibility Study derived NPV(8%) of $126 million (at $65/lb. uranium) for free. Even at $55/lb, the NPV is about $85 million, 3x that of the entire Company’s EV. Fundamentally the story has only become stronger, a story that does not require a near-term spike in uranium prices to be a big winner. Therefore, investors are faced with a compelling risk/reward opportunity.

Here’s a good audio interview of CEO Chris Jones, conducted by Jeb Handwerger.

Disclosure: Uranium Resources Inc. has a small market cap. Small market cap stocks are highly speculative, not suitable for all investors. I, Peter Epstein, own shares of Uranium Resources Inc. purchased in the open market. Mr. Epstein, CFA, MBA is not a licensed financial advisor. Readers should take that fact into careful consideration before buying or selling any stocks named herein.

Readers are encouraged to consult with their own investment advisors before buying or selling any stock, especially highly speculative ones like Uranium Resources Inc. At the time that this article was posted, Uranium Resources Inc. was a sponsor of: http://EpsteinResearch.com. Please visit: http://EpsteinResearch.com for free updates on URI and others across a range of sectors. Thank you for supporting my articles & interviews.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.