Even if it's not a huge purchase, we think it was good to see that Alexius Chan, the Non-Executive Director of Vital Metals Limited (ASX:VML) recently shelled out AU$84k to buy stock, at AU$0.10 per share. While we're hesitant to get too excited about a purchase of that size, we do note it increased their holding by a solid 32%.

The Last 12 Months Of Insider Transactions At Vital Metals

Notably, that recent purchase by Alexius Chan is the biggest insider purchase of Vital Metals shares that we've seen in the last year. Although we like to see insider buying, we note that this large purchase was at significantly below the recent price of AU$0.17. Because it occurred at a lower valuation, it doesn't tell us much about whether insiders might find today's price attractive.

In the last twelve months Vital Metals insiders were buying shares, but not selling. You can see the insider transactions (by companies and individuals) over the last year depicted in the chart below. If you want to know exactly who sold, for how much, and when, simply click on the graph below!

View our latest analysis for Vital Metals

ASX:VML Insider Trading Volume December 31st 2025

Vital Metals is not the only stock that insiders are buying. For those who like to find small cap companies at attractive valuations, this free list of growing companies with recent insider purchasing, could be just the ticket.

Insider Ownership Of Vital Metals

I like to look at how many shares insiders own in a company, to help inform my view of how aligned they are with insiders. Usually, the higher the insider ownership, the more likely it is that insiders will be incentivised to build the company for the long term. From our data, it seems that Vital Metals insiders own 8.8% of the company, worth about AU$2.2m. We do note, however, it is possible insiders have an indirect interest through a private company or other corporate structure. Whilst better than nothing, we're not overly impressed by these holdings.

So What Does This Data Suggest About Vital Metals Insiders?

The recent insider purchase is heartening. And an analysis of the transactions over the last year also gives us confidence. However, we note that the company didn't make a profit over the last twelve months, which makes us cautious. On this analysis the only slight negative we see is the fairly low (overall) insider ownership; their transactions suggest that they are quite positive on Vital Metals stock. While it's good to be aware of what's going on with the insider's ownership and transactions, we make sure to also consider what risks are facing a stock before making any investment decision. To that end, you should learn about the 5 warning signs we've spotted with Vital Metals (including 3 which shouldn't be ignored).

If you would prefer to check out another company — one with potentially superior financials — then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

As the Australian market approaches the end of the year, it appears to be winding down with a slight dip, likely due to profit-taking ahead of the holiday season. Despite this temporary lull, small-cap stocks continue to attract attention for their potential growth opportunities, especially in sectors like mining and technology where recent developments have shown promising signs.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 10.00% | 9.57% | ★★★★★★ |

| Joyce | NA | 9.93% | 17.54% | ★★★★★★ |

| Hearts and Minds Investments | NA | 56.27% | 59.19% | ★★★★★★ |

| Euroz Hartleys Group | NA | 1.82% | -25.32% | ★★★★★★ |

| Argosy Minerals | NA | -12.81% | -19.89% | ★★★★★★ |

| Focus Minerals | NA | 75.35% | 51.34% | ★★★★★★ |

| Djerriwarrh Investments | 2.39% | 8.18% | 7.91% | ★★★★★★ |

| Energy World | NA | -47.50% | -44.86% | ★★★★★☆ |

| Zimplats Holdings | 5.44% | -9.79% | -42.03% | ★★★★★☆ |

| Australian United Investment | 1.90% | 5.23% | 4.56% | ★★★★☆☆ |

Let’s dive into some prime choices out of from the screener.

Simply Wall St Value Rating: ★★★★★★

Overview: Cogstate Limited is a neuroscience solutions company that develops and commercializes digital brain health assessments globally, with a market capitalization of A$387.87 million.

Operations: Cogstate generates revenue primarily from its Clinical Trials segment, contributing $50.58 million, while the Healthcare segment adds $2.51 million.

Cogstate, a neuroscience tech firm focusing on digital brain health assessments, is capitalizing on strategic partnerships and AI innovation to broaden its market presence. With no debt compared to five years ago when the debt-to-equity ratio was 16.4%, Cogstate’s financial health seems robust. The company’s earnings growth of 86% over the past year surpasses the industry average of 20%. Analysts forecast an annual revenue increase of 7.6% over three years and project profit margins rising from 19.1% to 21.5%. Trading at A$1.69, with a target price of A$2.19, suggests potential upside amid competitive pressures and regulatory challenges.

ASX:CGS Debt to Equity as at Dec 2025GenusPlus Group

Simply Wall St Value Rating: ★★★★★★

Overview: GenusPlus Group Ltd specializes in the installation, construction, and maintenance of power and communication systems in Australia, with a market capitalization of A$1.14 billion.

Operations: GenusPlus Group generates revenue through three primary segments: Infrastructure (A$405.10 million), Energy & Engineering (A$224.06 million), and Services (A$122.11 million).

With a strong foothold in Australia’s renewable energy sector, GenusPlus Group is poised to benefit from the country’s grid upgrades and diverse project pipeline that reduces geographic risks. The company has strategically reduced its debt to equity ratio from 7% to 6.3% over five years, while maintaining profitability with more cash than total debt. Earnings growth of 83.6% last year outpaced the industry average by a significant margin, showcasing high-quality earnings potential. However, challenges such as integration issues from acquisitions and reliance on government infrastructure spending could impact future performance despite projected annual revenue growth of 14.2%.

ASX:GNP Debt to Equity as at Dec 2025Tasmea

Simply Wall St Value Rating: ★★★★★☆

Overview: Tasmea Limited specializes in providing shutdown, maintenance, emergency breakdown, and capital upgrade services across Australia with a market capitalization of A$1.10 billion.

Operations: Tasmea generates revenue primarily from Electrical Services (A$212.71 million), Civil Services (A$103.07 million), and Mechanical Services (A$144.87 million). Water & Fluid services contribute A$87.06 million to the total revenue.

Tasmea, a smaller player in the construction sector, showcases impressive earnings growth of 74.9% over the past year, significantly outpacing the industry average of 6.5%. Despite its high net debt to equity ratio at 59.8%, Tasmea’s interest payments are well-covered by EBIT at 10.5 times, indicating robust financial health in this regard. The company recently completed a follow-on equity offering worth A$27.5 million and announced an acquisition of WorkPac, suggesting strategic expansion plans. Trading nearly half below its estimated fair value and with forecasted earnings growth of 15.96% annually, Tasmea seems poised for further development despite its debt concerns.

- Dive into the specifics of Tasmea here with our thorough health report.

-

Evaluate Tasmea’s historical performance by accessing our past performance report.

ASX:TEA Debt to Equity as at Dec 2025Summing It All Up

- Gain an insight into the universe of 59 ASX Undiscovered Gems With Strong Fundamentals by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio’s performance.

- Discover a world of investment opportunities with Simply Wall St’s free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven’t yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:CGS ASX:GNP and ASX:TEA.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

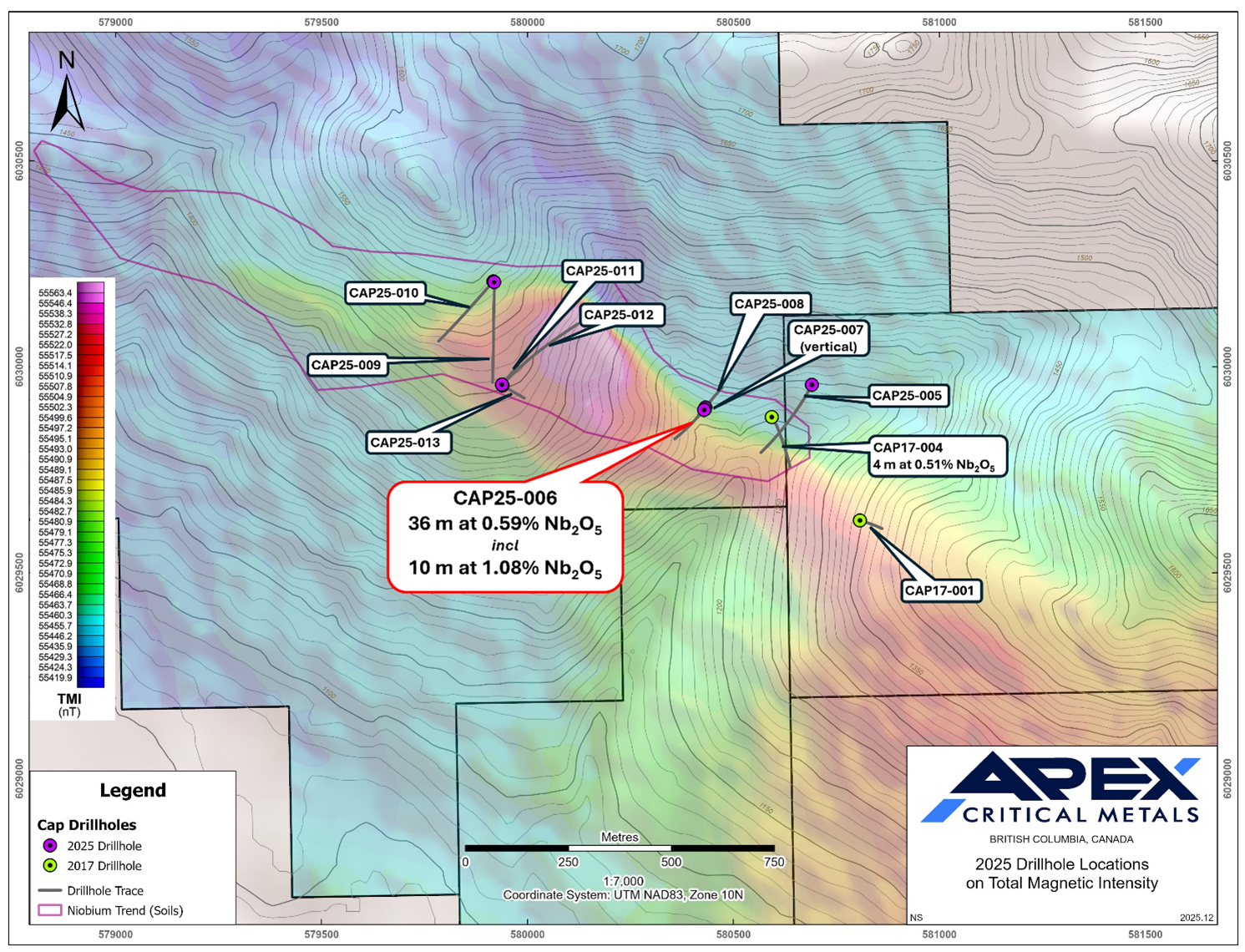

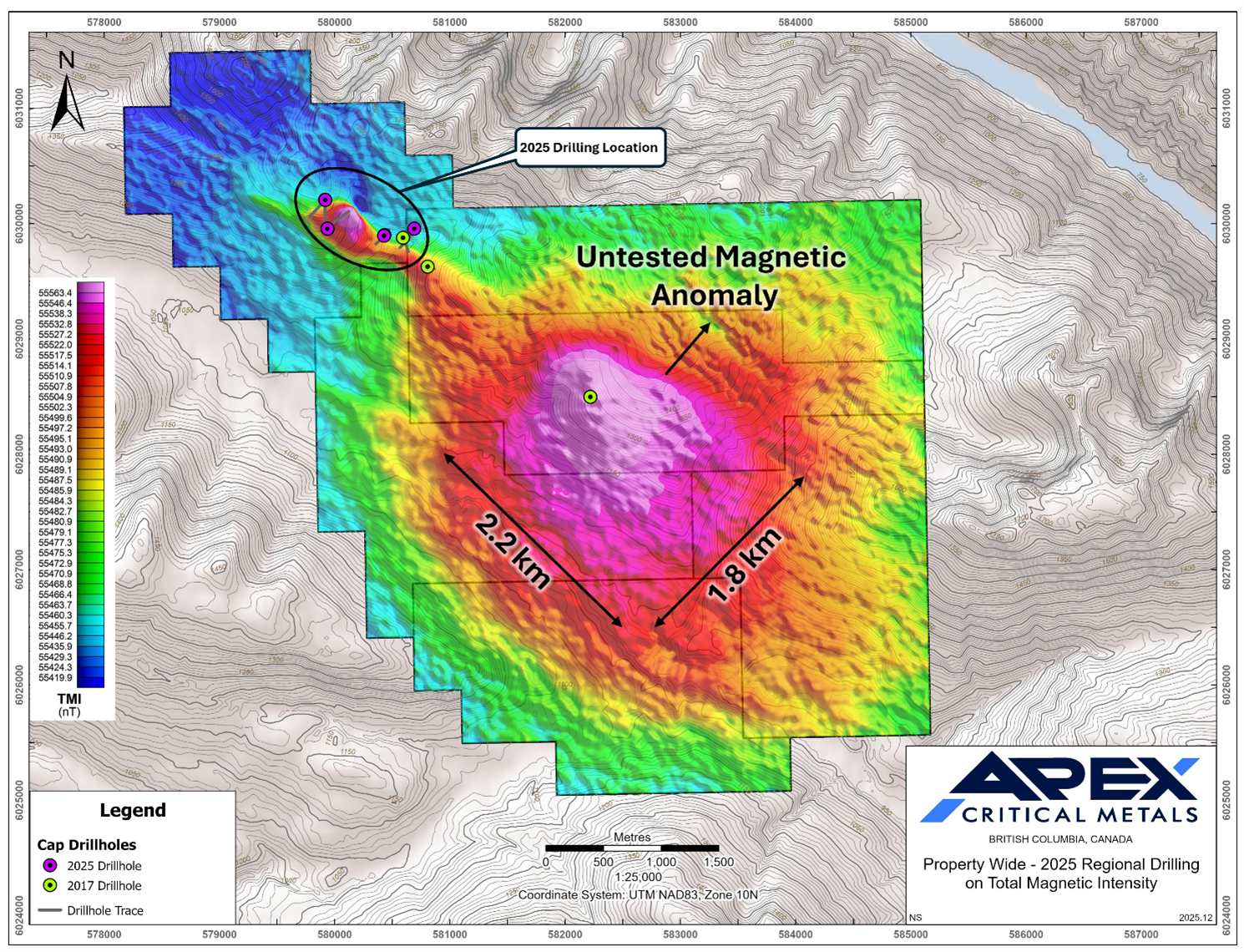

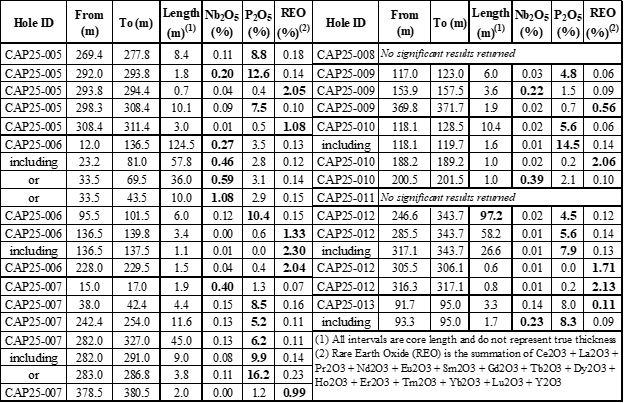

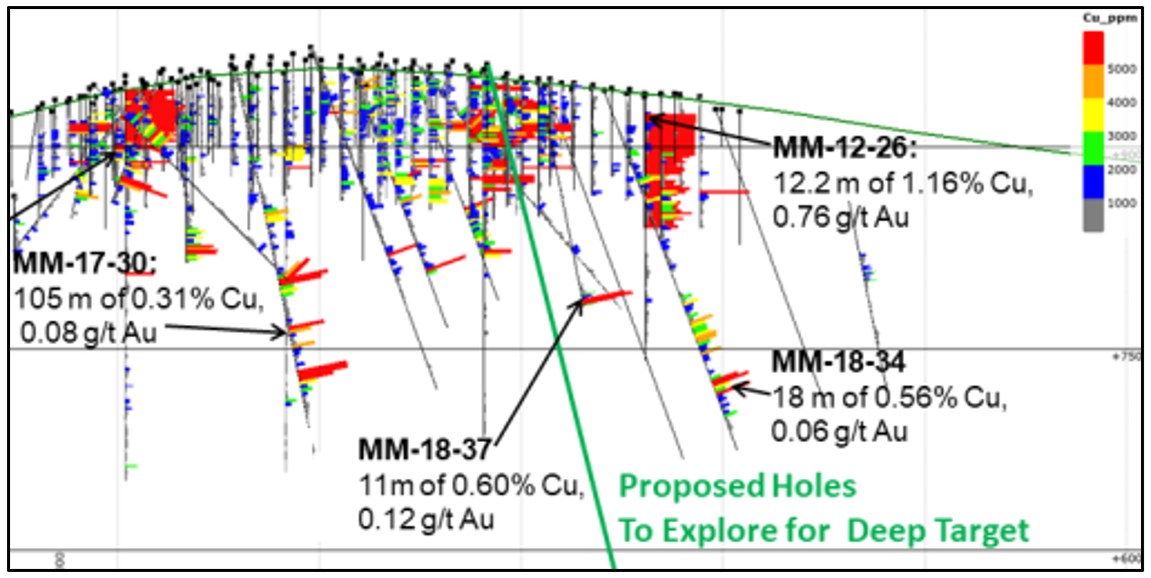

VANCOUVER, BC / ACCESS Newswire / December 31, 2025 / Apex Critical Metals Corp. (CSE:APXC)(OTCQX:APXCF)(FWB:KL9) ("Apex" or the "Company"), a Canadian mineral exploration company focused on the identification and development of critical and strategic metals, is pleased to provide a summary of all analytical results from its 2025 regional exploration drilling program and 2026 outlook at the 100%-owned Cap Critical Minerals Project ("Cap" or the "Project") in central British Columbia.

Highlights

-

Expanded mineralization from CAP25-006, which returned 124.5 m of 0.27% Nb₂O₅, encompassing the previously announced 36 m of 0.59% Nb₂O₅ that included 10 m at 1.08% Nb₂O₅.

-

The additional drill holes in 2025 were designed to test regional target areas. The niobium enriched discovery in CAP25-006 remains open in multiple directions and a priority area for follow-up drilling in 2026 (see Figure 1).

-

Multiple REE-enriched intervals were returned across the 2025 drilling, including two significant zones grading between 1.08% and 1.33% REO over 3.0 m and 3.4 m in CAP25-005 and CAP25-006, respectively, demonstrating strong rare earth potential within the carbonatite system.

-

Significant phosphate mineralization occurs in both high-grade and broad intervals, with P₂O₅ grades up to 16.2% over 3.8m (CAP25-007) and several intervals exceeding 5% P₂O₅; including 6.2% P₂O₅ over 45 m (CAP25-007) and 4.5% P₂O₅ over 97.2 m (CAP25-012)

-

The new geophysical survey results (see News Release dated November 12, 2025) show a massive buried magnetic anomaly that has yet to be tested at depth (see Figure 2). Testing this high-priority target and following up on the new near-surface niobium discovery will be the dual focus for 2026 drilling.

Sean Charland, CEO of Apex Critical Metals, stated: "The drilling highlight of the 2025 program remains the near-surface, high-grade niobium discovery, with the additional assay results showing a broader interval in CAP25-006 and further niobium, phosphate and REE mineralization in other regional target areas, which reinforces our interpretation of a large, fertile carbonatite system. We are equally excited by the intensity and scale of the untested magnetic anomaly to the southeast of our 2025 regional program, underscoring the opportunity and exploration upside at Cap."

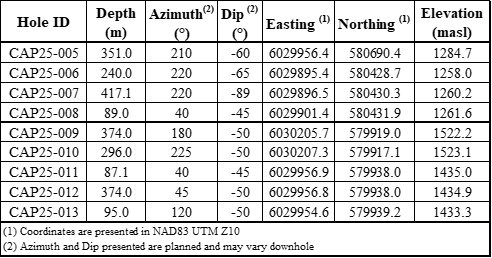

The 2025 exploration program consisted of nine (9) helicopter-supported NQ diamond drillholes totaling 2,323 m (Table 2). The remaining results confirm widespread niobium, rare earth element and phosphate mineralization across multiple drillholes and substantially expand the mineralized interval previously reported from discovery hole CAP25-006. Collectively, the results demonstrate that Cap hosts potential for a large, fertile, multi-phase carbonatite system that remains open and underexplored.

Previously released rush assays from CAP25-006 reported 36 m averaging 0.59% Nb₂O₅, including 10 m at 1.08% Nb₂O₅, beginning at only 33.5 m downhole (see News Release dated August 27, 2025). Complete assays now show that this zone is part of a much broader mineralized interval totaling 124.5 m averaging 0.27% Nb₂O₅, confirming continuity and scale. This niobium enriched zone was not directly followed up on during the 2025 first pass regional drilling campaign and remains open both laterally (see Figure 1 below) and at depth.

Figure 1: Map showing location of 2025 drillholes over total magnetic intensity from 2025 airborne survey

The assay results also demonstrate meaningful rare earth element potential at Cap. As outlined in Table 1, multiple REE-bearing intervals were intersected across the 2025 drilling, including intervals grading between 1.08% and 1.33% REO over 3.0 m and 3.4 m in CAP25-005 and CAP25-006, respectively. Localized samples exceeding 2% REO indicate enrichment and support a broader critical-metal signature within the carbonatite system (Table 1).

Phosphate mineralization is well developed across the Project, with assay results returning both high-grade and broad continuous intervals. Results reach up to 16.2% P₂O₅, over 3.8 m with intervals including 45.0 m at 6.22% from CAP25-007 and 58.2 m at 5.63% from CAP25-012 (Table 1). The distribution of these phosphate-rich zones across multiple drillholes further supports the interpretation of a large carbonatite system.

The Company completed a geophysical survey near the end of the exploration season concurrent to its final drill holes to better detail andto further refine subsurface targeting. The survey outlined a large magnetic anomaly interpreted to represent a buried intrusive body (Figure 2). To date, this anomaly has only been tested by a single historical (2017) drill hole that did not reach the interpreted target depth. The size, strength, and limited drill testing of this feature present a compelling opportunity for follow-up, with several well-positioned drill holes planned for the 2026 exploration season.

Figure 2: Map showing 2025 drilling location and significant untested magnetic anomaly to the southeast, outlined from 2025 airborne geophysical survey

Table 1 Drillhole Assay Summary

The Company will now incorporate the full 2025 assay dataset and newly acquired airborne magnetic survey results into an updated geological model. This work will support the design of the 2026 drill program, which is expected to focus on step-out drilling around the CAP25-006 niobium discovery and initial testing of high-priority targets generated from the 2025 airborne geophysical survey. The 2025 exploration program was a success in advancing the Company's understanding of the carbonatite system at Cap and refining the focus for the year ahead.

The near-term focus remains on the Company's flagship Rift Rare Earth Project in Nebraska, USA, where significant progress is being made towards a fully funded drill program, which is expected to commence in early Q1/2026.

Table 2 Drillhole Locations and Attributes

Quality Assurance / Quality Control

All drilling was completed using a helicopter supported diamond drill rig with NQ size core and all drill core samples have been or will be shipped to Activation Laboratories Ltd. preparation facility in Kamloops, British Columbia, for standard sample preparation (code RX1) which includes drying, crush (< 7 kg) up to 80% passing 2 mm, riffle split (250 g) and pulverize (mild steel) to 95% passing 105 µm. The samples were subsequently analyzed using Code 8 by XRF Nb₂O₅, ZrO2 and Ta2O5 (0.003%), Code 8 – REE Assay (lithium metaborate/tetraborate fusion with subsequent analysis by ICP and ICP/MS). Drill core was saw-cut with half-core sent for geochemical analysis and half-core remaining in the box onsite.

A Quality Assurance/Quality Control protocol was incorporated into the program and included the insertion of certified reference material and silica blanks at a rate of approximately 5% and 5%, respectively.

Qualified Person

The technical content of this news release has been reviewed and approved by Nathan Schmidt, P. Geo., a Qualified Person under NI 43-101 on standards of disclosure for mineral projects (EGBC Licence 48336). Mr. Schmidt is a Geologist with Dahrouge Geological Consulting Ltd. (EGBC Permit to Practice 1003035), the consulting firm engaged by Apex Critical Metals Corp. to conduct and oversee all of the Company's exploration work, including the 2025 drill program.

Mr. Schmidt has verified all scientific and technical data disclosed in this news release including the sampling and QA/QC results, and certified analytical data underlying the technical information disclosed. Mr. Schmidt noted no errors or omissions during the data verification process. The Company and Mr. Schmidt do not recognize any factors of sampling or recovery that could materially affect the accuracy or reliability of the assay data disclosed in this news release.

About Apex Critical Metals Corp. (CSE:APXC)(OTCQX:APXCF)(FWB:KL9)

Apex Critical Metals Corp. is a Canadian exploration company focused on advancing rare earth element (REE) and niobium projects that support the growing demand for critical and strategic metals across the United States and Canada. The Company's flagship Rift Project, located within the highly prospective Elk Creek Carbonatite Complex in Nebraska, U.S.A., hosts extensive rare earth rights surrounding one of North America's most advanced niobium-REE deposits. Historical drilling across the complex has reported broad intervals of high-grade REE mineralization, including intercepts such as 155.5 m of 2.70% REO and 68.2 m of 3.32% REO.

In Canada, Apex continues to advance its 100%-owned Cap Project, located 85 kilometres northeast of Prince George, British Columbia. The 2025 drill program confirmed a significant niobium discovery with 0.59% Nb₂O₅ over 36 metres, including 1.08% Nb₂O₅ over 10 metres, within a 1.8-kilometre-long niobium trend. The Cap Project continues to demonstrate strong potential for niobium mineralization within a large and previously unrecognized carbonatite system.

With a growing portfolio of critical mineral projects in both Canada and the United States, Apex Critical Metals is strategically positioned to help strengthen domestic supply chains for the minerals essential to advanced technologies, clean energy, and national security. Apex is publicly listed in Canada on the Canadian Securities Exchange (CSE) under the symbol APXC and quoted on the OTCQX market in the United States under the symbol APXCF, and in Germany on the Borse Frankfurt under the symbol KL9 and/or WKN: A40CCQ. Find out more at www.apexcriticalmetals.com and to sign up for free news alerts please go to https://apexcriticalmetals.com/news/news-alerts/, or follow us on X (formerly Twitter), Facebook or LinkedIn.

On Behalf of the Board of Directors

APEX CRITICAL METALS CORP.,

Sean CharlandChief Executive OfficerTel: 604.681.1568Email: info@apexcriticalmetals.com

Neither the Canadian Securities Exchange nor its Regulation Services Provider (as that term is defined in the policies of the CSE) accepts responsibility for the adequacy or accuracy of this release.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION:

This news release may contain "forward-looking statements" under applicable Canadian securities legislation. Forward-looking statements consist of statements that are not purely historical, including any statements regarding beliefs, plans, expectations or intentions regarding the future. Forward-looking statements in this news release include (without limitation) statements with respect to follow-up drilling on the Cap Project in 2026, the potential for the Cap Project to host a large, fertile multi-phase carbonatite system, statements regarding the Company's growing portfolio of critical mineral projects in Canada and the United States and the potential for exploration. Forward-looking statements are subject to various known and unknown risks and uncertainties that may cause actual results, performance or developments to differ materially from those contained in the statements. Risks that could change or prevent these events, activities or developments from coming to fruition include: the Company's properties are at an early stage of development and no current mineral resources or reserves have been identified by the Company thereof, that we may not be able to fully finance any additional exploration on the Company's properties; that even if we are able to raise capital, costs for exploration activities may increase such that we may not have sufficient funds to pay for such exploration or processing activities; the timing and content of any future work programs; geological interpretations based on drilling that may change with more detailed information; potential process methods and mineral recoveries assumptions based on limited test work and by comparison to what are considered analogous deposits that, with further test work, may not be comparable; testing of our process may not prove successful or samples derived from our properties may not yield positive results, and even if such tests are successful or initial sample results are positive, the economic and other outcomes may not be as expected; the anticipated market demand for REE and other minerals may not be as expected; the availability of labour and equipment to undertake future exploration work and testing activities; geopolitical risks which may result in market and economic instability. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The forward-looking statements herein are made as of the date hereof, and the Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

SOURCE: Apex Critical Metals Corp.

View the original press release on ACCESS Newswire

As the Australian market approaches the holiday season, it is witnessing a slight downturn, with the ASX experiencing a 0.2% drop amidst profit-taking activities and early closures for Christmas. Despite this lull, small-cap stocks continue to capture interest due to their potential for growth in sectors like precious metals and defense technologies. In this context, identifying undervalued companies with strong fundamentals and innovative strategies can offer promising opportunities for investors seeking to uncover hidden gems in Australia’s vibrant market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

|

Name |

Debt To Equity |

Revenue Growth |

Earnings Growth |

Health Rating |

|---|---|---|---|---|

|

Fiducian Group |

NA |

10.00% |

9.57% |

★★★★★★ |

|

Joyce |

NA |

9.93% |

17.54% |

★★★★★★ |

|

Hearts and Minds Investments |

NA |

56.27% |

59.19% |

★★★★★★ |

|

Spheria Emerging Companies |

NA |

-1.31% |

0.28% |

★★★★★★ |

|

Euroz Hartleys Group |

NA |

1.82% |

-25.32% |

★★★★★★ |

|

Argosy Minerals |

NA |

-12.81% |

-19.89% |

★★★★★★ |

|

Focus Minerals |

NA |

75.35% |

51.34% |

★★★★★★ |

|

Energy World |

NA |

-47.50% |

-44.86% |

★★★★★☆ |

|

Zimplats Holdings |

5.44% |

-9.79% |

-42.03% |

★★★★★☆ |

|

Australian United Investment |

1.90% |

5.23% |

4.56% |

★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Australian United Investment Company Limited is a publicly owned investment manager with a market cap of A$1.41 billion.

Operations: The company generates revenue primarily from investments, amounting to A$57 million. It has a market cap of approximately A$1.41 billion.

Australian United Investment (AUI) showcases a strong financial foundation with its net debt to equity ratio at a satisfactory 1.5%, reflecting prudent financial management. Over the past five years, AUI has reduced its debt to equity from 9.1% to 1.9%, indicating effective debt reduction strategies. The company’s high-quality earnings are complemented by robust interest coverage, with EBIT covering interest payments 22.8 times over, ensuring financial stability and resilience in challenging market conditions. Despite a modest annual earnings growth of 4.6% over the last five years, AUI remains profitable with positive free cash flow and no immediate cash runway concerns.

ASX:AUI Debt to Equity as at Dec 2025Fiducian Group

Simply Wall St Value Rating: ★★★★★★

Overview: Fiducian Group Ltd operates in Australia offering a range of financial services through its subsidiaries and has a market cap of approximately A$378.81 million.

Operations: The company’s primary revenue streams include financial planning (A$29.66 million), funds management (A$25.59 million), corporate services (A$17.67 million), and platform administration (A$16.45 million).

Fiducian Group, a nimble player in the financial landscape, stands out with its debt-free status over the past five years. This lack of debt removes any concerns about interest coverage and highlights its robust financial health. The company has demonstrated impressive earnings growth of 23.5% over the last year, significantly outpacing the broader Capital Markets industry growth of 6%. With high-quality earnings and a favorable price-to-earnings ratio of 20.4x compared to the Australian market’s 21.7x, Fiducian seems well-positioned for continued success in its sector.

-

Unlock comprehensive insights into our analysis of Fiducian Group stock in this health report.

-

Gain insights into Fiducian Group’s historical performance by reviewing our past performance report.

ASX:FID Debt to Equity as at Dec 2025Omni Bridgeway

Simply Wall St Value Rating: ★★★★★☆

Overview: Omni Bridgeway Limited operates as a global provider of dispute and litigation finance services across multiple regions including Australia, the United States, and Europe, with a market capitalization of A$432.40 million.

Operations: Omni Bridgeway generates revenue primarily from funding and providing services related to legal dispute resolution, amounting to A$87.77 million.

Omni Bridgeway, a promising player in the Australian market, recently turned profitable, making it stand out in the financial sector. The company’s price-to-earnings ratio of 1.2x positions it attractively against the broader Australian market at 21.7x. Despite a forecasted earnings decline averaging 148% annually over three years, revenue is expected to grow by nearly 24% per year. Omni Bridgeway’s debt management shines with a reduction in its debt-to-equity ratio from 18.7% to just 2.3% over five years and having more cash than total debt ensures financial stability moving forward into potential growth opportunities.

ASX:OBL Earnings and Revenue Growth as at Dec 2025Seize The Opportunity

-

Reveal the 59 hidden gems among our ASX Undiscovered Gems With Strong Fundamentals screener with a single click here.

-

Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

-

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

-

Explore high-performing small cap companies that haven’t yet garnered significant analyst attention.

-

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

-

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:AUI ASX:FID and ASX:OBL.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

THIS NEWS RELEASE IS NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

VANCOUVER, BC / ACCESS Newswire / December 30, 2025 / Stillwater Critical Minerals Corp. (TSX.V:PGE)(OTCQB:PGEZF)(FSE:J0G) (the "Company", or "Stillwater") is pleased to announce the closing of its previously announced "bought deal" private placement (the "Offering") for gross proceeds of C$17,000,220, which includes the exercise in full of an over-allotment option. Pursuant to the Offering, the Company sold 36,957,000 units of the Company (each, a "Unit") at a price of C$0.46 per Unit (the "Offering Price"). Under the Offering, Red Cloud Securities Inc. acted as co-lead underwriter and sole bookrunner along with Research Capital Corporation (collectively, the "Underwriters") as co-lead underwriter.

Each Unit consists of one common share of the Company (each, a "Common Share") and one-half of one common share purchase warrant (each whole warrant, a "Warrant"). Each Warrant entitles the holder thereof to purchase one Common Share (a "Warrant Share") at a price of C$0.64 at any time on or before December 30, 2028.

The Company intends to use the net proceeds of the Offering for the exploration and advancement of the Company's flagship Stillwater West Ni-PGE-Cu-Co+Au project in the Stillwater mining district in Montana, U.S., as well as for general corporate purposes and working capital, as is more fully described in the Amended Offering Document (as defined herein).

In accordance with National Instrument 45-106 – Prospectus Exemptions ("NI 45-106"), the Units were issued to Canadian purchasers pursuant to the listed issuer financing exemption under Part 5A of NI 45-106, as amended by Coordinated Blanket Order 45-935 – Exemptions from Certain Conditions of the Listed Issuer Financing Exemption (the "Listed Issuer Financing Exemption"). The Common Shares and the Warrant Shares underlying the Units are immediately freely tradeable in accordance with applicable Canadian securities legislation if sold to purchasers resident in Canada. The Units were also sold to purchasers in offshore jurisdictions and in the United States on a private placement basis pursuant to one or more exemptions from the registration requirements of the United States Securities Act of 1933, as amended(the "U.S. Securities Act"). All securities not issued pursuant to the Listed Issuer Financing Exemption are subject to a hold period in accordance with applicable Canadian securities law, expiring four months and one day following the issue date.

"As a result of strong support demonstrated in this placement, we are ending 2025 with funds in place for a robust 2026 season" said Michael Rowley, President and CEO. "We look forward to near-term catalysts including drill results and updates on government initiatives as well as the planned update to our mineral resource estimate as we advance Stillwater West as a primary source of ten minerals designated as critical in the U.S."

As consideration for their services in the Offering, the Underwriters received aggregate cash fees of C$987,114 and 2,145,900 non-transferable common share purchase warrants (the "Broker Warrants"). Each Broker Warrant is exercisable into one Common Share at the Offering Price for a period of thirty-six (36) months from the date of issuance. The Broker Warrants are subject to a hold period in accordance with applicable Canadian securities law, expiring four months and one day following the issue date, being May 1, 2026.

There is an amended and restated offering document (the "Amended Offering Document") related to the Offering that can be accessed under the Company's profile at www.sedarplus.ca and on the Company's website at www.criticalminerals.com.

The closing of the Offering remains subject to the final approval of the TSX Venture Exchange (the "TSXV").

The securities referred to in this news release have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the "U.S. Securities Act"), or any U.S. state securities laws, and may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons (as defined under the U.S. Securities Act) absent registration or any applicable exemption from the registration requirements of the U.S. Securities Act and applicable U.S. state securities laws. This news release shall not constitute an offer to sell or the solicitation of an offer to buy securities in the United States, nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.About Stillwater Critical Minerals Corp.

Stillwater Critical Minerals (TSX.V: PGE | OTCQB: PGEZF | FSE: J0G) is a mineral exploration and development company focused on its flagship Stillwater West Ni-PGE-Cu-Co + Au project in the iconic and famously productive Stillwater mining district in Montana, USA. With the addition of two renowned Bushveld and Platreef geologists to the team and strategic investments by Glencore plc, the Company is well positioned to advance the next phase of large-scale critical mineral supply from this world-class American district, building on past production of nickel, copper, and chromium, and the on-going production of platinum group, nickel, and other metals by neighboring Sibanye-Stillwater. An expanded NI 43-101 mineral resource estimate, released January 2023, positions Stillwater West with the largest nickel resource in an active U.S. mining district as part of a compelling suite of ten minerals now listed as critical in the USA.

Stillwater also holds a 49% interest in the high-grade Drayton-Black Lake-gold project adjacent to Nexgold

Mining's development-stage Goliath Gold Complex in northwest Ontario, currently under an earn-in agreement with Heritage Mining, and the Kluane PGE-Ni-Cu-Co critical minerals project on trend with Nickel Creek Platinum‘s Wellgreen deposit in Canada‘s Yukon Territory. The Company also holds the Duke Island Cu-Ni-PGE property in Alaska and maintains a back-in right on the high-grade past-producing Yankee-Dundee in BC, following its sale in 2013.FOR FURTHER INFORMATION, PLEASE CONTACT:

Michael Rowley, President, CEO & Director – Stillwater Critical MineralsEmail: info@criticalminerals.com Phone: (604) 357 4790Web: http://criticalminerals.com Toll Free: (888) 432 0075Forward-Looking Statements

This news release includes certain statements that may be deemed "forward-looking statements". In particular, this press release contains forward-looking information relating to, among other things, the Offering, the intended use of proceeds of the Offering and the receipt of final approval of the Offering from the TSXV. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Stillwater Critical Minerals believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource estimates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more information on Stillwater Critical Minerals and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedarplus.ca.

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

SOURCE: Stillwater Critical Minerals

View the original press release on ACCESS Newswire

Toronto, Ontario–(Newsfile Corp. – December 29, 2025) – Minnova Corp. (TSXV: MCI) ("Minnova" or the "Company") is pleased to announce it has directed A&B Global Mining, lead engineer on the Preliminary Economic Assessment, to evaluate and design a significant expansion of the PL Gold Mine's current 1,000 tonnes per day ("tpd") nameplate processing capacity. The current plan involves recommencing mining operations through open pit mining methods, with run-of-mine ("ROM") throughput aligned to process plant's nameplate capacity. On going work related to process plant refurbishment has recognized that the existing "front-end" crushing plant infrastructure potentially possesses capacity well in excess of 1,000 tpd.

Preliminary assessments of the primary Traylor Jaw and secondary Symons Short Head Cone crushers indicate that these robust components can support significantly higher volumes. Initial work on an expansion plan will consist of a Technical Audit & Capacity Analysis ("TACA"), including;

- Crushing Audit – verify existing crushers can sustain a crushing rate to achieve minimum 2,000 tpd.

- Motor/Drive Review – assess existing 100 HP motor on jaw crusher and 150 HP motor on the cone crusher to handle ore at increased throughput.

- Choke Point Identification – assess existing dust collection, ore chutes and transfer point capacities.

- Power Requirements – assess motor control center and transformer requirements at increased throughput rate.

Photo 1: Crushing and Screening Building and Mill Feed Infrastructure

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/3654/279121_986ddcfdd4a5583c_001full.jpg

Photo 2: Crushing and Screening Building and Mill Feed Infrastructure

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/3654/279121_986ddcfdd4a5583c_002full.jpg

Should the TACA assessment confirm the current crushing capacity exceeds 2,000 tpd, the expansion initiative will proceed to the Design & Engineering phase, with a target minimum ROM mill feed rate of 2,000 tpd. Achieving this goal will necessitate a comprehensive redesign of specific crusher plant processes, as well as the duplication of the following components: a) fine ore storage capacity, b) ore conveyor systems, and c) milling, gravity, flotation and concentrate leaching processes along with the existing Merrill-Crowe gold recovery circuit. All new equipment will be installed in parallel with the established infrastructure.

By doubling the processing plant ROM throughput capacity, Minnova aims to leverage existing infrastructure and dramatically enhance the project's economics in the current high gold price environment. This expansion initiative reflects the Company's commitment to maximizing the value of its existing infrastructure. The successful restart of the PL Gold Mine at a targeted 2,000 tpd throughput rate from open mining operations will position Minnova as a more significant gold producer, providing a robust operational foundation for the eventual transition to underground mining operations.

Option Grant

Pursuant to the Company's LTIP the Company announces that its board of directors has approved an option grant of 2,500,000 options to purchase common shares of the Company exercisable at a price of $0.20 per common share for a period of 5 years, to certain directors, officers, employees, and consultants. The common shares issuable upon exercise of the options are subject to a four month hold period from the original date of grant. These stock options vest immediately.

Qualified Person

Chris Buchanan, MSc, PGeo, is an independent consultant of the company and a qualified person under National Instrument 43-101, has reviewed and approved the scientific and technical information in this news release.

About Minnova Corp.

Minnova Corp. is a near term gold producer focused on the restart and expansion of its 100%-owned PL Gold Mine in the prolific Flin Flon Greenstone Belt of Central Manitoba. The project is situated on a past producing mine site and benefits from significant existing infrastructure, including a 1,000 tpd processing plant and valid underground mining permit (Environment Act License 1207E).

A positive 2018 Feasibility Study, based on an underground development plan and a gold price of US$1,250 per ounce, outlined a robust 5-year mine life with an annual production rate of 46,493 ounces. Considering current high gold price Minnova is revising the mine development plan to prioritize lower-cost open pit mining methods for the initial years of production before transitioning to underground methods.

A revised mine development plan that leverages the full 1,000 tpd process plant capacity and targets reduced operating costs compared to the previous underground-only model is underway and will be the subject of a Preliminary Economic Assessment and Feasibility Study to be completed in 2026. The current global gold resource remains open to expansion, as does the reserve. The Mineral Resource Estimate will be revised in 2026, using current consensus gold price assumption and will incorporate all drilling conducted after the 2018 Feasibility Study, including a 15,000-meter drill program currently in progress.

For more information please contact:

Minnova Corp.Gorden GlennPresident & Chief Executive OfficerTel: (647) 985-2785

For further information, please contact Investor Relations at info@minnovacorp.ca.

Visit our website at www.minnovacorp.ca.

Forward Looking Statements

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release contains certain "forward-looking information" within the meaning of applicable securities laws. Forward looking information is frequently characterized by words such as "plan", "expect", "project", "intend", "believe", "anticipate", "estimate", "may", "will", "would", "potential", "proposed" and other similar words, or statements that certain events or conditions "may" or "will" occur. These statements are only predictions. Forward-looking information is based on the opinions and estimates of management at the date the information is provided, and is subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information. For a description of the risks and uncertainties facing the Company and its business and affairs, readers should refer to the Company's Management's Discussion and Analysis. The Company undertakes no obligation to update forward-looking information if circumstances or management's estimates or opinions should change, unless required by law. The reader is cautioned not to place undue reliance on forward-looking information.

Not for distribution to U.S. Newswire Services or for dissemination in the United States. Any failure to comply with this restriction may constitute a violation of U.S. Securities laws.

NOT FOR DISSEMINATION INTO THE UNITED STATES

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/279121

As the Australian market winds down for the holiday season with a slight dip, largely due to profit-taking and in anticipation of Wall Street’s highs, investors are turning their attention to commodities like gold and copper which have recently seen notable gains. In this environment, identifying promising small-cap stocks requires a keen eye for companies that can capitalize on these sector trends while navigating broader market sentiment.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 10.00% | 9.57% | ★★★★★★ |

| Joyce | NA | 9.93% | 17.54% | ★★★★★★ |

| Hearts and Minds Investments | NA | 56.27% | 59.19% | ★★★★★★ |

| Spheria Emerging Companies | NA | -1.31% | 0.28% | ★★★★★★ |

| Euroz Hartleys Group | NA | 1.82% | -25.32% | ★★★★★★ |

| Argosy Minerals | NA | -12.81% | -19.89% | ★★★★★★ |

| Focus Minerals | NA | 75.35% | 51.34% | ★★★★★★ |

| Energy World | NA | -47.50% | -44.86% | ★★★★★☆ |

| Zimplats Holdings | 5.44% | -9.79% | -42.03% | ★★★★★☆ |

| Australian United Investment | 1.90% | 5.23% | 4.56% | ★★★★☆☆ |

Let’s dive into some prime choices out of from the screener.

Simply Wall St Value Rating: ★★★★★☆

Overview: Carlton Investments Limited is a publicly owned asset management holding company with a market capitalization of A$911.96 million.

Operations: Carlton Investments generates revenue primarily through the acquisition and long-term holding of shares and units, amounting to A$41.60 million.

Carlton Investments, a relatively small player in the market, has shown a steady earnings growth of 8.7% annually over the past five years. Despite its modest size, it boasts high-quality earnings and maintains an impressive interest coverage ratio of 3390 times through EBIT. The company has effectively managed its debt levels, reducing the debt-to-equity ratio from 0.03% to 0.02% over five years, indicating prudent financial management. While recent earnings growth at 0.09% lagged behind industry standards of 6%, Carlton remains free cash flow positive with A$39 million recorded recently, suggesting solid operational health and potential for future stability.

- Click here to discover the nuances of Carlton Investments with our detailed analytical health report.

-

Evaluate Carlton Investments’ historical performance by accessing our past performance report.

ASX:CIN Debt to Equity as at Dec 2025Metals X

Simply Wall St Value Rating: ★★★★★★

Overview: Metals X Limited is an Australian company focused on tin production, with a market capitalization of A$975.03 million.

Operations: The primary revenue stream for Metals X Limited is its 50% stake in the Renison Tin Operation, generating A$271.38 million. The company focuses on tin production in Australia.

Metals X, a nimble player in the mining sector, boasts a remarkable earnings growth of 708% over the past year, outpacing the industry average of 10%. This performance is bolstered by its debt-free status, contrasting with a debt-to-equity ratio of 58% five years ago. With a price-to-earnings ratio at just 6.9x, it offers compelling value against the broader Australian market’s 21.7x. However, recent financials include a significant A$38M one-off gain that might skew perceptions of ongoing profitability. Despite these fluctuations and forecasts suggesting declining earnings ahead, Metals X remains financially sound with positive free cash flow and no debt concerns.

- Take a closer look at Metals X’s potential here in our health report.

-

Explore historical data to track Metals X’s performance over time in our Past section.

ASX:MLX Debt to Equity as at Dec 2025Wagners Holding

Simply Wall St Value Rating: ★★★★★☆

Overview: Wagners Holding Company Limited is involved in the production and sale of construction and related building materials across several countries, including Australia, the United States, and New Zealand, with a market capitalization of A$703.03 million.

Operations: Wagners generates revenue primarily from Construction Materials (A$257.69 million), Project Services (A$105.71 million), and Composite Fibre Technology (A$68.45 million). The company’s net profit margin reflects its financial performance, influenced by its diverse revenue streams across multiple regions.

Wagners Holding, a small Australian player in the construction sector, is making waves with its focus on sustainable materials and infrastructure. Over the past year, earnings surged by 121%, outpacing industry growth of 3%. The company has reduced its debt to equity ratio from 66% to 28% over five years, showcasing financial prudence. With a net debt to equity ratio at a satisfactory 13%, Wagners seems well-positioned for future expansion. Analysts forecast an annual revenue growth of 6% for the next three years, although capital expenditure and raw material costs could impact earnings stability. Current share price sits at A$2.57 with an anticipated target of A$2.75.

ASX:WGN Debt to Equity as at Dec 2025Make It Happen

- Reveal the 59 hidden gems among our ASX Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Seeking Other Investments?

- Explore high-performing small cap companies that haven’t yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:CIN ASX:MLX and ASX:WGN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Zimplats Holdings' (ASX:ZIM) stock is up by a considerable 41% over the past month. However, we wonder if the company's inconsistent financials would have any adverse impact on the current share price momentum. Specifically, we decided to study Zimplats Holdings' ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Zimplats Holdings is:

2.2% = US$40m ÷ US$1.8b (Based on the trailing twelve months to June 2025).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each A$1 of shareholders' capital it has, the company made A$0.02 in profit.

View our latest analysis for Zimplats Holdings

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Zimplats Holdings' Earnings Growth And 2.2% ROE

It is quite clear that Zimplats Holdings' ROE is rather low. Even when compared to the industry average of 9.2%, the ROE figure is pretty disappointing. Given the circumstances, the significant decline in net income by 42% seen by Zimplats Holdings over the last five years is not surprising. However, there could also be other factors causing the earnings to decline. For example, the business has allocated capital poorly, or that the company has a very high payout ratio.

However, when we compared Zimplats Holdings' growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 12% in the same period. This is quite worrisome.

ASX:ZIM Past Earnings Growth December 27th 2025

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is Zimplats Holdings fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Zimplats Holdings Using Its Retained Earnings Effectively?

While the company did payout a portion of its dividend in the past, it currently doesn't pay a regular dividend. This implies that potentially all of its profits are being reinvested in the business.

Summary

In total, we're a bit ambivalent about Zimplats Holdings' performance. While the company does have a high rate of profit retention, its low rate of return is probably hampering its earnings growth. Up till now, we've only made a short study of the company's growth data. You can do your own research on Zimplats Holdings and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

As the U.S. stock market continues to reach new heights, with the S&P 500 setting all-time records, investors are increasingly interested in exploring opportunities beyond large-cap stocks. Amidst this backdrop of strong market performance and economic indicators, identifying promising small-cap stocks can offer potential for growth, particularly when these companies demonstrate solid fundamentals and insider confidence through recent buying activity.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Merchants Bancorp | 7.8x | 2.6x | 48.74% | ★★★★★★ |

| First United | 10.2x | 3.1x | 42.96% | ★★★★★☆ |

| Shore Bancshares | 10.6x | 2.8x | 39.92% | ★★★★☆☆ |

| Union Bankshares | 9.5x | 2.1x | 21.74% | ★★★★☆☆ |

| Angel Oak Mortgage REIT | 12.4x | 6.2x | 43.79% | ★★★★☆☆ |

| Farmland Partners | 6.4x | 7.9x | -90.27% | ★★★★☆☆ |

| Stock Yards Bancorp | 14.6x | 5.2x | 34.92% | ★★★☆☆☆ |

| MVB Financial | 10.3x | 2.0x | -10.87% | ★★★☆☆☆ |

| Omega Flex | 18.4x | 3.0x | 0.99% | ★★★☆☆☆ |

| Vestis | NA | 0.3x | -9.73% | ★★★☆☆☆ |

We’ll examine a selection from our screener results.

Simply Wall St Value Rating: ★★★★★☆

Overview: FMC is a global agricultural sciences company that provides innovative solutions for crop protection, with a market cap of $13.22 billion.

Operations: FMC’s revenue is primarily derived from its Innovative Solutions segment, which amounted to $3.61 billion. The company’s cost of goods sold (COGS) was $2.23 billion, resulting in a gross profit of $1.38 billion and a gross profit margin of 38.15%. Operating expenses include R&D costs, with recent figures showing an allocation of approximately $270.6 million towards research and development activities.

PE: -3.5x

FMC, a smaller player in the market, has seen its share price fluctuate significantly over the past three months. Despite this volatility, insider confidence is evident with recent purchases indicating potential value recognition. However, financial challenges persist as interest payments aren’t well covered by earnings and liabilities are entirely funded through external borrowing. Recent amendments to their credit agreement aim to manage leverage and dividend constraints until December 2028. With projected earnings growth of 65.93% annually, FMC’s future prospects remain intriguing despite current setbacks.

FMC Share price vs Value as at Dec 2025Granite Ridge Resources

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Granite Ridge Resources is engaged in the development, exploration, and production of oil and natural gas with a market capitalization of $1.52 billion.

Operations: Granite Ridge Resources generates revenue primarily from oil and natural gas development, exploration, and production, with recent quarterly revenue reaching $427.83 million. The company’s cost of goods sold (COGS) has increased to $80.33 million in the latest quarter, impacting its gross profit margin which stands at 81.22%. Operating expenses are substantial at $230.93 million, contributing to a net income of $37.49 million for the same period.

PE: 16.3x

Granite Ridge Resources, a small-cap company in the U.S., exhibits potential for value with insider confidence shown through recent share purchases. Despite facing financial challenges like high debt and reliance on external borrowing, Granite’s earnings have improved, reporting US$14.52 million net income for Q3 2025 versus US$9.05 million a year ago. Their involvement in Conduit Power’s natural gas project highlights strategic growth opportunities in Texas’ energy sector, aiming to enhance grid reliability by 2026.

- Get an in-depth perspective on Granite Ridge Resources’ performance by reading our valuation report here.

-

Assess Granite Ridge Resources’ past performance with our detailed historical performance reports.

GRNT Share price vs Value as at Dec 2025Herbalife

Simply Wall St Value Rating: ★★★★★☆

Overview: Herbalife is a global nutrition company that develops and sells dietary supplements, personal care products, and weight management solutions, with a market capitalization of approximately $1.27 billion.

Operations: India and the United States are key markets, contributing $857.70 million and $1.01 billion respectively to revenue, while Mexico adds $534 million. The gross profit margin has shown a range from 43.92% to 53.32% over recent periods, indicating variability in cost management relative to revenue generation. Operating expenses are primarily driven by general and administrative costs, with fluctuations impacting net income margins which have varied between 1.63% and 9.28%.

PE: 4.6x

Herbalife, a player in the nutrition industry, has seen insider confidence with recent share purchases. Despite a challenging financial position where interest payments aren’t well-covered by earnings and forecasts suggest declining earnings over the next three years, the company continues to innovate. Their Liftoff energy line expansion taps into a growing US$41.4 billion energy drink market projected for 2033. Recent investments include a US$7 million Center of Excellence in California to bolster product development and quality assurance efforts.

- Delve into the full analysis valuation report here for a deeper understanding of Herbalife.

-

Gain insights into Herbalife’s past trends and performance with our Past report.

HLF Share price vs Value as at Dec 2025Make It Happen

- Get an in-depth perspective on all 80 Undervalued US Small Caps With Insider Buying by using our screener here.

- Shareholder in one or more of these companies? Ensure you’re never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven’t yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include FMC GRNT and HLF.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

FMC Corporation's (NYSE:FMC) dividend is being reduced from last year's payment covering the same period to $0.08 on the 15th of January. Despite the cut, the dividend yield of 2.4% will still be comparable to other companies in the industry.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. FMC's stock price has reduced by 62% in the last 3 months, which is not ideal for investors and can explain a sharp increase in the dividend yield.

FMC's Future Dividend Projections Seem Positive

We like to see a healthy dividend yield, but that is only helpful to us if the payment can continue. Even though FMC is not generating a profit, it is still paying a dividend. Along with this, it is also not generating free cash flows, which raises concerns about the sustainability of the dividend.

According to analysts, EPS should be several times higher next year. Assuming the dividend continues along recent trends, we think the payout ratio will be 21%, which makes us pretty comfortable with the sustainability of the dividend.

NYSE:FMC Historic Dividend December 23rd 2025

View our latest analysis for FMC

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2015, the annual payment back then was $0.66, compared to the most recent full-year payment of $0.32. Doing the maths, this is a decline of about 7.0% per year. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

Dividend Growth May Be Hard To Achieve

Given that the track record hasn't been stellar, we really want to see earnings per share growing over time. Over the past five years, it looks as though FMC's EPS has declined at around 3.0% a year. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

We're Not Big Fans Of FMC's Dividend

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The company seems to be stretching itself a bit to make such big payments, but it doesn't appear they can be consistent over time. The dividend doesn't inspire confidence that it will provide solid income in the future.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've identified 3 warning signs for FMC (2 make us uncomfortable!) that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Toronto, Ontario–(Newsfile Corp. – December 22, 2025) – Minnova Corp. (TSXV: MCI) ("Minnova" or the "Company") is pleased to announce it has engaged Amps Powerline Inc. ("AMPS"), a Manitoba based industrial power contractor specializing in the construction, maintenance, and design of high voltage industrial systems. AMPS will work closely with ABGM, lead engineer and mine development consultant overseeing planned Preliminary Economic Assessment ("PEA") and updated Feasibility Studies ("FS") in 2026 for the re-start of the Company's PL Gold Mine located in Manitoba, Canada.

This engagement marks another significant step in advancing the PL Gold Mine towards production. AMPS will provide input into:

Reconnection and energization of the PL Mine site to the MB Hydro grid utilizing the Company's existing twenty-two kilometer power line infrastructure connecting the PL Gold Mine to MB Hydro grid power.

Site power distribution and refurbishment of crushing and process plant electrical power systems.

The power line infrastructure consists of a partially refurbished twenty-two kilometer, 3-phase 25kVa power line that connects the mine sites electric distribution grid to the Manitoba Hydro electric grid at a sub-station located at Sherridon MB.

Figure 1: Photos of Existing Power Line Infrastructure

To view an enhanced version of this graphic, please visit:https://images.newsfilecorp.com/files/3654/278858_minnova.jpg

About Minnova Corp.

Minnova Corp. is a near term gold producer focused on the restart and expansion of its 100%-owned PL Gold Mine in the prolific Flin Flon Greenstone Belt of Central Manitoba. The project is situated on a past-producing mine site and benefits from significant existing infrastructure, including a 1,000 tpd processing plant and valid underground mining permit (Environment Act License 1207E).

A positive 2018 Feasibility Study, based on an underground development plan and a gold price of US$1,250 per ounce, outlined a robust 5-year mine life with an annual production rate of 46,493 ounces. Considering current high gold price Minnova is revising the mine development plan to prioritize lower-cost open pit mining methods for the initial years of production before transitioning to underground methods. The new mine plan leverages the full 1,000 tpd mill capacity and targets reduced operating costs compared to the previous underground-only model. A revised mine development plan is underway and will be the subject of a Preliminary Economic Assessment and Feasibility Study to be completed in 2026.

The current global gold resource remains open to expansion, as does the reserve. The Mineral Resource Estimate will be revised in 2026, using current consensus gold price assumption and will incorporate all drilling conducted after the 2018 Feasibility Study, including the upcoming 15,000-meter drill program scheduled for 2025 and 2026.

For more information please contact:

Minnova Corp.Gorden GlennPresident & Chief Executive OfficerTel: (647) 985-2775

For further information, please contact Investor Relations at info@minnovacorp.ca

Visit our website at www.minnovacorp.ca

Forward-Looking Statements

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release contains certain "forward-looking information" within the meaning of applicable securities laws. Forward looking information is frequently characterized by words such as "plan", "expect", "project", "intend", "believe", "anticipate", "estimate", "may", "will", "would", "potential", "proposed" and other similar words, or statements that certain events or conditions "may" or "will" occur. These statements are only predictions. Forward-looking information is based on the opinions and estimates of management at the date the information is provided, and is subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information. For a description of the risks and uncertainties facing the Company and its business and affairs, readers should refer to the Company's Management's Discussion and Analysis. The Company undertakes no obligation to update forward-looking information if circumstances or management's estimates or opinions should change, unless required by law. The reader is cautioned not to place undue reliance on forward-looking information.

Not for distribution to U.S. Newswire Services or for dissemination in the United States. Any failure to comply with this restriction may constitute a violation of U.S. Securities laws.

NOT FOR DISSEMINATION INTO THE UNITED STATES

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/278858

PHILADELPHIA, Dec. 22, 2025 /PRNewswire/ — FMC Corporation (NYSE: FMC) announced today it will release its fourth quarter 2025 earnings on Wednesday, February 4, 2026, after the stock market close via PR Newswire and the company's website https://investors.fmc.com.

The company will host a webcast conference call on Thursday, February 5, 2026, at 9:00 a.m. ET that is open to the public via internet broadcast and telephone.

Conference Call Details:

Internet broadcast: https://investors.fmc.com

United States (Local): +1 646 844 6383United States (Toll-Free): +1 833 470 1428Global Dial-In Numbers: Global Dial-in NumberAccess Code: 827087

Pre-Registration Link: https://www.netroadshow.com/events/login/LE9zwo3lV0qrfzM9J1hL1dXMDtQBlK3ULBt

Webcast Details:https://events.q4inc.com/attendee/999618604

A replay of the call will be available via the internet and telephone from 11:00 a.m. ET on February 5, 2026, until February 12, 2026.

Internet replay: https://investors.fmc.comUnited States (Local): +1 929 458 6194United States (Toll-Free): +1 866 813 9403Access Code: 497154

About FMC

FMC Corporation is a global agricultural sciences company dedicated to helping growers produce food, feed, fiber and fuel for an expanding world population while adapting to a changing environment. FMC's innovative crop protection solutions – including biologicals, crop nutrition, digital and precision agriculture – enable growers and crop advisers to address their toughest challenges economically while protecting the environment. FMC is committed to discovering new herbicide, insecticide and fungicide active ingredients, product formulations and pioneering technologies that are consistently better for the planet. Visit fmc.com to learn more and follow us on LinkedIn®.

Cision

View original content to download multimedia:https://www.prnewswire.com/news-releases/fmc-corporation-announces-date-for-fourth-quarter-2025-earnings-release-and-webcast-conference-call-302648177.html

In recent market developments, the S&P 500 and Dow Jones Industrial Average have experienced declines following a surprising rise in unemployment, while the Nasdaq managed to tick higher, breaking its losing streak. Amid these mixed signals from major indices and economic indicators, investors may find opportunities in stocks that are perceived to be undervalued relative to their intrinsic value. Identifying such stocks requires careful analysis of financial health and growth potential within the context of current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

|

Name |

Current Price |

Fair Value (Est) |

Discount (Est) |

|

UMB Financial (UMBF) |

$118.98 |

$233.99 |

49.2% |

|

Perfect (PERF) |

$1.72 |

$3.43 |

49.9% |

|

Krystal Biotech (KRYS) |

$235.80 |

$469.93 |

49.8% |

|

Freshworks (FRSH) |

$12.39 |

$23.62 |

47.6% |

|

FirstSun Capital Bancorp (FSUN) |

$38.82 |

$73.56 |

47.2% |

|

First Solar (FSLR) |

$254.03 |

$482.71 |

47.4% |

|

Dingdong (Cayman) (DDL) |

$2.82 |

$5.45 |

48.3% |

|

DexCom (DXCM) |

$65.75 |

$127.60 |

48.5% |

|

Columbia Banking System (COLB) |

$28.95 |

$57.33 |

49.5% |

|

Bloom Energy (BE) |

$76.97 |

$148.02 |

48% |

We’re going to check out a few of the best picks from our screener tool.

Overview: Ligand Pharmaceuticals Incorporated is a biopharmaceutical company that develops and licenses biopharmaceutical assets globally, with a market cap of approximately $3.83 billion.

Operations: The company’s revenue primarily comes from the development and licensing of biopharmaceutical assets, totaling $251.23 million.

Estimated Discount To Fair Value: 15.1%