VANCOUVER, BC / ACCESS Newswire / June 16, 2026 / Apex Critical Metals Corp. (CSE:APXC)(OTCQX:APXCF)(FWB:KL9) ("Apex" or the "Company"), a mineral exploration company focused on advancing its strategic 100%-controlled Rift Rare Earth Project (the "Rift Project") within the Elk Creek Carbonatite Complex in southeastern Nebraska, U.S.A., is pleased to announce that the Company filed a technical report for the Rift Project entitled "NI 43-101 Technical Report on the Rift Project, Johnson and Pawnee Counties, Nebraska, USA" with an effective date of May 15, 2026, prepared for Apex by Robin J. Wilson, B.Sc. (Hons) Geology, MAusIMM, MAIG (the "Technical Report"). The Technical Report was prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects ("NI 43-101") and is available under the Company's issuer profile on SEDAR+ (available at www.sedarplus.ca).

About Apex Critical Metals Corp. (CSE:APXC)(OTCQX:APXCF)(FWB:KL9)

Apex Critical Metals Corp. is a Canadian exploration company focused on advancing rare earth element (REE) and niobium projects that support the growing demand for critical and strategic metals across the United States and Canada. The Company's flagship Rift Project, located within the highly prospective Elk Creek Carbonatite Complex in Nebraska, U.S.A., hosts extensive rare earth rights surrounding one of North America's most advanced niobium deposits. Two historical drillholes located within the 700 m corridor of interest returned broad intervals of >2.00% REO, with higher grade (>3.00% REO) intervals within. The Company's 2026 drilling has continued to demonstrate this grade profile and have expanded the footprint of the high-grade mineralization ("Trinity Zone) over approximately 380 m from the historical drillholes to-date. Additionally, drilling has delineated a new deeper horizon ("Neo Zone") of strongly elevated NdPr beneath the high-grade material with NdPr distributions between 30-50%. For more information, please see the Company's news releases dated April 7, 2026, April 28, 2026, May 6, 2026 and May 15, 2026, which are available under the Company's issuer profile on SEDAR+ (available at www.sedarplus.ca).

In Canada, Apex continues to advance its 100%-owned Cap Project, located 85 kilometres northeast of Prince George, British Columbia. The 2025 drill program confirmed an emerging niobium discovery with 0.59% Nb₂O₅ over 36 metres, including 1.08% Nb₂O₅ over 10 metres, within a 1.8-kilometre-long niobium trend. The Cap Project continues to demonstrate strong potential for niobium mineralization within a large and previously unrecognized carbonatite system.

With a growing portfolio of critical mineral projects in both Canada and the United States, Apex Critical Metals is strategically positioned to help strengthen domestic supply chains for the minerals essential to advanced technologies, clean energy, and national security. Apex is publicly listed in Canada on the Canadian Securities Exchange (CSE) under the symbol APXC and quoted on the OTCQX market in the United States under the symbol APXCF, and in Germany on the Borse Frankfurt under the symbol KL9 and/or WKN: A40CCQ. Find out more at www.apexcriticalmetals.com and watch our videos at https://apexcriticalmetals.com/apex-critical-metals-corporate-video/ and make sure to stay in touch by signing up for free news alerts at https://apexcriticalmetals.com/news/news-alerts/, or by following us on X (formerly Twitter), Facebook or LinkedIn.

On Behalf of the Board of Directors of

APEX CRITICAL METALS CORP.

Sean CharlandChief Executive OfficerTel: 604.681.1568Email: info@apexcriticalmetals.com

Neither the Canadian Securities Exchange (CSE) nor its Market Regulator (as that term is defined in the policies of the CSE) accepts responsibility for the adequacy or accuracy of this release.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This news release may contain "forward-looking information" as defined under applicable Canadian securities legislation and "forward-looking statements" as defined under applicable United States securities laws (collectively, "forward-looking statements"). Forward-looking statements consist of statements that are not purely historical, including any statements regarding beliefs, plans, expectations or intentions regarding the future. Forward-looking statements in this news release include (without limitation) statements regarding: the Company's exploration plans, drill programs and advancement of its mineral properties, including the Company's Rift Project, Cap Project, and other prospective asset; the potential for growing the portfolio through additional acquisitions or exploration; and the growing demand for critical and strategic metals across the United States and Canada. Forward-looking statements are subject to various known and unknown risks and uncertainties that may cause actual results, performance or developments to differ materially from those contained in the statements. Risks that could change or prevent these events, activities or developments from coming to fruition include: the Company's properties are at an early stage of development and no current mineral resources or reserves have been identified by the Company thereof, that we may not be able to fully finance any additional exploration on the Company's properties; that even if we are able to raise capital, costs for exploration activities may increase such that we may not have sufficient funds to pay for such exploration or processing activities; the timing and content of any future work programs; geological interpretations based on drilling that may change with more detailed information; potential process methods and mineral recoveries assumptions based on limited test work and by comparison to what are considered analogous deposits that, with further test work, may not be comparable; testing of our process may not prove successful or samples derived from our properties may not yield positive results, and even if such tests are successful or initial sample results are positive, the economic and other outcomes may not be as expected; the anticipated market demand for REE and other minerals may not be as expected; the availability of labour and equipment to undertake future exploration work and testing activities; geopolitical risks which may result in market and economic instability. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The forward-looking statements herein are made as of the date hereof, and the Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

SOURCE: Apex Critical Metals Corp.

View the original press release on ACCESS Newswire

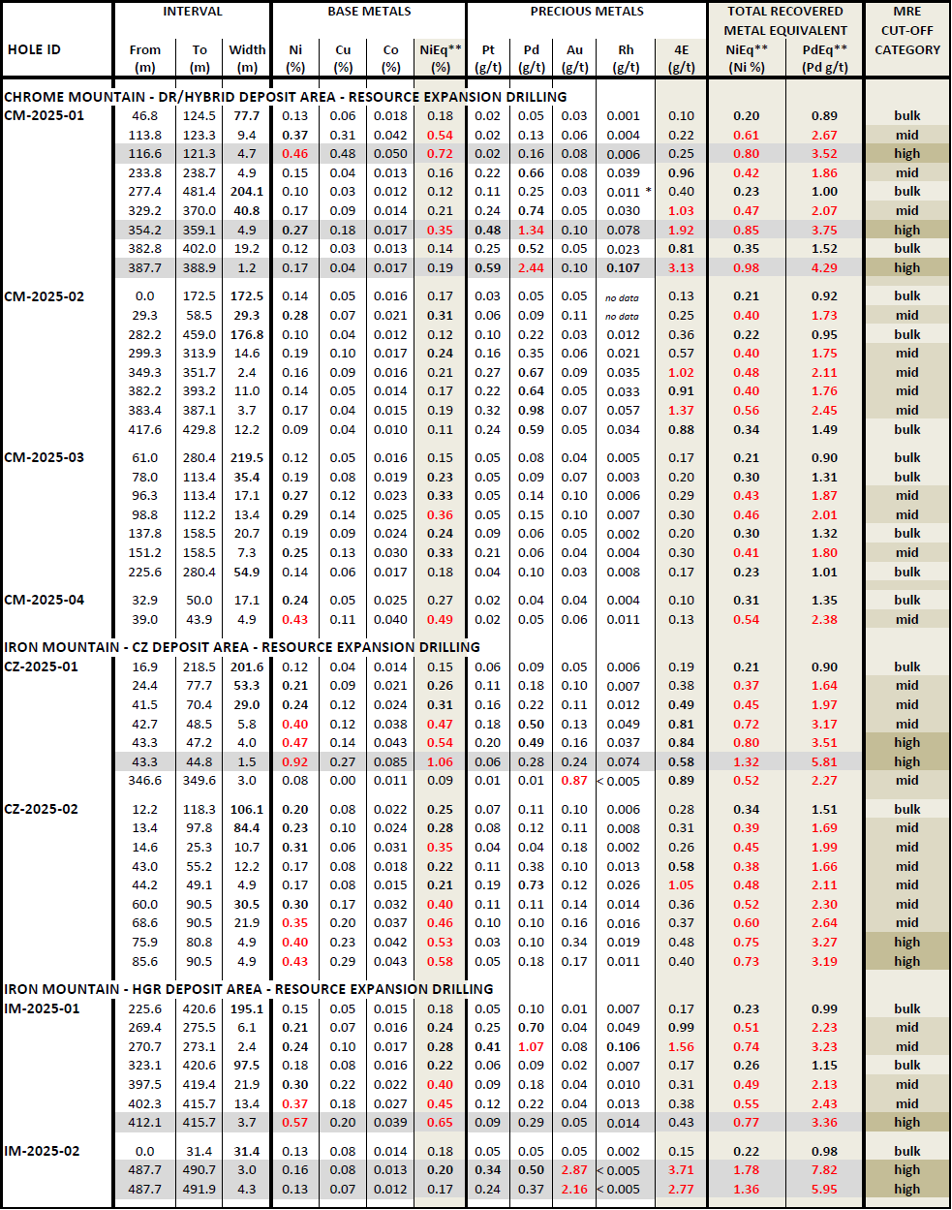

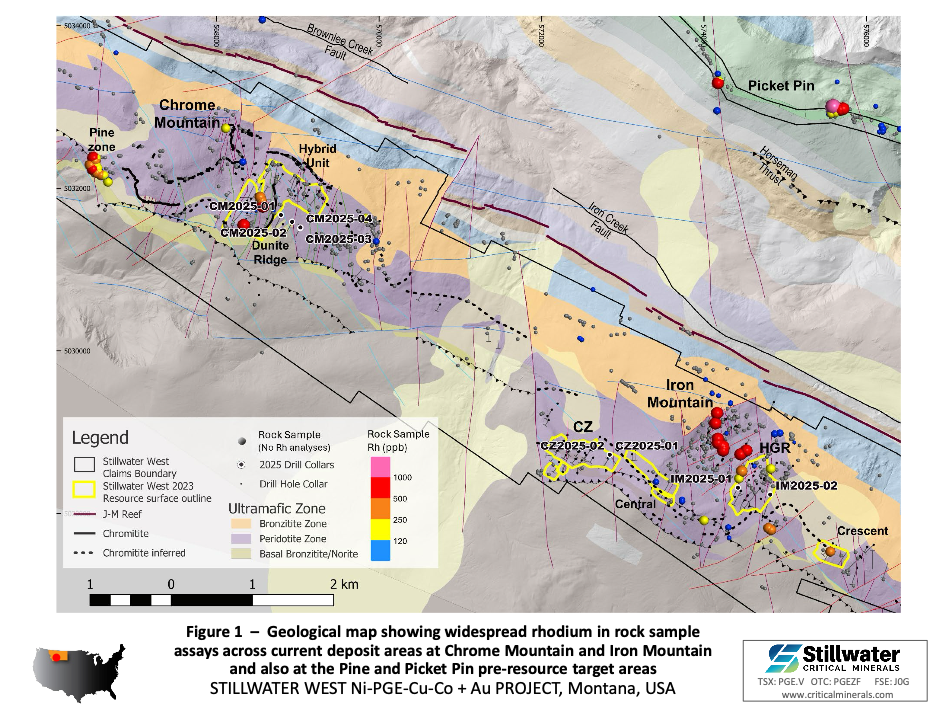

VANCOUVER, BC / ACCESS Newswire / June 15, 2026 / Stillwater Critical Minerals Corp. (TSXV:PGE)(OTCQB:PGEZF)(FSE:J0G) (the "Company", or "Stillwater") is pleased to announce that contractors have been retained and mobilization of drill rigs is expected in short order for the Company's largest exploration and resource expansion campaign to date at its flagship Stillwater West Ni-PGE-Cu-Co-Cr + Au project in Montana, USA.

The 2026 drill program is designed to build upon the successful 2025 program and the upcoming updated Mineral Resource Estimate, with a focus on expanding mid- to high-grade polymetallic sulphide mineralization within and adjacent to existing resource areas.

The program follows significant advancements achieved over the past year, including the expansion of the Company's geological model across more than 20 kilometres of strike length, completion of resource growth drilling, and continued refinement of multiple large-scale polymetallic sulphide targets identified through the Company's district-scale geological and geophysical programs.

Primary objectives of the 2026 field program include:

-

Expansion of existing near-surface resources at Chrome Mountain and Iron Mountain, the Company's primary resource growth areas, and other priority areas;

-

Continued delineation of higher-grade nickel-copper-PGE sulphide and polymetallic mineralization within the existing resource footprint;

-

Follow-up drilling on priority geophysical and geological targets identified through the Company's district-scale targeting programs;

-

Completion of ground geophysical surveys to refine existing deposit expansion targets and generate additional exploration drill targets across the project area;

-

Testing new zones of sulphide mineralization within the lower Stillwater Igneous Complex; and

-

Supporting future technical and economic studies through continued resource growth and geological de-risking.

Michael Rowley, President and CEO of Stillwater Critical Minerals, commented "We are excited to begin another important field season at Stillwater West as we continue advancing a large-scale domestic source of ten critical minerals in Montana. With strong support from our strategic partner Glencore plc, a growing U.S. focus on critical mineral security, and an upcoming updated Mineral Resource Estimate expected shortly, we believe 2026 will mark another significant step in advancing the project. Our objective remains clear: to continue growing and advancing the resource base while demonstrating the strategic importance of the Stillwater district to U.S. critical mineral supply chains."

Dr. Danie Grobler, Vice-President Exploration, commented "The successful completion of our 2025 drilling program has significantly advanced our understanding of the scale and potential of the Stillwater West project. The combination of resource expansion opportunities and multiple district-scale near-surface exploration targets provide an exceptional platform for continued growth as we advance one of the most significant undeveloped critical mineral systems in the United States.

Having spent much of my career working on large-scale polymetallic magmatic sulphide systems in South Africa's Bushveld Complex, including the Platreef deposit, I continue to be impressed by the geological similarities we are seeing at Stillwater West. While each project is unique, the scale of the mineralized system, the presence of extensive bulk-tonnage nickel-copper-PGE sulphide mineralization, and the opportunity for continued resource growth across a large district-scale land package underscore the significant long-term potential of the project."

Strategic Positioning

The Company believes that Stillwater West represents one of the largest undeveloped polymetallic critical mineral systems in the United States. The project hosts large-scale resources containing ten minerals identified as critical by the U.S. government and benefits from excellent infrastructure, access to power, water, rail and skilled labour within an established mining district. Results from the 2026 program are expected to contribute to ongoing resource growth, further definition of higher-grade mineralization, and the advancement of future development studies aimed at evaluating potential mining scenarios within the district.

Stillwater West hosts mineralization containing 1.6 billion pounds ("Blbs") of nickel, copper, and cobalt, 3.8 million ounces of platinum, palladium, rhodium, and gold, 2.3 Blbs of defined chromium plus undefined quantities of ruthenium and iridium. The project is located adjacent to Sibanye-Stillwater's producing operations in Montana's historic Stillwater mining district, providing access to established infrastructure, workforce, and mining expertise.

The Company expects to provide regular updates throughout the 2026 field season and looks forward to the release of the updated Mineral Resource Estimate in the near-term.

Upcoming Events

Company representatives will be attending the following events to discuss upcoming catalysts:

Fastmarkets Global Battery and Critical Materials Conference – Las Vegas, NV, June 22-25, 2026.

Montana Mining Association Annual Meeting 2026 – Butte, MT, USA, July 13-15, 2026.

Precious Metals Summit – Beaver Creek, CO, USA, September 22-25, 2026.

About Stillwater Critical Minerals Corp.

Stillwater Critical Minerals (TSXV:PGE)(OTCQB:PGEZF)(FSE:J0G) is a mineral exploration and development company advancing its 100%-owned Stillwater West Ni-PGE-Cu-Co-Cr + Au project in the Stillwater mining district of Montana, USA. Stillwater West is directly adjacent to Sibanye-Stillwater's operating Stillwater mines and processing infrastructure, the only primary platinum group element-producing complex in the United States. An NI 43-101 Mineral Resource Estimate released in January 2023 positions Stillwater West as one of the largest nickel and platinum group element resources in the United States and contains ten minerals currently listed as critical in the United States. With strategic investments by Glencore and an experienced technical team with expertise in Bushveld- and Platreef-style systems, the Company is advancing Stillwater West through ongoing resource expansion and technical studies.

Stillwater also holds a 49% interest in the high-grade Drayton-Black Lake-gold project adjacent to Nexgold Mining's development-stage Goliath Gold Complex in northwest Ontario, currently under an earn-in agreement with Heritage Mining, and the Kluane PGE-Ni-Cu-Co critical minerals project on trend with Nickel Creek Platinum's Wellgreen deposit in Canada's Yukon Territory. The Company also holds the Duke Island Cu-Ni-PGE property in Alaska and maintains a back-in right on the high-grade past-producing Yankee-Dundee in BC, following its sale in 2013.

FOR FURTHER INFORMATION, PLEASE CONTACT:Michael Rowley, President, CEO & Director – Stillwater Critical MineralsEmail: info@criticalminerals.com Phone: (604) 357 4790Web: http://criticalminerals.com Toll Free: (888) 432 0075

Forward-Looking Statements

This news release includes certain statements that may be deemed "forward-looking statements" or "forward-looking information". In particular, this press release contains forward-looking information relating to, among other things, the interpretation of exploration results, the potential for resource expansion, the timing and results of future resource estimates (including the targeted H1 2026 updated MRE), the timing and success of exploration activities, permitting timelines, and future plans and objectives of the Company. All statements in this release, other than statements of historical facts, are forward-looking statements that involve various risks and uncertainties. Although Stillwater Critical Minerals believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. For more information on Stillwater Critical Minerals and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedarplus.ca.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

SOURCE: Stillwater Critical Minerals Corp.

View the original press release on ACCESS Newswire

Rock Tech Lithium (RCK.V) has started trading its shares on Xetra, the electronic system of Deutsche Borse in Germany, under the ticker symbol RCK, the company said in a Friday news release.nnThe listing is expected to strengthen Rock Tech's presence in global capital markets, along with its listing in Canada and planned trading on NASDAQ.nnThe listing also broaden's the company's institutional investor base and enhances liquidity.nnTrading of Rock Tech's shares will be handled by mwb Wertpapierhandelsbank AG, as designated sponsor, with immediate effect.nnRock Tech's shares have already been available to German retail investors through venues such as Tradegate and Frankfurt, but the company recognizes Xetra as being Deutsche Borse's primary electronic trading platform and the reference market used by most German institutional investors.nnThis is not a new primary listing and does not change Rock Tech's status as a Canadian issuer. Rock Tech will continue to be governed by Canadian securities regulations and reporting requirements.

VANCOUVER, BC, June 9, 2026 /CNW/ – Eastern Platinum Limited (TSX: ELR) (JSE: EPS) ("Eastplats" or the "Company") is pleased to announce that the Supreme Court of British Columbia has struck out all three of 2538520 Ontario Limited's ("253") claims against the Company and its affiliates. The three proceedings include docket numbers S201427, S244818, and S252308. The Company and its advisors will review the decision in detail and consider next steps in due course.

About Eastern Platinum Limited

Eastplats owns directly and indirectly a number of PGM and chrome assets in the Republic of South Africa. All of the Company's properties are situated on the western limb (Crocodile River Mine) and eastern limb (Kennedy's Vale, Spitzkop, Mareesburg) of the Bushveld Complex, the geological environment that hosts approximately 80% of the world's PGM-bearing ore.

Operations at the Crocodile River Mine currently include mining and processing ore from the Zandfontein underground section to both produce PGM and chrome concentrates, respectively.

Cautionary Statement Regarding Forward-Looking Information

This news release contains "forward-looking statements" or "forward-looking information" (collectively referred to herein as "forward-looking statements") within the meaning of applicable securities legislation. Such forward-looking statements include, without limitation, forecasts, estimates, expectations and objectives for future operations that are subject to a number of assumptions, risks and uncertainties, many of which are beyond the control of the Company. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words "will," "plan," "intends," "may," "could," "expects," "anticipates" and similar expressions. Further disclosure of the risks and uncertainties facing the Company and other forward-looking statements are discussed in the Company's most recent Annual Information Form available under the Company's profile on www.sedarplus.ca.

In particular, this press release contains, without limitation, forward-looking statements pertaining to amongst other things, consideration of next steps based on the Supreme Court of British Columbia's decision. These forward-looking statements are based on assumptions made by and information currently available to the Company. Although management considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect. By their very nature, forward-looking statements involve inherent risks and uncertainties and readers are cautioned not to place undue reliance on these statements as a number of factors could cause actual results to differ materially from the beliefs, plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include, but are not limited to, unanticipated problems that may arise in the Company's production processes, commodity prices, lower than expected grades and quantities of resources, need for additional funding and availability of such additional funding on acceptable terms, economic conditions, currency fluctuations, competition and regulations, legal proceedings and risks related to operations in foreign countries.

All forward-looking statements in this news release are expressly qualified in their entirety by this cautionary statement, the "Cautionary Statement on Forward-Looking Information" section contained in the Company's most recent Management's Discussion and Analysis available under the Company's profile on www.sedarplus.ca. The forward-looking statements in this news release are made as of the date they are given and, except as required by applicable securities laws, the Company disclaims any intention or obligation, and does not undertake, to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained herein.

View original content to download multimedia: http://www.newswire.ca/en/releases/archive/June2026/09/c2622.html

Viewing insider transactions for Vital Metals Limited's (ASX:VML ) over the last year, we see that insiders were net buyers. This means that a larger number of shares were purchased by insiders in relation to shares sold.

While we would never suggest that investors should base their decisions solely on what the directors of a company have been doing, we do think it is perfectly logical to keep tabs on what insiders are doing.

The Last 12 Months Of Insider Transactions At Vital Metals

Over the last year, we can see that the biggest insider purchase was by Non-Executive Director Alexius Chan for AU$84k worth of shares, at about AU$0.10 per share. That implies that an insider found the current price of AU$0.11 per share to be enticing. While their view may have changed since the purchase was made, this does at least suggest they have had confidence in the company's future. We do always like to see insider buying, but it is worth noting if those purchases were made at well below today's share price, as the discount to value may have narrowed with the rising price. The good news for Vital Metals share holders is that an insider was buying at near the current price. Alexius Chan was the only individual insider to buy during the last year.

You can see the insider transactions (by companies and individuals) over the last year depicted in the chart below. By clicking on the graph below, you can see the precise details of each insider transaction!

Check out our latest analysis for Vital Metals

ASX:VML Insider Trading Volume June 9th 2026

Vital Metals is not the only stock insiders are buying. So take a peek at this free list of under-the-radar companies with insider buying.

Does Vital Metals Boast High Insider Ownership?

Looking at the total insider shareholdings in a company can help to inform your view of whether they are well aligned with common shareholders. We usually like to see fairly high levels of insider ownership. Our data indicates that Vital Metals insiders own about AU$2.8m worth of shares (which is 10% of the company). We do note, however, it is possible insiders have an indirect interest through a private company or other corporate structure. Whilst better than nothing, we're not overly impressed by these holdings.

What Might The Insider Transactions At Vital Metals Tell Us?

It doesn't really mean much that no insider has traded Vital Metals shares in the last quarter. On a brighter note, the transactions over the last year are encouraging. While we have no worries about the insider transactions, we'd be more comfortable if they owned more Vital Metals stock. While it's good to be aware of what's going on with the insider's ownership and transactions, we make sure to also consider what risks are facing a stock before making any investment decision. Every company has risks, and we've spotted 3 warning signs for Vital Metals (of which 2 make us uncomfortable!) you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Announces a significant vote of confidence from Company leadership, with members of management and insiders committing approximately $990,112.65 to acquire common shares of the Company at a deemed price of $0.28 per share, representing approximately 3.53 million shares. Ares Strategic Mining Inc shares C.ARS are trading up one cent at $0.28.

Read:

- Quantum Secure Encryption Scales Commercial Deployment as U.S. Pours Billions Into Quantum Computing

- The $1 Trillion Data Problem Quantum Computing Is About to Make Worse

- Seven Months After Its IPO, Starfighters Space (FJET) Lands in the Russell 3000® — And It Isn't Alone

- Cardiac AI Diagnostics Clears China Regulatory Gate Via Lishman Global As Edison Award, Northern California Deployment, And Indigenous Partnership Stack Validation

- The Quiet $35 Million Deal That Could Reshape the Western Rare Earth Race

Sociedad Química y Minera de Chile S.A. (NYSE:SQM) is one of the 8 Most Undervalued Growth Stocks to Buy Right Now.

n

On May 28, 2026, Scotiabank raised the firm’s price target on Sociedad Química y Minera de Chile S.A. (NYSE:SQM) to $105 from $100 and maintained an Outperform rating on the shares. Scotiabank said that, following the company’s Q1 results and guidance revisions, there are multiple ways to win with the stock.

n

Meanwhile, BofA raised the firm’s price target on Sociedad Química y Minera de Chile S.A. (NYSE:SQM) to $58 from $53 and maintained an Underperform rating on the shares. BofA cited “strong” Q1 operating results and raised its 2026-27 EBITDA estimates by 6.2%, reflecting higher Specialty Plant Nutrition volumes and modestly stronger lithium prices after a 15% rebound since the end of March.

n

n

On May 26, 2026, Sociedad Química y Minera de Chile S.A. (NYSE:SQM) reported Q1 revenue of $1.76B, above the consensus estimate of $1.70B. CEO Ricardo Ramos said the company delivered “strong results” in the quarter, with lithium sales volumes reaching approximately 69 thousand metric tons of LCE as SQM operated at full capacity to meet customer demand. Ramos said global lithium demand could exceed 1.9 million metric tons of LCE this year, while market dynamics suggest a tight supply-demand balance. SQM raised its expected sales volume growth guidance for the year from 10% to 15%.

n

Sociedad Química y Minera de Chile S.A. (NYSE:SQM) produces and sells specialty plant nutrients, iodine and its derivatives, and related products across Chile, Latin America, the Caribbean, Europe, North America, Asia, and internationally.

n

n

While we acknowledge the potential of SQM as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

n

n

n

READ NEXT: 33 Stocks That Should Double in 3 Years and Cathie Wood 2026 Portfolio: 10 Best Stocks to Buy.

n

Disclosure: None. Follow Insider Monkey on Google News.

Vancouver, British Columbia–(Newsfile Corp. – June 5, 2026) – Sego Resources Inc. (TSXV: SGZ) ("Sego" or "the Company"), has closed its non-brokered critical minerals flow through financing announced May 29, 2026, by issuing 21,200,000 common shares at $0.05 per share for gross proceeds of $1,060,000. The financing was oversubscribed due to investor demand. The closing of the placement is subject to receipt of approval of the TSX-V.

Private Placement

The offering consisted of 21,200,000 shares at $0.05 per share for gross proceeds of $1,060,000. There were no warrants attached to the private placement.

Finder's fees paid on the placement consisted of $52,500 and 1,050,000 share purchase warrants. The non-transferable share purchase warrants are exercisable at $0.05 for one year.

MI 61-101 Disclosure

MI 61-101 Disclosure

Elliot Strashin, an insider of the Company by right of holding >10% of the issued and outstanding shares of the Company, participated in the private placement for 2,000,000 common shares. A director of the Company, J Paul Stevenson, participated for 1,000,000 common shares. The participation by such insiders is considered a "related-party transaction" within the meaning of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions ("MI 61-101"). The Company has relied on exemptions from the formal valuation and minority shareholder approval requirements of MI 61-101 contained in sections 5.5(a) and 5.7(1)(a) of MI 61-101 in respect of related party participation in the Offering as neither the fair market value (as determined under MI 61-101) of the subject matter of, nor the fair market value of the consideration for, the transaction, insofar as it involved the related parties, exceeded 25% of the Company's market capitalization (as determined under MI 61-101).

All of the securities sold pursuant to the offering will be subject to a four-month-and-one-day hold period from the date of closing. The hold period will expire on October 6, 2026.

Proceeds of the private placement will be spent on exploration of the Company's Miner Mountain project. The gross proceeds received by the Company from the sale of the FT Units will be used to incur "Canadian exploration expenses" that are "flow-through critical mineral mining expenditures" (as such terms are defined in the Income Tax Act (Canada)) on the Company's properties located in British Columbia.

None of the securities issued in the Offering will be registered under the United States Securities Act of 1933, as amended (the "1933 Act").

There is no material change about the issuer that has not been generally disclosed.

For further information please contact: J. Paul Stevenson, CEO, and Director

(604) 682-2933 email: ceo@segoresources.com

About the Project

Sego is 100% owner of the Miner Mountain Project, an alkalic copper-gold porphyry and gold exploration project located near Princeton, British Columbia. The property is 2,056 hectares in size and is 15 km north of the Copper Mountain Mine operated by Hudbay Minerals Inc. Sego has a Memorandum of Understanding with the Upper Similkameen Indian Band on whose Traditional Territory the Miner Mountain Project is situated. Sego has received an Award of Excellence for its reclamation work on the Miner Mountain Project.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release. No regulatory authority has approved or disapproved the information contained in this news release.

This release includes certain statements that may be deemed "forward-looking statements". All statements in this release, other than statement of historical facts that address future production, reserve potential, exploration drilling, exploitation activities and events or developments that the Company expects re forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, statements are not guarantees of future performance and actual results or developments may differ materially from the forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include market prices, exploitation and exploration successes, continued availability of capital and financing, general economic, market or business conditions. Investors are cautioned that any such statements are not guarantees of future performance and those actual results or developments may differ materially from those projected in the forward-looking statements.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/300356

TORONTO, June 5, 2026 /CNW/ – Bravo Mining Corp. (TSXV: BRVO) (OTCQX: BRVMF) ("Bravo" or the "Company") today announces the results of voting from the Annual General and Special Meeting ("AGM") of shareholders held on June 4, 2026 (the "Meeting").

A total of 99,768,634 common shares were represented at the meeting, representing 72.83% of the issued and outstanding shares of the Company at the record date.

All matters presented for approval at the Meeting were approved by shareholders, as detailed below.

Number of Directors

Results of voting for the resolution to set the number of directors to be elected at four (4) were as follows:

|

Votes For |

% Vote For |

Votes Against |

% Vote Against |

|

99,713,160 |

99.94 |

55,474 |

0.06 |

Election of Directors

The following four individuals were elected as directors of the Company until the next annual meeting of shareholders or until their successors are elected or appointed, with the votes being cast by ballot were as follows:

|

Name of Nominee |

Votes For |

% Vote For |

Votes Withheld/Abstained |

% Withheld/Abstained |

|

Luis Mauricio F. Azevedo |

96,649,427 |

99.99 |

10,991 |

0.01 |

|

Margot Naudie |

90,721,193 |

93.86 |

5,939,225 |

6.14 |

|

Anthony Polglase |

96,649,427 |

99.99 |

10,991 |

0.01 |

|

Stephen Quin |

94,194,387 |

97.45 |

2,466,031 |

2.55 |

Appointment of Auditor

Results of voting for the resolution approving the re-appointment of KPMG LLP, Chartered Professional Accountants, as independent auditor of the Company for the ensuing year and authorizing the directors to fix the auditor's remuneration were as follows:

|

Votes For |

% Vote For |

Votes Withheld/Abstained |

% Withheld/Abstained |

|

99,750,360 |

99.98 |

18,264 |

0.02 |

Approval of Stock Option Plan

Results of voting by disinterested shareholders for the resolution to approve the Stock Option Plan were as follows:

|

Votes For |

% Vote For |

Votes Against |

% Withheld/Abstained |

|

36,043,432* |

93.65 |

2,443,529 |

6.35 |

|

* Excluding 58,173,457 shares held by Insiders |

Stock Option Grant

The Company also announces that it has granted a total of 2,182,000 stock options ("Options") to purchase common shares of the Company to directors, officers, employees and consultants of the Company pursuant to the Company's Stock Option Plan. Such Options are exercisable into common shares of the Company at an exercise price of $ 3.65 per common share, and vest as to 25% one year from the date of grant followed by 25% annually thereafter until fully vested. All the Options expire on June 3, 2031.

About Bravo Mining Corp.

Bravo is a Canadian and Brazil-based mineral exploration and development company focused on advancing its PGM+Au+Ni deposit while also exploring for IOCG-style Cu+Au and magmatic-style Ni+Cu+/-PGM+/-Au mineralization within its Luanga Project in the Carajás Mineral Province, Pará State, Brazil. Bravo is one of the most active explorers in Carajás.

The team, comprising of local and international geologists, has a proven track record of PGM, nickel, and copper discoveries in the region. They have successfully taken a past IOCG greenfield project from discovery to development and production in the Carajás while defining other significant deposit types in the region.

The Luanga Project is situated on mature freehold farming land and benefits from being located close to operating mines and a mining-experienced workforce, with excellent access and proximity to existing infrastructure, including road, rail, and hydroelectric grid power. Bravo's current Environmental, Social and Governance activities include planting more than 55,000 high-value trees in and around the project area and hiring and contracting locally.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

View original content to download multimedia: http://www.newswire.ca/en/releases/archive/June2026/05/c3852.html

Management Commits Additional Capital as Company Advances Toward Production, Government Deliveries, and Next Phase of Growth

n

VANCOUVER, BC – June 5, 2026 (NEWMEDIAWIRE) – Ares Strategic Mining Inc. (CSE: ARS) (OTCQX: ARSMF) (FRA: N8I1) is pleased to announce a significant vote of confidence from Company leadership, with members of management and insiders committing approximately $990,112.65 to acquire common shares of the Company at a deemed price of $0.28 per share, representing approximately 3.53 million shares.

n

The investment comes as Ares continues to achieve major milestones across its operations, including the commencement of mining, growing ore stockpiles at surface, continued construction progress across its processing facilities, and the recently announced U.S. Department of Defense fluorspar supply contract.

n

Management Demonstrates Confidence in Company's Future

n

The insider investment reflects management's belief in the Company's long-term value and future growth prospects. Over the past year, Ares has transformed from a development-stage company into an emerging producer with:

n

– Active mining operations at the Lost Sheep Mine;

n

– Growing surface ore stockpiles awaiting processing;

n

– Significant progress on both the Lumps Plant and Acidspar Flotation Plant;

n

– Major U.S. government contract awards;

n

– Strategic critical mineral positioning within the United States;

n

– A growing portfolio of assets and infrastructure.

n

James Walker, President and CEO of Ares Strategic Mining, commented: "Management believes the Company has reached a point where its operational progress, strategic assets, government relationships, and production trajectory are not fully reflected in the current market valuation. This investment demonstrates our confidence in the future we are building and our commitment to creating long-term value alongside shareholders."

n

Building Momentum

n

The Company believes it is entering one of the most significant periods in its history, with multiple catalysts expected over the coming months, including:

n

– Continued mine production and stockpiling;

n

– Advancement toward processing operations;

n

– Development of domestic acidspar production capacity;

n

– Execution of government contract opportunities;

n

– Expansion of commercial relationships;

n

– Continued strengthening of the Company's balance sheet and market position.

n

Walker concluded: "The story of Ares today is one of execution. We have built the mine, we are mining, we are building the processing facilities, and we are securing customers. Management's decision to invest nearly one million dollars alongside shareholders reflects our belief that the most exciting chapters of Ares are still ahead of us."

n

Renewal of Strategic Marketing and Investor Communications Program

n

The Company is also pleased to announce the renewal of its engagement with Pivotal CM Limited, which has supported Ares' investor communications, digital strategy, marketing initiatives, shareholder engagement, website management, conference organization, content development, and advertising campaigns.

n

Under the renewed arrangement, approximately US$356,250 of services will be satisfied through the issuance of common shares at the current market price, representing approximately 1.76 million shares, subject to regulatory approvals and final documentation. The renewed engagement is intended to support the Company's growing profile as it advances toward production and expands its visibility within North American and international capital markets.

n

Ares is also pleased to announce that the Company has agreed to the settlement of an aggregate of $69,046.47 of debt incurred by the Company for financial services provided by Prospero, and Craven Capital. The Company issued an aggregate of 246,595 common shares at a deemed price of $0.28 per Share.

n

Board Evolution Supports Company's Next Phase

n

The Company also announces that in response to public response, Lorenzo Esteva elected to step down from the Board of Directors. The Board thanks Mr. Esteva for his contributions and support during a period of significant growth for the Company.

n

Ares notes that certain public commentary regarding Mr. Esteva's prior regulatory history contained misrepresentation and erroneous characterizations. Responding to public comments, Mr. Esteva's lawyer clarified that he voluntarily resigned his FINRA registrations and disputed most allegations that have circulated publicly. The Company appreciates Lorenzo's professionalism throughout and regrets the inaccurate and false publications that caused him to step down. We wish him success in his future endeavors.

n

About Ares Strategic Mining

n

Ares Strategic Mining Inc. is a mining company focused on the development of its fluorspar projects in the U.S. The Company aims to become a significant supplier of high-grade fluorspar to North American markets, supporting industries vital to modern technology and infrastructure.

n

Lost Sheep Fluorspar Project – Delta, Utah

n

– 100% owned – 5,982 acres – 353 Claims

n

– Located in the Spor Mountain area, Juab County, Utah, approximately 214 km south-west of Salt Lake City.

n

– Fully Permitted – including mining permits.

n

– NI 43-101 Technical Report identified extensive high-grade fluorspar with low levels of impurities.

n

– Mining plan approved by BLM

n

First approved by Rex Rowley – Area Manager, Bureau of Land Management – 24th August 1992.

n

Renewed by Paul B. Baker – Minerals Program Manager, Bureau of Land Management – 12th December 2016.

n

ON BEHALF OF THE BOARD OF DIRECTORS OF ARES STRATEGIC MINING INC.

n

James WalkerChief Executive Officer and President

n

For further information, please contact James Walker by email at info@aresmining.com

n

DISCLOSURE AND FORWARD-LOOKING STATEMENTS:

n

Companies typically rely on comprehensive feasibility reports on mineral reserve estimates to reduce the risks and uncertainties associated with a production decision. Historically, situations where the issuer decides to put a mineral project into production without first establishing mineral reserves supported by a technical report and completing a feasibility study have a higher risk of economic or technical failure, though some industrial mineral ventures are relatively simple operations with low levels of investment and risk, where the operating entity has determined that a formal prefeasibility or feasibility study in conformance with NI 43-101 and 43-101 CP is not required for a production decision. Based on historical engineering work, geological reports, historical production data and current engineering work completed or in the process by Ares, the Company intends to move forward with the development of its Utah asset.

n

Certain information in this news release may contain forward-looking statements that involve substantial known and unknown risks and uncertainties. Forward-looking statements are often identified by terms such as "will", "may", "should", "anticipate", "expects" and similar expressions. All statements other than statements of historical fact included in this news release are forward-looking statements that involve risks and uncertainties. There can be no assurance that such statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from the Company's expectations include the failure to satisfy the conditions of the relevant securities exchange(s) and other risks detailed from time to time in the filings made by the Company with securities regulations. The reader is cautioned that assumptions used in the preparation of any forward-looking information may prove to be incorrect. Events or circumstances may cause actual results to differ materially from those predicted, as a result of numerous known and unknown risks, uncertainties, and other factors, many of which are beyond the control of the Company. The reader is cautioned not to place undue reliance on any forward-looking information. Such information, although considered reasonable by management at the time of preparation, may prove to be incorrect and actual results may differ materially from those anticipated. Forward-looking statements contained in this news release are expressly qualified by this cautionary statement. The forward-looking statements contained in this news release are made as of the date of this news release and the Company disclaims any intention or obligation to update or revise such information, except as required by applicable law.

View the original release on www.newmediawire.com

Toronto, Ontario–(Newsfile Corp. – June 2, 2026) – Olive Resource Capital Inc. (TSXV: OC) ("Olive" or the "Company") is pleased to provide investors an update on its investments for the period ending May 31, 2026.

Table 1: Olive's Investment Portfolio

| Name | Ticker | Sector | Category | (Audited)Value | (Unaudited)Value | (Unaudited)Value |

| Dec 31, 2025(1) | Apr 30, 2026(1) | May 31, 2026(1) | ||||

| Omai Gold Mines Corp.(2) | OMG.v | Precious Metals | Public Equity | $3,504,200 | $5,806,960 | $6,733,070 |

| Black Sheep Ventures Inc. | Private | Real Estate | Private Equity & Conv. Debenture | $1,527,912 | $1,541,063 | $1,514,543 |

| Arizona Sonoran Copper Co. | ASCU | Base Metals | Public Equity | $908,200 | $1,059,800 | $964,000 |

| Goldsky Resources Corp. (inc. Warrants) | GSKR.v | Precious Metals | Public Equity | $296,829 | $789,245 | $864,280 |

| Sun Valley Minerals Inc.(2) | Private | Precious Metals | Private Equity | $375,000 | $562,500 | $562,500 |

| Bravo Mining Corp. | BRVO.v | Precious Metals | Public Equity | $601,250 | $504,064 | $532,704 |

| GeoPark Ltd. | GPRK | Oil & Gas | Public Equity | $203,123 | $461,581 | $523,289 |

| Prospector Metals Corp. | PPP.v | Precious Metals | Public Equity | $295,029 | $455,699 | $486,698 |

| West Point Gold Corp.(2) | WPG.v | Precious Metals | Public Equity | $515,551 | $537,805 | $456,207 |

| Troilus Gold Corp (inc. Warrants) | TLG | Precious Metals | Public Equity | $482,000 | $327,500 | $455,000 |

| Other Public Equity Liquid Investments and Cash Equivalents (3) | $2,645,285 | $4,535,814 | $4,522,343 | |||

| Other Public Equity Fundamental Investments Incl. Warrants (4) | $4,031,648 | $1,968,791 | $2,473,948 | |||

| Other Private Equity, Loans, & Convertible Debenture Investments | $1,087,181 | $1,180,367 | $1,162,449 | |||

| Total | $16,473,208(5) | $19,731,191(5) | $21,251,033(5) | |||

Samuel Pelaez, the Company's President, CEO, CIO, and Director stated: "U.S. bond yields and the U.S. dollar both advanced in May. Gold and oil retreated as markets anticipate a resolution to the crisis at the Strait of Hormuz. Copper was a standout positive performer as warehouse inventories unexpectedly declined. Commodity equities outperformed their respective commodity references as perceived risk in markets decreased. At Olive, we made minor specific net additions to the portfolio. However, we remain cautious as major seasonal tailwinds begin to wind down at a time investors appear to show complacency toward the risks posed by a prolonged disruption in global energy markets."

Derek Macpherson, the Company's Executive Chairman stated: "Despite significant volatility in markets and most commodity related equity indices being relatively flat, Olive's portfolio continued to outperform, with the investments up more than 7% in the month. This is reflective in a shift in the portfolio as we look to add more copper exposure, following some significant wins with gold-focused equities. We continue to maintain above typical cash levels, based on our current market view and we are ready to take advantage of any market dislocations that may occur in the near-term."

Normal Course Issuer Bid ("NCIB")

As of the date of this release, the Company holds 4,000,000 common shares in treasury pending cancellation.

As of the date of this release Olive Resource Capital Inc. has 107,207,209 common shares outstanding inclusive of the shares in treasury pending cancellation.

About Olive Resource Capital Inc.:Olive is a resource-focused merchant bank and investment company with a portfolio of publicly listed and private securities. The Company's assets consist primarily of investments in natural resource companies in all stages of development.

For further information, please contact:

Derek Macpherson, Executive Chairman at derek@olive-resource.com or by phone at (416)294-6713 or Samuel Pelaez, President, CEO & CIO at sam@olive-resource.com. Olive's website is located at www.olive-resource.com.

Neither the TSX Venture Exchange Inc. nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange Inc.) accepts responsibility for the adequacy or accuracy of this release. The TSX Venture Exchange Inc. has in no way approved nor disapproved the information contained herein.

Cautionary Note Regarding Forward-Looking Statements: This press release contains "forward-looking information" within the meaning of applicable Canadian securities laws. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, identified by words or phrases such as "believes", "anticipates", "expects", "is expected", "scheduled", "estimates", "pending", "intends", "plans", "forecasts", "targets", or "hopes", or variations of such words and phrases or statements that certain actions, events or results "may", "could", "would", "will", "should", "might", "will be taken", or "occur" and similar expressions) are not statements of historical fact and may be forward-looking statements.

This news release includes forward-looking statements that are subject to risks and uncertainties. Forward-looking statements involve known and unknown risks, uncertainties, and other factors that could cause the actual results of Olive to be materially different from the historical results or from any future results expressed or implied by such forward-looking statements. All statements contained in this news release, other than statements of historical fact, are to be considered forward-looking, including, without limitation, statements concerning Olive's intended future disclosure practices. Although Olive believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Factors that could cause actual results to differ materially from such forward-looking information include, but are not limited to: past success or achievement does not guarantee future success; negative investment performance; downward market fluctuations; downward fluctuations in commodity prices and changes in the prices of commodities in general; uncertainties relating to the availability and costs of financing needed in the future; interest rate and exchange rate fluctuations; changes in economic and political conditions that could negatively affect certain commodity prices; and those risks set out in the Company's public documents filed on SEDAR+. Accordingly, readers should not place undue reliance on forward-looking information. Olive does not undertake to update any forward-looking information except in accordance with applicable securities laws.

This commentary is provided for general informational purposes only and does not constitute financial, investment, tax, legal or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. The information provided in this recording has been obtained from sources believed to be reliable and is believed to be accurate at the time of publishing but we do not represent that it is accurate or complete and it should not be relied upon as such.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/299744

- Sociedad Química y Minera de Chile S.A. recently held a board meeting on May 26, 2026, appointing Hernán Büchi Buc as Vice Chairman, and reported first-quarter 2026 results with sales of US$1,760.11 million and net income of US$364.72 million, both higher than a year earlier.

- The sharp increase in basic earnings per share from continuing operations to US$1.2769, compared with US$0.4815 a year ago, highlights a step-up in profitability that may influence how investors view the company’s earnings power.

- With this strong first-quarter earnings performance as context, we’ll now assess how the results may reshape Sociedad Química y Minera de Chile’s investment narrative.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Sociedad Química y Minera de Chile Investment Narrative Recap

To own Sociedad Química y Minera de Chile, you generally need to believe that lithium, iodine and specialty fertilizers can support attractive earnings, even through price swings and regulatory noise in Chile. The sharp Q1 2026 earnings jump is encouraging, but it does not remove key short term questions around lithium price volatility and the timing or terms of any Codelco related agreements, which remain the biggest swing factors for the story right now.

The Q1 2026 earnings release is the clearest reference point for assessing those catalysts today, with sales of US$1,760.11 million and net income of US$364.72 million well above the prior year’s levels. This step up in basic EPS to US$1.2769 gives investors more recent evidence about current earnings power, which may influence how comfortable they feel with higher capital spending plans and potential regulatory cost pressures tied to Chilean operations.

Yet despite the strong quarter, investors should be aware that mounting environmental and regulatory scrutiny in Chile could still…

Read the full narrative on Sociedad Química y Minera de Chile (it's free!)

Sociedad Química y Minera de Chile's narrative projects $6.5 billion revenue and $1.9 billion earnings by 2028. This requires 15.4% yearly revenue growth and about $1.4 billion earnings increase from $477.5 million today.

Uncover how Sociedad Química y Minera de Chile's forecasts yield a $75.33 fair value, a 12% downside to its current price.

Exploring Other PerspectivesSQM 1-Year Stock Price Chart

Some of the most optimistic analysts were already assuming revenue could reach about US$8.2 billion and earnings about US$2.3 billion, so Q1’s strong numbers may either support that upbeat view or prompt others to reassess how environmental and regulatory risks could still affect SQM’s long term path.

Explore 9 other fair value estimates on Sociedad Química y Minera de Chile – why the stock might be worth as much as 23% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sociedad Química y Minera de Chile research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Sociedad Química y Minera de Chile research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Sociedad Química y Minera de Chile's overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical datan and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or yourn financial situation. We aim to bring you long-term focused analysis driven by fundamental data.n Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.n Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SQM.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

The United States market has shown robust performance, climbing 1.6% in the last week and rising 28% over the past year, with earnings expected to grow by 17% annually. In this thriving environment, identifying small-cap stocks that may be undervalued and exhibit insider buying can provide unique opportunities for investors looking to leverage potential growth across various regions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Financial Institutions | 9.2x | 3.0x | 29.47% | ★★★★★☆ |

| Angel Oak Mortgage REIT | 12.9x | 5.8x | 26.66% | ★★★★★☆ |

| AVITA Medical | NA | 1.8x | 47.33% | ★★★★★☆ |

| Ferroglobe | NA | 0.6x | 21.14% | ★★★★★☆ |

| First Bancorp | 9.0x | 3.4x | 30.27% | ★★★★☆☆ |

| New Peoples Bankshares | 8.8x | 2.3x | 20.57% | ★★★★☆☆ |

| Similarweb | NA | 1.3x | 40.81% | ★★★★☆☆ |

| Metropolitan Bank Holding | 12.9x | 3.7x | 40.25% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 11.7x | 34.36% | ★★★☆☆☆ |

| Angel Studios | NA | 1.3x | -42.42% | ★★★☆☆☆ |

We’ll examine a selection from our screener results.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Arbor Realty Trust is a real estate investment trust that primarily focuses on investing in a diversified portfolio of structured finance assets in the multifamily, single-family rental, and commercial real estate markets, with a market cap of approximately $2.95 billion.

Operations: The company generates revenue primarily from its Agency Business and Structured Business segments. Its gross profit margin has shown a trend of reaching up to 93.44% in recent periods, indicating efficient cost management relative to revenue. Operating expenses, including general and administrative costs, form a significant portion of the company’s expenditure structure.

PE: 14.3x

Arbor Realty Trust, a smaller U.S. company, recently enhanced its financial flexibility by redeeming $787 million of notes and transferring $1.21 billion in assets to improved repurchase facilities with JPMorgan Chase Bank, N.A., boosting liquidity by $132.3 million. Despite a dip in net income to US$10.97 million for Q1 2026 from US$40.78 million the previous year, insider confidence is evident through share purchases earlier this year, suggesting potential growth prospects amidst current challenges like lower profit margins and impairment losses.

- Dive into the specifics of Arbor Realty Trust here with our thorough valuation report.

-

Examine Arbor Realty Trust’s past performance report to understand how it has performed in the past.

ABR Share price vs Value as at Jun 2026FMC

Simply Wall St Value Rating: ★★★★★☆

Overview: FMC is a company that operates in the agricultural sciences sector, focusing on providing innovative solutions, with a market capitalization of approximately $13.45 billion.

Operations: The company’s revenue primarily stems from its Innovative Solutions segment, with recent figures showing $3.43 billion in revenue. The gross profit margin has shown a notable downward trend, dropping to 32.09% as of March 2026. Operating expenses have been significant, with general and administrative costs being a major component alongside research and development expenses. Net income has experienced volatility, recently recording substantial losses driven by high non-operating expenses.

PE: -0.7x

FMC Corporation, a smaller player in the market, is catching attention with its recent financial maneuvers. Despite facing challenges like a net loss of US$281.3 million in Q1 2026 and declining sales, FMC’s strategic debt offerings—US$1.2 billion and US$750 million notes—aim to refinance existing obligations and support corporate activities. The company’s earnings are projected to grow significantly at 112% annually, hinting at potential recovery. Insider confidence through share purchases underscores belief in future prospects amid ongoing product innovations like Isoflex active’s EU approval for agricultural use starting 2027.

- Unlock comprehensive insights into our analysis of FMC stock in this valuation report.

-

Gain insights into FMC’s historical performance by reviewing our past performance report.

FMC Share price vs Value as at Jun 2026Exzeo Group

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Exzeo Group operates in the insurance industry, focusing on property and casualty segments, with a market capitalization of $3.45 billion.

Operations: Exzeo Group’s revenue is primarily derived from its Property & Casualty insurance segment, with recent figures showing $226.52 million. The company has experienced a notable shift in its financials, achieving a gross profit margin of 100% over the last six periods, reflecting efficient cost management.

PE: 15.4x

Exzeo Group, a dynamic player in the insurance tech sector, has caught attention with its recent inclusion in multiple Russell indexes, signaling potential growth. The company’s earnings for Q1 2026 reached US$20.41 million, up from US$17.95 million last year. Its innovative WindForm Pro solution addresses new regulatory requirements in Florida, enhancing operational efficiency for insurers. Insider confidence is reflected through a share repurchase program of up to US$12 million announced recently.

- Click here and access our complete valuation analysis report to understand the dynamics of Exzeo Group.

-

Evaluate Exzeo Group’s historical performance by accessing our past performance report.

XZO Share price vs Value as at Jun 2026Summing It All Up

- Click here to access our complete index of 73 Undervalued US Small Caps With Insider Buying.

- Shareholder in one or more of these companies? Ensure you’re never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven’t yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data n and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your n financial situation. We aim to bring you long-term focused analysis driven by fundamental data. n Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. n Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ABR FMC and XZO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

A month has gone by since the last earnings report for FMC (FMC). Shares have lost about 11.8% in that time frame, underperforming the S&P 500.

Will the recent negative trend continue leading up to its next earnings release, or is FMC due for a breakout? Well, first let's take a quick look at the latest earnings report in order to get a better handle on the recent catalysts for FMC Corporation before we dive into how investors and analysts have reacted as of late.

FMC’s Q1 Earnings Beat Estimates on Volume Gains and FX Tailwind

FMC reported a first-quarter 2026 adjusted loss per share of 23 cents. This compares unfavorably to the year-ago quarter’s adjusted earnings per share of 18 cents. The result was narrower than the Zacks Consensus Estimate of a loss of 39 cents.Quarterly revenues of $759 million declined 4% year over year but topped the consensus estimate of $721.8 million by 5.2%. Performance reflected favorable currency and stronger demand in select markets, partly offset by pricing pressure and partner-related volume headwinds. New active ingredient sales doubled year over year.Profitability also declined as lower pricing and higher costs more than offset benefits from volume and currency. Tariffs and unfavorable raw material costs were the key cost headwinds, while lower R&D expenses provided some relief. The decline was also driven by tax charges related to higher valuation allowances, along with lower sales, higher restructuring costs and higher interest expense.

Regional Sales Performance

North America sales increased 6% year over year to $198 million. FMC attributed the gain to high-teens sales growth for branded products led by herbicides, alongside solid growth in Plant Health and strong Cyazypyr performance. Sales topped the consensus estimate of $185.1 million.EMEA revenues rose 13% to $307 million on solid branded volume growth led by herbicides and Cyazypyr. Branded pricing was similar to the year-ago quarter, while registration losses were in line with expectations and represented an estimated 5% headwind. It outpaced the consensus estimate of $282.4 million.Latin America revenues fell 14% to $177 million. FMC cited lower branded volumes mainly for core portfolio products and a competitive market for core products that pressured branded pricing, though higher growth-portfolio sales led by Cyazypyr and new actives provided a partial offset. It missed the consensus estimate of $178.7 million.Asia revenues, excluding India, declined 36% year over year to $81 million. The company pointed to lower branded pricing in line with expectations and weaker insecticide volumes amid challenged grower economics tied to geopolitical uncertainty, partially offset by strong Cyazypyr growth. It beat the consensus estimate of $72.4 million.

Financials

The company had cash and cash equivalents of $390.9 million at the end of the quarter. Long-term debt was $2.77 billion.

Outlook

FMC reaffirmed its full-year 2026 outlook, calling for revenue excluding India of $3.6 billion to $3.8 billion and adjusted EBITDA of $670 million to $730 million. Adjusted earnings per diluted share are still expected in the $1.63-$1.89 range, while free cash flow is projected between negative $65 million and positive $65 million.The company’s full-year framework assumes interest expense of $255-$275 million and an adjusted tax rate of 16-18%, with depreciation and amortization of $160-$170 million. Capital additions and other investing activities are projected at $90-$110 million. FMC also expects the India contribution loss in 2026 to be roughly $90 million of revenue and $0 million of EBITDA.For the second quarter, FMC expects revenue excluding India of $850 million to $900 million, with adjusted EBITDA of $130 million to $150 million and adjusted earnings per diluted share of 16-26 cents. The company expects year-over-year pressure to be driven largely by reduced orders from diamide partners and the removal of India from the reported base period.

How Have Estimates Been Moving Since Then?

Since the earnings release, investors have witnessed a downward trend in fresh estimates.

The consensus estimate has shifted -47.5% due to these changes.

VGM Scores

At this time, FMC has a poor Growth Score of F, a score with the same score on the momentum front. However, the stock has a grade of C on the value side, putting it in the middle 20% for this investment strategy.

Overall, the stock has an aggregate VGM Score of F. If you aren't focused on one strategy, this score is the one you should be interested in.

Outlook

Estimates have been broadly trending downward for the stock, and the magnitude of these revisions indicates a downward shift. Interestingly, FMC has a Zacks Rank #3 (Hold). We expect an in-line return from the stock in the next few months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

FMC Corporation (FMC) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Vancouver, British Columbia–(Newsfile Corp. – May 29, 2026) – Sego Resources Inc.(TSXV: SGZ) ("Sego" or "the Company"), is pleased to announce a critical minerals flow through financing.

The gross proceeds of the financing will be used for exploration at the Miner Mountain project, located near Princeton, BC..

The Miner Mountain project is an Alkalic Porphyry Copper-Gold exploration project which encompasses near-surface disseminated gold mineralization and porphyry copper-gold targets.

Private Placement

The offering will consist of up to 19,400,000 flow-through common shares at $0.05 per share for gross proceeds of up to $ 970,000. There will be no warrants attached to the offering.

Insiders of the Company will participate in the private placement. A commission of 7% cash and 7% warrants exercisable at $0.05 for one year will be paid on a portion of the private placement .

This offering will be subject to the completion of formal documentation, receipt of all necessary regulatory approvals, including the TSX Venture Exchange and other customary conditions. All of the securities sold pursuant to the offering will be subject to a four-month hold period from the date of closing.

None of the securities issued in the Offering will be registered under the United States Securities Act of 1933, as amended (the "1933 Act").

There is no material change about the issuer that has not been generally disclosed.

For further information please contact: J. Paul Stevenson, CEO

(604) 682-2933

About the Project

Sego is 100% owner of the Miner Mountain Project, an alkalic copper-gold porphyry and gold exploration project located near Princeton, British Columbia. The property is 2,056 hectares in size and is 15 km north of the Copper Mountain Mine operated by Hudbay Minerals Inc. Sego has a Memorandum of Understanding with the Upper Similkameen Indian Band on whose Traditional Territory the Miner Mountain Project is situated. Sego has received an Award of Excellence for its reclamation work on the Miner Mountain Project.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release. No regulatory authority has approved or disapproved the information contained in this news release.

This release includes certain statements that may be deemed "forward-looking statements". All statements in this release, other than statement of historical facts that address future production, reserve potential, exploration drilling, exploitation activities and events or developments that the Company expects re forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, statements are not guarantees of future performance and actual results or developments may differ materially from the forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include market prices, exploitation and exploration successes, continued availability of capital and financing, general economic, market or business conditions. Investors are cautioned that any such statements are not guarantees of future performance and those actual results or developments may differ materially from those projected in the forward-looking statements.

NOT FOR DISTRIBUTION TO UNITED STATES NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/299494

Albemarle Corporation ALB remains committed to driving shareholder value by leveraging solid liquidity and healthy cash flows. At the end of the first quarter of 2026, ALB had liquidity of around $2.7 billion, including cash and cash equivalents of around $1.1 billion. It generated an operating cash flow of $346 million and free cash flow of $248 million in the quarter. ALB generated free cash flow of $692 million for full-year 2025, driven by strong cash conversion, lower capital spending and productivity measures. Free cash flow in 2026 is expected to be supported by the recent uptick in lithium prices, strong cash conversion and productivity. Its ability to convert improving operating performance into free cash is likely to result in incremental returns to shareholders. ALB expected full-year 2026 operating cash flow conversion to be within its long-term target range of 60-70% at the average lithium market price of $20 per kilogram.The company remains focused on maintaining its dividend payout. It has raised its quarterly dividend for the 30th straight year. ALB offers a dividend yield of 0.9% at the current stock price. Backed by healthy cash flows and sound financial health, the company's dividend is perceived to be safe and reliable.Among its peers, Sociedad Quimica y Minera de Chile S.A. SQM exited the first quarter with strong liquidity, with cash and cash equivalents being around $2.8 billion. Sociedad Quimica’s solid cash position supports its capital investment in growth projects and shareholder-friendly actions. Sociedad Quimica projects total capital expenditure of $2.7 billion for the 2025-2027 period, which includes the expansion of lithium carbonate and lithium hydroxide capacity in Chile. ICL Group Ltd. ICL ended the first quarter with cash and cash equivalents, and short-term investments and deposits of $581 million. Including unutilized revolving credit facility and securitization, ICL Group had cash resources of $1,491 million at the end of the quarter. ICL generated an operating cash flow of $195 million in the first quarter. It distributed roughly $224 million in dividends to its shareholders last year.

ALB’s Price Performance, Valuation & Estimates

Albemarle has gained 38.3% in the past six months compared with the Zacks Chemical – Diversified industry’s rise of 25.6%.

Image Source: Zacks Investment Research

ALB is currently trading at a forward price-to-sales ratio of 3.37, above the industry. It carries a Value Score of D.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for ALB’s 2026 earnings implies a year-over-year rise of 1,555.7%. The EPS estimates for 2026 have been trending higher over the past 60 days.

Image Source: Zacks Investment Research

ALB stock currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Albemarle Corporation (ALB) : Free Stock Analysis Report

Sociedad Quimica y Minera S.A. (SQM) : Free Stock Analysis Report

ICL Group Ltd. (ICL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

This article first appeared on GuruFocus.

- Lithium Sales Volume: Increased by 25% year-over-year, reaching approximately 69,000 metric tons of lithium carbonate equivalent.

- Contribution to Chilean State: Over $530 million in contributions through payments, taxes, and transfers to local governments in the first quarter.

- Projected Lithium Sales Volume Growth: Expected to grow by approximately 15% compared to 2025.