Investors with an interest in Mining – Miscellaneous stocks have likely encountered both Norsk Hydro ASA (NHYDY) and BHP (BHP). But which of these two stocks offers value investors a better bang for their buck right now? We'll need to take a closer look.

We have found that the best way to discover great value opportunities is to pair a strong Zacks Rank with a great grade in the Value category of our Style Scores system. The proven Zacks Rank emphasizes companies with positive estimate revision trends, and our Style Scores highlight stocks with specific traits.

Norsk Hydro ASA has a Zacks Rank of #1 (Strong Buy), while BHP has a Zacks Rank of #3 (Hold) right now. The Zacks Rank favors stocks that have recently seen positive revisions to their earnings estimates, so investors should rest assured that NHYDY has an improving earnings outlook. But this is only part of the picture for value investors.

Value investors also try to analyze a wide range of traditional figures and metrics to help determine whether a company is undervalued at its current share price levels.

The Style Score Value grade factors in a variety of key fundamental metrics, including the popular P/E ratio, P/S ratio, earnings yield, cash flow per share, and a number of other key stats that are commonly used by value investors.

NHYDY currently has a forward P/E ratio of 9.44, while BHP has a forward P/E of 16.39. We also note that NHYDY has a PEG ratio of 0.74. This popular figure is similar to the widely-used P/E ratio, but the PEG ratio also considers a company's expected EPS growth rate. BHP currently has a PEG ratio of 1.10.

Another notable valuation metric for NHYDY is its P/B ratio of 2.15. Investors use the P/B ratio to look at a stock's market value versus its book value, which is defined as total assets minus total liabilities. By comparison, BHP has a P/B of 3.75.

These are just a few of the metrics contributing to NHYDY's Value grade of B and BHP's Value grade of C.

NHYDY sticks out from BHP in both our Zacks Rank and Style Scores models, so value investors will likely feel that NHYDY is the better option right now.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Norsk Hydro ASA (NHYDY) : Free Stock Analysis Report

BHP Group Limited Sponsored ADR (BHP) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

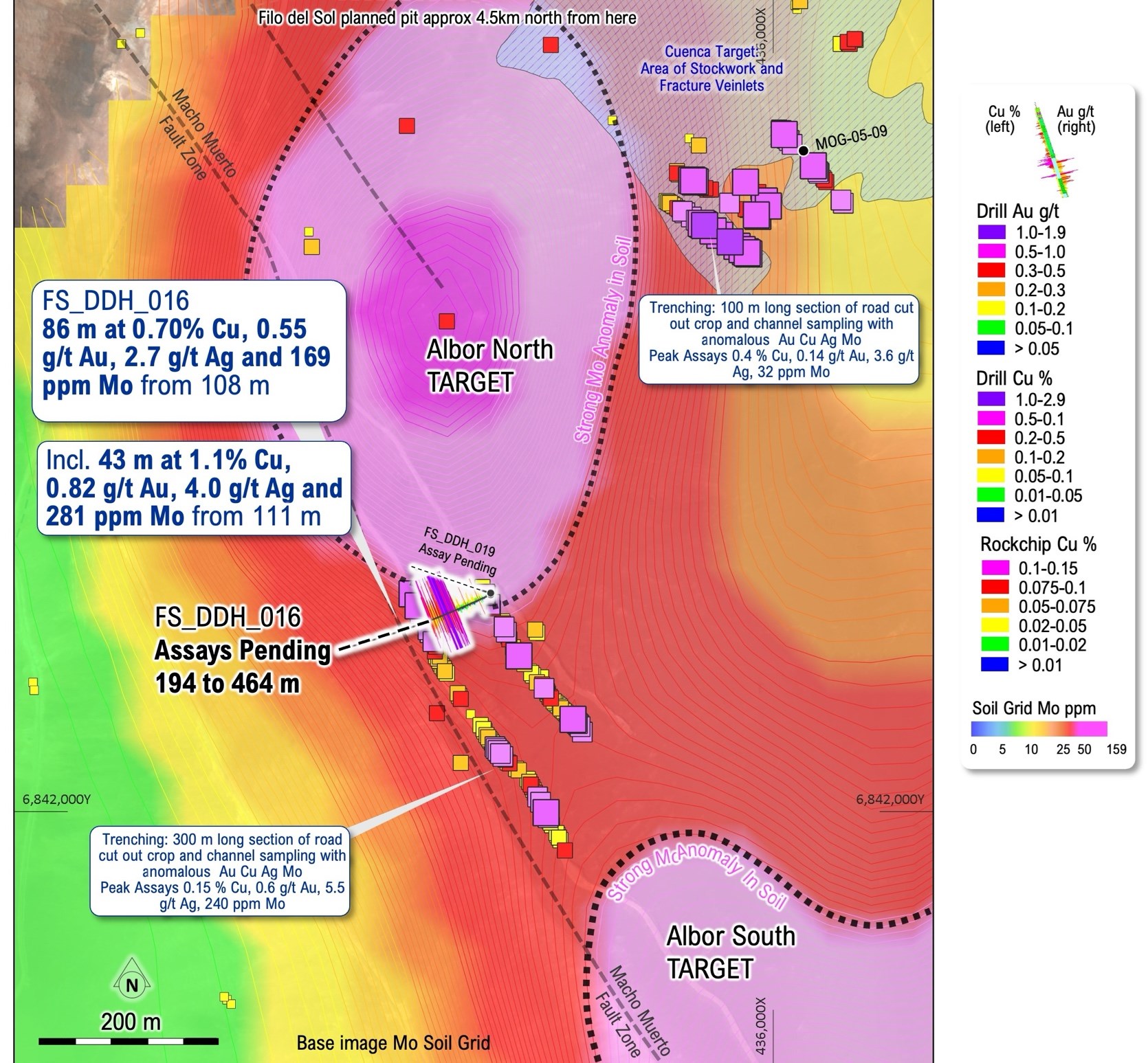

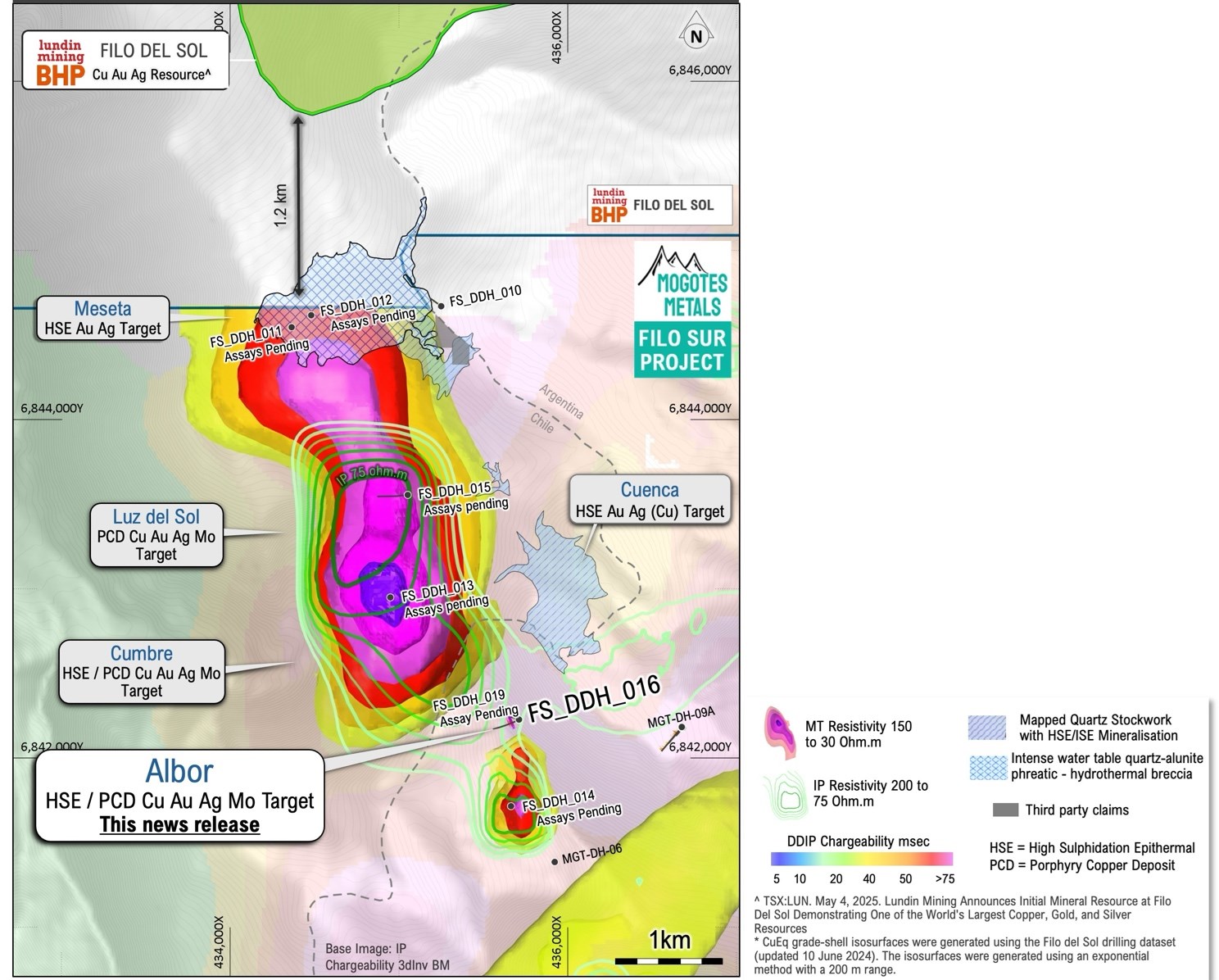

Toronto, Ontario–(Newsfile Corp. – May 14, 2026) – Mogotes Metals Inc. (TSXV: MOG) (FSE: OY4) (OTCQB: MOGMF) ("Mogotes", or the "Company") is pleased to announce partial laboratory assay results from diamond drillhole FS_DDH_016 at the Company's flagship Filo Sur project in Argentina, immediately along strike from BHP and Lundin Mining's Filo del Sol copper-gold-silver discovery¹.

Assays received for the first 194 m within the 464 m deep hole confirm a continuous zone starting from 108 m depth of near surface, high-grade copper-gold-silver-molybdenum mineralization within chalcopyrite – bornite – covellite bearing breccias, stockwork and dissemination within the altered porphyry matrix (Table 1). Mogotes geologists have noted strong parallels with the characteristics of mineralization in hole FS_DDH_016 and those reported from the nearby Filo del Sol deposit2.

Highlights

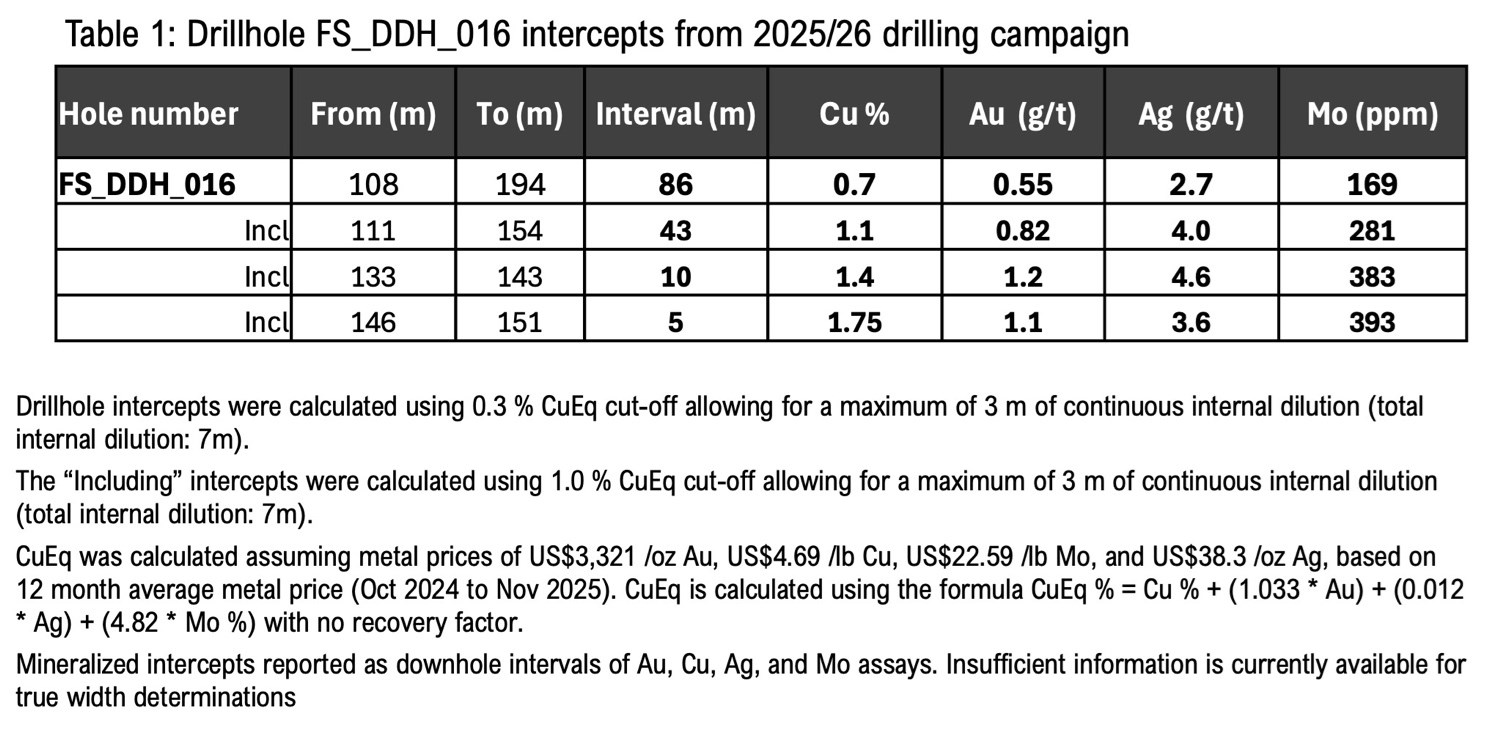

- 86 m at 0.7% Cu, 0.55 g/t Au, 2.7 g/t Ag & 169 ppm Mo from 108 m to 194 m down hole to end of assays received to date. (Table 1)

- Including 43 m at 1.1% Cu, 0.82 g/t Au, 4.0 g/t Ag & 281 ppm Mo from 111 m

- Reported interval ends in mineralization

- Assays for the remaining 270 m of the hole are pending.

- This interval also includes peak intercepts of:

- 10 m at 1.4% Cu, 1.2 g/t Au, 4.6 g/t Ag and 383 ppm Mo from 133 m.

- 5 m at 1.75% Cu, 1.1 g/t Au, 3.6 g/t Ag and 393 ppm Mo from 146 m.

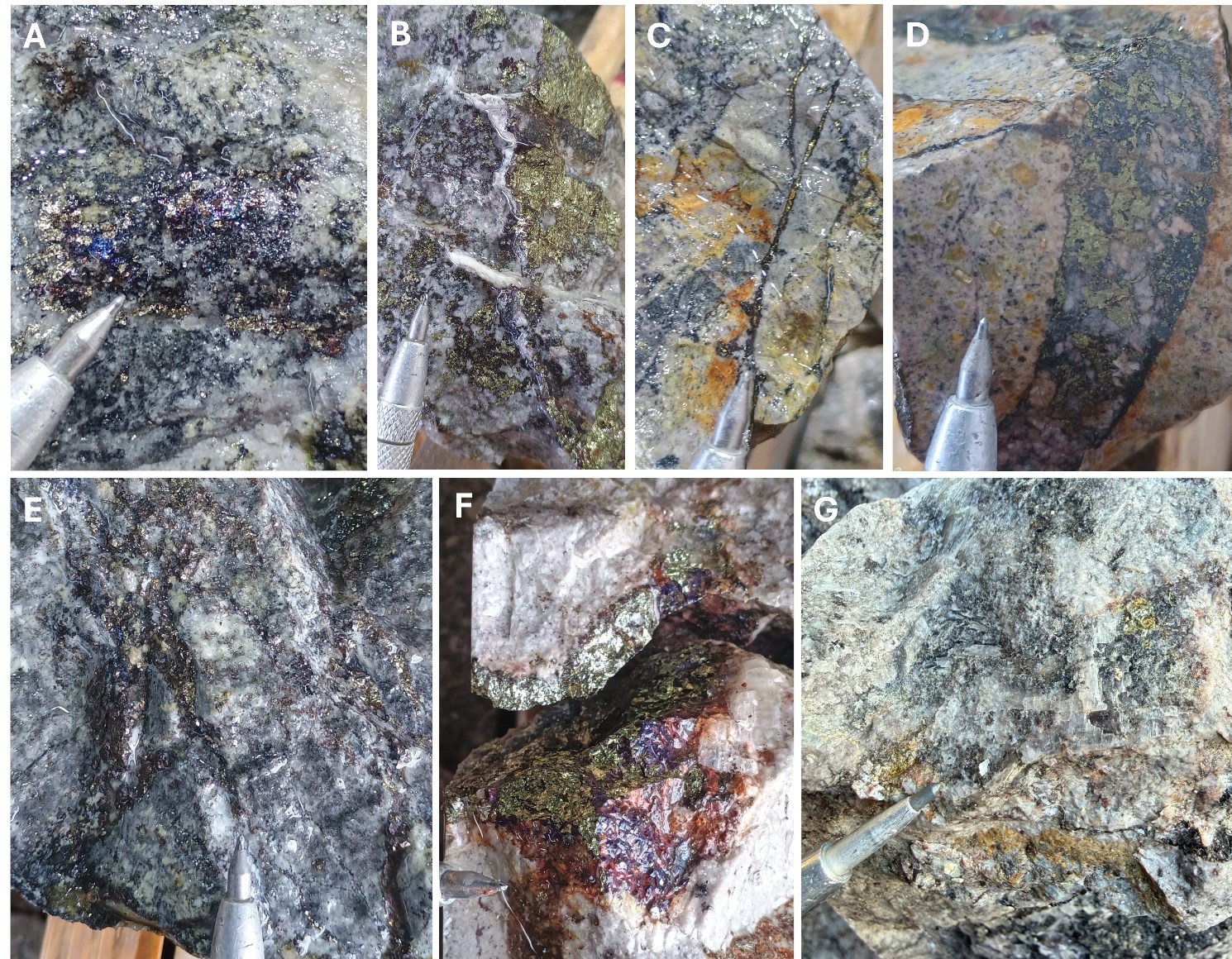

- Core shows evidence of several stages of mineralization as is seen in the nearby Filo del Sol deposit (Figure 3): chalcopyrite – bornite with porphyry-stage potassic alteration (breccias, stockwork, dissemination and anhydrite megacryst pegmatite veins), interpreted hypogene epithermal enrichment with fine grained dark copper minerals including probable covellite/digenite as disseminated overgrowths on pyrite and distinctive fracture coatings and localized sulphide rich veins with enargite, as well as some evidence of supergene copper mineralization with localized fracture coat malachite, brochantite and probable chalcocite.

- Shallow high-grade copper, gold, silver and molybdenum mineralization: mineralization starts at 108 m down hole, and trenching results along strike at surface indicate that mineralization projects to surface beneath a thin scree cover that may also be concealing a larger mineralized target.

- Generally low levels of arsenic for the Vicuña district: Arsenic levels are typically low (median for this interval is 2 ppm As) within this mineralized interval with only specific narrow structures with elevated arsenic indicating the local presence of the copper-bearing epithermal mineral enargite.

- Larger mineral system at play: The newly identified "Albor" target is part of a 3.5 km long Mogotes (Meseta – Luz del Sol – Cumbre – Albor) Miocene age target trend aligned within the regional scale, transorogen, Macho Muerto Fault Zone. Observed multistage alteration and mineralization features in the drill core suggest association with a larger Cu-Au-Ag-Mo mineral system.

- "Albor" is the second copper-gold-silver-molybdenum discovery by Mogotes in its inaugural drilling season at Filo Sur (see Cruz del Sur press release) and is part of the large Luz del Sol target trend where drill results are pending for a number of holes drilled in the 2025-2026 exploration season.

Figure 1: Core from 125.75m (FS_DDH_016), 125-126m assays at 1.67% Cu, 1.62 g/t Au, 1.69 g/t Ag, 685 ppm Mo

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_002full.jpg

CEO Comment

Allen Sabet, President and CEO of Mogotes, commented:

"In our first fully funded drill season at Filo Sur we have now made two significant copper-gold-silver-molybdenum discoveries at Cruz del Sur and at the Albor target, where we have just scratched the surface of something we believe will be significant.

"This partial assay release from Albor is a first hole into a shallow and high-grade copper-gold-silver-molybdenum system, strategically located adjacent to the large Vicuña district deposits, where BHP and Lundin Mining are developing the Josemaria copper-gold porphyry and evaluating development options for the very large Filo del Sol deposit.

"As this style of mineralization has implications for the broader Vicuña district, we felt it prudent to release partial results for FS_DDH_016 as received. We continue to be humbled by the geological endowment of this very special part of the world and are grateful for the continued support of our patient shareholders. Stay tuned for more!"

Figure 2: Plan View of Drillhole FS_DDH_016 and Albor Target Zones

Albor target zones untested by drilling prior to this campaign.

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_003full.jpg

Figure 3: Core photographs of FS_DDH_016 up to 194 m

All intervals shown are down-hole depth. (A, B, E, and G) Pyrite + chalcopyrite + bornite ± covellite ± digenite in hydrothermal breccia matrix. (A) 113-114 m. (B) 119-120 m. (E) 157-158 m. (G) 187-188m. (C, F, and D) Pyrite + chalcopyrite + covellite/digenite veins. (C) 116-117 m. (F) 180-181 m. (D) 135-136 m.

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_004full.jpg

Next Steps on rest of Filo Sur drill campaign:

- Lab assays for the 194–464 m portion of FS_DDH_016 are expected by end of May 2026.

- The drill campaign has now formally ended, with both Chile and Argentina field camps demobilized.

- Efforts were made to drill as much as possible this season, using 4 rigs and drilling a total of 6207 metres, of which 2652 metres have been reported on including in this press release.

- 3681 metres of drilling will be reported on in the coming months.

- Chile drill holes started later in the season and will be reported later than the Argentina drill holes due to timing of drilling and laboratory assay timing.

Figure 4: Filo Sur Project Luz del Sol Trend

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_005full.jpg

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_007full.jpg

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_008full.jpg

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_009full.jpg

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_010full.jpg

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_011full.jpg

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/10597/297424_bac167e3f45afbcc_012full.jpg

Table 2: Location details of FS_DDH_016

| Hole number | Initial Azimuth | Initial Dip | Depth (m) | Grid | Easting | Northing |

| FS_DDH_016 | 245.4 | -69.8 | 464 | UTM zone 19S | 435711 | 6842226 |

References

1 May 4, 2025. News Release, Lundin Mining Announces Initial Mineral Resource at Filo del Sol Demonstrating One of the World's Largest Copper, Gold, and Silver Resources. Lundin Mining

2 Perelló, J., Sillitoe, R. H., Rossello, J., Forestier, J., Merino, G., & Charchaflié, D. (2023). Geology of porphyry Cu-Au and epithermal Cu-Au-Ag mineralization at Filo del Sol, Argentina-Chile: Extreme telescoping during Andean uplift. Economic Geology, 118(3), 611–654.

About Mogotes Metals Inc.

Mogotes Metals Inc. is a mineral exploration company focused on copper, gold, and silver in the prospective Vicuña district of Argentina and Chile. The Company's flagship Filo Sur project adjoins Lundin Mining's Filo del Sol — one of the world's largest copper-gold-silver discoveries¹ — and lies along the same N-S trending belt as the Filo del Sol–Aurora deposits and NGEx Minerals' Lunahuasi and Los Helados copper-gold deposits.

For further information, please contact:

Mogotes Metals Inc.Allen Sabet, President and Chief Executive OfficerPhone: (647) 846-3313Email: info@mogotesmetals.com

Follow Us

Twitter: https://x.com/mogotesmetals

Additional Information

The information contained in this news release was accurate at the time of dissemination but may be superseded by subsequent news release(s). The Company is under no obligation, nor does it intend to update or revise the forward-looking information, whether as a result of new information, future events or otherwise.

Qualified Persons

The scientific and technical disclosure for the Filo Sur project included in this news release have been reviewed and approved by Stephen Nano who is the Qualified Person as defined by NI 43-101. Mr. Nano is a Director and Technical Advisor of the Company and is not independent.

Note that the Qualified Person has not verified the information regarding adjacent properties such as Filo del Sol and that the information regarding the mineralization of the Filo del Sol project is not necessarily indicative of the mineralization on the Filo Sur project.

Mogotes applies industry-standard exploration sampling methodologies and techniques. All geochemical soil, stream, rock and drill samples are collected under the supervision of the company's geologists in accordance with industry practice. Geochemical assays are obtained and reported under a quality assurance and quality control (QA/QC) program. Samples from Argentina are dispatched bagged in raffia bags and packaged for shipment by a dedicated truck to the ALS laboratory in Mendoza, Argentina. Samples from Chile are dispatched bagged in raffia bags and delivered to the ALS laboratory in Copiapo, Chile. These facilities carried out sample preparation (PREP-31B) which includes crush to 70% less than 2 mm, riffle split off 1 kg, pulverize to 85% passing 75 microns. The prepared samples are sent to the ALS laboratory in Lima, Peru for gold and multi-element analysis. Gold (Au-ICP21) was analyzed by fire assay fusion with ICP-AES finish on a 30 g sample. Samples were also analyzed for a suite of 48 elements (ME-MS61) with four acid digestion and ICP-MS finish.

Assay results from drill core samples may be higher, lower or similar to results obtained from surface rock, channel, trench samples due to surficial oxidation and enrichment processes or due to natural geological grade variations in the primary mineralization.

Cautionary Note Regarding Forward-Looking Statements:

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Certain statements made and information contained herein constitute "forward-looking information" and "forward-looking statements" within the meaning of applicable securities legislation (collectively, "forward-looking information"). The forward-looking information contained in this news release is based on information available to the Company as of the date of this news release. Except as required under applicable securities legislation, the Company does not intend, and does not assume any obligation, to update this forward-looking information. Generally, this forward-looking information can frequently, but not always, be identified by use of forward-looking terminology such as "plans", "expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "projects", "targets", "assumes", "strategy", "goals", "objectives", "potential", "possible", "anticipates" or "does not anticipate", or "believes", or variations of such words and phrases or statements that certain actions, events, conditions or results "will", "may", "could", "would", "should", "might" or "will be taken", "will occur" or "will be achieved" or the negative connotations thereof. All statements other than statements of historical fact may be forward-looking statements.

No assurance can be given that this information will prove to be correct and such forward-looking information included in this news release should not be relied upon. In particular, this press release contains forward-looking information pertaining to assumptions made in the interpretation of drill results, geology, grade, geochemistry, potential implications of geophysics interpretations, and continuity of mineral deposits; the assumption that any further assay results from the remaining approximately 270 m of drill hole FS_DDH_016, or from any other drill hole at the Filo Sur project, will return grades, widths or styles of mineralization comparable to the partial assay results from FS_DDH_016 reported in this news release; the assumption that visual estimates, core-logging observations and pXRF measurements referenced in this news release (including in the figure captions) will be confirmed by subsequent laboratory assays; the assumption that future drill holes at the Albor target or elsewhere on the Filo Sur project will encounter mineralization of similar grade, width, continuity or character to that reported herein; expectations regarding access and demand for equipment, skilled labour and services needed for exploration and development of mineral properties; and that activities will not be adversely disrupted or impeded by exploration, development, operating, regulatory, political, community, economic, environmental and/or health and safety risks. In addition, this news release may contain forward-looking statements or information pertaining to: potential exploration upside at the Filo Sur Project, including the extent and significance of the porphyry copper-gold system and the prospectivity of exploration targets; exploration plans and expenditures; the ability of the Company to conduct its field programs as planned; the success of future exploration activities; potential for resource expansion; ability to build shareholder value; expectations with regard to adding to its Mineral Reserves or Resources through exploration; ability to execute planned work programs; plans or ability to mobilize or add additional drill rigs; timing or anticipated results of laboratory results; government regulation of mining activities; environmental risks; unanticipated reclamation expenses; title disputes or claims; limitations on insurance coverage; and other risks and uncertainties. While the Company anticipates running an exploration program, it may encounter unexpected logistics, community, access, permitting, legal, environmental, drilling and other challenges, costs, or delays that could prevent the Company from completing the program on the expected timeline or at all. Any further drilling is dependent on pending results from this year's program and the Company securing additional funding. This program could be delayed or not be carried out at all.

Although the Company believes that the expectations reflected in such forward-looking statements and/or information are based on assumptions that are reasonable, undue reliance should not be placed on forward-looking statements since the Company can give no assurance that such expectations will prove to be correct. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements, including the risks, uncertainties and other factors identified in the Company's periodic filings with Canadian securities regulators, available under the Company's SEDAR+ profile at www.sedarplus.ca, as well as among other things: general business, economic and mining industry conditions; foreign exchange rates; geological conditions; the supply and demand for commodities; that financing will be available if and when needed on reasonable terms and that the Company will not experience any material labour dispute, accident, or failure of plant or equipment; the stability and predictability of the political environments and legal and regulatory frameworks; the ability of the Company to obtain, maintain, renew and/or extend required permits, licences, authorizations and/or approvals from the appropriate regulatory authorities; that contractual counterparties perform as agreed; and the ability of the Company to continue to obtain qualified staff and equipment in a timely and cost-efficient manner to meet its needs. These factors are not, and should not be construed as being, exhaustive. Although the Company has attempted to identify important factors that would cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated, or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. All of the forward-looking information contained in this document is qualified by these cautionary statements. Readers are cautioned not to place undue reliance on forward-looking information due to the inherent uncertainty thereof. Statements relating to "mineral resources" are deemed to be forward-looking information, as they involve the implied assessment, based on certain estimates and assumptions that the mineral resources described can be profitably produced in the future. Forward-looking information is provided for the purpose of providing information about management's current expectations and plans and allowing investors and others to get a better understanding of the Company's operating environment.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/297424

Freeport-McMoRan Inc. FCX delivered first-quarter 2026 earnings and revenue above expectations, driven by higher copper and gold prices, though weaker sales volumes were a drag. Its copper sales volumes tumbled approximately 25% year over year in the first quarter to 657 million pounds, and fell from 709 million pounds in the prior quarter. The downside primarily resulted from lower operating rates due to the temporary suspension of operations since the mud rush incident at the Grasberg Block Cave mine in Indonesia in September 2025. While the company’s outlook for copper sales volumes for the second quarter of 690 million pounds indicates a sequential improvement, it still suggests a 32% year-over-year decline. For full-year 2026, consolidated sales volume projections were revised lower to around 3.1 billion pounds of copper from the prior view of 3.4 billion pounds due to an expected delay in achieving full ramp-up of the Grasberg Block Cave mine. Sales volume growth underpins Freeport’s ability to leverage higher copper and gold prices, maintain margin expansion and deliver on its targets. Despite gains in realized prices, lower expected volumes are likely to strain its financials. Among FCX’s peers, Southern Copper Corporation SCCO logged lower copper sales volumes in the first quarter. Southern Copper sold 231,770 tons of copper in the quarter, declining nearly 5% year over year. Southern Copper also saw lower molybdenum sales volumes, which fell roughly 3% year over year. BHP Group Limited BHP saw lower year-over-year copper sales in the third quarter of fiscal 2026 (ended March 31, 2026). BHP Group’s copper sales for the quarter fell roughly 12% year over year to 468.7kt. BHP Group’s total copper sales for the nine-month period also declined around 7% from the prior-year period.

The Zacks Rundown for FCX

Shares of Freeport-McMoRan have gained 32.2% year to date compared with the Zacks Mining – Non Ferrous industry’s rise of 31%.

Image Source: Zacks Investment Research

From a valuation standpoint, FCX is currently trading at a forward 12-month earnings multiple of 23.29, a 3.5% discount to the industry average of 24.14X. It carries a Value Score of C.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for FCX’s 2026 and 2027 earnings implies a year-over-year rise of 44.6% and 34%, respectively. The EPS estimates for 2026 and 2027 have been trending higher over the past 60 days.

Image Source: Zacks Investment Research

FCX stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Freeport-McMoRan Inc. (FCX) : Free Stock Analysis Report

BHP Group Limited Sponsored ADR (BHP) : Free Stock Analysis Report

Southern Copper Corporation (SCCO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

OVERLAND PARK, Kan., May 13, 2026–(BUSINESS WIRE)–Compass Minerals (NYSE: CMP), a leading global provider of essential minerals, today announced that the company will participate in one-on-one meetings at Deutsche Bank’s 17th Annual Basic Materials Conference on June 2, 2026, in New York City.

Updated presentation materials will be available at the time of the event through the investor relations section of the Compass Minerals website at compassminerals.com.

About Compass Minerals

Compass Minerals (NYSE: CMP) is a leading global provider of essential minerals focused on safely delivering where and when it matters to help solve nature’s challenges for customers and communities. The company’s salt products help keep roadways safe during winter weather and are used in numerous other consumer, industrial, chemical and agricultural applications. Its plant nutrition products help improve the quality and yield of crops while supporting sustainable agriculture. Compass Minerals operates 11 production and packaging facilities with more than 1,800 employees throughout the U.S., Canada and the U.K. Visit compassminerals.com for more information about the company and its products.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260513367661/en/

Contacts

Investor Contact Brent CollinsVice President, Treasurer & Investor Relations+1.913.344.9111InvestorRelations@compassminerals.com

Media Contact Kevin GabrielSenior Director, Corporate Affairs+1.913.344.9265MediaRelations@compassminerals.com

- In early May 2026, Compass Minerals International reported fiscal second-quarter results showing sales of US$453.2 million and net income of US$12.7 million, marking a shift from a loss a year earlier.

- Alongside the earnings release, the company retired US$150.0 million of senior notes, extended its receivables facility to 2029, and simplified its portfolio by selling its Wynyard sulfate of potash business.

- We’ll now examine how Compass Minerals’ return to profitability and recent debt reduction efforts may influence its existing investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

Compass Minerals International Investment Narrative Recap

To own Compass Minerals today, you need to be comfortable with a business that still leans on highly variable winter Salt demand while working to strengthen its Plant Nutrition earnings and balance sheet. The return to profitability in the latest quarter and the retirement of US$150.0 million of senior notes help the near term story, but do not remove the key short term catalyst of operational execution in Salt or the biggest current risk of weather driven revenue swings.

Among the latest announcements, the full redemption of the remaining US$150.0 million of 2027 senior notes stands out as most relevant. It directly addresses earlier concerns about leverage, which had implied that a large share of future cash flows might be tied up in debt repayment rather than growth. For investors watching how quickly Compass can translate its recent profitability into more financial flexibility, this move is central to the evolving thesis.

But investors also need to be aware that Compass remains heavily exposed to unpredictable winter weather patterns, which…

Read the full narrative on Compass Minerals International (it's free!)

Compass Minerals International's narrative projects $1.3 billion revenue and $76.7 million earnings by 2028. This requires 2.1% yearly revenue growth and a $197.6 million earnings increase from -$120.9 million today.

Uncover how Compass Minerals International's forecasts yield a $25.75 fair value, a 9% downside to its current price.

Exploring Other PerspectivesCMP 1-Year Stock Price Chart

Four members of the Simply Wall St Community currently estimate Compass Minerals’ fair value between US$14.18 and US$25.75, highlighting very different expectations. You can weigh these views against the company’s continued dependence on volatile winter Salt demand, which has important implications for how steady future earnings might be.

Explore 4 other fair value estimates on Compass Minerals International – why the stock might be worth 50% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker – dig into the data and build a conviction that's truly your own.

- A great starting point for your Compass Minerals International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Compass Minerals International research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Compass Minerals International's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include CMP.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

- BHP Group lost a UK court appeal over its liability for the 2015 Brazil dam disaster, clearing the way for a major damages trial.

- Copper has overtaken iron ore as BHP’s largest earnings contributor, supported by demand from AI related infrastructure.

- BHP agreed a yuan priced iron ore deal with a Chinese state entity and is open to issuing yuan denominated debt.

ASX:BHP is trading at A$57.95, with the stock up 5.5% over the past week and 26.6% year to date. Over 1 year, the share price return is 60.8%, while the 3 year and 5 year returns are 53.6% and 84.9% respectively. These moves frame a company that is already in focus as it faces legal, earnings mix and funding changes at the same time.

For investors, the combination of a high profile UK legal process, copper taking the lead in earnings, and closer links to China’s currency and capital markets points to a company in the middle of significant shifts. How BHP manages legal liabilities, capital allocation and exposure across iron ore and copper will be key factors to watch when assessing risk and potential resilience in ASX:BHP.

Stay updated on the most important news stories for BHP Group by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on BHP Group.

ASX:BHP 1-Year Stock Price Chart

Quick Assessment

- ❌ Price vs Analyst Target: At A$57.95, BHP trades about 8.9% above the A$53.22 analyst consensus target.

- ❌ Simply Wall St Valuation: Shares are trading 44.5% above the estimated fair value, so the stock screens as overvalued.

- ✅ Recent Momentum: The stock is up 6.3% over the last 30 days, continuing a strong recent run.

There is only one way to know the right time to buy, sell or hold BHP Group. Head to Simply Wall St’s

company report for the latest analysis of BHP Group’s Fair Value.

Key Considerations

- 📊 The UK court setback keeps the 2015 Brazil dam disaster front and center, so legal provisions and potential damages remain an important part of the thesis.

- 📊 Copper now leading earnings, supported by AI related infrastructure demand, makes volume, pricing and new copper projects key data points to watch.

- ⚠️ The yuan priced iron ore deal and potential yuan debt increase exposure to Chinese credit and currency terms at a time when the stock already looks expensive on DCF estimates.

Dig Deeper

For the full picture, including more risks and rewards, check out the

complete BHP Group analysis. Alternatively, you can visit the

community page for BHP Group to see how other investors believe this latest news will impact the company’s narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include BHP.AX.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Freeport-McMoRan Inc.’s FCX shares have popped 48% in the past six months, thanks to its strong earnings performance riding on higher copper prices driven by concerns over tighter global supply and solid demand. Although sales volumes declined, the company saw a sharp increase in realized copper prices, driving its first-quarter earnings.Freeport has outperformed the Zacks Mining – Non Ferrous industry’s rise of 37.1% and the S&P 500’s increase of 9.4% over the same period. Its peers, Southern Copper Corporation SCCO and BHP Group Limited BHP, have rallied 28.7% and 47.7%, respectively.

Freeport’s 6-month Price Performance

Image Source: Zacks Investment Research

FCX stock is currently trading below the 50-day simple moving average (SMA). FCX has been trading above the 200-day SMA since late November 2025, suggesting a long-term uptrend. Following a golden crossover on July 8, 2025, the 50-day SMA is higher than the 200-day SMA, indicating a bullish trend.

FCX Stock Trades Below 50-Day SMA

Image Source: Zacks Investment Research

Let’s take a look at FCX’s fundamentals to analyze the stock better.

Freeport’s Growth Actions to Drive Capacity & Production

Freeport continues to leverage its portfolio of high-quality copper assets, emphasizing disciplined execution and organic growth initiatives to strengthen its production profile. At its Cerro Verde operation in Peru, a large-scale concentrator expansion provided incremental annual production of around 600 million pounds of copper and 15 million pounds of molybdenum. It has completed the evaluation of a large-scale expansion at El Abra in Chile to define a large sulfide resource that could potentially support a major mill project similar to the large-scale concentrator at Cerro Verde, with an estimated resource of approximately 20 billion recoverable pounds of copper. In Arizona, FCX is progressing with pre-feasibility studies at its Safford/Lone Star operations, with completion targeted for 2026, to assess a sizable sulfide expansion opportunity. It has expansion opportunities at Bagdad in Arizona that can more than double the concentrator capacity of the operation. Technical and economic studies have revealed the potential to build concentrating facilities to boost copper production by 200-250 million pounds annually. PT Freeport Indonesia (PT-FI) substantially completed the construction of the new greenfield smelter in Eastern Java during 2024, with the start-up of operations having commenced in the second quarter of 2025. The first production of copper anode was achieved in July 2025. PT-FI is also developing the Kucing Liar ore body within the Grasberg district with a targeted ramp-up to commence in 2030. FCX completed studies in 2025 that showed an opportunity to increase Kucing Liar’s design capacity to 130,000 metric tons of ore per day and reserves by roughly 20% at low costs.

FCX’s Solid Financial Health & Capital Discipline Bode Well

FCX has a strong liquidity profile and generates substantial cash flows, providing ample flexibility to fund expansion projects, reduce debt and enhance shareholder returns. It generated solid operating cash flows of $5.6 billion in 2025. Cash flows provided by operations surged 36% year over year to around $1.5 billion in the first quarter of 2026. Freeport ended the first quarter with strong liquidity, including $3.7 billion in cash and cash equivalents, $3 billion in availability under the FCX revolving credit facility, and $1.5 billion in availability under the PT-FI credit facility.At the end of the first quarter, Freeport had a net debt of $2.4 billion, excluding PTFI’s new downstream processing facilities. Its net debt is below its targeted range of $3-$4 billion. Freeport has a policy of distributing 50% of the available cash to its shareholders and the balance to either reduce debt or invest in growth projects. FCX has no significant debt maturities until 2027. Its long-term debt-to-capitalization is around 22.1% compared with 36.3% for Southern Copper and 29.3% for BHP Group.FCX offers a dividend yield of roughly 0.5% at the current stock price. Its payout ratio is 14% (a ratio below 60% is a good indicator that the dividend will be sustainable). Backed by strong financial health, the company's dividend is perceived to be safe and reliable.

Favorable Copper Prices Augur Well for Freeport

Prices of copper, the backbone of electrification, were volatile yet mostly favorable last year due to global economic and trade uncertainties. Copper prices started 2026 on a strong note, underpinned by robust demand from China and the United States. Structural tailwinds, including electric vehicles (EVs), renewable energy projects, data center growth and grid modernization, continue to boost copper consumption. Worries about tightening supply amid rising EV and infrastructure demand also supported the red metal. Supply risks increased amid concerns over lower output and potential disruptions at major global mining operations. These factors led to prices surging to roughly $6.4 per pound in late January. Prices of the red metal were mostly volatile during February, largely trading near $6 per pound. Copper prices came under pressure in March amid concerns about the impact of surging oil prices on the global economy due to the war in the Middle East, dragging down prices to a three-month low of around $5.3 per pound in late March. Prices rebounded in April on hopes of a de-escalation in the Iran war and are currently hovering around $6.2 per pound. Freeport’s average realized copper price climbed around 30% year over year to $5.78 per pound in the first quarter. Favorable prices are expected to continue to support its performance.

Higher Unit Costs Weigh on FCX’s Margins

Freeport faces headwinds from higher costs. Freeport's outlook for the second quarter of 2026 suggests higher costs on a sequential basis. It expects unit net cash costs to rise to $2.24 per pound, while projecting a full-year average of roughly $1.95 (compared with $1.65 in 2025). The projected second-quarter unit cost reflects a roughly 98% year over year and 17% increase from the prior quarter. The uptick in costs reflects higher costs of energy and other consumables due to the Middle East conflict and persistent pressure on volumes. Higher costs are expected to weigh on the company's margins.

Volume Weakness a Drag on FCX’s Prospects

Freeport’s copper sales volumes tumbled approximately 25% year over year in the first quarter to 657 million pounds, and fell from 709 million pounds in the prior quarter. The downside primarily resulted from lower operating rates due to the temporary suspension of operations since the mud rush incident at the Grasberg Block Cave mine in Indonesia in September 2025. While the company’s outlook for copper sales volumes for the second quarter of 2026 of 690 million pounds indicates a sequential improvement, it still suggests a 32% year-over-year decline. For full-year 2026, consolidated sales volume projections were revised lower to around 3.1 billion pounds of copper from the prior view of 3.4 billion pounds due to an expected delay in achieving full ramp-up of the Grasberg Block Cave mine. Lower sales volumes are expected to weigh on its top line.

FCX’s Earnings Estimates Going Down

Freeport’s earnings estimates have been going down over the past 60 days. The Zacks Consensus Estimate for 2026 earnings has been revised down over the same time frame.

Image Source: Zacks Investment Research

A Look at FCX’s Valuation

FCX is currently trading at a forward price/earnings of 21.52X, a 6.1% discount to the industry average of 22.91X. The FCX stock is trading at a discount to Southern Copper and at a premium to BHP Group.

FCX’s P/E F12M Vs. Industry, SCCO and BHP

Image Source: Zacks Investment Research

How Should Investors Play FCX Stock?

Freeport stands to benefit from progress in its expansion projects, which should boost production capacity. Its solid balance sheet offers the flexibility to invest in growth while continuing to support shareholder returns. Favorable copper prices further support the outlook. However, softer sales volume expectations and rising unit costs call for caution. Investors who already hold this Zacks Rank #3 (Hold) stock may find it prudent to maintain their positions.You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Freeport-McMoRan Inc. (FCX) : Free Stock Analysis Report

BHP Group Limited Sponsored ADR (BHP) : Free Stock Analysis Report

Southern Copper Corporation (SCCO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

VANCOUVER, BC / ACCESS Newswire / May 7, 2026 / Faraday Copper Corp. ("Faraday" or the "Company") (TSX:FDY) announces its financial results for the three months ended March 31, 2026.

Highlights Year to Date

-

Reported additional near-surface copper mineralization from eight drill holes at the American Eagle and Keel areas on March 24, 2026.

-

Closed a non-brokered private placement with participation by a Lundin Family Trust and BHP Group Limited ("BHP"), involving the issuance of 23,810,000 common shares at a price of $4.20 per share for aggregate gross proceeds of $100,002,000 on March 11, 2026.

-

Signed a letter of intent to acquire BHP's San Manuel property in Arizona on February 20, 2026, creating the potential for a multi-asset copper district in the USA (see news release dated February 20, 2026).

-

Reported near-surface copper mineralization from five drill holes in the American Eagle Area on January 22, 2026.

Upcoming Milestones

-

Drill results from the ongoing Phase IV drill program at the Copper Creek Project.

-

Signing definitive purchase agreements for BHP's San Manuel property in Arizona by the end of the third quarter of 2026.

Copper Creek Project Update

The project is a 100% owned, large copper deposit, located ~80 road kilometres ("km") northeast of Tucson, Arizona, and ~19 km northeast of San Manuel, Arizona. The resource area is ~3 km in length and is open in all directions. The property consists of ~80 square km of private land, patented and unpatented mining claims, and state prospecting permits. In addition, the Company controls ~26,000 acres of grazing leases which partially overlap with the claims and permits. The property is located within a historical mining district and a politically stable jurisdiction with extensive infrastructure including power, rail, roads, and access to skilled personnel.

The property is in the heart of the prolific southwestern porphyry copper region of North America at the projected intersection of a major northwest trending belt of copper deposits (Ray, Miami/Globe, Superior/Resolution, Johnson Camp) and a major east-northeast trending belt of deposits (San Manuel/Kalamazoo, Silver Bell, Lakeshore, Safford, Morenci).

The property hosts an early halo vein style porphyry copper deposit with high-grade, near-surface, breccia-hosted mineralization. Both mineralization types form the basis of the current Mineral Resource Estimate ("MRE") prepared in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum standards. Copper is the primary commodity, with molybdenum, silver and gold present in varying amounts associated with both types of mineralization.

On May 3, 2023, the Company announced an updated MRE and Preliminary Economic Assessment ("PEA") for the project, with a technical report titled "Copper Creek Project NI 43-101 Technical Report and Preliminary Economic Assessment" filed on SEDAR+ on June 13, 2023.

With a total of over 260,000 m of recent and historical drilling and modest past production, significant exploration upside remains. There are over 320 known breccia occurrences mapped at the surface, of which less than 15% have been drill tested and only 17 are included in the 2023 MRE.

In the Phase II drill program, assay results confirmed the potential for gold to occur in economic concentrations in certain phases of the mineralization. Gold is not currently included in the 2023 MRE. A sampling program for potential gold inclusion in future technical studies was undertaken. The results from the Childs Aldwinkle and Copper Prince breccias, as well as the Keel underground zone, have been returned and released. The Company continues to evaluate other areas for potential inclusion of gold in future mineral resource updates.

Phase III drilling was completed in mid-April 2025 with 79 drill holes and 30,071 m of drilling. All results from the Phase III drilling have been released. The program's framework was based on historical work, knowledge from the geological and recently updated structural model, the results from the Phase I and Phase II drill programs, geophysical and airborne spectral data sets, and economic criteria defined in the 2023 PEA base case. The focus of drilling was on the near-surface mineralization in the American Eagle, Area 51 and Rum areas.

On June 30, 2025, the Company received approval of its Exploration Plan of Operations ("EPO") by the BLM. The BLM published the final environmental assessment, and finding of no significant impact and issued a related decision record approving the EPO. The EPO includes up to 67 drill pads located on Federal land:

-

48 drill pads in or near the American Eagle area and the southern portion of the Mammoth resource area;

-

10 drill pads in or near other existing resource areas at Old Reliable, Globe, Copper Prince and Copper Giant; and

-

9 drill pads that enable reconnaissance drilling on previously untested targets.

Phase IV drilling commenced on September 18, 2025, with a planned 40,000 m diamond drill program with the goal of building on the Company's previous drilling success. The program will focus on the American Eagle area as well as new targets, infill, geotechnical, infrastructure, and hydrological drilling:

-

~20,000 m focused on American Eagle near-surface mineralization;

-

~10,000 m targeting oxide mineralization to increase the potential of copper cathode production; and

-

~10,000 m for new discoveries in the Copper Creek district.

The Company has reported results from metallurgical programs focused on grind size optimization that demonstrated the viability of coarse particle flotation, gold recoveries in concentrate and test work on near surface oxide mineralization.

The Company is focusing on exploration at the property while continuing to advance technical studies, environmental data gathering, and stakeholder outreach.

Financial Results

|

Three months ended |

||||||||

| In Canadian dollars |

March 31, 2026 |

March 31, 2025 |

||||||

| Exploration and evaluation expenses |

$ |

10,220,794 |

$ |

6,484,508 |

||||

| General and administration |

$ |

871,811 |

$ |

681,672 |

||||

| Share-based compensation |

$ |

652,018 |

$ |

384,126 |

||||

| Net loss |

$ |

9,891,214 |

$ |

7,820,431 |

||||

| Basic and diluted loss per share |

$ |

0.04 |

$ |

0.04 |

||||

Note: The financial information in this table was selected from the Company's condensed interim consolidated financial statements for the three months ended March 31, 2026 and 2025 (the "Financial Statements"), which are available on SEDAR+ at www.sedarplus.ca and the Company's website www.faradaycopper.com.

Selected Financial Information

| In Canadian dollars |

March 31, 2026 |

December 31, 2025 |

||||||

| Cash and cash equivalents |

$ |

120,799,916 |

$ |

37,880,822 |

||||

| Property and equipment |

$ |

17,724,931 |

$ |

17,513,854 |

||||

| Resource properties |

$ |

5,197,517 |

$ |

5,197,517 |

||||

| Total assets |

$ |

169,930,873 |

$ |

61,495,286 |

||||

Note: The financial information in this table was selected from the Financial Statements, which are available on SEDAR+ at www.sedarplus.ca and the Company's website www.faradaycopper.com.

Cash Flow, Liquidity and Capital Resources

The Company is a resource exploration-stage company and does not generate any revenue and has been mainly relying on equity-based financing to fund its operations. As at March 31, 2026, the Company had cash and cash equivalents of $120,799,916 (December 31, 2025 – $37,880,822) and current assets less current liabilities of $131,939,454 (December 31, 2025 – $35,424,377). While the Company has sufficient capital resources to fund its operations for the next 12 months, it is an exploration-stage company and does not anticipate achieving positive cash flow from operations for the foreseeable future. Accordingly, the Company anticipates needing to raise additional capital to fund its long-term business objectives.

During the three months ended March 31, 2026, cash provided by operating activities was $1,818,073 (2025 – cash used in operating activities of $9,253,611), cash used in investing activities was $24,472,947 (2025 – $222,601), and cash provided by financing activities was $105,572,608 (2025 – $35,200). The Company continues to incur operating costs primarily related to exploration and evaluation expenses. During the three months ended March 31, 2026, the Company raised net proceeds of $99,702,608 (2025 – $nil) from the issuance of common shares in a non‑brokered private placement. In addition, the Company raised $4,385,000 (2025 – $35,200) from the exercise of stock options and $1,485,000 (2025 – $nil) from the exercise of warrants.

On July 29, 2025, the Company completed a private placement financing for net proceeds of $46,964,411, which included share issuance costs of $1,809,039. The Company intends to use the proceeds from the financing to advance the Copper Creek Project and for general working capital purposes.

On March 11, 2026, the Company completed a private placement financing for net proceeds of $99,702,608, which included share issuance costs of $299,392. The Company intends to use the proceeds from the financing to advance the Copper Creek Project, due diligence and integration costs related to the acquisition of San Manuel, and for general working capital purposes.

Qualified Persons

The scientific and technical information contained in this news release has been reviewed and approved by Faraday's VP Exploration, Dr. Thomas Bissig, P. Geo., and VP, Projects and Evaluations, Zach Allwright, P.Eng.,who are considered a Qualified Person under National Instrument 43-101 – Standards of Disclosure for Mineral Projects ("NI 43-101").

About Faraday Copper

Faraday Copper is an exploration company focused on advancing its flagship copper project in Arizona, U.S. The Copper Creek Project is one of the largest undeveloped copper projects in North America with significant district scale exploration potential. Faraday has entered into a non-binding letter of intent with a subsidiary of BHP Group for the proposed acquisition of BHP's San Manuel Property, adjacent to the Copper Creek Project. The Company is well-funded to deliver on its key milestones and benefits from a management team and board of directors with senior mining company experience and expertise. Faraday trades on the TSX under the symbol "FDY".

For additional information please contact:

Stacey Pavlova, CFAVice President, Investor Relations & CommunicationsFaraday Copper Corp.E-mail: info@faradaycopper.comWebsite: www.faradaycopper.com

Cautionary Note on Forward Looking Statements

Some of the statements in this news release, other than statements of historical fact, are "forward-looking statements" and are based on the opinions and estimates of management as of the date such statements are made and are necessarily based on estimates and assumptions that are inherently subject to known and unknown risks, uncertainties and other factors that may cause actual results, level of activity, performance or achievements of Faraday to be materially different from those expressed or implied by such forward-looking statements. Such forward-looking statements and forward-looking information specifically include, but are not limited to, statements regarding: the Company's planned and ongoing exploration and drilling activities at the Copper Creek Project, including the scope, timing and results of the Phase IV drill program; the exploration potential and future development of the Copper Creek Project; the Company's ability to advance technical studies, environmental data collection and stakeholder engagement; the proposed acquisition of BHP's San Manuel property, including the ability to enter into and complete definitive purchase agreements and the expected timing thereof; the anticipated use of proceeds from recent financings; the sufficiency of the Company's capital resources to fund planned activities over the next 12 months; and the Company's expectations regarding future financing requirements.

Although Faraday believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements should not be in any way construed as guarantees of future performance and actual results or developments may differ materially. Accordingly, readers should not place undue reliance on forward-looking statements or information.

Factors that could cause actual results to differ materially from those in forward-looking statements include without limitation: market prices for metals; the conclusions of detailed feasibility and technical analyses; lower than expected grades and quantities of resources; receipt of regulatory approval; receipt of shareholder approval; mining rates and recovery rates; significant capital requirements; price volatility in the spot and forward markets for commodities; fluctuations in rates of exchange; taxation; controls, regulations and political or economic developments in the countries in which Faraday does or may carry on business; the speculative nature of mineral exploration and development, competition; loss of key employees; rising costs of labour, supplies, fuel and equipment; actual results of current exploration or reclamation activities; accidents; labour disputes; defective title to mineral claims or property or contests over claims to mineral properties; unexpected delays and costs inherent to consulting and accommodating rights of Indigenous peoples and other groups; risks, uncertainties and unanticipated delays associated with obtaining and maintaining necessary licenses, permits and authorizations and complying with permitting requirements, including those associated with the Copper Creek property; and uncertainties with respect to any future acquisitions by Faraday. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental events and hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and the risk of inadequate insurance or inability to obtain insurance to cover these risks as well as "Risk Factors" included in Faraday's disclosure documents filed on and available at www.sedarplus.ca.

This press release does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction to any person to whom it is unlawful to make such an offer or solicitation in such jurisdiction. This press release is not, and under no circumstances is to be construed as, a prospectus, an offering memorandum, an advertisement or a public offering of securities in Faraday in Canada, the United States or any other jurisdiction. No securities commission or similar authority in Canada or in the United States has reviewed or in any way passed upon this press release, and any representation to the contrary is an offence.

SOURCE: Faraday Copper Corp.

View the original press release on ACCESS Newswire

Dow Jones futures rose slightly early Thursday, along with S&P 500 futures and Nasdaq futures. Crude oil prices continued to slide on Iran deal hopes. Arm Holdings, Coherent and Albemarle were key earnings movers

The stock market rallied strongly Wednesday on Iran deal hopes and generally strong earnings. The S&P 500, Nasdaq and small-cap Russell 2000 all hit new highs.

Advanced Micro Devices soared on earnings, while Corning spiked on a big partnership with Nvidia. But there were some notable earnings losers, too.

TG Therapeutics bolted above a buy point on earnings. Rio Tinto, BHP Inc., ATI Inc. and Nvidia stock also moved above buy points.

Nvidia and Rio Tinto stock are on Leaderboard. AMD stock and ATI are on the IBD 50. Rio Tinto was Wednesday's IBD Stock Of The Day.

Dow Jones Futures Today

Dow Jones futures rose 0.2% vs. fair value. S&P 500 futures climbed 0.15% and Nasdaq-100 futures advanced 0.1%.

Crude oil futures fell 4% to nearly $91 a barrel. The U.S. is waiting for Iran's response to its latest peace plan.

The 10-year Treasury yield dipped to 4.33%.

Remember that overnight action in Dow futures and elsewhere doesn't necessarily translate into actual trading in the next regular stock market session.

Akamai, Iren Are Big Winners Late After AI-Led Market Retreat

Key Earnings

Arm Holdings, Coherent and Albemarle reported late Wednesday, along with AppLovin, Fortinet and many more.

ARM earnings beat but sales and sales guidance were just above consensus. The chip design firm initially jumped late but is sharply lower before Thursday's open. ARM stock surged 13.6% in Wednesday's session following strong results from fellow chipmaker AMD.

Coherent stock fell modestly after slightly beating views.

Albemarle earnings solidly beat. ALB stock jumped, signaling a move back toward a 206 cup-base buy point.

AppLovin stock rose slightly before the open while Fortinet soared on better-than-expected earnings, with both trying to recover from downturns.

Stock Market Rally

The stock market rally got a big boost from reports that a U.S.-Iran deal could be close. U.S. crude oil prices dived 7% to $95.08 a barrel, well below $100 but off early-Wednesday lows under $90. Generally positive earnings and other news also buoyed indexes.

The Dow Jones Industrial Average rose 1.4% in Wednesday's stock market trading. The S&P 500 index popped 1.5%, the Nasdaq composite jumped 2%, and the Russell 2000 gained 1.5%, all hitting new highs.

The Invesco S&P 500 Equal Weight ETF climbed 0.8%, briefly marking an all-time best intraday before backing off.

AMD stock spiked 18.6% on Wednesday's strong earnings and guidance. But Astera Labs reversed lower despite a beat-and-raise report, off 0.8% to just below a buy point. Lumentum Holdings sank 5.1%, Arista Networks dived 13.6%, and heavy construction firm Primoris crashed 50.1%.

Corning jumped 12% as Nvidia will help fund a massive expansion of the company's optical products capacity.

The 10-year Treasury yield fell six basis points to 4.35%.

ETFs

Among growth ETFs, the CapStone IBD 50 ETF stepped up 2.5%. The iShares Expanded Tech-Software Sector ETF fell 0.5%. The VanEck Vectors Semiconductor ETF surged 5.2%. Nvidia stock is the No. 1 holding in SMH, with AMD also a notable position and ARM also in the ETF.

ARK Innovation gained 3.9% and ARK Genomics ran 4.3% higher.

The SPDR S&P Metals & Mining ETF jumped 4.4%%. The Energy Select SPDR ETF tumbled 4.1%, while the Health Care Select Sector SPDR Fund rose a fraction. The Industrial Select Sector SPDR Fund advanced 2.6%. The Financial Select SPDR ETF climbed 0.5%.

Best Growth Stocks To Buy And Watch

Stocks In Buy Areas

Nvidia stock jumped 5.7% to 207.67, back above a 197.63 buy point from a cup base within a larger consolidation. NVDA has a 216.82 high-handle entry to the larger pattern, but broke the downtrend of that high handle Wednesday.

Rio Tinto gapped up 5% to 105.50, clearing a 101.33 cup-with-handle buy point. Base metal miner peer BHP stock leaped 6.4% to 84.33, topping a 81.26 entry from its own cup-with-handle base, according to MarketSurge. Both rallied with copper and other metal prices. Treasury yields and the U.S. dollar fell Wednesday.

ATI stock ran up 6.3% to 165.08, breaking the downtrend of a handle within a cup-with-handle base. The aerospace-exposed specialty metals play has a traditional buy point of 166.61.

TG Therapeutics stock surged 16.3% to 41.97, clearing a 38.38 early entry from a handle that was just a few cents too low to be proper. The year-long consolidation buy point is 46.48. Early Wednesday, TG Therapeutics missed earnings views on marketing and testing costs. But the biotech beat on revenue and guided up on full-year sales.

What To Do Now

The stock market rally continues to power ahead. Chip and AI stocks are still dominating, but some stocks from other sectors are showing strength too.

With the market running up for several days after pausing, the number of buying opportunities is slowing. But keep working on watchlists. Don't chase after extended stocks, and still be watchful for earnings. While there have been huge earnings winners, including AMD on Wednesday, the risk of big to huge losses is very real.

Read The Big Picture every day to stay in sync with the market direction and leading stocks and sectors.

Please follow Ed Carson on Threads at @edcarson1971 and X/Twitter at @IBD_ECarson for stock market updates and more.

YOU MAY ALSO LIKE:

Why This IBD Tool Simplifies The Search For Top Stocks

Want To Get Quick Profits And Avoid Big Losses? Try SwingTrader

IBD Digital: Unlock IBD's Premium Stock Lists, Tools And Analysis Today

Time The Market With IBD's ETF Market Strategy

How To Invest: Rules For When To Buy And Sell Stocks In Bull And Bear Markets

Average True Range: Your New Tool To Avoid Excessive Swings In Growth Stocks

Compass Minerals (CMP) came out with quarterly earnings of $0.63 per share, missing the Zacks Consensus Estimate of $0.66 per share. This compares to earnings of $0.63 per share a year ago. These figures are adjusted for non-recurring items.

This quarterly report represents an earnings surprise of -5.18%. A quarter ago, it was expected that this minerals producer would post earnings of $0.11 per share when it actually produced earnings of $0.43, delivering a surprise of +290.91%.

Over the last four quarters, the company has surpassed consensus EPS estimates just once.

Compass, which belongs to the Zacks Chemical – Diversified industry, posted revenues of $453.2 million for the quarter ended March 2026, surpassing the Zacks Consensus Estimate by 10.03%. This compares to year-ago revenues of $494.6 million. The company has topped consensus revenue estimates four times over the last four quarters.

The sustainability of the stock's immediate price movement based on the recently-released numbers and future earnings expectations will mostly depend on management's commentary on the earnings call.

Compass shares have added about 34.7% since the beginning of the year versus the S&P 500's gain of 6%.

What's Next for Compass?

While Compass has outperformed the market so far this year, the question that comes to investors' minds is: what's next for the stock?

There are no easy answers to this key question, but one reliable measure that can help investors address this is the company's earnings outlook. Not only does this include current consensus earnings expectations for the coming quarter(s), but also how these expectations have changed lately.

Empirical research shows a strong correlation between near-term stock movements and trends in earnings estimate revisions. Investors can track such revisions by themselves or rely on a tried-and-tested rating tool like the Zacks Rank, which has an impressive track record of harnessing the power of earnings estimate revisions.

Ahead of this earnings release, the estimate revisions trend for Compass was mixed. While the magnitude and direction of estimate revisions could change following the company's just-released earnings report, the current status translates into a Zacks Rank #3 (Hold) for the stock. So, the shares are expected to perform in line with the market in the near future. You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

It will be interesting to see how estimates for the coming quarters and the current fiscal year change in the days ahead. The current consensus EPS estimate is -$0.03 on $203.86 million in revenues for the coming quarter and $0.89 on $1.23 billion in revenues for the current fiscal year.

Investors should be mindful of the fact that the outlook for the industry can have a material impact on the performance of the stock as well. In terms of the Zacks Industry Rank, Chemical – Diversified is currently in the bottom 39% of the 250 plus Zacks industries. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

Another stock from the same industry, Olin (OLN), has yet to report results for the quarter ended March 2026. The results are expected to be released on May 7.

This chlor-alkali and ammunition producer' is expected to post quarterly loss of $0.67 per share in its upcoming report, which represents a year-over-year change of -1775%. The consensus EPS estimate for the quarter has been revised 88.6% higher over the last 30 days to the current level.

Olin's revenues are expected to be $1.57 billion, down 4.8% from the year-ago quarter.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Compass Minerals International, Inc. (CMP) : Free Stock Analysis Report

Olin Corporation (OLN) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE.

BHP Group's A$ fair value estimate has shifted from A$52.50 to A$53.40, giving you an updated anchor for how analysts are framing the stock today. That modest move lines up with recent Street research, where some firms have lifted price targets in A$, US$ and GBp while others remain cautious and hold to Neutral, Sell or Market Perform calls. As you read on, you will see how these changing targets fit into the broader analyst story and what signals to watch next.

What Wall Street Has Been Saying 🐂 Bullish Takeaways

- Argus has taken one of the more optimistic stances, lifting its US$ price target to $90 from $68 and pointing to what it describes as supportive long term fundamentals for BHP Group.

- Barclays, Citi and Berenberg have all raised their GBp targets through early 2026, which signals that several firms see room for the stock to better reflect their updated valuation work.

- Berenberg moved from an earlier Sell view to an upgrade in April 2026, suggesting that, in its view, execution and positioning now better support the stock than before.

🐻 Bearish Takeaways

- Bernstein trimmed its US$ target to $48 from $49.50 and kept a Market Perform rating, stressing that commodity mix and valuation remain central to its more measured stance.

- Several banks, including JPMorgan, Citi and Deutsche Bank, continue to sit at Neutral or Hold, reflecting caution around how BHP Group converts its asset base into growth and returns at current pricing.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there's more to the story. Head to the Simply Wall St Community to discover more perspectives!

ASX:BHP 1-Year Stock Price Chart

We've flagged 1 risk for BHP Group. See which could impact your investment.

What's in the News

- BHP entered an agreement with China Mineral Resources Group, indicating closer engagement with a major Chinese counterparty on iron ore supply and pricing terms.

- BHP reported March quarter production of 476.8 kt of copper, 62.8 Mt of iron ore, 3.8 Mt of steelmaking coal and 4.0 Mt of energy coal, along with year to date volumes across these commodities.

- BHP completed a long term silver streaming agreement with Wheaton Precious Metals International for its share of silver output from the Antamina mine in Peru, receiving upfront consideration of US$4.3b in exchange for a portion of future silver production.

- BHP's Board announced that Brandon Craig will become CEO on 1 July 2026, succeeding Mike Henry, and the company declared an interim dividend of US$0.73 per share for the six months ended 31 December 2025.

How This Changes the Fair Value For BHP Group

- Fair value in A$ has moved from A$52.50 to A$53.40.

- Assumed $ revenue growth has shifted from 1.07% to 1.15%.

- Assumed net profit margin has adjusted from 23.84% to 23.50%.

- The future P/E multiple has changed from 18.41x to 19.05x.

- The discount rate has remained unchanged at 8.56%.

Never Miss an Update: Follow The Narrative

Narratives connect BHP Group's business story to analyst forecasts and fair value estimates, updating as new data, news and projections come through. They give you a single place to see how the thesis is evolving over time.

Head over to the Simply Wall St Community and follow the Narrative on BHP Group to stay up to date on:

- How copper and potash projects are tied to decarbonization and electrification trends, and what that could mean for future demand for BHP Group's output.

- The role of long life, low cost assets and disciplined capital spending in supporting earnings resilience and BHP Group's capacity for shareholder returns.

- Key risks around iron ore concentration, project execution, regulation, inflation and ESG pressures that could affect margins and long term profitability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include BHP.AX.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

European equities traded in the US as American depositary receipts were tracking higher late Wednesday morning, rising 1.98% to 1,843.18 on the S&P Europe Select ADR Index.

From continental Europe, the gainers were led by accommodations booking company trivago (TRVG) and lender ING Group (ING), which advanced 14% and 5% respectively. They were followed by biopharmaceutical company Cellectis (CLLS) and lender Banco Santander (SAN), which climbed 4.8% and 4.2% respectively.

The decliners from continental Europe were led by internet advertising firm Criteo (CRTO) and petroleum refiner Equinor (EQNR), which shed 18% and 8.4% respectively. They were followed by semiconductor company Sequans Communications (SQNS) and oil and gas company Eni (E), which dropped 5.8% and 4.5% respectively.

The gainers from the UK were led by biopharmaceutical company Akari Therapeutics (AKTX) and insurance company Prudential (PUK), which rose 9.4% and 6.2% respectively. They were followed by mining company BHP Group (BHP) and lender Barclays (BCS), which were up 5.3% and 5.2% respectively.

The decliners from the UK and Ireland were led by biopharmaceutical companies Mereo BioPharma Group (MREO) and NuCana (NCNA), which fell 5.1% and 4% respectively. They were followed by oil and gas companies BP (BP) and Shell (SHEL), which lost 3.7% and 2.7% respectively.

OVERLAND PARK, Kan., May 06, 2026–(BUSINESS WIRE)–Compass Minerals (NYSE: CMP), a leading global provider of essential minerals, today reported fiscal 2026 second-quarter results. The company also announced that unionized employees at its Goderich mine have ratified a new three-year collective bargaining agreement.

Unless otherwise noted, it should be assumed that time periods referenced below are on a fiscal-year basis and financial amounts are in U.S. dollars.

MANAGEMENT COMMENTARY

"Consistent with our Back-to-Basics framework, during the quarter we took a significant step in strengthening our balance sheet by retiring the remaining $150 million of senior unsecured notes due in 2027 and removing our nearest debt maturity," said Edward C. Dowling Jr., president and CEO. "We had a strong winter across much of North America, and our Salt platform delivered on a high level of sales commitments while continuing to realize pricing gains. Our Plant Nutrition segment delivered another strong quarter at Ogden, with meaningful year-over-year improvement in cost performance and margins. Total company adjusted EBITDA for the quarter was $86.4 million, bringing us to $151.7 million for the first half of the year and on track to achieve our full-year outlook. We increased our Plant Nutrition guidance to reflect the strong results we continue to see in that operation, including higher expected sales volumes, better pricing and lower costs. We decreased our Salt guidance to reflect the differences in regional and product sales mix relative to forecast. Additionally, while we are seeing improvements in mine-level product costs, we have not yet achieved the level of production and efficiency gains in our mining operations that we had expected earlier in the year.

"Goderich mine is important for Compass Minerals, and I am pleased that we reached a new three-year agreement with the represented workforce. We believe we have struck a mutually beneficial arrangement that allows us to continue building upon the safe and reliable operations while allowing us to take steps to improve the mine's efficiency and flexibility.

"The hard work being done across the company is beginning to bear fruit. Some of this is manifesting itself currently in our financial results, while other initiatives will take a little more time. We know what we need to do and we are heading in the right direction, but there is more work to be done. We remain focused on reducing debt, improving our operations in all areas of the company, and building long-term value for shareholders."

QUARTERLY HIGHLIGHTS

- Net income of $12.7 million for the second quarter of 2026, compared to a net loss of $32.0 million in the prior year;

- Total company adjusted EBITDA for the second quarter of 2026 of $86.4 million, up 3% year over year;

- Operating earnings and adjusted EBITDA margins within the Salt business improved year over year; absolute operating earnings and adjusted EBITDA both declined 3% between comparative periods, driven principally by lower highway deicing sales volume;

- Continued improvements in pricing and cost structure increased Plant Nutrition segment operating earnings and adjusted EBITDA on both absolute and per-ton bases;

- Total debt declined 12% year over year to $713.0 million as March 31, 2026, while net debt decreased $119.2 million, or 16%, to $638.9 million over the same period; and

- Mid-point of full-year 2026 guidance for total company adjusted EBITDA maintained within modified range of $212 million to $236 million, reflecting stronger-than-expected results in the Plant Nutrition segment and adjustments related to changes in sales mix and operational matters in the Salt segment.

QUARTERLY FINANCIAL RESULTS

|

(in millions, except per share data) |

|

Three Months Ended Mar. 31, |

|

Six Months Ended Mar. 31, |

||||||||||||

|

|

2026 |

|

2025 |

|

2026 |

|

2025 |

|||||||||

|

GAAP Results: |

|

|

|

|

|

|

|

|

||||||||

|

Revenue |

|

$ |

453.2 |

|

$ |

494.6 |

|

|

$ |

849.3 |

|

$ |

801.8 |

|

||

|

Operating income (loss) |

|

|

56.0 |

|

|

|

(3.1 |

) |

|

|

92.6 |

|

|

|

(2.6 |

) |

|

Net income (loss) |

|

|

12.7 |

|

|